Abstract

In October 2014, the Australian National University announced that it was divesting from seven fossil fuel-intensive companies. This announcement sparked an unprecedented response in the community, both positive and negative. We examine this decision, the divestment movement in general, the science behind the issue and strategic responses, both policy and organisational. We argue that a confluence between policy responses and organisational responses is beginning to emerge that will lead to greater action on climate change.

1. Introduction

Fossil fuel divestment has become a new buzzword in debates around corporate engagement in climate change. The recent vote by the Council of the Australian National University (ANU) to divest itself of A$16 million worth of investments in coal and gas extraction has led to controversy among Australian public and private sector leaders. Among the divestments were holdings in seven fossil fuel-intensive companies: Iluka Resources, Independence Group, Newcrest Mining, Sandfire Resources, Oil Search, Santos and Sirius Resources. The vote also gained significant media and policy attention, both positive and negative. While the ANU’s divestment decision received significant backing – prominent Australians including former Liberal party leader John Hewson and former Liberal Prime Minister Malcolm Fraser put their names to an open letter of support – it also attracted substantial criticism. Several political and business leaders openly criticised the ANU’s move – among those Australian Prime Minister Tony Abbott (The Guardian, 2014).

Given these controversies, this paper examines the divestment debate (for other reviews, see Ansar et al., 2013; Davidson, 2014) and adds to discussions on corporate social responsibility and ethical investments (e.g., Chow et al., 2014; Griffin and Sun, 2013). The paper is structured as follows: in the first two sections, the paper provides a background to the divestment movement and outlines the science behind the issue. Next, the paper looks at possible strategies from policy and organisational viewpoints. We find that, initially, policy responses such as the European Emissions Trading Scheme (EU-ETS) and the abolished Australian Carbon Pricing Mechanism (CPM) were implemented in a top-down fashion to encourage action on climate change, but were criticised for not bringing about a rapid organisational transition towards a low-carbon economy globally. The divestment movement has attempted to fill this void at the organisational level by encouraging bottom-up support for climate change. This paper argues that we are now seeing a confluence between policy and stakeholder action. This should result in more effective outcomes in terms of more stringent policy action and grassroots support for a shift towards more sustainable models of doing business, thus highlighting that organisations are exposed to significant climate risks.

2. Divestment background

The fossil fuel divestment movement started as a grassroots movement at Swarthmore College in the US in 2011, with a student group asking their institution to freeze immediately new investments in the fossil fuel industry and to divest of stocks in the top 200 fossil fuel companies with the largest reserves. The student group followed in the footsteps of earlier college and university divestment campaigns in the US (Stewart, 2014). One of these earlier campaigns encouraged companies, insurers and pension funds to withhold their South Africa-related securities in an effort to end the Apartheid regime (Soule, 1997), while another campaign pressured companies to sell their shares in economic activities that were believed to fund the alleged genocidal activities by the Sudanese government (Soederberg, 2009). At least in the case of South Africa, divestment has been shown to have played a role in creating awareness of Apartheid-related issues. In 1977, the actions of students at Stanford University started an anti-Apartheid campaign with the result that 150 universities divested their interests in South Africa. Reportedly, Nelson Mandela later thanked the universities as he regarded their actions as a significant milestone in the campaign against Apartheid (Knight, 1990).

The fossil fuel divestment movement has now grown to over 560 campaigns globally and extends beyond academic institutions to also target cities, states, foundations and other institutions, such as religious organisations (Grady-Benson, 2014). The proliferation of the movement has been aided by modern technology platforms; for example, the Swarthmore group received support from the online campaign website 350.org. The website is led by environmental activist Bill McKibben who adopted this cause by embarking on a bus tour across the US to promote divestment (Stewart, 2014). The movement gained further traction when Stanford University decided to divest direct investments in coal mining in May 2014.

Are there other alternatives to divesting? One alternative would be to engage with companies and help with a movement to more sustainable practices. Some 200 major firms are now members of the World Council for Sustainable Development and as such have signalled their intention to engage and practice sustainability. Ansar et al. (2013) argue that divestment could lead to environmentally conscious investors being replaced by environmentally insensitive investors, thus potentially leading to a loss of influence by the environmentally conscious. Retaining of shareholding might give especially large investors the opportunity to influence firm decisions, including decisions to invest in cleaner technology and sequestration alternatives. However, the question remains how and if such an engagement can be successful and can result in firms adopting ‘real’ long-term sustainable solutions that are based on science, and not simply result in short-term fixes. Another alternative is to divest and then invest the divested funds in renewables. This could have the effect of stimulating discovery in much-needed battery technology or alternative power generation technologies, which could drive down the costs of renewables, thus making for a smoother transition from fossil fuels.

3. The science behind the divestment movement

The basis for the divestment movement is the current science on climate change. The Intergovernmental Panel on Climate Change (IPCC) has produced a comprehensive review of a large body of evidence showing that greenhouse gases (GHGs) are rising and that human activity is a key driving factor behind this trend (IPCC, 2014). The IPCC’s latest Synthesis Report established that there is a clear link between human influences, in particular the burning of fossil fuels, and the climate system (IPCC, 2014). The IPCC estimates that the emissions of carbon dioxide (CO2) from burning fossil fuels and industrial processes contributed about 78% of the total increase in global GHG emissions from 1970 to 2010. The question that is still scientifically uncertain is the quantity of GHG emissions that humanity can still emit without risking ‘dangerous’ levels of climate change. A commonly cited threshold is the ‘2°C target’ as an upper threshold for ‘safe’ levels of temperature rise (Randalls, 2010). The underlying assumption behind this target is that a global mean temperature increase of up to 2°C relative to pre-industrial levels is likely to allow society to adapt to climate change at globally acceptable economic, social and environmental costs (EU Climate Change Expert Group, 2008).

Calculations have shown that fossil fuel companies have proven reserves of nearly 3000 gigatonnes of CO2 (defined as those fossil fuel resources that can be recovered with current technologies at current prices), and that burning these reserves would greatly exceed the 2°C target (Meinshausen et al., 2009). In order to remain within a target of 2°C with a 50% probability, less than half of these reserves can be used in the future, resulting in a call for an upper limit on the usage of fossil fuel (Meinshausen et al., 2009). While the 2°C target has been widely adopted within the international scientific and political community (UNFCCC, 2014), it is a conservative target. The target dates to the 1970s when economists and scientists sought to develop guidelines and criteria for policy decision-making on climate change (Randalls, 2010).

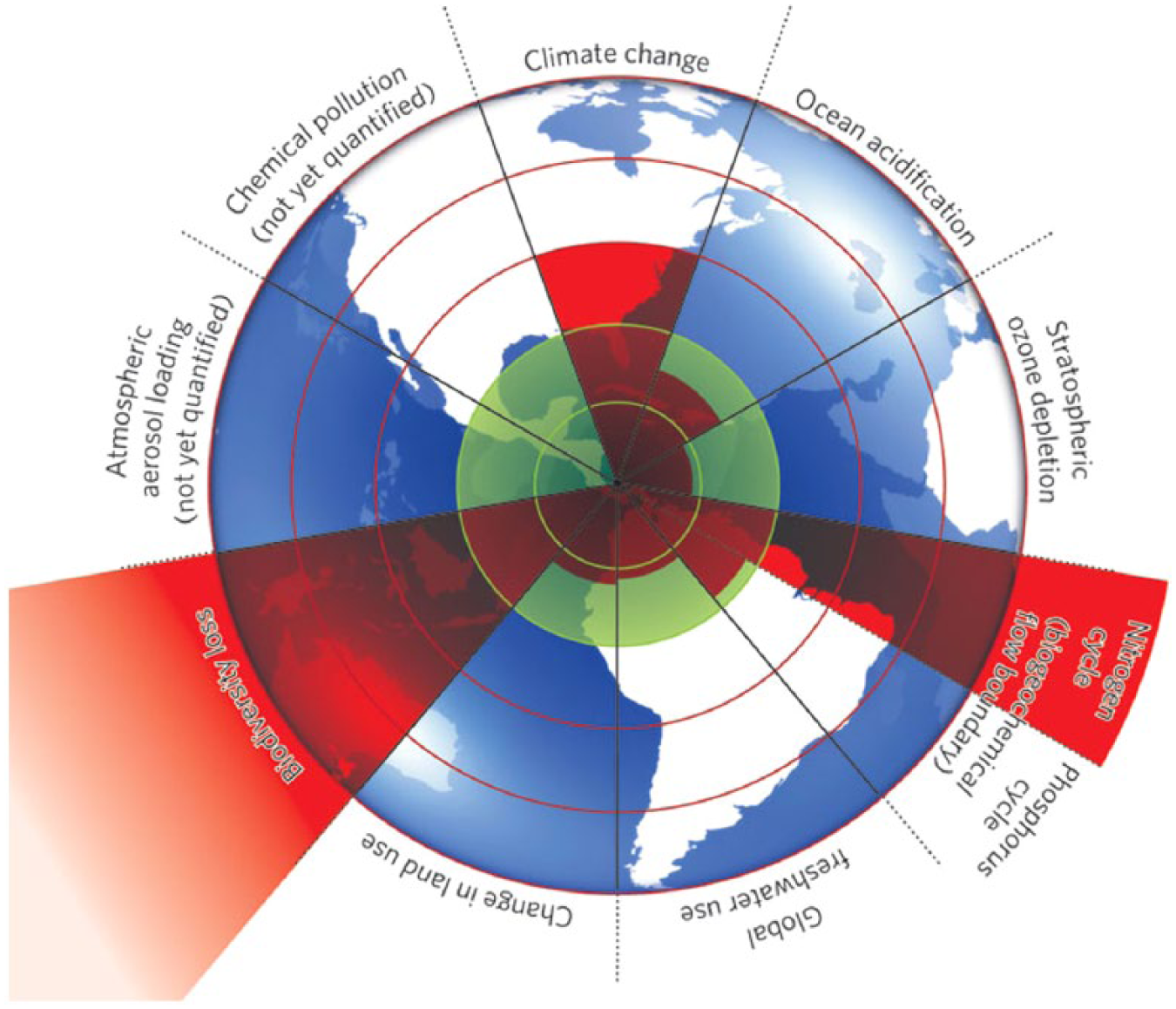

Some view the 2°C threshold estimate as too high (New et al., 2011). Global warming of 2°C means a significant level of climate change, with limited knowledge of the scope for adaptation, that is, the process of adjustment to actual or expected climate and its effects, in order to moderate harm or exploit beneficial opportunities (IPCC, 2012). Given these shortcomings and the growing levels of environmental problems, new approaches have emerged for assessing global sustainability. One such approach is the identification of key Earth system processes, referred to as ‘planetary boundaries’, which should not be transgressed if we want to sustain human life on the planet (Rockström et al., 2009a, 2009b). The nine processes are climate change, ocean acidification, stratospheric ozone depletion, interference with global phosphorus and nitrogen cycles, atmospheric aerosol loading, freshwater use, land use change, the rate of biodiversity loss and chemical pollution (see Figure 1). These processes are seen as interlinked, such that if one boundary is transgressed, safe levels for other processes could also be under serious risk.

Nine planetary boundaries (colour online only).

Figure 1 shows estimates of how seven of the nine planetary boundaries have changed from 1950 to present. 1 The area shaded in green is an estimation of the ‘safe’ space for human development, while the red wedges represent an estimate of the current status of each variable. The boundaries in three systems (climate change, rate of biodiversity loss and human interference with the nitrogen cycle) have already been exceeded and are either approaching or exceeding Earth system thresholds.

For climate change, Rockström and colleagues suggest boundary values of 350 parts per million CO2 (a measure of the concentration of CO2 in the atmosphere) and 1 W m−2 (a measure of the radiative forcing or imbalance in the Earth’s energy budget in watts per square meter) above pre-industrial levels, respectively. According to Hare and Meinshausen (2006), remaining within these boundaries will also give a high probability that the 2°C target is not exceeded. Since current levels of CO2 in the atmosphere are already at around 400 ppm, this approach indicates that the continued use of fossil fuel reserves places society at great risks. Given the significant uncertainty surrounding the duration over which boundaries can be transgressed before causing unacceptable levels of environmental change, Rockström et al. propose that immediate action be taken to either slow down or reverse trends. The Planetary Boundaries Framework also puts climate change in a broader context as it shows that climate change is only one of nine boundaries necessary to sustain human life.

4. Policy responses

The United Nations Framework Convention on Climate Change (UNFCCC; and later the Kyoto Protocol) were introduced as an international architecture for limiting GHG emissions. The Kyoto Protocol requires countries with emission reduction commitments to implement domestic measures to reduce their GHG emissions. 2 The effectiveness of different policy approaches to achieve commitments (carbon taxation versus emissions trading) has prompted debates in regards to the best option for GHG emission reduction efforts on an economic level. 3 The economic arguments generally favour the introduction of emission trading schemes over carbon taxation (Garnaut, 2011; OECD, 2013), based on the reasoning that individual emitters have different marginal costs of mitigation. An Emissions Trading Scheme (ETS) enforces a cap on total domestic emissions. The ability to trade emissions permits is meant to provide an opportunity for emitters to collectively find the least expensive way to achieve emission reduction targets.

One notable policy approach to meet the Kyoto commitment is the EU-ETS, which is currently the largest ETS in force. The difficulty with such action on the policy level is that it may not have led to strong organisational action and bottom-up support at the organisational level. While governments have put legislation and policies in place to mitigate emissions (and meet their commitments under Kyoto), the effectiveness of the existing approaches has been questioned in terms of achieving stringent emission reductions and fostering the transition towards a low-carbon society. For instance, the effectiveness of the EU-ETS to result in actual emission reductions was questioned due to the simultaneous economic downturn and the implementation of the 20/20/20 target (Linnenluecke and Griffiths, 2015). The Australian CPM never received much industry support from its onset. 4 This situation is now changing, especially with increased stakeholder pressures, as discussed in the next section on organisational action.

The Kyoto Protocol has also been criticised for not capturing countries with significant emission profiles (e.g., China), lax emission reduction targets and its potentially limited ability to bring about enough momentum for rapid changes on firm and industry levels. Prins and Rayner (2007) in the journal ‘Nature’ argue that the Kyoto Protocol may have become a limiting factor in addressing GHG emission reductions. While some commentators have used this argument to suggest that the Kyoto Protocol should be abandoned altogether, the argument by Prins and Rayner is that grand targets and national goals will only work in the context of developing and encouraging ‘social learning’ and experimentation at local and regional levels. The ultimate question is whether any ETS will lead to organisational strategies that go beyond compensation and result in the uptake of low-carbon, innovative technologies (Pinkse and Kolk, 2009). In the absence of strong institutional signals, there is significant scope for organisations to evaluate the performance of their investment over time, factoring in stakeholder pressures around carbon intensity.

5. Organisational responses

This section looks at action on the organisational level and in particular the ANU’s decision to divest, given that this action sparked debate in Australia. At Stanford University in the US, students successfully pressed the university to divest its stock in carbon-intensive companies. The US$18.7 billion divestment by Stanford far exceeds the estimated US$16 million ANU divestment (out of a US$1.1bn portfolio). The analysis below shows that the ANU’s decision to divest may not have been driven principally by concerns for the environment. Nonetheless, the ongoing media and policy debate surrounding the decision suggests that the pressure to divest from fossil fuels or carbon-intensive companies emanates from a view that governments are failing to act, and reflects the concern that asset owners, such as pension, superannuation and university endowment funds, are exposed to significant climate risks. For example, a recent study conducted by The Climate Institute estimated that some 55% of the world’s leading funds are invested in carbon-exposed industries and less than 2% of those funds in low-carbon-intensive industries (The Climate Institute, 2014).

5.1. Divestment by the Australian National University

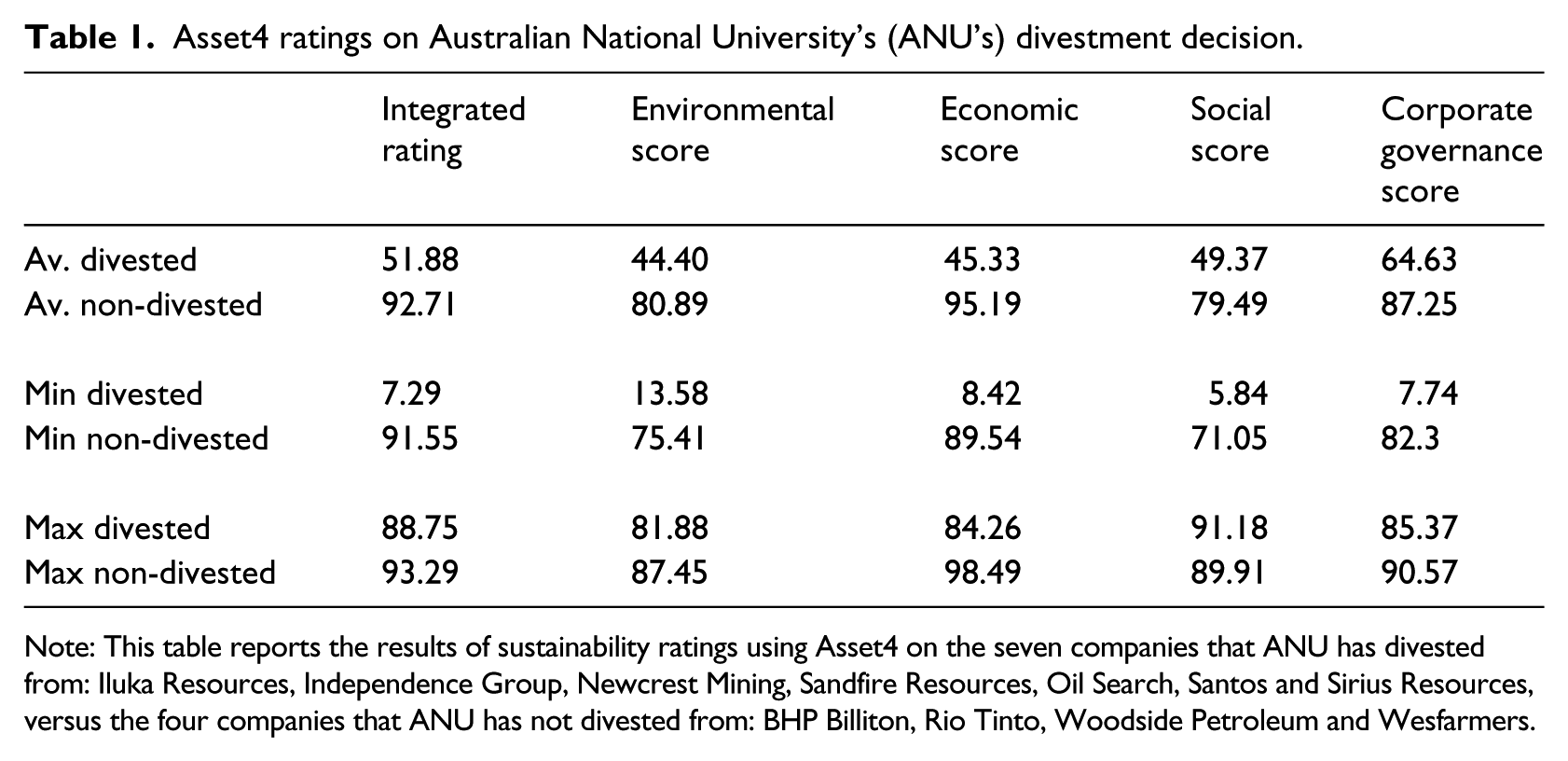

The ANU’s newsroom reported the decision to divest on the 3 October 2014. The stocks that were divested represented around 5.1% of the University’s holdings in Australian equities and approximately 1% of its total investment holdings. The ANU statement indicated that the decision was based on an independent report from CAER [Corporate Analysis Enhanced Responsibility], a firm that provides environmental, social and governance (ESG) ratings on companies. Nevertheless, ANU’s decision came under intense scrutiny. Fossil Free ANU campaign spokeswoman Louis Klee, for instance, pointed out that ANU divested from many, but not all of its fossil fuel investment. There were four companies involved in fossil fuels from which ANU did not divest – namely BHP Billiton, Rio Tinto, Woodside Petroleum and Wesfarmers.

We re-analyse the ANU’s decision using Asset4, an ESG research database provided by Thomson Reuters, which rates corporate performance on four pillars: environmental, economic, social and corporate governance (each rating ranges from 0/worst to 100/best). 5 The overall company ESG score, also called the Integrated Rating, is based on a roughly equal-weighted combination of all four pillar scores. Table 1 shows that, in 2013, the four fossil fuel companies from which ANU did not divest had an average total ESG score of 92.71 out of 100. The average scores for each of the four categories were also higher for the non-divested firms relative to the divested firms. Yet, when looking at minimum and maximum scores as well as (untabulated) individual values, it becomes evident that a company that was divested (Santos) had an overall ESG rating very close to 90 (at 88.75), which compares favourably with the average score of 92.71 for the non-divested group. Meanwhile, two of the non-divested firms (BHP and Woodside) had relatively low environmental scores of around 75, but high scores on all other factors, particularly economic performance, enabling them to gain a total average score across all of four categories of over 90. In other words, there are candidates in the divested group (such as Santos) that compare favourably with the non-divested firms on ESG scores alone.

Asset4 ratings on Australian National University’s (ANU’s) divestment decision.

Note: This table reports the results of sustainability ratings using Asset4 on the seven companies that ANU has divested from: Iluka Resources, Independence Group, Newcrest Mining, Sandfire Resources, Oil Search, Santos and Sirius Resources, versus the four companies that ANU has not divested from: BHP Billiton, Rio Tinto, Woodside Petroleum and Wesfarmers.

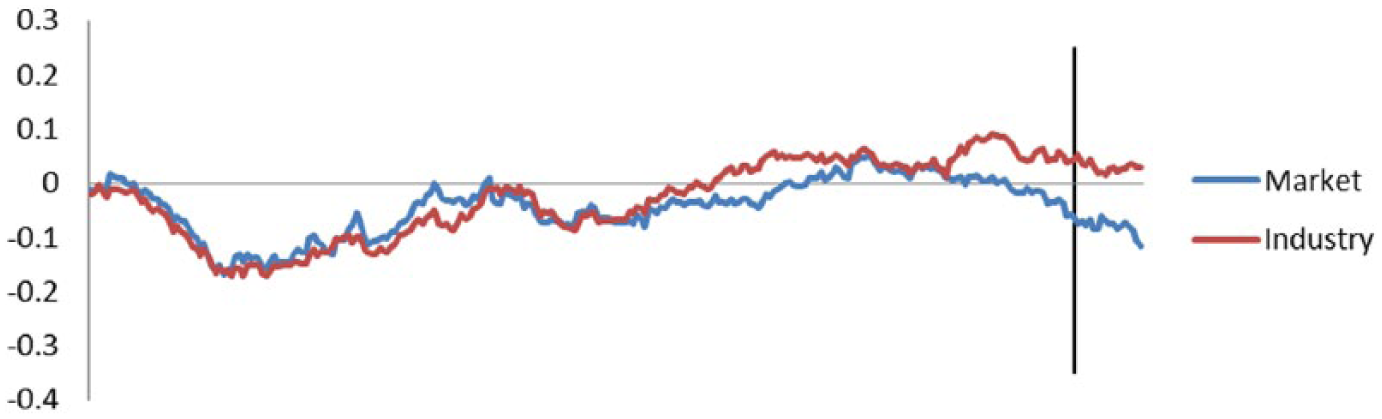

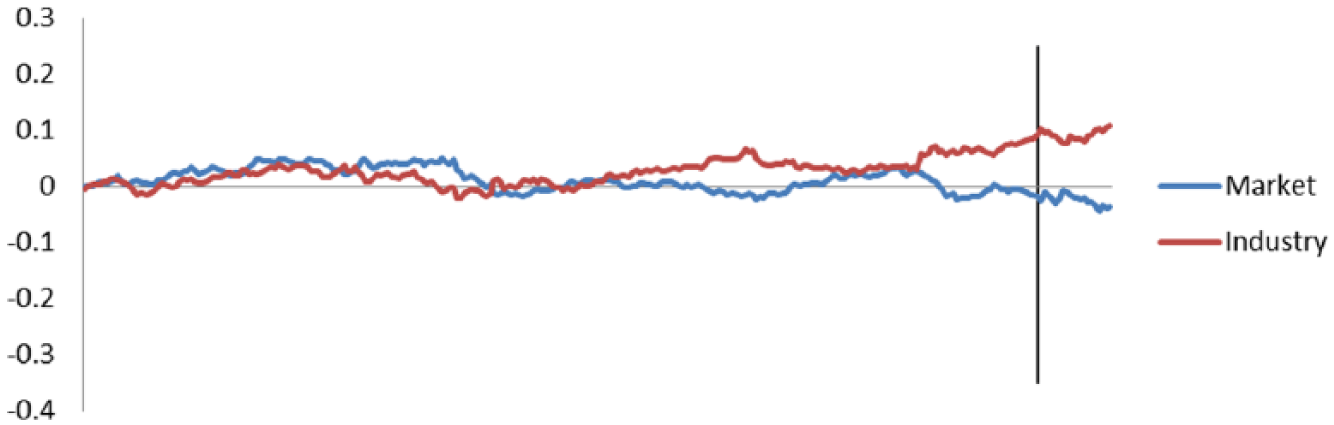

We next analyse market performance of the same firms. Figure 2 illustrates the average cumulative abnormal returns of the seven companies from which ANU divested. The data is from one year before the divestment date (3 October 2013) until three weeks after (28 October 2014). The divestment is indicated by the vertical line. Two benchmarks are used in calculating abnormal returns: the market return and industry returns. Figure 2 shows that for most of the year, the companies from which ANU divested underperformed the market consistently. Using an event window of three days before the announcement to three days after, we find a significant cumulative abnormal return when the market benchmark is used of −0.0072, which has a corresponding t-value of −2.15 and a p-value of 0.03. 6 Figure 3 shows the performance of the companies from which ANU did not divest in comparison.

Historic 1-year cumulative returns of the seven companies the Australian National University (ANU) divested from.

Historic 1-year cumulative abnormal returns of the four companies the Australian National University (ANU) did not divest from.

While the ANU appears to have taken a principled stance by divesting fossil fuel firms, the fact that some companies were divested despite seemingly good ESG ratings or other achievements was criticised in the press and by the affected companies. In contrast, the companies that were retained in the ANU’s portfolio have been argued to be larger contributors to CO2 and CH4 emissions. BHP Billiton, for instance, was found to be amongst the top 20 entities that have contributed to the cumulative CO2 and CH4 emissions from 1854 to 2010 (Heede, 2014). We see above that the stance has cost ANU little in terms of economic performance since the divested firms appeared to have inferior performance.

6. Markets

As outlined above, science indicates that less than 50% of the fossil fuel reserves can be used to remain within a 2°C threshold with a 50% probability. This gives rise to the possibility that fossil fuel assets become so-called ‘stranded assets’ (Ansar et al., 2013). ‘Stranded assets’ is the term used to reflect the known fossil fuel reserves that cannot be burned if the global community aims to limit global warming to 2°C. Taking into account the possibility of stranded assets, the price of a fossil fuel firm can be thought of in terms of the following equation:

where:

p is the probability that action will be taken to constrain the amount of carbon used to a level that limits any rise in temperature to a maximum of 2°C;

Pt is the observed market price of the fossil fuel firm.

The probability of stranded assets, p, is not 1 because, to date, fossil fuel companies in many jurisdictions do not pay the full market price for the CO2 emissions that they generate.

Future work can analyse Equation (1) using market prices and potentially back out the underlying parameters p,

However, in terms of the valuation equation above (Equation (1)) it may well be that (based on policy signals starting with the introduction of Kyoto) the market was already factoring in a significant probability (p) of stranded assets and that the 2009 publications lead to a minor increase in p with consequent price adjustment of a relatively low 2.48%.

7. Conclusion

The financial case for divestment is likely to increase with advances in alternative sources of energy and growing reputational effects from fossil fuel use, and in particular as the effects of breaching planetary boundaries become more visible. We are currently seeing greater action on climate change and shifts towards renewable energies on both policy and organisational levels. The change towards a low-carbon future that was led by countries and unions, such as the European Union (EU), will probably now be joined by the US and China in light of the latest climate agreement between the two economies, which will add further momentum to action on climate change. The latest deal between the US and China has the potential to be a significant step towards a global agreement on CO2 emission reduction efforts ahead of the next Paris meeting in 2015. Grassroots support through the divestment movement is rapidly spreading worldwide, creating stakeholder-driven support for action on climate change in addition to top-down policy measures. This confluence of the organisational and policy levels will see greater action on climate change.

Footnotes

Acknowledgements

Comments and suggestions by Karen Benson, Robert Faff and Jacqueline Humphrey are gratefully acknowledged.

Final transcript accepted 21 December 2014 by John Lyon (Guest Editor in Chief).

Funding

The project received funding from the Australian Research Council (ARC), grant #DP150102339 “The Importance of Being Politically Connected”.