Abstract

Numerous cities in the Global South display the symptoms of housing financialization without the vehicles through which investment capital typically circulates toward the built environment. In this paper, we put forward the notion of “ripples of financialization” to point to the extension of the speculative practices engendered by financialized building practices well beyond the high-end developments in which global capital lands via banking transactions. We do so through a case study of two lower-income neighborhoods in Beirut (Lebanon) with similar sociopolitical characteristics during the building boom (2004–2014) that followed the adoption of an aggressive national policy designed to incentivize the flow of foreign investments into real estate. Methodologically, the paper traces the practices of developers operating in these neighborhoods, showing that they exploited their positions in social, religious, and political institutions to channel capital flows into real estate development. Without directly relying on the new infrastructures of finance, developers and future homebuyers adopted “speculative attitudes” that reproduced the spatial patterns of housing financialization, effectively inducing deep transformations in how the city is built and inhabited. While reflective of Lebanon’s context, these patterns are likely to be reproduced in other contexts where the adoption of the neoliberal mantra has influenced urban governance. The findings are based on surveys of all housing production in Beirut since 1996, at least 40 in-depth interviews with developers, and the embodied knowledge of the researchers, who are long-term residents of the city.

Introduction

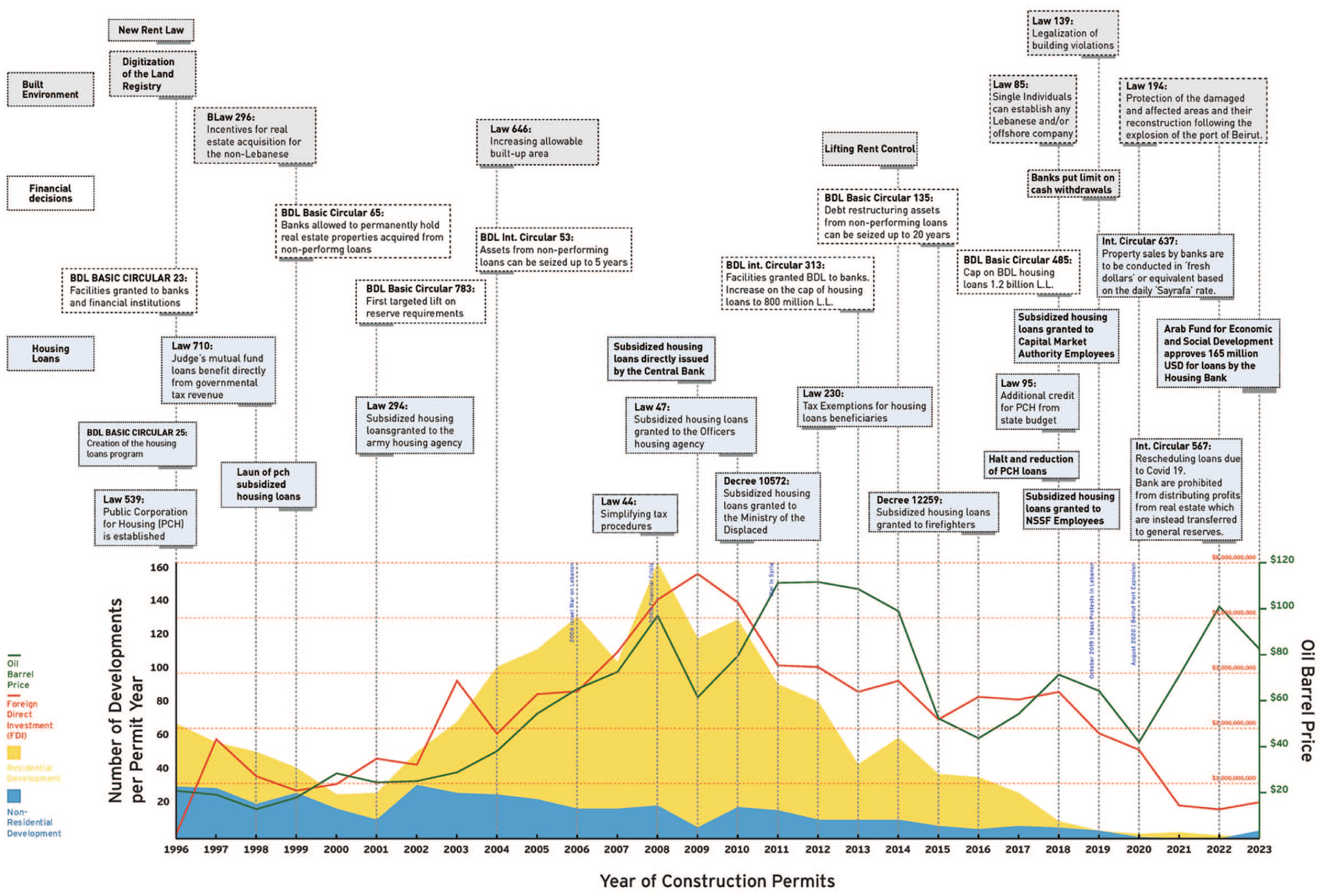

Between 2004 and 2014, Beirut (Lebanon) experienced a frenzied boom in the residential construction sector. In less than a decade, 10% of the city’s residential building stock was redeveloped, with high-rise apartment buildings spreading across city quarters. The boom unfolded in the context of a neoliberal economic turn during which a series of financial policies, 1 institutional changes, 2 and regulatory reforms 3 were introduced to attract local and international investments in the real estate sector (Beirut Urban Lab, 2020; Krijnen, 2016; Marot, 2018; Sakr-Tierney, 2017), particularly housing (Figure 1). 4 The new apartment buildings replaced older and more modest buildings and displaced residents. These new towers are higher and larger but also emptier than previous structures. 5 Many empty apartments function as “investments” or safety deposit boxes, reflecting the nature of Lebanon’s post-civil-war rentier economy, which relies on speculative real estate to attract and store foreign capital (Krijnen and Fawaz, 2010; Marot, 2018). A decade later, the boom has turned to bust, construction permits have plummeted, and construction is either stalled or moving slowly, while housing vacancy rates continue to rise as Lebanon experiences one of the worst financial meltdowns of the past century (according to the World Bank, 2024), the outcome of internal and geopolitical forces (Daher, 2022).

Building activities and policy changes in Beirut (1996–2023).

This pattern, in which a building boom fueled by foreign investment leads to empty apartments while the housing deficit for the urban majority soars, is a typical manifestation of the financialization of housing. The latter term refers to an assemblage of processes through which capital accrued via financial channels penetrates the built environment, abstracts land into an asset (Rolnik, 2021), and heightens the interdependence of capital accumulation and city-making, transforming infrastructure, waterfronts, and, especially in the past decade, housing (Fine, 2013; Krippner, 2005; Moreno, 2014; Sharma, 2021). In Fernandez and Aalbers’s (2020: 681) words, the “defining component of the financialization of housing” is “the transformation of residential real estate into a financial asset, opening channels for extraction by rentiers.” Consequently, “the production, finance, and purchase of housing are predominantly driven by financial motives rather than a will to use this housing as homes” (Fauveaud, 2020: 663). Over the past decade, the narrative of housing financialization has gained attention as scholars documented its materialization across cities in multiple corners of the globe.

Researchers who have tried to assess the impacts of housing financialization by looking at the transformation of housing from shelter into investment (Farha and Schwan, 2021; Rolnik, 2013) have drawn different conclusions than those seeking to measure and assess its existence by documenting reliance on financial tools. Indeed, research following the dominant model of the Global North (Erol, 2019; Fernandez and Aalbers, 2020; Socoloff, 2020) associates housing financialization with specific indicators, such as the weight and role of financial actors (e.g. banks, lenders, private equity funds, hedge funds), financial markets (e.g. stock exchanges, mortgage-backed securities), financial tools (e.g. mortgages—especially in foreign currency), and financial measurements (e.g. credit-scoring). However, in Beirut, but also Cairo, Istanbul, and other cities, the “symptoms” (e.g. oversupply, a soaring housing crisis, empty apartments, indebted households) are evident while the tools or vehicles through which investment capital circulates toward the built environment are limited. This has led some scholars to conclude that the impacts of financialization are timid, possibly confined to high-end quarters where investments visibly flow (Jorge, 2020).

Following this logic, researchers investigating housing financialization in cities of the Global South, such as Sao Paulo (Rolnik, 2021) and Cape Town (Migozzi, 2020), have focused on a relatively narrow section of high-end urban developments. In Beirut, this research has looked at the redevelopment of the city’s historic core and its seafront, where financial actors (e.g. bank subsidiaries, investment companies) initiated luxurious housing developments (Krijnen, 2016; Marot, 2018; Sakr-Tierney, 2017). These studies have usefully demonstrated the ascendency of financial actors in Beirut’s housing market and their connection to the ruling elite. However, by showing the impacts of housing financialization as largely contained in high-end housing segments, their conclusions fail to account for the scale of urban transformations that have reshaped the city since the neoliberal turn through what we term in this paper the “ripples” of financialization. Indeed, Beirut Urban Lab’s (BUL) 2018 survey of all building developments in Beirut between 1996 and 2018 found that bank subsidiaries and investment companies comprised only 5% of real estate developers operating in the city in the past two decades. 6 These “financialized” developers operated exclusively in the high-end market, developing about 20% of the city’s newly built-up areas and 10% of the new housing stock.

Meanwhile, the pattern of rapid development, replacement of old buildings, displacement, and empty apartments despite soaring housing demand; the euphoria associated with imagined future gains accrued by one’s ability to participate in the real estate business; and the expansion of borrowing practices for middle classes eager to acquire housing at any cost spread across the entire city (Beirut Urban Lab, 2020), even in the absence of financial companies and financial tools. Thus, a methodology that approaches housing financialization as the limited adoption of specific financial tools obscures the less visible development practices that occur simultaneously and relationally with these transformations, the “ripples of housing financialization” that intensely transform middle- and lower-middle market segments.

Research intent and arguments

This study provides an integrated understanding of the actors, processes, and institutions that channeled capital into Beirut’s middle-income housing segments during the building boom (2004–2014). Largely invisible to the metrics of capital flow designed to measure the penetration of financial capital in the housing markets of the Global North, this flow of investment capital is substantial and transformative, and as we will show, intertwined with the visible channels of financial capital documented in Beirut and beyond since they are incentivized by and invested in the reorganization of the regulatory frameworks (e.g. permitting, registration), the actions and behaviors of actors, and the dispositions and worldviews embodied in the city’s changing landscape well beyond financial actors. We propose the notion of “ripples of financialization” to point to the modalities through which capital seeps into middle-income neighborhoods, recognizing hence a relational framework of analysis that links developers and investors in these sections of the city to actors and practices associated with housing financialization in high-end markets, particularly the physical and affective disposition and intellectual labor deployed to accumulate capital through housing development and acquisition (Bear, 2020), without completely equating practices and channels to those adopted by banks and financial subsidiaries.

The study follows earlier works in associating financialization with a set of speculative behaviors that collectively shape multiple adaptive practices in housing development, including individual and household behaviors (Bear, 2020; Goldman and Narayan, 2021; Humphrey, 2020; Li, 2014), the modalities of housing production, and, more generally, the city’s organization. It approaches housing financialization as an assemblage of evolving speculative processes of city-making championed by multiple and not necessarily concerted actors hedging for financial gains through real estate. These actors extend the penetration of capital into the housing sectors of middle- and lower-income city quarters through informal, adapted, and extended modalities, without relying on the vehicles and tools typically documented in the financialization literature.

In conducting this analysis, we do not aim to decide whether these patterns fall within a strict definition of “financialization,” as stretching this definition may dilute more than clarify (Christophers, 2015). Nor do we take on the dualism of “high” and “low capital.” Instead, we find that the notion of “ripples” allows us to trace the patterns of reactions, resonance, learning, careful adoption, and eventually contributions of actors who extend the direct actions of financial actors into the built environment, and we propose to analyze these actions relationally with the practices of financial actors. Indeed, limiting the study of the modalities and repercussions of late neoliberalism, and hence housing financialization, to the high-end market segments and financial actors who mirror practices and actors documented in Western contexts does not account for the actually existing forms in which late neoliberalism has taken hold of cities (Peck et al., 2018), hijacking substantive sections of housing stocks as assets to be sold for future profit.

Paper structure

The paper is divided into five sections. Following this introduction, the second section sketches the broader picture in which housing financialization has unfolded in Lebanon, tracing the capital flows and regulatory changes characterizing the turn toward housing financialization as a key national strategy. After presenting our methodology in section three, the fourth section presents the main evidence behind the paper’s argument, diving into two of the city’s middle-income housing segments and providing insights into the practices of the developers who cultivated and exploited their positions in social, religious, and political institutions to channel capital flows into housing, developing the patterns we associate with “ripples” of financialization. The final section concludes by looking at the city level, showing the replication of these patterns within and beyond its borders and reflecting on the repercussions of this analysis.

Beirut: A macro or top-down reading of urban transformations and capital

To provide a “big picture” of this study’s context, we first frame the research on the ripples of housing financialization in Beirut through the macro-lens of financial capital flows, the most common approach to investigating urban financialization in the Global South (Aalbers, 2017; Pereira, 2017; Socoloff, 2020). This approach extends the early frameworks developed to study housing financialization in the capital cities of advanced economies, such as London, New York, or Tokyo (Aalbers, 2016; Aveline-Dubach, 2022), to “southern” national contexts. It proposes a relational structural approach at the national scale that distinguishes between a “core” or “central” Global North and “peripheral” southern contexts, with “dependent” financialization because the mechanisms underlying and pushing financialization depend on an influx of capital from central economies (Fernandez and Aalbers, 2020: 695). To assess the extent of financialization, scholars look at the volume of capital, its movements, and other financial indicators.

Applying this framework to Beirut by tracing the inflow of foreign direct investment (FDI) in Lebanon and the pattern of building development renders a direct correspondence between building activities and FDI during the study period. 7 Despite the absence of detailed published figures, there is sufficient evidence to indicate that real estate was one of the main destinations of these investments. 8 Figure 1 shows that the number of filed building permits in Beirut and FDI (mostly remittances) follow relatively similar trends. Furthermore, as 80% of buildings permitted between 1996 and 2021 were residential and there were no investments in infrastructure or other large-scale projects, we can assume that in Lebanon, housing was the main target of financial flows into real-estate (see Notes 1–4). Investors were typically Lebanese expatriates and Arab Gulf nationals. The Gulf’s model of rentier capitalism via real estate (Buckley and Hanieh, 2014) was an important example for Lebanon’s decision-makers during the post-civil-war era (Leenders, 2017). 9

The analysis of housing financialization from this lens is productive in recognizing the trans-scalar and relational dynamic of real estate financialization in Lebanon and the country’s position as a peripheral economy that receives foreign investments. However, this analysis does not explain the processes that incentivize and facilitate capital flows and the scales at which these are channeled. Indeed, as Figure 1 shows, over the past 30 years, an exhaustive review of the Official Gazette, newspapers, and the websites of major financial and public agencies that tracked incentives against building activities revealed the large number of incentives and facilities introduced by Lebanon’s public agencies to attract capital to the built environment (see also Krijnen, 2016; Marot, 2018; Sakr-Tierney, 2017). Thus, many capital restrictions were eased, including those limiting the foreign ownership of land and those mandating banks to sell seized property within a short period, housing loans were aggressively put forward as the sole “housing” policy, 10 property law was revised to reduce taxes, incentives were introduced for foreign investors to acquire property, 11 building and urban regulations were relaxed, 12 and exceptions were issued for large-scale redevelopment projects. This is well in line with other national contexts, where scholars documented the aggressive introduction of mortgages with diverging consequences and modalities (Aslan and Dinçer, 2018; Kutz and Lenhardt, 2016; Reyes and Basile, 2022) and the privatization of public housing (Chua, 2015; Rolnik, 2013), urban renewal projects (Yeşilbağ, 2020), and additional reforms (Aalbers, 2017; Feng et al., 2022; Goldman and Narayan, 2021; Halbert and Rouanet, 2014; Socoloff, 2020).

Furthermore, the financial actors and established developers relying on financial investments are only visible in Beirut when one looks at high-end quarters, or “financialization islands” (Krijnen, 2018). Conversely, as noted in the introduction, construction activities in low- to middle-income segments are obscured, despite intensive activities and transformations during the same period. Thus, the number of residential development projects initiated spiked between 2003 and 2008 in Beirut, with double the number of permits filed in 2008 than 2003. At the same time, the redevelopment of Beirut’s historic core by the private real-estate company Solidere functioned as a citywide price-setting benchmark, with land value increases spilling over surrounding neighborhoods, thereby shaping expectations of real estate profitability across the city and beyond (Marot, 2018). 13 This study turns to segments of the housing market which received large flows of capital without displaying the metrics of financialization documented in the high-end segments of Beirut’s residential markets.

To trace the flows of capital that are invisible to the banking metrics, the study zoomed down on the practices of developers, following the lead of scholars who have recently pointed to the role of local, non-state actors involved in steering housing financialization into specific cities and/or neighborhoods. The practices of these “agents of financialization” such as international investors who look for opportunities to place capital generated in northern contexts in the housing sectors of southern or lower-income countries or developers lobbying, facilitating, or influencing policy changes provide evidence of the unfolding of housing financialization. For example, Socoloff (2020) looked at the influential role of the coalitions pushing for housing reforms in Argentina’s hyperinflated economy. Similarly, Fauveaud (2020) investigated a handful of stakeholders (e.g. development agencies, public institutions, foreign and international investors, transnational developers, and brokers) acting as “agents of financialization” in Phnom Penh (Cambodia) by creating channels enabling the circulation of capital and its landing. Along the same lines, Goldman and Narayan (2021), Searle (2018), and Goodfellow (2020) documented the role of local intermediaries in creating an infrastructure for investments that enabled capital to penetrate housing markets and navigate or game the system to profit from home construction. These studies demonstrate the role of these actors in driving capital, and our findings concur with their assessment. This is not to say that social networks do not play a role in the high-end financialized markets of Beirut. To the contrary, there is ample evidence that social networks are deployed in high-end markets (Krijnen, 2016; Marot, 2018). Therefore, our focus on social networks and political and religious organizations is methodological, and it aims to render visible the otherwise stealthy (unnoticed) ways in which these institutions act as conduits to channel (investment) capital toward real estate, particularly housing, in a market segment where reliance on banking institutions is limited. By focusing on the less visible but no less insidious penetration of capital into middle- and lower-middle-income neighborhoods in Beirut and the actors and processes that enable it, the paper unravels what we have termed as “ripples of financialization,” trends that are likely unfolding in other cities where, similarly, the lucrative role of real estate has transformed popular perceptions of land and housing.

Methodology: Studying ripples in Beirut

We uncover the penetration of capital into the middle segments of the housing market and unravel the processes through which this occurs, and the infrastructures used to mediate and channel capital as investment into the built environment. To achieve this, we present an analysis of speculative housing investments in Beirut’s low- to middle-income housing market at a time when, on the one hand, national policies encouraged financialized housing developments while, on the other, the territorial sectarian organization of the city established during the civil war (1975–1990) was re-entrenched by the populist politics of the post-war era.

The paper takes two of Beirut’s low- to middle-income neighborhoods, Aysha Bakkar and Tarik El Jdideh, as case studies of this “segment” of the city’s housing market, chosen for their rapid and largely ignored transformations, as evidenced by the Beirut Urban Lab’s Beirut Built Environment survey of development activities. Initially, we approached the two neighborhoods separately. However, the mapping of developers revealed that they were roughly similar segments of the same housing market, known essentially for its prevalent Muslim Sunni 14 sectarian territorial identity. Therefore, we chose to write our findings through the entry points of the social institutions through which finances were channeled.

Sectarian territory

In referring to sectarian territorial identity, we adopt a definition of the sect as an attribute or product of class positioning as well as a mode of political and economic organization that can define geographies, leaders, and parties in the country rather than a group of religiously homogeneous individuals (Haddad et al., 2022; Salloukh et al., 2015). Thus, the identity of these neighborhoods as “Sunni” or, as often said, “Sunni strongholds” is the outcome of a historical accumulation of social, electoral, and economic practices that consolidated a population with specific political affiliations over time.

Since their early urbanization during the early 1920s, both Aysha Bakkar and Tarik ElJdideh have hosted prominent Sunni religious (e.g. Dar El Fatwa; al-Maqassed). With the outbreak of the civil war in 1975, Beiruti Sunni families moved into these neighborhoods when the city’s historic core, also its commercial center, became a conflict zone. This migration reinforced both economic activity and communal sectarian identity, as neighborhood residents established shops, clinics, and light industries as well as sect-based systems of service provision and distribution. Popular Sunni political parties also established their headquarters in the areas, and their presence helped consolidate the sectarian character of the neighborhoods, giving them significant political clout in Beirut’s urban geography (Mneimneh, 2019; Zaatari, 2019). In the landscape of Lebanon’s post-civil-war politics, these neighborhoods became electoral districts where clientelist networks tied to sectarian leaders concentrate, reinforcing collective dependencies on political patronage (Mouawad, 2021). This identity was further consolidated following sectarian clashes between Sunni and Shia Muslims, which started mid-2005 and intensified following the outbreak of the war in Syria in 2011. As we will see, these divisions were strategically mobilized by developers and political actors to accumulate capital and control the housing markets in a context where the influence of a national financial policy had rendered real-estate investments particularly lucrative.

Developers as entry point

We approached our topic of study through the developers who organize the market in these low- to middle-income neighborhoods. Starting from the well-established premise that property markets are produced through the labor of agents who circulate specific social constructs, institute market devices, and shape political contexts (Polanyi, 2002; Weber, 2019), we traced and linked processes of housing production, exchange, and acquisition by mapping all actors (e.g. clients, developers, brokers, bank employees granting loans, municipal officers) and locating them in relation to the social (e.g. sectarian/political, kin, religious) fields dominant in the neighborhoods where they work. In line with earlier studies that approached the housing market as a social field (Fawaz, 2008; Garcia and Jiménez, 1994; Weinstein, 2008; Zhang, 2011), we zoomed in on the figure of the developer as a central economic agent located in a historically and geographically specific context.

To be sure, it is possible to study high-end markets with the same approach, and earlier research provides evidence that the entry point of developers and the social networks on which they tap to exert influence on the regulatory environment that organizes building activities and facilitates investments in real estate across all market segments (Krijnen and Fawaz, 2010). However, as noted above, this approach is adopted because it allows us to render visible transactions otherwise invisible to the typical metrics of finance that rely on traditional banking and financial institutions.

Data collection

Data collection took place through fieldwork, during which researchers first identified all building activities of the past 2 decades in these neighborhoods, ascribed each development to one development agency and/or actor, and then profiled all 181 developers operating in the areas, which we roughly framed as a single market segment. We conducted in-depth interviews with 40 of these developers. Interview findings were triangulated with information in the commercial registry and through online research. 15 By crossing the field data with the list of building permits and websites, we geolocated all other building activities for each developer, investigating the spatialization of their activity in the city.

Authors leveraged their respective individual profiles to develop fine-grained research, with the privileged position as “insiders” in each neighborhood, enabling them to navigate otherwise inaccessible informal social institutions and build on an embodied knowledge of the areas. The shared “cognitive” capital with developers (Goodfellow, 2020) secured the competence to read, navigate, and negotiate presence through familiarity with the cultural and social practices.

Beyond formal finance infrastructure: Social, religious, and political networks as conduits for investment capital

During Beirut’s building boom (2004–2014), the neighborhoods of Aysha Bakkar and Tarik El-Jdideh experienced intensive development activities. Low-rise buildings and empty lots were gradually replaced by multistory residential apartment buildings. 16 In the study period (1996–2018), about 15% of the built fabric was redeveloped. Intensive building activities were incentivized by the changing regulatory framework: The 2004 building law, adopted amid intensive lobbying (Krijnen and Fawaz, 2010), made it particularly lucrative to replace pre-1971 residential developments, which were then capped at a limited number of floors. In turn, rising property prices created a growing interest in real-estate investments, which started in high-end segments of the market but spread to other neighborhoods of the city where developments multiplied with apartment prices spiking well-above the means of residents and higher and emptier buildings increasingly occupying the skyline without high rates of vacancy deterring additional investments. 17 Furthermore, interviewed developers frequently mentioned the attractive profits to be reaped from real estate as an incentive to change trades (e.g. selling a car dealership, a jewelry store, or even a medical practice) and invest in real estate, and they pointed to the development practices in the city’s financialized high-end sectors as evidence of success. Some also used the financialized market segments as training grounds, working for high-end developers before opening their own businesses, typically as consultant engineers, employees, contractors, or middlemen facilitating permitting or registration in Lebanon or the Arab Gulf. To be sure, real-estate speculative practices existed prior to the post-2004 boom, but the scale and imaginary of profit to be reaped through real-estate investments, the tolerance for high vacancy rates within a regulatory framework where vacant units are fully exempted from paying municipal and property taxes, and the ability to convince relatives and other actors to “invest” in real-estate for future resale rather than inhabitation all reflect transformations well-beyond earlier practices that rendered apartments “investments” with excessive disregard for any balance with their role as homes.

Thus, the general euphoria surrounding the promise of enrichment through real estate took strong hold in these neighborhoods, with numerous property owners rushing to partner with developers to replace their low-rise residences with towers and many professionals and business owners being lured into shifting their operations toward this sector with the expectation of rapid and substantial gains (Khechen, 2014). By investing their or their relatives’ savings or the profits made from selling their business, “amateur developers” initiated building activities alongside an earlier generation of professional developers who had substantially expanded their activities (Mneimneh, 2019; Zaatari, 2019). Funding relied on multiple sources, including “silent” investments but also forward payments (or off-plan, see Humphrey, 2020) by eager future homeowners or investors. The pace and scope of building increased rapidly, exceeding what was needed to account for population growth and pushing out numerous households residing as tenants in older structures. The latter often had to move far away to secure affordable shelter, since apartment prices doubled during the boom (Zaatari, 2019). Meanwhile, the newly built structures had high vacancy rates: about 23% of Aysha Bakkar’s and 15% of Tarik El Jdideh’s new apartments were vacant at the time of the 2018 BUL survey. Interviews indicated that empty apartments had been acquired as part of buyers’ investment strategies: Given a property framework that exempts vacant property from taxation, and low reliance on mortgages and construction loans, holding these units off-market functioned as a strategic monopolistic approach for asset preservation among both developers and investors who held these units for storing wealth and accruing potential appreciation rather than homes or even an income generating asset through rent (Fawaz and Zaatari, 2024). In sum, the possibilities opened by real estate development in the study period signaled that in many ways, a building boom with the same characteristics as other housing market segments described as “financialized” in Beirut and elsewhere was taking place. This is what we are terming “ripples,” given the relational nature of this development with the higher end, more visibly financialized market segments.

Despite the intensity of building activities, interviewed developers reported limited or inexistent reliance on formal financial instruments or institutions. Thus, the survey of all development projects in these areas in 1996–2018 found the involvement of bank real estate subsidiary firms as developers to be limited to two projects located in zones bordering higher-income neighborhoods. Moreover, reliance on supply-side and demand-side bank lending and financing schemes was uncommon among these developers, even after such facilities were introduced in the high-end markets from 2009 (Krijnen, 2018). Indeed, only a few projects were financed through bank construction loans, and this funding was only partial. 18 In addition, mortgaged loans for housing acquisition in all new developments in the neighborhoods were insignificant, including from Islamic banks. 19 Since the pace of building activities and patterns coincided with the city’s middle- and high-end housing market booms, which were affected by the involvement of banks in real estate (Krijnen, 2016; Marot, 2018; Sakr-Tierney, 2017), the absence of financial vehicles should evidently not deter us from reading these patterns relationally. As noted above, builders took advantage of regulatory changes (e.g. new building law) to build higher and more lucrative developments. There was also a similar frenzy or speculative outlook that gambled on the wealth to be accumulated from rapid development. However, the dissonance between the flow of speculative real estate investments into the built environment and the scarcity of financial instruments suggests that alternative channels were at work.

In the next paragraphs, we scrutinize the profiles and practices of the developers active in the areas as an entry point to studying the penetration of capital through local social institutions and familial and business networks as well as religious and political institutions in the neighborhood. These practices, we show, extended and amplified the effects of financial investments into real-estate, creating “ripples” of housing financialization across the city. Before doing so, we now turn to profile these actors.

A strong social and business profile

All developers operating in the study areas had a relatively similar social profile that played a central role in enabling their development practices, although they differed in the scale of their operations and years of involvement in the market. All men, these developers were mostly born and raised in Beirut, often within the same neighborhoods where they lived, went to school, established their offices, and worked during the building boom. These men also maintained tight social relations with other residents and cultivated these through attending and being involved in regular social events and gatherings (e.g. funerals, weddings). The more established among them tended to hail from well-established Muslim Sunni families with generational presence in the city, and they strengthened their social standing by engaging in local charitable and social organizations (e.g. Ajyalouna, Makassed, BAU Alumni, family associations 20 ), adopting a persona of social charitability that strengthened their visibility in the local community.

A notable strategy of social distinction in the local community included earning engineering or architecture degrees (by the developers themselves or their children), often in the main institution of higher learning located in this area, the Beirut Arab University, which is also recognized for its (Sunni) pan-Arab identity that strongly echoes the neighborhoods’ identity. Some developers even took on teaching in this institution. Although unnecessary for running a real estate business in Lebanon, pursuing higher studies had favorable outcomes for their businesses. First, they earned the title of “professor,” adding an extra layer of respectability and reputability to their profile. Second, they accessed networks of professionals, including developers, who also sought affiliation with the university, and established a network of actors who influence regulatory reforms and facilitate access to public institutions.

This profile corresponds to earlier practices of development that pervade the entire city. Studies in Beirut (Fawaz, 2008) and beyond (Topalov, 1987; Zhang, 2011) have shown that social and familial ties are often critical for developers to identify real estate opportunities and establish trust among local investors and property owners whatever the market segments. Thus, this “locally embedded” or “traditional” developer profile predated the post-war building booms for the most established ones, and it is largely identified as an element of the family-based nature of economic organization in Beirut, with developers relying on kin relations to organize their businesses, secure favorable deals, and build trust within the community. In turn, this active presence reinforced their positions as trusted “middlemen,” a critical position they employed to manage relationships among different stakeholders in real estate development.

Yet there were important transformations in the landscape of building development, many of which can be traced to trends set by financial investors. Indeed, the number of individuals involved in housing production had increased considerably. While some developers described themselves as “professionals” and had primarily worked in this sector as their main career, many others had recently switched to the “real estate business,” bringing capital they had earned in other enterprises into this “industry.” Most (80%) had a strong presence in Beirut’s trade and service sectors prior to entering real estate development, leading in prominent business sectors such as textiles, construction materials, imports, travel, oil and gas, electric appliances, and jewelry. Some perceived real estate as “diversifying” their investments by adding it to their portfolio, while many others, typically less “well off,” completely switched professions, opting to sell their previous businesses and assets to work as developers. In addition, several defined that their businesses had entered the business to “invest” the capital earned by a close relative (e.g. father, sibling) working abroad. As the business boomed, so did the developers’ networks, and the most established ones began to act as conduits for investments, conducting deals with Lebanese expatriates or foreigners whom they incentivized to invest in building activities for profit through individual informal agreements. Interviews showed that many of these clients acquired multiple homes, approaching property as investment to be resold rather than as homes. 21 Several developers further explained that they had multiple “investors” who acquired an apartment in each of their projects. In attracting investors, developers also explained that they relied on professional associations such as the Lebanese Order of Engineers and Architects, business organizations such as the traders’ society (e.g. IRADA or Businessmen Association for Support and Development), and local and international investment associations (e.g. International Group of Economic Policy Developers, IGEPD 22 ), among others. Their membership to these associations helped in displaying “credibility” to known investors, but also meeting new ones, and improving their access to capital. This strategic social and economic positioning also reinforced their credibility with clients and became an indispensable ingredient in their operations.

Despite these similarities, the developers differed considerably in their ability to leverage capital and manage a successful business. The more established could expand and tap into a wider capital base to attract financing, as shown below. Many others were less successful, eventually running into bankruptcy. Looking further, two main non-market institutions emerged as critical in facilitating the circulation of investment capital into housing: religious organizations or charities, and political parties. We now turn to religious networks as a main conduit of capital flow for a group of developers who leveraged “piety” to attract and channel investments.

Religious institutions and financial piety

During the building boom, religious institutions and the networks of actors and capital surrounding them formed an alternative channel through which capital was directed toward housing development. This channel exploited a moral religious observance that bans interest, and hence reliance on bank loans, to channel capital. However, it also directed the landed assets of these organizations into commercial housing, thereby bringing them closer to the sphere of speculative real estate investment. This pattern may well have become first visible during the takeover of religious assets in Beirut’s historic core through the integration of Waqf (i.e. religious) property into Solidere’s reconstruction project (Moumtaz, 2021). However, religious affiliation did not only grant access to property, but it also provided developers the “trust” and “reputation” needed for investors and clients to do business with them as “well-positioned” individuals in organizations with known religious aura. It is noteworthy that at the time of the research, Islamic Banking institutions played a relatively minor role, extending only a small number of housing loans. Instead, the focus of the study is on Islamic charities and well-off observant Muslim individuals who channeled funds without banks, seeking ways to accumulate capital through speculative real-estate investments while circumventing, at least formally, religious considerations.

The position and role of religious organizations in building development needs to be understood within the socioreligious contexts in which the studied developers operate. Islam forbids interest, and contemporary jurisprudence largely places banking practices associated with bank loans and bank investments under this label. As such, the typical financialization channels are religiously prohibited to observant Muslims. 23 In this context, developers who offered religiously permissible investments attracted religious investors who would have otherwise refrained from placing their money in real estate. Thus, several interviewed successful developers described themselves as “religiously observant” and explained that their affiliations and standing were key to their operations.

All in all, these “pious” developers built about a third (38%) of all new structures and accounted for 7 of the 10 largest developers in the studied areas. They were deeply embedded in the network of local Sunni religious charities, 24 with their affiliations sometimes dating back to their youth, when many received their religious education and volunteered as teenagers there. They now retained the same affiliations with managerial or honorary positions, regularly attending the neighborhoods’ mosques, participating in religious events, and organizing charitable activities (e.g. iftars during Ramadan, neighborhood cleaning, campaigns to secure basic needs and medication). Some even designed or built mosques pro bono for these associations. Others recounted traveling to the Arab Gulf for work during the civil war, where they forged social relations and raised capital that enabled them to act as benefactors and earned them respectability in their communities. One even noted traveling to the Gulf to study Islamic law, establishing social networks that enabled him to start his own religious organization upon returning to Lebanon.

Interviews further showed that the positionality of these developers as respectful of religious ordinances and affiliated with religious charities generated the necessary trust among pious potential investors, including expatriates, local businesspersons, relatives, or foreign Gulf investors looking for religiously permissible investment opportunities. Investors differed considerably in their profiles, with some being close relatives in professional sectors (e.g. medicine, trade), but they all shared reservations about loans and interest and were looking for religiously permissible channels of investment—which made financial institutions out of reach. Interviewed developers concurred that at least 30% of their project financing was secured through forms of “observant” investment. Furthermore, by selling homes to mostly Sunni constituencies, their business is seen as supporting and benefiting their pious community, enhancing their role as “benefactors” all the while, ironically, they were displacing members of these and other religious communities through their development interventions.

In addition to attracting pious investors and their capital, some developers also secured privileged access to the assets of these faith-based organizations. Thus, they partnered with the latter and developed some of their properties into commercial and lucrative projects. Three developers in Aysha Bakkar had utilized assets held by the religious organizations they were affiliated with to develop for-profit residential projects between 2009 and 2014, 25 all located on land originally slated for the development of social or communal services, such as schools and clinics. However, the lure of profit from residential real estate development encouraged the organizations to shift toward capitalizing on their assets and building for-profit and high-end housing. 26 During interviews, religiously networked developers explained that they had convinced board members that this change would secure higher returns. Conversely, religious assets were clearly a critical enabler for some developers to operate, given the prohibitive cost of land. They earned their profit in apartment units while the organizations typically sold their share of apartments to their members, who benefited from this transaction.

As noted above, the shift toward land development among religious organizations should be read in relation to a larger investment strategy, as evidenced through the work of Moumtaz (2021), who investigated the earlier disintegration of Muslim communal land (or waqf 27 ) through successive decisions by the state and the Directorate General of Islamic Waqf (DGIW) 28 in the context of the redevelopment of Beirut’s historic core during the post civil war period under the auspices of Solidere, a real-estate development company largely associated with the financial turn in land redevelopment in Beirut. Moumtaz (2021) argues that public institutions came to perceive waqf, or religious land, as an impediment to the circulation of capital and, consequently, to the advancement of the economy after the war. Consequently, the DGIW de-incentivized religious organizations from registering land as a religious commons or from developing buildings for communal use, and instead religious organizations subordinated the properties they owned to the logic of the market, treating them as part of financial or profit-accumulating strategies rather than preserving their use value for sustainable social functions.

Beyond this, interviews showed that developers’ positions in religious organizations also reinforced their standing as financial mediators by providing substantial symbolic capital through their flaunted affiliations with the religious charities they had either established or joined. In doing so, these developers were no different from large-scale developers who operate in higher-end neighborhoods and also tap into social positionality. Indeed, in a national context where judicial recourse is arduous and limited, social and symbolic capital play a critical role in facilitating transactions (Bourdieu, 2000; Fawaz, 2008). For the studied developers, these affiliations were, however, possibly more critical since they served as a foundation of trust in the neighborhoods they worked in and enabled them to tap into wide networks of landowners, clients, and investors, both locally and abroad, and for which they could not substitute bank support. Thus, Sunni Muslim religious organizations brought together Sunni individuals with diverse backgrounds and income levels, including landowners, potential clients, individual investors, and sometimes political figures or public officials. These formed the essential ingredients for housing production within this segment, with organization members trusting developers affiliated with or occupying managerial positions in these associations. This translated into a preference to buy apartments from or partner (for landowners) with these developers.

By leveraging religious affiliations and religious legitimacy to mobilize alternative financial infrastructure and repurpose assets owned by religious institutions for speculative real estate development, developers could extend and replicate the practices of high-end developments that relied more clearly on financial institutions to target a low- to middle-income Muslim Sunni market where they held a semi-monopolistic position in access to land, financing, and clients within a specific religious Muslim Sunni social field.

Leveraging political affiliations: State access and an investment front

Another network of social relations that proved critical for the circulation of capital into housing in these two neighborhoods tied developers to the handful of (Sunni) political parties based in these areas. Chief among these was Al Mustaqbal, or the “Future Movement,” the post-war political movement founded by late Prime Minister Rafic Hariri, whose philanthropic and business ventures are widely associated with Lebanon’s neoliberal post-civil war turn, particularly in its banking and real estate sectors (Leenders, 2017), as well as the financialization of real-estate starting with the redevelopment of Beirut’s historic core (Marot, 2018). Al Mustaqbal was in control of the prime minister position almost exclusively between 1990 and 2019, arguably occupying the most influential decision-making position in Lebanon, and it controlled the municipality of Beirut between 1996 and 2025, the authority entrusted with permitting buildings in the city. Given that Hariri was also the founder and main shareholder of the Banque de la Mediterranée (now Bankmed), one of Lebanon’s largest banks providing loans to both developers and future homeowners during building booms, the web of this particular political party was decisively more powerful than others nationally, and the party’s influence grew among the areas’ residents (Tarik El Jdideh was typically referred to as the “reservoir” of Al Mustaqbal). Several other Sunni political movements of less significance were also active, and developers with positions in these movements could sway votes in local and national elections and rely on these networks to influence the municipality and build credibility among their constituency.

The study showed that one in three developers operating in Aysha Bakkar and Tarik El Jdideh had direct ties to an active political party in their area, most of them to Al Mustaqbal. Some were directly affiliated, while others relied on a family member or business partner for the relationship, particularly if that individual held public office for a party (elected or appointed). A few held positions themselves as elected members of the Municipal Council of Beirut or as representatives on the council of the Order of Engineers and Architects. As with religious organizations, affiliation with political parties was associated with regular visible participation in party social events and direct involvement in elections. The developers also provided free services and non-monetary donations, such as equipment for local firefighting stations and infrastructural works (e.g. sewage pipes, road paving), to the political parties, which in turn earned them social respectability and trust among potential clients and investors. In doing so, they depicted their operations as developers as part of the services they present to the community, “helping” couples secure housing. However, proximity to Al-Mustaqbal also provided access to development networks aligned with the logic of real estate development and hence favors and benefits matching those of financial actors and, in some cases, to collaborations. However, given that the developers under study rarely worked through financial agencies, the distinction between the developers studied in this paper and financial actors should still be made.

Interviews with developers further showed that one critical advantage of political affiliation is the ability to display “strong clout,” and consequently reassure possible clients and investors that one can rapidly navigate the otherwise deeply corrupt and tortuous permitting process. Given Beirut’s precarious political and security conditions, the ability to navigate red tape eventually became a pre-requisite to operations. In that setting, political networks emerged as key enablers facilitating necessary paperwork for development activities. We list below the ways in which such political networks and public access became critical to generating the ripples of financialization or the circulation of capital in the built environment during this period.

First, affiliation with influential political institutions granted access to influential actors who facilitate permitting processes, particularly at the municipality of Beirut, a notoriously heavy and corrupt bureaucratic permitting system that is difficult to navigate without political mediation or informal networks. In addition, developers used these affiliations to secure infrastructure hook-ups, when and as needed, and circumvent additional scrutiny of the permit.

Moreover, affiliations meant social respectability and trust that reassured investors, landowners, and clients. A key guarantee was having an influential actor as a partner, ideally a well-positioned political figure or a connected actor (e.g. someone involved in the financialized real estate industry in downtown Beirut). Such partnership demonstrated the developer’s influential position, which in turn attracted additional investors to place their capital, landowners to partner in developments, and modest homebuyers who trusted a developer by virtue of these networks with forward payments. Finally, Al Mustaqbal’s infrastructure at times also meant the ability to secure housing loans through the banking network affiliated with the party, even if a client could not put forward the necessary documents or assets required by the banking system. Ultimately, these networks are no different from those deployed by financial actors and, in tracing them, we are not positing a binary between high or low capital. Rather, we seek to show that the ripples of financialization into the middle- and low-income markets were made possible through these influential relations.

Discussion and conclusions

The paper has put forward the notion of ripples of financialization to account for the multiple ways in which urban or housing financialization expands beyond the activities of financial actors, through which it is typically measured. By ripples, it points to the effects of changes in public regulations, financial flows, practices, habits, and dispositions toward an imaginary of wealth accumulated, all of which concur to entrench an urban environment documented by speculative urbanization.

Taking Beirut as a case study, the paper unraveled the practices of developers who fostered a speculative housing market attractive to investment, proposing a deep dive into their practices and worldviews (Bear, 2020). Through their activities, these developers intensified the flow of capital into housing and enabled and incentivized religious organizations, private businessmen, and individual households to participate on different scales and risk levels in the investment frenzy. While these practices do not rely on formal banking systems or investment vehicles, they should be read relationally with the deployment of financial tools that inspire, strengthen, and exacerbate speculative practices in the city, and with the same result: attracting investments in apartments that some seek to live in while others rely on just to safely “deposit” their cash and wait for the opportunity to reap a profit in a city where the “myth” of real estate never devaluing is powerfully mediatized and amplified and where public authorities introduce numerous facilities to encourage real estate investments.

The paper demonstrates that studies of housing financialization require careful documentation of local (individual and collective) practices and a relational analysis of trans-scalar relations that cannot be reduced to the binary of “dependent” or “peripheral” urbanization, even if the latter explains some elements of its unfolding. Therefore, approaches that address housing financialization through the lens of some benchmarks modeled in large-scale projects deployed in the context of advanced economies, whereby Beirut figures as some lesser version of an ideal model (Robinson and Roy, 2016) or a setting attempting to catch up with so-called developed economies (Rahnema and Bawtree, 1997), present skewed and limited reading of larger and more relational patterns.

These findings further present additional findings for cities rife with social divisions such as Beirut. Indeed, as seen in the paper, while capital penetration may appear seamless and pervasive, it still operates through locally rooted and deeply embedded social networks. Thus, capital is far from abstract. Indeed, we have shown how it circulates through the same religious networks that connect families, organizations, and political parties and reproduce the sectarian political system in Lebanon (Mouawad, 2021; Salloukh et al., 2015). Therefore, the production of financialized housing operates within the same narrow sectarian and conservative Sunni networks and reproduces the city’s territorial organization. As a result, and in strong contrast with financial capital that has erased these distinctions in high-end areas of the city, Beirut’s modest networks use and reproduce their sectarian territorial geography, similar to the way planning was found to protect them (Bou Akar, 2020).

Zooming out of the two neighborhoods to the city, we find that the patterns documented are replicated in other areas where similar geometries of territorial and classed segregation enable developers with marked sectarian and political affiliations to reproduce these practices in Beirut and its suburbs (Abou Ibrahim, 2021). Although the study did not dive into the specifics of each neighborhood, a rapid count of all 999 developers identified to have operated in Beirut between 1996 and 2018 indicated that the same territorial affinities whereby developers of a specific sect operate mostly within the confines of a sectarian territory existed. This pattern suggests that in addition to reproducing the classed geography of dispossession, development activities are simultaneously reproducing a sectarian geography, relying on the housing market as yet one more mechanism to entrench this territorial organization of Beirut. Far from a seamless flow of capital, the market therefore creates a multiscalar pattern of relations that ties a specific group of developers to clients and investors, all of whom together constitute the chain of social infrastructures that sustains housing financialization.

In closing, this account of Beirut is far from unique. As financialization seeps into cities, it also modifies imaginaries of the future and forces individuals—developers and homeowners—to engage in speculative practices if they are to stay in place. As such, this study offers a snapshot of a city that was once at the heart of a global economy (Issawi, 1964) and is today a battered urban area, largely ruined by the overlapping effects of the violence induced by war and capital (Fawaz et al., 2026). How this reality is lived is outside the scope of this paper. Nonetheless, it is only by understanding the deeply dispossessive effects of the penetration of capital and locating it comparatively with other cities who have endured similar realities due to the concerted efforts of global and local actors that we can begin to imagine possible pathways for a future where the daunting weight of financialization is put in check.

Footnotes

Acknowledgements

Fawaz and Zaatari contributed to the writing of this paper; all three authors contributed to the research project on which it is based. All three authors are grateful to the editor and the anonymous reviewers who provided valuable comments to an earlier version of this paper. We are also grateful to the Beirut Urban Lab for research support and intellectual engagement.

Author contributions

M.F. and A.Z. contributed to the writing of this paper; all three authors contributed to the research project on which it is based.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Funding for the research was secured through the Open Society Foundation and the Maroun Semaan Faculty of Engineering and Architecture at the American University of Beirut.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.