Abstract

This study explores the trend of profit rate and determines the factors that influence it in the Turkish manufacturing sector for the period between 1995–2024, following the methodology introduced by Basu and Manolakos. The profit rate reveals a declining trend, with temporary interruptions following the 2001 crisis, and it remains stagnant after the 2008–2009 crisis. The findings indicate that intensified exploitation operates as a significant countertendency, partially offsetting the downward pressure on profitability. Moreover, the impact of real wage deviations on the profit rate is shown to be conditional on the size of the reserve army of labor, highlighting the disciplining role of unemployment emphasized in Marxian political economy. Situated within Turkey’s post-2001 accumulation regime, the findings underscore the centrality of labor discipline and exploitation in sustaining profitability amid limited capital deepening.

1. Introduction

The law of tendency of the rate of profit to fall (LTRPF) has been one of the most controversial areas of research in Classical Marxian Political Economy. As the LTRPF points both to the capabilities of the capitalist mode of production and its inherent limitations, it is the most important law of political economy (Marx 1973: 748). It is essential to underline that the profit rate determines the valorization of the total capital advanced as well as regulates the rhythm and pace of capital accumulation indicating how the economy functions. The capitalist mode of production, driven by the motive for profit, the law of the tendency of the profit rate to fall, countertendencies, and the various modes of interaction between them, remains a critical area of study.

The discourse surrounding the LTRPF has prompted extensive debate, particularly its relationship to the large-scale economic structural crisis, however, the way the tendency interacts with countertendencies is often overlooked (Harvey 2016: 41; Roberts 2016: 55). Since the law was first apparently expressed in the third volume of Capital, with its countertendencies as a distinguishing feature, much of the recent literature has debated its relevance for understanding economic crises. The evolution of the crisis of the 1870s and the 1930s paved the way for the underconsumptionist interpretations of depression (Baran and Sweezy 1966), while the profit squeeze perspective and emphasis on the distributional aspect and circulation sphere were more common during the 1973 crisis and onwards (Glyn and Sutcliffe 1971; Weisskopf 1979). Among others, Grossman [1929] 1992, Yaffe (1973), and Shaikh (1987) are notable for interpreting the LTRPF as a crisis theory and a restructuring process in the capitalist mode of production.

Contemporary debates revived following the 2008 Crisis and assessed the power of Marxian theory to explain the dynamics of this crisis (Duménil and Lévy 2011a; Panitch and Gindin 2021). A prominent strand within this literature interprets the 2008 crisis primarily as the outcome of financialization, conceptualized either as a distinct phase of capitalism (Lapavitsas 2009) or as a historically specific circumstance of neoliberalism, closely linked to the erosion of US hegemony (Duménil and Lévy 2011b). This crisis-specific approach has become increasingly influential in Marxian literature, indicating that each crisis originates from a distinct and historically specific cause. To be sure, economic crises often evolve in an environment with unsold commodities, higher unemployment, or an inflationary context with decreasing profit rates. Moreover, it can appear as a financial crash or a stock market collapse. However, an exclusive focus on these surface manifestations risks obscuring the underlying accumulation dynamics shaped by the interaction between the main tendency and countertendencies (Shaikh 2011; Roberts 2016).

In the following years, new empirical methodologies have come to the fore, pointing to the intrinsic and contradictory dynamics of contemporary capitalism emphasizing the importance of Marxian categories such as surplus value, production and non-production labor, and their decisive role on profit rate and capital accumulation. These studies should be considered as an effort to emphasize the role of Marxian dynamics rather than variety of causalities, in the accumulation process and the crisis. Among others, Moseley (1987), differentiating between productive and unproductive labor, provides an alternative explanation to the arguments that attribute the decline in profit rate in the postwar US economy to a profit squeeze or slowdown in productivity growth, indicating that the decline in profit rate is determined by the rise in capital compositions rather than a decrease in the rate of surplus value. 1

All the above-mentioned studies provide valuable discussions on the determinants of capital accumulation and the profit rate; however, research examining the reciprocal relationship between the LTRPF and countertendencies still to be developed further (with Basu and Manolakos 2012; Maniatis and Passas 2014 being notable exceptions). While the current literature provides insightful comments about the LTRPF, overlooking these countertendencies puts a constraint on our understanding of how the intrinsic dynamics of capitalist production work.

This study contributes to this literature by analyzing how countertendencies and the LTRPF interact, rather than inferring whether the profit rate is falling or not as illustrated by the case of Turkish manufacturing industry between 1995 and 2024. We focus on the manufacturing sector in Turkey, employing a time series analysis methodology developed by Basu and Manolakos (2012) in which the profit rate is the dependent variable and each of the countertendencies is a covariate. The analysis builds on the previous studies that analyze and decompose the profit rate into distributional and technological components (Bakir and Campbell 2006; Eres 2007; Memis 2007), by emphasizing the role of countertendencies and the effect of the reductions of real wages below the value of labor power, and labor-market discipline and the rise in the intensification of exploitation, which is referred to as the increase in the rate of absolute surplus value (Basu et al. 2024) as mechanisms counteracting the tendency of the rate of profit to fall.

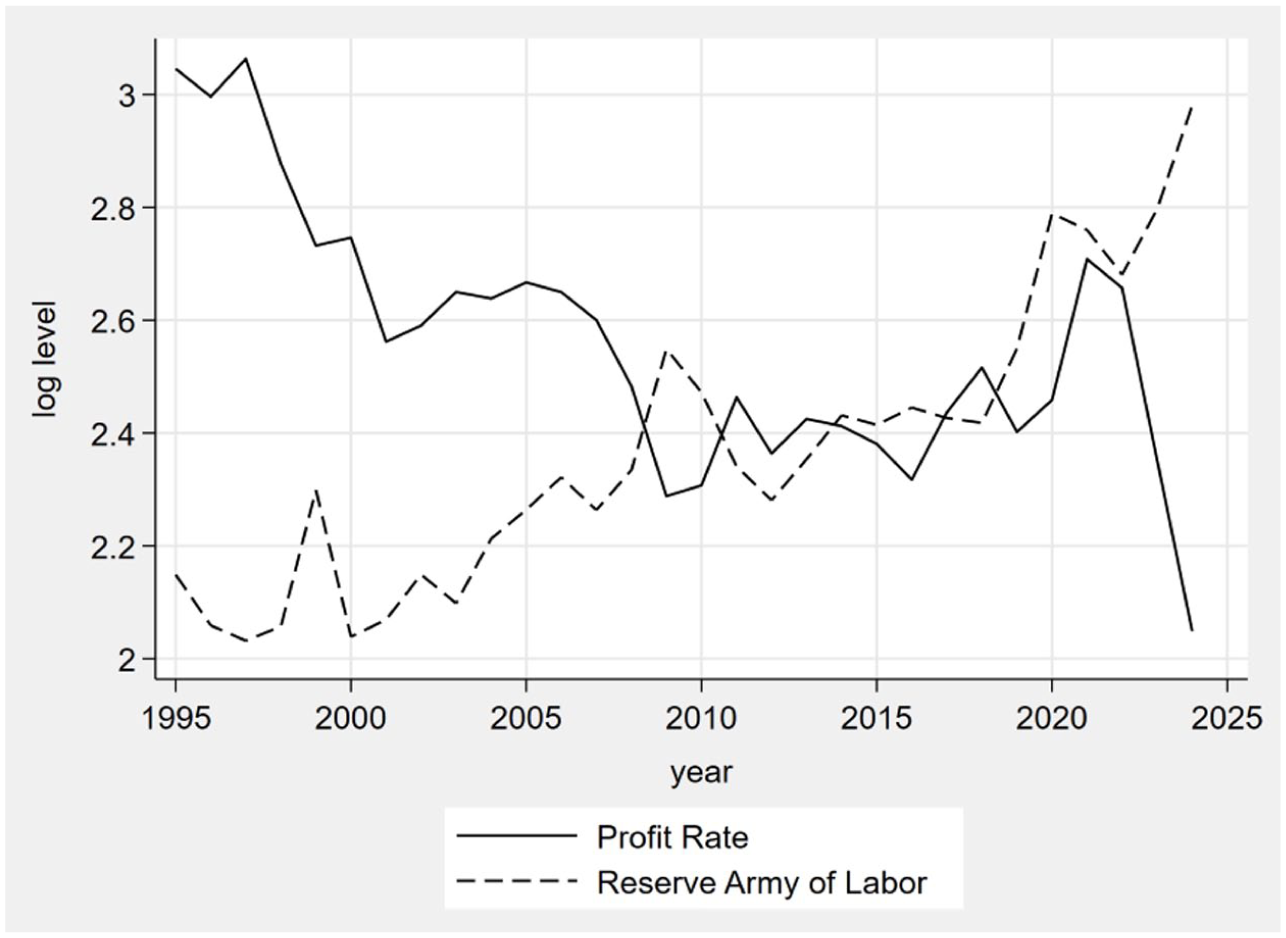

The empirical findings indicate that the rate of profit in Turkey’s manufacturing sector exhibits a persistent long-run decline over the sample period, consistent with the findings of Basu and Manolakos (2012) and Maniatis and Passas (2014). However, this downward tendency is not uniform and was temporarily interrupted in the aftermath of the 2001 crisis and during the 2008–2009 global financial crisis, after which the profit rate remains largely stagnant. Rising capital intensity exerts a negative effect on profitability, while countertendencies operating through labor relations—most notably the intensification of exploitation—partially offset this decline. Importantly, the analysis shows that the effect of real wage deviations on profitability is conditional on the size of the reserve army of labor, underscoring the disciplining role of labor-market slack. When situated within Turkey’s post-2001 institutional and political context, these results suggest that profitability has been sustained primarily through intensified exploitation, weakened labor bargaining power, and limited capital deepening.

The article is structured as follows: In the second section, the literature on the LTRPF is reviewed, with an emphasis on the need to analyze countertendencies. In the third section, the countertendencies and the calculation methods of the variables used in the econometric analysis are presented. This section also includes the econometric analysis and the findings. The final section presents the main findings of the analysis and concludes.

2. The Law of the Tendency of the Rate of Profit to Fall and Importance of Countertendencies

The capitalist mode of production is essentially a process of capital accumulation, and the rate of profit lies at the center of accumulation, as it is the key driving force that shapes the capitalist economies (Duménil and Lévy 1993: 314; Basu 2014; Shaikh 2016). Accordingly, the LTRPF stands at the very center of capital accumulation. However, Marx formulated this law together with a set of countertendencies, implying that the dynamics of capitalist production can only be properly understood by analyzing the interaction between the underlying tendency and the forces that temporarily offset or modify it (Ribeiro et al. 2017). A clear understanding of the mechanisms through which accumulation simultaneously generates rising productivity and declining profitability is therefore essential.

At the heart of the LTRPF lies the progressive increase in the organic composition of capital, driven by capitalists’ effort to raise surplus value and reduce unit production costs. This dynamic process unfolds under the combined pressures of both inter-class and intra-class struggles. Accordingly, each individual capitalist struggle to control the labor force, increasing the length and intensity of the working day, reorganizing the labor process, and reducing it to routine and repetitive tasks with the introduction of revolutionary production methods to increase the social productivity of labor (Marx 1976; Tsoulfidis and Tsaliki 2019). At the same time, competition among different capitals manifests itself in persistent pressure to reduce unit production costs in order to expand or maintain market share. This competitive environment necessitates the individual capitalist to invest more in technology to raise labor productivity by substituting more machinery and equipment for living labor (Shaikh 1987; Tsoulfidis and Tsaliki 2019).

The further mechanization and capitalization of the production process inevitably led to a rise in the organic composition of capital—where the value of constant capital increases and the labor required per commodity decreases—a phenomenon that Marx (1993) described as the real tendency of the accumulation process. According to this, an ever-growing mass and value of means of production is advanced per worker, driven by a given amount of variable capital. Technological progress, rising social labor productivity, and the tendential fall in the rate of profit thus emerge not as contradictory outcomes, but as interconnected results of the same accumulation dynamics (Marx 1993: 319).

Building on this theoretical foundation, the LTRPF has remained a central and contested concept in Marxian political economy, particularly in debates on the causes and dynamics of capitalist crises. 2 Although Marx (1993) formulated the law together with its countertendencies, much of the subsequent literature has focused on the tendency itself, often overlooking the historically specific and dynamic interaction between the two. Early crises, notably those of the 1870s and the 1930s, encouraged underconsumptionist interpretations emphasizing realization problems and demand deficiencies (Baran and Sweezy 1966), while analyses of the crisis of the 1970s increasingly highlighted distributional conflict and profit squeeze mechanisms in the sphere of circulation (Glyn and Sutcliffe 1971; Weisskopf 1979). In contrast, a distinct strand of Marxian analysis has interpreted the LTRPF as a systemic crisis theory rooted in accumulation dynamics and structural transformation (Grossman [1929] 1992; Yaffe 1973; Shaikh 1987). Contemporary debates, revitalized by the global financial crisis of 2008, have further reassessed the explanatory power of the LTRPF, often framing crisis as historically specific events with distinct proximate causes (Duménil and Lévy 2011a; Harvey 2016; Panitch and Gindin 2021). However, critics argue that such approaches risk privileging surface manifestations such as financial instability, unemployment, or inflation over the underlying accumulation dynamics shaped by the interaction between the main tendency and countertendencies (Shaikh 2011; Roberts 2016).

Nevertheless, the tendency of the rate of profit to fall cannot be considered as a continuous decreasing trend or as exempt from crisis recovery periods; instead, it reveals the capacity of capitalism to initiate the countertendencies (Mateo 2018). When countertendencies begin to operate, the valorization process of capital restarts, and capital accumulation can continue on an expanded scale (Grossman [1929] 1992: 78; Harman 2010). From this perspective, examining the impact of countertendencies to the tendency of the rate of profit to fall provides a dynamic analysis of capitalist accumulation and reveals how the system reproduces itself. This is because the tendency of the rate of profit to fall and the countertendencies are the laws of the accumulation process, and they operate at every phase of capital accumulation (Weeks 2011: 133).

Quite a number of studies have examined the dynamics of capital accumulation and the profit rate both using descriptive and econometric methods in line with Marxian theory. To the best of our knowledge, Basu and Manolakos (2012) are the first to use a time series framework to examine the effect of each countertendency on the profit rate in the United States. Maniatis and Passas (2014), following the method introduced by Basu and Manolakos (2012), analyze the Greek economy, employing Marxian categories of productive and unproductive labor. Fernández-Aguilera et al. (2022) use a panel data framework to analyze the countertendencies in the European case. The studies range from global (Basu et al. 2025; Maito 2014) to national economies. While a significant share of the studies focuses on the United States as the largest economy of the world (Duménil and Lévy 2002; Bakir and Campbell 2006; Mohun 2009; Tsoulfidis et al. 2019), the research on the other economies is progressing: Eres (2007) and Memis (2007) for Turkey; Vaona (2010) for Denmark, Finland, Italy, and the United States; Malikane (2017) for South Africa; Marquetti et al. (2019) for Brazil; Maniatis and Passas (2018) for Greece; Polanco (2019) for Chile; Jeong and Jeong (2020) for Korea, Marquetti et al. (2021) for United States and China; Duque-Garcia (2022) for Colombia; Ibarra (2024) for Mexico, among others.

Depending on how the countertendencies operate, the tendency of the rate of profit to fall may slow down, halt, accelerate, or temporarily reverse. It is therefore necessary to analyze how, within an economic structure in which maintaining profitability is the primary motivation, the expanded reproduction of capital both drives accumulation and, at the same time, undermines its material basis. In other words, it requires an examination of the mechanisms by which the capitalist mode of production reproduces itself (Shaikh 1978; Callinicos 2014; Tonak 2017). Although there are various aspects that can be categorized as countertendencies, 3 these factors influencing the tendency of the fall in the rate of profit are explained by Marx (1993) in their most general form as increasing the intensity of labor exploitation, reduction of real wages below the value of labor power, cheapening of the components of constant capital, the size of relative surplus population, foreign trade, and expansion of share capital.

3. Econometric Analysis for Manufacturing Sector

3.1. The model

Building on Basu and Manolakos (2012) with some extensions, the econometric model is constructed as a time series framework in which each countertendency serves as an explanatory variable and the profit rate is the dependent variable:

where

3.2. Data and variables

There are various methods to calculate the rate of profit, depending on the nature of the study and the characteristics of the economic unit to be analyzed (Duménil et al. 1987). The availability of accessible data sources should also be considered. The broadest definition of the profit rate, the general profit rate, is the ratio of aggregated net operating surplus to the capital stock, both in current prices (Shaikh 2016: 243). In line with this, Duménil and Lévy (1999) define the ratio of the difference in net value product and employee compensation to net capital stock. Eres and Bahçe (2015), Duque-Garcia (2022), and Marquetti et al. (2010) are the other works that adopt this definition. The measurements considering Marxian categories can be seen in Jeong and Jeong (2020) and Maniatis and Passas (2014). In this article, we adopted the average rate of profit approach by Duménil and Lévy (1999) and calculated it as a basic rate of return:

where

Capital stock is the most critical variable, since the rate of profit varies depending on the assumptions employed in its estimation. The OECD STAN database provides capital stock data for many economies, but Turkey is not included. In the AMECO and Extended Penn World Tables (EPWT) databases, Turkish data are available only at the aggregate level and are not disaggregated by main sectors. Since there are no officially released data for fixed capital stock for Turkey, 6 we estimated the fixed capital stock for the manufacturing sector from 1995 to 2024 from the accessible data sources of the Turkish Institute of Statistics (TURKSTAT) and the Strategy and Budget Office (SBO), following OECD (2009) guidelines and Paitaridis and Tsoulfidis (2025).

Firstly, aggregated gross fixed capital formation is compiled from the TURKSTAT database in chained 2009 TLs for the period between 1998 and 2024. The SBO database releases the level of gross fixed capital formation (GFCF) at the sectoral level for the period between 1998 and 2024.

7

Then the share of the manufacturing investments in the total GFCF is calculated. In accordance with the majority of the cited literature, residential buildings are excluded and all investment series are treated as machinery and equipment. These series were backdated to 1949 with growth rates derived from Saygılı et al. (2005) which represent the same trend with SBO series in common years.

8

To estimate the initial stock for 1949, we adopted the approach of AMECO (European Commission’s Directorate General for Economic and Financial Affairs), which assumes a uniform capital/output ratio equal to 3 for all countries. Following the estimation of base year stock in constant prices (

The fixed capital stock series between 1949 and 2024 is constructed, as in equation (3), where

As can be inferred from the equation above, capital stock is measured as gross fixed capital stock in this study. This choice follows the classical-Marxian perspective that, from the standpoint of an ongoing enterprise, the total capital advanced in production remains tied up throughout the life of fixed assets, regardless of physical depreciation. As Shaikh (2016) emphasizes, while gross capital stock more accurately reflects the full capital committed to production, net capital stock mechanically declines with the age of capital goods, imparting an upward bias to both the output/capital ratio and the rate of profit by linking capital valuation to realized profits, as in non-classical conventions (Shaikh 2016: 801–3). Although net capital stock may approximate long-run trends (Mejorado and Roman, 2024; Paitaridis and Tsoulfidis 2025), it understates the actual capital tied up in production, since older machines typically operate alongside new investments. Accordingly, the use of gross capital stock provides a conceptually consistent measure of the capital advanced in production and aligns with standard practices in national accounts and the classical theory of capital accumulation (Marx 1993: 335).

The manufacturing value added and employee compensation in current prices were obtained from the TURKSTAT database. Compensation to employees was adjusted for self-employment and later divided by manufacturing wage employment, and then deflated by CPI. The real wage per worker is then calculated. The labor productivity is the ratio of manufacturing value added to manufacturing employment in chained 2009 prices. The capital intensity is the ratio of the fixed capital stock to the sectoral employment. The relative price of capital goods is the ratio of the GFCF deflator to the CPI with the assumption that the capitalist compares the price of means of production to the costs of living labor (Basu and Manolakos 2012).

3.3. Descriptive statistics

In this section, time series and scattered plots of the estimated variables are presented. We use annual data from 1995 to 2024 for the Turkish manufacturing industry. In general terms, the trend in profit rate can be divided into two distinct periods. The first one spans the period from 1995 to 2009, characterized by the crucial economic and political instabilities marked by the crisis of 2001 and the relatively prosperous period experienced until the 2009 crash. The second period starts after the crisis of 2009 and lasted until the end of 2024. The second period includes the 2018 currency shock and the COVID pandemic.

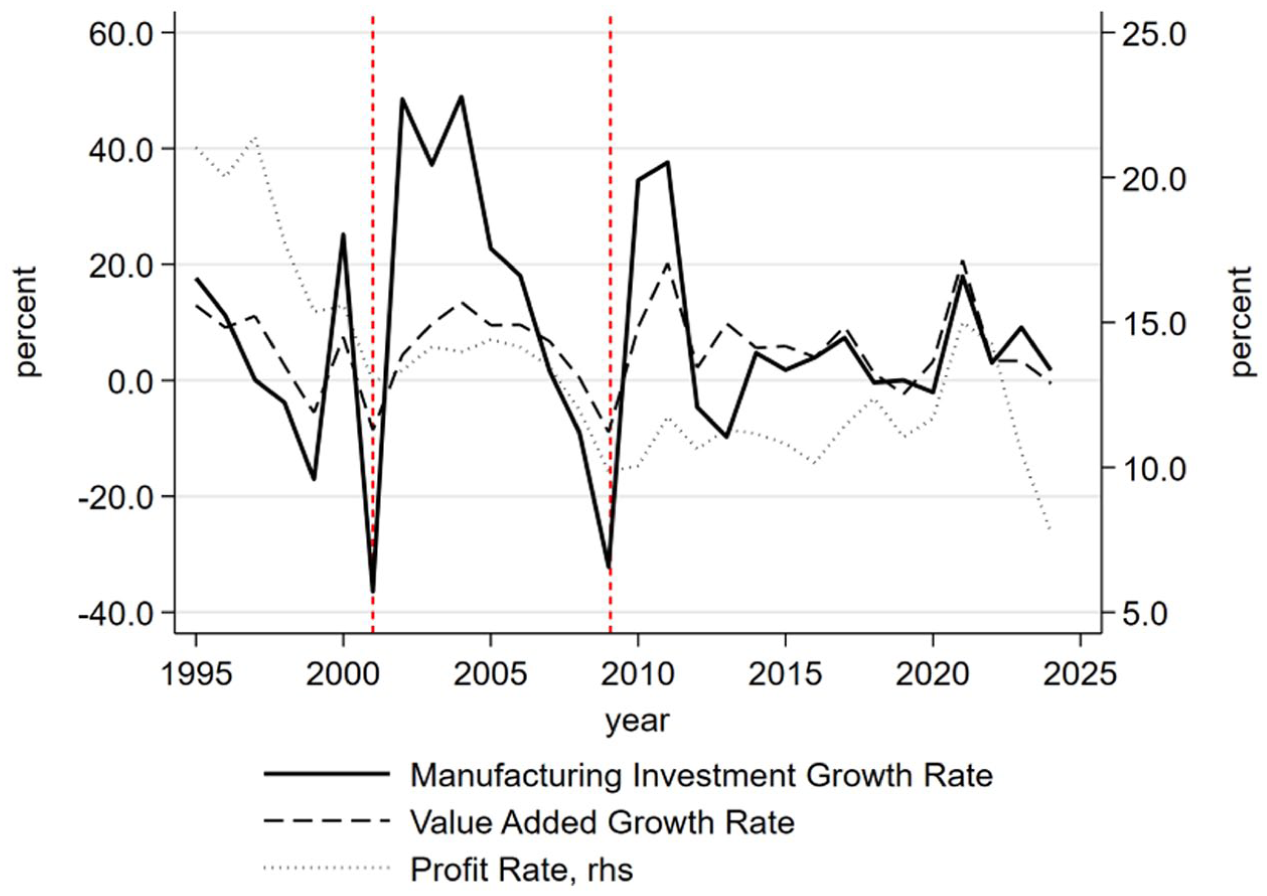

Figure 1 represents the profit rate along with the annual growth rates of sectoral value added and sectoral investment expenditures. As can be inferred from the figure, the linear trend of the profit rate is negative; accordingly, the estimated linear trend indicates that it declines on average by approximately 0.28 units per year over the sample period. This continuous downward trend was not interrupted, except for short-run increases, despite the recovery period during the post-2001 crisis. Since 2002, the Turkish economy has experienced a growth trend attributed to the expansion phase of the global economy and capital inflows (Boratav and Orhangazi 2022). This relatively prosperous period lasted until the Great Recession of 2008–2009, in which the economy shrank by 4.9 percent. This is also reflected in the cyclical downward movement of the profit rate, and a collapse in the growth rate of investment expenditures and value added. During the crisis, the profit rate dropped to its second-lowest point, from 12.96 in 2001 to 9.86 percent in 2009. After 2009, despite a slightly upward trend overall, both the profit rate and the growth rate of investment expenditures have not recovered to pre-crisis levels. These findings are visually consistent with the co-movements illustrated in the figure. This prolonged stagnation can be interpreted as complementary to findings from global research, which suggest that when the mass of real profit reaches a critical threshold, new investment expenditures are disincentivized by the persistent downward trend in the profit rate (Mejorado and Roman 2024; Mutlu and Tsoulfidis 2025).

The average rate of profit and the growth rates of sectoral value added and sectoral investment expenditure, 1995–2024. The vertical dotted red lines point out the economic crises of 2001 and 2008 that the economy experienced. The profit rate is plotted on the right-hand scale axis. Residual-based Engle-Granger tests fail to reject the null hypothesis of a unit root, indicating the absence of a long-run equilibrium relationship between profitability and investment. Short-run dynamics estimated in first differences reveal a positive and statistically significant elasticity of investment growth with respect to changes in the rate of profit (≈0.77).

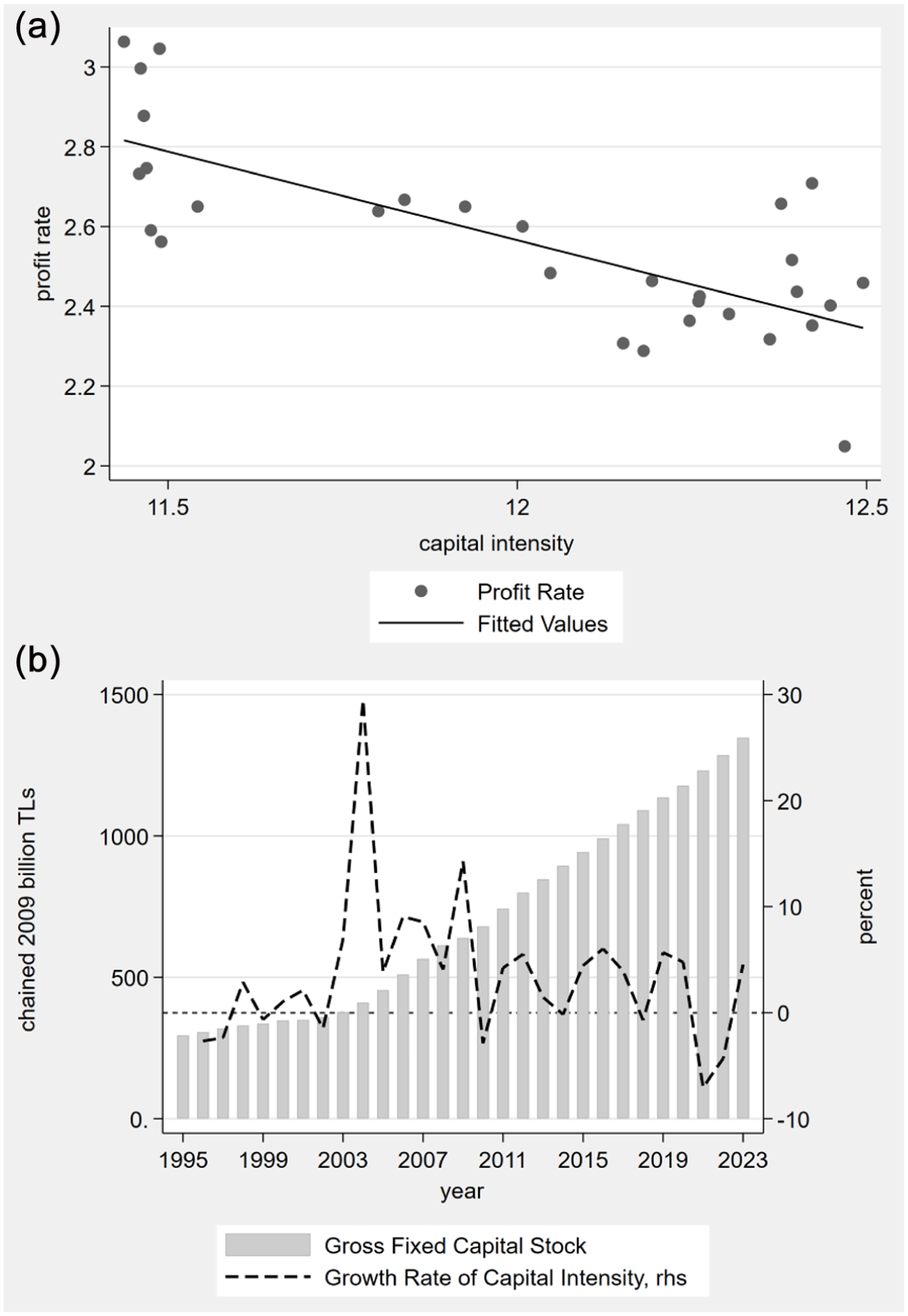

The capital intensity, defined as the natural logarithm of the ratio of gross fixed capital stock to the number of employees, is assumed to be countercyclical with the profit rate. This can be seen in figure 2a. Capital intensity, like the profit rate, rises rapidly during the 2002–2007 cycle, but this increase slowed down in the years following the 2008 crisis, as can be inferred from figure 2b. The annual average growth rate of capital intensity decreased from 10.3 percent between 2002 and 2007 to 2 percent between 2010 and 2024. This lack of adequate capital deepening gives rise to more sophisticated methods of surplus value extraction (Jeong 2017).

(a) Capital intensity and the profit rate. Both variables are log transformed. The dispersion of observations is more pronounced in the post-2009 period, suggesting that the global financial crisis may have altered the short-run relationship between the variables. A detailed analysis of crisis-specific dynamics is beyond the scope of this study. (b) Level of gross fixed capital stock and growth rate of capital intensity.

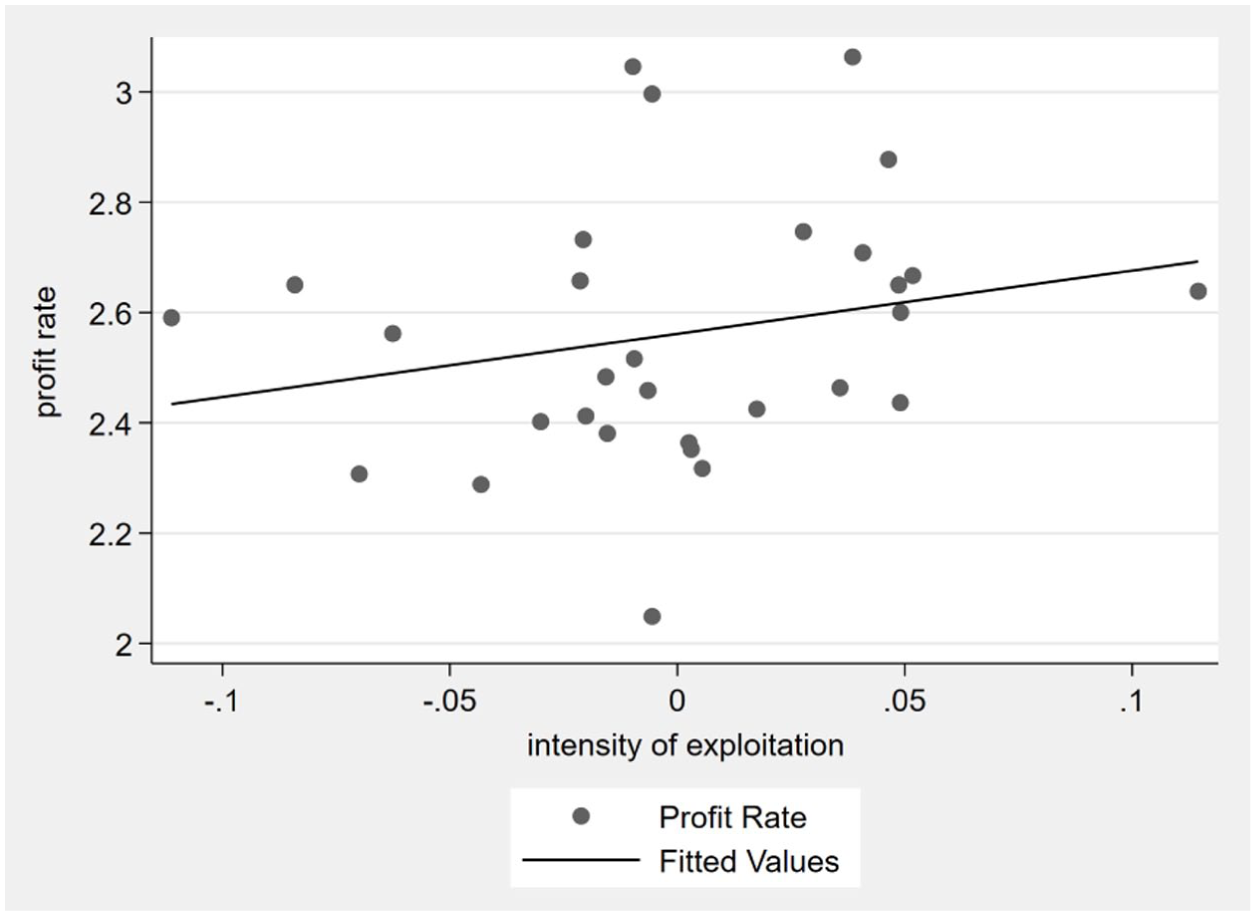

In discussing the counteracting tendencies to the LTRPF, Marx places particular emphasis on the intensification of exploitation through the extension of the working day (Marx 1993: 339). Extending the working day allows an increase in surplus value production without substantially altering the ratio of constant to variable capital, that is, the organic composition of capital. In this sense, an increase in the rate of absolute surplus value weakens the tendency of the profit rate to fall (Marx 1993: 341). By contrast, counteracting tendencies that operate through increases in relative surplus value may raise the organic composition of capital and thereby reinforce downward pressure on the profit rate. Accordingly, increases in surplus value that occur without changes in the organic composition of capital can be interpreted as a counteracting tendency.

In this study, the intensification of exploitation is conceptualized, under explicit assumptions, as an increase in the production of absolute surplus value. Beyond the extension of the working day, absolute surplus value can also be increased through the intensification of the labor process itself, such as by accelerating the pace of work or reducing unproductive time within the working day (Foley 1986; Catephores 1989; Hudson 2000). Time allocated to activities such as meals, rest, or other non-productive intervals—whether explicitly or implicitly regulated in labor contracts—can be compressed, thereby increasing the portion of the working day during which new value is produced without any change in production technology (Basu 2021).

While changes in capital intensity—that is, the ratio of constant to variable capital—affect labor productivity primarily in the long run, short-run fluctuations in labor productivity are shaped by non-technological factors such as working conditions, unionization, collective bargaining power, labor discipline, and the length and intensity of the working day (Maniatis and Passas 2014). In this sense, short-run variations in labor productivity can be understood as reflecting changes in the intensity of exploitation that arise independently of technological change and are closely related to class conflict (Basu and Manolakos 2012; Maniatis and Passas 2014).

Following this interpretation, the intensity of exploitation,

Intensity of exploitation and profit rate.

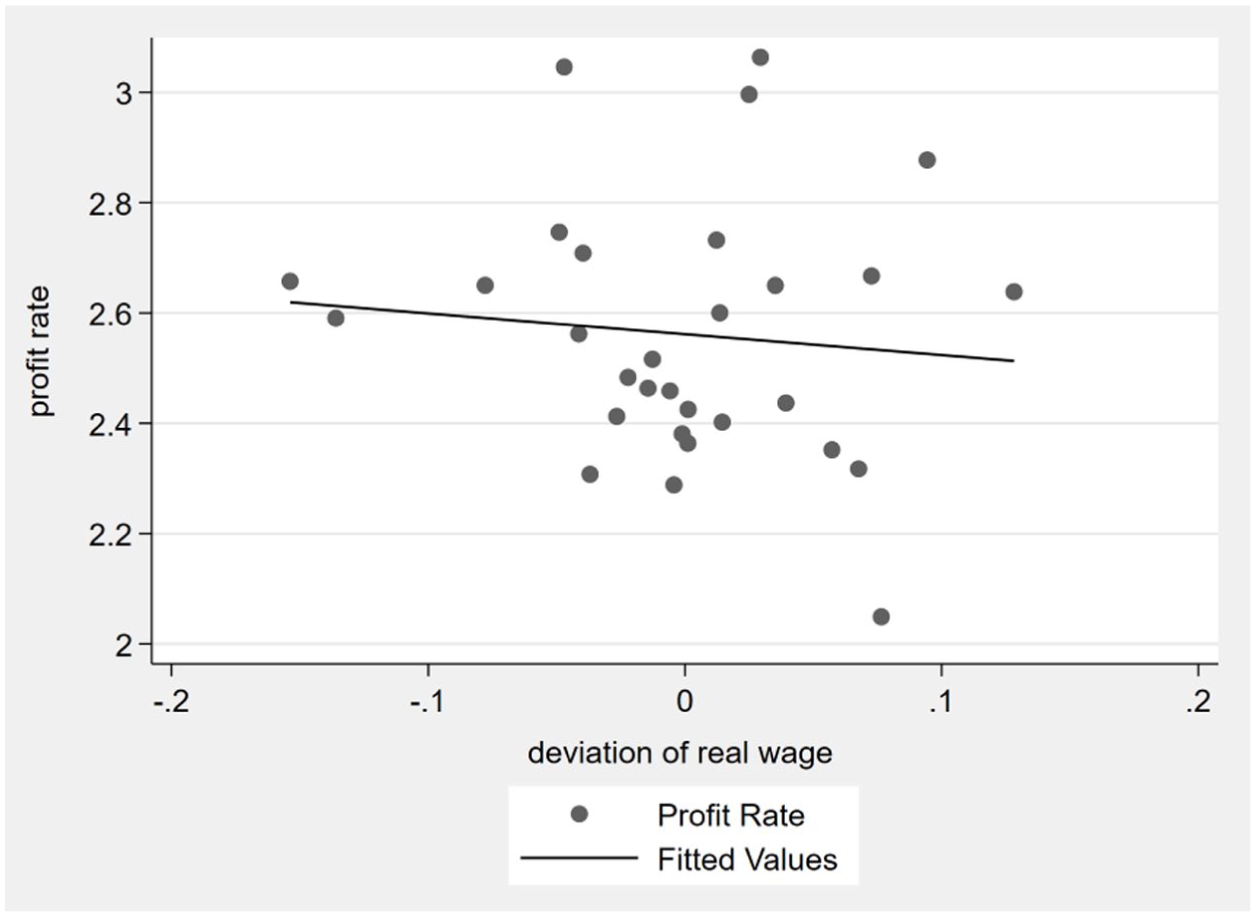

The reduction of real wage below to the value of labor power,

Reduction of real wage below the value of labor power and profit rate.

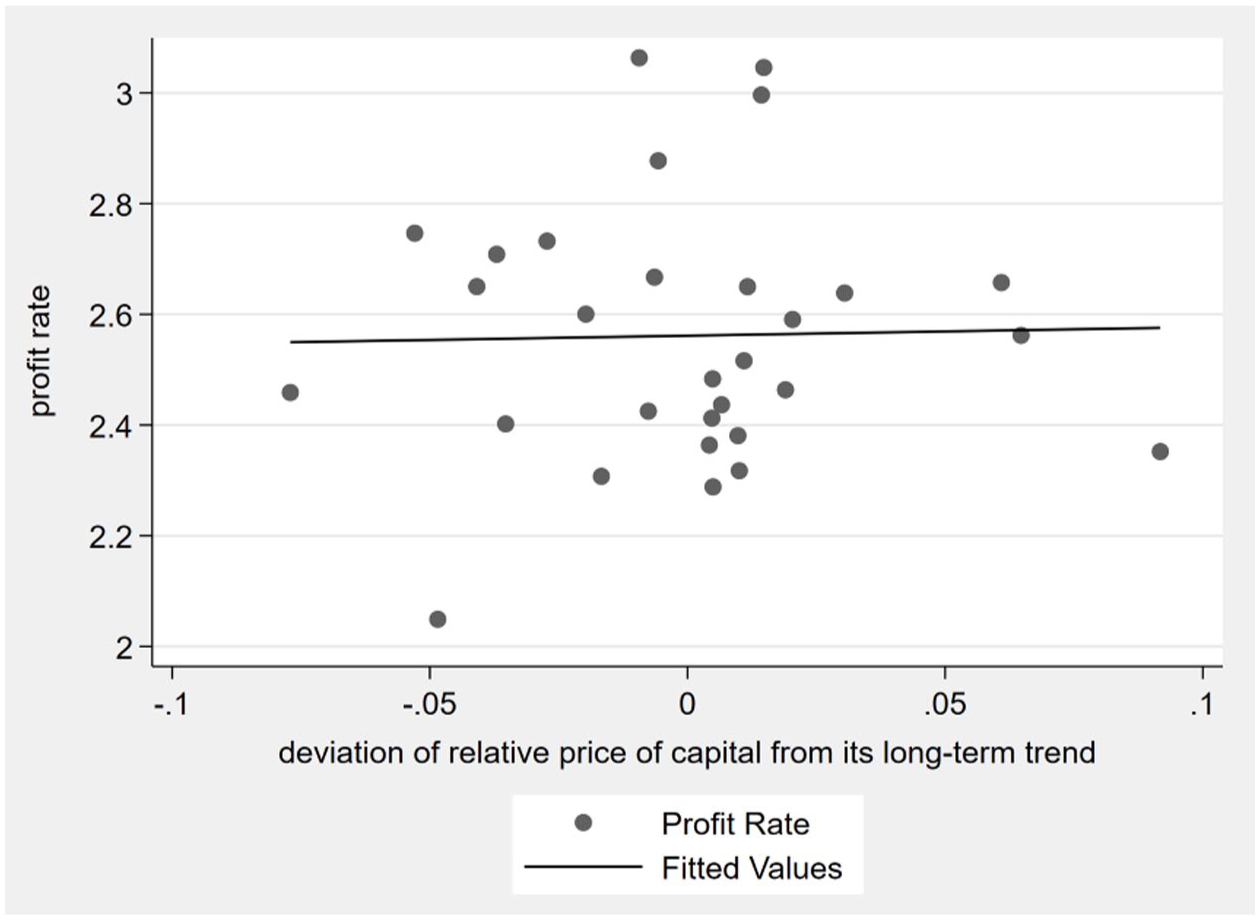

Relative price of the capital good and profit rate.

The reserve army of labor,

It should be added that

Rate of reserve army of labor and profit rate.

3.4. Methodology

The effects of countertendencies on the profit rate are analyzed using ordinary least squares; however, prerequisite steps must be completed to ensure valid statistical inference. The primary issue encountered in time series analysis is the non-stationarity of the data in hand. When a time series is non-stationary, the results of classical regression analysis become invalid, leading to what is known as spurious regression (Asteriou and Hall 2011). In non-stationary time series, both the mean and variance change over time, and the series lacks a long-run average to which it can converge. Additionally, as time progresses, the variance tends to infinity (Asteriou and Hall 2011: 335). In other words, in a stationary time series, shocks are transitory, the effect of the shock diminishes over time, and the series moves toward its long-run average; in contrast, time series with a stochastic trend do not approach the long-run level (Asteriou and Hall 2011; Enders 2014).

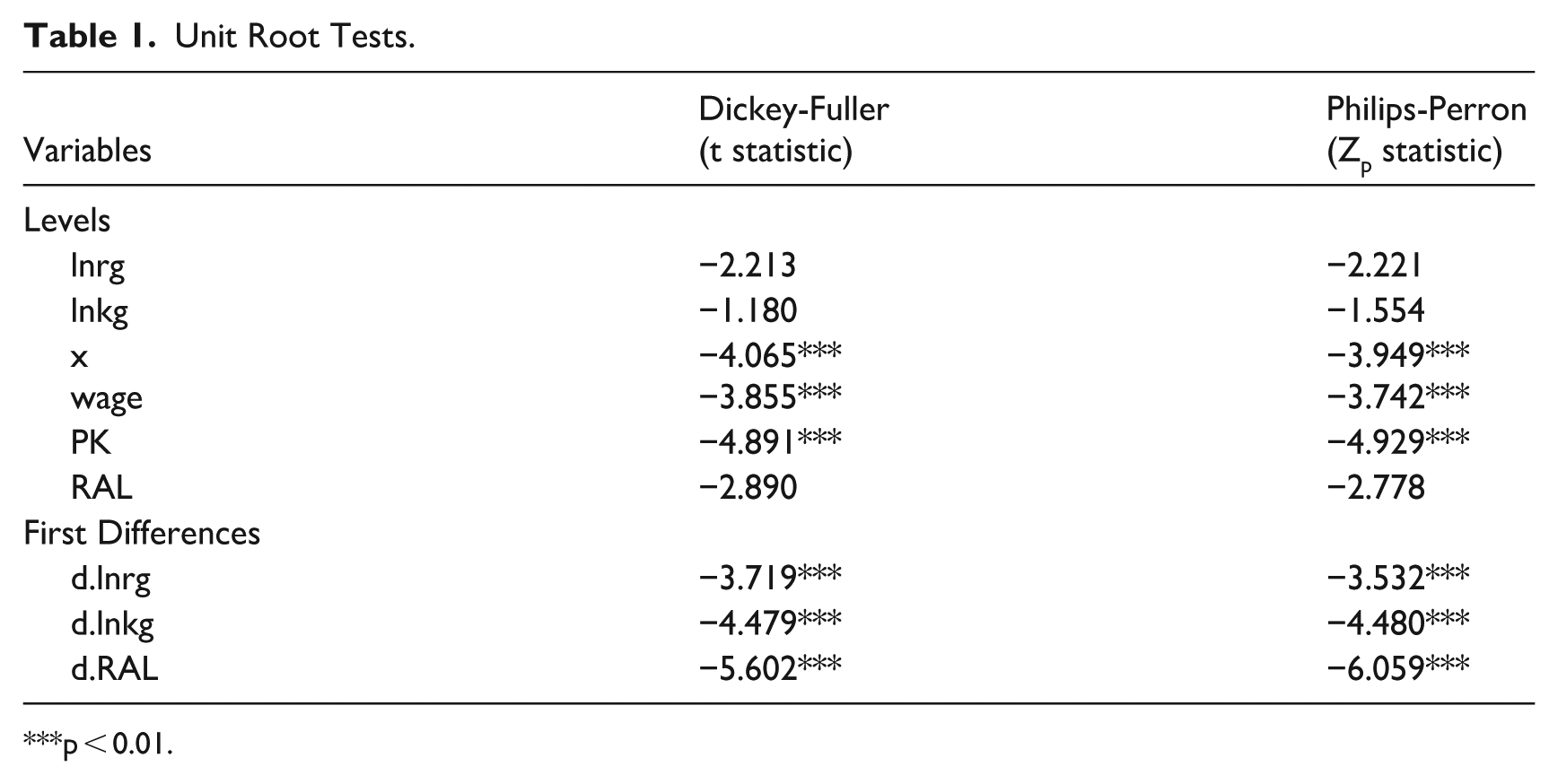

To check the non-stationarity of variables, we employed augmented Dickey-Fuller test (ADF) (Dickey and Fuller 1981) and Philips-Perron test (Phillips and Perron 1988) tests. According to the test results given in tables 1 and 2,

Unit Root Tests.

p < 0.01.

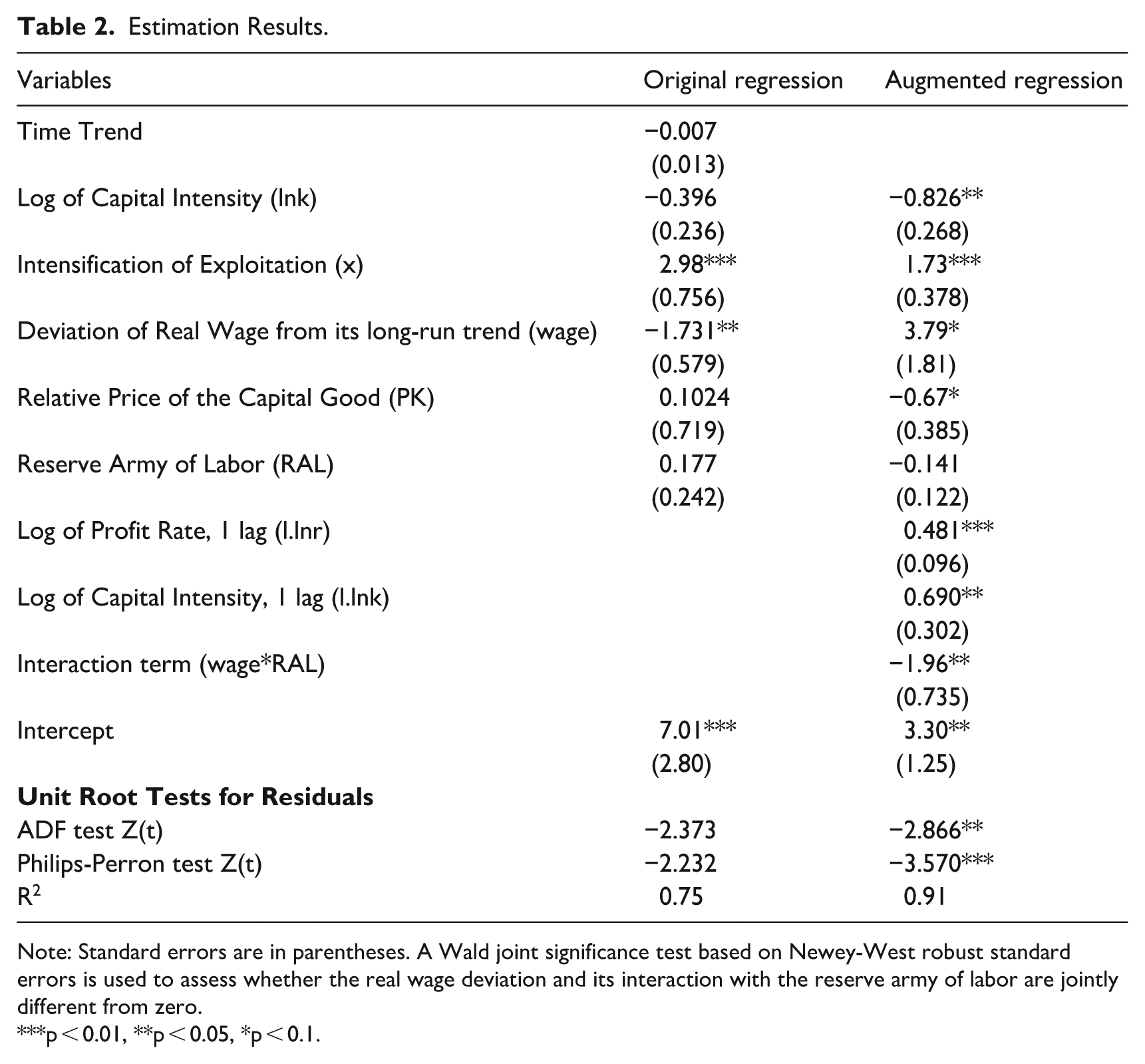

Estimation Results.

Note: Standard errors are in parentheses. A Wald joint significance test based on Newey-West robust standard errors is used to assess whether the real wage deviation and its interaction with the reserve army of labor are jointly different from zero.

p < 0.01, **p < 0.05, *p < 0.1.

Since the dependent and explanatory variables are not integrated at first order, the estimation of the original model with ordinary least squares could be a spurious regression. To test whether the original regression is spurious or not, a two-step cointegration framework is used as in Engle and Granger (1987). An Engle-Granger test based on the residuals of the long-run regression does not reject the null hypothesis of a unit root, indicating the absence of a stable cointegrating relationship. Given the short sample period, the analysis therefore focuses on augmented dynamic specifications to capture the short- and medium-run determinants of profitability rather than imposing a long-run equilibrium. To achieve this, the original regression is augmented with the lagged values of non-stationary variables,

Given the absence of cointegration and the consistent insignificance of the deterministic trend indicating that the long-run dynamics in the profit rate can be expressed with structural mechanisms rather than an explicit deterministic time trend, the augmented specification is estimated without a trend using ordinary least squares, with Newey-West heteroskedasticity and autocorrelation-consistent standard errors. Moreover, the

3.5. Results

The results of both estimations are given in table 2. The residuals of the original regression do not exhibit a unit root process. In the augmented regression, both the ADF and PP tests indicate that the null hypothesis of unit root can be rejected at the 10 percent significance level. Given the small sample size and the dynamic specification, this result provides supportive evidence that the estimated relationship is not spurious. 11

In the augmented regression, log of capital intensity is significant and negative, indicating that the profit rate declines as the capital intensity rises, which is linked to increased mechanization in the production process and a higher organic composition of capital. The coefficient for the lagged value of the profit rate is also positive and significant. The lagged value of capital intensity is significant and positive, indicating that the capital intensity of the production process in the previous period contributes to a higher rate of profit.

The coefficient for intensity of exploitation is significant and positive, aligning with Marxian theory and the findings of the literature cited above, confirms that short-run increases in labor productivity, when not driven by technological change, operate as a counterdendency by raising the rate of surplus value without increasing the organic composition of capital. This clarifies that, the augmented regression captures not only higher productivity, but also intensified labor utilization consistent with Marx’s concept pf absolute surplus value. Although weakly significant, lowering real wages below the value of labor power positively impacts the profit rate. The profit rate rises when real wages are below the value of labor power—i.e., when deviations from the trend are negative—while it falls when real wages exceed the value of labor power. 12

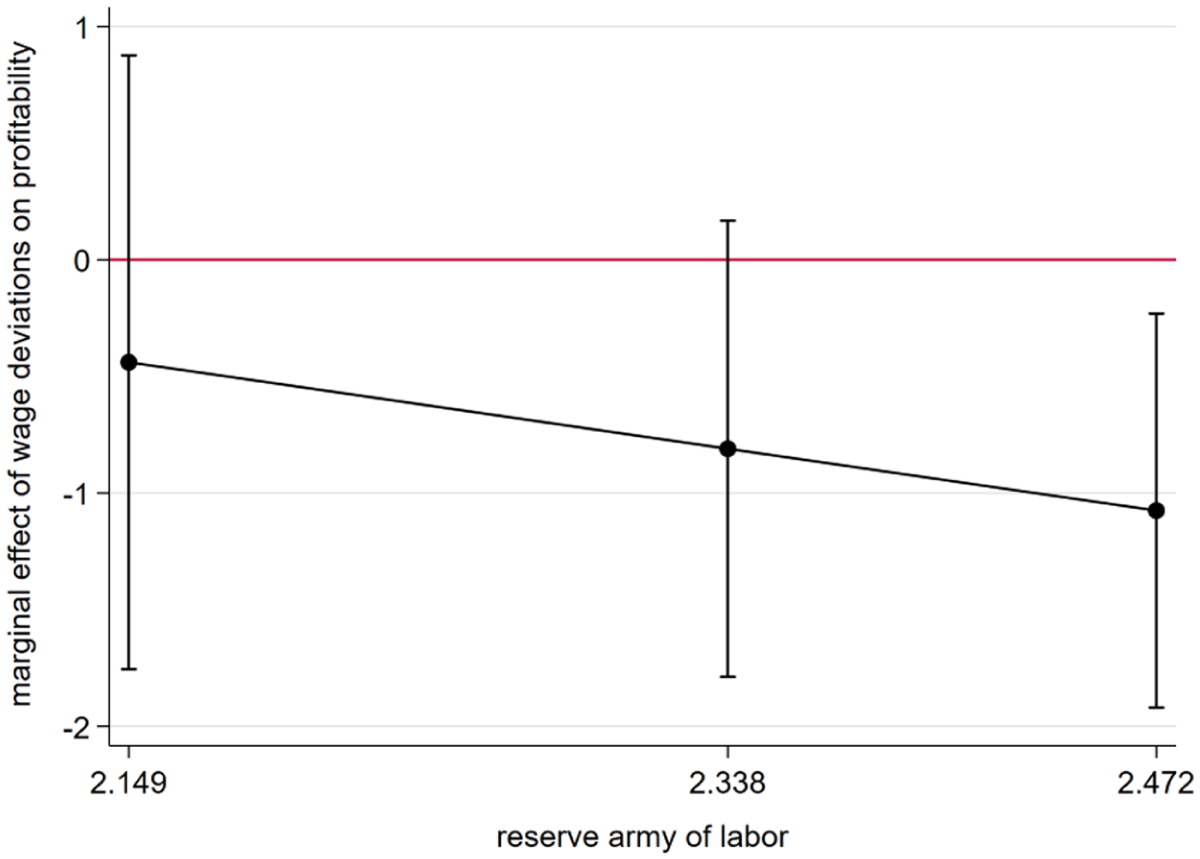

Importantly, the effect of real wage deviations on profitability is found to be conditional on the size of the reserve army of labor. The interaction between real wage deviations and the reserve army of labor is negative and statistically significant, indicating that the adverse impact of wage deviations on profitability intensifies as labor market slack expands. This conditional relationship is consistent with the disciplining role of unemployment emphasized in Marxian political economy (Marx 1976: 790; Foley 1986: 65). In this sense, the estimated relationship does not merely reflect a mechanical accounting identity but captures what Duménil and Lévy (1993: 266) describe as “the existence of quantitative regularities in the outcome of social conflicts between workers, motivated by the improvement of their working conditions and living standards, on the one hand, and firm resistance to the erosion of their profit rate, on the other.” Figure 7 illustrates this mechanism by reporting the model-implied marginal effect of real wage deviations on the profit rate evaluated at different levels of the reserve army of labor. While the effect is weak and statistically indistinguishable from zero at low levels of labor market slack, it becomes increasingly negative as the reserve army of labor expands.

Marginal effect of wages on profitability at different levels of the reserve army of labor.

Both the coefficients of intensity of exploitation, deviation of real wage below the value of labor force, and the conditional effect of the reserve army of labor should be evaluated with the social and political factors in Turkey in the research period that might have impacted the course of profit rate. The post-2001 accumulation strategy in Turkey has been systematically based on maintaining low labor costs and exploiting a disciplined, flexible, and disposable labor force in order to sustain export competitiveness. Central to this strategy were productivity gains driven largely by labor shedding rather than technological upgrading, alongside the institutionalization of labor market flexibility through the 2003 Labor Law, which expanded subcontracting, fixed-term contracts, and restrictions on collective bargaining and strike activity (Bozkurt-Güngen 2018; Erol 2018). As a result, organized labor was progressively weakened, a process further reinforced by large-scale privatizations that dismantled labor’s strongest organizational bases and rendered unions a marginal political actor (Akçay 2021). In this institutional setting, unionization and collective bargaining coverage remain extremely limited: while the official unionization rate is 14.5 percent, the effective rate falls to around 12 percent, and only 9–10 percent of workers—dropping to 4–5 percent in the private sector—are covered by collective agreements (DİSK-AR 2026a, 2026b). 13 Wage determination has thus increasingly gravitated toward the minimum wage, with 87.3 percent of wage earners earning at or below twice the minimum wage, giving rise to a “minimum wage trap” in which the minimum wage functions as a de facto average wage rather than a floor (Çelik 2022). These dynamics were deepened under the AKP and especially during the post-2016 state of emergency, when the authoritarian management of labor power further curtailed labor’s capacity to exert distributive pressure despite rising workplace-level unrest (Erol 2018; Pınar 2021). 14 At the same time, the large-scale incorporation of migrant labor into highly informal and labor-intensive sectors such as agriculture, construction, and textiles altered the composition of employment and reinforced wage suppression, functioning as an additional labor-disciplining mechanism for the working class as a whole (Aksu et al. 2022; UNHCR 2025; Saraçoğlu and Bélanger 2025). 15

The coefficient for the relative price of capital goods is statistically significant albeit weakly. This weak relation may be expected, as in a production structure where investment goods are primarily imported, the exchange rate largely determines the price of capital goods. Since the exchange rate is beyond direct control, capitalists tend to maintain or increase the profit rate by intensifying exploitation and lowering real wages below the value of labor power. Another explanation may be the ability of capitalists to directly pass on increases in investment costs to the price index of wage goods (see Memis 2007). The relationship between the price of capital goods (investment deflator) and the price of wage goods (CPI) shows a pattern in which the CPI rises faster than the investment deflator, particularly after 2015. 16

4. Conclusions

The discussion on the LTRPF has sparked significant debate, particularly regarding its connection to the widespread economic structural crisis. However, the intrinsic link between the main tendency and countertendencies has been largely ignored. Examining the relationship between the LTRPF and countertendencies, though, provides opportunities to better understand the functioning and restructuring of the capitalist economy. This study investigates the relationship between the trend in the rate of profit in Turkish manufacturing sector over the period 1995–2024, along with the countertendencies examined through time series analysis.

It adopts the methodology described in Basu and Manolakos (2012), in which the profit rate is the dependent variable and each of the countertendencies is a covariate. The parameters of the model are estimated by ordinary least squares, after performing unit root tests as described in Basu and Manolakos (2012). To align with the adopted methodology and transform the regression model into a cointegrating framework, the lags of the nonstationary variables are included in the model and the model is re-estimated. An interaction term is included to capture how the reserve army of labor indirectly shapes distributional conflict, rather than operating as an independent determinant of profitability.

According to the empirical results, the profit rate in the manufacturing sector declines in the long run and although the coefficient of the deterministic trend is insignificant, its estimated trend reveals an average by approximately 0.25 units per year over the sample period. This ongoing declining trend has been temporarily changed between the post-2001 crisis and the 2008–2009 Great Recession. After 2010, it has remained stagnant. In the long term, the rise in capital intensity leads to a decrease in the profit rate, consistent with the findings of previous studies.

One of the main findings of the present analysis is that the intensity of exploitation has a robust and positive effect on the profit rate, meaning that the long-term declining trend in the profit rate is countered by the intensification of exploitation. Demonstrating that the effect of real wage deviations on profitability is conditional rather than unconditional is another main finding of this article. Deviations of real wage from its long-term trend do not exert a uniform impact on the rate of profit; instead, their effect crucially depends on the size of the reserve army of labor. As labor market slack expands, the adverse impact of real wage deviations on profitability becomes increasingly pronounced, consistent with the disciplining role of unemployment emphasized in Marxian political economy (Marx 1976; Foley 1986; Duménil and Lévy 1993). This finding suggests that the reserve army of labor operates not merely as a background condition but as an active mechanism shaping the profitability dynamics.

These results acquire particular significance when situated within the institutional and political context of Turkey since the early 2000s. After the 2001 crisis, the decline in the profit rate is countered by further intensification of exploitation and the reduction of real wages below the value of labor power. The underlying dynamics are determined by factors such as the radical reorganization of the production process under conditions of insufficient capital deepening and the decline in the bargaining power of the working classes vis-à-vis the capital class.

Finally, while this study provides crucial insights into the dynamics of the profit rate, the role of the sixth countertendency—the expansion of share capital—needs to be acknowledged, particularly in Turkey, where its significance as a dynamic factor in the economy is often overlooked. Future studies should address this gap by integrating the role of financial and shareholder capital to enhance the profitability analysis.

Footnotes

Appendix

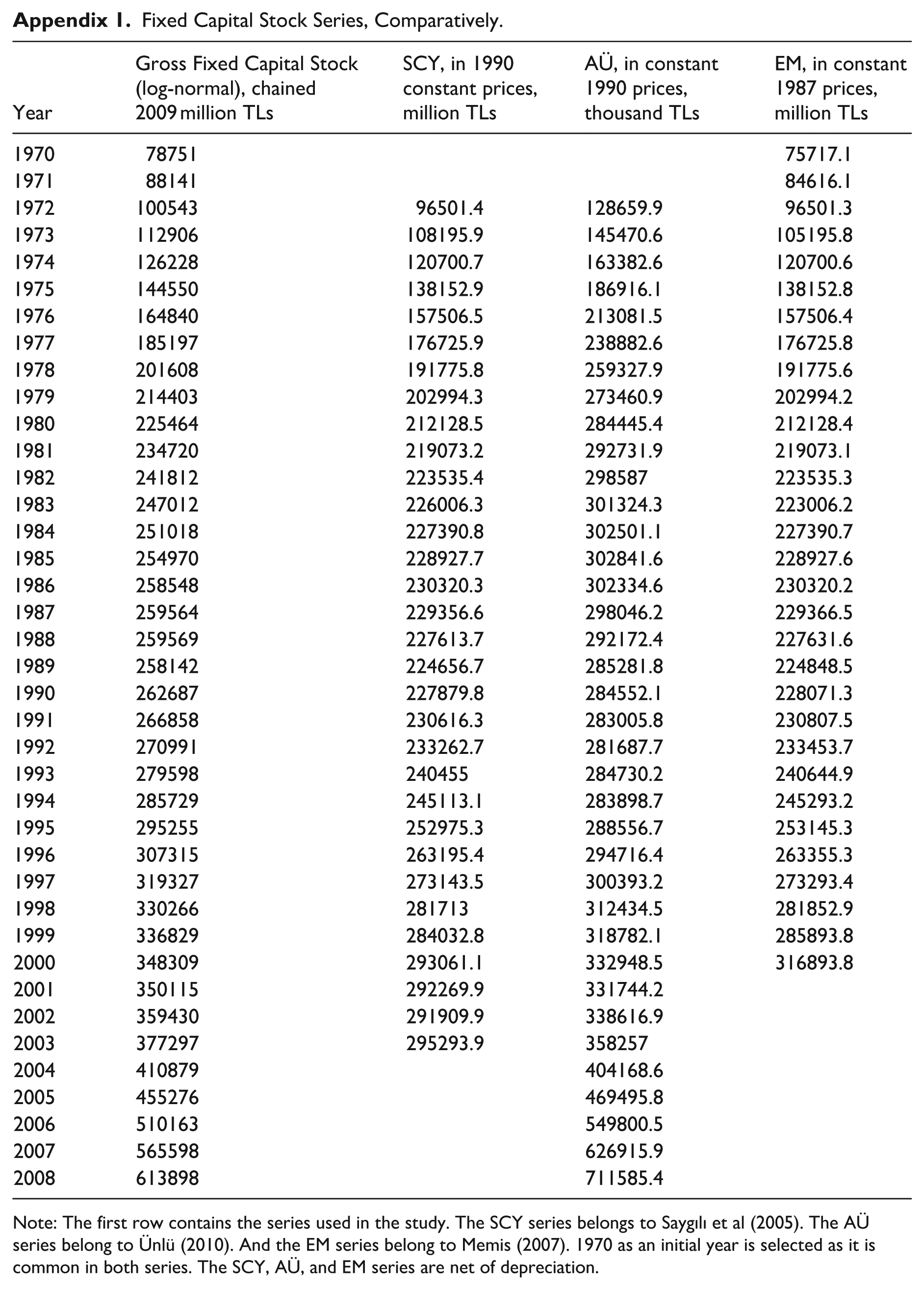

Fixed Capital Stock Series, Comparatively.

| Year | Gross Fixed Capital Stock (log-normal), chained 2009 million TLs | SCY, in 1990 constant prices, million TLs | AÜ, in constant 1990 prices, thousand TLs | EM, in constant 1987 prices, million TLs |

|---|---|---|---|---|

| 1970 | 78751 | 75717.1 | ||

| 1971 | 88141 | 84616.1 | ||

| 1972 | 100543 | 96501.4 | 128659.9 | 96501.3 |

| 1973 | 112906 | 108195.9 | 145470.6 | 105195.8 |

| 1974 | 126228 | 120700.7 | 163382.6 | 120700.6 |

| 1975 | 144550 | 138152.9 | 186916.1 | 138152.8 |

| 1976 | 164840 | 157506.5 | 213081.5 | 157506.4 |

| 1977 | 185197 | 176725.9 | 238882.6 | 176725.8 |

| 1978 | 201608 | 191775.8 | 259327.9 | 191775.6 |

| 1979 | 214403 | 202994.3 | 273460.9 | 202994.2 |

| 1980 | 225464 | 212128.5 | 284445.4 | 212128.4 |

| 1981 | 234720 | 219073.2 | 292731.9 | 219073.1 |

| 1982 | 241812 | 223535.4 | 298587 | 223535.3 |

| 1983 | 247012 | 226006.3 | 301324.3 | 223006.2 |

| 1984 | 251018 | 227390.8 | 302501.1 | 227390.7 |

| 1985 | 254970 | 228927.7 | 302841.6 | 228927.6 |

| 1986 | 258548 | 230320.3 | 302334.6 | 230320.2 |

| 1987 | 259564 | 229356.6 | 298046.2 | 229366.5 |

| 1988 | 259569 | 227613.7 | 292172.4 | 227631.6 |

| 1989 | 258142 | 224656.7 | 285281.8 | 224848.5 |

| 1990 | 262687 | 227879.8 | 284552.1 | 228071.3 |

| 1991 | 266858 | 230616.3 | 283005.8 | 230807.5 |

| 1992 | 270991 | 233262.7 | 281687.7 | 233453.7 |

| 1993 | 279598 | 240455 | 284730.2 | 240644.9 |

| 1994 | 285729 | 245113.1 | 283898.7 | 245293.2 |

| 1995 | 295255 | 252975.3 | 288556.7 | 253145.3 |

| 1996 | 307315 | 263195.4 | 294716.4 | 263355.3 |

| 1997 | 319327 | 273143.5 | 300393.2 | 273293.4 |

| 1998 | 330266 | 281713 | 312434.5 | 281852.9 |

| 1999 | 336829 | 284032.8 | 318782.1 | 285893.8 |

| 2000 | 348309 | 293061.1 | 332948.5 | 316893.8 |

| 2001 | 350115 | 292269.9 | 331744.2 | |

| 2002 | 359430 | 291909.9 | 338616.9 | |

| 2003 | 377297 | 295293.9 | 358257 | |

| 2004 | 410879 | 404168.6 | ||

| 2005 | 455276 | 469495.8 | ||

| 2006 | 510163 | 549800.5 | ||

| 2007 | 565598 | 626915.9 | ||

| 2008 | 613898 | 711585.4 |

Note: The first row contains the series used in the study. The SCY series belongs to Saygılı et al (2005). The AÜ series belong to Ünlü (2010). And the EM series belong to Memis (2007). 1970 as an initial year is selected as it is common in both series. The SCY, AÜ, and EM series are net of depreciation.

Acknowledgements

Generative AI assistance (PoolText and OpenAI’s ChatGPT, version 5.2) was used to enhance language clarity and streamline specific sections of the manuscript. All AI-generated content was critically reviewed and edited by the author. I am grateful to Elif Karaçimen, Emel Memiş Parmaksız, Emrah Er, and Ozan Mutlu for reading the first draft and providing valuable insights and feedback on the issues addressed in this manuscript, as well as to the reviewers. Any remaining errors or omissions are solely the responsibility of the author.

1

This branch of research was further developed by Shaikh and Tonak’s (1994) comprehensive analytical and empirical analysis, which includes construction of the productive and unproductive labor categories and Marxist approach to crises. Paitaridis and Tsoulfidis (2012) and ![]() applied a similar methodology to investigate the causes and implications of the 2008 crisis, underlining the role of the relative extension of the non-production area over the productive one in the structural crisis.

applied a similar methodology to investigate the causes and implications of the 2008 crisis, underlining the role of the relative extension of the non-production area over the productive one in the structural crisis.

3

Elveren et al. (2022) indicates that as the share of female workforce rises, the profit rate rises. ![]() assesses the role financialization as a sixth countertendency.

assesses the role financialization as a sixth countertendency.

4

5

The profit rate calculated in the study excludes the consumption of fixed capital and the net indirect business taxes, because of the lack of available and systematic data.

6

Capital stock data produced through special studies by experts of the former State Planning Organization, now the Presidency of Strategy and Budget, do exist; however, these data have been made available only insofar as they attracted the interest of researchers, and their dissemination has not been institutionalized in a systematic manner. In the absence of a regularly published and standardized data set, individual studies have been compelled to construct their own capital stock series based on assumptions tailored to their specific research agendas. Early studies on Turkey’s capital stock include Ebiri et al. (1977), Maraşlıoğlu and Tıktık (1991), and Saygılı et al. (2005), the third one being the most frequently cited. Other studies that estimate capital stock for the Turkish economy as a whole and for the manufacturing sector include ![]() , Ünlü (2010), and Bahçe and Eres (2012). Comparative capital stock series from Saygılı et al. (2005), Ünlü (2010), and Memis (2007) are presented in the appendix.

, Ünlü (2010), and Bahçe and Eres (2012). Comparative capital stock series from Saygılı et al. (2005), Ünlü (2010), and Memis (2007) are presented in the appendix.

7

8

Saygılı et al (2005) provides a detailed calculation of the fixed capital stock series, based on the methodology introduced by OECD (2001). We used the growth rates of the investment series in constant prices, provided in ![]() table 4.1, to back-cast our GFCF series.

table 4.1, to back-cast our GFCF series.

9

Series for comparison are given in the appendix.

10

The adjustment coefficient is the ratio of the sum of self-employed and wage/salary workers to the total wage/salary workers. The adjusted labor compensations is the product of adjustment coefficient and labor compensation of manufacturing sector.

11

The augmented regression reveals constant variance, when Breusch-Pagan/Cook-Weisberg tests are conducted. Ramsey-Reset test indicates potential nonlinearities. Given the presence of interaction terms and lagged dependent variables, this result is interpreted as suggestive rather than conclusive. The model already incorporated theoretically motivated nonlinearities through interaction terms between wage deviations and the RAL. CUSUM test for parameter stability shows no evidence of structural instability in the estimated coefficients. Control function tests are conducted to detect whether there are any endogeneities. Accordingly, we do not detect endogeneity in wage, x, and k, suggesting that OLS estimates are not driven by mechanical correlations rising from construction of the variables.

12

The change in the sign of the wage coefficient across specifications may be attributes to the differences in model structure rather than counter mechanisms. In the static regression, which does not exhibit cointegration, the wage coefficient captures short-run correlations between wage deviations and profit rate. Once dynamic adjustment and interaction effects are explicitly modeled, the wage coefficient no longer represents an unconditional effect. Instead, the impact of wages on profitability is shown to depend on the size of the reserve army of labor, with the interaction term capturing the economically meaningful channel (Brambor et al. 2006; ![]() ).

).

13

OECD data of Collective Bargaining Coverage also confirms this phenomenon. Turkey ranks the lowest rate of bargaining coverage among the countries covered in the data set (OECD Database 2024). Moreover, the highest average weekly working hours remained high in Turkey between 2004 and 2024, compared to the selected countries. Turkey shares the top position with Mexico and Colombia (![]() ).

).

14

This labor-suppressing attribute has been concretized in Mr. Erdoğan’s speech in the prolonged state of emergency days: “We are implementing the state of emergency so that our business world can work better. I ask: Do you have any problems or disruptions in your business world? When we came to office, there was a state of emergency. But all factories were under the threat of strikes. Remember those days. Is there anything like that now? On the contrary. Now, wherever there is a threat of a strike, we immediately intervene by making use of the state of emergency. We say no, we do not allow a strike here, because you cannot disrupt our business world” (![]() ).

).

15

16

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.