Abstract

Constraints on policy autonomy structurally stem from uneven capitalist development and pre-date neoliberalism, but their degree of restrictiveness varies depending on the balance of power among major states and the nature of their dominant classes. The analysis of China’s overseas development finance (CODF) reveals how its contender state-society complex relaxes external constraints on industrial policy autonomy. CODF expands finance for underfunded sectors, allows performance requirements, prioritizes the public sector, relaxes macroeconomic policies, and institutes a long-term derisking approach. It creates space for Southern countries’ political agency and terrain to grow a counterhegemonic historical bloc to transcend US-led (neo)liberal order. Still, the realization of CODF’s potential is contingent on political configurations of beneficiary countries and on the emergence of popular national forces capable of addressing the legacies of neoliberalism.

Keywords

1. Introduction

The revival of interest in structural transformation and the recognition of the role of industrial policy in the development process (e.g., Chang and Andreoni 2020; Stiglitz et al. 2009) have focused attention on the constraints of neoliberal global governance on policy autonomy, thus giving rise to the concept of development policy space (e.g., Mayer 2009). The literature focuses on international institutions shaped by core countries, concluding that the general trend is a shrinking of the policy space to a historical low. Strikingly, analysis has stopped short of considering the implications of involvement of the emerging countries in global governance on the policy autonomy of developing countries.

In turn, much has been written about how China’s international economic rise will transform the current structure of global economic governance (e.g., Petry 2020; Stephen and Parízek 2019; Strange 2011). Nevertheless, the debate has neglected the developmental impact of this role and has been shaped by an implicit normative assumption that takes for granted the inherent virtue of the international neoliberal order (e.g., Schweller 2011).

In particular, China has become the largest world economy in terms of purchasing power parity, and it became the leading trade power in terms of number of countries for whom it is the first partner. In the domain of development finance, it has become the largest public source of lending (Horn et al. 2021), driven by a mix of domestic political-economic underpinnings and strategic policy initiatives (Liu 2023). Persistent current account surpluses have generated vast foreign currency reserves, providing liquidity for overseas lending. Concurrently, industrial capacity in sectors like energy and transport infrastructure soared after emphasizing domestic investment-led growth following the 2008 crisis, thereby permitting firms to export part of the accumulated productive capacities abroad. China’s overseas development finance (CODF) also contributes to secure stable supplies of critical commodities (e.g., through direct access, trade route, and financial and monetary arrangements). Finally, strategic government policies—from the early 2000s’ Going Out strategy to the Belt and Road Initiative (BRI)—coordinate these push factors beyond profit making to advance political and economic objectives (e.g., Alshareef 2024; Moses et al. 2023).

Situated at the crossroads of discussions on development policy space and China’s role in global governance, this article assesses the ramifications of China’s mode of regulation of international economic relations on developing countries’ autonomy to implement structural transformation strategy by taking CODF as a case study. Structural transformation refers to the dynamic reallocation of economic resources (labor, capital) from low to high productivity sectors (mainly manufacturing), which leads to sustained productivity, income growth, and changes in an economy’s output composition. This process historically characterized industrialized countries during their development as they transitioned from agrarian to industrial economies (Kuznets 1966). In this process, states proactively play four key roles: (1) a regulator of capital and merchandise flows through tariffs, conditional subsidies, capital account regulations, and the like; (2) a producer through State-Owned Enterprises (SOEs); (3) a consumer through public procurement; and (4) a financial agent influencing and directing the allocation of credit (Peres and Primi 2009). The accomplishment of these roles requires an international environment that permits enough national policy autonomy.

To attain its findings, the article mainly investigates empirical works on CODFs that have discussed their developmental impacts (e.g., Chen et al. 2020; Corkin 2016; Dreher and Fuchs 2016; Chin and Gallagher 2019; Humphrey and Chen 2021; Malik et al. 2021; Moses et al. 2023) but have seldom focused the analysis on effects on the development policy space (e.g., Kaplan 2021). This current research therefore scrutinizes the literature to compile dispersed empirical elements on CODF’s features influencing beneficiary states’ freedom to use different tools of industrial policy within a structural transformation development strategy.

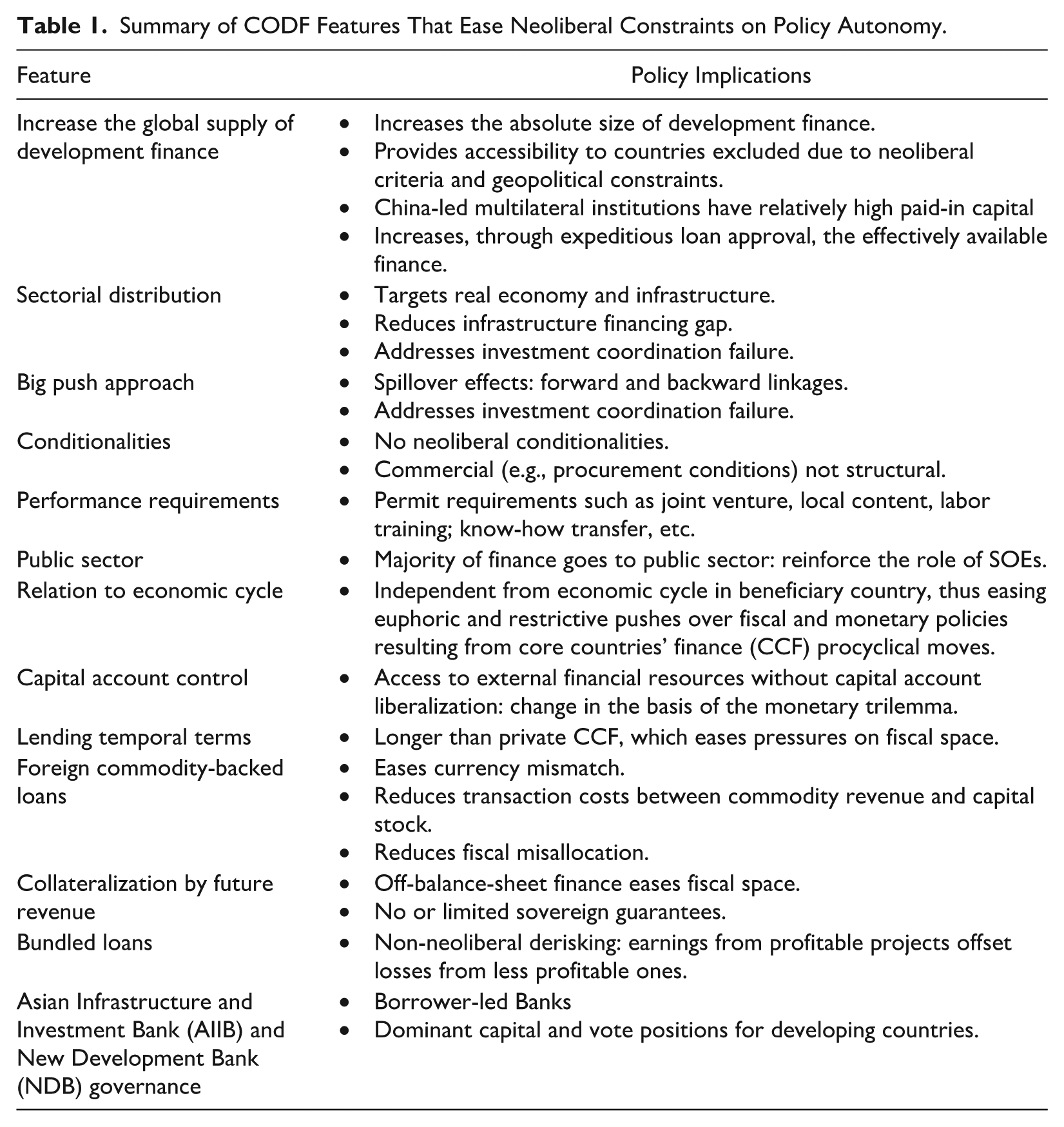

Conceptually, the article makes two contributions. First, it historicizes the concept of development policy space by arguing that peripheral autonomy is structurally constrained by capitalism’s uneven development, and core countries have been deploying policy constraints well before neoliberalism, and it argues that the degree of restrictiveness fluctuates depending on the balances of power between competing sociopolitical projects. Herein it is argued that the international role of China as contender state underpins a historical change that significantly eases neoliberal political and institutional constraints on Global South policy autonomy, including in the domain of development finance (see table 1). However, this does not automatically translate into effective transformative outcomes. The new space must be operationalized within an enabling policy framework oriented toward structural transformation in the beneficiary countries—a precondition that is not usually present in much of the Global South so far. Consequently, the realization of CODF’s potential hinges critically on domestic political configurations—specifically, the preferences of the dominant class and the composition of its broader sociopolitical coalitions, both within and beyond national borders.

Summary of CODF Features That Ease Neoliberal Constraints on Policy Autonomy.

Second, this effect of China’s ascent is interpreted through its contender state-society complex structure (Van der Pijl 1998, 2012), wherein the state orchestrates structural transformation through strategic industrial policy interventions (Breslin and Gabusi 2024). Consequently, China has an interest in maintaining and expanding its policy autonomy at the global level (Alshareef 2023; Strange 2011).

Section 2 introduces the theoretical framework. Section 3 discusses CODF’s features that increase the effective supply and accessibility to development finance in vital sectors. Section 4 analyzes key CODF’s characteristics that ease restrictions on policy instruments normally deployed within structural transformation strategy. Section 5 discusses CODF’s debt sustainability framework and coordinated credit space approach. Section 6 discusses how Chinese-led multilateral institutions have created spaces wherein the Global South can exert political power. The conclusion emphasizes the decisive role of beneficiary countries in realizing the potential of China’s international role.

2. Development Policy Space Beyond Neoliberalism: Capitalism’s Structural Constraints and the Rise of a Contender State

Development policy space refers to the ability of a country to exercise its own policy choices and the degree of freedom it has to design and implement policies in areas such as trade, investment, industrial development, social policy, and environmental protection (United Nations Conference on Trade and Development [UNCTAD] 2006).

This concept has gained prominence in response to the proliferation of both de facto and de jure neoliberal constraints (Mayer 2009) on the very industrial policy instruments that were used by core countries during their early development phases (Chang 2002). First, the access to the CCF has been accompanied by policy conditionalities that narrow beneficiary states’ ability to adopt industrial policy because of financial deregulation, privatization, budgetary austerity, trade liberalization, and so forth (e.g., Gabor 2021; Brunswijck 2019). Moreover, the rise of the Wall Street Consensus and the involvement of global institutional investors in financing infrastructure through derisking regulatory framework requires a reorientation of the fiscal and monetary policies to ensure steady cash flows for finance capital. It deepens the disciplinary stranglehold of institutional investors on policy autonomy and renders asset managers important stakeholders in national policy deliberations (Gabor 2021).

Second, the signing of the World Trade Organization agreements, followed by series of US and EU trade and investment agreements (e.g., Alshareef 2023, 2019), signaled the institutionalization of neoliberal policies into supranational legal and quasi-legal commitments, with enforcement mechanisms that go from investor-state dispute mechanisms to economic sanctions (Gill and Cutler 2014).

The literature on development policy space has extensively documented restrictive effects of neoliberal institutions on policy autonomy while also highlighting the remaining room in which to maneuver to implement industrial policy. However, this literature often lacks historical depth because it tends to limit its analysis to the neoliberal era and, strikingly, stops short of considering the expansion of policy space enabled by the emerging economies employing developmentalist strategies. This omission invites three critical interventions.

First, the policy autonomy of the Global South is structurally squeezed by their dependent position in the global dynamics of uneven capitalist development rather than by an extraordinary neoliberal mode of governing global economic relations. The objects of policy making—that is, the economic processes in terms of production, circulation, and distribution—are transnational and embedded in the global capitalist market, which inherently develops advanced core regions and underdeveloped peripheries, both articulated in hierarchical dependency relations. Peripheries occupy a lower position in the international division of labor and are often subject to structural constraints like technological dependence, unequal exchange and deteriorating terms of trade, and financial dependency (for a literature review, see Kvangraven 2021).

Second, neoliberalism needs to be grounded in sociopolitical struggles and their articulation at different geographical scales. The capital accumulation process does not automatically perpetuate itself but requires the application of political power and institutional mechanisms reflecting specific class interests (Cutler 2014). Rather than a mistaken ideology falling from the sky, neoliberalism embodies interests of transnational finance capital and is part of specific political adjustment to the crisis of corporate liberalism that crystallized during the 1960s (Overbeek and van der Pijl 1993). Accordingly, constraints on policy autonomy are integral to the new-constitutional disciplinary neoliberalism that transforms the conduct of public policy in accordance with the interests of transnational capital and monopoly profits, and subordinates national sovereignty to the core-led supranational institutions (Gill and Cutler 2014) and their drive to extend commodification under their control.

Indeed, restrictions on policy space are neither novel nor unique to the neoliberal era. Core countries have consistently constrained the use of industrial policy instruments by peripheral regions through colonial capitulation treaties (Chang and Andreoni 2020). Colonial financial committees of imperial powers managed colonies’ budgets and their international debt payments (Bihr 2018; Laurens 2017).

An overlooked dimension that distinguishes neoliberalism is the attempt by the dominant classes of core countries to recalibrate their authority over the fragmented political landscape of the global capital accumulation process following the decolonization waves. Neoliberal reforms represent a de facto political intervention against state-led development because they dismantle domestic industrialization attempts, reestablish colonial trade patterns, and weaken state capacity (Cheng 2025). These changes have effectively eroded the (possibility for) material economic bases for political independence, thus providing a political leverage for core countries.

Third, the level of international restrictions has fluctuated over time and is contingent upon the balance of power and the compromises struck between different constellations of classes at different geographical scales. For instance, the post-World War II era witnessed the lowest degree of supranational constraints on the national policy autonomy in the context of the presence of the Soviet Union and the broader communist movement, the national liberation movements, and the relatively strong trade unions in core countries.

Currently, the international rise of China opens a new era as it relaxes the external, political, and institutional (as opposed to structural) constraints on the development policy space. This process results from its power-weighted national preference regarding global governance (Stephen and Parízek 2019) and the international projection of elements of its domestic political economy (Stephen 2014).

China’s preferences can be understood through the contender state-society concept (Van der Pijl 1998) that prevails in the latecomers resisting the peripheralization, wherein the state becomes the subject of social development to overcome the domestic underdevelopment. In the form of the Chinese Communist Party (CCP), a “state class” holds power over the state apparatus, leveraging its influence to guide and socialize capital accumulation (Van der Pijl 2012).

The reference to the state-society complex allows one to move beyond the limitations of approaches such as the developmental state or state capitalism when analyzing China. It seeks to avoid any monolithic understanding of Capital with a big “C,” as well as any ahistorical analyses of state while apprehending China’s contemporary structure (Desai 2010). It also circumvents the economic determinism prevalent in dominant critical approaches by recognizing the possibility for the political sphere to assert dominance over the economic sphere and to socialize the capital accumulation process. As Desai (2013) notes, contender states may be socialist or capitalist. Indeed, the state is embedded in a particular configuration of social forces that defines “the limits or parameters of state purposes” (Cox 1987: 105). While state intervention is an inherent feature of all class societies—including under neoliberalism—the political-economic nature of a social model is determined not solely by the degree of state intervention in the economy but, more crucially, by its sociopolitical orientation and the class interests it serves.

For instance, debates on China’s political economy have long been underpinned by a dichotomous and overly institutionalist framing of the state-market nexus. However, their contradictory relationship—articulated dialectically and mediated by the CCP (Breslin and Gabusi 2024)—is intrinsically tied to the objective of achieving structural transformation away from China’s peripheral position within the capitalist dynamics of uneven development. This effect has produced a distinctive market structure and a state anchored in a unique social matrix where profitability and price mechanisms, for example, function as allocative instruments subordinated to the imperatives of developing productive forces (Zou 2014) and advancing socialist primitive accumulation (Cheng 2020).

China’s contender state-society complex has produced a particular mode of integration in the international markets (McNally and Gruin 2017; Strange 2011), which has been subjugated to the development of a nationally integrated and modern industrial system (Amin and Bush 2014). Here it should be noted that the 2008 crisis signaled that its contender state’s compromise with the neoliberal transnational class project attained its historical limits. To avoid being diluted in the heartland-centered circuit of capital, as were the fates of previous contender states (Van der Pijl 1998), the power of the CCP and the role of the state in the economy have been consolidated over the past decade. Concomitantly, China has intensified its demand for the change of global governance (Stephen 2014: 928) to ensure “an expansion, rather than accepting a contraction, of ‘development space”’ (Strange 2011: 540). Concretely, Beijing has intensified its multichannel engagement in global economic governance to secure an international regulatory framework that aligns with its development model (Alshareef 2023, 2019), thus easing the international constraints on the Global South’s policy autonomy.

The contender state institutional features are observable in the CODF, wherein the state-party nexus assumes a determinant role in its operational framework. First, financial institutions are state owned, and appointments within policy banks are subject to the authority of the CCP (Liu, 2023). For instance, China Development Bank (CDB) operates as a state-owned shareholding corporation owned by four major shareholders, and all of its top-level executives originate from the state-party apparatus in the domain of development finance (Chen 2020).

Second, the political level not only oversees the selection of projects and sectors to be financed but it also shapes institutional framework governing the policy banks operations (Liu 2023; M. Chen 2021). According to the economist in-chief of the CDB, Chinese development finance fulfills state objectives while it uses market checks-and-balances functions but without being profit driven (Zou 2014).

China’s institutions, such as the CDB and the Export-Import (EXIM) Bank of China (China EXIM Bank), have their roots in the country’s domestic development strategy. They have been mobilized within a selective industrial policy framework targeting priority sectors and technological advancement while seeking structural transformation of the economy (Chen 2020, 2021; Chin and Gallagher 2019; Zou 2014). This logic has since extended beyond borders, thereby shaping the institutions’ roles in global development finance.

Third, the party-state nexus also defines the overarching objectives of the policy banks’ outward push (Chin and Gallagher 2019), employing that push as a tool to address a set of multiscalar political and economic contradictions, such as exporting what the literature claims to be industrial overcapacity, securing access to primary resources, and more (e.g., Moses et al. 2023). Notably, CODF functions as a strategic tool for recycling and rebalancing China’s vast foreign exchange reserves. Instead of letting these reserves—mostly held in US dollars or Treasury securities—sit idle, Beijing channels them through policy banks and dedicated investment vehicles (such as the Silk Road Fund) into concessional and commercial loans, equity stakes, and project financing. By underwriting infrastructure projects, China effectively converts its dollar reserves into income-generating assets abroad (Liu 2023).

Fourth, development finance is one of the major areas in which China has proactively engaged to restructure global governance following the 2008 crisis—through bilateral relations, the establishment of AIIB and the NDB, and the active participation in the core-led multilateral banks, such as the World Bank Group (Humphrey and Chen 2021; Humphrey 2015). CODF exemplifies how the internationalization of institutional features from China’s contender state-society complex is recalibrating the global political economy in ways that expand development policy space. For instance, it operationalizes the “sovereign leveraged funds” model—rooted in China’s own domestic financial practices—by enabling large-scale project lending that remains largely off the balance sheets of beneficiary countries (Liu 2023), thereby expanding their fiscal space. More broadly, this approach marks a significant departure from the prevailing neoliberal debt-sustainability framework, which tends to prioritize short-term macroeconomic equilibrium over long-term developmental objectives and often employs debt as a mechanism of economic and (geo)political discipline over recipient states.

Finally, CODF is also shaped by geopolitical challenges faced by China. The contender state emerges within a global context marked by the presence of a heartland state-society complex that exercises dominance over the global circuit of capital, thus systematically thwarting the emergence of rival powers. Indeed, confrontation is inevitable between the contender and the heartland state-society complexes, and all contender states in the pre-atomic bomb era had to confront on the battleground the core state who enlists other states as part of a balance-of-power policy (Van der Pijl 1998). The United States’ strategic rebalancing toward China underscores its escalating confrontation with Beijing, which it designates as a peer competitor and systemic rival.

In this context, CODF might be geoeconomically leveraged to counter US balance-of-power strategy since it offers incentives to beneficiary countries to consider Beijing’s political preferences (Alshareef 2024). More broadly, the political-economic frame of CODF coheres with Chinese foreign policy that emphasizes national sovereignty, the non-interference principle, and win-win development partnership, which is contrary to the US interventionist and security-focused approach. Indeed, China’s economic weight along with its internationalization approach—which provides room for developmentalist states in a context of the deepening neoliberal crisis—could constitute a tangible basis for the construction of what Cox (1983) calls a counterhegemonic international historical bloc that endeavors to transcend the US-led neoliberal order.

Still, the full realization of development outcomes derived from the policy autonomy brought about by the emergence of China’s contender state-society complex will depend on the emergence of popular national forces in the Global South—capable of addressing the legacies of neoliberalism in their own countries and negotiating the effective use of Chinese investments and finance (Cheng 2025).

3. Scaling Up Development Finance: CODF’s Role in Bridging Investment Gaps in Vital Sectors

CODF has significantly expanded the global supply of development finance—more than doubling its amount (Chin and Gallagher 2019)—while extending its spatial reach, mitigating geopolitical conditionalities, lengthening its temporal horizons, and channeling capital into critical sectors historically neglected by traditional institutions.

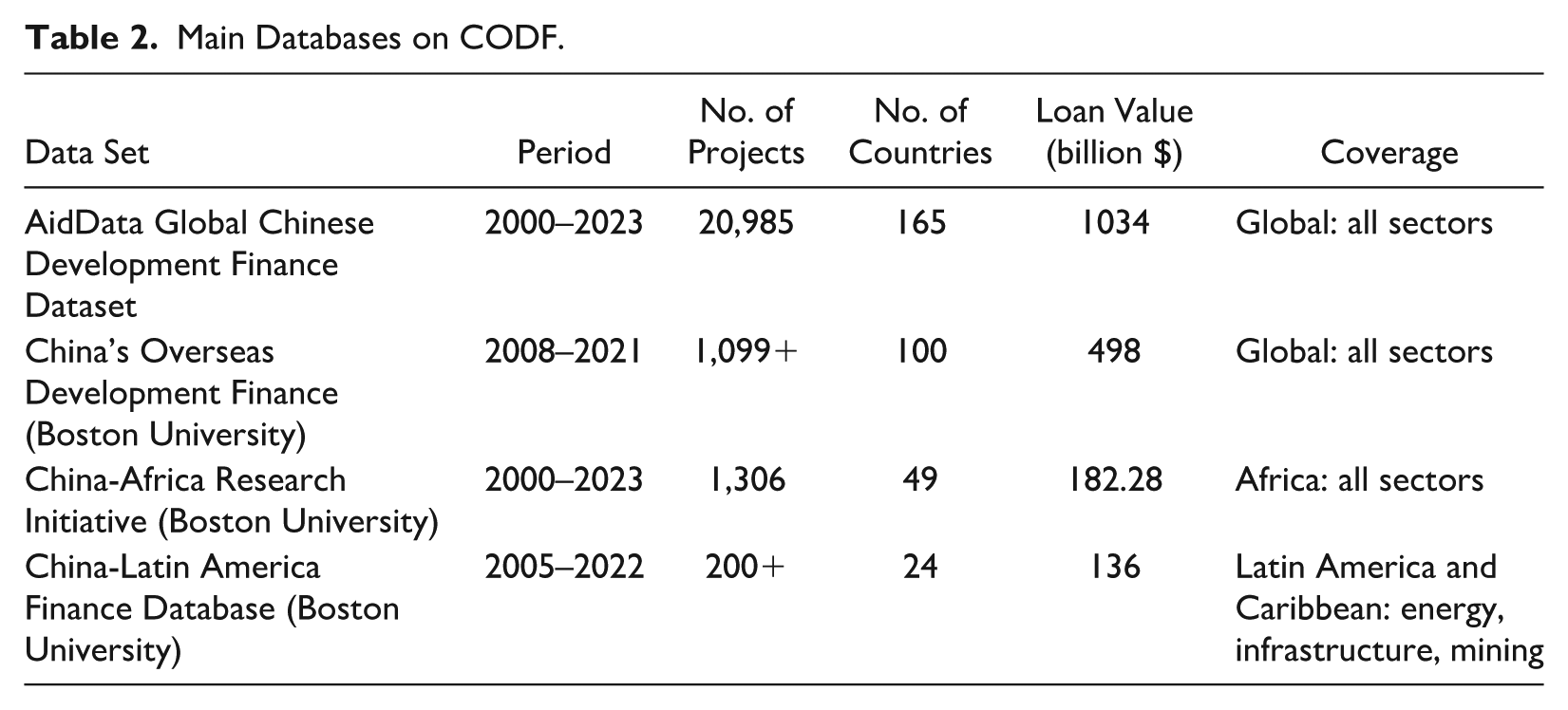

Bilateral lending—involving policy banks, commercial banks, SOEs, ministries, and a central bank—makes China the world’s largest official creditor, surpassing the World Bank and the IMF (Horn et al. 2021). Estimations of the value of bilateral flows vary depending on the data coverage. Table 2 lists major databases on CODF. One less explored avenue is the Chinese sovereign-backed overseas development, encompassing at least 19 funds with a total contribution of $213 billion in development finance. Their scale ranges from $500 million to $54.5 billion, and they primarily source their capital from the Ministry of Finance (MoF) or the policy banks (Larsen et al. 2023).

Main Databases on CODF.

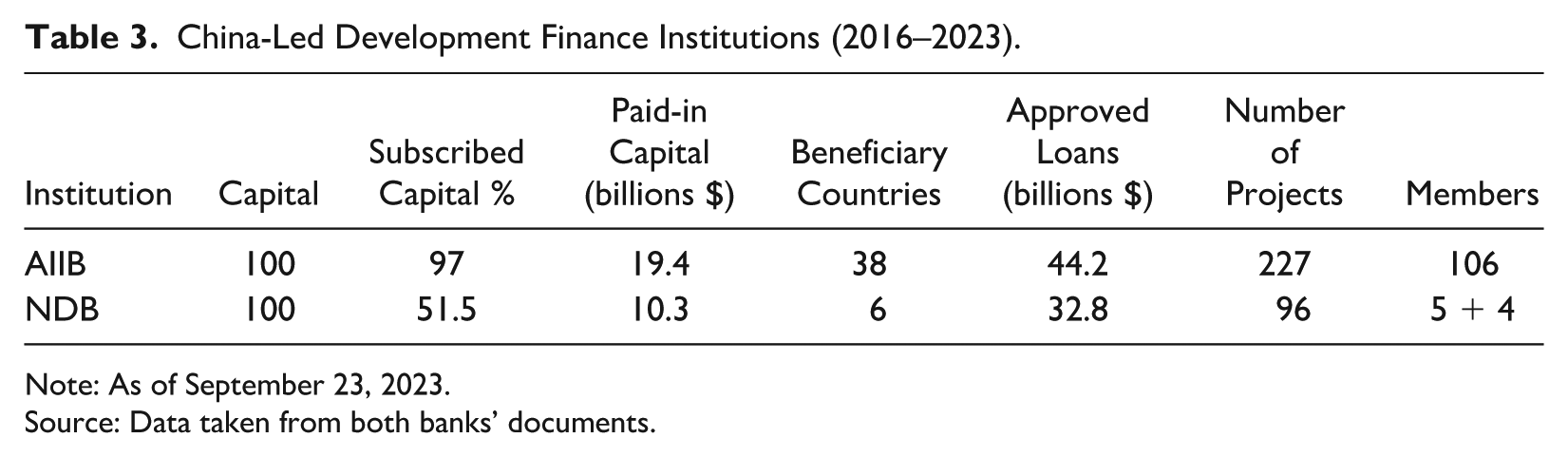

At the multilateral level, China has employed pragmatic strategies within the established institutions and outside it. Beijing took a shareholding stake and offered credit lines to small borrower-led banks in Africa and Latin America and has injected significant financial resources into major multilateral banks beyond the standard core share capital due to the refusal of core countries to increase paid-in capital by borrowing countries in the World Bank Group (Humphrey 2015; Humphrey and Chen 2021). In parallel, China has played a pivotal role in launching the NDB and the AIIB, whose paid-in capitals—which are most relevant in defining lending headroom—are better capitalized than west-led development banks (see table 3). Paid-in-capital of AIIB, NDB, and the International Bank for Reconstruction and Development (IBRD) amounted to 19.4, 20.5, and 7 percent, respectively, of subscribed capital (PwC 2022; IBRD 2022; NDB 2022). 1 Although AIIB has a broader geographical reach than NDB, the latter’s membership has been expanding. The United Arab Emirates, Bangladesh, and Egypt have already joined the bank, and Uruguay is a prospective member.

China-Led Development Finance Institutions (2016–2023).

Note: As of September 23, 2023.

Source: Data taken from both banks’ documents.

Importantly, this quantitative surge in global development finance has effectively reached countries with severely limited access to CCF because of high default ratings based on neoliberal eligibility criteria or due to geopolitical considerations. Between 2005 and 2017, 10 of the top 20 destinations for China’s energy financing—who do not receive financing from the World Bank in any significant amount—have received close to the total energy financed provided by the World Bank (Gallagher et al. 2018). Additionally, Chinese banks extend financial support to countries encountering difficulties in accessing global capital markets, such as Argentina and Ecuador (Gallagher et al. 2012).

In turn, the more efficient administrative structures of China-led multilateral banks and their decision-making processes that are more streamlined than their Western-led counterparts have resulted in shortening the temporal space needed to implement funded projects. While the average approval time for sovereign loans was 14 and 11 months for the World Bank and the Asian Development Bank, respectively (Humphrey 2015), the NDB’s loan approval process takes no more than six months (NDB 2023). This result has prompted the Asian Development Bank to halve its approval cycles (Kumar and Arora 2019).

On the qualitative edge, CODF is distinguished from CCF’s overfocus on relative micro-interventions in the service sector by its targeting of mega-projects in real sectors and big infrastructure such as transport, communications, and energy—including renewable, manufacturing, agriculture, and the like. During 2000–2012, 63 percent of CODF was dedicated to three hardware sectors: (1) energy; (2) industry, mining, and construction; and (3) transport and storage. This figure has increased to 76 percent during the first five years of the BRI implementation (Malik et al. 2021). During 2006–2015, overseas public lending of China’s two policy banks of electric power generation had financed more additional power-generation capacity globally (59 gigawatts) than the 10 largest multilateral development banks combined (55 gigawatts) (Chen et al. 2020).

This sectorial distribution helps mitigate the infrastructure financing gap that characterizes core countries-led financial architecture, estimated between $700 billion and $1.7 trillion (UNCTAD 2014). Indeed, official bilateral and multilateral financing for infrastructure has declined from over 70 percent of the operations of the World Bank in the 1950s and 1960s to a low of just 19 percent in 1999 (Humphrey 2015). Recently, it has slightly increased as a reaction to CODF; in 2016, it resided at 34 percent of total commitments by the World Bank Group and major regional multilateral development banks, or $34 billion (Humphrey 2018). In addition, the effective availability of private financing of infrastructure flowing from core countries’ financial centers is limited and decreasing, concentrated, procyclical, and highly volatile (UNCTAD 2019). For instance, major pension funds from the Organisation for Economic Co-operation and Development (OECD) dedicate only around 1 percent of their investments to infrastructure (OECD 2015). Middle-income countries received 98 percent of all private infrastructure financing between 2008 and 2017. Of this, 63 percent went to the upper tier of middle-income countries (Tyson 2018).

As a result, CODF significantly enhances the global supply of finance for infrastructure, which is a prerequisite for achieving structural transformation because it facilitates coordination, reduces firms’ transaction costs, and improves returns on investment. Hardware infrastructure is an essential tool for addressing one of the key challenges for industrialization—namely, investment coordination failure (Lin 2021).

4. Globalizing the Big Push: Patient Capital, State-Owned Enterprises, and Performance Requirements

Because CODF internationalizes key components of China’s investment-driven industrialization strategy, it is deployed within a policy framework that supports structural transformation and allows the use of industrial policy instruments that have been restricted by neoliberal institutions.

The financing model of Chinese state development banks mirrors the Big Push industrialization approach (Chin and Gallagher 2019) that views underdevelopment as a supply problem wherein the development of one sector/company is hindered by the lack of upstream/downstream sectors (egg-chicken problem) (Hirschman 1958; Rosenstein-Rodan 1943). Concretely, bilateral CODFs identify strategic regions and countries, calculating their potential land, mineral, and industrialization possibilities, and then bundles of loans are issued for an array of coordinated and corresponding projects to trigger a significant amount of economic activity (Chin and Gallagher 2019; Zou 2014: 125). Credit lines are exceptionally large, with loans typically amounting to billions of dollars—rather than the smaller hundreds of millions typically seen in financing by the West-led institutions. This trend has intensified since the launch of the BRI, with the number of mega-projects financed by loans worth $500 million or more tripling during the period from 2013 to 2018 (Malik et al. 2021). At the multilateral level, the AIIB adopts a project-based approach, and the NDB lends to national development banks that in turn follow a Big Push approach (Chin and Gallagher 2019).

Another fundamental change introduced by CODF in international finance is that developing countries now have a non-neoliberal source of finance that does not constrain beneficiary states’ macroeconomic and industrial policy autonomy. For instance, Angola rejected World Bank loans in favor of more appealing financial options offered by China (Corkin 2016). The AIIB explicitly states that it will not impose policy conditionalities on borrowing governments alongside its lending. Interestingly, some evidence suggests that the World Bank is delivering loans with fewer conditions to recipient countries that also have loans from China (Hernandez 2017).

Furthermore, the temporality of CODF flows alleviate pressures on the macroeconomic policy framework, and its patient capital allows governments more fiscal policy flexibility to pursue their domestic agendas and run higher budget deficits (Kaplan 2021). CODF’s lending maturity is comparable to that of official bilateral and multilateral lending (Malik et al. 2021; Morris et al. 2020), but it has a longer-term maturity horizon than the private source of capital from core countries (Kaplan 2021). On the other hand, in contrast to the procyclical behavior of CCF (UNCTAD 2019), CODF has continued to flow into developing countries during periods of volatility and economic crisis—for example, during the 2008 global financial crisis and the 2014 commodity correction. CODF typically views cyclical downturns as an opportunity to enter markets and build their market share. Consequently, CODF has changed the basis of the Mundell Fleming trilemma because countries can access international finance without the need to liberalize capital accounts, thus reducing financial instability and allowing for greater policy maneuverability (Kaplan 2021). Interestingly, this modality echoes China’s own innovative management of the monetary trilemma (McNally and Gruin 2017).

Moreover, CODF provides breathing space for beneficiary countries’ SOEs, which have long been under neoliberal pressure. China underscores the leading role of the public sector and has become the largest bilateral lender for public sector projects. Within the bilateral channel, less than 10 percent of CODF flows go to private entities (Horn et al. 2021). At the multilateral level, the share of approved projects for private sector borrowers is limited to 4.2 percent in AIIB and 17.5 percent in NDB. In the case of funds supported by China in the African Development Bank, Beijing has advocated for a financing structure of 80 percent for the public sector (Humphrey and Chen 2021).

Additionally, borrowers have important room to negotiate on employment, training, and local content. Certainly, China attaches purchasing and procurement conditions at the project level (Brautigam and Gallagher 2014). Although this is a common practice in official lending, where, for example, more than 85 percent of US-aid contracts go to US companies (OECD 2022), China’s policy banks permit sourcing of 30 percent (CDB) to 50 percent (EXIM banks) of projects’ inputs from non-Chinese contractors. Indeed, China government procurement laws provides an exception to the Buy China requirement in the case of its SOEs if goods or services are for use outside China (Grieger 2016). This factor is relevant in the case of CODF given that Chinese enterprises implementing projects are mainly SOEs. Angola, for example, negotiated so that up to 30 percent of their contracts’ values could be subcontracted to Angolan firms (Corkin 2016). Similarly, the China-Pakistan Economic Corridor Agreement allows subcontracting up to 30 percent of the contract value to Pakistani suppliers (Ghossein et al. 2021).

It is important to note that these local content requirements may not always achieve their intended effects because of factors inherent in the beneficiary country’s policy framework, such as trade policy that facilitates the import of foreign products, a lack of trained employees, corruption, prioritizing completion of the project over long-term developmental effects, and the like (Brautigam and Xiaoyang 2014; Corkin 2016). For instance, in Ethiopia’s railway procurement, a state-owned enterprise was contracted by the Chinese constructor to assemble 550 flat wagons locally. Despite early promise, only 330 were completed when the 2013 currency collapse halted input purchases and delayed a planned plant construction. Later, corruption scandals involving the Ethiopian company’s officials further undermined the project’s prospects (Y. Chen 2021).

Of particular significance in relation to technology and know-how transfer tied to CODFs are Chinese Agricultural Demonstration Centers, which are agricultural centers set up by Chinese companies and institutions to transfer technology and new methods of production through demonstrations and trainings, with the goal of ultimately increasing agricultural productivity and the full operation of these centers by the beneficiary state after a specific period (e.g., Xu et al. 2016). In the case of the transport projects, the Chinese approach entails broad cooperation and a long-term capacity-building program, which contrasts with a western contractor’s approach. In the context of the Ethiopia railway projects, there have been student exchanges, collaborations with Chinese specialized railway universities, and the establishment of a new Railway Technology Transfer Academy in Addis Ababa (Y. Chen 2021).

Although the implementation of these performance requirements is not without deficiencies and inconsistency, including a principal-agent problem (Brautigam 2009, 2021; Corkin 2016), China’s official recognition of the importance of these policy tools is a new global political-economic reality. This shift contrasts with the core countries’ mounting pressures on their use since the 1990s, whereby local content and technology transfer became legally restricted in their investment treaties and bilateral trade agreement (Chinese treaties do not share this tendency) (Alshareef 2017).

5. Long-Term Debt Sustainability Beyond Austerity and Original Sin: Strategic Debt Space, Commodity-Backed Finance, and Fiscal Flexibility

The CCF’s debt sustainability framework focuses on immediate insolvency and places excessive emphasis on short-term macroeconomic equilibrium like fiscal imbalances, public debt ratios, and exchange rate regimes. Instead, sustainability should be viewed as an integral component of long-term national development strategies that consider the entire developmental cycle rather than specific points along the growth path. Accordingly, deteriorating debt ratios while leveraging credit to create productive capacities are normal and necessary features of the early stages of development (e.g., UNCTAD 2019).

The Chinese debt sustainability framework for participating countries of the BRI argues similarly, stating that “Productive investment, while increasing debt ratios in the short run, can generate higher economic growth. . . leading to lower debt ratios over time” (MoF 2019: 4, emphasis added). The concrete implementation of CODF’s sustainability approach is distinguished by several features—some based on China’s domestic practices and others inspired by international financial sector standards, albeit adapted with a distinctly Chinese perspective.

First, CODF is externalizing the coordinated financing model that has allowed banks to control credit risk while boosting China’s economic growth (Chin and Gallagher 2019). This approach utilizes the “Input-Output Analysis Model for Strategic Credit Space,” which considers not only hard inputs and outputs like labor and infrastructure but also soft inputs and outputs, such as the financial and credit system (Zou 2014: 131). The study of “strategic credit space” encompasses a comprehensive evaluation of mid- and long-term development prospects within the broader credit environment, assessing both effective and potential solvency (Zou 2014: 123–24). Crucially, this endeavor is underpinned and facilitated by the Big Push approach, which employs bundled loans to address creditability concerns. Lending to multiple projects with varying risk profiles simultaneously enables the use of earnings from more-profitable projects to offset losses from less-profitable ones. According to the CDB economist-in-chief, this approach allows them to “fight a battle by pooling all resources together instead of guerrilla warfare” (Zou 2014: 18).

Second, commodity-backed loans (CBLs) are widely adopted by Chinese lenders, who primarily utilize commodities like oil, but who also will utilize cocoa beans in the case of Ghana and sesame seeds in Ethiopia. The funds generated from the sale of commodity exports are placed in an escrow account that can act as collateral and/or be employed to directly repay loans (Brautigam and Gallagher 2014; Gelpern et al. 2023). CBLs were utilized in 44 percent of China’s official lending between 2000 and 2017, with certain entities, such as CDBs and SOEs, employing them more frequently, with CBLs accounting for around 70 percent of their loans during the same period (Malik et al. 2021). China has itself experienced CBL with its external lenders (Brautigam 2009), and in its internal lending practice, provincial governments use state-owned properties, lands, and future revenues as collateral to borrow from the CDB.

Although collateralized borrowing is commonplace in conventional commercial banking, the unique aspect of CODF, besides its sheer scale, is that the lenders and borrowers are predominantly state entities, not private actors. Furthermore, the collateralized assets are state-owned rather than privately held (M. Chen 2021).

Although CBL is not immune to the risks associated with price volatilities in highly financialized commodity markets, it strikes a reasonable balance between reducing risk for lenders by allowing countries with less favorable credit ratings to finance projects at reasonable interest rates and enabling China to access primary resources (Brautigam and Gallagher 2014). Furthermore, CBL lowers transaction costs since it directly connects two separate supply chains, namely, resource extraction and infrastructure construction (Lin 2021). CBLs serve to restrain governments from diverting resource revenues toward consumption because of political pressures (Collier 2010). They also act as a deterrent to financial misappropriation and repayment delinquency. Approximately 82 percent of CDB’s collateralized lending goes to countries in the bottom (fourth) quartile of the World Governance Indicators Control of Corruption Index (Malik et al. 2021). Research indicates that governments allocate over 90 percent of CBL value for capital spending (Mihalyi et al. 2020).

Importantly, CBL mitigates the exposure of developing countries to a key element of their financial dependency: currency mismatch, whereby the revenue stream from a specific infrastructure project denominated in local currency cannot be used to repay loans denominated in foreign exchange. Thus, CBL reduces the amount of foreign exchange a country must have for repayments of foreign debts.

Third, CODF’s institutions have increasingly provided loans collateralized by future revenue of the projects they finance. This approach is appealing to public sector borrowers because it enables the funding of projects off balance sheet, thus easing the fiscal space of beneficiary states. Indeed, the portion of official lending directed to project companies rose from 31 percent to 68 percent between 2000 and 2017. This shift is explained by the increase in the share of official lending for special purpose vehicles (SPVs) from 8 percent to 31 percent. SPVs are independent legal entities established for the design, implementation, and operation of specific projects. This practice reflects a shift from full-recourse sovereign lending to limited-recourse project finance transactions. In a limited-recourse or no-recourse financing structure, the loan is repaid exclusively with the cash flow generated by the asset, such as toll revenue, container fees, or electricity sales. In some cases, a sovereign guarantee is required, which shifts the payment burden to the host country’s government if the project fails to generate sufficient revenue. Another practice that has gained popularity is issuing a loan to an SPV with a guaranteed return on equity provided by the host government instead of a full sovereign guarantee (Malik et al. 2021). This financing model is an adapted version of China’s Local Government Financing Vehicles that were devised to circumvent restrictions on local government expenditures (Bo et al. 2017). While there are concerns about problems of hidden debt, undisclosed government repayment liabilities, and the effectiveness of managing contingent liabilities, these practices can provide fiscal policy space by reducing the strain on the public budget.

6. Borrower-Led Multilateral Banks and the Geo-economics of Non-geopolitical Conditionalities

China-led multilateral banks provide new space in which developing countries exert paramount influence in terms of capital and voting shares. This evolution represents a historic shift in the governance of the traditional multilateral banks in which non-borrowing core countries have held dominance (Humphrey 2018).

The BRICS reached an agreement to provide each founding member of the NDB with equal voting power irrespective of the size of their economy even though the Chinese economy surpasses the combined size of the other members. Furthermore, they established that any future changes in the ownership structure should guarantee a majority share for developing countries. If industrialized countries seek to become NDB members, they are constrained to a maximum voting power of 20 percent and can only join as nonborrowing members. 2

In the case of AIIB, developing countries held approximately 72.8 percent of the subscribed capital and 71.6 percent of the voting power as of May 2023. The AIIB utilizes a GDP-based share formula to determine the capital subscription of its members while differentiating between regional or nonregional members. This approach is favorable to developing countries since they tend to have stronger GDP performance relative to other metrics used by the IMF that gives more weight to core and liberal economies (Gu 2017). The IMF’s formula includes a weighted average of GDP (50 percent), openness (30 percent), economic variability (15 percent), and international reserves (5 percent). 3 Certainly, with a 30.7 percent share of AIIB’s subscribed capital and almost 26.6 percent of total voting power, China has de facto veto power on key issues. However, China, unlike the United States, has refrained from making categorical demands within the AIIB; instead, it allows AIIB leadership the autonomy to shape its institutional identity and approach without imposing heavy-handed oversight (Humphrey 2020; Humphrey and Chen 2021).

Finally, China refrains from imposing direct and overt geopolitical conditions on its partners (Dreher and Fuchs 2016). This stance is evident in its collaboration with countries like India, which, despite significant political differences, is AIIB’s second-largest shareholder, with 8.6 percent of capital and 7.59 percent of voting shares. The two countries coexist as members of the NDB on equal terms, and their political disagreements, including territorial disputes, have not prevented the expansion of the bank or an arrival at consensus. Furthermore, CODF provides breathing space for countries with limited or no access to CCF for geopolitical reasons, such as Iran, Venezuela, and Russia (Gallagher et al. 2018). This avenue stands in contrast to the practices of core countries-led institutions, which are highly influenced by geopolitical motives (Dreher et al. 2015) and their increasing use of economic sanctions that restrict the access of targeted countries to both private and official financial sources.

However, the Chinese approach should not be mistaken for a lack of (geo)political interests. Instead, it operates within a distinct policy framework aligning with China’s status as a contender state facing mounting pressures from the contemporary heartland. First, CODFs play a role in securing China’s access to international resources, particularly in markets historically dominated by core countries. Additionally, they lay down trade routes that are less vulnerable and less reliant on those currently dominated by the United States. Second, CODFs are part of China’s geoeconomic instruments that create incentives to beneficiary countries to consider Beijing’s political interests and to distance themselves from US policies against China (Alshareef 2024). More broadly, focusing on sovereignty and noninterference while financing connectivity projects, creating bonds and links, and establishing mutually beneficial partnerships that emphasize developmental over security cooperation can all be considered integrated elements within a policy framework attempting to create what Cox (1983) calls an international historical bloc to transcend the US-led neoliberal order.

7. Conclusion: Opportunism and Political Agency in the Global South

The dynamics of the contender state-society complex have played a crucial role in shaping non-neoliberal regulations of CODF. This finding supports the proposition that China’s involvement in global governance can be seen as a fundamental element in the erosion of the neoliberal political project (Arrighi 2007; Strange 2011). In practical terms, CODF has led to a significant reconfiguration of the international development finance system, significantly diminishing external restrictions on the role of the state within structural transformation strategy.

Still, the realization of CODF’s potential hinges critically on domestic political configurations in beneficiary countries—specifically, the preferences of a dominant class and the composition of their broader sociopolitical coalitions, both within and beyond national borders. Empirical evidence indicates frequent misalignment between CODF inflows and host-country strategies to leverage investments for industrial upgrading (Corkin 2016; Brautigam and Xiaoyang 2014). Some Southern policymakers adopt a strategy of using their relationship with China to reduce external pressures and to bolster their bargaining power with core countries. This process seems to be often a part of a rather opportunistic stance making use of available resources from various sources, including the World Bank and the Eurobond market. For instance, Egypt combines CODF with IMF loans and IMF-aligned sources of finance within an overall policy framework shaped by neoliberal conditionalities and a rentier-capitalist class coalition, thereby diluting CODF’s transformative potential.

Consequently, CODF’s developmental efficacy remains contingent on whether dominant class coalitions’ policy framework align with—or subordinate—its use to agendas prioritizing productive capacity building over extractive or financialized accumulation. Counterdevelopment to US-centered neoliberalism “cannot only rely on the economic front, but more importantly, must act on the political front” (Cheng 2025, under “Conclusion”).

Future research should prioritize identifying typologies of developing countries’ strategic positioning within shifting global architectures while examining the mediating role of domestic sociopolitical dynamics—such as class interests, and transnational linkages—in shaping their policy choices.

Footnotes

Acknowledgements

I sincerely thank the Dr. Bin Li, Dr. Juan Santarcángelo, and Dr. Anthony Anastasi for their insightful comments and constructive suggestions, which significantly improved the clarity and quality of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

1

As of June 2022 for the first two and as of December 2021 for the later.

3.

IMF, IMF Quotas, http://www.imf.org/external/np/exr/facts/quotas.htm (visited October 19, 2021), ![]()