Abstract

Social housing policy in Ireland has evolved over several decades into a significantly marketized tenure which relies on, supports and expands the private housing market. In this paper we argue that it does so in ways that contribute to the financialization of housing by embedding housing in volatile financial market cycles. Although the majority of the literature on financialization, both in Ireland and internationally, has tended to focus on home ownership and mortgage markets, we argue that the retrenchment of social housing and the shift towards subsidized private rental accommodation have been key features of the process of financialization and of Ireland’s experience of boom and bust. The neoliberal turn in social housing policy, however, did not take shape in the form of either a coherent ideological project or a coherent suite of policy measures, but rather through the kind of piecemeal, ad hoc and typically ‘pragmatic’ processes identified by Kitchin et al. It is by examining the unfolding of these ad hoc processes that we identify both the neoliberalization of social housing policy and the interfaces between this process and that of financialization, particularly by highlighting how the former has enabled and facilitated the latter.

Introduction

Compared to most other English-speaking countries, the financialization of housing came late to the Republic of Ireland. Prior to the 1980s the private credit and housing markets were tightly regulated and underdeveloped, and private capital for housing was in short supply. The Irish government played a central role in providing housing capital by funding a large social housing building programme (which accounted for a majority of the housing built between the 1920s and 1950s) but also a large proportion of the capital required for the building and purchase of dwellings for owner occupation (Norris, 2016a). Such was the extent of Irish government subsidization of homeownership that Norris (2016b) argues that for most of the 20th century this was not a marketized tenure, but a ‘socialized’ tenure which was primarily state funded and, in the case of many dwellings, also constructed by local government.

Over the course of just a few years in the mid-1980s these distinctive housing supply and financing arrangements came to an abrupt end during a period of tax rises, public spending cuts and policy reforms introduced to manage a severe fiscal and economic crisis (Dukelow, 2011; Honohan, 1992). The private housing market was almost entirely deregulated, liberalized and financialized during this period as government mortgage provision and subsidies for homeowners were radically reduced; subsidization of the non-profit building societies was ended, and most government controls on capital flows, credit availability and interest rates were removed (Kelly and Everett, 2004). As a result, commercial banks quickly took over from government and building societies as the providers of almost all capital for private housing (Norris, 2016a).

The practical implications of these developments took a long while to materialize, but following the arrival of the ‘Celtic Tiger’ economic boom in the mid-1990s, and particularly after Ireland’s adoption of the euro in 1999, these became clear. At the same time, the euro eliminated exchange rate risk and facilitated low interest rates. This enabled enormous increases in bank funding, obtained via inter-bank lending, which generated a credit bubble (Norris and Coates, 2014). Mortgage debt per capita rose from 35% of the UK level in 1994 to 113% by 2007, and house prices increased to unprecedented levels (by 292% in nominal terms between 1996 and 2006) (European Mortgage Federation, 2012). Bank lending for residential development also increased radically and funded a concurrent housebuilding boom. From 2007 these interlinked bubbles deflated, starting with house prices, which fell by half between 2007 and 2012. From the following year this process and the wider economic crisis it precipitated were accelerated by the global financial crisis (GFC) (Norris and Coates, 2014).

There is thus a prima facie case for the structural relationship between neoliberalism and financialization in Ireland, as the deregulation of capital flows (Kelly, 2014), state withdrawal from the housing system (Norris, 2016a) and the promotion of mortgage-backed homeownership came together in an unprecedented property bubble (Downey, 2014). However, consistent with the international literature, which has likewise tended to focus on homeownership and credit markets (Beswick and Penny, 2018), social housing and the private rental sectors have been neglected. This has led to growth in private debt, especially mortgage credit, being presented as the defining feature of financialization as it is understood within the Irish literature (Kelly, 2014; McCabe, 2011). In this article we seek to contribute to a broader understanding of financialization in the Irish context, and indeed internationally, through an examination of the interaction between social housing policy and the private rental sector as it evolved from the late 1980s to the present. Analysing this set of changes, we argue, draws our attention to the way in which state intervention in these sectors has contributed to the embedding of housing within financial market cycles. Social housing policy has shifted towards the subsidization of private rental housing, and in doing so has embedded a growing segment of households within financial market cycles. This has played into these cycles, intensifying both boom and bust phases. Our analysis also seeks to further clarify the interaction between neoliberalism and financialization.

In what follows we present a detailed analysis of the relationship between housing, neoliberalism and financialization in Ireland since the 1980s, which elucidates the subtleties and complexities of this relationship and how it is manifested in the particular context of this country. We draw on the framework for policy analysis developed by Hacker (2005), which is particularly well suited to the analysis of the kind of piecemeal, incremental change that often characterizes processes of neoliberalization. To achieve this, our analysis examines social housing policy and focuses in particular on the three main mechanisms used to fund and deliver housing supports for low-income households in Ireland since the mid-1980s. We draw on extensive policy data, including parliamentary debates, policy documents and public spending trends, to examine how social housing policy change has unfolded and what this can tell us about the relationship with financialization and neoliberalism.

Neoliberalism, financialization and housing policy

This article, as noted in the introduction, argues that the relationship between financialization and neoliberalism is significant in understanding the transformation of the Irish housing system in recent decades. Both of these terms are, however, conceptualized in different ways within different literatures. In addition, both neoliberalism (Brenner et al., 2010b) and financialization (Aalbers, 2017b; Fine and Saad-Filho, 2017) are variegated processes which are embedded in and work through differing institutional configurations and political economic histories across different geographies. This section sets out the particular aspects of financialization and neoliberalism that are relevant to our analysis and clarifies how we conceptualize the relationship between the two to shed light on recent transformations of Irish housing.

Financialization, housing and financial cycles

There is by now a substantial literature on financialization. As yet, there is little consensus on how it should be conceptualized or theorized. As Manuel Aalbers (2017a: 543) notes, ‘[a]ny concept used across the social sciences and humanities is bound to be defined in myriad ways, especially relatively new concepts whose usage has spread rapidly in recent years’. Aalbers (2017a: 214) has, however, advanced a definition of financialization that serves as a point of departure: ‘the increasing dominance of financial actors, markets, practices, measurements and narratives, at various scales, resulting in a structural transformation of economies, firms … states and households’. This definition suggests two levels of analysis, and indeed this is reflected in the literature. On the one hand, financialization is used to theorize a new phase in capitalist political economy. On the other, it is used to analyse the transformation of specific areas of economy or society (e.g. housing).

To begin with the former, financialization is understood as the dominance of finance over the so-called real economy, in relation to its size or its centrality to profit and accumulation (Krippner, 2005). This manifests in the huge increase in private debt (Aalbers, 2017a) over recent decades; the proliferation of new financial products (Lapavitsas, 2013), the centrality of asset prices (Brenner, 2006); and the deregulation and expansion of capital flows (Kelly, 2014). In the Irish case, these developments have mainly occurred through Eurozone integration, which precipitated a huge increase in capital flowing into the Irish financial system, in turn making possible a colossal asset price bubble (Ó Rian, 2016).

In Ireland, as in so many other jurisdictions, housing and real estate played a key part in this process by absorbing the vast majority of the increase in private debt (Ó Rian, 2016). As such, many argue that housing is central to financialization (Aalbers, 2017a: Moreno, 2014). A growing literature has revealed a host of ways in which finance and housing are increasingly interrelated. This includes the impact of real estate investment trusts (REITs) on urban development (Rutland, 2010; Waldron, 2018) and housing (Beswick et al., 2016); mortgage securitization (Gotham, 2009); the transformation of housing into an asset at the level of individual subjectivity (Leyshon and French, 2009); and the impact of finance on social and private rental housing (Fields and Uffer, 2016; Wainwright and Manville, 2017). The consequences of the above processes are manifold. Research has focused on the growth of private debt (in particular residential and buy-to-let (BTL) mortgages) (Aalbers, 2017a); house price volatility (Norris and Coates, 2014); and the growth of homeownership (López and Rodríguez, 2011).

It is difficult, and beyond the scope of this article, to draw out a single definition of the financialization of housing from the literature. Our interest in this article is in Irish housing policy and the transformation of the Irish housing system over the last two decades. With this as our point of departure, we are particularly interested in financialization as a way of explaining housing system transformation. We advance here a conceptualization that centres on the processes through which housing becomes embedded in financial market cycles. This concern with cyclicality can help to better understand many of the impacts of financialization identified in the literature. For example, while the literature identifies the growth of private mortgage credit as a key impact of financialization, in many jurisdictions the issuing of mortgage credit has actually contracted radically in recent years and the criteria for accessing credit have been tightened substantially (Kemp, 2015). This is due to the cyclical nature of credit bubbles. Similarly, homeownership expanded across numerous jurisdictions, only to contract just as quickly after the crash (Forrest and Hirayama, 2015; Ronald and Kadi, 2017). Both house prices and supply have become increasingly cyclical as housing has become more tied to finance (for example, in Spain and Ireland; Norris and Byrne, 2015). This focus on cyclicality is also useful with regard to many of the current key issues in housing, which are strongly associated with the ‘bust’ phase of the cycle, such as mortgage arrears (García-Lamarca and Kaika, 2016; Waldron and Redmond, 2014); vacancy (O’Callaghan et al., 2018); distressed debt (Byrne, 2016b, 2016c); and ‘vulture funds’ (Beswick et al., 2016; Byrne, 2016a). In this article, we argue that transformations in social housing policy played an important role in embedding housing (especially the private rental sector) in financial market cycles. Social housing’s role has shifted over time towards the subsidization of the private rental sector, and this transformation has played a decisive role in the boom/bust phase of the 2000s, and indeed in the current volatility in the Irish housing system.

Our concern here echoes an emerging body of research on the financialization of social and affordable rental housing. There are three broad trends suggested by this research. First, the exhaustion of mortgage markets as a focus of investment and speculation by financial actors has created pressures to ‘open up’ rental properties as a new ‘asset class’. This is epitomized by private equity firms and hedge funds moving into the rental sector in countries such as the USA (Fields, 2017), Spain (Beswick et al., 2016), Germany (Fields and Uffer, 2016) and indeed Ireland (Waldron, 2018). This body of research tends to emphasize the way changing macro-level dynamics within the housing and financial systems create pressure for financial actors to penetrate new markets. Second, the growing involvement of financial actors and markets in the social and affordable rental housing sector is transforming, and ultimately undermining, the ‘social’ (i.e. non-market) dimension of the latter (Wainwright and Manville, 2017). This body of research tends to focus more on housing providers, such as housing associations, as the key level of analysis, and looks at their growing reliance on private finance (Aalbers et al. 2017; Wainwright and Manville, 2017). Third, and finally, Beswick and Penny (2018) argue that the local state can be understood as actively shaping the provision of social and affordable housing to enable the financialization of housing. The present article draws on and contributes to all these perspectives. Our focus, however, is more on the way in which longer-term changes in housing policy and the structure of the housing system, driven by the state, enable financialization. Rather than homing in on financial actors or on financialized housing providers, we shed light on how the state, in particular through neoliberalizing social housing policy, reshapes the housing systems in ways that much more fundamentally embedded the latter in the financial market and its boom–bust cycles.

Neoliberalism

Neoliberalism, even more so than financialization, is subject to varying definitions (Di Feliciantonio and Aalbers, 2018). The term is used in relation to the phase of capitalist political economy that followed the demise of the Keynesian–Fordist regimes of the post-war era, and is generally associated with the promotion (often by the state itself) of new markets and of market rationality, and consequently the retrenchment of many aspects of the welfare state and of state intervention in the economy (Brenner et al., 2010a, 2010b; Wacquant, 2010). There are two key aspects of this that help us link the level of macro political economy with the level of policy change (the latter being the chief concern of this article).

First, the centrepiece, internationally, of the shift towards neoliberal economic policy has been a shift in macroeconomic policy, particularly when faced with economic slumps, that is the move away from counter-cyclical Keynesian demand stimulus to a focus on the reduction of government debt and deficits to stimulate a resurgence in private investment and price stability (Blyth, 2013). Wolfgang Streeck (2014) conceptualizes this as the shift towards the ‘consolidation state’, where states, who increasingly turn to financial markets to finance expenditure, are subject to the pressures of maintaining ‘market confidence’ in their creditworthiness. This shift has played an important role in the development of Irish social and economic policy, as evidenced in the harsh austerity measures of the 1980s and again in the wake of the financial crisis (Dukelow, 2011). For Ireland, it is at the level of the EU and the Eurozone where this shift is most apparent, for example in the Maastricht convergence criteria, the Stability and Growth Pact, the Troika programmes and the European Central Bank’s focus on price stability (Blyth, 2013).

Second, reducing government debt and deficit levels, particularly in recessionary times, means retrenchment and, typically, marketization (Wacquant, 2010). Norris (2016a) argues that throughout much of the twentieth century, Ireland can be understood as a ‘property-based welfare state’ as housing formed a much more important component of state intervention and public spending than the social insurance schemes that are seen as the cornerstone of more typical Western European welfare states. Thus, it is perhaps unsurprising that a very significant amount of the retrenchment and marketization witnessed in Ireland since the late 1980s has focused on this area. Indeed, virtually the entire property-based welfare state was dismantled between the late 1980s and the late 1990s, triggering an intense process of marketization that was central to the property bubble of the 2000s (Norris, 2016a). Housing policy since the 1990s has been characterized by the expansion of mortgage-backed homeownership, the residualization of social housing, tax incentives and the rolling out of public–private partnerships for the regeneration of social housing estates (Downey, 2014; Hearne, 2011; McCabe, 2011). The replacement of traditional social housing to subsidized private rental accommodation, which is the focus of the present article, is consistent with this wider trend towards marketization (Byrne and Norris, 2018).

Stepping back from the above discussion of the literatures on neoliberalism and financialization, we can identify three sets of processes of particular relevance to the rest of the article. First, the shift towards fiscal consolidation and austerity at the level of macroeconomic policy. Second, the consequent retrenchment of welfare functions and their marketization. Third, the ways in which these changes, in particular marketization, cause an increasing integration of housing into volatile financial market cycles. In the following sections, we argue that these three lenses help us to understand the relationship between the processes of neoliberalism and financialization in the case of the transformation of social housing policy, and that this is central to understanding many of the key features of the contemporary housing system in Ireland today.

Importantly, however, this did not proceed by way of a coherent, ideologically explicit set of neoliberal transformations. Instead, as (Kitchin et al., 2012: 1306) argue, policy change has tended to occur in a manner that is ‘ideologically concealed, piecemeal, serendipitous, pragmatic and commonsensical’. In analysing this ‘piecemeal’ process, our analysis of Irish social housing policy reform draws on extensive policy data, including parliamentary debates, policy documents and public spending trends, which we interrogate with reference to Hacker’s (2004: 246) ideas about how policy reformers can circumvent ‘veto points’ by foregoing large-scale reform in favour of incremental changes that he labels ‘everyday forms of retrenchment’ (see also Hacker, 2005). He identifies three mechanisms that are commonly used to operationalize this strategy:

policy drift: when an existing policy is not updated to meet changing circumstances – this can be either unintentional or the effect of deliberate agenda blocking; layering: when reformers create new policies that can subvert old institutions; and conversion: policies are repurposed to achieve different objectives than before.

These three analytical lenses are not necessarily chronological. Instead, they seek to capture the process of incremental policy change, which will of course vary across different contexts. Hacker’s focus on incremental policy change is particularly useful in relation to processes of neoliberalization which occur in ad hoc and piecemeal fashions, and thus in analysing shifting relationships between state and market which may occur without any substantial discursive or ideological shift per se. In the Irish case discussed below, however, they do follow a chronological order that corresponds to the evolution of housing policy over recent decades. These three analytic lenses are deployed below in analysing changes in the financing, provision and delivery of social housing and social housing supports over the last 30 years.

Policy drift: fiscal consolidation and social housing funding

The mid-1980s was distinguished by a significant redirection in the welfare state, housing system, taxation and the role of government more broadly, and is generally identified as the start of neoliberalization and financialization in Ireland (Dukelow, 2011; Norris, 2016a). However, the radical reforms to the funding of social housing introduced during this period were not particularly neoliberal in design. In 1987 the century-old arrangements for funding social housing by means of local government borrowing (from banks or municipal bond issues) were replaced with capital grants from central government, which covered the entire costs of building or buying dwellings in this sector. The finance minister who announced this effective ‘nationalization’ of finance for social housing explained that the rationale was to bolster the financial sustainability of the sector, which had steadily weakened during the preceding three decades. Housing development loans were traditionally serviced using a combination of rents (which reflected the cost of housing provision) and local property taxes. However, income from the former declined when these ‘cost rents’ were replaced with income-related rents from the mid-1960s, and the latter were abolished in 1979 (Daly, 1997). The whole funding system was further weakened by the introduction of sales to tenants (from the 1930s in rural areas and the 1960s in urban areas). The finance minister claimed that local authorities could no longer afford to service their housing development loans by the mid-1980s, hence their abolition and replacement with capital grants. Perhaps cognizant of the widespread political support for social housing (certainly compared to the UK), he also felt obliged to assure members of parliament that these reforms would have ‘no adverse effect on the amount of funds available’ for social housing provision (MacSharry in Dáil Éireann, 1987, vol. 374, no. 2, col. 344).

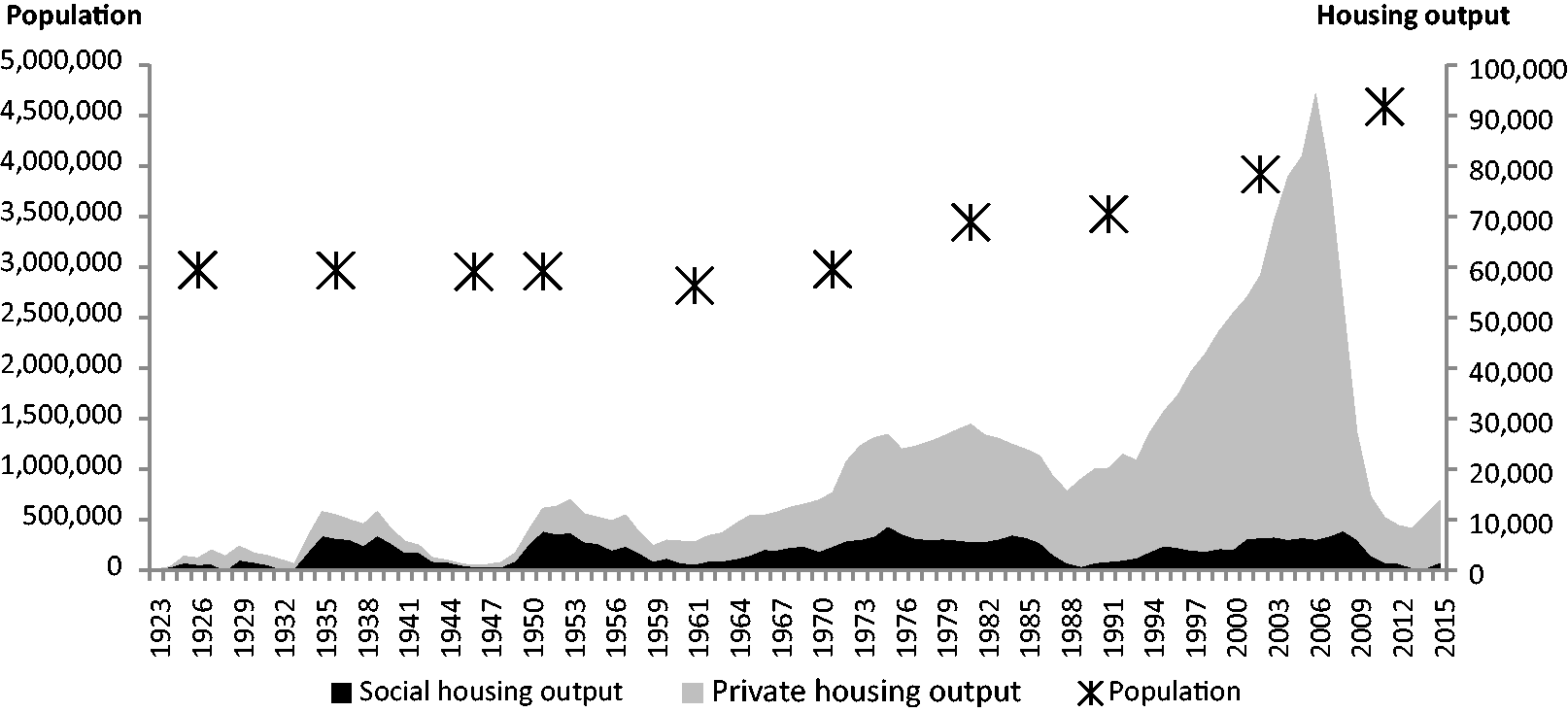

Figure 1, which compares social and private housing output in Ireland since the foundation of this state in 1922, demonstrates that in the short term this prophecy proved incorrect. Social housing funding and therefore output declined sharply following these funding reforms (from 6523 dwellings in 1985 to just 768 in 1989), which is not surprising in view of the weakness of the public finances throughout the late 1980s. Social housing accounted for just over half of total housing output in the 1930s and 1950s but, as private housing output grew, social housing’s relative contribution contracted to 11.0% of the total in the 1990s and 8.7% during the first half of the 2000s (see Figure 1). The combination of this relative decline in social housing output and sales of these dwellings to tenants effected a marked decline in the proportion of households accommodated in this tenure – which fell from 18.4% of households in 1961 to 9.7% by 2011 (Central Statistics Office, various years).

Population and social and private housing output in Ireland, 1923–2014.

This relative decline in social housing provision, in the context of an unprecedented economic and housing market boom and overflowing exchequer coffers, is related to the way in which the nationalization of funding for the sector facilitated what Hacker (2004, 2005) calls ‘everyday forms of retrenchment’. The use of public capital grant funding constrained investment because, like all capital projects, social housing is a ‘lumpy good’ that requires very high spending during the delivery phase. Raising loans or bonds that are repaid in small instalments distributes these costs over the long term and thereby renders them more affordable (Whitehead, 2014). Grant funding has the opposite effect – by paying most social housing delivery costs ‘up front’, this arrangement naturally restrains output rates by rendering it less easily affordable. Output was further restrained by the fact that these capital grants were funded entirely from central taxation, and consequently social housing had to compete for funding with all other public services. Nationalization of social housing finance also centralized control over investment decisions, which historically has been associated with retrenchment of this sector. Daly’s (1997) history of the housing ministry reveals consistent, but usually unsuccessful, efforts by civil servants to control ‘reckless’ borrowing by local authorities for social house building prior to the advent of grant finance.

Fiscal consolidation, especially reducing local authority borrowing, rather than any overt political hostility to the sector, drove the relative reduction in funding and output from the late 1980s. This has been the case to an even greater extent in terms of the government response to the post-2008 recession. Under the series of austerity budgets introduced in the wake of the crash, exchequer funding for social housing provision fell by an incredible 88% between 2008 and 2014, and output contracted from 7588 units in 2008 to just 642 units in 2014 (see Figures 1 and 2). For Murphy and Mercille (2015), this austerity constituted a ‘deepening of neoliberalism’, but Honohan (1992) argues that the focus of cuts on capital spending also reflects political expediency and practical imperatives. ‘Deferring’ capital spending is politically more palatable than cutting revenue spending by making public servants redundant and also more practicable than reducing spending on social security benefits during a recession, when unemployment is likely to be rising.

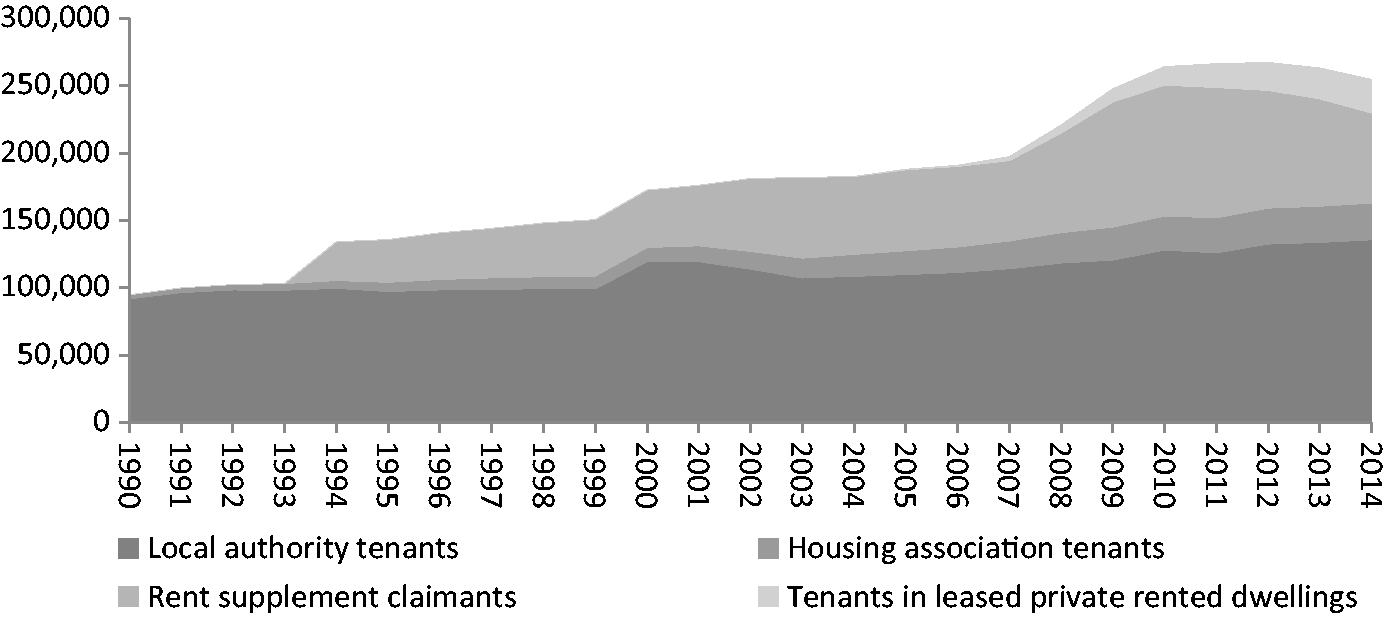

Households in social housing, private rented housing leased by government and in receipt of rent supplement and housing assistance payment, 1990–2014.

Policy layering: marketization and rent supplement

In tandem with the general contraction of the mainstream social housing tenure, its role was also slowly subverted by another response to the housing needs of low-income households – rent supplement, a cash subsidy towards the cost of benefit-dependant, private renting households’ rent. Rent supplement was introduced in 1977 and at the time was seen as a progressive and modernizing policy reform rather than a neoliberal one. The new payment replaced the ad hoc and discretionary contributions to rent provided under the ‘home assistance’ benefits system that had developed from the Victorian Poor Law and workhouse system (McCashin, 2004). The Labour Party minister who introduced the reform told parliament: ‘I regard this as an important step forward in the development of the social services and one that is long overdue. The Poor Law was the legal embodiment of the attitudes of the last century, harsh and unfeeling attitudes which should have no place in the society of today’ (Cluskey in Dáil Éireann, 1975, vol. 282, no.7, col. 1330). The same minister also oversaw a significant expansion of the (by Western European standards) minimalist Irish social security system, including the introduction of a range of benefits for lone parents for the first time (McCashin, 2004).

Take-up of rent supplement was initially very low, but it increased radically from the late 1990s as social housing output failed to keep up with population growth. Between 1994 and the peak of the property boom in 2006, rent supplement claimant numbers increased by 108%, whereas the number of social housing tenants increased by just 23.6%. Notably, by the early 2000s the primary driver of rising rent supplement claims was not new claimants but rather the lengthening duration of existing claims (and therefore falling rates of exit). By 2005, 55% of claimant households had relied on rent supplement for 18 months or longer (Norris and Coates, 2010). Thus, this benefit was transformed from a temporary housing support into a long-term one and therefore a de facto or ‘quasi-social housing’ sector, albeit a marketized one without the lifetime security of tenure rights enjoyed by mainstream social tenants (because rent supplement is withdrawn when claimants enter employment) (Hearne and Murphy, 2017). This gradual development introduced and normalized the policy of subsidized private rental housing, and thereby as Hacker (2004) predicts this ‘policy layering’ subverted or replaced traditional arrangements for housing low-income households by providing social housing. This policy layering also paved the way for the more recent, radical changes discussed below.

Policy conversion: housing assistance payment and leasing of private rented housing

While social housing finance was subject to very little analysis by policy-makers between the reform of these arrangements in the mid-1980s and the GFC in the mid-2000s, rent supplement was very regularly reviewed during this period (e.g. Department of Social and Family Affairs, 2006; Inter-Departmental Committee, 1999; Review Group, 1995). These reviews highlighted several problems, including:

rising claimant numbers due to rising benefit dependency (in the 1990s) and lengthening average claim duration (during the early 2000s); the related problem of the ‘unemployment trap’ as the benefit is withdrawn entirely once recipients enter full-time employment; rising costs for the Exchequer due to growing claimant numbers and increased average claim costs (which rose faster than general rent inflation throughout the 1990s); and rent supplement’s role in supporting inflation across the private rented market, claimants’ difficulty in finding landlords willing to accept the benefit and insecure and poor-quality accommodation.

From the mid-2000s a series of reforms was introduced to address these concerns. These reforms converted rent supplement from what was effectively (but unofficially) a form of quasi-social housing into an officially sanctioned replacement for social housing. However, unlike traditional social housing it does not provide security of tenure or a guarantee of affordable rents. Therefore it provides little of the insulation from the market enjoyed by mainstream social housing tenants (Hearne and Murphy, 2017).

This process saw the establishment of the housing assistance payment (HAP) in 2014, primarily in an effort to address the unemployment trap associated with rent supplement. Like rent supplement claimants, HAP claimants rent private dwellings and their rent is paid by the government, but unlike the former the latter continue to receive a subsidy towards rent costs if they enter employment (albeit at a reduced level). In addition, a series of schemes to lease private rented accommodation for re-letting to rent supplement recipients and applicants for social housing have been established since the mid-2000s and generated a veritable ‘alphabet soup’ of acronyms (including RAS (Rental Accommodation Scheme) and SHCEP (Social Housing Current Expenditure Programme)). The total number of private renting households in receipt of HAP and living in these leased dwellings increased from 505 in 2005 to 22,020 in 2014 – this accounted for approximately 7% of all private rented tenancies at the latter date; if rent supplement claimants are added, just under one-third of all private renting tenancies were receiving these government subsidies in that year (Central Statistics Office, various years) (see Figure 2).

By the standards of Wacquant’s (2010) analysis of the key features of neoliberalism, these are neoliberal policy reforms. They promote market solutions to social problems – indeed, supporting the expansion of the private rented sector is one of the explicit objectives of RAS (Norris and Coates, 2010). They also facilitate retrenchment of the welfare state both in terms of reducing public spending (total spending on mainstream social housing, rent supplement, HAP and leasing declined by just over half between 2007 and 2014) and reducing social rights (Department of Public Expenditure and Reform, various years). Notably, from the perspective of the latter concern, the Housing (Miscellaneous Provisions) Act, 2009 defined rent supplement, HAPs and leasing arrangements for private rented tenants as legally equivalent to mainstream social housing despite the marked difference in tenants’/claimants’ associated rights. Furthermore, recipients of RAS, HAP and SHCEP are removed from the waiting list for access to mainstream social housing on the grounds that their ‘long-term’ housing need has been met.

Despite their neoliberalizing impact, these reforms were rarely if ever explicitly legitimated with reference to neoliberal ideology. Indeed, they were very rarely debated at all by policy-makers – most were not debated in parliament and between the late 1970s and the late 2000s the Housing Ministry published no comprehensive policy statement that signalled the new overall direction of policy for all housing tenures. Instead, as Wacquant (2010) predicts, the introduction of RAS, HAP and leasing was justified on ‘efficiency’ and ‘value for money’ grounds in a series of technocratic reports. Their logic, however, clearly builds on the marketization involved in rent supplement. It does so by fully changing the meaning of social housing such that subsidized private rental housing is now part of this sector. This is the case in spite of the fact that subsidized private housing is provided by market actors (landlords) on a for-profit basis, priced according to the market rate, and does not provide lifetime security of tenure or indeed security of tenure of any sort (Hearne and Murphy, 2017). Subsidized private rental housing is now included in the government’s official social housing targets and figures, giving rise to widespread consternation among journalists, as it is no longer clear how much social housing (in the traditional sense) is actually being provided (Daly, 2018).

Embedding housing in financial cycles

The housing policy transformations discussed thus far have played a significant role in the process of financialization. Of course there are many facets and indeed drivers of this process. However, as most attention has focused on the role of capital flows (Ó Rian, 2016), banks (Kelly, 2014) and mortgage markets (Downey, 2014), taking a closer look at the impact of social housing policy can help further understand this process. This is particularly the case during the current housing market cycle (which began in approximately 2014), where the mortgage market has remained largely inactive and therefore the current phase of financialization looks rather different.

The key process we identify is that as social housing policy shifts towards the subsidization of private rental housing, it has embedded a growing segment of households within financial market cycles. This has played into these cycles, intensifying both boom and bust phases. It has also impacted of course on housing, in terms of its availability, affordability and quality. Given space constraints, however, our focus will be on how the policy transformations have fed into financial market cycles. This can be broken down into four dimensions.

First, by limiting the output of social housing in relative terms it directly enabled financialization by forcing more low- to middle-income working households into the housing market. Not surprisingly in the context of unprecedented rates of house price inflation, Figure 2 reveals that many of these households were pushed into the private rented sector, which accommodated just 8.1% of households in 1991, but expanded to include 18.6% of household by 2011. Declining homeownership rates have also driven the growth of the private rental sector.

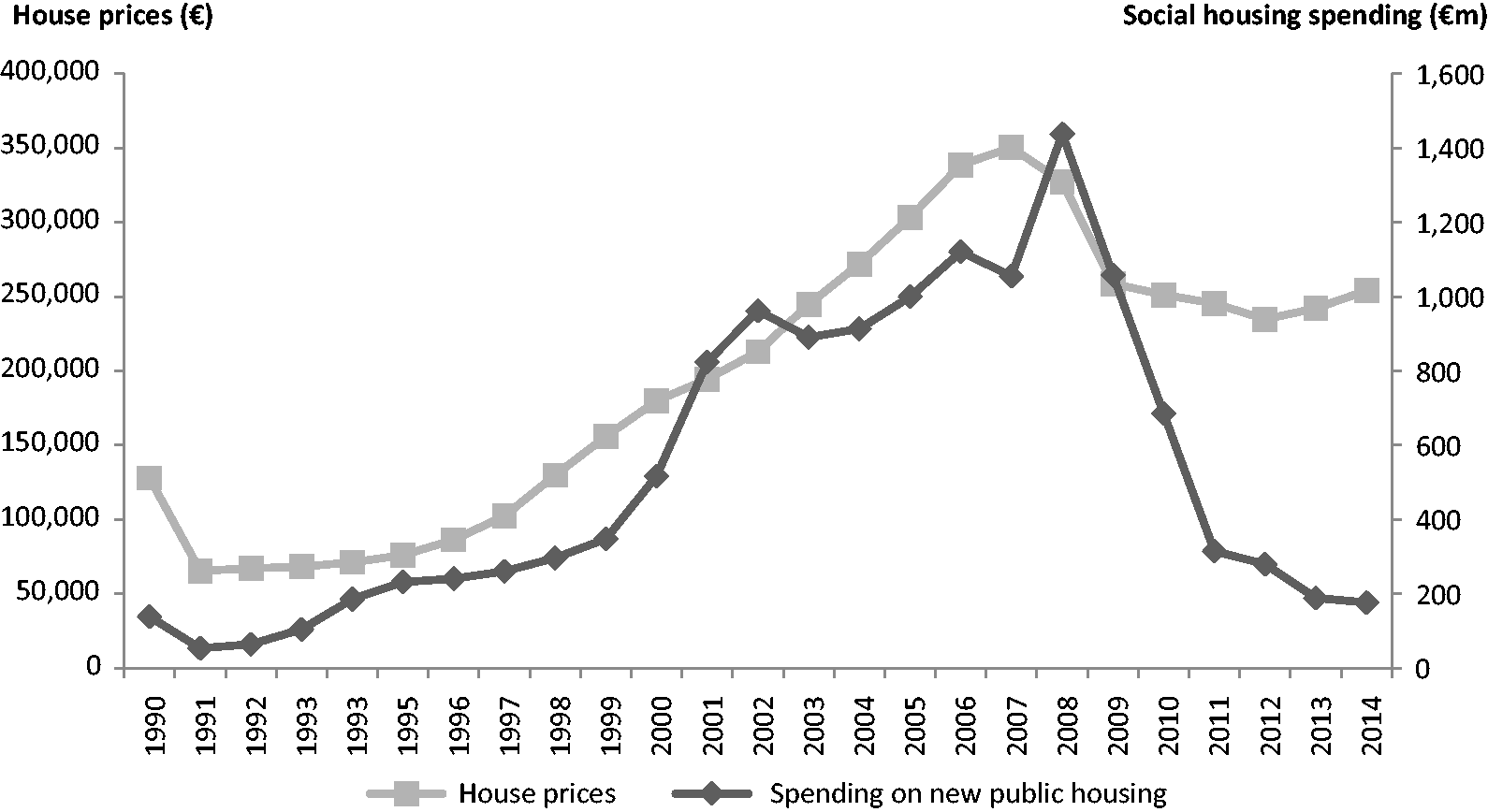

Second, the reforms made to social housing financing methods in the mid-1980s tied social housing output to market cycles. Figure 3 demonstrates that capital grant finance for social housing increased as the housing market boomed and collapsed in tandem with the market (see also Byrne and Norris, 2018). Indeed, there was a direct relationship between the two because property market-related tax revenue doubled during the first half of the 2000s and therefore helped to fund increased social housing output (Norris and Coates, 2014). When the Irish economy started to bust from 2007, falling house prices and house building rates were key drivers of falling employment and tax revenue and the weakening financial position of the banking sector. The cuts to social housing funding and output instituted at this time therefore also had a strongly pro-cyclical impact and helped to accelerate the bust (Byrne and Norris, 2018). By contrast, for example, during the economic and fiscal crisis Ireland suffered in the 1950s, borrowing had enabled governments to intervene counter-cyclically in the housing market by increasing social house building and thereby stimulating employment (see Figure 1) (Norris, 2016a).

House prices and public spending on new social housing provision, 1990–2014.

Third, the growth of rent supplement and other rent subsidies contributed to the expansion of private landlordism by subsidizing rents, thus inflating the yields in the sector. Prior to the mid-1980s, investment in private rented housing was not really a viable business proposition. Rent supplement increased private landlords’ profits by directly subsidizing a large proportion of private rented tenancies (around one-third of the total nationally during the late 1990s and early 2000s, but much more in low-rent urban areas) and also indirectly by effectively guaranteeing almost all landlords a minimum return (because they knew they could let their property for the relevant rent supplement rate). 1 More broadly, rent supplement thus acted as a ‘floor’ under rents, particularly in districts where this benefit subsidizes a large proportion of private tenancies (Department of Social and Family Affairs, 2006; Inter-Departmental Committee 1999).

Fourth, BTL mortgages suffered a significantly higher ratio of non-performing loans during the bust phase of the last cycle (from 2010). Indeed, 18% of BTL mortgages are still in arrears and the issuing of BTL mortgages remains low. The rapid expansion of BTL mortgages at the peak of the crisis contributed to the depth of the bust and the large debt-overhang, which, as noted by Turner (2017), is a key feature of financial crises.

A rapidly expanding and heavily subsidized private rental sector has played an important role in both the Celtic Tiger financial and housing market cycle and in the present phase. To begin with the former, as the property bubble reached its peak in the mid-2000s, growing homeownership gave way to a resurgence in the rental sector. Irish census data show that homeownership declined between 2002 and 2006 – from 79.7% to 77.2% of households. However, the most intense period of change came between 2006 and 2011, when the private rented sector expanded from 11.2% to 18.6% of households and owner occupation from 77.2% to 70.8% (Central Statistics Office, various years a). Housing affordability was an important factor here. Although, as Downey (2014) notes, loan-to-value, loan-to-income and mortgage maturities grew throughout the period, the gulf that opened up between wage growth and house price growth inevitably led to affordability issues. As such, a growing proportion of low-income households were left behind by the ‘homeownership dream’ and became a new generation of renters. Most importantly, BTL mortgages were introduced in the early 2000s. At the peak of the bubble, between 2004 and 2006, the proportion of outstanding mortgages held by homeowners fell by 6.7% while the proportion held by landlords expanded by 6.3% (Norris and Coates, 2014). What this suggests is that BTL investors piled into the housing bubble, thus driving house prices beyond the reach of first-time-buyers.

There is also emerging evidence that these policy reforms are supporting a new phase of financialization of the Irish housing market, which has emerged since the GFC, particularly in the private rented sector. Average rents nationally have increased a staggering 75% since 2012 and in 2018 surged 34% past their previous peak (Byrne, 2018). Sharp increases in rents, in the context of a growing sector, has been central to the wider recovery in the housing market and in residential investment over the last number of years (Savills, 2017). Forrest and Hirayama (2015: 233) argue that across the Anglophone world ‘a more vigorous, financialised private landlordism has emerged from the debris of the subprime meltdown’ and this development has been particularly strong in the Irish case. Since the GFC, BTL mortgage lending (and homeowner lending) has contracted significantly and the proportion of landlords purchasing with cash/equity investment has increased. It is particularly notable that a large proportion of investment in the rental sector currently takes the form of equity-backed purchases by private equity firms, REITs and international property companies (Savills, 2017). These intuitional investors accounted for 3.6% of all residential property purchases and 22.5% of all residential landlord purchases in 2010, but this rose to 15.5% and 48% respectively by 2017 (Central Statistics Office, various years b). These developments were precipitated by the difficulties that homeowners and domestic small residential landlords had in accessing credit after the GFC. They were also driven by the widespread sales of property development loans, sites and buildings to international institutional investors, particularly by the ‘bad bank’ established to recapitalize Ireland’s bust banking system (Byrne, 2015). However, these developments may be reinforced by the latest government supports for low-income renters. The latest iteration of the government’s rented housing leasing schemes has been specifically designed to target these institutional investors and the business sections of the newspapers are replete with announcements of funds and companies that have been established to take advantage of these subsidies (Burke, 2018; Horgan-Jones, 2016).

Conclusions

Social housing policy in Ireland has evolved over several decades into a significantly marketized tenure that relies on, supports and expands the private rental sector. The fiscal crises of the mid- and late 1980s served as the backdrop to this transformation of Ireland’s unique ‘property-based welfare state’ through the marketization of mortgage provision and the centralization and de-privatization of social housing finance. Both of these developments, in different ways, fed into the housing and property boom. In terms of our focus here – social housing policy – the long-term effect was a net reduction in the proportion of social housing and a consequent growing reliance on subsidized private rental accommodation. Subsidized private rental sector was established as a stop-gap measure that pre-dated the era associated with neoliberalism, but evolved in an ad hoc fashion as a fully fledged market-based substitute for social housing, or ‘quasi-social housing’ as we refer to it above. This in turn played an important role in the expansion of the private rental sector and therefore in the growth of the BTL mortgage sector and asset price inflation, particularly during the peak years of the boom.

The analysis presented above reveals that although the different individual measures were not accompanied by an explicitly neoliberal discourse, collectively they effected neoliberal outcomes. Taken together, the proportion of households accommodated in social housing or government-supported private rented housing remained static during this period. The proportion of households living in social housing declined, however, while reliance on subsidizing private rented housing increased markedly during the Celtic Tiger (see Figure 2). This trend intensified after the GFC as austerity policies strongly undermined social housing provision.

Through this approach the paper adds to our understanding of Ireland’s experience of housing financialization. Analysis of the financialization of housing in Ireland, and indeed internationally, has focused heavily on mortgage market deregulation, the credit and house price boom it enabled and the consequent increase in debt among homeowners. However, this article has demonstrated that the neoliberalization of social housing also played a key role in enabling this country to compensate for its late start in financialization and underdeveloped credit markets in the early 1980s, and transition to a highly financialized and hyper-competitive credit and private housing market by the late 1990s. Falling supply of mainstream social housing (in relative terms) and increased reliance on rent supplement-supported private rented housing to accommodate low-income households supported the lending to residential landlords, which was an important driver of mortgage credit growth during the house price boom and also one of the key sites of financial product innovation during this time.

The neoliberal reframing of social housing thus played a significant part in the volatile financial market cycles experienced by Ireland in recent years. The related policy changes did not, however, take shape in the form of either a coherent ideological project or a coherent suite of policy measures, but rather through the kind of piecemeal, ad hoc and typically ‘pragmatic’ processes identified by Kitchin et al. (2012). Moreover, this has taken place in the context of the decomposition of the Irish property-based welfare state and the particular political context of Ireland, characterized by the absence of widespread open hostility to social housing. This draws our attention to the variegated nature of both neoliberalism and financialization. In relation to neoliberalism, recent analysis by Di Feliciantonio and Aalbers (2018) introduces the idea of neoliberalism’s ‘prehistories’. They use this term in relation to the Mediterranean region and in particular the housing policies of Italy and Spain. In these countries, key features of neoliberalism, in particular the promotion of homeownership and the residual role of social housing, were already present under the post-war fascist regimes. Far from representing a rupture with allegedly more typical Keynesian–Fordist regimes, neoliberal housing policies built on and extended existing features of housing policy and political economy. Similarly, in the Irish context, Kitchin et al. (2012) advance the concept of ‘path amplification’ to conceptualize how recent Irish housing and planning policies build on the specific post-colonial context of Ireland (see also Norris, 2016a). These analyses are also salutary when it comes to conceptualizing financialization, a process that interacts with, works through and reshapes existing institutional structures and policy regimes (Aalbers, 2017b). Examining the unfolding of the processes of ‘drift’, ‘layering’ and ‘conversion’ can illuminate how neoliberal policy transformations interact with the further embedding of housing in financial logics and processes, particularly by highlighting how the former has enabled and facilitated the latter.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.