Abstract

This article investigates the dynamic relationship between wages and labor productivity in Spain from 1995 to 2024. While wages are assumed to evolve in line with labor productivity, empirical evidence suggests a decoupling between the two variables. We identify two distinct regimes in Spain: one characterized by a positive association between wages and productivity, and another marked by decoupling. We also observe that changes in these regimes coincide with changes in political leadership in the country: periods of center-left governance (PSOE) coincide with a certain wage-productivity alignment, while right-wing administrations (PP) tend to coincide with a wage-productivity decoupling. This highlights the political nature of wage-setting dynamics and challenges the view that wage stagnation is solely a consequence of weak productivity growth. We argue that political institutions and policy decisions might play a critical role in shaping the functional distribution of income.

1. Introduction

Over the past three decades, Spain has undergone a transformation in the functional distribution of income. Between the early 2000s and the COVID-19 crisis, the wage share in gross value added has shown a declining trend, consistent with patterns observed across both advanced and emerging economies (Ossa 2024; Manera et al. 2022). This erosion of the wage share is particularly relevant in the Spanish context, where household consumption—driven by wage income—has historically played a central role in sustaining economic growth (Dejuán et al. 2013). Despite the reduction in workers’ purchasing power, aggregate consumption did not collapse, largely because it was temporarily supported by rising levels of household debt (Álvarez et al. 2019; Bellettini and Delbono 2013; Febrero et al. 2019). However, the limits of this debt-driven model became evident with the 2008 global financial crisis (Barradas 2023; Bilbao-Ubillos and Fernández-Sainz 2022; Febrero et al. 2018).

A widely held view is that sluggish wage growth is primarily driven—if not entirely explained—by low productivity growth (Feldstein 2008). The rationale behind this argument is straightforward: In a competitive market, firms are only willing to pay wages that reflect workers’ marginal productivity. Thus, when output per worker stagnates or declines, employers have little incentive to raise wages. However, classical political economists, including Smith (1776) and Ricardo (1815, 1817), and Marx ([1867] 1992), emphasized that wages are not merely the result of market forces but reflect the distributional struggle between capital and labor. From this perspective, the wage share serves as a proxy for the bargaining power of workers relative to capital owners. In recent years, empirical research has increasingly pointed to a structural decoupling between wages and productivity, especially since the Great Recession (Ossa 2024; Brink et al. 2021; Dosi et al. 2020; OECD 2018; Sharpe and Uguccioni 2017). This trend raises fundamental questions about the political and institutional drivers of wage formation.

This article contributes to this debate by examining the relationship between wages and labor productivity in Spain from 1995 to 2024. Specifically, it explores whether the evolution of wages has mirrored productivity gains or whether a decoupling has taken place. To do so, we use a narrative approach and complement it with a Markov regime-switching vector autoregression (MS-VAR) model, which allows us to capture potential nonlinearities and regime shifts in the wage-productivity relationship. Importantly, we also assess whether these regime shifts align with changes in political leadership, thereby investigating the extent to which political factors might mediate wage dynamics.

Our findings reveal the existence of two distinct regimes: one characterized by a positive co-movement between wages and productivity, and another marked by a decoupling of these two variables. Strikingly, these regimes appear to correspond with changes in Spain’s national governments. Periods governed by the center-left Partido Socialista Obrero Español (PSOE) are generally associated with wage-productivity alignment, while periods under the conservative Partido Popular (PP) exhibit a decoupling. These results highlight the importance of the political context in shaping the distribution of economic gains, and they point to the need for further research on how institutional and policy changes influence wage setting and income distribution.

The remainder of the paper is structured as follows. Section 2 reviews the literature on the wages-productivity nexus. Section 3 reviews recent trends in the functional distribution of income in Spain. Section 4 presents the chosen variables and the empirical debates surrounding the wage-productivity link. Section 5 describes the empirical methodology. Section 6 presents the empirical results. Finally, section 7 offers concluding remarks and suggests avenues for future research.

2. Literature Review on the Nexus between Wages and Productivity

Neoclassical theory predicts that real wages move in line with labor productivity. However, since the 1970s, real wages for the typical worker in developed countries have stagnated, while labor productivity has continued to grow. This divergence explains the decline in the wage share, which falls when real wages grow more slowly than productivity. Why have wages and productivity decoupled to the detriment of the former?

Neoclassical contributions attribute the decline in the wage share primarily to technical change (see Kumhof et al. 2015; Burger 2015; Grossman et al. 2017; Mertens 2019; Knoblach et al. 2020; and Dolado et al. 2021, among others). Advances in information technology may have raised the productivity of physical capital relative to labor productivity, thereby reducing the wage share (OECD 2018). Beyond technical change, neoclassical authors also emphasize the weakening of unions. According to Rodrik (1999), improved outside options for capital owners reduce workers’ bargaining power. Globalization and financialization reinforce this mechanism (International Labour Office 2013).

Financialization increases the influence of aggressive, return-oriented investor institutions and expands outside options for domestic capital. When financial investors perceive higher returns abroad, they demand higher rates of return on domestic investment. At any given required rate of return, they therefore supply fewer investable funds domestically (Burger 2015). Higher required returns and a reduced supply of investable funds shift the investable-funds schedule upward. This shift exerts downward pressure on capital/output ratios. Firms then face stronger pressure to deliver higher returns. To meet this pressure, they typically adopt capital-augmenting, labor-saving technologies, which reduce labor’s income share (Burger 2015).

The discussion above suggests that the neoclassical approach explains changes in income shares through labor-saving technical change. These conclusions, however, rest on a well-behaved factor-substitution mechanism and on the associated tendency toward full employment. This mechanism cannot generate a well-defined, interest-elastic investment function from the demand for “capital” unless one assumes continuous full employment of labor. Such an assumption lacks legitimacy, since full employment should emerge from the analysis rather than serve as a premise (Petri 2019). 1 As Petri (2015, 2019) argues, this problem calls for the adoption of a fully non-neoclassical approach to distribution, employment, and growth.

Non-neoclassical economics rejects the view that competitive factor market forces determine income distribution. It nevertheless recognizes a causal link between functional income distribution and labor productivity. This causality is often indirect, contingent, and bidirectional. Distribution shapes both the level and the composition of demand and domestic production, as well as the direction of technical change. It also affects the social stability required for economic reproduction and the capacity of elites to block redistributive policies (Gethin et al. 2021) and to advance their own interests (Elkjær and Klitgaard 2024). In general, lower income inequality and a higher wage share in GDP are associated with faster productivity growth (Alcobia and Barradas 2025).

Private household consumption increases with households’ disposable income, but at a decreasing rate, that is, lower-income households tend to devote a higher share of their income to consumption than higher-income households (Kaldor 1940). To the extent that this demand is met by domestic production, GDP also increases. A higher wage share in value added therefore tends to raise the disposable income of a large share of the population and to reduce inequality, thereby inducing higher consumption and, thus, higher aggregate demand. Private investment is also stimulated as a result, since firms are required to meet the new demand under competitive conditions (Harrod 1939; Samuelson 1939; Hicks 1950; Serrano 1995). Taken together, these effects imply a higher level of GDP and, typically, productivity advances, as new investment tends to embody more advanced technologies (Labat-Moles and Summa 2024; Obst et al. 2020; Storm and Naastepad 2011). Additionally, higher economic growth can foster labor productivity through the so-called Smith effect or the Kaldor-Verdoorn effect. Both effects posit a positive relationship between economic performance and labor productivity, driven by increasing returns to scale. Finally, a more equitable income distribution is associated with lower household indebtedness and, therefore, with greater stability of consumption and of the economy as a whole (Barba and Pivetti 2009; Kumhof et al. 2015). Similarly, a more equitable distribution of wealth is associated with lower macroeconomic instability and with smaller collapses in consumption during crises (Chikhale 2023), as was also shown during the pandemic (Kuypers et al. 2022). 2

Nonmainstream approaches also link the decline in the wage share to globalization and financialization (Palley 2013; Stockhammer 2009; Hein 2015; Kohler et al. 2019, among others). However, these approaches do not rely on adjustments in the labor/output or capital/output ratios to explain distributive changes. They therefore reject the view that falling nominal or real wages provide a path to full employment, since employment depends on the principle of effective demand, even in the long run (Garegnani 1978). Instead, in most nonmainstream frameworks, wage dynamics reflect forces that extend beyond market mechanisms. Historical, institutional, and political factors play the central role.

In sum, both mainstream and nonmainstream economics expect a positive relationship between wages and labor productivity. Mainstream accounts allow this link to weaken because of technical change and financialization. Nonmainstream approaches instead emphasize political factors and the state of collective bargaining. In this context, the contribution of Paolo Sylos Labini proves especially relevant.

Sylos Labini (1984, 1999) argues that when collective bargaining and wage norms align wage growth with productivity growth, the economy tends to experience sustained and robust growth. The United States during the Keynesian regulatory era provides a clear example. The period of greatest wage share stability coincided with the phase of fastest economic growth. This stability peaked between 1950 and 1968, during the effective operation of the Treaty of Detroit (see Armstrong et al. 1991; Noah 2012). This landmark postwar agreement between the United Auto Workers and the major automobile firms—Ford, General Motors, and Chrysler—linked wage growth explicitly to labor productivity growth. The agreement subsequently shaped collective bargaining across large segments of the US economy until the late 1960s. This institutional framework stabilized income distribution and limited the growth of inequality while supporting high economic growth rates (Manera et al. 2016). Real wages sustained purchasing power and aggregate consumption without reliance on rising household indebtedness. At the same time, strong and predictable consumer demand generated profit expectations sufficient to sustain investment, employment, and long-run economic growth.

In sum, although nonmainstream economics also advances arguments that predict a coevolution of wages and productivity, it acknowledges that, empirically, wages and productivity rarely grow pari passu unless collective wage arrangements enforce such alignment (Manera et al. 2022). This observation motivates our research. We assess whether different political contexts and labor market regulations in Spain shape the propensity of wages and labor productivity to evolve in step.

3. Functional Distribution of Income in Spain

The production of goods and services, reflected in gross value added (GVA), is simultaneously a process of income generation for participants in production, either through their direct contributions or indirectly through property rights over productive factors. At this initial stage, income is distributed between total compensation for workers—which includes wages and employer contributions—and gross operating surplus, or profits, which encompass depreciation, dividend payments, and other returns. Consequently, the share of wages in GVA (the “wage share”) serves as a critical metric for understanding how income is allocated through market mechanisms to the majority of the population, excluding considerations of household composition, portfolio distribution, or state intervention. This represents the primary distribution of income.

Analyzing the functional distribution of income is valuable for at least two reasons. First, from a macroeconomic perspective, it facilitates the study of trends in the wage bill, the primary determinant of consumption, aggregate demand, and, consequently, investment (Hicks 1950). Second, functional income analysis remains pertinent because wages constitute the principal source of income for the majority of households. Indeed, Fujita (2023) presents a theoretical framework linking functional and personal income distribution from a Kaleckian perspective, thereby investigating the effects of changes in markups and interest rates on personal inequality using the Gini coefficient. Fujita’s findings reveal that an increase in markups, particularly when workers have weak bargaining power, leads to a rise in income inequality as measured by the Gini coefficient. Hence, the functional distribution of income might significantly influence personal income distribution.

From the perspective of classical political economists, the wage share reflects the relative bargaining power between labor and capital. Since the 1970s, labor income has stagnated globally, accompanied by a pronounced decline in the wage share of GVA across both advanced and emerging economies (Manera et al. 2022; Pérez-Montiel et al. 2024). Spain has followed a similar trajectory (Anghel et al. 2018; Uxó et al. 2024; Herrero and Cardenas 2024). According to Tridico and Pariboni (2018), Keynesian economists widely attribute this trend to the neoliberal turn initiated in the 1970s. Key policy shifts—including financial and labor market deregulation, trade liberalization, increased capital mobility, wage flexibilization, structural adjustment programs, the retrenchment of welfare states, the downsizing of public sector involvement, and the erosion of progressive tax regimes—are seen as central drivers of the declining labor share (Manera et al. 2019). Additionally, the post-Keynesian literature argues that financialization has impaired labor productivity through four main channels. These include weak macroeconomic performance, a declining labor income share, rising personal income inequality, and a deepening degree of financialization. The latter operates through its adverse effects on innovation, research and development, technological progress, and productive investment by nonfinancial corporations (Correia and Barradas 2022). The first three channels operate indirectly, whereas the fourth constitutes a direct mechanism through which financialization undermines labor productivity (Barradas 2023).

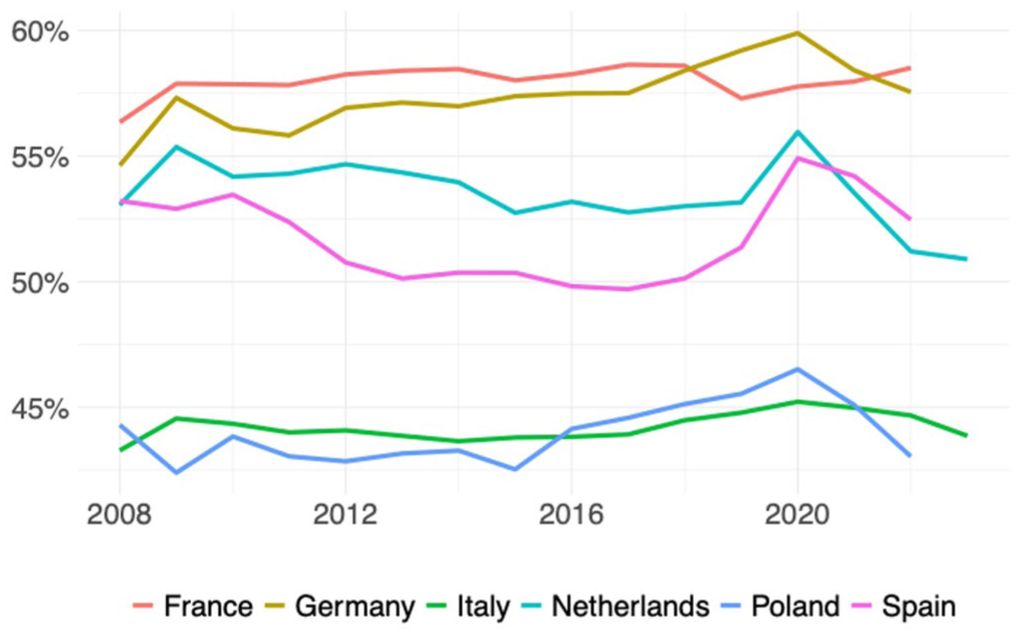

Between 2008 and 2023, the wage share in Spain followed a generally procyclical pattern, albeit with a certain lag (figure 1). In comparative perspective, Spain’s wage share in GVA has remained relatively low vis-à-vis neighboring countries such as Germany, France, and the Netherlands. Although higher than in Italy or Poland, Spain’s wage share was consistently below that of the Netherlands for most of the period under analysis, reaching a comparable level only in 2023. The significant decline observed in the aftermath of the Great Recession has been widely documented in the literature (Villanueva et al. 2020). Following the return to positive economic growth and employment expansion in 2014, the downward trend halted, giving way to a phase of relative stability, followed by a modest recovery starting in 2018. However, the wage share declined again between 2021 and 2023, largely as a result of inflationary pressures triggered by the COVID-19 crisis.

Wage share in gross value added at factor cost, 2008–2023.

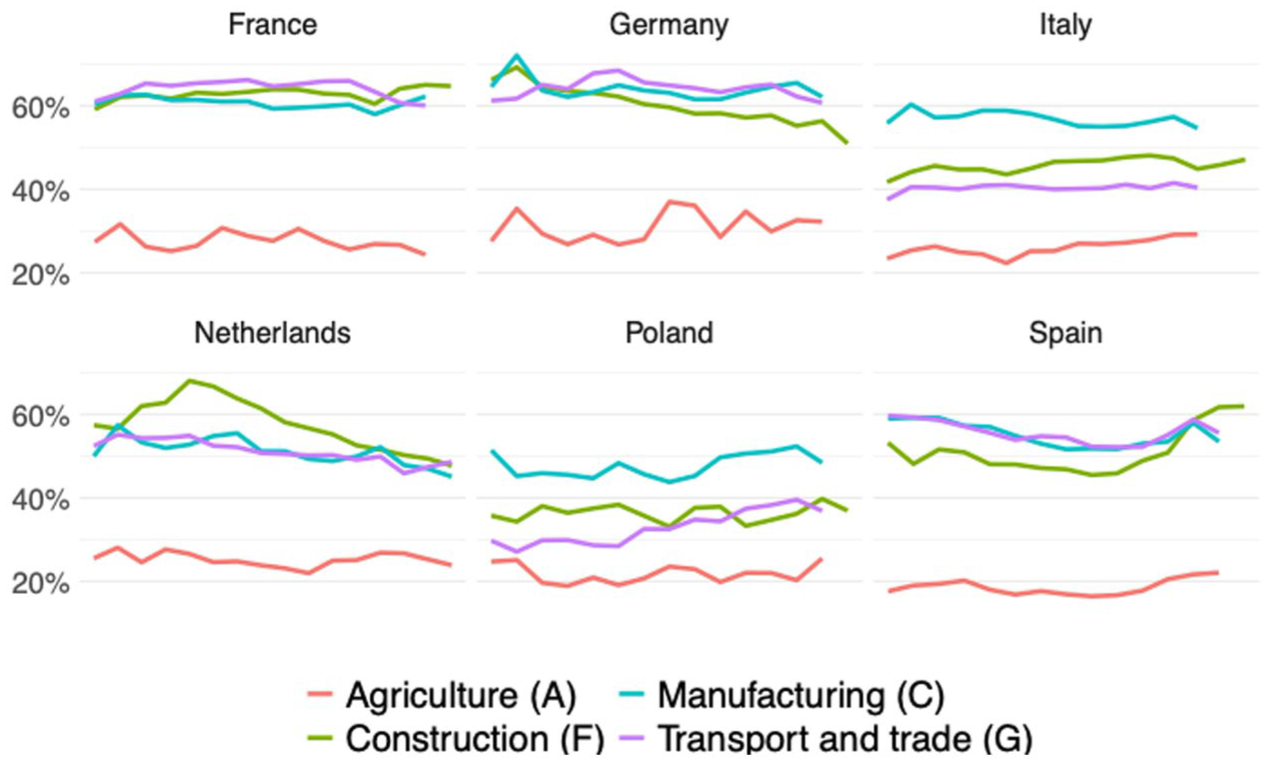

A sectoral breakdown of the wage share in Spain (figure 2) reveals consistently lower values in agriculture and construction, while the highest shares are observed in manufacturing, transportation, and trade. In comparison with the Netherlands, a salient divergence emerges in the construction sector, where the wage share has been substantially higher in the Dutch case throughout most of the period under review. Spain’s employment structure—which relies more heavily on construction than that of its neighboring countries—may help account for the persistent gap in aggregate wage share levels between the two economies. Furthermore, Germany and France consistently report higher wage shares than Spain across all major productive sectors.

Wage share in gross value added at factor cost by sector, 2008–2023.

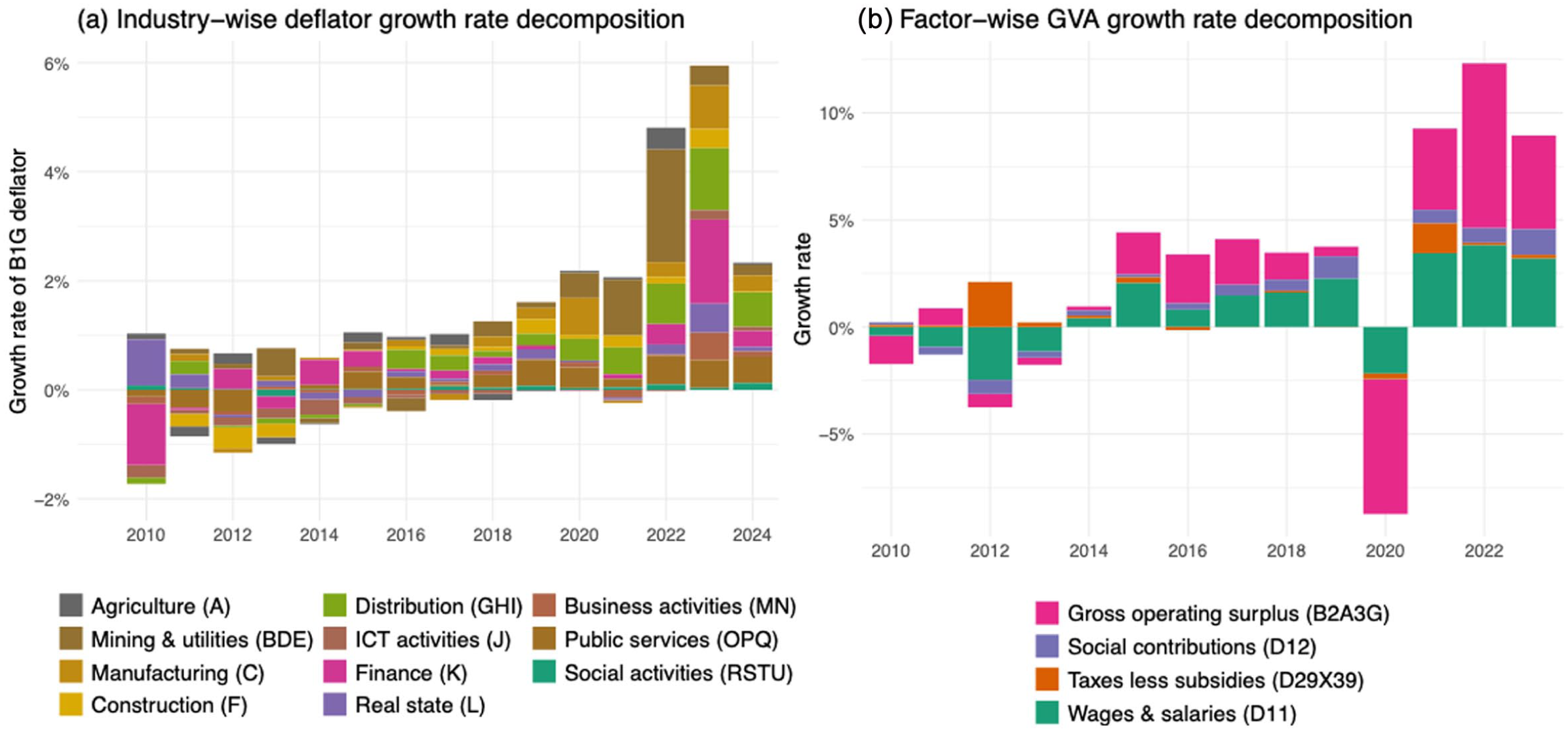

Further insight into the functional distribution of income can be obtained by decomposing the growth of GVA into its main components (figure 3). This decomposition distinguishes the contributions of (a) gross operating surplus, or profits (B2A3G), which include mixed income and imputed rents; (b) wages and salaries (D11); (c) employers’ social contributions (D12); and (d) net taxes and subsidies on production (D29X39). The evolution of nominal GVA is primarily driven by changes in profits (B2A3G) and wages (D11). During the deflationary phase from 2010 to 2014, wages and salaries registered the sharpest decline, while profits contracted only marginally. With the return of economic growth between 2015 and 2019, profits captured the majority of the gains—especially between 2014 and 2017—whereas wage growth contributed more modestly. This dynamic shifted in 2018 and 2019, when the labor share began to increase. In 2020, pandemic-induced shutdowns led to a sharp 13.9 percent contraction in business profits, accounting for 6.2 percentage points of the overall decline in GVA. By 2021, both wages and profits had rebounded; however, in 2022, profit growth once again outpaced wage growth, with profits increasing by 16.4 percent, compared to a 9.4 percent rise in wages and salaries. By 2023, profit growth had declined to 9.3 percent but remained above wage growth, which stood at 7.9 percent.

Growth of gross value added and factor decomposition, current prices: (a) industry-wise deflator growth rate decomposition and (b) factorwise GVA growth rate decomposition. This figure shows the growth rate of GVA at current prices decomposed by its components (right) and the growth rate of the GVA deflator decomposed by industry (left).

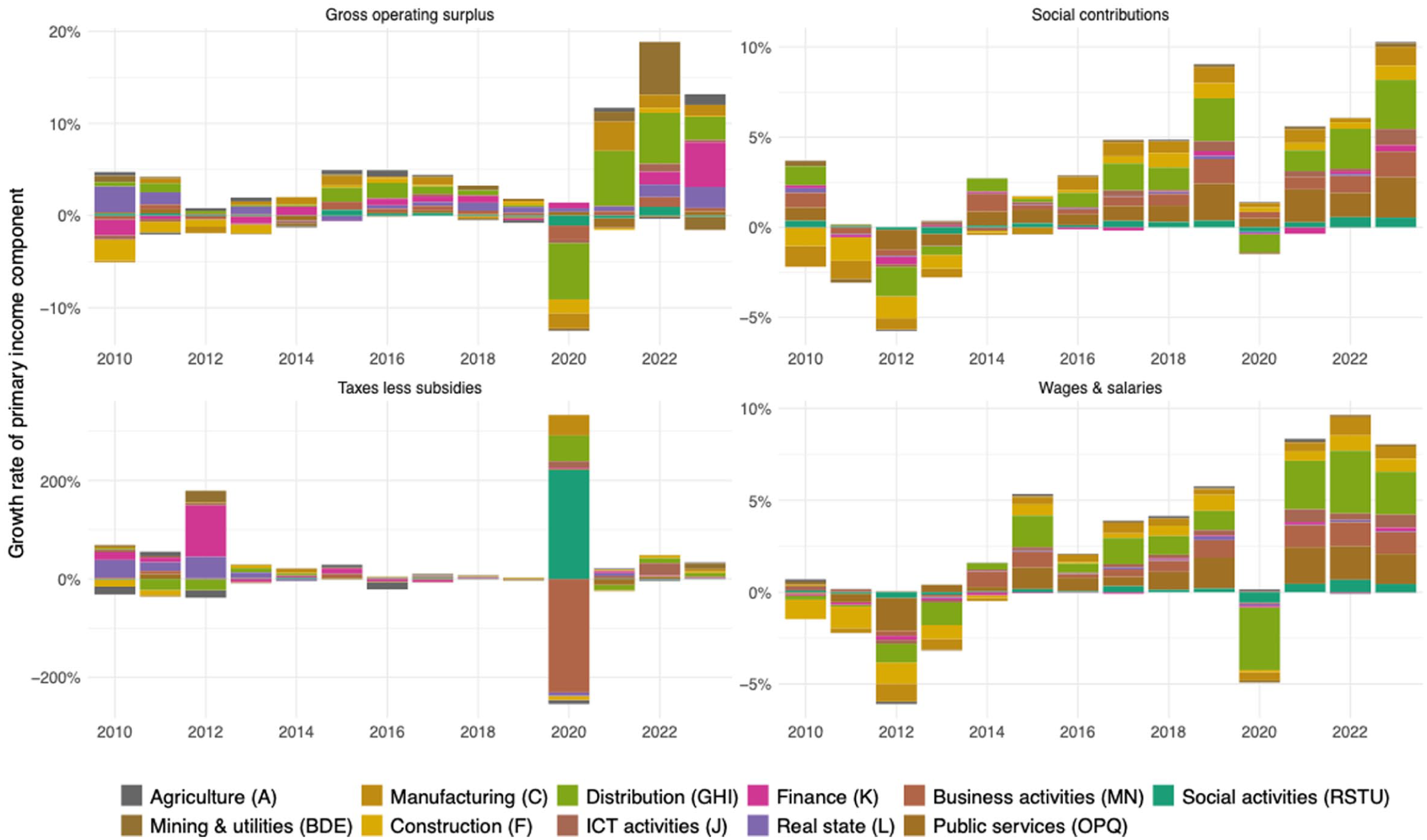

Sectoral dynamics further underscore the heterogeneous drivers of primary income growth and nominal GVA. Figure 4 presents a sectoral decomposition of the income components underlying the aggregate trends depicted in figure 3. The data indicate that, although business profits experienced a sharp acceleration in 2021 and 2022, wage growth had already accelerated prior to the pandemic but decelerated in its aftermath. The sectoral composition of growth also varied across periods. During the crisis years (2010–2014), profit growth was primarily driven by real estate, trade, transportation, and hospitality. In the post-pandemic recovery, trade and transportation remained key contributors, while manufacturing and utilities also emerged as leading sectors. These developments point to a redistribution of functional income in recent years, with capital capturing a growing share at the expense of labor.

Sectoral decomposition of primary income growth components.

4. Wages and Labor Productivity: A Preliminary Empirical Discussion

According to both neoclassical and non-neoclassical theories, the dynamics of wages and productivity are assumed to be connected (Feldstein 2008). Therefore, in this section, we focus on the dynamics of wages and link them to labor productivity.

A common way to relate wages and productivity is through the analysis of unit labor costs (ULC), which measure the relationship between nominal wages and real productivity. ULC are defined as the ratio of average labor costs (nominal wages including social contributions) to labor productivity:

where

ULC have played a central role in debates surrounding the need to restore competitiveness in the eurozone (Felipe et al. 2025). The issue was—and still is—particularly relevant for Greece, Ireland, Italy, Portugal, and Spain. Regardless of how the Great Recession began, analysts concluded that these countries faced a competitiveness problem; that is, labor was too expensive relative to productivity (Sinn 2014). Since devaluation is not possible within the eurozone, and fiscal flexibility is constrained by monetary union, adjustment had to occur through the labor market. As a result, policy discussions focused on how to reduce ULC. Several economists argued that, to close the “competitiveness gap,” especially with Germany, these five countries needed downward adjustments in relative wages, a process known as internal devaluation (Felipe and Kumar 2011). Spain followed this strategy through the labor market reforms of 2010 and 2012.

However, ULC offer only a partial view of the wage-productivity relationship. At the firm level, the indicator is straightforward: it shows labor costs per physical unit of output. At the aggregate level, however, productivity is measured using real GVA, not physical quantities, which has important economic and interpretive implications. Aggregate ULC are not simply the average of firm-level ULC. Instead, they reflect the functional distribution of income:

where

Why does this matter? At the macroeconomic level, ULC are not a straightforward measure of production costs. While ULC clearly reflect unit labor costs at the firm level, their aggregate interpretation is more ambiguous, as they combine information on prices, productivity, and income distribution. Moreover, using ULC as a policy variable frames the issue of competitiveness primarily from the perspective of firms. Workers may care about ULC insofar as they affect business viability, but they are also concerned with the evolution of real wages—that is, the purchasing power of their monetary wages over time. As a result, analyses based on ULC and those based on real wages may send conflicting signals to employers and employees. For instance, ULC may rise while real wages stagnate or decline, leading both firms and workers to perceive losses, or alternatively benefiting one group at the expense of the other. In such contexts, labor-capital conflict is likely to intensify, as appears to be the case in many countries and regions today, including Spain. This ambiguity underscores the need to directly compare the evolution of wages and nominal labor productivity.

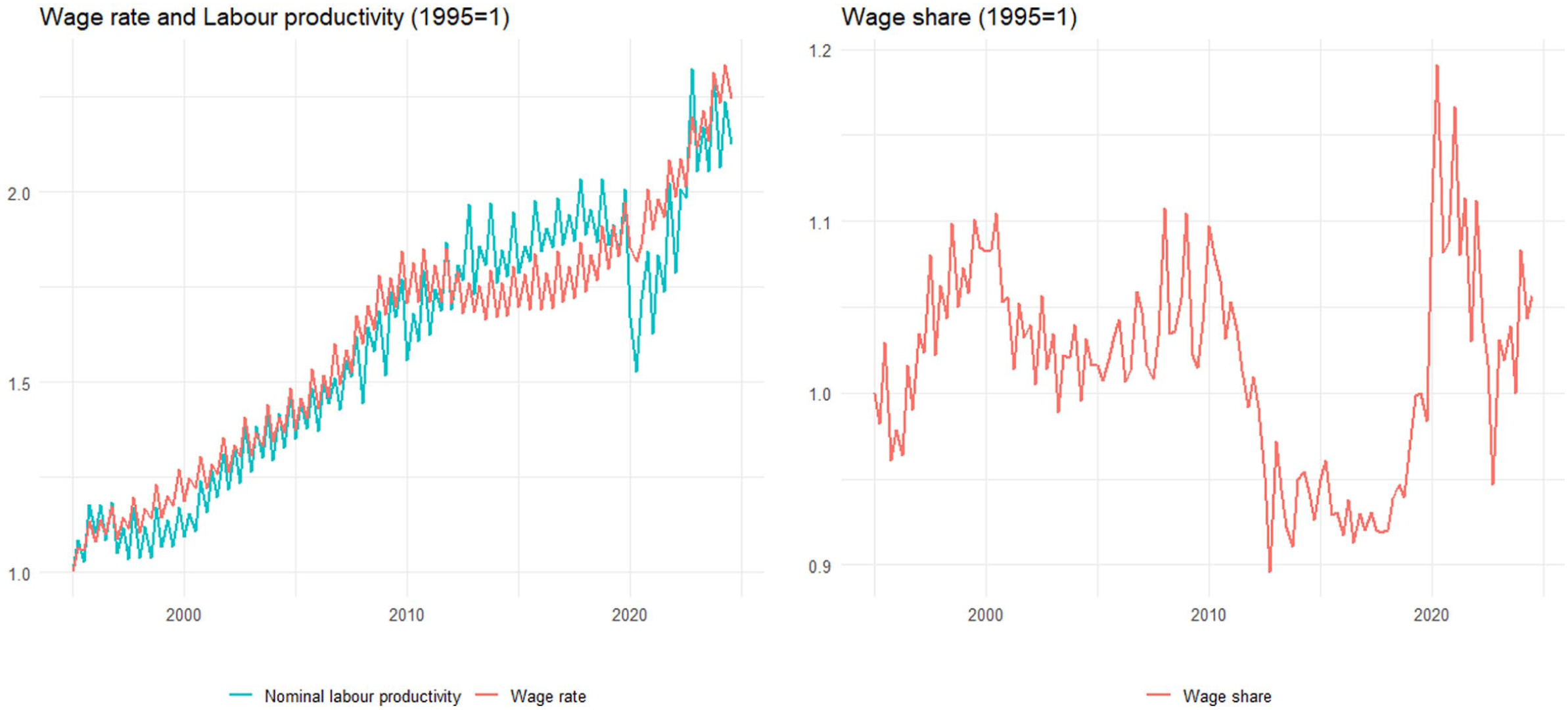

The wage-productivity link remains empirically ambiguous and context-dependent (Brink et al. 2021; Neira 2019; Nasir et al. 2022). However, some empirical evidence suggests a decoupling of wages and productivity in the post-1981 period (Ferguson 1969; Zafirovski 2003), and especially since 2008 (Dosi et al. 2020; OECD 2018; Sharpe and Uguccioni 2017), which calls into question the classical link between the two variables (Rubery 1997). Figure 5 shows that the wage-productivity decoupling is also evident in Spain, especially after the Great Recession. Thus, as stated, this article analyzes the dynamic relationship between the wage rate (

Wage rate and labor productivity in Spain, 1995–2024 (1995 = 1). We use quarterly data from Eurostat. Wages (

5. Methodology

In the context of possible breakdowns of the wage-productivity nexus, we consider potential asymmetries and nonlinearities within a Markov regime-switching approach. Thus, we study the relationship between wages and labor productivity in Spain by means of a Markov regime-switching VAR (MS-VAR) model. We use the Markov-switching VAR model to identify discrete changes in the regimes governing the dynamic relationship between wages and labor productivity over time. Rather than assuming a stable or time-invariant relationship between the variables, this approach allows the parameters of the wage-productivity nexus to differ across regimes that are endogenously determined from the data. These regime shifts follow a Markov process.

Unlike threshold models, the number of regime shifts identified by the MS-VAR model is based on a latent Markov process that is estimated directly from the data. In other words, the main advantage of the MS-VAR model over threshold models is that it does not require the researcher to pre-specify the threshold value or the transition variable prior to estimation. In its simplest form, the Markov process is memoryless; however, it can incorporate additional predictors—such as the lagged annualized wage rate—to influence transition probabilities. In this framework, the probability of moving to a different regime depends only on the current state, not on previous states. This captures the inherent unpredictability in the interaction between labor productivity and wages.

A defining feature of the model is its capacity to allow parameters—including variances of error terms—to vary across regimes (Hamilton 1994, chap. 22). These regimes may reflect states such as high or low wages. Estimating the transition probabilities enables the model to continuously adjust to evolving macroeconomic conditions, thus offering a flexible framework to explore nonlinearities in the labor productivity-wages relationship. We use a switching VAR model (Frühwirth-Schnatter 2006; Hamilton 1994; Krolzig 1997) to capture these nonlinear dynamics.

The base MS-VAR model assumes a k-dimensional VAR(p) process:

where

To further motivate the use of the MS-VAR model, we begin our analysis by identifying structural breaks in each equation and detecting nonlinearity in their residuals. We then conduct a Bayesian model comparison, using the marginal likelihood as the selection criterion, to formally determine the model that best captures the optimal number of regimes. Specifically, we compare the marginal likelihoods of MS-VAR specifications across combinations of the number of regimes M = 1, 2, 3, 4, 5, and the regime persistence parameter q = 0, 10, 50, 100, 500, 1000. For ease of comparison, we report the log marginal likelihood differences between each MS-VAR specification and the constant (linear) VAR model. A positive value indicates a better in-sample fit relative to the constant VAR. The results show that the specification with M = 2 and q = 50 yields the highest relative marginal likelihood, suggesting that the optimal number of regimes is two.

Since we consider the existence of two regimes, in equation (3) we define

Given the substantial increase in the number of parameters implied by regime-switching dynamics, we specify the model in a parsimonious bivariate framework. The analysis focuses on the joint dynamics of wages and labor productivity. Adopting a low-dimensional Markov-switching VAR allows for reliable estimation and clear identification of regime-dependent behavior, while avoiding overparameterization and instability that often arise in higher-dimensional nonlinear systems. The purpose of this specification is not to provide a full-fledged representation of the entire economic system but rather to isolate and examine changes in the dynamic relationship between wages and labor productivity across regimes, which would be obscured under linear or time-invariant models.

We do not assume constant transition probabilities. Instead, they depend on an intercept and lagged labor productivity. Following Krolzig (1997), we rewrite the model in switching intercept form to accommodate regime changes. In our specification, regime-switching applies to intercepts, lagged coefficients, and error variances. The transition probabilities between regimes follow a first-order Markov process, where:

and can be modeled using a logit function:

where

where

Estimating the model requires a recursive algorithm. At each step, filtered regime probabilities from period

6. Empirical Results

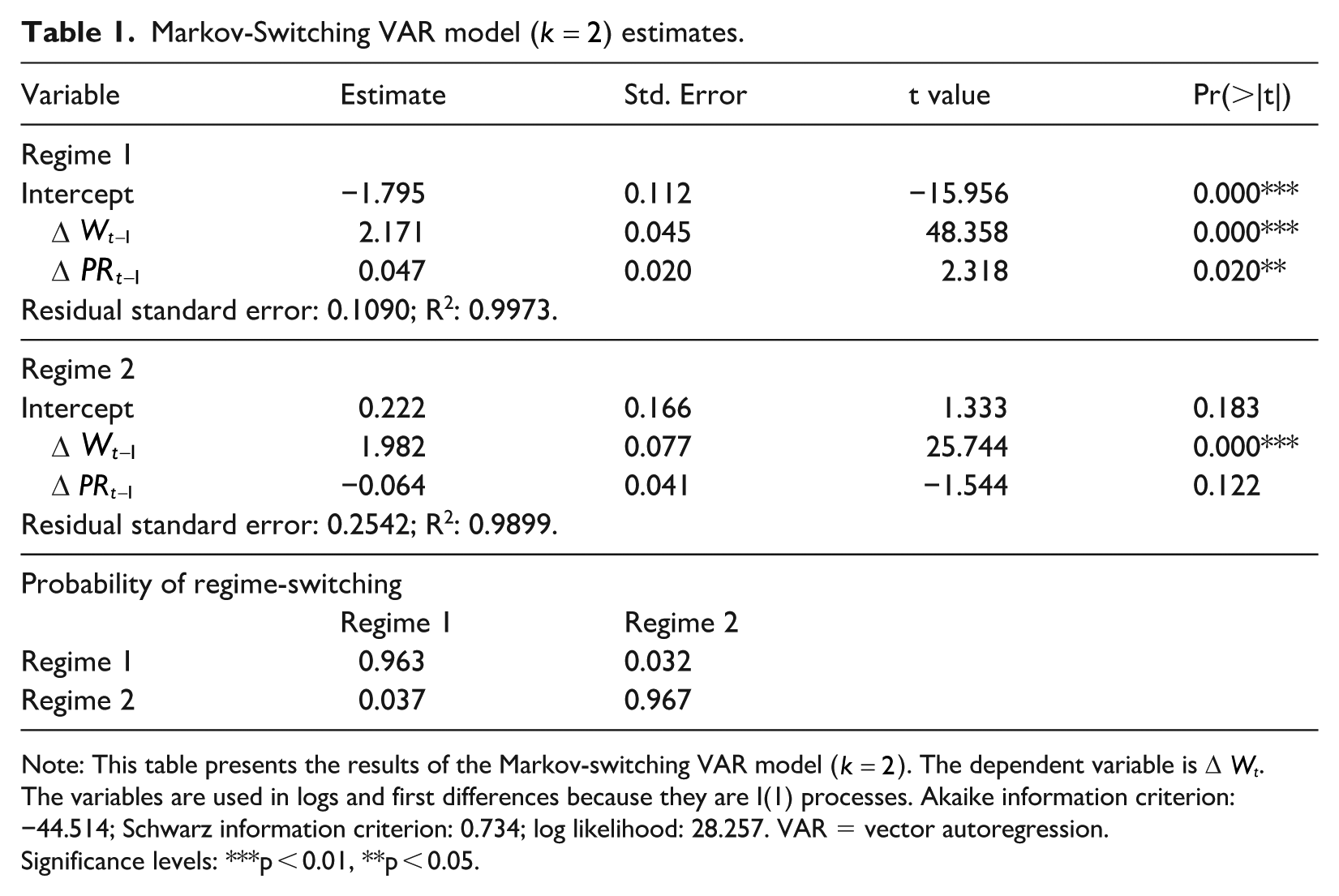

Table 1 reports the estimated MS-VAR model for the wage rate (w) and nominal labor productivity (

Markov-Switching VAR model (

Note: This table presents the results of the Markov-switching VAR model (

Significance levels: ***p < 0.01, **p < 0.05.

The specification of the model implies that the wage trend is, at every point in time, in one of the two regimes. Table 1 indicates that the standard deviation of the wage rate in regime 2 (0.2542) is higher than in regime 1 (0.1090), which probably means that wage growth changes more dramatically in regime 2 than in regime 1 (Lütkepohl and Netšunajev 2014). In addition, we find that the model exhibits the characteristics of a jumping-intercept regime-switching process in its dynamic behavior, since the intercept differs across regimes, and that the influence of exogenous shocks also displays prominent regime-specific features, since the standard deviation differs substantially across regimes. Table 1 also shows that the growth rate of w lagged one period has a significant positive effect on the growth rate of w itself, and that the growth rate of

We assess the robustness of the results with respect to lag length by re-estimating the two-regime Markov-switching VAR using longer lag structures (p = 2 and p = 4). The main qualitative findings are unaffected: Regime classification and smoothed regime probabilities remain very similar, and the regime-dependent dynamics between wages and labor productivity are preserved. Because of space constraints, detailed results are not reported here but are available from the authors upon request.

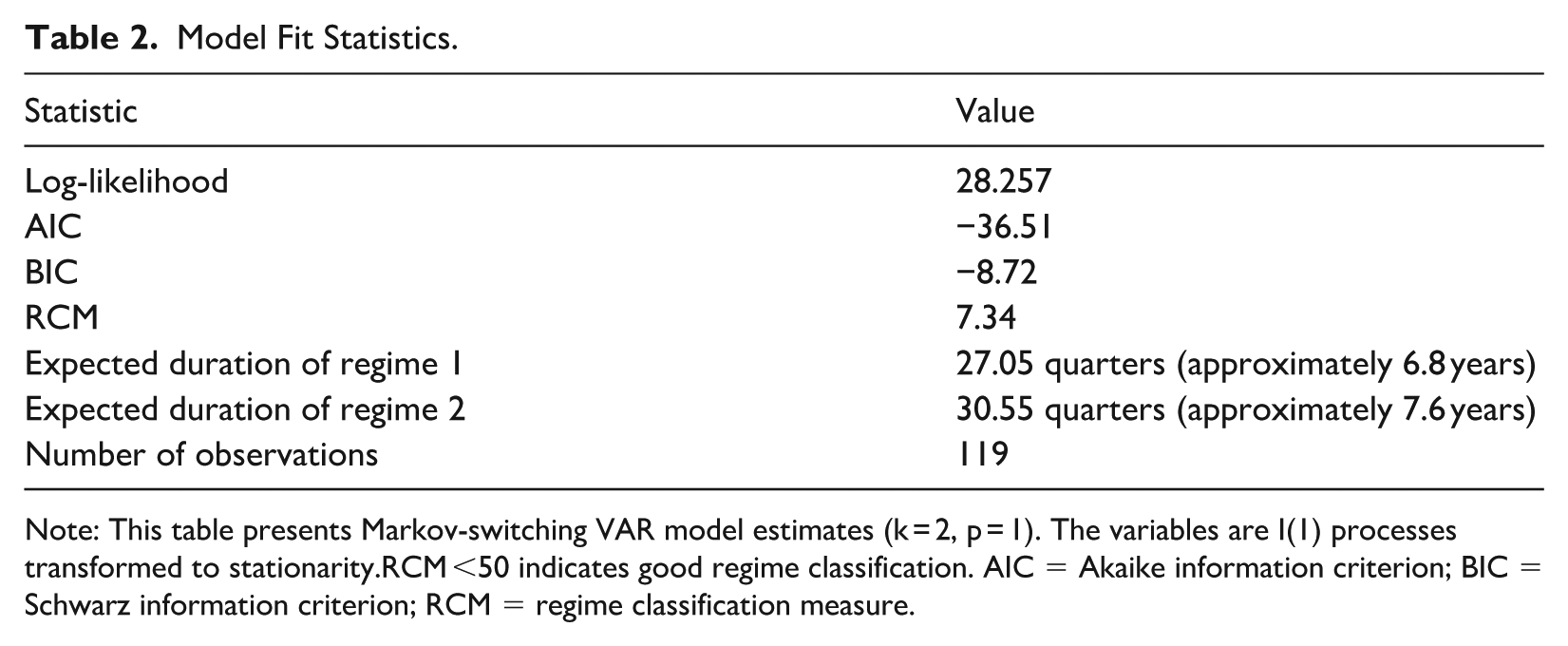

Table 2 reports model fit statistics and regime diagnostics for the baseline two-regime Markov-switching VAR with one lag. The model exhibits a good overall fit, as reflected in the log likelihood and information criteria values. The regime classification measure (RCM) equals 7.34, which indicates excellent regime separation and a high degree of classification accuracy. Estimated transition probabilities imply highly persistent regimes, with expected durations of approximately 27 quarters (6.8 years) for regime 1 and 31 quarters (7.6 years) for regime 2. These results suggest that the model captures economically meaningful and persistent phases rather than short-lived fluctuations, which supports the relevance of the two-regime specification.

Model Fit Statistics.

Note: This table presents Markov-switching VAR model estimates (k = 2, p = 1). The variables are I(1) processes transformed to stationarity.RCM <50 indicates good regime classification. AIC = Akaike information criterion; BIC = Schwarz information criterion; RCM = regime classification measure.

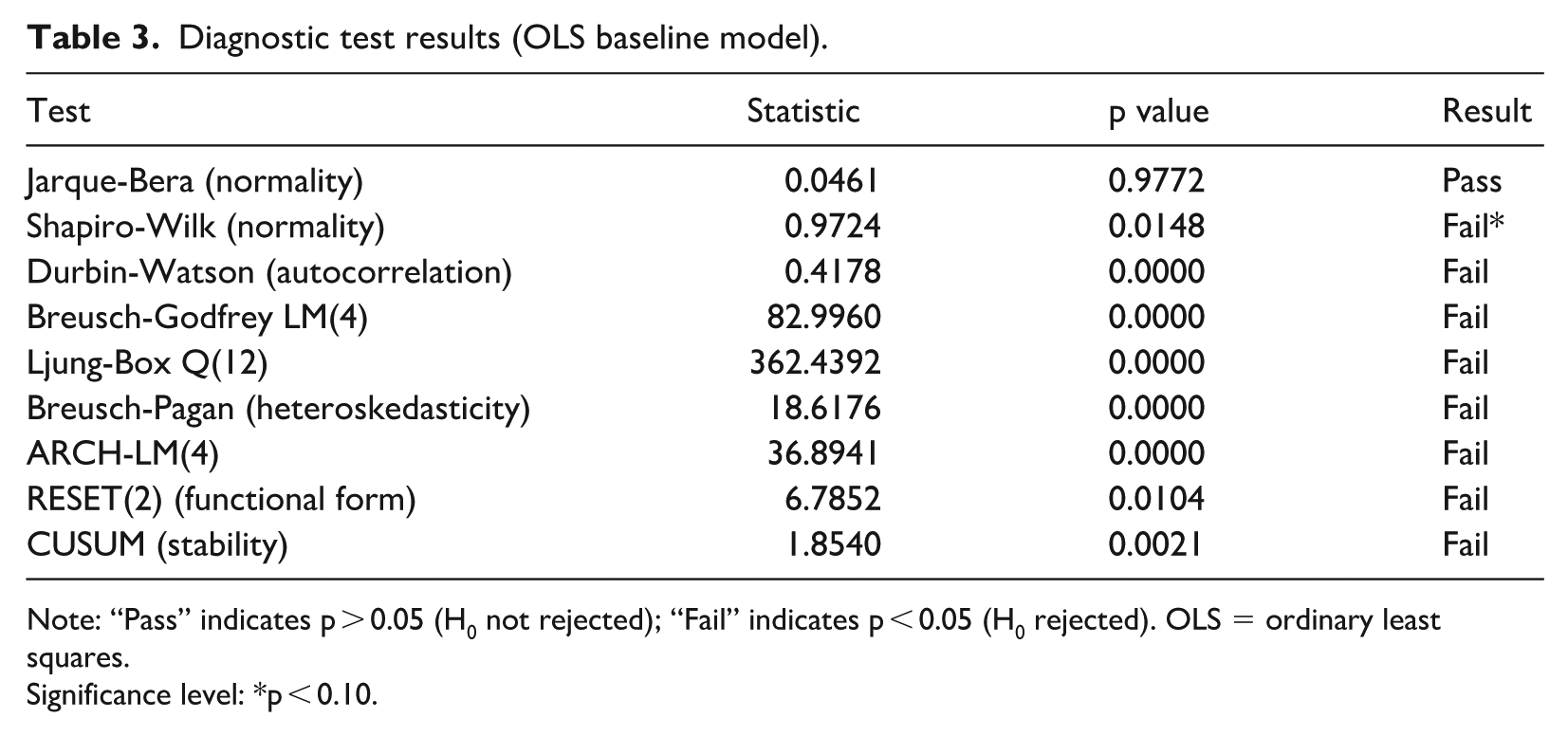

To motivate the use of a nonlinear regime-switching framework, table 3 reports standard diagnostic tests for a baseline linear ordinary least squares model. The results reveal substantial departures from the assumptions underlying linear time-invariant specifications. In particular, multiple tests strongly reject the absence of serial correlation and homoskedasticity, while functional-form and stability tests indicate structural instability over the sample period. These findings suggest that the wage-productivity relationship is characterized by time-varying dynamics and regime-dependent behavior that cannot be adequately captured by a linear model, thereby providing strong empirical motivation for adopting a Markov-switching specification.

Diagnostic test results (OLS baseline model).

Note: “Pass” indicates p > 0.05 (H0 not rejected); “Fail” indicates p < 0.05 (H0 rejected). OLS = ordinary least squares.

Significance level: *p < 0.10.

Additional evidence in support of regime-dependent dynamics is provided by breakpoint and stability diagnostics, which identify structural changes at observations corresponding approximately to the middle and late portions of the sample. These breakpoints are broadly consistent with the timing of regime transitions inferred from the smoothed probabilities of the Markov-switching model. While the breakpoint analysis is conducted independently of the MS framework, the alignment between both approaches reinforces the interpretation of the estimated regimes as capturing genuine structural changes in the relationship between wages and labor productivity.

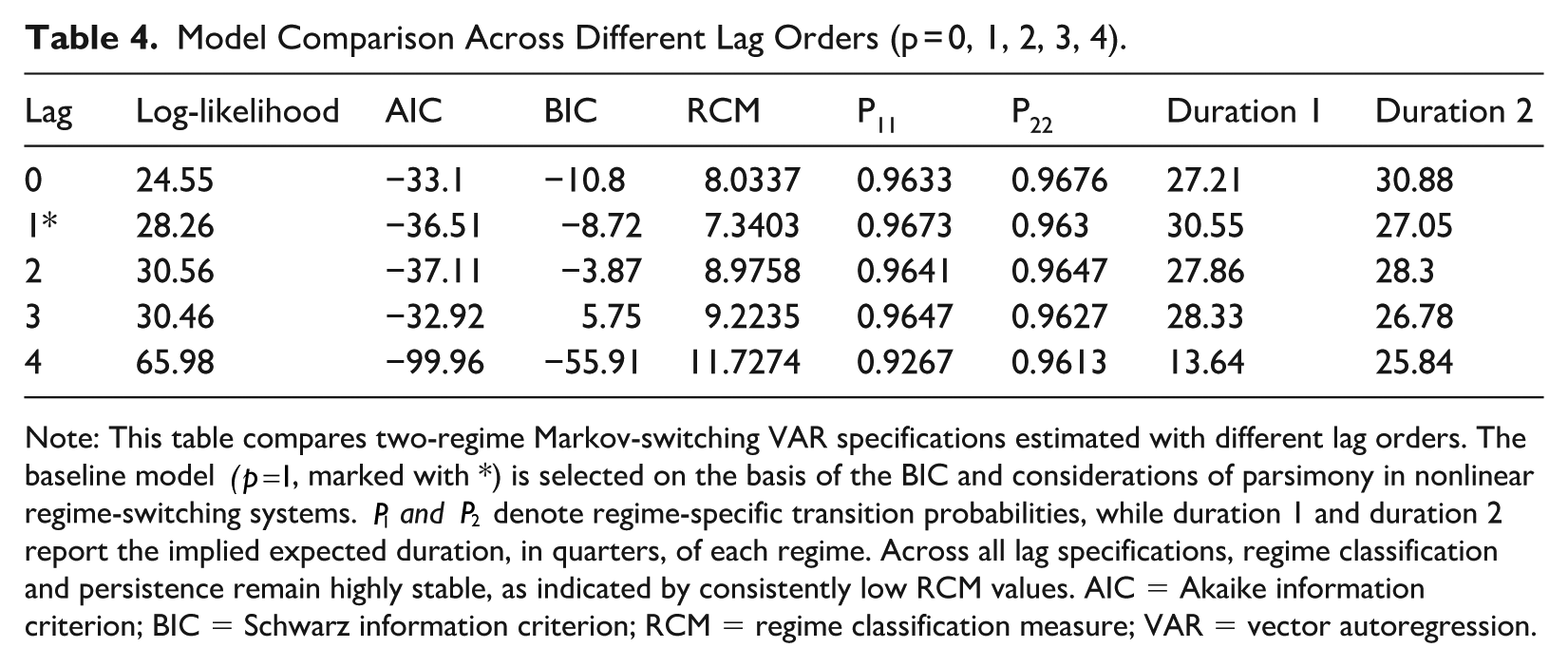

Table 4 examines the robustness of the results to alternative lag specifications, ranging from zero to four lags. While information criteria favor parsimonious models (p = 0 or p = 1), the key qualitative findings remain remarkably stable across all specifications. In particular, estimated transition probabilities display limited variation, regime persistence remains high, and all RCM values indicate excellent regime separation. Even when adopting longer lag structures, commonly suggested for quarterly data, the identification and interpretation of the two regimes are preserved. These results confirm that the substantive conclusions of the paper are not driven by the specific lag-length choice. Overall, the diagnostic and robustness evidence indicate that the estimated regime structure is stable, well identified, and robust to alternative dynamic specifications, lending credibility to the regime-dependent interpretation of the wage-productivity relationship.

Model Comparison Across Different Lag Orders (p = 0, 1, 2, 3, 4).

Note: This table compares two-regime Markov-switching VAR specifications estimated with different lag orders. The baseline model

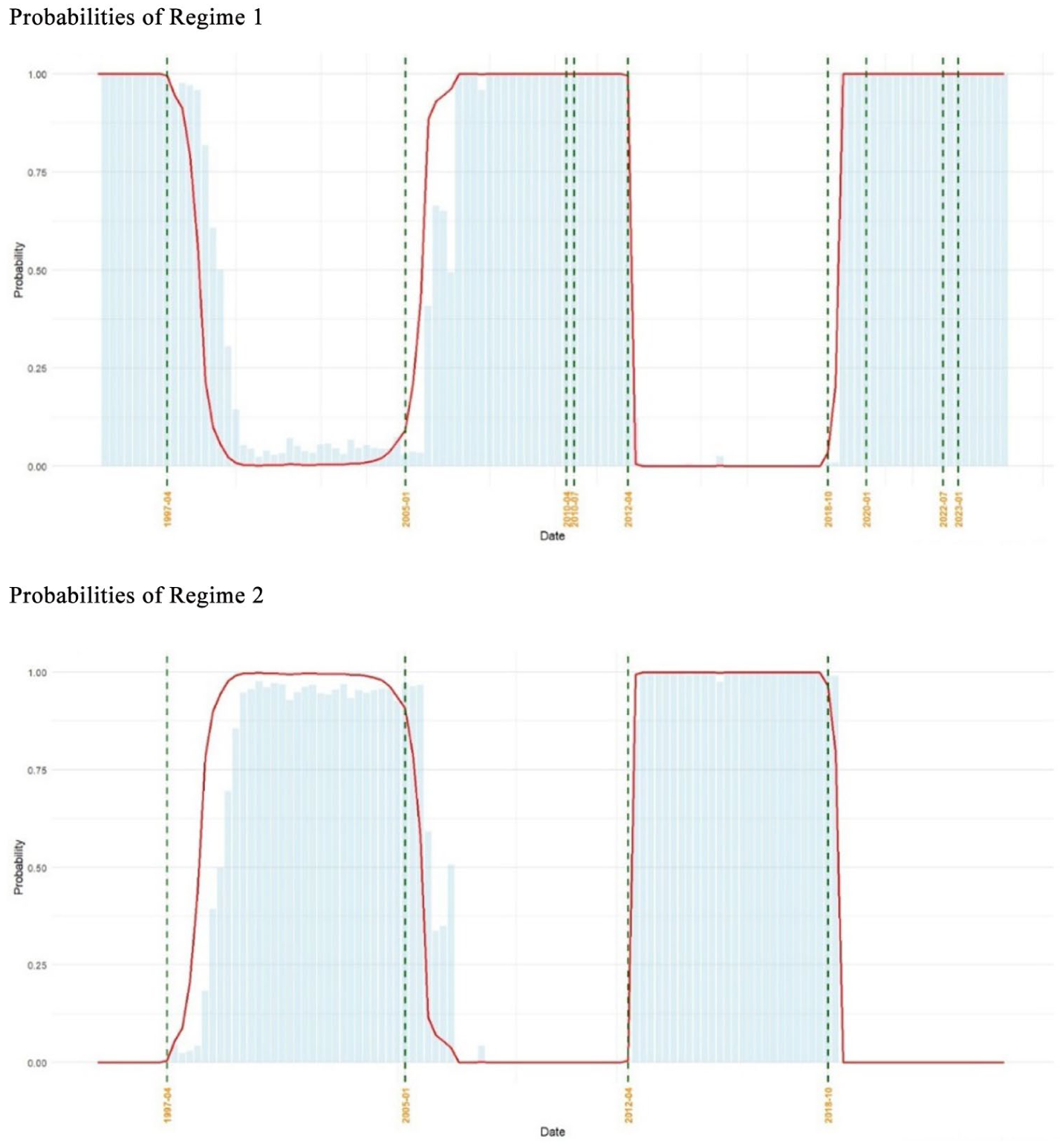

Figure 6 plots the smoothed probabilities for both regimes estimated from the MS-VAR model. The red line represents the smoothed probabilities, while the light-blue bars indicate the fitted probabilities. The green dashed lines mark the beginning and end of the condition under which the smoothed probability exceeds the fitted probability. The main conclusion is that the relationship between wages and productivity in Spain was in regime 1 between January 1995, the first observation in the series, and April 1997; between January 2005 and April 2012; and between October 2018 and the end of the sample. By contrast, it was in regime 2 between April 1997 and January 2005, and between April 2012 and October 2018.

Markov-switching VAR results. Regime probability. This figure displays the regime probabilities from the Markov-switching VAR model. The red line represents the smoothed probabilities, while the light-blue bars indicate the fitted probabilities. The green dashed lines mark the beginning and end of the condition under which the smoothed probability exceeds the fitted probability. VAR = vector autoregression.

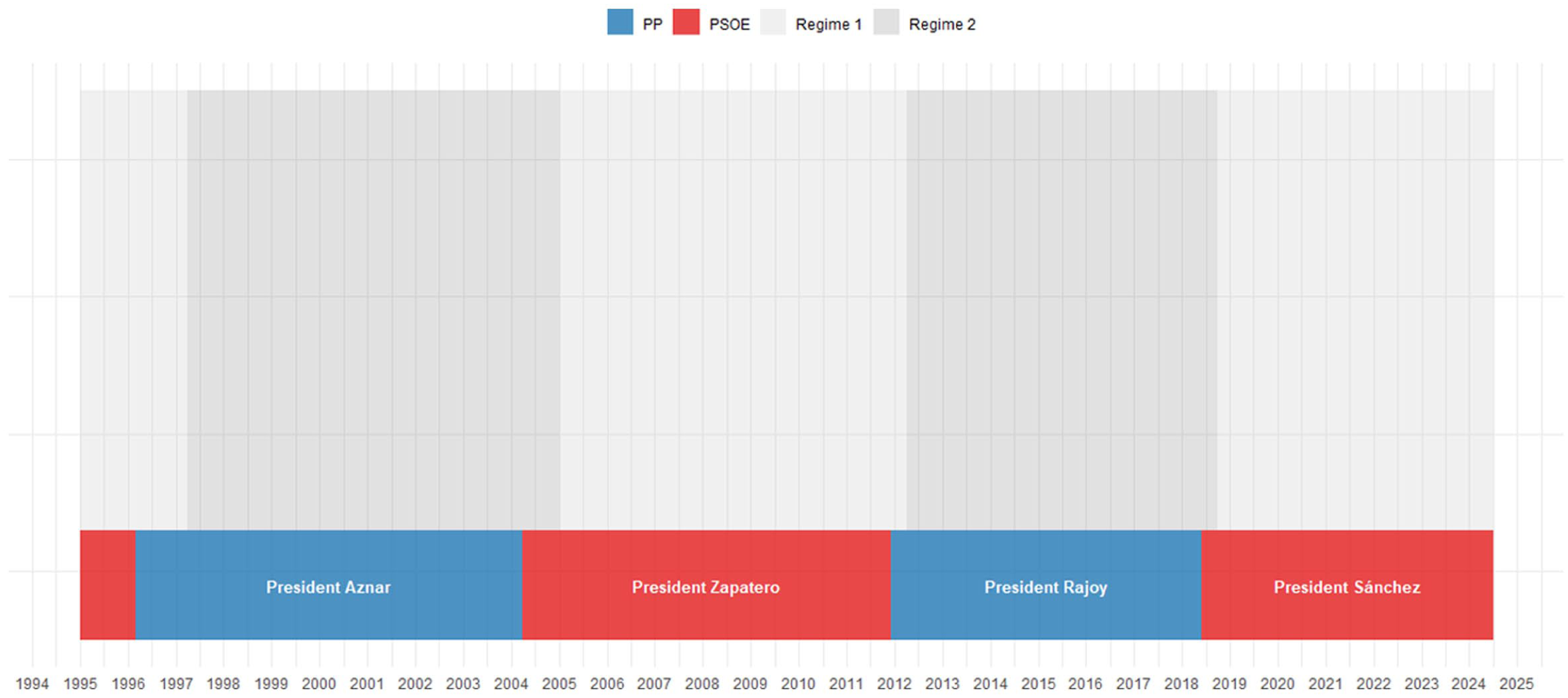

As figure 7 shows, these regime shifts closely align with the alternation in power between Spain’s two main political parties, the conservative PP and the center-left PSOE. The PP won the general election for the first time in March 1996, while the PSOE returned to power after winning the March 2004 election. The PSOE governed for two legislative terms, until the general election of November 2011. The PP then regained power in 2012 under the leadership of Mariano Rajoy and remained in office until a vote of no confidence in 2018. Since then, the PSOE has been in government, although, for the first time in Spain’s recent democratic history, in coalition with other parties.

Comparison of regime shifts and governing political parties in the general government (01/1995–07/2024).

Figure 7 indicates that, during periods of PSOE, the relationship between wages and productivity tends to be under regime 1. Conversely, under right-wing administrations (PP), wage growth and productivity dynamics tend to be under regime 2. We also observe that regimes tend to persist for a short period following a change in the governing political party. This likely reflects the minimum time required to initiate and implement a new legislative framework.

These regime-dependent patterns can be further contextualized by considering differences in wage-related policies implemented under PP and PSOE governments. Periods of PSOE governance have generally been associated with measures aimed at supporting wage growth and reinforcing wage-setting institutions, including increases in the statutory minimum wage, a stronger role for collective bargaining, and, in recent years, the partial reversal of earlier labor market deregulation. By contrast, PP administrations have tended to emphasize labor market flexibility and cost competitiveness, most notably through the 2012 labor market reform, which weakened collective bargaining coordination and increased downward wage flexibility.

This comparison, however, should not be interpreted as implying a universal or automatic partisan effect. Wage outcomes remain contingent on broader macroeconomic conditions and political constraints, and right-wing governments may also promote wage increases under specific circumstances. In the Spanish case, while these policy differences are broadly consistent with the regime-specific wage-productivity dynamics identified in figures 6 and 7, the relationship is neither mechanical nor uniform over time.

A more nuanced interpretation is required for the first PP administration under Aznar. As shown in figure 5, during the initial phase of this period (approximately 1997–2000), wage growth appears to outpace productivity growth, implying a temporary increase in the wage share. This is followed by a reversal during the period 2000–2004, when productivity growth exceeds wage growth.

This pattern, together with the lack of statistical significance of γ in table 1, suggests that the relationship between wages and labor productivity is not stable within regime 2. Rather than indicating a uniform decoupling in one direction, regime 2 is better understood as a phase characterized by an unstable or indeterminate relationship between wages and productivity. In particular, it encompasses episodes in which wages grow faster than productivity (1997–2000) as well as periods in which productivity outpaces wages (2000–2004 and 2012–2018), leading to an overall absence of a systematic relationship.

This interpretation is also consistent with the institutional context. Although the 1997 labor market reform is generally regarded as unfavorable to labor, the statutory minimum wage increased faster than inflation during the period 1997–2000, which may have contributed to the temporary improvement in wage dynamics. By contrast, during the period 2000–2004, minimum wage growth lagged behind inflation, contributing to the subsequent weakening of wage growth relative to productivity.

This narrative is consistent with the MS-VAR results, which identify regime shifts as probabilistic and time-varying rather than perfectly aligned with political mandates. In this sense, the model captures broader phases in the wage-productivity relationship that may overlap with, but do not necessarily coincide exactly with, electoral cycles. Therefore, the results should be understood as indicating a systematic association between political regimes and wage dynamics, while allowing for transitional periods and within-regime heterogeneity.

This said, the overall correspondence between political alternation and regime-dependent wage-productivity dynamics should be interpreted in light of the cumulative and institutional nature of labor market regulation in Spain. Major labor reforms, particularly those affecting collective bargaining coordination, dismissal protection, and wage-setting norms, do not merely alter incentives at the margin but reconfigure the balance of power between labor and capital. Changes such as the decentralization of collective bargaining, the weakening of ultra-activity, or the reduction of dismissal costs can have persistent effects on wage-setting behavior by reshaping expectations, threat effects, and coordination mechanisms across firms and sectors. In this sense, legislation can be effective not because it mechanically determines wages, but because it alters the institutional environment within which wages and productivity are jointly determined over time. The regime shifts identified in this article thus reflect broader transformations in the political and institutional framework of wage setting rather than the impact of isolated policy measures.

Therefore, several major labor market reforms provide a concrete institutional background for the regime shifts identified in this article. The 1994 reform expanded objective dismissal to include organizational and production-related causes, while the 1997 reform introduced a new open-ended contract with lower dismissal costs. The 2002 reform further strengthened employers’ position by eliminating procedural wages when firms acknowledged unfair dismissal and deposited the corresponding compensation. These changes increased firms’ ability to adjust employment conditions and strengthened the credibility of dismissal threats in wage bargaining, thereby exerting downward pressure on wage growth relative to productivity.

A key turning point occurred with the 2012 labor market reform, which significantly altered the structure of collective bargaining. In particular, it granted priority to firm-level agreements over sectoral agreements and limited the ultra-activity of collective agreements to one year. These changes weakened coordination in wage setting and increased downward wage flexibility, contributing to a more pronounced decoupling between wages and productivity during the subsequent period.

By contrast, the 2021 labor reform partially reversed these changes by restoring the central role of sectoral agreements and reintroducing indefinite ultra-activity. This institutional rebalancing strengthened collective bargaining coordination and reduced the scope for firm-level wage competition, thereby contributing to the observed recovery in wages relative to productivity.

The case of the Zapatero administration can be understood in this context. Despite the presence of earlier liberalizing reforms, collective bargaining institutions remained relatively coordinated and were supported by favorable macroeconomic conditions, allowing wages to evolve broadly in line with productivity. This suggests that the effects of labor market reforms are cumulative and mediated by institutional and macroeconomic conditions, rather than immediate or mechanically determined.

An additional dimension highlighted in the literature concerns the role of wage inequality in shaping the wage-productivity decoupling. In particular, studies for the United States show that the decoupling is substantially larger when focusing on nonsupervisory workers, as rising compensation at the top of the wage distribution, especially among executives and supervisory workers, partly masks stagnation for the majority of workers (Palladino 2021). This applies also for the Spanish case (see Ferrer and Pérez-Montiel 2025). From this perspective, aggregate wage measures may understate the extent of distributive tensions when wage gains are concentrated among higher earners. While comparable data distinguishing supervisory and nonsupervisory workers are not readily available for Spain over a long time horizon, this channel is conceptually relevant and complements the analysis of functional income distribution developed in this article. Accounting jointly for functional and personal income distribution remains an important avenue for future research.

7. Conclusion

This article has examined the dynamic relationship between wages and labor productivity in Spain over the past three decades. Contrary to the conventional view that wages closely track productivity, our findings suggest a more complex and politically contingent dynamic. We identify two distinct regimes: one in which wage growth and productivity growth are positively related (regime 1), and another in which wages and productivity relatively decouple (regime 2). Importantly, these shifts are not random but appear to coincide with political transitions between Spain’s two dominant parties—the conservative PP and the center-left PSOE.

While much of the existing literature attributes wage-productivity decoupling to structural and market-based factors—such as globalization, technological change, or institutional erosion—we find that political power also matters. Periods of PSOE governance are more frequently associated with regimes in which wages and productivity are statistically associated, whereas PP administrations correspond more often to phases of decoupling. This suggests that wage dynamics are not merely the outcome of impersonal market forces but are shaped by political choices, labor market reforms, and broader distributional coalitions.

Our results have several implications. First, they call for a reassessment of the dominant narrative that low wage growth in Spain is a natural consequence of low productivity growth. Second, they point to the importance of incorporating political variables into macroeconomic models of income distribution. Third, they open new lines of inquiry into the specific policy mechanisms—such as collective bargaining structures, minimum wage policy, and fiscal frameworks—through which political parties influence wage-productivity dynamics. In sum, this article underscores that the wage-productivity nexus is not stable, neutral, or automatic. Instead, it might be mediated by political decisions and institutional configurations that evolve over time.

Our analysis is subject to several limitations that also suggest directions for future research. The empirical strategy relies on a parsimonious, reduced-form regime-switching framework designed to capture broad shifts in the wage-productivity relationship, rather than to identify specific causal mechanisms. As such, the article abstracts from the explicit consideration of policy instruments, institutional variables, and distributional conflicts that may underpin regime transitions. Moreover, while the focus on Spain allows for a politically grounded interpretation of the results, it also limits the generalizability of the findings. Future research could build on this contribution by integrating regime-switching approaches with richer political and institutional indicators, exploring cross-country or comparative settings and examining how regime-dependent wage-productivity dynamics interact with inequality, demand formation, and macroeconomic instability.

Footnotes

Acknowledgements

The authors thank the three referees and the editor for their helpful and constructive comments and suggestions. The usual disclaimer applies.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was carried out thanks to the financial support of the research projects PID2024-157174NB-100 and PID2022-137648OB-C21, funded by Ministerio de Ciencia e Innovación (Madrid), MCIN/AEI/ 10.13039/501100011033 and by the European Regional Development Fund, “ERDF A way of making Europe.”

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

1

In the absence of continuous full employment, the rate of interest can only determine the desired capital/labor ratio. As ![]() argues, investment therefore remains indeterminate until firms determine their desired capital stock. This determination depends on desired productive capacity and, in turn, on expected demand and its evolution.

argues, investment therefore remains indeterminate until firms determine their desired capital stock. This determination depends on desired productive capacity and, in turn, on expected demand and its evolution.

2

This raises the question of how Spanish capitalism has sustained itself despite the long-term decline in the purchasing power of wage-earning households since the 1970s. Neither consumption nor investment has followed a secular downward trend proportional to the fall in the wage share. Several post-Keynesian contributions argue that household debt has increasingly replaced wages as the main driver of aggregate consumption (Febrero et al. 2019; Álvarez et al. 2019, among others). Rising income inequality has reinforced this process by fueling credit expansion and asset-price booms (![]() ). These dynamics have directed attention toward the sustainability of a debt-led growth regime—often described as financial capitalism—which ultimately collapsed in 2008.

). These dynamics have directed attention toward the sustainability of a debt-led growth regime—often described as financial capitalism—which ultimately collapsed in 2008.