Abstract

This paper demonstrates the infiltration of finance into increasingly niche real estate sectors, taking the example of the emergent Canadian purpose-built student accommodation (PBSA) sector since 2011. Drawing on a novel database of PBSA, qualitative document analysis, and key informant interviews, we uncover the business strategies and geographic patterns of investment in the sector. We then consider the local impacts of this phenomenon in Waterloo, Ontario, the country’s largest PBSA market, where finance-driven new-build studentification has contributed to higher housing costs and age segregation. This process of financialization has differed from other housing sectors as it depends on the creation of new student housing to provide an avenue for investment therein. At the same time, finance-driven new-build studentification functions as a spatial fix by directing investment to secondary cities. However, this process has been fragile, marked as much by failure as success, pointing to the limits of financialization.

Introduction

Purpose-built student accommodation (PBSA) has recently moved from an obscure sector to a mainstream worldwide asset class, with a record US$16.4bn invested in existing stock globally in 2016, topping the previous year’s record of US$15bn. Of this, the US and UK, widely considered the most established national PBSA markets, attracted roughly US$10bn and US$4bn respectively. Meanwhile, from 2013–2016, Canada attracted less than US$200 million. This is a disproportionately small amount, especially given that the Canada Pension Plan is a major PBSA investor abroad (Savills, 2015, 2016, 2017). Seeing the opportunity in underdevelopment, financial investors began in 2011 to create a market for PBSA in Canada, focusing on the luxury end of the sector and targeting secondary markets in southern Ontario.

We explore the financialization of private PBSA in Canada, documenting the business strategies of investors, its geographic concentration, and impacts on patterns of inequality in urban space. Our work brings together literature exploring the financialization of housing and rental apartments (e.g. Aalbers, 2016; August and Walks, 2018; Fields, 2015; Teresa, 2015), and work on student-oriented gentrification, or ‘studentification’ (Revington, 2018; Smith, 2005), to make two interrelated arguments. First, we argue that financial investment into niche sectors like PBSA has required finance to ‘make a market for itself’ through the physical creation of PBSA assets within the private sector. While ‘new-build studentification’ (Sage et al., 2013) has elsewhere been driven by student demand for housing in today’s knowledge-based economy (Foote, 2017; Moos et al., 2019; Nakazawa, 2017), we find in Canada that finance-driven demand for an investment product is propelling the creation of PBSA. Second, we extend Smith and Holt’s (2007) argument that studentification installs the cultural practices of gentrifiers in ‘provincial’ or ‘secondary’ cities. Beyond cultural practices, financialized PBSA provides new opportunities for capital investment in the built environment of secondary cities, offering a product that is differentiated from generic rental housing. Financialized PBSA, therefore, functions as a spatial fix, with implications for segregation, displacement, and affordability at the local neighbourhood scale.

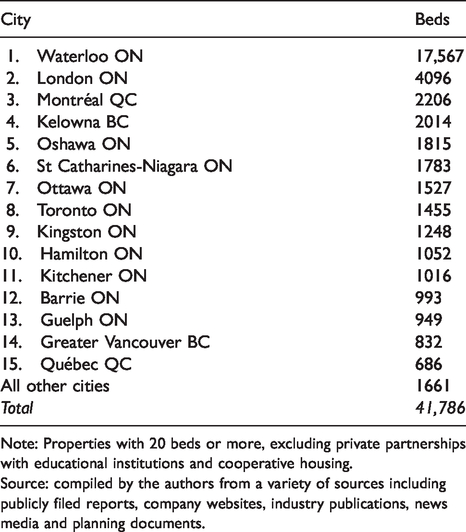

We begin by framing our study within literature on financialization, housing, and studentification. We then document the financialization of student housing in Canada, examining the business strategies and geographical investment patterns of the firms that are reshaping this sector. Next, we turn to a case study of Waterloo, Ontario, where five finance-backed firms have acquired 4259 beds in PBSA since 2012. Waterloo is a critical case, as it has the most advanced and most ‘financialized’ PBSA market. Home to the University of Waterloo (UW) and Wilfrid Laurier University (WLU), the city of 133,000 (within an urban region of 560,000) contains 42% of private PBSA in Canada – over 17,500 bed spaces. Our analysis asks what factors cultivate investor interest in student housing, and how this phenomenon affects student renters and the communities in which they live and study.

Financialization from home to dorm

Financialization has a variety of meanings (e.g. Christophers, 2015; French et al., 2011), but broadly refers to the increasingly dominant role of finance within global capitalism since the 1970s (Epstein, 2005; Krippner, 2005). Aalbers (2016: 2) defines it as ‘the increasing dominance of financial actors, markets, practices, measurements and narratives, at various scales, resulting in a structural transformation of economies, firms (including financial institutions), states and households’. With this process, non-financial sectors of the economy and daily life are being drawn into the orbit of finance, and made subject to its logics and practices (Foster, 2007; Martin, 2002). As a result, decision-making is increasingly shaped to align with the interests of investors, with a focus on delivering higher yields and building shareholder value, at the expense of other objectives (Erturk et al., 2008; Froud and Williams, 2007). In the case of real estate, treating properties as pure financial assets to be managed and traded to drive earnings for investors undervalues the social value of land, properties, and housing, and their usefulness for providing homes, places of refuge and sites for building community (Rolnik, 2013).

Scholars studying the financialization of property have called real estate assets ‘quasi-financial’ (Coakley, 1994) because they include physical structures that are spatially fixed, infrequently bought and sold, illiquid and not easily comparable (Gotham, 2006, 2009). Innovations to securitize real estate that emerged in the 1980s overcame these limitations by rationalizing buildings and properties into legible and tradeable commodities. Real estate investment trusts (REITs) and other innovations have transformed ‘illiquid commodities into liquid securities’ which can be bought and sold in capital markets (Gotham, 2009). REITs pool the capital of many shareholders to acquire portfolios of income-producing real estate assets. Investors buy shares of the total portfolio rather than an individual property, spreading risk over diverse assets and geographic areas, and eliminating the need for investors to have the local knowledge and expertise necessary for direct investment in real estate. Income is distributed to shareholders who can now treat real estate as an easily exchanged financial asset (Gotham, 2006; Waldron, 2018). August and Walks (2018) use the term ‘financialized landlords’ to refer to REITs and similar financial vehicles including private equity funds, institutional investors, and asset management firms that acquire rental housing properties. These entities differ from traditional landlords in that they aggressively manage housing as financial assets, affecting tenants but also remaking the sector for investors (August, forthcoming) – a process Ward and Swyngedouw (2018) call ‘assetization’.

Recent literature demonstrates how housing is central to financialization (Aalbers, 2017). Much of this has centred on single-family housing and homeownership, examining home loans, credit scoring, and mortgage securitization (e.g. Aalbers, 2016; Gotham, 2009; Walks and Clifford, 2015). Researchers have linked the financialization of housing with the global financial crisis and subsequent restructuring of housing and financial markets, and demonstrated how predatory lending and the foreclosure crisis targeted harm towards low-income, racially marginalized and disadvantaged homebuyers (e.g. Greece: Alexandri and Janoschka, 2018; Spain: García-Lamarca and Kaika, 2016; US: Wyly et al., 2006). Recently, financial firms have begun to target rental housing, intensifying ties between local properties and global finance (August and Walks, 2018; Beswick et al., 2016; Fields, 2015; Fields and Uffer, 2016; Teresa, 2015; Waldron, 2018; Wijburg et al., 2018). Tenants are often subject to harassment, eviction and reduced quality of life in buildings that are aggressively managed to deliver investor profits, which intensifies gentrification and deepens patterns of socio-spatial inequality (August and Walks, 2018; Fields, 2015; Fields and Uffer, 2016; Teresa, 2015).

The financialization of housing is related to the over-accumulation of capital in need of new avenues for profitable investment (Aalbers, 2016). Finance lubricates the switching of capital into real estate – or subsectors thereof (Charney, 2001) – to provide a temporary sectoral ‘fix’ (Beauregard, 1994; Harvey, 1982, 1985), but the financialization of housing also offers a ‘financial fix’ (Aalbers, 2016: 95) by promoting the circulation of capital in housing-backed securities. The financialization of new housing sub-sectors, and in new geographic contexts, can also be seen as a form of spatial fix, as in the case of inner-city mortgage lending in the US (Wyly et al., 2004) and debt-fuelled, speculative real estate investment in the European periphery (Alexandri and Janoschka, 2018; Byrne, 2016a, 2016b; García-Lamarca and Kaika, 2016; Waldron, 2018) in the lead-up to the global financial crisis. These dynamics are intrinsically linked to uneven development, as unevenness creates both opportunities for, and impediments to the profitable redeployment of capital (N Smith, 2008).

Financialization in new geographies and sectors implies the creation of markets. Interdisciplinary researchers have shown that markets – far from being natural phenomena – are socially constructed by a variety of actors and circumstances (Berndt and Boeckler, 2009). For example, interventions by the state have been crucial in enabling mortgage securitization and the formation of REITs (Gotham, 2006; Waldron, 2018) while promoting homeownership and marginalizing the social-rental sector (Alexandri and Janoschka, 2018; García-Lamarca and Kaika, 2016; Walks and Clifford, 2015). Private sector actors, meanwhile, engage in developing standardized techniques to measure and manage new types of assets (Fields, 2018). These market-making efforts have opened up new fields to investment and have enabled the development of new institutional architecture for financial vehicles that can harvest new sectors of the economy for profit with increasing sophistication.

Paralleling the transition of the multi-family rental market from the province of ‘mom and pop’ landlords to the domain of large-scale financial actors has been the emergence of ‘new-build studentification’ (Sage et al., 2013). Studentification entered the academic lexicon following a rapid rise in post-secondary enrolment in the UK during the 1990s, to describe the concentration of students in neighbourhoods near universities. Smith (2005) linked studentification with gentrification, outlining the economic, social, cultural, and physical changes that accompany a rise in student population. University life shapes both the class position and consumption preferences of ‘apprentice gentrifiers,’ as students inhabit locales consonant with social and cultural student identities (Smith and Holt, 2007; see also Chatterton, 1999). These authors see studentification as a central component of gentrification in secondary cities with universities.

In the UK, financialization of student housing first followed an ‘investification’ model (Hulse and Reynolds, 2018), in which one-off investors accessed buy-to-let mortgages (Leyshon and French, 2009) to purchase shared houses as income properties to meet increased student housing demand. This process was superseded in the mid-2000s as corporate investors entered the PBSA sector (Hubbard, 2009; Smith and Hubbard, 2014), and ‘trail blazed’ an agenda for financialization in the generic rental housing sector in the UK (Beswick et al., 2016). Local authorities also funnelled new-build studentification into designated areas, to protect established neighbourhoods from perceived issues with student housing, like parking pressures, noisy parties and physical deterioration (D Smith, 2008; in Canada, see [Revington et al., 2018]). While not always successful (Sage et al., 2013), these policies raise concerns about segregating wealthier students into higher-end purpose-built dwellings (Smith and Hubbard, 2014). The consolidation of PBSA portfolios by financialized landlords has led to increased rent levels, affecting both students and non-students in areas experiencing new-build studentification, in both the UK (Beswick et al., 2016; National Union of Students and Unipol, 2016) and the US (Laidley, 2014).

Despite the simultaneous emergence of new-build studentification and the financialization of residential real estate, studentification literature does little to expand on the role of finance. We fill this gap, exploring investor strategies and emergent geographies of PBSA in Canada, and contributing to debates on the dynamism of studentification and its links with urban processes (Foote, 2017; Moos et al., 2019; Revington, 2018; Smith and Hubbard, 2014). Student housing also presents an interesting case for scholars of financialization. Its swift rise from obscure sector to a global asset class demonstrates a trajectory that other niche residential asset classes may take (Savills, 2016). We bring these strands of scholarship together, outlining both the expansion and fragility of the financialization of PBSA.

Methods

First, we constructed a novel database identifying the location, bed count, and ownership of private PBSA in Canada. We identified PBSA through systematic internet searches specific to cities with post-secondary education institutions, a challenging task ‘since it is difficult to ascertain how PBSA is managed and controlled due to complex arrangements between organisations’ (Smith and Hubbard, 2014: 96). Where possible, details were gathered from real estate companies’ prospectuses, annual reports and other documents, either through their websites or public filings with the Canadian Securities Administrators (CSA, available at sedar.com). As not all properties are owned by publicly listed companies, and not all companies publicize the details of their holdings, we also consulted industry publications, news media, and planning documents pertaining to PBSA developments.

Second, we used qualitative document analysis to understand business strategies, geographical investment choices, and challenges facing firms. Third, to investigate impacts of this trend, we examined the case study of Waterloo, drawing on data from Statistics Canada, the Canada Mortgage and Housing Corporation (CMHC), municipal building permit records, and Waterloo’s Town and Gown Committee. Finally, we conducted semi-structured interviews (n = 20) with key informants involved in the student housing sector, between June and November 2018.

The financialization of student housing in Canada

In the US and UK, financial investors have targeted the off-campus PBSA market, which is home to 12% and 23% of post-secondary students in those countries respectively (Canadian Apartment Magazine, 2016). In Canada, only 3% of students live in such housing, positioning off-campus PBSA as an untapped market for investors. There were approximately 1.3m university students in Canada in 2017 (Universities Canada, 2017), about half living with family and 16% living in residence on campus. The remaining 33% living off-campus in rental housing are targets for the purpose-built sector (CHC, 2015b; CUSC, 2011; Vanecko, 2015).

While education is constitutionally a provincial responsibility, both the federal and provincial governments have pushed for increased participation in higher education (Kirby, 2007; Metcalfe and Fenwick, 2009). Canada is recruiting international students, hoping to attract 450,000 by 2022, a 22% increase over 2015 (Savills, 2017). These policies align with neoliberal agendas, aiming to promote growth by developing a highly educated workforce for the knowledge economy. International students are valued to generate revenue for universities to compensate for decreased public funding, and to relieve skilled labour shortages and demographic decline (Canada, 2014; Kirby, 2007; Trilokekar and Kizilbash, 2013).

State support for student housing, meanwhile, is minimal – it receives no mention in Canada’s 2017 National Housing Strategy, and state-run CMHC provides no dedicated financing for its construction. Since 2012, CMHC has offered mortgage insurance for student housing to private lenders, subject to higher premiums and other restrictions (which may be eased with institutional guarantees on the loan; CMHC, 2012). Eligible projects must be either on-campus or nearby, and were initially limited to unfurnished, self-contained units of no more than four bedrooms each off-campus. Changes in 2017 provided greater flexibility to borrowers through longer amortization periods, permissible non-residential components, and dropping restrictions on off-campus furnished suites (CMHC, 2017).

Yet demand for off-campus rental is expected to remain strong, since dormitory construction has not kept pace with enrolments, and since students typically live in dorms for one year (CUSC, 2011). There is also room to expand PBSA across Canada, beyond existing concentrations in Ontario (Table 1), and new construction is planned in Winnipeg, Hamilton, Calgary and elsewhere (Crowther, 2017; Keele, 2018; McFarland, 2018). For finance-backed firms, this landscape speaks to an opportunity to capitalize on, and indeed to create a market for PBSA, modelled after those in the US and UK.

Canada’s Largest Private PBSA Markets, 2018.

Note: Properties with 20 beds or more, excluding private partnerships with educational institutions and cooperative housing.

Source: compiled by the authors from a variety of sources including publicly filed reports, company websites, industry publications, news media and planning documents.

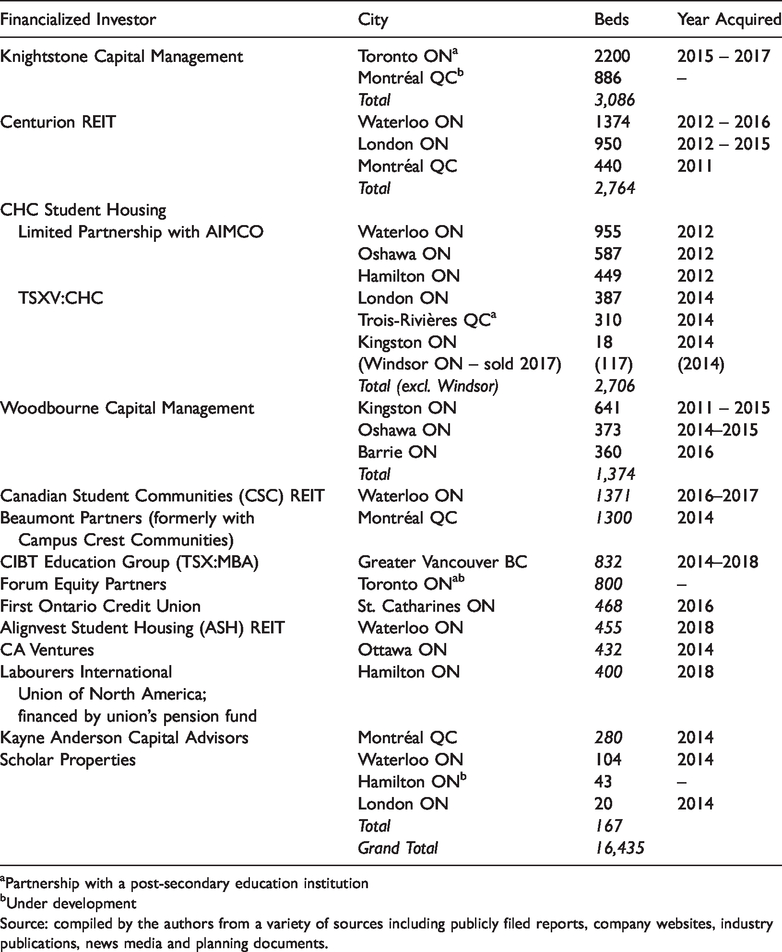

In the UK, the financialization of PBSA preceded that of other multi-family rental housing (Beswick et al., 2016). In Canada, conversely, financial investors began to transform the multi-family sector in the 1990s (August, forthcoming), while the incipient financialization of PBSA began in 2011 (Table 2). One of the first firms was Centurion Apartment REIT (2017a), which operates ten student housing properties under the brand name ‘The Marq’ with the objective of maximizing unit value and providing cash distributions to unit-holders while growing the REIT’s portfolio. Another is CHC Student Housing which includes a private partnership backed by AIMCO (which manages Alberta’s public pensions), and a public arm (TSXV:CHC), launched in 2014 (CHC, 2014; Smycorp, 2013). Private Canadian Student Communities (CSC) REIT was established in 2016 with two Waterloo buildings and the intention to expand to other cities (Marketwired, 2016). In addition to REITs, capital management firms such as Knightstone and Woodbourne have targeted PBSA for providing stable cash flow and high returns. Since 2013, CIBT Education Group (TSX:MBA), an operator of private colleges, language schools and recruitment services, has entered the student housing sector from a different angle. CIBT plans to house 10,000 students in an ‘Education Mega Center,’ ‘Global Education City’ and other developments across greater Vancouver by leveraging its contacts with 20,000 students from 42 countries to capitalize on the region’s low vacancy rate, high rents and reputation for education (CIBT, 2018; Seftel-Kirk, 2014).

Financialized Student Housing in Canada, 2018.

aPartnership with a post-secondary education institution

bUnder development

Source: compiled by the authors from a variety of sources including publicly filed reports, company websites, industry publications, news media and planning documents.

The financialization of PBSA in Canada also involves a unique ‘condo’ model, in which developers build student rental housing and sell units as investment properties, while assuming responsibility for property management and lease-up. For developers, this approach is more profitable than building first and then selling (or holding and renting out) a finished property, and it mirrors the virtual replacement, since the 1980s, of purpose-built rental construction with condominiums in Canada (Rosen and Walks, 2015). Unlike the generic condo market, however, in which owners may choose to rent out their unit rather than occupy it, in the student sector units are designed to be rented from the outset (or ‘buy to let’), and purchasers buy access to an expected income stream rather than a home – a form of ‘investification’ (Hulse and Reynolds, 2018). Local developers such as Kelowna’s Mission Group and Waterloo’s Prica Group and IN8 Developments have made extensive use of this model.

Some of Canada’s biggest financialized landlords are attentive to student housing but have stopped short of investing in PBSA. Timbercreek Asset Management, CAPREIT (Canadian Apartment Properties REIT), Mainstreet Equity (TSX:MEC), and Killam Apartment REIT – among Canada’s 12 largest landlords (August, forthcoming) – all offer dedicated webpages for students with search tools for off-campus rentals in their multi-family portfolios. Students and the low-cost housing they seek are clearly on the radar of these players as an untapped source for value extraction, whether this value is squeezed from their parents’ pockets or from their own future earnings in the form of greater debt loads.

The allure of student housing

A number of elements make PBSA attractive to investors. By-the-bed leasing generates higher returns than conventional rental housing (Smith, 2005; Smith and Hubbard, 2014) and parental guarantors reduce the risk of non-payment (CHC, 2015a). Apartments are typically arranged as four- or five-bedroom suites with shared kitchens and living areas to reduce costs. According to a partner in a student housing firm (L05), ‘the footprint of the bedrooms is much smaller than you would find in an apartment building … So, it allows us to have many more students housed in the same facility’, increasing revenue. PBSA is also seen as recession-resistant, since people return to school during economic downturns (Patterson, 2016).

Financialized landlords seek to ‘capitalize on the lack of high-end purpose-built student housing’ (Woodbourne, 2017) by ‘bringing to Canada an amenity-rich campus living experience’ modelled after the UK and Western Europe (Knightstone, n.d.; see also CHC, 2015a; Lobo, 2014; McFarland, 2018; Patterson, 2016). Unlike generic multi-family housing, in which financialized landlords purchase existing stock, the student sector includes new or freshly renovated ‘luxury’ developments. The former CEO of CHC explained that the opportunity in this sector is ‘modern student apartment buildings near campuses that include amenities … as well as parent-friendly touches such as ubiquitous security cameras’ (Perkins, 2013). Centurion’s first acquisition was ‘in a sorry state and clearly neglected’ before the company ‘injected significant capital’, installing granite counters and modernizing kitchens, bathrooms and common areas, and offering ‘premium amenities including fitness and weight training rooms, a theatre, a games room, a lounge, a study room, CCTV coverage, underground parking, and onsite staff’ (Anderson, 2013: 23-24). Knightstone (n.d.) argue the ‘spartan’, unsafe and unclean student living rite-of-passage is outdated, and that today’s generation is ‘sophisticated’, demanding ‘advanced technology, private baths, and resort-style facilities and services’. At their CampusOne residence in downtown Toronto, students pay US$1700 per room (before a meal plan), and get ‘condo-quality units … and a host of programming from yoga classes to animal-petting events’ (McFarland, 2018).

In part, luxury branding and security are meant to assuage parents’ concerns while targeting their wealth. CHC’s strategy assumes that ‘parents generally pay their kids’ rents’ (Perkins, 2013). One broker was frank about the business model: ‘Mom and Dad get shaken down to pay more rent because the kid wants a better place closer to the school, right?’ (R04). Regardless of who pays, this ‘luxury’ housing is a freshened-up version of low-cost, small, shared multi-family housing, and its rebranding allows financialized landlords to define a market and charge far more than students would otherwise be paying.

With a focus on driving revenues from a ‘luxury’ product, the ability to increase rents is important to investors. In Ontario, this is so easy that Centurion classifies student housing as ‘non-rent controlled’ (2017b: 56). Ontario restricts rent increases each year to a provincially set ‘guideline’ amount (1.8% in 2018). Rent is decontrolled, however, once a unit becomes vacant. Because of its high turnover, PBSA operators are well-poised to benefit from ‘vacancy decontrol’ (CHC, 2015a). In 2017, Centurion was unconcerned that a policy would extend rent controls to more buildings, expecting ‘virtually no impact on the student housing business’ because ‘residents move out as they graduate’ (2017a: 24).

In Canada, PBSA is also alluring because the potential market is growing. The sector is underdeveloped compared with the US and UK, and as investment opportunities flatten out abroad (Brass, 2018), a shift to countries like Canada is expected (Savills, 2015). International students are a potential source of demand (Savills, 2017), and industry watchers point to Canada’s weak currency and high university rankings as pull-factors. Meanwhile, Trump’s ‘Muslim Ban’ in the US and ‘Brexit’ in the UK may be push-factors. Indeed, 2017 saw an 11% increase in countrywide international enrolment (Bothwell, 2017).

A further appeal of Canadian PBSA is paradoxically the barriers to investment, beginning with the fragmented nature of ownership. In 2013, the CEO of CHC explained that ‘the marketplace itself is non-existent in Canada, and that’s one of the things that attracted us to it’ (Perkins, 2013). Centurion was similarly drawn to the potential for consolidation in the sector, describing it as ‘highly fragmented … with few dominant competitors, ripe for consolidation by a well-capitalized and focused acquisitions strategy’ (2017b: 55). This is in contrast to the generic multi-family sector, where competition for assets has brought down the capitalization (or ‘cap’) rate (the ratio of net operating income to asset price). As a director of one firm explained: ‘Multi-family’s full. … The whole reason for [investing in] student [housing] is that it’s got a disparate yield right now, right? We think that there’s compression in the cap rates, and we think that there’s an “oligopoly play” where you can be the dominant player in that space’ (L01). Centurion also spoke to other ‘barriers to competition’, including the need for specialized management skills; higher equity requirements to purchase large newly built properties; and the ‘niche and emerging nature of the business’ that has prevented participation by institutional investors (2017b: 55).

The perils of student housing investment

The same barriers to investment in PBSA that are prized by those who overcome them have kept financialization at bay. While the limited stock of existing properties is alluring to investors, it has resulted in what one broker referred to as ‘a terrible catch-22’ whereby ‘if there was more student housing product, there would be more buyers, but because there’s not much product to buy, there are no buyers’ (R04). Another broker concurred: ‘Other markets [aside from Waterloo] don’t have the availability, therefore don’t have the number of investors. … If they had the supply, they would have the demand’ (R03). Industry participants decried a lack of information about the sector in Canada, and the underdeveloped nature of the market means that consumers too are less familiar with PBSA (Morton, 2012; Peisner, 2014).

Firms have had to do substantial work to create this market by promoting familiarity with PBSA among financiers of construction and potential buyers, something interviewees described as ‘a big learning curve’ (R03) or an ‘extra step’ that few were willing to take (R05). Investors are wary of unproven markets, and banks have been hesitant to invest, due to their unfamiliarity with PBSA and the specialized management it requires (Morton, 2012; Peisner, 2014). Another broker lamented that financiers have ‘got to realize this is not a high-risk business as they think it is’, and the challenge is: ‘You have to teach the guy the student housing building first, before he can buy it. … The marketplace isn’t ready for something they don’t understand’ (R04). PBSA investors have also had to cultivate connections with developers. A partner at one firm explained: ‘It means we have to work with developers to really bring it along. And that’s quite similar at many university towns in Canada’ (L05).

Despite the recent spike in applications, Canada remains a minor destination for international students compared with Australia, the US, the UK and Western Europe (Statistics Canada, 2016), and many struggle to afford suitable housing (Calder et al., 2016). One broker explained that PBSA in Canada was not driven by an influx of wealthy international students: ‘A lot of people use the student visa in Canada as a way to immigrate here, right? They’re poor as heck. … They’re slumming it’ (R04). While some PBSA providers have attracted wealthy international students, most do not specifically market to them (L05, R03). Others are ‘less interested in international students’ because in the case of non-payment, ‘they’re very difficult to collect from’ without a guarantor in the country (L01). Meanwhile, Canada’s ageing population structure means new housing demand from domestic enrolment is not expected (McLerie, 2017).

Competition from the ‘condo’ model for PBSA is another barrier facing financialized landlords. Centurion’s (2017a: 26) management described the impacts: ‘Student condominiums have become hot with retail investors. As a result, a large number of the potential student sites are being built as for sale to retail investor condominiums. It makes sense for developers to do so as retail investors will pay substantially more than the REIT will for the same property.’

These barriers have kept most large players on the sidelines and have led to failure for some, demonstrating the fragility of the sector. In 2014, Campus Crest Communities, a US-based REIT, launched a joint venture in Montreal to convert two hotels to PBSA, only to sell their stake a year later based on poor performance (Kucharsky, 2015; PRNewswire, 2015). CHC’s public entity has also struggled, failing twice to raise funds for expansion (CHC, 2018), with analysts issuing a ‘distress warning’, raising ‘significant doubt’ over the firm’s ability to continue operating (The Deal, 2018). Financial difficulty is also widely rumoured to be affecting the private CSC REIT and its development arm, JD Development Group.

In response to these challenges, some operators are finding greater opportunities and less risk in public-private partnerships to build or redevelop on-campus housing (Brass, 2018; McFarland, 2018). An example is ‘The Quad’ in Toronto, where York University has partnered to build an 800-bed residence with developer Campus Suites and private equity firm Forum Equity Partners (Canadian Apartment Magazine, 2013). The dynamics of these partnerships, which differ from purely private investment in PBSA, are an important area for future study.

Geographies of student housing investment

The most obvious geographic strategy for PBSA providers is to locate near post-secondary institutions (Patterson, 2016). CHC, for instance, acquires properties within 2 km of a school (CHC, 2015a). Another strategy is to build near downtown or amenity-rich areas desirable to students, which lend themselves to a ‘student habitus’ (Chatterton, 1999; Hubbard, 2009). In London, Ontario for example, Centurion and CHC’s properties are near Richmond Row, a popular nightlife area north of the city centre.

More interesting is the concentration of PBSA in particular cities. In Canada it is largely a ‘secondary market’ phenomenon (Table 1). As one interviewee described: ‘Sudbury can be an A market, if you’re in the right location. You don’t have to go to Toronto or Montréal to be in an A market’ (L01). In the competitive landscapes of larger cities, prime sites for PBSA are outbid for other uses, such as luxury condominiums, retail, or offices (Lobo, 2014; Savills, 2016). As one broker recounted, ‘it’s hard to find the land to make it work’ in these cities ‘because other guys want to buy it. Condo guys want to buy it. Office guys want to buy it’ (R04). By contrast, in secondary markets, PBSA can outbid most competitors for good sites. A broker in Waterloo (R01) reported that for his clients, ‘the profitability here is much better than what they’re able to achieve in Toronto, so their investment dollars come here’. A developer’s representative (R06) agreed: ‘From a developer standpoint … investing in Waterloo is much easier than investing in, say, Toronto, because the input is lower.’ Furthermore, students are dispersed in larger cities, related to options for cultural consumption citywide (Allen and Farber, 2018; Malet Calvo, 2018), whereas smaller cities cannot absorb students within the existing rental stock, especially if students represent a large or rapidly increasing proportion of the population (Munro et al., 2009).

This bias towards secondary cities is not uniquely Canadian. In the UK, consultants JLL (2017: 10) found that despite a doubling of PBSA over the last decade, on a per-student basis, London faces a ‘chronic undersupply’ relative to the countrywide average. They attributed this shortfall to high development costs, competing urban regeneration projects, requirements to provide affordable units and high development charges in some boroughs. Conversely, provincial cities like Loughborough and Liverpool have high rates of PBSA provision, with the latter apparently overbuilt (Hubbard, 2009; Mulhearn and Franco, 2018). Likewise, the most active US markets for PBSA in 2018 were Tallahassee, Florida and College Station, Texas (Gunn, 2018). First-tier cities like New York, Boston, Washington DC, the Bay Area, and Los Angeles are conspicuously absent from the top 20 despite the presence of large, well-regarded institutions in these regions.

Canadian PBSA is heavily concentrated in southern Ontario. The region is one of the most densely urbanized parts of the country, with many mid-sized cities and universities located near Toronto (Addie et al., 2015). As one broker noted: ‘You can’t understate the proximity to capital markets and proximity to people with access to capital’ (L09). A partner in a Toronto-based firm explained, ‘It’s easy to get in the car and drive [to other cities in southern Ontario] if something needs to be dealt with right away, versus if we’re [invested] in Halifax or New Brunswick or Alberta’ (L05). Additionally, despite the seemingly footloose nature of financial investment in a globalized economy, locational preferences of firms are linked to the historical rootedness of their managers. All of CHC’s (2015b) directors, for example, held degrees from Ontario universities or had experience in the region, and Centurion CEO Greg Romundt graduated from Western University in London (Ruddy, 2015).

Local impacts at the leading edge: the case of Waterloo

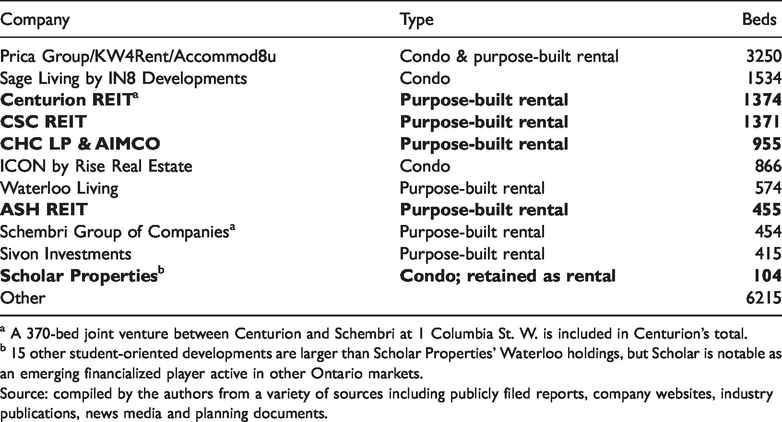

Waterloo represents the leading edge of the financialization of PBSA in Canada. Five financialized landlords own 24% of the stock (Table 3) in a market representing 42% of the country’s PBSA, with the remainder including beds run by private family firms, co-operative housing, and units in investor-owned condos. According to a local landlord and broker, financialization is a new trend. ‘Since 2003,’ he explained, ‘I’ve seen the landscape of student housing change from primarily mom-and-pop ventures to substantial interest from REITs and institutional investors in the upscale mixed-use student accommodations’ (quoted in Patterson, 2016). These developments are reshaping the community around UW and WLU, presenting a novel Canadian example of finance-driven new-build studentification.

Major Players in Waterloo PBSA (financialized landlords in bold), 2018.

a A 370-bed joint venture between Centurion and Schembri at 1 Columbia St. W. is included in Centurion’s total.

b 15 other student-oriented developments are larger than Scholar Properties’ Waterloo holdings, but Scholar is notable as an emerging financialized player active in other Ontario markets.

Source: compiled by the authors from a variety of sources including publicly filed reports, company websites, industry publications, news media and planning documents.

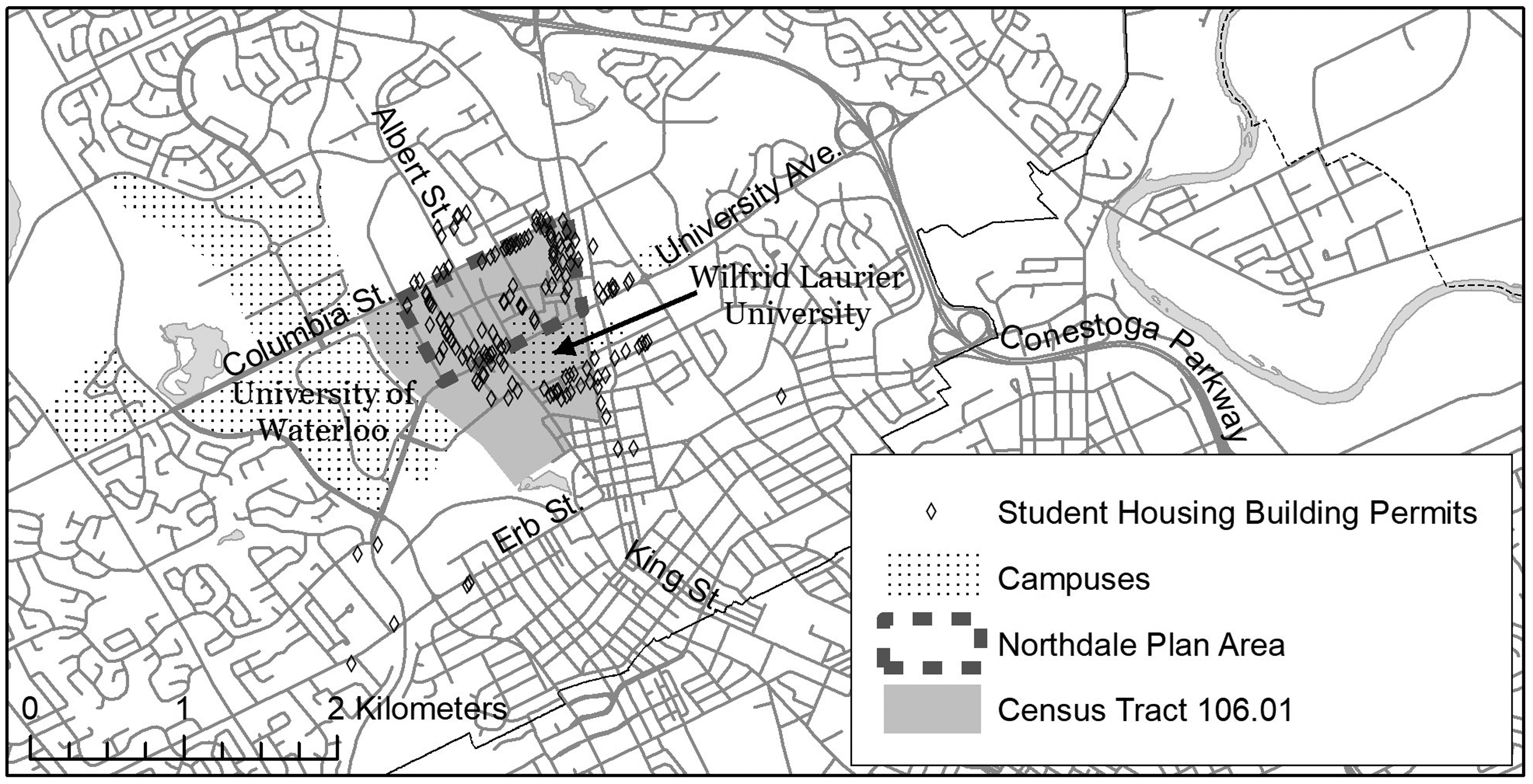

A highly concentrated Waterloo PBSA boom has taken place, with building permits issued for 15,000 bedrooms between 1997 and 2016, in a region with 40,000 university students – capacity to house 38% of students in purpose-built student housing, compared with 3% nationwide (Canadian Apartment Magazine, 2016). Some 67% of building permits fell within a single census tract, which contains the Northdale neighbourhood (Figure 1). In the decade to 2011, UW and WLU experienced growing enrolment, and developers responded by building student rental housing, often in small apartments of four units with five bedrooms each. This was followed by the construction of larger, higher-amenity buildings, even after enrolments levelled off post-2011, in line with local planning goals to increase densities and improve development in the university precinct (McLerie, 2017; MMM Group, 2012; Revington et al., 2018). Financial vehicles have targeted this newer PBSA, built or acquired since 2012. Their focus fits the recommendations of market analysts: locations with high-ranking anchor universities that ‘are “rising stars” teaching courses that the new workforce wants’, and ‘embedded in local industry’ with a focus on science, technology, engineering and mathematics (STEM) subjects, as these ‘reflect a changing global jobs market’ (Savills, 2015). In Canada, UW is the paradigmatic ‘entrepreneurial university’, internationally known for its STEM programmes, links to industry, and for training high-tech workers for both local firms and Silicon Valley (Bathelt et al., 2011; Bramwell and Wolfe, 2008; Gellman, 2016; Winter, 2013).

Student housing development in Waterloo is concentrated in and around the Northdale neighbourhood.

PBSA developments are reshaping Northdale dramatically, replacing suburban-style bungalows (often shared by students) with high-rise towers. This is leading to housing improvements for some, as previous rental options were in notoriously bad shape (Waterloo Chronicle, 2010). It is also intensifying the concentration of students into one area, a trend that reinforces patterns of gentrification and age segregation (Smith and Hubbard, 2014). For residents who remain in the area, these changes contribute to a lost sense of place (Davidson and Lees, 2010). As one long-time resident of the neighbourhood told the city council, ‘I am just appalled at what’s happened in Northdale and I’m not the first one to say that’ (quoted in Beattie, 2016), while another complained: ‘Additional concrete bunkers are still springing up faster than weeds on a wet day. If this is the future, thank goodness I enjoyed the past’ (Crockford, 2015). For others, it engenders displacement, including direct displacement of households to make way for these developments, and exclusionary displacement of future residents (Marcuse, 1986) who will be barred by high rental prices or excluded as non-students. ‘The areas around the university are beginning to look like a Monopoly board,’ remarked a 72-year resident. ‘Alas, there are too few houses for our hardworking families’ (Holmes, 2014).

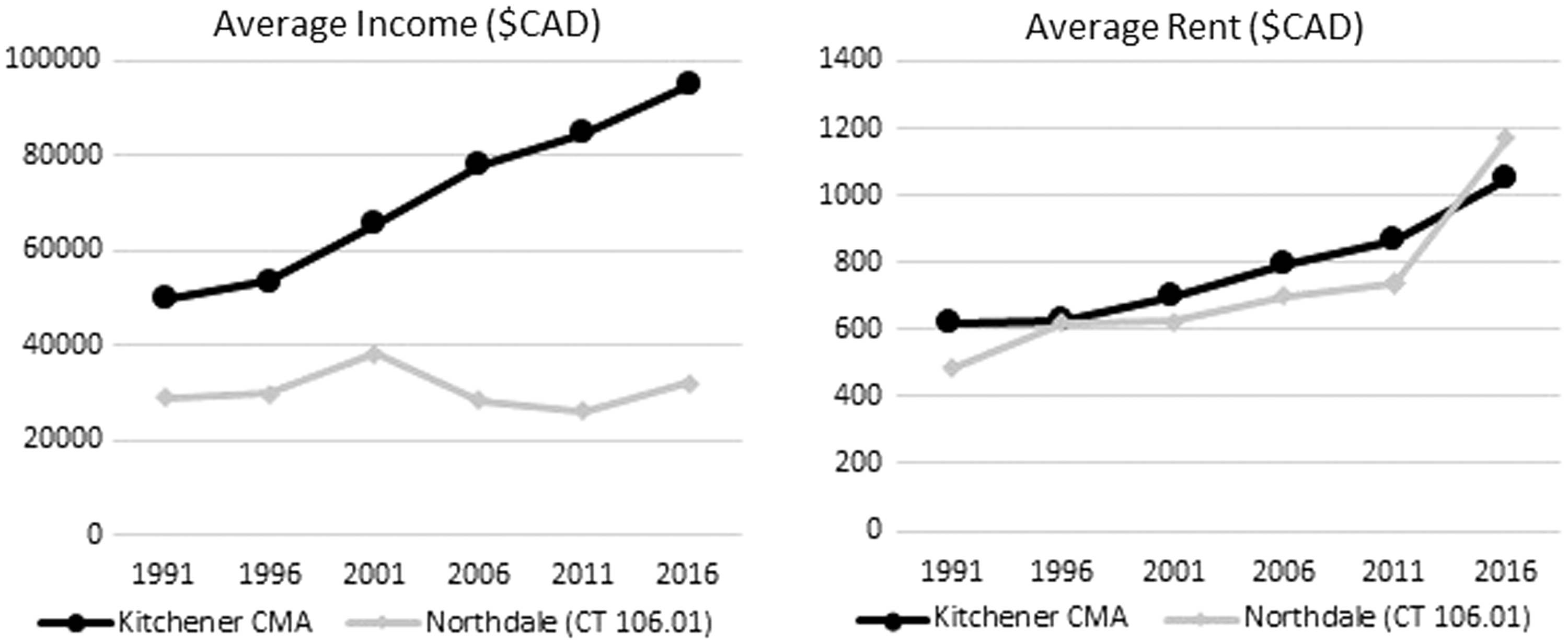

The financialization of PBSA appears to be affecting local housing affordability. As a long-time student housing area, Northdale has retained persistently lower-than-average incomes. Even as incomes rose by 90% between 1991 and 2016 in the wider metropolitan area, incomes in Northdale stagnated (Figure 2). Rents, however, skyrocketed in Northdale from 2011–2016, surpassing region-wide average rent levels after two decades of lagging behind. This sharp increase in Northdale’s rents took place during the period of large-scale, finance-backed PBSA development. The city’s Town and Gown Committee estimates that rents for a student bed in Waterloo increased by 25% between 2003 (at the start of the PBSA boom) and 2014, after accounting for inflation (Brieva and Marfisi, 2016). According to CMHC, rents for some types of student accommodation softened after 2014 but remained notably high for apartments, which contain most new development in areas closest to campuses (McLerie, 2017). Another study found that students in Waterloo paid an estimated 10% more rent than employed households (Pi, 2017). As in the UK and US, the financialization of student housing appears to be increasing housing costs for low-income students and non-students alike.

Average rent and income in Northdale (CT 106.01) and Kitchener-Cambridge-Waterloo CMA, 1991–2016.

The business models that drive these changes are based on squeezing money from students, many of whom are beset with financial hardship from attending university. From 2000–2010, over half of Ontario students graduated with debt, and the average amount owed increased from CAD$22,700 to CAD$26,900 (Statistics Canada, 2014). The Canadian Federation of Students (2015) has raised particular concern about increases in the number of students with large debts (over CAD$25,000) and the rapid rise of private debt as opposed to government student loans. While some parents may pay for pricier PBSA, students, their families and their future earnings are ultimately a new source of value extraction for investors.

A back-to-school movement by capital, not just students 1

We argue that firms play a key role in creating Canada’s financialized PBSA sector, in what can be understood as a twofold market creation story. On one level, a market is being created for off-campus PBSA itself – a market that did not widely exist before in Canada. The creation of this market entails not only expansion into new geographic areas, but also efforts to develop familiarity with PBSA among students as consumers, and among potential lenders (Morton, 2012; Peisner, 2014; interviews). Simultaneously, modelled after the US and UK, a market is being created for PBSA as an investment asset (whether through REITs or other vehicles, or through the purchase of condominiums for rental) – investment products that did not formerly exist in Canada. Importantly, it seems that the second trend is increasingly driving the first: the material market for PBSA is being created to provide a market for investment therein.

This trajectory of financialization differs from other sectors of the housing market. With multi-family housing or home mortgages, financialization has reshaped markets, but not created them (e.g. August, forthcoming; Walks and Clifford, 2015, respectively, in Canada). Even the creation of a new asset class from single-family rental (SFR) homes in the US did not create the sub-market; it involved securitizing, at scale, homes that were ‘long part of the overall rental picture in the United States’ (Fields, 2018: 123). In Canada, PBSA is scarce in most places, and investors are making a market for this product as they build it.

The state’s actions affect the PBSA market but are secondary and incidental. As such, theories that emphasize the state’s role in facilitating the financialization of broad sectors of real estate (such as home mortgages or rental housing) may be less helpful for understanding niche sub-markets like student housing. Nonetheless, reduced funding for post-secondary education has created an opening for private PBSA, and state-led internationalization strategies (to drive enrolment growth) promise a source of demand. Federal legislation enabling REITs in 1993 is also a crucial state intervention to facilitate the financialization of real estate (Gotham, 2006; Waldron, 2018). Federal mortgage insurance has played a minor role and is subject to restrictions. Arguably, the most important intervention has been through local planning: Waterloo enabled higher-density PBSA to promote intensification, and to address town-gown conflicts (Revington et al., 2018), inadvertently creating an opportunity for financialization.

The Waterloo case illustrates the shift from demand-driven to finance-driven new-build studentification. While Nakazawa (2017) argues that studentification is rooted in growing numbers of students, this alone cannot explain the variegated geographies of studentification. New-build studentification does not simply arise from growing post-secondary enrolment in a restructuring knowledge-economy city (Foote, 2017; Moos et al., 2019). Indeed, it emerges from intentional efforts by firms to create products for investors. As a local planner perceived: ‘It wasn’t necessarily driven through student demand, although there was some component of that. But I think a lot of the demand came from the investor demand for an investible vehicle’ (P02).

Our study also illustrates the broader function of financialized PBSA within a capitalist political economy. We build on Smith and Holt (2007), who demonstrated how studentification fuels gentrification in the UK’s provincial towns. While they focus on students as consumers who drive this change, we argue that it is also driven by capital seeking a spatial fix. Contemporary finance-driven new-build studentification enables investment in the built environment of secondary cities, which may be overlooked by conventional real estate investment but may be ideal for PBSA. Financialized PBSA offers an outlet for capital to overcome barriers, including high land costs (in bigger cities) and decreased place advantage (in smaller ones). It also offers advantages as a ‘sectoral’ capital switch (Charney, 2001), with expectations for greater yield compared to other investments.

This spatial and sectoral switching of capital has implications for new patterns of uneven development. In Canada, the small flourishing of financialized investment that we document is largely concentrated in a handful of southern Ontario university towns. Waterloo, the most advanced PBSA market in the country, exhibits key factors that attract financialized investment. It is a secondary city with a high-tech university, recent surges in enrolment, international students and connections with key players working in financialized firms. Within Waterloo, development is heavily concentrated, remaking the Northdale area physically and socially, creating a segregated student-oriented district, and engendering displacement and gentrification. It is also reshaping local affordability, driving high rents that affect both students and non-students alike. Moreover, it is capitalizing on housing need facing the (typically) low-income population of students, many of whom take on substantial debt during their studies.

Yet, as our work demonstrates, the process of finance-driven new-build studentification in Canada has been a rocky road. Even as some firms plan to expand nationally, many have struggled, speaking to the fragility of this process as it evolves in Canada and reflecting the volatility of financial investment (Aalbers, 2017). For critics of the unjust social and spatial outcomes associated with the financialization of real estate, these fractures can be explored for insights into how to alter, transform and prevent the unfolding of this process.

Conclusion

Our research demonstrates, in the Canadian context, the incipient financialization of PBSA, a niche sector said to represent an emerging global asset class (Savills, 2016). This case underlines the variegated nature of processes of financialization (Aalbers, 2017), which have unfolded differently within the same country for very similar asset classes. Financialization is rampantly transforming generic multi-family rental housing across Canada (August, forthcoming), as financialized vehicles capitalize on strong existing demand, and purchase existing, ageing stock from non-financial entities and then reposition it to be more profitable. With PBSA, by contrast, the pattern has been reversed – demand has been actively cultivated by key players in the industry, who seek to create the PBSA product and drum up consumer interest in higher-cost student housing, in order to create an asset class for investors. The creation of this market is a response to investor demand and seeks to replicate markets seen in the US and UK in a place where the form was virtually non-existent. Financialization is driving urban development to satisfy investor demand for new products (rather than simply colonizing and capitalizing on existing sectors); in other words, making a market for itself. In addition, this involves the ‘fast’ transfer of ‘ideas that work’ from entirely different jurisdictions, mirroring neoliberal ‘fast policy’ (Peck and Theodore, 2015), but implemented by actors in the private sector, not the state.

The shift from demand-driven to finance-driven new-build studentification since 2011 represents a sectoral switching of capital in search of new opportunities for profitable investment from ever more niche real estate sectors, as well as a geographic switching into secondary centres. In this sense, studentification is more than an expression of provincial gentrification (Smith and Holt, 2007) – it is characteristic of capitalist urbanization more generally (Harvey, 1985). The Waterloo case, as an exemplar of this trend, illustrates the challenges of age segregation and housing affordability that arise from the financialization of PBSA, as well as the role of local planning in enabling it. However, outside Waterloo, this process has also been fragile, pointing to the precarity of financial expansion into niche sectors, possibly presenting an opening to develop more equitable alternatives to financialized PBSA.

Further research should examine the dynamics of university-private sector housing partnerships and the changing role of the neoliberal university in (financialized) student housing. Given the emerging popularity of these partnerships, there is a role for institutions to cap rent at affordable levels, or to partner instead with not-for-profit entities to develop PBSA. Also, to the extent that further expansion of financialized PBSA depends on permissive local planning, tools like inclusionary zoning could be used to support production of affordable housing and limit financialization. Stronger support from government and universities for affordable student housing options would also circumscribe opportunities for financialized landlords. Another avenue for future research would explore this phenomenon as part of the financialization of housing across the life course, extract valuing from students, renters (August, forthcoming) and seniors living in retirement and long-term care facilities (Horton, 2019), and how value-grabbing (Andreucci et al., 2017) in real estate from cradle to grave drives indebtedness and affects well-being. There is an opportunity to explore the links between this financialization affecting people via real estate with the financialization of social reproduction, in which social policy retrenchment and neoliberal austerity are reshaping education, health care, care labour and survival, more broadly (Federici, 2014; Karaagac, 2019; Roberts, 2016).

Footnotes

Acknowledgements

Earlier versions of this paper were presented at the Urban Affairs Association conference in Toronto in April 2018, at York University in October 2018, and the University of Waterloo in March 2019; thank you to those who provided feedback. The paper benefitted in particular from conversations with Luisa Sotomayor and Allison Evans at York University, and Markus Moos and our colleagues in the Cities Cluster at the University of Waterloo. Critical comments from three anonymous reviewers and editor Brett Christophers greatly improved the paper. Errors and omissions remain the responsibility of the authors.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: Nick Revington’s portion of this work was supported by a Social Sciences and Humanities Research Council of Canada CGS-Doctoral Scholarship [grant number 767-2016-1258]. The views expressed in this article are purely those of the authors and do not necessarily reflect those of the funding body.