Abstract

Achieving the European Union’s recycling targets requires a substantial expansion of separate collection, for which municipal waste charges (MWCh) may play a dual role by financing local services and shaping behavioural incentives. This article provides a descriptive longitudinal assessment of MWCh in Spain, a relevant case for countries and regions transitioning from predominantly flat charging systems towards more incentive-oriented models under increasingly demanding recycling and cost recovery requirements. The analysis draws on the fiscal ordinances for 2015 and annually for 2018–2024 of 131 municipalities, covering 33.7% of the Spanish population in 2024. It combines qualitative profiling of charging systems, quantitative benchmarking of household and business fees, estimation of cost coverage using the national budget database for local entities, and a nationwide mapping of pay-as-you-throw (PAYT) schemes. The results show that flat fees continue to predominate for households, whereas fee modulation, where present, remains only weakly related to waste generation or source separation. Cost coverage also remained incomplete, with an estimated value of 52.6% in 2023. PAYT diffusion was still limited: by 1 January 2025, 39 municipalities had adopted PAYT, covering about 1.4% of the Spanish population. More broadly, the Spanish case highlights the challenge of reconciling cost recovery, behavioural incentives and distributive fairness in local waste charging.

Keywords

Introduction

Municipal solid waste (MSW) management remains a central issue in the European Union (EU) environmental agenda, given its links to circular economy objectives, climate change mitigation, and the prevention of marine litter (Bayar et al., 2021; Gautam and Agrawal, 2021; Oosterhuis et al., 2014; Tisserant et al., 2017).

In this context, the EU Waste Framework Directive (Directive 2008/98/EC; hereinafter WFD) has established increasingly demanding recycling targets for municipal waste: 50% by 2020, 55% by 2025, 60% by 2030, and 65% by 2035. Additional targets also apply to specific waste streams such as packaging, paper and cardboard, and glass. Spain already failed to meet the 2020 municipal recycling target and remains at risk of missing the 2025 target (European Commission, 2023). Achieving these levels requires a substantial expansion of separate collection, for which economic, fiscal, and regulatory instruments are highly relevant (Dubois and Eyckmans, 2024; European Topic Centre on Waste and Materials in a Green Economy and European Environment Agency, 2022; Eurostat, 2025; Sastre et al., 2018; Watkins et al., 2012).

Among these instruments, municipal waste charges (MWCh) are especially relevant because they not only finance waste services but may also shape the incentives faced by households and businesses. If properly designed, MWCh can help operationalise two core principles of EU environmental policy: the polluter-pays principle and the waste hierarchy. International literature suggests that charging systems linked to actual waste generation may provide stronger incentives for waste prevention and source separation than flat-rate schemes, although their performance depends heavily on tariff design, local service organisation, treatment infrastructure, and public acceptance (Beccarello and Di Foggia, 2022; Cheng et al., 2022; Emmanouil et al., 2022; OECD, 1972; Rizzo and Secomandi, 2024; Romano and Masserini, 2023; Svatikova et al., 2025; Taylor, 2000; Ukkonen and Sahimaa, 2021; United Nations, 1992).

Against this background, Spain provides a relevant case study for an international audience. It combines a historical predominance of flat or quasi-flat MWCh, a still very limited diffusion of pay-as-you-throw (PAYT) schemes, and a recent regulatory reform aimed at requiring differentiated local charges and full cost recovery. This combination makes Spain a useful case for examining how municipal charging systems evolve under growing regulatory pressure to improve cost recovery while strengthening incentives for waste prevention and source separation (Alzamora and Barros, 2020; Chamizo González et al., 2018; Law 7/2022, 2022; Puig-Ventosa and Calaf Forn, 2024).

This article builds on previous work profiling MWCh in Spain in 2015 Puig-Ventosa and Sastre, (2017). Its aim is to provide a descriptive longitudinal assessment of the evolution of MWCh in Spain over 2015–2024. Specifically, the article analyses changes in charge design and benchmark fees, examines aggregate cost coverage, and maps the diffusion of PAYT schemes across the country (Puig-Ventosa and Calaf Forn, 2024). PAYT is understood here as any individualised waste charging scheme that links payment to the actual generation of waste, including save-as-you-throw (SAYT) variants.

Causal assessment, including the effects of recent legal reforms or PAYT adoption on waste outcomes, is outside the scope of this article. Rather, the article focuses on documenting institutional and fiscal changes over time and discussing their relevance in light of broader policy and international evidence.

Changes in the Spanish regulatory framework regarding MWCh, 2015–2024

The general legal framework governing how municipal waste collection and treatment services are financed in Spain has already been described elsewhere Puig-Ventosa and Sastre, (2017). However, relevant changes have occurred since 2017 following several recommendations formulated by the European Commission in the compliance assessment exercise carried out in 2014–2015 (European Commission, 2016), and in the early warning reports published in 2018 (European Commission, 2018) and 2023 (European Commission, 2023). In these documents, MWCh were identified as a key tool to increase the separate collection of municipal waste. However, several flaws were identified within the Spanish regulatory framework regarding MWCh: the fact that the financing of MSW services through specific charges such as MWCh was not mandatory, and that, where they were in place, full cost coverage was not mandatory either. Furthermore, implementing PAYT schemes instead of flat rates has been repeatedly recommended.

These issues were partly addressed through Law 7/2022 of 8 April on waste and contaminated soils for a circular economy, which transposed the WFD. Article 11 establishes that, in accordance with the polluter-pays principle, local entities must introduce, within 3 years of the entry into force of the law, a differentiated charge or, where appropriate, a compulsory non-tax public levy ensuring full cost coverage for local waste management services. The law also states that the charging system should allow the implementation of PAYT schemes and may incorporate differentiation or reductions linked, among other aspects, to home or community composting, participation in separate collection systems, and situations of social vulnerability.

For the purposes of this article, the two main regulatory changes are, first, that MWCh became mandatory in Spain from 10 April 2025 and, second, that these charges must ensure full cost coverage. The law also allows and encourages the implementation of PAYT schemes, although it does not make them mandatory.

Literature on MWCh in Spain

A literature review on MWCh in Spain until 2017 was already carried out elsewhere Puig-Ventosa and Sastre, (2017). Since then, several works have further explored this field. Alzamora and Barros (2020) analysed Spain together with 17 other countries worldwide to characterise charging systems and the existence of PAYT schemes among other relevant variables. Spain was profiled as having predominantly flat rates.

Xevgenos et al. (2015) included three Spanish municipalities as examples of successful PAYT and door-to-door collection experiences (e.g. Hernani, Verdú, Argentona).

Chamizo González et al. (2018) analysed 52 Spanish provincial capitals in order to assess whether MWCh complied with the polluter-pays principle, using a dataset covering the period 2009–2014. Their results confirmed that PAYT was infrequent and that flat fees were the most common charging system.

Weber et al. (2019) analysed unit pricing schemes, including PAYT, in four Spanish municipalities, linking the instrument to improved separate collection as well as to questions of environmental justice and grassroots local initiatives. In turn, Puig-Ventosa and Calaf Forn (2024) focused on PAYT in Spain, concluding that fewer than 1% of municipalities in Spain had such schemes in place, covering a very small share of the Spanish population.

However, the available scientific literature remains fragmented. Existing studies either provide a 1-year profile of MWCh, focus on selected successful municipalities, analyse a restricted subset of large cities, or concentrate specifically on PAYT deployment. A nationwide longitudinal assessment of changes in tariff design, benchmark fees, cost coverage, and PAYT diffusion over 2015–2024, in the context of recent regulatory reform, is still lacking. This article addresses that gap by providing a structured longitudinal dataset on municipal waste charging systems in Spain, a benchmarking exercise of cross-municipality heterogeneity in tariff design, cost coverage and PAYT diffusion, and a descriptive basis for future policy evaluation studies.

Methods

This study adopts a descriptive longitudinal approach to examine the evolution of MWCh in Spain for 2015 and 2018–2024. The analysis is based on the yearly review of the fiscal ordinances regulating local waste collection and/or treatment, compiled in a database for a panel of between 125 and 131 municipalities covering all Spanish Autonomous Communities.

The methodological approach combines four components. First, MWCh were profiled using a set of qualitative variables describing their main institutional and design features. Second, a quantitative benchmarking exercise was carried out for an average household and for a predefined set of commercial activities, in order to calculate comparable annual fees across municipalities and years. Third, in view of the regulatory requirement of full cost coverage introduced by Law 7/2022, the costs of municipal waste management and the revenues from MWCh were compared using the Database on Budget Data of Local Entities published by the Spanish Ministry of Finance and Public Administration. Fourth, PAYT schemes in Spain were separately mapped and profiled. Causal assessment, including the effects of recent legal reforms or PAYT adoption on waste outcomes, is outside the scope of this article. The study is designed to document institutional and fiscal changes over time rather than to identify policy effects.

Sampling approach

The empirical analysis is based on a longitudinal panel of municipalities derived from the sample used in Puig-Ventosa and Sastre (2017). That original sample was deliberately maintained in order to preserve comparability with the previous study and to support a consistent assessment of changes in municipal waste charging ordinances over time.

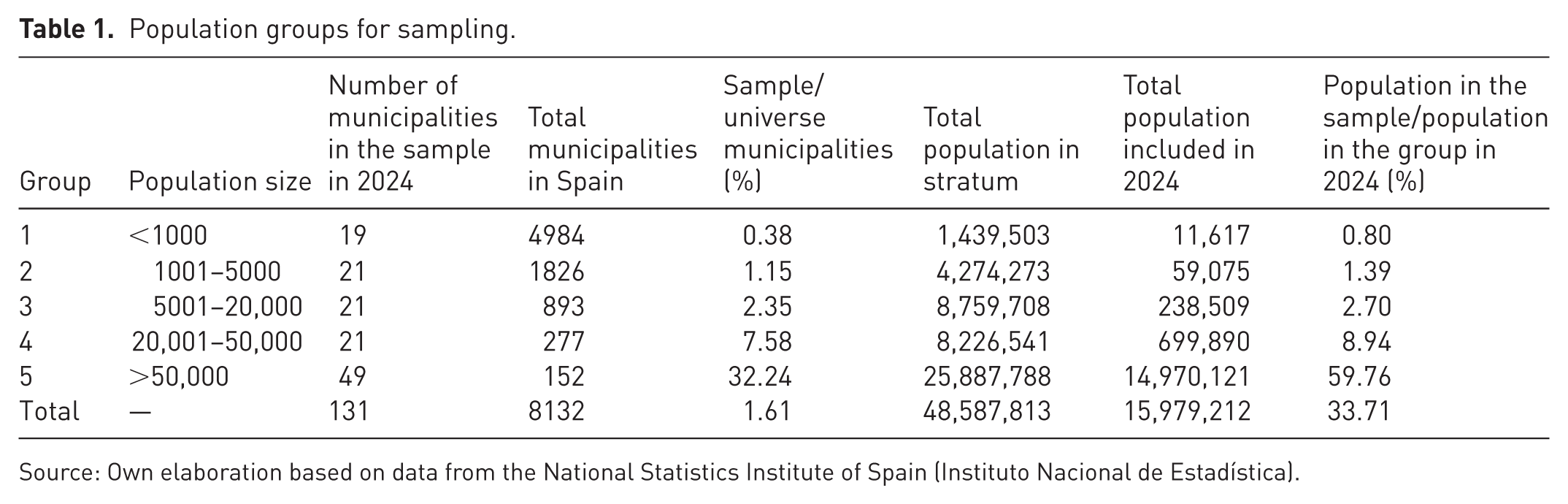

An initial sample of 125 municipalities was divided into 5 groups according to their population size (Table 1). Sampling was designed to include all provincial capitals plus at least one municipality from each autonomous community (AC) in each population size group. During the period analysed, the sample was gradually expanded to 131 municipalities in order to preserve the analytical structure by population groups when some municipalities crossed group thresholds as a result of demographic changes.

Population groups for sampling.

Source: Own elaboration based on data from the National Statistics Institute of Spain (Instituto Nacional de Estadística).

The purpose of the sample is not to provide statistical representativeness of the approximately 8132 Spanish municipalities. Rather, it was designed as a structured panel for ordinance-based longitudinal comparison, combining territorial coverage across all AC with the inclusion of municipalities of different population sizes. This design gives a comparatively broad view of municipal charging configurations over time. The spatial distribution of the municipalities included in the panel is shown in Supplemental Figure S1.

In 2024, the sample covered 15,979,212 inhabitants, equivalent to 33.7% of the Spanish population. Population coverage is especially high in the largest population group, while much lower in the smaller groups. Accordingly, the results should be interpreted as descriptive evidence from a selected longitudinal panel of municipalities, not as nationally representative municipality-level estimates. Given the greater population coverage of larger municipalities and the inclusion of all provincial capitals, some observed patterns may reflect the characteristics of larger and more administratively structured municipalities more strongly than those of the full municipal universe.

Groups 1, 2, and 3 initially included 19 municipalities each in 2015 and reached 19, 20, and 21 municipalities, respectively, in 2024. These municipalities were selected by ensuring territorial coverage across the 17 AC and adding a small number of additional municipalities chosen from the remaining candidates within each group. Group 4 originally included the provincial capitals within that population range together with municipalities selected from the remaining eligible candidates, and one additional municipality was later incorporated due to population changes. Group 5 is formed by the 49 provincial capitals within this population size group.

Qualitative variables

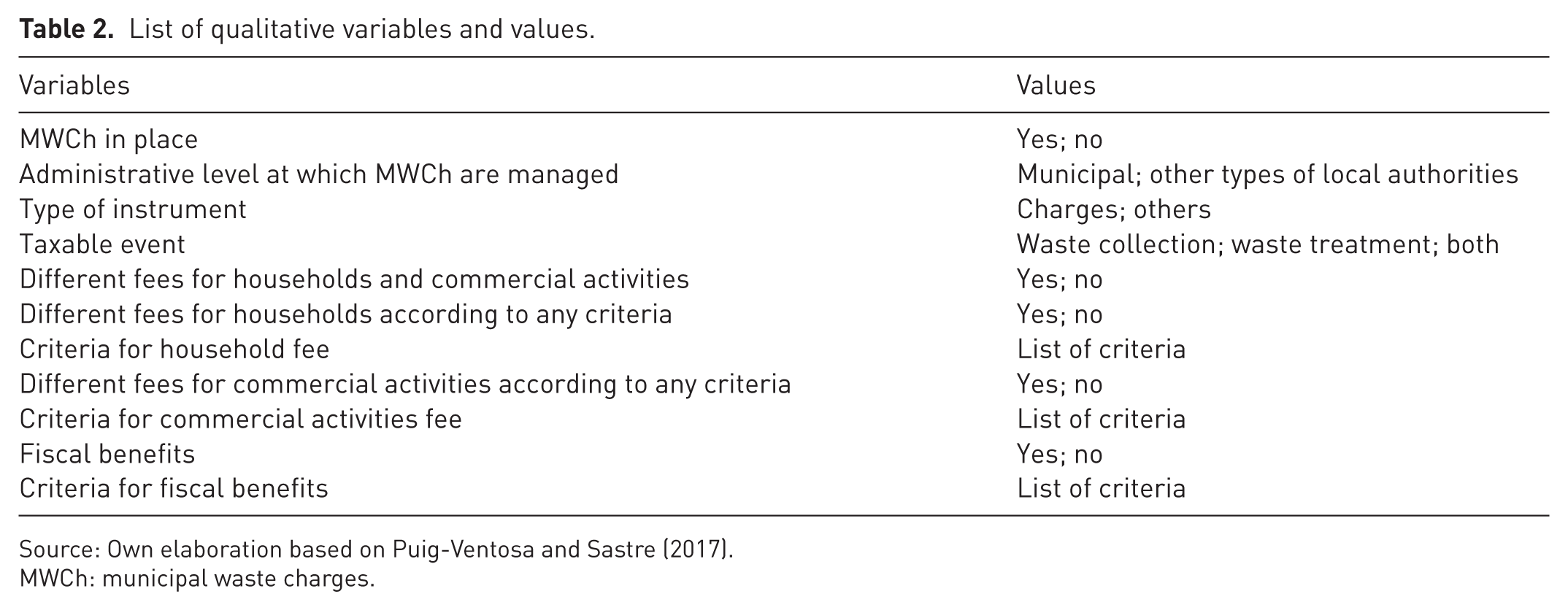

The qualitative variables defined in Puig-Ventosa and Sastre (2017) were recorded. These cover 11 analytical categories related to the main features of MWCh in Spain, which were coded as variables adopting several possible values and registered in a database (Table 2).

List of qualitative variables and values.

Source: Own elaboration based on Puig-Ventosa and Sastre (2017).

MWCh: municipal waste charges.

Quantitative variables

The quantitative analysis was carried out separately for households and for a set of predefined commercial activities, building on the categories defined in Puig-Ventosa and Sastre (2017).

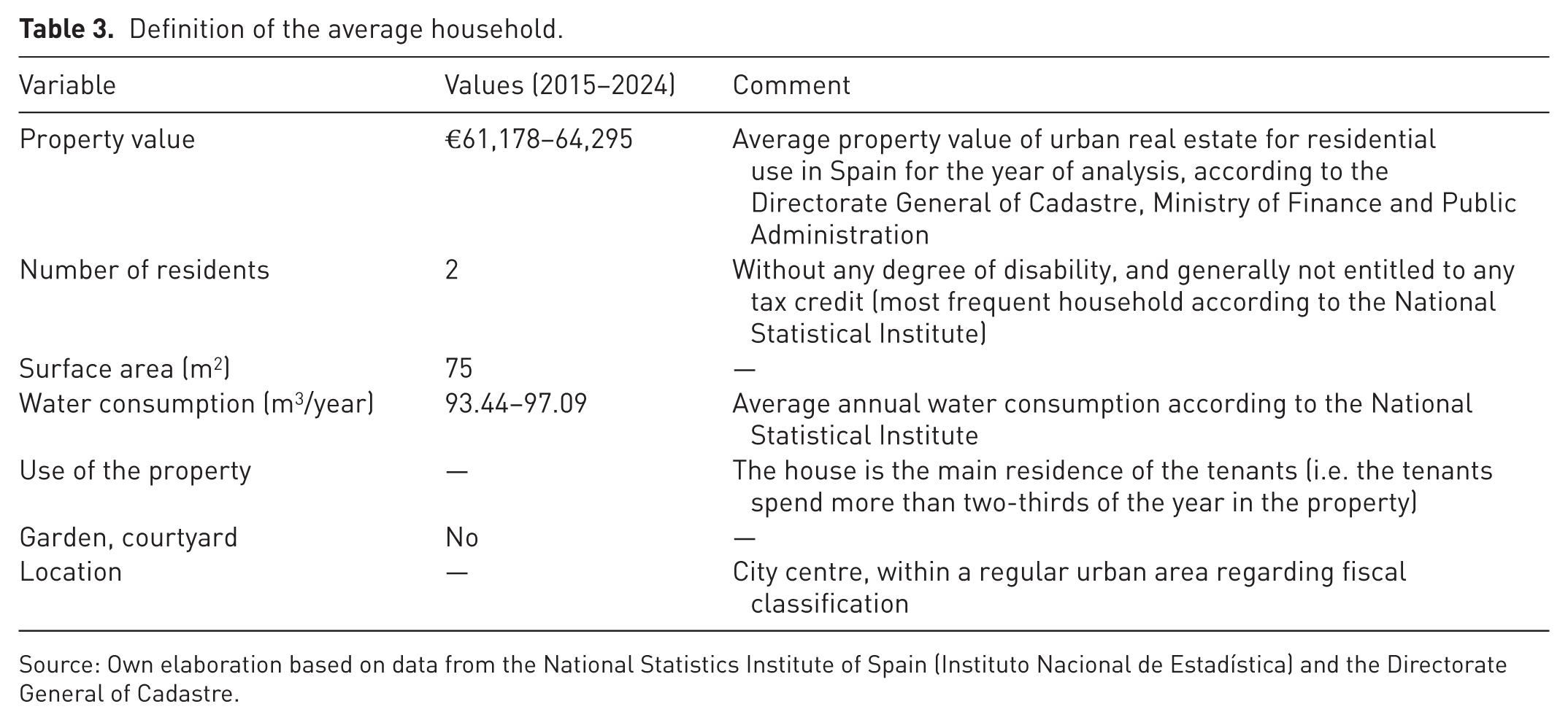

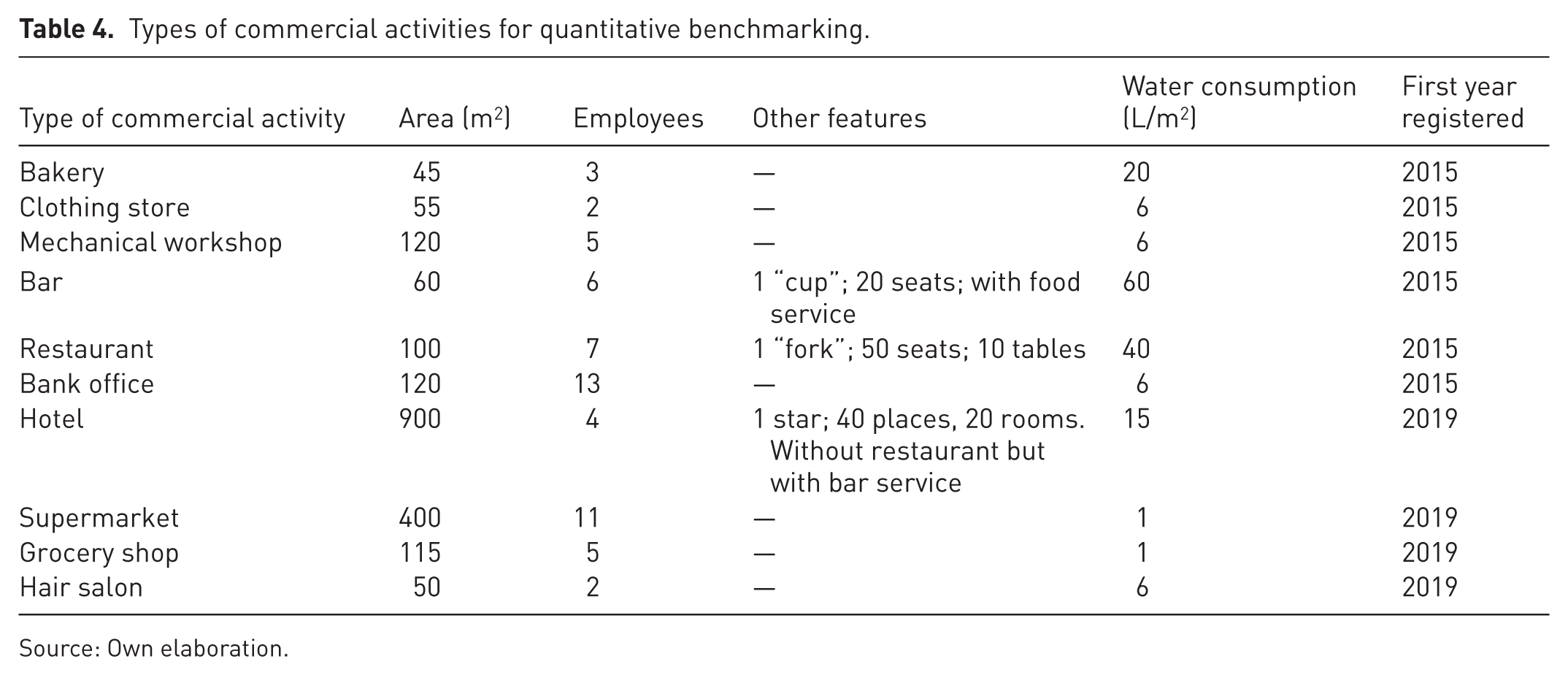

Households were approached by defining an average household with regard to key variables (Table 3). Commercial activities were addressed through the definition of several types of common commercial activities (Table 4). The types of commercial activities were expanded in 2019 to include hotels, supermarkets, grocery shops and hair salons since then.

Definition of the average household.

Source: Own elaboration based on data from the National Statistics Institute of Spain (Instituto Nacional de Estadística) and the Directorate General of Cadastre.

Types of commercial activities for quantitative benchmarking.

Source: Own elaboration.

Based on the specifications laid down in the corresponding fiscal ordinances, the applicable fees for the average household and for each type of commercial premises were individually calculated for every municipality in the sample and recorded in a database.

Cost coverage

Cost coverage was estimated by comparing the costs of waste collection and treatment with the revenues of MWCh from the Database on Budget Data of Local Entities (CONPREL), published by the Spanish Ministry of Finance and Public Administration. Although this database has some limitations discussed in Puig-Ventosa and Sastre Sanz (2023), it remains the only source allowing this estimate on a nationwide basis.

Mapping PAYT schemes

Considering the limited number of experiences of PAYT schemes among Spanish municipalities, a specific mapping was carried out to estimate the population already subject to unit pricing and its evolution over time.

Since there are no official sources addressing the application of PAYT in Spain, the compilation was carried out based on technical literature review and consultation with municipal officers. PAYT is understood here in a broad sense, including SAYT schemes and other individualised charging variants. The resulting database cannot therefore be considered official and may not capture all municipalities applying PAYT. It covers municipalities that were operationally applying PAYT, as well as municipalities that had applied it in the past, up to 1 January 2025. According to the Catalan Waste Agency (personal communication), the number of municipalities approving PAYT schemes in Catalonia increased significantly during 2025. However, those recent developments fall outside the temporal scope of this article.

Results

Qualitative variables

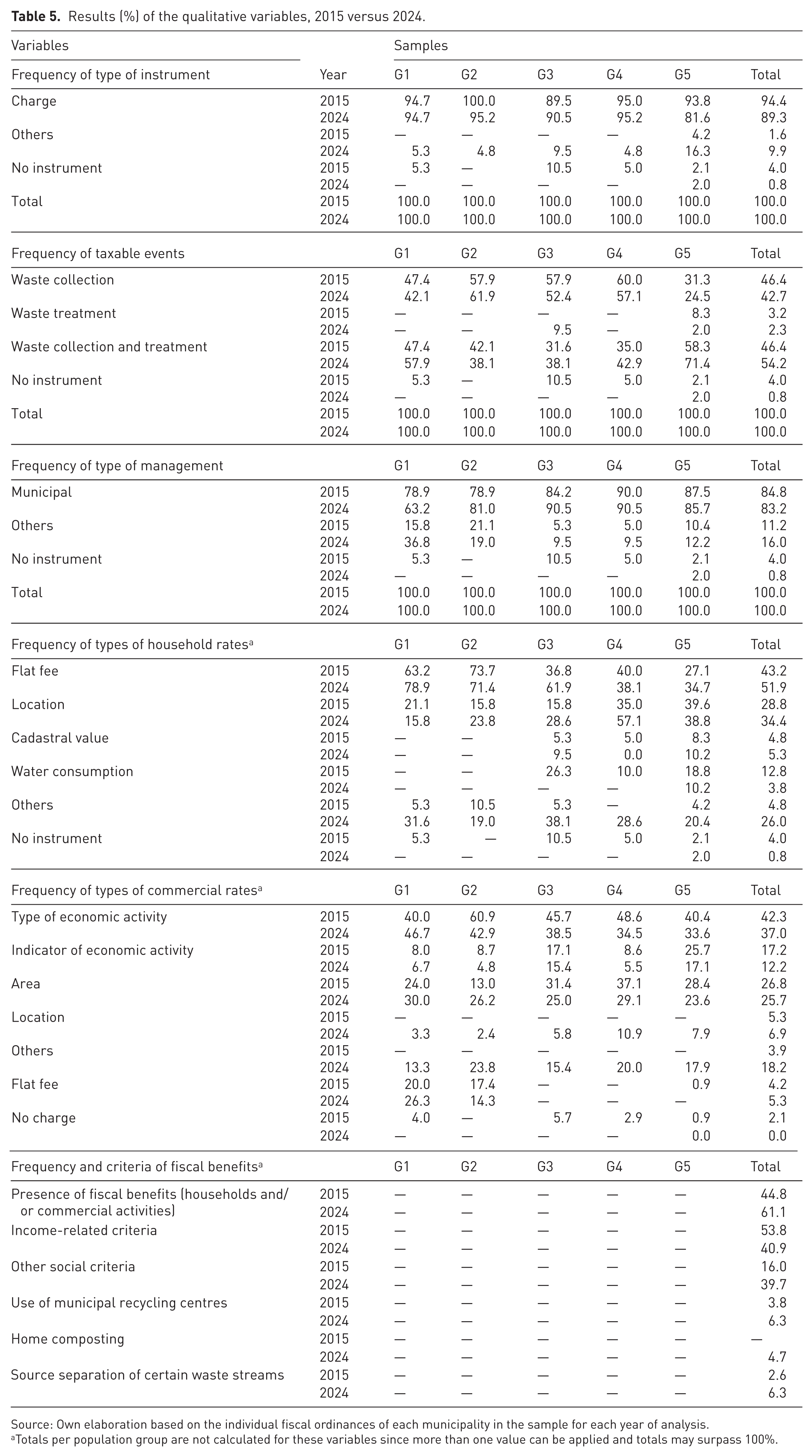

The comparison between the results for the qualitative variables in 2015 and 2024 is shown in Table 5. The share of municipalities covered by MWCh and other types of fees related to waste management grew between 2015 and 2024. Only 0.8% of the sample was not covered by any fee in 2024, whereas in 2015 this proportion was 4.0%. In fact, the whole of the sample except one municipality in G5 had some kind of fee in 2024. Charges remained the most common instrument (89.3%) although there was a significant increase in the frequency of other types of instruments such as public prices (“precios públicos”), and combinations of these and charges.

Results (%) of the qualitative variables, 2015 versus 2024.

Source: Own elaboration based on the individual fiscal ordinances of each municipality in the sample for each year of analysis.

Totals per population group are not calculated for these variables since more than one value can be applied and totals may surpass 100%.

The taxable event defines the services for which the charge is levied, either waste collection or treatment, or both. Therefore, unless both collection and treatment are included within the taxable event, there will be costs out of the scope of the charge that should be financed by other sources of revenue. The overall trend was an increase in the frequency of municipalities including both concepts, from 46.4% in 2015 to 54.2% in 2024, which was sharper in G5 (71.4%). However, it was still common for charges to cover waste collection only (42.7% of the sample in 2024). In some cases, the taxable event as formally stated in the ordinance may not fully coincide with the actual scope of the charge.

MWCh continued to be mostly managed by municipalities themselves in 2024 (83.2%). The proportion of municipal management was lower in G1 (63.2%) than in the other population groups.

Regarding household fee modulation, little has changed between 2015 and 2024. Flat fees were the most common configuration, particularly in smaller population size groups. Where some type of fee modulation is introduced, the location of the household is the preferred criterion (34.4%), whereas the remaining criteria decreased in frequency between 2015 and 2024.

For commercial activities, modulated fees are preferred over flat fees in all population size groups (92.4%) although flat fees are still present in more than 20% of municipalities in G1. The type of economic activity (37.0%) remained the predominant criterion for modulation although its frequency decreased from 2015. Surface area (25.7%) is also a relevant criterion for modulation. The rest of the criteria had a much lower frequency among which the indicators of economic activity (e.g. sales, number of employees) dropped from 17.2% to 12.2% in 2024.

Tax credits and fiscal benefits applied to households were found in 55.0% of the sample in 2024, and in 61.1% when commercial activities are considered. These figures have grown as compared to 2015 (44.8%). Among social criteria, those related to income remain the most relevant. The use of environmental criteria increased since 2015 although the overall frequency was still low in 2024. The most common environmental criteria in 2024 were related to the correct separation of certain waste streams (6.3%), home composting (4.7%), and the use of recycling centres (6.3%).

Quantitative benchmarking

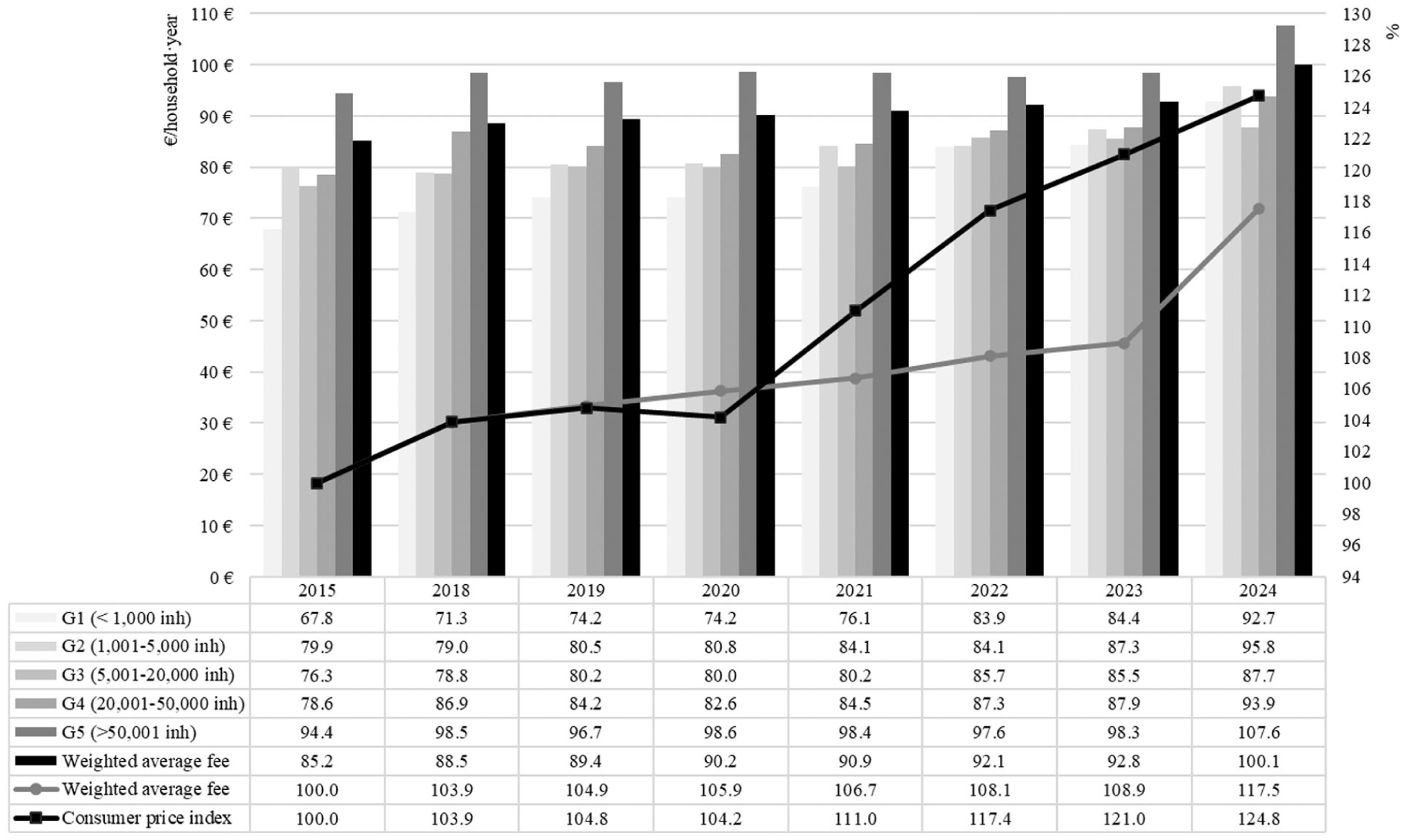

Household fees are presented in Figure 1. The weighted average of the annual fee in 2015 was €85.2 per household, and it increased to €100.1 in 2024, which implies an increase of 17.5% over the period. Compared with the consumer price index for the period (24.8%), MWCh increased less than consumer prices (Instituto Nacional de Estadística, 2024). In fact, from 2021 to 2023, inflation increased much faster than fees. In 2024, by contrast, MWCh fees increased above inflation.

Evolution of household nominal fees in Spain, 2015–2024.

Average fees per household have been consistently higher in the most populated municipalities (€107.6 in 2024, for group G5), whereas the lowest average fees were found in the smallest ones (€92.7 in 2024, G1). In the rest of population size groups, there was no clear relationship between fee levels and population size. Regarding fee levels and inflation per population size group, municipalities under 1000 inhabitants experienced an increase above inflation (36.7%), whereas in the rest of the groups, fee increases were below inflation, particularly in the largest municipalities (13.9%).

Commercial fees have risen in the past 10 years for all categories of commercial activities below inflation except for bakeries, restaurants, and hotels. The pattern in 2024 was similar to that in 2015: high variability across every activity type (see Supplemental Table S2 and Figure S3). Extreme examples of this can be found in hotels in G2 where fees ranged from €21.0 to more than €11,132.0 or bank offices in G5 where they ranged from €51.3 to €5,217.6. Average fees tend to be higher in the largest municipalities compared to the smallest ones although this trend cannot be generalised across population size categories.

The highest average fees in 2024 were found for supermarkets (€791.5 per year) and hotels (€776.4 per year), whereas the lowest average fees were those applied to hair salons (€196.5 per year).

Cost coverage

According to the Spanish Ministry of Finance and Public Administration Database on Budget Data of Local Entities, the most recent data available are for 2023, when overall cost coverage is estimated at 52.6%, which implies a decrease as compared to 2022 (57.7%) and 2021 (59.8%). Costs were €4516 million whereas revenues were €2376 million. Costs increased markedly in 2023 as compared to 2022 (€3947 million). This increase coincided with the first year of implementation of the Spanish landfill and incineration tax, also introduced by Law 7/2022, although the contribution of this factor cannot be isolated.

PAYT in Spain

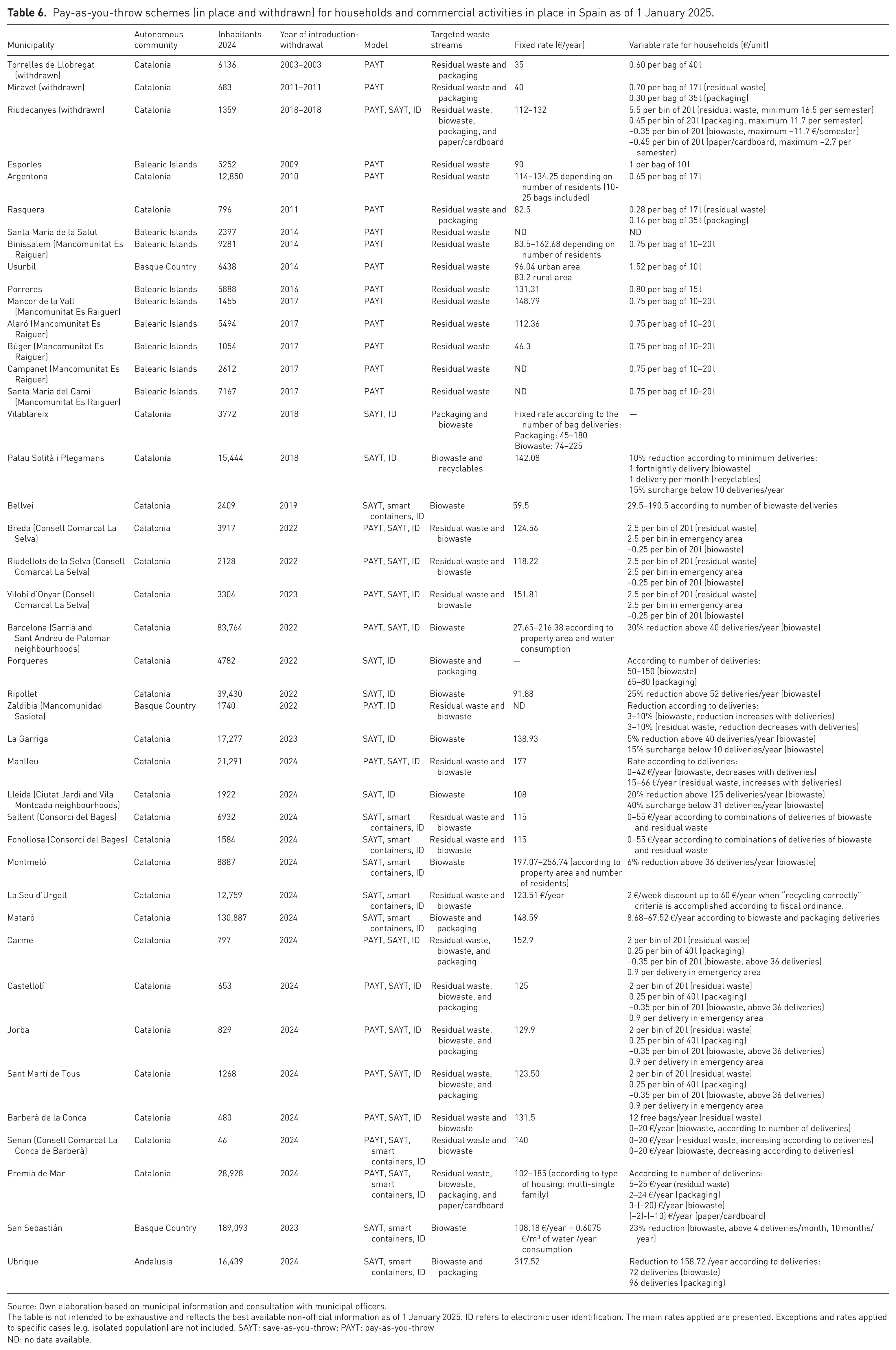

According to the available information, by 1 January 2025, 39 municipalities were applying PAYT in Spain and 3 municipalities had applied PAYT in the past but withdrew it (Table 6). The population covered by these schemes reached approximately 680,000 inhabitants, equivalent to 1.4% of the Spanish population. Most of these municipalities adopted PAYT schemes recently, with 24 municipalities having put PAYT in place from 2022 onwards.

Pay-as-you-throw schemes (in place and withdrawn) for households and commercial activities in place in Spain as of 1 January 2025.

Source: Own elaboration based on municipal information and consultation with municipal officers.

The table is not intended to be exhaustive and reflects the best available non-official information as of 1 January 2025. ID refers to electronic user identification. The main rates applied are presented. Exceptions and rates applied to specific cases (e.g. isolated population) are not included. SAYT: save-as-you-throw; PAYT: pay-as-you-throw

ND: no data available.

The configuration of PAYT schemes in Spain varies across key variables such as the waste streams subject to unit pricing, fee levels, and the specific charging model applied. The resulting diversity reflects the limited but heterogeneous development of PAYT experiences across Spanish municipalities.

Discussion

Since 10 April 2025, Spanish local authorities are legally required to have MWCh in place, and these must reach full cost coverage. A clear description of the situation in 2024 is therefore relevant as a benchmark immediately prior to the entry into force of these obligations. The value of this article lies in documenting the longitudinal evolution of municipal waste charging systems in Spain, benchmarking their heterogeneity across municipalities, and identifying the extent to which current tariff structures remain weakly aligned with cost recovery, behavioural incentives, and the diffusion of PAYT.

As shown above, by the end of 2024, most Spanish municipalities had not embraced major changes in their MWCh design: the dominant pattern remained one of high variability across municipalities, whereas fee levels generally did not ensure full cost coverage.

The available evidence suggests that the practical implementation of the polluter-pays principle remained limited over the period analysed. On the one hand, the low overall cost coverage implies that in 2024, a great share of waste management costs was still financed through other resources. Furthermore, as fee modulation (where present) is generally not related to waste generation, those taxpayers not contributing to the source separation of waste may still be cross-subsidised by those generating less and better separated waste. Flat fees remained the most common charging system. However, although PAYT still has very little presence in Spain, both interest in these schemes and the number of municipalities applying them have increased.

These findings are consistent with the still limited performance of Spain and most of its regions in separate collection. According to the most recent available data (Ministerio para la Transición Ecológica y el Reto Demográfico, 2025), in 2022 Spain collected 26.5% of municipal waste separately, ranging from 54.0% in Navarra to 12.5% in Extremadura. In turn, these collection figures keep Spain at risk of missing the EU recycling target of 55% in 2025, with 42.9% reported in 2022, and 41.4% estimated for 2023. More broadly, the Spanish case fits within an international pattern in which flat or weakly differentiated municipal charging systems continue to coexist with ambitious recycling objectives, whereas more incentive-based schemes such as PAYT remain unevenly deployed (Alzamora and Barros, 2020; Cheng et al., 2022; Di Foggia and Beccarello, 2023). A recent increase in fee levels has been observed, particularly in 2024, although these increases have not been accompanied by significant changes in fee modulation. Where modulation is present, the variables used are only indirectly related to waste generation and separate collection, with the exception of a small number of municipalities with PAYT schemes (Table 6).

Increasing fees in the absence of consumption-related or behaviour-related fee modulation may reinforce the regressive trait of MWCh in Spain – that is, their tendency to impose a proportionally higher burden on low-income households. This tension between revenue adequacy, behavioural incentives, and distributive fairness is also reflected in the international literature on waste charging and PAYT implementation (Drosi et al., 2020; Emmanouil et al., 2022; Ghazaryan et al., 2025; He et al., 2025). In this context, several challenges and opportunities are worth analysing.

Challenges

Although the most relevant barrier identified in 2017 has been overcome, that is, making MWCh and full cost coverage mandatory, the evidence presented here suggests that legal change alone may not be sufficient to alter tariff design in the short term. Unless further specification on fee modulation is introduced, flat fees are likely to remain the most common option in the short term. The implementation of mandatory full cost coverage makes taxpayers immediately conscious about waste management costs. In the coming years, it will be possible to assess whether the recent increase in the perceived cost of waste services prompts taxpayers to advocate for fairer and more equitable charging schemes. It will also be possible to assess whether such schemes are more effective in combining cost recovery, distributive fairness and stronger incentives for separate collection. So far, the descriptive evidence presented here suggests that higher fee levels can coexist with highly regressive charging designs, particularly flat fees, without any clear parallel shift towards stronger fee modulation linked to waste generation or source separation. There are municipalities where higher and close to full cost coverage fee levels were already implemented before Law 7/2022 and flat fees remain in place. A related challenge is dealing with how the total costs of waste management should be shared between households and commercial activities, which adds further complexity to the design of equitable and behaviourally effective charging schemes.

In our view, meeting EU recycling targets in Spain will likely require, among other factors, a much wider deployment of PAYT and other high-performance separate collection systems. However, the present analysis does not allow us to determine whether mandatory adoption would be the most appropriate regulatory route.

Additional challenges include the lack of binding targets for separate collection and/or recycling at local level. This gap entails an unclear allocation of responsibility to individual municipalities in contributing to national and regional targets. Therefore, there is a lack of institutional mechanisms to stimulate the increase of separate collection at local level and related instruments such as PAYT.

A further challenge is the absence, in 2025, of an official and systematic source of information on local waste collection results and charging models in Spain (Autoridad Independiente de Responsabilidad Fiscal, 2023). Although some regions, such as Catalonia, make this information available, there is still no centralised platform where comparable local data can be systematically accessed. These governance and information gaps are consistent with implementation barriers identified in the broader literature, including limited local data, uneven administrative capacity, and weak institutional support for tariff reform (Batista et al., 2021; Cheng et al., 2022; de Sousa Dutra and Siman, 2024).

Opportunities

Among the opportunities associated with the new full cost recovery requirement, higher fee levels may lead to greater taxpayer demand for PAYT. Once fee levels are high enough to increase taxpayer awareness of MWCh and of the possibility of reducing costs by participating in separate collection, the demand for collection and charging systems rewarding participation might increase. This possibility is consistent with international evidence showing that public support for PAYT and related schemes is shaped not only by fee levels but also by perceptions of fairness, transparency, and individual accountability (Emmanouil et al., 2022; Ghazaryan et al., 2025; He et al., 2025; Zhang et al., 2023).

A related opportunity is the degree of legal flexibility currently available to local authorities to implement more incentive-oriented charging systems, including PAYT, SAYT, and more targeted fiscal benefits or reductions.

In addition, the growing practical experience with PAYT and other advanced charging systems suggests that commercial activities may offer a particularly suitable entry point for implementation. A phased approach, beginning with selected economic activities (e.g. large waste generators) and only later extending to households, could facilitate institutional learning and operational adjustment before wider municipal rollout (Alves et al., 2020; Diaz-Farina et al., 2025; Messina et al., 2023).

Finally, the recent implementation of complementary instruments such as the landfill and incineration taxes introduced by Law 7/2022 strengthens the policy rationale for reconsidering how waste management costs are allocated among taxpayers. In this context, the debate is not only about increasing revenue but also about whether cost allocation can be made more transparent, more behaviourally effective, and more consistent with the polluter-pays principle (Abu-Qdais et al., 2023; Di Foggia and Beccarello, 2023).

Limitations and future research

This study has some limitations. Its design is descriptive and longitudinal and therefore does not allow for the identification of causal effects of PAYT adoption or recent legal reforms on waste management outcomes. In addition, the municipal panel was constructed for longitudinal comparison rather than for statistical representativeness of the full universe of Spanish municipalities. In particular, the inclusion of all provincial capitals and the much greater population coverage of larger municipalities mean that some observed patterns may reflect the characteristics of larger and more administratively structured municipalities more strongly than those of the full municipal universe. This is potentially relevant for outcomes such as tariff design, cost coverage, and PAYT diffusion. The PAYT database is based on the best available information and may not capture all existing experiences. Future research could build on improved local data on charging systems, separate collection and waste generation outcomes to support more robust policy evaluation, including panel regressions and difference-in-differences approaches.

Conclusions

MWCh are a key instrument for ensuring sufficient and stable economic resources for the provision of waste collection and treatment services at the local level. In addition, if appropriately designed, they may support waste prevention and separate collection and thereby contribute to progress towards the recycling targets established in the WFD, which Spain is still far from meeting.

This article has presented a methodology to characterise MWCh and has applied it to the analysis of 131 municipal ordinances regulating MWCh over the period 2015–2024. The sample includes all provincial capitals and covers 33.7% of the Spanish population in 2024.

The results show that flat fees remain the most frequent charging system for households, whereas fee modulation, where present, is generally based on variables only weakly related to waste generation and source separation. Environmental fiscal benefits remain infrequent. The average annual fee per household reached €100.1 in 2024, representing an increase of 17.5% since 2015, compared with a 24.8% increase in the consumer price index over the same period. Although 2024 marked the first year in which waste fees increased faster than the CPI, MWCh remained far from full cost coverage.

The regulatory changes introduced through Law 7/2022 create an important window of opportunity, since both the implementation of MWCh and their full cost coverage became mandatory. However, these changes do not in themselves ensure the adoption of charging systems aligned with the polluter-pays principle or the waste hierarchy. More broadly, the Spanish case illustrates a wider challenge faced in other contexts: increasing cost recovery does not automatically imply stronger behavioural incentives, fairer cost allocation, or a wider deployment of PAYT and other high-performance separate collection systems. Without more substantial progress in cost recovery, fee modulation, and the wider deployment of PAYT and other high-performance separate collection systems, the contribution of MWCh to separate collection and recycling is likely to remain only partially realised.

Supplemental Material

sj-docx-1-wmr-10.1177_0734242X261461026 – Supplemental material for Growing fees, modest signals: Evolution of municipal waste charges in Spain (2015–2024)

Supplemental material, sj-docx-1-wmr-10.1177_0734242X261461026 for Growing fees, modest signals: Evolution of municipal waste charges in Spain (2015–2024) by Sergio Sastre Sanz, Ignasi Puig-Ventosa and Maria-Calaf Forn in Waste Management & Research

Supplemental Material

sj-docx-2-wmr-10.1177_0734242X261461026 – Supplemental material for Growing fees, modest signals: Evolution of municipal waste charges in Spain (2015–2024)

Supplemental material, sj-docx-2-wmr-10.1177_0734242X261461026 for Growing fees, modest signals: Evolution of municipal waste charges in Spain (2015–2024) by Sergio Sastre Sanz, Ignasi Puig-Ventosa and Maria-Calaf Forn in Waste Management & Research

Supplemental Material

sj-docx-3-wmr-10.1177_0734242X261461026 – Supplemental material for Growing fees, modest signals: Evolution of municipal waste charges in Spain (2015–2024)

Supplemental material, sj-docx-3-wmr-10.1177_0734242X261461026 for Growing fees, modest signals: Evolution of municipal waste charges in Spain (2015–2024) by Sergio Sastre Sanz, Ignasi Puig-Ventosa and Maria-Calaf Forn in Waste Management & Research

Footnotes

Acknowledgements

The authors wish to thank Pablo Pellicer and Raimon Rafols for their valuable contribution to the update of the municipal waste charges dataset. Their careful data gathering and verification efforts were essential to the development of this study.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The database used in this article was originally built within the project “Las tasas de residuos en España,” which was funded by the Institute for Fiscal Studies (Spanish Ministry of Finance and Public Administration) in 2015.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability statement

Data related to the qualitative and quantitative variables of municipal waste charges are contained in the fiscal ordinances of each municipality included in the sample, which are available online through the corresponding municipal websites. A compilation of these ordinances prepared by the authors is available at: https://fundacioent.sharepoint.com/:f:/g/Eh7wILlB31FEqx0AKlrKEA0BnRM7XN4ySKqDQcfAntJp-Q?e=jypcue. Data on cost coverage were obtained from the Database on Budget Data of Local Entities (CONPREL), published by the Spanish Ministry of Finance and Public Administration, and are available online at: ![]() .

.

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.