Abstract

Existing studies highlight the importance of air pollution in stock market participants’ information production. We extend this literature by investigating the impact of air pollution on management earnings forecasts among Chinese listed firms. Our findings show that air pollution significantly decreases management earnings forecasts voluntarily released by firms. Empirical results are robust to alternative measures, additional controls, the pseudo forecast date test, the difference-in-differences method and the instrumental variable approach. We further identify managerial ability and management mood as underlying mechanisms. The effects of air pollution are more pronounced among firms with fewer female executives, older executives, and less-educated executives.

1. Introduction

In the modern economy, firms are confronted with a myriad of external influences that extend beyond traditional financial considerations. In particular, natural environmental factors such as climate change (Pankratz et al., 2023; Zhang et al., 2018) and natural disasters (De Mel et al., 2012; Hosono et al., 2016) have become increasingly prominent in discussions around corporate operations. Among these factors, the influence of air pollution on the corporate information environment stands out as a crucial yet underexplored dimension. 1 While existing literature has recognised the negative impact of air pollution on the disclosure behaviours of analysts and investors (Li et al., 2020; Pankratz et al., 2023), few studies have examined how air pollution influences management disclosure behaviour, a critical component of the information environment that shapes investment decisions and market reputation. Therefore, this study addresses this research gap by examining how air pollution influences management earnings forecasting behaviour. By analysing listed firms in China, we aim to quantify and understand the impact of air pollution on management disclosure behaviour.

Management earnings forecasts (MEFs) refer to forward-looking statements made by executives regarding the firm’s anticipated financial performance. The forecasts include estimates of key financial indicators, such as revenue, earnings, and earnings per share, providing valuable insights for investors, analysts, and stakeholders in assessing the firm’s expected economic values (Hirst et al., 2008). Theoretically, MEFs could be adversely affected by air pollution through several mechanisms. First, prolonged exposure to poor air quality causes health risks (e.g. respiratory and cardiovascular diseases) (Ebenstein et al., 2017; Graff Zivin and Neidell, 2013), which can impair executives’ managerial abilities (Tan et al., 2021). This may alter the tendency and content of earnings releases, leading to a reduction in MEFs (Baik et al., 2011; Xing et al., 2019). Second, air pollution can induce negative emotional states such as stress, anxiety, and anger (Buoli et al., 2018; Zhang et al., 2017). These unfavourable emotional influences may prompt executives to adopt more cautious decisions, which may lead to a decline in MEFs (Bamber et al., 2010; Chen et al., 2022a). Despite extensive discussions, empirical evidence on the effect of air pollution on MEF disclosure remains limited, primarily due to challenges in data collection and the development of a credible empirical design.

China provides an excellent opportunity to investigate the role of air pollution in MEF disclosure. 2 First, the country faces persistent and complex atmospheric environmental issues. Rapid economic growth and regional disparities result in varying air pollution levels across cities, while national efforts to improve air quality create temporal variations. 3 These variations provide a valuable research context for examining the impact of air pollution on MEF disclosure. In addition, the transparency of earnings forecasting by listed firms in China offers detailed insights into how air pollution affects management’s financial forecasting over time.

Examining China’s listed firms from 2010 to 2021, this study indicates that firms tend to decrease the voluntary release of MEFs following increases in air pollution. The main results remain robust across a series of checks that consider alternative measures for MEFs and air pollution, as well as additional controls (air quality uncertainty, earnings announcement, and regional characteristics) in the regression. Moreover, we employ the pseudo forecast date test, the difference-in-differences (DID) method, and the instrumental variable (IV) approach to verify the reliability of empirical results. Further analysis reveals that managerial ability and management mood serve as operating mechanisms driving the air pollution effect. The heterogeneity analysis suggests that the effects of air pollution are more pronounced among firms with fewer female executives, older executives, and less-educated executives.

The first contribution of this study is that we extend the growing body of literature on the role of air pollution in the corporate information environment. Previous studies have well-documented that air pollution negatively influences analyst earnings forecasts (Li et al., 2020), information asymmetry between traders (Xiao, 2022), and the financial reporting quality issued by executives (Hu et al., 2022), which are key elements in shaping the corporate information environment. However, few studies have considered management decisions regarding earnings forecasts, although its importance for the corporate information environment has been confirmed in existing studies (Goodman et al., 2014; Hirst et al., 2008). Our study reveals a significantly negative relationship between air pollution and MEF disclosure. Furthermore, we explore the heterogeneous effects across management characteristics, including gender, age, and education. To the best of our knowledge, this is among the first studies to provide quantitative evidence on the impact of air pollution on MEF disclosure.

Second, this study contributes to the current literature on underlying mechanisms driving the effect of air pollution on the corporate information environment. Previous studies focus on the information behaviours of managers, analysts, and traders, and identify several mechanisms through which air pollution operates, such as mood, forecast boldness, corporate governance, and managerial human capital (Li et al., 2020; Xiao, 2022). The results of these studies are highly dependent on specific scenarios related to mechanism outcomes, sample selection, and empirical methodology. Our study contributes to the existing literature by examining the mechanisms behind the effect of air pollution on MEF disclosure, an area that has received limited attention. Empirical results support managerial ability and management mood as the key mechanisms driving our findings on MEFs.

Third, our study also contributes to the literature on the relationship between environmental conditions and corporate behaviour in developing countries. Previous research has extensively examined how environmental conditions influence corporate behaviour in developing countries such as Brazil, Russia, and South Africa (Liu et al., 2024b; Zhou et al., 2024; Crick et al., 2018). Due to differences in culture, corporate practices, and environmental regulations, the impact of environmental conditions on corporate behaviour may vary across developing countries. This study makes a valuable contribution to the empirical literature by examining the effect of air pollution on MEF disclosure in China. Numerous studies have investigated the determinants of MEFs among Chinese listed firms, including shareholder characteristics (Nie and Jia, 2021), board composition (Xing et al., 2019), customer concentration (Mei and Jing, 2024), internal control audits (Xia et al., 2024), digital transformation (Liu et al., 2024a), policy intervention (Ding et al., 2021) and so on. However, the impact of air pollution on MEF disclosure remains underexplored. Our study contributes to filling this research gap.

The structure of this study is organised as follows. Section 2 reviews the literature and develops hypotheses. Section 3 describes the data, variables and sample. Section 4 outlines the empirical model and discusses the results. Section 5 provides conclusions.

2. Literature review and research hypothesis

2.1. Air pollution and MEFs

The existing literature consistently demonstrates the adverse impact of air pollution on human health, primarily focusing on measurable outcomes such as hospitalisation, mortality rates, healthcare expenditure and life expectancy. However, these health outcomes likely represent only a fraction of the broader issues caused by air pollution. A growing body of research has begun to examine the role of air pollution in non-health outcomes, such as labour productivity (Chang et al., 2019; Fu et al., 2021), human capital migration (Chen et al., 2022b; Xue et al., 2021), employee incentives (Chan et al., 2022; Wang et al., 2021) and innovation (Ma and He, 2023; Tan and Yan, 2021). The vast majority of these studies highlight the negative externalities of air pollution, with underlying mechanisms primarily rooted in physiological factors, including inflammation, oxidative stress, cardiovascular and respiratory diseases and endocrine disruptions.

In capital markets, a growing body of research examines the impact of air pollution on agents’ behaviours that shape the corporate information environment. First, a set of studies focus on investor reactions. For instance, Li and Peng (2016) demonstrate that air pollution exerts contemporaneous negative and lagged positive effects on stock prices, while Xiao (2022) finds that air pollution exacerbates information asymmetry among investors. Second, another stream of literature explores management responses. Hu et al. (2022) reveal that air pollution reduces financial reporting quality, potentially due to anxiety and depression among corporate managers. Similarly, Wu et al. (2022) suggest that firms respond to heightened air pollution levels by adopting more conservative accounting practices and incorporating cautious estimates in financial reporting. Third, other studies investigate analysts’ behaviours. Li et al. (2020) find that analysts exposed to air pollution are less likely to issue timely forecasts or improve forecast accuracy, and Dong et al. (2021) note that deteriorating air quality reduces analysts’ optimism in profit forecasts. Drawing on the existing literature, we posit that air pollution tends to negatively impact corporate decision-making, resulting in a decrease in MEFs. The hypothesis is formulated as follows:

H1: Air pollution decreases the disclosure of management earnings forecasts.

2.2. Mechanisms

As defined by Demerjian et al. (2012), managerial ability refers to the proficiency of the management team in effectively leveraging corporate resources (e.g. capital, labour and land) to make strategic decisions that generate revenue, profit, and overall firm value. Notably, the existing literature suggests that air pollution significantly worsens physical health (Aguilar-Gomez et al., 2022) and reduces the accumulation of executive talent (Xue et al., 2021), leading to a deterioration in firms’ managerial ability. In addition, managerial ability has been well-documented as a critical determinant of MEF disclosure (Baik et al., 2011; Xing et al., 2019). Firms with high managerial ability often exhibit advanced strategic forecasting, efficient resource allocation, and environmental adaptability (Simamora, 2021; Ting et al., 2021). These firms are more likely to respond proactively to the adverse effects of air pollution by adapting their technology and management strategies, compared to firms with lower managerial ability. Based on the above discussion, we argue that the managerial ability of firm executives is a key mechanism driving the negative impact of air pollution on MEF disclosure. We anticipate that firms with low-ability executives will be more adversely affected by air pollution regarding their MEFs than those with high-ability executives. The hypothesis is given as:

H2a: The negative influence of air pollution on MEF disclosure is more pronounced for firms with low-ability executives.

Mood refers to a temporary emotional state or feeling that individuals experience (Eldar and Niv, 2015; Saviola et al., 2020), including emotions such as optimism, pessimism, happiness, sadness, anger and others. Current research extensively highlights the pivotal role of mood in cognitive processes and judgement, influencing individual decision-making (Vinckier et al., 2018; Weinrabe et al., 2023). Positive mood is linked to increased creativity and a greater propensity for risk-taking, while pessimistic mood tends to induce risk aversion and a focus on potential threats or downsides in decision-making (Harada, 2020; Mastria et al., 2019). A growing body of literature suggests that mood serves as an important mechanism driving the negative impact of air pollution on agents’ behaviour within the capital market. For example, Lepori (2016) documents that the negative relationship between air pollution and stock returns is mediated by investors’ moods. Dong et al. (2021) propose that analysts’ forecast pessimism is influenced by mood during site visits, suggesting mood as a likely mechanism for the impact of air pollution on analysts’ earnings forecasts. Compared to firms with pessimistic executives, those led by optimistic executives are more inclined to implement proactive strategies to mitigate the adverse effects of air pollution. Consequently, we posit that management mood serves as a potential operational mechanism. We expect that firms with pessimistic executives will be more adversely affected by air pollution in their MEFs than those with optimistic executives. The hypothesis is specified as follows:

H2b: The negative influence of air pollution on MEF disclosure is more pronounced for firms with pessimistic executives.

3. Data, variables and sample

3.1. Data

The dataset for this study integrates multiple sources. First, we collect data on MEFs from the RESSET Financial Research Database, a comprehensive financial platform widely used in academic research and industry analysis. An important feature of the RESSET database is its provision of detailed information on MEFs, allowing us to construct voluntary MEFs for firms. In addition, to obtain data on firm characteristics, we use the China Stock Market & Accounting Research (CSMAR) database, a leading resource for financial and economic research focused on the Chinese market. The CSMAR database offers extensive data on stock markets, corporate financials, corporate governance, mergers and acquisitions, and macroeconomic indicators. Air pollution data are sourced from the China National Environmental Monitoring Centre (CNEMC), which operates under the Ministry of Ecology and Environment of the People’s Republic of China. The CNEMC manages an extensive network of monitoring stations that provide real-time data on various environmental parameters, enabling us to conduct detailed analyses of air pollution trends across regions. Due to statistical limitations, some cities lacked Air Quality Index (AQI) records in the CNEMC before 2014. We address this data gap by supplementing AQI data from local governments through the Qingyue Open Environment Data Centre. Weather data are obtained from the National Centers for Environmental Information of the US National Oceanic and Atmospheric Administration.

3.2. Variables

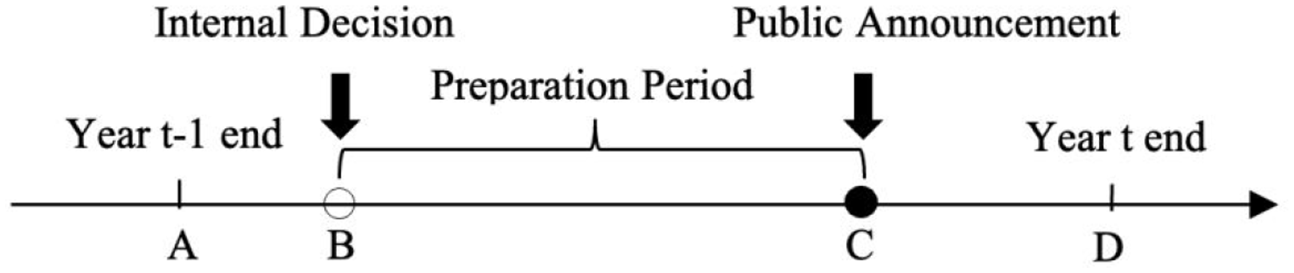

In China, MEFs can be issued either compulsorily, as required by regulatory authorities under specific circumstances, or voluntarily, at the discretion of the firm’s management. Voluntary MEFs are characterised by their flexibility and strategic use, enabling firms to proactively communicate expected financial performance and strategic intentions to investors. In this study, the dependent variables we examine are the issuance and frequency of voluntary MEFs. Specifically, MEF issuance (Issuance) is defined as a dummy variable that equals 1 if a firm voluntarily discloses at least one MEF in a given year, and 0 otherwise. MEF frequency (Frequency) is measured as the total number of MEFs voluntarily issued by a firm in a given year. Figure 1 illustrates the timeline for a voluntary MEF disclosure in China.

Timeline for the voluntary MEF disclosure in China.

To construct the independent variable, we adopt the logarithm of the annual average AQI for each city (LnAQI). According to CNEMC standards, the AQI is a numerical scale used to assess ambient air quality based on the concentrations of six major air pollutants, including sulphur dioxide (SO₂), nitrogen dioxide (NO₂), particulate matter (PM₂.₅ and PM₁₀), carbon monoxide (CO), and ozone (O₃). Each pollutant is assigned a sub-index based on its concentration relative to national air quality standards. The AQI is then determined by the highest sub-index among these pollutants. Therefore, higher AQI values indicate more severe levels of air pollution.

This study includes a series of controls for firm characteristics and weather conditions. The firm controls include the logarithm of firm size (LnSize), debt-to-asset ratio (Leverage), market-to-book ratio (MB), earnings increase (EarnIncrease), negative profitability (Loss), institutional ownership (Instown), the count of analyst teams tracking a firm (Analysts), and industry competition (Competition). In addition, weather controls include the logarithm of precipitation (LnPreci) and wind speed (Speed). The definitions of key variables are reported in Supplemental Appendix Table A1.

3.3. Sample

3.3.1 Sample construction

To construct the study sample, we align data on firms, pollution, and weather based on the cities where the headquarters of listed firms are located. We excluded observations that met any of the following criteria: (1) firms labelled as special treatment by stock exchanges, (2) firms in the financial sector, (3) missing air pollution data, (4) missing control variables, (5) fewer than 20 observations from the same city. The resulting sample comprises 13,706 observations used to examine the frequency of MEFs voluntarily released by firms. Considering government policies mandating earnings forecasts, we further exclude firms meeting any of the following conditions: (1) negative net profit, (2) negative net assets, and (3) positive net profit fluctuating by more than 50% compared to the previous year. This refined sample totals 5,580 observations for analysing MEF issuance. The procedure of sample construction is provided in Supplemental Appendix Table A2.

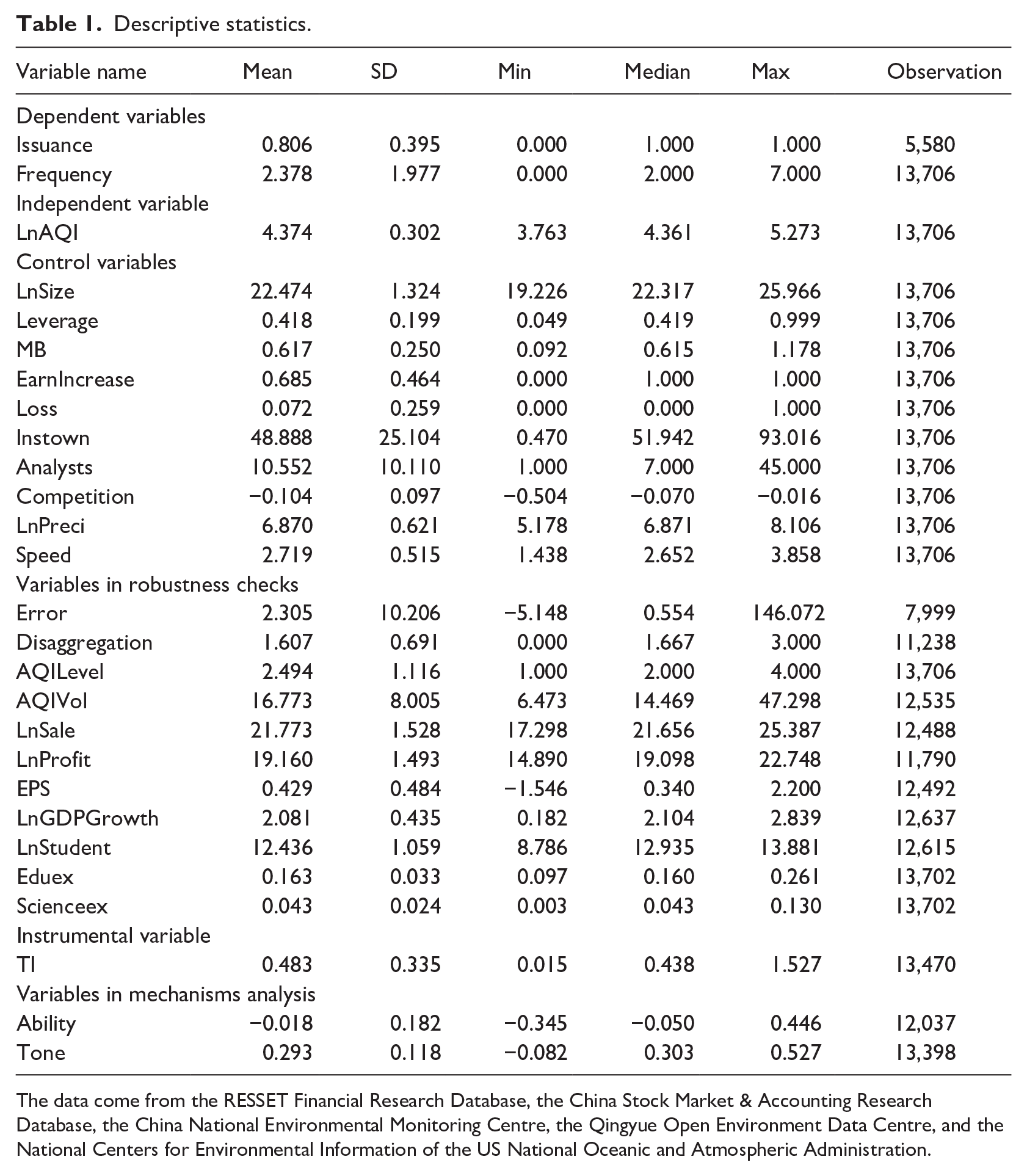

3.3.2 Descriptive statistics

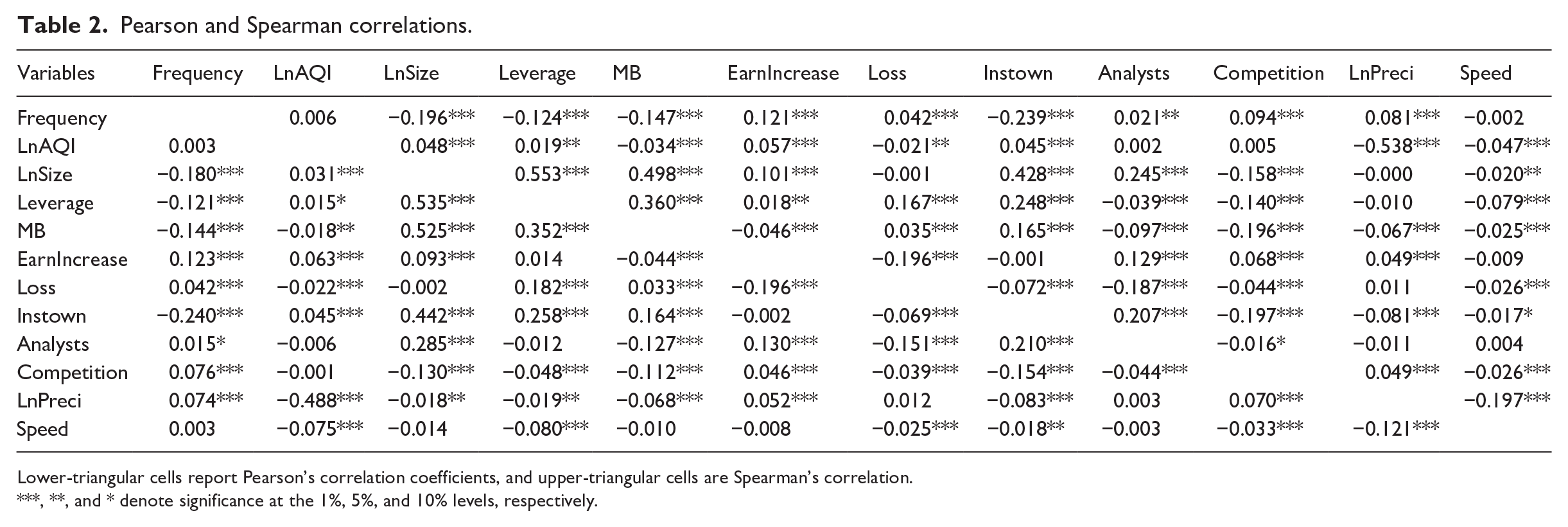

Table 1 reports descriptive statistics for key variables. During the sample period from 2010 to 2021, 80.6% of firms voluntarily issued MEFs at least once, with an average frequency of 2.378 per year. The average AQI was 83.290, with a standard deviation of 28.123. Regarding firm characteristics, the average firm size was 15.735 billion RMB, with a leverage ratio of 41.8% and a market-to-book ratio of 0.617. In addition, 68.5% of firms experienced earnings increases, while 7.2% reported negative net profits. Institutional investors held an average of 48.9% of shares, and firms were tracked by an average of 10.552 analyst teams. Industry competition, measured using the Herfindahl-Hirschman Index, had a mean value of -0.104. In terms of weather conditions, the average annual precipitation was 1,153.880 mm, while the mean wind speed was 2.719 m/s. Table 2 presents the results of Pearson and Spearman correlation analyses for key variables.

Descriptive statistics.

The data come from the RESSET Financial Research Database, the China Stock Market & Accounting Research Database, the China National Environmental Monitoring Centre, the Qingyue Open Environment Data Centre, and the National Centers for Environmental Information of the US National Oceanic and Atmospheric Administration.

Pearson and Spearman correlations.

Lower-triangular cells report Pearson’s correlation coefficients, and upper-triangular cells are Spearman’s correlation.

**, and * denote significance at the 1%, 5%, and 10% levels, respectively.

4. Empirical model and results

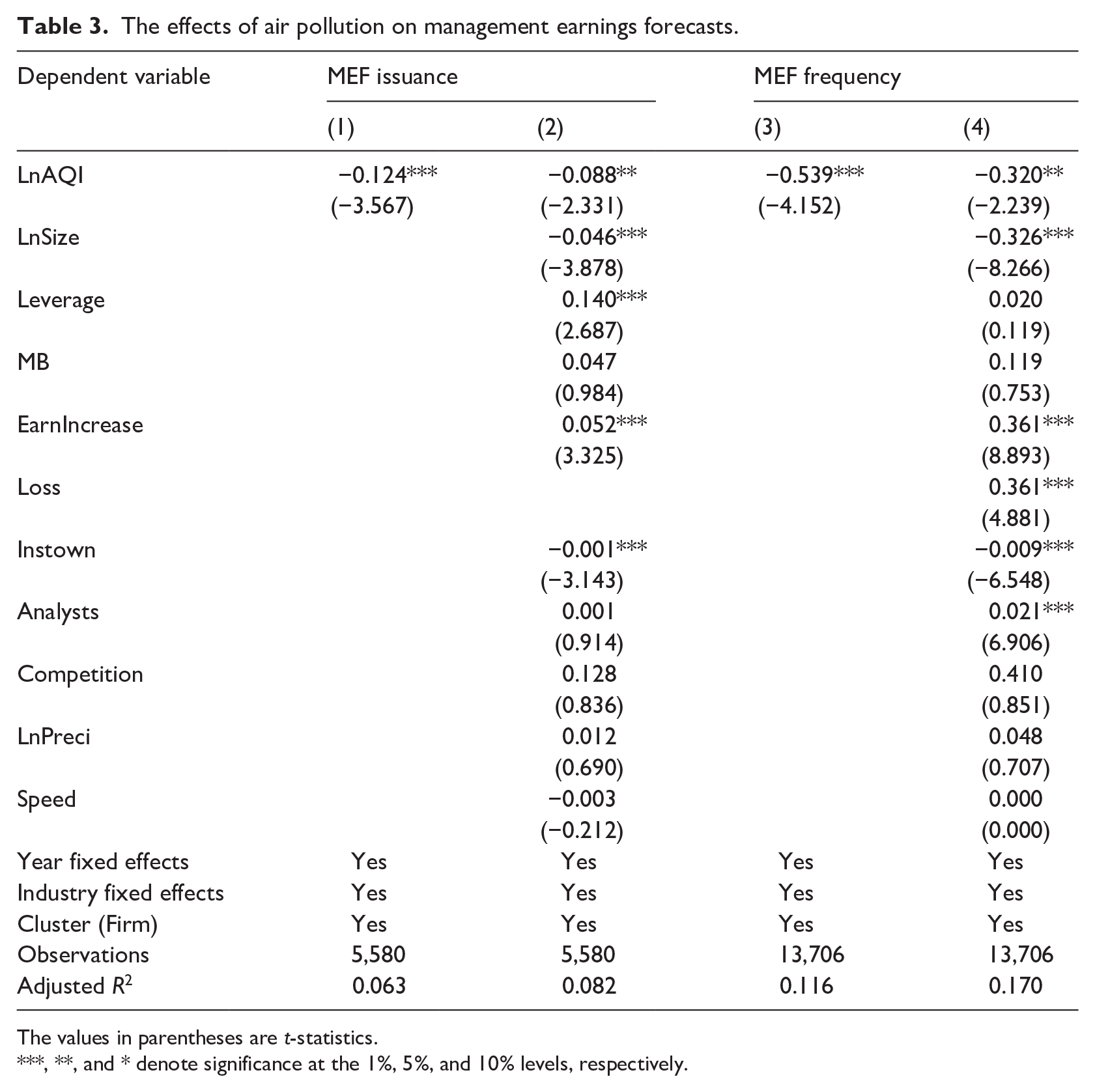

4.1. Air pollution and MEFs

To identify the effect of air pollution on MEF disclosure, we specify the Ordinary Least Squares (OLS) model as follows:

where i and t denote firm and year, respectively. MEF represents either MEF issuance or frequency, while LnAQI refers to the logarithm of the annual average AQI of the city where the firm’s headquarters is located. The coefficient of interest,

Table 3 presents the results for the effect of air pollution on MEF disclosures. The first two columns examine MEF issuance, while the last two columns explore MEF frequency. In column (1), the regression with year and industry fixed effects shows that the coefficient estimate of air pollution is significantly negative for MEF issuance. This result remains consistent after the inclusion of control variables in column (2). Similarly, in columns (3) and (4), coefficient estimates of air pollution are significantly negative for MEF frequency. These findings provide suggestive evidence of a negative relationship between air pollution and MEF disclosure. Notably, the statistically insignificant coefficients for precipitation and wind speed in the regressions suggest that weather conditions have minimal impact on MEF disclosure, which is consistent with previous studies (Wang et al., 2021).

The effects of air pollution on management earnings forecasts.

The values in parentheses are t-statistics.

**, and * denote significance at the 1%, 5%, and 10% levels, respectively.

4.2. Robustness tests

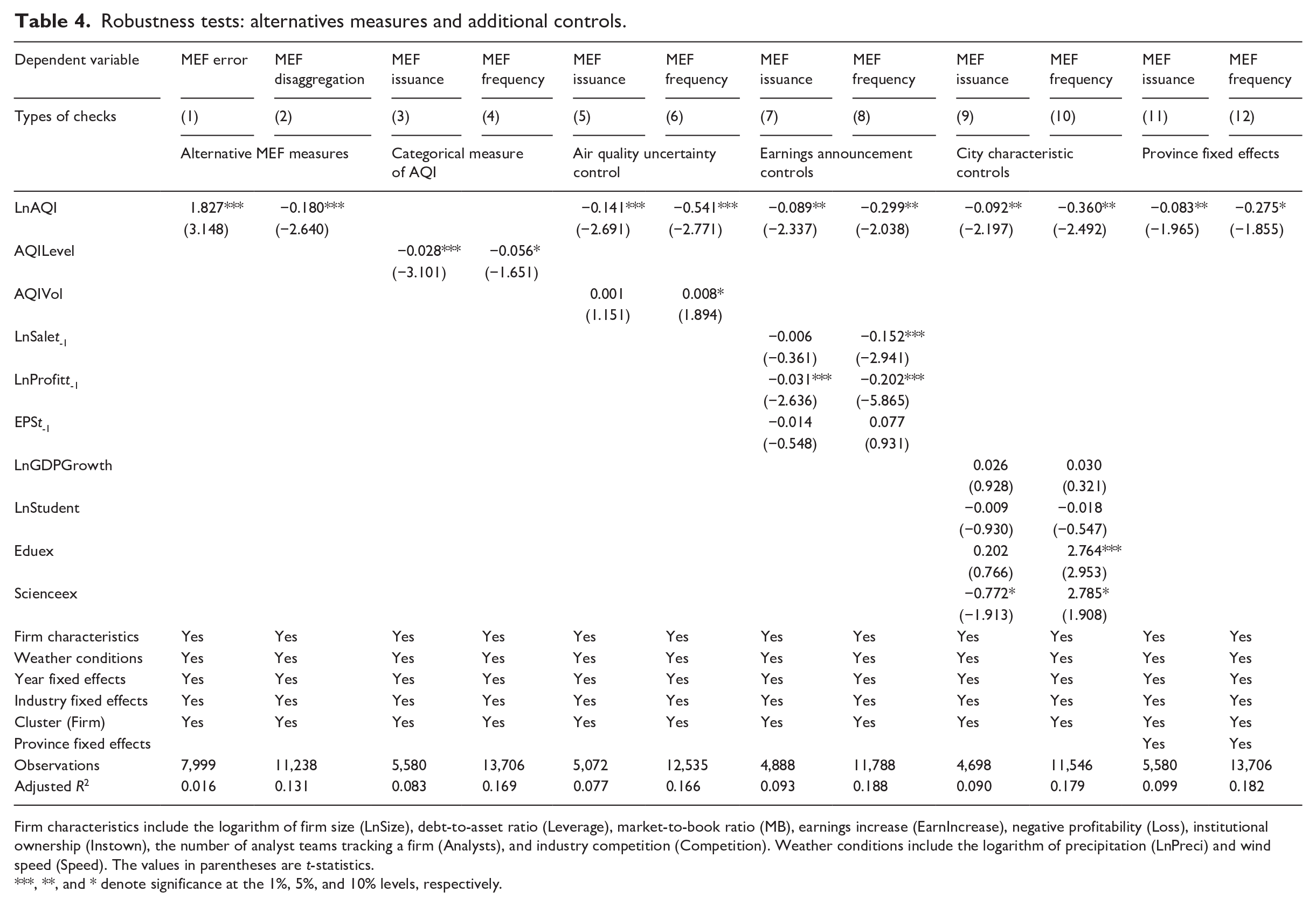

4.2.1 Alternative measures

MEF measures. In this analysis, we conduct a robustness check by replacing the dependent variables with MEF error and disaggregation, which are used to measure the quality of MEFs (Guan et al., 2020). Specifically, MEF error is defined as the absolute value of the difference between the predicted and actual net profit, divided by the actual net profit. Meanwhile, MEF disaggregation refers to the average number of financial forecasting items – such as operating income, net profit, net profit growth rate, and earnings per share – reported in the firm’s MEF(s) for a given year. The results are summarised in the first two columns of Table 4. Column (1) reveals a significantly positive relationship between air pollution and MEF error, while column (2) shows a negative association between air pollution and MEF disaggregation. In summary, empirical results suggest that firms in cities with more severe air pollution tend to provide less accurate and less detailed MEFs. These findings are consistent with our main conclusion that air pollution negatively affects MEF disclosure.

Robustness tests: alternatives measures and additional controls.

Firm characteristics include the logarithm of firm size (LnSize), debt-to-asset ratio (Leverage), market-to-book ratio (MB), earnings increase (EarnIncrease), negative profitability (Loss), institutional ownership (Instown), the number of analyst teams tracking a firm (Analysts), and industry competition (Competition). Weather conditions include the logarithm of precipitation (LnPreci) and wind speed (Speed). The values in parentheses are t-statistics.

**, and * denote significance at the 1%, 5%, and 10% levels, respectively.

AQI measure. To further examine the robustness of the results, this study replaces the original AQI with a categorical measure of the AQI (AQILevel) in the regression analysis (Dong et al., 2021). Specifically, AQILevel values are assigned as follows: 1 for AQI between 0 (inclusive) and the first quartile (inclusive), 2 for AQI between the first and second quartiles (inclusive), 3 for AQI between the second and third quartiles (inclusive), and 4 for AQI above the third quartile. Thus, a higher AQILevel indicates more severe air pollution. The results in columns (3) and (4) of Table 4 show that coefficient estimates of AQILevel remain significantly negative, suggesting that our findings are robust to the alternative AQI measure.

4.2.2 Additional controls

Air quality uncertainty. Existing literature highlights the importance of air pollution uncertainty in a firm’s information production (Hu et al., 2022). It is questionable whether estimation results are sensitive to the inclusion of air pollution uncertainty. To address this concern, we conduct a robustness check by adding air pollution uncertainty in the regression, which is measured by the standard deviation of the AQI (AQIVol). The results in columns (5) and (6) of Table 4 still show a significantly negative relationship between air pollution and MEF disclosure. These findings indicate that our results are robust to the inclusion of air quality uncertainty.

Earnings announcement. Firm executives may bundle earnings forecasts with prior earnings announcements to help investors interpret financial information. Insufficient control of this factor may lead to biased estimation results. To address the bundling concern, this study adds controls for earnings announcements from the previous year, including operating income (LnSale), net profit (LnProfit), and earnings per share (EPS). Columns (7) and (8) of Table 4 show that coefficient estimates for air pollution remain significantly negative, suggesting that air pollution adversely impacts MEFs. This empirical evidence alleviates the bundling concern in our estimation.

Regional controls. Previous literature has documented the role of regional characteristics in MEF disclosure (Maslar et al., 2021). It is natural to ask whether the estimation results are sensitive to regional characteristics. To deal with this concern, we incorporate city-level characteristic controls, including GDP growth rates (LnGDPGrowth), the number of college students (LnStudent), the proportion of education expenditure in fiscal spending (Eduex), and the proportion of science expenditure in fiscal spending (Scienceex). Columns (9) and (10) of Table 4 indicate that coefficient estimates of air pollution remain significantly negative after the inclusion of city characteristics. In addition, to further examine the robustness of our result, we include province fixed effects in the regression to control for unobserved heterogeneity (Zhang et al., 2019). Columns (11) and (12) of Table 4 still show negative effects of air pollution on MEF disclosures. In sum, our findings are robust to the inclusion of regional controls.

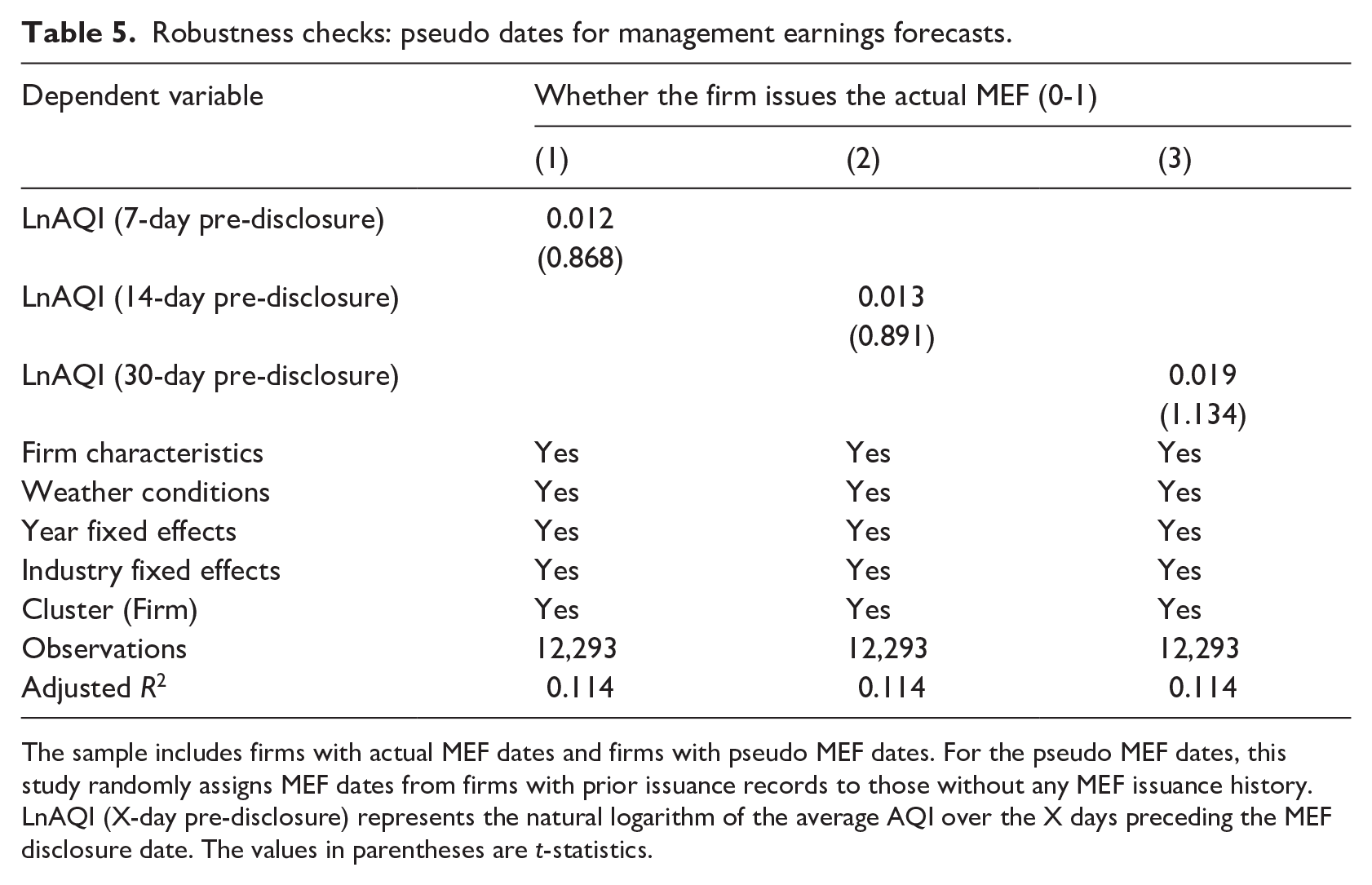

4.2.3 The pseudo forecast date test

In this analysis, we conduct an additional robustness test using pseudo MEF dates. Specifically, we randomly assign MEF dates from firms with prior issuance records to those without any MEF issuance history (3,577 observations). We then construct a new sample by combining firms with actual MEF dates and firms with pseudo MEF dates. Subsequently, we match these MEF dates with daily AQI data to calculate average AQI levels across various pre-MEF time windows (7-day, 14-day, and 30-day periods). The outcome we examine in this robustness check is whether the firm issues the actual MEF. Given that the new sample contains a significant number of firms with pseudo MEF dates, we anticipate that air pollution will not significantly influence MEF disclosure. The results in Table 5 demonstrate statistically insignificant coefficient estimates across all examined time windows, suggesting that air pollution has little effect on MEF disclosures. These findings align with our expectations, confirming the robustness of empirical results to the pseudo forecast date test.

Robustness checks: pseudo dates for management earnings forecasts.

The sample includes firms with actual MEF dates and firms with pseudo MEF dates. For the pseudo MEF dates, this study randomly assigns MEF dates from firms with prior issuance records to those without any MEF issuance history. LnAQI (X-day pre-disclosure) represents the natural logarithm of the average AQI over the X days preceding the MEF disclosure date. The values in parentheses are t-statistics.

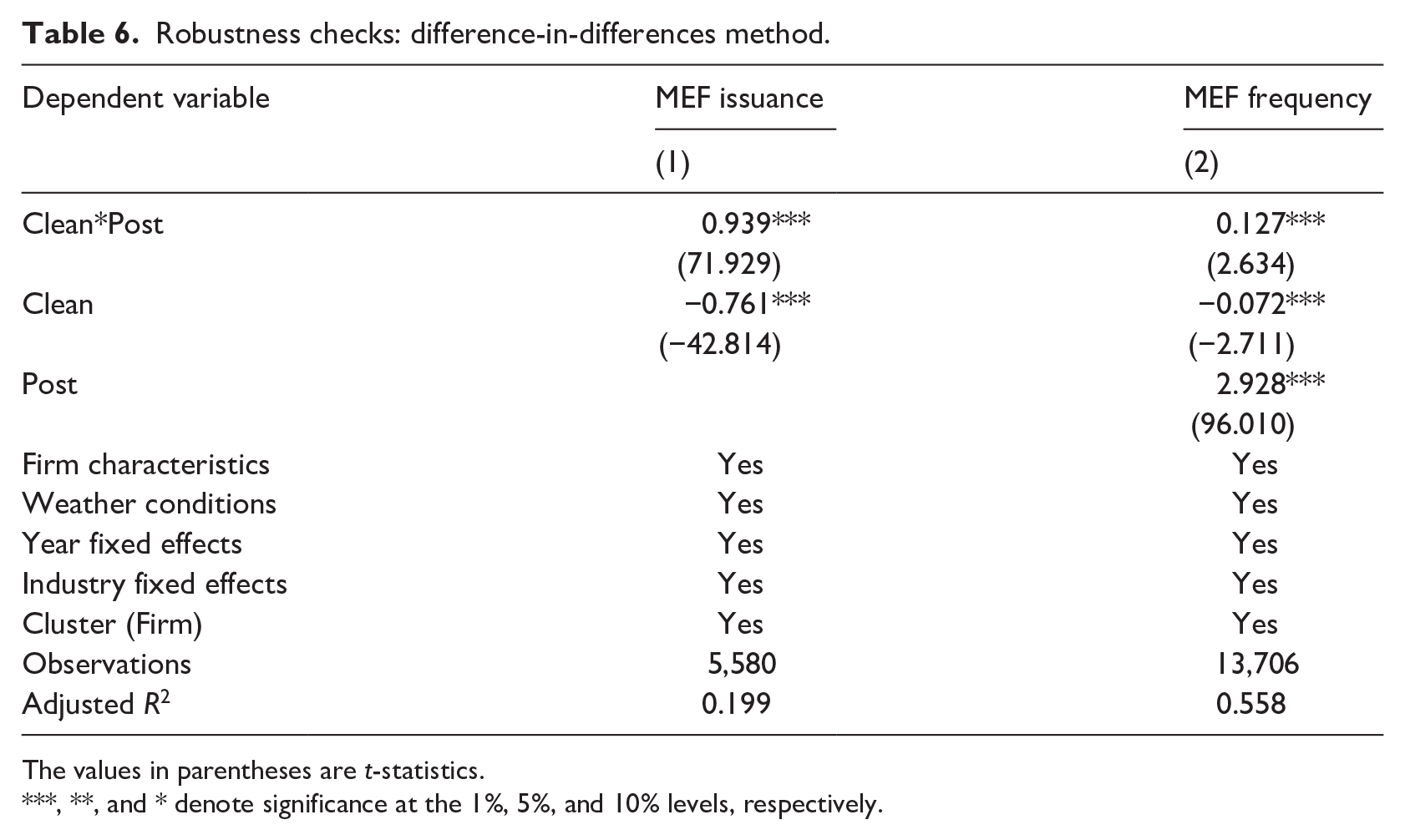

4.2.4 DID method

To further validate the findings, we follow the existing literature (Li et al., 2020) to adopt the DID method as a robustness check. The equation is specified as follows:

where Clean equals 1 if the AQI difference between any two adjacent quarters within a year is negative and its absolute value exceeds one standard deviation of the quarterly AQI for the full sample, and 0 otherwise. Post equals 1 for the year in which the MEF is released, and 0 otherwise. The independent variable of interest is the interaction term (Clean*Post). If air pollution effects on MEFs exist, we should expect the coefficient

Robustness checks: difference-in-differences method.

The values in parentheses are t-statistics.

**, and * denote significance at the 1%, 5%, and 10% levels, respectively.

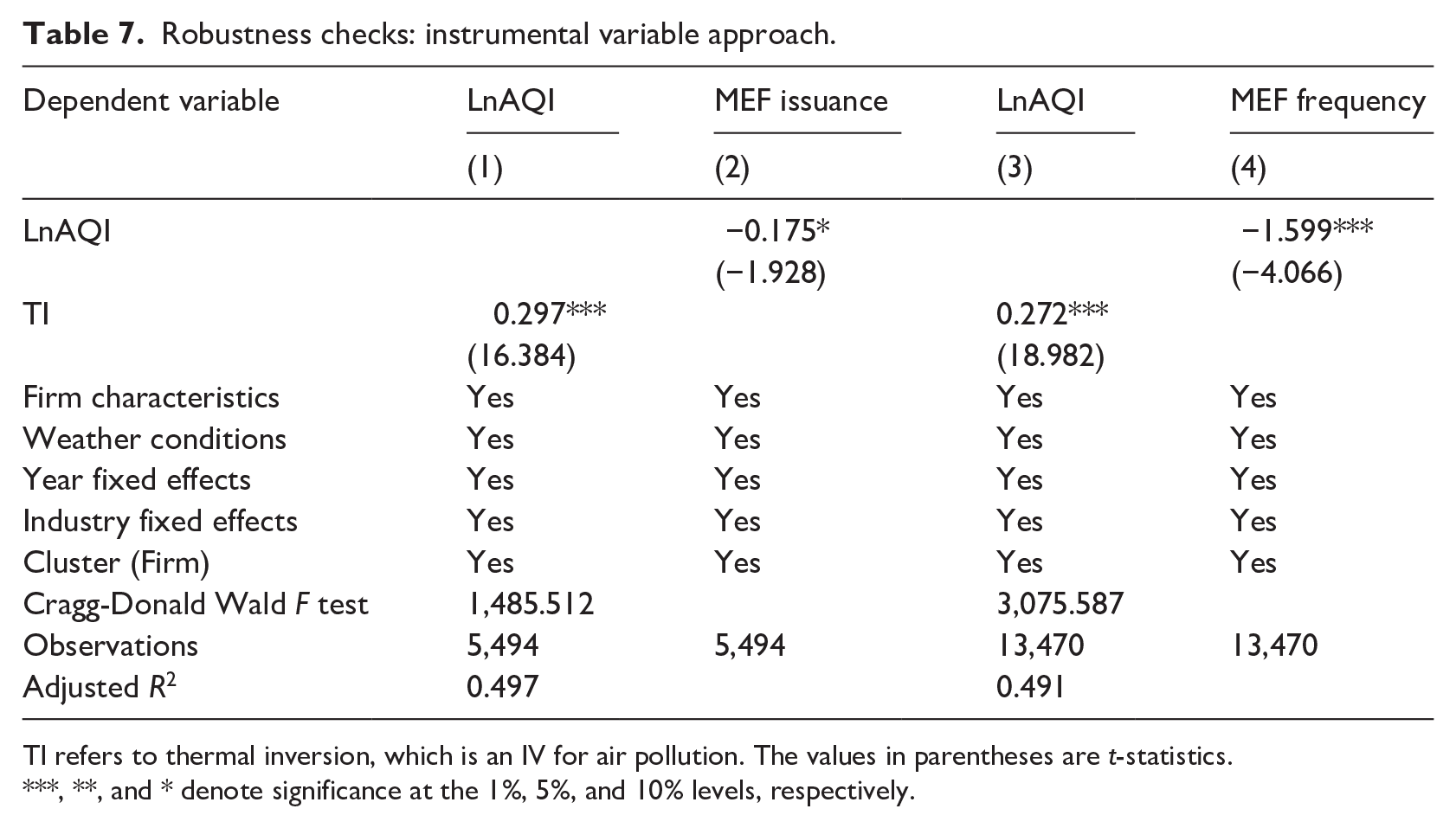

4.2.5 IV approach

Although the regression has included a rich set of control variables, we cannot exclude the possibility of unobserved factors that influence both the AQI and MEFs, leading to biased estimation results. This study further addresses the endogeneity concern by adopting an IV method based on thermal inversion (TI). We choose this instrument for two reasons. First, TI is positively correlated with air pollution. The TI phenomenon occurs when a layer of warm air acts as an atmospheric lid over cooler surface air, physically inhibiting the vertical dispersion of ground-level pollutants (Arceo et al., 2016). This meteorological mechanism creates positive associations between TI events and air pollution. Second, TI satisfies the exclusion restriction. As a transient meteorological phenomenon, TI is unlikely to influence firm decision-making through channels other than air pollution.

The TI data are from the Modern-Era Retrospective Analysis for Research and Applications version 2 satellite. This satellite divides the Earth into grids of 0.5° by 0.625° (approximately 50 km by 60 km) and records air temperature across 42 vertical layers, from the surface up to 36,000 m, with measurements taken every 6 hours. The TI intensity for each city is determined by calculating the average temperature difference between the second layer (320 m) and the first layer (110 m) across all grid cells within the city’s boundaries. The IV used in this study is a binary variable for TI that equals 1 if the average temperature difference in the local city is positive, and 0 otherwise.

Table 7 reports the IV results for the effect of air pollution on MEF disclosure. The first-stage regressions in columns (1) and (3) show positive relationships between TI and air pollution, as expected. In addition, the results for the Cragg-Donald Wald F statistics indicate that the IVs pass the weak instrument test. In columns (2) and (4), the second-stage IV regressions reveal that coefficient estimates are significantly negative for both the issuance and frequency of MEFs. These results provide strong evidence that air pollution significantly decreases MEF disclosure.

Robustness checks: instrumental variable approach.

TI refers to thermal inversion, which is an IV for air pollution. The values in parentheses are t-statistics.

**, and * denote significance at the 1%, 5%, and 10% levels, respectively.

4.3. Mechanisms

4.3.1 Managerial ability

One interpretation of our results is that air pollution influences MEFs through its negative impact on managerial ability. Existing literature has established a positive relationship between managerial ability and MEF disclosure (Baik et al., 2011). Air pollution may decrease managerial effectiveness by compromising executive health and hindering talent recruitment, ultimately leading to a reduction in MEFs. To explore whether managerial ability is a valid mechanism, this study examines whether firms with low-ability executives are more negatively affected by air pollution. Based on previous literature (Demerjian et al., 2012), we measure a firm’s managerial ability as follows. First, we employ Data Envelopment Analysis to calculate firm efficiency scores, which maximise sales revenue based on six firm-specific inputs: net property, plant, and equipment; intangible assets; purchased goodwill; R&D expenditure; cost of goods sold; and selling, general, and administrative expenses. The efficiency scores capture both managerial ability and firm-specific characteristics. Second, we adopt the Tobit model to isolate managerial ability from firm characteristics. The equation is specified as follows:

where i, j, and t indicate firm, industry, and year, respectively. Firm characteristics in equation (3) include firm size (Totalassets), market share (Marketshare), free cash flow (FCF), listed years (Age), the degree of internationalisation (FC), and the Herfindahl-Hirschman Index (HHI). Year and industry fixed effects are included to control for unobserved heterogeneity. It is important to note that the residual (εi,t) is used as a proxy for the firm’s managerial ability.

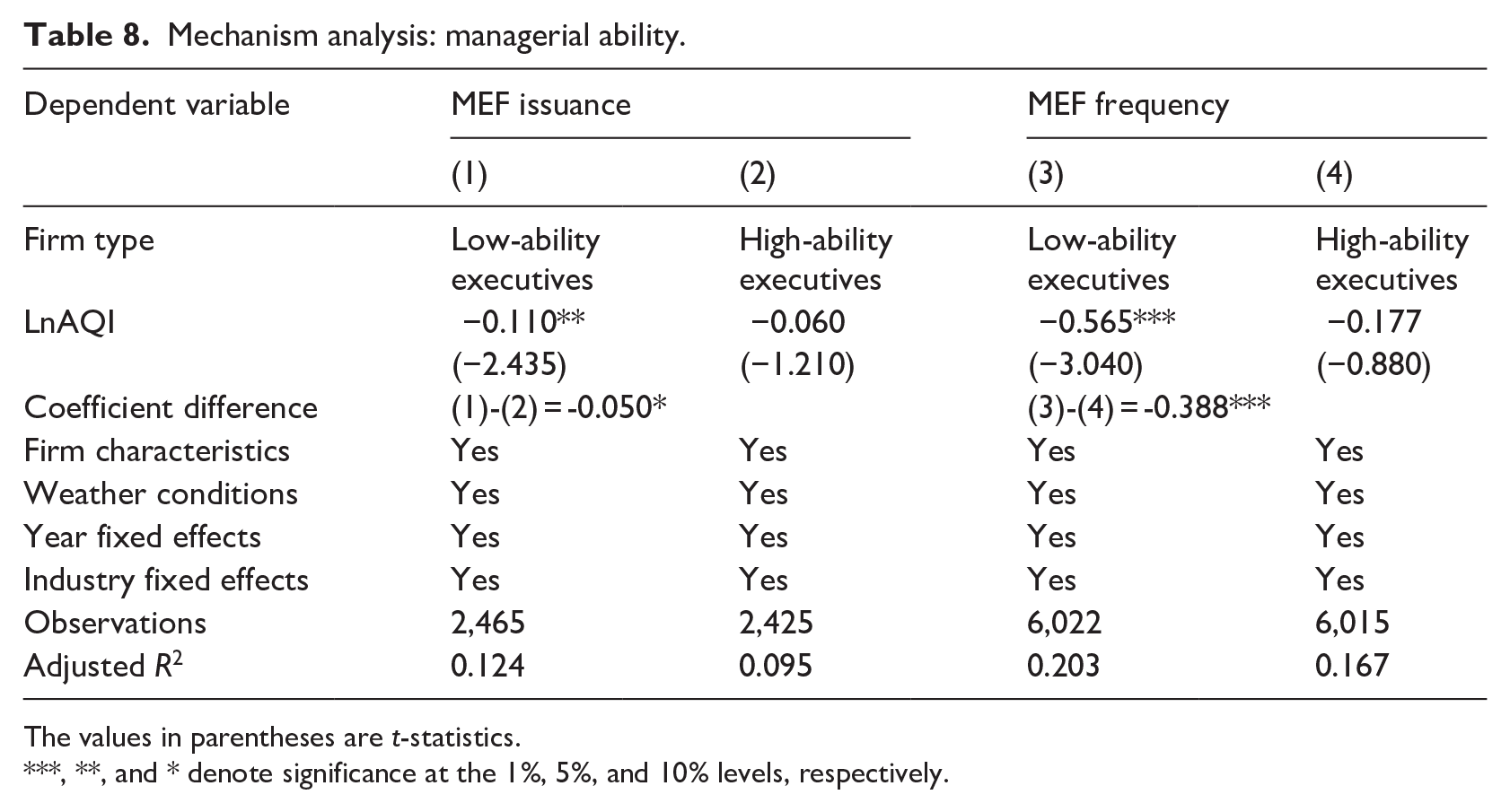

Based on the median value of managerial ability, this study splits the sample into two groups: firms with low-ability executives (managerial ability ⩽ median) and firms with high-ability executives (managerial ability > median). In Table 8, columns (1) and (3) indicate significant negative coefficient estimates of air pollution for firms with low-ability executives. In contrast, we find insignificant results for firms with high-ability executives in columns (2) and (4). To sum up, empirical results show that the negative effects of air pollution on MEFs are more pronounced for firms with low-ability executives. These findings provide suggestive evidence that managerial ability is an operating mechanism driving the negative impact of air pollution on MEF disclosure.

Mechanism analysis: managerial ability.

The values in parentheses are t-statistics.

**, and * denote significance at the 1%, 5%, and 10% levels, respectively.

4.3.2 Management mood

Another interpretation of our findings is that air pollution affects MEF disclosure by its detrimental effect on management mood. Specifically, air pollution may induce negative emotional responses in executives by impairing their cognitive processing and fostering conservative decision-making behaviour, resulting in a decline in MEFs. To investigate whether management mood serves as a feasible mechanism, this study examines whether firms with pessimistic executives are more significantly affected by air pollution. We follow previous research (Hu et al., 2022) to measure management mood using positive and negative words in annual reports based on the dictionary developed by Loughran and McDonald (2011). The definition of management mood is given as follows:

where Tonei,t represents management tone for firm i in year t. In addition, positive words and negative words denote the counts of positive and negative sentiment words in annual reports, respectively. A higher management tone value indicates a more positive executive mood.

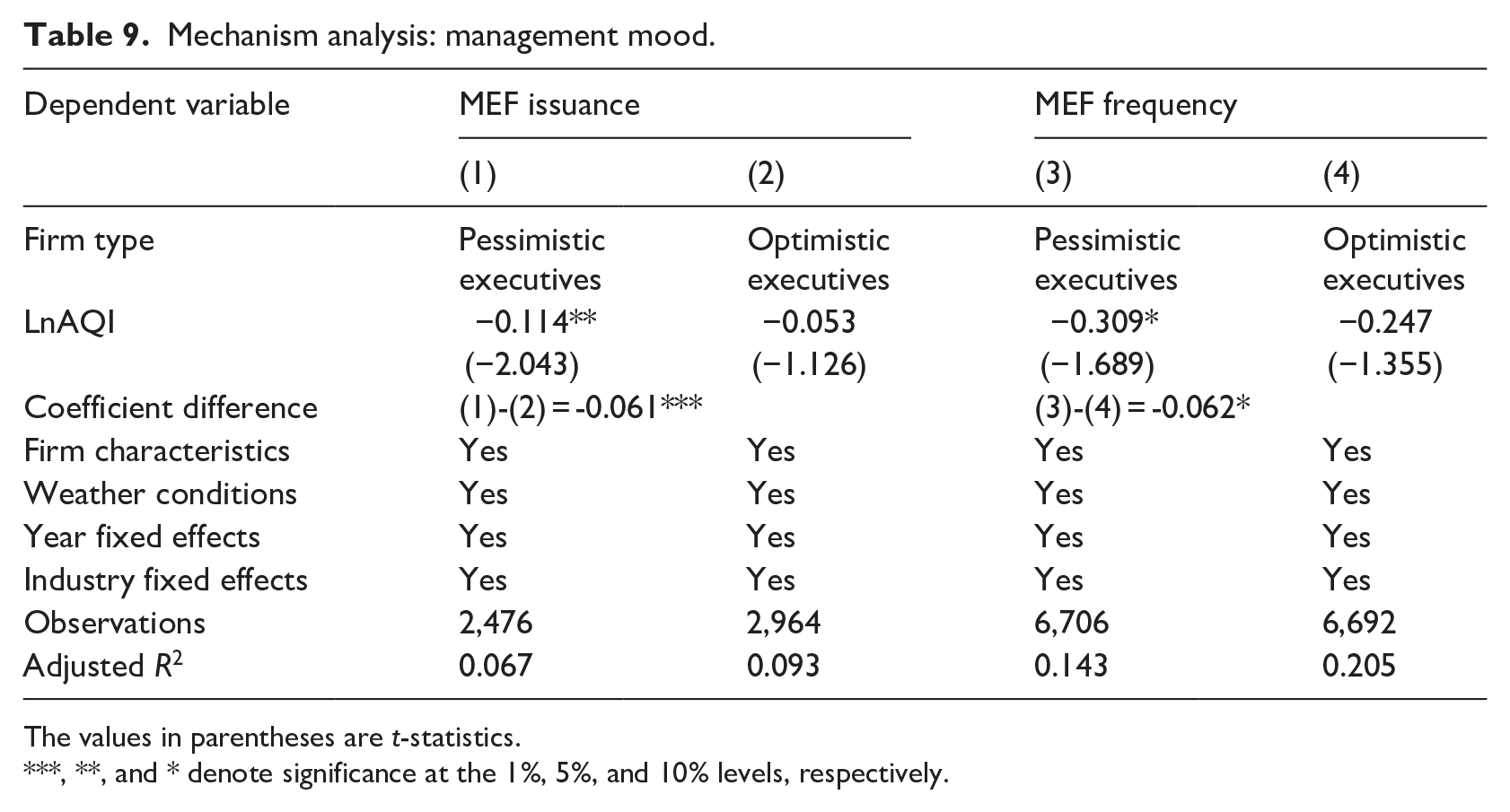

Based on the median value of management tone, this study divides the sample into two groups: firms with pessimistic executives (tone value ⩽ median) and firms with optimistic executives (tone value > median). In Table 9, columns (1) and (3) indicate that coefficient estimates are significantly negative for firms with pessimistic executives, suggesting that air pollution adversely affects MEF disclosure. In contrast, columns (2) and (4) report statistically insignificant results for firms with optimistic executives. These findings provide evidence that management mood is a potential mechanism through which air pollution influences MEF disclosure.

Mechanism analysis: management mood.

The values in parentheses are t-statistics.

**, and * denote significance at the 1%, 5%, and 10% levels, respectively.

4.4. Heterogeneous effects

4.4.1 Gender

Prior research indicates that female executives face unfavourable labour market expectations due to social stereotypes (Lee and James, 2007), which often attribute their success to effort or luck rather than recognised ability. In such contexts, female executives may strategically disclose MEFs to demonstrate managerial competence (Francoeur et al., 2023). Consequently, firms with fewer female executives may experience more pronounced effects of air pollution on MEF disclosure than those with more female executives.

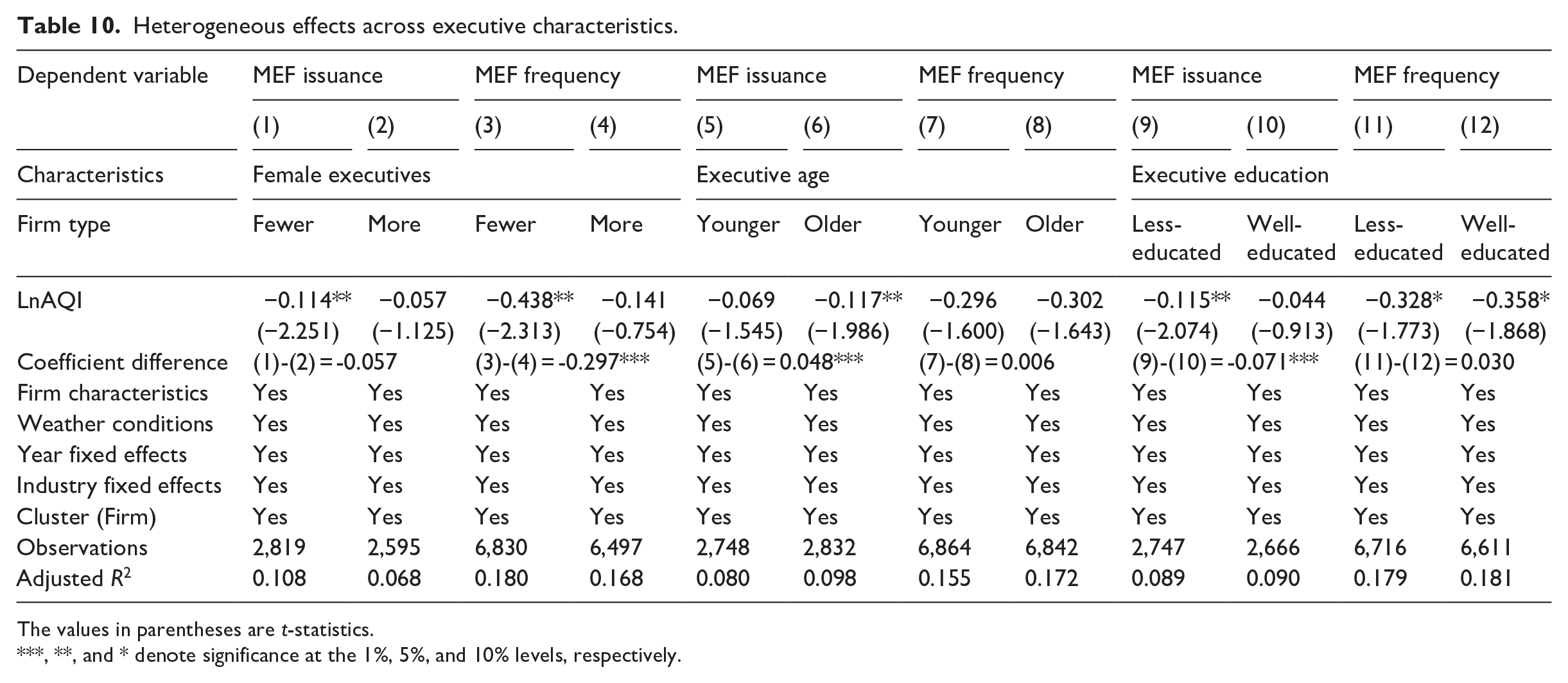

To conduct the heterogeneous test, we separate the sample into two groups based on the median proportion of female executives: firms with fewer female executives (female proportion ⩽ median) and firms with more female executives (female proportion > median). Columns (1) and (3) of Table 10 suggest that coefficient estimates are significantly negative for firms with fewer female executives. However, in columns (2) and (4), we find insignificant results for firms with more female executives. This empirical evidence suggests that the effect of air pollution on MEF disclosure is primarily driven by firms with fewer female executives.

Heterogeneous effects across executive characteristics.

The values in parentheses are t-statistics.

**, and * denote significance at the 1%, 5%, and 10% levels, respectively.

4.4.2 Age

Existing literature offers conflicting perspectives on the role of executive age in decision-making. On one hand, older executives are often perceived as more risk-averse due to their extensive experience with economic fluctuations (Malmendier and Nagel, 2011). In contrast, younger executives tend to be more proactive and eager to demonstrate their managerial capabilities, which may lead to more MEF disclosures (Dai et al., 2013). This suggests that firms with older executives may exhibit stronger negative effects of air pollution due to their risk-averse tendencies. On the other hand, some studies argue that older executives, with their deeper understanding of the business environment (Huang et al., 2012), may be better equipped to buffer against air pollution shocks. This implies that firms with older executives could be less sensitive to air pollution in terms of MEF disclosure.

To examine the heterogeneous effects by executive age, this study splits the sample into two groups based on the median age of the executive team: firms with younger executives (age ⩽ median) and firms with older executives (age > median). In Table 10, columns (5) and (6) show that both coefficient estimates for MEF issuance are negative, but the result is only statistically significant for firms with older executives. However, we find no statistically significant evidence regarding the frequency of MEFs in firms with either younger or older executives. In summary, our findings provide suggestive evidence that the negative effect of air pollution on MEF disclosure is primarily driven by firms with older executives.

4.4.3 Education

Current studies consistently indicate that education plays a crucial role in enhancing management capabilities (Nadkarni and Herrmann, 2010), including analytical skills, decision-making abilities, and execution competencies. Well-educated executives are more likely to adopt effective measures to mitigate the adverse impacts of air pollution, such as formulating and implementing environmental policies, introducing clean production technologies, or optimising resource allocation. Thus, the impact of air pollution may vary across firms with different education levels of executives.

To test this heterogeneity, we divide the sample into two groups based on the median proportion of executives with tertiary education: firms with less-educated executives (education proportion ⩽ median) and firms with well-educated executives (education proportion > median). Columns (9) and (11) of Table 10 indicate that coefficient estimates of air pollution are significantly negative for MEFs in firms with less-educated executives. For firms with well-educated executives, we find coefficient estimates are also negative in columns (10) and (12) but the result is only statistically significant at the 10% level for the MEF frequency. To sum up, these findings provide suggestive evidence that the impact of air pollution is mainly driven by firms with less-educated executives.

5. Conclusion

This study investigates the relationship between air pollution and voluntary MEFs among Chinese listed firms. Empirical results indicate the negative effect of air pollution on MEF disclosure. These findings are robust to a series of tests, including alternative measures, additional controls, the pseudo forecast date analysis, the DID estimation, and the IV approach. We further identify managerial ability and management mood as operating mechanisms through which air pollution influences MEF disclosure. Heterogeneous analyses show that the adverse effects of air pollution are more pronounced in firms with fewer female executives, older executives, and less-educated executives.

Our findings offer several important policy implications. First, policymakers should implement stricter industrial emission standards to mitigate the negative impact of air pollution on MEF disclosure. Second, governments could consider providing health support services to alleviate stress and emotional fluctuations among firm executives. Third, based on the results of heterogeneity analyses, governments may design targeted measures to help firms buffer against adverse air pollution shocks, such as promoting gender diversity in leadership, improving office environments, and enhancing executive education backgrounds.

Although our research focuses on China, its implications may extend to other countries experiencing similar developmental trajectories and persistent air pollution challenges. In recent decades, nations such as India and South Africa have also faced significant air pollution issues. Our findings provide insights into how air pollution influences firms’ MEF behaviour, highlighting its negative impact on executives’ information production. When interpreting the results, it is important to note that our estimation captures only the short-term response of MEFs to air pollution. In the long term, firms may adopt adaptive measures to mitigate the effects of air pollution, such as installing air purification systems and implementing flexible working hours. As a result, our findings may overestimate the role of air pollution in MEFs. Future research could explore how firms’ adaptive behaviours influence MEF disclosure in response to air pollution.

Key theoretical and policy implications:

Supplemental Material

sj-docx-1-aum-10.1177_03128962251331084 – Supplemental material for The impact of air pollution on management earnings forecasts: Evidence from China

Supplemental material, sj-docx-1-aum-10.1177_03128962251331084 for The impact of air pollution on management earnings forecasts: Evidence from China by Zengfu Li, Xin Kuang, Yue Gan, Zheng Pan and Yangjun Cai in Australian Journal of Management

Footnotes

Acknowledgements

We are grateful to the Editor-in-Chief, Andrew Jackson, and two anonymous reviewers for their insightful comments and suggestions. All remaining errors are our own.

Final transcript accepted on 11 March 2025 by Andrew Jackson (Editor-in-Chief).

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the National Natural Science Foundation of China (72373044) and the Higher Education Teaching Reform and Research Project of Zhongkai University of Agriculture and Engineering (JG2024014).

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.