Abstract

This article examines borrower acceptance in consumer marketplace lending using a unique dataset from the largest platform in Australia, Society One. Applications are initially filtered through an automated decision tree based on a third-party Veda (Equifax) credit score. At the second stage of assessment, loan applications are underwritten by the platform before being offered to sophisticated investors for purchase. The platform accepts around 11% of completed applications, with around 55% declined by an automated decision process and the remaining 34% by the manual underwriting process. More than 80% of purchased loans were made to borrowers with credit scores classed as ‘Good’, ‘Very Good’ or ‘Excellent’ (the threshold for ‘Good’ being a score of 622). However, underwriters decline around two-thirds of these higher credit score applicants, showing the importance of the underwriting process to the platform’s growth.

JEL Classification:

1. Introduction

This article analyses the determinants of consumer funding success on an Australian marketplace lending platform, Society One. A unique feature of the Australian marketplace lending environment relates to Australian Securities and Investments Commission’s (ASIC, 2014) responsible lending guidelines. Under these directions, loan applicants are required to submit to a manual underwriting process to ensure that the loan being sought is ‘not unsuitable’ for them. We aim to determine the extent to which the manual underwriting process impacts credit provision, beyond information contained in borrower credit scores. As the platform is competing for highly creditworthy customers against established financial institutions, we also aim to determine whether the growth of the platform has been driven by a decline in lending standards. We argue that the underwriting process is valuable in explaining credit decisions of the platform and demonstrate that the rate of applicant funding success, 11.01% on average, does not appear to be increasing over time.

Prior research into determinants of loan funding success and loan performance in marketplace lending has examined platforms in the United States, such as Prosper.com and Lending Club, and to some extent platforms in China and elsewhere (Duarte et al., 2012; Emekter et al., 2015; Freedman and Jin, 2017; Hertzberg et al., 2018; Iyer et al., 2016; Jagtiani and Lemieux, 2018; Lin et al., 2013, 2016; Netzer et al., 2016; Sonenshein et al., 2011). Our study examines the determinants of funding success in marketplace lending while departing from earlier studies in several ways. First, this is the first study that we are aware of which examines the determinants of funding success for an Australian platform. With the notable exception of Davis and Murphy (2016), there has been no published academic study of marketplace lending in Australia.

Second, we examine a unique and previously unexamined consumer loan marketplace, Society One, which was the largest consumer loan platform by value of loans issued in Australia at the time of this study. 1 The borrower application process on the Society One marketplace differs in critical respects from that observed on Prosper.com and Lending Club in the United States. In the first phase of the decision process, Society One filters prospective borrowers based on minimum credit score and income thresholds. In the second phase, unique to the Australian setting, the loan is underwritten by the platform’s loan officers, rather than ultimate lenders. The automated decision process relies on information provided by a third-party credit bureau (Veda), including prior credit applications and defaults. The supplemental underwriting process is required to verify applicant information and evaluate their capacity to service a loan, in line with regulatory requirements.

Our study aims to explore the role of the loan underwriting process in determining funding success on the platform. As online lending platforms such as Society One are seeking to establish market share from traditional banks, without holding a large pool of pre-existing credit information about prospective borrowers, it is crucial that they can adequately screen applicants. Australia’s relatively unsophisticated credit scoring environment and ASIC’s strict responsible lending guidelines render the underwriting process necessary, but we aim to explore the extent to which underwriting filters out applicants who exceed the first-stage credit score and income threshold.

We observe all 250,276 fully and partially completed consumer loan applications from the time the platform commenced operations in August 2012 until August 2017. We observe individual loan applications across traditional credit scoring metrics, including third-party credit scores for prospective borrowers, plus demographic information including age, occupation, employment status, income and loan purpose. Finally, we supplement our primary dataset by matching the postcode of all loan applicants with the Australian Bureau of Statistics’ Socio-Economic Index for Areas (SEIFA) (ABS 2013) to determine whether additional information provided on local socioeconomic factors (or unobserved underwriting factors) also explains loan funding success.

We present a preview of the results as follows. Of prospective borrowers who complete their application, 11.01% are accepted by the platform, while 54.74% of applicants are filtered through the automated decision process and 34.25% are declined by the (manual) underwriting process. Thus, the secondary step of manual underwriting is an important determinant of loan funding success on the platform; a large proportion of applicants meet the credit score hurdle but are subsequently denied based on other factors.

Successful applicants to the platform have higher Veda (Equifax) scores, 2 which like the US FICO score is a numerical indicator of an individual’s credit reputation: 80.54% of loans are purchased from borrowers with VedaScores externally classified as ‘Good’, ‘Very Good’ or ‘Excellent’, with the lower bound for ‘Good’ set at a score of 622. In contrast, 37.71% of applicants who were declined by underwriters and 12.54% of applicants who were automatically declined by the platform’s decision algorithm exhibited VedaScores of ‘Good’ or above. Applicants with VedaScores below 509 (classified as ‘Below Average to Average’), including negative VedaScores (indicative of prior adverse credit events) or zero VedaScores (without credit history), were accepted on the platform in only 0.26% of cases. This supports the platform’s contention that they aim to provide funding to mainly prime borrowers.

We use logistic regression models to illustrate the value of underwriting variables beyond the VedaScore in the loan acceptance process. The underwriting variables help predict both those applicants who pass the first stage and those who are ultimately accepted. Despite large growth in the number of loans funded on the platform, the acceptance rate on the platform has not significantly increased over time, controlling for other factors. Thus, we attribute the growth of the platform to increasing borrower awareness rather than declining lending standards.

2. Credit information in consumer lending marketplaces

In this section we compare the current study with the prior literature examining marketplace lending, and form hypotheses based on the Society One setting.

2.1. Comparison with Existing Marketplace Lending Studies

A critical question in the empirical literature on marketplace lending relates to how lenders or platform operators can evaluate available credit information from prospective borrowers. Certain features of the early Prosper lending marketplace in the United States between 2006 and 2008 provided the basis for several studies (Iyer et al., 2016; Netzer et al., 2016; Sonenshein et al., 2011).

For instance, loan listings by prospective borrowers included a range of non-traditional credit information. Alongside traditional credit information, such as the prospective borrowers’ FICO score, loan amount and term sought, borrowers were also able to post a narrative description in support of their loan application and a profile photo of themselves. As a result, extant studies have utilised novel features of these markets as forms of field experiment to investigate the role of non-traditional or soft information as signals for borrower credit quality.

Society One does not, however, use information from narratives or photographs of applicants in making credit decisions. Rather than selecting loans on individual borrower profiles, investor funds are allocated by an auto-bidding system based on their allocation preferences. Our setting differs from Emekter et al. (2015) and others on the literature on funding success (e.g. Freedman and Jin, 2017; Iyer et al., 2016; Lin et al., 2013) in two main respects. First, the platform underwrites loans before offering to lenders, rather than directly offering borrowers meeting the credit score threshold to lenders. This additional layer may help to eliminate potential borrowers based on unverifiable or adverse information that is not reflected in credit scores. Second, lenders are either institutions or sophisticated individuals and do not select specific loans for investment, but are allocated to fund fractions of loans in line with their stated risk preferences. Thus, soft information is used neither by borrowers nor by the platform underwriters.

2.2. Hypothesis development

To formalise the discussions made in the previous sections, we construct the following hypotheses.

H1. Underwriting variables (information beyond that contained in credit scores only) exhibit significant explanatory power determining loan application outcomes.

H2. The growth of the platform is due to increased awareness by consumers and not declining lending standards.

3. Institutional setting

Australia’s banking sector is generally considered to be ‘an established oligopoly with a long tail of smaller providers’ (Productivity Commission, 2018: 37). This view of the Australian banking system as an oligopoly has been supported by earlier studies, such as Kirkwood and Nahm (2006). Others such as Allen and Powell (2012) have noted the dominance of the ‘big four’ banks by assets, while Tran et al. (2017) have examined the credit quality of consumer mortgage bank loans in Australia. Together the largest four banks accounted for 79% of total domestic bank assets and 82.4% of total domestic household lending in Australia at the end of June 2017 (authors’ estimate based on Australian Prudential Regulatory Authority (APRA) 2017). There is a very high rate of bank penetration in Australia, with an estimated 97.7 % of people aged above 18 having a bank account (Connolly, 2014). However, unsecured personal loan interest rates have remained relatively high, despite significant decline in bank funding costs over the past decade. Marketplace lending thus has the potential to compete against the banking sector by providing lower cost personal loans to borrowers. Enhancing financial inclusion to borrowers that are underserved by the status quo arrangements (e.g. Jagtiani and Lemieux, 2018) does not appear to be an aim of marketplace lenders at present.

Marketplace (and peer-to-peer) platforms in Australia offered their first loans in 2012 (Society One) and 2014 (RateSetter, Australia). Society One was Australia’s largest consumer marketplace lending platform by the reported total value of loans issued in this period, with over AUD$254 million in consumer loans issued from 2 August 2012 until 8 August 2017, and its lending volume is followed by the next largest provider, RateSetter Australia (Whyte, 2017). Although the platform also offers secured business loans to agricultural borrowers, most of the platform’s lending by value is to consumers. The average (median) loan size issued to consumers on the platform during this period was AUD$19,272 (US$16,000). On the funding side, the Society One marketplace is open only to wholesale investors, that is, institutional and sophisticated (accredited) investors.

Online marketplace lending in Australia has grown rapidly from a low base. From AUD$2.39 million (US$2.14 million) in loan value reported in 2013, the cumulative equivalent of AUD$329.7 million (US$238.6) in marketplace consumer loans was made in Australia in the years from 2013 to 2016 (Garvey, 2017) – a growth rate of about 110 percentage points over the 3-year period. By comparison, the growth rate of total reported household credit outstanding, which includes credit cards and other household loans but excludes housing credit, was a 14.9 percentage point change over the same period from 2013 to 2016 (authors’ estimate based on data in APRA, 2017). Of this 14.9 percentage point growth, loans to households via credit cards increased 3.4% and ‘Other’ household credit (category heading reported by APRA, 2017) increased 17.8%.

Thus, the growth rate of marketplace consumer lending in Australia between 2013 and 2016 appears to have been over seven times faster than the reported growth of personal non-housing credit on an economy-wide basis over the same period. To put this in perspective, the total cumulative value of marketplace consumer lending by the end of 2016 was very small – about 0.2% of total reported personal credit outstanding (non-housing) in Australia, which grew from AUD$129.6 billion to AUD$153 billion between 2013 and 2016 (authors’ estimates based on RBA, 2017b). The penetration of marketplace lending in Australia is qualitatively similar to the United States, which experienced a growth rate in lending of 163% between 2011 and 2015 (Tomlinson et al., 2016: 5), although constitutes less than 1% of the overall consumer credit outstanding (Perkins, 2018).

Despite the small share of marketplace consumer loans funded compared to the value of non-housing personal bank lending in Australia, marketplace loans offer cash loan rates at potentially lower than the equivalent bank rates. For instance, the average unsecured fixed term personal lending rate across Australian banks was around 14% per annum in 2013–2016 (RBA, 2017a). In comparison, 3- to 5-year term loans on Society One averaged 12.3% per annum for borrowers.

4. Data

Our dataset is provided by Society One and includes anonymised information on loan applications and approvals, as well as investor portfolios and their preferences. The period covered by the data is from 2 August 2012, when the platform commenced operations, until 9 August 2017.

4.1. Loan applications

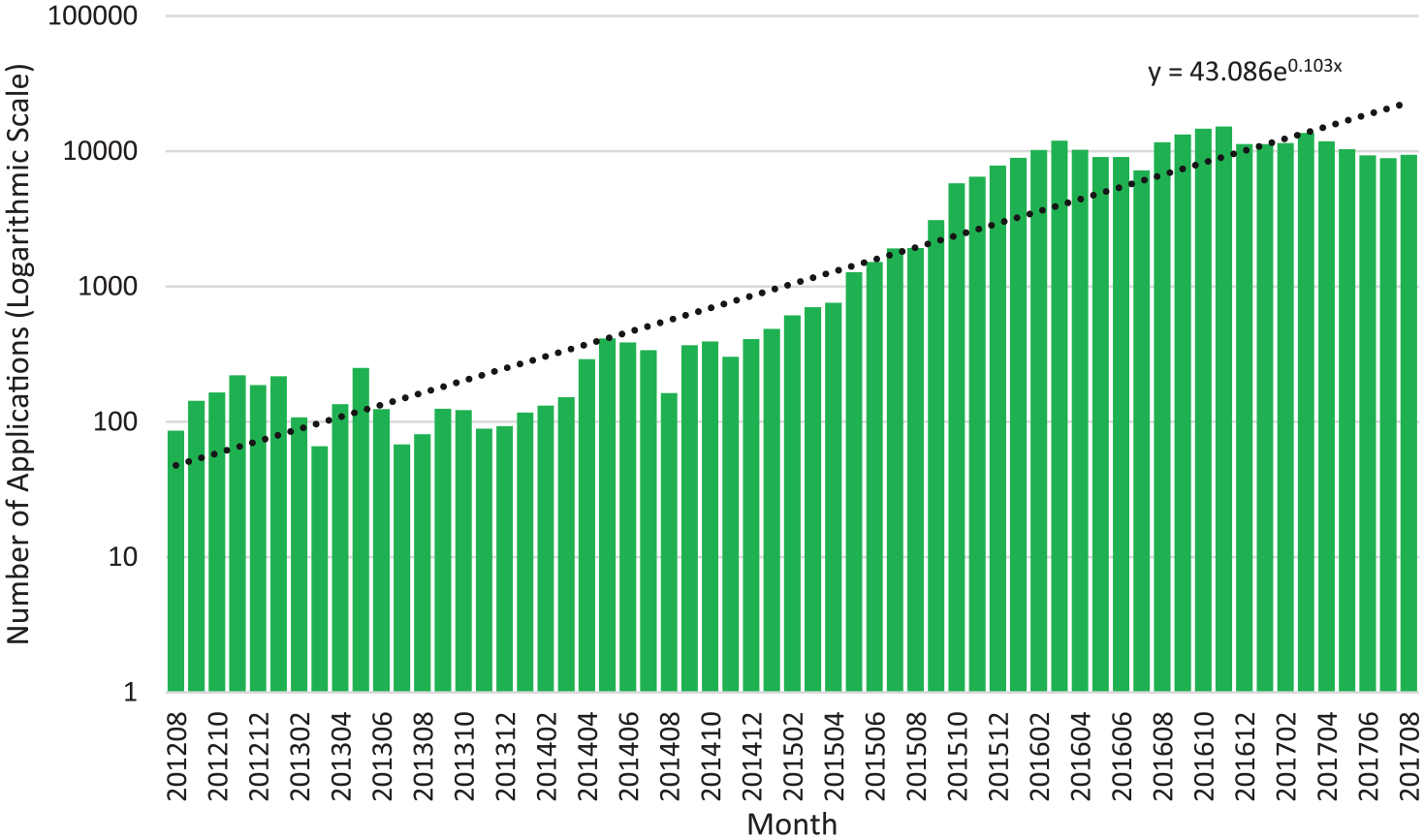

The data consist of 250,276 fully and partially completed loan applications, an average of 4103 applications per month over the 61-month period. The platform experienced substantial growth in the volume of applications over the period studied. During the 2013–2014 financial year, a total of 2068 applications were made on the platform, while 141,141 applications were made in the 2016–2017 financial year. Monthly growth rate of applications has averaged 14.04% over the platform’s life, as represented graphically in Figure 1.

Monthly number of applications for Society One, August 2012 to August 2017, plotted in log-scale.

Applicants to Society One are required to meet several criteria before being eligible to apply for a loan. These are clearly reported on the website and include the following: Australian citizenship or permanent residency, age of 21 or above, employment income of more than AUD$30,000 per annum, an ability to afford the loan, a minimum of 18 months of credit history, no hardship, no bankruptcy (pending or previously) and that the loan is for an individual, not a business. Each loan application made online through the Society One website is retained, provided applicants enter enough details to allow for a credit check. This requires the loan applicant to input details including date of birth, address, and tenure at their current address. Following verification with Veda (Equifax), further information about applicants is acquired; it is from this we obtain most of the data we analyse.

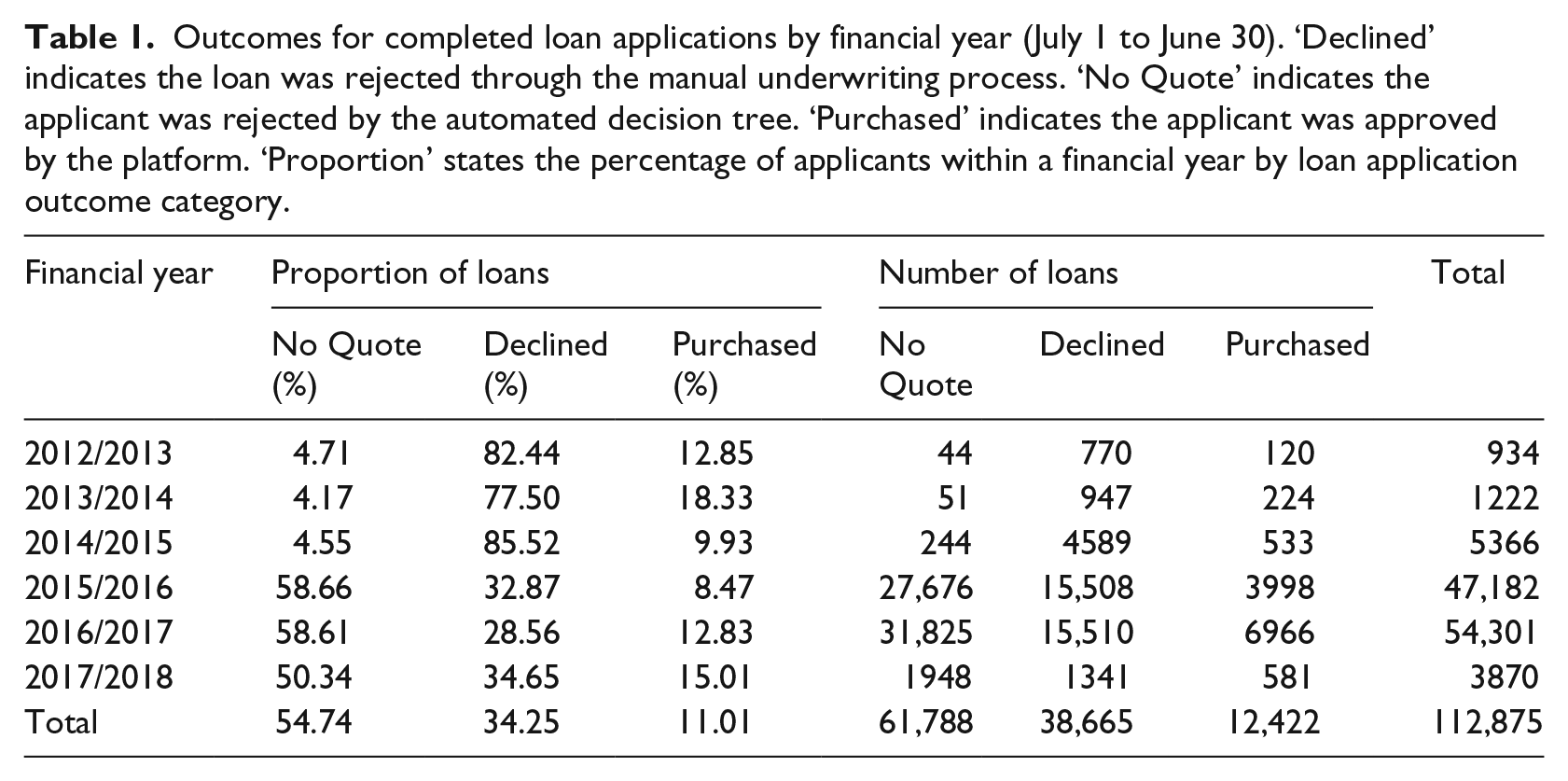

More than half (53.07%) of platform participants commence but do not conclude their application; cancellation of the application by the borrower may be driven by an inability to obtain documentation to finalise the application or an undesired initial (automated) quotation. We subsequently eliminate incomplete or cancelled applications from the analysis, leaving us with 112,875 loan applications with a decision. The statistics on loan outcomes by financial year are reported in Table 1. The loan application outcomes are further broken down into three categories: (a) No Quote (rejected by decision process), (b) Declined (by underwriter) and (c) Purchased (accepted). Appendix I, Figure 3 presents a flowchart of the application process.

Outcomes for completed loan applications by financial year (July 1 to June 30). ‘Declined’ indicates the loan was rejected through the manual underwriting process. ‘No Quote’ indicates the applicant was rejected by the automated decision tree. ‘Purchased’ indicates the applicant was approved by the platform. ‘Proportion’ states the percentage of applicants within a financial year by loan application outcome category.

The number (proportion) of completed applications that are accepted (Purchased) by Society One is 12,422 (11.01%) over the life of the platform. Just over one-third (34.25%) of loan applicants are declined by the platform’s underwriters (Declined), with the remainder (54.74%) denied a quote by the platform due mainly to a low credit score (No Quote). Among loan applications that were declined, there is a clear change following the start of the 2015–2016 financial year in the decision-making process. Prior to this point, fewer than 5% of completed applications were automatically rejected by the platform. However, this figure has grown substantially since the start of the 2015–2016 financial year, resulting in a greater than 50% share of applications being denied due to the automatic decision-making process thereafter.

Underwriting loans is relatively more costly (time-consuming and labour-intensive) compared with the automated decline. The growth of the platform has been driven, in part, by changing the decision tree towards automated loan processing. Under the ASIC regulation RG209, however, part of the underwriting process requires lenders to enquire into and verify credit applicants’ financial statements (ASIC, 2014). Under the Responsible Lending obligations in the National Credit Act, the lender must ensure that the credit contract is ‘not unsuitable’ for the consumer (RG 209.2), including whether the borrower would be unable to meet their payment obligations (or only with substantial hardship). All borrowers who are ultimately accepted by the platform need to be spoken to by the platform to ensure they understand the conditions of the loan.

4.2. Loan outcomes by VedaScore range

VedaScores, like the US FICO scores, 3 are numerical indicators of an individual’s credit reputation. Veda was one of three major ‘third-party’ credit bureaus in Australia, the others being Dun & Bradstreet (Illion) and Experian. Veda was then acquired by Experian in 2016. Until 1 July 2018, however, Australia operated under a negative credit reporting regime, and information about the creditworthiness of borrowers was only available based on recent credit applications, prior delinquencies (adverse events), open credit lines and residential address, 4 supplemented with public information from court records or ASIC records. VedaScores are not based on gender, race, dependents, salary or asset holdings due to the Privacy Act (1988). The three credit bureaus based their credit scores on somewhat different information, and there may be discrepancies between them based on what information they have available. For example, a credit issuer such as bank or telecommunications firm may only report applications to one of the credit bureaus, and this would be unknown to the other two.

According to Veda, scores typically fall in the range of 0–1200, where a higher credit score indicates a superior credit reputation. Individuals without a credit history (e.g. never having held a post-paid mobile phone contract or a utility bill in their name) will have a credit score of 0. Some individuals in the dataset hold a negative credit score, indicative of prior adverse credit events, and applications that do not reach the underwriting phase of the application may not have their credit score reported in the data. Equifax notes that personal loan issuers are likely to rely mainly on the credit score (rather than accompanying credit report) when making lending decisions. We are not aware of any prior studies that have used the VedaScore to assess personal loan issuance in Australia.

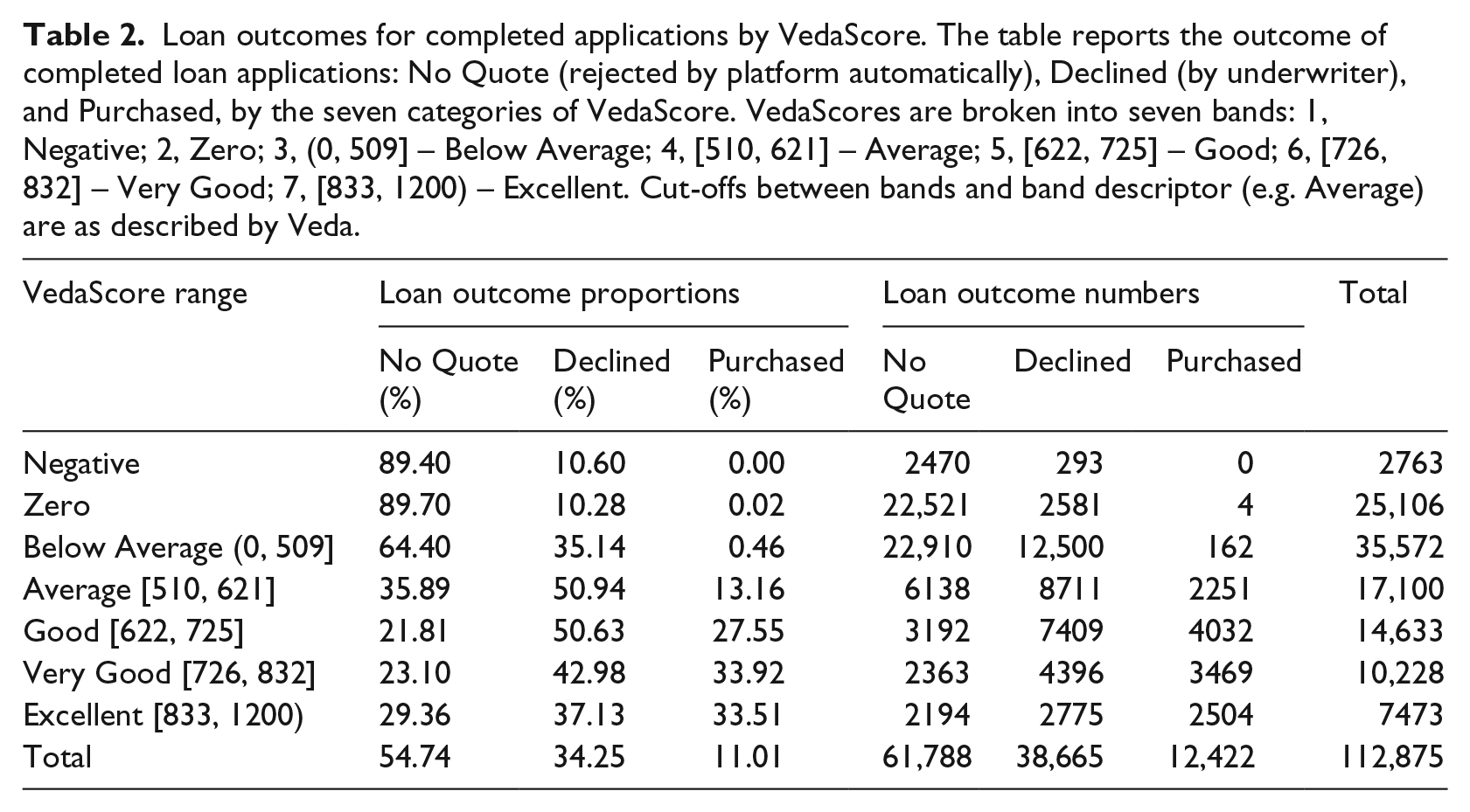

Table 2 reports loan application outcomes for completed applications by ranges of VedaScore. We use the publicly reported VedaScore bands as cut-offs, which Veda (Equifax) determines as indications of applicant quality (e.g. https://www.finder.com.au/vedascore). An applicant in the range (0, 509] is classified as ‘Below Average to Average’, indicating a position in the bottom 20% of Veda’s credit-active population. The four other positive categories of VedaScore represent the higher four quintiles of the population. These are stated as [510, 621] – Average; [622, 725] – Good; [726, 832] – Very good; and [833, 1200) – Excellent.

Loan outcomes for completed applications by VedaScore. The table reports the outcome of completed loan applications: No Quote (rejected by platform automatically), Declined (by underwriter), and Purchased, by the seven categories of VedaScore. VedaScores are broken into seven bands: 1, Negative; 2, Zero; 3, (0, 509] – Below Average; 4, [510, 621] – Average; 5, [622, 725] – Good; 6, [726, 832] – Very Good; 7, [833, 1200) – Excellent. Cut-offs between bands and band descriptor (e.g. Average) are as described by Veda.

From Table 2, most applicants had a credit record that could be retrieved (25,106 of 112,875 (22.24%) applicants exhibited a zero-credit score) by the platform. VedaScore is a strong predictor of loan application success; applicants with superior credit history are far more likely to have their loan accepted on the platform. Nearly all successful applicants (98.66%) exhibited VedaScores above 509, and 33.74% of applicants with VedaScores classified as ‘Very Good’ or ‘Excellent’ had their loan accepted on the platform (compared to the unconditional acceptance rate of 11.01%). Only four (0.01%) applicants were accepted on the platform with a non-positive VedaScore, and 89.67% of such borrowers were automatically rejected by the decision tree. 5 Rejected applicants with higher credit scores (510+) are more likely to be declined by the underwriter than the automated decision process. The exact threshold for automated denial by the platform is time-varying, fluctuating with the risk appetite of the platform investors and the platform’s ability to underwrite loans across the risk spectrum.

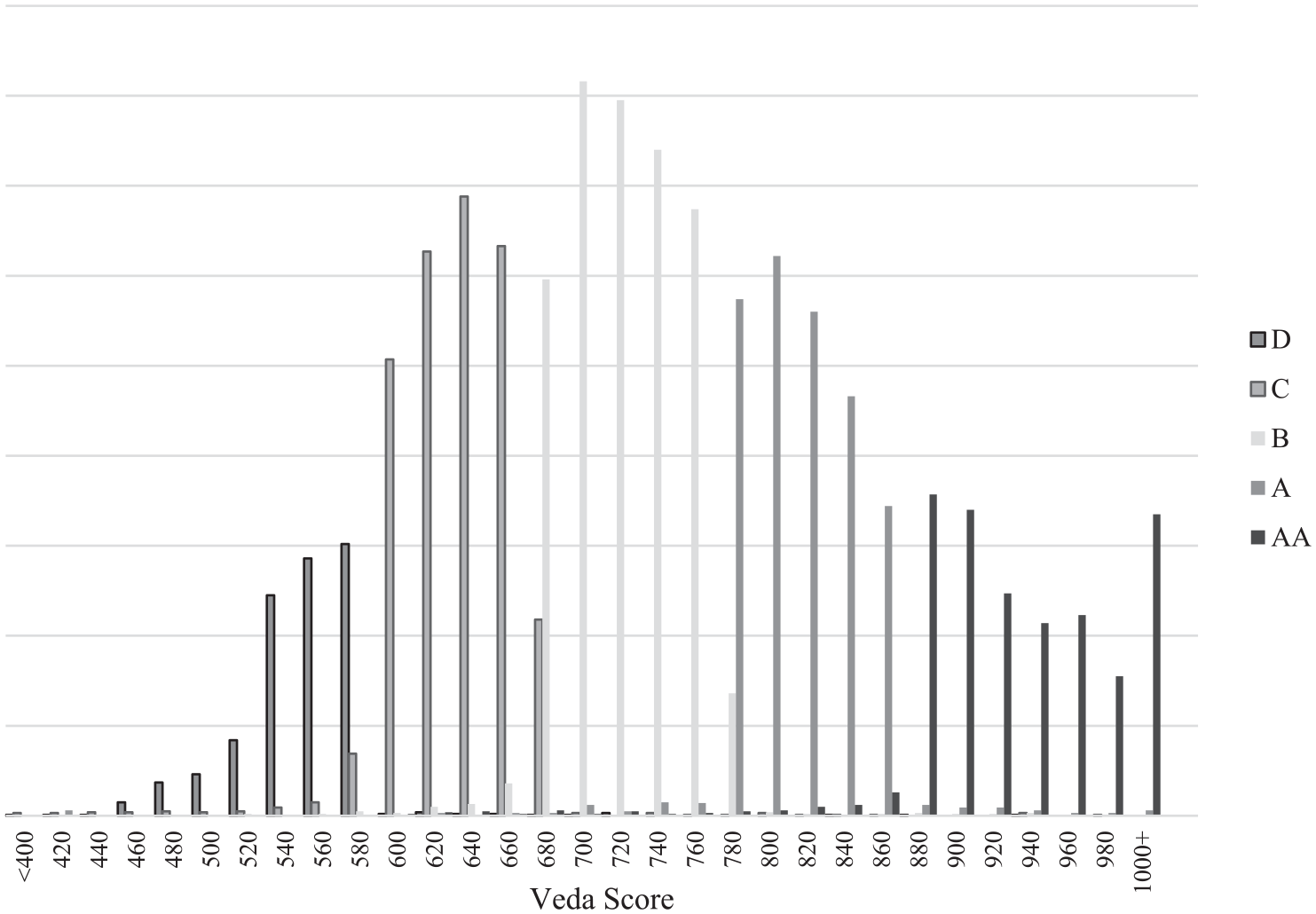

Following acceptance, loans on the platform were grouped into risk categories AA, A, B, C and D, where AA (D) are the lowest (highest) risk and borrowers are provided with lower (higher) interest rates on their loans. While the exact interest rate offered to borrowers depends on the demand from lenders, the risk categorisation depends nearly exclusively on VedaScore, rather than underwriter risk assessment. For example, 93.6% of borrowers with a VedaScore between 640 and 659 were assessed as risk grade C. Figure 2 presents graphical evidence showing loan grades by VedaScore; loan risk grades are determined by distinct thresholds in VedaScores.

Credit grade of issued loans by VedaScore range.

5. Predicting loan acceptance on the platform

We aim to determine the significance of the ‘underwriting’ variables used by the platform in determining whether a loan is purchased by the platform. To do this, we run logistic regressions to predict whether an applicant will pass each phase of the application process based on ranges of VedaScores and other observable characteristics of the borrowers (underwriting variables).

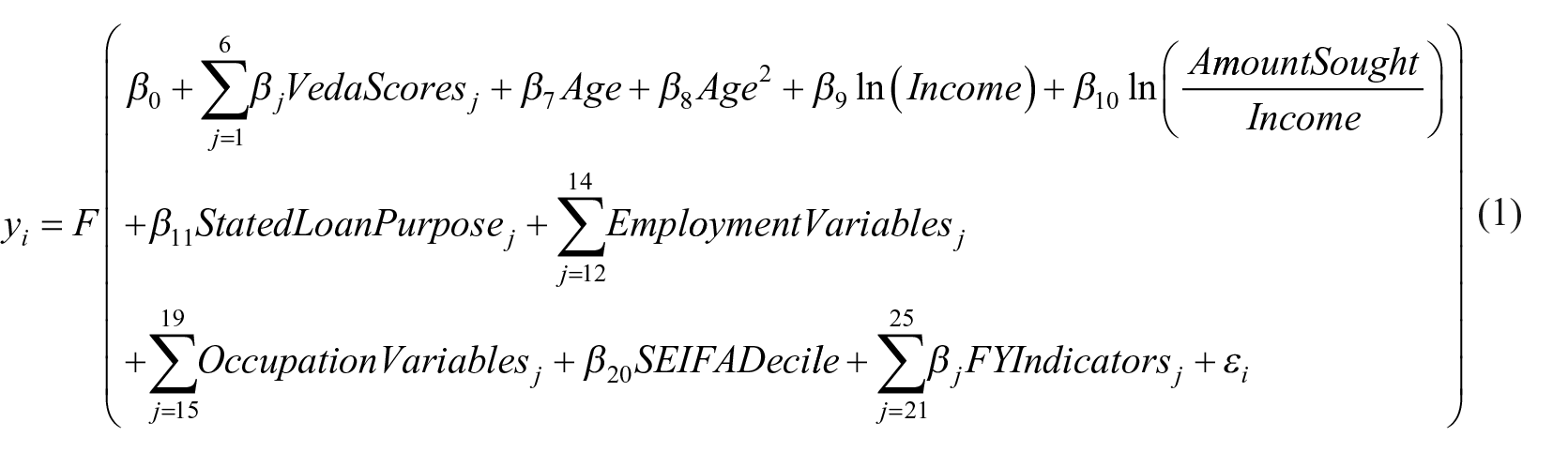

We model the probability of loan passing the process on the platform using a logistic regression model

where

We specify two models, one for each phase in the process. In Model 1, the dependent variable

5.1. Independent variables

The independent variables used in the logistic regression models in equation (1) are as described in Table 3. Panel A reports the definition of the dependent variables and Panel B reports the definitions of the independent variables used in both models.

Definition of dependent variables and independent variables used in equation (1) to determine loan funding success.

SEIFA: Socio-Economic Index for Areas; ABS: Australian Bureau of Statistics.

We construct VedaScore indicator variables that take the value of 1 if loan applicant

Assuming that older applicants exhibit higher creditworthiness, we predict that the sign of the coefficient of

The model is augmented with a

Indicator variables for the applicant’s employment status are added to the model; these are

We provide further information on the loan applicants in terms of their occupation. The indicator variables used here are

Our final variable is

Finally, we add financial year indicator variables, with the first year of platform operation, 2012–2013, omitted. These variables are defined as

6. Results

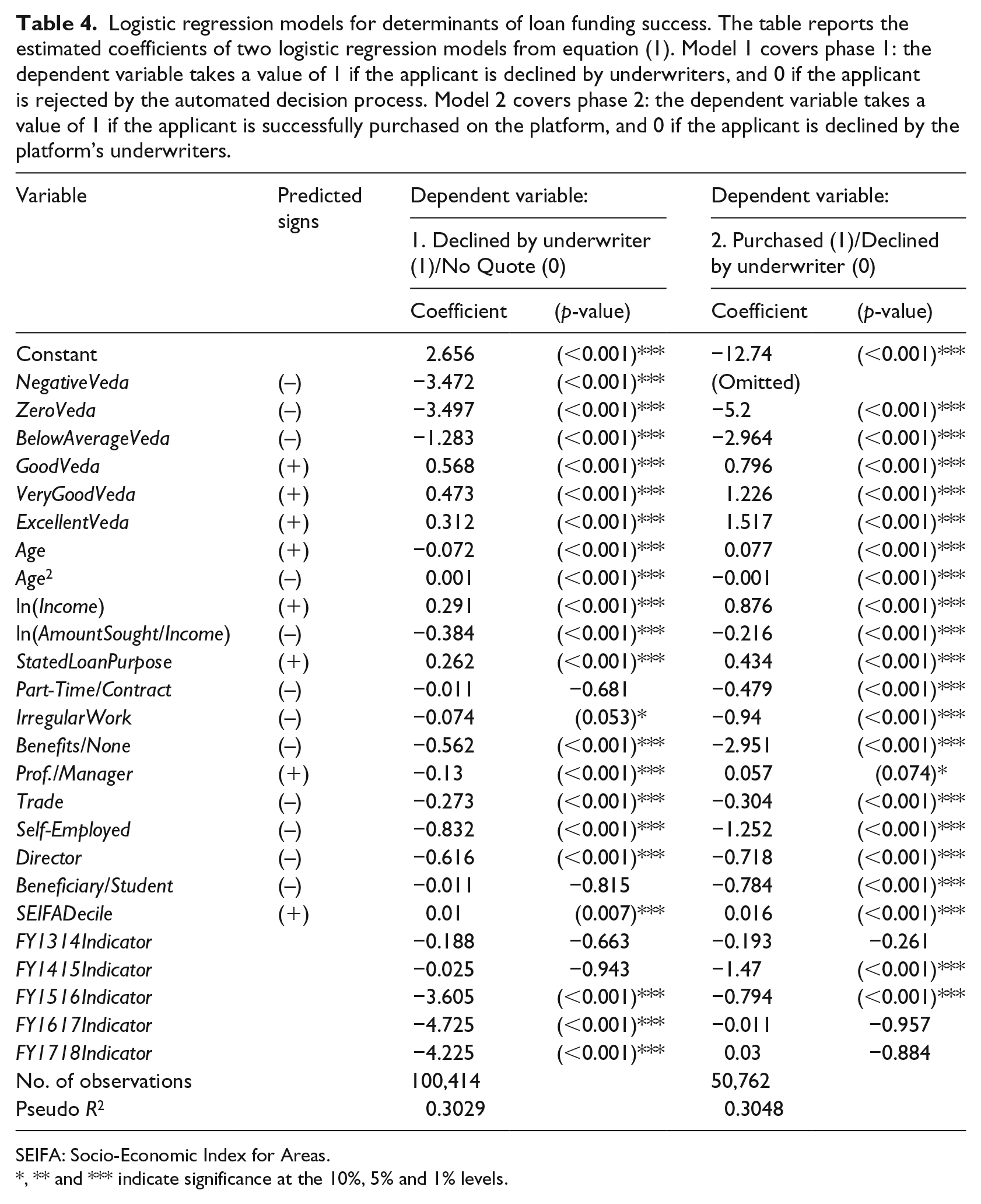

Table 4 reports the results of the logistic regression models. Model 1 uses only the sample of loans that were not accepted by the platform, with the dependent variable taking the value of 1 if the applicant was declined by underwriters, and 0 if the applicant was rejected by the automated decision tree. The coefficients for the VedaScore indicator variables each take their expected signs. Those with Negative, Zero or Below Average VedaScores are less likely than those with Average VedaScores to make it past the initial stage of the decision tree, while applicants with Good, Very Good or Excellent VedaScores are more likely to make it through the first-stage filtering process.

Logistic regression models for determinants of loan funding success. The table reports the estimated coefficients of two logistic regression models from equation (1). Model 1 covers phase 1: the dependent variable takes a value of 1 if the applicant is declined by underwriters, and 0 if the applicant is rejected by the automated decision process. Model 2 covers phase 2: the dependent variable takes a value of 1 if the applicant is successfully purchased on the platform, and 0 if the applicant is declined by the platform’s underwriters.

SEIFA: Socio-Economic Index for Areas.

, ** and *** indicate significance at the 10%, 5% and 1% levels.

While the automated decision tree largely relies on the credit score threshold to reduce the number of applicants who reach the underwriting process, several of the auxiliary variables are significant determinants of reaching this second stage. Older applicants, applicants with lower incomes and applicants seeking a large loan relative to their incomes are all less likely to reach the underwriting phase of the application process. This information is largely self-reported at the initial stage (before verification by underwriters), but their significance indicates that they are informative in how the platform filters applicants. For example, an applicant seeking a large loan relative to their income (possibly an older applicant) is more likely to be denied a quote, even if they have a good credit score.

Employment and occupation variables indicate that those with less consistent work or receiving benefits and those with less regular incomes (tradespeople, directors or self-employed) are less likely to reach the underwriting phase than those employed full-time. This is probably capturing variation within credit score categories (for instance, riskier applicants in the Good VedaScore range). The Financial Year indicator variables clearly demonstrate that applicants in later years are far more likely to be rejected by the automated decision process, as noted from Table 2. Although it is (presumably) not part of the automated decision process, the positive and significant coefficient for the SEIFA Decile demonstrates that some unobserved applicant characteristics render those in better socioeconomic areas more likely to reach the underwriting phase of the process.

Model 2 examines only those applications that have cleared the first hurdle, that is, reaching the underwriting stage. The dependent variable takes the value of 1 if the applicant is purchased by the platform, and 0 if the applicant was declined by the underwriter. Thus, the sample of applicants has been approximately halved from the first model.

7

The VedaScore indicator variables remain significant. The interpretation here is that once the underwriting phase is reached, applicants with higher credit scores exhibit characteristics that indicate creditworthiness, at least beyond the underwriting variables considered in our model. The underwriting process requires examination of bank statements, for example. The characteristics of those with higher credit scores (i.e. in the ‘Very Good’ or ‘Excellent’ VedaScore ranges) appear to show increased appeal to the platform underwriters. A test of the coefficients indicates that the coefficient of ‘Excellent’ Veda is greater than ‘Very Good’ Veda

The remaining underwriting variables take their predicted signs. Loan acceptance is quadratic in Age and older applicants are more likely to be purchased than younger applicants, but the likelihood of loan purchase declines for much older applicants. Applicant income and loan serviceability –

Loans with a stated purpose are more likely to be purchased by the platform, with the underwriting process appearing to prefer applicants with a specified need for funding (either directly or indirectly). Applicants with full-time employment (the reference category among employment variables) have a greater likelihood of acceptance. In contrast to Model 1, part-time employees tend to be eliminated at the underwriting stage. As employment status is not included in the VedaScore, and presumably part-time employees (ceteris paribus) are less able to service personal loans, this appears to validate the underwriting process. Similarly, underwriters are far more likely to decline those with less consistent employment (self-employed, tradespeople or directors), providing credence to their abilities.

The coefficient of the variable

The interpretation of the

Based purely on the acceptance rates by socioeconomic status (i.e. ignoring the effects of other variables), borrowers in decile 10 of the SEIFA index were purchased on 30.0% of occasions, versus 17.0% for borrowers from decile 1, conditional on reaching the underwriting phase. Although the socioeconomic index is likely to be indirectly embedded into a VedaScore, it appears to provide additional explanatory power for loan acceptances.

Our other main hypothesis relates to the growth of the platform in terms of volume. The sign of the coefficients of the Financial Year indicator variables is used to test this hypothesis. In Model 1, all the financial year coefficients are negative or insignificant. Thus, in years after 2012–2013 of the platform’s operation, applicants are more likely to be denied a quote. In Model 2, we similarly find negative or insignificant coefficients. Conditional on reaching the underwriting phase, applicants do not appear to be more likely to be accepted in later years, supporting Society One’s contention of only accepting highly creditworthy borrowers. Taken together, the results imply that the platform is receiving more loan applications across the board, but that the loans issued are not substantially declining in quality. We leave the ultimate analysis of loan repayments or delinquency for future research.

7. Conclusion

This article has examined the structure and determinants of loan funding on the largest consumer lending marketplace platform in Australia, Society One. We find that underwriting variables provide significant explanatory power in determining loan acceptance in logistic regression models also including personal credit (Veda) scores. While the platform has exhibited strong growth in lending volumes over its period of operation, we argue that the growth has not been driven by declining lending standards.

Australia’s relatively unsophisticated credit scoring environment (in place over the duration of this study’s sample period) and responsible lending guidelines enforced by ASIC have meant that the manual underwriting of loans (a costly, time-consuming exercise) has been a necessity. The growth of online lenders such as Society One should be aided by the implementation of Comprehensive Credit Reporting. The information gap between traditional banks and new entrants being reduced should lower the cost of credit assessment and enhance competition for consumers.

Creditworthiness is also shown to be strongly related to the SEIFA index. Future research could focus on the characteristics of borrowers in different socioeconomic areas of Australia. In particular, it would be useful to understand how existing credit scoring models could be improved and how access to credit could be improved to those in lower socioeconomic areas.