Abstract

To improve consumers’ financial decisions, many policy makers support financial education programs. However, some eligible consumers do not participate, limiting program effectiveness. The authors examine a home-buying and mortgage education website offered to more than 6,000 prospective home buyers, documenting differences in take-up (i.e., who decides to participate) and duration of use by consumers’ demographic characteristics, objective knowledge, and subjective knowledge. These analyses rely on a unique data match between surveys measuring consumers’ characteristics and clickstream data tracking website use. The results show that older participants and first-time home buyers are more likely to take up the website, but otherwise there is little relationship between observable demographics and take-up. Consistent with enrichment theory, consumers who are more objectively knowledgeable have higher take-up. However, consistent with “feeling of knowing” research, a one-standard-deviation increase in subjective knowledge is associated with approximately a ten-percentage-point decrease in take-up (controlling for other factors). Subjectively knowledgeable consumers also use educational materials for a shorter duration. The findings add to literature on consumer information search and inform policy makers about consumers’ use of online financial education.

Keywords

To help consumers make informed financial decisions, many policy makers support educational programs to raise consumers’ financial literacy (World Bank 2014). Nevertheless, there is significant debate over these programs (Fernandes, Lynch, and Netemeyer 2014), as there is still “much to learn” about programs’ costs and benefits (Lusardi and Mitchell 2014, p. 37). One issue in measuring the effectiveness of financial education is take-up—that is, who decides to participate—as programs cannot feasibly reach all consumers, and programs that serve only highly literate consumers are likely missing their intended audience. Research that does not account for voluntary differences in take-up can suffer from “selection bias,” wherein results are misleading because participants are not representative of a broader population (see Meier and Sprenger [2013]). Unfortunately, because a significant proportion of the research on financial education programs uses data solely from participants (Collins and O’Rourke 2010), the issue of program take-up remains relatively unexamined. The primary purpose of this article is to determine whether consumers who choose to take up free online financial education differ from those who do not participate in such education efforts, in terms of their demographic characteristics and prior knowledge. To do so, we analyze a unique data set containing survey measures of consumers’ characteristics and self-reported use of financial education matched with website clickstream data capturing their take-up decisions and duration of use.

Correlates of Financial Education Take-Up

Relatively few studies have concentrated on the types of consumers who are willing to take up financial education (Collins and O’Rourke 2010), as many do not collect data on nonparticipants (exceptions include Clark, Lusardi, and Mitchell [2017], Duflo and Saez [2003], and Meier and Sprenger [2013]). Indeed, we are unaware of any previous research explicitly studying take-up of home buying or mortgage education. As such, the closest research may be that examining the characteristics of individuals who seek out investment advice and education (see Bucher-Koenen and Koenen [2012], Kramer [2016], Lin and Lee [2004], and a review in Scholl et al. [2018]). Generally, these studies show that those with higher income and educational attainment are more likely to take up investment advice. Expanding this research into financial education, we ask: RQ1: How does use of a financial education website correlate with consumers’ demographic characteristics?

Relationships Between Objective Knowledge, Subjective Knowledge, and Information Search

To understand take-up of financial education beyond demographic characteristics, we draw on theoretical literature describing the relationship between prior knowledge and take-up of consumer product information (e.g., Klein and Ford 2003; Park and Lessig 1981). Starting with Brucks (1985, p. 2), researchers interested in prior knowledge began to distinguish between objective knowledge, defined as “what is actually stored in memory,” and subjective knowledge, or “what individuals perceive that they know.” While these two measures can be highly correlated (Disney and Gathergood 2013; see also Carlson et al. [2008]), Alba and Hutchinson (2000) show that, on average, subjective knowledge is often greater than objective knowledge.

Table 1 shows research examining the relationship between prior knowledge and search for financial education, financial advice, and consumer product information. The first row of Table 1 suggests that, with few exceptions, there is a positive correlation between objective knowledge and information search. In contrast, the second row of the table shows significant disagreement regarding the relationship between subjective knowledge and search, with different researchers finding that this relationship is positive or negative. Finally, the bottom row of Table 1 shows research using proxies for knowledge, such as product experience. These papers also show a mix of empirical patterns.

Literature Examining the Relationship Between Prior Knowledge and Information Search.

a Indicates that the research includes multiple knowledge types and thus appears in multiple rows.

Notes: The classification of knowledge type in this table reflects the authors’ judgment and may deviate from the characterization in the original work. For example, Locander and Hermann (1979) examine “specific self-confidence,” an aggregate rating of how confident people are in their ability to assess goods in a purchase situation. We classify this rating as subjective knowledge. Throughout the literature, search is measured in multiple ways, including how many product attributes consumers examine, the number of questions asked, the number of shops or sellers visited, and time spent searching.

This variety in empirical findings has led to different theories about the relationship between prior knowledge and search, which vary in whether they emphasize the costs or benefits of search (see Stigler [1961]). Research supporting “enrichment theory,” which posits a positive relationship between prior knowledge and search, suggests that having higher objective knowledge allows consumers to more easily process information, and having higher subjective knowledge allows consumers to perceive themselves as skilled processors of information (Johnson and Russo 1984; Ward and Lynch 2019). Either way, reduced processing costs lead to increased search. In contrast, research on the “feeling of knowing” suggests there is a negative relationship between prior knowledge and search (Kramer 2016; Wood and Lynch 2002). Consumers who objectively know more (or subjectively feel that they know more) have less to learn and therefore perceive fewer benefits of searching (Schmidt and Spreng 1996). “Inverted U-shape” theories combine these two lines of thinking. Specifically, consumers with low objective knowledge have limited ability to process information because their knowledge structures are not well-developed, while consumers with high objective knowledge are not motivated to search because they can assess products using preexisting knowledge (Johnson and Russo 1984). For subjective knowledge, those who feel ignorant may be too intimidated to search, while those who feel knowledgeable may believe they do not need to search. As such, only consumers with moderate levels of knowledge will search. Here, we ask: RQ2: How does use of a financial education website relate to consumers’ prior knowledge, as measured by (a) objective knowledge, (b) subjective knowledge, and (c) home-buying experience?

Accuracy of Self-Reported Measures of Search

The majority of research on information search analyzes data from laboratory studies or surveys (e.g., Ratchford, Lee, and Talukdar 2003; Urbany, Dickson, and Wilkie 1989). Unfortunately, it is unclear whether surveys provide an accurate measurement of “search” behavior (Krosnick 1999; Stone et al. 2000). We are aware of only one consumer search study that compared survey and nonsurvey data to examine the accuracy of reported search (Newman and Lockeman 1975). In this study, one of the authors “unobtrusively observed” (p. 218) women shopping at a department store and recorded the number of information sources used and the time spent in the store. A few days later, the authors surveyed the women and asked them to report these measures. Newman and Lockeman (1975) found that the observational search amount was more than double the surveyed search amount, suggesting that surveys may not always be a reliable way to measure consumer search. Therefore, in the current study, we gauge the overall accuracy of surveyed search by asking, RQ3: Do survey and clickstream measures of take-up align and show similar relationships with prior knowledge?

Overview of the Current Research

This study explores use of a financial education website by analyzing data from more than 6,000 prospective home buyers. We examine four topics: (1) the demographic characteristics associated with financial education use (measured through take-up and duration of use); (2) the demographic characteristics associated with objective and subjective mortgage knowledge; (3) the relationships between prior knowledge (objective knowledge, subjective knowledge, and experience) and financial education use; and (4) the relationships between survey and clickstream measures of take-up, including whether they are similarly related to prior knowledge. We contribute to literature on consumer search by analyzing a large sample of participants who search in a natural setting. In contrast, research on the relationship between prior knowledge and search often relies on relatively small studies; the median sample size used in the studies shown in Table 1 is 268 participants. Our analyses provide information on whether the relationship between prior knowledge and financial education take-up is positive, negative, an inverted U-shape, or nonexistent. In addition, we help inform policy discussions on financial education by studying variation in financial knowledge and the characteristics of those who are likely to take up financial education.

Method

Participants

Our data come from a longitudinal study of prospective U.S. home buyers conducted in 2016 (Beckett and Chin 2019). Prospective home buyers were recruited by email from Zillow, a real estate website, and were asked to participate in a government study on home buying. We sent emails to prospective participants in four waves consisting of approximately 385,000, 1,056,000, 2,255,000, and 1,504,000 recruitment emails. In total, 98,872 potential participants responded to these initial invitations. We then screened respondents, with the criteria that they were involved in financial decisions in their household, planning to buy a house in the next three months, and not professionally involved in the real estate industry. 1 The screening procedures retained 23,407 respondents. Of those, 19,394 completed a baseline enrollment survey and were randomly assigned to one of three groups. The current study examines the 6,461 prospective home buyers who were assigned to the “online financial education” group. We retained data from the 6,277 participants who reported key survey measures of subjective and objective mortgage knowledge (see the “Survey Data: Measuring Prior Knowledge and Background Characteristics” subsection) and omitted the remaining participants.

Table 2 displays characteristics of our participants as compared to the 2015 National Survey of Mortgage Originations (NSMO), a nationally representative survey of mortgage borrowers. 2 The table shows that, despite potential differences between prospective home buyers (in our sample) and mortgage borrowers, many sample characteristics are similar. Our study had proportionally fewer participants with a college degree, but more with some college education, and a lower credit score distribution.

Demographic Characteristics of Study Participants and Comparison to the 2015 NSMO.

a Includes respondents who reported being American Indian/Alaska Native or Native Hawaiian/Pacific Islander and respondents who reported multiple race categories.

b Includes associates and technical degrees.

c In the NSMO, credit scores are from Vantage, whereas in our sample they are self-reports. Statistics for the sample do not sum to 100% because participants could report “I don’t know.”

d In the NSMO, home buyers are classified as first-time home buyers (37.1%), investment, seasonal, or relative purchases (7.9%) or repeat home buyers.

Study Background

Study duration and activities

Prospective home buyers first completed an enrollment survey. They were then invited to complete follow-up surveys at two-week intervals until they bought a house or 12 weeks passed (for details, see Beckett and Chin [2019]). Those who missed two follow-up surveys were not invited to the remainder of the study. Among those who enrolled, 72.8% completed the first follow-up survey, and 43.3% missed two follow-up surveys.

At the end of every survey, participants were encouraged to visit a website containing educational material on how to buy a home and acquire a mortgage. The encouragement varied depending on participants’ reported progress searching for a home. Representative language is, “You told us that you’re searching for a home, but don’t quite feel ready to buy. Perhaps you still have questions about the process, or want a better sense of what you’re getting into financially. The Consumer Financial Protection Bureau’s new

After enrolling, participants received a follow-up email thanking them for their participation and reminding them about the website (“In two weeks, we’ll contact you again to see how things are going. In the meantime, check out the Consumer Financial Protection Bureau’s free ‘

Financial education website

The financial education website contained comprehensive information on home buying, including information on mortgage applications, comparing mortgages, and the mortgage closing process. As all participants stated that they were planning to buy a home in the next three months, this information was presented in what financial educators call a “teachable moment,” when it should have been most effective (Kaiser and Menkhoff 2017). Since the time of this study, the website has been updated and improved; thus, our results may not fully reflect current materials.

Clickstream Data: Measuring Take-Up of Financial Education Resources and Extent of Use

We tracked take-up of the financial education website using unique hyperlinks in the survey and emails (see samples in the previous “Study Duration and Activities” subsection). Clicking on these links created a cookie on participants’ browsers that detected future visits to the educational website. To protect participants’ privacy, the cookies did not record any information outside of the educational website, and all cookies were disabled at the end of the study. Furthermore, the clickstream data were anonymous and matched to survey data through a third party. The clickstream data included information on website pages that participants visited, the time when they entered each page, duration on each page, and the activities they performed. We examined take-up and the total time that participants spent on the website, following Couper et al. (2010).

Calculating take-up

We classified study participants who visited the financial education website as having “taken up” the website. Overall, 37% of the study participants took up the website in the first two weeks, and 47% of participants did so in total (Table 3).

Summary Statistics and Correlations Between Primary Measures.

Notes: All correlations are significant at α = .05, with the exceptions of the correlations between duration in the first two weeks (#7) and objective knowledge (#1), and survey data take-up (#6) and subjective knowledge (#2).

Calculating extent of use through duration on website

The website system captured the duration of visits in two ways. Activity within the website, such as navigating from one page to another, was captured precisely using timestamps. In contrast, activity that took participants off the website (including closing the website browser) was only captured through a backup timer. This timer checked for active use after a user entered a page, and it recorded durations of 20 seconds or one, three, five, or ten minutes. There was no record made after 30 minutes without mouse movement. We calculated the aggregate duration of all the pages a participant visited, using the backup timer for pages for which the timestamp values were missing. This calculation means that visits of less than 20 seconds were recorded as 0 seconds long.

Table 3 shows summary statistics on website usage. The distribution of durations was skewed; the median time spent on the website in the first two weeks was 264 seconds, but 11.4% of visitors had durations of 0 seconds. These 0-second durations included users who exited the website after less than 20 seconds and were therefore not recorded by the timer system.

Survey Data: Measuring Take-Up of Financial Education Resources

On all follow-up surveys (i.e., those administered after enrollment, during weeks 2–12), participants reported which of 11 information sources they used to gather general mortgage knowledge, including a “government website.” 4 The specific wording was, “Since we last heard from you, how often have you used the following sources to learn about the mortgage process and the kinds of mortgages generally available?” Participants could indicate how frequently they had used each source (never, once or twice, or three or more times).

Participants who indicated using a government website were directed to a follow-up question asking, “Which government websites did you use to learn about the mortgage process and the kinds of mortgages generally available?” and saw a list of nine possible sources. 5 We classified respondents who reported the Consumer Financial Protection Bureau’s (CFPB’s) website as having taken up the relevant financial education website, “Owning a Home.” This classification may undercount those who visited “Owning a Home,” as participants who did not realize that it was a government website missed the initial question that would allow them to choose this option. The two-step question structure was important for reducing contamination in associated research that required encouraging certain participants to visit that website (Beckett and Chin 2019). Table 3 shows that 6% of respondents to the first follow-up survey stated that they visited the website.

Survey Data: Measuring Prior Knowledge and Background Characteristics

Objective knowledge

Objective knowledge was measured using a 12-item multiple choice scale (for questions and answers, see the Web Appendix). Nine questions concentrated on mortgage knowledge. For example, one question asked, “Typically, if a borrower pays extra toward their mortgage’s principal balance each month, how does that affect the borrower’s total mortgage costs over the life of the loan?” with response options of “The total costs are lower” (correct), “The total costs are the same,” “The total costs are higher,” or “I don’t know.” We designed these questions in consultation with CFPB mortgage experts and subsequently refined them using cognitive interviews (Visser, Krosnick, and Lavrakas 2000) and an online survey with 103 consumers (Beckett and Chin 2019).

Three questions measured general financial literacy (Lusardi and Mitchell 2011). The two scales were originally designed as separate measures; however, factor analysis suggested one factor (eigenvalue = 4.84), and the two subscales were moderately correlated (r = .52, p < .001). As such, we combined the measures, scoring participants’ responses so that they ranged from 0 to 12, before standardizing the values. “I don’t know” responses were coded as incorrect.

Subjective knowledge

Subjective knowledge was calculated as the sum of six multiple choice questions eliciting consumers’ confidence in their ability to evaluate mortgage information and navigate the mortgage lending process (α = .82; for questions and answers, see the Web Appendix). For example, one item asked, “How confident are you that you can tell when a mortgage offer is a bad deal?” with the response options of 0 = “Not at all confident” to 2 = “Very confident.” These questions were designed in consultation with CFPB mortgage experts and informed by research on consumers’ perceived mortgage abilities (Department of Housing and Urban Development [HUD] 2017) and financial skills (CFPB 2017). They were subsequently refined using cognitive interviews (Visser, Krosnick, and Lavrakas 2000) and an online survey with 103 consumers (Beckett and Chin 2019). We used the standardized values in our analyses.

Psychological and economic characteristics

The enrollment survey also collected the following characteristics. Time preferences were measured using a series of two questions that asked respondents to trade off between a smaller amount of money delivered sooner and a larger amount of money delivered later (e.g., “Hypothetically, would you prefer to receive $20 today or $25 in four weeks?”), yielding four groups (for a similar elicitation, see Read [2001]). Risk preferences were measured in a similar way (e.g., “Hypothetically, which would you prefer: a 50% chance of getting $35, or a 100% chance of getting $15?”), resulting in four categories (for a similar elicitation, see Hsee and Weber [1999]). We measured participants’ subjective numeracy using three items from Fagerlin et al. (2007) and internal versus external locus of control using four questions on individual agency (Rotter 1966).

We expected that more patient participants would be more likely to take up financial education (Meier and Sprenger 2013). We did not have hypotheses about the remaining measures, and we used them for exploratory analyses.

Demographic characteristics

At enrollment, participants reported age, race, educational attainment, household income, and credit score (see Table 2). We also asked whether participants had previously bought a home, and, if so, the year of their most recent home purchase (before 1999, 2000–2004, 2005–2007, or 2008 onward). Some literature has used product experience as a proxy for, or separate construct from, objective and subjective knowledge (Table 1). We follow this approach by controlling for home-buying experience in our analyses. Table 3 shows descriptive statistics for our primary measures, including participants’ home-buying experience, and correlations between them.

Analytic Plan

The home-buying study lasted for 12 weeks after enrollment, allowing us to study take-up over 12 weeks. However, our primary analyses concentrate on take-up in the two weeks following enrollment. We emphasize this two-week period for two reasons. First, participants’ behavior affected communications about the website from weeks 2 through 12. Specifically, participants who stopped answering surveys were not encouraged to visit the website as much as those who continued (described in the “Study Duration and Activities” subsection), possibly leading to differences in take-up. Second, researchers have documented “mere measurement” and “panel conditioning” effects, whereby answering survey questions about certain topics can affect respondents’ behaviors and subsequent survey responses on those topics (e.g., Fitzsimons and Morwitz 1996; Halpern-Manners, Warren, and Torche 2014). Both of these factors are mitigated over the first two weeks, when all participants received the same number of reminders to visit the website and answered information search questions only once. 6 We show results for the 12-week study period as robustness checks.

Results

What Demographic Characteristics Are Associated with Financial Education Take-Up?

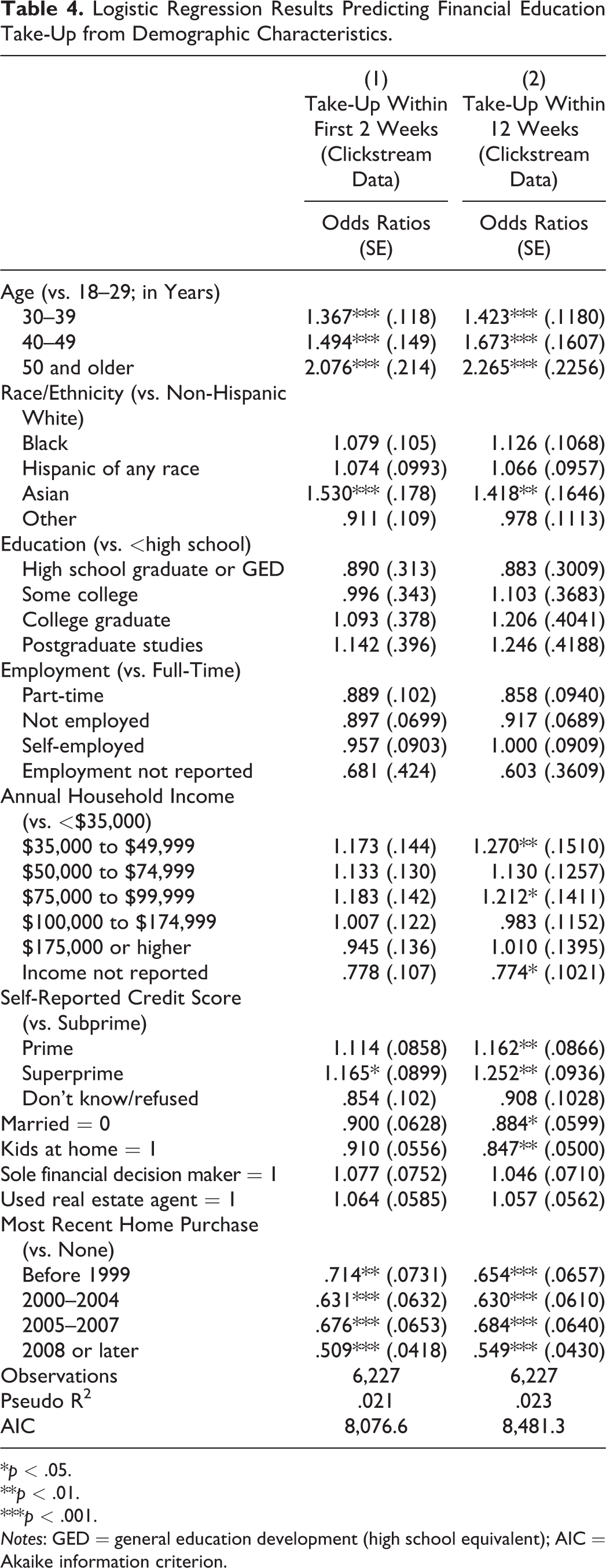

We ran a logistic regression predicting take-up (vs. no take-up) based on demographic characteristics (Table 4). Perhaps surprisingly, the results show that demographics did not generally predict take-up. The exceptions are that, controlling for other demographic characteristics, older participants were more likely to visit the website than younger participants, and Asians were more likely to use the website than members of other racial and ethnic groups. Prior home-buying experience was negatively related to website take-up; the more recent the home-buying experience, the less likely a participant was to use the website.

Logistic Regression Results Predicting Financial Education Take-Up from Demographic Characteristics.

*p < .05.

**p < .01.

***p < .001.

Notes: GED = general education development (high school equivalent); AIC = Akaike information criterion.

Robustness checks

Demographic patterns were consistent when examining take-up over the entire 12-week study (Table 4). The results for this period also show that unmarried participants, participants who had children at home, and participants with lower self-reported credit scores were less likely to visit the website.

What Demographic Characteristics Are Associated with Amount of Website Use?

We ran a regression predicting the number of seconds that participants stayed on the website, using demographic characteristics. Conditional on visiting the website at all and controlling for other demographic characteristics, older participants (age 50+ years) spent less time on the website than younger participants (age 18–29 years) (Table 5). In addition, participants who reported having a real estate agent used the website for a longer time. No other demographic characteristics significantly correlated with the amount of time spent on the website.

Linear Regression Results Predicting Website Visit Duration (Seconds) from Demographic Characteristics.

*p < .05.

**p < .01.

***p < .001.

Notes: GED = general education development (high school equivalent); AIC = Akaike information criterion.

Robustness checks

The second column of Table 5 shows that, when analyzing the 12-week period, participants aged 50 years old and over used the website for a significantly shorter period than younger participants. Furthermore, participants who had purchased a home since 2007 used the website for less time than prospective first-time home buyers.

What Demographic Characteristics Are Associated with Objective and Subjective Mortgage Knowledge?

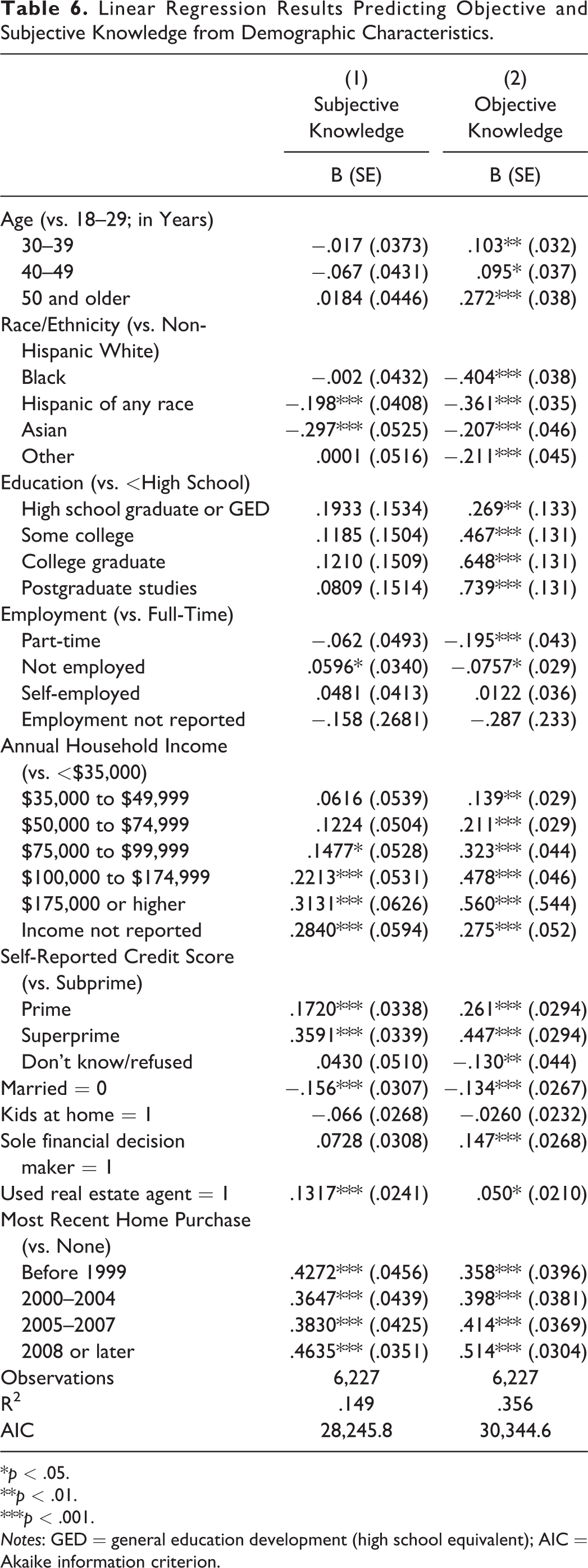

Using linear regressions, we found that both objective and subjective knowledge were positively correlated with income, credit score, being married, having a real estate agent, and prior home-buying experience (Table 6). Age, educational attainment, and being the sole financial decision maker were positively correlated with objective knowledge; however, even though they knew more, these participants did not have higher subjective knowledge. Finally, Hispanic and Asian participants had lower subjective knowledge than non-Hispanic white participants, and non-Hispanic white participants had higher objective knowledge than those from all other groups (Table 6).

Linear Regression Results Predicting Objective and Subjective Knowledge from Demographic Characteristics.

*p < .05.

**p < .01.

***p < .001.

Notes: GED = general education development (high school equivalent); AIC = Akaike information criterion.

What Is the Relationship Between Financial Education Take-Up and Prior Knowledge?

We used a logistic regression to predict take-up in the first two weeks after enrollment (vs. no take-up) based on objective knowledge, subjective knowledge, and home-buying experience, controlling for psychological, economic, and demographic characteristics (see Table 7 and the Web Appendix). This regression provides significantly more explanatory power than one that omits subjective and objective knowledge (likelihood ratio test χ2(2) = 178.78, p < .001). The results show that, after controlling for other characteristics, a one-standard-deviation increase in objective knowledge is associated with an increase in the odds of take-up by 1.29. For a one-standard-deviation increase in subjective knowledge, the odds of take-up decrease by 1.49 (= 1/.67). 7 The results also suggest that participants with home-buying experience were less likely to visit the website than those with no experience, and this difference was largest among those with recent home-buying experience (i.e., who had bought their most recent home in 2008 or later). 8

Logistic Regression Results Predicting Financial Education Take-up.

*p < .05.

**p < .01.

***p < .001.

Notes: AIC = Akaike information criterion. Control variables include all demographic characteristics shown in Table 4, plus measures of risk preferences, external locus of control, subjective numeracy, and time preferences.

An alternative way of understanding these results is to estimate the probability of take-up for consumers with different levels of objective and subjective knowledge (Figure 1). To do so, we model a consumer with average characteristics and apply different levels of objective or subjective knowledge. Because certain knowledge combinations are empirically rare (e.g., no participants have the maximum measured objective knowledge and minimum measured subjective knowledge), we simultaneously adjust both levels of knowledge using sample averages. For example, when calculating take-up for the subjective knowledge score of +1 standard deviation, objective knowledge is set to .4 standard deviations. Figure 1 shows that moving from −3 to +3 standard deviations of objective knowledge predicts an increase in take-up from approximately 23% to 51%, and the same change in subjective knowledge predicts a decline in take-up from approximately 67% to 14%.

Predicted probability of financial education take-up for varying levels of prior knowledge.

To gauge the possibility of an inverted U-shaped relationship between prior knowledge and take-up, we used three methods. First, we changed our regression models to include three levels of absolute objective knowledge (low = 0–4, medium = 5–7, and high = 8–12) and subjective knowledge (low = 0–4, medium = 5–6, and high = 7–12), with cutoffs designed to provide a roughly even distribution of participants across the three categories, following Kiel and Layton (1981). This approach revealed monotonic relationships between take-up and prior knowledge. Second, in a separate model we included both linear and squared terms for standardized objective and subjective knowledge. This approach showed very small coefficients on the squared terms, with varying statistical significance (odds ratio on objective2 = .95, p = .05; odds ratio on subjective2 = .96, p = .07). Finally, we used Lind and Mehlum’s (2010) method, which is similar to that described by Simonsohn (2018), to look for a point at which the slope of a relationship changes signs. This test fails to reject a monotonic relationship between prior knowledge and take-up. Thus, we conclude that there is no inverted U-shaped relationship between knowledge and take-up.

Robustness checks

Controlling for other characteristics, we found that objective knowledge was positively correlated with take-up and subjective knowledge was negatively correlated with take-up over the entire 12-week study period (Table 7, column 2).

What Is the Relationship Between Extent of Financial Education Use and Prior Knowledge?

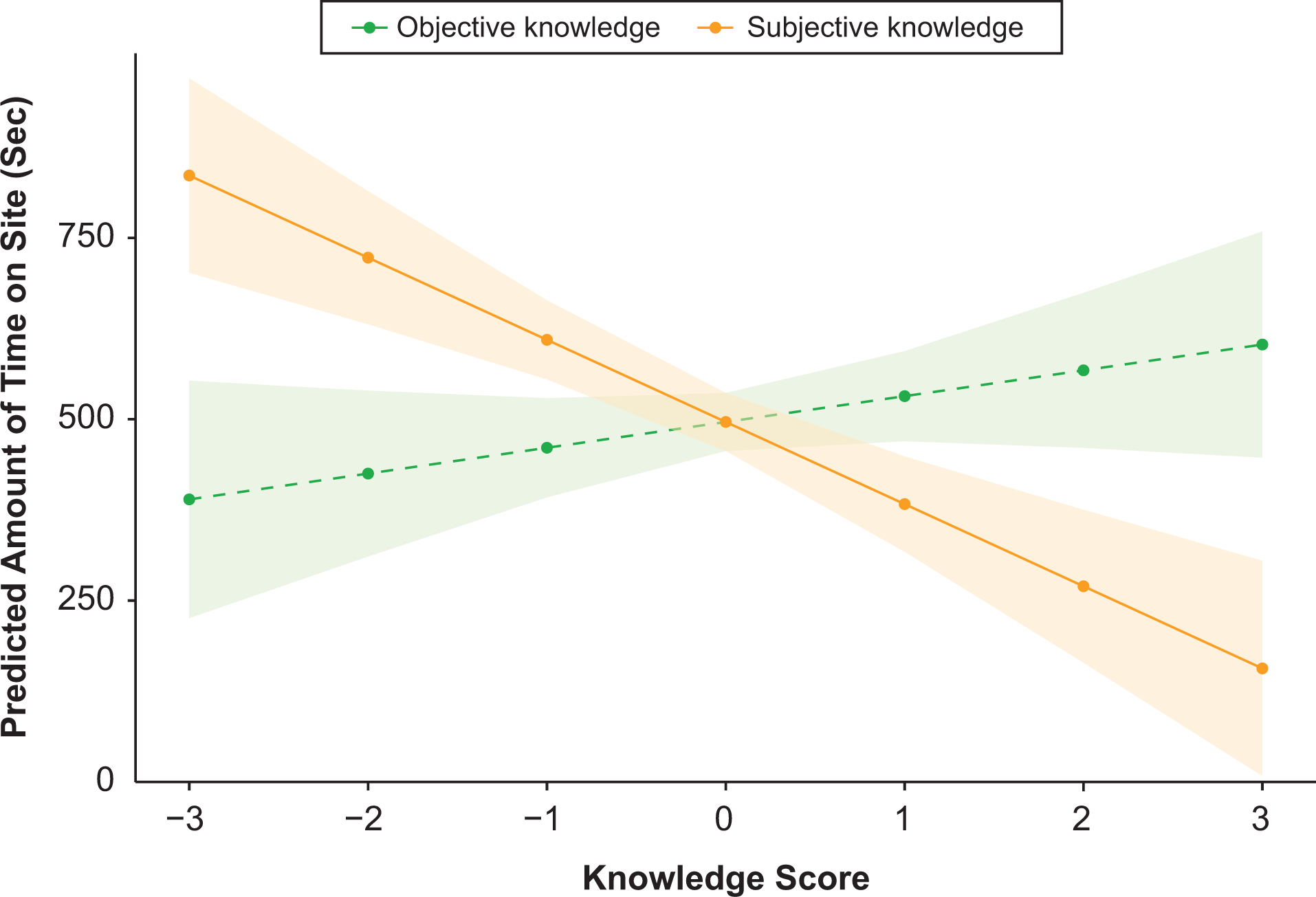

We ran a linear regression on visit durations based on consumers’ objective knowledge, subjective knowledge, and home-buying experience, controlling for psychological, economic, and demographic characteristics (Table 8). This expanded regression provides significantly more explanatory power than one that omits prior knowledge (likelihood ratio test χ2(2) = 13.94; p = .001). The results suggest that, controlling for other characteristics, a one-standard-deviation increase in subjective knowledge is correlated with a 105-second reduction in the time spent on the website, whereas a one-standard-deviation increase in objective knowledge is correlated with a (not statistically significant) 49-second increase. 9 Figure 2 displays the predicted duration of participants’ visits at each level of prior knowledge, using average consumer characteristics and measures of prior knowledge that are updated dynamically.

Linear Regression Results Predicting Website Visit Duration (Seconds).

*p < .05.

**p < .01.

***p < .001.

Notes: AIC = Akaike information criterion. Control variables include all demographic characteristics shown in Table 5, plus measures of risk preferences, external locus of control, subjective numeracy, and time preferences.

Estimated duration of financial education website use (seconds) for varying levels of prior knowledge.

To test for an inverted U-shaped relationship, we used the same three methods as for take-up. Neither the categories of prior knowledge (i.e., high, medium, and low) nor the quadratic terms showed any indication of a U-shaped relationship (B on objective2 = 28.9, p = .23; B on subjective2 = −17.2, p = .43). The test developed by Lind and Mehlum (2010) also failed to reject a monotonic relationship between prior knowledge and duration.

Robustness checks

Using the entire 12-week study period, a linear regression model showed that a one-standard-deviation increase in objective knowledge was associated with a 152-second increase in time spent on the website, while a one-standard-deviation increase in subjective knowledge predicted a 147-second decrease in duration (Table 8, column 2). Prior home-buying experience was associated with a decrease in the time spent on the website; however, the statistical significance of this relationship varied. These results were consistent when accounting for potential measurement error by winsorizing times over 30 minutes or excluding durations recorded by the backup timer (see the “Limitations and Directions for Future Research” subsection).

Do Survey and Clickstream Measures of Take-Up Align and Show Similar Relationships with Prior Knowledge?

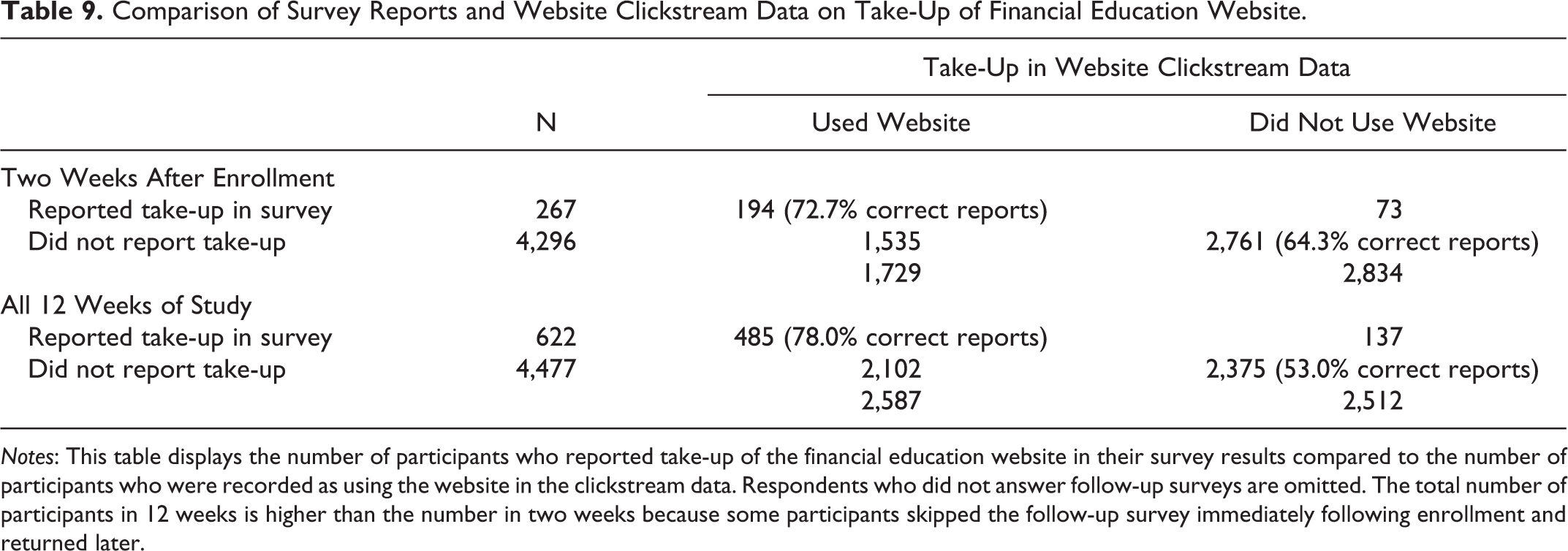

To provide a comparison to prior literature that relies on surveys, we compared survey and clickstream measures of take-up (Table 9). As shown, there is some mismatch between the two sources, as the survey reports (5.9% of respondents in the first two weeks) indicate less use than the clickstream data (37.9%). 10 However, participants who reported visiting the survey were fairly accurate; Table 9 shows that in the first two weeks following the enrollment survey, 267 people reported using the website, of which 194 (72.7%) were located in the clickstream data. Similarly, among the 4,297 participants who did not report using the website, 2,761 (64.3%) were not located in the clickstream data. These patterns mean that there is a positive correlation between the two measures of take-up (see Table 3).

Comparison of Survey Reports and Website Clickstream Data on Take-Up of Financial Education Website.

Notes: This table displays the number of participants who reported take-up of the financial education website in their survey results compared to the number of participants who were recorded as using the website in the clickstream data. Respondents who did not answer follow-up surveys are omitted. The total number of participants in 12 weeks is higher than the number in two weeks because some participants skipped the follow-up survey immediately following enrollment and returned later.

To study the relationship with prior knowledge, we ran a logistic regression predicting reported take-up as opposed to clickstream take-up (Table 7, column 3). As shown, the results were robust across the two data sources. For each standard-deviation increase in objective knowledge, the odds of reported take-up increased by 1.48. For a one-standard-deviation increase in subjective knowledge, the odds of take-up decreased by 1.20 (= 1/.83). Participants with previous home-buying experience were also less likely to report take-up.

General Discussion

Assessments of financial education programs are limited by a lack of research on who decides to take up those programs (Collins and O’Rourke 2010; Lusardi et al. 2014). We examine this issue using clickstream data and self-reported measures of take-up from a large number of prospective home buyers over three months. In doing so, we first explored the relationship between take-up and consumers’ demographic characteristics. Predicting take-up from demographic characteristics alone is difficult, with only age and previous home-buying experience being significantly related. In contrast to research on investment advice (e.g., Scholl et al. 2018), we did not find consistent patterns between take-up and consumers’ educational attainment or household income.

We next explored how consumers’ demographic characteristics related to their prior knowledge, finding that income, credit score, being married, having a real estate agent, and previous home buying experience were positively correlated with both types of knowledge. Education, age, and being the sole financial decision maker were only positively correlated with objective knowledge. Together with our previously reported findings, these results show that younger consumers were both less knowledgeable and less likely to take up the free educational materials offered to them during this study. As such, policy makers may be particularly interested in outreach efforts for younger home buyers. At the same time, certain groups with low objective knowledge, such as first-time home buyers, did take up financial education; these individuals may require less effort to engage.

Third, we explored the relationship between take-up and consumers’ prior knowledge, finding support for two theories. Consistent with “enrichment theory” (Johnson and Russo 1984), consumers with higher levels of objective knowledge are more likely to take up financial education about home buying and mortgage shopping. Consistent with “feeling of knowing” theories (Wood and Lynch 2002), consumers with higher subjective knowledge are less likely to take up financial education and, when they do engage, use it for a shorter amount of time. Consumers with previous home-buying experience, a proxy for knowledge, were also generally less likely to take up financial education. These findings add to literature on consumer search, which continues to debate whether the relationship between prior knowledge and search is positive, negative, an inverted U-shape, or nonexistent (see Table 1 and Jiang and Rosenblum [2014]). Our results are counter to prior null findings (e.g., Kramer 2016) and those suggesting an inverted U-shaped relationship (e.g., Bettman and Park 1980; Raju, Lonial, and Mangold 1995). Furthermore, the effects were large; for instance, moving from lowest to highest objective knowledge approximately doubled the likelihood of visiting the website, while going from highest to lowest subjective knowledge more than tripled the likelihood.

Finally, we examined the relationship between survey and clickstream measures of take-up. Despite some mismatch between the sources on an individual level (Table 9), we found that survey reports of search were a reasonable proxy for actual search, as there was a positive correlation between the two measures, and estimated relationships with prior knowledge were similar across both. This comparison may increase confidence in research that relies primarily on self-reported search behavior, a measurement issue that, to our knowledge, only Newman and Lockeman (1975) have explored.

Limitations and Directions for Future Research

The primary limitation of the current study is that we did not manipulate consumers’ home-buying experience, objective knowledge, or subjective knowledge, and therefore cannot say that changes in prior knowledge cause changes in financial education take-up. With correlational analyses, alternative explanations are possible. For example, consumers who systematically vary in their use of financial education may grow to have different objective and subjective knowledge. To explore such alternatives, research could examine whether the patterns between prior knowledge and take-up are robust when including other (currently unavailable) characteristics, such as maximizer tendencies, need for cognition, or conscientiousness. More directly, research could pursue experiments that manipulate prior knowledge and measure effects on information search. To our knowledge, only Wood and Lynch (2002) have experimented with prior knowledge in this way; consistent with our results, these authors find a negative relationship between subjective knowledge and search.

A second issue is potential measurement error with clickstream data, which comes in at least four forms. First, if a participant cleared their website browser’s cookies and returned to the financial education website without using a customized hyperlink, we would omit the return visit. Second, if a user clicked on a customized link in one browser and returned through a direct visit on another browser, we would not capture their direct visit. Third, users may have skipped the hyperlink altogether and searched for the “Owning a Home” website. In that case, we would have completely missed their website use. Finally, we may have overestimated the duration of use among users who left the website open for an extended period without being present. Each of these issues may cause some noise that could affect our results.

Finally, while our research provides a robust analysis of financial education take-up, it does not examine outcomes such as home or mortgage choice. Engaging in financial education could improve consumer outcomes by helping consumers prepare for closing or identify better mortgage rates. Conversely, education could crowd out other activities, such as talking with real estate agents or lenders about the mortgage process. Research has shown that subjective knowledge may affect financial decision making for outcomes beyond take-up (see Hadar, Sood, and Fox [2013]), making it critical to test financial education programs for a variety of effects.

Policy Implications

Policy makers considering financial education programs may be interested in using our results to inform policy design. In this section, we highlight three themes from this research that may be useful: (1) factors affecting take-up and use, (2) online education, and (3) targeted “just in time” education.

Factors affecting educational take-up and use

To increase take-up, policy makers could experiment with different ways of advertising education, especially among groups that are generally unlikely to engage. Consumers who feel unknowledgeable are more likely to use financial education, raising the possibility that illustrating low subjective knowledge may help increase take-up. If policy makers cannot observe consumers’ subjective knowledge, they could also try to target specific groups. For example, in this study, younger participants had lower take-up rates and therefore may benefit most from additional encouragement.

A second question is how to keep users engaged; in the current research, many website visitors left after fewer than 20 seconds. An initial step could be to analyze clickstream data to understand which areas experience significant drop-off. Policy makers could also test pages to understand users’ reactions and see whether reactions vary across different groups. For example, older adults used the website for a shorter time than younger consumers in this research, so older adults may have different perceptions of usability. Finally, policy makers might draw on other research for ideas about increasing engagement. For instance, they might attempt to increase the number of opportunities that consumers are exposed to educational materials, as repeated exposure to visual displays increases liking, even for financial documents (Chin and Bruine de Bruin 2019; Kunst-Wilson and Zajonc 1980).

Online education

Online education programs are relatively inexpensive to disseminate, with the website here advertised to more than 6,000 prospective home buyers through a single email campaign. By allowing consumers to engage with financial information alone (vs. with an observer present), online programs might also receive more attention (Chin and Beckett 2019). Indeed, we find that online financial education may not be subject to the same demographic selection as traditional programs, as lower-income and less educated respondents show take-up that is statistically indistinguishable from that of higher-income and more educated respondents, all else being equal.

At the same time, online education might also neglect the needs of some consumers, such as those who prefer to have a teacher available to explain financial concepts. Although we cannot speak to this question directly, other research suggests that there is a positive correlation between speaking with others about financial topics and undertaking beneficial financial decisions such as enrolling in automatic savings (Middlewood et al. 2018). Future research should examine whether online programs underserve consumers who prefer these social interactions.

Targeted “just in time” financial education

“Just in time” education (Fernandes, Lynch, and Netemeyer 2014) is designed to be relevant to consumers’ information needs. One practical challenge with targeted education is reaching consumers at the relevant decision point. For our research, we asked prospective home buyers how likely they were to buy a home in the next three months. Without additional experimentation, it is unclear whether consumers need to receive education earlier (e.g., years in advance, to save a larger down payment) or closer to their home purchase. More generally, policy makers might need to think creatively about how to access consumers at the right times. The results here show a weak positive correlation between using a real estate agent and website take-up. As such, real estate agents may be one potential avenue for disseminating education to prospective home buyers.

Conclusions

Efforts to promote financial literacy and informed decision making will be more effective when consumers take advantage of educational resources that are available. By better understanding the psychological and demographic profiles and underlying decision-making processes of those who take up financial education programs, it may be possible to design and distribute financial education materials more effectively.

Supplemental Material

Supplemental Material, jppm.18.105_web_appendix - Take-Up of Financial Education: Demographic Characteristics and Prior Knowledge

Supplemental Material, jppm.18.105_web_appendix for Take-Up of Financial Education: Demographic Characteristics and Prior Knowledge by Alycia Chin and Alanna K. Williams in Journal of Public Policy & Marketing

Footnotes

Author Note

This work was completed primarily when the authors were employed by the Consumer Financial Protection Bureau. However, this article is the result of the authors’ independent research and does not necessarily reflect the views of the Consumer Financial Protection Bureau or the United States. The Public Company Accounting Oversight Board, as a matter of policy, disclaims responsibility for any private publication or statement by any of its economic research fellows, consultants, or employees.

Acknowledgments

The authors thank staff of the Consumer Financial Protection Bureau for their invaluable help in conducting this research, including Megan Thibos, Kelley Holden, Dustin Beckett, Daniel Banko-Ferran, Anirudh Rajashekar, and David Zimmerman. They also thank Wändi Bruine de Bruin, Cäzilia Loibl, Zoe Pham, Suzanne Shu, Eric Van Epps, and seminar participants at the PCAOB, the Cherry Blossom Financial Education Institute, and the conference of the American Council on Consumer Interests for helpful comments on this research.

Associate Editor

Lauren Block

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.