Abstract

Interest rates are a key economic indicator and to date no academic study has attempted to track Irish rates over the course of the eighteenth century. The purpose of this paper is thus to provide a time series of interest rates for the Irish mortgage market for that century. This examination of how they moved and compared to those elsewhere provides insights into the Irish economy and how it reacted to external events such as the South Sea Bubble or the wars with France, as well as local banking failures and a booming land market. Interest rates are ‘an important index of the quality of the institutional framework’ and this paper shows how they were influenced by institutional pressures including the usury and penal laws. The paper therefore seeks to address two important questions. How did Irish interest rates compare with English rates and did interest rates influence the development of the Irish economy?

Introduction

In the particular context of eighteenth-century economies, North and Weingast claimed that the Glorious Revolution was key to subsequent British economic growth, increasing the predictability of government and reducing the chances of expropriation, thus enhancing and securing property rights and enabling state borrowing at lower interest rates. This in turn helped the development of the Financial Revolution and brought lower private sector interest rates which stimulated investment and entrepreneurial activity. 1 However, Ireland did not enjoy some of the key institutional benefits ascribed by North and Weingast to the English regime change: for instance judicial independence. 2 It is difficult to measure and assess institutional change, but North and Weingast argued that capital market conditions provide ‘one of the few means for empirically evaluating the effects of the Glorious Revolution’. 3 Hence the importance of interest rates.

The paper has the following structure. Firstly, the previous scholarship is reviewed. The background economic and institutional structure is then addressed, before presenting the main results gained from the data in the Irish Register of Deeds. 4 Data regressions are provided to show what features of the mortgages influenced interest rates. The Irish rates are then compared to English ones. Finally, initial conclusions as to the research questions are provided.

Since one of the key questions this paper seeks to answer is the nature of the relationship with English interest rates, I needed to have access to time series of eighteenth-century rates in England. There are many sources for general interest rates, but surprisingly relatively little scholarly work has been undertaken on English mortgage rates. For reasons of consistency and scope, I have used the data compiled by Ward. 5

Turning to the Irish economy of the eighteenth century, the key works are those of Cullen, who described the Irish economy as experiencing a ‘secular expansion of striking force for the greater part of the eighteenth century’. 6 As regards the credit markets, Lynch and Vaizey took the view that, given the limited size of the internal Irish markets of the eighteenth century, the economy was largely insulated from credit crises. 7 Cullen views this position as untenable and, as we will see below, my new evidence would be supportive of Cullen's viewpoint. 8

Any assessment of financial conditions would be pointless unless the background as to price inflation was understood. The primary work on compiling a cost-of-living price index was completed by Kennedy and shows, with the exceptions of the famine years of 1740 and 1800, long-term price trends as broadly flat for the first half of the century and then prices doubling over the second half. 9

In the eighteenth century, Ireland had a curious constitutional position. It was ‘a province of Britain’ which was ‘not a colony, for it had its own monarch…parliament and privy council’ and thus laws and regulations differed. 10 In both England and Ireland, maximum usury interest rates applied however throughout the eighteenth century. In Ireland, these were higher than in England, being 10% up until 1703, when the rate was reduced to 8%. There were further reductions in 1721, to 7%, and to 6% in 1731. 11 English usury rates were reduced from 6% to 5% in 1714, but otherwise remained unchanged. 12 The law on usury applied to loans including mortgages with an amount loaned of more than IR£100, but it did not seem to apply to other forms of financial transactions such as annuities. 13 Usurious deals will have occurred, for example through the practice of an added ‘douceur’ given to the lender. 14 The level of, and need for, a usury rate was controversial and was notably the subject of a debate between Jeremy Bentham and Adam Smith. 15 It should be noted that, in the absence of deposit bank accounts or stock exchanges, mortgages and loans were a significant, perhaps the dominant, investment sector for those with investment capital. 16

Mortgages typically took a legal form where the lender did not enter into use of the pledged property unless the borrower defaulted. Although the stated duration is often for a short period of a year or less, in reality, after an initial period, the lender could unilaterally demand repayment or the borrower could, equally unilaterally, choose to repay. 17 Whilst these were open-ended contracts, the average real duration of the first 200 Irish mortgages which were certified as repaid in the Register was calculated by Twomey at around six years. 18 Twomey stated that ‘lenders had legally enforceable processes by which they could take valid security for their loans’. 19 However, recovery could be an expensive and lengthy process, particularly when borrowers appealed to English courts through ‘writs of error’ and the additional costs and risks to lenders should not be underestimated. 20

We are fortunate that a central Register of Deeds was established in Ireland, covering significant financial transactions including, for our purposes, mortgages. The purpose of the Register was to provide security to purchasers and prevent forged and fraudulent transactions and it was founded to enforce the Penal Laws. 21 When a deed or transaction was registered, a memorial containing the main clauses was entered in the Register and these records exist from 1708 onwards. 22 Mortgages were recorded within the Register along with property sales, leases and other similar transactions.

In any economic study, transaction costs are of importance and in Ireland intermediary and enforcement costs were present. In a rare example where such costs are quoted in the memorial this brought the effective interest rate payable up to in excess of 22%, but in general they will not have had such a large impact on the effective interest rate. 23 Unlike England, Ireland had no central bank during most of the eighteenth century, until the establishment of the Bank of Ireland in 1783. 24 Attempts were made in the 1720s and 1730s to establish a central bank but were defeated in the Irish parliament. 25

The Register of Deeds

My primary source of data was the Register of Deeds. The data are of high quality and available online through the Mormon Church website, since the memorial books were microfilmed in the 1960s as part of the Church's project to baptise the dead. I gathered simple data, where it was available, on the amount of loan, interest rate, location of the security (by province), its nature (whether urban property or rural land), the location of the lender (whether in Ireland or elsewhere) and the year of the transaction. 26 Unfortunately, given the options to repay at any future date or to call in the loan, the term of the loan is rarely available in the eighteenth-century Register data and thus I was unable to determine any expected durations and thus to construct any yield curves.

The Register is a very useful source since it has not been systematically searched for interest rate information for the complete century by any previous scholars. 27 O’Rourke and Polak used the Register to establish a ‘Property Transaction Index’ by calculating ‘the number of memorials lodged in the Registry from 1708 to 1988’. 28 They helpfully used this index to identify trends in economic activity. However, there is a problem with their methodology when they seek to identify the impact of specific events such as the famine of 1744. They used the year when property transactions were lodged in the Register, but many transactions were registered well after the date of the transaction. For instance, in a random sample of 300 transactions lodged in 1744, just over a third related to transactions from prior years dating as far back as 1700. 29 The current work uses the year the transaction occurred not that when lodged with the Register.

The Register is, however, subject to bias, both from a geographic perspective and by the choice of those who wished transactions registered and were willing to pay the relevant costs. 30 There is, of course, a concern that the data contained in the Register are not fully reflective of the Irish Catholic majority, but the capital and land was held primarily by the Protestant elite. The contents of the memorials are also dependent on the choice of the scribe/parties as to what he/they thought was necessary to record in the memorial as a summary of the transaction concerned. There are, for instance, many mortgage memorials which refer only to ‘interest’ rather than describing or specifying the rate to be paid. To test whether there was a systematic over or under-statement of rates in the memorials I compared the Register data with a sample of original mortgage data from the Public Record Office of Northern Ireland, PRONI, and the limited number of Irish newspaper mortgage advertisements. 31 This showed no systemic bias in the Register data.

In order to adopt a systematic approach I extracted a sample of transactions where the interest rate payable is described, either explicitly or stated as being at a ‘legal’ or ‘lawful’ interest rate, for each year up to 1799. A total of 4,978 interest rates were gathered. The data within any particular year were selected randomly from the memorials available, and at least 40 datapoints were obtained per year for each year from 1708 in order to ensure a minimum number of annual observations. This ensures that the selection is not biased, since the output is an average interest rate per year with a sufficient number of observations. However, more memorials were examined and data were obtained for the earlier years of the Register's operation, since these had a higher potential for containing data on the period prior to the Register's foundation in 1708. 32 One important assumption is the interpretation of the interest rate applicable when a mortgage is described as being at ‘legal’ or ‘lawful’ interest. It has previously been assumed to be equal to the usury rate and I have also adopted this assumption. 33

Results

The data gathered are shown in Figure 1 and the Appendix.

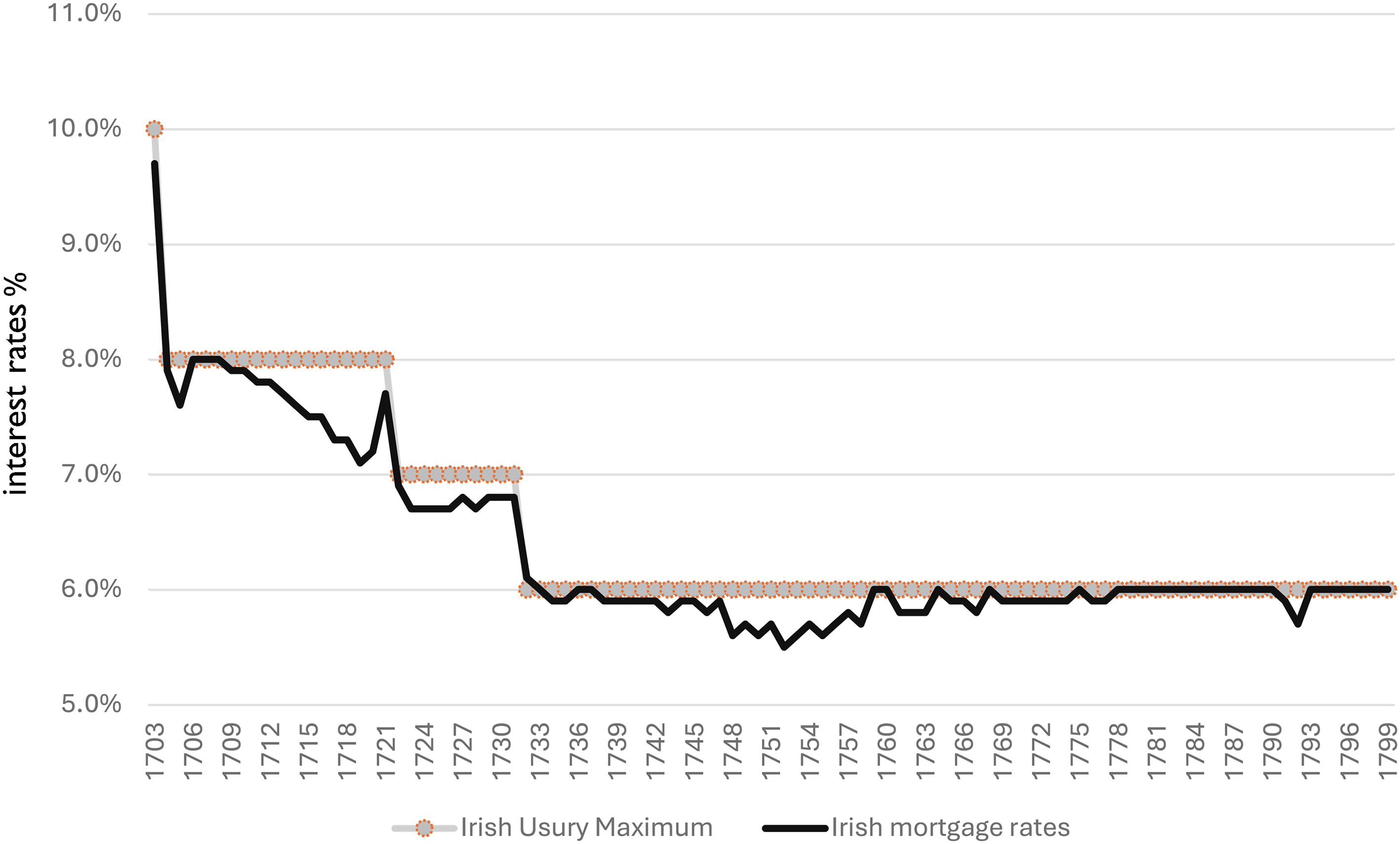

Eighteenth-century irish mortgage interest rates.

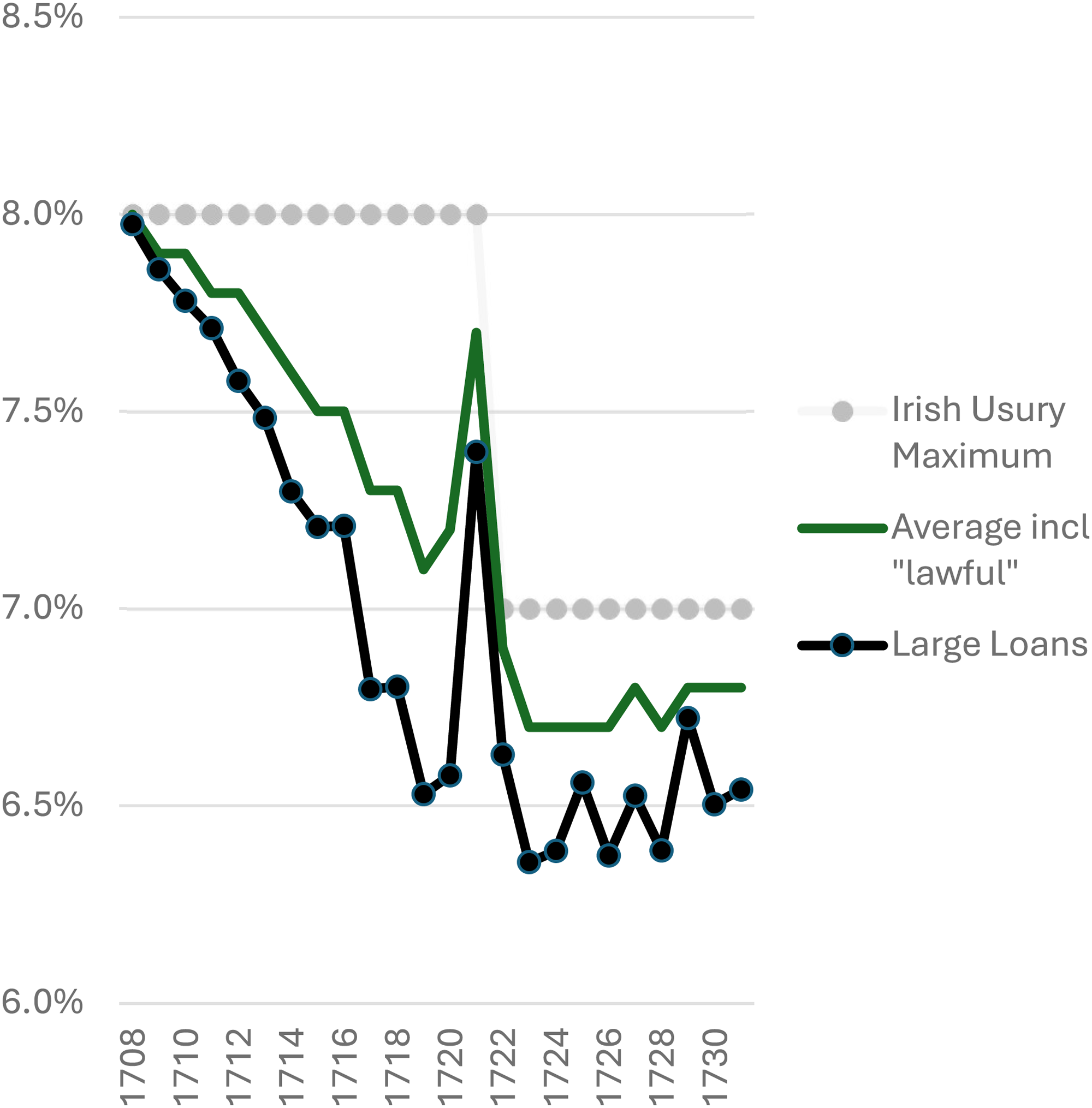

There are four distinct periods which correspond to the usury rates then applying. In the 8% usury period there does appear to be a steady decline to close to 7%, before an uptick in rates in 1721. 34

The financial events of 1720 to 1721 are particularly complex from an Irish perspective. Not only did this period include the Mississippi and South Sea Bubbles, but also the proposal of the establishment of an Irish National Bank which would issue loans at 5% interest rates. 35 In 1721, the proposal to establish the Irish National Bank was defeated but a bill reducing the usury rate to 7% passed. Rates climb sharply in that year, particularly for larger loans, and are shown in Figure 2.

Irish mortgage interest rates 1708 onwards.

In relation to the South Sea Bubble, Walsh noted that the gentlemen of Ireland ‘went late into the stocks, bought dear, extracted all the foreign gold out of Ireland, which is the best part of their current coin, to make those purchases, so that money is become extremely scarce’ and the data shown in Figure 2 are entirely consistent with such changes in the Irish money supply. 36 It also shows that Cullen's statement that ‘the Irish financial world escaped from the direct consequences’ of the South Sea Bubble is incorrect. 37 Furthermore, it adds to the evidence that Walsh provided on the widespread effect of the South Sea Bubble, which contradicts Hoppit's view that the Bubble was essentially a London-based phenomenon. 38

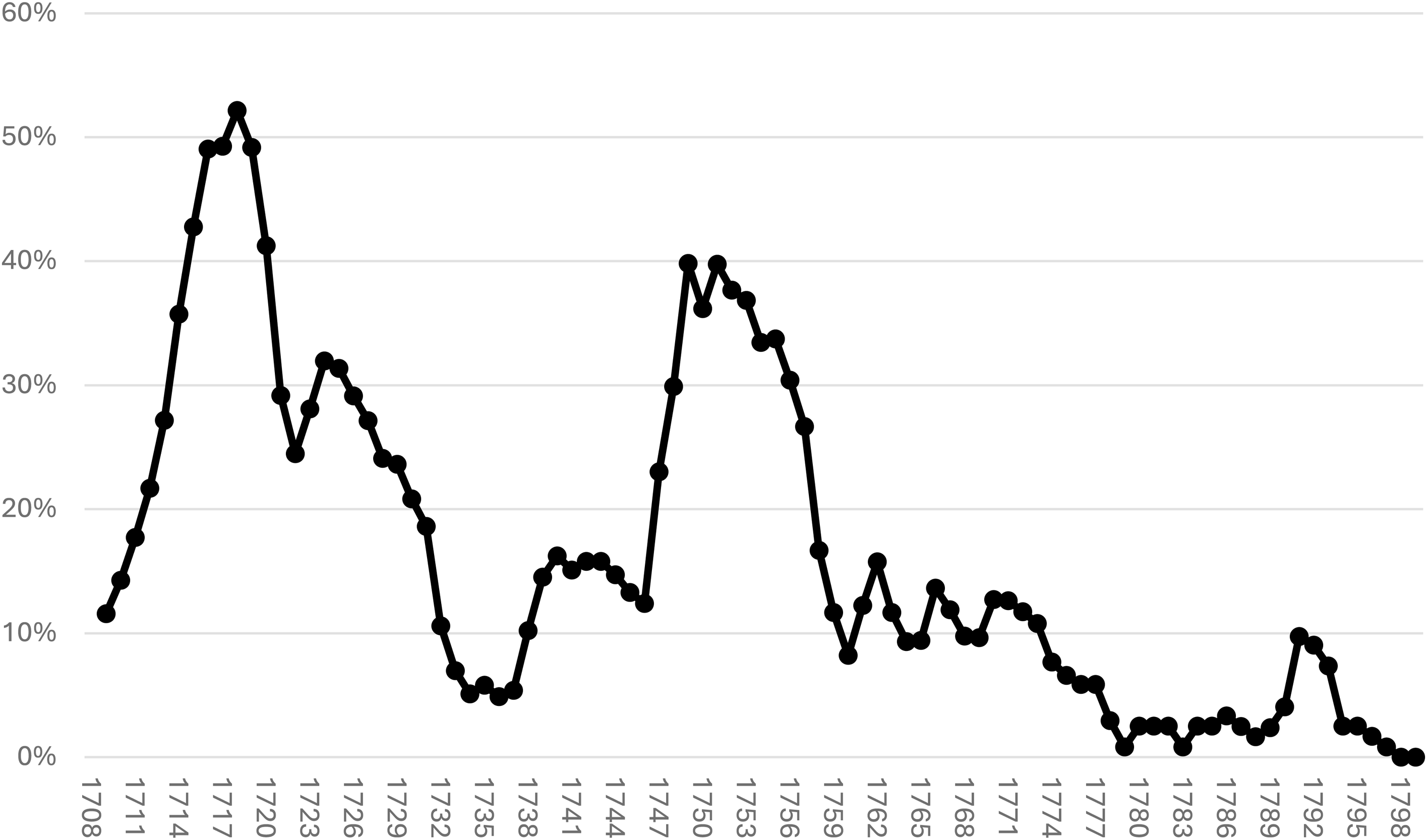

Another way of looking at the data is to consider the percentage of transactions that were undertaken where the interest charged was under the usury rate, and thus rates were being determined by some form of market mechanism rather than by convention. The proportion of these deals is shown in Figure 3, which shows, more clearly than Figure 1, an uptick in true market activity between 1748 and 1758.

Irish mortgages – percentage of deals under usury rate – three year average.

After an initial period when the interest rate was naturally declining as usury rates were high, the peak of true market activity and sensitivity was in the 1750s but from the 1760s onwards typically 90% or more of all activity was simply transacted at the usury rate and the interest rate market had ceased to function.

To explain these patterns, it would be ideal to have a yearly indicator of money supply in Ireland, to assess the relationship with interest rates but this is clearly unachievable. There were no national statistics and the money supply of specie in Ireland was composed largely of foreign coins. Contemporary estimates of the amounts of money in circulation are viewed as ‘notoriously inaccurate’. 39

Cullen, however, believed that up until the 1730s there was an acute scarcity of specie in Ireland, but supply improved from the 1730s to the end of the 1740s. He then noted that in the 1750s ‘all the Irish banks were affected by a general shortage of cash’ as imports increased and remittances to absentee landlords continued and, indeed, three Dublin banks collapsed. 40 However, my interest rate data do not support this view as interest rates were lower in the 1750s compared to the previous two decades as is evidenced in Figure 1. Cullen, however, also identified an increase in bank note issue associated with the ‘greatest boom in Irish history’ from 1749, which would have contributed to lower interest rates and although the timing is not exact this could explain the sharp rise in sub-usury activity I have identified in 1748 in Figure 3. 41

Twomey described the Irish mortgage market as ‘vibrant’ and this may arguably be the case for the period he studied between 1710 and 1730, but for the period after 1760 it was stagnant and moribund. 42

A contemporary concern of certain commentators was that English investors were extracting profit from the Irish economy, not only by their direct ownership of land as absentee landlords, but also by their actions as mortgagees receiving interest payments. 43 It is evident, however, that the Irish mortgage market was almost exclusively internal given the location of the participants, and the contemporary concerns were misguided, since of the 4,978 mortgage memorials reviewed only 2.2% involved lenders from outside Ireland (normally England as may be expected). Interestingly, there are only two lenders in the sample from Scotland which would indicate little or no commercial contact between Ulster and Scotland, despite the presence of a large Ulster-Scots population and the geographic proximity. Similar numbers would be seen for borrowers.

Twomey noted that ‘there was an almost complete absence of foreign (English) participation in either the land or the mortgage market’. 44 My wider data would support this finding, but one of Twomey's other conclusions, that Jonathan Swift was a private lender ‘who took a very professional and, for this period, a sophisticated approach to the management of his lending portfolio’ can be challenged. 45 Of the eight loans that Swift made, where we know the date, amount and interest rate, they were generally to people of similar social status to himself. Six were made at rates below the market equivalent, at an average overall rate differential of 0.5%. 46 So he was making less money than he could have. Perhaps this reflects Swift's humanity more than his business acumen.

Interest Rate Drivers

There are many possible determinants of the rate of interest, both over time and within a particular timeframe. The available data permit an analysis of some of the correlations for interest rates within certain timeframes including size of loan, geographical location of security by province and whether urban or rural, and the location of lender. However, there are some unobservable explanatory variables that may well also have influenced interest rates within the sample, including participant religion, reputation, degree of social networking and expected term of the arrangement.

As regards the size of the loan, this varies from a minimum of IR£5 to a maximum of IR£60,000. 47 To give some idea of the relative size of these amounts, the average wage for a semi- or unskilled worker in Dublin at the beginning of the century was around a shilling a day, so IR£5 would constitute perhaps four months’ wages. 48 In the vast majority of cases the security granted for a mortgage was real estate either of an urban nature, typically a house or a vacant lot, or rural acres of land. 49

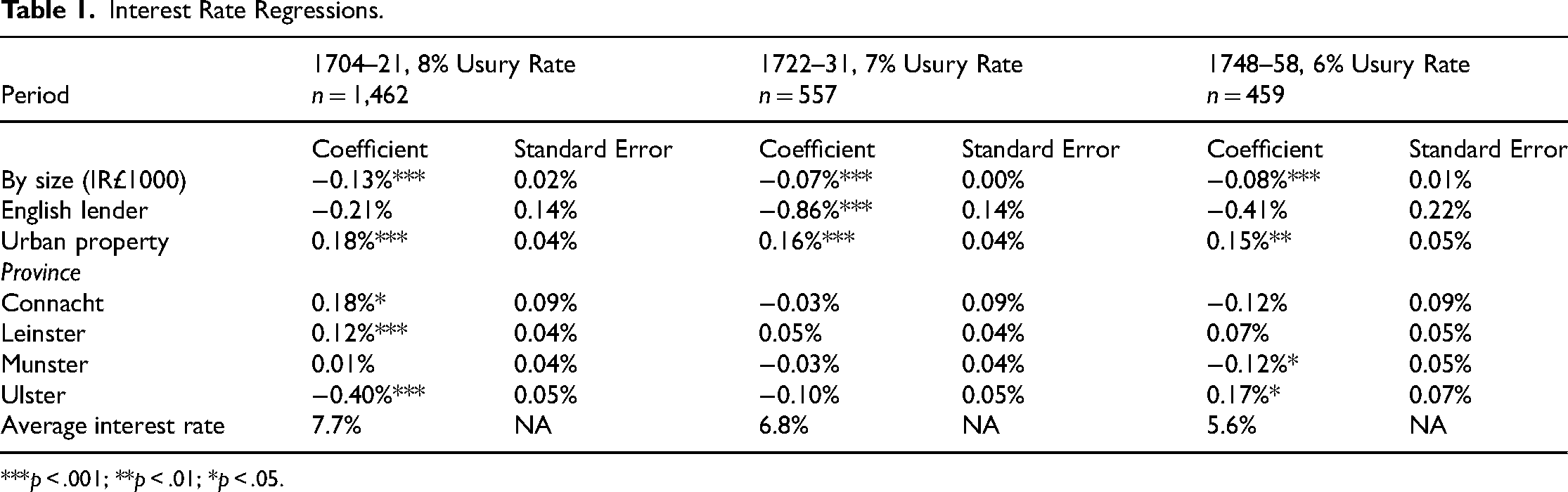

Given the very significant influence of the level of usury rate on the market it is appropriate to assess the correlations per usury period, and only when there is some significant market variability in the interest rate. These periods are 1704–1721 for 8%, 1722 to 1731 for 7% and 1748 to 1758 for 6%.

The main regression equation is:

The results show a negative and significant relationship between the size of the loan and the interest rate charged in all periods. Thus, the larger the size of the loan, the lower the interest rate. 50 There is also a positive and significant relationship between urban loans compared to rural ones. That is that loans made on town or city property tended to be at higher interest rates than those for agricultural land. One reason for this may be that some of the urban mortgages are speculative building loans of a short-term nature where the duration of the loan is so short that the interest rate paid is commercially insignificant compared to the other profits, costs and risks of building housing. 51 However, there are also fundamental differences in the risk profile of different types of security and this was understood by at least some participants in the market. A contemporary commentator in England in 1739 suggested that the rates of interest underlying different transactions should reflect the security and other features of the property. In particular, he suggested that for the purchase of good rural land, 4% would be appropriate, but that 5.5% or 6% should be used for well-situated houses. 52

Interest Rate Regressions.

***p < .001; **p < .01; *p < .05.

The relationship between rates for loans where the lender is English compared to Irish show a negative correlation. That is English lenders achieved lower interest rates than Irish ones, although the statistical significance is lower than other relationships, possibly reflecting the small number of cases in which English lenders were involved. Apart from a potentially lower rate of interest in Ulster and a corresponding higher rate in Leinster in the earlier period, there are no clear trends by province, implying a good degree of geographic transfer of information and increasing internal market integration.

Analysis – Comparison with Other Irish Interest Rates

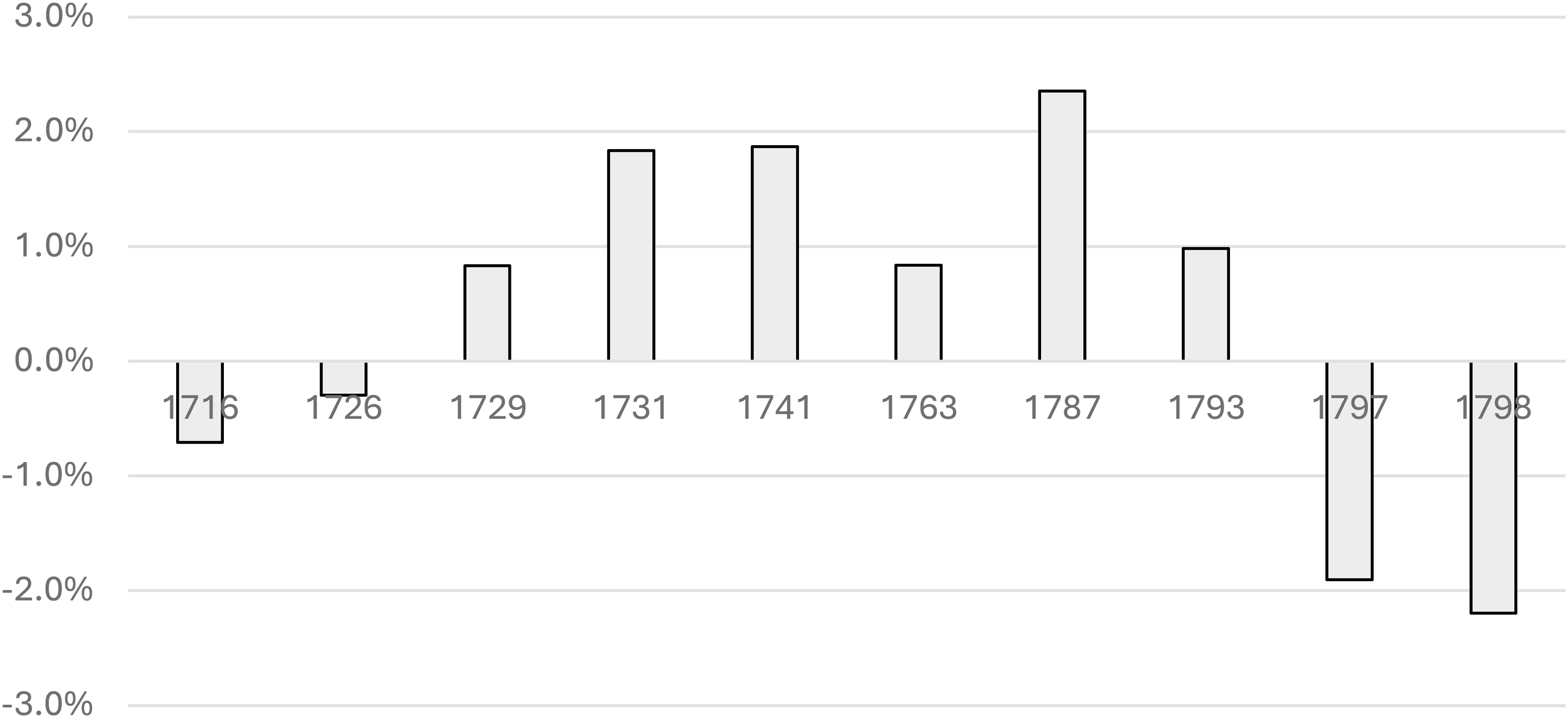

Person-to-person mortgage interest rates can be compared with other rates to establish a more detailed hierarchy of rates and risk premia. The first Irish government debt was issued in 1716 at the ‘legal’ rate of 8% (payable half-yearly) and the early issues of debt were issued at attractive rates. 53 However, from 1729, Irish state debt would generally be raised at rates below that of the private market, reflecting the ‘normal’ view of the risk premium between government and private debt, and the emerging market perception that the Irish state would honour its debt. The risk premium only reversed at the very end of the century when the need to raise funds to fight the French wars raised state interest rates in Ireland above the usury maximum of 6%. The risk premia or spreads are shown in Figure 4. 54

Risk premia: Private less state interest rates.

The Register mortgage rates almost exclusively relate to person-to-person loans. A comparison with the private ‘institutional’ market can be made by examining the borrowing rates of Dublin Corporation as set out in the Calendar of Ancient Records of Dublin. 55 Data for the earlier part of the century are insufficient for any statistical analysis, but for the period from 1708 to 1731 when the usury rates were 8% or 7% and the Register rates were generally a little below these maxima, the Corporation maintained a policy of 6% interest rates. 56 This trend of generally lower Corporation rates continued throughout the century, probably reflecting the stronger security provided by Corporation rather than personal debt. The comparison also shows that the Corporation's interest rate was more variable than private debt. This reflects the ‘commoditisation’ that was possible for the Corporation's debt compared to the illiquid and variable nature of private mortgages which were less uniform and thus less tradeable and comparable and therefore moved more slowly when market conditions, such as money supply, changed.

A further comparison of mortgage rates with the short-term shadow interest rates determined by Cassidy shows that, as may be expected, the short-term rates are more volatile, although there is no strong correlation between the short-term and longer rates. 57

Analysis – Comparison with English Rates

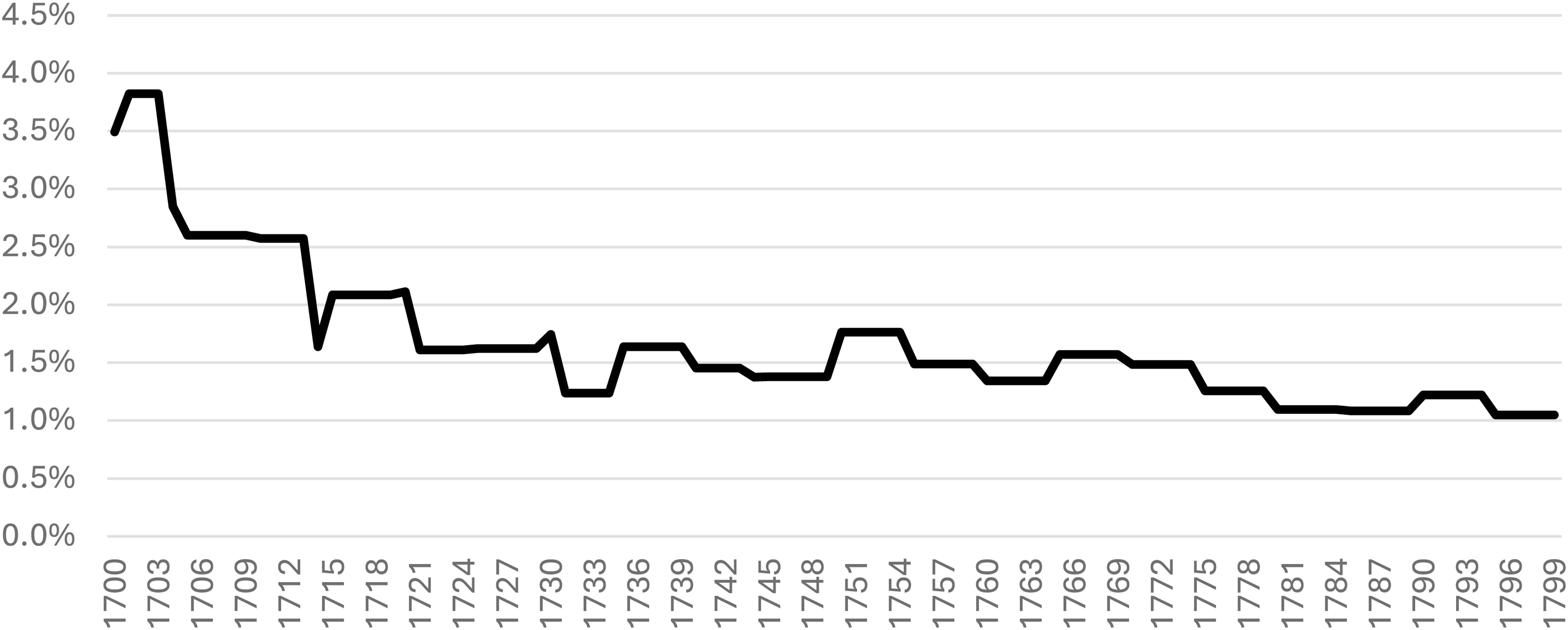

Comparison with English mortgage rates is problematic since there are a variety of sources available for these which all suffer from some flaws, but I have used the data compiled by Ward, even though it must be pointed out that Ward was only able to collect 584 data points for the English market for the eighteenth century compared to the 4,978 within the Irish sample.

The comparison is shown in Figure 5. 58

Irish less English mortgage rates spread – 1700–1799.

For the bulk of the period the spread between English and Irish rates was around 1.5%. There is a gradual decline, though it needs to be borne in mind that from 1760 onwards the Irish rates were typically constrained by the usury rate of 6%, and the English rates at the end of the century were similarly constrained by their usury rate of 5%.

As noted above, the Irish mortgage market was essentially insular with little direct involvement from English participants. However, some participants in the market were aware of the comparison with English rates. Consider the following conjecture from 1799 and relating to the Act of Union: ‘why pay six per cent on mortgages here, when in England the common interest is four, the highest five?’. 59

Irish interest rates were, however, strongly correlated with the yield on Bank of England stock, which can be considered as a proxy for longer-term English rates, during the period up to 1760. We are thus left with two remaining questions as regards determinants of Irish interest rates. Why was the essentially internal Irish market apparently so closely linked to Bank of England stock yields? And was the persistent differential between Irish and English mortgage rates justifiable by economic fundamentals?

Explaining the Correlation Between Irish Mortgage Rates and Bank of England Yields

It is clear that in certain Irish circles market participants had an understanding of English markets and the new securities that had become available during the early part of the century. For instance, Jonathan Swift wrote to Esther Johnson (Stella) ‘let me beg you to buy Bank Stock …, which has fallen near thirty per cent. And pays eight pounds per cent’. 60 Although Stella was herself English, for those elite Irish investors with the connections to invest in England, investment in Bank of England stock or other securities was available. Swift did indeed invest £300 on his own account in Bank of England stock in 1710, funding his purchase from monies in Ireland. 61 However, most Irish investors did not have access to the English markets and thus full market integration cannot explain the correlation between Irish mortgage rates and Bank of England yields. Of the 1,268 investors within the opening list of Bank stockholders of 1694 only four listed an Irish residence. 62 The number of individual stockholders from Ireland had only grown to 26 by the 1720s. 63 It later declined to five by 1750. 64 Therefore the close correlation of the rates cannot be due to the effect of these acting as alternative investments within a strongly integrated financial system. Rather I believe that the reason for the strong correlation is that these are two disconnected investments which react, other than at the time of the South Sea Bubble which had a particular impact on the Bank of England stock, in the same way to external stimuli such as a declaration of war.

Explaining the Persistent Spread Between Irish and English Mortgage Rates

Whilst the discussion above dealt with the tendency of Irish rates to move in tandem with certain English ones, it does not deal with the issue of the maintenance of a gap between equivalent rates. By way of a simple comparison, in the period from 1710 to 1760, English Bank stock yields averaged 4.4%, English mortgage rates 4.8% and Irish mortgage rates 6.4%. Was this 1.6% ‘risk premium’ justified by economic fundamentals?

There are a number of economic factors which could explain this persistent premium. Firstly, perhaps property rights were better secured in England than in Ireland? Were the ‘institutions’ in the broad sense attributed to the term by North, as the ‘rules of the game’, better in England than Ireland? 65 This seems difficult to justify given that, in practical terms, from 1708 Irish real estate was better secured than most English titles by the recording and search capabilities that the Register provided, whereas most of England lacked any land registry. A more telling argument is the ‘political’ one that Irish real estate was at greater risk of appropriation, given that much of it had been confiscated and redistributed only in the last century, to a much greater extent than in England. 66 Thus from a lender's perspective, ‘regime change’ was a significant risk for the security offered. Whilst these considerations may be considered valid at the beginning of the period, when the Register was not yet established and some confiscations of Jacobite land were relatively recent, they do not, in my opinion, hold much validity for the later periods. If anything, by the mid-eighteenth-century Irish real estate was better secured than English and the risk premium should thus have been in the opposite direction. Improved perceived security of Irish real estate may however explain the reduction in the risk premium from 2.5%/3% to 2% by 1714 shown in Figure 5.

So if the quality of the title of real estate was not the reason for the persistent risk premium what other reasons could be posited? It could be that Irish borrowers were more likely to default and less likely to pay interest on time than English ones. I believe we can set aside any cultural differences or attitudes as to the honouring of debt, which would appear to me to be unlikely given the similarities between the English and Irish societies involved. 67 It might be the case that there was a difference in the quality of the security itself. In this case, relative security would be linked to the likelihood that Irish rents, which underlay the valuation of the security and the ability of the borrower to repay, were less secure than English ones. However, I have found no strong evidence to suggest that, in the eighteenth century, Irish mortgages were inherently riskier than English ones.

But was there another driver that kept Irish rates high? There is a link between mortgage rates and the valuation of land within a local risk/return hierarchy. Mortgage rates are a function of the actual and anticipated return on land, a risk premium on mortgages vis-a-vis land and the relative taxes and administration. If the risk premium, taxes and administration do not change over time, then mortgage rates are a function of the return on land. Rates of return on Irish land appear to have been significantly above those on English land as rents increased. 68 As a result the market could support higher mortgage rates. Another way of looking at this is to state that Irish borrowers could afford to pay higher rates on their mortgages given the high rates of return they enjoyed on their land ownership. This was not the case in England, and in my view, it is the main reason why Irish rates remained persistently higher than English ones.

Impact on Irish Economy

The remaining research question relates to the impact of interest rates on the Irish economy. Lower interest rates are generally viewed as a positive encouragement for the funding of private investment initiatives, for instance, agricultural improvement, mercantile ventures or industrial development. The higher interest rates prevalent in Ireland compared to England cannot have assisted in the deployment of these initiatives in Ireland and this was understood by local businessmen. For instance, James Laffan of Kilkenny, in a pamphlet of 1785 calculated that the annual cost of running a ship of £1000 capital value was £197 in Ireland compared to £158 in England, the difference being caused solely by the interest rate differential.

69

The fact that mortgage finance was important to mercantile/industrial development is supported by the rationale for the establishment of the first English register of deeds in the West Riding of Yorkshire. The motive for establishing the register in West Yorkshire was that this was: the principal place in the north for the cloth manufacture and most of the traders therein are freeholders, and have frequent occasions to borrow money upon their estates for managing their said trade, but for want of a register find it difficult to give security to the satisfaction of the money lenders.

70

Another economic consequence relates to the Penal Laws, which can, in economic terms, be viewed as promoting ‘rent-seeking’ through the restrictions on access to the land and credit markets. Rent-seeking is generally regarded as injurious to overall economic wealth and development since it is an inefficient distribution of resources and does nothing to encourage productivity growth. 73

The 40 years after 1760 were ones where the usury rate was dominant, that is that very few transactions occurred at rates lower than 6%. During this period, the ‘natural’ rate of interest, if it had been unconstrained by usury would have been higher than 6%, as evidenced by the rates of return on annuities/rent charges. 74 In this circumstance, capital holders would have been reluctant to lend money at uneconomic rates and the credit market failed to operate. Significant credit rationing would have occurred. This market failure would mean that money would have been tight, in the sense that the supply of capital would have been restricted and this would have limited the ability of entrepreneurs to borrow, and would have further impeded economic growth in the commercial and industrial sectors, during a period when the agrarian sector was booming.

Concluding Remarks and Future Research

To conclude, the analysis presented above will have demonstrated the usefulness of the data contained within the Register of Deeds. This paper has provided evidence that the impact of the South Sea Bubble was not confined to the London markets. Also that natural reductions in the rate of interest occurred at the beginning of the century, despite the fact that in Ireland, some of the British institutions so stressed by North and Weingast as being key to interest rate reductions, were not present. It can be proposed that it was political stability, as the threat of Jacobite regime change lessened, rather than institutional changes, that led to this reduction in interest rates. In passing, I demonstrated that Dean Jonathan Swift was lacking in financial acumen.

Turning to the main conclusions as to the research questions posed, the data have shown that for the first 60 years of the century, interest rates fell to levels which were closer to, but still higher than, English ones. For the remainder of the century, the market was moribund and effectively constrained to the usury rate of 6%. In the first period, rates moved in parallel with comparable English ones, despite the lack of direct integration between the markets. This can be attributed to the two markets reacting in similar ways to external stimuli such as wars.

Throughout the century, however, Irish rates remained stubbornly higher than English ones and this will have hindered entrepreneurial and industrial activity in Ireland. This feature was not due to a conventional ‘risk premium’ difference between the two markets. The security of Irish mortgages was, if anything, stronger than that for English ones. Rather I believe it was primarily driven by the risk/return hierarchy within the Irish markets, specifically the comparison between the returns available on Irish land as rents grew from very low levels and lending rates. This conjecture as to returns on Irish land, however, needs to be quantified, and this is the subject of my future research.

Footnotes

Declaration of Competing Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Notes

Author’s Biography

Appendix. Yearly Data.

Year

n

Average Rate

% Under Usury

Year

n

Average Rate

% Under Usury

Year

n

Average Rate

% Under Usury

1700

3

8.7%

67%

1734

44

5.9%

7%

1767

40

5.8%

15%

1701

10

8.6%

70%

1735

45

5.9%

7%

1768

42

6.0%

5%

1702

12

10.0%

0%

1736

51

6.0%

4%

1769

42

5.9%

10%

1703

10

9.6%

27%

1737

49

6.0%

4%

1770

41

5.9%

15%

1704

6

7.9%

17%

1738

61

5.9%

8%

1771

43

5.9%

14%

1705

8

7.6%

38%

1739

49

5.9%

18%

1772

43

5.9%

9%

1706

14

8.0%

0%

1740

47

5.9%

17%

1773

42

5.9%

12%

1707

14

8.0%

0%

1741

45

5.9%

13%

1774

45

5.9%

11%

1708

135

8.0%

9%

1742

43

5.9%

15%

1775

41

6.0%

0%

1709

157

7.9%

10%

1743

47

5.8%

19%

1776

46

5.9%

9%

1710

173

7.9%

15%

1744

45

5.9%

13%

1777

45

5.9%

9%

1711

152

7.8%

18%

1745

43

5.9%

12%

1778

44

6.0%

0%

1712

110

7.8%

21%

1746

47

5.8%

15%

1779

47

6.0%

0%

1713

67

7.7%

27%

1747

47

5.9%

11%

1780

40

6.0%

3%

1714

88

7.6%

35%

1748

46

5.6%

43%

1781

40

6.0%

5%

1715

65

7.5%

46%

1749

43

5.7%

36%

1782

40

6.0%

0%

1716

66

7.4%

48%

1750

47

5.6%

40%

1783

40

6.0%

3%

1717

71

7.2%

54%

1751

40

5.7%

33%

1784

40

6.0%

0%

1718

88

7.3%

45%

1752

40

5.5%

46%

1785

40

6.0%

5%

1719

113

7.1%

57%

1753

41

5.6%

34%

1786

40

6.0%

3%

1720

66

7.2%

44%

1754

40

5.7%

30%

1787

41

6.0%

2%

1721

69

7.7%

23%

1755

42

5.6%

36%

1788

40

6.0%

3%

1722

49

6.9%

20%

1756

40

5.7%

35%

1789

40

6.0%

0%

1723

47

6.7%

30%

1757

40

5.8%

20%

1790

43

6.0%

5%

1724

47

6.7%

34%

1758

40

5.7%

25%

1791

40

5.9%

8%

1725

48

6.7%

32%

1759

40

6.0%

5%

1792

41

5.7%

17%

1726

50

6.7%

28%

1760

40

6.0%

5%

1793

40

6.0%

3%

1727

62

6.8%

27%

1761

41

5.8%

15%

1794

40

6.0%

3%

1728

96

6.7%

26%

1762

41

5.8%

17%

1795

40

6.0%

3%

1729

53

6.8%

19%

1763

45

5.8%

16%

1796

40

6.0%

3%

1730

54

6.8%

26%

1764

42

6.0%

2%

1797

40

6.0%

0%

1731

51

6.8%

18%

1765

40

5.9%

10%

1798

40

6.0%

0%

1732

49

6.1%

12%

1766

44

5.9%

16%

1799

40

6.0%

0%

1733

54

6.0%

2%