Abstract

Purpose:

This article examines whether CEOs with not-for-profit (NFP) leadership positions (NFP CEOs) influence the likelihood of corporate misconduct. We also test whether directors on boards with NFP leadership involvement (NFP boards) strengthen or weaken the association described above.

Design/methodology/approach:

We embrace multiple perspectives in developing our hypothesised associations. Based on benevolent leadership and upper-echelon theoretical perspectives, we hypothesise a negative association between NFP CEOs and corporate misconduct. Then, drawing on competing arguments in the literature, such as CEO power and moral licensing, we hypothesise a positive association between NFP CEOs and corporate misconduct. The NFP CEOs and directors are recognised for their involvement in not-for-profit leadership roles concurrently with their corporate leadership roles. Corporate misconduct refers to any unethical event by firms that negatively influences stakeholders. We hand-collected data for a sample of Australian-listed firms from 2010 to 2019.

Findings:

Our baseline results indicate a positive association between NFP CEOs and misconduct, aligning with the competing hypothesis. We further document a positive moderating role of NFP boards on the association between NFP CEOs and misconduct. Tests of theoretical arguments suggest that the positive association between NFP CEOs and misconduct is driven by potential conflicts of priorities and/or moral licensing. However, the additional analysis indicates that NFP CEOs with four or more positions are less likely to be associated with corporate misconduct. We contend that this nuanced result stems from differences in moral ethics among NFP CEOs.

Originality/value:

Our research contributes new insights into the determinants of corporate misconduct, particularly the relationship between leaders’ moral characteristics and misconduct. The originality of this study lies in examining the bright-side characteristics of leaders in influencing corporate misconduct, in contrast to most prior research on dark-side characteristics.

Research limitations/implications:

New knowledge of the drivers of corporate misconduct is essential in pursuing avenues to prevent, detect, and discourage unethical actions by firms. We contribute to the literature and practice by examining the link between CEOs’ moral characteristics and corporate misconduct, providing insights into the complexities that drive or impede misconduct.

JEL Classification:

G41, M14

1. Introduction

Rio Tinto’s conduct reflects a corporate culture which prioritised commercial gain over the kind of meaningful engagement with Traditional Owners that should form a critical part of their social licence to operate. (Parliamentary Committee of Juukan Gorge Incident) (Ker, 2020)

This study examines the potential influence of CEOs serving on not-for-profit (NFP) boards on corporate misconduct. Prior research that has extensively examined the impact of executive and director characteristics on corporate misconduct (e.g. litigation, financial misreporting, and unethical practices) (Schnatterly et al., 2018) has predominantly focused on traits associated with the so-called “dark side” of leadership, including narcissism, overconfidence, and impulsivity (Free, 2015). These studies suggest that such traits may foster corporate cultures that prioritise financial performance over ethical considerations. In contrast, this study explores whether “bright side” characteristics, such as moral orientation, demonstrated through personal life engagement in philanthropic actions, may mitigate misconduct, thereby offering a novel and compelling direction for inquiry.

Investigating the antecedents of corporate misconduct broadens both scholarly and regulatory understanding. Unethical corporate behaviour violates the principle of social licence to operate, given the significant harm it causes to investors, markets, and society. Such behaviour manifests in various outcomes, including legal violations, negative social impacts, environmental damage, consumer harm, and employee dissatisfaction. A recent study in the United States suggests that two-thirds of financial frauds go undetected. The authors quantify the pervasiveness of corporate fraud (including the share of undetected), indicating that financial misrepresentation and securities fraud in the US firms destroy approximately 1.6% of equity value ($830 billion in 2021) (Dyck et al., 2024).

Prior research on the antecedents of corporate misconduct is predominantly from the United States, which limits its generalisability to other jurisdictions. Meta-analyses suggest that the relationships between corporate governance and misconduct differ cross-nationally, despite similarities in the legal and institutional environments of countries (Neville et al., 2019; Paruchuri et al., 2024). Stakeholder influence, CEO compensation structures and employment contracts, executive talent market, tenure of leaders, and incentive structures are recognised as different in other jurisdictions from the US governance system (Hodne et al., 2013). The influence of any (dark or bright side) CEO characteristics on corporate misconduct is less understood in the Australian context (Shen, 2021). There is minimal research on corporate fraud in this context (a few exceptions include Capezio and Mavisakalyan, 2016; Chapple et al., 2014; Chapple and Tan, 2012; Sharma, 2004; Tan et al., 2017). The limited research on corporate misconduct in Australia may be attributed to the absence of publicly accessible, centralised data repositories, such as the Accounting and Auditing Enforcement Releases (AAER) available in the United States (Davidson, 2022).

Agency theory predominates research in corporate misconduct, although more recently the behavioural agency model posits that CEO risk preferences are driven by their perceptions of fairness (Jain et al., 2024). This article examines the potential relationship between CEOs’ moral values and corporate misconduct through the lenses of benevolent leadership theory and upper-echelon theory (UET). We expect that the ethical disposition of NFP CEOs, 1 recognised as benevolence in this study, will positively reflect in the firm’s decision-making and compliance culture, lowering the likelihood of misconduct. We hypothesise a negative association between NFP CEOs and misconduct. While this expectation is supported by the literature and intuition, a strong opposing narrative has also emerged from prior work, adding tension to this inquiry. Moral licensing theory suggests that engaging in ethical actions can lead to the subsequent acceptance of unethical actions by acquiring a moral licence (Bouzzine and Lueg, 2023; Safari, 2022). This suggests that NFP CEOs may be positively associated with the likelihood of corporate misconduct.

We follow prior literature in defining misconduct broadly as organisations’ behaviour that deceives or swindles, or negatively impacts shareholders or other stakeholders (Carberry et al., 2018; Conyon and He, 2016; Neville et al., 2019). We hand-collected data on NFP positions and corporate misconduct for ASX 300-listed firms from 2010 to 2019 and tested hypothesised associations using multivariate analyses. Our results support the competing hypothesis that NFP CEOs are positively associated with misconduct. However, the additional analysis reveals a non-linear relationship between NFP CEOs and misconduct, with the relationship becoming negative when CEOs hold four or more NFP positions.

Given the nuanced findings, we provided and tested several theoretical explanations. First, NFP CEOs are likely to have larger social networks through their service on NFPs, which can increase their decision-making power (Chahine et al., 2021) and busyness (Gray and Nowland, 2018). Powerful and/or busy CEOs may be less inclined to prioritise an ethical corporate culture and to implement strong internal controls because of their greater re-employability (Cingano and Rosolia, 2012). This proposition was tested in multiple ways, including the use of an additional CEO power and/or busyness proxy that could overlap with NFP CEOs (i.e. multiple corporate directorships). The results indicate that NFP CEOs and the most powerful CEOs in terms of networks are two distinct groups, thereby confirming that CEO power does not explain the relationship between NFP CEOs and misconduct.

Second, NFP CEOs are likely to prioritise stakeholder interests more (Feng et al., 2023), potentially creating a conflict of priorities between meeting shareholders’ and stakeholders’ interests. This could divert their focus from the strict enforcement of corporate governance policies and oversight that could prevent non-compliance. In addition, prior research suggests that individuals who have engaged in ethical actions may be more likely to act irresponsibly in the future, a phenomenon known as moral licensing (Bouzzine and Lueg, 2023). These arguments were tested by examining the associations between NFP CEOs, corporate social responsibility (CSR) performance, and corporate misconduct. The analysis suggests that CSR performance mediates the positive linear relationship between NFP CEOs and misconduct. This confirms our conjecture that excessive focus on serving stakeholders may either morally license unethical actions or distract from upholding effective governance. However, given that CEOs with four or more positions are negatively related to misconduct, moral licensing and/or conflicting priorities cannot fully explain the results. We contend that CEOs’ benevolence can manifest at varying levels depending on the intensity of their involvement in social causes through NFPs. Behavioural ethics research indicates that leaders who internalised moral values through extensive engagement in ethical actions are more likely to consistently apply moral reasoning to their decisions, avoiding moral licensing (Boegershausen et al., 2015; Brown and Treviño, 2006; Conway and Peetz, 2012). This means that NFP CEOs with more positions constitute a distinct, benevolent group in which moral consistency is more likely, allowing the negative influence of misconduct to be rationalised.

This research makes significant contributions to the literature. First, the study establishes a methodology for collecting data on corporate misconduct from publicly available sources. In the absence of an existing data repository on misconduct in the Australian context, our research offers methodological insights for future research. Second, this research contributes to the limited Australian misconduct literature, encouraging researchers to adopt such unobtrusive measures in examining misconduct (Chapple et al., 2014; Chapple and Tan, 2012; Tan et al., 2017). Third, corporate fraud studies often examine a single type of fraud (e.g. lawsuits, self-reported fraud) (Capezio and Mavisakalyan, 2016; Chapple et al., 2014). We contribute to the literature by defining a broad variable for corporate misconduct. Finally, we add to the limited literature investigating the influence of CEO/director bright-side characteristics (e.g. ethics) on corporate outcomes (Chapple et al., 2025; Feng et al., 2023; Weerasinghe et al., 2024).

The study’s findings offer valuable insights into corporate practices. Continuous updates on drivers and impediments to corporate misconduct are essential to pursuing avenues to prevent, detect, and deter unethical actions by firms. Our results will be insightful for firms in structuring corporate governance and leadership. Suppose a firm seeks a new CEO or directors to prevent or reduce its propensity for misconduct. The results suggest that NFP CEOs are generally unlikely to fulfil this objective unless their involvement in NFP positions is extensive (i.e. four or more positions). For firms prioritising CSR activities, the study’s results indicate that appointing NFP CEOs/directors may be beneficial; however, such engagement may lead to ineffective corporate governance and enforcement. Firms and advocates for ethical corporate cultures should be aware of this complication to avoid potential misevaluations. Finally, our results do not suggest that moral characteristics lead to adverse outcomes; instead, we provide evidence of the conditions under which NFP CEOs are effective in mitigating or driving misconduct. Thus, our results will be of interest to NFP leaders and firms seeking to understand the influence on corporate outcomes and misconduct, enabling them to pursue other avenues to fulfil their obligations (e.g. strengthening corporate governance, Carè and Fatima, 2024; or through compensation arrangements, Jain et al., 2024).

2. Literature review and hypothesis development

2.1. NFP CEOs and corporate misconduct: Main narrative

Adopting UET, the link between various CEO characteristics and corporate misconduct is well established; however, with a predominant focus on CEOs’ dark-side characteristics (Capalbo et al., 2018; Olsen and Stekelberg, 2016). The CEOs’ bright-side characteristics (e.g. benevolence, prosociality, altruism) have been examined to a lesser extent, primarily focusing on their influence on corporate ethical aspects. Studies in international contexts indicate that prosocial CEOs are associated with more employee-friendly policies, higher customer satisfaction, lower executive turnover, and higher CSR performance (Feng et al., 2023). Similarly, Liu et al. (2023) employed CEOs’ personal charitable donations as a proxy for prosocial behaviour to examine their influence on the cost of debt. Haynes et al. (2015) conceptualised the influence of altruistic managers on corporate long-term decisions and financial performance due to their concern for benefitting others. Berson et al. (2008) examined the associations between CEO values (self-direction, security, and benevolence) and organisational culture and outcomes, finding a positive association between benevolent CEOs and organisational supportive cultures (trustworthy and friendly environment). This body of empirical evidence indicates that CEOs with prosocial tendencies are likely to encourage actions benefitting the well-being of others (Liu et al., 2023).

Similar evidence exists in the Australian context, examining the link between the ethical characteristics of CEOs and directors (as recognised through their involvement in NFPs) and corporate ethical outcomes. More benevolent directors on boards are associated with higher environmental performance in Australian-listed firms (Chapple et al., 2025). Benevolent CEOs are positively related to corporate social performance (Weerasinghe et al., 2024). Building on these, we argue that NFP CEOs will consider others in their organisational decision-making and promote an ethical corporate culture.

The NFP CEOs are distinct from their counterparts who do not serve on NFPs for three leading reasons. First, by serving on NFPs, these CEOs who display virtuous behaviour are likely to have a higher ethical stance and are oriented to serve a wide range of stakeholders (Bekkers and Wiepking, 2011; Feng et al., 2023; Liu et al., 2023). Second, they are likely to be exposed to more significant ethical accountabilities and broader perspectives, as the operational objectives differ between for-profit and not-for-profit organisations (Ward and Miller-Stevens, 2021). Finally, with exposure to the values and ethics of other directors who primarily serve on NFPs, corporate CEOs are likely to develop positive personal values (social cohesion effect) (Fredette and Sessler, 2021). Due to the ethical stance, diverse perspectives, and exposure to higher accountabilities, NFP CEOs are a distinct group of CEOs from other CEOs who are employed only in the corporate sector.

This distinction is recognised as benevolent, aligning with the normative definition of indicating concern for others’ good and well-being (Steinbach et al., 2021) and the benevolent leadership model proposed by Karakas and Sarigollu (2012). The model suggests three dimensions of leaders’ benevolence: morality (ethics and values), community (contributions to society), and spirituality (positive influence on corporate culture) (Karakas and Sarigollu, 2012). The CEOs serving on NFPs commit “time” and “talent” to these organisations, 2 indicating a form of social activism and perceived benevolence. On one side, these CEOs have chosen to contribute to social causes by joining NFP organisations, suggesting a moral disposition. On the other hand, by serving on NFP boards, these CEOs are increasingly exposed to for-purpose accountabilities (Ward and Miller-Stevens, 2021). Relatedly, UET asserts that corporate outcomes reflect the characteristics of its top leaders (Hambrick and Mason, 1984). Empirical evidence supports UET, finding that the personal characteristics of CEOs and directors influence corporate misconduct (Carè and Fatima, 2024). Corporate leaders’ personal ethics are integrated into the organisational roles and culture, encouraging ethical practices and discouraging unethical practices, such as misconduct (Brown et al., 2005; Ho et al., 2015; Páez and Salgado, 2016; Zalata et al., 2022). Corporate compliance culture is nurtured by a code of conduct (Al-Okaily, 2024) and by the decisions and values of its leaders (Bridges, 2018); thus, the values of NFP CEOs are expected to be reflected in corporate decision-making and subsequent outcomes.

Corporate leaders’ benevolence is crucial in developing an ethical culture, ensuring the well-being of stakeholders (Karakas and Sarigollu, 2012). The CEOs who choose to serve on NFPs demonstrate a personal commitment to a sense of obligation towards society, thereby resonating with the notion of benevolence (Chapple et al., 2025). Relatedly, UET provides that leaders’ dispositions, cognitive biases, and personal experiences are integrated into corporate decision-making (Osei Bonsu et al., 2024). The personal ethics of corporate leaders promote an ethical corporate culture, discouraging unethical practices and reducing the likelihood of misconduct (Brown et al., 2005; Ho et al., 2015; Páez and Salgado, 2016; Zalata et al., 2022). From the perspectives of benevolent leadership and UET, we argue that NFP leaders are likely to act on their moral disposition when making corporate decisions and policies, thereby discouraging a culture of non-compliance. This leads to the following hypothesis:

Hypothesis 1A. NFP CEOs are negatively associated with the likelihood of corporate misconduct.

2.2. NFP CEOs and corporate misconduct: Opposing view

The discussion above suggests that increased corporate ethical activities may benefit stakeholders in firms managed by NFP CEOs. However, this phenomenon is complex, as several forces (linked to the CEO’s character) operate concurrently, influencing corporate culture and, consequently, the likelihood of misconduct. Thus, competing arguments can also be developed, creating tension within our research inquiry. By serving on NFPs, CEOs may expand social networks and decision-making power within firms. Strong social ties increase the likelihood of re-employment and provide a safety net for CEOs (Cingano and Rosolia, 2012), and enhance their influence in decision-making (Chahine et al., 2021; Khanna et al., 2015). Prior research indicates that CEOs’ discretionary power in corporate decision-making can increase the likelihood of misconduct (Altunbaş et al., 2018; Khanna et al., 2015). This means that powerful CEOs may focus less on nurturing an ethical culture and could weaken corporate governance mechanisms, thereby increasing the likelihood of misconduct (Pandey et al., 2026).

Relatedly, a higher inclination to serve stakeholders might lead to a conflict of priorities, resulting in the typical principal–agent problem (Jensen and Meckling, 1976). Due to exposure to societal issues through service in NFPs, NFP CEOs might prefer to meet stakeholder demands through corporate leadership (Weerasinghe et al., 2024). This means that these CEOs face the conundrum of prioritising shareholder interests versus stakeholder interests. This excessive attention to stakeholder needs may distract NFP CEOs from implementing and maintaining strict enforcement of corporate governance mechanisms. For instance, greater engagement in CSR initiatives to serve stakeholders requires the use of limited corporate resources, which could otherwise be allocated to internal governance functions. A lack of focus on corporate governance functions increases the likelihood of misconduct (Chapple et al., 2020). This view is supported by extant research indicating that misconduct is more prevalent in firms with higher CSR performance (Bouzzine and Lueg, 2023). Thus, this alternate perspective suggests that NFP CEOs could be positively associated with the likelihood of corporate misconduct.

Another leading view is moral licensing, which posits that people who have engaged in ethical behaviour in the past may act irresponsibly in the future (Bouzzine and Lueg, 2023). This means that by engaging in ethical actions in their personal life by serving on NFPs, CEOs may feel licensed to ignore or be less attentive to governance mechanisms in setting an ethical firm culture, thus leading to higher misconduct. Similar to the contention of conflicting priorities, moral licensing theory explains the possibility that NFP CEOs are positively associated with the likelihood of misconduct, leading to the development of the competing hypothesis:

Hypothesis 1B. NFP CEOs are positively associated with the likelihood of corporate misconduct.

2.3. NFP CEOs and NFP boards

Boards of directors are the primary internal corporate governance mechanisms for ensuring that management decisions are made and monitored. While the key decisions are at the discretion of CEOs, boards are responsible for advising and monitoring management actions, ensuring shareholders’ and other stakeholders’ preferences are upheld. Prior literature indicates nuanced dynamic relationships between CEO and board characteristics in corporate strategic decisions. Studies indicate corporate leaders’ social homogeneity, known as “homophily,” could be beneficial or detrimental to firms (Perchard and MacKenzie, 2021). Homophily is recognised as a basis for forming social ties between leaders with similar social attributes, thereby shaping group dynamics and performance (Alzayed et al., 2024; Riordan and Shore, 1997). The implications of such homophily between board members and CEO–board members is mixed. Political homophily (sharing similar political views) between CEOs and directors facilitates CEOs’ communication of adverse information to boards (Dasgupta et al., 2021). Female CEOs and board gender diversity interact positively in information sharing and knowledge expansion, which helps overcome systemic biases and leads to higher environmental performance (Birindelli et al., 2019).

In contrast, Liu (2018) indicated that female CEOs reduce environmental lawsuits in firms with low board gender diversity. Similarly, high board gender diversity reduces the incidence of lawsuits when male CEOs manage firms. This finding contradicts the positive impact of homophily and suggests that the interaction between homogeneous leaders may be complementary. As Liu (2018) suggested, the ethical values of female leaders (either CEOs or directors) are pronounced in the absence of such characteristics in leadership. To this end, CEOs and directors serving on NFP leadership indicate homophily in perceived benevolence; however, their interactions in influencing corporate culture may be complementary or supplementary. The NFP boards can either strengthen or weaken the relationship between NFP CEOs and misconduct, depending on whether homophily effects hold for benevolent CEOs and directors. Given this contingency, we hypothesise the role of NFP boards reflecting both narratives as follows:

Hypothesis 2A. The association between NFP CEOs and corporate misconduct is strengthened by NFP boards.

Hypothesis 2B. The association between NFP CEOs and corporate misconduct is weakened by NFP boards.

3. Data and methodology

3.1. Sample selection

Our sample is ASX 300-listed firms from 2010 to 2019. We use the 2020 ASX 300 firm list as the base year. The final sample comprises 1029 firm–year observations after merging all variables, excluding financial firms (due to differing reporting and regulatory environments) and firms with missing data.

3.2. Empirical models and variables

To test H1 and H2, we run binary logit regressions (BLR) and zero-inflated negative binomial (ZINB) regressions using the following econometric model. This model is modified to include the interaction term in testing H2. All variable definitions are provided in Appendix 1 and discussed below. The association between NFP CEOs and misconduct may exist in reverse causation. All explanatory variables are lagged by one year (t-1) to reduce reverse causality concerns. However, we acknowledge that lagging does not fully eliminate the threat of reverse causality, and we employ additional robustness checks in Section 4.3 to validate the results.

Equation (1) assesses the association between NFP CEOs and corporate misconduct.

3.2.1. Corporate misconduct

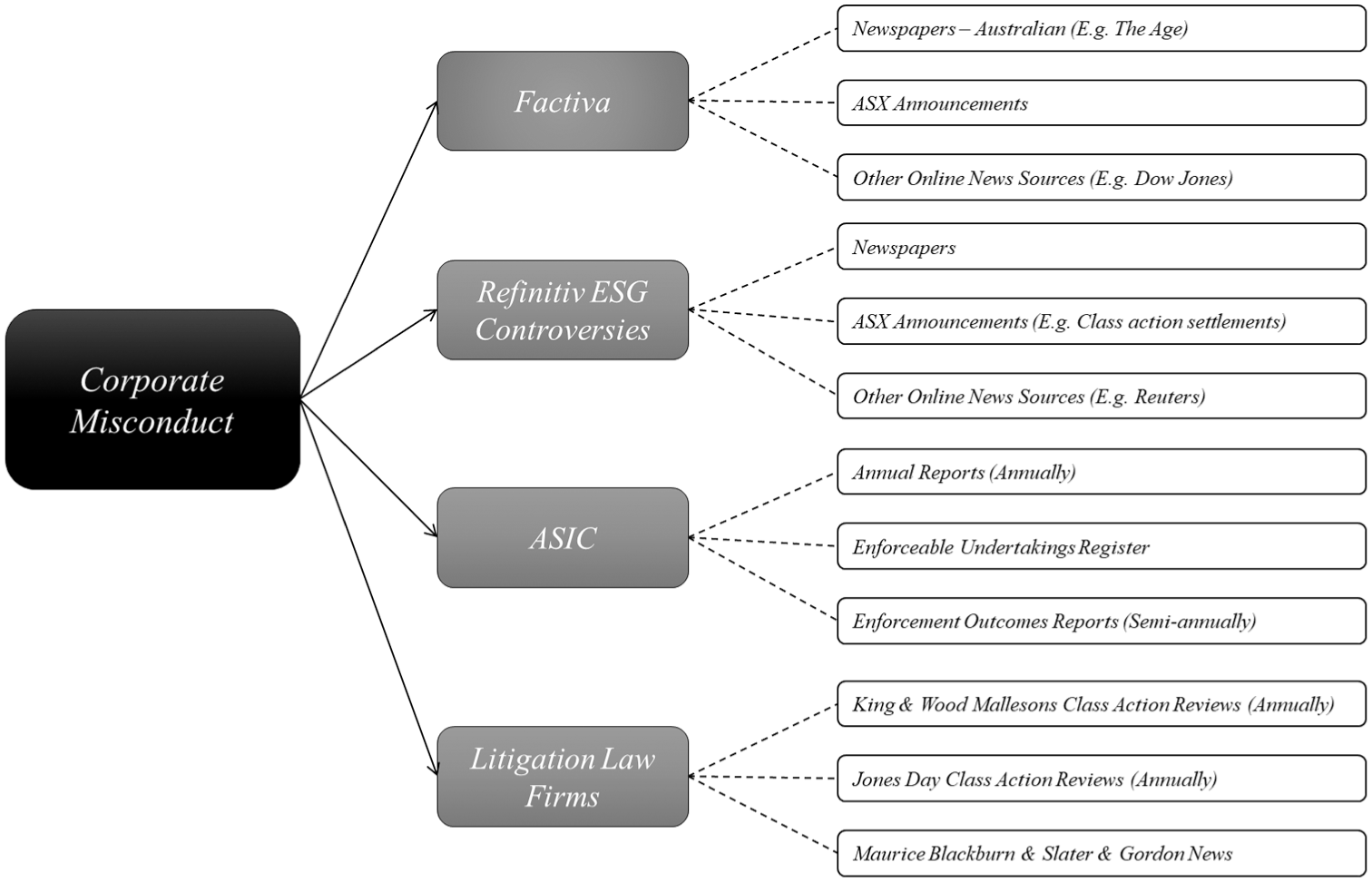

Misconduct is any behaviour of organisations that deceives, swindles, or negatively impacts shareholders or other stakeholders (Carberry et al., 2018; Conyon and He, 2016). Misconduct includes, but is not limited to, accounting fraud, tax fraud, corruption, human rights violations, discrimination, pollution, cartels, and negative actions towards Indigenous communities or other minorities. Using key term searches, a hand-collected dataset is created by identifying the corporate misconduct reported in the press (electronic newspapers) for the sample period. The primary electronic press sources were accessed via the Factiva database. The identified misconduct data are then corroborated by three additional sources: Australian Securities and Investments Commission (ASIC) regulatory reports, class action reviews by litigation law firms, and Refinitiv Environmental, Social, and Governance (ESG) controversies (Figure 1). Similar or identical news sources have been previously used in governance research to identify misconduct (Carberry et al., 2018; Chapple et al., 2014). Our misconduct measure encompasses a broad range of misconduct reported in the news media, regardless of the severity of the event. The ESG rating institutions, such as Refinitiv, provide a score for ESG controversies based on news media coverage and capture 23 ESG-related issues (Agnese et al., 2023). However, these ratings are based on the extent to which news is reported in global media; thus, they may be subject to selection bias, potentially resulting in underdetection of events (Barkemeyer et al., 2023). Therefore, while we use Refinitive ESG controversies to corroborate our hand-collected data, these are not used as the primary source.

Sources of misconduct identification.

What is unethical can be subjective depending on different perspectives; however, research indicates that investors and other stakeholders react to news of organisational misconduct (Carberry et al., 2018; Dai et al., 2015). As a global example, Volkswagen’s stock price plummeted by 30% in the week the media reported the emissions scandal (Carberry et al., 2018; Topham, 2015 ). Dai et al. (2015) revealed that media plays a role in corporate governance by disseminating news, resulting in litigation risk concerns, reducing information asymmetry, and influencing insiders’ wealth and reputation. Further, misconduct is not always illegal; however, it often results in negative consequences for stakeholders, firms, and society. The recent Rio Tinto incident is an example of cultural vandalism in destroying an Indigenous sacred site, indicating the pervasiveness of unethical corporate actions, attracting significant reputational damage for the firm and its leaders and irreversible damage to Indigenous heritage (Saldanha, 2020). Despite this, Rio Tinto’s action was legal (Saldanha, 2020).

We examine the continuum of corporate misconduct from legal to illegal to unethical actions. While corporate actions such as the Volkswagen scandal are both unethical and unlawful, Rio Tinto’s incident lies in the legal but unethical realm of the continuum, and we recognise both events as examples of misconduct. Regulators do not enforce legal yet unethical events through legal proceedings. Thus, we recognise the role of media in disclosing unethical events of organisations and rely on negative news to capture corporate misconduct. We do not attribute corporate misconduct to management’s intention to engage in unethical actions, as misconduct is a consequence of a non-compliant corporate culture (Carberry et al., 2018) within organisations; thus, management intentions are irrelevant.

3.2.2. NFP CEOs and NFP boards

The NFP CEOs and boards are recognised through involvement in NFP leadership positions. Data are hand-collected by accessing biographies of CEOs/directors from annual reports and company official websites, following Weerasinghe et al. (2024). Keyword 3 searches are conducted in annual reports using the Connect4 database, and CEO/directors’ biographies are manually read to identify possible NFP positions. 4 All biographies are read twice to ensure that no positions are overlooked. The possible NFP list is then used to identify and verify NFP status through a detailed search of the Australian Business Number (ABN), the Australian Charities and Not-For-Profit Commission (ACNC), ASIC, and organisational websites. The NFP CEOs is a count variable representing the number of NFP positions a CEO holds in a year. The NFP boards is the percentage of the board serving in NFP leadership positions.

3.2.3. Control variables

Control variables are categorised into three broad levels: firm-level variables related to misconduct, CEO-level variables, and corporate governance variables. Firm-level variables include return on equity, firm size, firm age, capital expenditure, leverage, the market-to-book value of equity, and cash holdings (Biggerstaff et al., 2015; Capalbo et al., 2018; Chapple et al., 2014). The CEO characteristics include tenure, duality, and gender (Biggerstaff et al., 2015; Burns and Kedia, 2006; Khanna et al., 2015). Corporate governance variables include board size, % of independent directors, number of board meetings per financial year, % of independent directors on the audit committee, and board gender diversity. To assess the strength of external monitoring, we use the ownership concentration of institutional investors (Biggerstaff et al., 2015; Khanna et al., 2015), and the auditor type (Big4 or not). These variables have been consistently shown in the literature to be associated with corporate misconduct. All our empirical tests include industry and year fixed effects.

4. Empirical results

4.1. Summary statistics

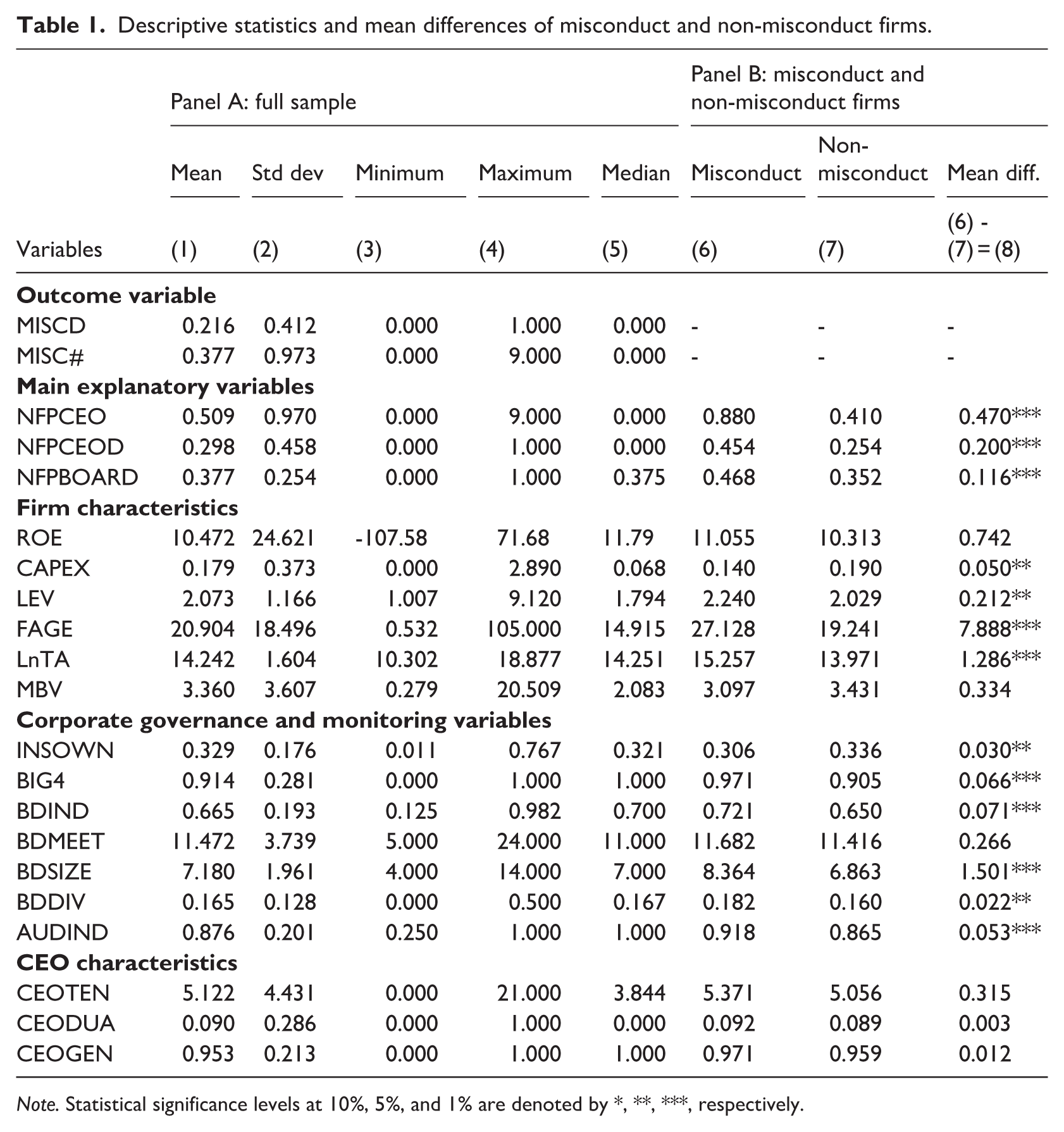

Table 1 reports descriptive statistics for the variables used in the study, including statistical differences between the misconduct firms and the non-misconduct sample. This table indicates that corporate misconduct (MISC#) ranges from 0 to 9 events with a mean of 0.377. The NFP CEO variable ranges from 0 to 9, with an average of 0.509. The dummy NFP CEO variable indicates a mean of 0.298, suggesting that CEOs with NFP positions manage 30% of firms. On average, directors with NFP positions comprise 38% of boards. The NFP CEOs and NFP boards exhibit significant mean differences at the 1% level (0.470*** and 0.116***) between the sample groups of firms with and without misconduct. At the preliminary level of analysis, this indicates that NFP CEOs are likely to be associated with misconduct. Concerning the direction of the relationship, the misconduct firm sample has higher mean values of both variables than the non-misconduct firm sample, suggesting a positive association between NFP CEOs and misconduct. In terms of firm characteristics, capital expenditure, leverage, firm age, and total assets exhibit significant differences in means between the sample groups. On the other hand, the return on equity and market-to-book value variables do not show significant differences in means, suggesting they are unlikely to be related to misconduct. Regarding corporate governance and monitoring variables, all variables exhibit significant mean differences between misconduct firm groups, except for the number of board meetings.

Descriptive statistics and mean differences of misconduct and non-misconduct firms.

Note. Statistical significance levels at 10%, 5%, and 1% are denoted by *, **, ***, respectively.

We examine Pearson correlations of the variables in unreported results. Most correlations are low to moderate (below 0.5), except between board size and firm size (0.652***), and between board independence and audit committee independence (0.675***). Variance inflation factors (VIFs) and tolerances were examined, finding that VIFs were below 3 and tolerances were above 0.3, indicating no threat of multicollinearity (Tabachnick et al., 2013).

4.2. Hypothesis testing

Two regression techniques are employed to examine the hypothesised associations: BLR and ZINB regressions. The dependent (misconduct) variable is presented as a binary variable (MISCD) in BLR. The misconduct count variable (MISC#) ranges from 0 to 11 with a non-parametric zero-inflated right-skewed distribution. Thus, ZINB is the most appropriate method for the nature of the MISC# variable (Lambert, 1992; Motalebi et al., 2023). The ZINB assumes that the data arise from two distribution sets, where structural zeros are from a binary distribution and non-negative outcomes are from a count distribution.

4.2.1. NFP CEOs and corporate misconduct

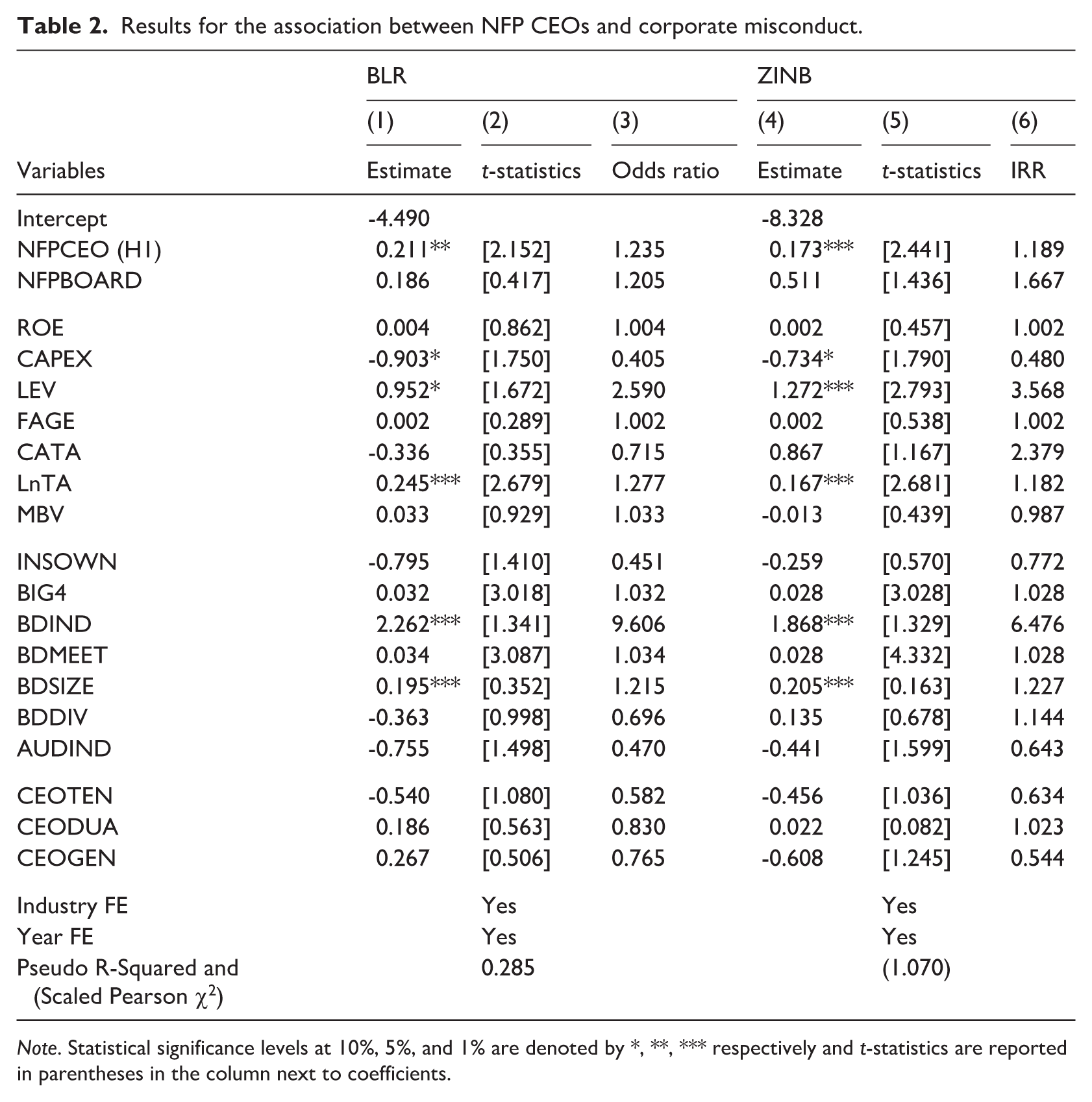

Table 2 reports the regression results for H1. Columns (1) to (3) present the BLR results with coefficients, t-statistics, and exponential coefficients (odds ratios) (Lemeshow et al., 2013; Osborne, 2016) and columns (4) to (6) present the ZINB regression results. Exponential figures are essential for assessing the strength of the associations, and coefficients provide the direction of the associations.

Results for the association between NFP CEOs and corporate misconduct.

Note. Statistical significance levels at 10%, 5%, and 1% are denoted by *, **, *** respectively and t-statistics are reported in parentheses in the column next to coefficients.

In the BLR model, NFP CEOs have a significant positive association with corporate misconduct (β = 0.211, p < 0.05), with an odds ratio of 1.235. This suggests that, controlling for other covariates, the odds of a firm being a misconduct firm are 23.5% higher in firms managed by NFP CEOs. These findings support the opposite narrative (H1B). In this regression, the NFP boards variable is insignificant, indicating no association with the likelihood of a firm being a misconduct firm. Several control variables indicate associations with the likelihood of misconduct. Among the firm characteristics, capital expenditure, leverage, and firm size (LnTA) exhibit significant positive coefficient estimates. Board independence and size are also significant and positively associated with misconduct. Conceptually, although board independence and size are intended to enhance monitoring and governance, thereby reducing the likelihood of misconduct, our results suggest otherwise. The CEO tenure, gender, and duality variables are insignificant.

The ZINB regression indicates similar results. The NFP CEOs are significantly and positively associated with corporate misconduct (β = 0.173, p < 0.05), supporting H1B, with an IRR of 1.189. The NFP boards are not associated with misconduct. Regarding firm characteristics, the results indicate that firm size and leverage are positively associated with the likelihood of misconduct. In contrast, firm capital expenditure is negatively related to the likelihood of misconduct events. Return on equity, firm age, cash holdings, and market-to-book values are not significant, indicating no association with misconduct. Of the governance and monitoring variables, board size and board independence are positively associated with misconduct. Board gender diversity, Big 4 auditors, and audit committee independence are non-significant. None of the three CEO characteristics are significant, indicating no association with misconduct. These associations are partially consistent with the literature on misconduct. For example, the positive link between firm size and misconduct is consistent with Capezio and Mavisakalyan (2016); Chahine et al. (2021); Khanna et al. (2015); Kim et al. (2022), and Malm et al. (2021), the leverage result with Biggerstaff et al. (2015) and Khanna et al. (2015).

The results of the baseline regressions support H1B and do not support H1A, indicating a significant positive association between NFP CEOs and corporate misconduct. Firms with NFP CEOs are more likely to have misconduct than their counterparts, supporting the opposite narrative discussed in Section 2.2. Potential explanations for these results are discussed in Section 4.4.

4.2.2. Moderating role of NFP boards

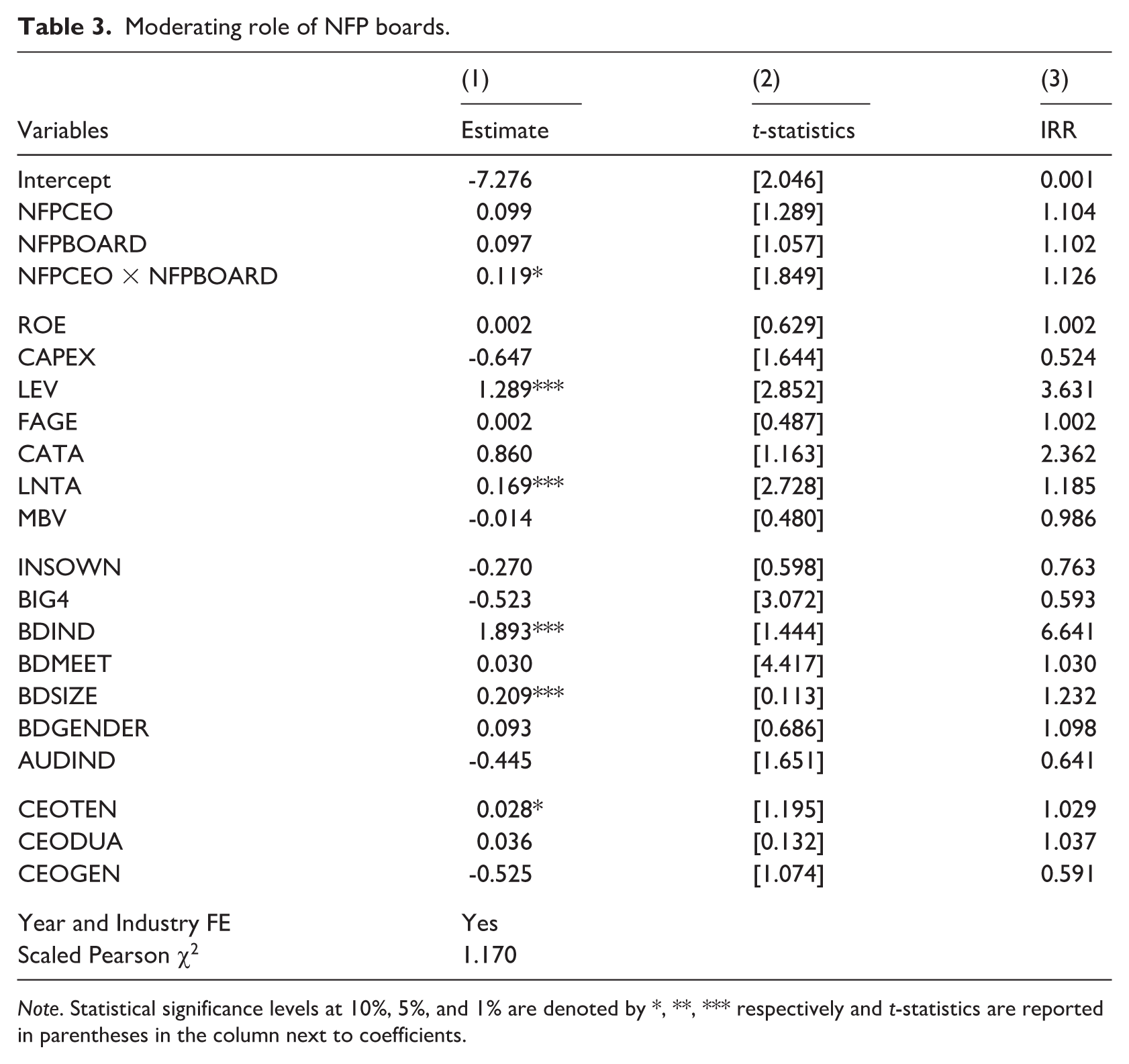

Table 3 reports the ZINB regression results of H2. The results indicate that the interaction term (NFPCEO × NFPBOARD) has a significant positive association with misconduct (β = 0.119, p < 0.10), aligning with H2A. This suggests that having more NFP directors on boards increases the likelihood of misconduct in firms managed by NFP CEOs. The result is contradictory regarding the positive effect of social homophily and consistent with the negative consequences of having homogeneous CEOs and directors in leadership (Liu, 2018).

Moderating role of NFP boards.

Note. Statistical significance levels at 10%, 5%, and 1% are denoted by *, **, *** respectively and t-statistics are reported in parentheses in the column next to coefficients.

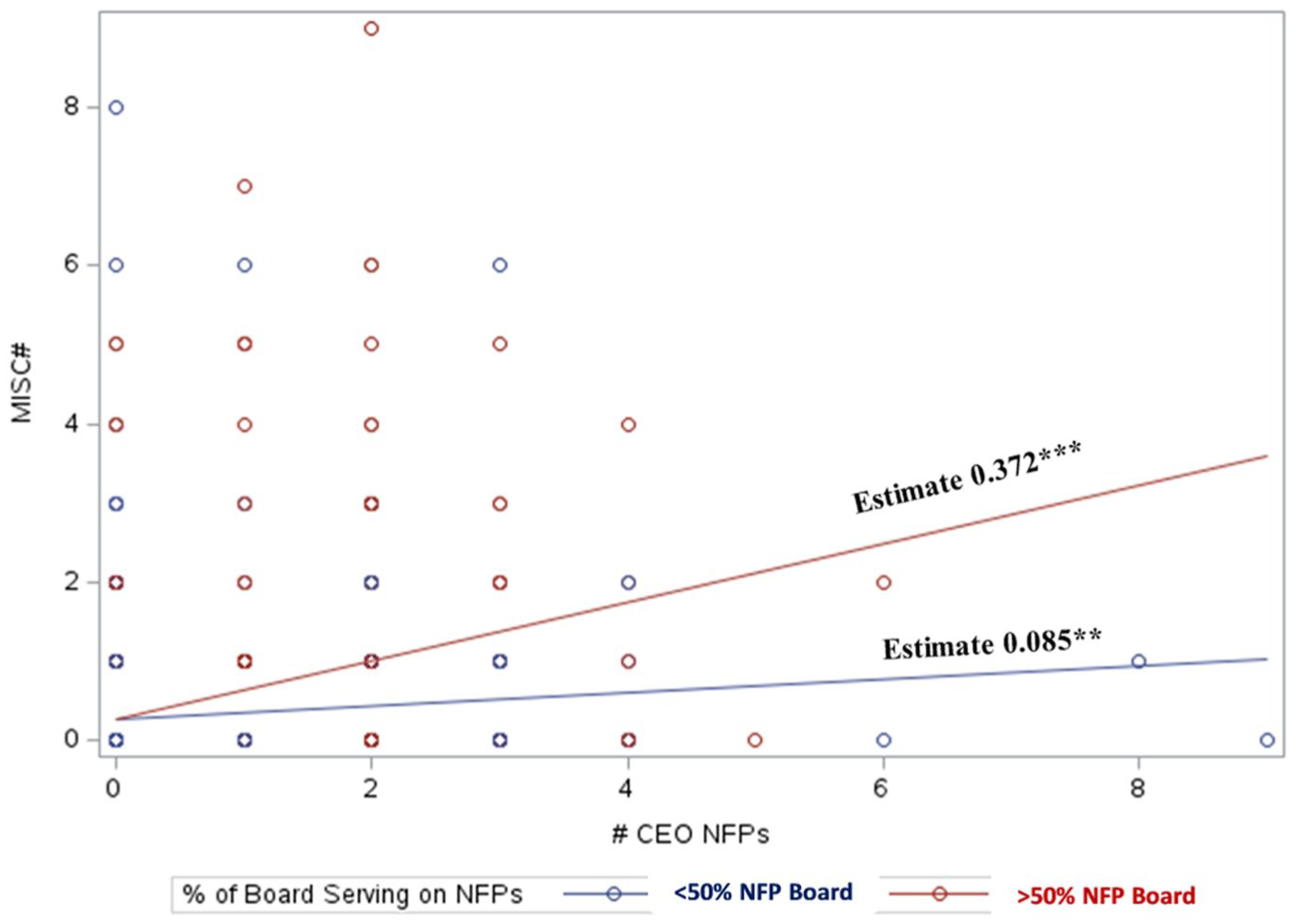

To test the form of this amplifying effect, the association between NFP CEOs and boards, and misconduct is charted (Figure 2). Misconduct and NFP CEOs are presented as count variables, and NFP boards are categorised under two levels: <50% and >50% of the board serving on NFPs. As expected, the interaction plot indicates a positive interaction effect. Both levels of NFP boards moderate the association between NFP CEOs and misconduct, and this influence is significantly more substantial when NFP boards comprise more than 50% of the board (slope = 0.372***).

The interaction between NFP CEOs and NFP boards.

4.3. Robustness tests

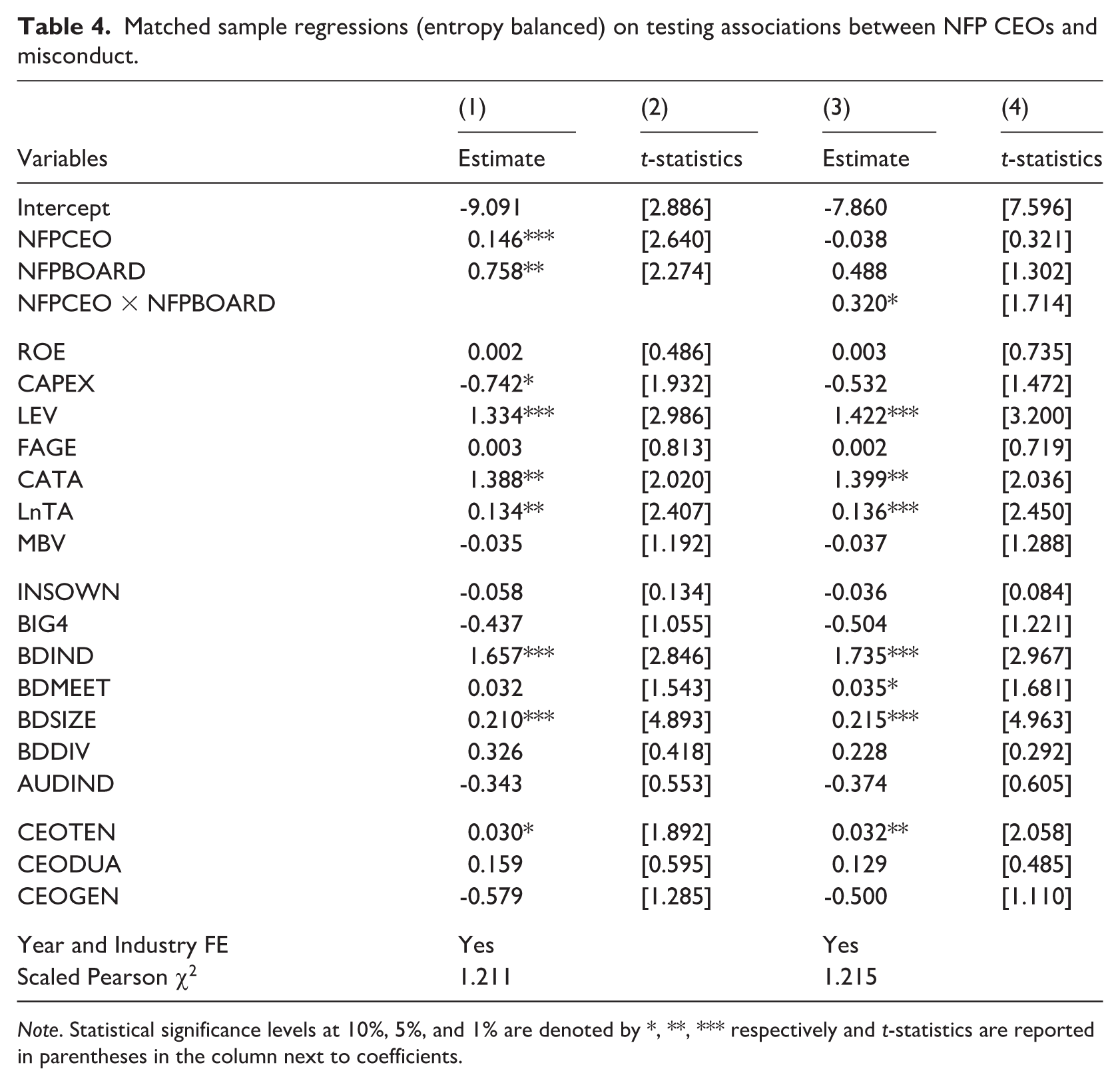

To validate our findings, we employ a robust multivariate matching technique, entropy balancing (Hainmueller, 2012). The entropy balancing method is used in recent research to assess the robustness of regression findings, in conjunction with propensity score matching (PSM) (Bhandari and Golden, 2021). We used covariates that were significantly correlated with the dependent variable (DV, NFP CEOs) in entropy-weighted estimation. The matching was performed using the binary form of NFP CEOs as the DV, equalling 1 if the firm’s CEO is an NFP CEO and 0 otherwise (non-NFP CEO), and all other relevant variables as explanatory variables. The resulting entropy-weighted sample was then used to conduct ZINB analysis. Entropy balancing produced a sample with zero mean differences between the two groups, indicating less bias. Table 4 reports the post-entropy weighting regression results. The regression results for the entropy-weighted sample remain unchanged from those for the baseline, with a significant positive association between NFP CEOs and misconduct (β = 0.146, p < 0.01) and a positive interaction effect between CEO and NFP boards (β = 0.321, p < 0.05). In unreported testing, we also employed a PSM approach to generate a matched sample and performed regressions using the PSM sample; the results remain consistent.

Matched sample regressions (entropy balanced) on testing associations between NFP CEOs and misconduct.

Note. Statistical significance levels at 10%, 5%, and 1% are denoted by *, **, *** respectively and t-statistics are reported in parentheses in the column next to coefficients.

4.4. Discussion and additional analyses

The results support the opposite narrative outlined in Section 2.2. However, before examining alternative explanations further, we first investigate whether the results are robust to a possible non-linear relationship between NFP CEOs and misconduct.

4.4.1. Is there a non-linear relationship between NFP CEOs and misconduct?

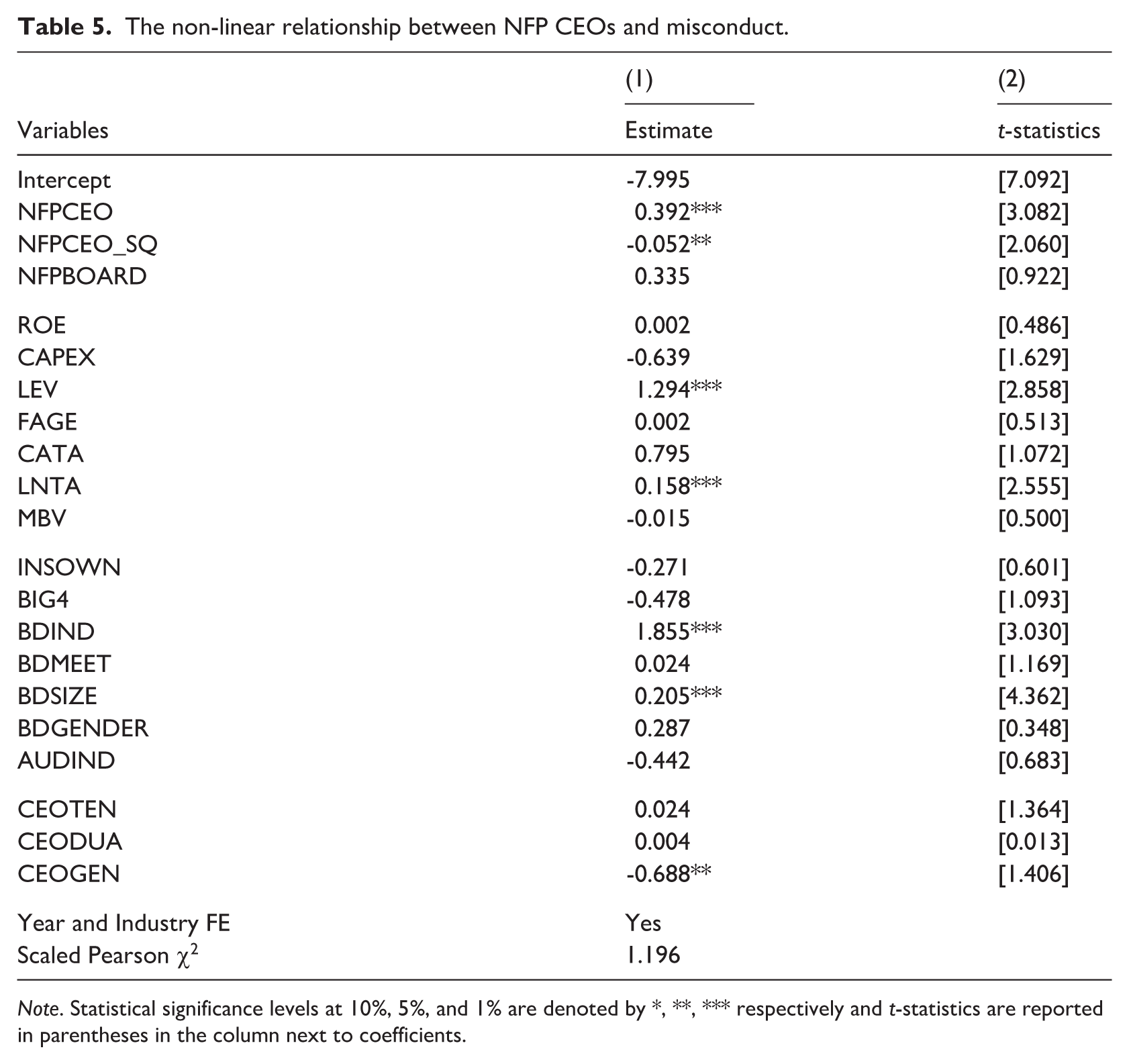

Our prior regressions indicate a positive relationship between NFP CEOs and corporate misconduct; however, the assumption is that this relationship is linear. Prior research in corporate governance and management indicates the possibility of non-linear relationships between corporate leadership and outcomes (Ntim, 2015). Given the range of NFP positions held by the CEOs (from 0 to 9), a non-linear influence on misconduct is possible. In other words, the number of NFP positions of CEOs may differently influence the likelihood of misconduct. To test this, we include a squared term of NFP CEOs (NFPCEO_SQ) in the model when performing the ZINB regression, following prior research (Ntim, 2015; Roberson and Park, 2007).

The results indicate that the squared NFP CEO variable has a significant negative relationship with misconduct, whereas NFP CEOs exhibit a positive relationship (β = -0.052, p < 0.05, Table 5). This suggests a non-linear relationship (i.e. an inverted U-shaped) between NFP CEOs and misconduct. The non-linear threshold point is computed by dividing the linear coefficient for NFP CEOs (= 0.392) by twice the non-linear coefficient (= 0.052 × 2), yielding a value of 3.76 (Kusi, 2025). This means that CEOs with fewer than four NFP positions are more likely to engage in misconduct. However, CEOs with four or more NFP positions are associated with a decreased likelihood of misconduct. Notably, this nuanced effect before and after the threshold point is consistent with both H1A and H1B. However, across all cases, the overall effect is that NFP positions at all levels remain positively related to misconduct.

The non-linear relationship between NFP CEOs and misconduct.

Note. Statistical significance levels at 10%, 5%, and 1% are denoted by *, **, *** respectively and t-statistics are reported in parentheses in the column next to coefficients.

While CEOs with four or more NFP positions are negatively associated with misconduct, the full sample results (due to the influence of NFP CEOs with less than four positions) remain positively associated with misconduct, which warrants explanation. Thus, we expand on and test the arguments for the opposing narrative presented in Section 2.2. These explanations support a positive association between NFP CEOs and misconduct and include CEO power and busyness, conflicting priorities, and moral licensing.

4.4.2. Are NFP CEOs the most powerful or busy CEOs?

Beyond perceived benevolence, CEOs serving on NFPs may also experience increased power, reputation, and busyness. The CEOs may be more socially connected with other directors through NFP positions. Access to external social ties through serving on NFPs may provide CEOs with greater discretionary power in their corporate decision-making (Chahine et al., 2021; Khanna et al., 2015), provide a safety net, and increase the likelihood of re-employment (Cingano and Rosolia, 2012). Research indicates that increased CEO power increases the likelihood of corporate misconduct (Altunbaş et al., 2018; Chahine et al., 2021; Khanna et al., 2015). Relatedly, serving on NFPs may also enhance CEOs’ reputations, which may not necessarily help prevent misconduct. For instance, prior research finds that award-winning or “superstar” CEOs subsequently underperform their peers and spend more time on public and private activities outside the firm (Malmendier and Tate, 2009; Wade et al., 2006). Award-winning CEOs are more likely to engage in financial misconduct after receiving media attention and being perceived as the best leaders (Li et al., 2022).

Another possibility is the busyness of CEOs due to the increased duties and responsibilities of serving in multiple leadership roles (Gray and Nowland, 2018), which may result in less efficient enforcement of corporate governance mechanisms within the organisations they manage. Evidence suggests that busy CEOs and directors are associated with increased corporate earnings management (Ferris and Liao, 2019). Thus, in theory, any of these functions can increase the likelihood of misconduct.

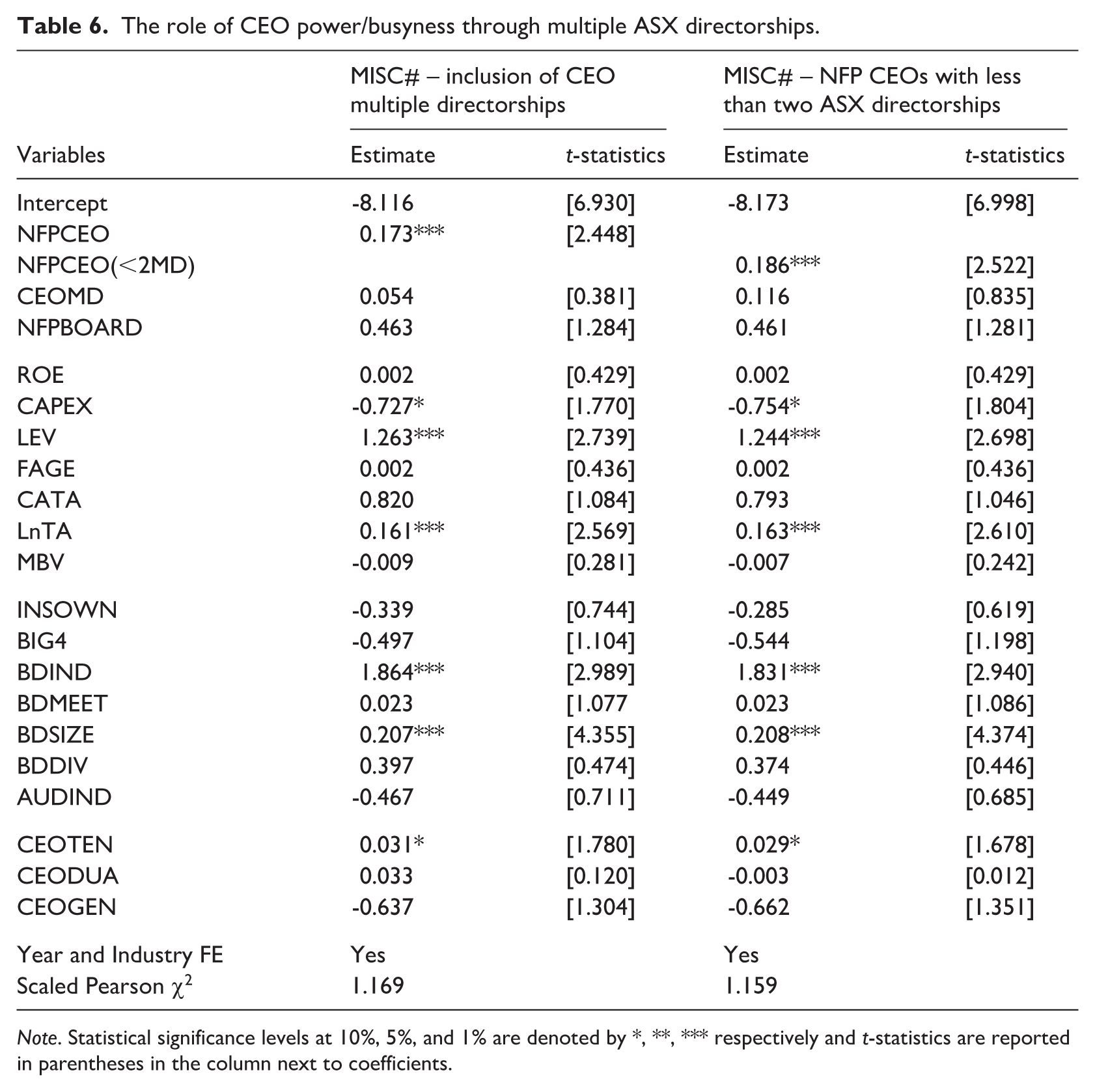

If our results are driven by power or busyness, NFP CEOs should be among the most powerful or busiest CEOs within the sample firms (e.g. those with the most extensive networks). The CEO power can be proxied through multiple indicators, such as the CEO’s tenure in the position, dual role as the CEO and chair of the board, compensation, and external networks (Bachmann et al., 2020; Chahine et al., 2021). The baseline analysis included two of these power proxies, duality and tenure; however, these two are less likely to overlap with NFP CEOs, given that NFP CEOs are recognised for their external work with NFPs. As an additional proxy, and one that can overlap with NFP CEOs, we used CEOs’ multiple ASX corporate leadership positions. Multiple corporate directorships serve as an established proxy for CEO busyness and power due to workloads and external social ties, respectively (Chahine et al., 2021; Khanna et al., 2015)

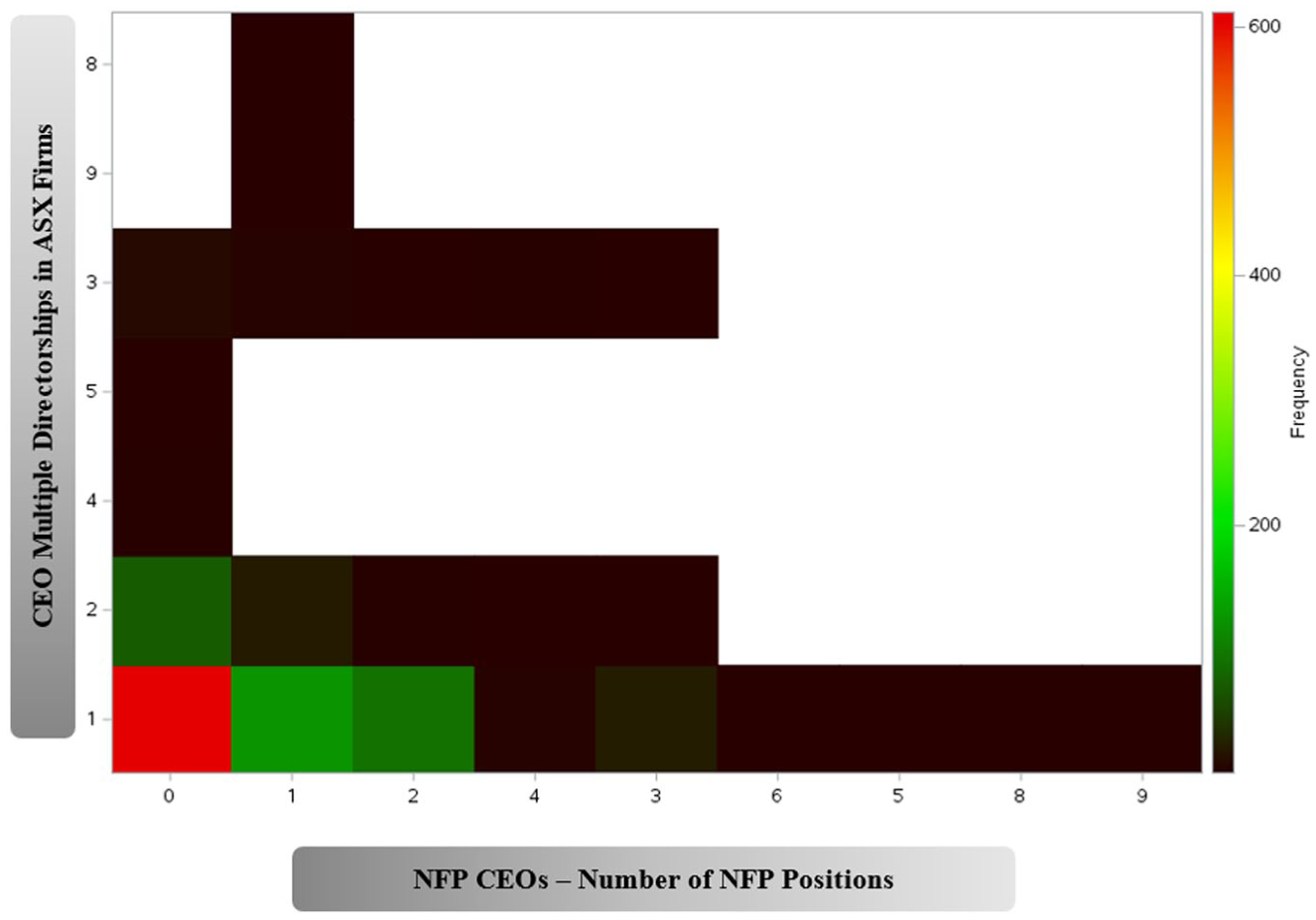

If power or busyness drives the results, we expect substantial overlap between NFP CEOs and the multiple ASX directorships. The aim is to determine whether these NFP CEOs are the most powerful and busiest within the sample, based on their external connections and workload. Figure 3 presents a heat map of NFP CEOs across multiple ASX directorships. The black colour represents the lowest frequency reported; green, the second-lowest; yellow, the second-highest; and red, the highest. The highest frequency, red, is reported with one listed firm directorship and zero NFP positions. Other directorships in listed firms, ranging from three to nine, are only evident in zero and one NFP positions. When the number of NFPs increases, there is no evidence of more than two other directorships in ASX-listed firms. Thus, the results indicate that the most networked CEOs in the sample and NFP CEOs form two distinct groups, suggesting that the NFP CEOs are not the most powerful group of CEOs.

Heat map representing the link between NFP CEOs and multiple directorships.

Next, we include the CEO’s multiple directorships (CEOMD) as a control in the model and re-perform the analysis, finding that our previous results remain unchanged and the new variable is insignificant (β = 0.054, p > 0.10, Table 6). In addition, to isolate the effect of NFP CEOs, we created another variable that included only NFP CEOs with two or fewer ASX directorships (NFPCEO < 2MD) and re-examined the relationships, ensuring power and benevolence do not overlap. The results remain consistent, indicating a positive association between NFP CEOs and misconduct. Thus, we find no evidence that CEO power and/or busyness helps explain the positive relationship between NFP CEOs and corporate misconduct.

The role of CEO power/busyness through multiple ASX directorships.

Note. Statistical significance levels at 10%, 5%, and 1% are denoted by *, **, *** respectively and t-statistics are reported in parentheses in the column next to coefficients.

It is important to note that the additional tests of CEO power and busyness align with the non-linear results. The original linear result is that NFP CEOs are positively associated with the likelihood of corporate misconduct (i.e. supporting the opposite narrative). The non-linear results indicate that NFP CEOs with four or more positions are associated with a lower likelihood of misconduct (i.e. supporting the main narrative). One could argue that CEOs’ power and busyness increase with the number of NFP positions, thereby increasing the likelihood of misconduct. However, this is valid only if the CEO’s power and busyness can explain the positive association between NFP CEOs and misconduct. The above analysis confirms that NFP CEOs constitute a distinct group with fewer ASX directorships, suggesting that NFP CEOs are neither the most powerful nor the busiest in terms of multiple directorships. Thus, the positive association between NFP CEOs and misconduct cannot be explained by CEO power or busyness. The fact that the results are not driven by CEOs’ power and busyness is consistent with the non-linear positive association between NFP CEOs with four or more positions and misconduct.

4.4.3. Do firms with NFP CEOs have higher CSR and misconduct?

The second argument stems from the conflict of priorities hypothesis. The NFP CEOs are more likely to focus on serving a wide range of stakeholders, resulting in higher attention to CSR activities than their counterparts. Excessive attention to stakeholders over shareholders (referred to as the conflicting interest proposition) may create typical agency problems and potentially lead to inefficiencies in mainstream business focus, decision-making, strict enforcement of governance, and internal controls. Finally, engaging in NFP roles may lead CEOs to feel morally licensed, making them less responsible in establishing an ethical corporate culture. These complexities (conflicting priorities and moral licence) may distract from or lead to the ignoring of their governance role in firms, which is essential to maintaining an ethically compliant culture. If this argument is valid, firms managed by NFP CEOs should exhibit higher CSR performance and higher rates of misconduct.

Regarding recent empirical evidence, Weerasinghe et al. (2024) found that CEOs serving in NFPs increase corporate social performance. Chapple et al. (2025) indicated that benevolent directors on boards enhance corporate environmental performance. Bouzzine and Lueg’s (2023) found that misconduct is higher in firms with higher CSR engagements, suggesting that firms might use past CSR performance as a moral licence to foster a corporate misconduct environment. Although engaging in more CSR activities undoubtedly serves stakeholders, it is unclear whether such activities ultimately produce benefits or drawbacks for firms. It is also an unresolved phenomenon in the literature whether CSR engagement is an indicator of good governance or merely a result of a manager’s self-interest motives (Gillan et al., 2021). These findings offer insights into our puzzle and suggest that NFP CEOs may increase the likelihood of misconduct and CSR performance, aligning with our moral licensing and conflicting priorities proposition.

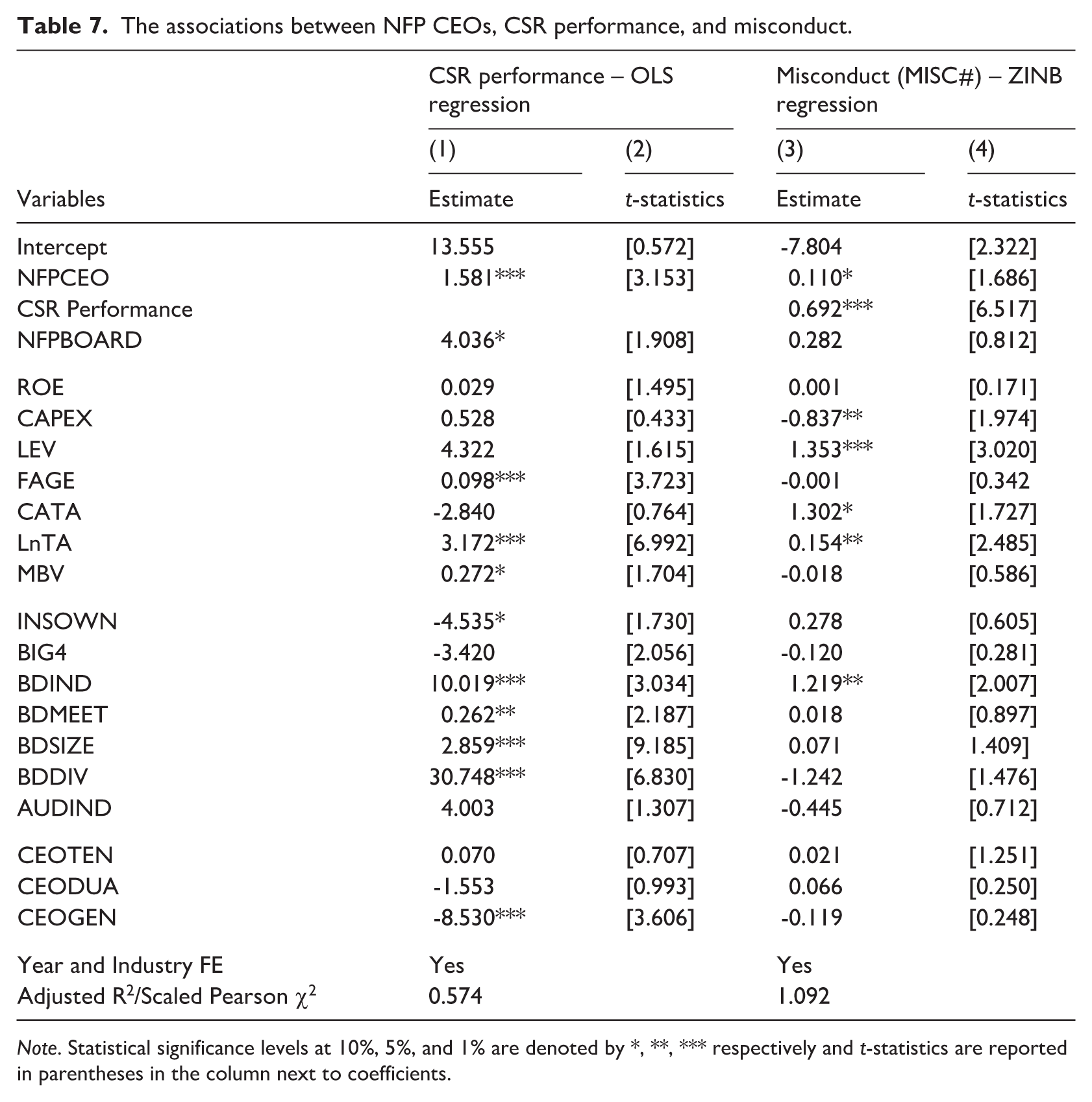

To test whether our conjectures are valid, we test the associations between NFP CEOs and CSR performance and misconduct. We use Refinitiv ESG scores as a proxy for CSR performance. This measure represents corporate performance scores related to ESG aspects encompassing more than 400 metrics (Ehlers et al., 2023). We obtain the Refinitiv ESG scores, excluding ESG controversies (not the combined score), to avoid potential overlap between CSR and misconduct measures, as the misconduct measure includes controversies. The results are reported in Table 7.

The associations between NFP CEOs, CSR performance, and misconduct.

Note. Statistical significance levels at 10%, 5%, and 1% are denoted by *, **, *** respectively and t-statistics are reported in parentheses in the column next to coefficients.

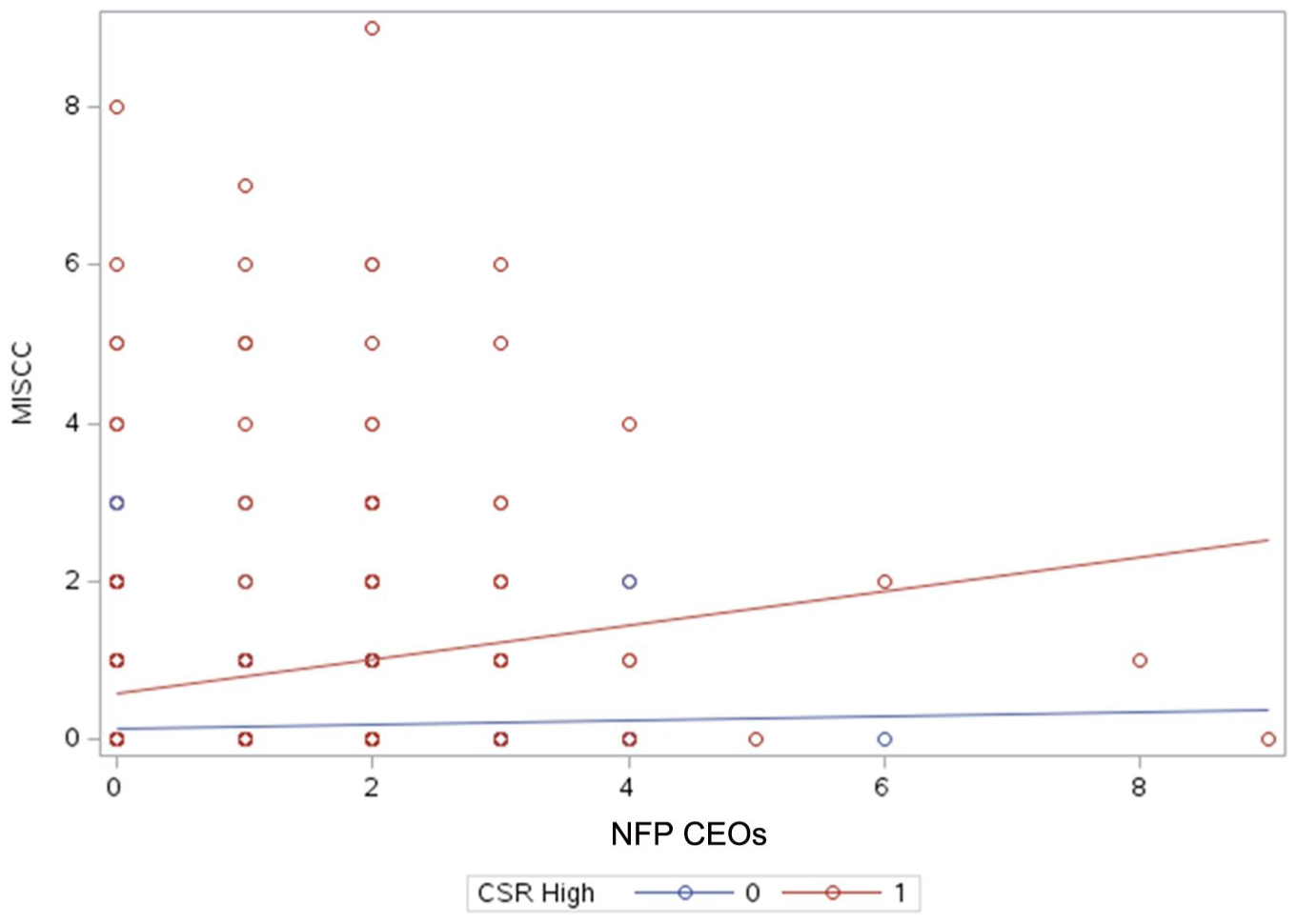

In the OLS regression, NFP CEOs are significantly and positively related to CSR performance (β = 1.581, p < 0.01). In the ZINB regression, CSR performance is significant (β = 0.692, p < 0.01), indicating a positive association with the likelihood of misconduct. This confirms that firms managed by NFP CEOs exhibit higher CSR engagement and a higher likelihood of corporate misconduct, supporting our propositions of conflicting priorities and moral licensing. To further assess the nature of the relationship between NFP CEOs, CSR performance, and misconduct, we charted the covariances of these variables. In Figure 4, the Y axis represents misconduct, the X axis represents CEO NFP positions, and the red and blue lines represent CSR-high firms (CSR score ⩾ 50%) and CSR-low firms (<50%), respectively. As evident, CSR-low firms have a steady line from CEO NFP 0 to the end, indicating that the level of misconduct does not increase in low CSR firms along with NFP CEOs. In contrast, the level of misconduct among high CSR firms has shown a significant upward trend, coinciding with the rise of NFP CEOs.

The moderating role of CSR performance on the association between NFP CEOs and misconduct.

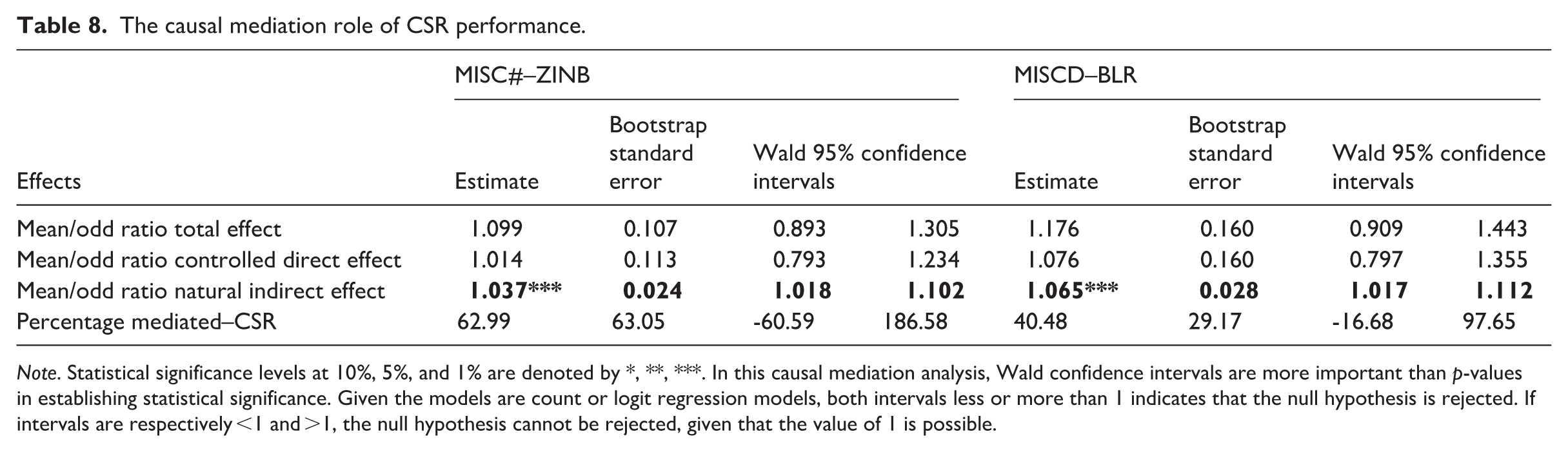

However, the positive moderation may not indicate a causal relationship between NFP CEOs, CSR, and misconduct, leaving uncertainty as to whether this argument is solid. To further test the conflicting priorities conjecture, we examine whether CSR mediates the relationship between NFP CEOs and misconduct. Identifying direct and indirect effects in this relationship is helpful in this context. We employ a single mediator regression model, utilising the Proc CAUSALMED function, to estimate both direct and indirect effects, along with bootstrapped standard errors and Wald confidence intervals (Hardy et al., 2025). The null hypothesis is rejected if the values are not equal to 1 in odd ratio estimations; thus, the confidence intervals should not fall within this range (e.g. 0.8 to 1.10) (VanderWeele and Vansteelandt, 2010). The CSR performance is specified as the mediator variable. The results are shown in Table 8. The mediator analysis reveals a significant indirect effect of NFP CEOs on misconduct through CSR performance (β = 1.037, Wald CI = 1.018, 1.102, p < 0.01). This means that the NFP CEOs’ causal effects on misconduct occurred through CSR. In other words, the positive relationship between NFP CEOs and misconduct is driven by higher CSR performance. Thus, this mediation analysis validates our conjecture of conflicting priorities.

The causal mediation role of CSR performance.

Note. Statistical significance levels at 10%, 5%, and 1% are denoted by *, **, ***. In this causal mediation analysis, Wald confidence intervals are more important than p-values in establishing statistical significance. Given the models are count or logit regression models, both intervals less or more than 1 indicates that the null hypothesis is rejected. If intervals are respectively <1 and >1, the null hypothesis cannot be rejected, given that the value of 1 is possible.

The results above somewhat contradict the findings of the non-linear analysis, which indicate that NFP CEOs with four or more positions are negatively associated with misconduct. This is because, if moral licensing and conflicting priorities arguments are valid in explaining the positive link between NFP CEOs and misconduct, these issues ought to intensify when benevolent CEOs hold more NFP positions. However, the non-linear result indicates otherwise, that after four or more NFP positions, the relationship between CEOs and misconduct is negative. Our contention for this contradictory result is on the potential distinct maturity of benevolence in CEOs. The benevolence of CEOs, which is proxied by involvement in NFP leadership, can be recognised through varying degrees of engagement in ethical actions in their personal lives and may be associated with different levels of moral development or manifestation. In other words, CEOs with four or more NFP positions could constitute a distinct group with higher manifested benevolence, reflecting relatively greater engagement with social causes than other NFP CEOs with few positions. This contention potentially explains the positive and negative associations between NFP CEOs and misconduct at different levels of benevolence.

Prior literature on the behavioural ethics of leaders provides some insights. Brown and Treviño (2006) argued that leaders’ moral ethics can vary depending on their moral reasoning abilities. For instance, leaders with higher moral reasoning are more likely to view situations as involving multiple behavioural options and to uphold internally held values and standards, relative to leaders with low moral reasoning. These leaders are more likely to sustain their ethical leadership over time through moral identity internalisation and complex moral reasoning of ethical implications. The moral identity internalisation among leaders is more likely to result in consistent prosocial behaviour and less likely to lead to moral licence (Boegershausen et al., 2015; Conway and Peetz, 2012). From this perspective, NFP CEOs with higher engagement in social causes demonstrate a higher level of benevolence and potential higher level of moral reasoning in corporate decision-making, resulting in sustained ethical leadership. The consistency of ethical leadership means that these leaders are less likely to have conflicting moral priorities or moral licensing. While testing this contention is beyond the scope of the study, potential distinct higher level of benevolence and internalised moral values potentially explain the linear and non-linear results between NFP CEOs and misconduct.

5. Conclusion

We investigate whether NFP CEOs are associated with corporate misconduct. We further investigate the moderating role of NFP boards in this association. Drawing from UET and benevolent leadership theoretical lenses, we hypothesise a negative association between NFP CEOs and corporate misconduct. In contrast, drawing from conflicting priorities, CEO power, and moral licensing theoretical lenses, we hypothesise a competing association, that NFP CEOs are positively associated with misconduct. In examining these associations, we utilise novel, hand-collected data on corporate misconduct and follow the prior literature in collecting NFP positions of CEOs. Controlling for firm, CEO, and board characteristics, we estimate a series of regressions and find a significant positive association between NFP CEOs and corporate misconduct. We further document a positive moderating role of NFP boards on the association between NFP CEOs and misconduct. The results are robust to matched samples generated through entropy balancing and PSM approaches.

We posit three explanations for this relationship. First, NFP CEOs are likely more inclined to serve a wide range of stakeholders (Karakas and Sarigollu, 2012), potentially leading to conflicting priorities and less emphasis on strong governance and enforcement. Second, research shows that past ethical actions (e.g. engaging in CSR activities) may lead to the acceptance of future unethical conduct, a phenomenon known as moral licensing (Bouzzine and Lueg, 2023). We tested these arguments by examining the associations between NFP CEOs, CSR performance, and corporate misconduct, finding support. The CSR performance has a positive moderating effect on the relationship between NFP CEOs and misconduct. In addition, we examine whether CSR performance has a causal mediation role. The mediation analysis indicates that NFP CEOs influence misconduct through CSR performance. This confirms our conjecture regarding potential conflicting priorities, implying that an excessive focus on serving stakeholders may result in either being morally licensed to ignore or accept unethical actions or distract from upholding effective governance.

Finally, we posit that increased CEO power and busyness may explain the results. Even if unintended, serving on NFPs is likely to increase CEOs’ social ties, which may enhance their busyness and decision-making influence in their firms (Chahine et al., 2021; Khanna et al., 2015). In additional analysis, CEOs’ multiple ASX directorships are included in the regression model as an additional proxy for power and busyness. Furthermore, we created another NFP CEO variable that includes only NFP CEOs with fewer than two ASX directorships. The results remain consistent, indicating that NFP CEOs have a positive influence on misconduct. We further validate this through a descriptive analysis of the overlap between NFP CEOs and powerful, busy CEOs in the sample, finding that they are distinct groups. Thus, the positive relationship is not driven by CEO power and/or busyness. This leaves us with the empirical evidence primarily supporting the conflicting priorities and moral licensing conjecture. The results will be insightful for firms in CEO recruitment decisions and performance evaluation strategies.

The additional non-linear analysis indicates that, after a certain threshold of CEOs’ NFP positions (i.e. four or more), the relationship between NFP CEOs and misconduct becomes negative. This opposite result contradicts our arguments on conflicting priorities and moral licensing, as NFP CEO groups (with four or more NFP positions) and those with fewer NFP positions differ in their influence on the likelihood of misconduct; thus, the theoretical arguments may not fully apply. While the above theories, particularly moral licensing, are applicable to the linear relationship, the non-linear relationship needs to be explained further. Our contention regarding this nuanced relationship between NFP CEOs and misconduct is that NFP CEOs differ in the level of manifested benevolence, with CEOs holding four or more positions more likely to have higher moral identity internalisation, resulting in enhanced moral reasoning in decision-making and reduced risk of moral licensing. This may explain why NFP CEOs with more NFP positions are less likely to commit misconduct. The implication is that the influence of NFP CEOs should be considered with caution, as benevolence levels may vary with the level of engagement in NFP positions, which in turn could influence subsequent moral consistency or licensing.

Our results are not without limitations. The research utilises a sample of Australian-listed firms for analysis; therefore, the generalisability of the results to other markets with different characteristics is uncertain. Also, although we collect misconduct data from multiple conceptually different data sources and corroborate them, we may not have captured all misconduct, as the very nature of this behaviour makes it difficult to detect. Extending our methodology, future researchers may identify misconduct events using data sources not available in this research. Another standard limitation in misconduct research is the time lag between events, as it is not possible to observe the exact point of misconduct. In addition, though we used techniques to ensure the robustness of the measure, our measure of NFP CEOs may not fully capture individual virtue, given the complexity of individual decision-making. Thus, future research may use different proxies or other methods (e.g. psychometric methods) to identify CEOs’ moral characteristics. We also acknowledge that our results may be subject to endogeneity issues, as unobserved variables may influence the likelihood of misconduct. Although entropy balancing and PSM are robust techniques for minimising sample bias, they do not entirely address concerns about unobserved variables. Finally, while we provide an explanation for the differences between linear and non-linear analyses of the relationship between NFP CEOs and misconduct, testing these differences is beyond the scope of this study. Future research can further investigate whether the explanations of moral consistency and moral licensing is empirically valid.

Footnotes

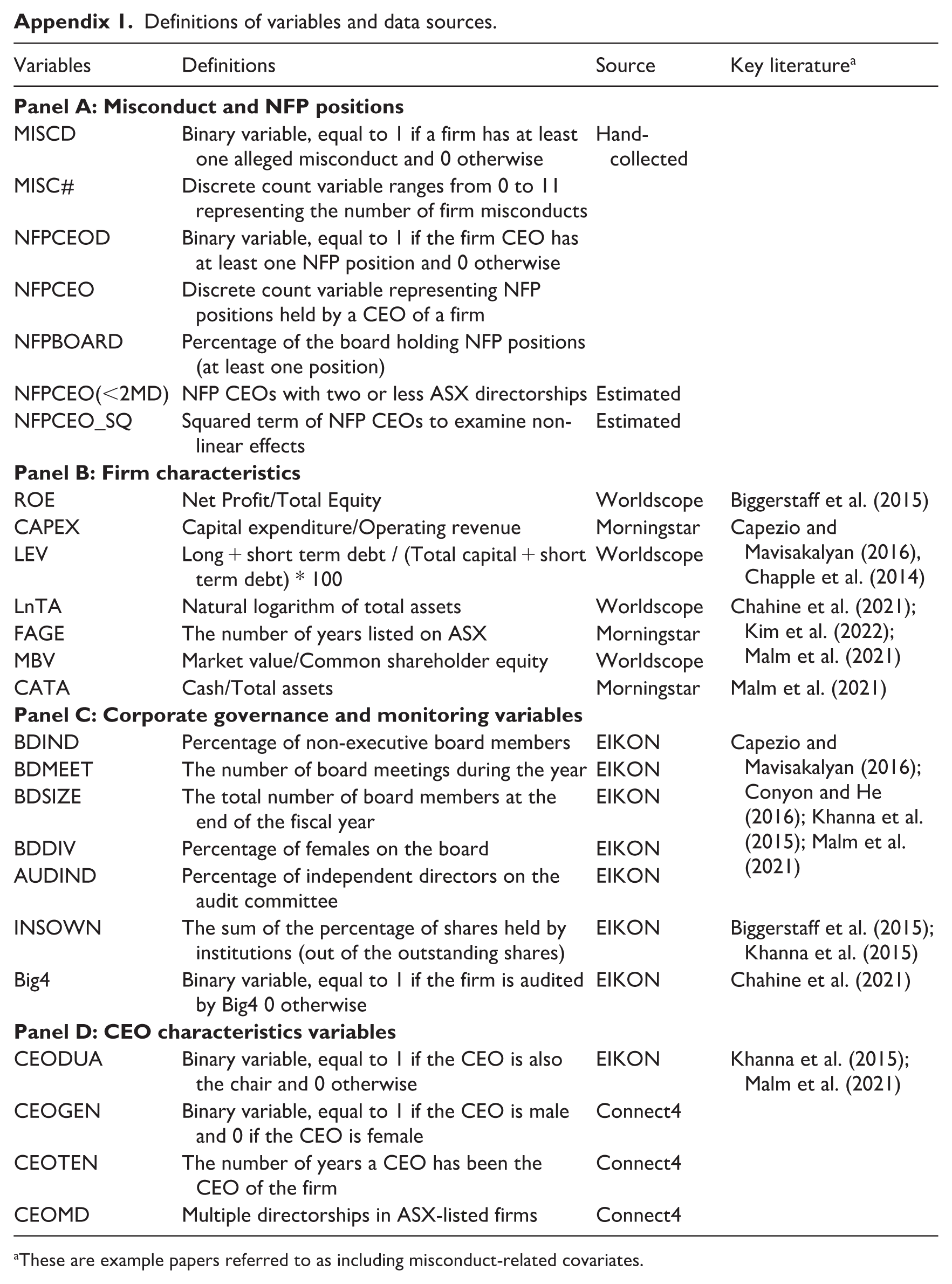

Appendix

Definitions of variables and data sources.

| Variables | Definitions | Source | Key literature a |

|---|---|---|---|

|

|

|||

| MISCD | Binary variable, equal to 1 if a firm has at least one alleged misconduct and 0 otherwise | Hand-collected | |

| MISC# | Discrete count variable ranges from 0 to 11 representing the number of firm misconducts | ||

| NFPCEOD | Binary variable, equal to 1 if the firm CEO has at least one NFP position and 0 otherwise | ||

| NFPCEO | Discrete count variable representing NFP positions held by a CEO of a firm | ||

| NFPBOARD | Percentage of the board holding NFP positions (at least one position) | ||

| NFPCEO(<2MD) | NFP CEOs with two or less ASX directorships | Estimated | |

| NFPCEO_SQ | Squared term of NFP CEOs to examine non-linear effects | Estimated | |

|

|

|||

| ROE | Net Profit/Total Equity | Worldscope | Biggerstaff et al. (2015) |

| CAPEX | Capital expenditure/Operating revenue | Morningstar | Capezio and Mavisakalyan (2016), Chapple et al. (2014) |

| LEV | Long + short term debt / (Total capital + short term debt) * 100 | Worldscope | |

| LnTA | Natural logarithm of total assets | Worldscope | Chahine et al. (2021); Kim et al. (2022); Malm et al. (2021) |

| FAGE | The number of years listed on ASX | Morningstar | |

| MBV | Market value/Common shareholder equity | Worldscope | |

| CATA | Cash/Total assets | Morningstar | Malm et al. (2021) |

|

|

|||

| BDIND | Percentage of non-executive board members | EIKON | Capezio and Mavisakalyan (2016); Conyon and He (2016); Khanna et al. (2015); Malm et al. (2021) |

| BDMEET | The number of board meetings during the year | EIKON | |

| BDSIZE | The total number of board members at the end of the fiscal year | EIKON | |

| BDDIV | Percentage of females on the board | EIKON | |

| AUDIND | Percentage of independent directors on the audit committee | EIKON | |

| INSOWN | The sum of the percentage of shares held by institutions (out of the outstanding shares) | EIKON | Biggerstaff et al. (2015); Khanna et al. (2015) |

| Big4 | Binary variable, equal to 1 if the firm is audited by Big4 0 otherwise | EIKON | Chahine et al. (2021) |

|

|

|||

| CEODUA | Binary variable, equal to 1 if the CEO is also the chair and 0 otherwise | EIKON | Khanna et al. (2015); Malm et al. (2021) |

| CEOGEN | Binary variable, equal to 1 if the CEO is male and 0 if the CEO is female | Connect4 | |

| CEOTEN | The number of years a CEO has been the CEO of the firm | Connect4 | |

| CEOMD | Multiple directorships in ASX-listed firms | Connect4 | |

These are example papers referred to as including misconduct-related covariates.

Acknowledgements

This paper is based on Ashesha Weerasinghe’s Doctor of Philosophy research project conducted under QUT and the Australian Government’s Research Training Program scholarship.

Final transcript accepted 16 April 2026 by Helena Spiropoulos (AE Accounting).

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.