Abstract

Financial inclusion is one of the top priorities on the global development agenda. Financial literacy is identified as one major challenge in promoting financial inclusion. The paper develops a validated and reliable scale for assessing the financial literacy of the rural population in India, using data from villages in Maharashtra. The study considers the factors of knowledge, behavior, and attitude for the development of the scale. The scales are developed through five studies, including focus group interviews and survey data collection. Exploratory and confirmatory factor analysis are used for testing and validation of scales. Further, ANOVA is used to explore the relationship between the factors of financial literacy and socioeconomic parameters. The study uses both qualitative and quantitative methods. The study concluded that financial literacy is higher among people with bank accounts. Income level, education, and gender are found to be related tofinancial literacy. Financial literacy is lower among the female population, and it increases with income level and age, and varies by occupation. The study has implications for policymakers. Financial literacy can be enhanced by including it in the school curriculum, offering financial literacy programs for women, and raising awareness of government schemes and interventions.

Keywords

Introduction

The level of financial literacy worldwide is low, regardless of the development of financial markets. 1 Even in developed countries, people are often poorly informed about financial products and services. 2 So, the level of financial literacy among the youth is also low, 3 and many individuals cannot make sound decisions even regarding essential financial products such as savings. 4 Likewise, financial literacy is also low in India. 5 Financial literacy improves people’s knowledge of products and services, which are essential for information processing, selection, and use. 6 People with high financial knowledge tend to save more, which prepares them to deal with macroeconomic shocks and ultimately supports the economy’s financial stability. 7 Financial literacy enables people to improve their skills and abilities to make informed and effective decisions about the use and overall management of money, 8 thereby promoting the financial well-being of individuals. 9 On the other hand, individuals with lower levels of financial literacy are unable to process information accurately and make informed financial decisions. 10 They are more likely to fall into over-indebtedness and consequent financial distress. Financial illiteracy constrains people from saving and investing for retirement, adversely affecting their financial well-being in old age. 2

Several factors affect individuals’ levels of financial literacy. People with high incomes and substantial savings have greater financial knowledge. Higher savings may induce people to acquire the knowledge needed to manage them. 11 Further, it was found that gender also matters, as men are more likely to experience financial distress as compared to women. 12 Financially illiterate and weaker sections of society, such as the poor, illiterate, minorities, and women, are most vulnerable to financial hardships in retirement. 2 People’s financial literacy is dependent on several socio-economic factors and is a lifelong process involving knowledge, behavior, and life situations. 13 Financial literacy is a core skill for people operating in increasingly complex financial environments. 14 It is an essential investment in human capital, but its development should be related to the economic environment of the people. Therefore, governments worldwide are developing national strategies to provide lifelong financial education to their citizens. 15 On the same lines, the Government of India, through the Reserve Bank of India, has initiated measures to increase financial literacy amongst the people by introducing Financial Literacy and Counseling Centers (FLCCs) to provide consumers with financial counselling. Moreover, interactive websites have been developed to help students nurture financial literacy early. 16

To undertake sustainable, effective initiatives to improve financial literacy in India, it is necessary to develop a validated, reliable measurement scale. It is also necessary to identify the factors that contribute to the development of financial literacy. This will help develop effective financial education programs. There is considerable discrepancy in the literature on how to measure financial literacy. This study develops a scale for measuring the financial literacy of the rural population in India. It addressed research questions “What are the socioeconomic factors associated with financial literacy?” and How these factors are associated with the level of financial literacy of the rural population in India? The study develops a valid and reliable scale for assessing financial literacy in rural India. It will also help develop customized financial education programs for various segments of the rural population in India. A literature review The methodology.and findings are discussed in later part of the paper. The paper concludes by discussing the summary, conclusion, and policy recommendations.

Literature review

This section is divided into three subsections. introduces the concept, identifies factors influencing financial literacy, and discussions on scale development in financial literacy.

The concept of financial literacy

Financial knowledge largely explains financial literacy. 17 The knowledge component should include understanding market principles, instruments, organizations, and regulations. 18 It should also include the basic economic concepts for sensible saving and investment decisions. 1 Compounding interest rates should also be included, as they develop the ability to make decisions regarding debt contracts. 19 Financial literacy refers to a person’s ability to manage their money and financial matters. 20 Thus, financial literacy leads to financial capability, enabling people to participate in economic activities that lead to fulfilling lives. 21 However, acquiring the skills to manage financial resources effectively for a lifetime and achieve financial well-being is necessary. 22

Thus, financial literacy is the ability to process economic information and make informed decisions about financial planning, wealth accumulation, debt, and pensions. 4 Financial awareness, knowledge, skills, attitude, and behavior are necessary to make sound financial decisions and achieve individual financial well-being in due course. 23 Moreover, financial skills are linked to knowledge and behavior. 24 As per conceptual definitions, “financial literacy is a measure of the degree to which one understands key financial concepts and possesses the ability and confidence to manage personal finances through appropriate, short-term decision-making and sound, long-range financial planning, while mindful of life events and changing economic conditions.” The operational definitions identify four operating areas for individuals proficient in managing personal finances: saving, borrowing and investing, and budgeting. 25 Financial knowledge is a core component of financial literacy, but a person’s behavior and attitudinal characteristics also play a significant role in financial decision-making. 17 Attitudinal factors, such as risk aversion, anxiety, and pessimism, negatively influence financial behavior. Therefore, three factors, namely, financial knowledge, behavior, and attitude, should be considered while developing a concept of financial literacy. 20

Factors influencing financial literacy

Financial literacy and behavior have their roots in a person’s childhood. These depend on the family’s educational background, especially the mother’s education. It is also influenced by the extent of mutual interaction among family members on financial matters. 26 Living in a joint family (in which adult members make financial decisions) negatively affects financial literacy, whereas living in a family with consultative decision-making positively affects it. 27 At the school level, subjects such as mathematics and sciences 26 and subsequent work experience in financial matters directly affect a person’s financial behavior in succeeding years. 28 However, the role of parents in developing financial knowledge, attitudes, and behaviors is substantially more significant than that of work experience and high school financial education combined. 29 However, it is found that school attainments, coupled with financial literacy, are highly related to a person’s wealth accumulation in subsequent life. 30

Financial literacy is related to socio-demographic variables 3 such as education, age, gender, income, and occupation. 31 Generally, women are less financially literate than their male counterparts. 32 Also, higher age and higher income are associated with greater financial literacy. 33 It is observed that, in matriarchal societies in India, where women are heads of families, they possess higher levels of financial literacy than their male counterparts. This implies that being head of the family is an advantage for acquiring financial literacy. 34

A person’s financial behavior is impacted by their financial knowledge and attitude. 35 Attitudinal problems, such as inadequate self-control, delayed decision-making, and failure to respond to acquired information, hinder the development of financial literacy. Some socio-demographic barriers to financial literacy include low or unstable income and low age. 36 Financial education can address these issues. 37 A recent study found that financial literacy was significantly influenced by demographic factors such as age, gender, income, religion, social groups, educational level, occupation, and others. 38 It is also reported that gender impacts the level of financial literacy. 39 A study on students’ financial behavior found that financially literate students are more likely to exhibit better financial behavior. 40 Financial attitudes, financial behavior, and financial knowledge are key determinants of financial literacy. 41 Another study on college students found that financial literacy improved their thrift behavior and led them to save more. 42

Financial literacy measurement and scale

Various studies have used various determinants to measure financial literacy. Financial education 43 and financial knowledge 44 are among the key determinants of financial literacy. Financial behavior is an important determinant of financial literacy and shapes an individual’s financial situation. 44 A short scale for financial literacy comprising 12 questions across three dimensions: financial knowledge, attitude, and behavior was developed. 45 Further, another study concluded that financial literacy improved financial well-being directly and indirectly (mediated) through financial behaviors. 46 To measure financial literacy, four components, that is, Money basics (including time value of money, purchasing power, personal financial accounting concepts), borrowing, investing (i.e., saving present resources for future use through the use of saving accounts, stocks, bonds, or mutual funds), and Protecting resources (either through insurance products or other risk management techniques) should be considered. 47

In a study on investors, it was reported that emotional intelligence had a direct relationship with financial literacy and financial risk tolerance and an indirect relationship with financial behavior. 48 A recent study examined the concept of financial competence. It concluded that a more comprehensive measure, encompassing financial knowledge and non-cognitive factors such as financial behaviors and attitudes, should be used to assess it. 49 Another study included 23 items across four dimensions (financial security, financial tranquillity, financial freedom, and satisfaction with financial management) to measure the financial well-being of consumers of financial products. 50 Another scale contained 25 items to measure five different aspects of subjective financial well-being (general subjective financial well-being, money management, peer comparison, having money, and financial future). 51 It is important to note that various authors have developed scales based on different dimensions of financial management.

Methodology

Scale development and validation process

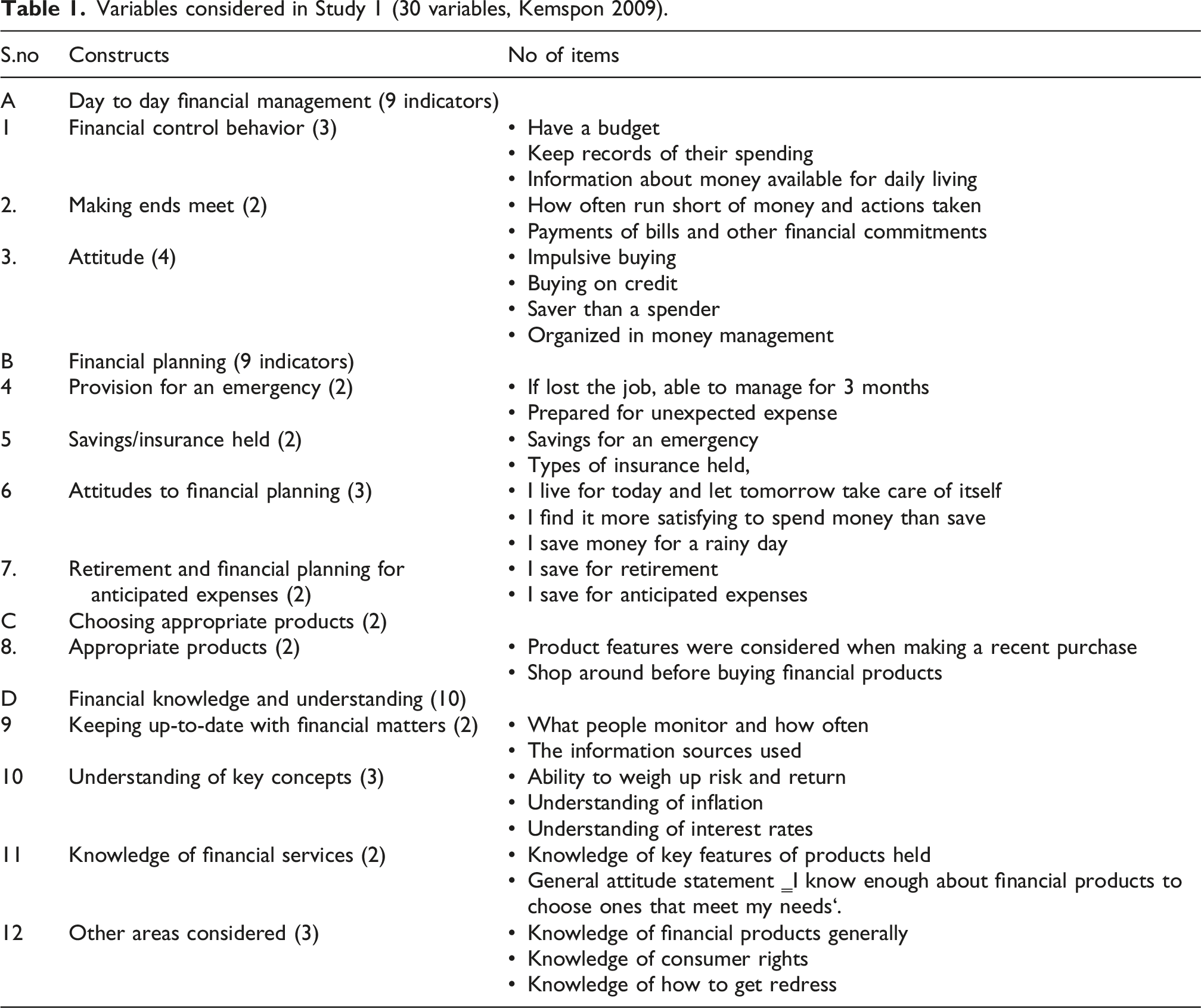

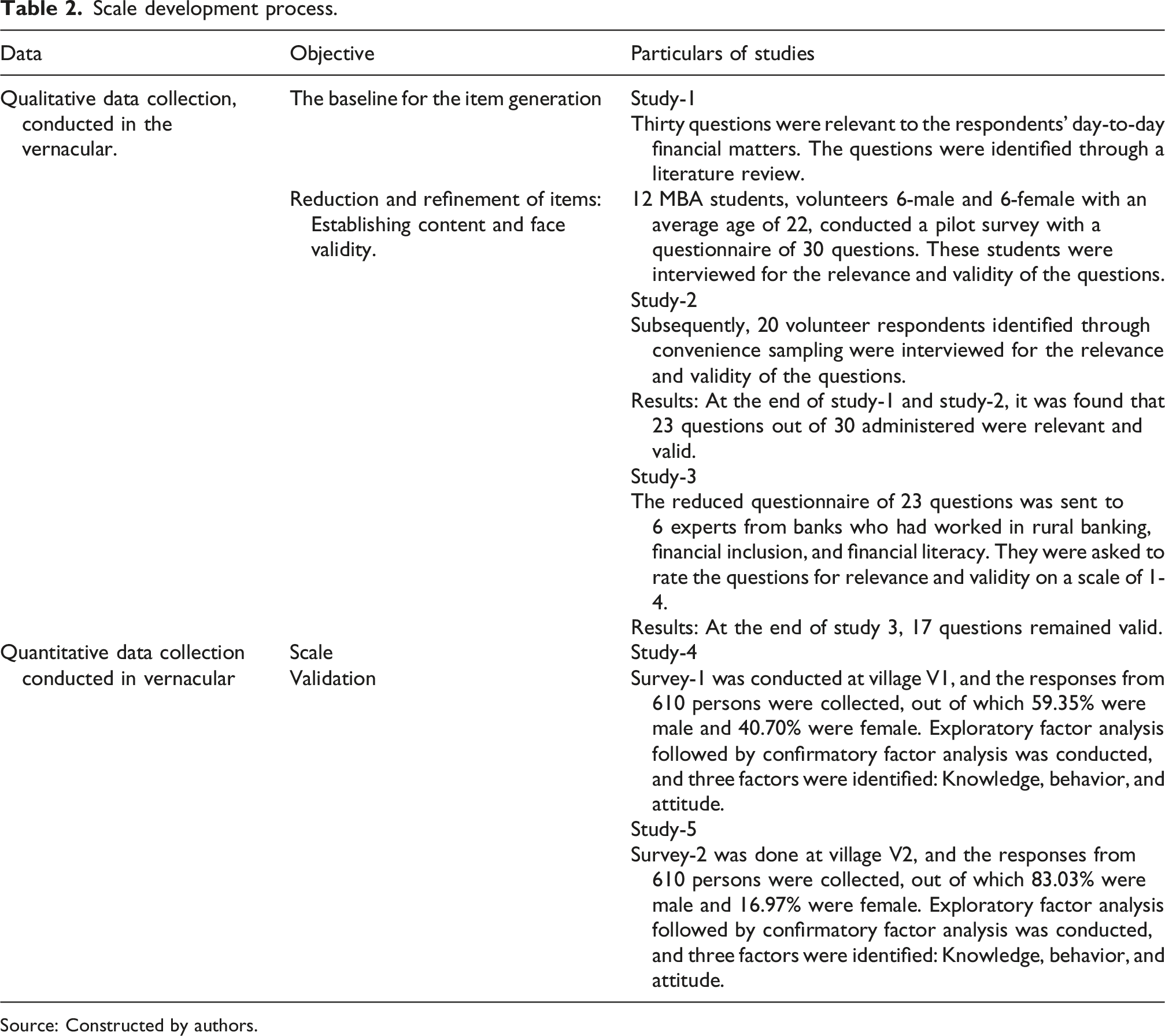

We have followed the scale development and validation guidelines provided by researchers.52,53 After a thorough literature review, we identified knowledge, behavior, and attitude as the factors for the development and validation of the questionnaire for survey.4,14,54 A comprehensive qualitative approach for reducing and refining questions followed the literature review.

Variables considered in Study 1 (30 variables, Kemspon 2009).

Scale development process.

Source: Constructed by authors.

Study 2: After that, the reduced questionnaire was administered to 20 prospective respondents for perusal, and they were interviewed to determine the relevance and validity of the questions. These respondents were selected through convenience sampling. After reviewing the responses, two additional questions were deleted (Study-2, Table-2).

Study 3: The questionnaire, containing 23 questions, was validated after Study 1 and Study 2 and sent to experts in financial literacy for their perusal. These bankers were selected using purposive and convenience sampling. These bankers worked in financial inclusion and had a good understanding of the concept and field realities. All these discussions were held in person and orally.

Content validity: To ensure the scale is reliable and valid, we have confirmed that the questionnaire items are relevant to financial literacy. This is done in two stages: (i) the items are selected based on an extensive literature review and (ii) the domain experts judge the content (for each item in the instrument). The content validity index (CVI) for individual items (I-CVI) and the scale (S-CVI) is used as a criterion for assessing the reliability and quality of the developed scale. 56

A panel of six content experts is requested to rate each scale item’s relevance to the underlying construct on a 4-point scale: 1 = Not relevant; 2 = Somewhat relevant; 3 = Quite relevant; 4 = Highly relevant. Based on the experts’ ratings, the I-CVI for each item is above 0.80, with an average I-CVI of 0.86. Furthermore, the S-CVI value is 0.96 (>0.80). Thus, each item in the questionnaire is relevant, and the scale is valid and reliable. 57 The final questionnaire, derived from Studies 1, 2, and 3, contained 17 questions and was used in the final survey. Further scale validation was done after conducting Exploratory and Confirmatory Factor Analysis. Table 2 provides an overview of the entire scale development process, which covers data collection from three qualitative and two quantitative sources.

Scale development: Study-4

We selected Village 1 (V1) for the survey, located approximately 20 km from Pune city in the state of Maharashtra, India. The selection of this village was purposeful due to its feasibility and data access. The sample comprises 59.35% of the male population and 40.70% of the female population. Most respondents (82.8%) have visited the bank and have bank accounts. The percentage of respondents in the 18-40 age group is 54.6%. Furthermore, 95.41% of the respondents are literate, 48.2% are engaged in business or employment, and 25.9% are homemakers. Most of the sample population (78.2%) is poor, with an annual income below 0.25 million. The selected 12 students (six male and six female) visited the respondents at their residences. They explained the questionnaire in the vernacular and noted their responses. Sufficient time was given to each respondent to reflect on their replies. Of the 620 respondents, 10 questionnaires were found to be incomplete; the remaining 610 were included in further analysis.

Study-5

We selected a tribal village (V2) for the survey, about 290 km from Pune city in Maharashtra State, India. The selection of this village was also purposive, and one factor was its better accessibility. The sample comprises 387 respondents, of whom 83.2% are male and 16.8% are female. The females in the village did not participate in the study because of cultural issues. This village was anterior and females did not interact with outsiders much. Most respondents (76.2%) are agriculture laborers or small farmers with annual incomes below Rs. 0.25 million. The illiteracy rate was 27.4%, and 95.9% had active bank accounts. A tiny proportion of respondents (1.3%) were working as housewives. The percentage of respondents aged 30 or older was 87.0%. Bharat Agro Industries Foundation, an NGO working in the area, conducted this survey.

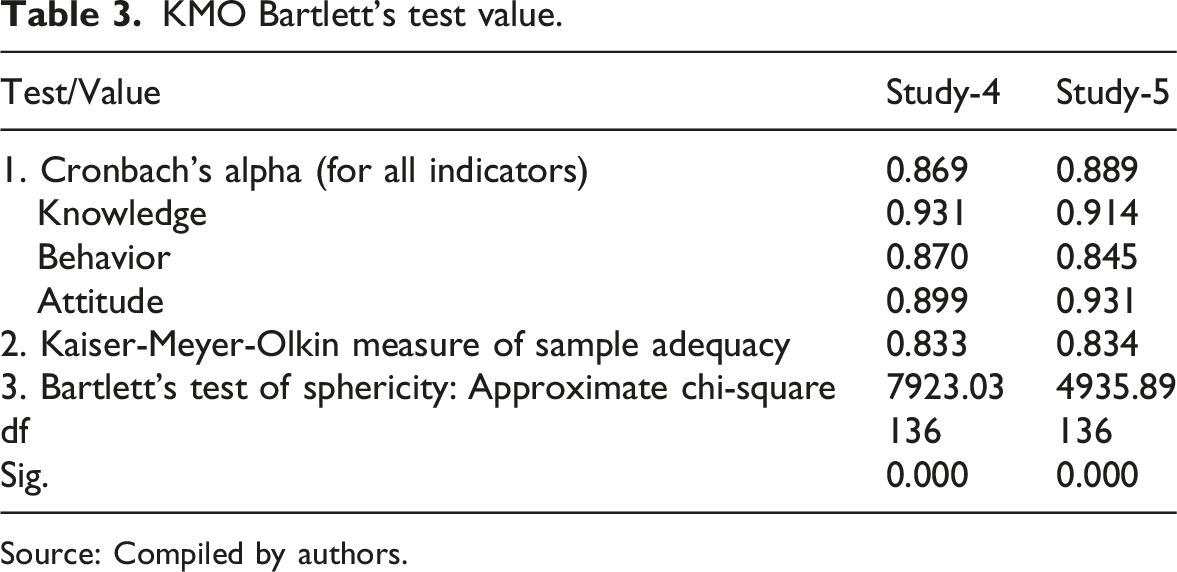

Exploratory and Confirmatory Factor Analysis

KMO Bartlett’s test value.

Source: Compiled by authors.

Alpha levels above 0.9 are excellent, and those above 0.8 are very good. 60 Cronbach’s alpha value above 0.7 indicates high internal consistency. 61 Thus, the construct has internal consistency as measured by Cronbach’s alpha. KMO statistics is 0.833 (threshold limit 0.5), and Bartlett’s test significance level is 0.000 (threshold sig level <0.05). This data is suitable for factor analysis. 62 Three factors emerged from the EFA: knowledge, behavior, and attitude. These factors explain 70.45% and 70.01% of the data variance for studies 4 and 5, respectively.

However, Cronbach’s Alpha has limitations as a measure of reliability. Therefore, researchers have suggested an alternative measure called Composite Reliability. 63 They have recommended a threshold value of 0.70 for “Composite Reliability” and have suggested that even a value of 0.6 can also be considered. Accordingly, we calculated Composite Reliability scores for the factors of Knowledge, Behavior, and Attitude, which were 0.95, 0.90, and 0.91, respectively. These exceed the threshold value of 0.70 recommended. Hence, the items are consistent. Further, we have tested the construct’s Convergent Validity and Discriminant Validity.

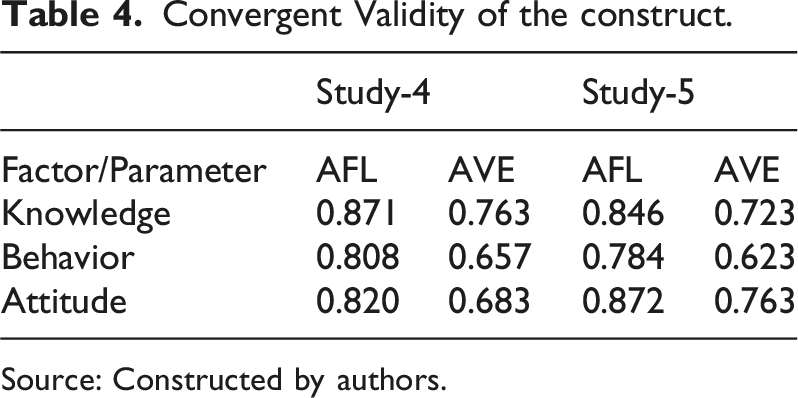

Convergent validity

Convergent Validity of the construct.

Source: Constructed by authors.

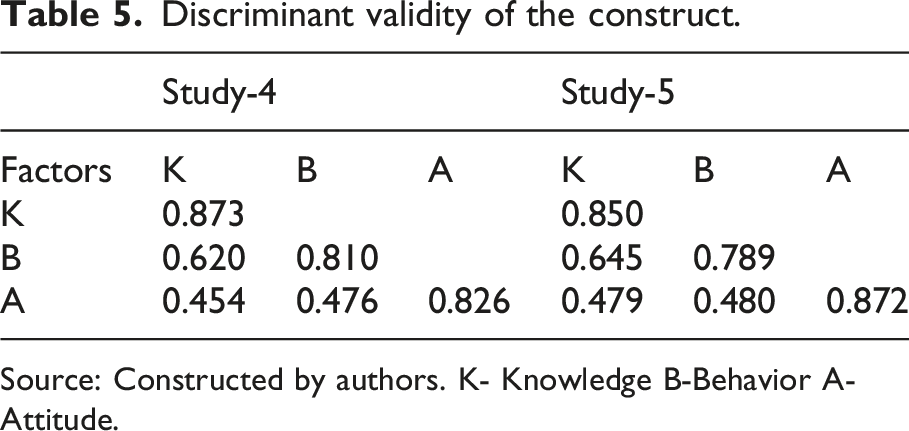

Discriminant validity

Discriminant validity of the construct.

Source: Constructed by authors. K- Knowledge B-Behavior A- Attitude.

Findings and discussions

This section presents the study’s results across all 5 phases and discusses them. This study adopted a mixed-methods design and used both qualitative and quantitative methods. The first three stages were qualitative and aimed to contextualize the scale for the Indian context by gathering opinions from various groups. In the second stage, a quantitative study was conducted in two different villages with different socio-economic conditions.

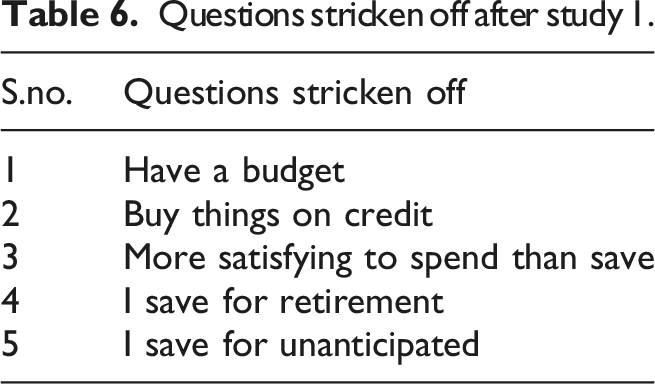

Questions stricken off after study 1.

Study 2: This round was meant to pretest the questionnaire. In round 2, again, 20 volunteers were randomly identified and were given the list of indicators. Two more items were struck off, that is, knowledge of consumer rights and knowledge of how to obtain redress. At the end of study 2, a total of 23 variables were identified.

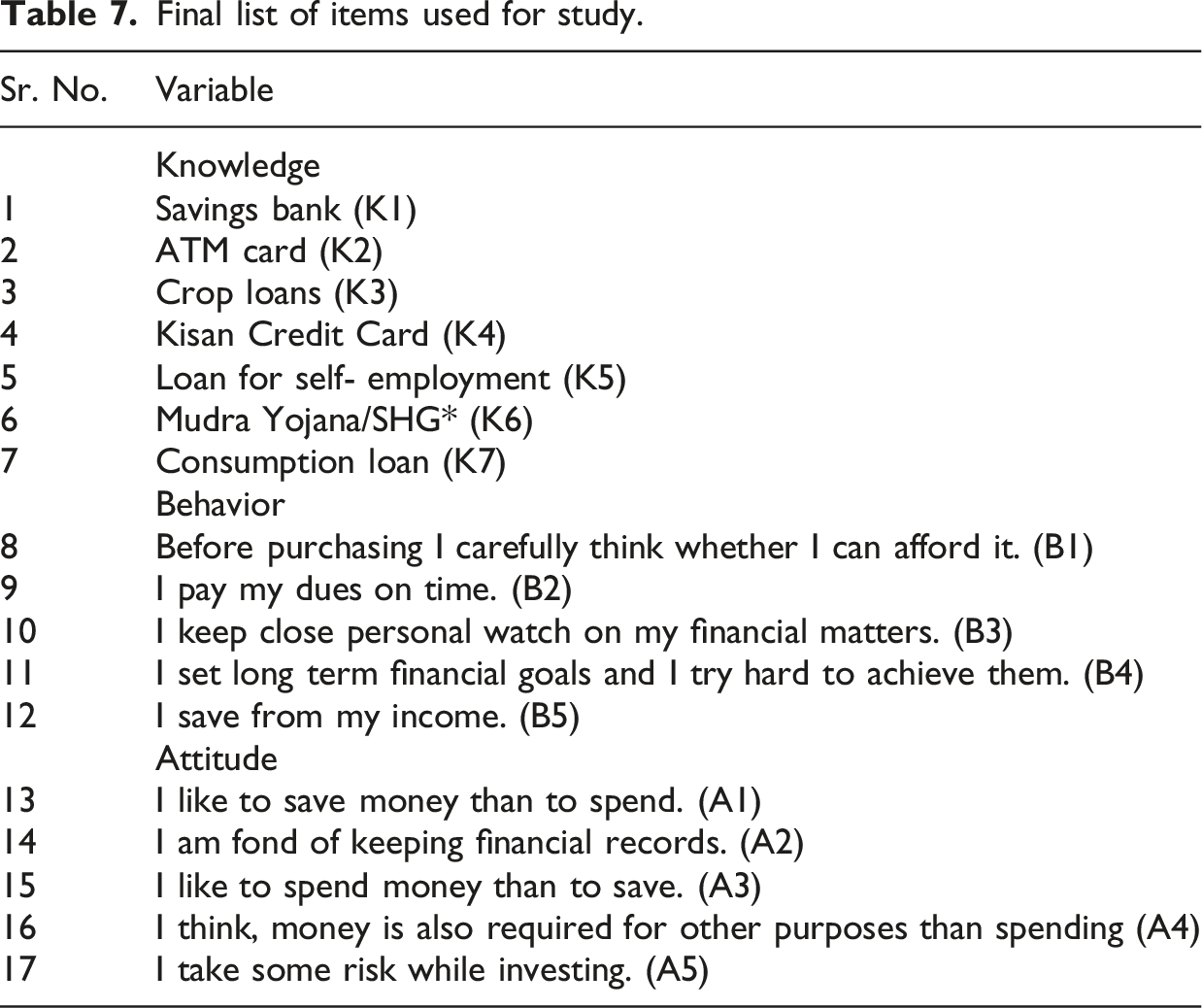

Final list of items used for study.

Study 4 and 5: The objective of this stage was to explore the significance of various factors identified through the earlier 3 stages of the study.

Results of exploratory factor analysis

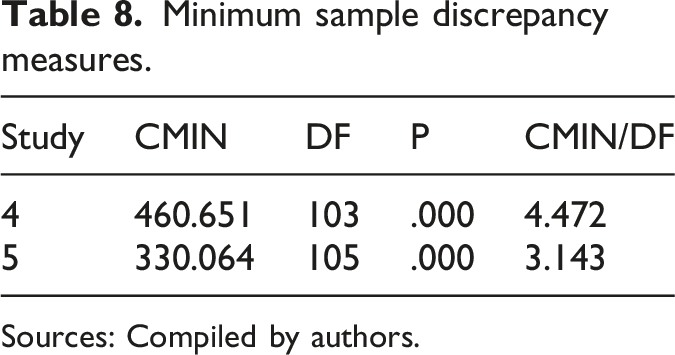

The KMO was 0.833 and 0.834 for studies 4 and 5, respectively, and Bartlett’s test of sphericity was significant (p < 0.000). Three factors have emerged from the data explaining 70.45%, and 70.01% of the total variance for studies 4 and 5, respectively. The factor loadings ranged from 0.71 to 0.95 and 0.66 to 0.96 for the respective studies. We also examined cross-loadings and found that all were below 0.4 (the maximum cross-loadings were 0.142 and 0.144 in the respective studies). Thus, EFA results showed strong correlations among the variables, and the data were suitable for factor analysis. 59 Therefore, we have decided not to exclude any items at this stage and proceed with Confirmatory Factor Analysis. The model fit summary in the case of both studies 4 and 5 is as follows:

Model fit summary

Minimum sample discrepancy measures

Minimum sample discrepancy measures.

Sources: Compiled by authors.

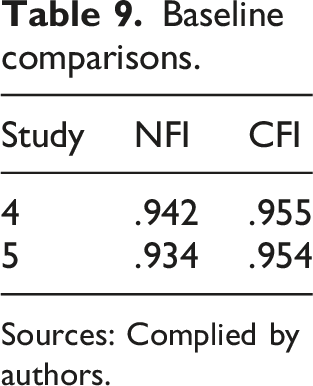

Baseline comparisons

CFI (Comparative fit index)

Baseline comparisons.

Sources: Complied by authors.

Normed-fit index (NFI)

The NFI for study 4 is 0.942, and for study 5, it is 0.934. These values above 0.90 indicate a good fit. 70

Minimum sample discrepancy functions

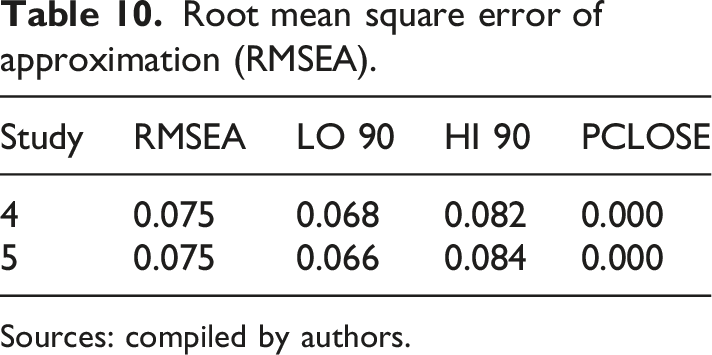

Root mean square error of approximation (RMSEA).

Sources: compiled by authors.

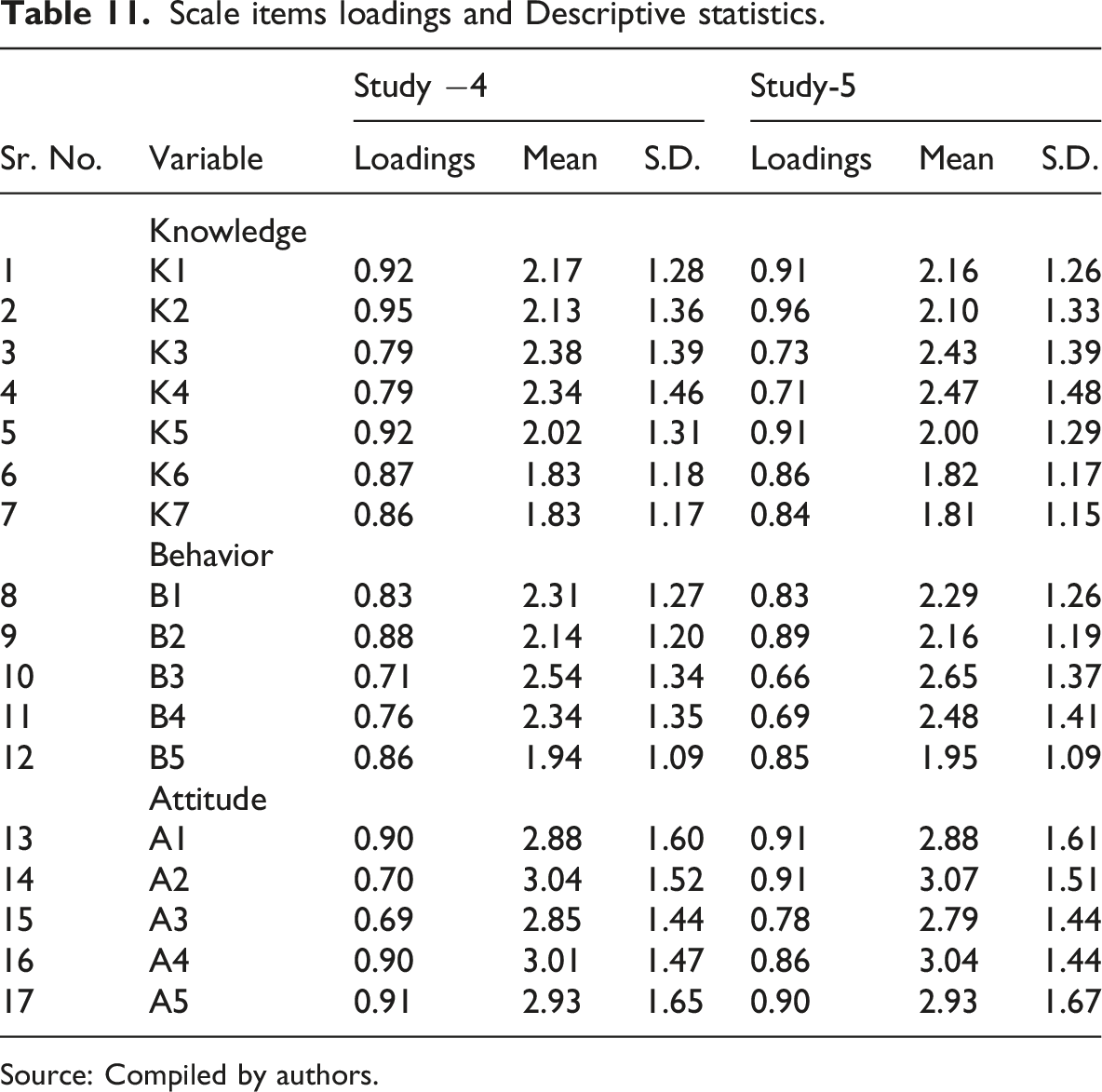

Scale items loadings and Descriptive statistics.

Source: Compiled by authors.

We considered loading between 0.5 and 0.6 acceptable in Confirmatory Factor Analysis.

72

On perusal of Table 8, it is observed that the average scores for the scale items for studies 4 and 5 are 2.42 and 2.41, respectively. These scores are low, indicating low financial literacy among the

To compare whether the means of the two groups are significantly different, we used a t-test. However, when ANOVA is applied to three or more groups, it does not identify significant differences between pairs of means. Therefore, we have used post hoc tests for multiple-group comparisons. 73

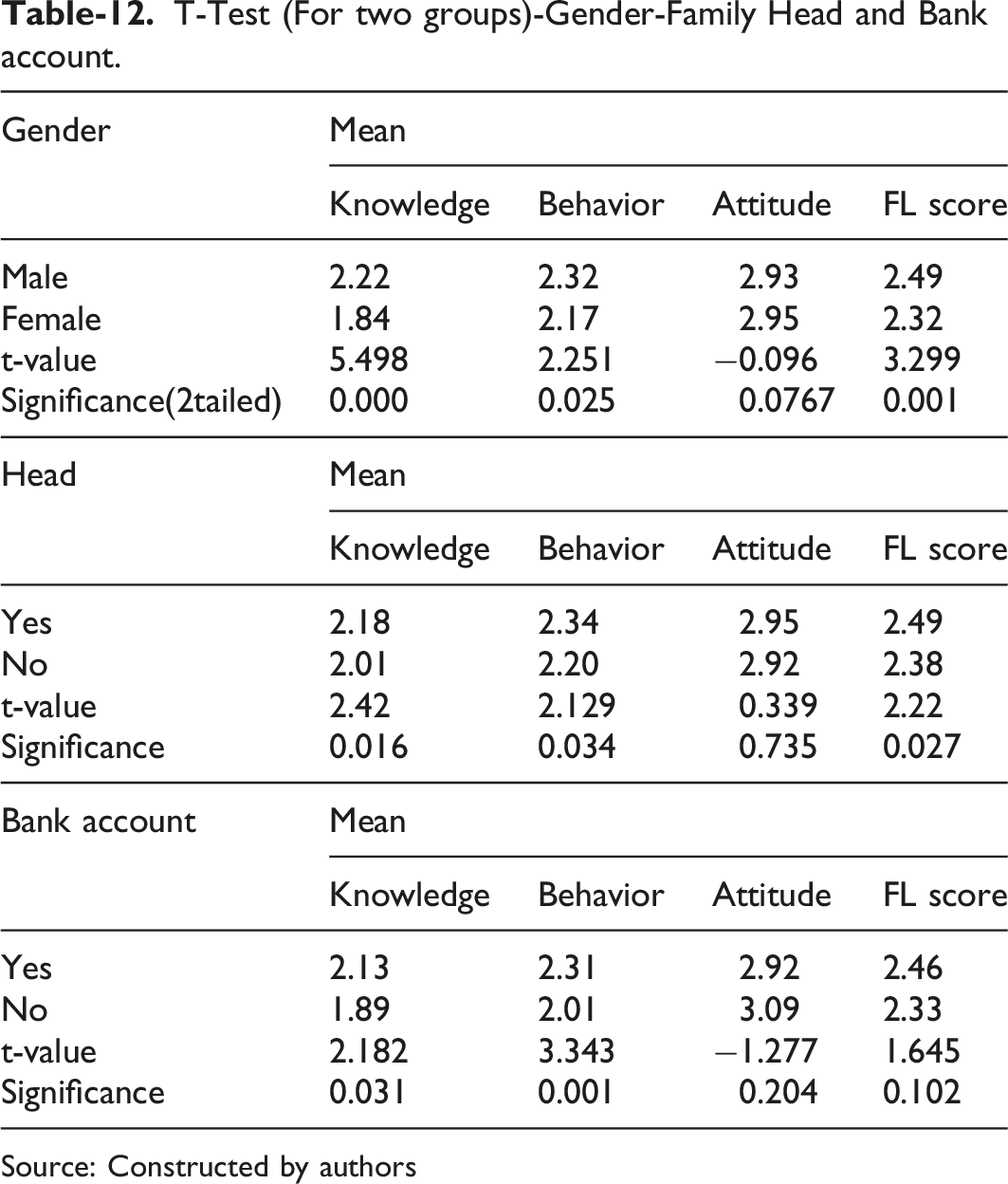

T-Test (For two groups)-Gender-Family Head and Bank account.

Source: Constructed by authors

It is observed from Table 8 that the average scores for the factors “knowledge,” “behavior,” and financial literacy are significantly higher for male respondents than for female respondents. However, the score for the factor’ attitude’ is higher for female respondents. This confirms the existing findings. 74 In India, male family members handle all significant financial matters, and women have no financial autonomy. This tradition is more prevalent among low-income families. 75 As a result, male members had more exposure and opportunities to learn than female members. Therefore, male respondents’ “knowledge” and “behavior” scores are higher than female respondents.

The parents of low-income families in rural India do not share any financial matters with their children, especially the female child. Financial socialization in the family is critical in acquiring financial knowledge and developing favorable financial behavior. 26 In general, there is discrimination against the female child in every aspect of life in rural Indian families. 76 Therefore, the chances of a female child acquiring “knowledge” or a positive behavior are lower than those of males at preschool age. Moreover, the role of parents in shaping future financial behavior and attitudes is significantly more important than school education and work experience. 29 Furthermore, many Indian women face numerous cultural, financial, psychological, and even physical barriers that hinder their becoming financially literate. 77 These findings confirm the researchers’ conclusions that, in general, women are less financially literate than their male counterparts. 32

Further, the average scores of heads of family for knowledge and behavior are significantly higher than those of non-heads of family. The family heads are responsible for all financial matters. They have better opportunities to acquire and practice their financial knowledge through actions and decision-making. This justifies their higher score regarding the factors “knowledge” and “behavior.”

The respondents with bank accounts scored significantly higher only on “knowledge” and “behavior.” The average scores of those with bank accounts are significantly higher concerning “knowledge” and “behavior.” This aligns with the existing literature, which indicates that experiences from operating bank accounts significantly better financial knowledge and behavior. 26

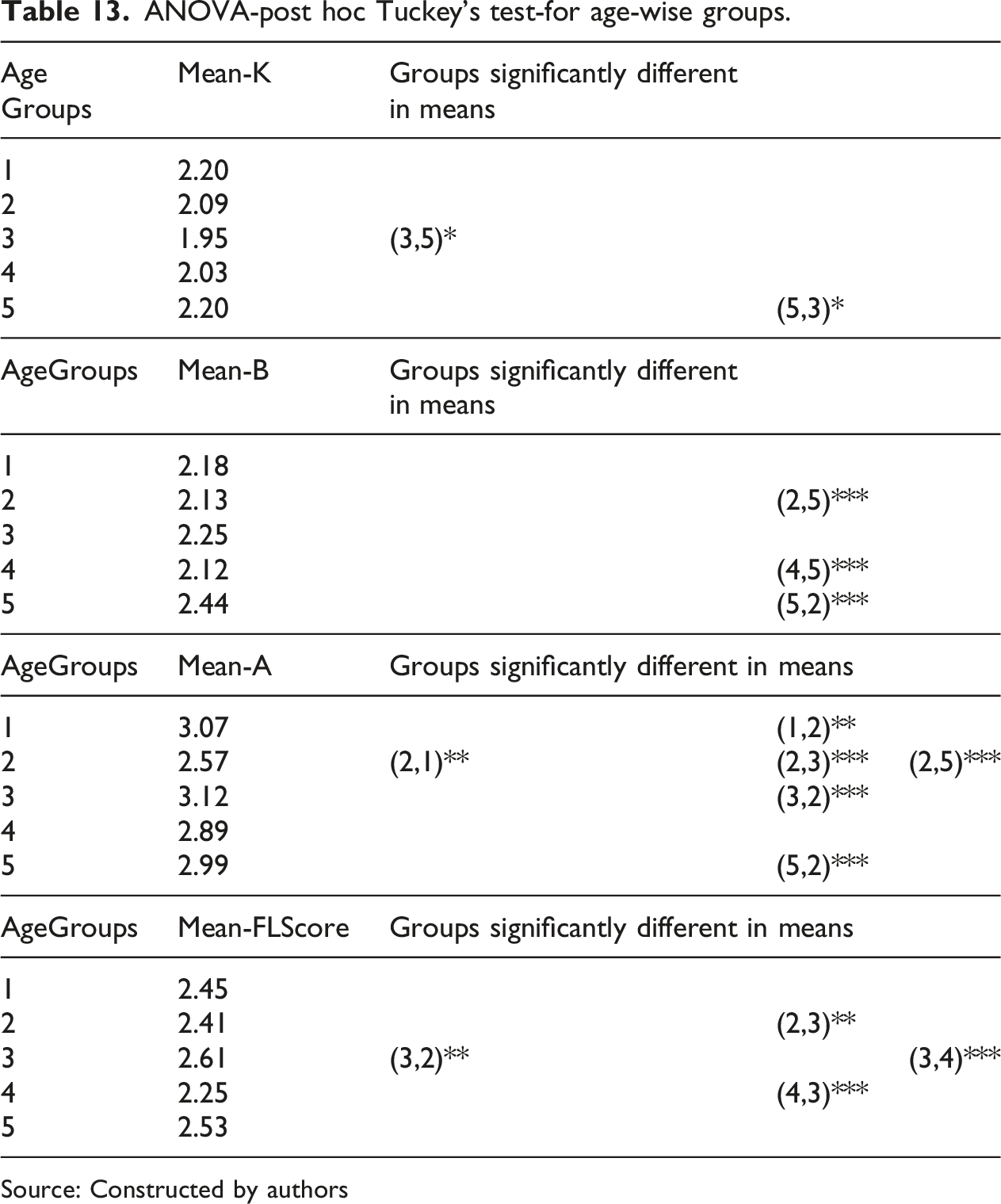

ANOVA-post hoc Tuckey’s test-for age-wise groups.

Source: Constructed by authors

The average score for the factor’ behavior’ is higher for the respondents above 40.. 35 These findings align with the literature, which indicates that financial literacy is age-dependent.31,33

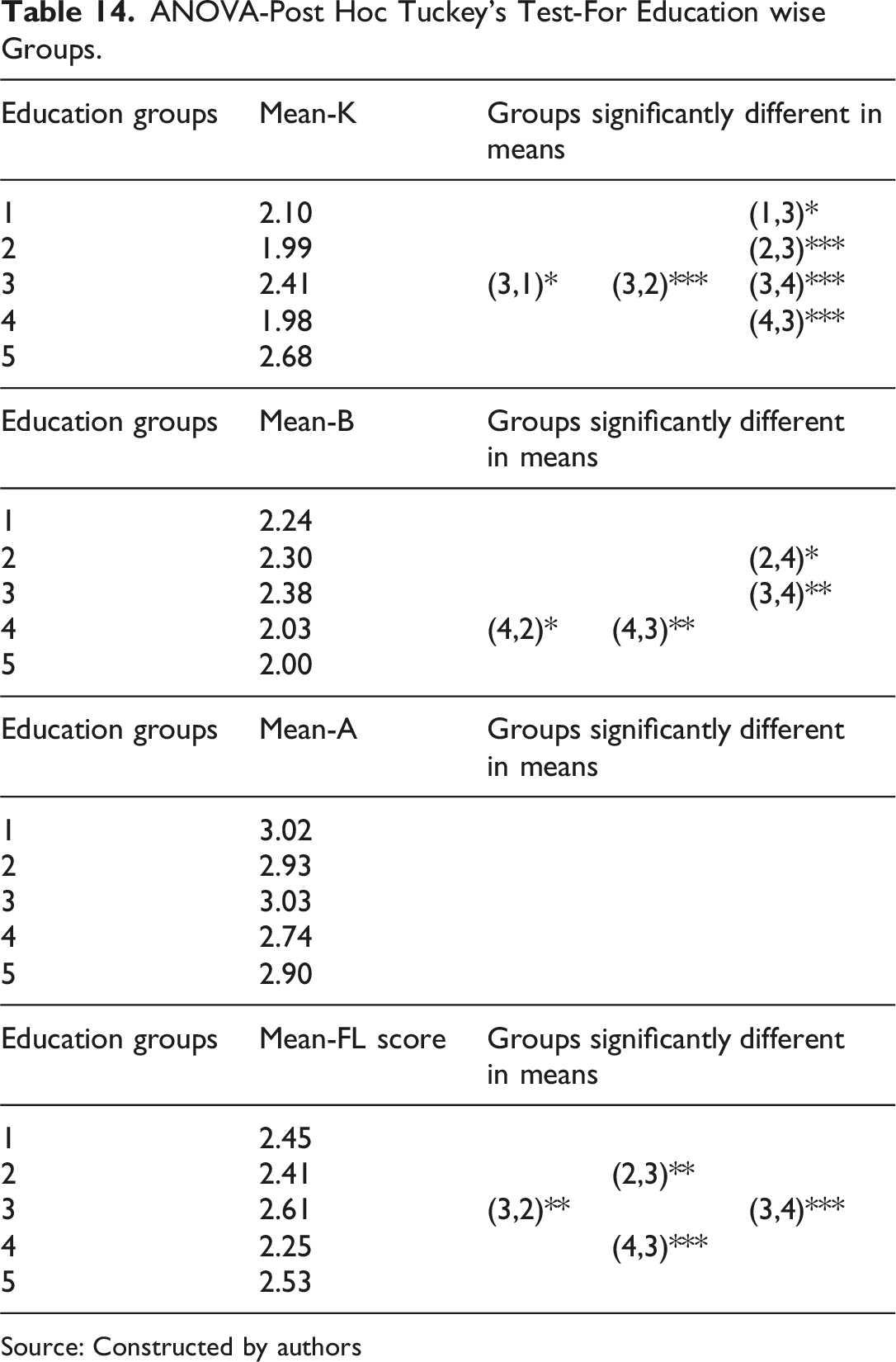

ANOVA-Post Hoc Tuckey’s Test-For Education wise Groups.

Source: Constructed by authors

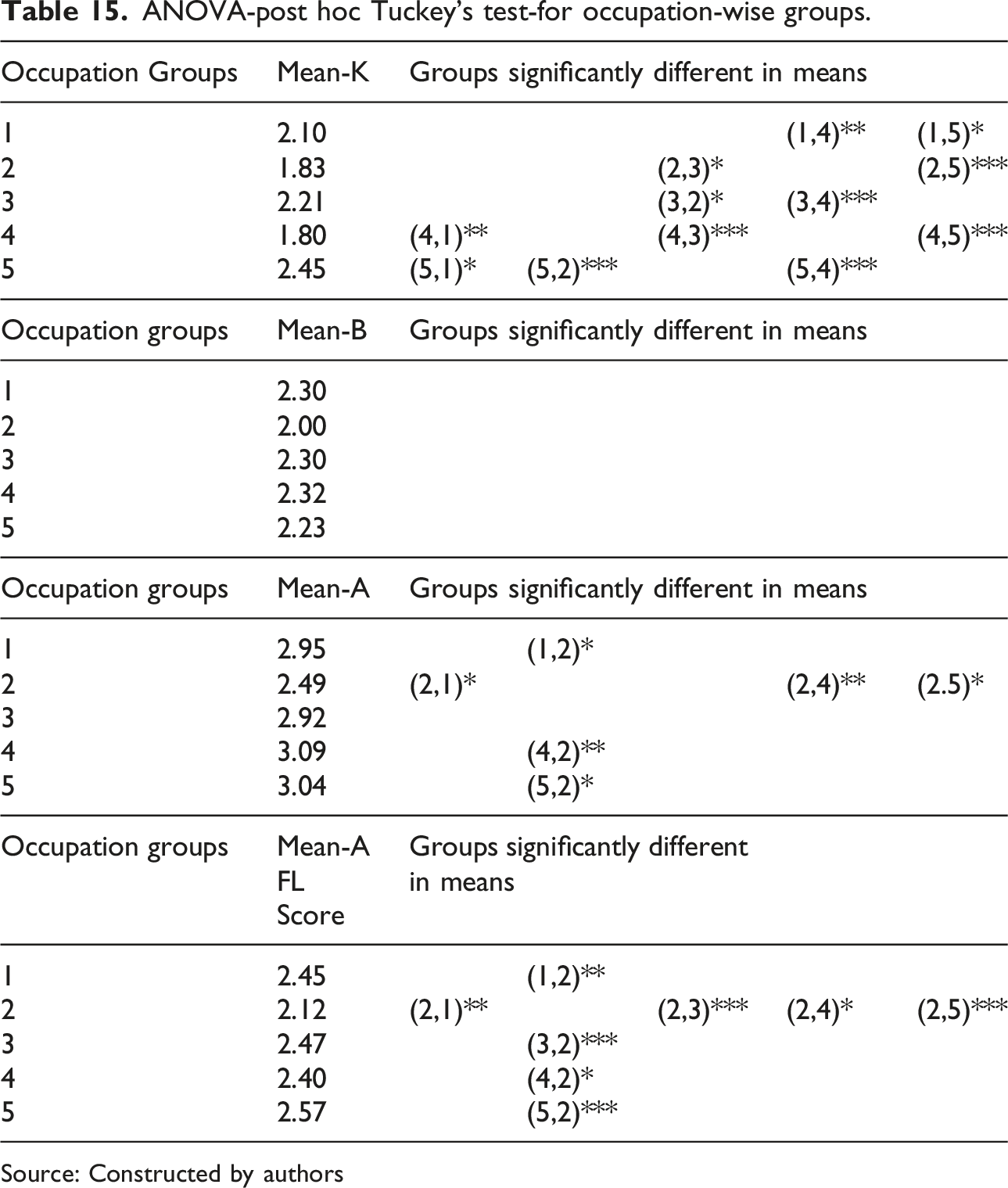

ANOVA-post hoc Tuckey’s test-for occupation-wise groups.

Source: Constructed by authors

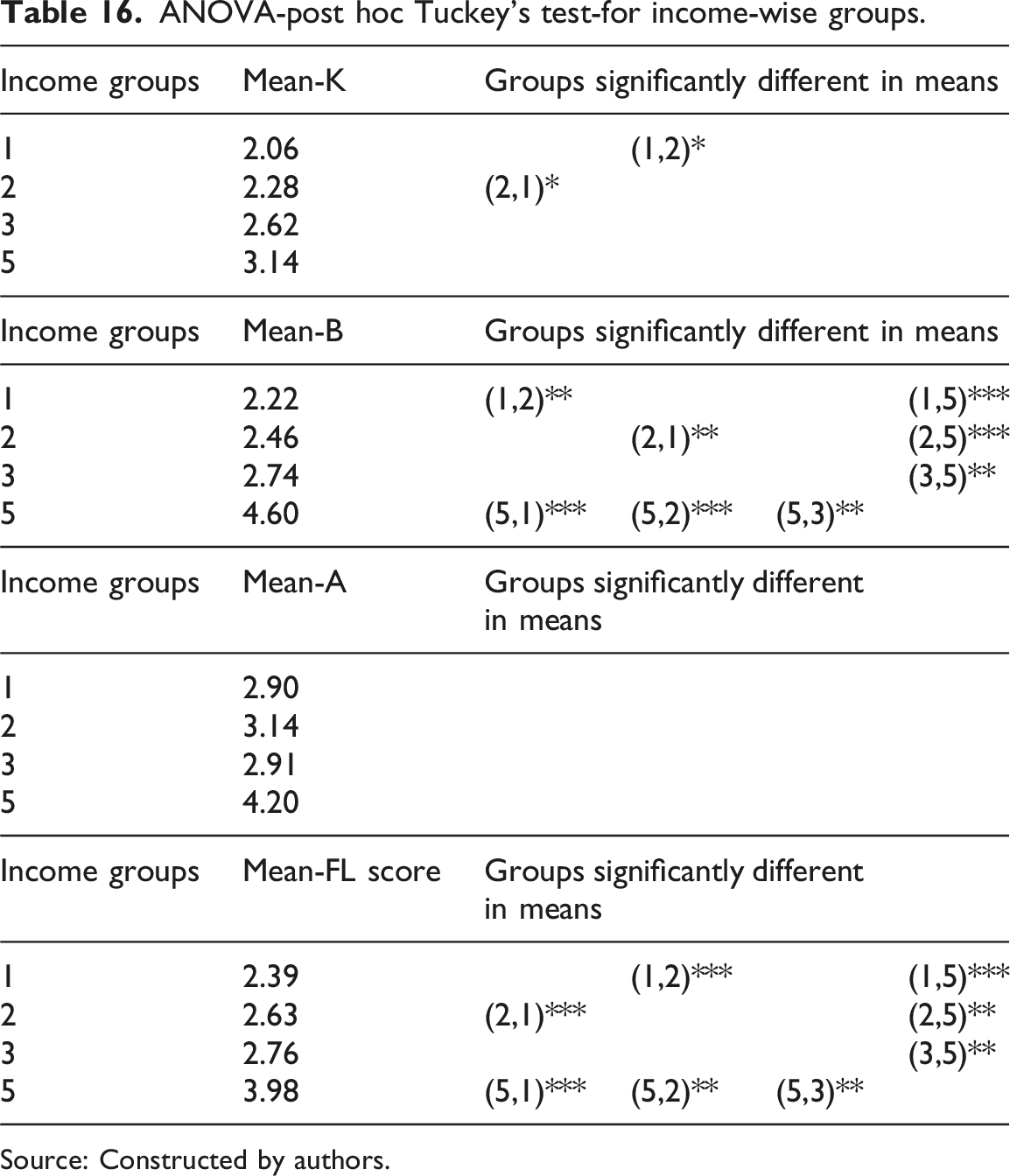

ANOVA-post hoc Tuckey’s test-for income-wise groups.

Source: Constructed by authors.

Conclusions

We have developed a validated scale for measuring the financial literacy of the rural population in India. As far as the authors know, few attempts have been made in India to develop such a scale. The questionnaire has been prepared based on a literature review and comprises questions on knowledge, behavior, and attitude. The questions are simple and relate to the respondents’ financial environment. Also, the level of questions matches the respondent’s level of financial engagement. The explanatory variables identified in the literature include gender, age, education, income, occupation, and binary variables such as gender, family head, and bank account. The relationships between these variables and knowledge, behavior, and attitude factors have been examined. The reduction of questions and validation was achieved through a series of 5 studies. While conducting a survey, we took the necessary measures to avoid common method bias. 55 The construct has been validated through exploratory and confirmatory factor analysis. Structural Equation Modelling was performed using SPSS AMOS-25. Finally, the factors associated with financial literacy were identified using ANOVA.

The study’s findings reveal that the financial literacy score for male family heads is higher than that of their female counterparts who are not family heads. Furthermore, the labor category has the lowest score, followed by homemakers. Financial literacy is associated with age, income, education, and occupation. Moreover, education and income are found to positively associated with financial literacy. It was found that male respondents’ knowledge and behavior scores were significantly higher than those of female respondents. However, the “attitude” score of female respondents is significantly higher than that of male respondents. It is therefore concluded that financial literacy is significantly varied across gender. It is further observed that being “head of the family” or having a “bank account” significantly impacts knowledge and “behaviour.” Therefore, it is established that both these parameters positively associated with financial literacy. Furthermore, it was found that the average scores for “knowledge” were high for young respondents (18-23) and the mature group (above 40). The average score for the factor’ behavior’ is highest for the respondents above 40, and the financial literacy score is found to be highest for the age group of 30-35 years. Thus, it is concluded that financial literacy is influenced by age, with higher levels among the young and mature, but lower among those aged 36 to 40. The component’s “knowledge” score is lowest for “illiterate” respondents and highest for “postgraduate” respondents. This shows that education positively and significantly affects the “knowledge” components of financial literacy. Moreover, the “labor” category scores for all the components are low. The “knowledge” score is lowest for the “housewife” category and highest for students. However, the scores for “behavior” and “attitude” among housewives are the highest. Financial literacy score shows significant differences across almost all occupational groups. It is observed that “knowledge,” “behavior,” and financial literacy scores increase with income. Moreover, the scores for all three financial literacy components, namely, “knowledge,” “behavior,” and “attitude,” are highest for the high-income group (with an annual income of more than Rs. 1 million).

Limitations and policy implications

This study was conducted in one state of India. For generalization to the wider areas, it needs to be tested across various geographic regions. We propose testing the model across various regions as a future direction for the research. This scale can be used to measure financial literacy in rural areas and to formulate strategies to improve it accordingly. It is important to note that knowledge-based financial literacy should be made context-specific, that is, tailored to different segments, such as farmers versus business people. The curriculum needs to be designed to meet the needs of different segments. Further, financial literacy initiatives should also ensure a focus on different aspects of financial literacy, that is, not only knowledge but also attitude. The findings of the present study are unique in the following aspects, which have policy implications: (i) Financial literacy is improved by opening bank accounts, (ii) The female members have significantly better scores in “attitude” as compared to their male counterparts; however, their “knowledge” scores are lowest. (iii) Education improves financial literacy (iv) Housewives are the best in “behavior” and “attitude.” (v) Improving the people’s income will enhance their financial literacy.

Based on these findings, it is suggested that the following measures be initiated to improve financial literacy amongst rural people in India. (i) Efforts should be made to open bank accounts for all unbanked adults and to provide them with income-generating activities and (ii) The focused financial literacy programs should be developed and conducted for women, homemakers, and the labor class. As they are better in their attitude and behavior, financial knowledge will help improve their financial literacy. The latter program will help reduce malpractices and financial exploitation of people experiencing poverty. However, such programs should be grounded in day-to-day experiences and learners’ local context, and supported by specially designed teaching aids, such as learning through viewing and the enactment of practices. 86 (iii) Financial literacy should be introduced in the school and graduation curriculum and (iv) financial literacy should be included in all skill development programs. (v) As one of the components of our model was government schemes, we suggest that awareness camps by banks should be conducted in rural areas to make them aware of recent programs and their benefits. The study needs to be tested in infrastructure-deficient areas of India, such as the northeastern states, desert regions like Jammu and Kashmir, and the Ladakh region.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Declarations

• This manuscript has not been published in any form.

• “The material in the manuscript will not infringe upon any statutory copyright.”

• “The paper will not be submitted elsewhere while under JFCP review.”