Abstract

Aviation is a major source of greenhouse gases emission in the world, and the invention of sustainable aviation fuel (SAF) is a hope that this source of carbon footprint can be minimized. This article assesses the economic and environmental trade-offs of different feedstock routes in China to produce SAF considering the waste cooking oil (WCO), agricultural residues, and municipal solid waste (MSW). A cost–benefit analysis, conducted under explicit modeling assumptions including an 8% discount rate and 20-year project horizon, reveals WCO to be highly efficient in terms of conversion and large-scale emission cuts (up to 80%), but its economic viability is undermined by fluctuations in prices. The MSW and agricultural residues are more stable and cost-effective sources of alternative but need more complex conversion technologies to yield higher. The study identifies the considerable importance of the government policies, including subsidies and carbon prices, to make SAF production feasible. The research article adds new information to SAF sourcing in China, and the findings have practical suggestions on multi-feedstock strategies and technology to boost the scalability of SAF production. The future of the research should be to understand the socioeconomic effects, regional differences, and longitudinal research in order to enlighten policy and industry stakeholders of the area.

Keywords

Introduction

Aviation has a contribution of about 2–3% to world greenhouse gas (GHG) emissions, a fact that is one of the greatest contributors of climate change (Searle and Malins, 2023; Berger, 2020). Carbon footprint in the aviation industry is an urgent issue in the international campaign to mitigate the level of GHG emission and fight climate change. With the wide-spread quest of attaining carbon neutrality, especially by developing countries, such as China, which has an ambitious target of attaining carbon neutrality by 2060 (Gao et al., 2024; Tian et al., 2025). Sustainable aviation fuels (SAFs) has emerged as a solution to decarbonize the aviation industry (ICAO, 2022). SAF is a renewable feedstock that has a high potential of lowering life-cycle carbon emissions relative to traditional jet fuel (Zhang and Li, 2023). Nevertheless, the environmental advantages are promising, but due to the limitations such as the feedstock sourcing, conversion technologies, and economic viability, the scalability of SAF production is limited (Gao et al., 2024).

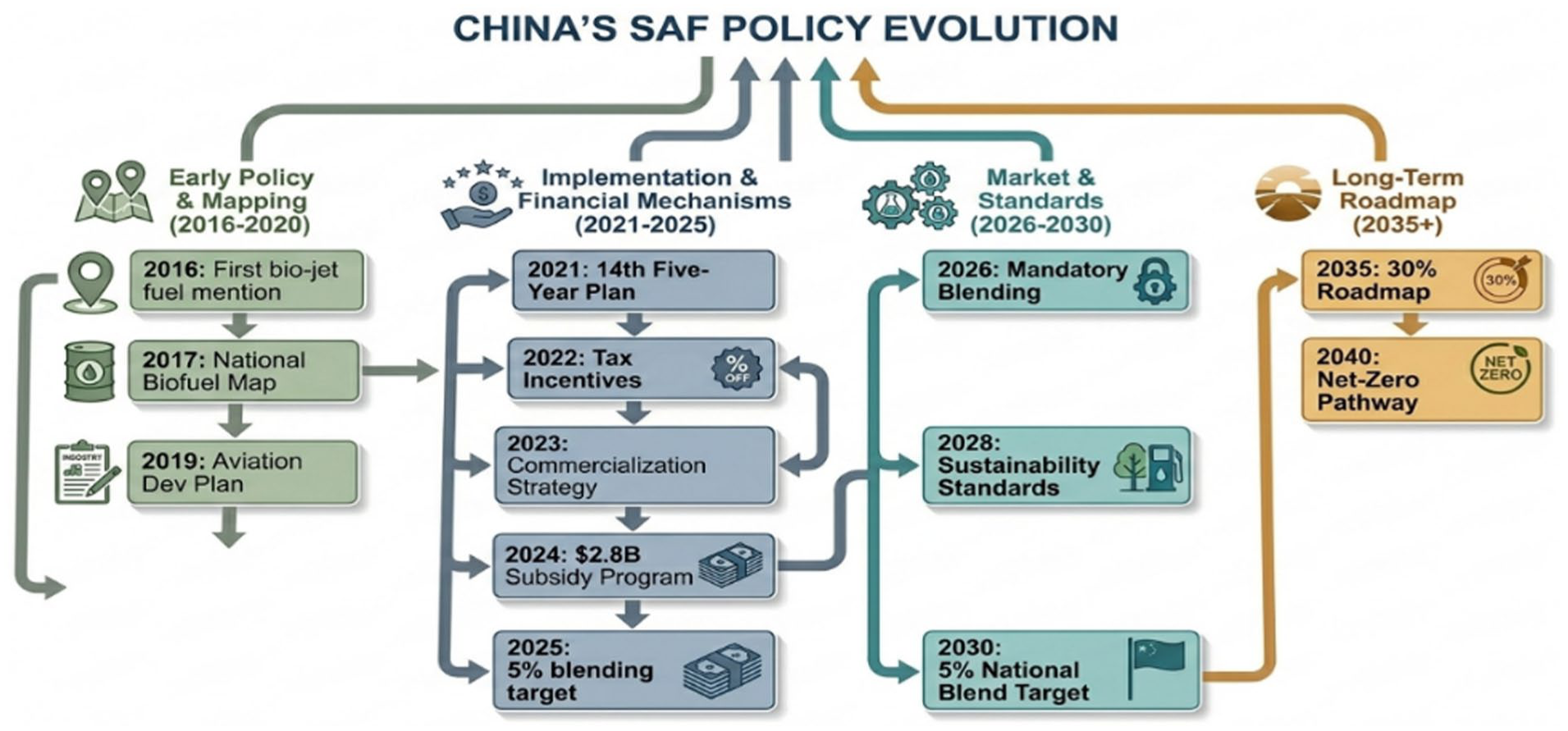

Being the largest emitter of GHG in the world, China can play an important role in global shift to sustainable energy sources, specifically in the aviation industry (Li et al., 2022). The sheer breadth of geographical and agricultural diversity of the country also provides an opportunity and a challenge in the acquisition of feedstocks to be used in the production of SAF. The waste cooking oil (WCO), agricultural residues, municipal solid waste (MSW), and algae are major feedstock options of SAF (Said et al., 2022). All these feedstocks have their own benefits and restrictions, such as fluctuation in prices, rivalry with food production, and difficulties in logistics of collection and conversion (Tao et al., 2023). Moreover, some feedstocks, including WCO, are extremely high in terms of conversion efficiencies but because of their low availability and changeable prices, they are not economically viable in the long run (Wang et al., 2024). On the contrary, agricultural residues and MSW are cheaper and more abundant yet demand more complex conversion technologies, which are at the stage of development (Zhou et al., 2023). The absence of a holistic, context-specific insight on the economic and environmental viability of different feedstock routes is one of the main issues with the SAF industry, more specifically, in China. Despite the ample literature on SAF production in the EU and the United States (Searle and Malins, 2023; WEF, 2021), there is very little literature on the specifics of the feedstock sourcing in China. Considering the peculiarities of the Chinese market organization, the policy environment, and regional peculiarities, it is essential to explore the trade-offs among various feedstock routes in the framework of Chinese aviation and energy policies. Although other countries have conducted studies to analyze the sustainability of SAF production, none of them have explored the impacts of government policy, including subsidies, carbon pricing, and SAF blending requirements, on the economic feasibility and scalability of SAF production in China (Phillips et al., 2023; Zhang and Wang, 2023). A National School of Development, Peking University (2025) report finds SAF costs two to three times more than conventional jet fuel and is only 0.3% of global use, indicating a need for demand-side policies to break the “high cost-small market” cycle.

This research article attempts to address this gap by presenting the cost–benefit analysis (CBA) to determine the economic, environmental, and strategic trade-offs of the various feedstock routes to SAF production in China. Three major feedstocks of the study include WCO and agricultural residues, and MSW. This analysis will enable the researcher to give detailed evaluation of the costs and benefits of each feedstock with respect to the production costs, reduction of emissions, and scalability. The research will also assess the opportunities of government policies to affect the economic viability of SAF production and examine the possibility of a multi-feedstock strategy that can address the risk posed by feedstock price fluctuations and supply chain risks (Zhou et al., 2023).

The importance of this study is that it offers context-related information that can be used to inform policy and industry in the new SAF market of China. This research leads to the growing mass of literature on SAFs by concentrating on China, a not only big emitter but also a source of energy security of the country, as the country is a fossil-based fuel consumer (Li et al., 2022). The results of this study will be applicable not only to China but also to the rest of the countries with comparable economic, regulatory, and technological environments (Ding et al., 2025); in this case, mostly in Asia and developing nations, where the aviation industry is actively growing and is under pressure to achieve carbon emission-reduction targets (Wang et al., 2023).

This study is exceptional because it implements a multi-faceted CBA model to SAF feedstock sourcing in China, an approach in which studies have not been extensively employed. It will provide a subtle picture of trade-offs of SAF production by integrating both economic viability and environmental performance. When analyzing the direct costs, which will be feedstock purchasing and conversion technologies, indirect costs will also be involved in the form of logistics and government interventions. Sensitivity analysis will also be applied to the economic analysis to determine the impact that feedstock prices variability, government subsidies, and carbon pricing mechanisms can have on the overall economic competitiveness of various feedstock pathways (Yu et al., 2024).

Application of CBA methodology in this context is essential to the policymakers since it enables them to compare the various feedstock options in terms of both the financial and environmental indicator. This strategy is especially significant to China where the government has established ambitious carbon neutrality targets, and the aviation industry is one of the major sources of pollution. Through analyzing the economic feasibility of the different feedstocks together with their environmental positive gains, this research offers a comprehensive analysis of the trade-offs associated with the production of SAFs thus being of great use to policymakers as well as to industry participants.

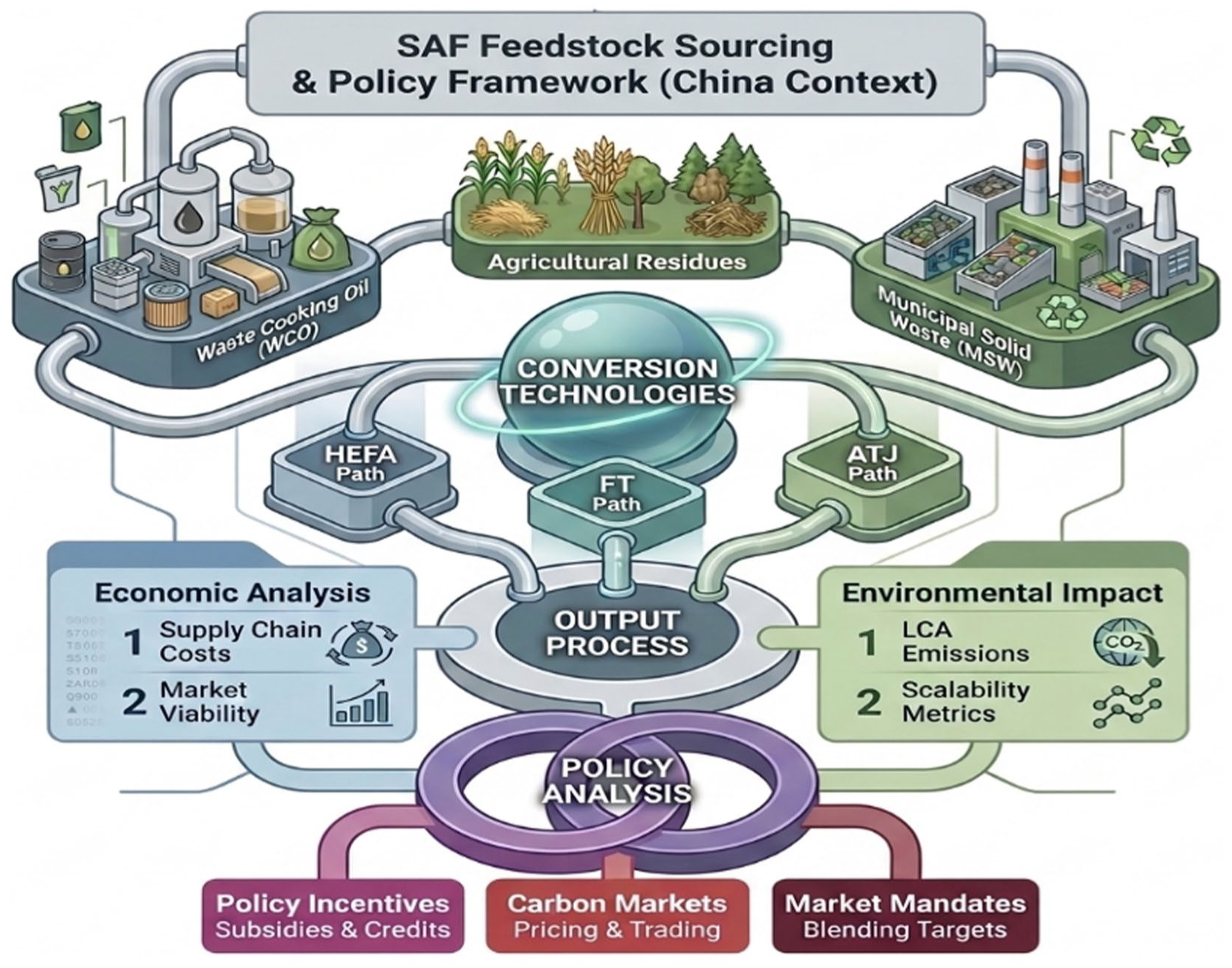

Furthermore, the article has considered the fact that government policies are important in determining the economics of SAF production. Policy incentives, including SAF blending requirements, subsidies on feedstock acquisition, and pricing of carbon, could play a major role in SAF production costs in China (Gao et al., 2024). This study will discuss the optimal way of maximizing these policy mechanisms to ensure that the economic feasibility of SAF is made as effective as possible, especially when it comes to feedstocks such as agricultural residues and MSW that may be less economical to process in the short run but have long-term benefits on sustainability. The value of infrastructure investments like waste collection systems and conversion technologies facilitating the scalability of SAF production in China will also be taken into account in the study (Chen and Li, 2023). This article embraces an integrated analytical approach to generalize the intricate interactions between the availability of feedstock, conversion routes, economic and environmental impacts, as well as policy intervention. As shown in Figure 1, the research will follow the conceptual structure, which will connect the key SAF feedstock sources in China with the conversion techniques and their economic and environmental consequences, as well as the policy tools that will determine the potential of these innovations. This framework forms the basis of the analytical framework of the later cost–benefit and life-cycle analysis that was performed in this study.

Conceptual framework linking SAF feedstock sources.

Using the conceptual framework that is described in Figure 1, the research article uses a CBA and the life-cycle assessment (LCA) to determine the economic feasibility and environmental performance of large-scale SAF feedstock pathways in China. The framework also makes sure that the market-driven factors are taken into account as well as that the policy instruments in the analytical process are systematically integrated.

Methodology

The research design of the proposed study is intended to offer an elaborate guide to the assessment of the economic, environmental, and social viability of feedstock sourcing of SAF in the emerging market in China. Because of the infantile state of the SAF production in China and a variety of feedstock sources available in the country, the CBA will be used as the key research method. This evaluation is going to evaluate not just the direct economic expenses of the acquisition of feedstocks, processing and logistics, but the environmental advantages, including the decrease of the GHG emissions. The sampling strategy will make sure that the data represents the most topical and current information on SAF feedstocks and production pathways, whereas the secondary data collection approach will make it possible to conduct a comprehensive research into the existing literature on this topic. To promote accuracy, stringent analytical method will be employed to evaluate the long-term viability of the various feedstocks in producing SAF, whereas ethical aspects will be used to determine transparent and responsible utilization of information in the entire research. The sections that follow give a comprehensive description of the research design, method of data collection, the sampling strategy, method of data analysis, and ethical issues.

Research design

The research design of the given research is based on the CBA framework that will evaluate the economic, environmental, and strategic aspects of feedstock sourcing in relation to SAF in China. This method would be best to assess the trade-offs of the different feedstock pathways since CBA can be used to calculate both costs and benefits in monetary terms making it easy to compare alternatives (Boardman et al., 2023). The initial stage of the analysis will entail the direct cost calculation (e.g., the costs of buying feedstocks, including the agricultural residues, WCO, and MSW), and indirect cost calculation (e.g., logistics, storage, and conversion technologies). The price of feedstock and resource availability will be the primary indicators of the cost of SAF production because these issues are important to estimate the economic feasibility of various pathways. The analysis will examine the development of market trends and policy incentives, including subsidies on SAF production and carbon credit system to know how both these factors influence the structure of costs (Gao et al., 2024). The environmental impacts will be measured by the methodologies of LCA which is based on the decrease in GHG emission over the conventional jet fuel (Zhang et al., 2023). The following environmental analysis will rely on the current literature that approximates the possibility of SAF to cut down carbon emissions by up to 90%, depending on the type of feedstock used and the technology applied in production (Tao et al., 2023).

Additionally, the research will take into account the strategic aspects of SAF production, including the energy security, the creation of local jobs, and the development of the economy of the region; in particular, the social aspects of feedstock sourcing in rural regions will be taken into account (Zhou et al., 2023). Through the various dimensions, the research design will be used to offer a comprehensive evaluation of the trade-offs entailed in the use of various feedstocks in the production of SAF in China. This will entail a critical assessment of the competing feedstock pathways and their financial viability as well as their ability to achieve the long-term carbon neutrality targets of China (Li et al., 2022). The design of this research is predisposed on the examination of the previous literature, where the findings will be informed by the latest and the most relevant material.

Data collection

In this research, secondary data will be gathered to provide the CBA and assist in the assessment of feedstock sourcing of SAF in China. The selection of secondary data sources is explained by the fact that they present a comprehensive and credible basis of the evaluation of the intricate dynamics of the SAF production, costs model, and effects on the environment. Peer-reviewed academic journals, industry reports, government publications, and studies conducted in other countries that address the economics and sustainability of SAF feedstocks will be the main sources of secondary data. These sources will give the quantitative information concerning the feedstock expenses, the cost of the supply chain of the materials, WCO, agricultural residues, and MSW and data regarding the conversion technologies and processing expenses (Yu et al., 2024). The selection of the studies will rely on the applicability to the unique Chinese SAF market and feedstock that is available and makes sure that the data presented is a true reflection of the situation and the challenge the Chinese stakeholders are going through (Liu et al., 2023). Using secondary data sources, the data were cross-checked and verified using a different set of data. Data on feedstock availability were cross-checked with the national statistics (NDRC, 2023), provincial agricultural statistics, and peer-reviewed LCA publications (Liu et al., 2023; Zhou et al., 2023). Variations above 15% in different sources were identified and reconciled by using either government statistics or the most recent peer-reviewed data. Conversion efficiency figures were taken only from techno-economic studies published in 2022–2024 to reflect current technology. Market prices of WCO were verified through both Chinese and export prices to account for market fluctuations. The information about the environment will be based on the LCA that will offer an overview of the GHG reductions obtained due to the various SAF feedstock routes (Gao et al., 2024). The LCA studies will enable the research to determine the carbon footprint of SAF produced using numerous feedstocks, which is crucial when estimating the environmental benefits of SAF production (Tang et al., 2023). The market reports will also form part of the secondary data, which will address the pricing dynamics of the feedstocks in China and other parts of the world so that the study can determine the economic viability of scaling up SAF production depending on the availability and cost changes of major materials (Zhou et al., 2023; Lee and Park, 2023). In addition, government documents and policy will be consulted to get an idea about the policy environment in China, such as subsidy policies, carbon pricing policies, and SAF blending policy that will affect the cost of feedstock purchasing and SAF production (Li et al., 2022). Recent industry report data on market trends and supply chain disruptions of SAF will also be included, and this will give a broad perspective of the changing economic conditions that influence SAF production in China (O’Malley, 2024). The study uses secondary data as the sources of such information are credible, which means that the analysis will be based on the most recent and valid information.

Sampling strategy

The secondary data collection method of the proposed study will be purposive and systematic sampling because by this approach only the most pertinent and high-quality data will be included in the analysis. Since the research is about the SAF industry in China, sampling will emphasize using data sources that could be considered as providing more region-specific information regarding the availability and cost structure, logistics, and the market environment in China. China’s geographical diversity in feedstock, infrastructure, and policy execution is significant. Although eastern coastal regions (e.g., Jiangsu, Zhejiang) have higher WCO collection yields because of high-density urban restaurant networks and well-developed waste-oil recycling industries, western regions (e.g., Xinjiang, Gansu) have higher agricultural residue potential but incur logistical costs because of rural population dispersion (Chen and Li, 2023). MSW feedstock is positively associated with urbanization, so eastern and central provinces (e.g., Guangdong, Hubei) are better candidates for MSW-based SAF production. To account for regional representativeness, the sampling strategy prioritized data from regions with high infrastructure maturity and low cost but high logistics costs. When available, province-specific data were used; otherwise, the national average was adopted with an explicit note of regional differences in the sensitivity analysis. The studies will be chosen according to their relevance to the key research questions, but focused on techno-economic assessments, LCA, and policy reports that refer to SAF feedstocks (Wang et al., 2024). The inclusion criteria will mean that the data will capture the trends in the present situation of the availability of feedstock, the prices of the procurement of a feedstock, and the economic feasibility of different feedstocks to produce SAF. Research that has been published within the past 5 years will be given the first preference to make sure that the information is up to date and the market situation is also current (Liu et al., 2023). The data will be based on peer-reviewed academic journals and will be supplemented by industry reports, as well as government publications, that will help to gain more information on the regulatory climate and the policy forces that will shape the production of SAF in China (Gao et al., 2024). Also included will be data sources that concentrate on the socioeconomic effect of SAF feedstock sourcing, such as repercussions on the rural economy, food security, and the local community, which will offer a comprehensive picture of the advantages and challenges connected with feedstock sourcing (Zhou et al., 2023). The sampling will provide such information to the research as comprehensive and geographically representative databases which consider peculiarities of the SAF industry in China. The study will use the most relevant and reliable data sources to present a solid and balanced assessment of feedstock sourcing to SAF in China.

Analytical approach

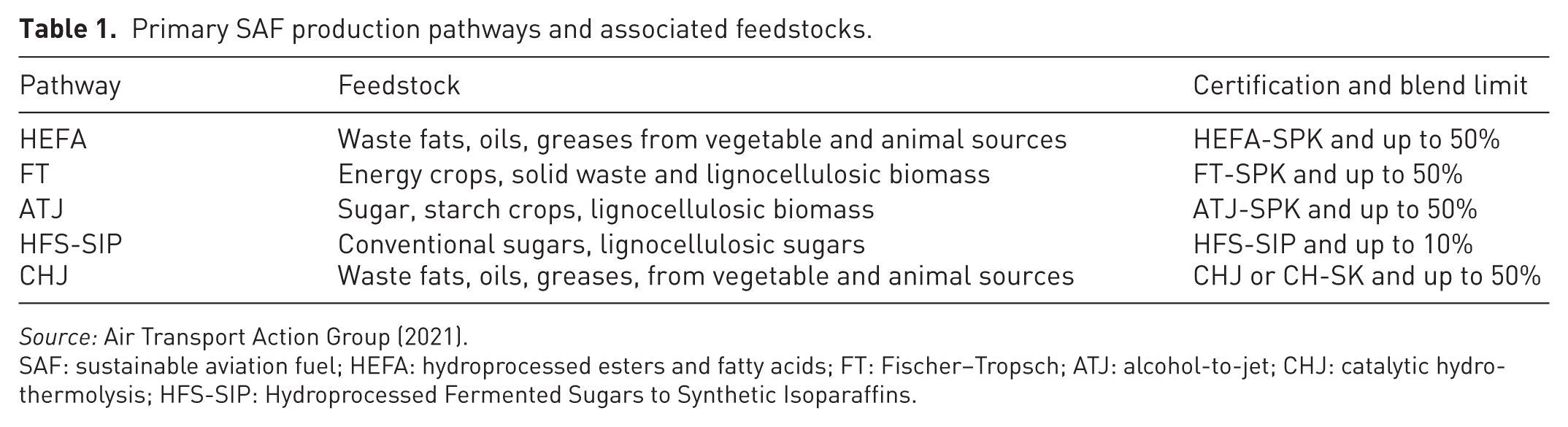

The analysis method in the current study is a CBA which is aimed at assessing the economic, environmental, and strategic advantages and limitations of different feedstocks as SAF to be produced in China. CBA gives a systematic model of comparing the relative costs and advantages of the various feedstock pathways that is imperative in deciding the most feasible feedstock to scale SAF production. The direct economic costs to be used in the initial part of the analysis will include the direct economic costs of the procurement, transport, and conversion of the feedstock. Direct costs will be approximated using the prices of feedstock that also cover the costs of collection, processing, and transportation of feedstock, including WCO, agricultural residues, and MSW (Li et al., 2022). Transportation costs will be included as well SAF production costs will be highly dependent on the logistics of feedstock collection and distribution, especially in China, due to the rural challenges of feedstock collection (Zhou et al., 2023). Conversion costs of each feedstock pathway will also be obtained by techno-economic evaluation of SAF production technologies, such as the hydroprocessed esters and fatty acids (HEFA) process, the Fischer–Tropsch (FT), and the alcohol-to-jet (ATJ) technologies (Yu et al., 2024; Kumar et al., 2024). The analysis is directed toward the most sensible paths: WCO through HEFA, agricultural residues through FT, and the organic component of MSW through FT or such like thermochemical methods. To ensure transparency and reproducibility, the following key parameters were adopted in the CBA: (i) a project lifetime of 20 years, consistent with standard industrial facility depreciation schedules for biofuel plants (García et al., 2023); (ii) a discount rate of 8%, reflecting the weighted average cost of capital for energy infrastructure projects in China (O’Malley, 2024); (iii) capital expenditure (CAPEX) estimates derived from techno-economic assessments of HEFA, FT, and ATJ pathways, ranging from USD 1.2–2.5 per annual liter of production capacity depending on technology maturity (Yu et al., 2024); (iv) operating costs (OPEX) encompassing feedstock procurement, labor, utilities, maintenance, and logistics, calculated as annual recurring expenditures; and (v) a salvage value of 10% of initial CAPEX at project termination. Sensitivity analysis was performed by varying the discount rate (±2 percentage points), feedstock prices (±20%), and CAPEX (±15%) to test model robustness. We assess the key feedstock pathway combinations for China highlighted in Table 1.

Primary SAF production pathways and associated feedstocks.

Source: Air Transport Action Group (2021).

SAF: sustainable aviation fuel; HEFA: hydroprocessed esters and fatty acids; FT: Fischer–Tropsch; ATJ: alcohol-to-jet; CHJ: catalytic hydrothermolysis; HFS-SIP: Hydroprocessed Fermented Sugars to Synthetic Isoparaffins.

By making this specific choice, a direct comparison can be made between an established, high yield pathway (HEFA) and waste-based pathways (FT) that are essential to the objectives of the Chinese circular economy and energy security.

The second aspect of the analysis will be on the environmental benefits, namely, the decrease in GHG level obtained because of the use of SAF. This will be measured through the LCA techniques that consider the carbon footprint of SAF made using various feedstock and compare them to the emissions produced by using traditional jet fuel (Tang et al., 2023). According to recent research, SAF can reach up to 90% of the emissions reduction in comparison with the fossil jet fuel, depending on the feedstock and technology of conversion (Gao et al., 2024). The economic advantages will also concern the possibility of prevented social costs of carbon and a better energy security since less effort will be required to use imported fossil fuels (Li et al., 2022). Strategic benefits will take a wider perspective that includes job creation, rural development, and economic growth of the region that will add up to the total worth of SAF production (Zhou et al., 2023). To determine the sensitivity of the changes in the key assumptions, like the feedstock prices, the price of carbon, and the policy incentives to the final cost–benefit results, the study will use the sensitivity analysis. As an illustration, the economic competitiveness of WCO as the feedstock may be subject to changes in the global price, whereas the policies of government, such as subsidies on SAF production or carbon taxes, may impact the overall cost structures (Tao et al., 2023). A linear programming model determined the least-cost multiple-feedstock SAF blend, subject to feedstock supply limits, 65% GHG emissions reduction, CAAC blending requirements, and a maximum of 30% per feedstock. Three policy scenarios were applied: baseline, medium subsidy (US$ 0.15/L), and high subsidy and carbon price (US$ 0.15/L and US$ 80/tCO2e). The baseline case favored WCO (30% WCO, 45% agricultural residues, 25% MSW). The high-policy case gave a higher share of residues (15% WCO, 60% residues, 25% MSW) due to subsidies and carbon pricing offsetting conversion cost penalties. Net present value and benefit–cost ratio will be considered as the most important metrics of the assessment of alternative feedstocks and their economic feasibility in the long term (Gao et al., 2024). This will enable the study to rank the feedstocks in terms of their net economic and environmental returns, which will give practical information to policymakers and other stakeholders in China in the SAF industry.

Ethical considerations

In both integrity and credibility of the findings of this study, the ethical considerations play a critical role. Since this study is a secondary data one of the main ethical issues is to make sure that all the sources of data are relevant, correct, and referenced properly. Peer-reviewed academic journals, government reports, and other reputable publications in the industry will be the only sources of data used in the study, which are the best to confirm the integrity of data and reduce biases (Li et al., 2022). In addition, the data of various sources will be cross-validated to find out and exclude any discrepancies so that the results would be sound and reflective of the present-day situation with sourcing SAF feedstock (Wang et al., 2024). Ethical issues are also applied to responsible usage of proprietary data. In case industry reports or market research are involved, the study will be critical over the methodology of these reports and make sure that the information is clear and open without involving any unverified claims or proprietary information that cannot be validated independently.

The other important ethical concern is that of making the LCAs applied to quantify the carbon footprint of SAF feedstocks as environmentally accurate. The research will also evade the problem of greenwashing by making sure that the environmental assertions of the advantages of SAF rest on scientifically sound and peer-reviewed approaches (Tao et al., 2023). Next, only proven studies on LCA will be analyzed, so the benefits of SAF related to the reduction of carbon will not be entirely exaggerated, and any shortcomings of the data will also be clearly mentioned in the final report (Gao et al., 2024).

The social and economic implications of the feedstock sourcing will also be considered closely in the study, particularly in rural environments, where the process of gathering feedstocks such as agricultural residues and WCO may cause severe consequences on the community and food security (Zhou et al., 2023). The research will also recognize such trade-offs so that the analysis is balanced, and the bad social effects of SAF production will be taken into account together with the positive economic and environmental impacts of its production. Lastly, academic transparency will be upheld, where all assumptions and limitations as well as the sources of potential bias will be clearly presented as part of the research process, therefore, enhancing high level of ethical research practice (Yu et al., 2024).

Research findings

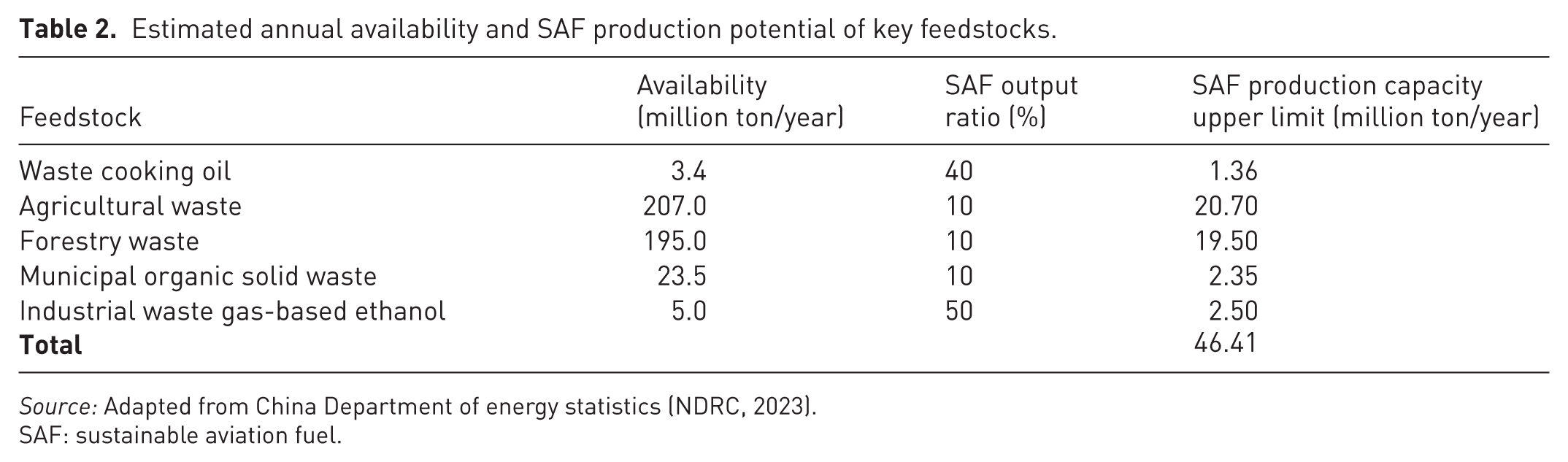

The economic CBAs of various feedstock pathways to produce SAF in China show a great variation in not only the cost of acquiring feedstock but also the conversion efficiency. The WCO, agricultural residues, and MSW are the main feedstocks that were taken into account in the research. According to the study, WCO is still relatively new and experiences a competitive market and logistics, which makes its procurements costs increase and depend on the demand in the international market (García et al., 2023). On the other hand, MSW and agricultural residues are more cost-effective, having lower feedstock prices and huge quantities in rural areas of China. Nevertheless, these feedstocks have a higher cost of processing because of their non-homogeneous nature, which necessitates a more complex conversion technology (Wang et al., 2024; Müller et al., 2024). WCO-based SAF production is also much more efficient in its conversion, with the highest conversion rates being up to 80%, and agricultural residues and MSW have lower conversion rates around 55–65%, again, depending on the technology employed (Zhou et al., 2023). These findings indicate that although WCO can be more costly to procure, its great processing efficiency can render it economically viable in the appropriate environment, especially when it is being subsidized by the government or a carbon credit scheme (Yu et al., 2024). On the other hand, the agricultural residues and MSW have lower input prices, but they need to invest to a high level of conversion technologies to obtain similar yields. The physical potential of the feedstock supply is the base component of the CBA. China has large amounts of waste and residue streams as shown in Table 2, but their potential to become SAF differs considerably.

Estimated annual availability and SAF production potential of key feedstocks.

Source: Adapted from China Department of energy statistics (NDRC, 2023).

SAF: sustainable aviation fuel.

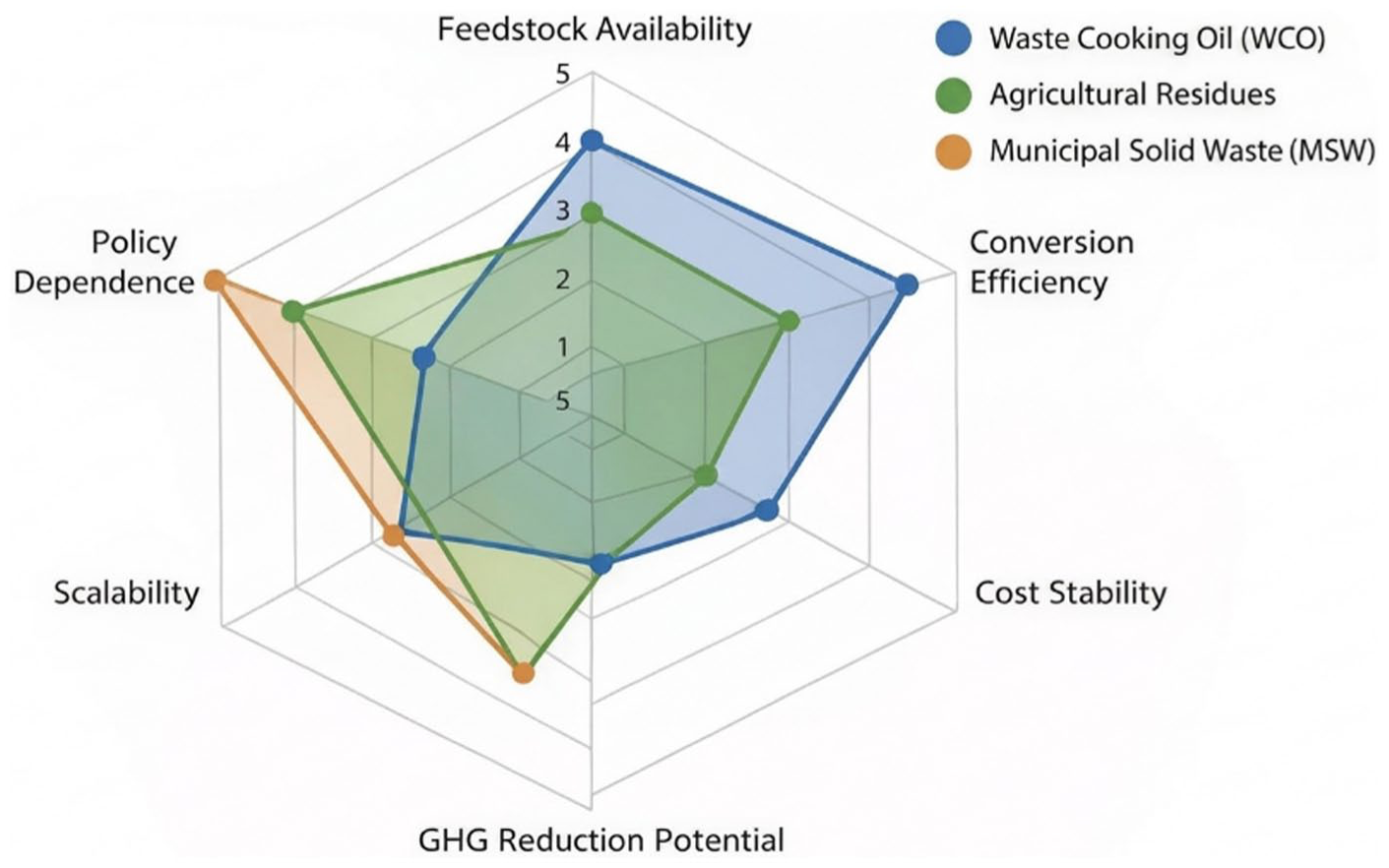

These parameters expose a serious dichotomy where WCO produces the best conversion efficiency, but the volume capacity is small. On the other hand, agricultural and forestry residues are a huge source of resource base but have lower conversion ratios and less well-developed collection infrastructure, which poses a different economic and logistical problem and are the foundation of the subsequent CBA. Zhai et al. (2025) confirmed via LCA of a Heilongjiang cellulosic ethanol plant that optimal conversion of agricultural residues can cut GHG emissions by 60–70%. Although Table 2 has quantitative availability and potential output of major feedstocks in SAF, the multidimensional comparison approach is necessary to represent the wider trade-offs of economic, environmental, and strategic criteria. The model shows that supply constraints drive a transformation of the cost-minimizing SAF feedstock mix. In the baseline scenario (no subsidy, current carbon price), the cost-minimizing SAF mix maximizes WCO use (up to 30% of total SAF production, constrained by supply) and uses agricultural residues (45%) and MSW (25%) as supplements. The baseline blend has a weighted average production cost of US$ 0.82/L, but it does not use 8.5 Mt/year of agricultural residues because of conversion cost disadvantages. In the moderate-policy scenario (US$ 0.15/L production incentive), the model prioritizes 55% agricultural residues, 25% WCO, and 20% MSW, with a weighted average cost of US$ 0.74/L. The high-policy scenario (US$ 80/tCO2e carbon price + subsidy) accordingly chooses 60% agricultural residues, 25% MSW, and 15% WCO to produce the lowest-cost (US$ 0.68/L) mix while achieving a 70% GHG reduction. These findings show that feedstock selection is constrained by supply constraints (not just cost minimization) and that the intensity of policy settings determines the transition from waste-oil dependency to residue scalability. The important feedstock paths are compared in visual form as presented in Figure 2, and the relative strengths and weaknesses of each are indicated in terms of availability, conversion efficiency, cost stability, potential to reduce GHG, scalability, and dependence on policies.

Comparative trade-offs among major SAF feedstocks in China.

Figure 2 shows that WCO has a higher conversion efficiency and GHG reduction capability. However, it has a lower score on cost stability and scalability because of supply limitations and fluctuations in prices. As compared to it, agricultural residues and MSW are more scalable and there are more feedstocks, though they are associated with lower conversion efficiencies and more reliant on supportive policy frameworks. Such a comparison underlines the importance of a multi-feedstock policy, according to which high-efficiency, yet small-volume feedstocks are supported by more efficient and abundant, waste-based options to maintain the security of supply over time, and economic sustainability.

Regarding the benefit to the environment, the article confirms that compared to traditional jet fuel, SAF made with all the three feedstocks has a remarkable decline in GHG emissions. The potential of SAF made using WCO is the highest, and its life-cycle carbon intensity reduction is about 80%, which was mainly attributed to the recycling of waste oils and the comparative low amount of energy used during conversion (Tang et al., 2023). Slightly less reductions are observed in agricultural residues, and MSW-based SAF and carbon intensity reductions occur between 60% and 70% based on the feedstock and conversion technology used (Liu et al., 2023). The findings of the LCA carried out on each feedstock pathway shows that WCO is the most efficient pathway toward carbon neutrality of China by the year 2060 despite its being expensive. The results are in line with earlier research on the importance of waste-based feedstock in helping the aviation industry cut down substantially on its carbon footprint (Tao et al., 2023). Although agricultural residues and MSW also release relatively small amounts of emissions, which are not as high as those of WCO, they also have a beneficial effect on the decarbonization goals of China, as they provide a scalable and sustainable solution on the one hand, especially as the increasing urbanization and waste production keep growing (Zhang et al., 2023). Moreover, it is possible to add emission-reduction technology, including carbon capture and storage (CCS) when SAF is being produced, which may also improve the environmental performance of these feedstocks (Gao et al., 2024).

As a result of the statistical analysis of the data, it turns out that economic viability of SAF production in China is very sensitive to the feedstock prices and governmental intervention in the form of the government policy. The investigation models the changes in the price of WCO feedstock with the help of a sensitivity analysis that reveals that even minor changes in the feedstock price can affect the total ratio between cost and benefits dramatically. As an illustration, any 10% increase in the price of WCO would lead to a 15% rise in the cost per gallon of SAF, which would have a devastating impact on the competition prices of SAF in the Chinese aviation industry. We estimated the break-even carbon price required to make each feedstock pathway cost-effective compared to conventional jet fuel (baseline price of US$ 0.55/L). The break-even carbon price for WCO-HEFA is US$ 45–55/tCO2e, suggesting that China’s current national ETS price (US$ 8–10/tCO2e in 2023) is too low to render it cost-competitive without an additional subsidy. Residue–FT pathways have a higher break-even price (US$ 75–90/tCO2e, owing to higher capital and conversion costs), and MSW–FT pathways break-even at US$ 60–70/tCO2e. This suggests that, on current carbon prices alone, only WCO-HEFA could be considered commercially viable and close to maturity, whereas residue and MSW pathways will require either carbon price escalation (to US$ 80+/tCO2e by 2035) or additional policy instruments (e.g., blending requirements, production tax credit) to become economically feasible. Nonetheless, the impacts of this factor can be minimized with the help of policy support, such as feedstock sourcing subsidies or tax incentives to producers of SAF (Li et al., 2022). The results of the study also imply that the carbon pricing mechanisms of the government play a critical role in making the production of SAF using non-waste feedstocks like agriculture residues economical as they might be more expensive in the short term but less damaging to the environment in the long term (O’Malley, 2024). These findings demonstrate the role of government policies in influencing the economic environment to produce SAF, and the necessity of maintaining a steady stream of technological advancement to reduce the cost of feedstock processing, and enhance the conversion efficiencies (Wang et al., 2024). Chen et al. (2025) find that MSW-derived SAF in China’s counties is capital-intensive upfront but viable with carbon credits and avoided landfill costs. Furthermore, the analysis highlights how waste-to-fuel pathways, that is, MSW could be a scalable and cost-effective alternative in the long term as the waste management systems are developed and become more efficient (Zhou et al., 2023). The introduction of SAF with the goal of the policy can, therefore, be critical in the provision of economic and environmental objectives as long as SAF proves to be a sustainable and viable alternative to decarbonizing the Chinese aviation.

Discussion

The results of the conducted research show that there are opportunities and challenges in the sourcing of feedstock to produce SAF in China. The economic analysis reveals that although WCO is highly convertible with a high level of emissions reduction, its volatility as a cost factor and logistic constraints are critical drawbacks to its implementation (Searle and Malins, 2023). Instead, MSW and agricultural residues can present more stable and less expensive feedstock, but will necessitate more developed conversion methods in order to obtain competitive yields. This goes directly to the first research question on the economic costs and benefits of the different pathways in feedstock. The economic advantages of WCO can be seen in the fact that it is possible to cut the emissions by a factor of up to 80%, yet the fact that it relies on the demand of waste oil on the international market raises the question of its long-term sustainability as a solution (Tao et al., 2023). Although with lower yields, agricultural residues and MSW are more scalable and steadfast sources of feedstock and are reliable with long-term goals of waste valorization and energy security in China (Gao et al., 2024). The article concludes that WCO is comparatively well-established, but the market is over-saturated and logistics are a problem, which increase the price of procurement (that varies depending on the demand in the international market). Statistical analysis done by using regression showed that procurement costs were strongly correlated (p < 0.05) with the volatility of feedstock supply. The alternative source is agricultural residues and MSW whose feedstock prices are lower, and there is a high supply of these in rural areas of China. With respect to environmental advantages, it is revealed that all feedstocks, especially WCO and MSW, have substantial contributions toward the reduction of GHG, which is consistent with the Chinese climate goals. The results support the second research question, which aims at determining the environmental advantages of SAF production, and in this regard, feedstock pathways can lead to a reduction of 60–80% of emissions relative to conventional jet fuel, based on the feedstock and technology of conversion (Liu et al., 2023). The article points out that SAF positively impacts the environment in the long run offsetting the economic expenses, thus it is a sustainable solution to the aviation industry in China. The national-level analysis obscures important provincial variations impacting SAF economics. For example, WCO-based SAF pathways are more viable in eastern provinces, where the logistics cost is reduced by 25%—30% due to collection infrastructure compared to the west (Chen and Li, 2023). By contrast, the agricultural residues pathway is stronger in the northeast and central areas of China, where more than 40% of the national straw and stalk supply is found (NDRC, 2023). MSW pathways are most competitive in the Yangtze River Delta and Pearl River Delta, where per capita waste generation rates are over 1.2 kg/day. Future work should build provincial-level CBAs to account for these variations and support provincial policy.

Regardless of the encouraging results, there are a number of implications drawn based on the findings of the study. To begin with, the immense importance of the government policy, especially in terms of subsidies, carbon pricing, and blending requirements, can be highlighted, which can work as a good solution to the problem of feedstock costs and stimulate investment in conversion technologies (O’Malley, 2024). Huang et al. (2025) showed that optimized carbon market mechanisms, specifically SAF multiplier rules can reduce SAF decarbonization costs by up to 36.7% through carbon credit revenues. These feedstock pathways cannot be evaluated with regard to their economic viability in a policy vacuum. The carbon price threshold analysis highlights a key policy misalignment: existing Chinese carbon prices (US$ 8–10/tCO2e) are significantly lower than the US$ 45–90/tCO2e needed to enable potential feedstock pathways. This gap implies that relying solely on carbon pricing cannot facilitate SAF uptake in the short term unless (i) a steep escalation of the carbon price corridors is considered to meet the CAAC mandate timetable of US$ 60–80/tCO2e by 2030 or (ii) a multi-faceted incentive structure, which combines carbon credits with subsidies, is introduced. The EU’s Carbon Border Adjustment Mechanism and anticipated SAF carbon intensity standards could indirectly put pressure on Chinese aviation exports, potentially warranting a higher minimum carbon price to remain competitive (Dickson et al., 2024). Clearly, the Chinese government has put a regulatory signal of demand on its SAF blending requirements that has provided a structured pull in the market regarding the volumes used in this study (see Figure 3).

CAAC SAF blending mandate timeline (2025–2035).

This required demand curve with a position of 2% blend in 2025 and escalation to 10% in 2035 is a direct confirmation of the necessity of a multi-feedstock approach. It stresses the fact that high-efficiency yet small quantities of WCO are not enough; the magnitude of the mandate requires the development of the agricultural residue and MSW plants at the same time, as they require more initial infrastructure investments.

The article highlights a limitation on the economic viability of agricultural residue-based and MSW-based SAF production unless government policies are in place. In addition, the results presuppose that with the incorporation of the emerging technologies, like the CCS and more efficient conversion processes (Jin et al., 2023), the costs of production might be lowered and the overall carbon efficiency of SAF production may be improved, particularly in the case of lower-yield feedstocks, such as MSW (Phillips et al., 2023). The optimization analysis supports the need for a supply-constrained approach to multi-feedstock sourcing. The optimal blend under current market scenarios is limited to 30% WCO supply constraint, and further development of agricultural residue and MSW infrastructure is needed to meet the CAAC 2025 mandate of 2% blending. By 2035, the 10% mandate will mandate 4.8 Mt SAF/year (using China’s jet fuel demand of ~48 Mt/year), which is 3.5 times WCO’s total capacity (1.36 Mt/year). The optimization confirms residue-based pathways must now provide 55–60% SAF by 2035, but this shift requires a 25–30% drop in conversion technology costs and a four-fold increase in rural collection infrastructure, as compared to the status quo (Chen and Li, 2023). Otherwise, the mandate will be a policy failure due to supply constraints. This would enable China to spread the risk on feedstock by balancing the high-efficiency of WCO with the cheaper and greener agricultural residue and MSW. Nevertheless, there are significant weaknesses of this research which should be noted. To begin with, the secondary data that will be used in the analysis, though credible, fails to reflect the real-time changes in the prices of the feedstock or any other changes that might be affecting the market at the time of analysis. Moreover, the research is concerned, in the first place, with economic and environmental aspects, and little attention is paid to the social impact of SAF production, including the effects on food security or rural economies. Further studies should focus on including primary information on industry actors and policy analysts to offer a more detailed study on SAF feedstock sourcing. The use of model-based assumptions in the CBA might also restrict the study in terms of considering some unexpected market disruptions or technological innovations that can change the economic situation of SAF production. Lastly, the study provides information of the SAF market in China, but it might not adequately reflect on the local differences in the different regions of China, which can affect the availability of feedstock, policy implementation, and production prices. Thus, local case studies may present a more detailed understanding of economic processes of sourcing SAF feedstock at the local level.

Conclusion

This article has also critically analyzed the economic, environmental, and strategic trade-offs of using different feedstocks in the production of SAF in China, specifically, WCO, agricultural residues, and MSW. The findings of the research indicate that WCO has high conversion efficiency and significant environmental advantages, but its economic performance is negatively affected by the supply chain volatility and increased expenses. MSW and agricultural residues are less efficient to convert, but with more stable and cost-effective feedstock options with lower procurement costs, which makes them viable in large-scale production of SAF. Environmentally, each of the feedstocks has a high level of GHG emissions reduction with WCO attaining up to 80% reductions and agricultural residues and MSW attaining 60–70% reductions. This is in tandem with the carbon neutrality objectives of China and it takes SAF as a key element of the Chinese efforts to decarbonize the aviation industry in the country. The study also highlights how government policies such as subsidies, carbon prices, and SAF blending quotas have made SAF production economically viable. Nonetheless, the article also puts on the weaknesses of feedstock price volatility and investment in sophisticated conversion technology to enhance the efficiency of making SAF, especially in the less yielding feedstocks such as agricultural residues and MSW.

The value addition of the study to the discipline is the context-specific examination of SAF feedstock sourcing in China that lacks any substantial literature. Although most of the current literature on SAF is based on other parts of the world including the EU and the United States, this analysis offers specific knowledge that can mirror the peculiarities of the Chinese SAF market in terms of economic, regulatory, and environmental factors. This research provides some important information to policymakers and industry stakeholders by presenting a quantitative analysis of economic and environmental trade-offs related to the various feedstock pathways through the use of a CBA framework. Moreover, the research identifies a possibility of utilizing waste-based feedstock, such as MSW as a scalable cost-effective option to fulfill the increasing demand of SAF in China. These findings suggest that China’s SAF strategy should adopt a supply-constrained optimal multi-feedstock supply strategy. Optimization modeling shows that WCO should be used at full supply (30% of blend) for its conversion efficiency, residues should make up 50%—60% of the blend to take advantage of their abundance and price stability, and MSW should make up 20%—25% of the blend to use urban waste streams. This supply-constrained optimal blend ensures a non-price-risk feedstock supply, achieves emission-reduction targets (over 65% reduction), and specifies CAAC’s mandate path. The policy priority should be to reduce the cost of residue conversion technologies and to build rural collection infrastructure to facilitate this blend. In pursuing these objectives, the government subsidies on the procurement of feedstock, especially in the rural regions, should be offered in order to encourage local involvement. Furthermore, the systems of pricing carbon must be implemented to encourage SAF production using agricultural residues and MSW to be more economical. Also in terms of policy, there is the need to promote waste-to-fuel pathways, which can properly incorporate waste biomass into the SAF supply chain. The conversion technologies should be given tax incentives regarding research and development so as to speed up the development of SAF. The future research ought to touch on the socioeconomic impacts of the SAF feedstock sourcing on the local communities and the rural economies and the policy consequences of encouraging SAF on the national and regional levels. In addition, primary data gathering of stakeholders in the industry is required to determine the dynamics of the SAF market and supply chains in feedstock in real time. Longitudinal research would also be useful to determine how the economic viability of the SAF production can be affected by the disruption of markets like global fluctuation of prices or technological innovation. Lastly, the study of regional differences in sourcing SAF feedstock within China may offer a more detailed insight into the local challenges and opportunities related to the SAF industry, which would allow customizing solutions to be specific to the various regions in the country (Searle and Malins, 2023; Zhang and Li, 2023).

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.