Abstract

In the past two decades, many international airline carriers have expanded their cooperation by forming various joint ventures (JVs). One key feature of these JVs is that they require carriers to determine certain airfares jointly and integrate their operations as a single carrier in the market for international air travel. This paper tries to evaluate the impact of JVs on airfares. The focus is on a set of behind-to-gateway markets between a non-gateway U.S. city and a foreign gateway city, where both online and codeshare flights are offered, to study how the airfares of online flights are affected after carriers form JVs. A new hypothesis is discussed that JVs increase the airfares of online flights. Based on this hypothesis, an empirical model is built to evaluate the Oneworld alliance’s transatlantic JV established in July 2010. This empirical analysis, which uses the U.S. Department of Transportation (U.S. DOT)’s Airline Origin and Destination Survey (DB1B) international data from 2008 to 2013, indicates that the Oneworld transatlantic JV increased airfares of online flights by about 3%–4% in the behind-to-gateway markets. Previous studies, which emphasized the airfare reductions of codeshare flights in the connecting markets, may have overestimated the benefits to consumers from JVs. U.S. DOT can better protect consumers by evaluating plausible airfare increases in online flights in the behind-to-gateway markets when reviewing new applications for JVs.

Keywords

The rapid development of joint ventures (JVs) is a key feature of the international airline industry. Many members of the three major airline alliances (Star, SkyTeam, and Oneworld) have further expanded cooperation by forming JVs. In 2016, 81% of the travelers who flew between the U.S. and Europe used an airplane operated by a JV ( 1 ). More recently, there is a new wave of JVs in the transpacific markets. Air Canada and Air China concluded a JV agreement in 2018, and the JV between American Airlines (AA) and Qantas got approval in 2019. In addition, the formation of JVs may no longer be limited to members of the same airline alliance. Some proposed new arrangements in 2019, like the JV between Westjet and Delta, and the JV between Japan Airlines and Hawaiian Airlines, have included independent airline carriers (Westjet and Hawaiian Airlines) which do not belong to any major alliance.

Except for mergers, JVs are considered the highest level of cooperation in the international airline industry ( 1 ). Compared with other types of cooperation (e.g., codeshare agreements), one unique feature of JVs is that they require partners to jointly determine airfares and operate as a single carrier in the relevant markets. Another form of cooperation that is closest to a JV is antitrust immunity (ATI). However, ATIs are essential components for the new proposed JVs and most of the ATIs have been upgraded to JVs in the recent decade. As a result, it is possible to broadly categorize international airline cooperation into two groups. In the first group, there are standard interline agreements, codeshare agreements, and alliance membership, where airline carriers can cooperate on many functions like aircraft maintenance or frequent flier programs, excluding pricing. Each carrier simply chooses airfares to maximize its own profits. In the second group, there are JV agreements with ATI that can fully integrate partners into a single carrier for international air travel services. Note that this study does not distinguish between JV and ATI, and will simply use the term JV to represent the second group. An additional reason that no distinction is made is that the recent empirical paper by Brueckner and Singer shows that JV and ATI’s airfares in connecting markets are very similar ( 2 ).

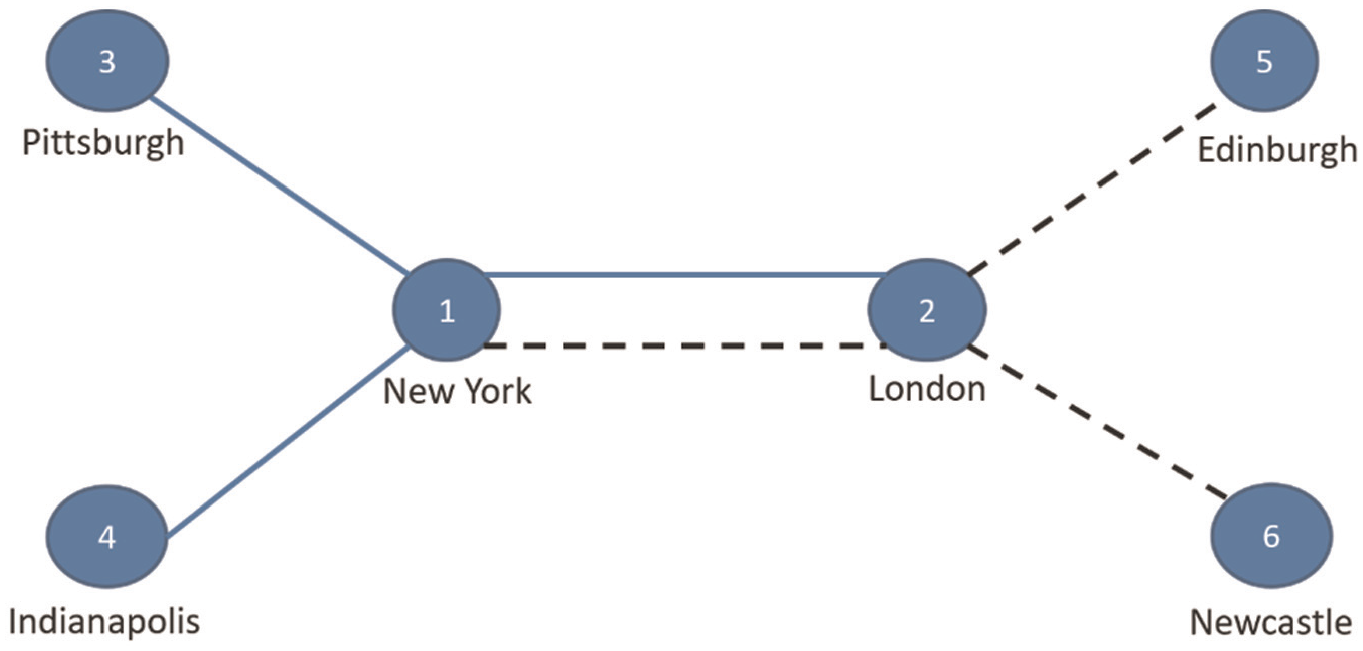

Since JV partners can jointly determine airfares in concerned markets, consumers are likely to be affected by JVs. To illustrate the impact of JVs, a simplified international airline network structure with two hub-spoke components is looked at, as shown in Figure 1. The straight lines represent AA, and the dashed lines represent British Airways (BA) in this network. The two carriers, AA and BA, use New York and London as hub cities. These two carriers are key members of the Oneworld alliance, and they have had a JV since 2010. In this network, circles represent cities, and lines that connect two cities represent nonstop flights offered by the two carriers. In the gateway-to-gateway market, the carriers usually compete against each other for consumers. However, because of government regulations, air travel in the behind-to-beyond markets between a non-gateway U.S. city and a foreign non-gateway city must combine flights from both AA and BA. Existing literature often emphasizes two major effects of a JV. On the one hand, a JV removes competition in the gateway-to-gateway market and consumers might be worse off in this market. On the other hand, a JV can eliminate the problem of double marginalization and reduce airfares of codeshare flights (i.e., flights operated by more than one carrier) for consumers in the connecting markets. Without JV, each carrier adds a markup over cost for its portion of the codeshare flights to maximize its own profits without considering potential negative effects on the other carrier. This so-called double marginalization problem leads to inefficiently high airfares of codeshare flights, which hurt both consumers and carriers in the connecting markets. Therefore, the government regulations on JVs seem to show a consistent pattern: “approving JVs unless carriers’ networks overlap too much” ( 1 ).

A stylized airline network for American Airlines (AA) and British Airways (BA).

This paper focuses on international air travel in the behind-to-gateway markets between cities like Pittsburgh and London, where both online (i.e., flights operated by a single carrier) and codeshare flights are offered. A study is made of how the airfares of online flights are affected by JVs, and a new hypothesis is discussed, that JVs can increase the airfares of online flights. The U.S. Department of Transportation (U.S. DOT)’s Airline Origin and Destination Survey (DB1B) international data from 2008 to 2013 is used to develop an empirical analysis of the Oneworld alliance’s transatlantic JV established in July 2010. It is found that the JV increased airfares of online flights in the behind-to-gateway markets by about 3%–4%. The conclusion in the literature that JVs only increase airfares of nonstop flights in the gateway-to-gateway markets and reduce airfares of codeshare flights in the connecting markets fails to fully account for the impact of JVs on consumers. Therefore, U.S. DOT’s current regulation may overlook some potential costs of JVs to consumers in the connecting markets.

Literature Review

The competitive effects of international airline JVs were first analyzed theoretically by Brueckner ( 3 ). His model, without product differentiation, shows that air travels in the behind-to-gateway markets, where both online and codeshare flights are available, are often unaffected by a JV. Carriers with the same constant marginal cost charge the same monopoly prices for these kinds of markets before and after forming a JV. One of the key reasons for this result is that the model does not allow product differentiation, which means that consumers only choose the flights with lower airfares. By charging monopoly prices for online flights, the carriers in these behind-to-gateway markets get the optimal profits, and they have no incentive to engage in offering codeshare flights (or codeshare flights can only have the same prices as the online flights). The JV could not stimulate carriers to change prices, since pre-JV prices are already optimal for profit maximization in these markets. Brueckner, by assuming the presence of economies of densities, also finds that consumers in these markets generally benefit from a JV ( 3 ). However, the empirical evidence of this paper indicates that codeshare flights often have higher airfares than online flights in the same behind-to-gateway markets before forming a JV, and consumers might have chosen both kinds of services. This implies that modeling airline demand without product differentiation may not be realistic. More recently, Fu and Tan developed a theoretical model with product differentiation to study the impact of different forms of airline cooperation ( 4 ). Their model focuses on the differences between ATI and JV agreements. Tan and Zhang use the multinomial logit (MNL) demand system, which is widely used to model air travel (see Garrow for a comprehensive review), to evaluate the impact of JVs on different kinds of city-pair markets such as the behind-to-gateway market between Pittsburgh and London ( 5 , 6 ). They show that the airfares of online flights increase, and the airfares of codeshare flights decrease, after forming JVs in the behind-to-gateway markets.

To the best of the authors’ knowledge, the outcome that the airfares of online flights in behind-to-gateway markets get higher after forming a JV has not yet been identified in previous empirical studies ( 1 , 7 ). Papers by Calzaretta et al. and Brueckner et al. mainly show that, as airline carriers improve their cooperation, airfares for the interline or codeshare flights fall ( 8 , 9 ). Bruckner and Singer also show that the airfares of both ATI and JV are similar to the airfares of online flights in the connecting markets, and they emphasize the two main effects of a JV: airfares increase in the inter-hub markets, while airfares decrease in codeshare/interline flights ( 2 ). The current empirical study, based on a differences-in-differences (DID) methodology, identifies the new costs of JVs to consumers from online flights in the behind-to-gateway markets. The empirical strategy is similar to the one used by Luco and Marshall who study the impact of vertical mergers between the upstream companies (e.g., the Coca-Cola Company and PepsiCo) and the downstream bottlers in the U.S. carbonated-beverage industry ( 10 ).

Competitive Effects of JVs

Figure 2 decomposes the network in Figure 1 and illustrates the behind-to-gateway market between Pittsburgh and London, with the straight lines representing AA and the dashed line representing BA. Consumers in this city-pair market can choose between the AA-BA codeshare flights and the AA online flights. Current empirical literature implies that the airfares of the codeshare flights would decrease if AA and BA form a JV because of the elimination of double marginalization. However, an interesting question is how the airfares of the AA online flights would change. Since these two kinds of flights are differentiated and competing for the same set of customers in the same market, it is reasonable to believe that the JV can also affect AA’s online flights.

The flights of American Airlines (AA) and British Airways (BA) in the city-pair market between Pittsburgh and London.

In a separate paper, the authors develop a game-theoretic model to show that JVs reduce airfares of codeshare flights and increase airfares of online flights in the behind-to-gateway markets, based on the MNL demand system ( 5 ). Also, these two airfares converge to the same level following a JV when the two carriers have similar product qualities and marginal costs. One way to understand this result is that AA may try to use lower airfares of online flights to incentivize BA to lower its airfares so that AA can alleviate the double marginalization problem in the codeshare flights (see Hendricks et al. for a similar result in a model without product differentiation) ( 11 ). Another way to see this is that potential double marginalization in the codeshare flights generates higher costs for AA, causing AA to lower its airfares of online flights so that more consumers can take the more efficient online flights. As a JV fully integrates the two carriers, they no longer have incentives to price noncooperatively for the codeshare flights, and the double margins are eliminated. They simply choose airfares for both kinds of flights to maximize joint profits after forming a JV. Therefore, lower airfares of online flights are not needed anymore, and a JV increases airfares of online flights and reduces airfares of codeshare flights. As airfares of online flights increase, it is possible that these increases are so significant that airfares of codeshare flights also get higher (see Salinger for a detailed analysis of this problem) ( 12 ). The authors tend to believe this extreme result is less likely and is generally inconsistent with existing empirical evidence, which often concludes that JVs reduce airfares of codeshare flights. Another possible outcome is that the decreases in the airfares of codeshare flights may be so significant that they also reduce the airfares of online flights. Fu and Tan use a linear demand model with product differentiation and show that airfares of both codeshare flights and online flights under a JV are lower than airfares under simple codeshare without ATI ( 4 ).

In summary, although JVs can reduce or eliminate the double marginalization problem in the codeshare flights, their impact on online flights is uncertain. Different theoretical models illustrate that JVs can lead to higher or lower airfares of online flights in the behind-to-gateway markets. The next two sections will introduce the Oneworld transatlantic JV and the data used for the empirical analysis, and develop a DID analysis to evaluate the impact of the Oneworld transatlantic JV on online flights in the behind-to-gateway markets.

Brief Background and Data

In July 2010, AA, Finnair (AY), BA, Iberia (IB), and Royal Jordanian (RJ), five major carriers from the Oneworld alliance, received approval for their ATI ( 13 ). In October 2010, BA, IB, and AA officially launched their JV. Note that 2010Q3 is considered as the quarter when the JV started following the previous discussions about the equivalence between JV and ATI in recent years. Since AY had already entered into an ATI agreement with AA in 2002, an attempt is made to evaluate the impact of new members, BA and IB, on the U.S./U.K./Spain/France markets. (RJ’s service is negligible in this region). Because of a large amount of empirical research about the impact of JVs on codeshare flights, the focus is on evaluating the impact of the Oneworld transatlantic JV on online flights in the behind-to-gateway markets. To simplify the notation in the following analysis, BA and IB are also combined, which were officially merged in January 2011.

Flight information in the connecting markets is from the Airline Data Inc’s “GatewaySup” survey from 2008 to 2013. It is drawn from U.S. DOT’s DB1B international data which contain a 10% random sample of itineraries involving a U.S. airport. Each observation in the database contains information on airfare, the number of passengers (original record times 10), operating and marketing carriers, the number of coupons, fare class, the route (which includes the origin airport, the connecting points, and the destination airport) and the total distance at the itinerary level by quarter. The database provided by Airline Data Inc is often used in academic research (e.g., papers by Calzaretta et al., and Ito and Lee) ( 8 , 14 ). Like many other studies using U.S. DOT’s DB1B international data, trips without any U.S. carrier segment are unobservable. This does not affect the current study, because the existing data have sufficient information about codeshare flights, and only the impact of the JV on AA’s online flights is studied. Since BA’s online flights are unobservable in this survey, it is not possible to examine whether its online flights are affected by the JV in a similar manner. However, as discussed in Brueckner and Singer, foreign carriers and U.S. carriers have similar airfares, and using only U.S. carriers’ airfares of online flights is a reasonable approach in studying connecting markets ( 2 ). Therefore, it is expected that the JV has a similar impact on BA’s online flights.

The data is processed following standard approaches in the literature. Only round trips with no more than eight segments are included, and each travel leg cannot have more than four segments. Itineraries with fares less than $200 are excluded, since these tickets may be purchased using frequent flier programs. Also, only economy class itineraries are included. Additionally, AA’s regional carriers are re-coded with AA’s carrier code, since regional carriers are not involved in determining airfares. Airports are grouped into cities, and markets are defined as city pairs following U.S. DOT’s Master Coordinate table ( 15 ).

Airline Cooperation

Following the results from Ito and Lee, three types of flights in the behind-to-gateway markets are identified, based on the operating carriers of the segments of the itineraries ( 14 ). Each city-pair market in the sample must have online flights offered by AA (type 1 flight), and two other categories of flight are identified: codeshare flights between AA and BA (type 2 flight) and codeshare flights between AA and non-BA carriers (type 3 flight). Based on the previous discussion, it is assumed that the carriers started their joint pricing after receiving ATI in 2010Q3. Therefore, 2008Q1–2010Q2 is the pre-JV period, and 2010Q4–2013Q4 is the post-JV period. Data from 2010Q3 is dropped in the regression analysis since it is not possible to determine whether the itineraries were before or after the JV was approved. It is anticipated that carriers’ pricing would change from noncooperative to fully integrated in these two periods.

Descriptive Statistics and Variables

A total of 687 city-pair markets in the U.S./U.K./Spain/France region are identified, where AA offers connecting online flights. These markets are all between U.S. cities and five major European cities (London, Manchester, Madrid, Barcelona, and Paris). It is also ensured that these markets did not have AA nonstop flights in the pre-JV period.

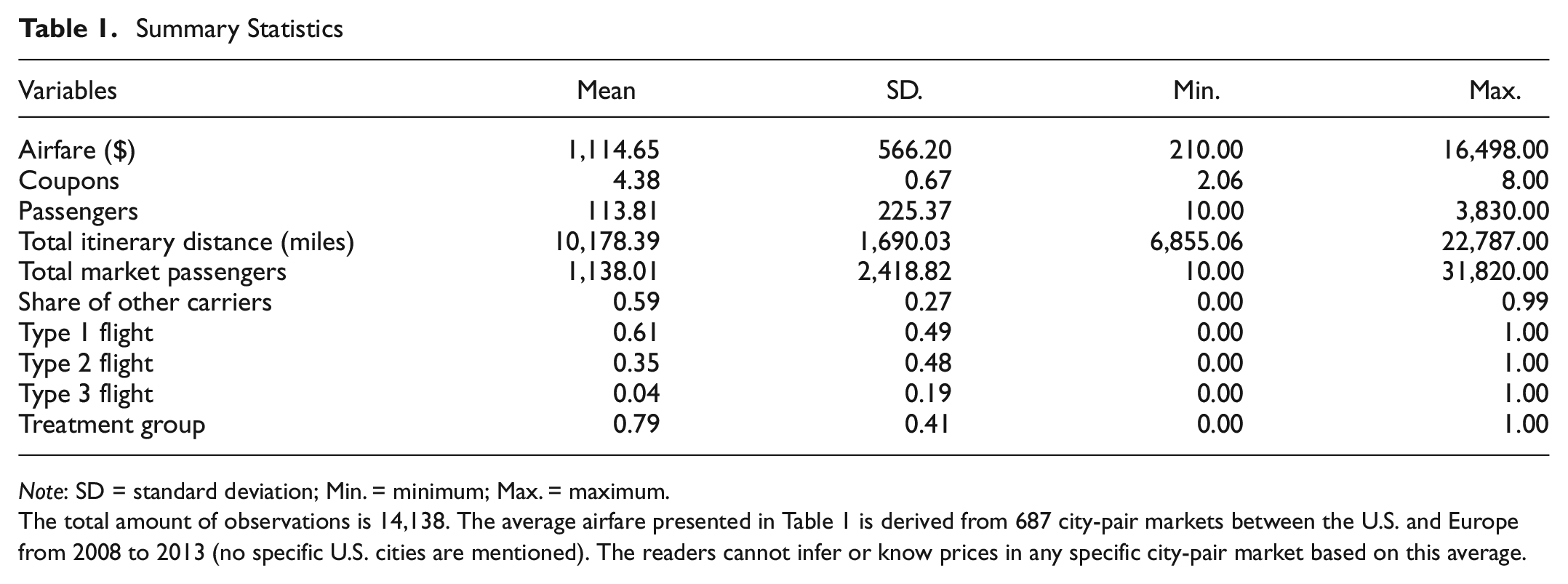

Based on the three types of flight, itineraries are aggregated up to the type-market-quarter level by computing passenger-weighted average variables (airfare, coupons, total itinerary distance), and the total amount of observations (i.e., aggregate itineraries) is 14,138. Summary statistics for the key variables are shown in Table 1. Note that, following the paper by Gillespie and Richard, this regression analysis also reports results using individual itineraries ( 16 ). Itineraries that are different from the three types of flights are dropped, but information from these itineraries is still used to calculate the total number of passengers and share of carriers other than AA and BA in the city-pair markets.

Summary Statistics

Note

The total amount of observations is 14,138.

Table 1 shows that, for each aggregate itinerary, the average airfare is $1,114.65 and the average number of coupons is 4.38. On average, each aggregate itinerary has 113.81 passengers and a total distance of 10,178.39 mi. The total number of roundtrip passengers is used to measure the size of the market, and the market share of carriers other than AA and BA is used to measure the level of competition from other carriers in the markets. It is also noted that these two variables may not be accurate for some city-pair markets because the DB1B international data do not have information about flights operated only by foreign carriers. Foreign carriers are only observed when they offer connecting flights with some U.S. carriers. However, the two variables do not significantly affect the results, and the main conclusion still holds if they are dropped in the regression analysis. Additional information about the city population and income will be incorporated into analysis in the future.

Lastly, three dummy variables, type 1, type 2, and type 3, are used to identify whether the aggregate itinerary is an AA online flight, an AA-BA codeshare flight, or an AA-non-BA codeshare flight. Since there is only a small amount of AA-non-BA flights in this kind of market, to find a suitable control group for AA-BA flight is quite difficult with the current sample. The variable treatment group identifies whether an aggregate itinerary is from a city-pair market affected by the JV or not. If a market has both type 1 and type 2 services before and after forming a JV, then each observation in such a market has the dummy variable treatment group equal to one. If an observation is from a city-pair market without type 2 services, then this observation is in the control group unaffected by the JV. The current sample includes large amounts of observations that are affected and also those that are unaffected by the JV.

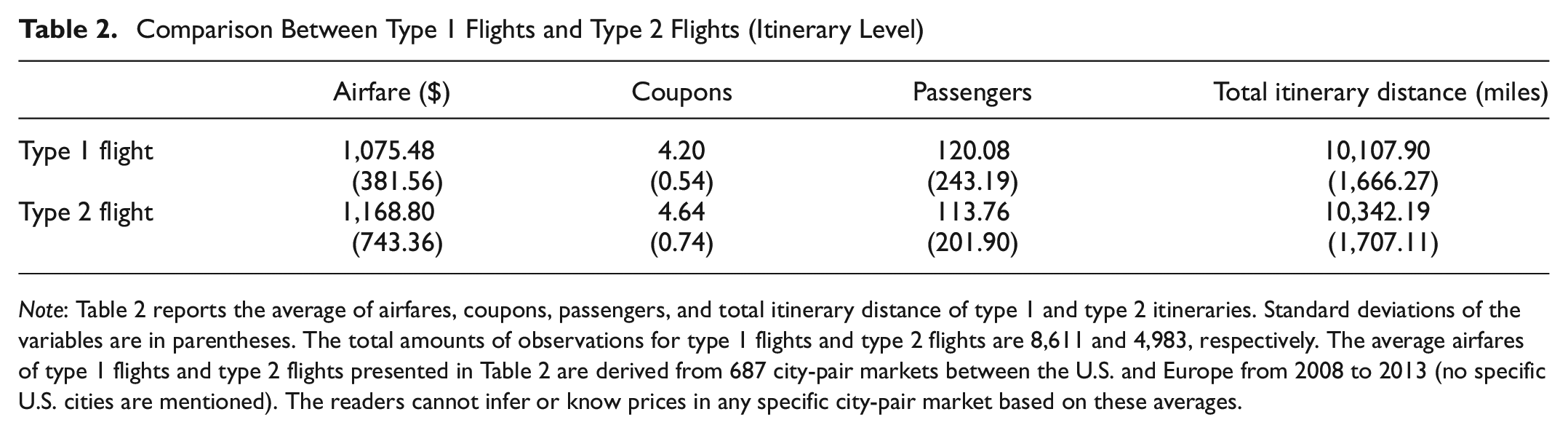

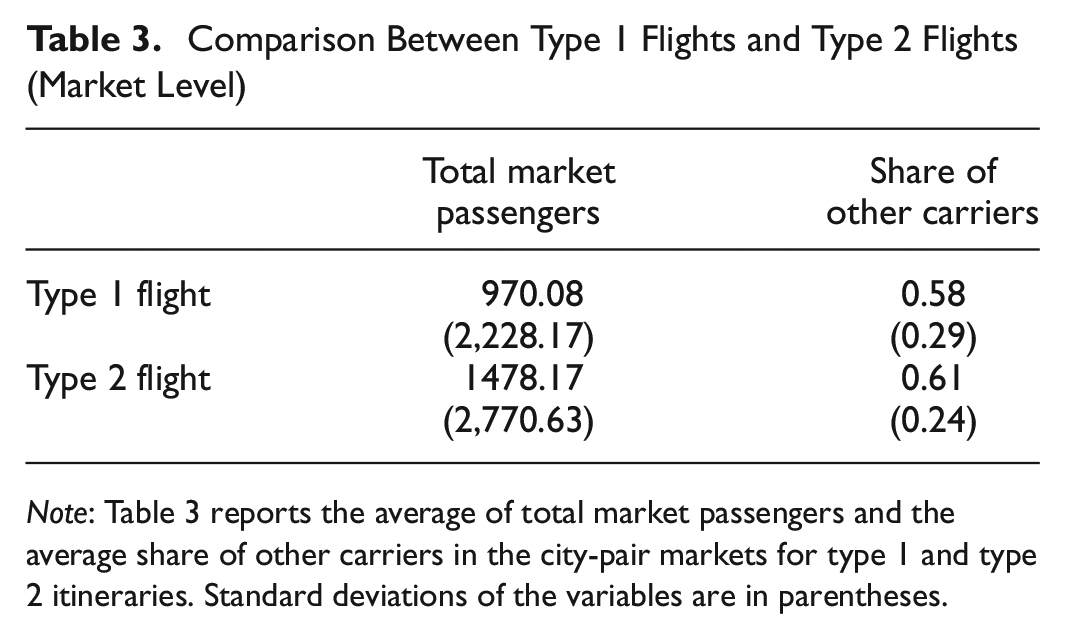

AA online flights and AA-BA codeshare flights are also compared in Tables 2 and 3. Table 2 reports the itinerary-level characteristics of AA online flights and AA-BA codeshare flights. Table 3 reports the market-level characteristics of AA online flights and AA-BA codeshare flights. It can be seen that codeshare flights are, on average, more expensive than online flights, with more coupons and longer distances. Also, more passengers choose online flights. In relation to the market-level comparison, it is seen that codeshare flights are offered in the markets with higher total passengers and more competition from other carriers.

Comparison Between American Airlines (AA) Online Flights and American Airlines-British Airways (AA-BA) Codeshare Flights (Itinerary Level)

Note

Table 2 reports the average of airfares, coupons, passengers, and total itinerary distance of type 1 and type 2 itineraries. Standard deviations of the variables are in parentheses. The total amounts of observations for AA online flights and AA-BA codeshare flights are 8,611 and 4,983, respectively.

Comparison Between AA Online Flights and AA-BA Codeshare Flights (Market Level)

Note

Table 3 reports the average of total market passengers and the average share of other carriers in the city-pair markets for type 1 and type 2 itineraries. Standard deviations of the variables are in parentheses.

Figure 3 shows the evolution of the airfares of AA’s online flights (type 1) versus the airfares of AA-BA codeshare flights (type 2) in markets that are affected by the JV (treatment group). Before 2010Q3, it is possible to see a pattern that online flights are cheaper than codeshare flights. It is consistent with the theoretical model with MNL demand which shows that, when carriers have similar marginal costs and qualities of services, online flights have airfares lower than codeshare flights. After 2010Q3, it is seen that airfares of these two types of flights were converging, and, gradually, online flights were even slightly more expensive than codeshare flights. It provides some preliminary evidence that a JV can decrease the airfares of codeshare flights and increase the airfares of online flights. However, it is noted that the global financial crisis in 2008 might also reduce airfares before 2010. A simple comparison of airfares before and after the formation of the JV in the treatment group cannot accurately measure the impact of the JV.

Average airfares of American Airlines (AA) online flights and American Airlines-British Airways (AA-BA) codeshare flights in markets exposed to joint venture (JV).

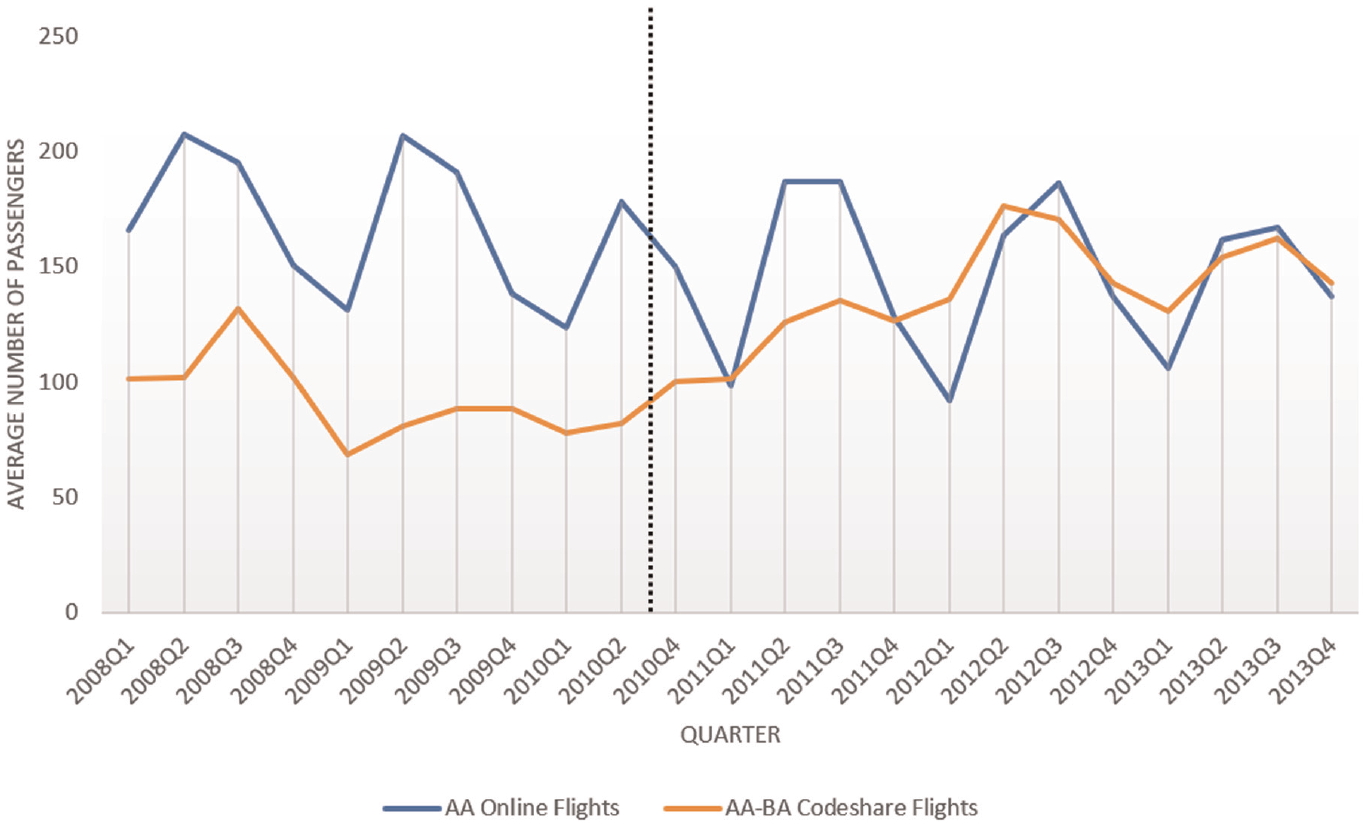

Figure 4 illustrates the trends of the average number of passengers of AA online flights and AA-BA codeshare flights. The average number of passengers using AA online flights slightly decreased after forming the JV, while AA-BA codeshare flights attracted a lot more consumers after 2010Q3. It also supports the discussion that theoretical models in the airline industry should incorporate the feature of product differentiation. Airfare is not the only factor in determining the consumers’ choices. Even though codeshare flights were more expensive than online flights without JV, consumers still chose codeshare flights because of other considerations like schedules or brands. Figure 4 also illustrates the importance of understanding the impact of JVs on online flights. Since a higher number of consumers were using online flights before 2010Q3, a small increase in the airfares of online flights, following the theoretical model with MNL demand, can lead to a high impact on consumer welfare.

Average number of passengers of American Airlines (AA) online flights and American Airlines-British Airways (AA-BA) codeshare flights in markets exposed to joint venture (JV).

Differences-In-Differences (DID) Analysis

The DID analysis attempts to simulate an experimental research design. The treatment group includes city-pair markets that were exposed to the JV, and the control group includes city-pair markets that were unaffected by the JV. The control group helps to provide a counterfactual for what would have happened to the treatment group in the absence of the JV. By comparing airfare changes of the online flights in the treatment group to the airfare changes of the online flights in the control group from 2008 to 2013, it is possible to more accurately measure the impact of the JV on online flights.

In this model, dummy variable

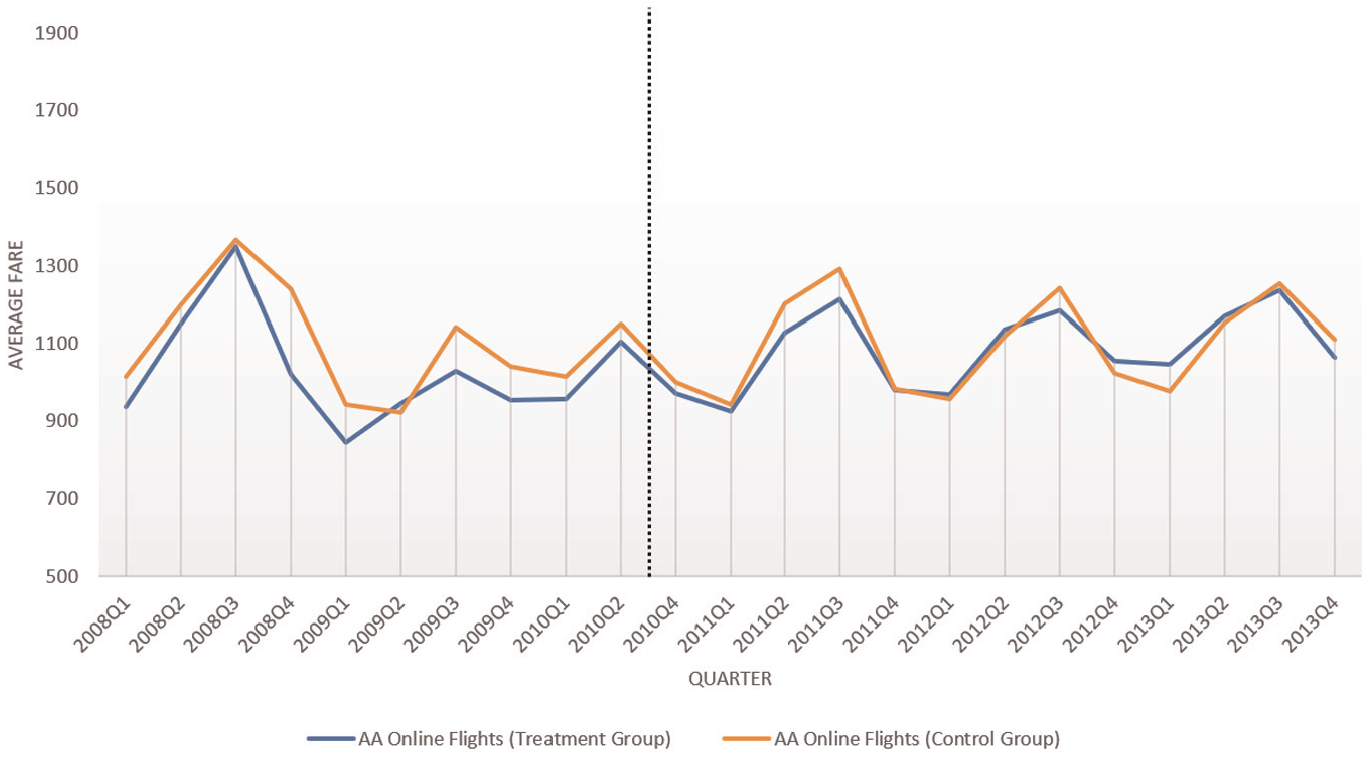

The key assumption in the DID analysis is the parallel trend, which is a critical requirement for identifying a valid control group. The airfares in the treatment group should have the same trend as the airfares in the control group before the formation of the JV. Figure 5 illustrates that the average airfares of the online flights, in both the treatment and the control groups, followed a similar trend before 2010Q3. The regression model with leads and lags is also estimated and no evidence is found of differential trends before forming the JV (more details of these findings are provided in the next section). All these results suggest that the treatment group and the control group followed a similar trend before the JV; therefore, a reliable control group has been identified. Moreover, it has been found that the carriers continued to offer both codeshare flights and online flights in most of the city-pair markets after forming the JV in the treatment group. Only about 6% of the markets no longer observe AA-BA codeshare flights or AA online flights after the JV, and most of these city-pair markets have relatively small market sizes with scarce observations of AA online flights or AA-BA codeshare flights before 2010Q3. These two kinds of flights may fail to be observed after 2010Q3 because of other demand shocks unrelated to the JV, or because the DB1B data only contain a 10% random sample of itineraries. Therefore, AA did not select specific city-pair markets for the JV, and the authors believe that the potential selection issue is not a major concern in the DID analysis.

The evolution of airfares of American Airlines (AA)’s online flights in the treatment and control group.

Results and Discussion

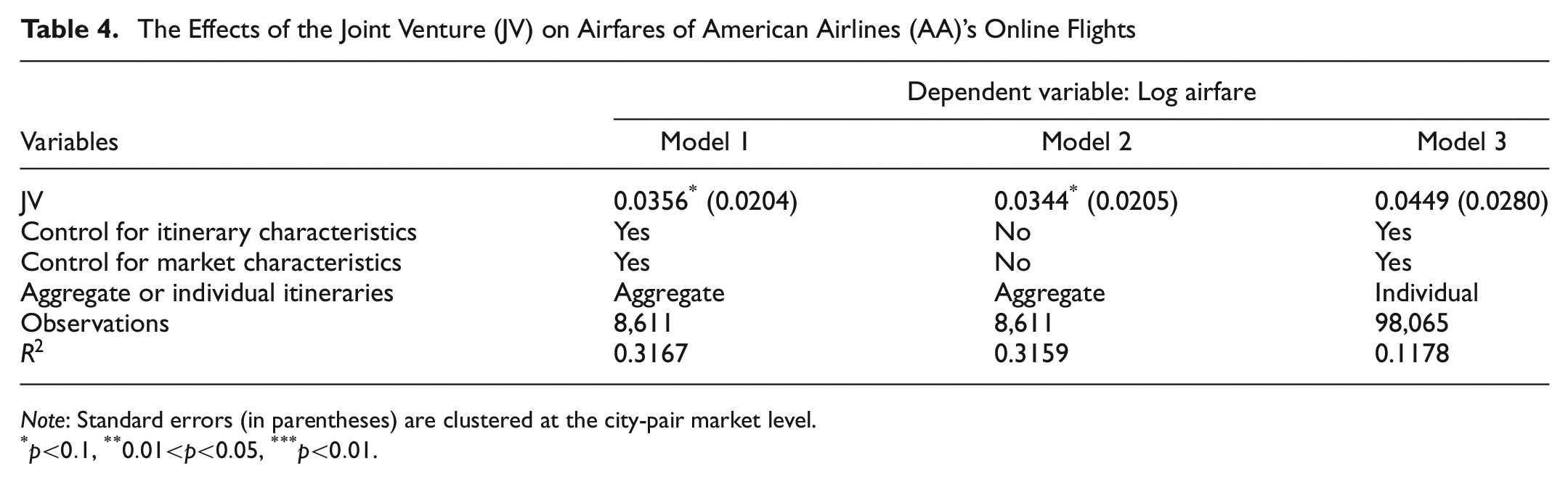

Table 4 shows the empirical results, where Model 1 uses the aggregate itineraries for AA’s online flight, Model 2 uses the aggregate itineraries and excludes all control variables, and Model 3 uses individual itineraries. Model 1 shows the main result that the Oneworld transatlantic JV has increased the airfares of AA’s online flights in behind-to-gateway markets by 3.56%. Other empirical studies (e.g., papers by Calzaretta et al., and Brueckner and Singer) repeatedly show that JVs can reduce airfares of codeshare flights in connecting markets by about 7% ( 2 , 8 ). Since the number of passengers who chose online flights was larger than the number of passengers who chose codeshare flights without the JV, the costs from higher airfares of online flights might have offset many of the benefits from lower airfares of codeshare flights for consumers.

The Effects of the Joint Venture (JV) on Airfares of American Airlines (AA)’s Online Flights

Note: Standard errors (in parentheses) are clustered at the city-pair market level.

The robustness of this analysis is further explored with different specifications. Model 2 and Model 3 show that the Oneworld transatlantic JV has increased airfares of AA’s online flights by 3.44% and 4.49%, respectively. Like the results from Gillespie and Richard, models with aggregate itineraries and models with individual itineraries can lead to different estimations of the parameters ( 16 ). Model 3 shows that the JV has a slightly higher impact on the airfares of online flights, though its p-value is 0.109. Expanding the sample size to all European countries and including better control variables (like population and average income) may lead to a more accurate estimation of the impact of the JV.

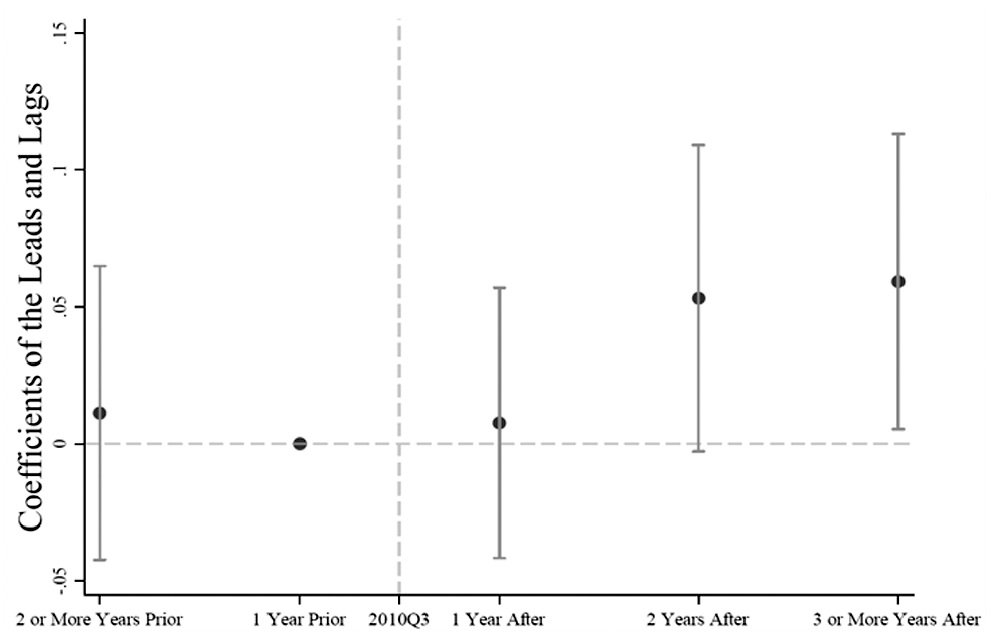

Lastly, the baseline empirical model with leads and lags is estimated to study whether there were differential trends before forming the JV and when the airfares of AA’s online flights in markets exposed to the JV started to change (see Luco and Marshall for details of this approach) ( 10 ). Figure 6 shows no statistical evidence that online flights in the treatment and control groups followed different trends before the JV. It also shows that the airfares of AA’s online flights did not immediately change after forming the JV. The airfares of online flights in markets exposed to the JV took more than a year to increase by about 5%. Many time-consuming institutional changes caused by the JV (e.g., building a revenue-sharing system) may delay the impact on airfares of online flights.

Dynamics of the impact on airfares of American Airlines (AA)’s online flights.

Concluding Remarks

The rapid development of JVs in the international airline industry has helped more and more airline carriers to coordinate their airfares. Existing literature indicates that JVs can reduce airfares for consumers in connecting markets and increase airfares for consumers in inter-hub markets. The focus of this study is on one set of behind-to-gateway markets with both online flights and codeshare flights which is largely overlooked in the literature. In these markets, the competition between online flights and codeshare flights can lead to different results concerning the impact of JVs. Specifically, JVs may reduce airfares of codeshare flights and increase airfares of online flights. U.S. DOT’s DB1B international data is used, and a DID analysis is developed to show that the Oneworld alliance’s transatlantic JV increased airfares for online flights in the behind-to-gateway markets. Therefore, U.S. DOT can better protect consumers by carefully evaluating this possibility of airfare increase in the behind-to-gateway markets when reviewing new JV applications.

There are several directions for future research. The authors will expand the sample size to include all European countries and evaluate the impact of JVs on codeshare flights to see if the DID analysis would lead to consistent and robust conclusions. In addition, since JVs can help carriers to coordinate their schedules and provide better services, it is necessary to incorporate potential quality changes of the flights into the analysis and develop a structural model to accurately measure the impact of JVs on consumer welfare in the connecting markets. Moreover, further theoretical studies that compare different models with product differentiation can help understand the impact of JVs in different markets.

Footnotes

Acknowledgements

The authors thank Eric Amel, Frank Berardino, John Carlsson, Xiao Fu, Nicholas Janota, Rajat Kochhar, Michael Leung, Jonathan Libgober, Kevin Neels, Robert Samis, Liying Yang, Anming Zhang, and the participants in the ACRP regular meetings for their valuable comments and suggestions. The authors are particularly grateful to Robert Samis of the Federal Aviation Administration (FAA) and Lawrence Goldstein of the Airport Cooperative Research Program (ACRP) for helping them to get access to the DB1B international data.

Author Contributions

The authors confirm contributions to the paper as follows: study conception and design: G. Tan, Y. Zhang; data collection: G. Tan, Y. Zhang; analysis and interpretation of results: G. Tan, Y. Zhang; draft manuscript preparation: G. Tan, Y. Zhang. All authors reviewed the results and approved the final version of the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Yinqi Zhang gratefully acknowledges financial support from the Transportation Research Board’s ACRP Graduate Research Award, which is sponsored by FAA and administered by ACRP. The authors also thank the Institute for Economic Policy Research at the University of Southern California for sponsoring the data subscription.