Abstract

A persistent imbalance exists between financial and climate vulnerabilities: Financially vulnerable consumers contribute the least to climate change, yet they suffer the most from its negative impacts, while the opposite is true for wealthier consumers. A conceptual framework formalizes these dueling tensions and acknowledges that increasing available financial resources can reduce consumer financial vulnerability and bolster climate resilience, but it also can encourage more consumption and create larger ecological footprints that accelerate climate change. Consumers experiencing climate-induced harms (economic, food and water access, health, social and institutional) enter a reinforcing feedback loop, such that their recovery from these harms depletes their financial resources, increasing their financial vulnerability in the future. To break this cycle, a stakeholder-centric approach should focus on climate mitigation interventions (reducing ecological footprints) while advocating for increased focus on adaptation interventions (building resilience to anticipated and experienced climate impacts) across macro (public policy), meso (organizations), and micro (consumer) levels. A proposed framework offers guidelines for intervention designs and research opportunities for providing actionable strategies for policymakers, marketers, consumers, and communities. By defining climate change as both an environmental crisis and a social justice challenge, this research highlights its contributions to both financial vulnerability and economic inequality.

Keywords

Average temperatures in the 21st century have been the hottest on record (NASA 2025) and are expected to continue rising in the foreseeable future, getting dangerously closer to a notable threshold: Scientists have warned that at 2°C above preindustrial era levels, catastrophic outcomes are frighteningly possible (Intergovernmental Panel on Climate Change 2023). Climate change has already altered the global climate system, leading to intensified extreme weather events, rising sea levels, diminished crop and dairy production, and worse air and water quality. These trends largely can be attributed to humans’ consumption-related activities (Lynas, Houlton, and Perry 2021): Producing, consuming, and disposing of goods and services generates CO2 and other greenhouse gases beyond what ecosystems can absorb, resulting in a warmer planet. To remain sustainable as a species, humans should be consuming no more resources than the planet can replenish. Instead, at the time of writing, the human population is consuming 1.7 times more resources (Global Footprint Network 2025), an imbalance that will rise to three times more by 2050 if “business as usual” persists (World Wildlife Fund 2012).

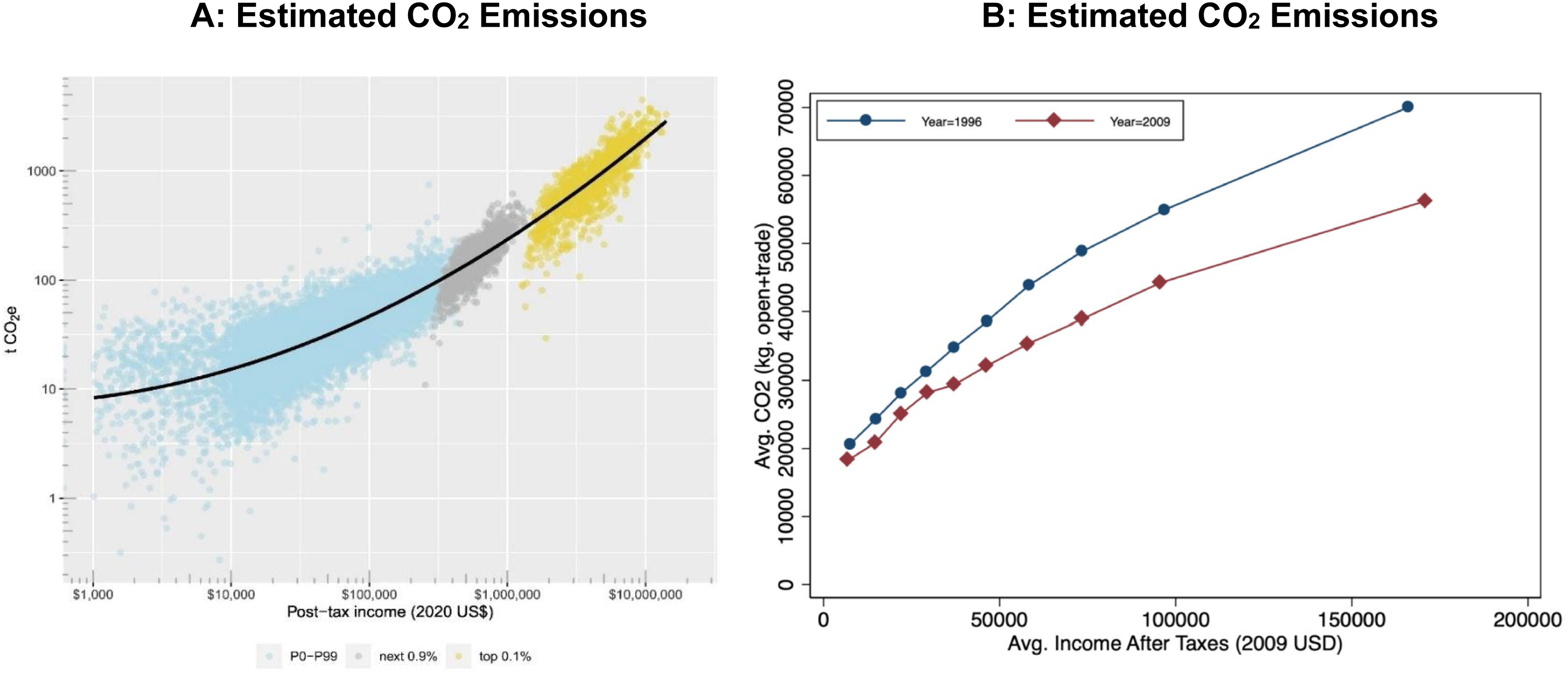

Although all consumers contribute to such climate change outcomes, affluent households tend to consume far beyond their “nature-given budget” (i.e., their share of Earth's biocapacity), whereas financially vulnerable people generally consume less. Yet because vulnerable communities lack the resources to avoid or recover from disasters induced by climate change, they also suffer the most from the negative effects, which threaten where they live, the food they can buy, their healthcare access, and myriad other societal considerations (Parks et al. 2023), thereby exacerbating social inequalities (Gilli et al. 2024). The United States historically has been the biggest emitter of CO2 and contributed most to the climate crisis (Ritchie 2019), but even within that nation, tracing carbon emissions by income levels reveals disproportionate contributions. As Figure 1, Panel A, shows, prior research estimates the wealthiest 10% of U.S. households (by income) generate around 40% of U.S. carbon emissions, whereas the bottom 50% of U.S. households are responsible for only roughly 30% of emissions (Starr et al. 2023). The contrast gets even starker at income distribution extremes; similar imbalances mark other countries too (Chancel 2022). Panel B of Figure 1 illustrates other research (Sager 2019) describing a concave emissions–income relationship, estimating that carbon emissions indeed increase with income, though at a decreasing rate.

Household Carbon Emissions by Income.

In parallel, global data indicate that people living in poverty are systematically more exposed to climate hazards (Winsemius et al. 2016). In the United Kingdom, lower-income communities are more likely to live in high flood-risk areas (Walker and Burningham 2011); in the United States, the poorest one-third of the population accounts for the majority of excess hurricane-related deaths (Parks et al. 2023); and in Bangladesh, lower-income households face higher exposure to the risk of flooding (Brouwer et al. 2007). Lower-income and racial/ethnic minority households also tend to be hit hardest by power system disruptions (Coleman et al. 2023). Such vulnerabilities, when combined with the lost income and spiking food prices that often follow from such hazards, as well as sparse resources to achieve recovery, impose intense burdens on the members of society least able to bear them, for a crisis they did not cause. In short, financial and climate vulnerabilities are deeply intertwined.

In 2015, the United Nations (UN) introduced 17 broad Sustainable Development Goals (SDGs) to guide efforts to address climate change, poverty, and inequality. However, progress toward some goals can come at the expense of others. Achieving Goal 1 (No Poverty) by lifting people out of poverty would enable them to consume more, which may threaten to increase the global ecological effects and thus undermine Goals 12 (Responsible Consumption) and 13 (Climate Action). Such incompatibility raises a key research question: What safeguards can ensure that efforts to reduce financial vulnerability do not translate into concomitant increases in unsustainable consumption, ecological footprints, and climate vulnerability? In seeking an answer, we explore different policies aimed at building climate change resilience among financially vulnerable populations. Although our analyses center on the United States, the resulting insights are broadly applicable to global contexts.

Specifically, we adopt a stakeholder-centric approach to governments, organizations, and consumers. In general, macro-level government policy interventions have the broadest and most lasting impact, followed by meso-level organizational strategies and then micro-level individual behaviors. As prior research suggests, societal and macro-level interventions can be more effective than individual actions, because the global transformations required to combat climate change benefit more from systemic solutions than from individual-level behavioral change (Connolly, Loewenstein, and Chater 2025). Yet such interventions often are delayed by political constraints and polarization (Blanz and Gaitan 2023). Meso-level business strategies instead promise feasible, near-term options, which can be implemented more rapidly than macro-level policies and likely have more impact than consumers’ individual solutions (Nenkov 2024). Accordingly, we prioritize macro- and meso-level strategies while still recognizing the supportive role of micro-level behaviors, reflecting the need for coordinated, multilevel approaches to reducing consumer financial vulnerability (CFV) and strengthening climate resilience, without unnecessarily increasing ecological footprints. 1

With this approach, our research makes three contributions to marketing and public policy literature. First, drawing from the financial vulnerability literature (Salisbury et al. 2023), we propose a theory-driven definition of consumer climate vulnerability (CCV) as the degree to which a consumer or household is at risk of future harm due to climate change, and we address its dynamic interplay with CFV. In proposing a conceptual framework of this intersecting relationship, we conceptualize climate change–induced harm as a multidimensional construct that reflects both direct and indirect effects. Second, we identify four key implications of the proposed conceptual framework, which can guide climate intervention designs and research. In particular, these implications suggest that the most effective climate policies achieve multipronged goals, aimed at reducing both financial and climate vulnerabilities. Third, our stakeholder-centric approach reveals several climate mitigation and adaptation interventions and research opportunities for addressing the intersection of CFV and CCV. In this sense, we add new perspectives on how marketing can foster consumer well-being (Mende and Scott 2021; Nenkov 2024; White, Habib, and Hardisty 2019) and advance the understanding of climate change as both an environmental and a social justice issue (Uenal et al. 2021).

To establish these contributions, we introduce our conceptual framework in the next section, outlining the relationships among financial resources, consumption, CCV, CFV, and climate change–induced harm. Next, we present four key implications of these relationships, before identifying related climate mitigation and adaptation interventions and research opportunities for addressing the goal of lifting up financially vulnerable consumers without increasing future climate change–induced harm.

Conceptual Framework: Linking CFV and CCV

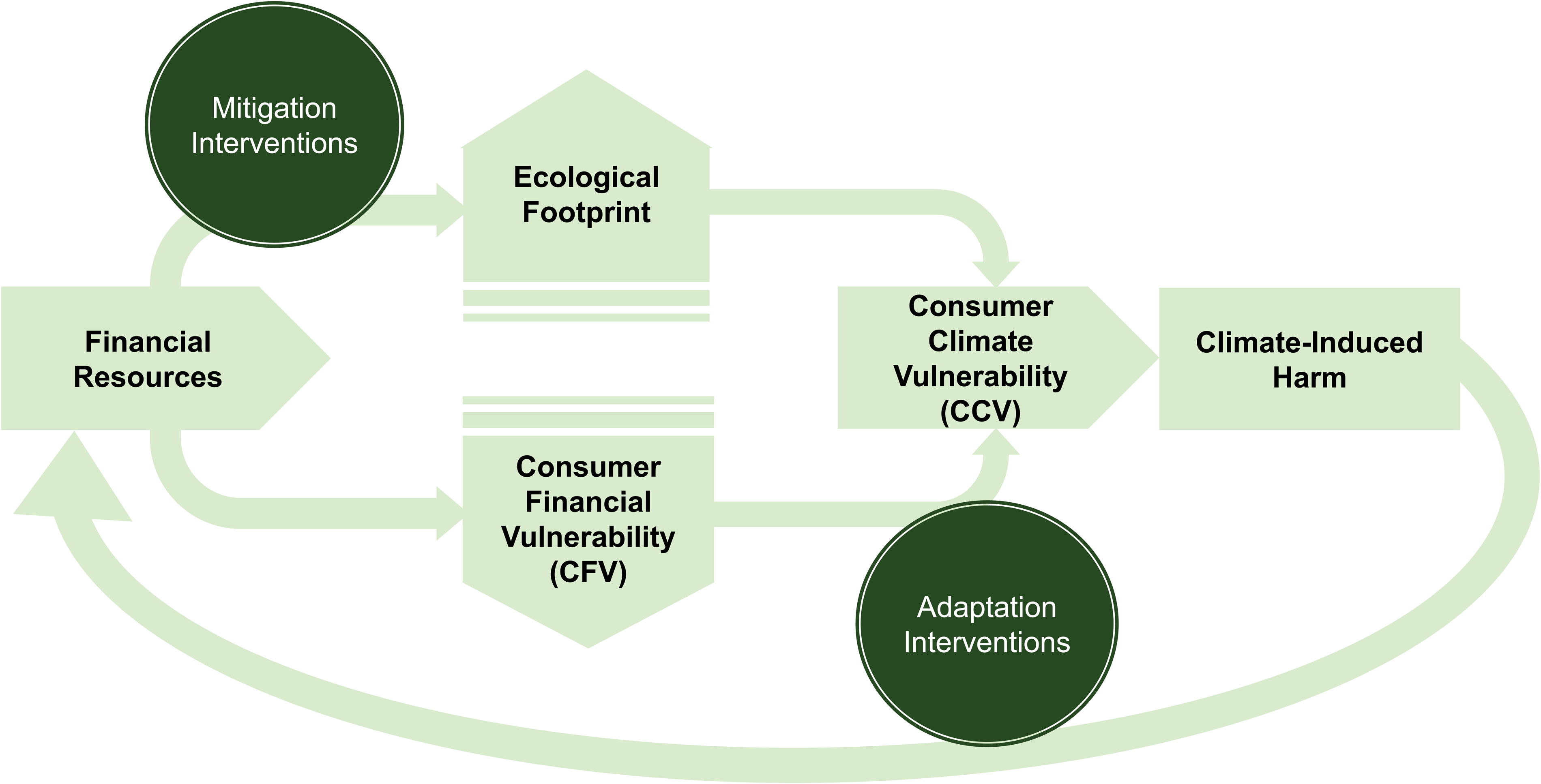

The conceptual framework in Figure 2 illustrates the dynamic, interdependent relationship between CFV and CCV, as well as the key tension it produces: Increasing consumers’ financial resources can reduce their financial vulnerability and climate vulnerability by enhancing their resilience, but it also can increase their climate vulnerability if additional resources support consumption lifestyles that are more resource-intensive and environmentally unsustainable. Higher incomes generally are associated with larger ecological footprints, which refer to the impact each person makes on the natural environment due to their lifestyle (Sager 2019; Starr et al. 2023). Larger ecological footprints intensify climate change trends, heightening the overall risk of climate-related harm. Those experienced harms in turn can deplete consumers’ financial resources and reinforce vulnerability across domains (Ratcliffe et al. 2020). We address each element in this framework in the following sections.

Conceptual Framework.

CFV

Access to financial resources directly influences CFV, or the degree to which a consumer or household is at risk of future harm due to their level of available financial resources (Salisbury et al. 2023). Financial resources can come from multiple sources, such as personal resources (e.g., income, savings, home equity), social capital and relationships (e.g., support from family, friends, churches), financial institutions (e.g., access to credit, homeowners’ insurance, medical insurance), and government institutions and programs (e.g., Medicare, the Federal Emergency Management Agency [FEMA]; Blocker et al. 2023; Salisbury et al. 2023). Consumption choices, including how people allocate their available resources and make spending and saving decisions, influence their CFV. People do not need to be experiencing harm currently to be vulnerable to it. That is, CFV represents the risk of future harm due to the amount and type of financial resources likely to be available (Salisbury et al. 2023). Accordingly, low income is not the only marker of high CFV; for example, inadequate access to affordable credit, or financial resource volatility—as might result from commission-based, gig, and seasonal employment—can also elevate CFV.

Moreover, CFV is dynamic and shifts along a low-to-high continuum, on which every consumer falls somewhere. Consumers can experience financial vulnerability to varying degrees at different points in their lives. Circumstances or events often create inflection points that increase a consumer's CFV (e.g., divorce, job loss, environmental disasters) or diminish it (e.g., inheritance, job promotion, becoming eligible for Medicare). Thus, in addition to investigating how CFV relates to the risk of experiencing climate-induced harm, we account for the capacity of climate mitigation and adaptation interventions to influence these relationships.

Financial Resources, Ecological Footprint, and Climate Change

Greater financial resources indirectly might heighten climate vulnerability, by expanding the ecological footprint associated with consumption decisions. As we noted with Figure 1, both within and across countries, emissions are unequal and disproportionately higher among the wealthy (Chancel 2022). Income has been a key predictor of people's ecological footprint, showing positive correlations with energy use and greenhouse gas emissions (Goldstein, Gounaridis, and Newell 2020). Thus, consumption choices link financial resources to ecological footprints (Nielsen et al. 2024), but as Figure 1 shows, this relationship appears nonlinear (Sager 2019; Starr et al. 2023). When consumers experience high CFV, increasing their financial resources (e.g., Kamakura and Mazzon 2015) can enable them to rise out of poverty and meet basic consumption needs (Viswanathan and Rosa 2010; Viswanathan et al. 2012), which implies a larger ecological footprint through expanded (adequate) consumption (Hill 2002). At moderate and lower CFV levels, consumers have greater flexibility for making consumption choices that increase their ecological footprint only modestly or, as some have argued, could even decrease it (Nielsen et al. 2021; Stern 2017). Yet wealthier households are more likely to leverage global supply chains, which amplify emissions (Feng, Hubacek, and Song 2021), and they shape social and cultural norms for living “the good life” (Nielsen et al. 2021, p. 1013), by signaling status through increased consumption. Moderate-CFV consumers thus might allocate their discretionary income to conspicuous consumption, to emulate wealthier consumers (Charles, Hurst, and Roussanov 2009; Han, Nunes, and Drèze 2010). Access to credit also supports larger homes (Adelino and Robinson 2023) and purchases of status goods (Li et al. 2021). Such status-driven consumption patterns amplify ecological footprints, through greater resource use and carbon emissions (Eufrasio Espinosa and Koh 2024), so they threaten to exacerbate climate change, intensify hazards, and strain adaptive capacity, thereby increasing consumers’ vulnerability to the impacts of climate change.

The CFV–CCV Relationship

CCV stems from sensitivity to climate impacts, balanced with the capacity to anticipate, cope with, or adapt to those impacts. When CFV increases (decreases), an individual or household has less (more) access to financial resources that can reduce the risk of experiencing climate change harms, along with greater (diminished) exposure to climate hazards and weaker (stronger) capacities to cope and adapt (Baker 2009; Campbell 2025). In other words, as CFV increases, so does CCV.

Consumers subject to greater CFV often live in areas that are more susceptible to climate-related hazards, like floodplains or urban heat islands, or near industrial zones where storm damage can trigger toxic releases (Guivarch, Taconet, and Mejean 2021). These communities often are served by aging, substandard infrastructure that is poorly equipped to withstand extreme weather events (Chamlee-Wright and Storr 2009b; Guivarch, Taconet, and Mejean 2021). Affordable housing units may lack proper insulation, storm proofing, or drainage systems, which increases residents’ vulnerability to floods, heat waves, and storms (Adeyemi et al. 2024). Nor do financially vulnerable consumers have ready access to resources to prepare for disasters, evacuate, secure insurance coverage, or support postdisaster recovery (Verschuur et al. 2020). Such vulnerabilities are compounded by systemic barriers to aid and housing, such that climate change–related damage might force people to liquidate essential assets, undermining their long-term resilience and perpetuating loss cycles (Hutton et al. 2022). Due to financially vulnerable populations’ generally high sensitivity to climate-related impacts and limited adaptive capacity, a risk-reinforcing cycle persists.

In contrast, reliable access to resources reduces sensitivity to climate impacts and enhances people's capacity to adapt. Wealthy households might choose to purchase properties in high-risk areas, such as oceanfront locations or wildfire-prone hillsides, because their financial resources grant them a higher risk tolerance (Diosdado et al. 2024; Hutton et al. 2022). For very wealthy consumers, property loss might represent only a minor fraction of their net worth, so they can “take the hit” and rebuild or relocate without major disruption (Markhvida et al. 2020). This contrast underscores how deeply climate vulnerability is shaped by financial vulnerability.

Climate Change–Induced Harm

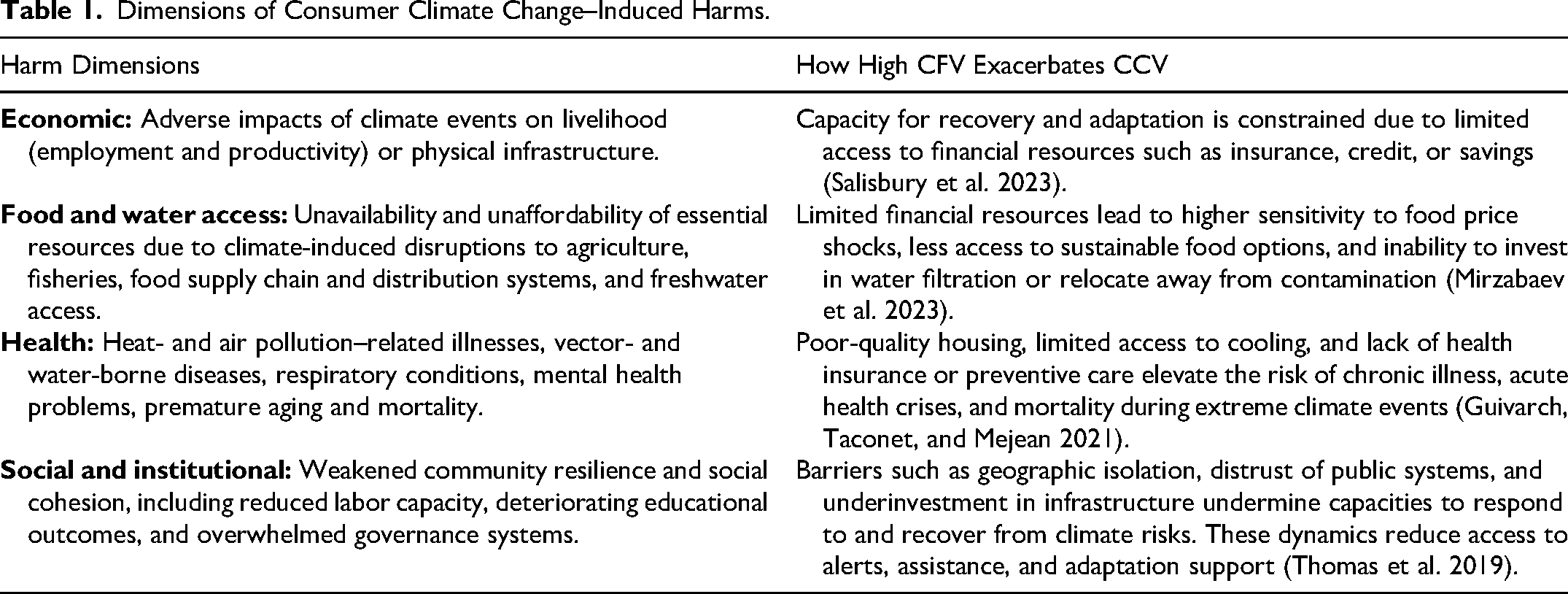

We conceptualize climate change–induced harm as a multidimensional construct that spans interrelated domains and reflects both direct and indirect effects of climate change, as detailed in Table 1. (Table W1 in the Web Appendix also provides more detailed examples.)

Dimensions of Consumer Climate Change–Induced Harms.

Economic harm captures the adverse impacts of climate events on physical infrastructure, employment, and recovery and adaptation capacities, due to limited access to financial resources such as insurance, credit, or savings (Brunetti et al. 2021). Climate-induced events often damage infrastructure, disrupt trade (Mikaelsson and Dzebo 2023), and cause loss of personal or community possessions (Baker, Hunt, and Rittenburg 2007). They also impose additional costs, such as evacuation expenses, lost income, temporary housing demands, and debris removal costs (You and Kousky 2024). Heat stress reduces labor productivity, particularly in industrial sectors like construction and agriculture, leaving workers at greater risk of being exposed to extreme temperatures, with insufficient access to cooling systems (Kjellstrom et al. 2009).

We therefore predict that economic harm triggers a recursive system among CFV and CCV. Financially vulnerable consumers frequently live paycheck-to-paycheck, lack emergency savings (or “slack resources”; Blocker et al. 2023; Salisbury et al. 2023), and do not have adequate insurance coverage. For example, Australian households located in flood-prone areas often have no or not enough insurance, particularly if they are lower-income households, which reduces their future capacity to absorb shocks and recover (Plass and Zinn 2025). For these households, climate disasters that damage property, interrupt work, or destroy assets lead to more prolonged and severe economic disruptions. Furthermore, in climate-sensitive sectors, such as agriculture, construction, or hospitality, employees also are more vulnerable to work disruptions due to climate shocks, thereby reinforcing their employment precarity (Guivarch, Taconet, and Mejean 2021). Even if public assistance is available, delays in disbursement, limited digital access, and missing documentation can delay or prevent recovery among financially vulnerable populations. Thus, CFV increases the likelihood of experiencing material harm during climate events and then also constrains the speed and comprehensiveness of recovery, perpetuating a cycle of vulnerability (Chamlee-Wright and Storr 2009b).

Still, affluent households are not immune to climate-related threats, such as flooding and wildfires. 2 Many affluent consumers purchase homes in high-risk “danger zones,” seemingly with the assumption that their ample resources insulate them from loss (Markhvida et al. 2020). Recent climate events question such assumptions though; wealthier homeowners with high-value Western U.S. properties face greater wildfire risks than neighboring, lower-income residents in safer areas (Wibbenmeyer and Robertson 2022). Some of the most expensive U.S. real estate lies along coastlines, putting it at risk of rising seas and flooding. Similar concerns have provoked policy responses in other countries, such as Japan, which mandates flood-risk disclosures for all housing transactions (Aiba, Hasegawa, and Shirai 2025). Because climate change can degrade quality of life broadly, it thus exposes even the most privileged consumers to risks that their financial resources alone cannot fully mitigate (Wibbenmeyer and Robertson 2022).

Food and water access harm stems from the unavailability or unaffordability of essential resources due to climate-induced disruptions to agriculture, fisheries, food supply chains and distribution systems, and freshwater access (Mirzabaev et al. 2023). When climate change raises temperatures, shifts precipitation patterns, and induces more frequent extreme weather events, these outcomes strain water supplies and disrupt agricultural productivity, leading to reduced crop yields (Kaur et al. 2022), higher food prices (Hultgren et al. 2025), and intensified food and water scarcity (Mirzabaev et al. 2023). These issues disproportionately affect financially vulnerable households, which typically spend a larger share of their budgets on basic necessities. When climate events raise food and utility prices, high-CFV households are more strongly affected (Mirzabaev et al. 2023). Households with constrained resources also may be unable to afford filtration systems, bottled water, or relocation away from areas with compromised water quality, thus deepening their short- and long-term vulnerability.

The health harm dimension includes heat- and air pollution–related illnesses, vector- and water-borne diseases, respiratory conditions, mental health problems, and premature mortality (Rocque et al. 2021). Rising temperatures accelerate the spread of infectious diseases such as Lyme disease (Dumic and Severnini 2018); they also can increase depression and anxiety in response to heat waves and environmental degradation (Clayton 2021). In this domain, high CFV again exacerbates CCV, through a recursive impact on financial resources. Because financially vulnerable consumers often reside in high-risk geographies with lower housing costs (e.g., urban heat islands, flood-prone areas), their baseline exposure to environmental hazards is higher (Rocque et al. 2021). Furthermore, their housing tends to be older and poorly insulated, without air conditioning, proper ventilation, or structural protection against storms or flooding (Intergovernmental Panel on Climate Change 2023). If their financial vulnerability also prevents them from obtaining health insurance, access to preventive care, or early treatment or evacuation (Guivarch, Taconet, and Mejean 2021), the delayed care and overcrowded public health services that tend to occur during climate emergencies can exacerbate chronic conditions, trigger acute health crises, and increase mortality rates. Excess heat exposure prompts increased emergency visits, cardiovascular stress, and elevated mortality, particularly among low-income populations with restricted access to cooling infrastructure (Mullins and White 2019). A limited ability to absorb health-related shocks thus can initiate a feedback loop that compounds both CFV and CCV over time.

Finally, social and institutional harm refers to climate-related damages to community resilience, social cohesion, educational outcomes, and governance systems (Thomas et al. 2019). Climate change threat perceptions tend to heighten perceptions of intergroup threats and expressions of racism (Uenal et al. 2021), as well as contribute to higher crime rates, particularly in economically disadvantaged areas (Heilmann, Kahn, and Tang 2021). These dynamics weaken social capital (i.e., connections among individuals, groups, and organizations; Aldrich, Page-Tan, and Paul 2016) by fragmenting community ties; they also undermine informal support systems, at the moments they are most needed (Chamlee-Wright and Storr 2009b). Such risks increase with CFV (Thomas et al. 2019), in that financial vulnerability often is accompanied by geographic isolation, reduced political voice, and constrained access to social networks that might facilitate resource sharing or information dissemination. Such structural limitations can be deadly during climate events (Thomas et al. 2019). Households with limited internet access might not receive early warnings, renters without formal lease agreements may not qualify for relocation support, and immigrant or minority communities with histories of discrimination may avoid interacting with government agencies. The local governments in economically marginalized areas also tend to function under budgetary constraints that limit their ability to invest in climate-resilient infrastructure, such as flood barriers, cooling centers, or emergency shelters. These institutional shortfalls disproportionately burden financially vulnerable residents, who rely more on public services during crises. Repeated experiences of inadequate support diminish trust in public institutions, further reducing social capital. Such losses amplify vulnerability by reducing collective efficacy and long-term adaptive capacity, which in turn can slow down evacuations, prevent collective action, and produce poorer postdisaster recovery outcomes (Aldrich, Page-Tan, and Paul 2016). These compounding effects of institutional neglect, social marginalization, and geographic precarity illustrate the cascade of CFV to CCV that extends beyond households to harm entire neighborhoods or demographic groups (Chamlee-Wright and Storr 2009a).

The four domains of climate-induced harms are interconnected; harm in one domain often amplifies vulnerability in others. A health crisis can trigger job loss, which deepens the risk of economic/material harm; a job loss may reduce access to affordable housing, which increases climate exposure; and all of them may undermine institutional engagement, further isolating households from support systems. Thus, everyone, regardless of CFV level, is at some degree of risk of experiencing these interconnected, harmful consequences of climate change.

A Reinforcing System

Experiencing and recovering from climate-induced harm drains financial resources, reduces self-protection capacity, and increases dependence (Baker 2009). This inflection point might increase CFV, regardless of the CFV level prior to the harm (e.g., environmental disasters; Ratcliffe et al. 2020). Prior research has identified this negative feedback loop: CFV increases the likelihood and severity of disaster-related losses, and then these losses further increase CFV (Vasilyan and Ben Bih 2023). This recursive loop, depicted in Figure 2, also underscores the need to conceptualize CFV and CCV as interdependent, mutually reinforcing constructs. Just as increased financial resources can expand ecological footprints and systemic emissions, limited financial resources can amplify climate harms by constraining people's adaptive capacity, increasing their exposure, and delaying recovery (Baker 2009). Addressing CFV thus is not only an issue of economic justice but a prerequisite for equitable climate adaptation.

Mitigation and Adaptation Interventions

Finally, two types of climate-related interventions influence CCV (see Figure 2): mitigation interventions, which moderate the relationship between financial resources and ecological footprints, and thus affect contributions to climate change, and adaptation interventions, which moderate the relationships between CFV and CCV, as well as between experiences of climate-induced harm and future financial resource availability. That is, mitigation interventions seek to curb greenhouse gas emissions or reduce the pollution generated by consumption, as might be exemplified by green finance policies that align financial systems with environmental sustainability goals through loans, investments, bonds, or insurance; organizational investments in eco-friendly production and marketing processes; and individual sustainable behaviors, like reducing car and air travel. Ultimately, mitigation actions aim to reduce the detrimental effects of human consumption on the climate. Adaptation interventions instead seek to reduce CCV by building resilience to anticipated or previously experienced climate impacts. Such actions may be proactive, such as preparation before climate change–related events occur, or reactive, including recovery efforts after climate change–induced harms occur. Adaptation interventions could reduce or exacerbate the effect of CFV on CCV though, depending on the design and implementation. For example, early warning systems might help households prepare and evacuate, but if they require costly technologies or subscriptions, such that financially vulnerable households cannot afford them, they may deepen existing inequalities. Other actions might take the form of investments in climate-resilient infrastructure (e.g., roads, facilities, homes) to better withstand climate events (e.g., floods, heat waves). Reactive adaptation, designed to counteract the detrimental impact of climate-induced harms on financial resources, might include tax relief and automatic filing extensions in areas that have experienced climate disasters or establishing flexible work policies and paid climate leave. Ultimately, the goal of adaptation actions is to build resilience to climate change.

Implications for Designing Interventions

The proposed framework reveals four central implications for consumers, organizations, and policymakers, as we detail next.

Implication 1: Address dueling pathways—interventions that increase available financial resources to reduce CFV should do so without unduly increasing ecological footprints

Financial resources can have double-edged effects on consumers’ financial and climate vulnerabilities. On the one hand, increasing financial resources should reduce CCV, because greater access to financial resources decreases CFV, which minimizes the risks associated with climate-induced harms. On the other hand, more financial resources encourage increased consumption and larger ecological footprints, contributing to further climate change and intensified CCV across the entire CFV spectrum. These conflicting pathways likely differ in strength, and their implications for CFV, climate change, and CCV should vary according to whether available interventions strengthen or weaken their impact.

Research involving consumers in diverse countries (e.g., Brazil, Denmark, India, Nigeria, United States) shows that people misunderstand the impact of financial wealth on climate change, because they underestimate the ecological footprint of the increased consumption associated with affluence (Andretti et al. 2024; Nielsen et al. 2024). Consumers with greater wealth also tend to underestimate their own carbon footprint, perceiving it as closer to ideal than it actually is (Köchling et al. 2025). As people gain greater access to financial resources and secure their financial status, they likely focus on the benefits they can gain from increasing their immediate consumption, rather than reducing their future vulnerability to climate-induced harm (e.g., buying climate insurance). Their decisions also may be driven by consumerism culture, in combination with the temporal discounting that tilts people's attention toward immediate needs and desires over future threats (Polasky and Dampha 2021). Such common tendencies highlight the need for interventions designed to increase awareness of how certain consumption patterns (e.g., purchasing larger homes, flying more frequently, investing in carbon-intensive assets) expand ecological footprints, then persuade people to reduce their carbon-intense consumption. Other policies should incentivize and enable consumers to allocate more of their financial resources to consumption and investments that foster climate adaptation and resilience efforts, without increasing their ecological footprints.

Implication 2: Close the gap—interventions should weaken the link between CFV and CCV, while reducing CCV for all

As financial vulnerability increases, so does CCV, resulting in disparate levels of vulnerability to climate-induced harm between populations with lower versus higher CFV (Parks et al. 2023). Adaptation interventions aim to lower CCV overall; we propose that they should explicitly target the reinforcing link between CFV and CCV, to avoid the risk that financially vulnerable groups bear a disproportionate share of climate vulnerability. Ideally, interventions implemented across macro, meso, and micro levels would reduce CCV for all while simultaneously narrowing the vulnerability gap between low- and high-CFV populations, such that the ultimate benefits are distributed more equitably.

Not all interventions achieve such dual goals, and they might even intensify the CFV–CCV link. Climate-resilient real estate developments provide general protection against flooding and wildfires, but the benefits are often captured disproportionately by affluent households that can afford to purchase these protected, resilient properties (Bazbauers 2022). Well-intentioned but maladaptive interventions might reduce immediate risks for financially vulnerable consumers but increase CCV for society at large, leaving everyone worse off. For example, building cooling centers and expanding air conditioning access for vulnerable populations can lower heat-related health risks, but such measures may prove detrimental in the long term by increasing energy demands, grid strain, and emissions that exacerbate overall climate vulnerability.

Implication 3: Disrupt feedback loops—interventions are needed to minimize depletion of financial resources after experiencing climate-induced harm

The harms induced by climate change often deplete financial resources and increase CFV, regardless of prior CFV levels (see the feedback loop in Figure 2). Experiencing unforeseen climate-induced crises, such as environmental disasters or infectious diseases, and changing circumstances, such as forced relocation due to climate change, represent salient examples of inflection points at which consumers’ CFV increases (Salisbury et al. 2023).

To clarify this implication, we offer a hypothetical example of John, a 68-year-old retiree living in the Southeastern United States, who receives a stable monthly income from his pension and enjoyed financial security until a recent, intense hurricane flooded his region, damaging his house and almost everything inside. John's home insurance policy did not cover flood damage, making it impossible for him to repair his home and recover from his financial losses. Having lost his house, John had to relocate to an apartment in another region, which physically separated him from sources of social capital that he had spent decades building. The hurricane thus disrupted John's access to multiple resources, including wealth tied up in real estate and social capital obtained through relationships, leaving him with fewer resources after the flood receded.

The example is hypothetical but realistic. Traditional homeowners’ insurance policies do not cover flood damage, and only 4% of U.S. homeowners maintain flood insurance (Joint Economic Committee 2024). The increasing frequency of climate disasters has led many insurers to stop writing any policies in high-risk regions and sharply increase premiums, such that average insurance premiums increased 44% between 2011 and 2021 (Joint Economic Committee 2024). Without the resources provided by climate insurance and other forms of institutional aid, people struggle to recover from climate harms due to natural disasters. Without appropriate climate adaptation interventions, climate-induced harms spanning economic, food and water access, health, and social and institutional domains further erode financial resources, in a reinforcing feedback loop that exacerbates CFV over time.

Implication 4: Tackle interconnected harms—interventions should strive to address more than one dimension of climate-induced harm at a time

The deeply interconnected forms of harm demonstrate the universality of the risk of climate-induced harm. Financial resources might reduce some risks, but no one is fully immune to the cascading social, psychological, health, economic, and infrastructural consequences of climate change. For example, financial resources might enable people to rebuild or relocate, but they cannot offset social harms created by the displacement of neighborhoods, communities, and cultural heritage; the psychological harms resulting from trauma and stress (Prayag, Ozanne, and Spector 2021); health harms, such as heat-related illnesses, accelerated aging, and exposure to vector-borne diseases (Dumic and Severnini 2018); and infrastructural harms, which arise when grids fail or supply chains break down, limiting access to essential food, water, and medical care. As climate events become more frequent and severe, they expose everyone, regardless of financial resources, to climate-induced risks that cannot be remedied easily by financial means. Therefore, any effective policies and adaptation interventions must address more than one of the four dimensions of climate-induced harm.

Opportunities for Intervention Design

These implications combine to suggest that the most effective climate policies are those that achieve multipronged goals and account for both financial and climate vulnerabilities. Existing policies instead tend to address climate and financial vulnerability as separate challenges, leveraging either environmental regulation or economic relief. This siloed approach also overlooks how traditional forms of economic advancement (e.g., dependence on personal cars, ownership of large houses, resource-intensive lifestyles) perpetuate inequality while also increasing climate harms. If such patterns replicate more widely as people gain more financial stability, global ecological footprints could soar. To break this cycle, policy interventions must pursue a new course that allows for economic uplift without reproducing unsustainable behaviors. Such a demand implies the need for a leapfrogging approach: Instead of outdated, environmentally damaging development models, financially vulnerable populations might transition directly into cleaner, more efficient, and more resilient consumption alternatives. Similar to how some developing countries bypassed landline infrastructure and moved straight to mobile phones (Huang 2011), financially vulnerable populations might skip carbon- and waste-intensive consumption patterns and adopt sustainable practices from the outset. Such a transformation demands coordinated changes at three levels: macro, in the form of enabling public policies and investment; meso, involving organizational innovation and industry adaptation; and micro, focused on individual and community engagement in sustainable actions.

Interventions and Research Opportunities

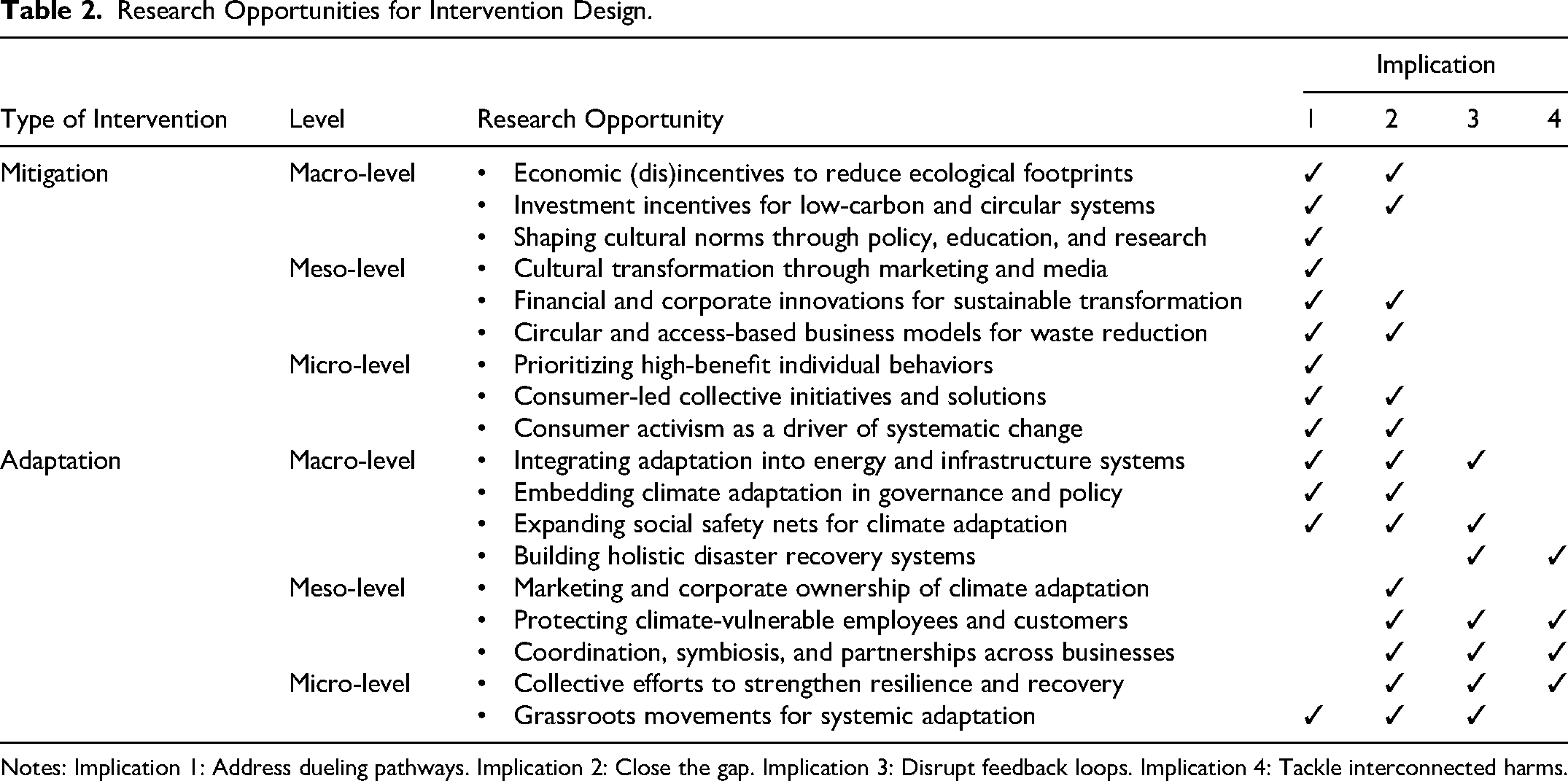

In addition to accounting for all three levels, we postulate that reducing CCV requires two complementary intervention approaches: mitigation efforts to target the root causes of climate change by discouraging carbon- and waste-intensive consumption and production, together with adaptation efforts to enhance consumer and community capacities to withstand and recover from climate shocks. We argue that implementing these strategies in combination can weaken the reinforcing cycle between CFV and CCV. In the following sections, we present specific insights into mitigation and adaptation interventions at the macro, meso, and micro levels. Macro- and meso-level policies promise greater impacts, but micro-level actions are essential to sustain broader, system-level efforts (Connolly, Loewenstein, and Chater 2025; Nenkov 2024). A comprehensive review of existing climate interventions is beyond the scope of our research (see instead Ford, Berrang-Ford, and Paterson 2011). We detail interventions that stem specifically from the four implications of our framework while also offering suggestions for further research along these lines (Table 2).

Research Opportunities for Intervention Design.

Notes: Implication 1: Address dueling pathways. Implication 2: Close the gap. Implication 3: Disrupt feedback loops. Implication 4: Tackle interconnected harms.

Mitigation via Macro-Level Policy

The most established climate mitigation policies worldwide focus on the energy and emissions sector, using tools such as carbon pricing, renewable energy standards, or zero emission vehicle mandates (see Table W2 in the Web Appendix for an overview). These measures seek decarbonization outcomes by targeting high-impact sectors, like transportation and electricity, supported by infrastructure policies (e.g., expanded electric vehicle [EV] charging stations). Policies focused on waste reduction, such as extended producer responsibility and right-to-repair laws, instead promote resource efficiency and circular economy practices. Furthermore, governance measures such as mandatory ESG (environmental, social, and governance) reporting requirements (e.g., the European Union's Corporate Sustainability Reporting Directive, in effect as of 2025; European Parliament and Council of the European Union 2022) are designed to enhance corporate accountability.

The European Union thus far has taken the lead in adopting such policies, such that its mitigation interventions exhibit substantial breadth and integration. Seemingly due to such comprehensive, coordinated climate governance, Europe displays a substantially lower per capita ecological footprint than the United States, despite similar quality-of-living levels (Web Appendix, Figure W1). In contrast with the European Union's well-managed climate governance system, and reflecting persistent polarization and legislative deadlock at the federal level, the United States relies on a fragmented mix of state-led initiatives (e.g., California's 2022 Truth in Recycling law; California Legislature 2021) and voluntary private-sector measures (e.g., B-Corp certification). This disparity reveals opportunities for the United States to scale up proven strategies, such as Europe's investments in renewable energy, green infrastructure, and responsible production systems.

Beyond federal efforts, state-level climate policies might catalyze national transformations. When states adopt ambitious sustainability regulations, firms with national distribution networks usually are compelled to standardize their practices across all markets to achieve economies of scope. Going forward, states should continue pursuing bold mitigation measures. Federal resources can amplify these impacts and ensure that financially vulnerable consumers are protected. Efforts to design and assess such macro-level mitigation policies, in ways that simultaneously reduce ecological footprints, reshape consumption norms, and enable equitable outcomes for consumers, will require additional insights from dedicated research, particularly in light of persistent political and regulatory uncertainty, fragmented governance, and inconsistencies in ESG and corporate adaptation mandates (Pappas 2024).

Economic (dis)incentives to reduce ecological footprints

Policies designed to curb high carbon-emitting consumption are essential to achieving sustainability goals. Differentiated carbon pricing, such as higher taxes on emissions due to frequent air travel, large homes, and large vehicles, targets the outsized ecological footprints of affluent consumption. Such measures promise to cut global household emissions by 100 gigatons of CO2 equivalents by 2050, covering nearly 75% of what is needed to meet the 2°C climate target (Oswald et al. 2023). These interventions also might help prevent the translation of reduced CFV into greater carbon-emitting behavior.

In parallel, it is important to encourage sustainable behaviors, as might be achieved by offering subsidies and rebates for energy-efficient appliances or grants for community-owned renewables. These initiatives reduce the upfront costs of sustainable options and increase access to choices that reduce ecological footprints. Thus, they could help upwardly mobile households bypass the high-carbon-consumption stages in favor of lower-impact alternatives. Further research is needed to assess the efficacy and consumer acceptance of such sustainability policies, and especially the effects on consumers as their access to financial resources increases.

Investment incentives for low-carbon and circular systems

Policies can create incentives for sustainable investments, such as tax credits for investing in solar, wind, and other renewable energy sources. Green financing, bonds, and loans also can support investments in low-carbon transit (e.g., electric buses, bike lanes, regional rail) and encourage organizations to pursue renewable or efficient energy sources, pollution prevention and control, biodiversity conservation, and sustainable land and water use (Ozili 2022), thereby redirecting private capital flows toward decarbonization. Another option for motivating corporations to reduce waste and pollution might involve extended producer responsibility schemes and tax credits tied to circular business models. Research should identify and define policies that can incentivize leapfrog innovation by rewarding firms that bypass incremental improvements and adopt transformative, low-carbon, and circular technologies. For example, how can subsidies for green hydrogen, carbon capture and storage, and advanced renewable systems accelerate decarbonization, and how can grants for developing bio-based, repairable, or fully recyclable materials reduce waste?

Incentives for sustainable and inclusive infrastructure and urban planning, such as walkable neighborhoods, protected bike lanes, and reliable green public transportation, remain underdeveloped, despite their potential for simultaneously reducing emissions and improving public health (Millard-Ball et al. 2025). Comparative studies could test which incentives most effectively reduce financial vulnerability while lowering greenhouse gas emissions, addressing different approaches adopted in various global regions (e.g., the United States vs. the European Union or Japan) that offer distinct levels and types of regulatory support.

Shaping cultural norms through policy, education, and research

Governments also shape cultural norms through laws and policy (Nyborg 2003). State-supported campaigns might dissociate consumption from social status while promoting low-carbon lifestyles (e.g., Sweden's “flight shame” movement), thereby defining sustainable choices as aspirational and encouraging reduced consumption even when financial resources are ample. Information disclosure regulations (e.g., mandated true-cost carbon labeling that discloses life-cycle emissions) also can help empower consumers and pressure firms to innovate. Research into optimal designs for cultural norm-shifting and information disclosure policies, such that they simultaneously decrease emissions and alleviate financial vulnerability, could help ensure that sustainable choices are both aspirational and accessible across socioeconomic groups.

Moreover, we call for more research related to climate change education. Incorporating climate science in K–12 curricula and higher education may increase climate change beliefs and concerns and encourage more sustainable consumption decisions (Elmor et al. 2024). If curricula also incorporate lessons about the social and economic inequities embedded within climate change and its impacts, this knowledge may deter young people from unnecessarily expanding their ecological footprint as they grow into adulthood and acquire wealth.

Finally, in line with recent calls for more societally impactful research (Ozanne et al. 2024), governments could support research into ways to advance the multiple, sometimes conflicting aims of the UN SDGs, such as reducing poverty (Goal 1) while fostering responsible consumption (Goal 12). Such efforts will require longitudinal data collection, dissemination for both research and monitoring purposes, and advanced methods (e.g., system dynamics, machine learning) to identify financially vulnerable consumers and the constraints they face.

Mitigation via Meso-Level Interventions

Companies and other organizations have achieved varied progress in mitigating and adapting to climate change (Polman and Bhattacharya 2016). Most large companies track their emissions and comply with regulations for reduced emissions, but fewer acknowledge the risk of climate disasters, such as by making energy efficiency upgrades or weatherproofing their facilities. Even fewer companies identify climate change as an opportunity to invest in mitigation tactics, like mapping supply chain risk, tying executive compensation to climate outcomes, or disclosing climate risk to investors (e.g., Task Force on Climate-Related Financial Disclosures 2023). Thus, substantial challenges, and misaligned economic incentives, persist. Firms benefit from increased sales, environmental externalities remain largely unpriced, and existing infrastructure creates lock-in effects that lower incentives to invest in sustainable innovation (Kenter et al. 2025). In addition, when companies adopt sustainability initiatives, they tend to remain siloed rather than integrated across business functions, limiting their strategic impact and constraining the pace and scope of meaningful progress (Bhattacharya 2019). Researchers might work to identify effective strategies used by companies that actually conduct business through a sustainability lens and integrate people and planet considerations into every business decision, from the mailroom to the boardroom (e.g., Patagonia). The biggest opportunities for U.S. companies may result from moving beyond pilot projects and embedding climate mitigation into their core operations

Cultural transformation through marketing and media

Companies’ marketing can reinforce harmful consumption norms or promote sustainable ideals. Repositioning behaviors such as repair, reuse, and secondhand purchasing as aspirational rather than frugal should help redefine societal views of prosperity and normalize such behaviors, even among the affluent. Advertisers and media sources are essential to such a cultural shift; though a majority of advertising professionals report concern about their sector's environmental impact (Decision Marketing 2024), the industry continues to portray material accumulation as a primary marker of success. To address this tension, the Good Life 2030 project (Purpose Disruptors 2026) details how advertising can normalize alternative visions of success that emphasize health, community, and nature instead of accumulation. In addition, companies might use nudges, such as default green settings (e.g., preselecting energy efficient appliance modes), to influence behavior (Thaler and Sunstein 2009) in ways that could expand and normalize sustainable practices.

Status-driven consumption instead reinforces a “consumption–status–carbon” loop, in which upward mobility fuels higher-carbon lifestyles. Various contextual factors, such as local income inequality, exposure to elite consumption norms, and the availability of low-carbon alternatives, might shape this loop. Branding, cultural narratives, and digital media underlie such factors, so marketing scholarship should uncover options for reframing status around sustainability. For example, under which conditions does financial security lead to sustainable rather than carbon-intensive behaviors? How might prestige be decoupled from material excess and redefined according to low-carbon practices? Research into such questions should assess both the direct effects of marketing interventions (e.g., aspirational repositioning, nudges, alternative visions of prosperity) and the broader social dynamics of status and consumption norms that marketing helps construct.

Financial and corporate innovations for sustainable transformation

Financial institutions and corporations can catalyze resource allocations and behavioral efforts toward sustainability. Innovations such as green credit scoring or preferential loan terms for EV purchases, solar installations, or home retrofits tie financial incentives directly to low-carbon behaviors. They thus help channel resources toward mitigation while also enabling consumers with limited means to overcome the upfront cost barriers and avoid financial strain aftershocks. Research should evaluate whether offering these financial products also helps mitigate expanding ecological footprints, especially among consumers exposed to higher CFV.

Beyond financial products, firms can promote sustainability through greater transparency. Sustainability metrics, such as climate risk scores for real estate (e.g., Redfin) or carbon labeling on products (e.g., Oatly), can inform consumer decision-making and encourage more sustainable choices; as research shows, eco-labels increase sustainable choices (Elmor et al. 2024). Such transparency efforts face challenges though, as when public backlash led Zillow to remove climate risk scores from its platforms (Brown 2025). Political and social challenges thus continue to constrain climate disclosure.

Industry pioneers can pursue reformulations and technological innovations, with the recognition that transformative corporate innovations generate new knowledge that can be deployed in additional applications. With leapfrog strategies, firms also can bypass resource-intensive practices and move directly to sustainable solutions, for example, smart grid systems that enable real-time energy optimization, circular economy models that remove waste from production cycles, or bio-based materials that replace fossil-based inputs. These initiatives remain constrained by the capital intensity and limited availability of many clean technologies, including EV infrastructure, which remains a significant barrier to widespread adoption (Powell and Johnson 2024). We call for research into which financial, social, and institutional drivers most effectively encourage both greater transparency and firm-level innovations that can enable systemwide transformation.

Circular and access-based business models for waste reduction

Waste reduction and product longevity are powerful mitigation levers, as can be achieved through circular and access-based business models. Circular economy initiatives, such as repair services, resale platforms, leasing, and trade-in programs, directly reduce emissions from production and also lower replacement costs for households (Ozanne, Prayag, and Sistig 2026; Philip, Ozanne, and Ballantine 2019), such that they can deliver both ecological and financial benefits (Andrade and Vieites 2025). Access-based consumption models, such as renting, borrowing, and sharing goods, also lower environmental impacts by reducing demand for resource-intensive production while expanding access to high-quality products. Libraries of things, which allow people to borrow rather than buying infrequently used items, reduce costs while building social ties based on sharing (Ozanne and Ozanne 2011). Platforms like Rent the Runway already have illustrated how access-based models can scale across industries. Research into market trends and long-term performance outcomes should include considerations of how these business models can attract consumer demand, while reducing carbon emissions and CFV.

Mitigation via Micro-Level Interventions

Even if many consumers recognize the urgency of climate change, their actions often fail to align with their responsible intentions (White, Habib, and Hardisty 2019), sometimes due to barriers created by low efficacy perceptions or minimal visibility of sustainable practices in daily life (Andrade and Vieites 2025). In turn, consumers often overestimate the environmental benefits of visible but relatively low-impact behaviors, like purchasing “green” products or recycling (Winterich, Reczek, and Bollinger 2023). Such misperceptions help give affluent households a false sense of having done “enough.” They also encourage financially constrained consumers to adopt similar behaviors, which impose unnecessary costs on their already limited budgets. For example, they might feel compelled to replace existing products with “greener” alternatives, even if the new production generates emissions that undermine any promised environmental gains.

Sustainable options such as access-based consumption are increasingly prevalent, though it remains unclear whether all forms of sharing are equally effective (Eckhardt et al. 2019). Food redistribution likely delivers meaningful gains, by reducing waste and improving access; ridesharing instead might displace more sustainable alternatives such as public transit (Schor 2016). Due to such unintended outcomes, well-meaning choices may paradoxically reinforce the CFV–CCV link or exacerbate financial pressures. Research also is needed to determine what interventions can propel consumers to make sustainable choices and adopt low-carbon lifestyles, even as their available financial resources increase.

Prioritizing high-benefit individual behaviors

At the individual level, the largest ecological gains require high-leverage choices, such as reducing air travel, driving less or going car-free, downsizing home energy use, and lowering red meat consumption. Yet consumer research tends to investigate sustainable behaviors with relatively limited environmental benefits, such as recycling (Lembregts and Cadario 2024). Because the wealthiest households account for a disproportionate share of consumption-related emissions, behavioral changes among these cohorts can yield greater benefits. To encourage such shifts, research is needed to test communication and other strategies that raise climate mitigation literacy, reveal true impact magnitudes, and support long-term adherence to sustainable behaviors that matter, without placing undue burdens on financially vulnerable consumers.

Consumer-led collective initiatives and solutions

Community-based initiatives reveal a way for individual actors to exert constructive effects and weaken the link between financial and climate vulnerability. For example, repair cafés offer the multiple benefits of lowering replacement costs, cutting waste, and limiting demand for resource-intensive production (Madon 2022; Ozanne, Prayag, and Sistig 2026). Cooperative purchasing offers another example: A solar-buying cooperative in Columbus, Ohio, enabled 15 households to install rooftop panels, saving an estimated $1.1 million in lifetime energy costs while reducing carbon emissions (Brown and Kaiser 2025). In addition to reducing environmental impacts, these collaborations strengthen community resilience and foster social cohesion. Moreover, affluent consumers seem amenable to sharing initiatives (e.g., the first modern car-sharing service launched in Switzerland, an affluent society; Turoń 2023), so they might act as early adopters and diffuse sharing practices more widely. In addition to examining barriers to adopting such initiatives among consumers affected by different levels of CFV, further research could identify viable strategies for building collectives that reduce emissions.

Consumer activism as a driver of systematic change

The role of consumer activism also warrants further research. Boycotts, grassroots advocacy, donations to climate organizations, and consumers acting as influencers who share sustainable content on social media represent powerful potential drivers of change (Goldwert et al. 2026). These individual actions can push companies and municipalities to offer lower-emission products, reuse infrastructures, and sustainable systems, which in turn lower barriers to sustainable practices. Right-to-repair legislation in several countries has resulted at least partially from the efforts of consumer activists (Marikyan and Papagiannidis 2024) and has made product repair more accessible and affordable. This example illustrates a broader dynamic: Individual actions, when aggregated, send powerful signals that normalize sustainable behavior and catalyze broader shifts. However, financial vulnerability can influence people's capacity to engage in consumer activism. Do groups at risk of greater CFV face more structural barriers (e.g., time, financial resources, digital access) to their participation, compared with more affluent activists? Perhaps even more important, does climate activism that includes members of financially vulnerable groups generate distinct outcomes?

Adaptation via Macro-Level Interventions

Even if mitigation is critical, it is no longer sufficient. It must be complemented by adaptation strategies to address escalating climate risks, as extant warming effects become irreversible (NASA 2025). In the United States, adaptation policies thus far have exerted limited impacts, due to federal oversight constraints and reactive approaches. For instance, infrastructure, governance, and resource management systems are insufficient, including fragile energy systems that highlight the need for grid investments and missing heating/cooling plans, water regulations, and housing support. Loans and grants for home upgrades and energy costs are minimal, and disclosure and waste reduction mandates are sparse. Finally, no clear, standardized policy covers financing, climate risk disclosure, or insurance against climate shocks. Instead, some state and local governments have adopted more advanced adaptation policies (e.g., Connecticut, Maryland, Washington, DC), such as green banks and energy programs that fund solar, weatherization, and electrification projects for low-income communities. The California Wildfire Mitigation Program offers financial assistance and education to low- and moderate-income households to support retrofitting and hardening homes at high risk of wildfires (California Governor’s Office of Emergency Services 2026).

As was true of mitigation efforts, European policy offers a roadmap for adaptation. The EU Adaptation Strategy, adopted in 2021, seeks climate resilience and neutrality by 2050 and includes energy-vulnerable households in the planned green transition (European Environment Agency 2026). Its example highlights the benefits of an integrated framework that balances resilience, justice, and climate neutrality. We leverage this insight to identify opportunities for research into coordinated policies that equitably enhance resilience, by shifting from temporary provisions to proactive, long-term empowerment and narrowing the gap between low- and high-CFV communities.

Integrating adaptation into energy and infrastructure systems

Relying solely on any single energy source, even if clean (e.g., hydroelectric), raises the likelihood of disruptions (e.g., due to extended droughts), which increase energy prices, CFV, and CCV. Scholars should identify climate-resilient expansion strategies that enhance grid resilience, including energy storage systems that absorb excess power from (ideally renewable) energy sources and discharge it during high-demand scenarios or outages (Ibrahim, Ilinca, and Perron 2008). The capacity to provide stable supply, even during extreme events, is particularly beneficial to households that face high CFV, uncertain incomes, and rising energy bills (Salisbury et al. 2023). Governments also could incentivize leapfrog innovations in other infrastructure developments (e.g., climate-resilient building materials) through well-designed mandates or subsidies, and trusted institutions (e.g., schools, healthcare centers) should be retrofitted as emergency hubs. Post–climate disaster reconstruction and adaptation create a critical juncture: If poorly designed, without sufficient research support, these efforts might exacerbate existing inequalities and leave financially vulnerable populations at even greater risk; if implemented thoughtfully, they offer an opportunity to address historical injustices and build more equitable, resilient, and better adapted systems (Cinner et al. 2018). Another key topic for continued research involves the potentially positive spillover effects of adaptation efforts, such as employment generated by green jobs programs in which workers retrofit homes, restore wetlands, and install resilience infrastructure, which would align financial stability with climate protection.

Embedding climate adaptation in governance and policy

Government procurement contracts might advance adaptation efforts if they mandate that suppliers use climate-resilient materials, such as drought-resistant landscaping and water-permeable infrastructure. Bureaucratic initiatives that expedite permits for actors that meet such standards also could remove key barriers for infrastructure adaptation (Burgess et al. 2023). Research that compares the effectiveness of such measures for encouraging less resource-intensive practices could accelerate the transition to sustainable, climate-ready infrastructure. In turn, governments have a complementary but distinct role in determining the informational and coordination channels, or barriers, that shape households’ and firms’ ability to anticipate and respond to climate risks. Early-warning systems and seasonal climate forecasts can inform farmers about which crops are likely to yield more in shifting environmental conditions (Cinner et al. 2018), which would limit their exposure to climate shocks and, thus, downstream CCV. Through education, governance efforts can cultivate greater preparedness and empower citizens to respond to climate shocks. Integrating climate resilience into curricula enables young students to develop knowledge and skills to anticipate and address climate risks. Adult education and workforce training can equip communities and industries with practical strategies for adapting to extreme weather, resource stress, and infrastructure vulnerabilities.

Expanding social safety nets for climate adaptation

Research should investigate robust social safety nets, in terms of how they can be designed and expanded to address climate disaster recovery needs. For example, researchers could test whether affordable climate risk insurance or climate-triggered cash transfers (e.g., activated during heat waves or crop failures) reduce administrative and financial strain on households and prevent vulnerable families from spiraling into debt. Expanding existing programs (e.g., unemployment insurance, Medicaid, SNAP) to include climate-sensitive triggers might establish a critical buffer for populations exposed to greater CFV, though continued research also is needed to find effective ways to finance such measures. Perhaps governments could issue environmental impact bonds, linking investor returns to flood control, wildfire prevention, and resilient water system projects. Similar strategies exist globally; for example, Brazil's tax-free investment infrastructure and agriculture bonds tie financial returns to tangible resilience outcomes (World Bank 2024). Research on how to implement effective tools would shed light on the implications of financial innovation and social safety nets for both climate and financial vulnerability.

Building holistic disaster recovery systems

Finally, we call for research that details the long-term, holistic recovery needs of populations affected by climate change. Postdisaster recovery extends beyond financial support and requires attention to multiple dimensions (Baker 2009; Prayag, Ozanne, and Spector 2021). A promising area of inquiry pertains to how federal adaptation policies might add social and emotional recovery to existing or new financial initiatives, such that people experiencing any level of CCV or CFV can benefit by reestablishing community ties and expediting emotional reconciliation. The effectiveness of various holistic recovery programs, such as community networking and support groups (especially following relocations), trauma therapy, religious counseling, and other similar services, also needs to be examined. Studies could focus on existing examples, like the FEMA Crisis Counseling Assistance and Training Program (FEMA 2026) and CalHOPE (California Department of Health Care Services 2026), which provide disaster survivors with crisis counseling and mental health support.

Adaptation via Meso-Level Interventions

Adaptation efforts often need to be localized, to reflect local climatic conditions (Tietjen, Clark, and Coughlan de Perez 2024). Yet businesses’ well-established procedures for managing operational crises also suggest their capabilities for responding to climate-related disruptions (Chamlee-Wright and Storr 2014; Ozanne and Ozanne 2021). Some firms already have embedded climate risk into their enterprise management, upgraded their operations (e.g., Duke Energy's “self-healing technology” [Duke Energy 2026]), and strengthened their supply chains, in efforts to both reduce their exposure to climate-induced harm and attain reputational and competitive benefits. Still, corporate adaptation remains fragmented and underfunded, relative to the scale of climate risk. Many companies continue to treat sustainability as peripheral and dedicate small, siloed teams and minimal budgets (often a fraction of their research and development budgets) to it, without integrating such goals into their core performance indicators or executive incentive criteria. Only 30% of U.S. employees believe their company even has a purpose beyond profit maximization (Bhattacharya and Jekielek 2023).

Marketing and corporate ownership of climate adaptation

Firms and public agencies, including nonprofits, should exploit their marketing resources to increase consumers’ awareness of climate risks and climate-resilient practices (Nardini et al. 2022). Persuasion tactics like emotional appeals are effective in shaping risk perceptions (Skurka et al. 2018). The U.K. flood insurance scheme Flood Re's campaign, “Protect the heart of your home,” depicts emotional scenes of flood damage to highlight the personal costs of inaction and encourage consumers to take preventative actions, like purchasing climate insurance (Cavendish 2026). Marketing-informed nudges, such as default enrollment in climate insurance, could increase adoption too. The effectiveness of such persuasion tactics and intervention strategies likely depends on the context though, indicating the need for research into how to tailor them to diverse populations.

Beyond marketing, firms could accelerate adaptation efforts by building sustainability ownership (Bhattacharya 2019) in all departments and employees. They also must consider the social dimensions of climate change adaptations, to ensure that such shifts do not disadvantage workers or vulnerable communities. In their lobbying efforts, firms could call for progressive climate policies that address systematic gaps, to move beyond pilot projects and integrate mitigation and adaptation efforts deeply into operations, supply chains, and corporate strategy. Research needs to detail precisely how firms can embed sustainability ownership throughout their ranks, as well as assess whether adaptation strategies inadvertently exacerbate the financial and climate vulnerability of employees and surrounding communities.

Protecting climate-vulnerable employees and customers

Corporate policies can function to protect employees and customers who are financially and climate vulnerable. Climate-flexible labor policies, like adjusted work hours during heat waves and paid leave for declared emergencies, protect the health and income of employees. Corporate “climate savings accounts” and relief pools can encourage savings and thereby help financially vulnerable employees access preventative adaptation tools before disasters strike, then provide these employees with immediate resources for evacuation and other expenses during crises. In parallel commitments, firms can protect their customers by offering affordable, climate-resilient products and services (e.g., flexible utility billing during heat waves) and ensuring equitable access through tiered pricing, subsidies, or community partnerships. To increase customer resilience, they might offer early-warning systems and targeted support. Research into such corporate mechanisms might not only detail their effects on the financial and climate vulnerability of employees and customers but also account for the implications for firm outcomes, including employee and customer satisfaction and loyalty, as well as firm profits (Ozanne et al. 2016).

Coordination, symbiosis, and partnerships across businesses

Through coordination, it might be possible to maintain services for vulnerable groups even during disruptions, as well as find solutions for consumers recovering from harm (Baker 2009). Established institutions could offer bundles of culturally specific and appropriate service offerings, such as skills training or legal, medical, and financial services, in collaboration with relevant providers, which should facilitate hastier recuperation (Chamlee-Wright and Storr 2009a). Commercial spaces and alternative consumer markets can enhance resilience through synergies that increase community connectivity, develop skills, and establish stronger recovery systems (Chamlee-Wright and Storr 2014; Ozanne and Ozanne 2016). Larger, vertically integrated companies also can leverage their logistics economies of scale to deliver essential aid rapidly to affected communities (Ozanne and Ozanne 2021). Public–private and business–nonprofit partnerships have demonstrated ability to expand access to critical services and resilience support, as when Airbnb launched a program during Hurricane Sandy in 2012 that allowed hosts to offer free accommodations to evacuees and allowed local authorities to leverage the firm’s communication network to coordinate support and disseminate information (Ozanne and Ozanne 2021). Continued research could detail appropriate partnership structures and incentive schemes that best deliver resilience at scale and create equitable outcomes.

Adaptation via Micro-Level Interventions

Adaptation efforts possess an inherent and unique advantage over mitigation: They can be implemented locally, with context-specific solutions (Chamlee and Storr 2009a). But even as awareness of climate risks grows, household-level adaptation remains limited. In New York City, nearly half of all households have taken no steps to prepare for flooding; those that have tend to prioritize small, visible actions, like stockpiling sandbags, rather than more protective steps like relocation (Buchanan, Oppenheimer, and Parris 2019). Access remains a critical barrier too, particularly for households with greater CFV. In Canada, where floods cause significant property damage, Canadians support flood insurance as a means of recovery, but their low demand and willingness to pay for coverage suggest affordability constraints, especially in high-risk areas (Henstra et al. 2019). Without accessible financial and community support, adaptation gaps risk exacerbating the CFV–CCV link, highlighting the need for research into which behavioral, financial, and social features can make adaptation more inclusive.

Collective efforts to strengthen resilience and recovery

Individual residents and communities can share resources to boost their combined resilience and recovery. For example, communities might undertake joint purchases of emergency kits or water-saving devices, bulk home retrofits for insulation and ventilation, and community-based insurance programs. Following extreme climate events, social networks can provide critical financial (e.g., loans, gifts for repairs) and nonfinancial (e.g., search-and-rescue efforts, emotional support) resources for disaster recovery (Aldrich 2018; Aldrich and Meyer 2015; Aldrich, Page-Tan, and Paul 2016; Chamlee-Wright and Storr 2009b). In the aftermath of floods in Mozambique, households without ploughs, cattle, or other assets relied on exchange relationships to secure these resources (Brouwer and Nhassengo 2006). After an earthquake in Christchurch, New Zealand, residents exchanged their time, expertise, and human resources through a time bank initiative (Ozanne and Ozanne 2021). Research can identify which coordination and financing models best encourage acceptance of such initiatives among various households; how different communication channels affect the speed, equity, and span of participation; the interactions of decentralized, social capital–based models with formal disaster assistance; and which features of governance best balance rapid response with accountability.

Collective preparedness also matters, as might be achieved through local alert systems (SMS trees, apps, radio groups) and social media that provide real-time information and action guidelines before and during crises. In neighborhoods where residents have collaborated on prior civic projects, social ties likely are activated already, which facilitates sharing of information, material resources, and psychological support (Aldrich 2018). Moreover, people's decisions are influenced by surrounding others; households are almost twice as likely to relocate before floods if neighbors also do so (Buchanan, Oppenheimer, and Parris 2019). Studies of collective engagement might identify how it can be mobilized to support preparedness efforts, which social levers reduce consumer resistance to climate-resilient behavioral changes, and how digital platforms can scale up support without undermining local responsiveness.

Finally, community efforts build trust and cohesion, which strengthen long-term resilience. Recovery from extreme climate events is a shared experience, and community efforts can grant members a sense of control and togetherness (Baker, Hunt, and Rittenburg 2007). Community support also can extend to emotional and social support. Research into the role of communities could specify their capacities for helping members recover from (or prevent) interconnected types of climate-induced harm, as well as how individual access to or perceptions of social capital shape their reliance on informal versus formal recovery mechanisms.

Grassroots movements for systemic adaptation