Abstract

Agglomeration is typically used to explain the benefits of central business districts (CBDs) in large urban areas, but the pandemic has called into question the primacy of CBDs. Previous studies have relied on observational data that uses past behaviour as a predictor of future behaviour. Instead, we conducted a stated preference experiment with 789 businesses to generate robust predictions about the likely future behaviour of firms. Controlling for differences between our sample and the target population in terms of firm size, sector, revenue, and location, we estimate that the average compensating rent differentials for CBD locations are positive and estimated to be $875 per sqm per annum, higher than current market rent differentials in most Australian urban areas. We take this to mean that a substantial proportion of firms strongly value CBD locations and are willing to pay a significantly large premium for the same. Our findings indicate that the changes that were observed in relation to firm location preferences during the pandemic, sometimes characterised as the “donut effect,” are unlikely to be sustained in the long term as the underlying demand for commercial real estate in CBD locations is still strong.

Introduction

At the height of the COVID-19 pandemic, CBDs in major cities became ghost towns. Images of empty streets in once bustling centres became emblematic of lockdown restrictions as people stayed home in attempt to slow the spread of the infection. Firms scrambled to support their employees to work remotely, and as a result remote work grew from around 6% pre-pandemic to 60% during lockdowns (Aksoy et al., 2025). Online retail shopping also spiked, and education pivoted to online forums. Suddenly, CBDs were no longer essential sites from which firms, institutions, and individuals functioned; we learned ways to conduct our business and our lives without travelling to the busiest, most tightly packed areas of our cities. Since the height of lockdown restrictions, remote work has settled into a steady pattern of around 25% of workdays globally (Aksoy et al., 2025): a significant leap from pre-pandemic levels, but also much lower than during lockdowns. Remote work appears to have become an established feature of contemporary working conditions, and online retail and education have also persisted at higher levels than pre-pandemic (Diaz-Gutierrez et al., 2024; Ma and Lee, 2025). What does this mean for CBDs? Will the long-established principles of agglomeration ensure that CBDs continue to rebound and thrive, or will some other mechanism in which centralisation is less critical become established?

The settling of remote work at around a quarter of all workdays would seem to imply a long-term shift in preferences towards remote work rather than a short-term pandemic disruption, but we have limited evidence of the long-term locational preferences of firms in a post-pandemic climate. To date, most studies have relied on observational indicators, such as rent trends, vacancy rates, office space absorption, or relocation patterns, to assess firm behaviour (Fieger et al., 2023; González-Leonardo et al., 2022, 2023; Huang et al., 2023; Rosenthal et al., 2022; Zhou et al., 2021). While valuable, such metrics are susceptible to short-term disruptions like lockdowns, movement restrictions, and changes in public health policy. These disruptions disproportionately affected firms in dense inner-city neighbourhoods, especially CBDs, during the height of the pandemic. Using observational data, it can be difficult to disentangle temporary shocks, such as those caused by lockdowns, from longer-term structural shifts in location preferences.

In contrast, our study investigates how firm location preferences may evolve in the longer term, particularly in response to lasting structural changes such as the normalisation of remote work, increased digitisation, and the expansion of flexible workplace models. Rather than inferring preferences from past behaviour, we employ a stated preference (SP) experimental approach, which allows us to directly assess how firms weigh trade-offs between CBD and non-CBD locations under hypothetical future scenarios. Using this approach, we isolate structural shifts in firm behaviour from temporary pandemic-related disruptions, and address our research questions: (1) Does agglomeration remain the dominant driver of firm location preferences in a post-pandemic context; (2) How do preferences for CBD locations vary across firms, sectors, and spatial contexts; and (3) What do these preferences imply for the future demand and resilience of CBD office markets?

To this end, we conducted a nationally representative online survey, recruiting 789 Australian business owners and senior managers with decision-making authority over business location. Respondents were presented with carefully designed SP experiments in which they evaluated alternative office location scenarios that varied primarily in terms of rent costs and proximity to the CBD. This design enabled us to estimate firms’ willingness to pay for CBD versus non-CBD locations, and to assess how these preferences compare to existing rent differentials observed in commercial property markets. By directly eliciting firm preferences for different location characteristics in a post-pandemic economy, our study provides forward-looking insights into the structural demand for CBD office space—offering a predictive perspective that observational data alone cannot capture.

Our analysis finds that pre-pandemic preferences for CBD locations in the largest metropolitan areas have remained relatively stable. The average Australian firm is estimated to be willing to pay $875 more per sqm per annum for a CBD location, and 34% of Australian firms are willing to pay at least $1000 more per sqm per annum for a CBD location. These compensating rent differentials are above current market rent differentials. We note that as the market is not in equilibrium, there is likely to be a relocation of firms from suburban locations to the CBDs within capital cities. These findings support that: the CBD has maintained its retentive and attractive powers and there is no evidence for the “donut effect” in this context (Ramani and Bloom, 2021); the effect of increasing returns (Krugman, 1999, 2009) shows no signs of abating; and that agglomeration is likely to continue to be a driving force for CBDs, perhaps even intensifying. While remote work, increased digitisation, and the expansion of flexible workplace models continue to drive changes in CBD dynamics and commuter activity, these have not weakened the agglomerative benefits of CBDs.

In summary, this article makes four key contributions. First, it expands the empirical base on firm location preferences using a large nationally representative dataset, providing robust insights into post-pandemic urban dynamics. Second, it employs a novel experimental approach through stated preference modelling, allowing for a more precise assessment of firm trade-offs between CBD and non-CBD locations. Third, it synthesises the economic and social forces shaping firm location choices, integrating insights on digital transformation, workplace flexibility, and urban restructuring. Finally, it challenges the donut effect hypothesis by demonstrating that the underlying demand for CBD locations remains strong.

Agglomeration: Benefits, costs, and pandemic impacts

Urban economics explains the spatial organisation of firms as the outcome of a trade-off between agglomeration benefits and costs. Firms benefit from proximity to other firms, workers, and consumers through mechanisms such as shared labour pools, access to specialised inputs, reduced matching frictions, and knowledge spillovers (Duranton and Puga, 2004; Glaeser, 2010; Marshall, 1890; Rigby and Brown, 2015). These benefits are typically strongest in dense employment clusters, particularly central business districts (CBDs), which maximise accessibility within metropolitan regions (Glaeser, 2011; Rosenthal and Strange, 2004). At the same time, agglomeration generates diseconomies, including high land rents, congestion, pollution, and other urban disamenities (Brinkman, 2016; Gyourko et al., 2013; Hoffmann, 2019; Richardson, 1995). The observed concentration of firms in CBDs can therefore be understood as an equilibrium outcome in which the productivity advantages of proximity outweigh these costs for a substantial subset of firms and activities (Krugman, 1991; Tabuchi and Thisse, 2011; Thisse et al., 2021).

This concentration of firms within CBDs has, in turn, given rise to their broader economic and social significance. CBDs have evolved into dense, multifunctional nodes that operate as major transport hubs, centres of corporate and government decision-making, focal points for advanced services, and locations offering the highest levels of access to urban amenities. In this sense, CBDs play a disproportionately important role in structuring economic activity and social interaction within cities. While this broader perspective is important for understanding the role of CBDs in urban systems, the focus of this paper is specifically on firm location behaviour. CBDs are, first and foremost, business districts, and their persistence ultimately depends on whether firms continue to value the advantages associated with dense central locations.

The COVID-19 pandemic introduced a large and sudden shock to this balance by altering the conditions under which proximity generates value. In particular, the rapid adoption of remote work, the expansion of digital communication and consumption, and heightened sensitivity to public health risks reshaped both the benefits and costs associated with dense urban environments. These changes operate through multiple, interacting mechanisms, making the net effect on agglomeration theoretically ambiguous.

First, the pandemic may have weakened some agglomeration benefits by enabling key economic interactions to occur without physical proximity. Firms adopted digital tools for communication, coordination, and service delivery, allowing access to labour, consumers, and some forms of knowledge exchange to be achieved remotely (Amankwah-Amoah et al., 2021; De et al., 2020; Roggeveen and Sethuraman, 2020; Schilirò, 2021; Vargo et al., 2021; Webb et al., 2021). Although most pronounced during lockdowns, many of these practices have persisted, with remote and hybrid work stabilising at around a quarter of all workdays globally (Aksoy et al., 2025). To the extent that routine interactions and market access can be maintained digitally, the necessity of physical co-location may be reduced for some activities.

Second, hybrid work may simultaneously strengthen other agglomeration mechanisms. By reducing the amount of space required per worker, hybrid work allows more firms and workers to locate within high-value central areas, potentially increasing the effective density of human capital. This may reinforce labour market pooling, expand local consumer bases, and enhance opportunities for interaction and learning, particularly for activities that continue to rely on face-to-face engagement (Delventhal et al., 2022; Gokan et al., 2022; Lennox, 2020; Rappaport, 2022).

Third, the pandemic increased the salience of public health risks associated with density. During the pandemic, densely populated urban environments were perceived as sites of elevated risk, leading to sharp declines in activity within CBDs. Although the immediate threat has receded, this shift in risk perception may persist, influencing worker preferences and organisational policies. If so, this would increase the perceived costs of dense central locations, particularly for firms reliant on large on-site workforces.

Finally, the widespread adoption of remote and hybrid work may have reduced some of the traditional costs of agglomeration, particularly those associated with commuting. Lower commuting volumes and flatter peak demand can alleviate congestion and improve travel time reliability for remaining commuters (Delventhal et al., 2022; Rappaport, 2022). In addition, firms may be able to draw on a broader labour pool if workers are less constrained by daily commuting requirements (Hansen et al., 2023).

Taken together, these mechanisms suggest that the pandemic does not uniformly weaken or strengthen agglomeration, but rather reconfigures its underlying drivers. Some benefits of proximity have become more substitutable through digital technologies, while others remain tied to dense, face-to-face environments. Similarly, some costs of agglomeration may have diminished, while others have become more salient. The overall effect is therefore ambiguous and ultimately depends on how firms evaluate these competing forces when making location decisions. Understanding these behavioural responses is central to assessing the long-term resilience of CBDs in a post-pandemic economy.

Are CBDs bouncing back?

Empirical findings on the resilience of cities and CBDs post-pandemic are heterogeneous, with forecasts ranging from swift rebounding to hastening decline. For example, Brail and Kleinman (2022) found that second-tier cities such as Toronto demonstrated resilience and adaptability during the pandemic and found no evidence of large-scale impacts on either economic activity or population. A German study found a lack of evidence for a flattening of the housing bid-rent curve in CBDs (Beze and Thiel, 2025). A US study found that offices were beginning to recentralise post-pandemic and challenged the narrative that the pandemic was causing urban core decline (Graves et al., 2023). New Zealand research found spending patterns in CBDs had shifted with increased spending on home, recreation, groceries, liquor, and entertainment, but decreased spending on hospitality. Overall, the authors concluded not that the CBD was in decline, but that CBDs and their users were adapting (Fieger et al., 2023). Meanwhile, two different Spanish studies found (1) no evidence of the donut effect (González-Leonardo et al., 2023) and (2) heterogeneity in degrees of resilience between employment sectors (Sánchez-Moral et al., 2024).

Conversely, research from New Delhi found that the pandemic hastened the decline of CBDs and suggests that CBDs need to be reinvented for the current climate (Jha, 2021). Research on eighty-nine US cities found commercial rents declined post-pandemic, especially in cities that relied on public transit, implying preferences for lower density locations (Rosenthal et al., 2022). And research into sixty Chinese cities found the pandemic reduced the price premium for tall buildings, and increased it for residential buildings, indicating a growing preference for lower density living (Huang et al., 2023).

Taken together, this brief overview of the global literature on the impact of the pandemic on cities and CBDs demonstrates that city size and extant characteristics, industry type and resilience, transport options, and firm and residential location preferences are amongst the factors that will impact a CBD’s response to a significant disruption such as the pandemic. As yet, it is unknown how this effect will play out. Some suggest that the rise of remote work will catalyse a more fundamental restructuring of urban land use, with declining demand for CBD office space, rising commercial vacancies, and new pressures on city planning and governance (Brail and Kleinman, 2022; Ramani and Bloom, 2021), while others, as we have seen, predict increased human capital density (Delventhal et al., 2022; Gokan et al., 2022; Lennox, 2020; Rappaport, 2022). The sharp increase in CBD office vacancies during the early stages of the pandemic appeared to support this former view—referred to as the “donut effect” by Ramani and Bloom (2021). Yet subsequent studies have provided evidence that the donut effect was not widespread or persistent (Beze and Thiel, 2025; González-Leonardo, et al., 2023; Graves et al., 2023; Lennox, 2020). There is no universal acceptance of which mechanism will predominate as a long-term structural outcome, and to date, findings are heterogeneous and largely based on observational studies. This leaves scope for experimental studies such as this to make predictions about likely future firm location preferences and the impacts of these preferences for CBD resilience.

Experiment design

We conducted an online stated preference (SP) survey between December 2022 and February 2023, targeting Australian business owners and senior managers with decision-making authority over firm location. The survey collected information on business characteristics, current location, pandemic-related operational changes, working-from-home practices, and future location preferences.

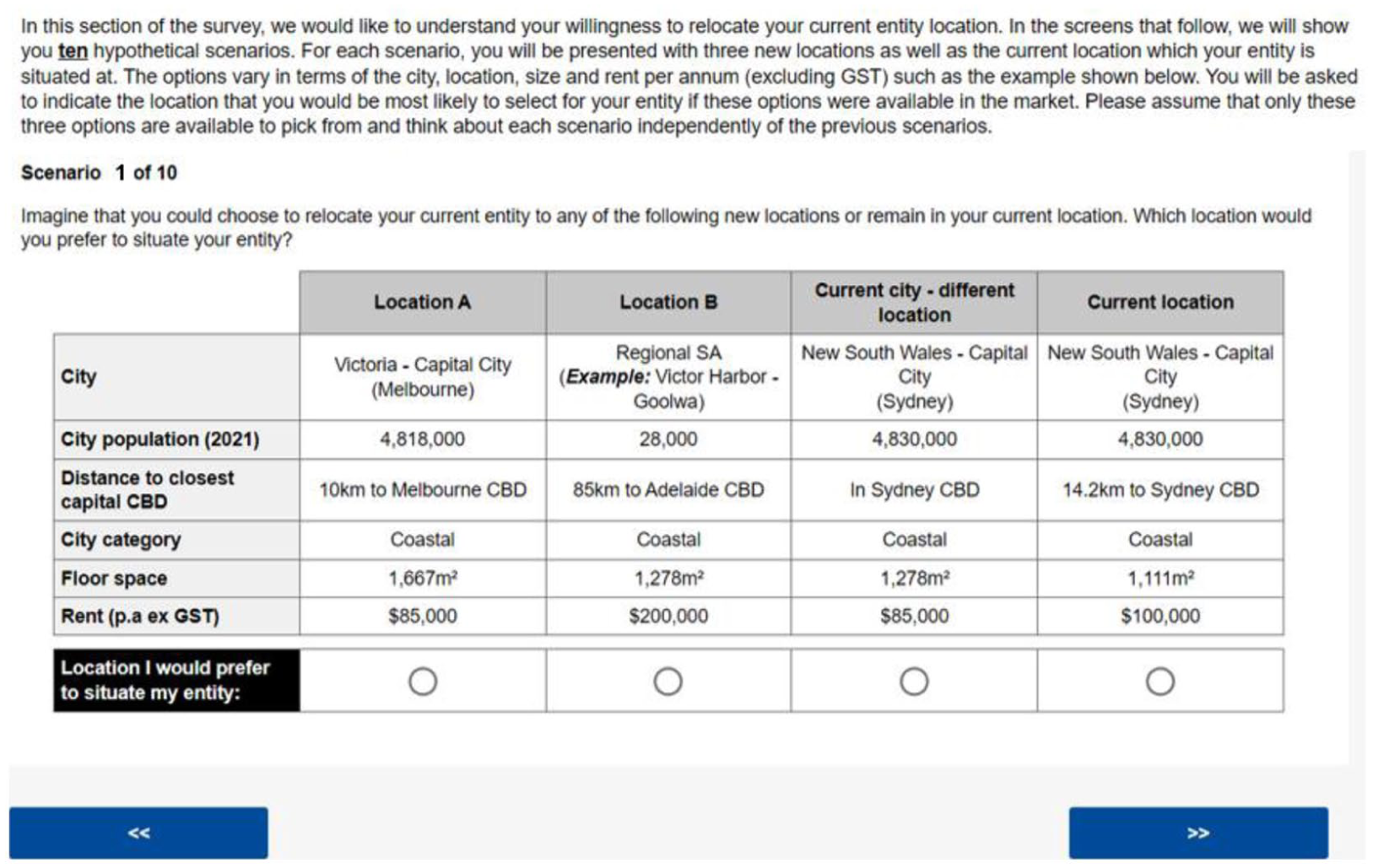

To elicit forward-looking preferences, respondents were presented with a series of hypothetical relocation scenarios in which they evaluated alternative office locations. In each scenario, respondents could choose between relocating to one of three new locations or remaining in their current location. The alternatives varied along key attributes, including rent, available floor space, and proximity to the nearest CBD. Attribute levels were systematically varied using an experimental design to enable identification of trade-offs between cost and location characteristics.

Two of the three relocation options in each scenario were randomly drawn from a set of 68 Australian significant urban areas (population >20,000), while the third option was a location within the respondent’s current city. For locations within capital cities, distance to the CBD was explicitly varied. Rent and floor space were specified relative to each firm’s current conditions to ensure that scenarios were realistic and interpretable across a heterogeneous sample.

SP experiments provide a structured framework for analysing trade-offs under hypothetical but policy-relevant conditions, and are particularly well suited to contexts characterised by structural change, where past behaviour may not reliably predict future decisions (Louviere et al., 2000; Mitchell and Carson, 2013). In the context of the COVID-19 pandemic, where observed market outcomes reflect a combination of temporary disruptions and emerging long-term adjustments, this approach allows us to isolate firms’ underlying preferences for location attributes.

Each respondent completed 10 choice scenarios (Figure 1), generating repeated observations of location preferences under varying conditions. While the scenarios are necessarily hypothetical, the design reflects current market conditions and organisational practices at the time of the survey. As such, the results should be interpreted as capturing firms’ stated preferences under post-pandemic conditions, rather than realised behaviour.

Example scenario to elicit firm preferences for relocation to different locations.

Sampling frame

The survey targeted Australian business owners and senior managers with individual or shared authority over firm location decisions, verified through screening questions. While relocation decisions are often made within broader organisational structures, the sample captures the perspectives of those directly involved in, or influential to, these decisions.

Recruitment was undertaken through the market research firm PureProfile, which maintains a large national panel of business respondents. Given the specialised target population, an initial target of approximately 1000 responses was set, with 789 completed responses ultimately obtained.

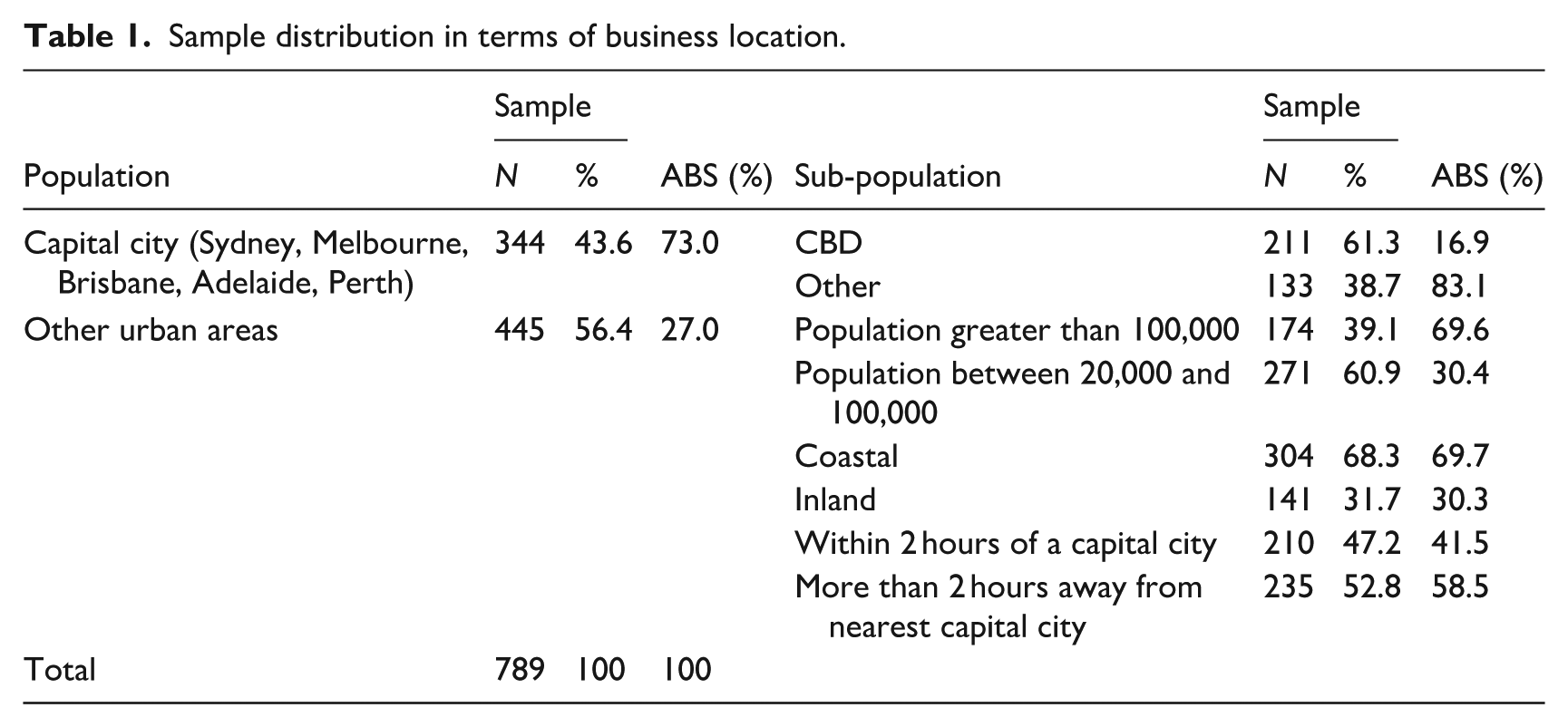

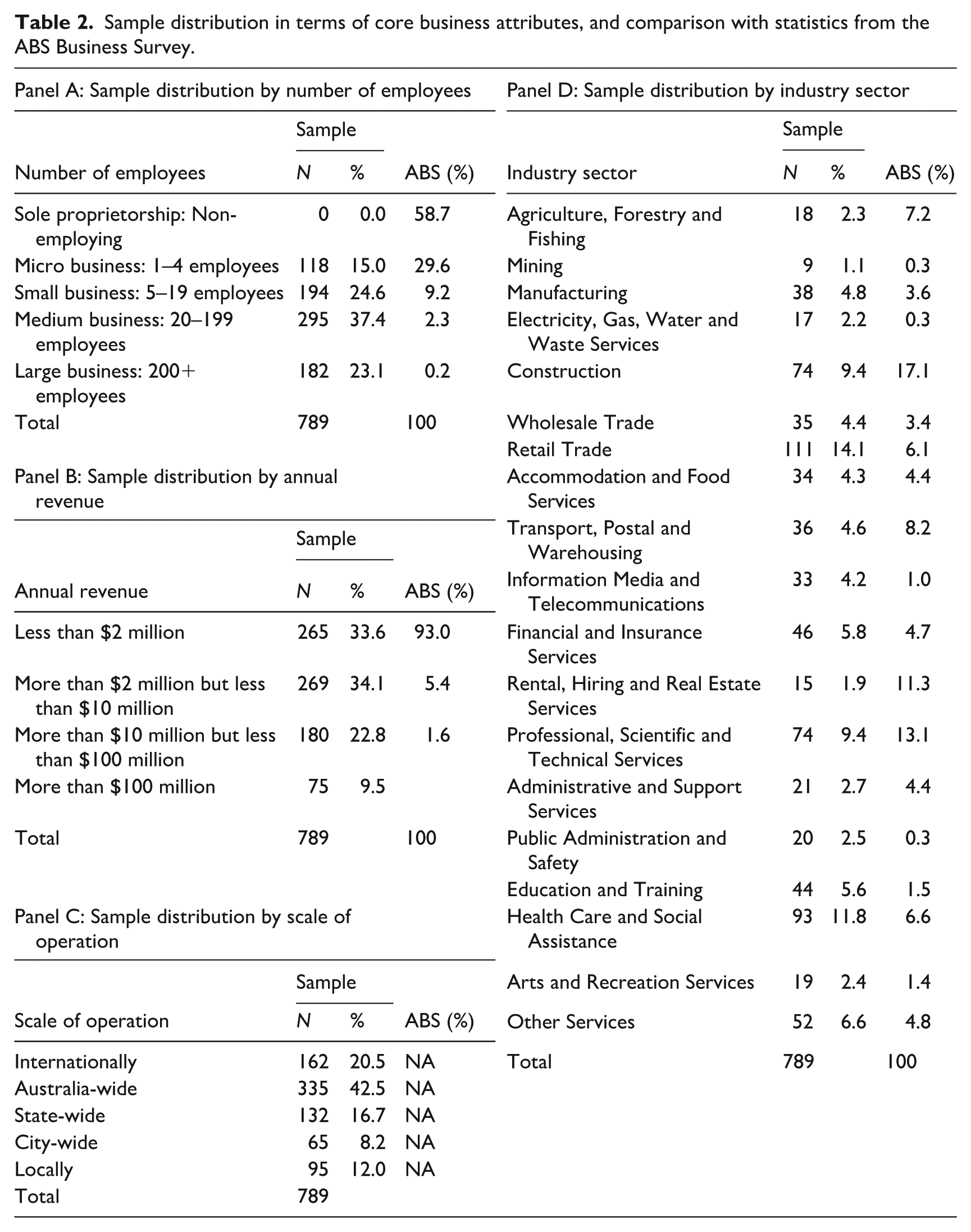

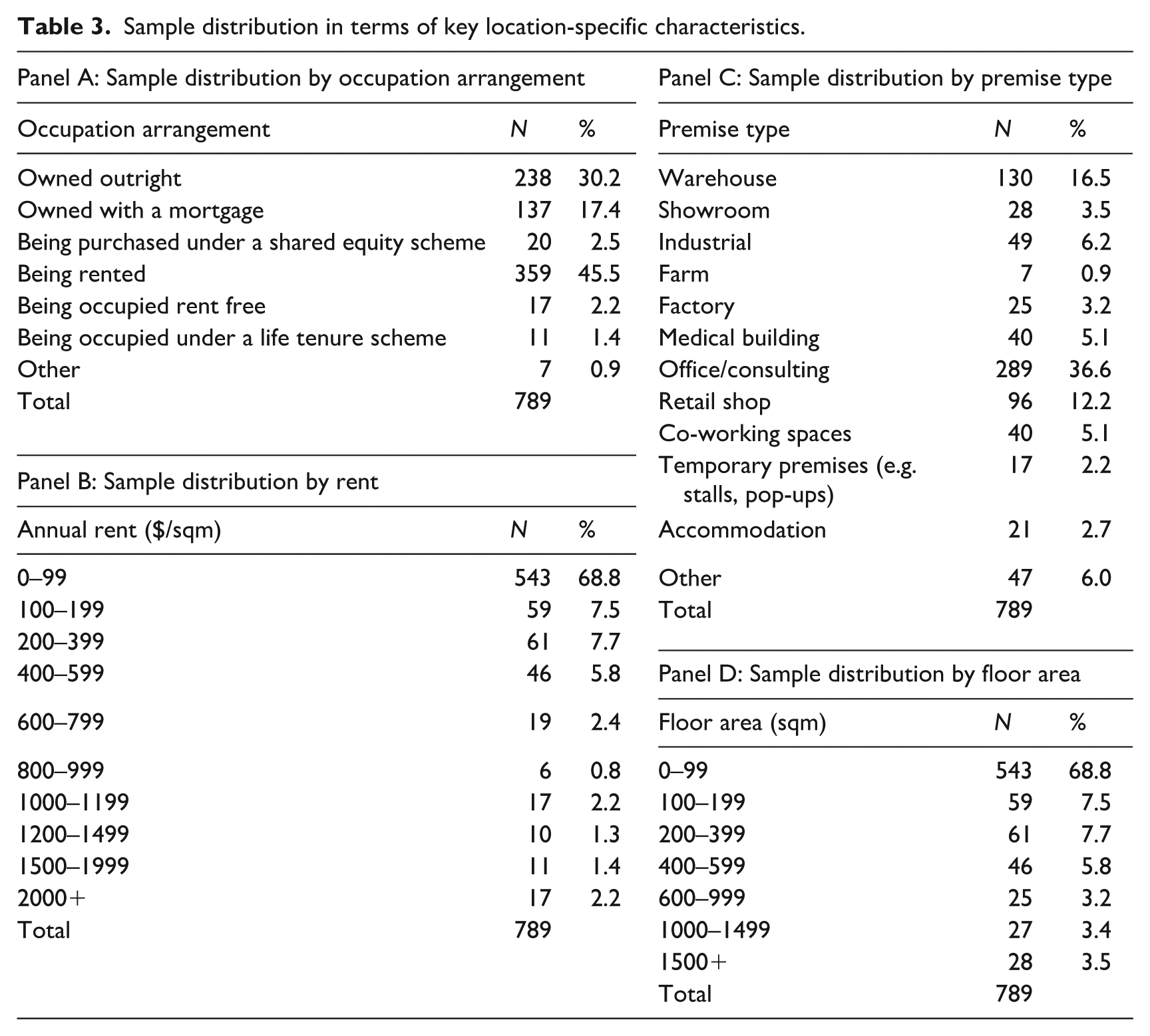

Tables 1 to 3 summarise the sample across key dimensions. Table 1 reports the geographic distribution of firms, showing coverage across capital cities and regional areas, with a higher representation of CBD-based firms within major cities than in the general population. Table 2 presents core business characteristics, including firm size, revenue, sector, and scale of operations. The sample includes a relatively higher proportion of medium and large firms compared to the population, reflecting the focus on firms that exert greater influence on commercial real estate markets. Table 3 reports location-specific characteristics, including occupation arrangement, rent levels, premise type, and floor area, indicating broad coverage across different types of business environments. To account for differences between the sample and the broader population of Australian firms, all results are reweighted based on firm size, sector, revenue, and location.

Sample distribution in terms of business location.

Sample distribution in terms of core business attributes, and comparison with statistics from the ABS Business Survey.

Sample distribution in terms of key location-specific characteristics.

In addition to the survey, qualitative insights were obtained through 47 interviews with senior industry stakeholders, including commercial landlords, property agents, and asset managers. These interviews are used to contextualise and interpret the quantitative findings.

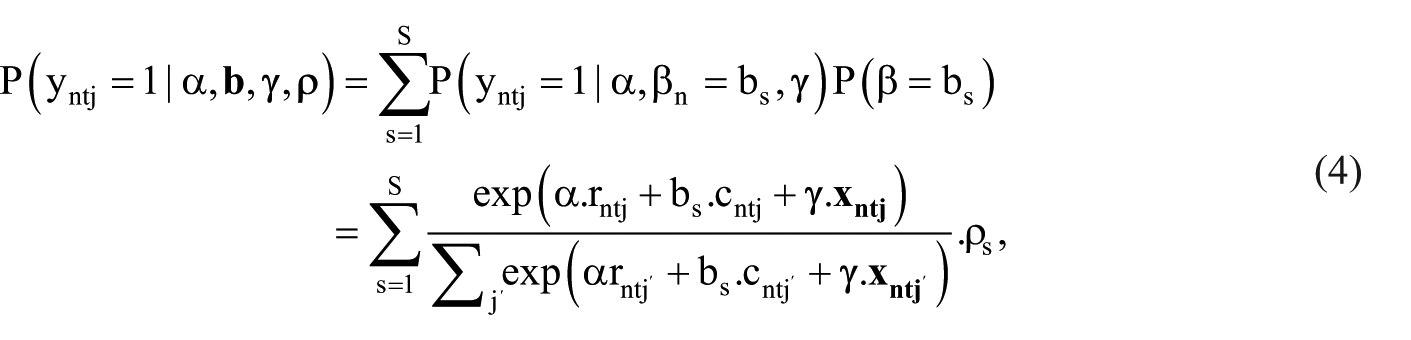

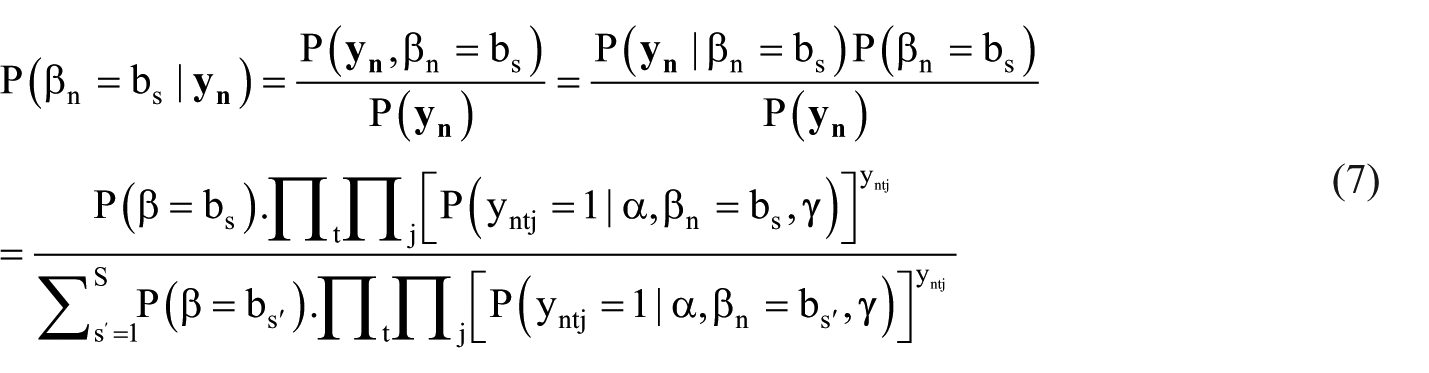

Model of firm location

Assume that firm

where

Assuming that all firms are seeking to maximise their utility, and that the stochastic component

where we introduce the binary variable

where

where we use

which can be maximised to derive estimates for each of the model parameters

Once the model parameters have been estimated, we can apply Bayes theorem to equation (5) to derive the posterior probability of class membership for each firm in our sample, based on their vector of observed choices

These posterior probabilities can subsequently be used to estimate compensating rent differentials for CBD locations for each firm in our sample:

These can be aggregated across dimensions of interest such as firm size, sector, and location, to examine how compensating rent differentials might vary as a function of each of these attributes, and reweighted to account for differences between our sample and the broader business population, ensuring that our estimates are representative at the population level.

Results and findings

Responses to the SP experiments from the 789 business owners and senior business managers who participated in our online survey were used to estimate a model of firm location preferences, and to derive compensating rent differentials for CBD locations for each firm in our sample: that is, how much extra they are willing to pay for a CBD location over a non-CBD location within the same urban area, as described in the “Experiment design” section.

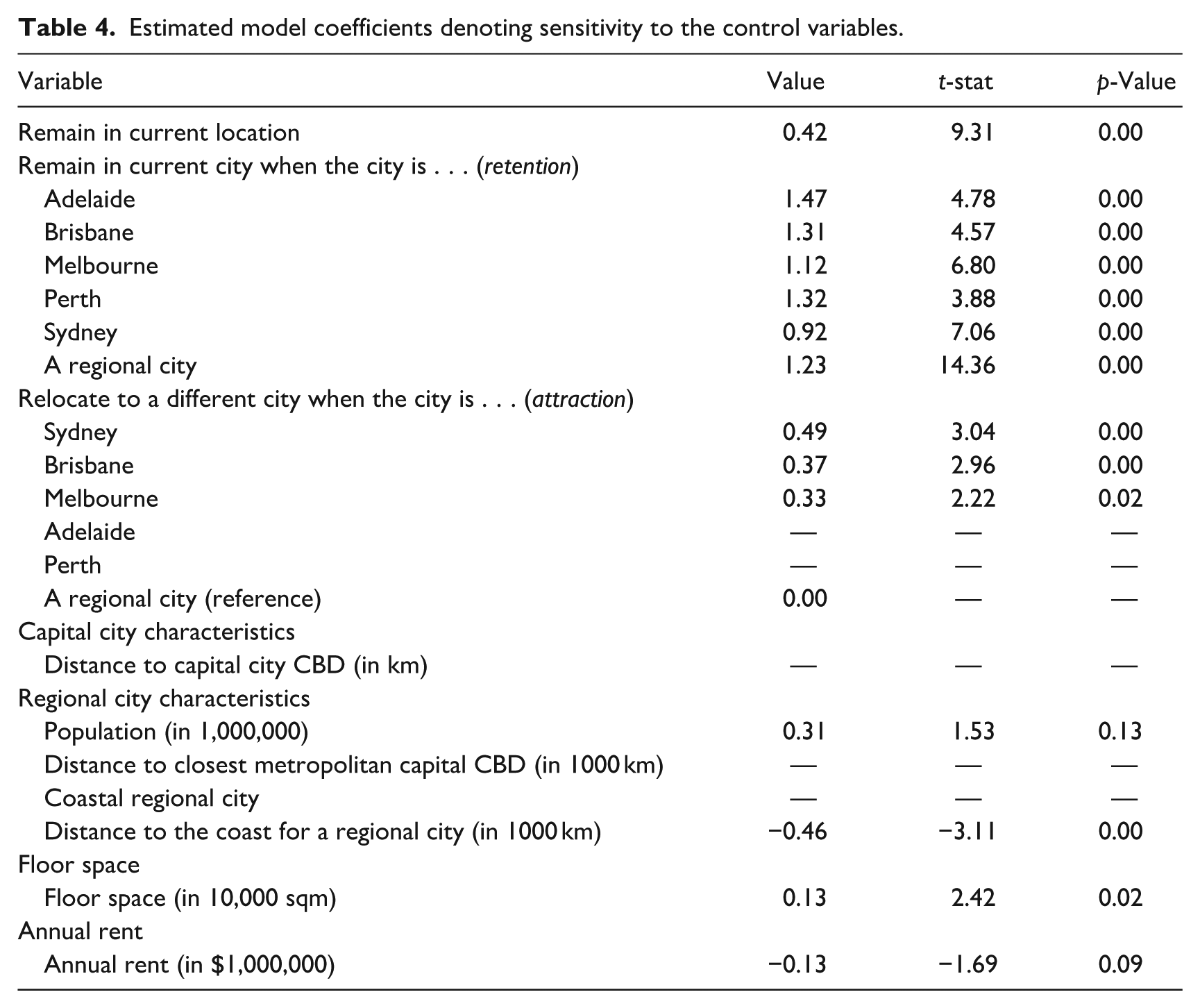

We estimated different model specifications, and we report results for our final and preferred model specification in this section. The final model specification has a McFadden’s R-squared of 0.170. Table 4 presents estimates for model coefficients denoting sensitivity to the control variables, as denoted by

Estimated model coefficients denoting sensitivity to the control variables.

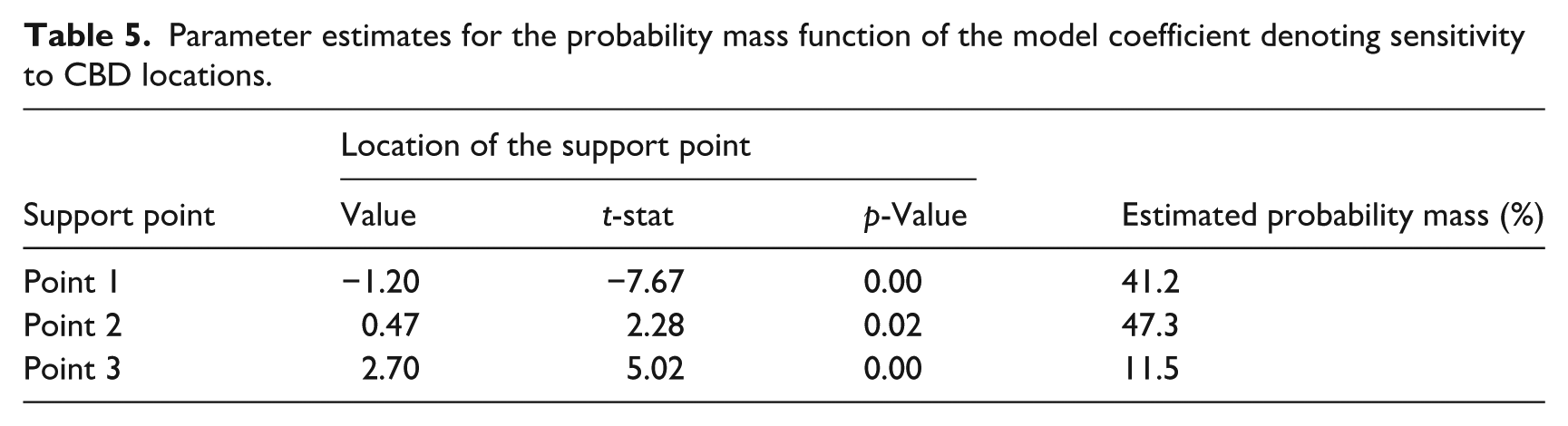

Similarly, Table 5 presents estimates for the parameters

Parameter estimates for the probability mass function of the model coefficient denoting sensitivity to CBD locations.

Over the following paragraphs, we summarise the key findings from the model in terms of compensating rent differentials for CBD locations. Note that our analysis controls for differences between our sample and the target population of all Australian firms in terms of firm size, sector, revenue, and location. To structure the presentation of results, we first examine aggregate firm preferences for CBD locations to assess whether agglomeration remains the dominant driver of location decisions (RQ1). We then explore heterogeneity in these preferences across cities, sectors, workplace types, and firm characteristics (RQ2), to understand how the value of CBD locations varies across different economic contexts. Finally, we consider the implications of these findings for the future demand and resilience of CBD office markets (RQ3).

Aggregate preferences for CBD locations

We begin by examining aggregate firm preferences for CBD locations to assess whether agglomeration remains the dominant driver of location decisions in a post-pandemic context (RQ1). This provides a baseline indication of the overall strength of demand for central locations across Australian firms.

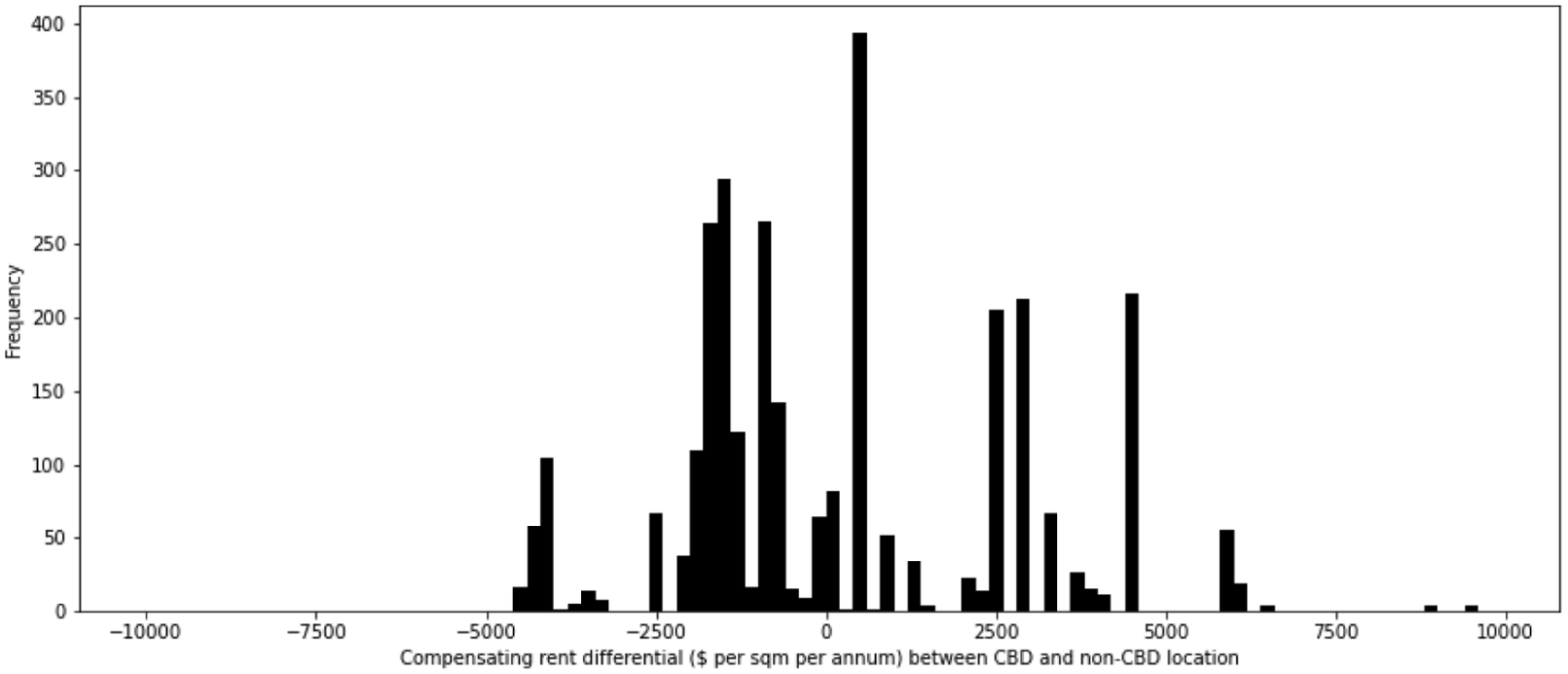

Figure 2 plots the estimated distribution of compensating rent differentials (CRDs) for CBD locations across Australian firms. We estimate that the median Australian firm is indifferent between CBD and non-CBD locations: that is, the compensating rent differential between the two locations for the median firm is close to zero. However, the average compensating rent differential is positive and estimated to be $875 per sqm per annum. A substantial proportion of firms highly value CBD locations, and are willing to pay a significantly high premium for the same—34% of Australian firms are estimated to be willing to pay at least $1000 more per sqm per annum for a CBD location. Based on 2024 office space market data, current rent differentials between CBD and suburban locations are roughly $200–$400 in most large urban areas in Australia, though they are as high as $400–$800 in Sydney, where average CBD rents are $1460 per sqm per annum (CBRE Research, 2024; PCA, 2024). Our average estimate is higher than current differentials across most large urban area markets. In general, our findings indicate that there is still a strong demand for CBD locations among a sizeable proportion of Australian firms.

Estimated distribution of compensating rent differentials for CBD locations across Australian firms.

Heterogeneity in firm preferences

We next examine how preferences for CBD locations vary across firms, sectors, and spatial contexts (RQ2). This heterogeneity provides insight into which types of firms continue to benefit most from agglomeration and which are less reliant on central locations.

Figures 3 to 7 present box-and-whisker plots of CRDs between CBD and non-CBD markets, disaggregated by a range of firm and workplace characteristics. The wide dispersion of values makes visual interpretation challenging, but this variation is itself informative: it highlights the heterogeneity of Australian firms and the diverse economic functions that CBDs continue to serve. To capture this nuance, we report both means (shown as black dots) and medians (as black vertical lines), as each provides complementary insights. Medians are less sensitive to outliers and offer a clearer indication of the “typical” firm within each subgroup, whereas means reflect the influence of small but important minorities of firms that place very high value on CBD locations. In sectors and workplace types where such skewness is substantively meaningful, this distinction is especially informative. For these variables, we therefore order categories by their median CRDs; for other variables, we retain the natural or categorical ordering. Together, these visualisations provide a detailed and robust picture of how CBD preferences vary across different types of firms and contexts.

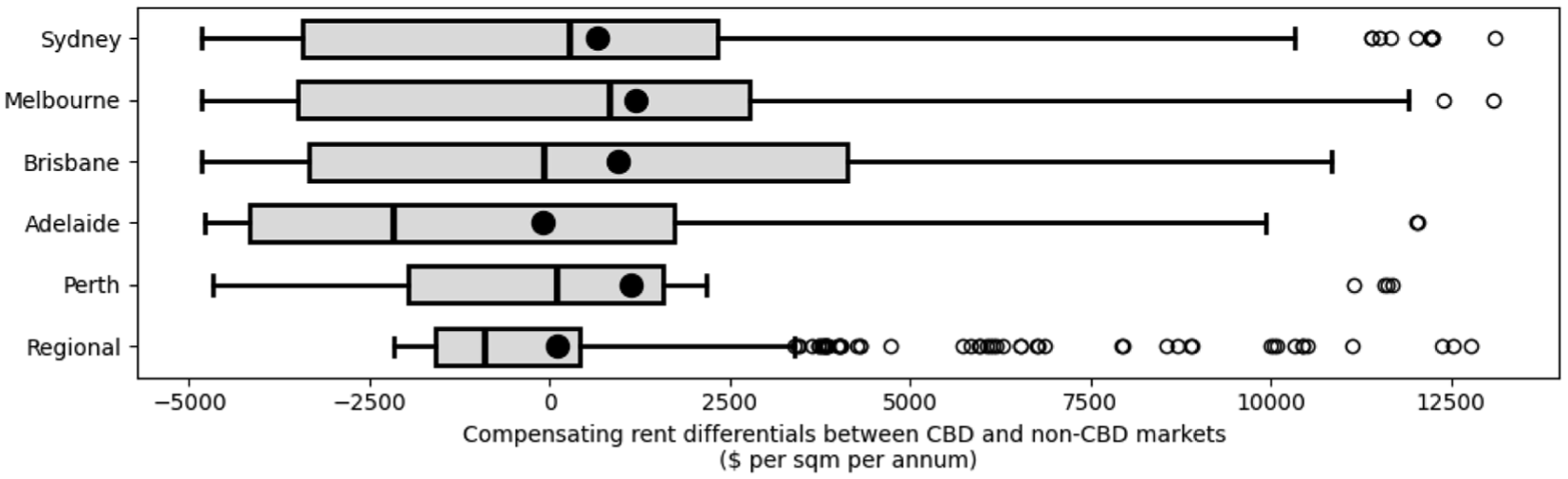

Estimated compensating rent differentials between CBD and non-CBD markets as a function of the city where firms are currently located.

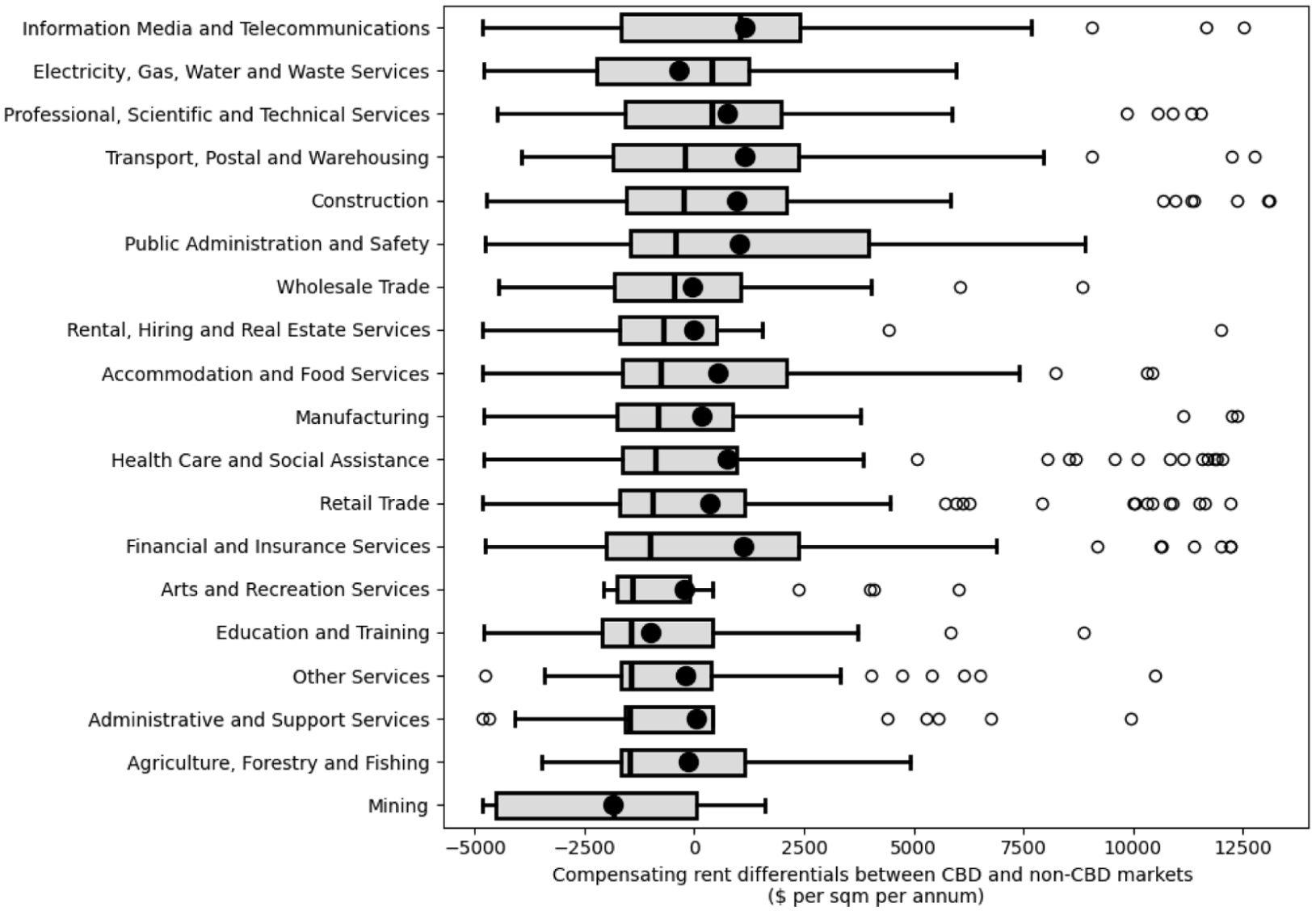

Estimated compensating rent differentials between CBD and non-CBD markets by firm sector.

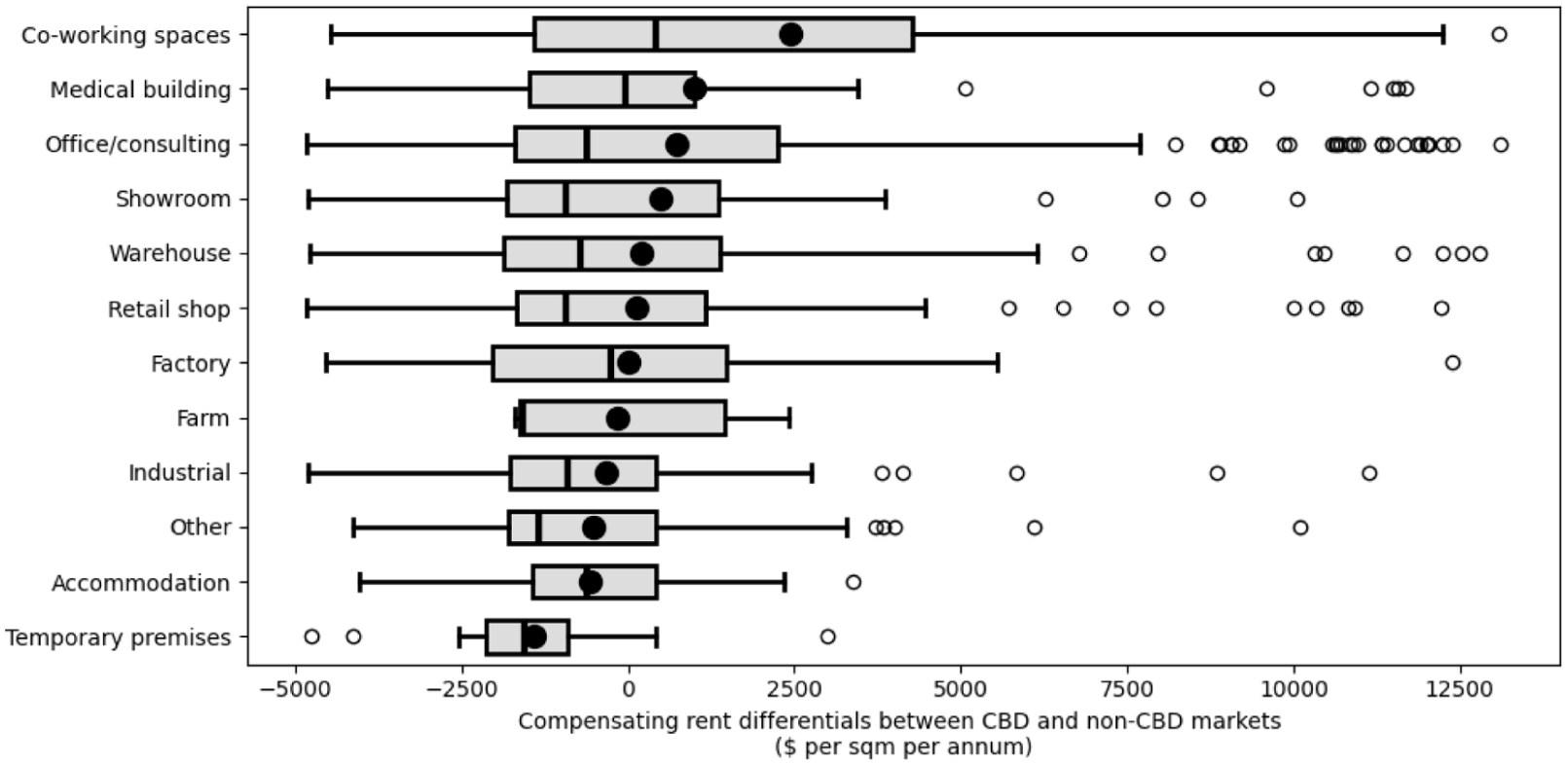

Estimated compensating rent differentials between CBD and non-CBD markets within capital cities by firm workplace type.

Estimated compensating rent differentials between CBD and non-CBD markets by firm size.

Estimated compensating rent differentials between CBD and non-CBD markets, based on whether the firm is currently located in a capital city CBD or not.

Figure 3 compares average CRDs across Australia’s major cities and regional centres. A clear spatial gradient emerges. Melbourne, Perth, and Brisbane exhibit the highest mean CRDs, typically close to or exceeding $1000 per sqm per annum, consistent with their relatively monocentric structures where CBDs remain the primary centres of employment. Sydney shows a more moderate CRD, around $650, reflecting its polycentric urban form and the greater dispersal of firms across multiple sub-centres. As expected, Adelaide and regional locations record near-zero CRDs, suggesting that smaller cities lack the scale necessary to generate strong agglomeration benefits. These results highlight how differences in metropolitan structure shape firms’ valuations of central locations.

Figure 4 disaggregates CRDs by industry sector and reveals systematic patterns aligned with established theories of agglomeration. The sectors with the highest median CRDs, such as Information Media and Telecommunications, Electricity, Gas, Water and Waste Services, Professional, Scientific and Technical Services, and Transport, Postal and Warehousing, are those most strongly linked to centrality advantages and agglomeration economies. These industries rely heavily on access to dense labour markets, proximity to suppliers and clients, and opportunities for knowledge exchange, and their consistently positive medians reflect this dependence. In contrast, sectors with low or negative median CRDs, such as Mining, Agriculture, Forestry and Fishing, Administrative and Support Services, Other Services, and Education and Training, tend to be land-intensive, resource-dependent, or less reliant on knowledge spillovers. These industries benefit less from CBD proximity and often require larger or specialised premises that are more feasibly located outside capital-city cores. Across the full distribution, means are often higher than medians in knowledge-intensive sectors, reflecting the presence of a minority of firms that place extremely high value on CBD locations. This divergence underscores the conceptual distinction between industries driven by agglomeration benefits and those whose production processes are shaped predominantly by land, input, or resource requirements rather than urban density.

Figure 5 reinforces these sectoral patterns by illustrating how operational requirements shape firms’ spatial preferences. Workplaces that are inherently urban in function, most notably co-working spaces and medical buildings, exhibit the highest median CRDs, reflecting the importance of client accessibility, centralised amenities, labour market depth, and proximity to professional networks. Several workplace types, most notably co-working spaces, medical buildings, office/consulting premises, retail shops, and showrooms, exhibit a substantial gap between their medians and means. In these categories, the median firm is willing to pay only modest premiums for CBD locations, yet the mean is pulled sharply upward by a small minority of firms reporting very high CRDs. This pattern indicates that while CBD locations offer limited incremental value for most firms in these segments, there exists a distinct subset that derives exceptional benefit from centrality, client proximity, or access to specialised labour and amenities. By contrast, factories stand out for the opposite reason: the mean and median are very close, indicating that firms in this category are far more homogeneous in their preferences, with few extreme outliers. Although the median CRD for factories is moderately positive, suggesting some value placed on centrality, the absence of highly positive or highly negative tails explains the tight clustering around the central tendency. Other workplace types, such as warehouses, industrial premises, accommodation, and other services, show relatively modest median CRDs, reflecting mixed or limited dependence on CBD attributes. At the lower end of the distribution, temporary premises and farms exhibit negative medians, consistent with activities for which land availability, transport access, or low rents dominate location decisions. Together, these patterns reveal how workplace form shapes the distribution, not just the average level, of firms’ spatial preferences. Some workplace types display a broad dispersion with a minority of CBD-dependent firms, while others reflect much more uniform preferences across the sector.

Figure 6 shows how CRDs vary by firm size. Medium-sized firms exhibit the highest average CRDs, suggesting they are best positioned to benefit from external agglomeration economies. Smaller firms typically lack the scale to fully capitalise on these advantages and tend to face greater budget constraints, resulting in lower average CRDs. Large firms, meanwhile, may internalise many agglomeration benefits within their own multi-site structures, reducing their reliance on the CBD. This non-linear pattern is consistent with theories emphasising that agglomeration benefits are most valuable to firms that are large enough to participate in dense business networks but not so large that they can substitute for them internally.

Finally, Figure 7 compares CRDs for firms currently located in capital-city CBDs to those situated elsewhere. Firms already in CBDs exhibit markedly higher CRDs, often well above prevailing rent differentials, highlighting strong locational stickiness. Once embedded within CBD networks, firms appear to place substantial value on the accumulated advantages of proximity to clients, suppliers, skilled workers, and complementary firms. This revealed preference reinforces the broader conclusion that, despite structural shifts such as remote work and digitisation, CBDs continue to deliver significant benefits that many firms are willing to pay a premium to retain.

Taken together, these results highlight several consistent sources of heterogeneity in firms’ valuation of CBD locations. Preferences are strongest in large, monocentric cities where agglomeration benefits are most pronounced, and in sectors and workplace types that rely on dense labour markets, client accessibility, and knowledge exchange. Firms operating in knowledge-intensive industries and service-oriented environments exhibit particularly high willingness to pay for central locations, often with a small but influential subset placing extremely high value on CBD proximity. In contrast, firms in land-intensive, resource-based, or routine service sectors show weaker or even negative preferences for CBD locations, reflecting a greater reliance on space, cost minimisation, or decentralised operations. Differences by firm size and current location further reinforce these patterns, with medium-sized firms and those already embedded in CBDs exhibiting the strongest preferences. Overall, the value of CBD locations is not uniform, but varies systematically with the economic function, spatial context, and organisational characteristics of firms.

Implications for CBD office markets

While the preceding results establish strong stated preferences for CBD locations, we now consider the implications of these preferences for the future demand and resilience of CBD office markets (RQ3). We compare stated preferences with observed market indicators and relocation patterns to assess whether current market trends reflect structural change or temporary adjustment.

We use our model to estimate the relative current demand for office space in CBD locations across Australian firms. At current market rent differentials, our model estimates that the demand for office space in CBD locations would be 67% of the total demand for office space, measured in terms of the proportion of office space occupied by firms that are willing to pay more for a CBD location than the given rent differential. CBD locations have historically comprised roughly 70% of total office stock in Australian cities prior to the pandemic (PRP, 2018). Therefore, our model indicates that preferences for CBD locations among Australian firms have remained more or less stable following the pandemic.

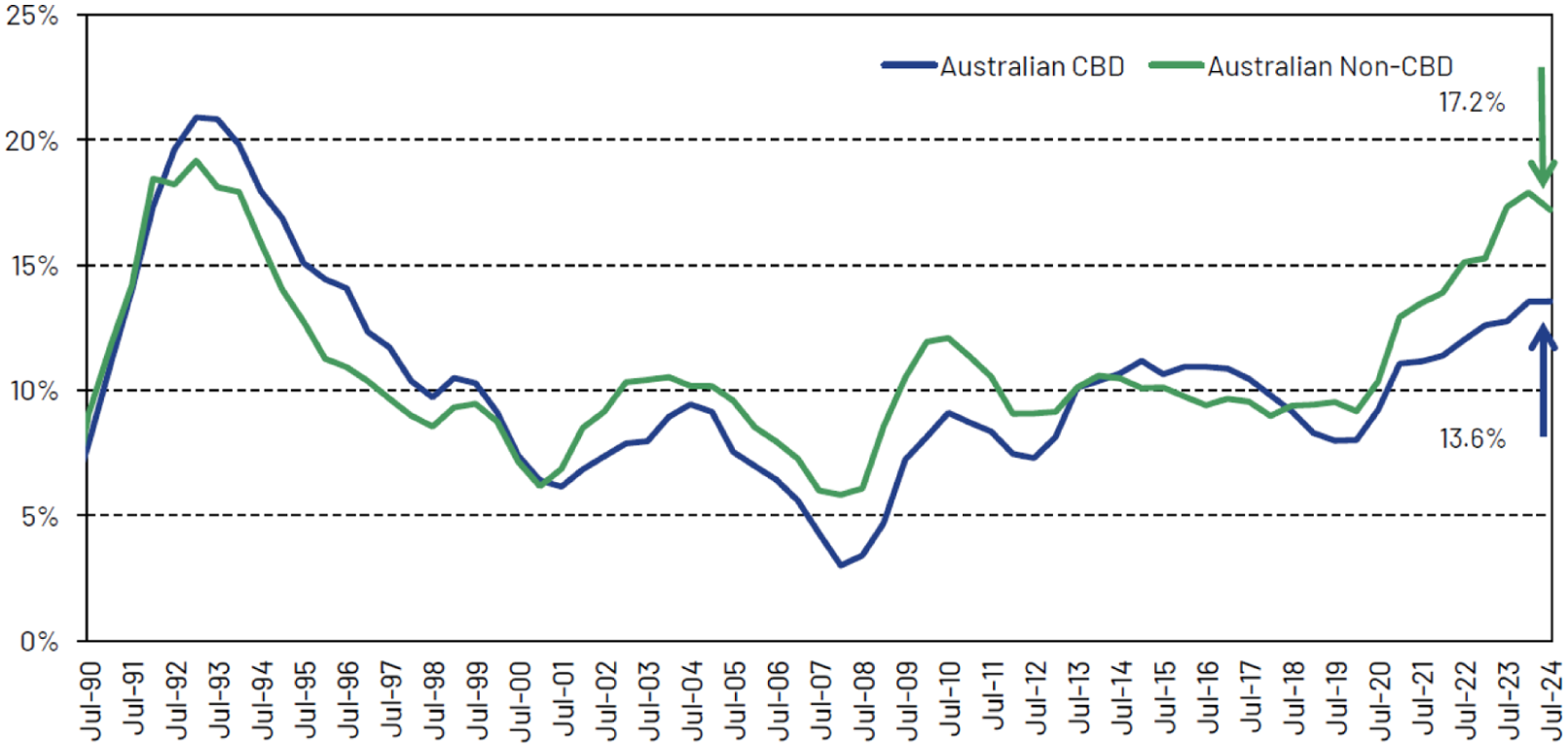

While these findings might seem contrary to high levels of vacancy rates currently observed across most Australian business districts, more detailed spatial analysis of secondary data obtained from the Property Council of Australia on vacancy levels across different cities and districts supports our findings (PCA, 2024). As seen in Figure 8, as of July 2024, vacancy rates are higher in non-CBD markets (17.2%) than CBD markets (13.6%). We note further that secondary business districts in the largest capital cities, such as Crows Nest/St Leonards in Sydney and St Kilda Road in Melbourne, have higher vacancy rates than primary CBDs in Sydney and Melbourne. In general, vacancy rates have grown across most markets, due most likely to the short-term impacts of lockdowns and border closures that severely hindered economic activity during the pandemic, as well as long-term impacts of increased uptake of remote working, which has likely deflated the net demand for office space across all locations, CBD and otherwise.

Average vacancy rates in office space across CBD and non-CBD markets in Australia over time.

Our finding is further supported by observed relocation patterns during the pandemic. Of the 789 firms in our sample, 47 firms reported relocating within a capital city since the onset of the pandemic. Of the 23 firms that were previously located in a capital city CBD, 19 relocated to another location within the same CBD, and only 4 firms moved to a non-CBD location. In contrast, of the 24 firms that were previously located in a non-CBD location within a capital city, 12 firms moved to another non-CBD location, but 12 firms moved to a CBD location. Similar findings were picked up by our qualitative interviews as well: Recently, one client moved 90 per cent of their operation from what is now seen as an inferior suburban office park location and relocated in the CBD. Rent is not a primary driver for such clients. They want CBD amenities to attract staff . . . There is an increasing recognition that suburban office parks are just not a great place to work. Although this view is more widely held by younger people it is not limited to them. Employers are also recognising that employees in their 20s need time to learn their craft in the workplace and gain a certain level of confidence through mentoring. This is just easier in CBD locations. (Metropolitan agent/landlord)

In the early days of the pandemic, there was some speculation in support of the hub and spoke model of firm location, where large firms retain their existing CBD headquarters facility, albeit downsized, and couple it with one or more smaller, decentralised facilities that could be located in lower-rent suburban, out of town locations, or in different metropolitan cities entirely. However, we find limited support for the model. Only 4% of the 789 firms in our survey indicated that they were highly likely to open a satellite premises in the next 2–3 years. Our qualitative interviews found that early investigations by firms or their agents into the hub and spoke model revealed that it would be too costly to put into practice. Additionally, there was a strong feeling that the model would lead to duplication of functions in multiple locations, reducing efficiencies and driving up costs, as indicated by the following comment from a real-estate agent: There was a lot of talk about the hub and spoke model but companies don’t like it because it adds cost. Some companies like PWC or Deloitte have a Parramatta office, but they did that because of the government trends, so they might let employees work there but they were based there anyway. I am not aware of any company that has set up in suburban locations without a reason like this. There is too much cost involved. (Commercial real-estate agent)

In summary, despite the multiple and potentially offsetting mechanisms through which the pandemic could reshape firm location preferences, the empirical evidence points to a clear and consistent pattern. While digital technologies and hybrid work have reduced the necessity of physical proximity for some activities, these effects have not fundamentally displaced the role of CBDs within large metropolitan areas. Instead, CBDs continue to be the most preferred long-term locations for a substantial share of firms, particularly those operating in dense urban economies where agglomeration forces remain strongest. At the same time, this persistence is not uniform: the value of CBD locations varies systematically across cities, sectors, and firm types, reflecting underlying differences in production processes and spatial requirements. Taken together, these findings suggest that the pandemic has not overturned the logic of agglomeration, but has instead reinforced a more differentiated and selective role for CBDs within the urban system.

Conclusions

This paper uses a novel experimental approach to forecast the long-term effects of the pandemic on firm location preferences. Our research shows that pre-pandemic preferences for CBD locations in the largest metropolitan areas have remained relatively stable. The average Australian firm is estimated to be willing to pay $875 more per sqm per annum for a CBD location, and 34% of Australian firms are willing to pay at least $1000 more per sqm per annum for a CBD location. These compensating rent differentials are above current market rent differentials. We note that as the market is not in equilibrium, there is likely to be a relocation of firms from suburban locations to the CBDs within capital cities. This is also reflected in our relocation findings with a greater proportion of firms relocating into CBDs than out of CBDs.

The pandemic has impacted remote work with over 20% of the workforce in developed economies such as Australia now anticipated to be working remotely on any given day in the long term (Aksoy et al., 2025; Vij et al., 2023a). CBD workers were more likely to work remotely than those employed in the suburbs, and related research has found that knowledge workers and highly skilled workers are more likely to work remotely (Gokan et al., 2022; Vij et al., 2023b). With firms likely to remain in their CBD locations while continuing to support remote work practices, a prediction of reduced CBD activity seems sensible—hence a potential hollowing out of CBDs, or the donut effect (Ramani and Bloom, 2021), is plausible. However, our research indicates that the donut effect is unlikely to occur. Rather, our research supports Rappaport’s (2022) prediction that suburban firms are likely to relocate to the CBD if real estate becomes freed up by the smaller footprints of current CBD firms. Our findings also support Delventhal et al.’s (2022) findings regarding the strength of CBDs, and Australian research by Lennox (2020) in which jobs remain in the core of CBDs, while workers live further from CBDs and commute less frequently. This would imply that CBD real estate use will intensify as firms require less space than in pre-pandemic times, but more firms occupy CBD addresses. Rappaport (2022) noted that if fewer people commute to the CBD, transport times would be reduced and congestion would ease; however, this will depend on the densification effect of new firms moving into CBD spaces.

A further potential impact on firm location is possible. If residents spend more time working remotely, it is likely that this will create new demand for services in these suburbs and new firms will establish in these areas. This suburban densification effect requires further research, and this investigation will inform the salience of Florida et al.’s (2023) prediction that CBDs will undergo microgeographic changes such as becoming less focussed on economic purposes and more aligned to social and cultural purposes. Our research indicates that CBDs will retain their economic purpose and firm densification is likely to generate microgeographic change, rather than CBDs becoming places of cultural gathering.

Taken holistically, our evidence indicates that the CBD has maintained its retentive and attractive powers, that the effect of increasing returns (Krugman, 1999, 2009) shows no signs of abating, and that agglomeration is likely to continue to be a driving force for CBDs, perhaps even intensifying. Despite the significant disruptive effects of the pandemic and increased digitisation, agglomeration still predominates. Our evidence supports Florida et al.’s (2023) predictions that “The winner-take-all economic geography of cities will remain in force” and that “medium-sized cities and rural areas, especially those far from dynamic economic centres, may lose out.” Further, it offers an alternative to Ramani and Bloom’s donut effect, providing evidence that firms are still drawn to the agglomerative powers of CBDs and that CBDs are unlikely to hollow out, even given the disruption of the pandemic, the settling of remote work patterns and flexible workplace models, and increased digitisation. Given the significance of these disruptions, and despite the pandemic-era migration of CBD and city residents to regional areas, it would seem that the supremacy of the CBD is unlikely to abate; CBDs have proven extraordinary resilience and ability to reconfigure and adapt to post-pandemic and digital-age shifts.

Our results are specific to Australia; however, we note three reasons our results may be generalisable outside of Australia: (1) the remote work practices recorded in Australia are replicated across developed countries around the world (Aksoy et al., 2025); (2) digitisation of work, shopping, and education is occurring globally and is in no way unique to the Australian context; and (3) various observational studies worldwide have generated comparable evidence of the persistence of CBDs (such as Beze and Thiel, 2025; González-Leonardo, et al., 2023; Graves et al., 2023; Lennox, 2020). What remains unknown is whether these Australian experimental results might be replicated in other similar economies globally; this presents an opportunity for further study. Especially while observational data-based evidence of the donut effect remains mixed, an experimental approach might provide insights into likely longer-term CBD resilience.

The impact of the pandemic on developed regions is of great interest as governments continue to wrestle with concerns about mega-city infrastructure failure and regional employment and population collapse. As Krugman (2009) has shown, the initial choice of location for economic activity may come from a geographic advantage such as access to trade routes, but the effect of economic concentration can be arbitrary and the “function of initial conditions or historical accident.” The “historical accident” of the pandemic may boost some places and create a small advantage that triggers growth, which then in turn facilitates increasing returns. Our evidence shows that centripetal forces are continuing to draw firms to the centre, but the centrifugal effect of workers pushed to the peripheries due to diseconomies of transport costs, overcrowding, pollution, health concerns, etcetera, can also reinforce the primacy of the CBD if remote work allows the boundaries of cities to both accommodate growth and provide suitable access to the centre. It may be that the cities that provide the conditions for both of these centrifugal and centripetal forces to thrive are the places where post-pandemic growth flourishes.

Footnotes

Acknowledgements

The authors would like to thank Leanne Johnson, Lucy Williams, Ray Liang, and Amirreza Rahmani for providing essential feedback on different aspects of this study.

Ethical considerations

This research was undertaken in accordance with the protocols established with the approval of the University of South Australia’s Human Research Ethics Committee (Approval number 204655).

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by iMOVE CRC and supported by the Cooperative Research Centres programme, an Australian Government initiative; and the Commonwealth Department of Infrastructure, Transport, Regional Development, Communications and the Arts (DITRDCA).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability statement

Data can be made available to interested parties on request.