Abstract

In the eighteenth century, about 12% of Atlantic slave-trading voyages organized under the French flag ended in shipwreck, condemnation of the vessel by Admiralty authorities, capture by privateers or pirates, or with the enslaved men and women on board taking control of the ship. During this period, a commercial solution was available to insulate slave traders from the financial losses that shipwreck, capture, and revolts represented to them: marine insurance policies, written to cover the estimated value of enslaved people and slaving vessels. According to early modern merchant manuals and legal commentaries, insurance underwriters compensated losses during slave-trading ventures according to stable principles that were consistent throughout the Atlantic world. In this article, however, I explore new evidence beyond these published sources by comparing the terms of 13 marine insurance policies underwritten in France to cover investments in slave-trading ships and in enslaved people. In these contracts, we find that purchasers of insurance coverage and underwriters added conditions not foreseen in merchants’ and lawyers’ manuals, as well as lines that contradicted the terms such guidebooks and commentaries claimed were standard. Marine insurance policies that covered slave-trading ships were used to hand off the possible financial fallout from profoundly unpredictable situations—not only conflicts between European powers, but also violent encounters between enslavers and captives, between European and African slave traders, and wars between African kingdoms. Insurance policies underwritten on the hulls and cargoes of slave ships thus show that marine insurance in the early modern world was a tool for redistributing both Knightian risk and Knightian uncertainty.

This article will examine the insurance of slave-trading ships in France during the eighteenth and early nineteenth centuries. The Ordonnance de la Marine (1681), the first codification of maritime law in France, allowed merchants to insure the body (corps) of their vessels, the merchandise they transported overseas, and even “the ransom price of the persons they will bring out of slavery” (as originally conceived, the costs of ransoming Christian subjects who had been captured in the Mediterranean by Muslim corsairs). 1 The Ordonnance did not explicitly authorize the insurance of enslaved Africans, but through a legal analogy that equated the value of goods exchanged in African ports for slaves with the “ransom price” mentioned in the law, marine insurance policies underwritten on the value of enslaved Africans trafficked in the Atlantic became enforceable in French courts. 2 Investors in slave-trading ventures during the eighteenth century routinely insured their stakes in both the bodies of vessels and in cargoes. The practice became so firmly established that is difficult to find slave-trading voyages that were not insured. 3 After the French Revolution, the insurance of slave-trading vessels and of human cargoes continued once Napoleon reinstated the slave trade in France in 1802, and even persisted after the slave trade was legally abolished, through decrees in 1815 and 1817. 4

According to early modern merchant manuals and legal commentaries, insurance underwriters compensated losses during slave-trading ventures according to stable principles that were consistent throughout the Atlantic world. During the Middle Passage, deaths and injuries among the enslaved either attributed to the “perils of the sea” (périls de la mer) or inflicted by white crews in repressing revolts were covered. Insurance could not be claimed for “natural death” (mort naturelle), including for deaths resulting from sickness, inadequate hydration and nutrition, and suicide. 5 In this article, however, I explore new evidence beyond these published sources by comparing the terms of actual marine insurance policies that covered investments in slave-trading ships and in enslaved people. In these contracts, we find evidence that a strategic language game was in play. Purchasers of insurance coverage and underwriters fiddled with the terms of coverage to calibrate their financial exposure. They often added conditions not foreseen in merchants’ and lawyers’ manuals, as well as lines that contradicted the terms such guidebooks and commentaries claimed were standard.

In contrast to many narrative accounts written by slave traders, which “giv[e] little attention” to “the actual day-to-day experience of the crossing” and are strikingly indifferent towards enslaved people's ordeal and towards their actions, in insurance policies, French investors and insurers did not avert their eyes from the brutality of the slave trade and its impact on other human beings. 6 The terms of these policies confronted head-on fettered captives’ despair and desperate attempts to end enslavement through escape, overpowering the crew, drowning, or suicide. The negotiation of insurance coverage was an occasion for investors and underwriters to anticipate the financial consequences of violent and grotesque events that could possibly set back their trade. Insurance policies thus demonstrate that investors in the slave trade and underwriters ascribed agency to enslaved people, as well as to African merchants and rulers. We must bear in mind, in interpreting these contracts as historical sources, that insurance agreements were negotiated before or soon after vessels set sail and referred to hypothetical, not actual, events. Yet it made economic sense for insurance buyers and underwriters to focus their negotiations on situations that experience showed could imperil the profitability of slave-trading ventures. Since terms of coverage were selected to place bounds on each side's liability and to help them avoid litigation in the future, the language of insurance policies reflects slave traders’ expectations about how and at which stage resistance, revolts, or interruptions in trading tended to manifest.

Marine insurance coverage of slave ships should take center stage in our thinking about risk and uncertainty in the premodern world, even though the sector represented only a minor share of the insurance business in the eighteenth and early nineteenth centuries, in terms of the volume of contracts and value of insurance premiums. 7 Many economic historians present marine insurance as one of the key financial tools that allowed medieval and early modern merchants to redistribute the risks of navigation. 8 However, marine insurance policies along all lines of trade did not only protect merchants’ investments against storms or accidents at sea that followed predictable or seasonal patterns. By default, policies covered pirate, privateer, and enemy navy attacks—threats posed by human agents and linked to political and historical processes that brought a deeper level of uncertainty into underwriters’ calculations. Marine insurance in the early modern world was a tool for redistributing both Knightian risk and Knightian uncertainty (analytical categories I explore in the following section), and I argue that insurance policies underwritten on the hulls and cargoes of slave ships bring this into sharper focus. Marine insurance policies that covered slave-trading ships were used to hand off the possible financial fallout from profoundly unpredictable situations—not only conflicts between European powers, but also violent encounters between enslavers and captives, between European and African slave traders, as well as wars between African kingdoms.

Marine insurance policies, the main typology of source that I employ in this essay, remain largely unexplored in the historiography of the transatlantic slave trade. One reason for their neglect is that in most French ports, as in many other jurisdictions across the Atlantic world, the marine insurance policy was a private contract, that is an acte sous seing privé. According to the custom in most local markets, merchants did not have their policies notarized. As a result, few insurance policies originated during the early modern period (or copies of their complete terms and clauses) were archived. 9 Given that the transatlantic slave trade was only one channel in a global network of exchanges, the numbers of insurance policies underwritten on slave ships and their human cargoes that are preserved is even smaller. These documents’ rarity and their unpredictable division among diverse archival series and the papers of different merchants made them inappropriate for determining the dimension, the demography, and the shifting geographies of the transatlantic slave trade: the research questions that animated historiography in the second half of the twentieth century and inspired the SlaveVoyages digital history project. 10

For a new generation of scholars, it has become more urgent to recover individual narratives of enslavement, as well as to conceptualize and introduce new categories of analysis, such as gender and commodification. As approaches to studying the transatlantic slave trade have shifted, historians have been led to criticize research that centers commercial and accounting documents like insurance policies. Their sense is that such records can only be mined for quantitative data. Scholars also fear that these sources have obscured the violence of the slave trade, both from investors in the eighteenth and nineteenth centuries and from researchers in the present day. 11

In this article, far from ignoring the language and specificities of slave-traders’ marine insurance policies in order to extract statistics from them, I offer a close, qualitative reading of 13 insurance policies underwritten in five different French ports. 12 I have set this small sample of policies against other more abundant insurance-related sources, including 76 more concise references to completed insurance transactions in the account books of underwriters and of shipowners (armateurs); French admiralty court records; and other legal archives that describe accidents, armed conflicts, and commercial disputes that arrived in the course of trading. Records of insurance premiums and slave-trading vessels’ destinations pulled from account books aid in showing how the premiums and destinations quoted in the 13 complete policies compared with more general trends. The court records I examine provide context for understanding the risks and uncertainties of the slave trade and describe specific instances that resulted in insurance claims.

Throughout this essay, I focus on slave trading within the French Atlantic and on the insurance of French slave ships because the slave insurance policies underwritten in France that I have uncovered and analyzed appear to be more idiosyncratic, less standardized, and more generous in extending coverage to traders than similar policies underwritten in other jurisdictions, such as in Britain, the Netherlands, and Spain. According to historians who have studied the practices of insurers in these rival empires, marine insurance policies on slave trading ships and enslaved people were nearly identical to contracts that covered vessels and cargoes in other lines of trade. These scholars claim that the terms of slave insurance policies made only cursory mention of enslaved men and women themselves, and references to events including acts of resistance that could destroy their realizable value were even rarer. 13 Pearson and Richardson contend that in their sources “there is not a hint that slaves were regarded by those involved in the business as anything other than a cargo of goods”. 14 Yet Pearson and Richardson's research, like that of other historians thus far who have worked on the history of insurance in the slave trade using British, Dutch, and Spanish archives, is based on sources such as underwriters’ books and commercial manuals that do not record the detailed terms of insurance agreements. Very few examples or transcriptions of insurance policies on slave ships underwritten by British, Dutch, Spanish, and Portuguese subjects have appeared in the historical literature. 15

Shipowners outfitting vessels for slave-trading voyages may have had less liberty in negotiating insurance coverage within other empires than within France. If so, insurance policies originated in France may offer unusual insight into what merchants arming vessels for the Atlantic slave trade defined as its most serious hazards. Over time, however, frequent communication and exchanges across imperial borders and merchants’ ability to arrange insurance coverage in a distant port would probably have minimized important differences in underwriters’ practices. Another possibility is that many of the marine insurance policies originated in ports like Bristol or Amsterdam did contain a variety of terms similar to those in the French policies we will see. Research projects already in gear will hopefully make many more insurance contracts underwritten on slave ships available to historians, opening up the possibility of better cross-imperial comparisons. 16

An economist's distinction between risk and uncertainty

In the nineteenth and early twentieth centuries, economists had little to say about market transactions when information was imperfect, or about producers’ choices to invest or to enter a new market when the consequences of their decisions were uncertain. Then came an important shift, perhaps not by coincidence in the wake of the First World War, when Frank Knight introduced risk and uncertainty to the discipline as core concepts. Although in common speech risk and uncertainty are often used as synonyms, Knight wanted to separate and precisely define the two terms, establishing a critical “distinction between measurable risk and unmeasurable uncertainty”. 17 Knight interpreted risk as the possibility of a good or asset—or even a life—being destroyed or coming to harm, when we can accurately estimate the chances of that unwanted outcome occurring based on past experience. To estimate risk, we must be able to group together many homogenous cases—printer cartridges subject to bursting during factory production, roller-suitcase handles which are either intact or broken after one year of frequent use, infants who may be discovered at birth to have a given genetic disorder, etc. 18 In such cases, the frequency of adverse outcomes in the past shows us what to expect in the future. However, for the most part, in markets and in many other contexts, we face uncertainty in the future: a decision we have to make or the launch of a new commercial venture which “is so entirely unique that there are no others or not a sufficient number to make it possible to tabulate enough like it to form a basis for any inference of value about any real probability in the case we are interested in”. 19 Knight supposed that insurance markets could be set up to cope with measurable risk, but not with uncertainty. Insurers would only agree to assume the financial burden of an adverse outcome if its chance of occurring was a known quantity, a statistic that could be pinned down by looking to the past.

Risk and uncertainty, these two poles established by Frank Knight, have continued to orient research into the historical foundations of marine insurance and of other technologies for sharing the perils of ocean voyages. According to Douglass North's influential account of marine insurance's beginnings, these markets appeared when the dangers of navigation were transformed from uncertainties into risks through advances in shipbuilding and cartography. 20 However, the earliest examples of marine insurance contracts have been traced back to the late thirteenth century, and by the sixteenth century Italian merchants had introduced insurance contracts to most European ports. 21 Ship construction, cartography, and navigators’ training improved gradually over the early modern period, but both the conception and the widespread adoption of marine insurance pre-date by several centuries meaningful upgrades in the safety of shipping. 22 The impact of safety improvements, such as the technique of sheathing ships in copper, was mainly felt between 1780 and 1830, when it translated to a reduction by half in the incidence of accidents on many sea lanes and in insurance rates. 23 North's explanation of the insurance industry's rise seems to mistake the sequence of events: marine insurance markets preceded most improvements in the safety of navigation. However, there is a second reason why historians of insurance commonly disagree with North's progressive narrative of the uncertainties of navigation recast as measurable risks. Scholars working in archives across Europe and the Atlantic World have repeatedly shown that merchants had no mathematical or actuarial tools for calculating the rate of shipwrecks and other accidents at sea, throughout the early modern period and even into the nineteenth century. 24 If risk, as Knight has defined it, must be subject to measurement and tabulation, then it would seem that it was present only in a nascent form in the preindustrial world.

The solution Giovanni Ceccarelli offers to this problem is that early modern underwriters developed reliable “proto-probabilistic” methods for estimating risk. 25 They may not have employed statistical techniques or systematically recorded the rate of ship and cargo losses, but their typically long professional experience gave them an implicit database of past accidents to draw upon. Underwriters of the eighteenth and early nineteenth centuries could accurately compare voyages based on the safety of different sea lanes, the protection that a certain construction and firepower offered to different vessels, and other variables, and tailor insurance premiums to each case. As I show in a separate investigation—a quantitative study of insurance premiums related to all lines of trade recorded in Marseille, Bordeaux, and Nantes between the 1680s and 1820s—marine insurance underwriters did price voyages according to stable and reasonable principles during peacetime. Merchants’ and brokers’ ability to shop around for coverage, advertising the details of their voyages to different underwriters in the same city, but also to insurers resident in other regions or abroad, meant that premiums tended to align with the proportion of similar voyages affected by loss. 26

For further evidence that this kind of proto-probabilistic reasoning guided marine insurers’ decisions, we can consider that the marine insurance business was the first example David Hume turned to in his reflections on probability in 1739: I have found by long observation, that of twenty ships, which go to sea, only nineteen return. Suppose I see at present twenty ships that leave the port: I transfer my past experience to the future, and represent to myself nineteen of these ships as returning in safety, and one as perishing … But as we frequently run over those several ideas of past events, in order to form a judgment concerning one single event, which appears uncertain; this consideration must change the first form of our ideas, and draw together the divided images presented by experience; since ‘tis to it we refer the determination of that particular event, upon which we reason.

27

Hume observed that people interested in the safe return of ships reasoned by projecting their knowledge of the past into the future. He understood that this method of reasoning yielded imperfect knowledge “which cou’d not produce assurance in any single event”, but that the accuracy of the predictions it generated improved with repeated observations or “experiments”. However, the mixed results of these repeated experiments were not related or given weight through an equation; instead “the fancy melted together all those images that occur, and extracted from them one single idea or image, which is intense and lively in proportion to the number of experiments from which it is deriv’d”. 28 In the eighteenth century, a merchant or a philosopher like Hume did not instinctively turn to mathematics or to a formal system to filter past experience or “experiments” and create forward-looking predictions. The “fancy” or judgement played a role in deriving a single conclusion from diverse past experiences.

In this section of A Treatise of Human Nature, “On the probability of causes”, Hume seized on only one dimension of the business of insuring ships in the early modern world. Commercial ventures in this world were not only imperiled by storms or pirates, risks which affected individual voyages arbitrarily and could be estimated based on past experience. They were also threatened by swings in political fortunes and by conflicts. Privateering, or attacking merchant ships flying an enemy state's flag, was considered a legitimate part of warfare in the eighteenth and early nineteenth centuries. 29 A declaration of war, then, could change the entire landscape of risks. 30 It was thus also the work of an insurance underwriter to foresee such historical conjectures, a task for which past experience could not necessarily serve as a guide. For this reason, Hannah Farber has recently put forward the idea that marine insurance in early modern ports “consisted of a business of uncertainty layered on top of a business of risk”. 31 I agree with Farber's recharacterization of marine insurance as a tool that was used to cope with both risk and uncertainty. This idea's best illustration is the insurance of ships and cargoes in the transatlantic slave trade.

Marine insurance policy for the Perrier, dated 19 April 1791 (Archives départementales de la Gironde, 7 B 1663).

This darkest corner of early modern insurance markets also offers a powerful historical corrective. Political transformations on the African continent, diplomatic initiatives launched by African polities, and the structures of local markets where European traded for slaves have long remained virtually invisible in histories told from a European perspective. 32 In contrast, the negotiation of insurance coverage for slaving-trading ventures proves that the commercial culture in African polities and signs of political upheaval in the region were carefully monitored by French traders in the eighteenth and nineteenth centuries. Gauging and understanding these was indeed key to securing their investments in the Atlantic slave trade.

Navigational risks of the slave trade

Better than any other segment of the market, insurance policies on the hulls and cargoes of slave ships reveal how risk and uncertainty were layered in early modern marine insurance contracts. In French ports, underwriters used the same printed forms as a starting point, whether they were drawing up a marine insurance policy for a slave-trading ship or for a vessel occupied in another line of trade (Figure 1). To take as an example the form commonly used in Bordeaux during the late eighteenth century: underwriters agreed to shoulder the burden of “all perils of the sea, of fire, of winds, of friends, of enemies, of letters of marque and counter-marque, of arrest and detention of whichever Kings, Princes, or Lords”. 33 Policies covering slave ships, no differently than those relating to other types of commerce, therefore included protection against all losses attributable to the “perils of the sea” (périls de mer), that is to storms and adverse conditions at sea, and to seizure of the ship's consignment of slaves by privateers or pirates. 34 It is already clear from the compendium of perils mentioned in Bordeaux contracts that marine insurance policies were used to trade risks—mainly natural hazards, occurring at predictable rates, according to fixed distributions—as well as to pass on the uncertainties of long-distance trade. The standard language of marine insurance contracts referred to human history and acts of violence—especially to wars that led to privateering and to the confiscation or detention of foreigners’ trade goods and ships—that were too unique to be foreseen using proto-probabilistic logic.

Certain marine insurance policies underwritten on French slave ships stand out from other examples because they include additional, handwritten clauses elaborating on and adding to the list of uncertainties being passed on. In a later section we will examine these extra handwritten lines, in which underwriters and slave-trade investors grappled with uncertainty, human agency, and the possibilities of revolt and war. Such events appeared in insurance contracts because of their evident potential to destroy slave-traders’ profits, but they should not eclipse the “perils of the sea, of fire, of winds” to which vessels and enslaved people were exposed during trafficking.

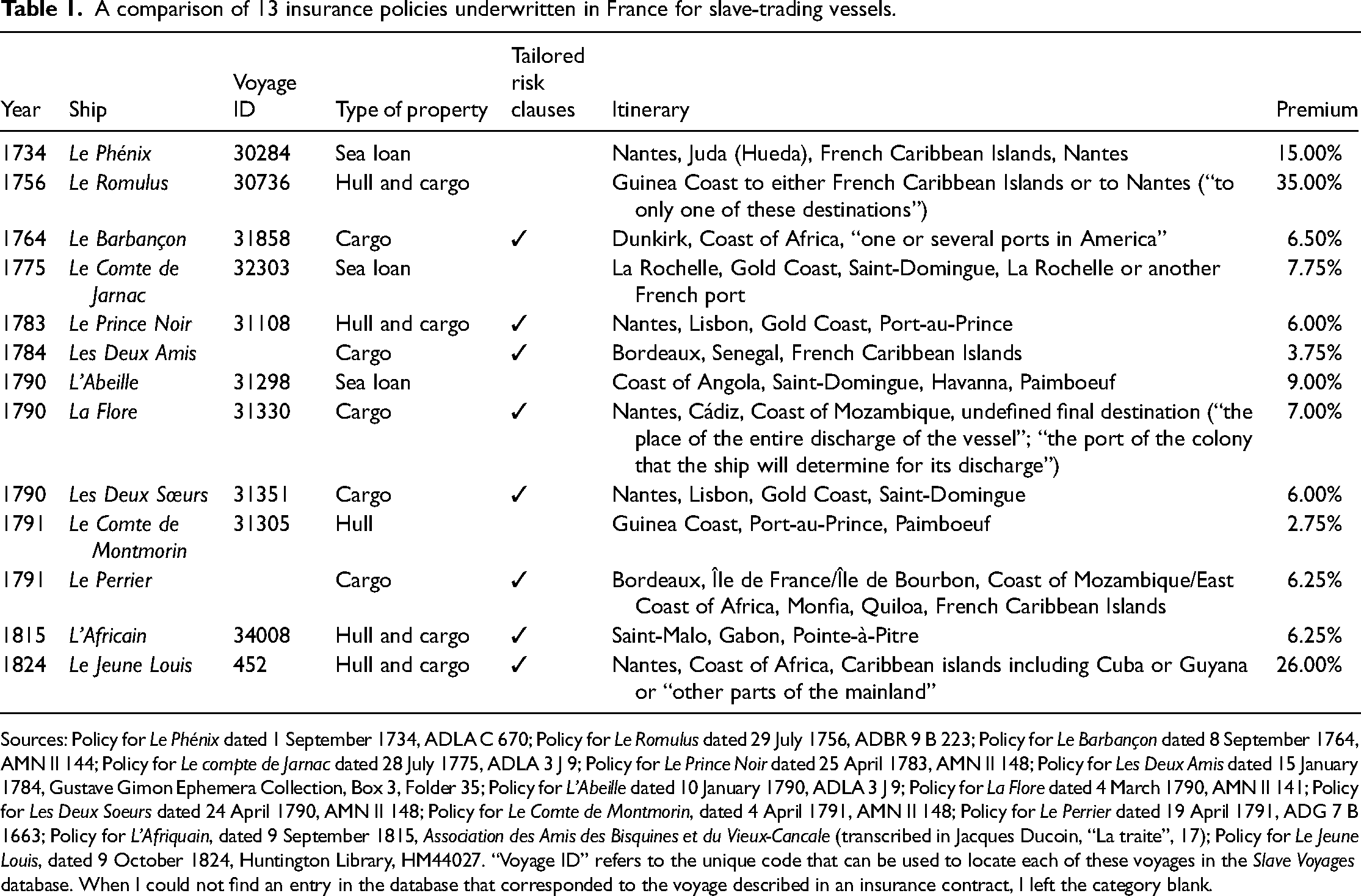

There were significant navigational challenges involved in trading along the African coast. Slave-trading ships rarely traced a direct line from a French port to a specific African market, and then to a colony in the Americas. These were multi-stage voyages, with itineraries which could be modified in response to fresh information about which ports were well-supplied with captives, and what European or regionally produced goods were in demand in those places. 35 French slave ships often made a preparatory stop in another European port—Lisbon is the city most frequently named in insurance contracts—in order to purchase items in high demand in African markets but not available in France, such as Brazilian tobacco (Table 1). In the next stage of these ventures, it was not unusual for slave-trading vessels to put in at several ports on the African coast in order to gather enough trafficked men, women, and children to make the transatlantic crossing profitable. 36

A comparison of 13 insurance policies underwritten in France for slave-trading vessels.

Sources: Policy for Le Phénix dated 1 September 1734, ADLA C 670; Policy for Le Romulus dated 29 July 1756, ADBR 9 B 223; Policy for Le Barbançon dated 8 September 1764, AMN II 144; Policy for Le compte de Jarnac dated 28 July 1775, ADLA 3 J 9; Policy for Le Prince Noir dated 25 April 1783, AMN II 148; Policy for Les Deux Amis dated 15 January 1784, Gustave Gimon Ephemera Collection, Box 3, Folder 35; Policy for L’Abeille dated 10 January 1790, ADLA 3 J 9; Policy for La Flore dated 4 March 1790, AMN II 141; Policy for Les Deux Soeurs dated 24 April 1790, AMN II 148; Policy for Le Comte de Montmorin, dated 4 April 1791, AMN II 148; Policy for Le Perrier dated 19 April 1791, ADG 7 B 1663; Policy for L’Afriquain, dated 9 September 1815, Association des Amis des Bisquines et du Vieux-Cancale (transcribed in Jacques Ducoin, “La traite”, 17); Policy for Le Jeune Louis, dated 9 October 1824, Huntington Library, HM44027. “Voyage ID” refers to the unique code that can be used to locate each of these voyages in the Slave Voyages database. When I could not find an entry in the database that corresponded to the voyage described in an insurance contract, I left the category blank.

As an illustration, the insurance policy on the Perrier, signed in Bordeaux in 1791, has a lengthy handwritten section which describes the voyage the insured ship was attempting (Figure 1). The purchaser of this policy was a resident of La Rochelle, Pierre Mathurin du Jardin, who was insuring a rather small sum, 3,800 livres, in Bordeaux through an agent. The sum befitted du Jardin's position as the surgeon on the ship. His property among the cargo is carefully noted as 200 containers of merchandise, one trunk with more goods and 273 “piastres gourdes” (a type of currency), and “three barrels of eau-de vie”. The intended course of the voyage is described at length, and it was a flexible schedule: from in front of this city of Bordeaux going to the Îles de France and de Bourbon, to later go from the said place of Île de France, to the Coast of Mozambique, Eastern Coast [of Africa] to Monfia, Quiloa, or Mozambique (putting in if the situation demands it at the Île de Bourbon or at Madagascar) in one or many ports, anchorage points or places in the said Eastern Coast, whether in going up [the coast], going down, or retracing, wherever it will seem good to the Captain to go to trade Blacks, gold dust, leather, elephant tusks, dye woods, or other Effects or merchandises of whatever sort, whether they proceed from the Slave Trade or otherwise … to then from the said coast of Mozambique, Monfia, Quiloa, or Eastern Coast go to the French Islands of America, in whatever ports, anchorage points, or places where the Captain will judge it is right to go for the good and the advantage of his commerce, even from one port to another … We permit him to make during the whole course of his voyage as detailed above, all the stops and breaks, whether forced or voluntary, that the captain will find it convenient to make for the good and the advantage of his commerce or the health of the blacks, permitting the said ship to make a stop at the Cape of Good Hope, whether in going or in coming from the slave trade.

37

With the addition of clauses insisting on the shipmaster's freedom to enter “many ports, anchorage points” and to make any “stops and breaks”, the insurance policy for the Perrier foresaw that the ship's trade along the eastern coast of Africa would last many months and could involve the exchange of commodities such as ivory and gold dust, as well as captives. The complex itineraries of the Perrier and of other slaving vessels were an adaptation to the structure of slave markets, but they increased these voyages’ navigational risks, because in the age of sail, wooden ships were much safer on the open sea than while they were trying to dock or trying to leave a port. In 1791, the year that the Perrier departed on its voyage, the Postillon de Bourbon wrecked on the same stretch of coast while trying to enter a harbor after nightfall. 38 (Similar circumstances were described in many reports of wrecks or damages (avaries) in the eighteenth century; passing through shallow waters with poor visibility was treacherous.) The path that the Postillon and the Perrier were both travelling, to the Indian Ocean coast of Africa, was not a main highway of the slave trade but had gained notoriety in the last quarter of the eighteenth century. 39 As French slave-traders expanded their zone of operation to the coast of Mozambique or East Africa, they faced additional navigational challenges, as the monsoon season would then have to determine the timing of their outward and return voyages.

Spending time at anchor exposed wooden hulls to shipworm. This could happen when waiting on the monsoon winds, or while slave traders were purchasing captives. Months-long loading times were not unusual in the ports where French subjects commonly traded. 40 The physical deterioration of a ship known as the Vainqueur, during the time that it lay at anchor in Senegal and French Cayenne, probably contributed to the vessel's sinking in 1786. The Bordeaux-based vessel had traded in Senegal for just four or five weeks, but had then remained anchored in the intermediate port of Cayenne for a full three months. 41 Afterwards, even a collision with a soft obstacle, a mud bank, as the vessel was en route to Guadeloupe, was enough to fatally damage the ship. According to one witness, following this collision, which ruptured the Vainqueur's hull, white crew members made no effort to save the 30 enslaved men, women, and children who were on board, simply abandoning them to go down with the ship. A single adolescent girl was able to swim beyond the wreckage and was saved. 42

Storms and reefs were natural hazards the Atlantic slave trade shared with other lines of trade and were foreseeable. However, when these dangers struck a slave ship, the experience was terrifying, as the story of the men and women who perished with the Vainqueur shows, and the number of human lives at stake was obviously greater. Another well-documented case, reported in a Nantes news gazette in 1765, is that of a craft called the Troqueuse, which was pulled out to sea during a storm while bringing captives down the coast of Senegal, intending to rendezvous with a larger vessel. It proved impossible to return to the African coast, so the shipmaster set a course across the Atlantic to Martinique, although there were meager provisions for the 37 enslaved Africans, two Luso-African slave-traders, and three white sailors on board. The winds were favorable for 19 days, but this was followed by several days of calm, which made the enslavers fear that water and food supplies would not last. The shipmaster “had resolved to throw (jeter) his Blacks into the sea to at least save the rest of the crew”, a plan that amounted to drowning 37 people en masse. 43 However, before carrying out this resolution, he fell ill, and at about the same moment the winds picked up, allowing the boat and all on board to gain Martinique. The enslaved survivors of the crossing were sold, while the black traders journeyed to Nantes “and appeared at the Exchange, where people made them welcome”—presumably they could eventually have returned to Senegal as passengers on another slave ship. 44

Slave traders’ greater challenges: negotiating across cultures, political uncertainty, and revolt

The Troqueuse case shows that dangers began before the ubiquitous Middle Passage. Even more troubling to merchants than the perils of navigating Atlantic coastlines were threats linked to cross-cultural trade and conflicts in Africa. French insurance records as well as legal records repeatedly underscore the fact that the African coast in the eighteenth and early nineteenth centuries was not a zone of colonial control. When outfitting a slave ship, merchants and shipmasters had to approach Africans as clients, studying local tastes and adapting their operations to local styles of negotiation. 45 French enslavers either catered to African consumers’ preferences and honored the terms of trade or experienced commercial failure and reprisals.

French speakers would call the African intermediaries from whom they purchased captives courtiers, using the same professional term that they applied to French dealers who matched buyers and sellers in various markets, including insurance brokers. 46 There are reports in French admiralty courts of sailors receiving patronage or recompense from African kings or rulers for having suffered an injury in their service. Such royal gifts included enslaved individuals. 47 However, French slave traders could offend local merchants or authorities as well as ingratiate themselves. One French shipmaster—Leterrier, the commander of a vessel called the Duc d’Arcourt—was forbidden to return to a comptoir in Angola after he scandalized indigenous merchants by bringing them unattractive and spoiled goods. Another member of the crew had to negotiate in his place from then on, but the substitute was unable to purchase the hoped-for number of enslaved men and women, which impacted French investors’ returns on this voyage. 48

Leterrier, in this case, faced commercial consequences for his dishonest or ill-judged manner of trading, but African coastal polities had more serious sanctions to impose on Europeans who broke their commitments to local merchants. In one instance in 1787, a botched hostage exchange led to lawsuits in France and an insurance claim involving the owners of the Blouin and the Darcy. The Darcy had received nine hostages or pawns from merchants in Gabon. The hostages were individuals with kinship ties in the area where the trade was taking place, a port near the mouth of the Gabon (present-day Komo) River, which French admiralty officials transcribed as Fétiche. The pawns served as a guarantee that the local intermediaries would return with captives in exchange for the merchandise that the commander of the Darcy, Chambert, had already handed over. However, instead of waiting for the hostages’ family or allies to return, Chambert departed the coast for America. The hostages were almost certainly enslaved and sold. This violation led to the arrest and detention of Amiaud, who had command of the Blouin, and six of his sailors at the Port de Fétiche. Identified as belonging to the same nation as the Darcy traders, these men were made to take the place of the stolen hostages and assume responsibility for their countrymen's dishonorable actions. “Considerable sacrifices” were demanded of Amiaud “to obtain his liberty”.

49

In order to rule on this case, the Admiralty Court of Bordeaux opened an inquest to determine the usage or the different usages employed … in the region of the mouth of the Gabon on the Coast of Africa: that is, the formalities that are observed there by the captains who after having made their trade for blacks on this part of the Coast, and who still have on board the hostages who were given to them by the blacks of the land, want to way anchor without exposing themselves to the irritation of these blacks.

50

Presumably, if during this investigation Chambert and the owners of the Darcy were discovered to have broken the customary law in the region, they would have been liable for the damages claimed by Amiaud and for wages and compensation owing to the sailors who had also been detained.

A further dangerous possibility for French traders was getting caught in the cross-fire of a war while trading on the coast. In 1727, a French slave-trader's merchandise was destroyed in a blaze during the final stages of the kingdom of Dahomey's conquest of Hueda. 51 The French merchant began his petition for an insurance reimbursement by describing the conflict: “the king of Dahomey entered the Kingdom of Juda [Hueda] with a powerful army”. The king, Dadá Agaja, and his soldiers “burned everything down to the smallest houses, and all the effects and merchandise that were found in the storehouses”. 52 Acts of violence and provocation on the coast of Africa could also be committed as extensions of European conflicts, as was the case in 1776, when a French slave-trading ship was captured by a British vessel and detained in Senegal, along with the captives and merchandise it was carrying. 53

The weeks and months slave ships spent in African ports were also uniquely perilous because captives selected for embarkation were likely to revolt and to attempt escape at this stage. Experienced traders learned to expect resistance during coastal trafficking or as the enslaved were transported downriver in smaller crafts, and there are many reports in legal sources of revolts within sight of the African coast.

54

In one case in 1791, a Nantes merchant wished to claim reimbursements for 31 captives who had died while they were being held on board the main ship, as it remained anchored on the coast. During the course of the Trade, a black who had come up onto the bridge with the others that were being made to take the air, threw himself of his own will into the sea and drowned himself. Shortly after the end of the Trade, there was a revolt on board, and to repress it, the crew were obliged to fire on the captives. There were 25 killed on the spot, and five gravely wounded … Eight days later these five blacks died from their wounds.

55

The Chamber of Commerce in Bordeaux issued a statement encouraging the merchant to proceed with this claim, opining that the merchant could pursue his insurers for these deaths.

In 1780, a group of enslaved people were able to gain control of the brigantine Oiseau soon after it departed the coast. The mutineers must have made a deal with the white crew; however, the details of their contract were obscured in the incident report that was eventually registered in Marseille. The leaders of the revolt secured their freedom and “entirely pillaged” the Oiseau, leaving the vessel and 21 remaining captives in the hands of the French crew. After this event, the Oiseau departed again from Gorée to make for Martinique, but it sank in open water, apparently with no further loss of life among members of the crew, who chose to save only four individuals, abandoning 17 enslaved people on board the sinking ship. 56

Containing human agency and uncertainty through insurance

Insurance underwriters and buyers had two reactions to these uncertainties of the slave trade. They charged or were willing to pay higher premiums than were demanded to cover other voyages. They also reacted by fiddling with the terms of contracts, enumerating the uncertainties of the trade and dividing them between underwriters’ and policyholders’ responsibilities. The printed forms used to draft marine insurance contracts in French cities were adaptable, featuring blank space near the top of the sheet for the contracting parties to add specific terms to the policy by hand. Insurance policies covering the French slave trade do not converge on a single model. The handwritten, tailored sections of surviving policies vary significantly from one contract to another. Too few policies whose full terms are in intact have been found in French archives for us to assert what were the common patterns in the language of these contracts. My evidence in this section is drawn from just 13 examples of insurance policies on French slave ships, housed in seven different archives (Table 1). 57 However, even this small sliver of the market can give a sense of the kinds of experiments that merchants were making to adapt the basic marine insurance policy for the Atlantic slave trade.

What had previously been known about this sector of the marine insurance business in France was mostly based on normative sources, such as legal and commercial handbooks. According to the principles of slave insurance, as we find them described in legal treatises and merchant manuals, the slaughter of captives who rose up in revolt against the crew was an insurable loss, but underwriters of slave ships did not assume liability for “natural deaths” resulting from illness, malnutrition, and suicide. 58

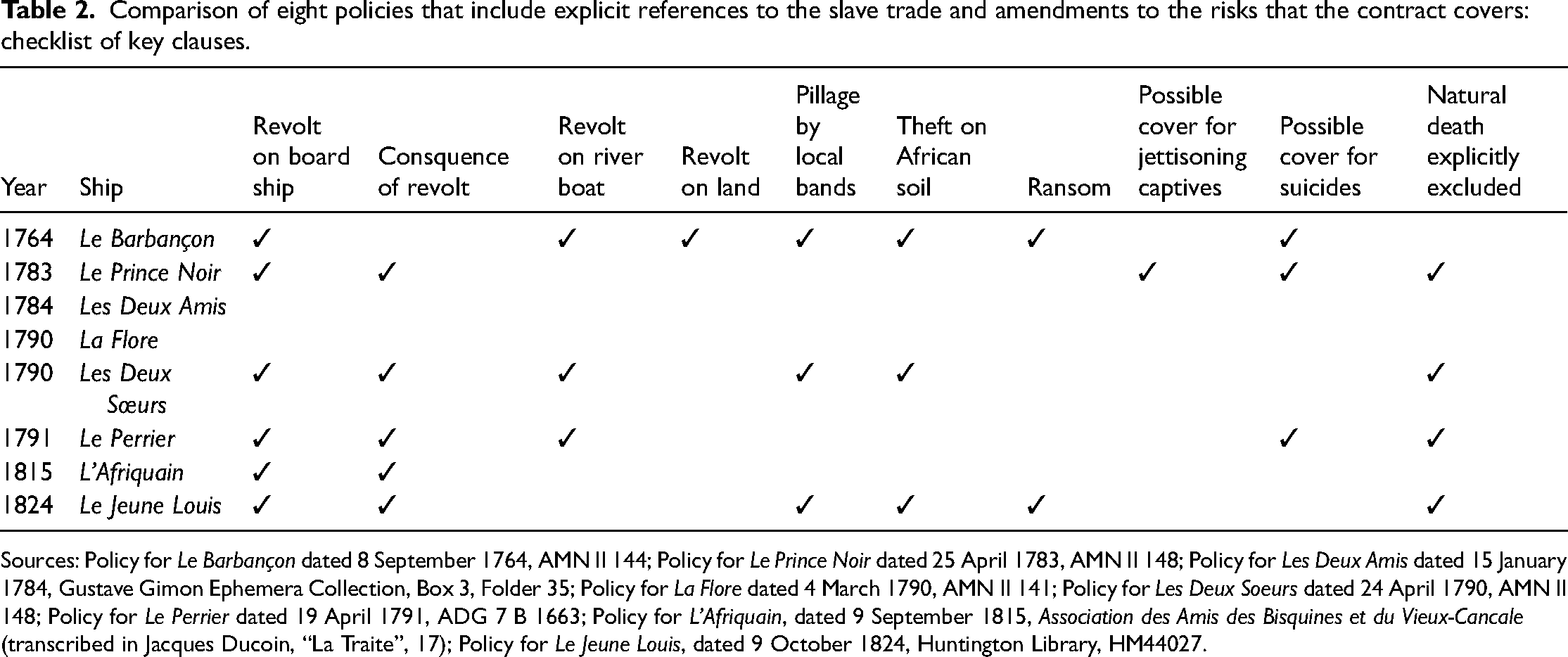

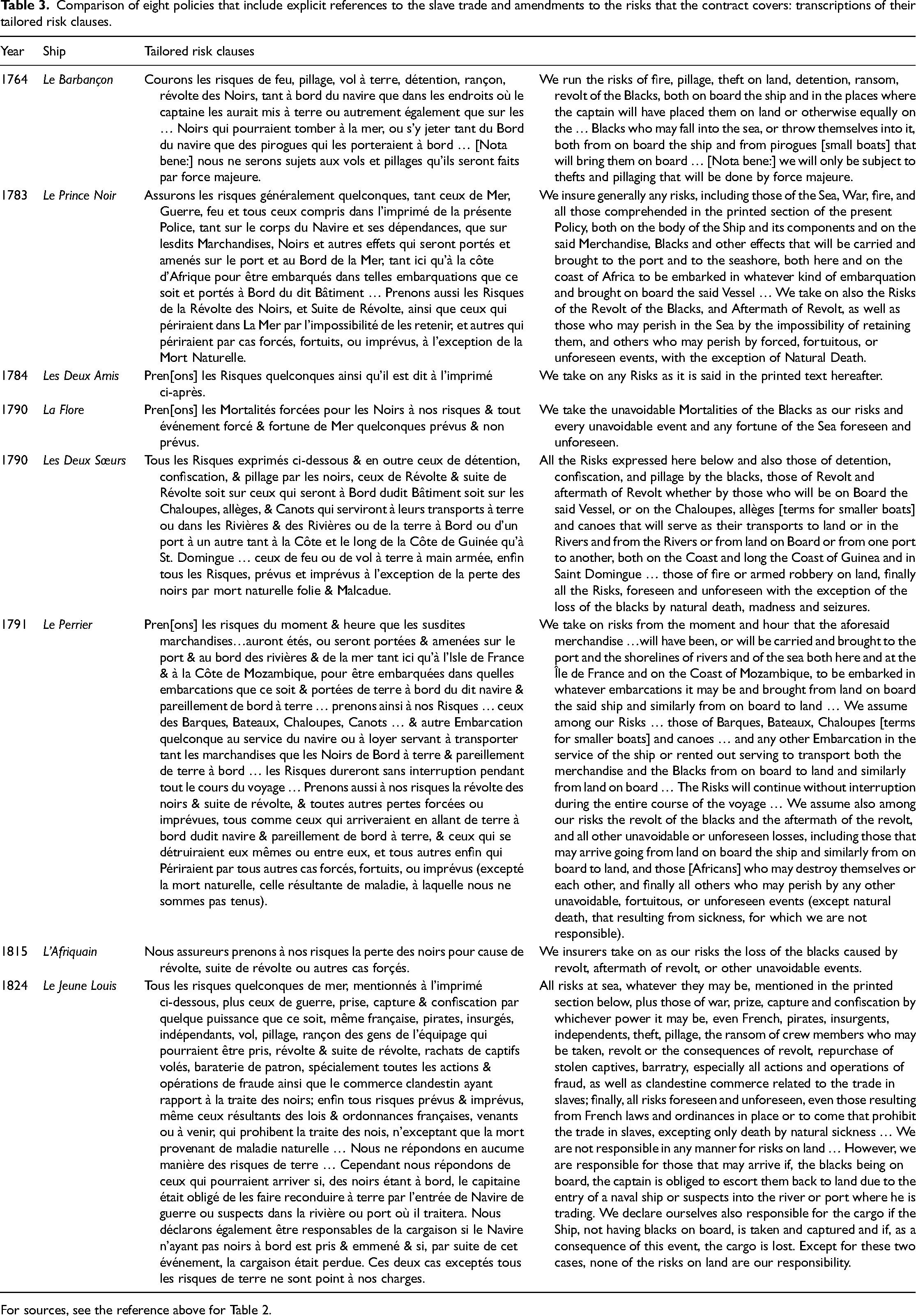

The bright line that legal commentaries tried to draw between insurable and uninsurable or “natural” deaths was not so clear in practice. Limiting the financial fallout from violent resistance certainly was a top concern for investors, and, predictably, six policies underwritten on slave consignments listed insurrection on board the main ship as an insurable risk. (See Tables 2 and 3 for comparisons of eight insurance policies whose handwritten sections refer to slave trading.) In contrast, these contracts’ concept of “natural death” was unstable and somewhat negotiable. The policy on the Perrier almost equates “natural death” with “that resulting from sickness”, a very limited definition that might have allowed the insured to claim damages for captives that harmed themselves. 59 In 1790, however, the underwriters of the Deux Soeurs, included folie (madness) and malcadue (a reference to epilepsy or fainting) in their definition of natural death, excluding claims related to these conditions. 60 Underwriters were not of one mind about how to categorize emotional and spiritual disturbance.

Comparison of eight policies that include explicit references to the slave trade and amendments to the risks that the contract covers: checklist of key clauses.

Sources: Policy for Le Barbançon dated 8 September 1764, AMN II 144; Policy for Le Prince Noir dated 25 April 1783, AMN II 148; Policy for Les Deux Amis dated 15 January 1784, Gustave Gimon Ephemera Collection, Box 3, Folder 35; Policy for La Flore dated 4 March 1790, AMN II 141; Policy for Les Deux Soeurs dated 24 April 1790, AMN II 148; Policy for Le Perrier dated 19 April 1791, ADG 7 B 1663; Policy for L’Afriquain, dated 9 September 1815, Association des Amis des Bisquines et du Vieux-Cancale (transcribed in Jacques Ducoin, “La Traite”, 17); Policy for Le Jeune Louis, dated 9 October 1824, Huntington Library, HM44027.

Comparison of eight policies that include explicit references to the slave trade and amendments to the risks that the contract covers: transcriptions of their tailored risk clauses.

For sources, see the reference above for Table 2.

The treatment of suicide was also much less clear in practice than in legal manuals. References in insurance contracts to the enslaved who would “perish in the sea” or “throw themselves in”, to those “who will destroy themselves or one another” seem to include men and women who drowned themselves or found another way on board of ending enslavement through suicide. 61 A policy from 1764 for the voyage of the Barbançon provided insurance for “the blacks who might fall in the sea, or throw themselves in either from on board the ship or from pirogues [a variety of small boat]”. Even more shocking is the inclusion, in one policy, of a clause that seems like it could condone slave jettison, or throwing living captives overboard, as the shipmaster in the Troqueuse case above had contemplated. 62 In 1784 the contract for the Prince Noir made insurers responsible for reimbursing the value of captives “who will perish in the sea by the impossibility of retaining them”. 63 A year after the infamous Zong case was argued in London, were these underwriters meaning to suggest that in a similar situation where vital food and water supplies ran low, the policyholder would be reimbursed for the slaves it was “impossible to retain”? 64

Another characteristic of policies that covered French slave ships never mentioned in law commentaries and merchant manuals is that they could be written to extend the bounds of coverage beyond the sea, and even beyond riverine spaces in Africa. In the contract for the Deux Soeurs, insurers accepted the risks of “detention, confiscation, and pillage by the blacks” resident in the regions where the ship was going to trade, “fire or theft on land by armed forces”. 65 A 1764 policy for the Barbançon included the theft, pillage, or detention of trade goods or captives on land in African ports, and the resistance of captives detained on land. 66 A third example, an insurance contract for the Jeune Louis, which transported captives to Cuba illegally in 1824, promised reimbursement in the event of “theft, pillage, the ransom of crew members who may be taken”. 67 A version of the printed insurance form briefly used in Nantes during the mid eighteenth century even extended marine insurance coverage by default to the “Land in Africa”. The short but significant new line concluded the section in the policy that defined insurable losses. It bound the underwriters to cover “generally all other perils, fortunes or fortuitous events that could arrive in whatever manner, foreseen or unforeseen, both at Sea, and on Land in Africa by force majeure”. 68 With the inclusion in the contract of losses in Africa by force majeure, theft of the goods French subjects traded for slaves, and possibly the escape of captives from forts or enclosures on land, would have been subject to insurance claims. 69 All mention of risks “on Land in Africa” was, however, struck from later versions of the Nantes insurance formula.

Such clauses stretched the marine insurance contract to its limits by making underwriters absorb losses inflicted by armed bands attacking on land or local rulers imposing commercial sanctions. Depending on their exact wording, insurance contract terms that covered confiscation would have also provided a guarantee against other European powers’ theft or capture of goods and captives. The Jeune Louis contract, for example, clearly covered uncertainties “resulting from laws and ordinances in place or to come that prohibit the trade in slaves” as well as “capture and confiscation by whichever power it may be”. 70

Analysis without calculation

In drafting insurance policies for slave-trading voyages, inserting clauses to cover pillage, confiscation, and the cost of ransoming the crew, French underwriters were taking into account political futures in Africa and in Europe, the likelihood of revolt, as well as the stochastic risks of the transatlantic slave trade. As underwriters and investors negotiated the price of coverage, they were translating the variegated (and horrifying) risks and the uncertainties of the trade into a single number, an insurance premium. The complexity of this calculation, and the scarcity of information at the disposal of slave traders and underwriters, meant that a mathematical model would not serve. Pricing insurance coverage was a matter (to use Hume's phrase) of “melting together” one's own past experiences, qualitative reports from those recently returned from the trade, and rumors of wars brewing in the Atlantic.

Thanks to the efforts of David Eltis, Stephen Behrendt, David Richardson, and many other researchers who contributed to the creation of the SlaveVoyages database, historians of the transatlantic slave trade know the statistics of mortality and the incidence of revolt on slave ships better than early modern investors. During an average voyage in the second half of the eighteenth century, it is likely that 11–13% of captives purchased by Europeans died before being transported to a slave market in the Americas. 71 Insurrections broke out during an estimated 10% of slave-trading voyages. 72 Insurers or investors in the slave trade lacked the bird's-eye view that allows historians to calculate such figures. There is no evidence that they tried to compile actuarial tables on the survival rates of enslaved men, women, and children, 73 and indeed, their estimates of mortality could be far off the mark. One plan or so-called “prospectus” for arming a 200-ton ship for the slave trade estimated that 5% of captives would perish. 74 Mortality rates among captives differed widely from voyage to voyage, which helps to account for these investors’ mistake. The distribution of mortality rates is skewed, meaning that a small proportion of voyages were truly catastrophic for enslaved Africans’ survival. 75 Even historians who have calculated mortality rates on board slave ships find it difficult to show, using a single measure, how deadly the typical voyage was. 76 The fluctuation in mortality rates on slave-trading ships made experience a less sure guide in underwriting the slave trade, compared with other lines of trade. Even those who would be expected to have had the most direct and practical knowledge, shipmasters, would see voyages with wildly varying mortality rates over the course of their careers. 77

To make the underwriting process more difficult, insurers often only received bare-bones information about the individual voyages they were being asked to cover, especially in cases when they were sought out by merchants based in distant ports. In an example from 1786, a merchant in Bordeaux penned an insurance order to his correspondents in Nantes. He wanted to protect his investment in the Courrier d’Affrique, a ship being outfitted for a slave-trading voyage. For the agents in Nantes to fulfill such a request, they needed to know some critical information, which underwriters would need to price the insurance contract: the name of the ship and skipper; the model of the vessel (it was a brick); the value of the coverage and whether cargo or keel was the object of the insurance (12,000 livres sur corps et quille and 16,000 sur cargaison); and the targeted destination or destinations. 78 Underwriters in Nantes would use the scant information in this private letter to create a baseline insurance premium for the Courrier d’Affrique, which they might then adjust based on information circulated by letter or orally.

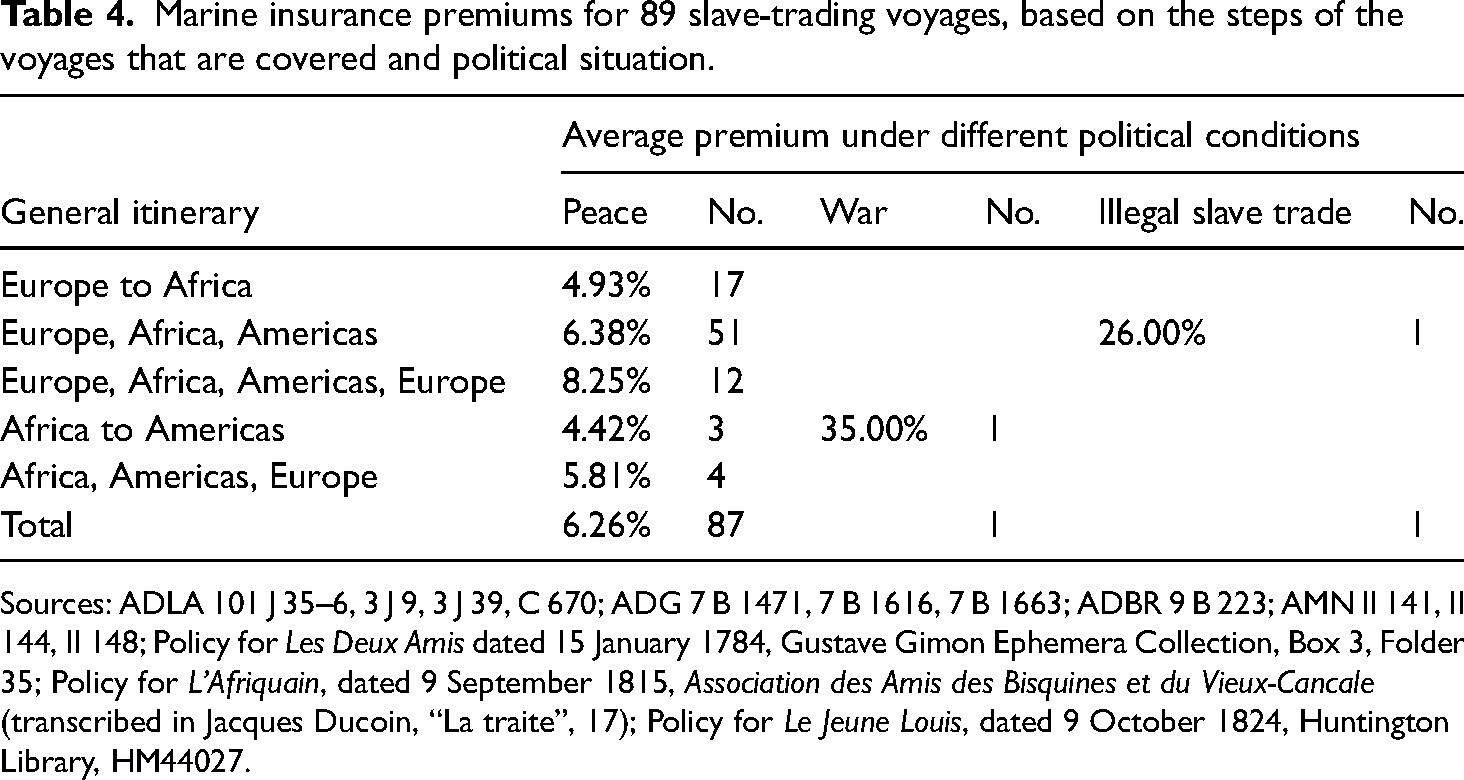

Underwriters used the length of slave-trading voyages and the number of port entries that would probably be required as general rules of thumb for determining premiums. If we break down the premiums on 89 vessels going to Africa, there are patterns according to the lengths and trajectories of these voyages (Table 4). 79 A voyage from a European to an African port was about 4.9%. Adding on the Middle Passage, the average rate increased to 6.4%, and insuring a voyage to Africa, to American slave markets and back to Europe was the most expensive, 8.3% on average. Fairly often, contracts made provision for a stop on the way to Africa in Lisbon or another Portuguese or Spanish port. Interestingly, these breaks in the journey are associated with slightly lower premiums, perhaps because they added a degree of certainty about the itinerary of a voyage—vessels going to Africa could always make intermediary stops wherever the shipmaster deemed necessary, so for the contract to indicate where these were likely to take place was extra information for the insurers.

Marine insurance premiums for 89 slave-trading voyages, based on the steps of the voyages that are covered and political situation.

Sources: ADLA 101 J 35–6, 3 J 9, 3 J 39, C 670; ADG 7 B 1471, 7 B 1616, 7 B 1663; ADBR 9 B 223; AMN II 141, II 144, II 148; Policy for Les Deux Amis dated 15 January 1784, Gustave Gimon Ephemera Collection, Box 3, Folder 35; Policy for L’Afriquain, dated 9 September 1815, Association des Amis des Bisquines et du Vieux-Cancale (transcribed in Jacques Ducoin, “La traite”, 17); Policy for Le Jeune Louis, dated 9 October 1824, Huntington Library, HM44027.

Aside from these geographic patterns, insurance premiums were significantly and strongly impacted when the chances of capture by privateers or British naval ships mounted. Thus we see the Romulus being insured at a rate of 35% near the beginning of the Seven Years’ War and the Jeune Louis covered at a rate of 26% in 1827, after France had abolished the slave trade. Such increases in insurance premiums during turbulent moments in inter-imperial politics were based on qualitative, not quantitative analysis.

Conclusion

As he first shone a spotlight on the nature of uncertainty as opposed to risk, Knight observed that even when we are really dealing with uncertainty, we do attempt to calculate “the value or validity or dependability of our opinions and estimates, and such an estimate has the same form as a probability judgment”. 80 That is, even predictions for the future that have no statistical basis are often expressed in numbers, as though we were stating a probability. Knight attributed this to the imprecision of language and of the economic concepts available at his time, but the business of insuring the slave trade shows that converting uncertainty into a price or premium has a long history. In the eighteenth and early nineteenth centuries, it was not considered irrational or particularly aggressive for insurers to attach numbers to potential outcomes whose probabilities they could not in any sense calculate. 81

Early modern underwriters were willing to stake capital without the comfort of actuarial data. Their bets were out in front of the systematic collection of data on accidents at sea which would eventually allow probability theory to be applied to marine insurance. Their main expertise was in hoarding correspondence and information in order to anticipate the global political crises and wars that would affect the safety of merchant ships on various sea lanes. Historical accounts of how insurance grew and ramified usually place the financial instrument in the same lineage as the development of mathematics and probability theory, as their practical application. 82 A promising alternative narrative would place marine insurance in a lineage of climate science or “storm science”. 83 Yet the expertise and the data used by early modern insurers also make them akin to historians or social scientists. Dealers in both risk and uncertainty, underwriters’ focus was anxiously fixed on the uncertainties of long-distance trade represented by wars, decisions by foreign rulers to arrest and confiscate merchants’ goods, revolts by captives or sailors, and other events rooted in human agency.

Policies underwritten on slave ships and on trafficked men and women in France are the prime example of how early modern marine insurance contracts blended risk and uncertainty. Believing that the default terms of marine insurance policies left their flanks unprotected, many slave traders added terms in their contracts’ blank spaces and margins to ensure they were covered against their trade's unique uncertainties. These contract amendments invariably insisted on the underwriters’ responsibility for the violent deaths of captives who resisted their enslavers, showing that investors in the slave trade had learned to expect resistance from the Africans they embarked. Some of the French insurance policies I analyzed appear to cover risks that the secondary literature says were uninsurable: risks of force majeure on dry land in Africa and losses among the captives owing to suicide. French legal treatises ruthlessly categorized the latter as a cause of “natural death”, but actual insurance policies could be construed as covering these losses. The shifting language of slave insurance policies illustrates that investors in France faced difficulty in predicting how encounters with captives, local intermediaries, and African rulers would prove dangerous. French merchants visibly struggled to define and categorize the risks and uncertainties of the slave trade.

Footnotes

Acknowledgements

The research for this article was completed with the support of the Economic History Association, which awarded me a Sokoloff Fellowship in the 2021–2022 academic year. I presented an early version of this project at the American Society for Legal History Conference in 2021, and I am very grateful to Hannah Farber, Christian Burset, James Oldham, Amalia Kessler, Lauren Benton, and other participants in the conference for their comments on my paper and for encouraging me to keep digging. Many thanks to Gijs Dreijer, Lewis Wade, and all the faithful attendees of the seminar on Risk and Uncertainty in the Premodern World, who also heard me present this research at an early stage. I also wish to thank Francesca Trivellato, Greg Mark, Naomi Lamoreaux, Sabine Go, Jake Dyble and Gregory Smaldone for reading with great care and patience my dissertation chapter on insurance in the French slave trade. Your comments and probing questions shaped the present article. Many thanks to the anonymous reviewers, whose suggestions helped me to clarify my thinking and greatly improved this text. Finally, I owe a special debt to Erika Vause, who originally uncovered the policy for Les Deux Amis and generously shared this precious source with me.

Author contribution

Sole author.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethical approval

Not applicable.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Economic History Association and the Sokoloff Fellowship program, the Institute of Historical Research, the University of London, and the IHR Partnership Seminar Series).

Notes

Author biography

Mallory Hope is postdoctoral research fellow at the Center for History and Economics, Harvard University. She recently finished her PhD on the insurance market in late eighteenth-century France at Yale University and has published on the French insurance market and its relationship to the slave trade.