Abstract

A high percentage of men and women are purported to justify intimate partner violence (IPV) in countries that are steeped in patriarchy even in the presence of programs such as microfinance that aim to address gender equity. This article examines two assertions that emerge from the literature on microfinance and its potential for positive outcomes for women who participate in it: (a) Microfinance participation is associated with reduced justification of IPV, and (b) microfinance participants with control over their own resources are less likely to justify IPV when compared with microfinance participants who do not have control over their resources. Couples data from a nationally representative survey, the Bangladesh Demographic and Health Survey, were used in the present study. Propensity score matching and logistic regression analyses were conducted to reveal that (a) microfinance participation was not associated with justification of IPV and that (b) women who participated in microfinance were less likely to justify IPV when they had no control over their resources. Implications for practitioners and policymakers are discussed.

Introduction

Intimate partner violence (IPV) is a pervasive problem affecting 30% of women globally, according to a recent World Health Organization (WHO, 2015) report. In Southeast Asia, the lifetime prevalence rate of IPV is higher than the global rate at 37.7% (WHO, 2015), whereas in Bangladesh it is close to 60% (Bangladesh Demographic and Health Survey [BDHS], 2009). Such high rates of IPV are an indication of the extent to which ideologies that support IPV are prevalent (Schuler, Yount, & Lenzi, 2012). Such ideologies inform belief systems, which means, individuals justify IPV, particularly in patriarchal systems that subjugate women in all aspects of their lives, thus normalizing violence against women (Anwary, 2015; R. Campbell & Wasco, 2005; Fahmida & Doneys, 2013; Heise, 1998; Lawoko, 2006; Mookherjee, 2012; O’Donnell, Smith, & Madison, 2002).

It is in the presence of this patriarchal paradigm that women’s groups have campaigned for women’s rights in Bangladesh, culminating in the creation of laws to protect women from violence, as well as economic institutions such as microfinance that aim to empower women (Anwary, 2015; Kabeer, 2012). The present study examines attitudes regarding IPV among women participating in microfinance, that is, whether they are more or less likely to justify IPV when compared with nonparticipants of microfinance. Second, this study examines the interaction effect of microfinance participation and control over resources on justification of IPV, as economic intervention means little for women if they have no control over their resources/earnings acquired through said intervention (Goetz & Gupta, 1996; Hermes & Lensink, 2011). This is particularly important because, research shows, many women hand over their loans to their husbands (Karim, 2014).

Justifying IPV

Extant literature indicates that the key reason for which women remain in violent relationships, or are coerced into accepting and justifying IPV, has to do with economic dependency on abusive partners. Studies show that employed women are more likely to leave abusive relationships, indicating the importance of personal resources in their decision to remain or leave abusive relationships (Estrellado & Loh, 2013; Gelles, 1976; Strube & Barbour, 1984). But seen with the literature that indicates that women who try to leave often face escalated violence or even death when they are found out points to why women may still tend to remain in such relationships (Campbell et al., 2003; Fleury, Sullivan, & Bybee, 2000).

Another reason why women tend to justify IPV is because they have to make sense of their own violent situations and circumstances and support their own actions (or inactions) which then allows them to remain in abusive relationships (Eckstein, 2011). Other reasons, such as not having anywhere to go, having children to take care of, limited freedom of movement and autonomy, and disability, which arguably are also related to limited economic resources, also contribute to justification of IPV (Herbert, Silver, & Ellard, 1991; Martin et al., 2000; Saxton et al., 2001; Singh & Cready, 2015).

Thus, the current study problematizes the notion of justification of IPV, suggesting that some women justify violence as a mechanism to accept their decision to remain in violent relationships in the presence of factors—including structural issues—that keep them in the relationship (Cooke, 2015). This means that the reasons for which women are unable to leave abusive relationship are at the root of the reasons for which they may justify IPV. For others, justification of IPV comes with being part of an environment that espouses patriarchal notions of family and society formation (Hunnicutt, 2009; R. Jewkes, Levin, & Penn-Kekana, 2002; Khan, 2005; Yllo & Straus, 1990). In line with that argument, the current study assumes that not only men, but women may justify violence in intimate partner relationships/marriages when overarching social structures are patriarchal in nature (Schuler & Islam, 2008).

Justifying IPV allows for the maintenance and continuation of IPV in the lives of women, which ultimately has immense costs: individual, social, economic, and political (Plichta, 2004; Reeves & O’Leary-Kelly, 2007). Scholars argue that the individual and community costs are higher in developing countries where institutions are weak in terms of providing help to individuals experiencing IPV as the responsibility of providing help gets relegated to immediate families and community members who may not have the infrastructure to actually provide help (Devries et al., 2013).

Recently, however, more women have been found to be seeking formal help from law enforcement for IPV in Bangladesh, indicating perhaps a change in mind-sets about IPV being a private matter that should be resolved at home. This change may be attributed to high-publicity cases of IPV such as the case of Rumana Manzur, whose husband blinded her in violent rage (Anwary, 2015) as well an increase in gendered “empowering” institutions such as nongovernmental organizations (NGOs) such as microfinance that aim to empower women by providing them with micro loans utilizing a collateral-free group lending model that may have positive spillover effects even if poverty estimates may not change over time (Amin, Hossain, & Mathbor, 2013; Basher, 2007; S. S. Chowdhury & Chowdhury, 2011; Chowdhury, 2010; Dalal, Dahlström, & Timpka, 2013; Fernando, Heston, & American Academy of Political and Social Science, 1997; Hoque & Itohara, 2009; T. B. Hossain, Bhuiyan, Siwar, & Ismail, 2013; Lewis, 1997; Mainuddin, Ara Begum, Rawal, Islam, & Shariful Islam, 2015).

In short, this body of literature lead to the assertion that economic independence enables women to leave violent relationships; which means, in the context of this study, economic independence—through microfinance—may allow women to refrain from justifying IPV, as they would then have the freedom to leave, negating the need to justify their own (in)actions to remain in the relationship.

Microfinance and Justification of IPV

Microfinance is a broad term that constitutes financial services, such as credit, insurance, and savings, available to women living in poverty in Bangladesh. Starting out as a micro-loan program to encourage women to build microenterprises to lift themselves out of poverty, some microfinance organization now also include services such as savings account and saving for education for children of microfinance participants (Counts, 2008; Pitt, Khandker, & Cartwright, 2006; Yunus, 2003, 2007).

Microfinance emerged in Bangladesh in the 1970s with Mohammad Yunus’ Grameen Bank, which he built to expand financial inclusion by providing banking services to individuals who are traditionally deemed non-creditworthy. Microfinance organizations, instead of requiring participants to put down collateral, group them into “lending groups” such that all members of the group are held accountable for repayment of the individual loans. The lending groups meet biweekly with an officer from their microfinance organization during which payments and repayments are made and discussions are had about their business practices. Recent research indicates that not all microfinance organizations create lending groups, some are like moneylenders who charge high interest rates on loans (Amin et al., 2013; Cons & Paprocki, 2010; Grameen Bank, 2015; Hermes & Lensink, 2011; A. N. M. Z. Hossain, 2015; T. B. Hossain et al., 2013; Weber & Ahmad, 2014).

Microfinance can be viewed as economic resources that have the potential of generating future income. Proponents of microfinance contend that participating in microfinance has the potential to increase options for women including the option to leave abusive relationships (Basher, 2007). However, microfinance participation has been found to increase experience of IPV among wealthier women as couples may experience status inconsistency (Murshid, Akincigil, & Zippay, 2016). To understand why that may be, the current study aims to provide an understanding of whether microfinance participation allows women to accept IPV, which in turn may allow its maintenance, as the previous study suggests. Thus, the first hypothesis to be tested in this study is that participating in microfinance allows women to justify IPV. However, the opposite could be true, too; access to economic resources may reduce their economic dependency on their husbands, which in turn may create an opportunity for increased odds of leaving abusive relationships (Tolman & Rosen, 2001).

Extant literature also suggests that economic resources need to be coupled with agency over said resources for women to leave abusive relationships, particularly in the context of poverty (Ali & Hatta, 2012; Amin & Becker, 1998). It is the extent to which women have control over their assets or businesses that allow women to have agency and control in the household, which is why it is important to examine the interaction effect of microfinance participation and control over assets on justification of IPV. Thus, the second hypothesis to be tested is that microfinance participants who have control over their own earnings and assets are less likely to justify IPV (Goetz & Gupta, 1996; Kabeer, 2001; Uddin, 2015; Ullah & Hultberg, 2009).

Method

Data

The couples data from the BDHS (2011) were utilized in this study, ensuring that women are matched on characteristics of their husbands as well as their own, thus taking into account individual, household, and relational characteristics that may impact microfinance participation.

Complex sampling design was used to recruit participants of the study from all seven divisions of the country, which was divided into enumeration units with 100 households making up one enumeration unit. After these clusters were created, households were randomly chosen from which the study participants were selected after establishing residency and gaining consent.

The sample size of the original study was 17,141 women aged between 12 and 49 years, and one third of the men married to the women. The current study, however, restricts the sample by using couples data and listwise deletion of missing data. The inclusion criteria of current study were married women between the ages of 15 and 49 who responded to questions related to microfinance participations and the battery of questions on attitudes toward IPV, and control variables which restricted the size to 1,356. The BDHS (2011) data set does not consist of questions on experience of IPV, which precludes the current study from distinguishing between women who experienced IPV and women who justified IPV.

Measures

Justification of IPV is defined in this study as accepting IPV, that is, various forms of violence that are used to control others in an intimate partner relationship, including physical, emotion, sexual, and financial forms of violence (Schuler, Lenzi, & Yount, 2011). The justification process can take the two following forms, even though there are likely to be variations or a mix of these two forms: (a) It is focused on the inability of the perpetrator of violence to control himself—the argument being more salient for sexual crimes, and/or (b) it is focused on the individuals against whom violence has been perpetrated, who blame themselves, or are blamed for the violence. In cultures where men’s subordination of women is widespread and normalized, it is likely that women hold similar ideas about women’s place not just in society but in their households and their relationships (Koziol-McLain, Giddings, Rameka, & Fyfe, 2008; Lees, 1997; Salam, Alim, & Noguchi, 2006).

In the current study, justification of IPV was constructed as women who justified partner violence under certain circumstances: if the wife burns food while cooking, if she neglects children, if she refuses to have sexual intercourse with her husband, and if she goes out without her husband’s permission. If they responded that they justified “wifebeating” under any of the above circumstances, they were deemed as those who justified IPV (justification of IPV = 1). These reasons that were provided to respondents to choose from are based on the normative binary framework of patriarchy and gender, reflecting a system that subordinate women and confer traditional gender roles that require being conformed to, so as to maintain that subordination. When women are unable to adhere to such roles, they justify IPV, allowing men to have their heteronormative privilege over them, which precludes them from having any other identity, and paying for the perceived emasculation that occurs when gender roles are threatened by accepting their own subordination (Anwary, 2015; Butler, 1990). Based on this characterization of IPV and subjugation by Anwary (2015) and Butler (1990), this variable was constructed as a dichotomous variable in which women who identified with at least one of the above statements were deemed to justify IPV. Given that the scenarios provided by the BDHS were not exhaustive, it would be erroneous to categorize those who agree to more than one statement as someone who justifies IPV more strongly than someone who agrees to one.

The key independent variable, microfinance participation, was measured as a dichotomous variable based on membership in one of five microfinance organizations and “any other” not identified by the Demographic and Health Survey questionnaire: Grameen, Brac, Asa, Proshika, and BRBC—all of which use a group lending model in the absence of collateral to provide individual loans to women while all group members are held responsible for loan repayment of group members. Respondents who said they belonged to one or more of these organizations were construed as microfinance participants (microfinance participant = 1). Control over resources was measured through questions on women’s decision-making power over their own earnings. If respondents made sole decisions or joint decisions, they were identified as having control over their resources. If respondents indicated that their husbands made decisions over their earnings, they were identified as not having control over their resources.

Salient control variables were selected from the literature to control for extraneous factors that may affect attitude towards IPV. The demographic variable wealth assets was measured as a dichotomous variable based on an index that constituted material assets that respondents owned, thus differentiating between respondents who owned wealth assets and those who did not. The rest of the demographic variables included age, husband’s age, education level, husband’s education level, employment status, religion, media exposure, number of household members, and gender of household head. Responses pertaining to husbands’ age and education, and gender of household head were cross-checked by comparing the responses of women and their husbands. In case of disparity between the respondent and their husbands’ responses, the cases were eliminated and treated as missing. All missing data were handled through listwise deletion.

Analytic Plan

Univariate analyses were conducted to provide descriptive statistics of all the variables: justification of IPV, microfinance participation, control over resources, and demographic variables.

Propensity score matching (PSM) techniques were used to assess the difference between women participating in microfinance and women not participating in microfinance in terms of justification of IPV. PSM techniques were chosen for its ability to address self-selection and endogeneity biases that are inherent in all cross-sectional survey data. This technique creates treatment (microfinance) and control (non-microfinance) groups based on propensity scores that match women from treatment group to women in control group based on demographic and other variables that may influence microfinance participation. The isolates the treatment (microfinance participation) that differentiates between the treatment and control groups and allows for causal inferences to be made.

Logistic regression was then used to identify the interaction between microfinance participation and control over resources on justification of IPV. This was done to further the research on the difference that microfinance participation may make on justification of IPV to take into account the role that control over resources may play on justification of IPV, given that many women give control of their loans to their husbands which may potentially negates the effect of microfinance participation on women (Goetz & Gupta, 1996; Karim, 2014).

Results

Sample Characteristics

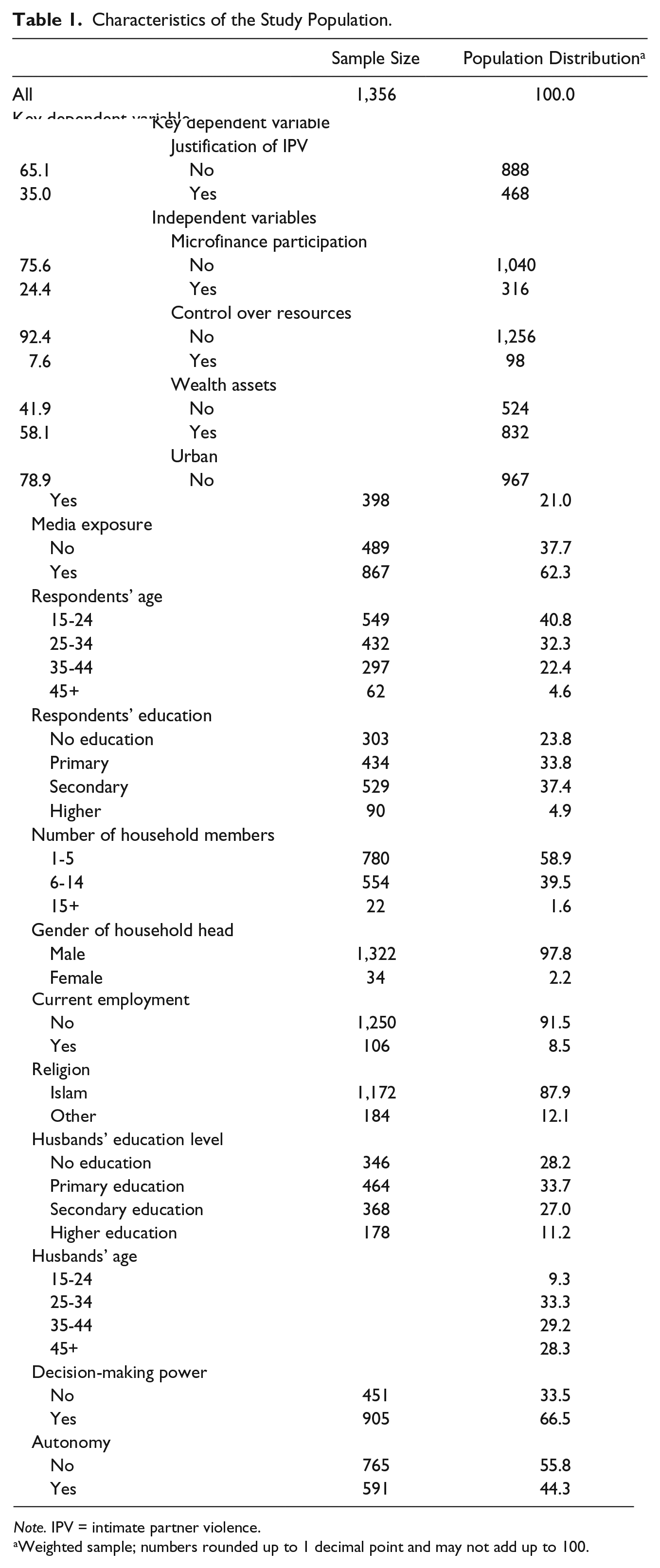

After accounting for missing values, the sample size was restricted to 1,356 respondents. Population estimates (i.e., weighted estimates) calculated for the study population (Table 1) revealed that 35% of the study population justified IPV, 24.4% participated in microfinance, while only 7.6% of the study population had control over their own resources even though approximately 58% of the study population reported to owning household assets. Twenty-one percent of the study population lived in urban areas, 62.3% had exposure to media, 97.8% of the study population reported that their households were headed by males, 87.9% reported to being Muslim, and 91.5% were not employed at the time of the interview. In terms of age, 40.9% were between 15 and 24 years, 32.3% were between 25 and 34 years, 22.4% were between 35 and 44 years, and 4.6% were over 45 years old. In terms of their husbands’ age, only 9.3% were between 15 and 24 years, 33.3% were between 25 and 34 years, 29.2% were between 35 and 44 years, and 28.3% were over 45 years old. In terms of respondents’ education, 23.8% reported to not having any education, 33.8% reported primary education, 37.4% reported secondary education, and 4.9% reported higher education. In terms of the husbands’ education, 28.2% reported to not having any formal education, 33.7% reported completing primary education, 27% reported completing secondary education, and 11.2% reported higher education. In terms of decision making, 66.5% reported that they had decision-making power in the household, that is, they made decisions either independently or in collaboration with their husbands, and 44.3% said they were autonomous and had freedom of movement when it came to seeking health care services for themselves.

Characteristics of the Study Population.

Note. IPV = intimate partner violence.

Weighted sample; numbers rounded up to 1 decimal point and may not add up to 100.

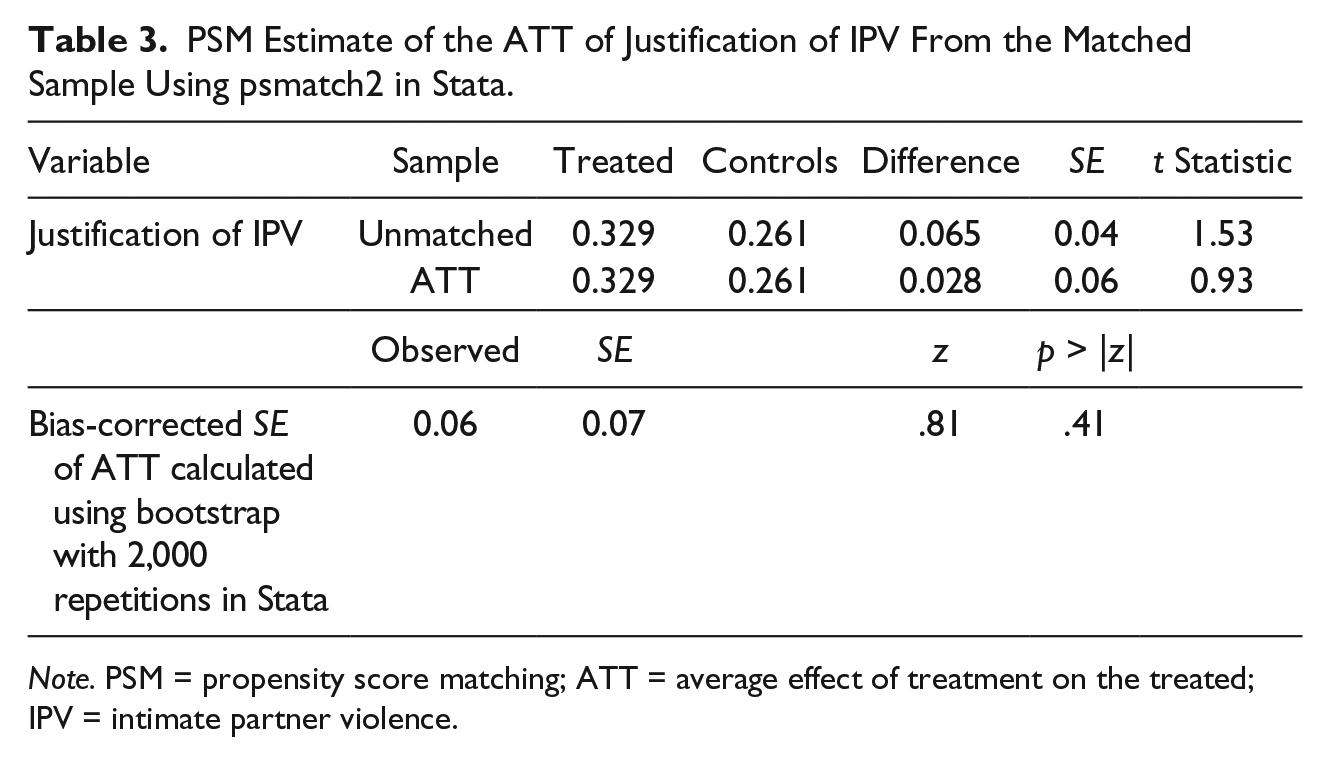

Average Effect of Treatment on the Treated (ATT) Estimate From PSM

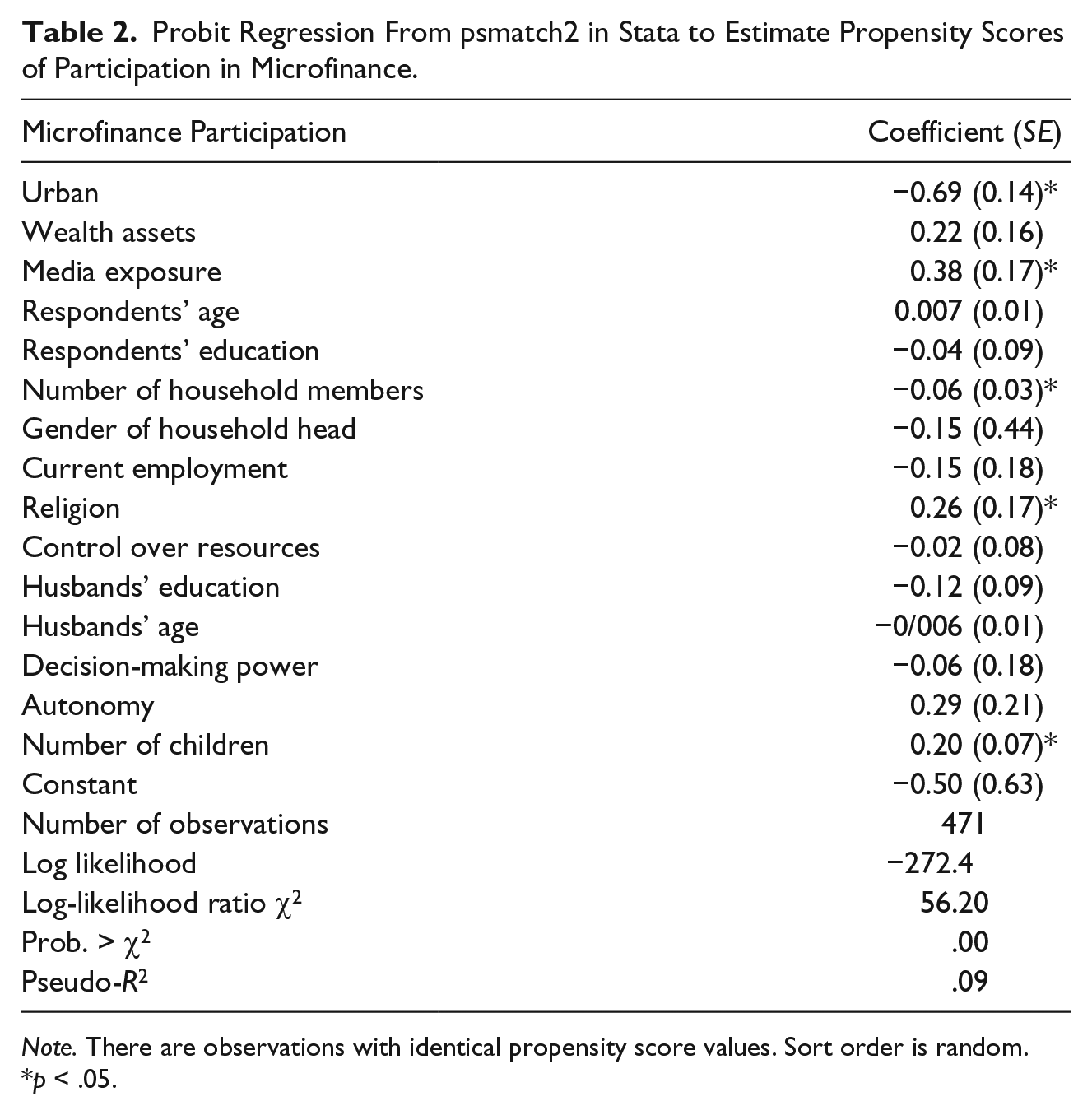

PSM techniques were implemented to compare microfinance participants with nonparticipants who had the same propensity to participate in microfinance using psmatch2 in Stata 13. Microfinance participants were treated as the “treatment group” whereas nonparticipants were treated as the “control group” in this study. Table 2 shows results from the probit regression that was generated as the propensity score of microfinance participation was estimated. Table 3 shows the postmatching results of the estimation of the ATT. The ATT revealed a comparison between the unmatched and matched samples of treatment and control groups. The unmatched sample of microfinance participants and nonparticipants showed a difference of 6.5 percentage points in terms of justification of IPV. The ATT estimation indicated that the difference in justification of IPV between participants and nonparticipants based on the matched sample was only 2.8 percentage points. Neither of the estimates were significant at the .05 level; the estimate from the unmatched sample was found to be significant at the .1 level. Bootstrapping the ATT 2,000 times confirmed that the difference in justification of IPV among the two groups was not significant at the .05 level.

Probit Regression From psmatch2 in Stata to Estimate Propensity Scores of Participation in Microfinance.

Note. There are observations with identical propensity score values. Sort order is random.

p < .05.

PSM Estimate of the ATT of Justification of IPV From the Matched Sample Using psmatch2 in Stata.

Note. PSM = propensity score matching; ATT = average effect of treatment on the treated; IPV = intimate partner violence.

Logistic Regression

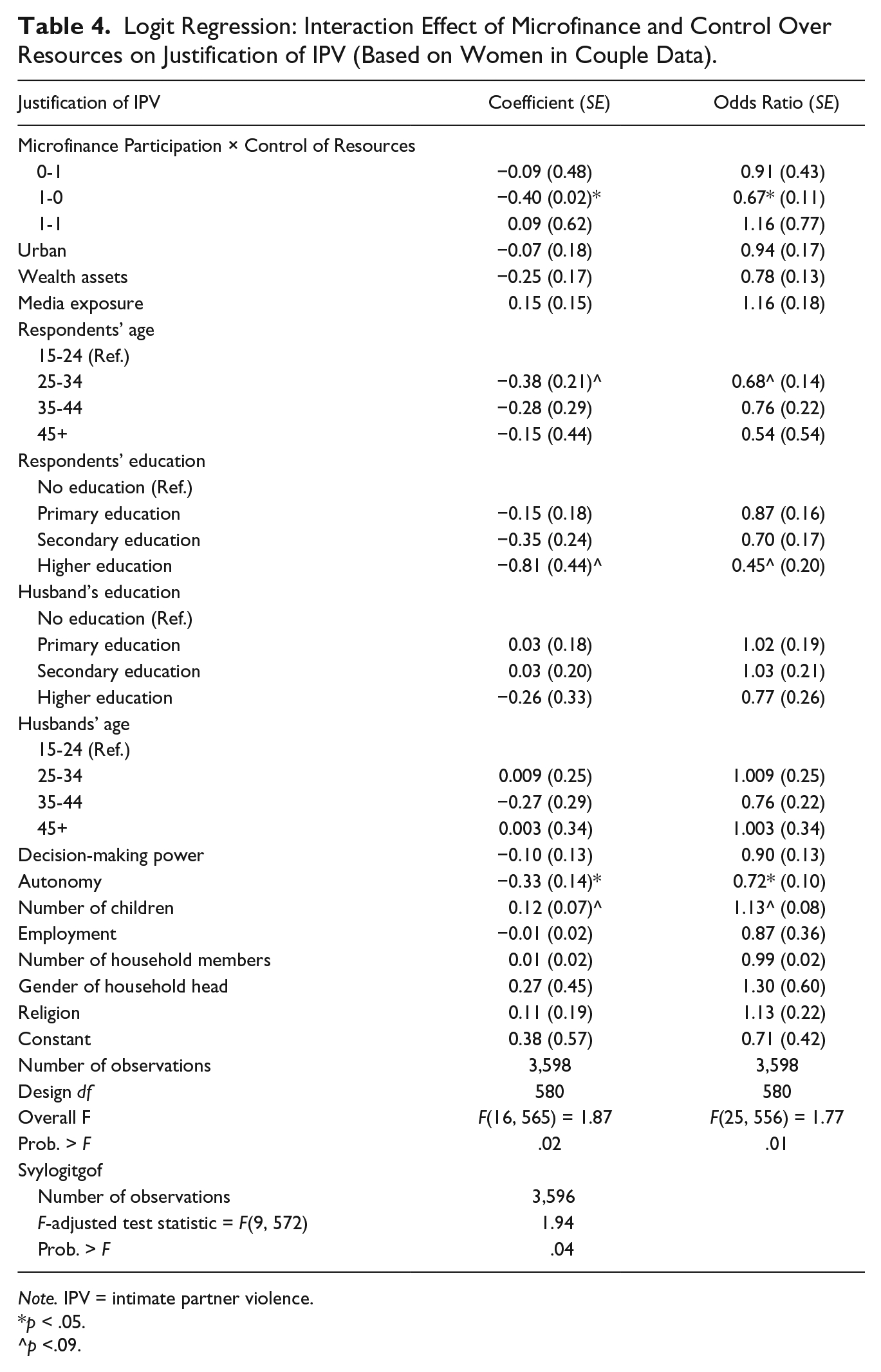

Logistic regression analyses were conducted to assess the role of “control over resources” among microfinance participants on justification of IPV (Table 4). Results revealed that when microfinance participants had control over resources, justification of IPV increased by 0.09, but this was not significant. On the contrary, when microfinance participants had no control over their resources, justification of IPV significantly reduced by 0.40 (odds ratio [OR] = 0.67; p < .05). Justification of IPV was also found to be significantly negatively associated with autonomy (β = −.33, OR = 0.72; p < .05). In addition, being between the ages of 25 to 34 years was marginally significant (β = −.38, OR = 0.68; p < .1), that is, justification of IPV was less among women aged between 25 and 34 years when compared to women between the ages of 15 and 24 years. Having more children was also marginally associated with justification of IPV (β = .12, OR = 1.13; p < .1). All other variables were not significantly associated with justification of IPV.

Logit Regression: Interaction Effect of Microfinance and Control Over Resources on Justification of IPV (Based on Women in Couple Data).

Note. IPV = intimate partner violence.

p < .05.

p <.09.

Discussion

The findings of the present study revealed that microfinance participants are perhaps not much different from nonparticipants in terms of justification of IPV, indicating that the spillover effect of microfinance does not include changes in attitude towards IPV. This drives home the point that a loan by itself cannot change mind-sets, and that national development plans that aim to empower women should be specific about goals, instead of using empowerment as a catch-all phrase to mean positive outcomes for women (Hanchett, 1997; Junankar et al., 2009; Pal & Dutta, 2015).

The second piece of finding from this study indicating that microfinance participants who had control over resources were more likely to justify IPV, at first glance, appears to counter what the literature says about economic independence and its negative association with justification of IPV. But there are three explanations that may be applicable, each by itself or all together. First, it is possible that microfinance participants who have control over their resources, which means they have a say in the spending of their own money, are among the more successful entrepreneurs who, in turn, are likely to be the ones who turn over their loans to their husbands to run the business. If that is the case, it is likely for a woman, for example, to justify IPV to justify remaining in the relationship, particularly if she and her husband have invested in a loan that is in her name and she needs him to run the business. The added dependency on an aggregate level may be at the root of the increased odds of justifying IPV (Watt, Bobrow, & Moracco, 2008).

Second, it is possible that microfinance participants who have control over their own resources are less likely to leave the stability of having a family and a business that allows them economic freedom, something that they would have to potentially forgo if they decided to leave the relationship, thus justifying (and accepting) IPV in exchange for resources to have control over.

Third, given the high prevalence of lifetime IPV, which is reported by almost 60% of representative samples (BDHS, 2009), as well as high rates of poverty in Bangladesh, women are perhaps more likely to prioritize poverty-reducing strategies over violence-reducing strategies that have implications for her entire family, including their children and parents.

Implications for Policy and Practice

Microfinance practitioners have much to learn from the study findings, particularly regarding the importance of bundling social services with microfinancial services. Microfinancial services, across the world, have been “coupled” with various interventions, indicating the salience of this model. For example, it has been used for reducing HIV risk behaviors (Pronyk et al., 2008), to control tuberculosis (Boccia et al., 2011), for depression (Ssewamala, Neilands, Waldfogel, & Ismayilova, 2012), as intervention for sex workers (Tsai, Witte, Aira, Altantsetseg, & Riedel, 2011), to address AIDS and gender inequality in South Africa (Kim et al., 2007), for global health (Patel, 2014), and more widely to eradicate poverty (Pitt et al., 2006). Bundling microfinance with couple’s intervention regarding gender dynamics and healthy relationships would be a first step toward addressing the problem of justification of IPV such that women and their husbands would learn that violence is not acceptable.

The most important takeaway from the study is perhaps regarding control over resources that suggests that men as heads of household are still in control of resources, including resources that women bring to the household. In the event that women do control the resources, it appears that they accept and justify IPV as part of that equation. This is extremely important for microfinance organizations to understand and be in a position to change (Gill & Stewart, 2011). Microfinance, as a gendered tool, should not be allowed to be oppressive but progressive, and organizations must take steps to prevent women from becoming “free labor” for their husbands and work toward its goal of creating women entrepreneurs with control over their own lives, resources, and bodies (Kabeer, 2005; Karim, 2014).

Finally, the present study should be seen with studies that question the role of empowerment in general, and microfinance in particular, in reducing IPV to provide at least a partial explanation for which IPV rates do not fall with microfinance participation (Chin, 2012; Junankar et al., 2009; Murshid et al., 2016; Pal & Dutta, 2015; Rahman, Hoque, & Makinoda, 2011; Schuler, Lenzi, Nazneen, & Bates, 2013).

Limitations and Future Research

Despite the use of PSM techniques that address self-selection bias, the use of cross-sectional data makes it difficult to make causal inferences. At the same time, self-reported data are prone to social desirability bias, particularly when sensitive questions such as those pertaining to IPV are asked. Future research should use panel data to mitigate issues regarding causality.

A limitation with the BDHS questions pertaining to justification of IPV that scholars such as Schuler and colleagues (2012) have found is that it underrepresents the proportion of individuals who justify IPV, indicating that providing further context may generate a higher number of individuals who justify IPV.

The study is also limited in its ability to provide the context in which microfinance participants’ control over resources may be associated with justification of IPV, revealing a need for qualitative studies to explore the perspectives of women participating in microfinance regarding how microfinance may affect their relationships with their husbands and the role that their husbands play in their microbusinesses.

Footnotes

Acknowledgements

The author is grateful to Macro International for making the Bangladesh Demographic and Health Survey (BDHS, 2011) data set available for analysis. Many thanks to all respondents who took part in the study and anonymous reviewers for helpful comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.