Abstract

The aim of this article is to explain the factors that underpinned the expansion of the Spanish shipbuilding industry during the Francoist regime, when it grew to rank fourth in the league of shipbuilding nations in the 1970s. After a brief description of the evolution of its output and markets, the article focuses on three aspects of shipbuilding: technology and costs; industrial structure and ship specialisation; and, above all, the strong government support that made this industry one of the symbols of the international success of the Franco’s new developmental policies.

Although the rise of shipbuilding in Spain appears to have taken some people by surprise, it is, with the development of the holiday industry, the facet of the Spanish economy best known abroad … Spain to-day in effect is the third shipbuilding country.

The Spanish shipbuilding industry has traditionally been considered one of the prime examples of economic development during Franco’s regime: a sector initially concentrated on the domestic market, which after the 1960s focused increasingly on the international front (by 1970 it was the industrial sector with the greatest propensity for export) and which made Spain one of the world’s leading producers in the 1970s behind Japan, Sweden and Germany. During this period, along with other manufactured products such as footwear, ships topped the list of Spanish exports. 1 The Francoist regime, in fact, frequently extolled the sector as one of the leading examples of its successful development policy. Traditional explanations, using an applied-economics methodology, emphasise a number of factors, such as the export backup instruments wielded by the governments of the time, the low labour costs of a relatively well-qualified workforce, and the dearth of industrial conflict. 2 The evidence furnished in this article suggests that the competitiveness of Spanish shipyards was more the result of government interventions than other factors. In an international market such as the shipbuilding sector, with very little transparency (and in which the main yards were generously assisted by their respective states), it was financing terms, rather than prices, which were usually the primary factor influencing potential buyers. Thus this article will focus on aid from the state, which was also directly and heavily involved in the sector through tariff policy and, most especially, through concessions of public monies in the form of construction premiums, tax breaks, export credits and the Concerted Action programmes implemented in shipbuilding. Other factors will also be referred to, such as Spanish shipyards’ production specialisation, foreign technology transfer and the implications in terms of access to external markets.

The article comprises the following sections: first, there is an examination of output figures, exports and foreign markets for Spanish shipyards from 1950 to 1979; this is followed by an analysis of the industrial structure of the sector and specialisation in different types of vessels, and the implications for exports and international competitiveness; and finally, there is an assessment of the impact and role of state aid. Even though the conclusions of this article need to be borne out by a more ambitious research effort (on the mechanisms for access to markets, for instance), a clear explanation emerges; that is, more than low labour costs, the export success of Spanish yards during this period was largely due to the low cost of capital and the concealed dumping perpetrated by the authorities, against an international backdrop of ever-increasing demand.

Shipbuilding output, exports and markets, 1950–1979

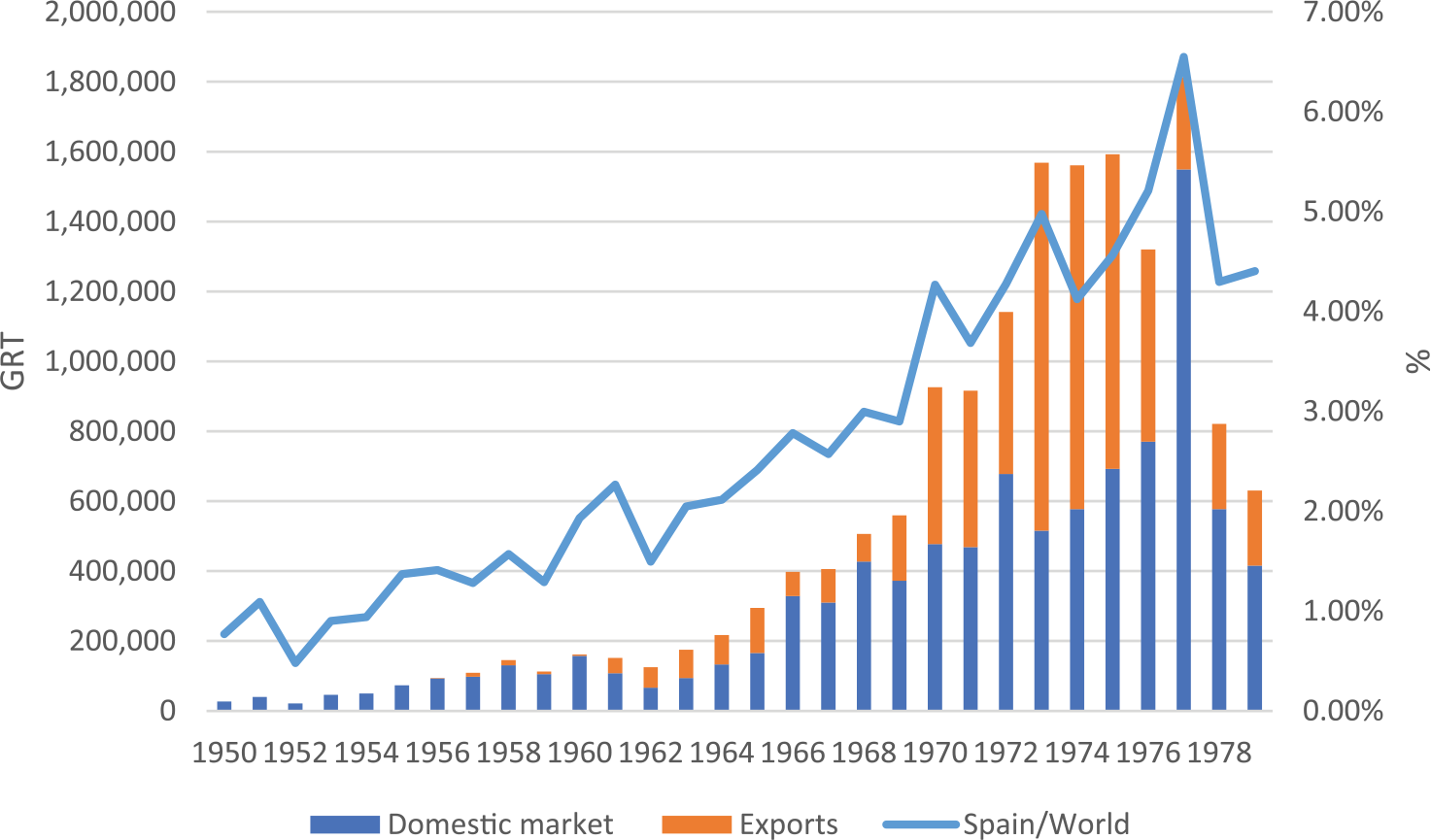

The Spanish shipbuilding industry experienced substantial growth throughout this period, especially during the years of so-called ‘Developmentalism’, with production rising from a gross registered tonnage (GRT) of 160,000 in 1960 to a GRT of over 1.6 million in 1975, peaking at an all-time high in 1977 when it topped 1.8 million (see Figure 1). Whereas in the first half of the 1950s, the country had accounted for less than 1 per cent of world shipbuilding tonnage, by the 1970s Spain accounted for more than 4 per cent, making it the world’s fourth largest producer after Japan, Germany and Sweden. 3

Spanish shipbuilding output by markets and world share, 1950–1979 (GRT).

This expansion was due partly to a surge in demand in both the domestic and foreign markets, and also the increased availability of sheet steel for ship construction, which had been the main handicap in the sector in the 1940s and 1950s. 4 By 1960, the sector’s production capacity far outstripped the needs of the domestic market, mainly due to the expansion policy implemented in the 1940s and 1950s at the outset of Franco’s regime by Spain’s National Industry Institute (‘INI’), which had established two new shipyards in Seville and Ferrol (the property of the public companies Elcano and Bazán) and had taken over a third yard, Astilleros de Cádiz; and also due to a less well-known process that entailed the overhaul of machinery and production equipment, and the widening of slipways, during the late 1950s. 5 The Spanish Shipbuilders’ Association (Construnaves) was created in 1959, and one of the first steps it took was to establish a Technical Commercial Service to help boost exports. The scheme focused on enhancing slipway usage and reducing costs. 6 In any case, the problem of surplus capacity was the keynote throughout the 1960s. 7

Although some vessels were exported in the course of the second half of the 1950s (accounting for six per cent of total output), almost all authors agree that the sector’s export business took off in 1960. Fairplay dubbed this the year in which the Spanish shipbuilding industry ‘was put on the map’. 8 Over the entire period between 1960 and 1979, exports accounted for 42 per cent of production, performing better during the 1970s (45 per cent) than in the preceding decade (28 per cent). They reached a much higher proportion, however, in 1970–1974, accounting for over 55 per cent of output. In the 1960s, exports performed better in the first half of the decade, accounting for 33 per cent of output, than in the second, when they represented 29 per cent. In the latter half of the 1970s, exports accounted for 35 per cent of total output. Between 1964 and 1975, vessel exports represented more than a quarter of Spain’s equipment goods, and between three per cent and six per cent of total exports. 9

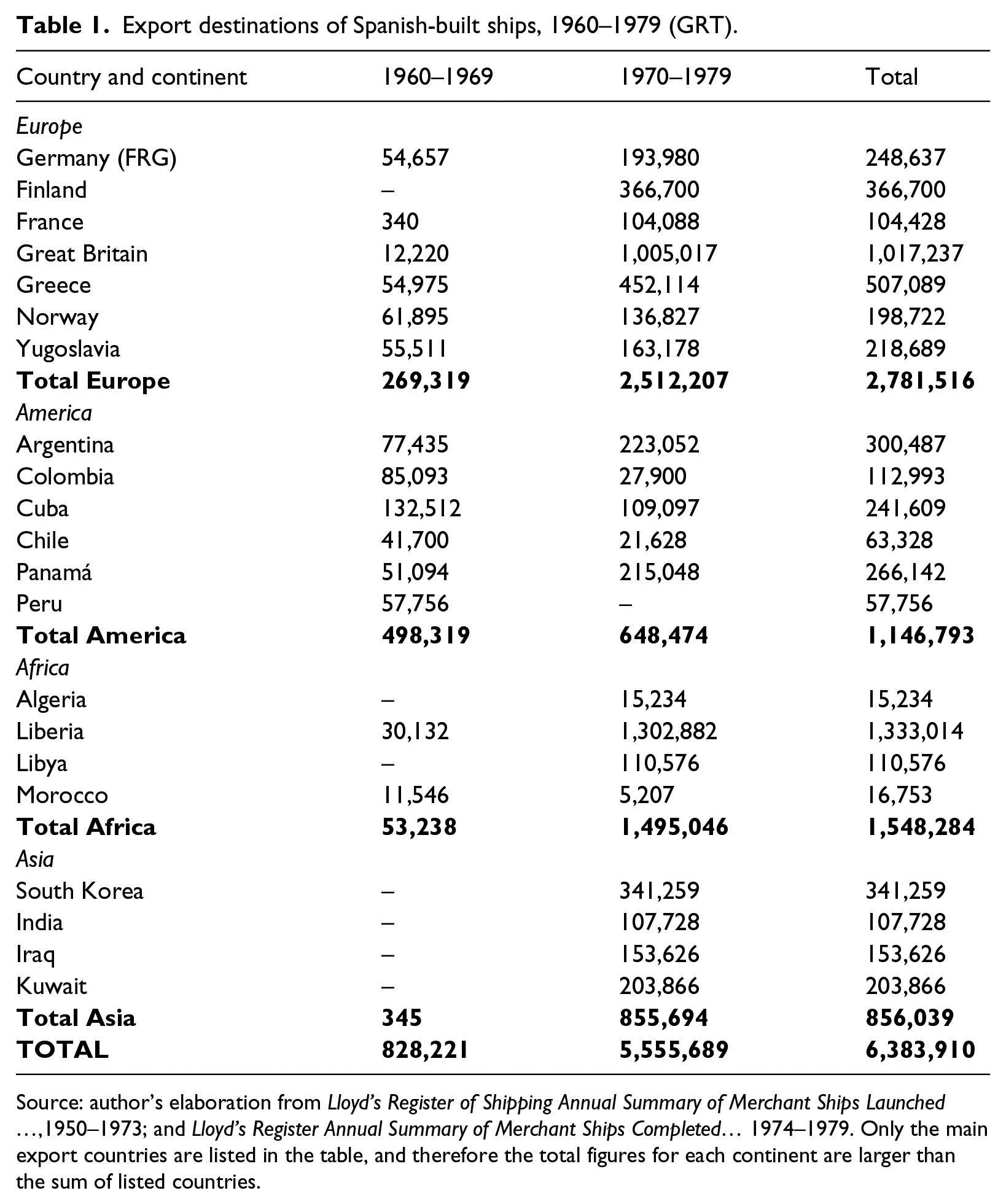

Most exports of Spanish ships in the second half of the 1950s (33,363 GRT) were destined for the Latin American market: Colombia, Paraguay and Brazil took up 73 per cent of the exported tonnage between them, the remainder being a cargo ship sold in Britain, the largest vessel exported by Spanish yards during this period (see Table 1). Latin America was the largest foreign market in the 1960s, representing 60 per cent of exports. 10 It was followed up by Europe with 32 per cent and, well behind, Africa with six per cent. Spanish shipyards took full advantage of the close links – trading and cultural – between Spain and the republics of Latin America. In the case of Cuba, the largest market of all, Spain called up its historic links to the island, ignoring the US embargo decree and opposition. 11 In the case of Argentina, a large volume of exports in the course of this decade related to the Hispano–Argentinian agreement to pay off Spain’s debt with ships for Argentina’s merchant navy. 12 A considerable portion of exports were fishing craft, because some Latin American countries needed to enlarge and renew their fleets and required Spain’s experience in this field. 13 Indeed, in 1967, Fairplay acknowledged that Spain was the main supplier of new ships in Latin America. 14

Export destinations of Spanish-built ships, 1960–1979 (GRT).

Source: author’s elaboration from Lloyd’s Register of Shipping Annual Summary of Merchant Ships Launched …,1950–1973; and Lloyd’s Register Annual Summary of Merchant Ships Completed… 1974–1979. Only the main export countries are listed in the table, and therefore the total figures for each continent are larger than the sum of listed countries.

In the 1970s, however, Spanish shipyards were competing in more developed markets, where access was more difficult and the conditions of international competition much tougher. Europe had become the main destination for Spanish ship exports, and now accounted for 45 per cent. The American market had fallen back to fourth place (12 per cent), surpassed by Africa, now taking up 27 per cent of exports, and also Asia, with 15 per cent. Within Europe, the United Kingdom had become the largest market, a phenomenon related to the serious lack of competitiveness in British yards. 15 It was followed up at some distance by Greece and Finland. 16 Liberia, one of the world’s major flags of convenience and an open market with much competition, was the largest market in Africa. In Asia, South Korea was the main buyer, followed by a number of leading oil exporters such as Iraq and Kuwait, countries with which Spain had good diplomatic and trading relations (as it did with almost all North African countries). 17

Industrial structure, ship specialisation and the implications for competitiveness and exports

During this period, the Spanish shipbuilding industry had a twofold structure. On the one hand, there were a small number of large shipyards (Sociedad Española de Construcción Naval, Euskalduna, Unión Naval de Levante, Astilleros de Cádiz, ASTANO) specialising in the construction of larger vessels using relatively simple technology, for which demand had soared: oil tankers and cargo vessels (bulk cargo or general cargo). In this segment, which contributed the bulk of exports during at least the entire decade of the 1960s, the hand of the state was most apparent. There were also a large number of small and medium-sized yards specialising in the construction of fishing vessels. 18 As Table 2 shows, oil tankers and cargo ships accounted for more than 90 per cent of the tonnage built in Spain between 1967 and 1979, but for only 31 per cent of the actual number of vessels. Conversely, fishing craft represented 55 per cent of the number of vessels, but only four per cent of the tonnage.

Spanish shipbuilding output by types of ship, 1967–1979 (number and GRT).

Source: author’s elaboration from Lloyd’s Register of Shipping Annual Summary of Merchant Ships Launched …,1950–1973; and Lloyd’s Register Annual Summary of Merchant Ships Completed… 1974–1979.

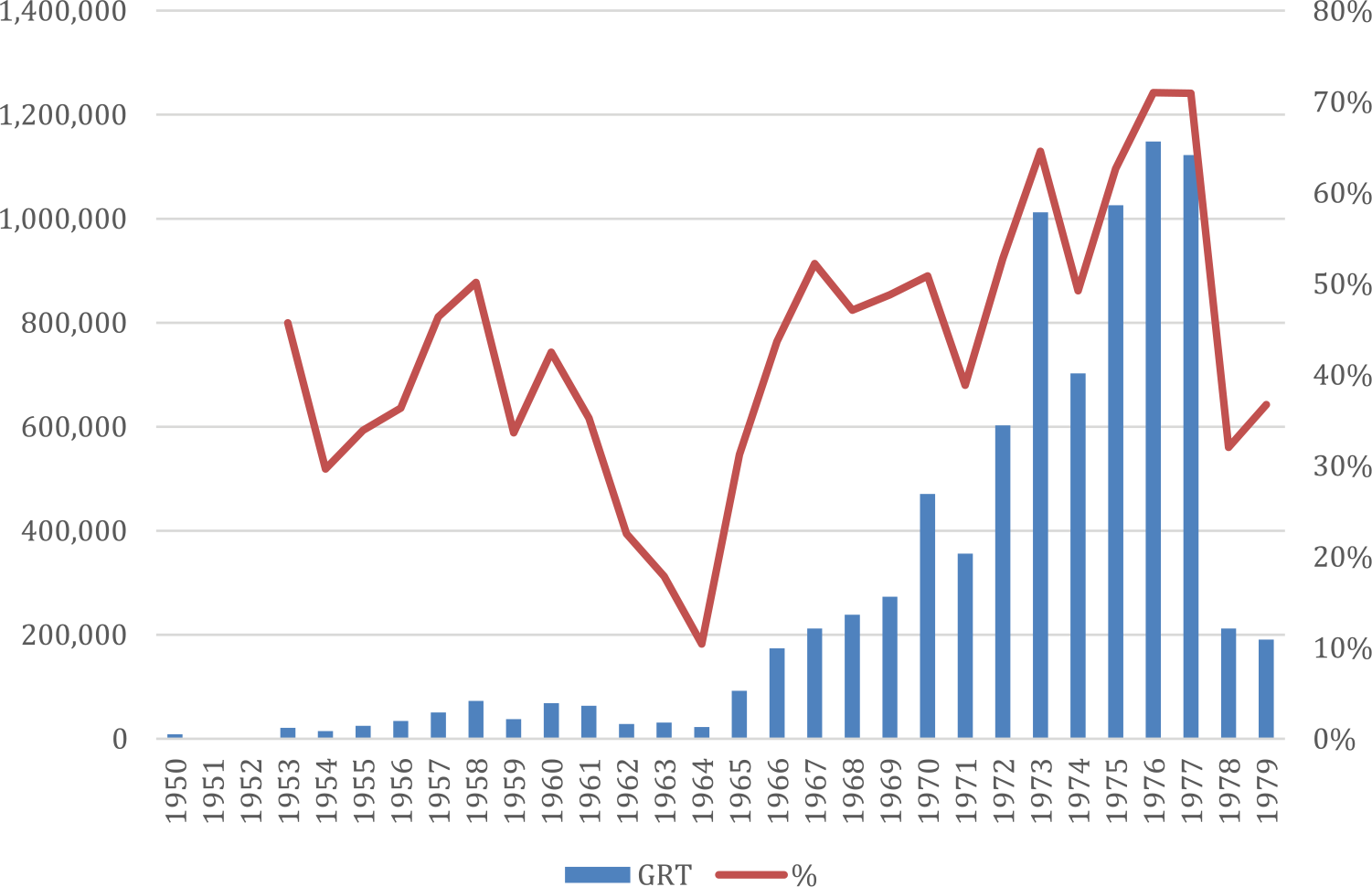

Like other leading shipbuilders of the time, especially Japan and Sweden, Spain increasingly specialised in the construction of large oil tankers, demand for which rose faster than for other types of vessel on both the domestic and foreign markets. 19 Spanish crude oil imports rose significantly during this period as a result of the country’s intense and rapid economic development. Refining capacity multiplied at this time, from two refineries with a total output of 1.15 million tonnes in 1950 to 9 refineries with a capacity of 40 million tonnes by 1971. 20 Most Spanish refineries had links with major international oil groups such as Continental Oil, with interests in the Algeciras refining plant, or Gulf Oil, which controlled 38 per cent of the equity of the Somorrostro refinery near Bilbao. The stakes held by these shareholder groups helped them secure Spanish government permits to freely import part of their crude oil requirement. In return, they undertook to enter into contracts with Spanish yards for part or all of the shipping fleet required. 21 Indeed, although in the first half of the 1960s oil tankers accounted for 25 per cent of total production (in GRT), in the second half this rose to 46 per cent. In the 1970s, the proportions were 53 per cent and 61 per cent (see Figure 2). In the first half of the 1970s, Spanish shipyards built the world’s largest oil tankers, following up behind the Japanese. 22

Oil tankers built in Spanish shipyards, 1950–1979 (GRT and % over total output).

Up to the mid 1960s, surplus capacity in the sector enabled the Spanish yards to offer very short ship construction lead times, and in certain situations this was a decisive factor in landing contracts. 23 As of this point, however, discussions ensued in relation to the need to boost the production capacity at Spanish shipyards. 24 It was against this backdrop, which was also characterised by Europe’s obsession to compete in terms of size with the largest Japanese shipbuilders, that a business concentration process was set in motion by the state. 25 This business concentration not only entailed an increase in the average size of companies, but also strengthened the oligopolistic trend in the sector. These variables showed positive correlation with another characteristic of the industry, the intensity and speed of foreign technology transfer by means of technical assistance contracts and licences operated by the main companies involved. 26

Technology and costs

Technology transfer through technical assistance contracts and licences helped companies to rapidly upgrade their operation, but this restricted the scope for gaining access to world markets, due to the habitual clauses in such contracts. However, with respect to the shipbuilding industry, it ought to be pointed out that the licences were specifically used to manufacture ship engines and other components, the design and production of which had already been officially standardised. They could not be applied to processes involving the design, assembly and finish of vessels, where technology was in many cases transferred on an informal basis, and in practice this meant that the Spanish yards could gain access to world markets with no restrictions. 27 In fact, many manufacturers of engines, machinery and other components eventually exported these items already fitted to the vessels. 28

One example of this was the rapid spread of the principle of standardisation of the design and construction of ships in Spain, which was taken up by the yards and also encouraged by the state. Standardisation was fully in step with another principle which was undertaken by Spanish shipyards in the 1950s, that of scientific management. 29 Of all Spain’s shipbuilders, it was perhaps the Euskalduna yard that was the first to embrace standardisation. In 1968, the company declared it had achieved ‘full standardisation in the work carried out at our yard’. That same year it offered four types of standard vessel (three bulk-carriers and a refrigerated cargo vessel), which were warmly welcomed by both the domestic market and by foreign buyers, especially the Santa Fe series. 30 Mass production of vessels enabled the yard to reduce costs and lead times, and to boost its productivity. 31 It was reported in 1973 that Spain was a competitive country, particularly in terms of certain types of standardised vessels, despite rising wage costs and more expensive raw materials and components. 32 In this scenario of a commitment to standardisation, some mention should be made of the introduction of a major innovation in ship design, the FORAN integral computer-assisted design system, developed and patented by Spanish engineering company SENER. 33 Visible progress was also made by the industry in the manufacture of diesel engines for vessels and other ship components, in all cases on the basis of products or prototypes originally imported and built through licences. 34

The fact was that in the mid-1960s there were no visible differences between the technology used (machinery and equipment) by Spanish shipyards and their European competitors. Most of the machinery and equipment used originated in countries that specialised in building these items. 35 The authors of a number of studies at the time observed that one of the comparative advantages enjoyed by the Spanish shipbuilding industry lay in the peculiar combination of a relative abundance of business experience and qualified labour (due to its previous industrial tradition), with few industrial conflicts and considerably lower wages in relation to wage costs in western Europe. Conversely, other developing countries (Greece, Portugal, South Korea and Brazil), where wages were similar or even lower, lacked the experience and qualifications of the Spanish workforce. 36 In any case, some of these studies also observed that the ultimate repercussions of low wages on total costs were limited due to levels of productivity, which were lower than in the shipyards of more developed nations. 37 According to a number of reports, the advantage of low labour costs gradually petered out in the 1960s due to a rapid surge in wages, which outstripped other countries, and also because of an increase in productivity. 38

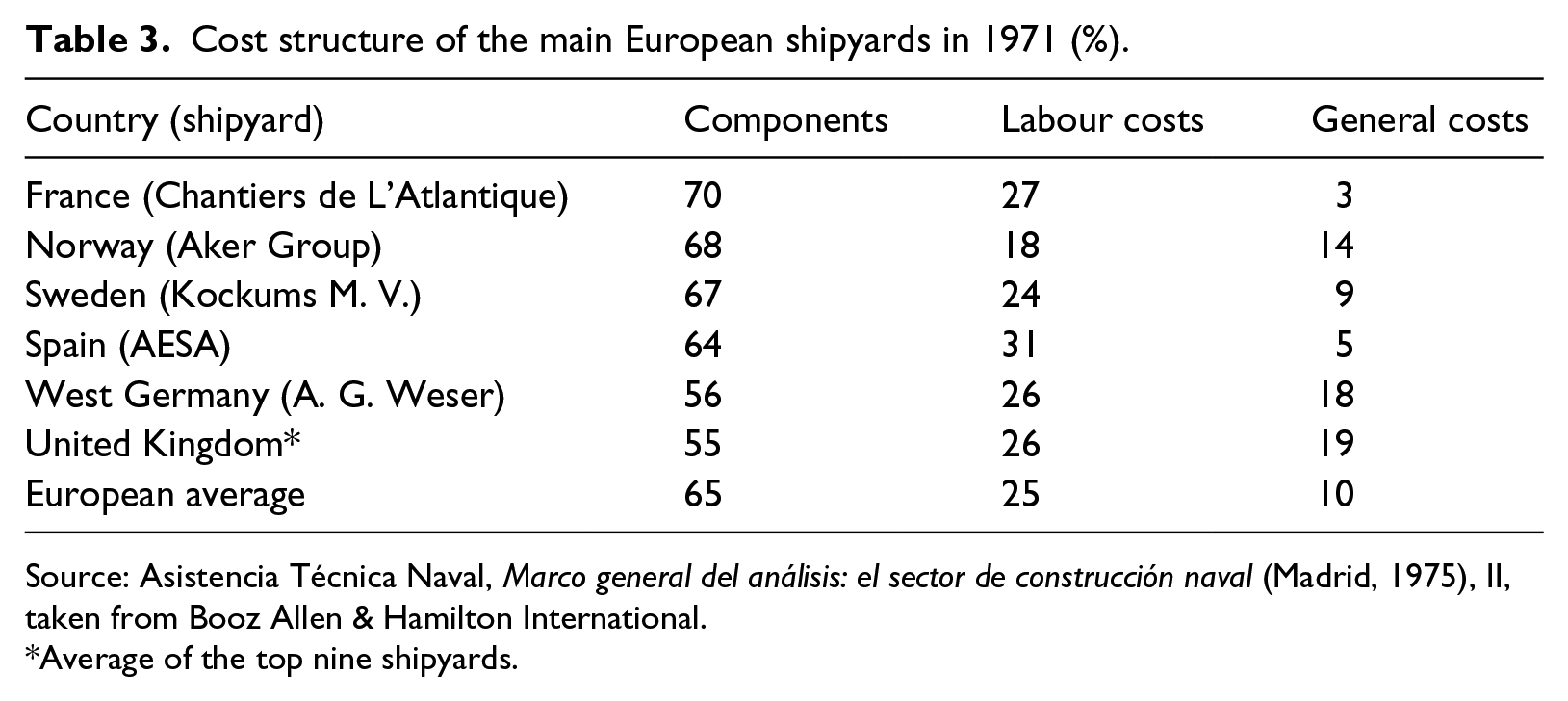

In the early 1970s, the cost structure of Spain’s shipbuilding industry was by and large no different to the European average (see Table 3). At first glance, however, it is rather surprising to find that Spanish staff costs were the highest of all the countries covered by the sample. The ship engineering consultant who drew up the table considers this discrepancy is probably due to different accounting procedures for the various items; specifically, employers’ social security contributions would be booked under general expenditure in European shipyards and not under staffing costs, as in Spain, although they admit this assumption has not been verified.

Cost structure of the main European shipyards in 1971 (%).

Source: Asistencia Técnica Naval, Marco general del análisis: el sector de construcción naval (Madrid, 1975), II, taken from Booz Allen & Hamilton International.

Average of the top nine shipyards.

The role of the state: A protected domestic market and an abundance of public funds on a discretionary basis 39

The shipbuilding policy applied during Franco’s so-called ‘Developmentalism’ made no major changes to the guidelines laid down in Spain’s Merchant Navy Renewal and Protection Law of May 1956, which reserved the domestic shipbuilding market for Spanish yards, and in return offered ship operators cheap credit terms as compensation for the obligation to build ships in Spain. The only OECD countries to operate such high levels of protection of their domestic markets were Japan and Turkey. 40 Elsewhere, the country with a policy more closely resembling the Spanish system was South Korea, which intervened in the 1960s in favour of its shipyards, and most particularly the export of vessels, at the cost of shipowners’ interests. 41

The 1960 Tariff is a valid example of this policy to support shipyards. On the one hand, in the unlikely event a shipowner obtained an import permit, it would have to pay an average tariff of 20 per cent on the value of the vessel, the highest rate applied by any OECD country. 42 On the other hand, it established a special classification for sheet steel for vessels, with a 5 per cent tariff, while the tariff set for other iron and steel products exceeded 35 per cent. 43 It also established a permit for the free importation (with no tariff payment) of some materials to build ships for export, a measure that was not initially applied to vessels for the domestic market. 44 The intention was to reduce the disadvantage posed by the Spanish shipbuilding industry’s need to import part of its steel, other raw materials and components, and the consequent adverse repercussions on competitiveness. 45 In any case, the shipyards requested a broader exemption. Enrique Sendagorta, who was managing director of SECN and chairman of Construnaves, repeatedly complained in the mid-1960s about a policy of tariffs applied to imports of shipbuilding materials and components (with the exception of a small amount that was exempt from tariffs), with serious repercussions for the final price and competitiveness. 46 Indeed, around 1970, steel prices in Spain were still higher than in other competitor countries, such as Japan. There were also problems in relation to regular supplies that obliged Spanish shipyards to hold stocks of steel representing the equivalent of two months’ production, compared to between five and ten days’ work at Japanese yards. 47

One concern that was even more important than the reservation of the domestic market was the considerable state aid offered to the shipbuilding industry. This was for several reasons. First, as stated in the OECD report and by many other writers, in a sector with such an overcapacity and fierce competition from abroad, most shipyards received government aid. 48 Also, more so than the prices offered, it was financing terms that played the key role in the award of construction contracts. 49 In this situation, the Spanish yards, like their competitors, were compelled to finance their customers in the short and medium term, and this led to some very serious liquidity problems indeed. In the 1960s, Spanish shipyards were forced to undertake long-term debt to maintain levels of production, which explains the ever-increasing presence of banks among the shareholders of private yards and a greater dependence on the preferential financing conditions granted by the state. 50 In the 1970s, Fairplay reported a shortage of capital as one of the major problems facing Spanish shipbuilders struggling to manage their order books. 51

Throughout Franco’s regime the merchant fleet and shipbuilding were two of the sectors that gained most from the preferential finance circuits fostered and regulated by the state, circuits where the discretionary criterion of the authorities favoured a strategy to seek out revenue by businesses, either individually or by sectors. 52 Between 1965 and 1975, the financing circuits channelled an average of four out of every ten pesetas of total funding for the private sector. 53 In the case of the shipyards, there were various types of aid: outright subsidies such as shipbuilding premiums, tax incentives and, at a later stage, the Concerted Action programme; and preferential credit terms, such as those applied to ship exports.

The shipbuilding premiums aimed to offset cost differences between Spanish yards and their foreign counterparts. A rather low fixed amount had been established until the 1956 Law was introduced. Henceforth, it was established as a percentage on the basis of the value of the vessel (9 per cent if the propulsion unit was manufactured in Spain, and 6 per cent otherwise). After 1959, shipbuilders were entitled to a different kind of assistance in the form of tax breaks, which were initially granted for exported vessels, and this included ships for the domestic market as of 1966, at 12 per cent on the value of the vessel (after the premium had been deducted). 54 The aid scheme for shipbuilders, like the naval credit system for shipowners, gave rise to a large number of practices that circumvented or infringed the law and enabled shipowners and shipyards to secure more capital and more operating subsidies respectively than those laid down in law. 55 Several authors have claimed, but not actually proved, that a common practice was to artificially inflate the prices of vessels in order to boost aid, and that this practice was known about and even assisted by the authorities – the Merchant Navy Subsecretariat, in this case, which was tasked with appraising the value of the vessels on which credits and aid were based – in order to drive up the credit coverage afforded to the shipowners and the direct subsidies paid to the yards. However, as Pastor admits, any examination of this practice ‘poses all kinds of difficulties in view of the secrecy surrounding it and the fact that it was obviously illegal’. Likewise, Arias concedes that this kind of fraud is ‘difficult to prove’. 56

Private documentation from business files sheds some light on these practices. Although my references are in relation to ships built for the domestic market, there are no arguments to cast any doubt on their application to vessels for export. The Naviera Aznar company, for example, signed a contract with the Euskalduna yard in 1967 to build the bulk carrier Monte Zapola for 258.7 million pesetas, and the premiums and tax breaks went to the shipyard. The Merchant Navy Subsecretariat’s appraisal put the official value of the ship at 379.7 million pesetas, a 46 per cent mark-up on the real price. This brought in 75.6 million pesetas for the yard in premiums and tax incentives, 24 million pesetas more than it would have received if the real price had been applied, and Naviera Aznar secured a credit of 231.8 million pesetas, when the price it had to pay the shipyard, less the premiums and tax breaks, was only 207.2 million pesetas.

57

The case of the Monte Zapola was apparently not an exception, but rather the norm, although of course the benefits obtained depended on the difference between the official appraisal and the real value of the ships. In 1969, Juliana Constructora Gijonesa reported to Naviera Aznar as follows:

We hereby declare that the contract valid for construction of a 6,400 DWT timber carrier, construction nº 193, is that signed on 10 August 1968, in the amount of 105,000,000 Ptas., and that the contract signed by both our Companies on 9 April 1969 shall only be valid for the purposes of naval credit.

58

Some considerable differences may also be observed in the ferries built by Unión Naval de Levante for Naviera Aznar on a 1971 contract. In the case of the Monte Granada vessel, the Subsecretariat’s appraisal was 24 per cent more than the real price, giving the yard a subsidy of 252.9 million pesetas in premiums and tax breaks, 38.5 million pesetas more than it would have received with the real price. Naviera Aznar, meanwhile, obtained a credit of 1,138 million pesetas, when the price it had paid the shipyard was 1,125 million pesetas. In this case, however, the disagreements that arose between Naviera Aznar and the shipyard due to the yard’s considerable delay in delivery of the ferries led to legal proceedings between the two parties, which commenced in 1974 and ended with an arbitration ruling in the autumn of 1976. Both parties acknowledged there were two contracts, an official contract stating a higher price than the real price in order to secure more credit, premiums and tax incentives, and a real price, establishing the sum to be paid to the shipyard by the operator. 59 There were also differences between the real price and the official price for vessels built by other companies in the Aznar group, such as the ro-ro ships ordered from Astilleros y Construcciones of Vigo by Naviera de Exportación Agrícola in 1975, although these were on a smaller scale. 60

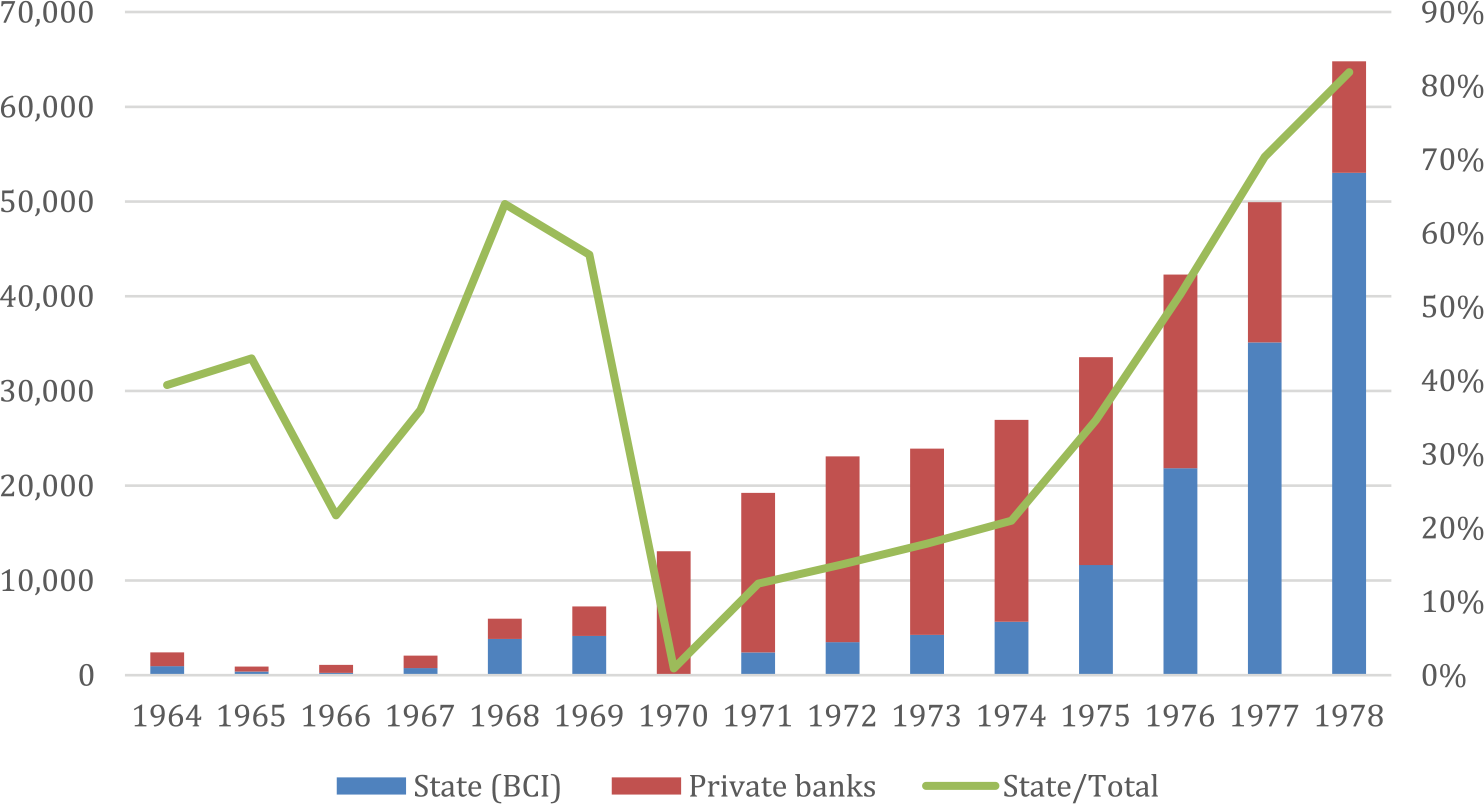

Spanish shipyards therefore received a generous amount of public funds as construction premiums, in addition to tax incentives. But that was not all. Like many other countries, after 1960 Spain operated an export credit system involving both public and private banks, with interest considerably lower than the official market rates. 61 This instrument was used to help the yards to sell outside Spain, by enabling them to offer financing terms to buyers at least similar to those offered by competitor shipyards in other countries. 62 In the 1960s, most of the state’s ship export credits were granted through the state-owned Banco de Crédito Industrial. Between 1970 and 1975, however, private banking accounted for almost all export credit. After 1976, when banks withdrew from the sector, most credit was again supplied by the state (see Figure 3). 63

Ships’ export loans to Spanish shipyards, 1964–1979 (million pesetas).

The last chapter in state aid for the sector was the Concerted Action programme in the shipbuilding industry, which was approved in 1967 and granted tax and credit incentives of up to 4,000 million pesetas between 1968 and 1971. The main objective of the Ministry of Industry was to foster the concentration of Spanish yards in order to streamline production capacity, make use of economies of scale, and boost competitiveness. But there were other more specific reasons too: on the one hand, the serious financial difficulties of shipyards and their main shareholders and creditors, the state in the case of Astilleros de Cádiz, and Banco Urquijo and Banco Hispano Americano in the case of SECN and the Euskalduna yard; there was also a situation, of which the Minister of Industry, Gregorio López-Bravo (a naval architect who had been managing director of SECN in the late 1950s), was well aware – a considerable overcapacity within the sector, not unrelated to the policy operated by the INI in the 1950s. 64

The most visible outcome of the Concerted Action programme, though not the only outcome, was the creation of Astilleros Españoles, S. A. (AESA) in 1969. The new organisation was a merger of three companies – a state-owned company, Astilleros de Cádiz, and two private businesses, SECN and Euskalduna. The main objective of the Ministry of Industry’s Concerted Action programme in the sector was to encourage mergers. AESA was incorporated in December 1969. However, the three merged companies had struck a preliminary agreement for the operation on 14 June that year, and this was ratified by the Spanish government two weeks later. Under this agreement, which would only be enacted if the Ministry of Finance approved the tax exemptions stipulated in the Concerted Action legislation, the new company was to be incorporated with a share capital of 2,850.6 million pesetas, in two equal stakes held by the INI, the owner of Astilleros de Cádiz, and the private yards (SECN was to have a stake of 31.77 per cent, and Euskalduna 18.23 per cent). 65

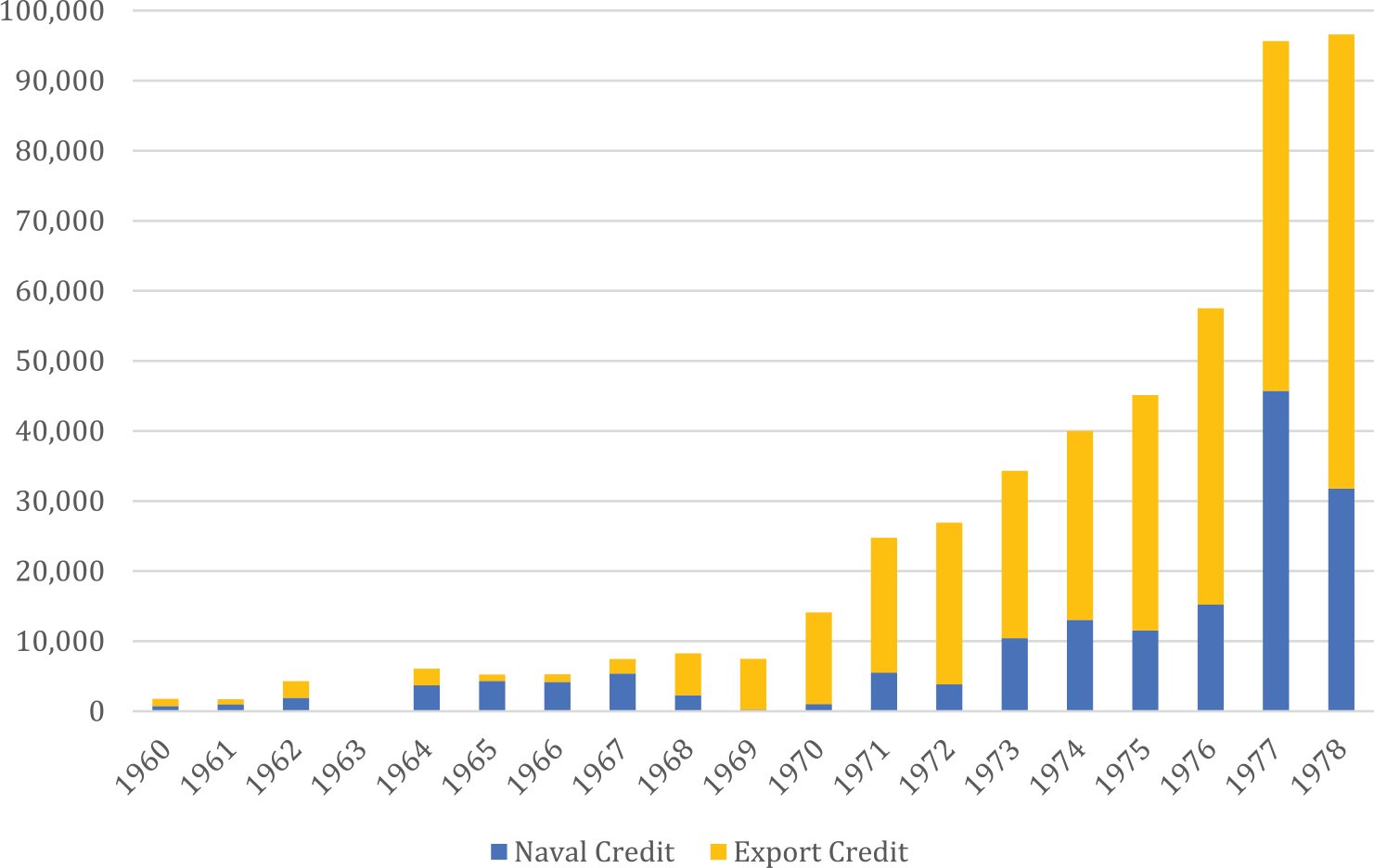

The shipyards’ Concerted Action programme was one of the items allocated to Naval Credit, and accounted for a major slice of this in the 1970s: between 1970 and 1976 it represented almost one fifth of the total. Since the mid-1960s, Spanish shipowners had repeatedly complained that, in contrast to the tendency to withdraw from direct funding for the sector, the state increased the official credit granted to the yards, either directly or through export credit. 66 Figure 4 compares naval credit to the official credit granted for ship exports (including the export credit provided by the private banking sector) between 1960 and 1978. Throughout this period, naval credit absorbed 161,973 million pesetas whereas official export credit almost doubled that figure at 320,551 million pesetas. It should also be noted that naval credit allocated credit to the shipyards, the normal credit and credit through the Concerted Action programme, as already mentioned. 67 Therefore, official credit was much more to the benefit of the yards, and their export business in particular, than Spain’s merchant navy vessels.

Naval credit and ships’ export loans to Spanish shipyards, 1960–1978 (million pesetas).

Conclusions

With the exception of the first section, which addresses output and export markets, the research carried out to date is more suggestive than conclusive. To be more specific, much research work is still needed to provide empirical evidence concerning competitiveness factors at Spanish shipyards during Franco’s developmental regime. In any case, the conclusions arising from this initial approximation, based on an international comparison and sources of various types and origins, focus more on financial costs and the public aid system than on other factors such as wages and labour costs. Some of the data cast more than reasonable doubt on the reliability of ‘official’ selling prices and valuations of vessels, which in one way or another are used to draw up the indicator of comparative advantages. In other cases, sales of vessels formed part of broader agreements regulating payments of government debt, financial assistance to third countries, or simply considerations which foreign oil groups were compelled to offer in return for investing in Spain’s flourishing oil-refining industry in the 1960s.

In terms of its apparent results, the shipbuilding industry certainly performed to the entire satisfaction of the Spanish government during the period known as Francoist Developmentalism (c.1959–1975). It would hardly be superfluous to bear in mind, as did Fairplay, that ‘the important point is not the “glory” of coming high in any league table, but whether the economic results in terms of a return on capital invested, both private and public, are also encouraging’. Development in the sector produced a number of benefits, despite low or non-existent profit: a boost for employment, a knock-on effect on ancillary industries, foreign currency earnings, and business for the banking system. 68 The opportunity costs, however, of a maritime policy that afforded priority to the interests of shipyards to the detriment of those of the merchant navy, were steep. Although the issue is not directly addressed in this article, it should at least be remembered that the Spanish shipping sector was unable to access the world market in vessels (both new and second-hand), and therefore had a more restricted supply (in terms of quantity and types) at higher prices, and also had a weaker bargaining position with such a concentrated and oligopolistic industry, and this all had adverse repercussions on its global competitiveness. 69 Almost all modern authors have concurred with this diagnosis, and some, such as Campos, have specifically postulated that exports of ships generated less revenue than on the domestic market, and that the priority of shipping policy should have been to assist merchant shipping. 70 Why, then, did all the governments of the time operate a different policy? This was due to, first, the powerful interests of both the state and most private banks in the shipbuilding industry, which were much more important than the interests they also had in shipping; 71 and, second, to the strong political power of a small group of naval architects in the Ministries of Trade and Industry during developmental Francoism, leaded by Gregorio López-Bravo, who became Minister of Industry (1962–1969), which shaped the state’s trade and industrial policy towards the shipbuilding industry’s interests. 72 These two factors remained in place in the period of economic crisis and industrial restructuring that followed. 73

Footnotes

Funding

Financial support from HAR2016-76198-P (AEI/FEDER, UE) and Basque Government IT897-16 is acknowledged.

1.

Bank of Spain’s Statistics Journal, several years, Angel Viñas and others, Política Comercial Exterior en España (1931–1975) (Madrid, 1979); Carmela Martín, L. R. Romero and Julio Segura, Cambios en la Estructura Interindustrial Española (1962–1975) (Madrid, 1981).

2.

Jurgen B. Donges, ‘From an Autarchic Towards a Cautiously Outward-Looking Industrialization Policy: The Case of Spain’, Weltwirtschaftliches Archiv Bd., CVII (1971), and La Industrialización en España: Políticas, Logros, Perspectivas (Barcelona, 1976); Viñas and others, Política Comercial; Mikel Buesa and Jose Molero, ‘La industrialización en la segunda mitad del siglo XX’, in Juan Velarde, Ed., 1900–2000 Historia de un esfuerzo colectivo: Cómo España superó el pesimismo y la pobreza (Madrid, 2000), 681–735, among others. The argument that low labour costs were central to shipbuilding growth was frequently wielded by analysts and publicists within the sector.

4.

Rafael Vega and Lucas Beltrán, ‘Construcción Naval’, in A. de Barcena and others, Estudios sobre la Unidad Económica de Europa. Tomo VIII. Consecuencias que para los diversos sectores de la economía española tendría su eventual integración en una unidad económica europea perfecta. Parte segunda (Madrid, 1959), 456–533; and Fairplay, 7 July 1960, 125; Fairplay, 2 November 1961, 41. However, despite a substantial surge in domestic iron and steel production, even by 1970 the sector was still compelled to import between 20 per cent and 25 per cent of the steel it required, Fairplay, 5 February 1970, 64. The Spanish iron and steel industry did not succeed in meeting domestic demand until 1971, Emiliano Fernández de Pinedo, ‘Desarrollo, crisis y reconversión de la siderurgia española a través de una empresa vizcaína, AHV (1929–1996)’, Ekonomiaz, 54, No. 3 (2003), 42–3.

5.

Concerning INI policy in this sector, see Jesús M. Valdaliso, ‘Programas navales y desarrollo económico: la Empresa Nacional Elcano de la Marina Mercante y el sueño industrializador de Suanzes, 1942-1963’, Revista de Historia Industrial, 12 (1997). Concerning extensions and improvements to Spanish shipyards in the late 1950s, see Rafael Vega, ‘Inversiones en la industria naval española’, Economía Industrial, 1, No. 1 (1964), 35–43; Stefan Houpt and José M. Ortiz-Villajos, eds., Astilleros Españoles 1872–1998: La construcción naval en España (Madrid, 1998), 199–242; and Jesús M. Valdaliso, ‘Nacimiento y desarrollo de la industria naval del hierro y el acero en el País Vasco: el caso de Vizcaya (c. 1889–1979)’, Itsas Memoria, 2 (1998).

6.

Fairplay, 4 June 1959, 1.289, and 11 June 1959, 1.334; Marine Engineering, ‘La construcción naval en España está haciendo grandes progresos’, Ingeniería Naval, 33, No. 365 (1965), 439; and Enrique Sendagorta, ¡Aquí estamos! Recuerdos autobiográficos de mi familia y de mis tiempos (Salamanca, 2008), 281 and 353.

7.

Fairplay, 6 July 1961, 123; Valdaliso, ‘Programas navales’; and Sendagorta, ¡Aquí Estamos!, 360–1.

8.

Vicente Cervera, ‘La actividad exportadora del sector construcción naval’, Economía Industrial, VII, 74 (1970), 33; and Fairplay, 7 July 1960, 125.

9.

The export figures, in millions of current pesetas, are taken from Bank of Spain’s Statistics Journal, several years. ‘In 1970, shipbuilding became the first Spanish industry that produced more for the export than for the domestic market’, Donges, ‘From an Autarchic’, 63.

10.

In terms of actual value, the data were not so different, Viñas and others, Política Comercial, vol. 2, 1,338. The structure of ship exports by markets contrasts with that of total Spanish exports, which were mostly accounted for by EEC member states, Viñas and others, Política, II, 1,335.

11.

Fairplay, 23 January 1964, 27.

12.

Fairplay, 5 November 1959, 41, and 6 September 1962, 38. In the case of the contract for 11 cargo ships for the Líneas Marítimas Argentinas company, awarded in 1962, the Spanish government agreed to allocate 25 per cent to the Hispano–Argentinian debt agreement. Good financing terms and the possibility of quasi-immediate availability of the vessels, rather than prices, which were more expensive than those of other offers, proved decisive in winning the contracts.

13.

Fairplay International Spanish Shipping and Shipbuilding, 12 October 1967, 47–9.

14.

Fairplay, 12 January 1967, 175.

15.

Tony Slaven, ‘Marketing Opportunities and Marketing Practices: The Eclipse of British Shipbuilding, 1957–1976’, Research in Maritime History, 2 (1992), 125–51; and Lewis Johnman, ‘Internationalisation and the Collapse of British Shipbuilding’, Research in Maritime History, 14 (1998), 319–53.

16.

Shipyards such as Euskalduna were very successful indeed in the Greek market, thanks to a standardised offer of vessels and payment facilities for buyers, Fairplay, 4 September 1969, 83.

17.

Fairplay, 6 July 1972, 95–7. The Spanish government granted dollar loans to countries such as Tunisia to help them buy ships built in Spain, Fairplay, 3 April 1969.

18.

Ansgar Eussner, The Spanish Shipbuilding Industry and the Accession of Spain to the EC: Adjustment Requirements and Problems (Berlin, 1979), 25; Jesús Valdaliso, ‘Programas navales’, and ‘Crisis y reconversión de la industria de construcción naval en el País Vasco’, Ekonomiaz, 54, No. 3 (2003). Around 1962, the small yards were still producing for the domestic market: A. Segui and J. Torroja, ‘The Small Yards in Spain and the International Market’, Fairplay Spanish Supplement, 4 October 1962, xvii. However, from at least 1965 onwards, they had begun to export, Fairplay Spanish Supplement, 28 October 1965, xxix.

19.

See, respectively, Tomohei Chida and Peter N. Davies, The Japanese Shipping and Shipbuilding Industries: A History of their Modern Growth (London, 1990); and Kent Olsson, ‘Big Business in Sweden: The Golden Age of the Great Swedish Shipyards, 1945–1974’, Scandinavian Economic History Review, 43, No. 3 (1995), 310–38.

20.

Fairplay Spanish Shipping and Shipbuilding Survey, 23 October 1969, 27.

21.

Concerning Continental Oil, see Fairplay 10 October 1968, 46. Concerning Gulf Oil, Fairplay 24 September 1968, 44, 14 November 1968, 46, and 16 January 1969, 46.

22.

Lloyd’s Register Annual Summary of Merchant Ships Launched during 1972, and 1973; and Lloyd’s Register Annual Summary of Merchant Ships Completed during 1974.

23.

Fairplay, 2 November 1961, 41. Donges, Industriqlización, 207–8, also singles out this factor.

24.

Fairplay, 1 September 1966, 40. By 1964, it was observed that it took a considerable amount of time to complete the ship, Fairplay, 2 July 1964, 117.

25.

For some examples of this process, see Valdaliso, ‘Nacimiento’, and Houpt and Ortiz–Villajos, eds., Astilleros. Several writers agree that the shipbuilding industry was a tightly regulated sector, with high entry barriers and an oligopolistic system in place. For example, see Mikel Buesa and Luis E. Pires, ‘Intervencionismo estatal durante el franquismo tardío: la regulación de la inversión industrial en España (1963–1980)’, Revista de Historia Industrial, 21 (2002), 159–98; and Mar Cebrián, ‘La regulación industrial y la transferencia internacional de tecnología en España (1959–1973)’, Investigaciones de Historia Económica, 1, No. 3 (2005), 11–40.

26.

See Cebrián ‘La regulación’, for an empirical verification of this relationship.

27.

Nor were the licences the only procedure used. In some cases, mixed enterprises were set up with stakes held by the foreign parent and its Spanish partners, companies such as SENER or Sociedad Española de Construcción Naval (SECN, henceforth), see Fairplay, 7 July 1960, 137, and 14 January 1965, 73. See also Jesús M. Valdaliso, ‘The Diffusion of Technological Change in the Spanish Merchant Fleet in the XXth Century: Available Alternatives and Conditioning Factors’, Journal of Transport History, 17, No. 2 (1996), 95–115, for information on the industry manufacturing diesel engines for vessels.

28.

Julio Rojo, ‘El desarrollo tecnológico en la industria española de construcción naval’, Economía Industrial, 9, No. 103 (1972), 82–3.

29.

By the public company operating in the sector, Elcano, and also in more general legal stipulations such as the Law of 1956 assisting mass production of ships, Fairplay, 6 September 1962, 38.

30.

Cía. Euskalduna, Activity Report 1968, 10; Fairplay, 22 February 1968, 37, 4 September 1969, 83, and 8 January 1976, 91.

31.

Houpt and Ortiz-Villajos, eds., Astilleros, 228–9. Fairplay, 28 November 1968, 36, noted that the yard ‘boasted one of the best productivity records in Spain’.

32.

Fairplay, 11 January 1973, 109. According to a productivity index based on installations, Spanish shipyards ranked in the middle, after the Scandinavian, Japanese and German shipyards, but before the French, Italian, North American and British, Fairplay, 16 May 1974, 44.

33.

The system was adopted by the state-owned company Bazán in 1969, Fairplay, 6 November 1969, 101. It was consolidated in the 1970s as a ship-design benchmark worldwide.

34.

The case of diesel engines for ships is analysed in Valdaliso, ‘The Diffusion’. A further example was a new design for ship hatches, patented by the Consulmar firm in the UK, Fairplay, 8 December 1960, 61.

35.

Marine Engineering, ‘Construcción naval’, 439.

36.

Rafael Vega, ‘La construcción naval española’, Economía Industrial, 2, No. 13 (1965), 17–18. According to Fairplay, 6 July 1961, 123, Spanish wages were indexed at 100 compared to an index of 235 in the United Kingdom.

37.

Vega and Beltrán, ‘Construcción Naval’, 510, estimated total cost savings in the late 1950s of between 3.55% and 5.61% with respect to Germany.

38.

Fairplay, 28 May 1964, xlix. These trends rose in the 1960s throughout Spanish industry – see Rafael Myro, ‘La industria: expansión, crisis y reconversión’, in José L. Garcia, ed., España, Economía (Madrid, 1989), 204–8.

39.

One aspect not addressed in this article is monetary policy and the exchange rate which, during certain periods, as in the devaluation of the peseta in 1959 and 1967, or the devaluation of the dollar in 1971, had major repercussions on exports. See Fairplay, 19 September 1959, 325, 14 January 1960, 173–5, 30 November 1967, 33, and 17 February 1972, 56.

40.

OECD, The Situation in the Shipbuilding Industry (Paris, 1965); José M. De Puelles, ‘Las ayudas a la construcción naval en los principales países industriales’, Economía Industrial, 4, No. 44 (1967), 35–43. According to Fairplay’s comments on the OECD report, State help gave the Spanish shipbuilding industry ‘a degree of protection rivalled only in the United States’, Fairplay, 11 November 1965, 39.

41.

Tae Woo Lee, ‘Government Policy for the Development of Shipbuilding and Shipping Industries in Korea’, Journal of Humanities and Social Sciences of Korea Maritime University, 4 (1996), 159–77.

42.

OECD, Situation, 35–6 and 87.

43.

Fairplay, 21 April 1960, 34. The anti-deregulatory nature of the 1960 Tariff has been addressed by many authors, such as Luis Gámir, coord., Política Económica de España (Madrid, 1975) and Enrique Fuentes Quintana, ‘Tres decenios de economía española en perspectiva’, in García, ed., España. Economía, 1–75.

44.

Fairplay, 13 July 1961, 49. This measure, in place until 1966, drove prices up by 20 per cent on the domestic market, Fairplay, 14 January 1965, 147. Comments by Spanish shipowners on the 1960 Tariff were particularly harsh: see Carlos Angulo, ‘Los nuevos aranceles y la importación de buques’, OFICEMA, 60, July (1960), 15–20; Speech by Eduardo de Aznar, OFICEMA, July (1960), 24–34; Editorial, ‘On ship imports’, OFICEMA, February (1964), 20–21.

45.

This had already been pointed out in reports by Vega and Beltrán, ‘Construcción Naval’, 488, in the late 1950s.

46.

Enrique Sendagorta, ‘The Immediate Future of the Shipbuilding Industry’, Fairplay’s Spanish Supplement, 28 October 1965, xxv–xxvii; and statements in Fairplay, 2 March 1967, 67.

47.

José L. Valdivieso, ‘El acero en la construcción naval’, Economía Industrial, 7, No. 74 (1970), 47–8.

48.

OECD, Situation. Concerning Japan, see Chida and Davies, Japanese Shipping; for South Korea, see Lee, ‘Government Policy’, 162–5.

49.

Juan J. Bosch, ‘La financiación de buques en España’, Economía Industrial, 7, No. 74 (1970), 30.

50.

Jesús M. Valdaliso, La Familia Aznar y sus Negocios (1830–1983) (Madrid, 2006), 192–201. The 1967 Euskalduna Activity Report provides a very clear summary of the problem: ‘On the one hand, the structure of our capital is at odds with the current turnover. On the other, the system stipulated by the current provisions to fund shipbuilding has not worked properly. Ships are built in months … but then they are paid for eight years after delivery … In other words, our work has been financed by delayed payment to our suppliers, who have helped us, and by short-term credits unrelated to the special lines in place’, Valdaliso, Familia, 196.

51.

Fairplay, 7 January 1971, 133.

52.

Concerning the preferential finance circuits, see R. Poveda, ‘Política monetaria y financiera’, in Gámir, coord., Política, 33–75; Juan R. Cuadrado, ‘Financiación privilegiada al sector privado y desequilibrios regionales’, Información Comercial Española, 526–7 (1977), 120–37; and Jaime Requeijo, ‘Los circuitos privilegiados de financiación y la reforma del Crédito Oficial’, Información Comercial Española, 596 (1983), 78–81.

53.

The total figures are Cuadrado’s, ‘Financiación privilegiada’.

54.

Santos Pastor, El Transporte Marítimo en España (PhD Thesis, Madrid, 1982), chapter XI, and Joaquín Alonso, Los Medios Jurídicos y Económicos de la Política Marítima en España (Madrid, 1982) chapter V, provide a summary of the main provisions of construction premiums and tax incentives. Donges, Industrialización, 83–4, has demonstrated that above all the tax breaks proved an effective export subsidy, because the amount exceeded the tax for which Spanish companies were liable. Viñas and others, Política Comercial, I, 270–71, corroborate this.

55.

It should be remembered that the Matesa scandal broke at the end of the 1960s, leading to the resignation of several ministers. See Gabriel Tortella and Juan C. Jiménez, Historia del Banco de Crédito Industrial (Madrid, 1986); and Juan C. Jiménez, ‘Banca pública e industrialización en España: empresas y empresarios, vistos a través del Banco de Crédito Industrial’, in Juan C. Jiménez, ed., Empresas y empresarios españoles en la encrucijada de los noventa (Madrid, 1993), 33–70.

56.

Alonso, Medios, 85, states this practice benefited both shipowners and shipbuilders. Pastor, Transporte, 716–7, 760 and 776, associates the benefits of this practice of ‘inflating’ the worth of vessels with shipowners only, but forgets that the premiums and tax incentives, which were also based on the value of ships, were granted to the shipyards. See also José C. Arias, La Banca Oficial en España (1970–1984) (Madrid, 1986), 157; and Julio García, ‘Política empresarial pública 1973–1988’, in Pablo Martin-Aceña and others, Empresa pública e industrialización en España (Madrid, 1990), 229, who, like Pastor, quote civil servants.

57.

Archives of the Provincial Council of Bizkaia (AFB), Fondo Sota y Aznar (FSA), Shelf number 2964/5, Construction and financing of the Monte Zapola vessel, 1967.

58.

AFB, FSA, Shelf number 2518/3, Letter from S. A. Juliana to Naviera Aznar, 10 April 1969.

59.

AFB, FSA, Shelf number 2647/3, Reply to pleas by Naviera Aznar, by Unión Naval de Levante; and Shelf number 2672/4, Reply by Naviera Aznar to pleas by Unión Naval de Levante.

60.

AFB, FSA, Shelf number 2829/3, Application for credit for the construction of a ro-ro vessel by Naviera de Exportación Agrícola, 1975. The yard’s offer entailed income of 87.3 million pesetas in premiums and tax breaks, 7.5 million more, and a credit for 87 per cent of the ship’s value, instead of the legal maximum of 80 per cent.

61.

Donges, Industrialización, 90–2, and Alonso, Medios, 169–78. Concerning official export credit in the second half of the 1960s, Jiménez, ‘Banca pública’, quotes interest rates of 9–10 per cent on the market, and 5–5.90% on the preferential circuits. From 1971 to 1978, credit for ship exports accounted for 22 per cent of total export credits, Alonso, Medios, 182.

62.

In 1969, the OECD attempted to harmonise ship export credit terms among its member states, in a bid to prevent a credit war situation. Bosch, ‘La financiación’, 30, and Alonso, Medios, 178–9

63.

The trend is similar to that of the total export credit, see Viñas and others, Política Comercial, I, 276–8.

64.

Bosch, ‘La financiación’, 31–2; Houpt and Ortíz-Villajos, eds., Astilleros, 321–6; Valdaliso, ‘Programas navales’, and Familia, 198–9; and Sendagorta, ¡Aquí Estamos!.

65.

The new company was incorporated with a syndicated share agreement between the INI and Banco Urquijo and Banco Hispano Americano, with a fixed board of directors over the first five years, Valdaliso, Familia, 199–200; and Houpt and Ortiz-Villajos, eds., Astilleros, 323–4. Another merger was arranged between Astilleros Construcciones S.A. and Construcciones Navales Yarza S.A. ASTANO and Unión Naval de Levante entered into an association for shipbuilding design and research, Francisco García, ‘La Acción Concertada en el sector de industrias navales’, Economía Industrial, 7, No. 74 (1970), 9–16.

66.

Concerning export credit, see Arias, Banca, 81 and following, and Alonso, Medios. Ship export credits accounted for most of the total export credit in the first half of the 1970s, although subsequently they declined in the wake of diminishing exports due to economic crisis.

67.

The breakdown of figures is from Banco de Crédito a la Construcción, Activity Reports 1965 to 1978.

68.

Fairplay, 12 November 1970, 41–3. However, the expression ‘moving up in the league’ is taken from Fairplay, 16 May 1974, 39.

69.

Valdaliso, Familia, 172–4, and ‘Spanish Shipping Firms in the Twentieth Century: Between the Internationalisation of the Market and the Nationalism of the State’, International Journal of Maritime History, 19, No. 2 (2007), 1–21. Sendagorta acknowledged this in the first half of the 1960s, although he added that ‘Today, the situation has changed, and Spain, for certain types of ships, is competitive’, Sendagorta, ‘Immediate Future’, xxvii. The Director-General of Navigation, Pascual Pery, claimed in 1966 that Spanish shipowners paid a 20 per cent mark-up for a ship built in Spain, Fairplay, 15 September 1966, 54. Pastor, Transporte, 716–26, presents empirical evidence which seems to suggest that, between 1966 and 1972, for certain types of ships, bulk carriers and oil tankers, the construction price was similar to or lower than on world markets. The information supplied by Valdaliso in ‘The Diffusion’, and Familia, claims that the Spanish shipbuilding industry did not have sufficient technical capacity to build certain types of ship (container vessels, ro-ro ships, ferries), and this had an adverse effect on Spanish shipowners. Foreign publications such as Fairplay or, perhaps more significantly, Información Comercial Española (ICE), a magazine published under the auspices of the Ministry of Trade, backed this fact and supported the position of the shipowners – although ICE qualified its support. See the ICE Editorial, 470 (1972), 31–4, or the reports by the Fairplay correspondent in Spain, in the special editions of 28 October 1965, and 12 October 1967.

70.

Ramiro Campos, ‘Análisis económico del sector de construcción naval español y de sus relaciones estructurales con el transporte marítimo’, Revista de Economía Política, 71 (1975), 39–139.

71.

Pedro Sancho, Transporte Marítimo y Construcción Naval en España (Madrid, 1979); Valdaliso, Familia, 283–4; and Sendagorta. ¡Aquí estamos!, 363–7. The close relations between the shipyards and private bankers are acknowledged in OECD, Situation, 68. For the whole industrial sector, see Buesa and Pires, ‘Intervencionismo estatal’.

72.

Gregorio López-Bravo, who had been Managing Director of SECN, became General Director of Foreign Trade in the Ministry of Trade in 1959; then, in 1960, he moved to the Presidency of the Instituto Español of Moneda Extranjera (Spanish Agency of Foreign Currency), and later to the Ministry of Industry, and in 1969 to the Ministry of Foreign Affairs. His successor in Foreign Trade was his fellow naval architect and friend, Enrique Sendagorta, who had started Construnaves in 1959; see Sendagorta, ¡Aquí estamos!, 288 and 311, and Fairplay, 28 October 1965, Fairplay Spanish Supplement, i. López-Bravo and Sendagorta were presidents of the Spanish Association of Naval Architects and responsible for the creation of the Corp of Naval Architects in Spain in 1960, José M. Sánchez, ‘Historia de la creación del Colegio’, Ingeniería Naval, LXXXVI, 957 (2017), 55–7. For other sectors where engineers and technicians came to ‘capture’ the state, see also Pedro Fraile, ‘Spain: Industrial Policy under Authoritarian Politics’, in James Foreman-Peck and Giovanni Federico, eds., European Industrial Policy: The Twentieth Century Experience (New York, 1999), 233–67.

73.

When the foreign market collapsed in the wake of the economic crisis that ensued in 1974, the state strove to rectify the situation of the yards by stimulating domestic demand. The first measure taken to this end was the so-called ‘Million tonne competition’ approved in 1976, which briefly kept facilities in production, albeit at the cost of increasing the excess capacity in the Spanish merchant navy; Valdaliso, ‘Spanish Shipping Firms’, 12. During the subsequent period of restructuring, the shipbuilding industry was one of the sectors that benefited most from public aid: see Blanca Simón, Las Subvenciones a la Industria en España (Madrid, 1997), and Valdaliso, ‘Crisis y reconversión’.