Abstract

This study examined potential predictors of financial well-being in older adults. Data were drawn from the Health and Retirement Study, focusing on psychosocial, demographic, and lifestyle variables. Random Forest analysis was performed to assess the relative importance of 47 potential predictors, offering a data-driven evaluation of which factors are most strongly associated with subjective financial well-being. Results showed that psychological variables (particularly chronic stress, life satisfaction, perceived control, and optimism) were stronger predictors than demographic indicators. Among demographic variables, education was the most important. The results suggest that financial well-being reflects individuals’ ability to maintain a sense of satisfaction, optimism, and agency in the face of life challenges, rather than being determined solely by economic or demographic conditions.

• Provides a data-driven ranking of 47 potential predictors of financial well-being in older adults using machine learning. • Demonstrates that psychological variables (e.g., chronic stress, control beliefs, optimism) are more predictive of financial well-being than demographic characteristics. • Suggests that financial well-being reflects a dynamic balance between environmental demands and psychological resources.

• Supports the development of interventions that enhance psychological resilience (e.g., stress management, control beliefs) to improve financial well-being in later life. • Suggests that financial well-being policies should consider psychosocial resources in addition to financial literacy. • Financial service providers and aging professionals could incorporate psychological assessment to identify individuals at risk.What this paper adds

Applications of study findings

Introduction

A substantial proportion of older adults worldwide experience financial strain (Federal Reserve Board, 2013; Huang et al., 2020), which has been associated with various adverse outcomes, including an increased risk of depression (Ettman et al., 2023). Therefore, ensuring the financial well-being of older adults warrants careful attention. Financial well-being is defined as “a state wherein a person can fully meet current and ongoing financial obligations, can feel secure in their financial future, and is able to make choices that allow them to enjoy life” (p. 1, Consumer Financial Protection Bureau, 2015). Financial well-being consists of four distinct dimensions: (1) control over daily finances, including paying bills on time and managing debt; (2) capacity to absorb financial shocks, such as having savings, insurance, and emergency support; (3) progress toward financial goals, like debt repayment or retirement savings; and (4) financial freedom to make life choices, enabling experiences without financial stress (Consumer Financial Protection Bureau, 2017). Low financial well-being is linked to negative psychological and health outcomes, while high financial well-being is associated with positive outcomes in older adults (Khan et al., 2017; Tucker-Seeley et al., 2009).

A growing body of empirical research has examined the predictors of financial well-being. For example, Garðarsdóttir and Dittmar (2012) found that materialistic values negatively predict financial well-being. Personality traits have also been implicated, with emotional stability and conscientiousness emerging as positive predictors (Joshanloo, 2022). Additionally, self-efficacy (individuals’ belief in their ability to manage life demands) has been identified as a significant predictor (Tang, 2021). Research has also highlighted financial perceptions and knowledge, financial stress, and both short- and long-term positive financial behaviors as important predictors (Fan & Henager, 2021). Demographic characteristics have received particular attention. For instance, Geng (2021) reported that women tend to experience lower financial well-being than men, while being married is associated with greater financial well-being regardless of gender. Educational attainment has also been consistently linked to higher levels of financial well-being (Assari et al., 2024). While these findings have advanced understanding of financial well-being, the literature remains fragmented. Due to the absence of comprehensive meta-analyses, insights are scattered across individual studies, each of which typically investigates a limited set of predictors.

Several integrative models have been proposed to synthesize findings in the financial well-being literature. A prominent example is the framework developed by Brüggen et al. (2017), which categorizes potential predictors of financial well-being into contextual (e.g., national economic growth) and personal domains. Personal factors include demographic characteristics (e.g., age, gender, education), individual skills, attitudes, and motivations (e.g., financial knowledge), personality traits (e.g., self-efficacy, values, trust), financial behaviors (e.g., spending habits), and life events. Similarly, Nanda and Banerjee (2021) reviewed research on subjective financial well-being and highlighted the importance of both macro-level contextual factors and individual-level factors such as materialism, spending patterns, self-control, saving orientation, and income insecurity. Based on the existing literature, personal predictors of financial well-being can be broadly organized into the following key categories. (1) Psychological Factors ○ Personality traits (e.g., conscientiousness, emotional stability, self-efficacy). ○ Value orientations and attitudes (e.g., materialism, trust, financial attitudes). (2) Demographic characteristics (e.g., age, gender, education, ethnicity) (3) Social and relational factors (e.g., perceived discrimination, loneliness, isolation, family support) (4) Financial Factors ○ Financial behaviors (e.g., spending patterns, saving habits, investment behaviors) ○ Financial skills and knowledge (e.g., financial literacy, saving orientation, and capability to manage financial resources effectively). ○ Financial circumstances and life events (e.g., income security, employment status, unexpected expenses, career changes).

This categorization is not exhaustive but captures the key themes emphasized in prior empirical and conceptual work. While these categories emerge from prior research, important gaps remain. In particular, their relative importance is not well understood. Because the evidence comes from diverse studies with varying methodologies and samples, it remains unclear how predictors and categories rank in predicting financial well-being.

Present Study

The present study addresses this key gap in the financial well-being literature by applying machine learning techniques to evaluate the relative importance of a broad set of predictors in a large sample of older adults. The study excludes potential financial predictors, which are often highly correlated with financial well-being, and instead examines 47 variables chosen for their theoretical and empirical relevance to aging populations, including demographic characteristics, social and relational attributes, and psychological factors. Rather than testing predefined hypotheses, the study adopts an exploratory, data-driven framework. By using a machine learning approach, this study enables the simultaneous examination of these potential predictors, providing a more integrated understanding of the factors that contribute most strongly to financial well-being in later life.

It is important to clarify that predictive modeling and causal inference represent distinct analytic goals (Arif & MacNeil, 2022). Predictive models, such as the machine learning approach applied here, are designed to identify patterns that maximize the accuracy of predicting an outcome given a set of inputs. The estimated importance of predictors in such models reflects their contribution to prediction accuracy, not their causal influence. The goal is to examine whether the outcome can be predicted from the observed values of the predictors, regardless of whether those predictors are causes, consequences, or merely correlates of the outcome. By contrast, causal inference requires explicit modeling of temporal ordering, confounding, and counterfactual assumptions in order to estimate the effect of one variable on another (Leist et al., 2022). The present cross-sectional predictive design does not meet these requirements, and therefore this is not a causal modeling study. The value of a predictive approach lies in identifying a set of variables that are most informative for prediction, which can subsequently guide future longitudinal and causal analyses.

Methods

Participants

The data analyzed in this study were drawn from the 2022 wave of the Health and Retirement Study (HRS) Core Project, specifically the Psychosocial and Lifestyle section. The data (version V3.0) were accessed in February 2025 at https://hrsdata.isr.umich.edu. The HRS is a nationally representative longitudinal panel study that focuses on U.S. adults primarily aged 50 and above. Following data cleaning and the handling of missing values (as described below), the final sample consisted of 4,317 participants (mean age = 69.2, median = 69, SD = 10.39), of whom 59.8% were women.

Variables

The outcome variable, financial well-being, was measured using the 10-item Consumer Financial Protection Bureau Financial Well-Being Scale (CFPB, 2017). The first six items were rated on a 1 (Completely) to 5 (Not at all) scale, and the next four on a 1 (Always) to 5 (Never) scale. The scale demonstrated strong internal consistency (Cronbach’s alpha = .895). The Psychosocial and Lifestyle section of the HRS encompasses a wide array of variables. For this study, all relevant variables were incorporated, with the exception of overlapping variables such as the single-item life evaluation measure, which was deemed redundant in light of the 5-item life satisfaction scale. Four financial variables pertaining to household income, perceived financial situation, control over financial situation, and financial strain were excluded from the analysis due to high intercorrelations and strong conceptual overlap with the financial well-being outcome. In contrast, the item related to ongoing financial strain from the Ongoing Chronic Stressors scale (ongstress) was retained, as its removal would not substantially affect the overall scale score. This decision was informed by a high correlation coefficient of 0.981 between the total scores with and without this item. Consequently, to preserve the integrity of the scale as a whole, the item was retained. Additionally, variables with limited applicability to participants or considerable missing data (e.g., work-related variables) were excluded from the analysis. Ultimately, 47 potential predictor variables were included. All study variables are defined in Table S1 in the supplementary material based on their contents, and further information about these variables can be accessed via official HRS documents at https://hrsdata.isr.umich.edu. Figure 1 provides a list of the variables along with brief definitions. Variables

Missing Data Imputation

A total of 4,335 individuals completed the financial well-being scale and were included in the study. However, 18 participants who were missing more than 30% of the predictor variables (i.e., more than 13 out of 47 variables) were excluded from the analysis. This resulted in a final sample of 4,317 participants, each with no more than 13 missing values across the 47 predictors. Missing values were imputed using a random forest-based imputation procedure implemented through the missRanger package in R (Mayer, 2024) with 1000 trees. This approach uses the predictive capabilities of the Random Forest algorithm to estimate missing entries by modeling them as functions of the non-missing data (Stekhoven & Bühlmann, 2012).

Feature Selection

To refine the predictor set, a feature selection method based on the simulated annealing algorithm was applied (Henderson et al., 2003). The algorithm initially explores many possible models and may accept worse-performing ones to avoid being trapped in poor solutions. Over time, it becomes more selective and concentrates on better-performing models. This process is modeled after annealing in metallurgy, where gradual cooling leads to a stable and optimized structure (Kuhn & Johnson, 2020). When integrated with repeated cross-validation, this approach provides a robust mechanism for identifying combinations of predictors that yield improved model performance without overfitting. This analysis was implemented via the caret package in R (Kuhn, 2008), with Random Forest serving as the underlying modeling algorithm. The procedure involved 100 iterations, employing 5-fold cross-validation repeated five times.

Random Forest Analysis

A Random Forest regression approach was applied in this study to model the outcome variable, using the package randomForestSRC in R (Ishwaran & Kogalur, 2023). This algorithm constructs a collection of decision trees, each trained on a distinct bootstrap sample of the data, and synthesizes their outputs through aggregation to generate final predictions (Hastie et al., 2009). Owing to their inherently nonparametric design, random forests are particularly advantageous for analyzing social science data, where variable types, distributions, and functional relationships often vary widely. They are capable of accommodating such complexity without relying on distributional assumptions, and have demonstrated strong performance in high-dimensional analytical contexts (Chen & Ishwaran, 2012).

Model evaluation was conducted using out-of-bag (OOB) estimation, a method intrinsic to the Random Forest algorithm. During training, approximately one-third of observations are excluded from each tree’s bootstrap sample, and these excluded cases serve as an independent unseen test set for estimating model error (Hastie et al., 2009). This built-in validation technique minimizes the need for additional cross-validation procedures and offers a practical means of evaluating model generalizability.

Hyperparameter tuning is a vital step in machine learning workflows, as model performance is often sensitive to the specific values chosen. In Random Forest models, important hyperparameters include the number of predictors considered at each split (mtry) and the minimum number of observations required in a terminal node (nodesize), both of which influence the model’s complexity, generalizability, and predictive accuracy (Biau & Scornet, 2016). To identify suitable values for these parameters, a grid search was conducted over a defined set of candidate values. The number of trees was fixed at 1,000, higher than the commonly used default of 500. The mtry parameter was varied from 3 to 14, while nodesize was tested across values ranging from 3 to 10, based on recommendations from the literature (Boehmke & Greenwell, 2020; Genuer & Poggi, 2020). This resulted in 96 unique hyperparameter combinations, each of which was evaluated using 5-fold cross-validation. The tuning process was implemented using the mlr3 package in R (Lang et al., 2019).

In response to the increasing emphasis on transparency and interpretability in the application of machine learning to social science (Molnar, 2020), two diagnostic tools were employed. First, variable importance was assessed using a permutation-based procedure, which evaluates the effect of randomizing each variable on the model’s predictive accuracy (Fife & D’Onofrio, 2022). This is achieved by iteratively permuting (or shuffling) the values of each predictor variable while holding the values of all other variables constant, and measuring the decrease in model performance. Second, partial dependence plots were generated to illustrate the average marginal relationship between selected predictors and the outcome, controlling for other variables in the model (Ryo, 2022).

Results

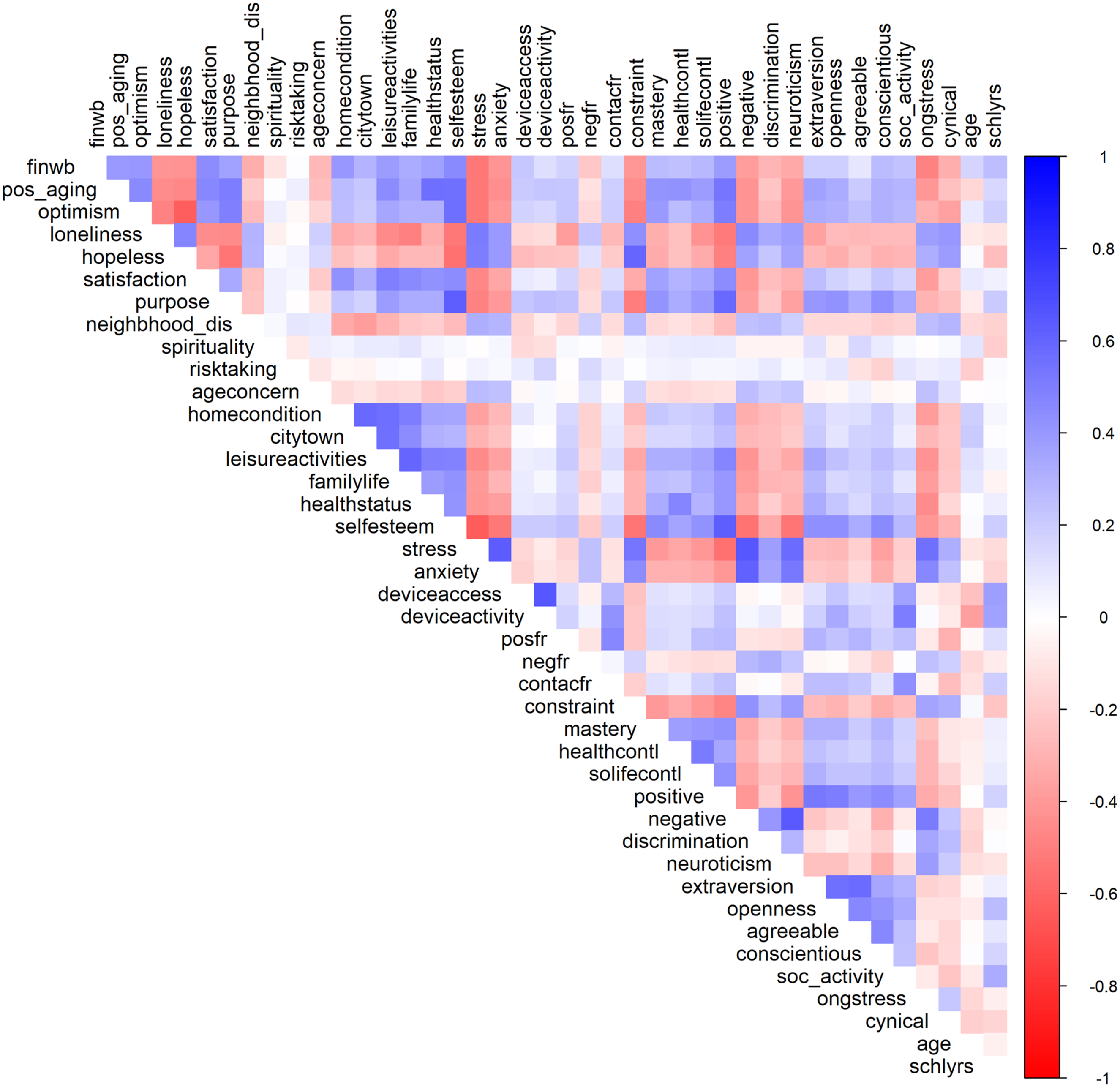

Figure 2 shows Spearman correlations between all non-binary variables of the study. The results of the feature selection analysis are presented in Table 1. Of the original 47 predictors, 24 were retained, while 23 were excluded. Conceptually, the selected variables tended to reflect stable cognitive appraisals of life conditions (e.g., life satisfaction, satisfaction with home condition), access to social and structural resources (e.g., having friends and family, relationship quality, years of schooling, U.S.-born status), and behavioral or personality characteristics related to control, engagement, and planning (e.g., optimism, purpose, conscientiousness, extraversion, constraints on personal control). In contrast, the eliminated variables were more likely to involve general affective well-being variables (e.g., stress, anxiety, positive affect, negative affect), basic demographic factors (e.g., age, gender, race), and broader personality traits less directly tied to financial behavior (e.g., openness, agreeableness, cynical hostility). Correlations Variable Selection Results

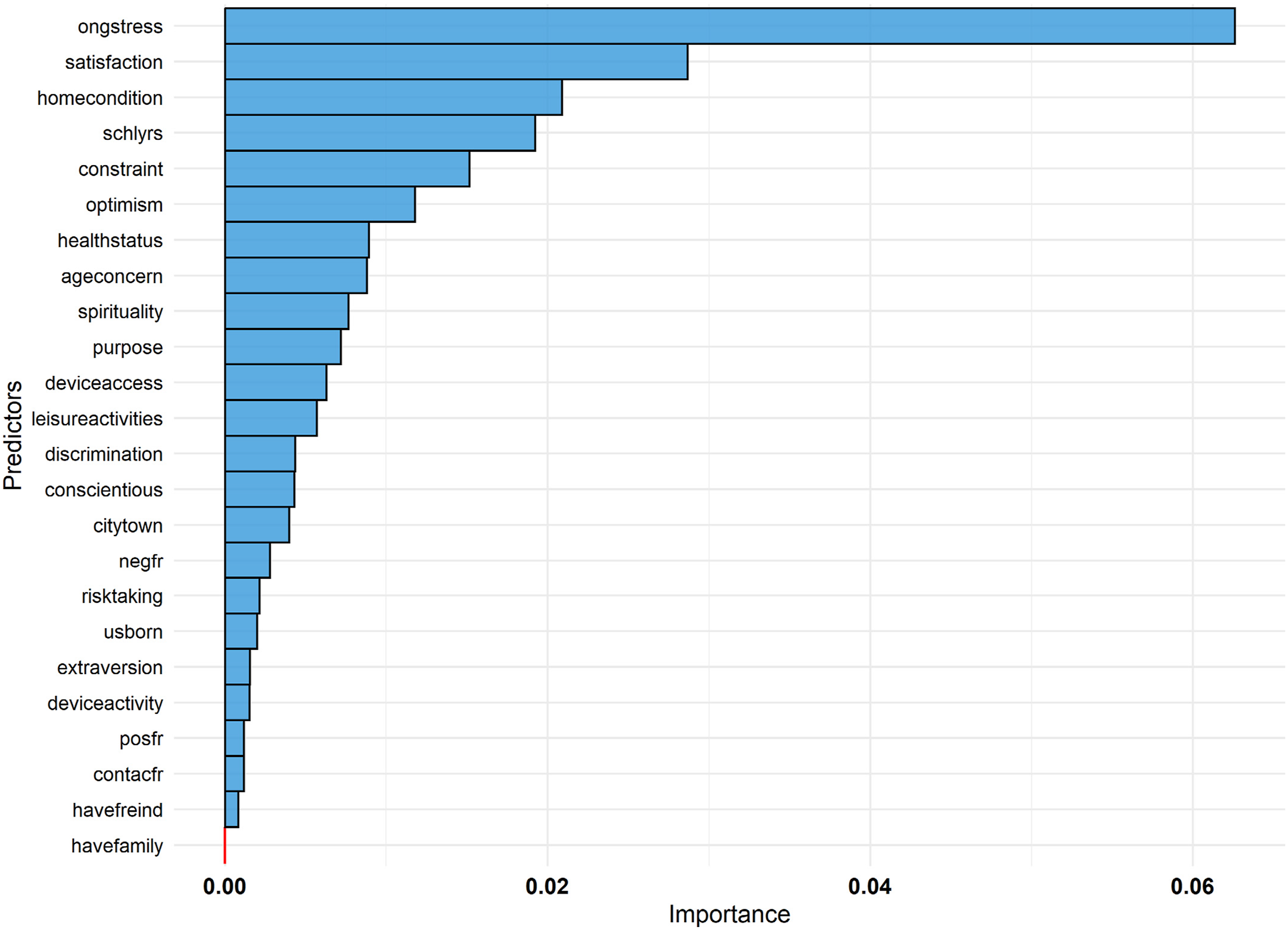

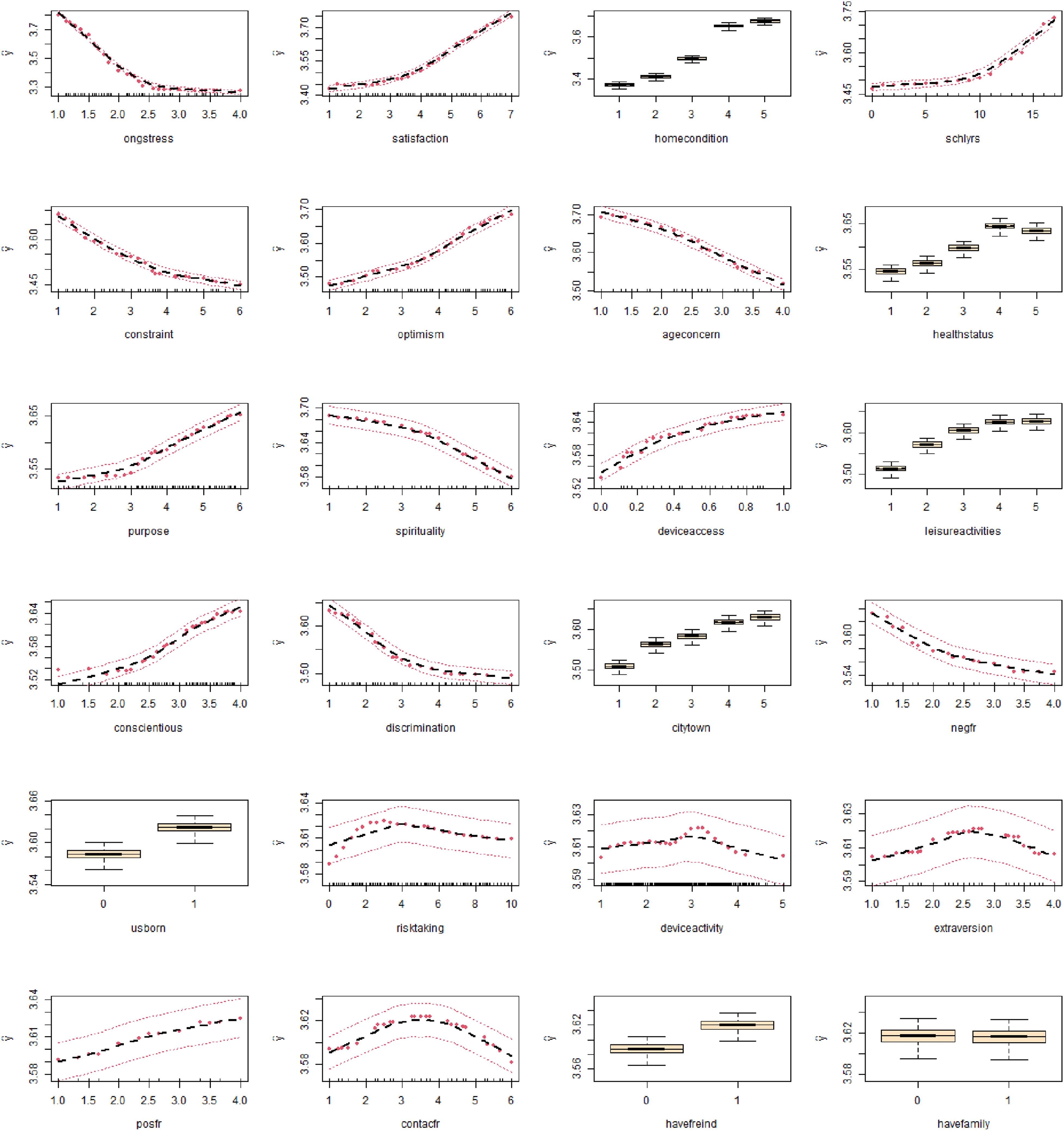

The combination that achieved the best overall performance in hyperparameter tuning was mtry = 6 and nodesize = 4. These values were used in the final Random Forest model using 24 selected predictors. The Random Forest model with 1000 trees yielded an OOB R2 of 0.444 and an OOB mean squared error (MSE) of 0.379. In psychological research, an R2 value of this magnitude is generally considered substantial (Whittier et al., 2024). Permutation-based variable importance scores were computed for all predictors and are presented in Figure 3. The strongest predictor was ongoing chronic stressors (ongstress). In addition to chronic stressors, several other factors emerged as significant predictors of perceived financial quality of life, including general life satisfaction, satisfaction with one’s living place, educational attainment, perceived constraints on personal control, and optimism. Figure 4 presents the partial dependence plots, illustrating the direction of the relationships between each predictor and financial well-being. Variable Importance Partial Dependence Plots

Discussion

Top Predictor: Ongoing Chronic Stressors

The results indicate that ongoing stressors are the strongest predictor of financial well-being. The chronic stressor scale used in this study captures both the presence and emotional impact of several stressors experienced across multiple domains, including health, family, work, finances, housing, interpersonal relationships, and caregiving. Prior research has consistently shown that chronic stress undermines cognitive functioning and increases vulnerability to various forms of mental illness in older adults (Marin et al., 2011). In particular, chronic stress impairs executive function (mental processes related to planning, organizing, and carrying out actions), particularly cognitive flexibility (an individual’s capacity to adjust their behavior in response to changing environments or to suppress outdated information in order to acquire new knowledge) (Girotti et al., 2024). These cognitive abilities are critical for effective financial decision-making and self-regulation (Gladstone & Barrett, 2023). Long-term exposure to chronic stressors may erode cognitive functioning, thereby compromising one’s ability to manage finances competently and maintain a stable sense of financial well-being. This supports the view that financial well-being is not merely the result of internal traits or financial behaviors, but is shaped by persistent structural pressures that wear down individuals’ capacity to plan, adapt, and feel in control.

Other Key Predictors

In addition to chronic stressors, several other factors emerged as significant predictors of perceived financial quality of life, including general life satisfaction, satisfaction with one’s living place, educational attainment, perceived constraints on personal control, and optimism. The association between life satisfaction and financial well-being has been well-documented (Foong et al., 2021). Prior research has shown that economic status is more strongly linked to life satisfaction than to other aspects of well-being, such as emotional well-being (Nilsson et al., 2024). While financial well-being is often conceptualized as a determinant of life satisfaction in later life (Yeo & Lee, 2019), it is also plausible that a generally satisfying life provides individuals with greater cognitive and emotional resources for making sound financial decisions. Emerging longitudinal research shows that life satisfaction can indeed function as a predictor of various positive outcomes, not solely as an outcome (Joshanloo, 2023). Ultimately, it remains for future longitudinal studies to clarify the direction of the link between life satisfaction and financial well-being, but a mutual relationship seems plausible.

Satisfaction with one’s housing condition also emerged as an important predictor. This variable likely reflects a sense of material stability and security, emphasizing the importance of having a safe and adequate physical environment for fostering financial confidence and planning. General life satisfaction and satisfaction with one’s living situation thus appear to be important components of perceived financial well-being. These findings suggest that financial well-being is not solely determined by financial skills but is also shaped by broader life evaluations and concrete aspects of one’s daily living conditions.

Educational attainment (measured in years of schooling) is a well-established structural predictor of financial outcomes (Furnham & Cheng, 2017), likely functioning through increased access to employment opportunities, higher income potential, and improved financial literacy. Its predictive value in the current study reinforces its role in shaping more favorable financial trajectories and confirms it as the most influential demographic variable in the model. Education may also serve as a resource that increases individuals’ perceived control over life outcomes (Dalgard et al., 2007), which itself emerged as a key psychological predictor of financial well-being. Perceived constraint on personal control (the belief that one has limited influence over life outcomes) emerged as the next strongest predictor. This finding aligns with prior research suggesting that perceived control is a key precursor to effective financial decision-making (Shim et al., 2009). A low sense of control may hinder adaptive financial behaviors, such as budgeting, saving, and seeking financial guidance, as individuals who feel hopelessly constrained may view financial challenges as insurmountable, leading to avoidance or disengagement.

Lastly, optimism (the general expectation that future outcomes will be positive) was also a key predictor of financial well-being. Optimism has been linked to more proactive and effective economic behaviors. For instance, recent evidence from cross-sectional and longitudinal analyses across multiple countries has shown that optimism predicts greater savings over time, even when controlling for a range of demographic, psychological, and financial variables (Gladstone & Pomerance, 2025). Optimistic individuals may be more likely to engage in planning and problem-solving activities (Carver & Scheier, 2024), which can enhance both financial control and resilience. Optimism may serve as a motivational resource, encouraging individuals to persist in financial planning and adapt to financial challenges over time. While it is not a substitute for structural advantage, optimism may help sustain engagement under uncertainty and buffer against demoralization. This aligns with control-based models of behavior (Hong et al., 2021), which suggest that negative outcomes (e.g., financial disengagement) can result not necessarily from lack of ability but potentially from learned helplessness or diminished sense of efficacy.

Predictors of Secondary Importance

Several variables demonstrated nontrivial predictive value for financial well-being, suggesting secondary influences that are nonetheless worth considering. Satisfaction with one’s physical health has been associated with greater financial well-being, likely because it reflects perceived capability and personal security, both of which are relevant to financial independence and planning (Birkenmaier et al., 2023). Age-related concerns, that is, anxiety about potential losses associated with aging, have been linked to a pessimistic outlook that may reduce motivation for financial preparation and increase vulnerability (Gum & Ayalon, 2017). Spirituality or religiosity emerged as a generally negative predictor, consistent with findings by Kose and Cinar (2020), who reported a generally inverse relationship between personal religiosity and financial well-being. A sense of purpose, by contrast, may support goal-directed behavior and long-term financial planning (Schippers & Ziegler, 2019). Availability and possession of modern technological tools and gadgets and satisfaction with one’s leisure activities predict higher financial well-being. Access to electronic devices and engagement in leisure activities may promote financial well-being in older adults by supporting social connection, cognitive engagement, and autonomy. These two predictors have also been linked to other indicators of optimal aging (Joshanloo, 2025). Overall, although these several variables were not among the strongest predictors, these results underscore the relevance of health perceptions, aging-related concerns, and lifestyle resources such as digital access and leisure engagement in predicting older adults’ financial well-being.

Implications

The primary contribution of this study is the systematic ranking of predictors of financial well-being, clarifying their relative importance. Psychological variables (e.g., chronic stress, perceived control, optimism) showed stronger associations with financial well-being than demographic factors. Chronic stress was the most influential predictor, followed by life satisfaction and perceived control. Among demographic variables, education was most important, exceeding factors such as country of birth, age, race, and gender. This rank-ordering identifies the domains that most strongly relate to financial well-being and provides an empirical basis for prioritizing interventions. Conceptually, the results support a framework that views financial well-being as a dynamic balance between environmental demands and psychological resources. The results imply that while financial resources remain important, well-being also depends on individuals’ ability to manage stress, sustain agency, and mobilize resources. These findings underscore the central role of psychological processes in shaping financial well-being and offer guidance for advancing theory and developing interventions beyond purely economic perspectives.

Although correlational, the findings suggest implications for interventions to enhance financial well-being in older adults. The prominence of chronic stressors across health, housing, family, and work highlights the need for coordinated, multi-sector approaches rather than treating financial problems in isolation. Integrated models should address housing stability, healthcare, family support, and employment assistance. Financial service providers and social workers could incorporate brief assessments of chronic stress, optimism, and perceived control and other psychological variables, given that these psychological indicators may shape financial outcomes alongside demographic and income factors. Early identification of high stress, low control, or declining cognitive functioning could enable timely referrals to support services before financial problems escalate.

Limitations and Future Directions

Several limitations should be acknowledged. First, the cross-sectional design limits causal inference. Longitudinal or experimental studies are necessary to establish directionality and examine potential reciprocal relationships. Second, the generalizability of the findings may be restricted to populations similar to the current sample. Replication in culturally and economically diverse populations is needed. Third, while the study adopted an inclusive approach by considering a wide range of variables, it was constrained by the availability of items/variables within the Psychosocial and Lifestyle section of the HRS. In addition, this study focused on potential psychological, social, and demographic predictors. Consequently, some relevant factors, such as materialism or financial factors, were not included (Fan & Henager, 2021).

Another limitation to consider is that the unique context of 2022, marked by the ongoing COVID-19 pandemic, likely influenced the financial well-being of older adults in this study. Many older individuals may have exited the labor force due to health concerns linked to COVID-19, resulting in the loss of expected income sources and heightened financial strain. Pandemic-related financial challenges, such as reduced income and increased expenses, have been shown to negatively affect older adults’ economic security and subjective well-being (Samuel et al., 2022). Recognizing this impact is important for interpreting the study’s findings. Finally, this study employed the CFPB Financial Well-Being Scale. The scale is a widely used instrument for assessing financial well-being, and its validity has been demonstrated in prior research (Consumer Financial Protection Bureau, 2017; Howat-Rodrigues et al., 2021). It shows strong associations with objective indicators of economic security, including household income, thereby supporting its construct validity (Consumer Financial Protection Bureau, 2017; Heck et al., 2024; Khashadourian & Harrison, 2024). Nonetheless, it is important to recognize that alternative conceptualizations and measures of financial well-being exist, some of which differ in scope and emphasis from the CFPB scale (Aubrey et al., 2022). Moreover, the CFPB scale has been criticized for capturing financial well-being as a unidimensional construct, given that its items load onto a single latent factor (Aubrey et al., 2022). Consequently, future research would benefit from replicating these findings using alternative conceptualizations of financial well-being.

Conclusion

This study provides an updated understanding of financial well-being, highlighting its psychological foundations. Beyond economic conditions and demographics, financial well-being is strongly linked to chronic stress, life satisfaction, perceived control, and optimism. These factors reflect the interaction of environmental pressures, cognitive appraisals, and psychosocial resources. The prominence of chronic stress, alongside optimism and perceived control, shows that financial well-being depends on individuals’ ability to sustain agency and positive outlooks despite ongoing challenges. This perspective moves beyond economic-centric views, emphasizing that sustainable improvements require addressing both chronic stressors and the psychological resources that support financial adaptation. By advancing this integrative approach, the study contributes to the refinement of conceptual models of financial well-being and offers practical guidance for interventions aimed at older adults.

Supplemental Material

Supplemental material - Financial Well-Being in Older Adults: A Machine Learning Analysis of 47 Potential Predictors

Supplemental material for Financial Well-Being in Older Adults: A Machine Learning Analysis of 47 Potential Predictors by Mohsen Joshanloo in Journal of Applied Gerontology.

Footnotes

Ethical Consideration

Consent for Publication

Informed Consent was obtained from all participants.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Supplemental Material

Supplemental material is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.