Abstract

In most sales organizations, salesforce performance evaluation has mostly relied on reflective metrics such as sales volume, revenue, and manager’s evaluations of salesforce, and hence they have limited insight into how a salesperson will do going forward and what types of training and incentives will be most effective. Sales organizations should emphasize sustaining and improving their salesforce performance by proactively reallocating investment in incentives and training resources. The main question is what type of incentives and training will bring out the best in a high performer or help a promising sales employee improve? Salesperson’s intrinsic value measurement and analysis provides directions for finding an answer. With this approach, sales organizations can then make strategic decisions about rewards and training optimization. These findings will help organizations reallocate their expenditure levels (i.e., training and incentive investments) to maximize salesperson’s intrinsic value, enhance salesperson’s future performance and ultimately boost revenue and profitability.

Keywords

Introduction

This research studies the impact of salesforce investment on training (directed toward improving the salesperson’s knowledge, skills and abilities [KSAs]) and reward (used to encourage the salesperson to perform better) on salesperson’s future performance. It is imperative that managers have the ability not only to measure a salesperson’s current performance but also to predict the salesperson’s performance in the future for better reallocation of incentives and training resources. In most organizations, sales employees are usually made up of mainly solid performers (60%), with smaller but roughly equal proportions of laggards and rainmakers (20% each). 1 Though most incentives and training programs approach these three groups as if they were the same, each group has different incentives and training needs. Salespeople can underperform because of a misalignment of their internal motivation with the type of training and incentives they receive.

Sales organizations should emphasize sustaining and improving their salesforce performance by proactively reallocating investment in incentives and training resources. It will not only help top performers shine but will also help drive laggards to the middle of the curve. The main question is what type of incentives and training will bring out the best in a high performer or help a promising sales employee improve? Salesperson’s intrinsic value (SIV) measurement and analysis provides directions for finding an answer. Intrinsic value is derived from a combination of monetary value (i.e., sales revenue and profitability) and relationship value (i.e., customer relationship and retention) of the salesforce and includes their short-term as well as long-term potential. SIV measurement enables organizations to investigate how organizational factors such as training and incentives can affect future sales performance of salespeople. With this approach, sales organization can then make strategic decisions about rewards and training optimization. These findings will help organizations reallocate their expenditure levels (i.e., training and incentive investments) to maximize SIV, enhance a salesperson’s future performance and ultimately boost revenue and profitability.

Training and Incentives: Major Drivers of Sales Performance

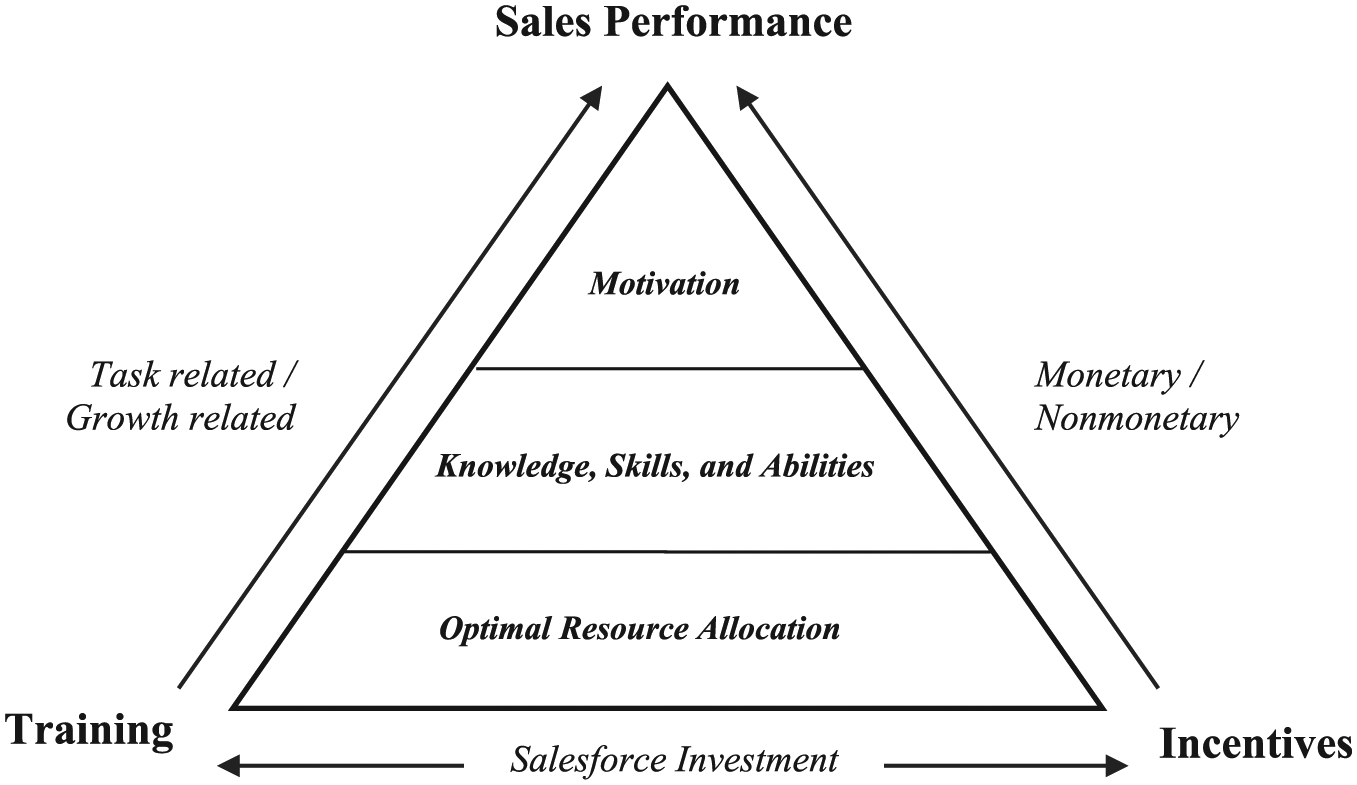

As training and incentives are major drivers of enhancing sales performance, sales organizations spend heavily on it to improve sales performance (Figure 1). Investment in sales training and incentives and its impacts on sales performance are explained below.

Salesforce investment in training and incentives: Enhancing performance.

Sales Training

Training can be defined as a planned program within the organization that endeavors to bring about relatively permanent changes in employee knowledge, skills and behavior. If one has “some level of talent,” then sales training can be instrumental in helping convert that talent into positive results. 2 Salespeople need “grooming” to succeed, and this grooming is an investment that is made by the organization in the form of training.3,4 Organizations spend millions of dollars on training employees, and sales training takes a significant portion of that budget. 5 Sales training involves a systematic attempt to understand, describe and transfer “good selling practices” to sales personnel and represents the largest portion of total training expenditures in the United States. 6 Research suggests that training may increase the salesperson’s knowledge base and skill level, resulting in higher performance. 7 Research found that following training, sales team morale and retention rates were boosted while securing new advertisers and revenues. 8

Training may improve sales performance (and also profits) by increasing productivity, improving morale, reducing turnover, improving customer relations and improving management of time and territory. 9 Effective sales training also enhances retention of sales employees. Many organizations, such as IBM, Hitachi Data Services and Wyeth Pharmaceuticals, have leveraged sales training to improve overall firm performance and establish strategic advantage by attracting and retaining best sales talent.10,11 High retention rate (96% in 1999) is believed to save the SAS Institute US$75million a year. 12

Skillful salespeople are particularly important for a sales organization to maintain its competitive edge in the face of intense market competition. 13 Sales organizations, therefore, must train their salespeople in the areas of product-specific knowledge, selling and negotiation skills, customer behavior, industry trends and market conditions. 14 Training also boosts profits by increasing revenue while lowering the firm’s selling and supervision costs. A study of Nabisco’s sales training program found a $122 increase in sales and a 20-fold increase in profit for every dollar invested in training. 15

Various Types of Training

The content of training for salespeople can be categorized into (1) product knowledge, (2) company knowledge, (3) market/industry awareness and (4) selling techniques and related topics. 9 The nature of a typical sales training program also varies depending on whether it is standardization (i.e., common to all salespeople), top-down (i.e., management decides), mandated (i.e., nonvoluntary), structured (i.e., formal and centralized) or in a class-room setting (by in-house or outside experts). 16 The American Society for Training and Development (ASTD; now Association for Talent Development [ATD]) divides the major sales training methodologies into two categories: self-study (i.e., readings, preworkshop assignments and programmed instruction) and workshops (i.e., lecture, discussion, on-the-job training, case study and role-plays). 17

Sales training is categorized into two categories: task related and growth related. A majority of training and development efforts undertaken by sales organizations are geared toward increasing the salesperson’s KSAs that are considered relevant for selling effectiveness. Task-related KSAs pertain to essential elements that a salesperson must possess to begin selling the company’s offerings. However, to function effectively in the current and future marketplace, sales organizations must take a more proactive approach toward sales training by moving beyond task-related KSAs and focusing more on a full range of salesperson competencies. 18 In this context, growth-related training focuses on developing leadership, team, customer engagement skills, negotiation strategies and adaptability.

Optimal Mix of Training

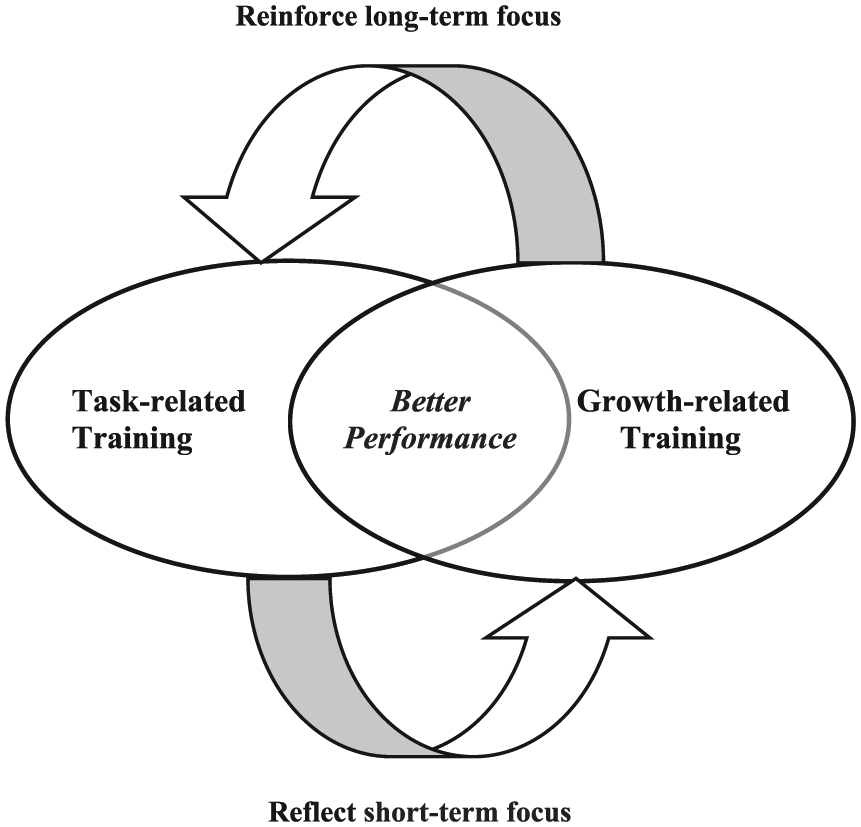

Training types such as task- and growth-related training are mutually reinforcing (Figure 2). Growth-related training focuses on adaptive and problem-solving skills, and hence can increase a salesperson’s performance in part by enhancing his or her ability to apply information and tactics developed in task-related training. The benefits of this synergy between the two types of training are greater in the long term than in the short term.

Task-related and growth-related training: Complementary relationship.

Sales practitioners have suggested sales training as a waste of resources unless it is made sustainable and hence advocate sustainability through proper mapping and performance management to keep the momentum up and the training alive. 18 With the proper mix of task- and growth-related training, organizations can help salespeople strike the best balance between short-term revenue (with new customer acquisition) and long-term retention (cross-selling and up-selling with existing customers; Figure 2).

Sales Incentives

Organizations are recognizing that paying above or at market levels is not sufficient to encourage, motivate and retain their salespeople. Accordingly, sales organizations use various rewards mechanisms and frequently reallocate and realign salespeople to motivate them to expend more effort and eventually perform better. 19 Changes in reward systems have long been known to affect employee motivation and performance. Nearly 80% of U.S. organizations make meaningful changes to their salesforce rewards programs every 2 years or less. 20

Various Types of Incentives

Rewards that employees receive for performing their jobs are intrinsic as well as extrinsic. Intrinsic rewards reflect employees’ psychological satisfaction resulting from performing their tasks, while extrinsic rewards are based on performance-based incentives. Extrinsic motivation is mainly divided into two components: compensation (financial rewards) seeking and recognition (nonfinancial rewards) seeking. 21 Financial (monetary) and nonfinancial (nonmonetary) rewards are not the opposite ends of a spectrum. Rather, they represent two distinct dimensions, and a salesperson can have both an incentive and a recognition orientation.

Sales employees may have great potential that can be reached only if they get the right motivational tools. For the recognition-seeking sales employees, sales managers may emphasize nonfinancial rewards because they will further enhance motivation. Similarly, compensation or incentives-driven sales employees’ performance may fall if a manager overemphasizes nonfinancial rewards and neglects financial rewards. The more employees feel dissatisfied with their financial rewards, the higher the risk that they leave the organization. 22 The size, scope and formality of nonfinancial recognition schemes vary immensely. Nonfinancial rewards are more likely to enhance interest and involvement in the job. 23

Optimal Mix of Incentives

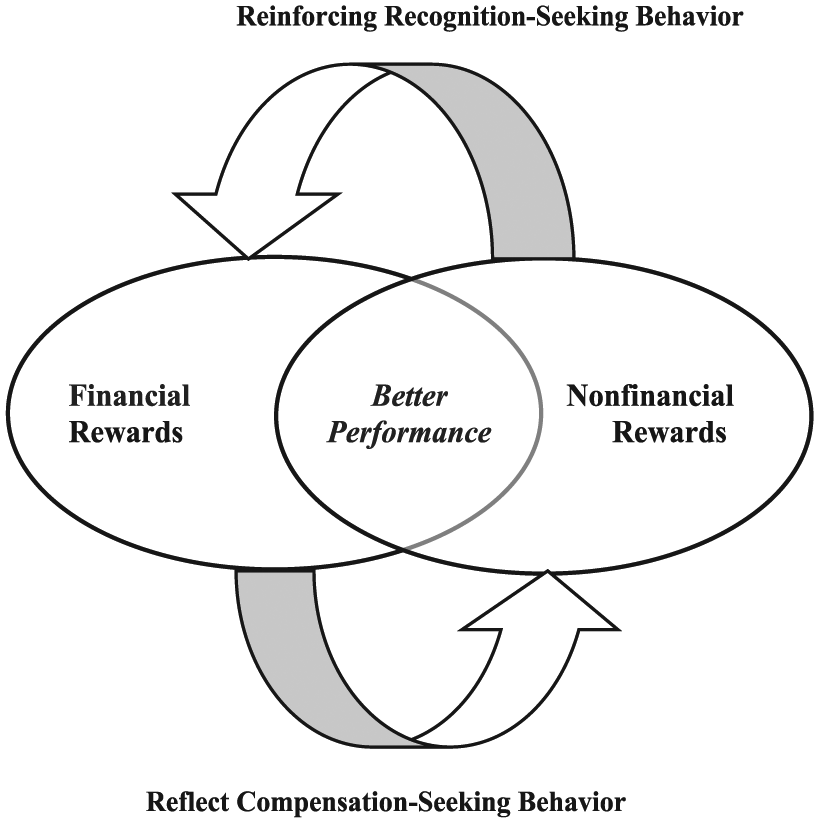

The optimal mix of financial and nonfinancial rewards encourages the salesperson to perform better (Figure 3). It is important to provide the appropriate financial rewards, but it is also necessary to complement these with other rewards types. 24 Employees’ personalities affect the attractiveness of a variety of rewards types. 25 Employment level can also affect employee preferences for certain rewards 26 as can personal characteristics such as age. 27 Organizations should pay attention to individual differences (e.g., age, tenure, educational background) in rewards preferences among employees. Individuals may favor different rewards/incentives according to their needs, education, social status and circumstances. 28 Employees’ behavior and attitudes are affected by their satisfaction with both financial and nonfinancial rewards. 29 Findings show that employees’ initial motivation and satisfaction may have improved with a pay raise or cash bonus, but the effects were shorter lived than the motivating effects of nonfinancial rewards. 30

Optimal mix of financial and nonfinancial rewards: Enhancing sales performance.

Need for Salesforce Investment Management: Higher Incentives and Training Costs

In view of escalating budget for sales incentives and training, it is important for sales organizations to optimally allocate these resources to enhance sales performance and retain their best salespeople. According to a Center for American Progress report, the cost for replacing an employee is roughly 21.4% of his or her annual salary. 31 Hence, retention of an employee is very important for organizations from the cost perspective. If the best salespeople are not retained, a firm can be negatively affected from the operational level to the strategic level.32,33 As explained below, sales incentives and training are major expenditure for sales organizations.

Higher Costs of Sales Incentives

Salespeople can underperform because of a misalignment of their extrinsic motivation with the type of rewards they receive. 34 Therefore, reward should be customized to carefully match employees’ characteristics, situations and preferences, which are often idiosyncratic to each salesperson. WorldatWork reported that effectively implemented nonfinancial rewards programs can achieve a return on investment (ROI) three times higher than cash incentive programs. 35 From a cost perspective, managing the salesforce is an expensive proposition in itself as the U.S. economy spends $800 billion on salesforce every year, which is approximately three times the average advertising spend in the same period. 36

Higher Costs of Sales Training

Training expenses have risen steadily over the years as it includes many cost components such as cost of instructional materials, living and transportation expenses, instructional staff, outside courses and seminars, management time spent with the salesperson and the opportunity cost of lost sales. Businesses spend a massive amount on salesforce training. The ATD estimated that U.S. businesses spent $15 billion every year on sales training, which amounts to approximately $2,000 per salesperson. 37 According to the ATD 2016 State of the Industry report, employees averaged 33.5 hours of training in 2015, while organizations spent an average of $1,252 per employee on training and development initiatives. 38 The cost of recruiting, training and managing a sales trainee, combined with the opportunity costs of lost sales from an unmanned territory, was estimated to be as high as $75,000. 39 A prior study found that firms spend between $22,500 and $28,455 on an average to train a salesperson, 40 while in the technical markets, this training cost can be as high as $100,000.41,42

Salesperson’s Performance Evaluation: Traditional Versus Forward-Looking Metrics

Owing to the significant investments made in the salesforce in terms of incentives and training, it is important to study the impact of such an investment on a salesperson’s performance. Most sales organizations rely on backward-looking methods (often referred to as predictive analytic) to gauge the impact of huge spending on training and incentives. Traditionally, salesforce performance evaluation has mostly relied on reflective metrics such as sales volume, revenue and manager’s evaluations of the salesforce. Accordingly, the performance of salespeople can be divided into four categories: stars, stable, learners and laggards.

In most sales organizations, star salespeople outperform their peers because they are highly motivated, know the products and customers well and know how to forge a long-term relationship with prospects and customers, and hence they have a high customer retention rate. There is need to retain such star salespeople because they are crucial in gaining competitive intelligence in the marketplace and also act as the custodians of the firm’s relationship with the customer.43,44 However, no salesforce consists entirely of stars. Typically, salesforce classification (i.e., stars, stable, learners and laggards) is based on their reported performance, but it does not provide any clues on sustenance of their performance.

Because firms measure only past sales performance by using traditional metrics, they have limited insight into how a salesperson will do going forward and what types of training and incentives will be most effective. 45 Also, a salesperson’s performance evaluation based solely on sales ranking is not effective because there are difficulties associated with measuring differences across salespeople, markets and product categories. 46 To resolve this, one approach might be to benchmark sales efforts against the competition, 47 but most organizations cannot gather accurate information about competitors’ efforts or account for the unique circumstances of their operations. A better solution therefore is to implement internal benchmarking, which identifies performance standards and areas for potential growth by comparing the firm’s own salespeople with one another. 48 There are many advantages in applying internal benchmarking: It draws from available observable data, sets more realistic goals and allows for the transfer of best practices. 49

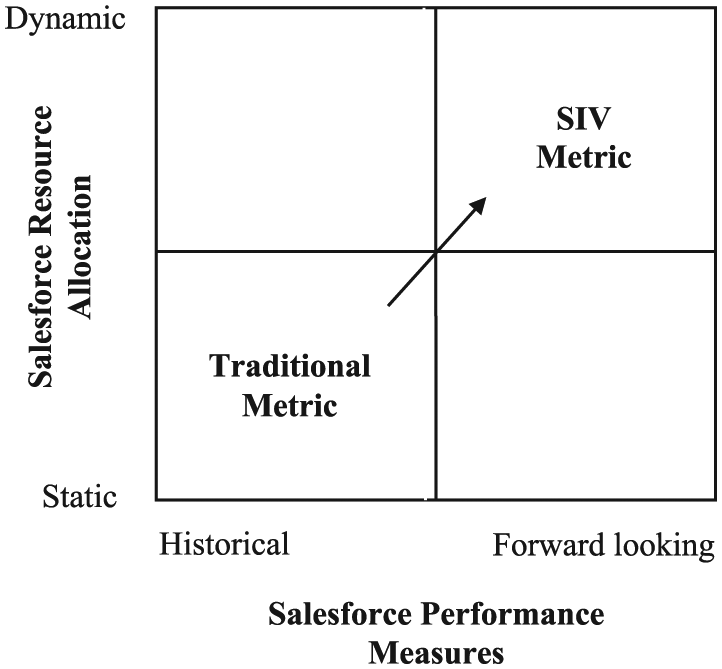

Hence, for such internal benchmarking, there is need for a metric for predicting the overall value of salespeople to aid in effectively managing (acquiring, developing, allocating, evaluating and rewarding) and retaining these crucial organizational assets. Sales managers are often faced with decisions regarding which salespeople to retain and which to let go. In such situations, they typically use traditional metric based on reflective measures of salesforce performance evaluation and ranking (Figure 4).

Salesforce performance evaluation metrics: Traditional versus forward looking.

However, in some cases, reflective measures could prove myopic and expensive for the sales organizations because significant training and reward investments have already been made toward developing the salesperson. Given the dynamic and extremely competitive nature of the marketplace, one-size-fits-all approach to salesforce ranking and evaluation may be suboptimal. Hence, sales organizations must adapt to the ever-changing marketplace to identify a better approach for salesforce performance evaluation. By looking not just at the end results sales employees have generated but also at their future sustainability, sales organizations may find that top performers are more valuable than originally thought and low performers even more costly. This research provides a forward-looking SIV metric for internal benchmarking of sales employees by measuring intrinsic value of salespeople by predicting their short-term as well as long-term potential and hence analyzing sustainability of their performance (Figure 4).

Salesperson’s Performance Evaluation in Dynamic Environment: Developing SIV Metric

As salespeople are a critical resource in organizations, effective utilization of this resource should be a central management focus. Traditionally, salesforce performance evaluation metrics used by organizations can be categorized into (1) evaluations by knowledgeable others (e.g., peer evaluations, manager evaluations), (2) self-evaluations and (3) quantitative measures. 50 Evaluations by knowledgeable others and self-evaluation metrics tend to suffer from respondent subjectivity biases. However, quantitative measures are objective measures of performance but tend to reward salespeople’s past behavior while ignoring future performance potential.

To account for a dynamic market environment, sales organizations need to adopt a model-based approach in evaluating the salesperson’s performance. An important criterion that must be satisfied in a model-based approach is that the salesperson evaluation metric must be built up from customer-level profitability measures (e.g., customer lifetime value [CLV]). It is to be noted that all estimation models have limitations, such as difficulties in determining changes in the environment, new costs, market conditions, marketing efforts, seasonality, legal changes and so forth. However, these difficulties are small in comparison with the great benefits that can be obtained from applying such models.51,52

There is much interest for sales organizations to understand how their actions affect the long-term performance of their salespeople. During the lifetime of a salesperson, different incentives and trainings costs are incurred. 53 A salesperson may have great potential that can be reached only if he or she gets the right tools. For example, an incentive-driven salesperson’s performance may fall off if his or her manager overemphasizes training and underuses monetary and other rewards. Likewise, a training-driven salesperson may be losing his or her edge because the management focuses more on rewards or provides too much task-related and not enough growth-related training. Therefore, the establishment of a salesforce performance metric based on salesforce resource investment (i.e., incentives and training) is imperative.

In this context, there are two human resource accounting methods available for valuation of human resource in the organizations: those using a cost approach and those using a value approach. 54 The difference is based on whether an employee is viewed in terms of costs-to-date or in terms of expected contributions. Cost approaches focus on historical costs incurred to hire, train and maintain employees or on replacement costs that would be incurred if an employee were to be replaced. Value approaches consider present value of the employee’s stream of net future contributions to the firm. 55 A better understanding of the value of the salesperson should lead to better allocation of salesforce resources (i.e., training and incentives) and effective management of salespeople. The less valuable salespeople must be identified and motivated to achieve a higher level of value or be moved out of their organization.56-59 Thus, a better understanding of the value of the salesperson may lead to changes in the way these salespeople are managed.

Determining the intrinsic value of an individual salesperson is important for determining the most valuable salespeople as well as for determining the less valuable ones. The importance of having a suitable metric for salesperson evaluation is further evident when managing salesforce turnover, which is considered a major pain point for sales organizations. 60 As churning salespeople could take valuable customers with them, it is therefore extremely important for the sales organization to know which salespeople are more valuable (in terms of intrinsic values), whom to focus on retaining and whom to let go.

To calculate SIV, managers need to estimate the CLV of the salesperson’s existing and prospective customers. The use of CLV to measure the future cash flows for each salesperson ensures that the SIV metric is customer-centric as well as forward looking. SIV metric developed in this research use the value approach to evaluate and demonstrate the effects of salesforce investment on training and incentive on intrinsic value of salespeople. As a value-based performance evaluation metric, SIV enables sales organizations to concentrate their resources on retaining sales employees who have high intrinsic value or properly training and incentivizing existing low-performing sales employees to increase their sales performance.

SIV metric values the salesperson on the basis of the overall (short term and long term) future performance potential and hence encourages managers to focus not only on the short-term outcome but also on the long-term performance potential. If such intrinsic valuation is not done, then the management runs the risk of making salesforce investment decisions that may improve profits in the short run, but may also have negative effect in the long term.

SIV Metric: Calculation Methodology

SIV is determined by calculating the net present value (NPV) of future cash flows from a salesperson’s customers measured in terms of CLV after accounting for the costs of the salesperson (i.e., cost of developing, motivating and retaining salesperson). CLV by definition considers all costs incurred to attract and retain a customer, including the costs of the salesforce (e.g., interest creation, meetings, delivery and support). SIV is influenced by CLV, which in turn depends on the salesforce in the form of sales activity and sales efforts. A salesperson’s selling efforts influence customer behavior (e.g., customer acquisition, customer retention and customer expansion in the form of cross-selling/up-selling), which in turn affects customers’ CLV. 61

Salespeople affect CLV by generating sales from maintaining and enhancing existing customer relationships (i.e., farming activities or customer retention) and/or prospecting for new customers (i.e., hunting activities or customer acquisition). Furthermore, customer acquisition activities are generally evaluated in terms of “wins” such as how many new accounts salespeople acquire, whereas retention activities in terms of “losses,” such as how many existing customers defect. Each of these activities is critical for firm success in business to-business (B2B) markets. 62 Customer acquisition activities involve securing initial orders from new customers, including prospecting, generating leads, precall planning and delivering sales presentations. Customer retention activities entails selling to existing customers, such as building long-term relationships, creating efficiencies in order taking and increasing share of wallet through cross-selling and up-selling efforts.63,64

By measuring the value of the salespeople using the SIV metric and linking the sales performance with the types of training and incentives each salesperson receives, it is possible to identify various categories of salespeople in terms of performance and reallocate the training and incentives to maximize their performance. SIV for various sales employees is computed as the profits from the customers managed by the salesperson minus the optional training costs and any incentives paid discounted to present value.

In the above formula, SIVs measures intrinsic value of salesperson “S.” The NPV of future contribution margin (CM) associated with salesperson “S” is measured in terms of the total CLV from his or her existing customers as well as expected value from new customers. The second term in the SIV metric accounts for the cost that the sales organization incurs on the salesperson and includes the NPV cost of training and incentivizing the salesperson. The effect of task- and growth-related training, though positive, diminishes as the training hours increase because the cost structure of training begins to dominate the SIV. Thus, an overtrained salesperson leads to a higher cost structure and lower SIV than does an optimally trained one.

Deployment of Salespeople Valuation Model: Various Case Studies

Case Study 1

This case study refers to a company established in Bogota, Colombia. Its core business is to provide security products and services such as alarms, closed circuit television, remote monitoring and access control systems to small- and medium-size enterprises in the Colombian market. For this study, data were collected for a year’s period from the beginning of 2014 to the end of 2014 for nine salespeople. The data include aspects of revenues and costs, peer effect and retention rates. The company had not previously calculated the value of their salespeople and thus ranked salespeople according to revenue generated. Thus, with the salesperson valuation model, the company was receiving new information as now all salespeople were ranked according to their valuation. As training impact is variable across salespeople, such a valuation model allows practitioners to control the training and evaluate the individual’s pace of implementation. This model enabled the company to analyze salesforce investment decisions and also the financial impact of improvement efforts. The valuation model suggested that the bulk of a company’s salespeople have lower valuation when measured as percentage of a firm’s salesforce equity (SE). The SE is the sum of the lifetime value of all salespeople. The bulk of a firm’s salespeople, that is, 77.7% (7/9), have low salesperson lifetime value (SLV) and produce approximately 36.6% of the firm’s SE. In contrast, the high SLV category, though only 22.2% (2/9) of a firm’s salespeople, produces approximately 63.4% of the firm’s SE.

This model also enabled the financial impact of improvement efforts to be analyzed. With the predictive model, the firm was able to establish a relationship between training cost and sales performance and ultimately ROI. The firm found that investment of US$1,000 per salesperson training will improve sales performance. If it is assumed that the revenues increase by 2.5%, the model indicates that SE will improve by US$26,227 (12.9%), resulting in an ROI of 191.4%, which indicates that the program has the potential to be a large success. With the valuation model available for salespeople, it was possible to review the existing incentive and training plan. If the incentive and training “intervention” costs are higher than the expected return, in consideration of the termination costs, it suggests that the salesperson needs to be terminated when it is no longer appropriate to invest in sales employees. 65

Case Study 2

A Fortune 500 B2B software, hardware and services company had been using reflective metric such as revenue generated for valuing its salespeople, and accordingly salespeople who brought in the most sales were considered “stars.” The main objective of the B2B company was to identify the impact and effectiveness of training and incentive plan on the future performance of salespeople. The company developed a salesforce valuation model for evaluation and management of salespeople. The sample size for the study was 484. Data were collected from three sources: (1) transactional data from the customer, (2) reported data from the salesperson and (3) organizational factors (training and incentive data) over a period of 7 years (i.e., 2004-2010). Data were collected by company visit and field study. Tenure of the salesperson, territorial/geographical differences among salespeople, market size and competition were used as control variables.

The company found strong associations between training, incentives and a salesperson’s future performance. On the basis of those findings, the company was able to segment the salespeople into two broad categories: training-driven and incentive-driven salespeople. For the company under study, optimal hours of training to maximize salesperson’s future value (SFV) for incentive-driven and training-driven salespeople were found to be 17 hours and 29 hours, respectively. The optimal annual amount of training for salespeople in the training-driven segment is 70% more than what is best for incentive-driven salespeople. The impact of $1,000 increase in incentives on SFV after 1 year for incentive-driven and training-driven salespeople was found to be $1,876 and $1,371, respectively.

Monetary incentives were calculated as the average annualized commission payments beyond the base salary. The company used peer recognitions such as awards and commendations as a nonmonetary incentive to motivate the salesforce. Peer recognitions (proxy for nonmonetary incentives) as the annualized average number of times the salesperson was recognized within the firm through e-mail, newsletters, commendations and awards. The monetary and nonmonetary rewards have a greater impact on SFV when combined. The company used the salesforce valuation model to prioritize investment in high future value (i.e., high SFV) salespeople while reducing those investments in low future value (i.e., low SFV) salespeople. This valuation approach allowed the firm to reallocate salesforce resource, that is, incentives and training investment across salespeople, resulting in an 8% increase in SFV and 4% increase in sales revenue. 34

Determining Salesperson’s Intrinsic Value: Calculation Methodology

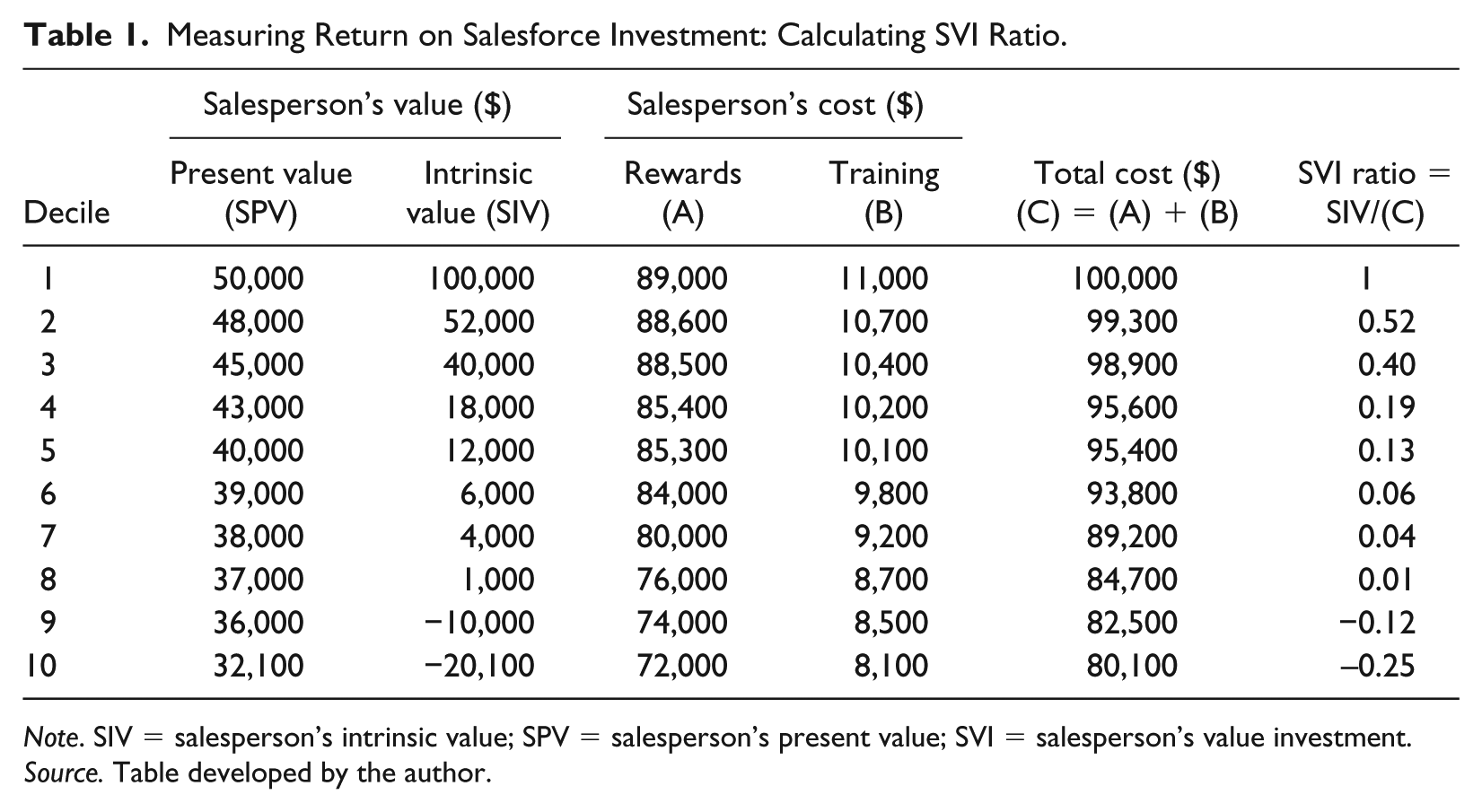

In this hypothetical illustration of a sales organization that segments salespeople into deciles, based on past performance, use SIV approach for ranking of salespeople. After the sales organization determined the salesperson’s present value (SPV) across various groups, it has correlated the current sales performance with the prior rewards and training in each segment to develop a holistic picture of how such rewards and training investment influences performance of sales employees. In this exercise, tenure, market competitiveness and sales territory are used as control variables. Next, SIV and SVI (salesperson’s value investment) ratio for the sales employee in each decile are calculated. SVI ratio is the ratio of SIV and the cost of salesforce investment (i.e., costs of rewarding and training the salesperson). However, measuring, managing and maximizing SIV is not an easy task. It requires that, in salesforce resource allocation decisions, both the benefits and the costs are considered. Table 1 shows SPV, SIV and SVI ratio for all segments of salespeople.

Measuring Return on Salesforce Investment: Calculating SVI Ratio.

Note. SIV = salesperson’s intrinsic value; SPV = salesperson’s present value; SVI = salesperson’s value investment.

Source. Table developed by the author.

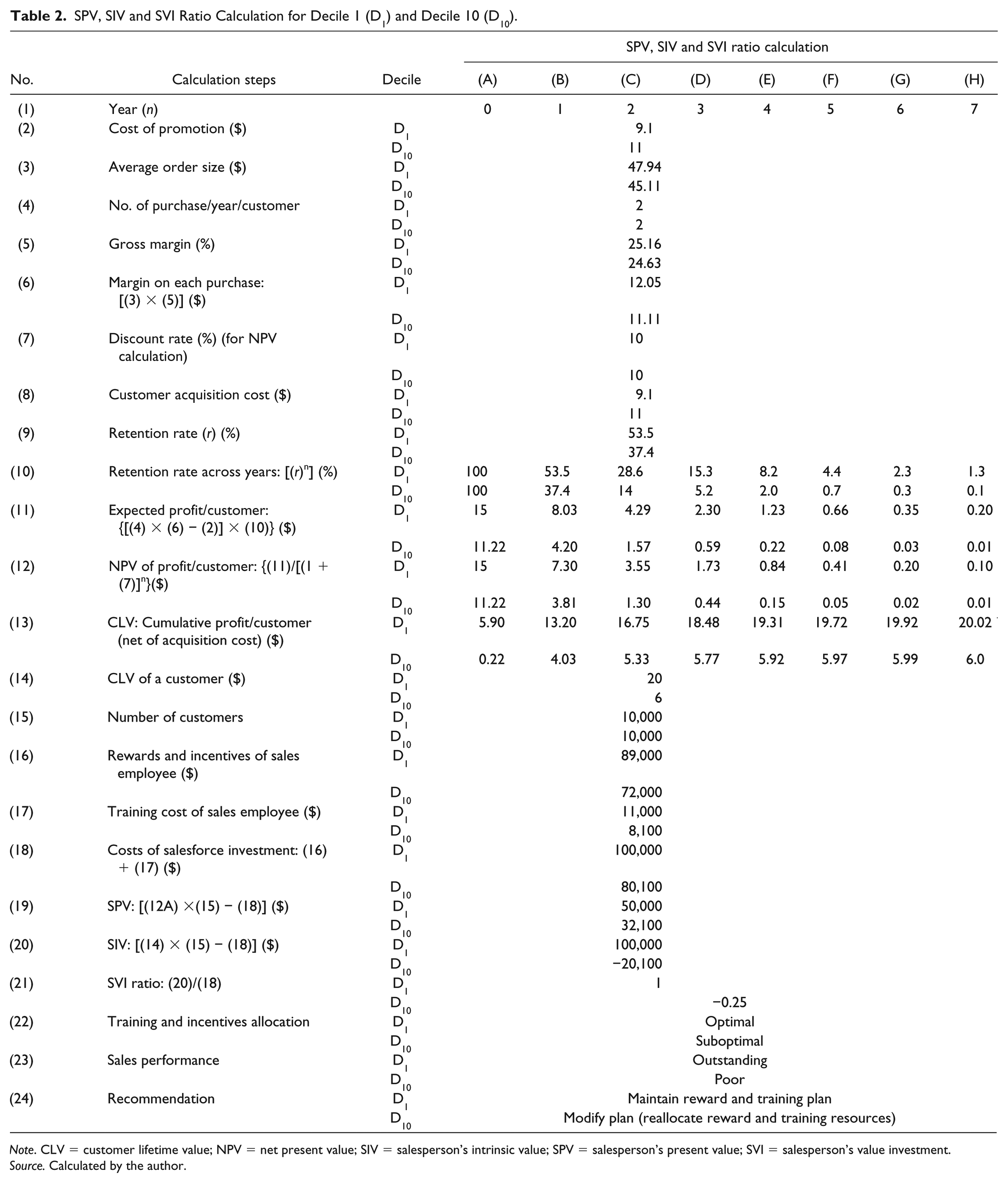

SPV, SIV and SVI ratio calculation methodology for Decile 1 and Decile 10 is given in Table 2. Higher value of SVI ratio is preferred because it reflects more profit potential. For salespeople in Decile 1, SVI ratio is high (i.e., 1 compared with −0.25 for Decile 10). SVI ratio identifies the amount of value created by salesperson per unit of investment.

SPV, SIV and SVI Ratio Calculation for Decile 1 (D1) and Decile 10 (D10).

Note. CLV = customer lifetime value; NPV = net present value; SIV = salesperson’s intrinsic value; SPV = salesperson’s present value; SVI = salesperson’s value investment.

Source. Calculated by the author.

According to Table 2, SPV for Decile 1 and Decile 10 is $50,000 and $32,100, respectively. However, calculations show that SIV for Decile 1 and Decile 10 is $100,000 and $−20,100, respectively. Similarly, SVI ratio for Decile 1 and Decile 10 is 1 and −0.25, respectively. Sales organizations with appropriate reallocation of rewards and training mix may increase performance of salespeople in lower deciles, particularly those with negative SIV and SVI ratio.

Managerial Implications and Limitations

There is increased recognition and acceptance of customer relationship management (CRM)–based valuation methods in management practices 66 as CRM recognizes that although acquiring customers is important, maintaining customer relationships—and ongoing revenue streams—is even more critical for profitability.67,68 This research focus for developing SIV metric has several potential implications for sales managers who use CRM systems to proactively manage the customers as well as the salesforce. Advanced CRM systems that already implement the CLV metric could easily adopt the SIV metric because of the inherent dependence between the SIV and the CLV metrics. Analogous to customer acquisition using a CLV-based approach, SIV metric allows sales organization to profile the “top” SIV candidate using internal benchmarking of sales employees.

Sales managers play a vital role in the development of the salesperson. 69 As such in the case of an underperforming salesperson, the manager can use the SIV metric to reallocate salesforce investment in training and incentives for enhancing the salesperson’s performance. Using the SIV metric, sales organizations can identify which salesperson in their salesforce is likely to be the most valuable as well as profitable in the future. The results presented in this study can also help in salesperson hiring/selection decision, salesperson career development and managing salesperson churn.

SIV is a predictive analytic that forecasts intrinsic value of salespeople and tends to recognize building and sustaining customer relationships as assets and reposition customer focus from short-term profits to a long-term relationship value. Such futuristic analysis provides the starting point for finding an answer to the effective salesforce resource allocation questions:

How should the future potential of the salesperson be measured?

What are the drivers of a salesperson’s future performance, and what is their impact?

Is there significant heterogeneity within the salesforce that affects intrinsic value?

What type of rewards and training will bring out the best in a high achiever or help a promising sales employee improve?

However, there are also certain limitations of SIV metric as explained below:

SIV metric is based on CLV and hence under certain circumstances its measurement becomes more complex. This calculation approach requires proper allocation of the costs of the salesperson for each customer, which will not be easy especially in companies with a salesforce structure organized by product, or when two or more salespeople interact with the same client. Similarly, CLV also varies in the situation of changing customers among salespeople, as a result of different customer–salesperson relationships. 70

SIV metric links organizational factors (e.g., training and incentives) to an SIV but do not investigate the role of the salesperson’s cognitive and attitudinal elements (e.g., motivation, ability/aptitude) that could mediate the effect between organizational variables and SIV. Future research could study the mediating variables and adopt a dynamic model to describe the time-varying effects of the parameters in a more “continuous” sense, thereby building on this research stream.

SIV metric does not explicitly account for dynamics in the parameter estimates. Research could develop a structural model to dynamically exploit these parameters in salesperson’s future valuation and SIV estimation.

Conclusion

SIV metric provides decision frameworks to sales organizations for determining salesforce resource allocation. Reallocating and optimizing a salesperson’s training and incentive resources according to the SIV metric can improve sales performance. By implementing the SIV metric, sales organizations can not only identify a better salesperson but also realize why a salesperson’s profit potential (i.e., intrinsic value) is plateauing/decreasing while another salesperson’s intrinsic value is high.

Research also emphasizes that all sales employees do not perceive organizational rewards and training alike because for some groups certain needs can be more prominent than others. A combination of incentives and training needs had the biggest impact on salespeople’s intrinsic value. Reallocation of incentives and training resources based on SIV metric not only reduces sales employee turnover but also enhances performance of retained employees because it takes into consideration the needs of the sales employees and the requirements of the organization. Building an SIV model allows an organization to develop its salesforce as a distinctive competency that is extremely difficult for others to imitate and can, therefore, create a significant competitive advantage.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.