Abstract

Reports of renewed of interest in Employee Stock Purchase Plans have recently appeared, perhaps driven in part by the robust state of the stock market, that give a positive glow to these plans. But HR professionals should react with caution and carefully examine all aspects of these plans before enhancing or adopting one. Plans have recently been terminated and made less attractive to employees, and many companies have passed on the idea. Important data affecting plan design and employee participation have not been reported that contribute to a low level of interest. Involvement of major HR consultants is lacking and HR specialists appear to be in no hurry to champion these plans. Despite these factors, HR professionals should give these plans serious consideration because of their potential value for compensating employees in certain circumstances.

In recent months, articles in business magazines and HR professional journals have appeared suggesting that Employee Stock Purchase Plans (ESPPs) are experiencing a resurgence of interest among employers. The articles are based on recent surveys showing that, for example, companies are enhancing the attractiveness of these plans by increasing employee discounts on company stock purchases.

ESPPs appear to have experienced a peak in interest in the early 2000s, well before the steep decline in the stock market during the Great Recession. In addition, before 2005, companies were not required by accounting rules to consider the sale of shares to employees as a business expense in financial reports. These plans appear to be benefitting now from the new highs in the stock market that make many employees feel upbeat about investing in stocks.

Evaluating these plans is a challenge for HR professionals, as they are an uncommon employee benefit and receive little attention from HR consultants. A clear picture of successful plans and important information on plan features, employee participation, investment behaviors and returns are hard to find, as described below. Despite these obstacles, HR professionals should give these plans serious consideration because of their potential value for compensating employees in certain circumstances.

The Basics

ESPPs allow employees to purchase common stock in their company directly from their employer through accumulated after-tax payroll deductions, up to specified maximums. Shares are typically made available to the plan through issuance of additional shares of company stock.

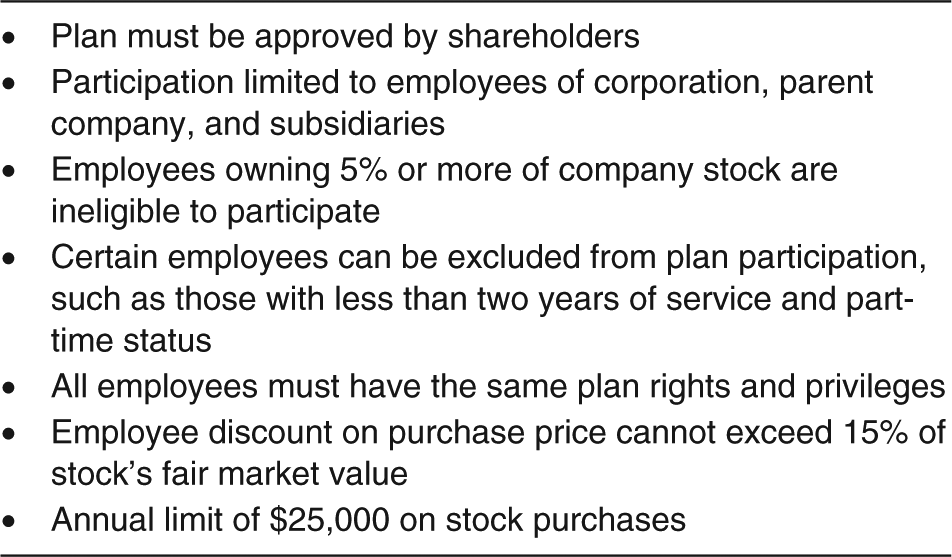

Shares are often purchased at a discount from the market price of up to 15%, whereas some plans offer matching shares instead of a discount. Some have favorable rules for determining the fair market value of the stock to be purchased to which the discount can be applied. Some allow employees to sell their shares immediately after purchase to ensure an investment gain, whereas others stipulate a holding period to promote a sense of company ownership. If a plan meets requirements in the U.S. tax code (see Figure 1), as is frequently the case, participants are eligible to receive favorable capital gains tax treatment when they sell their shares. Although plans can be international in scope, this discussion pertains to U.S. employees in most respects.

Summary of basic rules for offering tax-advantaged ESPPs under U.S. Internal Revenue Code.

Prevalence

ESPPs are an uncommon employee benefit in the United States. According to the Society for Human Resource Management (SHRM) 2013 Employee Benefits Survey of SHRM members, 12% work for organizations that offer ESPPs, as compared to 92% that offer a 401(k) savings plan. 1

This result is somewhat expected given that 52% of the survey sample were members who worked for privately owned, for-profit organizations; 19% who worked for publicly owned, for-profits; 23% who worked for nonprofits and 6% who worked for governmental agencies. Nonprofits and governmental agencies do not issue stock, and ESPPs are not popular in privately held for-profit organizations, due to the high level of tax and administrative complexity inherent in these plans. 2 There are a surprisingly high number of privately held companies. According to one source that specializes in collecting information on them, among the over 150,000 firms operating in the United States that generate over $10 million in annual revenues, roughly 90% are privately held, for-profit companies. 3

These factors combine to make ESPPs a rare benefit for U.S. employees. Their prevalence in for-profit, publicly owned companies has not been determined. Recent reports on usage and participation are described below.

Usage Reports

One of the challenges in understanding ESPPs is that there is no single source of information on the current popularity of these plans, so it is necessary to rely on surveys from several sources to get a feel for plan usage, as shown below. And there are questions about survey samples. None of the reports claim a survey sample that is random and representative of the entire universe of companies with ESPPs. The National Center of Employee Ownership (NCEO) estimates that there were 4,000 ESPPs at year-end 2011. 4 Also, an academic study of ESPPs involving about 1,500 companies is not cited here because of much of the data was obtained from a sample of company documents dated in 2002 to 2007, well before the stock market crashed and important changes were made in U.S. accounting rules for such plans that affected usage. 5 Surveys summarized below cover at most 581 plans.

According to PricewaterhouseCoopers (PwC) 2012 Global Equity Incentives Survey of 351 multinational companies, 9% of companies eliminated their plan in the prior year and 38% did so over the previous 2-3 years. 6

According to Ayco’s 2012 survey of 180 corporate partners, about 5% eliminated their ESPP. 7 Ayco is a provider of financial counseling and education services for corporate executives, employees and high–net worth individuals and families.

According to the 2011 The National Association of Stock Plan Professionals (NASPP) Domestic Stock Plan Survey of 581 companies, the percentage of companies offering ESPPs was 52%, down from 64% in 2004. The survey was conducted by Deloitte Consulting and NASPP, in conjunction with the Certified Equity Professional Institute (CEPI).

Matching these less than stellar trends in usage are employee participation rates for companies that offer ESPPs, as summarized below.

Participation

High rates of participation in these plans remain a lofty goal according to industry experts, as noted below 8 :

According to the 2012 PwC survey noted above, the majority of companies that formerly reported a participation rate of 26%-50% now have a 0% to 25% rate.

According to the 2011 NASPP survey noted above, only 25% of respondents reported participation in excess of 50%, whereas 40% reported 20% or less. The 25% percentage increases to 34% for firms offering a 15% discount on the purchase price.

According to a 2009 survey of 412 companies by the NCEO and the CEPI, 43% reported a decline in participation in the prior 2 years. 9 According to the NCEO 10 : “Rates of participation vary widely, with median levels around 30% to 40% of eligible employees.”

Plan Changes

One indication of how valuable these plans are to companies is the changes in these plans that have made in recent years or are planned for the near future. Some are making plans more attractive to employees by, for example, increasing the discount on the purchase price and extending the period of time over which the stock is priced. This “look-back feature” feature allows participants to purchase shares at the lower of the stock price at the beginning or end of a period of time, which is typically 6 months.

Other companies are taking opposite actions, perhaps because of the trend toward performance-based compensation plans that are received more favorably by shareholders who must approve plans that require the issuance of company stock. 11 Another action that makes plans less attractive is taken to avoid expensing the stock sale to employees in company financial reports. This is done by meeting “safe-harbor” provisions in accounting rules that prohibit look-back periods of any length and cap discount rates on share prices at 5%. 12

According to the 2009 NCEO and CEPI noted above, 18% of respondents stated they had made changes to their plans in the prior 12 months. The two most common changes were reducing the length of the offering period (4.1%) and eliminating a look-back feature (3.5%).

According to the 2011 PwC Global Equity Incentives Survey of 147 multinational companies, 32% of plans qualified as safe harbor plans in 2011, up from 22% in 2007. In 2011, 70% had no look-back provision, up from about 55% in 2007. About 10% had a 6-month employee purchase period in 2011, down from about 20% in 2007. 13

According to the 2011 NAASP survey noted above, the percentage offering a 15% discount was 71%, down from 87% in 2004. Sixty-two percent offer a look back feature, down from 82% in 2004. Twenty percent offered a 12- or 24-month look-back period, down from 43% in 2004.

According to a 2012 Fidelity Investments survey of 422 stock plan decision makers, 51% stated they planned to change their ESPP in the next 3 years. Some were making the plans more attractive to employees—31% were either introducing a larger discount or adding a look-back period. Some were making their plans less attractive. Fourteen percent were lowering or eliminating the discount and 11% were either shortening or eliminating the look-back period. 14

In April 2013, it was reported that at least 100 companies have adopted an ESPP since January 2012, whereas another 175 have amended an existing plan, including a number of companies that have resumed offering discounts. 15 This report is difficult to place into context, but in one respect the numbers are not persuasive if the goal is to promote these plans. According to the U.S. Securities and Exchange Commission 16 and Blumberg LLP, 17 there are about 10,000 to 15,000 publicly traded U.S. companies, and according to NCEO estimates, 4,000 have ESPPs. That means that of the 6,000 to 11,000 firms without plans, about 100, or an estimated 0.9% to 1.7% have adopted a plan since January 2012, and an estimated 175, or 4.3%, out of 4,000 companies with an existing plan have amended it. In addition, we do not know how many plans were discontinued and amended to make them less favorable to employees over the same period.

Gaps in Information

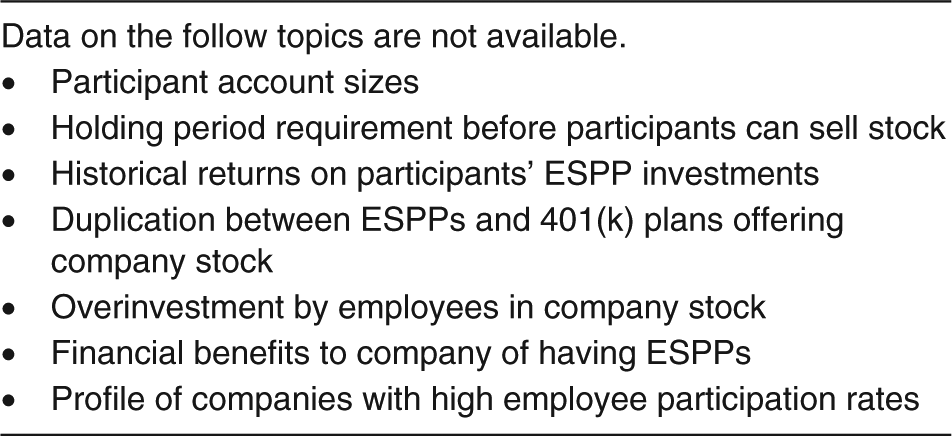

The general picture that emerges from these reports is that ESPP usage and participation are down from prior years. The recent good years in the stock market could change that picture, but many companies are also moving away from service-based equity plans in favor of rewards more aligned with company and employee performance. 18 As HR professionals monitor these forces and attempt to put these plans into perspective, they are hindered by the lack of important information about these plans as described in Figure 2.

Gaps in information about ESPPs.

Participant Accounts

Information on the size of employee ESPP accounts has not been made public by the organizations operating in this sphere. The NCEO indicates that most employees do not commit large sums to these plans. This fact and the fact that many employees do not enroll are the reasons why it believes that an ESPP is an ineffective means for creating an ownership culture. Yet, according to the above-cited 2011 NASPP survey, 93% of companies cite promoting a sense of employee ownership as the top reason for having one. 19

Holding Period

Experts tend to identify three plan features that drive employee participation—the discount on the purchase price, the look-back period for determining the price and the length of the period during which they can purchase the stock. For some reason, they do not consistently mention the holding period, which is the amount of time employees must hold the purchased shares before they can be sold. The first three factors determine the price a participant pays for the stock, whereas the holding period is crucial for determining whether a participant realizes an investment gain after making a purchase on favorable terms. Some plans have a quick sale provision, which provides for the automatic sale immediately following purchase.

Employees who view the plan as a stock-trading tool, rather than a long-term investment, will consider this factor closely. For example, an assured 15% gain on an investment over a 6- month period is an outstanding return that is enough to make ESPPs a valuable benefit for employees. Some employees may view a holding period as an unreasonable restriction, since their ESPP account has been funded by their contributions, not the company’s, as would be the case for stock options. Although they are said to be common, data on the number of plans having a rapid sale provision and the number of participants taking advantage of one could not be found.

Employee Return on Investment

Reports on the performance of employee investments in ESPPs, which would help HR leaders decide whether adopt a plan, are also hard to find. If employees are not experiencing a reasonable rate of return, and large numbers have discontinued participation because of it, a company might hesitate to offer such a plan. Participation in an ESPP is more than an expression of commitment to a company for many employees—it is an important investment of their hard-earned income. Fidelity research shows that many employees use ESPPs to save for retirement.

If that investment sours, important employee financial goals will not be met, which also could result in negative feelings toward the company. One research study showed that when a company offers company matching in a 401(k) plan, it is interpreted by employees as an endorsement of company stock as an investment. 20 The same dynamic could be operating in an ESPP with potential harmful consequences for employee relations.

Basis of Comparison

In describing the advantages of ESPPs, the tendency of some proponents is to compare them to other equity plans, such as a stock option plan, rather than a 401(k) plan. If the purpose of ESPP is to broaden the employee ownership base, then the basis of comparison for lower level employees who do not receive stock options is the 401(k) plan. Like 401(k) plans, ESPPs apply to all levels of employees, require an employee contribution to participate and provide benefits that are not based on employee performance. The ESPP stock purchase discount feature is also similar monetarily to the company match provided in a 401(k) plan.

Proponents need to compare ESPPs to 401(k) plans in a meaningful way to make a solid case why an employer would offer an ESPP instead of, or in addition to, a 401(k) plan that offers company stock as an investment option or as a company match. In addition, they need to explain why an employee would choose to invest in a plan that violates one of the cardinal rules of good investing—diversification—over one that offers it, a 401(k) plan. Some employees invest in ESPPs to meet their needs in retirement, apparently without having the protection of asset diversification. One study estimated that long-term investments in company stock sacrifice 42% of a stock’s market value, after accounting for the costs of inadequate diversification. 21

Some proponents cite the greater accessibility of funds with an ESPP as compared to a 401(k) plan and the lack of a 10% tax penalty for early withdrawals. In making the comparison, they fail to consider 401(k) plan features that are unavailable to ESPP participants, in addition to diversification, such as the ability to

withdraw their contributions without satisfying a holding period requirement;

take and repay tax free loans, generally within 5 years, that preserve accumulated savings and tax benefits at distribution;

move monies in and out of company stock to safer investments as market conditions change;

rollover assets without tax penalties to other tax deferred accounts on termination;

receive free investment advice from company approved sources and

enjoy participant safeguards under the Employee Retirement Income Security Act, which covers 401(k) plans but not ESPPs.

The question of whether to offer an ESPP, in addition to a 401(k), should receive a thorough analysis, for the decision to add an ESPP may represent a duplication of benefits.

Overinvestment in Company Stock

In 2006, Congress passed the Pension Protection Act, the most comprehensive reform of the nation’s pension laws since enactment of the Employee Retirement Income Security Act of 1974. One of the Act’s provisions addressed employees’ tendency to be overinvested in company stock in their 401(k) plan.

The Pension Protection Act gave participants the right to immediately diversify their own contributions out of employer stock at any time. And after completing 3 years of service, they have the right to diversify out of company stock provided through an employer’s matching or other contributions. 22 According to an Employee Benefit Research Institute study, 30 which uses the largest, most representative repository of information about individual 401(k) plan participant accounts, the share of 401(k) accounts invested in company stock was 8% in 2011. Since 1999, this percentage has fallen by more than 50%. 23

Despite the trend to reduce exposure, employees at some of the largest U.S. corporations have 70% of their 401(k) plan assets invested in company stock, according to Morningstar Investment Management. In 2012, employees in 184 plans had at least 20% of their assets invested in company stock. 24 Financial experts generally agree that no more than 10% to 20% of assets in a diversified portfolio should be in company stock. 25

According to finance professors and investment professionals, overinvestment in company stock is also a concern for our total wealth, which is made up of two parts—our financial capital and our human capital. The concern relates to employees that have human capital, the ability to earn a living, in addition to financial capital, invested in the same company, such as through an ESPP. This makes company stock a riskier investment for this group, since the health of both types of assets depends on the fortunes of their employer. 26

Discussions of the over-investment issue and the number of companies that have both an ESPP and a 401(k) offering company stock could not be located.

Financial Benefits to Company

The financial benefits to the company of having an ESPP are sometimes not clearly spelled out. Most commonly, companies issue additional shares of stock to fund an ESPP and experience a cash inflow when it is purchased by employees. As a result, ownership of the company is diluted, but it has no major effect on outward cash flow. HR professionals would benefit from knowing the relative costs of corporate borrowing versus issuing stock to raise capital.

In addition, there is no charge to earnings on the company’s income statement when the plan is positioned inside the safe harbor, otherwise there is. Finally, some companies use employees’ ESPP accumulated payroll deductions for general corporate purposes until the stock purchase is made for employees, whereas others pay interest to employees on these funds.

Without a full explanation of financial impact, HR professionals may get the impression that the sole benefit for adopting a plan is to attract and retain employees.

Success Profiles

Success stories of companies that are satisfied with their ESPP are easy to find, but a detailed general description of those with high participation rates is hard to find. Readers are told that the plans do better in technology companies than in financial and manufacturing companies, but the specific reasons why are not given.

Could it be that technology companies used an ESPP following an initial public offering (IPO) that drove an increase in the company’s stock value? Do employees of such firms have more disposable income to invest than those employed in other sectors? Is the workforce better educated and more comfortable with making stock market investments? Does Wall Street have a more favorable opinion of technology companies that bolsters the value of their stock? To what extent is favorable plan design the primary reason for the positive reaction of employees?

Without a clear picture of what makes these plans successful, the task of determining if an ESPP is right for their company is made more difficult for HR professionals.

Strong HR Interest Lacking

ESPPs are a somewhat “orphan” concept in HR management, primarily because they are limited in application to public traded, for profit organizations. This may be one reason why substantial involvement of major HR consulting firms, such as Hay, Hewitt, Towers Watson and Mercer, is lacking. They are usually key players that assist HR professionals by researching, promoting and defining the proper role for individual programs in a company’s HR strategy.

With no major HR consultants involved to provide guidance, HR professionals must perform a thorough job of evaluating all sources of information and ask the right questions before making decisions about adopting or enhancing these plans.

Specialists within HR do not appear to be jumping at the chance of championing these plans, as described below:

SHRM considers ESPPs a form of compensation. 27

WorldatWork, an association of primarily compensation professionals, considers them an employee benefit. 28

The Employee Benefit Research Institute, which is the largest association of benefits professionals, makes no mention of them in its “bible” on employee benefit programs, Fundamentals of Employee Benefit Programs. 30 A library database search of the association’s two periodicals, Benefits Magazine and Benefits Quarterly, shows that no articles have ever been published on the subject.

The lack of strong ownership increases the difficulty of finding a receptive audience in HR to whom to sell these programs.

Closing Thoughts

Interest and good news about ESPPs recently appeared, but HR professionals should react with caution. Plans are also being terminated and made less attractive to employees, and many companies have decided to pass on the idea. Important factors affecting plan design and strategy have not been reported and vetted. It is too soon to tell whether the recent surge in interest represents a sign of new life or is a temporary phase that will dissipate once the stock market declines and emphasis on performance based compensation grows.

Despite a host of potential negatives, there are at least two very good reasons to consider adopting an ESPP. One is that these plans can be designed to provide employees with an outstanding, assured 15% or greater return on investment, by combining a stock purchase discount with an immediate sale option. A second is that ESPPs are a logical means in start-ups for extending company ownership to employees that are ineligible for stock options. The bottom line for many decision makers is whether there are better ways of building goodwill with employees than by helping them be successful stock traders and shareholders, and whether scarce compensation dollars would be better spent on programs driven by employee performance. Situations such as these could be examined with less uncertainty if the information that is essential for putting ESPPs in clear perspective were available.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.