Abstract

This article aims to explore the short- and long-run impact of foreign direct investment (FDI), financial development (FD), capital formation, and the labor forces on the economic growth of Bangladesh. We applied the Granger causality test and Vector Error Correction Model (VECM) for this study. The World Bank data for the period of 1990–2018 are taken into account for the analysis. Our findings suggest, in the long run, capital formation has a positive impact, and in the short run, it has a negative impact on gross domestic product (GDP) implying a lack of higher efficiency is persisting in capital management. Similarly, labor forces have an insignificant impact in the short run and a negative impact in the long run on GDP, which confirms the presence of a huge number of unskilled laborers in the economy with inefficient allocation. The impact of FD is found tiny positive in the short run but large negative in the long run on GDP indicating vulnerability of banking sector. These also confirm fraudulence and inefficient use of the domestic credit supplied to the private sector. The impact of FDI is approximately null both in the short and long run, indicating Bangladesh fails to achieve the long-term benefits of FDI. Finally, this study suggests using FDI more in the capital intensive project of the public–private partnership venture than infrastructural development only and also improving the credit management policy of the banking sector.

Introduction

The economy of Bangladesh is strategically important for Southeast Asia because of its geographical location and seaport facilities. In the fiscal year (FY) 2018, Bangladesh was the second-fastest growing economy in the world with its highest gross domestic product (GDP) growth rate of 7.86%, and in the FY 2017, the GDP growth rate was 7.28% with a per capita income of $1610. In 2019, the real GDP growth rate of Bangladesh was above 7% and its potential growth rate indicating a steady rise in its economy (The World Bank, 2018a, 2018b, 2019).

A developing countries GDP is increased only when continuous development takes place in the agricultural, industrial, and financial sectors of the respective country. To sustain economic development for a longer period, efficient allocation of capital and labor forces is keenly required. If a country fails to ensure efficient allocation of its capital and uses more unskilled labor forces in the production processes, it apparently would result in lower economic growth than expected. Sometimes this may also cause negative GDP growth too.

Capital formation starts from savings which are the portion of national income not spent in the consumption. Next, the savings are transformed into loanable funds and finally, the funds are converted into investment capital or disbursed as credit through the financial system. However, developing countries mainly accumulate the capital from the two sources: (a) foreign direct investment (FDI) and (b) financial development (FD), that is, domestic credit supplied to the private sector.

FDI is considered a well-known source of investment capital and technical know-how for a developing country for long. According to Griffin and Pustay (2007), an investment would be considered as FDI if it owns 10% or more voting capital of a foreign firm. Farrell (2008) defined FDI as a package of technology, management, and entrepreneurship along with capital supply. Later, Salorio and Brewer (1998) added that reinvested earnings and short- and long-term intracompany debt flows are also considered as FDI. Therefore, FDI provides local firms with skilled technical know-how beyond their border and enable them to improve their product quality and enter into the wider market places.

Countries mainly accept FDI to accelerate the economic growth through capital formation in the potential sectors. Several pieces of research support this theoretical concept across the world (e.g., see Choe, 2003; Chowdhury and Mavrotas, 2006; Griffiths and Sapsford, 2003). Some studies also find bidirectional causality between FDI and economic growth (see Al-Iriani, 2007; Chakraborty & Nunnenkamp, 2006). In recent times, Ibrahiem (2015) confirms FDI has a long-run positive impact on the economic growth of Egypt. He also finds that the correct spillover of FDI, that is, public–private partnership firm increases more real per capita GDP in Egypt.

Earlier, Borensztein et al. (1998) and De Mello (1999) examined the relationship between FDI and economic growth in a sample of Organisation for Economic Co-operation and Development (OECD) and non-OECD countries over the period of 1970–1990. Their study suggests two critical findings: First, the extent of technical know-how and the technology determines the long-run economic growth of the host countries, and second, the more host country substitutes FDI against domestic investment, the more economic growth is achieved. This is also suggested by Hermes and Lensink (2010), who find strong evidence of FDI’s positive impact on the economic growth of 37 countries where developed financial system persists. Thus, it is expected that an efficient allocation of FDI will accelerate the economic growth of a country.

But, studies also find the weak, null, and insignificant impact of FDI in the economic growth of many underdeveloped, developing, and a few developed countries across the world (e.g., see Ericsson and Manuchehr, 2001; Sarkar, 2007). Okumoko et al. (2018) find an insignificant but long-run positive impact of FDI in the economic growth of Nigeria and (Ek, 2007) finds the same in China. Moreover, Aga (2014) finds an insignificant short-run positive impact of FDI on the economic growth of Turkey.

In recent times, Sokhanvar (2019) finds FDI has a negative impact in the economic growth and fails to accelerate the tourism industry of the seven selected European countries. Before him, Khaliq and Noy (2007) evidenced a negative impact of FDI on economic growth of 47 countries around the world. However, this is also factual that the negative impact is observed mainly in the underdeveloped and developing economy where financial markets are hardly efficient.

By FD, we mainly refer to providing liquidity in the capital market which increases the economic production level and finally increases the economic growth of a country. Caporale et al. (2004) and Levine and Zervos (1998) find market liquidity has more impact on economic growth than market size. However, this statement is mostly applied in the emerging markets (Rousseau & Wachtel, 2000).

In addition to the developed economy, FD accelerates the developing country’s economic growth too (Gregorio & Guidotti, 1995; Shan & Morris, 2002). Estrada et al. (2010) confirmed a significant positive and similar impact of FD in the economic growth of the developing countries of Asia.

However, the optimum benefit of FD depends on the strong financial system which ensures efficient allocation of the financial resources. Were et al. (2012) show if the prospective investors and entrepreneurs are given credit as their need, they can establish businesses that afterward significantly contribute to the economic growth of a country. Thus, an efficient allocation of domestic credit to the private sector is essential for accelerating the economic growth.

Choong and Lim (2009) evidenced FDI and FD exert a positive impact on the economic growth of Malaysia. Saini et al. (2010) confirmed the benefit of FDI is attainable only when the financial market development exceeds a standard level. Until then, the benefit cannot be optimum.

On the contrary, literature also evidenced the weak and negative impact of FD on economic growth. For example, Arıc (2014) finds a strong negative influence of FD on the economic growth of many European Union countries. And earlier, Iheanacho (2016) confirmed a short-run negative impact of FD on the economic growth of Nigeria, a developing country of Africa.

Khan (2008) finds an insignificant long-run and significant short-run impact of the real deposit rate on the economic growth of Pakistan. He argued that in the long and short run, the interest rate has a low impact on the supply of funds indicating the importance of the availability of funds than the cost in Pakistan.

Moreover, Adu et al. (2013) evidenced a more rational finding from the above studies of FD. They evidenced that FD has both positive and negative impacts on the economic growth of a country depending on the proxies used as FD indicators in the respective country.

By labor productivity, we usually mean output (measured in terms of GDP per capita) produced by a unit of labor. Developing countries usually follow the labor-intensive production system due to the cheap labor cost. Labor productivity mainly depends on the quality of the labor forces which is measured in terms of their skills and efficiency and also depends on the uses of capital and technology. As skilled labor can contribute more to economic growth than unskilled labor, therefore, if any increase in the labor forces, keeping other things being constant consequences proportionately more increases in the GDP, the labor forces are considered skilled and their allocation is also efficient. On the contrary, if any increase in the labor forces fails to increase the GDP proportionately, the newly injected laborers are unskilled and their allocation may not be efficient too.

Generally, this is unusual to think that FDI, FD, capital formation, and labor forces have no significant impact on the economic growth of a country. Specifically, as capital is the main driver of an economy and a portion of which is generated from the FDI and FD, their contribution to economic growth is undeniable.

But from the literature discussion, the findings of FDI, FD, and economic growth nexus are not uniform. Literature offers the positive, negative, and insignificant impact of FDI and FD on the economic growth of many countries specifically in the developing countries of the world. Therefore, we intended to investigate the impact of FDI, FD, capital formation, and labor forces on the economic growth of Bangladesh, a developing country of Asia.

Given the above discussion, the contribution of this article is as follows: (a) Although many factors contribute to the growth process of a country, the impact of FDI, FD, capital, and labor forces at a time is rarely explored in Bangladesh. Hence, our article will fill up this research gap; (b) the article has used recent up-to-date data which are more relevant as the economy of Bangladesh is growing fast nowadays. Therefore, investigating the effect of these factors in the growth process using up-to-date data is vital for the Bangladesh economy; (c) besides, this article is finished just before the CORONA pandemic, hence this findings will be a benchmark findings for further research afterward, and (d) finally, we applied the VECM model after a huge examination of the data properties by applying a number of econometric models, and therefore, the findings of the study are highly reliable for higher level policy making.

Data

We obtained the yearly data of GDP, FDI, FD, Capital, and Labor forces of Bangladesh from 1990 to 2018 from the World Development Indicator of World Bank. Here, GDP is the gross domestic product in the U.S. dollar (constant US$ 2010), which is also an indicator of economic growth. FDI represents the net inflows of FDI in the balance of payment account in the U.S. dollar. FD represents the financial development of the country, which is the allocation of domestic credit to the private sector (% of GDP). Capital is the total amount of investment in Bangladesh’s economy in the U.S. dollar (constant 2010 US$), and labor is the total number of working people engaged in the economic activity in those years.

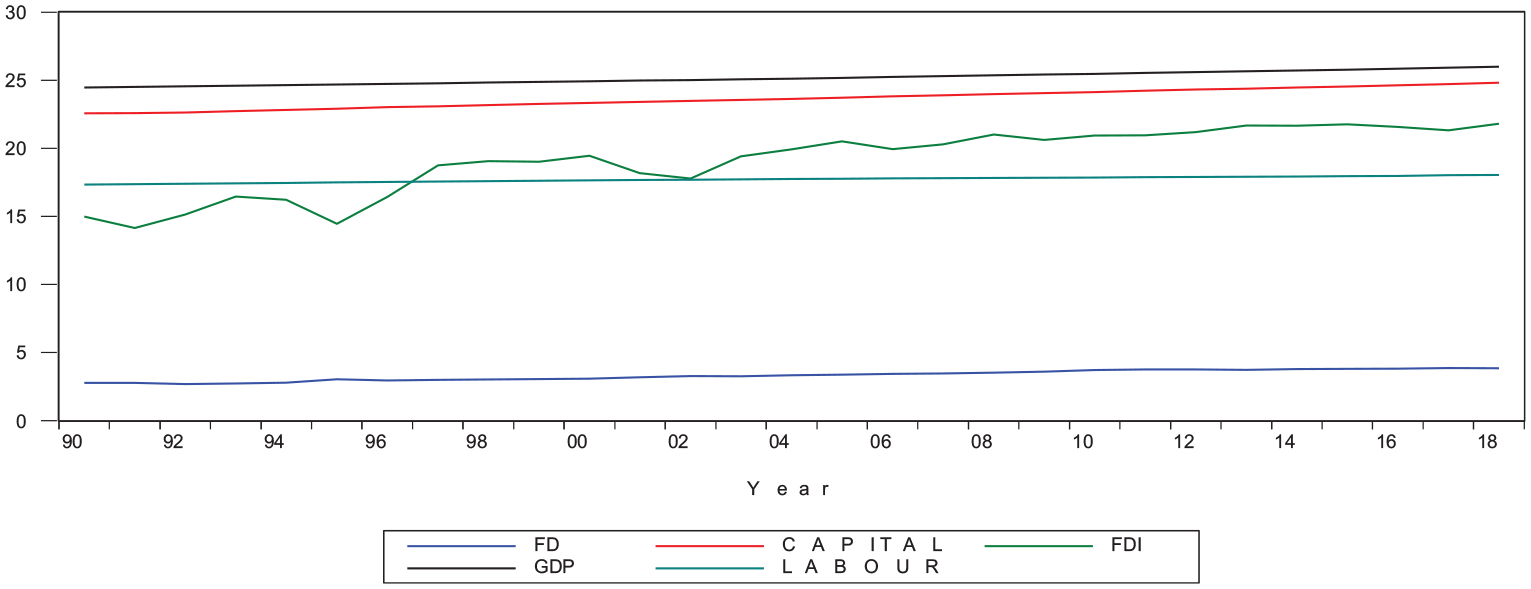

Applying econometric modeling requires the same order of integration in the data set (Shahbaz & Rahman, 2010). Therefore, we transform the data into the log–linear specification to have consistent estimates. Figure 1 shows, except labor, all the variables have a steady upward trend after logarithmic transformation confirming a nonstationary data set at level. However, though little fluctuations are persisting in the labor, the data have an upward trend too resulting in a nonstationary series.

Logarithmic transformation of the data set.

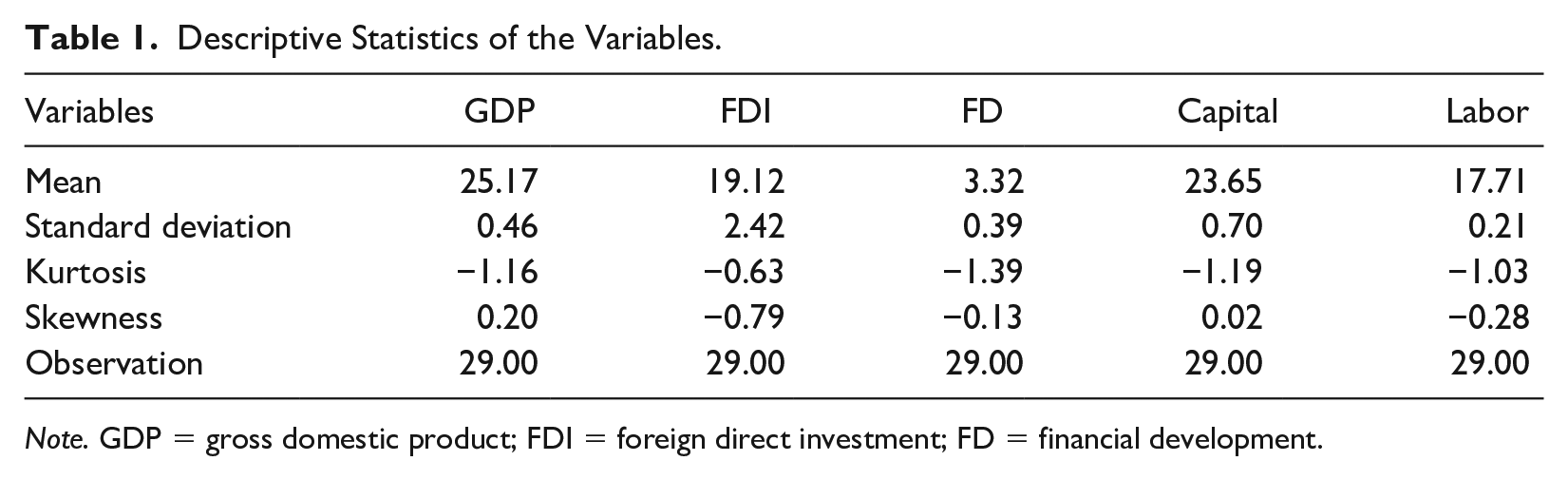

The descriptive statistics display in Table 1 show the standard deviation of FDI is 2.42 which is higher compared with the other variables in the data set. This indicates, only FDI inflow has a higher variation during the sample period. Besides, except FDI, the skewness of the rest series are near to 0 and their kurtoses are ≤1 confirms the persistence of a relatively smooth trend in the GDP, FD, Capital, and Labor.

Descriptive Statistics of the Variables.

Note. GDP = gross domestic product; FDI = foreign direct investment; FD = financial development.

Methodology Development

Production Function

We begin by considering capital and labor are the main drivers of the economic growth of a country. We mainly follow the neoclassical production function which is as follows:

where K stands for capital and L stands for the labor force. The two main sources of capital are FDI and FD. The country mainly accepts FDI for holding the development project as well as establishing new private ventures. FD fosters economic growth by providing domestic credit to the private sector. As FDI and FD are the components of capital, and capital itself impacts the economic growth of a country distinctively, the eventual augmented neoclassical production function for developing the framework of our study is as follows:

Considering Equation 2, the study aims to investigate the following null hypotheses as a predictor of the economic growth of Bangladesh:

Model Selection

To examine the short- and long-run relationship of time series variables, researchers applied a variety of econometric models in the literature. Among them, the most used method is the ordinary least square (OLS) method. However, in recent times, Vector Autoregressive Model (VAR) and Autoregressive Distributive Lag Models (ARDL) have also been applied by several researchers (see Iheanacho, 2016).

VAR models are mainly two types: (a) unrestricted VAR model and (b) the Vector Error Correction Model (VECM). Employing an unrestricted VAR model requires the data to be stationary at level I(0), or at first difference I(1), and employing VECM requires the data to be non stationary at level but stationary at the first or second difference. On the other hand, applying the ARDL model requires the data can be stationary at level, that is, I(0) or first difference, that is, I(1), but it should not be stationary at the second difference, that is, I(2) at all. Therefore, we applied the augmented Dickey–Fuller (ADF) test and the Phillips–Perron (PP) test for checking the stationary attributes of the data set.

Lag Selection

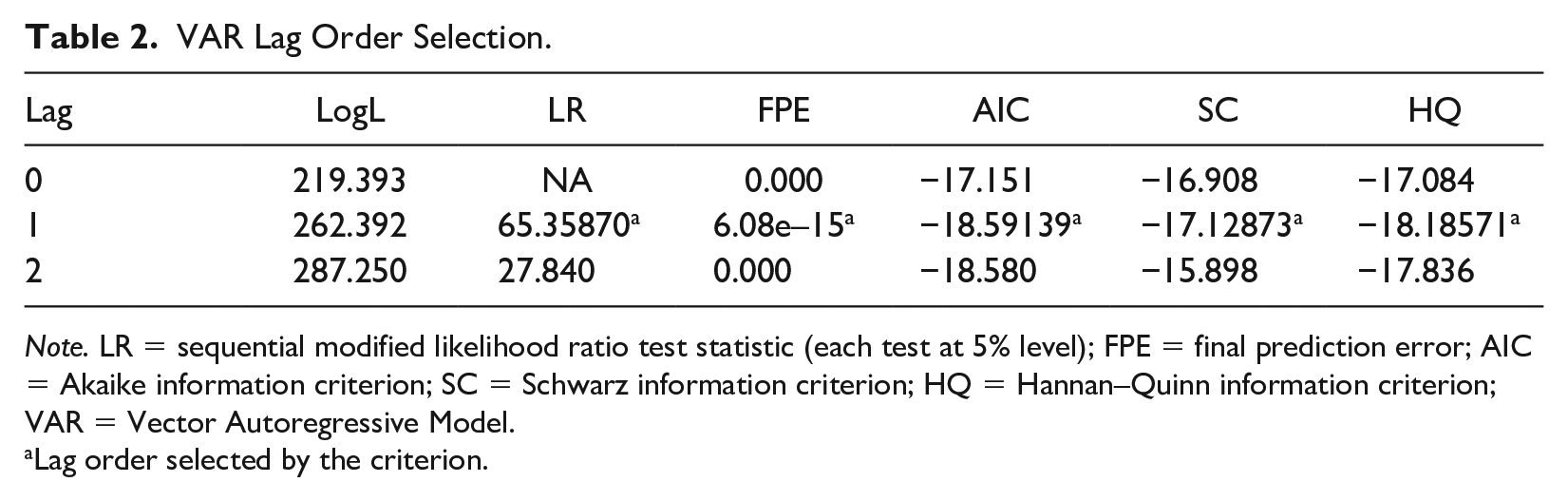

We applied the VAR model to determine the optimum order of lag for applying the ADF and PP tests. Table 2 shows that the major lag selection criteria confirm lag one series for further analysis.

VAR Lag Order Selection.

Note. LR = sequential modified likelihood ratio test statistic (each test at 5% level); FPE = final prediction error; AIC = Akaike information criterion; SC = Schwarz information criterion; HQ = Hannan–Quinn information criterion; VAR = Vector Autoregressive Model.

Lag order selected by the criterion.

ADF Test and Phillips–Perron Test

As after the logarithmic transformation of the variables, an upward trend is evident in Figure 1, and so, we applied the following ADF test (with trend) equation and Phillips–Perron test with drift equation for checking the stationary properties of the series. The equations of the ADF and PP tests are as follows:

If the absolute ADF and PP test statistics are more than their absolute test critical values, we confirm the series is stationary, or otherwise, the series has a unit root. Besides, if

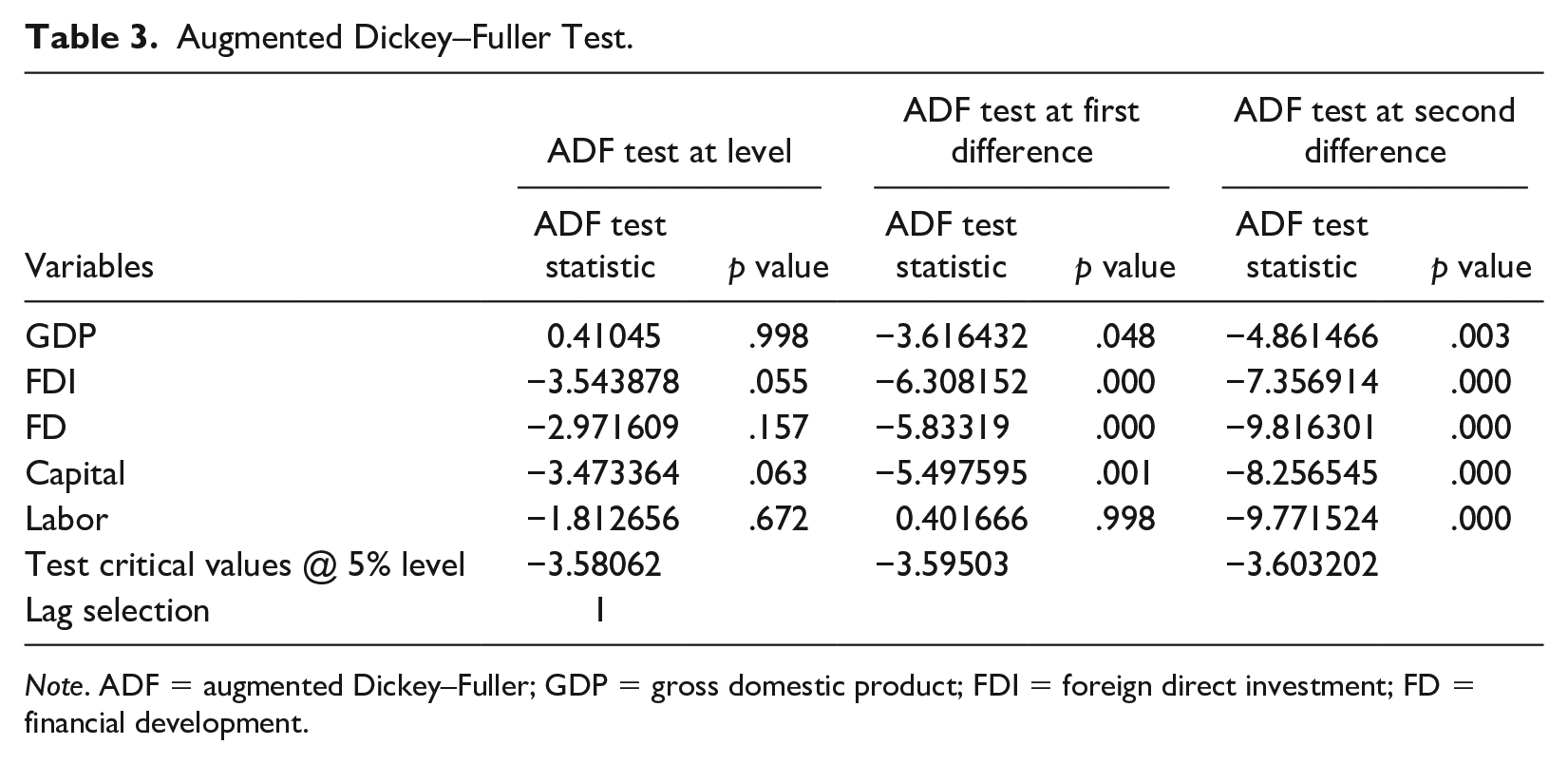

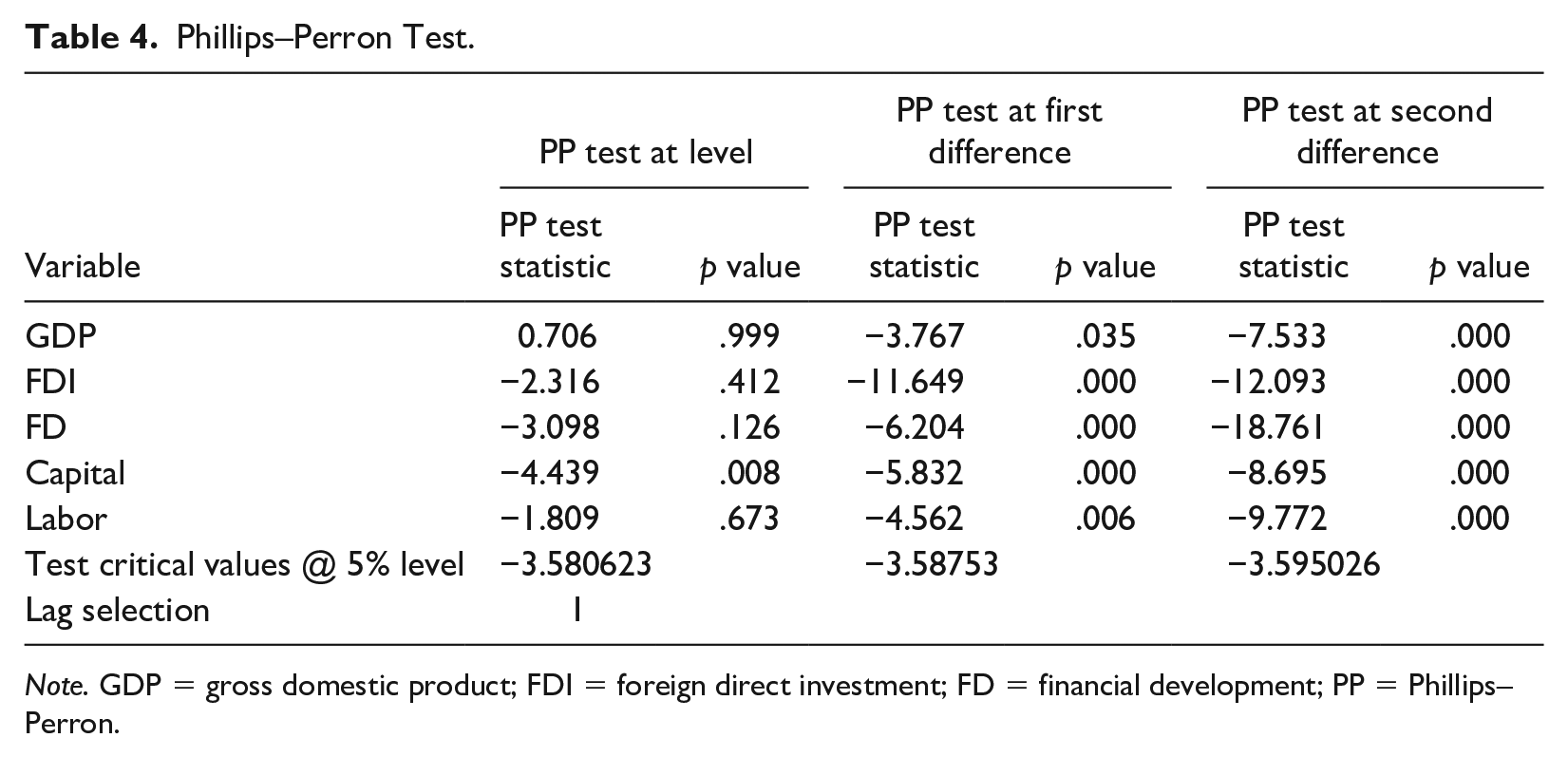

In Tables 3 and 4, the ADF test at level and first difference data and the PP test at level data of the lag one series find GDP, FDI, FD, and Capital are stationary and Labor remains nonstationary which prohibits us from applying the unrestricted VAR model and partially satisfying the first requirement of the VECM to apply. Therefore, we further applied the ADF and PP test at the second differenced data of the same lag series. The findings suggest that all the variables turn to stationary at a 1% level of significance which restricts us from applying the ARDL model and allows us to employ the VECM for this study. Prior to applying VECM, we also employed the Granger causality test on the second differenced data to cross-examine whether the variables do Granger to cause each other or not.

Augmented Dickey–Fuller Test.

Note. ADF = augmented Dickey–Fuller; GDP = gross domestic product; FDI = foreign direct investment; FD = financial development.

Phillips–Perron Test.

Note. GDP = gross domestic product; FDI = foreign direct investment; FD = financial development; PP = Phillips–Perron.

Johansen Test of Co-integration

VECM requires having at least one co-integrating equation among the variables, otherwise, unrestricted VAR models should apply (Asari et al., 2011).bib6 Moreover, if all the variables of a multiple time series data have a unit root at level, there are at most

H0: The level data have a linear trend, but the co-integration equation has no trend but intercept only.

H1: The level data have no linear trend, but the co-integration equation has a trend but intercept only.

Johansen and Juselius introduced two tests of co-integration, which are the trace test and the maximum eigenvalue test.

Trace Test

Let, Π is the co-integrating vector and r be the rank of Π, which is the number of co-integrating vectors in the equation. Then, the null and alternative hypotheses of testing co-integration equations are as follows:

If

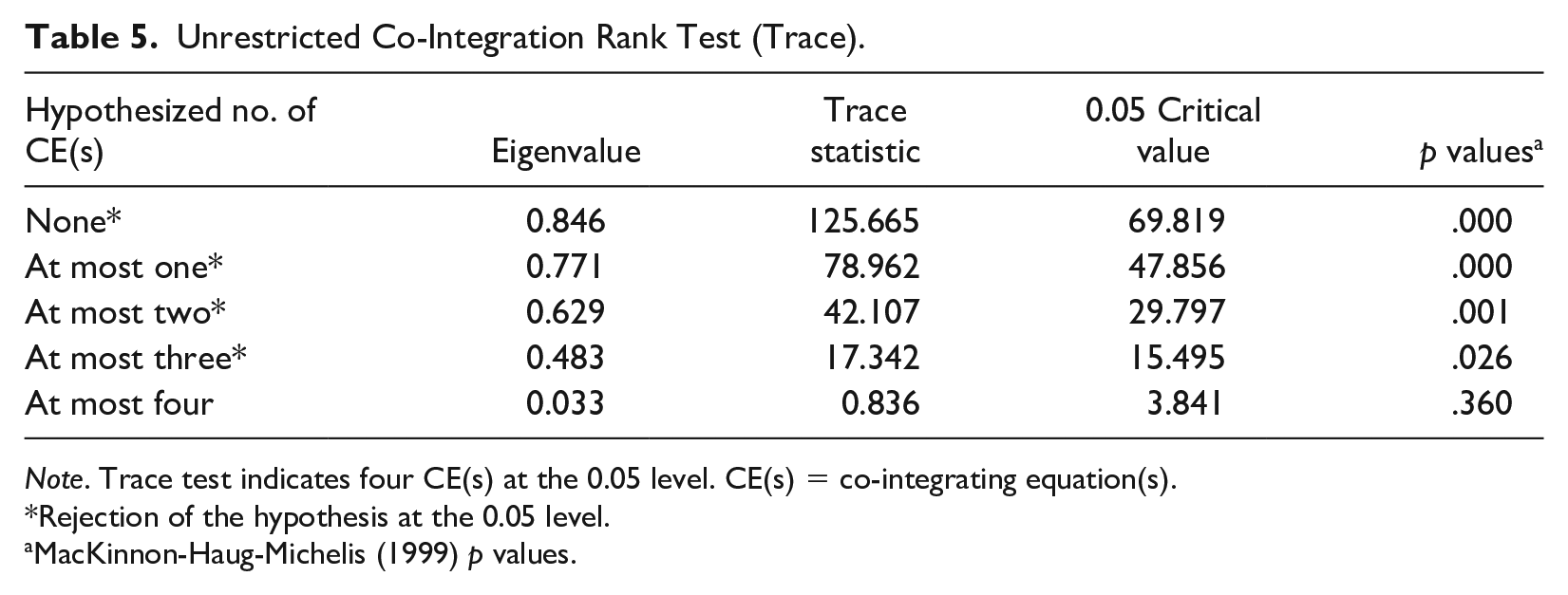

This procedure will continue till the subsequent null hypothesis can be rejected at (p < .5). The trace test display in Table 5 clearly shows that there are at least four co-integrating equations among the variables.

Unrestricted Co-Integration Rank Test (Trace).

Note. Trace test indicates four CE(s) at the 0.05 level. CE(s) = co-integrating equation(s).

Rejection of the hypothesis at the 0.05 level.

MacKinnon-Haug-Michelis (1999) p values.

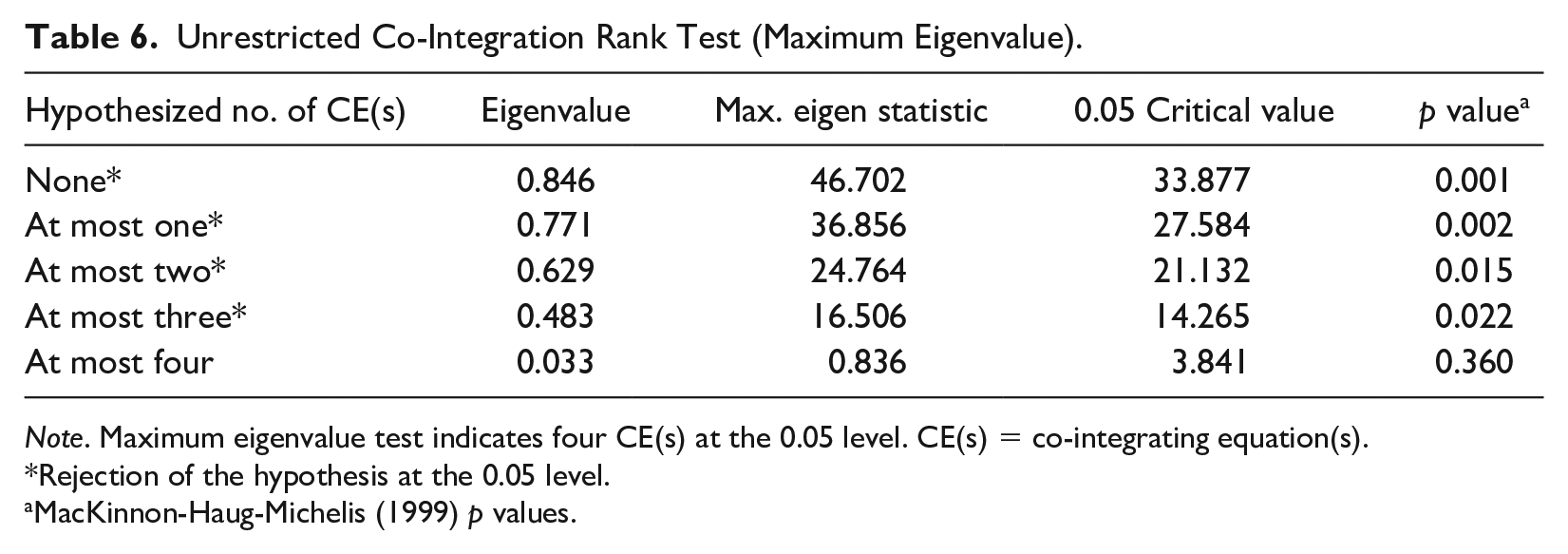

Maximum Eigenvalue Test

In the maximum eigenvalue test, if the Max-Eigen statistic is more than the critical value and

The maximum eigenvalue test in Table 6 clearly shows that the last highest Eigen-statistics is 16.506 with

Unrestricted Co-Integration Rank Test (Maximum Eigenvalue).

Note. Maximum eigenvalue test indicates four CE(s) at the 0.05 level. CE(s) = co-integrating equation(s).

Rejection of the hypothesis at the 0.05 level.

MacKinnon-Haug-Michelis (1999) p values.

The Model

Granger Causality Test

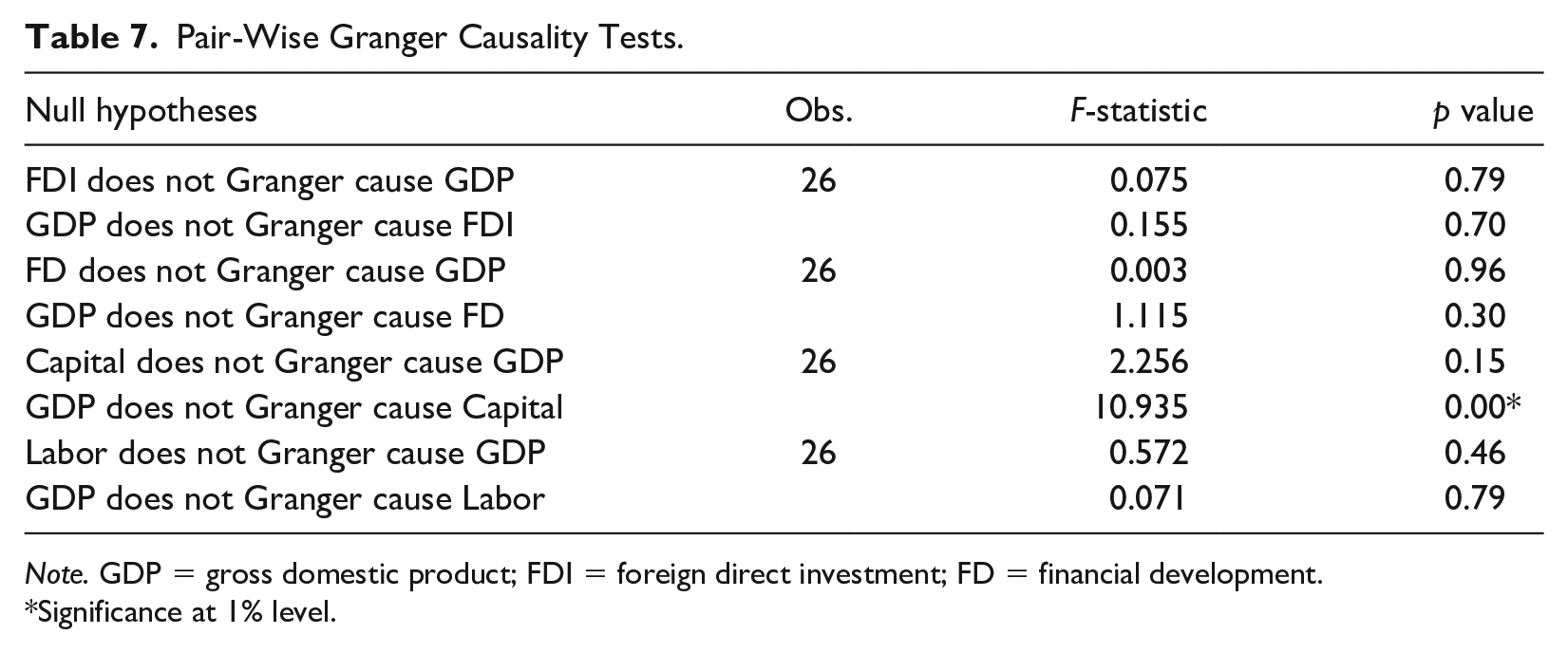

We applied the Granger causality test first introduced by Granger (1969) to examine the potential predictive power of the explanatory variables on GDP. According to the Granger causality test, if a time series lag value has any significant impact (measured by F-test) on the future value of other time-series data, the earlier series Granger to cause the later series. We check the reciprocal causality of GDP with the other variables.

The results of this test are summarized in Table 7. The findings of the Granger Causality test confirm only GDP Granger to cause the capital at a 1% significant level. Precisely, the 1-year lag value of the GDP has a causal relationship with the capital formation in Bangladesh. The underlying reason is the increasing GDP growth rate in recent times attracts foreign investors who are investing more in Bangladesh than before. Specifically, China, Japan, and South-Korea are expanding their business operations in the various economic zones which led Bangladesh’s economy to expand widely now a day. On the contrary, Capital formation has no causal relationship with the GDP in the long run. The reasons are inefficient allocation, misuse of capital due to lack of efficiency, scam in project operation, and the presence of a huge number of unskilled laborers in the economy. No other variables Granger to cause the GDP and vice versa.

Pair-Wise Granger Causality Tests.

Note. GDP = gross domestic product; FDI = foreign direct investment; FD = financial development.

Significance at 1% level.

VECM

Having found at least four co-integrating equations among the variables, we apply VECM for measuring the extent of short- and long-run relationships of the FDI, FD, Labor, and Capital with GDP. The conventional VECM directs that the last period deviation (error) from the long-run equilibrium of a VAR model influences the short-run dynamics of the dependent variable in addition to the influences of the lagged values of dependent and explanatory variables on dependent variable. The equations of the VECM are as follows:

In Equation 9, the error correction term

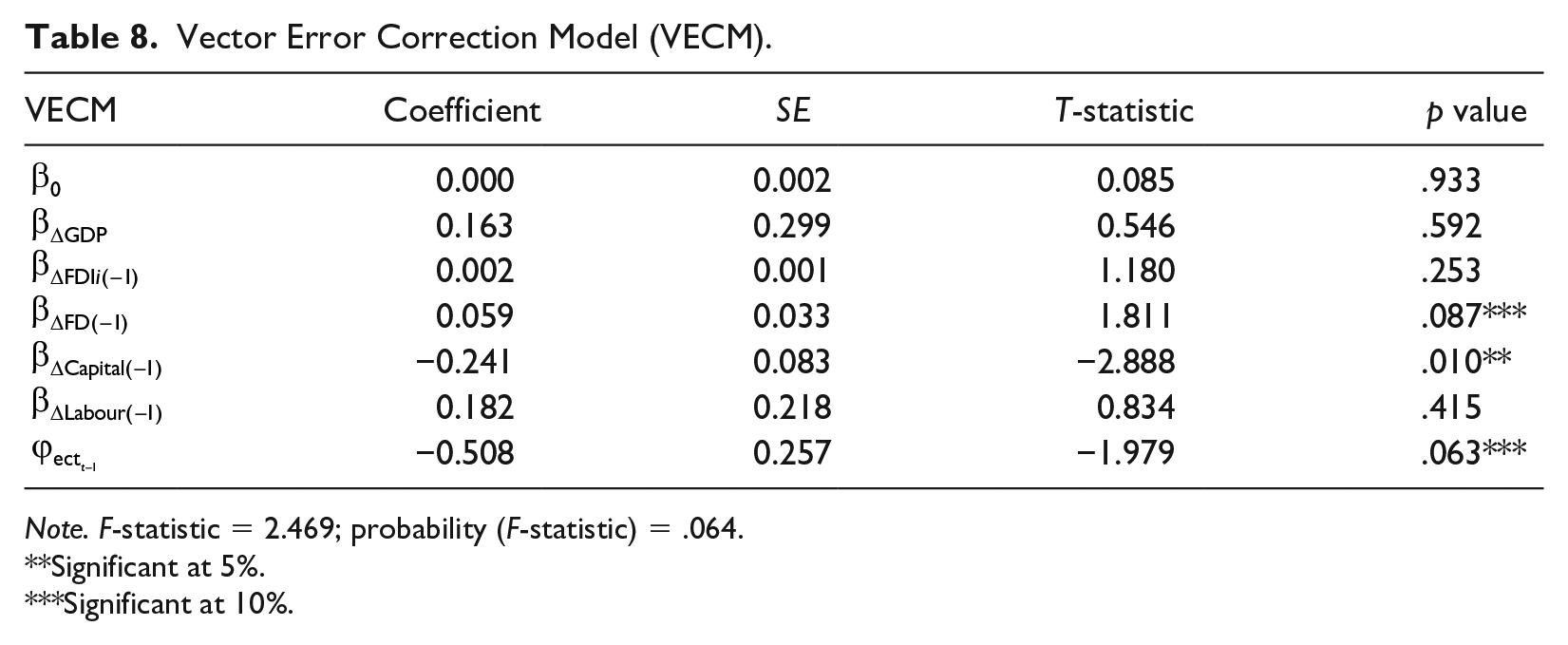

Vector Error Correction Model (VECM).

Note. F-statistic = 2.469; probability (F-statistic) = .064.

Significant at 5%.

Significant at 10%.

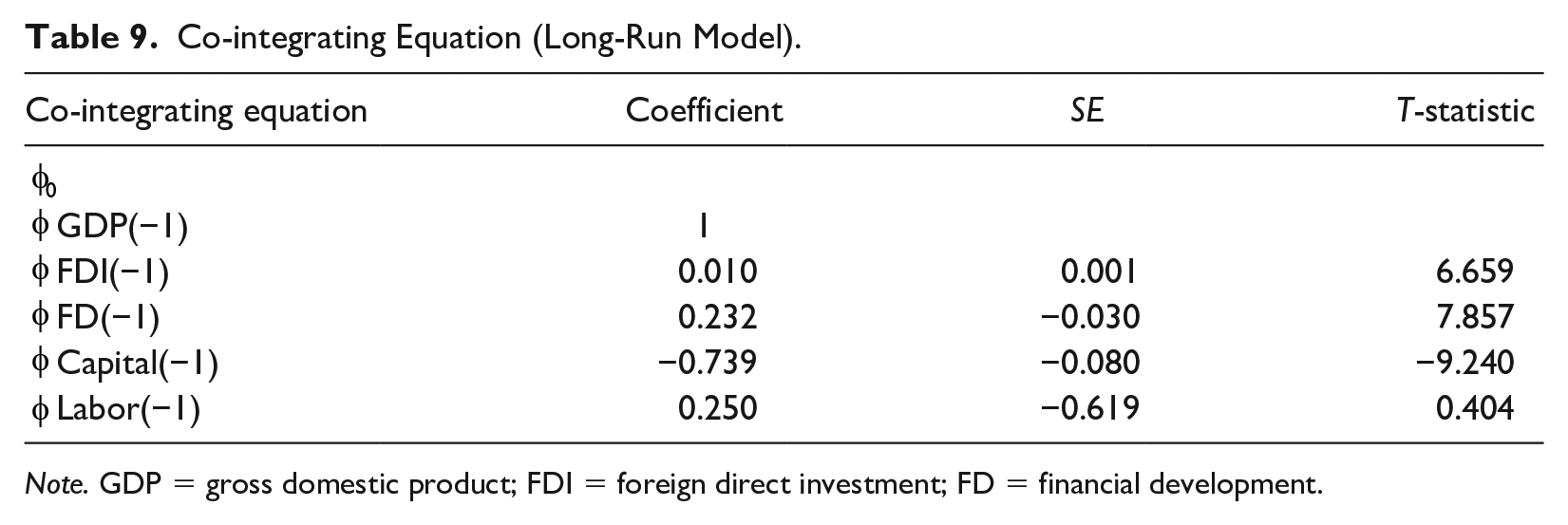

Co-integrating Equation (Long-Run Model).

Note. GDP = gross domestic product; FDI = foreign direct investment; FD = financial development.

Putting the values of error correction coefficients from Table 8 in Equation 9, the VECM stands as follows:

Putting the values of co-integrating coefficients from Table 9 in Equation 10, the error correction term of the VECM stands as follows:

In Table 9 and Equation 12,

Result and Discussion

In Table 8, the VECM intercept

In Table 9, the long-run co-integrating coefficients

The likely explanations of the negative influences are but not limited to the following; first, a significant percentage of government investment is injected in the long-run projects which requires much time to accelerate the GDP. Therefore, in the short run, far less than the optimum output of capital formation is observed. However, in the long run, the impact is positive and reasonable indicating capitals are moderately stepping up the pace of economic growth. Second, a huge amount of private investment is continuously injecting in the many new ventures which are also taking much time to surface their positive influences on GDP. And finally, most of the capital is invested in the labor-intensive sectors where labor forces are mainly unskilled and underutilized. Therefore, any injection of capital in those sectors outcomes less than the optimum output until the labors become fully utilized and skilled.

In Table 8, the short-run coefficient of the lagged values of FD is positive (.059) and significant at a 10% level implies; domestic credit disbursement has a slightly positive impact on the economic growth of Bangladesh. But in the long run, it is negatively co-integrated with the GDP authenticates the present exposed position in the banking sector. This finding is similar to the findings of Yucel (2009) who finds a negative influence of FD on economic growth.

The likely reasons for the long-run negative influence of FD on GDP are as follows: (a) First, an excessive amount of default loan is disbursed in recent years in the banking sector which lessens sharply the benefits of credit disbursement. Moreover, Nag (2019) reported that default loan, excluding bad-debt written off increased to Tk 93,278 crore in 2018 warrants the vulnerable situation in the banking sector; (b) second, lack of good governance consequences various irregularities and inefficiency in loan performance. According to the WEF (2019), Bangladesh performed the lowest in the bank soundness in Asia. (c) Finally, sector-wise discrimination in loan disbursement is higher in the banking sector. All these causes short-run lower impact and long-run negative impact of FD to the economic growth of Bangladesh.

The short-run coefficient of the lagged values of GDP is positive but not statistically significant, indicating the absence of short-run causality between the lagged values of GDP with GDP. This finding is similar to the findings of

The short-run coefficient of the lagged values of FDI is also positive but small (.002) and insignificant. Moreover, the long-run co-integration of FDI with GDP is also small (.5 of .010) but negative implying almost a null impact of FDI on GDP both in the short and long run. The probable reason is, in Bangladesh, although a fewer portion of FDI is invested in the manufacturing sector, a major portion of FDI is mainly injected in the infrastructural development and therefore estimating FDI’s actual impact on the economic production is not justified. Moreover, Rahman (2015) found, FDI negatively impacted the economic growth of Bangladesh both in the short and long run. Comparing him, the contribution of FDI may be increased in GDP in recent years.

The short-run coefficient of the labor forces

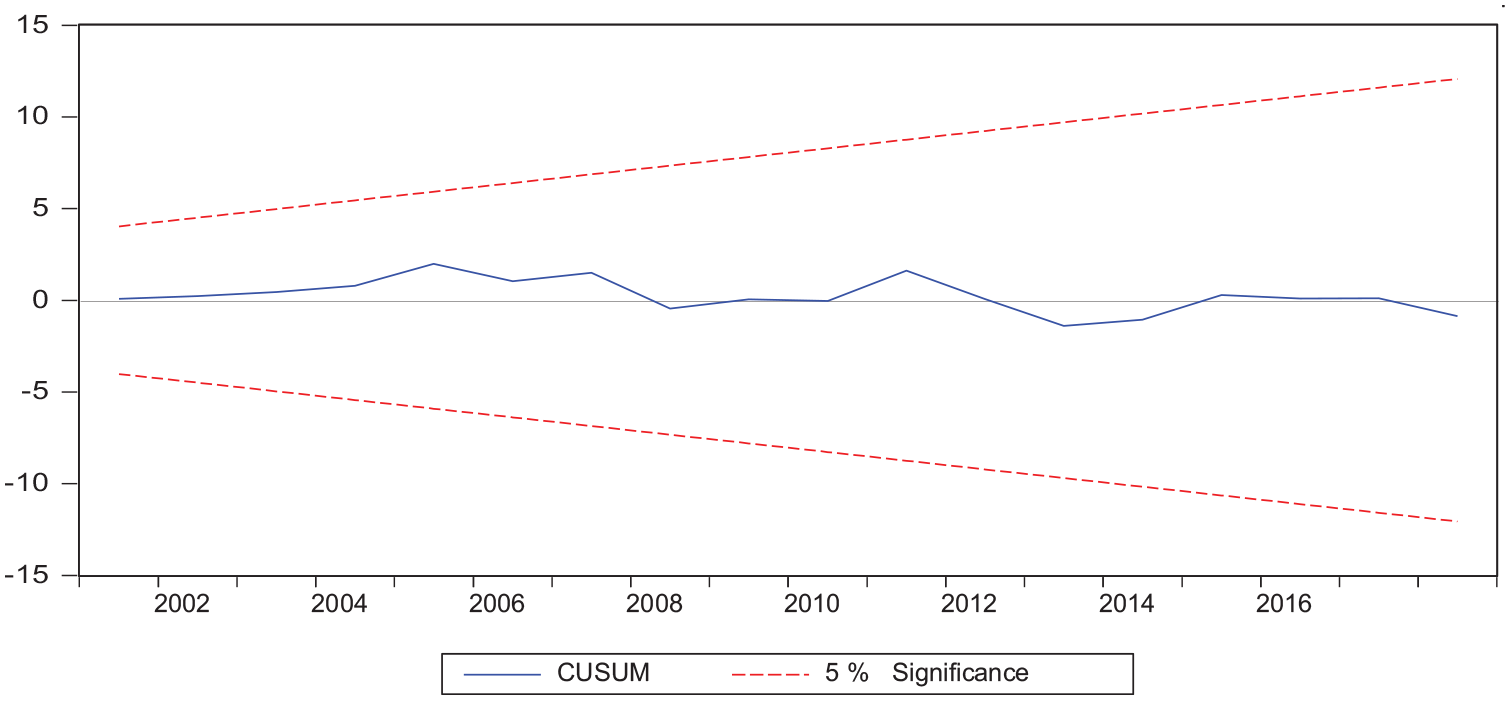

Stability Diagnostic of the VECM

We checked the fitness and stability of the VECM using Breusch–Godfrey Serial Correlation Lagrange multiplier (LM) test and cumulative sum (CUSUM) test. The

Breusch–Godfrey Serial Correlation LM Test.

LM = Lagrange multiplier.

Stability test.

Conclusion

The impact of FDI, FD, capital formation, and the labor force are found diverse from country to country due to country-specific factors, market maturity, and the use of different estimation methods. Specifically, the literature review of more than 50 articles from 1994 to 2012 by Almfraji & Almsafir (2013) evidenced a huge contradictory relationship of the FDI with economic growth. Those pieces of literature confirm that the impact of FDI is found positive, negative, and null in the GDP of many developed and developing countries.

In our study, we find capital formation has a long-run positive impact on the GDP which signals the capital market of Bangladesh is becoming more efficient day by day. Currently, investors are investing more in the capital market, which in turn accelerates the GDP growth rate in the long run. On the contrary, the long-run negative influence of the labor forces indicates a huge number of unskilled laborers are engaged in the production process. This also indicates the presence of disguised unemployment in Bangladesh. Similarly, the influence of FD is also negative exposing the current weak scenario of the banking sector. Due to inefficient allocation and misuses of FDI, it has a null impact on the economic growth of Bangladesh. Thus, Bangladesh fails to achieve the desired benefits from FDI both in the short and long run. Similarly, FD also has a null impact on GDP indicating the private sector misuses the domestic credit and the banking sector is inefficient in credit management.

Based on these findings, the policy recommendations are that Bangladesh should allocate FDI and domestic credit to the productive private sectors efficiently to ensure long-run economic growth. Corrective measures should be taken to ensure providing credits to genuine investors and borrowers in the banking sector. Emphasis should be also given to establish a more capital-intensive industry along with a significant number of labor-intensive industries so that long-run economic growth can be achieved easily. Besides, more industry-wise training institutes and technical schools and colleges require establishing and an effective body of the government should regularly monitor to ensure the availability of the skilled and trained labor forces in the economy.

Footnotes

Acknowledgments

The authors acknowledge Athya Sanjida and the anonymous reviewers for their valuable suggestions to improve the quality of the paper.

Availability of Data and Materials

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.