Abstract

Pay transparency has drawn substantial attention from scholars in recent years, resulting in an expanding body of knowledge on this important topic. However, the literature has developed in a fragmented manner with an array of labels and conceptualizations across several largely disconnected dimensions. Pay transparency measurement scales have also emerged in a piecemeal fashion and lack cohesion in the operationalization of pay transparency dimensions. The current research develops a more cohesive and comprehensive multi-dimensional pay transparency framework and measurement scale. The paper reviews and integrates the pay transparency literature into a coherent, multi-dimensional framework founded on employee awareness perceptions of pay information rather than on objective organizational actions or employee behaviors. Following established scale development techniques, the present study creates and validates a multi-dimensional pay information awareness scale that may serve to facilitate future research on pay transparency. Implications are discussed, along with limitations and directions for future research.

Pay transparency increasingly has captured the interest of scholarly researchers and organizational practitioners alike (Avdul et al., 2024; Brown et al., 2022; McMullen & Dahle, 2024; Trotter et al., 2017). Indeed, there is a global trend toward mandating pay transparency practices, with at least 14 US states and municipalities enacting such laws since 2020 (PayAnalytics, 2023), and pay transparency policies are frequently touted as a potential remedy for a variety of issues including pay inequality and the gender wage gap (Baker et al., 2023; Obloj & Zenger, 2022). Pay transparency has typically been subdivided into three distinct dimensions including outcome pay transparency, which involves the organization sharing information regarding actual or aggregate pay amounts, process pay transparency, which entails the organization sharing information about how pay is allocated, and communication pay transparency, which occurs when employees share pay information with one another (Bamberger & Alterman, 2024). More recently, an additional dimension has begun to emerge, archival pay transparency, which involves employees obtaining widely available pay information from various websites such as Salary.com, PayScale, and Glassdoor (Brown et al., 2023). Pay transparency has been linked to a range of outcomes including societal level gender pay equity, organizational level profitability and innovation, and individual level performance, justice perceptions, satisfaction, commitment, and turnover (Brown et al., 2022).

However, this growing body of literature is currently limited by several concerning issues. First, the research stream has largely developed in a fragmented and piecemeal fashion that lacks cohesion and clarity (Bamberger, 2023). For instance, an array of terms including pay openness, pay secrecy, and pay information disclosure has been used synonymously with pay transparency in the literature (Brown et al., 2022). Moreover, some empirical studies focus solely on outcome pay transparency, others only on process pay transparency, while still others focus on pay transparency in general without specifying the type (Brown et al., 2022; Trotter et al., 2017). Rarely, if ever, have the various types of pay transparency been explored using a comprehensive and interconnected approach. Second, existing measures of pay transparency have also developed in a disconnected fashion. There is currently no overarching measurement scale developed specifically to assess the various dimensions of pay transparency. Rather, separate scales for pay transparency dimensions have been created, usually for use in a specific empirical study by the researchers (e.g., Day, 2012; Hartmann & Slapničar, 2012; Smit & Montag-Smit, 2018, 2019). Third, current conceptualizations and measures of pay transparency lack a consistent operationalization of pay transparency dimensions. Specifically, the measures of outcome pay transparency and process pay transparency (e.g., Day, 2012; Smit & Montag-Smit, 2019) refer to actions of the employer, whereas measures of communication pay transparency and archival pay transparency (Brown et al., 2023; Smit & Montag-Smit, 2018, 2019) refer to actions of the employee. These limitations and inconsistencies pose serious problems for scholars seeking to formulate and test hypothesized models to advance pay transparency research and for practitioners attempting to understand the impact of various types of pay information on their employees as they make decisions about when and how to disclose pay information.

The purpose of the current paper is to conceptualize and define a more cohesive and comprehensive multi-dimensional pay transparency framework and to develop an accompanying measurement instrument. First, we provide a critical review of the pay transparency literature. Then we synthesize this extensive, if somewhat disjointed, body of knowledge into a unified coherent, yet multi-dimensional framework based on employee awareness of pay information rather than on the organization’s objective policies and actions or the employee’s behaviors in sharing or accessing pay information. As Lewin et al. (1936) insightfully noted, behavior is based not upon objective reality, but upon individual perceptions of reality. Consequently, we argue that employee pay information awareness is the most appropriate lens for understanding and measuring pay transparency rather than objective organizational policies or employee actions. Finally, using the resulting conceptual pay transparency framework, we follow established comprehensive scale development techniques (e.g., Hinkin, 1998) to create and validate a multi-dimensional pay information awareness scale that may serve to facilitate future research on pay transparency and individual outcomes.

Literature Review

Pay Transparency

Pay Transparency Dimensions.

Outcome Pay Transparency

Outcome pay transparency refers to the organization’s sharing of pay outcome information with employees (Bamberger & Alterman, 2024). In the literature, this dimension of pay transparency is also variously labeled as “pay outcome transparency” (Arnold et al., 2018), “pay disclosure” (Brown et al., 2022), “pay communication” (Day, 2012), “distributive pay transparency” (Montag-Smit et al., 2023), and sometimes simply as “pay transparency” (e.g., Hartmann & Slapničar, 2012; Schnaufer et al., 2022). Pay outcome transparency can be further divided into two subdimensions: actual outcome pay transparency, which provides specific amounts of individual pay, and aggregate outcome pay transparency, which provides aggregated salary ranges for certain jobs (Bamberger, 2023). There has been much debate in research and popular media around outcome pay transparency and whether organizations should disclose actual and/or aggregate pay information (Bamberger, 2023; Scott et al., 2020). Research suggests that greater outcome pay transparency may be essential in resolving gender, racial, and ethnic pay inequities (Trotter et al., 2017), and that when pay is perceived as unfair, outcome pay transparency may negatively affect pay satisfaction (Scheller & Harrison, 2018) while increasing turnover intentions (Schnaufer et al., 2022). Unfortunately, research also suggests that, despite narrowing wage gaps, workers may pay the price for outcome pay transparency in the form of pay compression or an overall decrease in average compensation as employers seek to level performance-based pay (Lam et al., 2022; Obloj & Zenger, 2022).

Process Pay Transparency

Process pay transparency refers to the sharing of information regarding how pay is decided and distributed in the organization (Arnold et al., 2018; Wong et al., 2023). Scholars also refer to this dimension of pay transparency as “pay process transparency” (Bamberger & Alterman, 2024), “pay procedure transparency” (Arnold & Fulmer, 2018), and “procedural pay transparency” (Arnold et al., 2024). Voluntary process pay transparency is much more common in organizations than voluntary outcome pay transparency (Arnold et al., 2018), likely because there are few if any significant downsides involved when employers openly explain the process by which pay decisions are made (Bamberger, 2021). Better still, there seem to be abundant upsides to ensuring employees are aware of the process by which their pay is determined. Research examining process pay transparency as a distinct dimension reveals that it is positively associated with pay satisfaction (Folger & Konovsky, 1989), productive workplace behaviors (SimanTov-Nachlieli & Bamberger, 2021), organizational commitment (Day, 2012), employee trust in their employer (Montag-Smit & Smit, 2021Montag‐Smit & Smit, 2021), constructive employee social interaction (Arnold et al., 2018), pay satisfaction (Day, 2012), motivational climate (Tenhiälä et al., 2024), and organization performance (Arnold et al., 2018).

Communication Pay Transparency

Outcome and process pay transparency denote the extent to which organizations share information with their employees. In contrast, communication pay transparency concerns the extent to which organizations allow employees to share pay-related information with each other (Arnold & Fulmer, 2018; Bamberger, 2021, 2023; Wong et al., 2023). This dimension is most often labeled communication pay transparency but is also referred to as “communication openness transparency” (Alterman et al., 2021), “employer pay communication restrictiveness” (Brown et al., 2023), and simply “pay transparency policy” (Cragun et al., 2021). While some organizations may attempt to limit employee pay information sharing (Arnold et al., 2018), the amount of control employers realistically have over employee pay communications is questionable. Smit and Montag-Smit (2019) show that employees exhibit distinct preferences for the extent of pay-related information they are willing to share independent of the organization’s pay communication transparency level. Additionally, laws and regulations in the US, Canada, Australia, and the EU prohibit employers from restricting employee pay communication.

Archival Pay Transparency

Archival pay information is an emerging source of pay information that we propose is another distinct dimension of pay transparency. Archival pay information is shared worldwide via platforms such as Salary.com, Payscale.com, Indeed.com, and others. These platforms broadly collect and share pay information with users by job title and geography, incorporating compensable factors such as education, professional certification, and years of experience. Smit and Montag-Smit (2019) explored the behavior associated with seeking archival pay information, while Brown et al. (2022) assert that, when outcome pay transparency within the organization is lacking, employees will look for pay-related information from archival pay sources. Archival pay transparency—the extent to which people are aware of pay information from archival sources—is conceptualized as a unique and distinct dimension, as shown in Table 1, because pay information is gained indirectly from sources outside the organization, whereas outcome, process, and communication pay transparency refer to information gained directly from sources inside the organization including other employees or the organization itself.

Pay Transparency Measurement

Few validated instruments exist to measure the dimensions of pay transparency, and the absence of a comprehensive scale has required researchers to create their own study-specific measures (e.g., Arnold et al., 2024; Day, 2012; Hartmann & Slapničar, 2012). Additionally, aside from Smit and Montag Smit’s (2019) single-item assessing archival pay seeking behavior, our search of the literature failed to uncover any measure for archival pay transparency. Despite identifying several rigorous studies within the literature that each offer various ad hoc measures for pay transparency, when considered collectively, the body of research is neither comprehensive nor cohesive. This fragmentation is further compounded by inconsistent definitions, labeling, and measurement across the pay transparency dimensions.

For example, Day (2007, 2011, 2012) measured a construct labeled “pay communication” with four author-developed items relevant to outcome pay transparency and process pay transparency but not communication pay transparency. Day (2012) measured “perceived pay secrecy policies” with ten author-developed items relevant to communication pay transparency. Hartmann and Slapničar (2012) developed their own scale of four items relevant to outcome pay transparency that they labeled simply “pay transparency.” Smit and Montag Smit (2018) measured a construct labeled “level of non-disclosure” with four author-developed items specific to outcome pay transparency and “level of communication restriction” with four author-developed items specific to communication pay transparency. Smit and Montag-Smit (2019) also measured “pay secrecy policies” with one author-developed item focused on outcome, but not process, pay transparency. Scott et al. (2020) measured employer “pay communications” with seven items collectively relevant to outcome and process pay transparency comprised of four author-developed items and three that were adapted from Scarpello & Jones (1996) alongside a construct they labeled “pay transparency” measured with three author-developed items relevant to communication pay transparency and process pay transparency but not outcome pay transparency. Alterman et al. (2021) measured “pay secrecy perceptions” with five author-developed items specific to process pay transparency and communication pay transparency but not outcome pay transparency. Most recently, Arnold et al. (2024) developed a six-item scale with two items (one item each at the individual and group levels) to measure “procedural variable pay transparency,” two items (one item each at the individual and group levels) to measure “distributive variable pay transparency,” and two items (one item each at the individual and group levels) to measure “variable pay communication restriction.” Finally, we found a few examples of studies using scales developed in earlier research. SimanTov-Nachlieli and Bamberger (2021) used Day’s (2012) four-item scale to measure process pay transparency and Smit and Montag-Smit’s (2018) four-item scale to measure outcome pay transparency, while Tenhiälä et al. (2024) used five items from Day (2007) to measure procedural pay transparency. Apart from these examples, the vast majority of pay transparency studies we reviewed labeled, defined, segmented, and measured the same pay transparency constructs differently.

Pay Information Awareness: A Measurement Framework

This lack of alignment in pay transparency research makes it difficult to draw generalized conclusions, conduct systematic reviews and meta-analyses, and integrate research, posing significant challenges to ongoing theoretical development. Indeed, as Gerring (2012) noted: Concept formation lies at the heart of all social science endeavors. It is impossible… even to conceptualize a topic, without putting a label on it. Concepts are integral to every argument for they address the most basic question of social science research: what are we talking about? (p. 12)

Building on the existing literature as reviewed above, we now conceptualize a cohesive and comprehensive framework for a measurement scale of pay transparency.

In developing our conceptual pay transparency measurement framework, we propose consistently assessing pay transparency dimensions using the concept of pay information awareness, which is the extent to which employees are aware of the information revealed to them through each pay transparency dimension. When communicating information, both the transmission and reception of the information are critical components for organizational processes (Orpen, 1997). Existing pay transparency concepts tend to originate from the information provider’s perspective, while awareness is a distinct but related concept that originates from the information receiver’s perspective (Segijn et al., 2021). We propose measuring pay transparency based on the employee’s (receiver’s) perceptions, much like other related constructs are measured such as justice (Day, 2011), pay for performance contingency (Belogolovsky & Bamberger, 2014), pay equity (Cragun et al., 2021), and fairness (Hartmann & Slapničar, 2012). As noted earlier, behavior is based not upon objective reality, but upon individual perceptions of reality (Lewin et al., 1936).

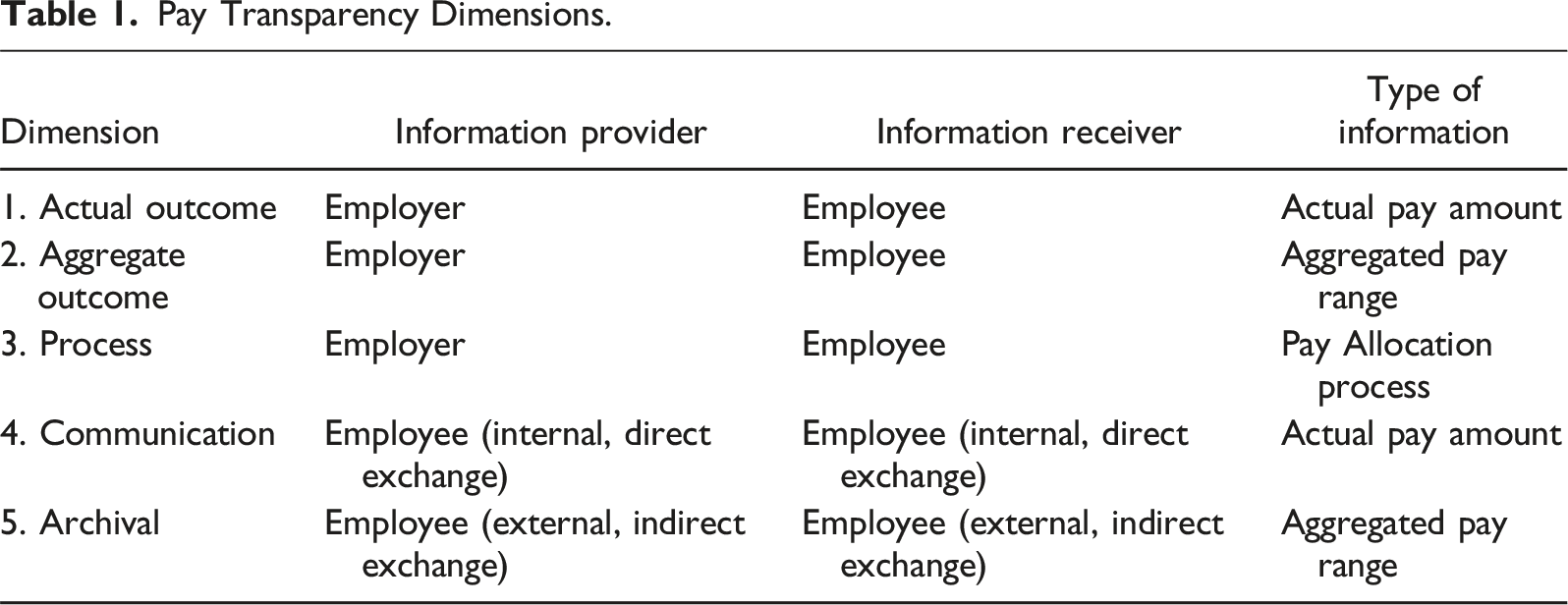

On this basis, we offer the following operationalized definitions of five primary dimensions of employee pay information awareness that may serve as manifest variables reflecting the underlying latent dimensions of pay transparency: 1) Actual outcome pay information awareness refers to the extent to which employees are aware of organization-provided information concerning the specific amount of pay employees receive; 2) Aggregate outcome pay information awareness refers to the extent to which employees are aware of organization-provided information concerning the general range of pay that employees receive; 3) Pay process information awareness refers to the extent to which employees are aware of organization-provided pay processes and practices information; 4) Communication outcome pay information awareness refers to the extent to which employees are aware of pay information by communicating with coworkers; and 5) Archival pay information awareness refers to the extent to which employees are aware of pay information from archival pay information sources.

Pay Information Awareness and Orbiting Concept Definitions.

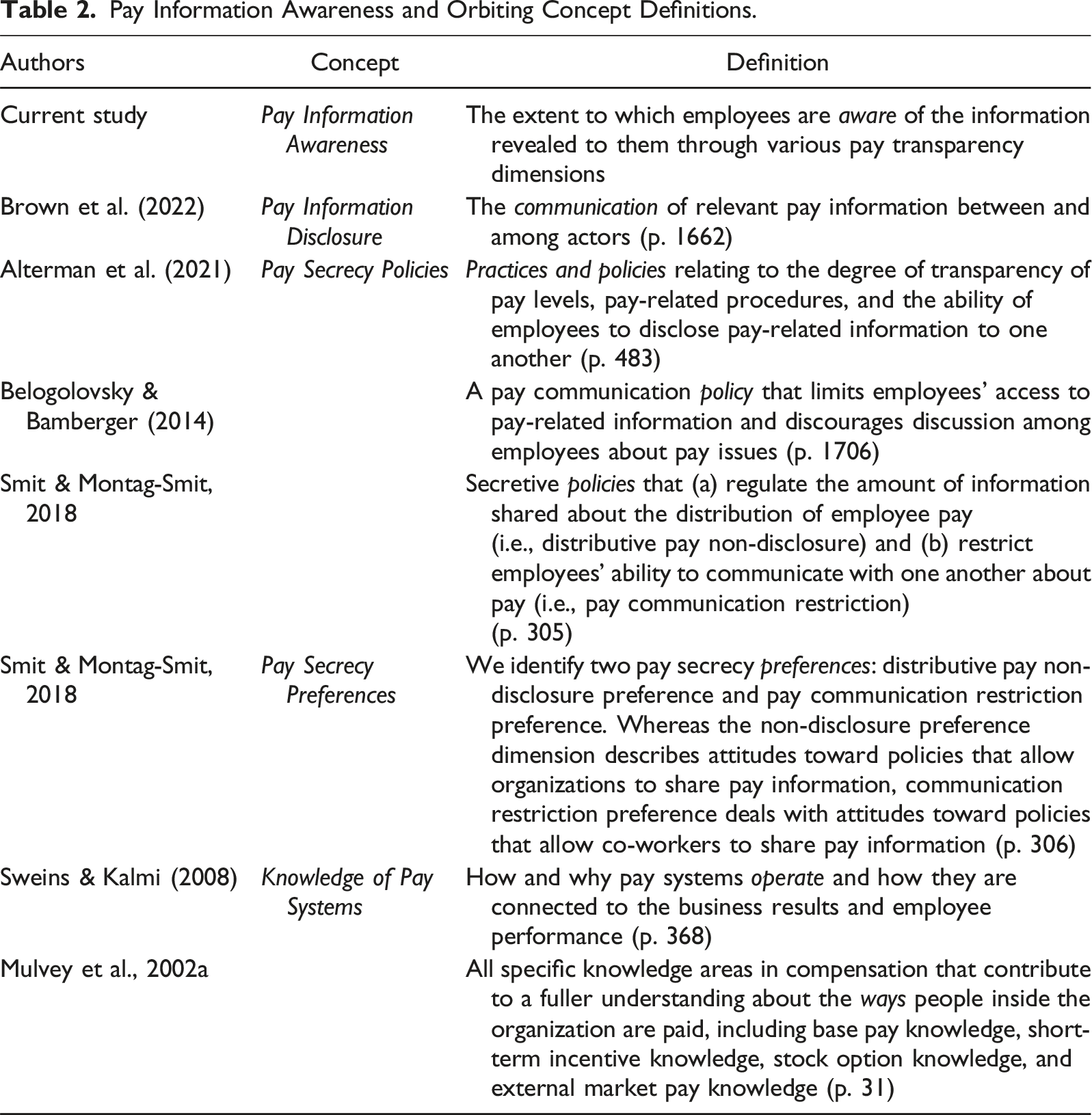

As shown in the table, the term pay information disclosure refers to the communication of pay information (Brown et al., 2022), and tends to focus on the actions of the organization in the transmission of pay information. In contrast, our conceptualization of pay information awareness focuses on the reception of pay information by the employee. In short, communication efforts by the organization or other actors do not necessarily ensure the reception or awareness of pay information. Next, the concept of pay secrecy policies focuses on the practices and policies of the organization that limit or regulate the level of pay information available to employees (Alterman et al., 2021; Belogolovsky & Bamberger, 2014; Smit & Montag-Smit, 2018). Although likely to be related, such pay secrecy policies and practices appear to be distinct from our concept of pay information awareness. Similarly, the idea of pay secrecy preferences refers to individual predilections for the extent to which one’s organization or co-workers should share pay information (Smit & Montag-Smit, 2018). Here again, our conception of pay information awareness as the extent to which employees are aware of pay information appears to be distinguishable from employees’ preferences for the extent to which pay information should be shared.

Finally, the term knowledge of pay systems refers to understanding how and why pay systems operate and the ways people are paid in organizations (Mulvey et al., 2002a, 2002b; Sweins & Kalmi, 2008). Knowledge of pay systems tend to focus on very specific aspects of how pay systems function as reflected in measurement items such as “I know how to exercise my stock options,” “I understand how bonuses are funded,” and “I know what influence the market has on my base pay level” (Mulvey et al., 2002a, 2002b). For example, Sweins and Jussila (2010) found that employee knowledge and understanding of the objectives of a deferred profit-sharing pay system resulted in increases in a number of positive outcomes including work inputs and workplace attachment. In a similar vein, Shaw and Gupta (2007) measured a concept they refer to as pay system communication with items such as “Drivers know exactly what they have to do to get pay raises” and “The pay system is clearly communicated to drivers.” These concepts are analogous to Williams and Levy’s (1992) general conceptualization of perceived system knowledge, which they applied in the context of understanding performance appraisal systems. It is important to note, however, that understanding how one’s performance appraisal system operates is distinct from having an awareness of the information generated by that system. Indeed, while such a knowledge and understanding of a pay system’s objectives may be useful in understanding employee outcomes, it appears to be distinctive from an employee’s awareness of pay information. In summary, as proposed and delineated here, pay information awareness as a comprehensive conceptualization of pay transparency operationalized in terms of information awareness has the potential to lay solid groundwork for meta-analyses and longitudinal studies, guide the direction of future research and organizational practice, and consequently facilitate a more thorough understanding of the effects and implications of pay transparency to both the individual employee and the collective organization.

Methods

Based on past scale development research (e.g., Srivastava & D’Souza, 2021) and the specific advice of Hinkin (1998), we used the following steps to create and validate the Pay Information Awareness Questionnaire (PIAQ) as an applied measure of pay transparency: (1) item generation and content validation, (2) questionnaire administration, (3) exploratory factor analysis, (4) confirmatory factor analysis, and (5) verification of convergent, discriminant, nomological validity.

Item Generation and Content Validation

As recommended by Hinkin (1998), we used logical partitioning, a deductive approach to scale creation, to generate scale items. We performed a comprehensive review of existing literature, as described above, which we used to develop conceptual definitions of the five dimensions of pay information awareness presented earlier. These definitions were then used as the foundation for the generation of 8 items for each of the five dimensions resulting in an initial 40-item scale. To evaluate the extent to which the items sufficiently sample and accurately represent the content universe of the pay information awareness dimensions, the authors performed a series of content validation analyses (Colquitt et al., 2019; Podsakoff et al., 2016). Content validation represents an essential step of scale development as it allows the assessment of a construct’s definitional correspondence, the degree to which scale items are related to the focal concept’s definition, as well as its definitional distinctiveness, the extent to which scale items are more strongly related to the focal concept’s definition than to definitions of other similar, yet distinct concepts (Colquitt et al., 2019).

Initially, thirteen management professors, doctoral students, and compensation practitioners were recruited as subject matter experts (SMEs) to evaluate the content validity of the PIAQ. SMEs completed a Qualtrics survey that required them to sort each randomly presented item into a corresponding category containing the label and definition of each of the five respective dimensions. Adhering to the guidelines proposed by Colquitt et al. (2019), we calculated two indices to assess the content validity of each of the 40 items. First, we examined the proportion of substantive agreement (psa = nc ⁄ N) where N = the total number of SMEs and nc = the number of SMEs sorting an item correctly. Second, we assessed the substantive validity coefficient (csv=(nc-no) ⁄ N) where no = the maximum number of times an item was incorrectly sorted onto the wrong dimension. The psa statistic ranges from 0 (no SMEs sorted the item correctly) to 1 (all SMEs sorted the item correctly) while the csv index ranges from −1 (no SMEs sorted items correctly) to 1 (all SMEs sorted items correctly) (Colquitt et al., 2019).

The results of the content validity analyses demonstrated that thirty items exhibited “very strong” agreement (p sa > 0.80, c sv > 0.61) between the SMEs that a given item represented the specified dimension of pay information awareness. An additional seven items demonstrated “moderate to strong” agreement (p sa > 0.60, c sv > 0.21) that a specified item represented the focal dimension. From the content validation analyses, a reduced 37-item PIAQ emerged, allowing us to move forward in collecting data using the newly pared-down scale.

Questionnaire Administration: Procedures and Sample

After receiving approval from our institution’s Institutional Review Board, the reduced 37-item PIAQ was administered to a sample of full-time employees. Study participants were recruited through the social networks of undergraduate students enrolled in an introductory management course at a large mid-Atlantic university in the United States. To be eligible for study participation, prospective respondents were required to: 1) be at least eighteen years of age and 2) work full-time (at least 30 hours per week). Cases that 1) demonstrated missing data, 2) failed to pass the attention check, 3) received a captcha score indicating a non-human participant, or 4) did not meet the indicated inclusion criteria were removed using listwise deletion. Due to the importance of ensuring our sample consisted of only full-time workers, a separate question asking participants to indicate their employment hours per week was included in the survey to eliminate non-eligible respondents. After case deletions, the final sample size consisted of 404 participants. 56% of participants identified as female, with an additional 44% percent identifying as male. The sample was 93.8% Caucasian/White, 2.5% African American/Black, 1.7% Hispanic, 1.0% Asian, 0.7% other, and 0.2% Pacific Islander. The average age of participants was 45.50 with a standard deviation of 14.66 and ages ranging between 18 and 78.

Exploratory Factor Analysis (EFA)

We next conducted an exploratory factor analysis (EFA) to confirm the a priori five-factor structure and assess the internal reliability of the PIAQ (Fabrigar & Wegener, 2011). Using Mplus 8.9 (Muthén & Muthén, 1998-2017), an EFA with oblique rotation was performed on the reduced 37-item PIAQ. As per Hinkin’s (1998) recommendations, the Eigenvalues-greater-than-one standard (the Kaiser criterion) and the scree test of the percentage of variance criterion were utilized to identify interpretable factors. As anticipated, the EFA confirmed five factors with Eigenvalues greater than one. Additionally, only two items demonstrated either poor loadings on the correct factor or inappropriate cross loadings (Hinkin, 1998). Aiming for a concise and parsimonious final scale comprised of the best performing items, we removed these two weaker items along with eleven additional items demonstrating the lowest factor loadings to arrive at a reduced 24-item PIAQ.

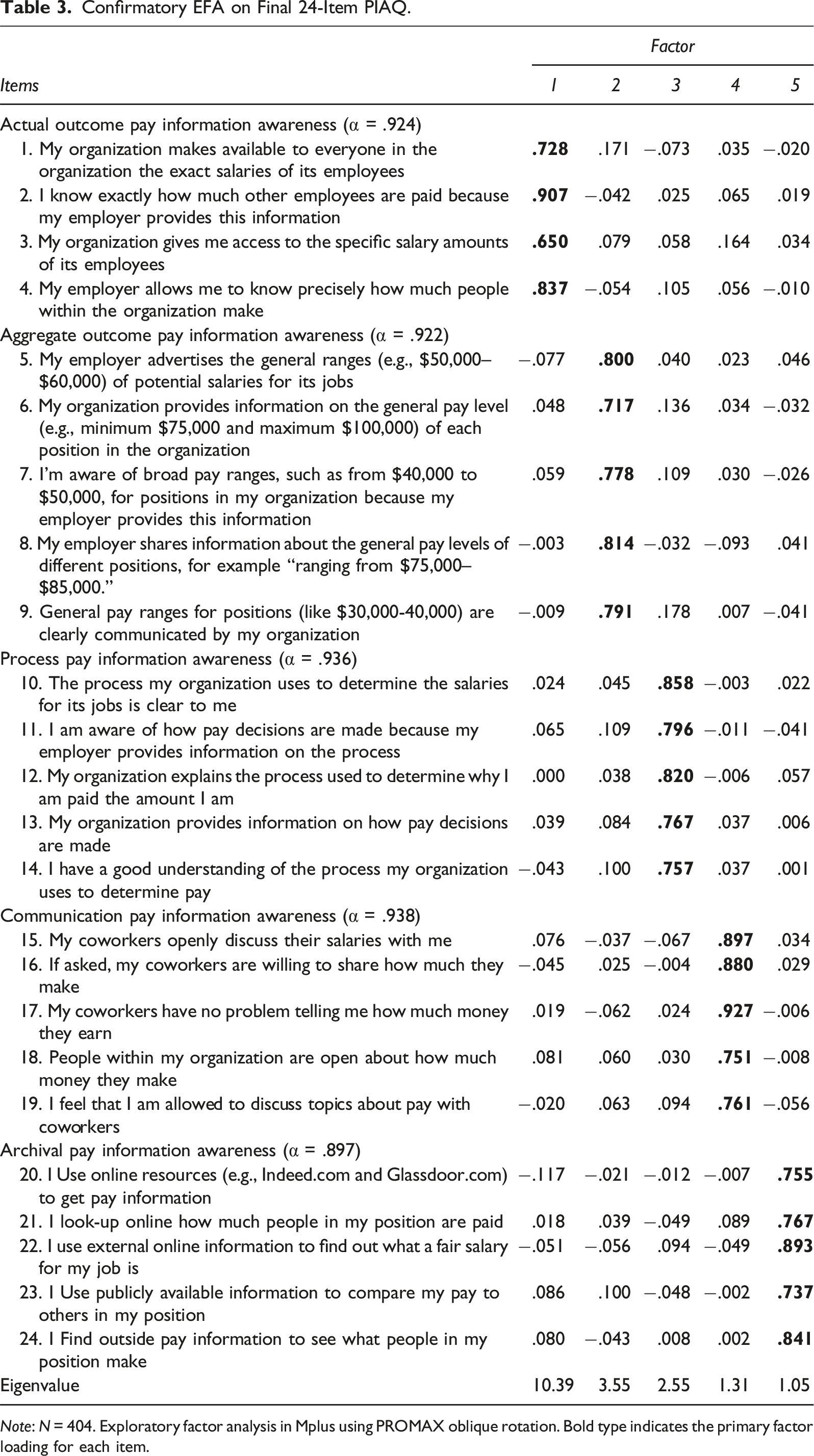

A subsequent confirmatory EFA was performed on the final 24-item scale, which similarly revealed a factor structure consisting of the expected five factors with Eigenvalues greater than one. The five factors demonstrated Eigenvalues of 10.389, 3.549, 2.551, 1.308, and 1.047, respectively. Table 3 shows the rotated factor loadings for each of the 24 items. Four items represented the actual outcome pay information awareness dimension (Cronbach’s alpha = 0.924), five items represented the aggregate outcome pay information awareness dimension (Cronbach’s alpha = 0.922), five items represented the pay process information awareness dimension (Cronbach’s alpha = 0.936), five items represented the communication pay information awareness dimension (Cronbach’s alpha = 0.938), and five items represented the archival pay information awareness dimension (Cronbach’s alpha = 0.897). As demonstrated in Table 3, all primary factor loadings exceeded the recommended cutoff value of 0.40, no items exhibited cross-factor loadings greater than 0.30, and no differences between primary and alternative factor loadings were greater than 0.20 (Hinkin, 1998).

Confirmatory EFA on Final 24-Item PIAQ.

Note: N = 404. Exploratory factor analysis in Mplus using PROMAX oblique rotation. Bold type indicates the primary factor loading for each item.

Confirmatory Factor Analysis (CFA)

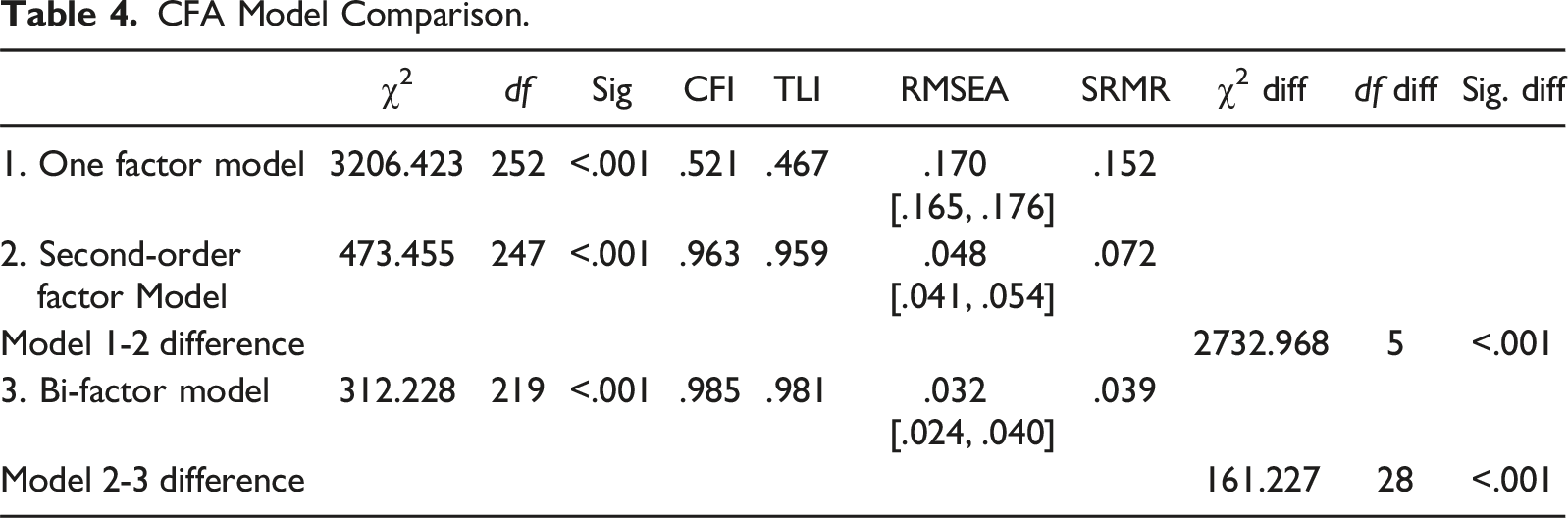

Using Mplus 8.9 (Muthén & Muthén, 1998–2017), a series of confirmatory factor analyses (CFA) were performed. In accordance with established practice, the fit of three alternative models to the data was evaluated (Chen et al., 2006; Rindskopf & Rose, 1988). First, a one-factor model specifying all 24 items loading on a single global pay information awareness factor was examined. Next, a second-order factor model consisting of five first-level factors of actual outcome pay information awareness (4 indicators), aggregate outcome pay information awareness (5 indicators), pay process information awareness (5 indicators), communication pay information awareness (5 indicators), and archival pay information awareness (5 indicators) serving as indicators for the second-order factor of pay information awareness was assessed. Finally, a bi-factor model comprised of both a separate global pay information awareness factor and five correlated factors for each of the five dimensions was evaluated. To identify and compare the standardized CFA models, the variances of the latent variables within the bi-factor model were fixed to one.

Table 4 provides a summary of model fit statistics for the CFA models (Chen et al., 2006; Rindskopf & Rose, 1988). The one factor model demonstrated poor fit with the data (χ2 [252] = 3206.423, p < .001, CFI = .521, TLI = .467, RMSEA = .170 [.165, .176], SRMR = .152), while the second-order factor model indicated adequate fit (χ2 [247] = 473.455, p < .001, CFI = .963, TLI = .959, RMSEA = .048 [.041, .054], SRMR = .072). However, the bi-factor model revealed the best fit of the three tested models (χ2 [219] = 312.228, p < .001, CFI = .985, TLI = .981, RMSEA = .032 [.024, .040], SRMR = .039). Chen and colleagues (2006, p. 190) suggest that bi-factor models may be used in the case that: (a) there is a general factor that is hypothesized to account for the commonality of the items; (b) there are multiple domain specific factors, each of which is hypothesized to account for the unique influence of the specific domain over and above the general factor; and (c) researchers may be interested in the domain specific factors as well as the common factor that is of focal interest. CFA Model Comparison.

Based on the results of the CFA analyses, it appears that the bi-factor model consisting of a global pay information awareness factor and five correlated factors representing each of the five dimensions is the most appropriate factor structure for the PIAQ (Chen et al., 2006; Rindskopf & Rose, 1988). Nevertheless, due to the adequate fit displayed by the second-order factor model, it is important to note that in certain cases, such as when researchers are interested in a single dimension of pay information awareness or when working with smaller samples, utilizing the second-order factor structure for the PIAQ may be appropriate (Goodboy et al., 2021). Given the confirmatory EFA and CFA results described above, the 24-item instrument was accepted as the final version of the PIAQ.

It is important to consider that the same data set was used for both the EFA and CFA analyses in this scale development process. When EFA is used in an exploratory manner to extract a scale’s factor structure, followed by a CFA to confirm that structure, a second sample is often recommended for the confirmatory analysis to avoid capitalizing on chance (Hurley et al., 1997; Williams & Hanna, 2023). However, when testing an a priori specification of a scale’s factor structure, it may not only be acceptable to use a single data set for both a confirmatory EFA and a confirmatory CFA, but it may even be preferred because these two analyses provide differing lenses for assessing the appropriateness of a scale’s factor structure for the same data (Williams & Hanna, 2023). Williams and Hanna (2023) further explain: In considering this issue, it is important to remember that although EFA and CFA share certain features, including the assumption that scores on items are a function of something unobserved or latent in the form of a factor, they are different statistical techniques. The underlying computations involved are different, as are the resulting parameter estimates and model diagnostic information. More importantly, both EFA and CFA statistical models can be used in either an exploratory or confirmatory approach.

In the current scale development study, we used both the EFA and CFA analyses as differing and complimentary tests for confirming the a priori five-factor structure of the PIAQ in our data.

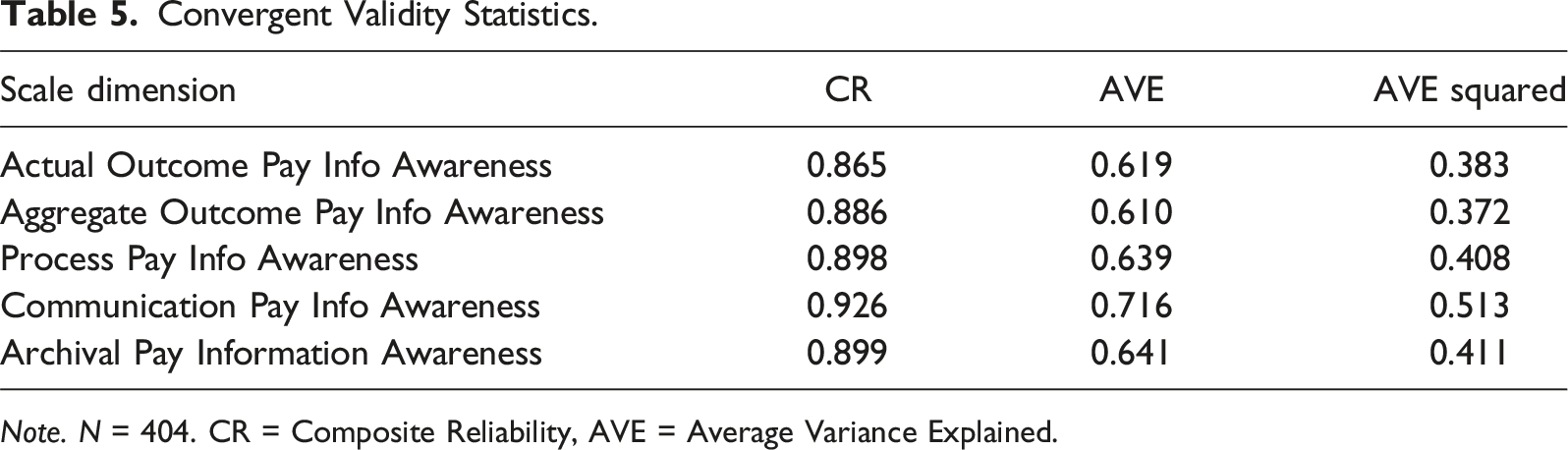

Convergent, Discriminant, and Nomological Validity

Convergent Validity Statistics.

Note. N = 404. CR = Composite Reliability, AVE = Average Variance Explained.

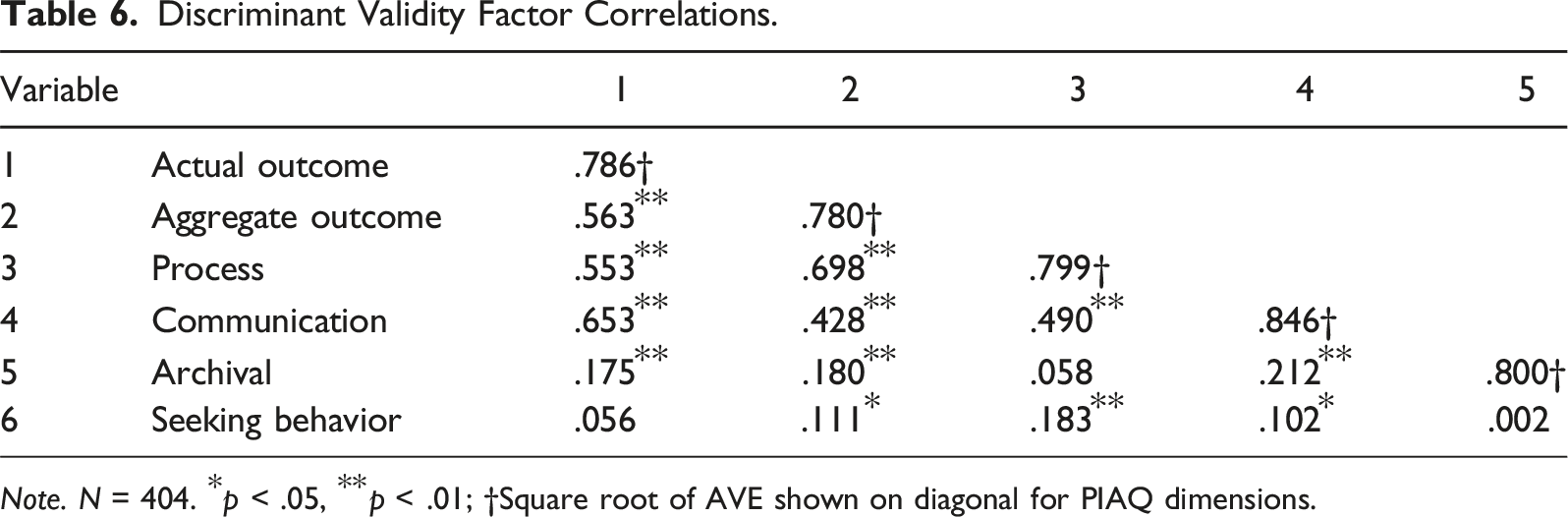

Discriminant Validity Factor Correlations.

Note. N = 404. *p < .05, **p < .01; †Square root of AVE shown on diagonal for PIAQ dimensions.

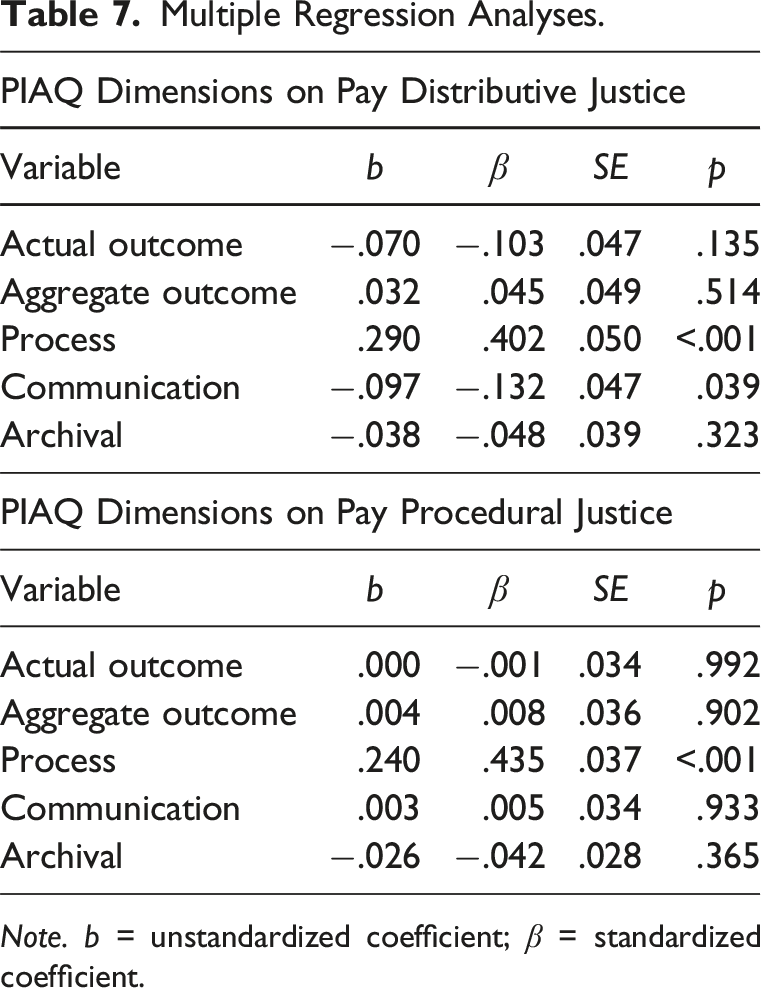

We then explored the nomological validity of the scale to confirm that theoretically hypothesized relationships exist between the measured pay information awareness dimensions and other, theoretically relevant, concepts. Individuals use pay information to make evaluative judgments about their organization, such as how fairly they are treated (Colquitt et al., 2006). As such, an individual must have some degree of awareness about relevant pay information to inform their organizational justice perceptions. Distributive justice refers to the extent that individuals feel the outcomes they receive are fair, while procedural justice captures the perception that the decision-making process by which those outcomes were derived is accurate, unbiased, and just (Colquitt et al., 2006). It seems theoretically reasonable to suggest that the various pay information awareness dimensions may differentially impact individuals’ distributive and procedural justice perceptions.

Multiple Regression Analyses.

Note. b = unstandardized coefficient; β = standardized coefficient.

Discussion

Pay transparency policies and practices have been increasingly scrutinized in recent years by both academics and managers (Bamberger & Alterman, 2024). Of particular interest is employee behavioral and attitudinal reactions to various types of pay transparency information (Scott & Jordan, 2018). Yet, the expanding body of pay transparency literature is somewhat disjointed and no comprehensive and cohesive measurement scale has been offered to date. In the present study, we advance a comprehensive multi-dimensional pay transparency framework and an accompanying measurement instrument that operationalizes pay transparency through the lens of employee awareness of pay information. We began by critically reviewing the pay transparency literature with special attention to pay transparency measurement. Next, we advanced employee pay information awareness as an appropriate framework for assessing pay transparency across its various dimensions. Finally, we developed and validated the 24-item Pay Information Awareness Questionnaire (PIAQ) as a cohesive multidimensional measure of pay transparency. Our research has important implications for pay transparency theory and practice.

Theoretical Implications

This study makes important theoretical contributions to the pay transparency literature. First, our critical review and scale development build on existing research to facilitate a greater degree of integration and cohesion for this fragmented body of knowledge. Our multidimensional pay transparency framework and accompanying measurement scale exhibit a robust bi-factor structure that aligns with our a priori research-based, theoretical conceptualizations of the pay transparency dimensions, while showing good convergent, discriminant, and nomological validity. Second, operationalizing pay transparency in terms of employee awareness of various types of pay information provides a consistent and cohesive lens for studying pay transparency founded on employee perceptions. Past research has inconsistently operationalized various forms of pay transparency in terms of organizational policies and actions in some instances and employee actions and behaviors in other instances. Our framework and scale consistently assess pay transparency dimensions in terms of employee pay information awareness perceptions. This is important because employee attitudes and behaviors in response to organizational pay transparency are likely to be based not on the objective actions of the organization but rather on the employees’ pay information awareness perceptions. Consequently, the PIAQ scale has good potential for facilitating important future research in the pay transparency domain.

Practical Implications

Our research also offers implications for pay transparency practice and policies. First, unlike past conceptualizes that focus simply on the extent to which organizations take actions and set policies to provide pay transparency information, our framework and scale serve as tools that may allow organizations and practitioners to understand the impact of their pay transparency actions and policies on employee pay information awareness and ultimately on employee attitudes and behaviors. Second, the nomological validity findings presented here may help practitioners to make better informed decisions about how best to provide pay information based on employee justice reactions. Our results, as summarized in Table 7, suggest that process pay information awareness is positively and significantly related to both pay distributive justice and pay procedural justice perceptions, while other types of pay transparency information may be unrelated or negatively related to employee fairness reactions. Employees are likely to first seek comparative pay information from the organization (i.e., outcome and process pay information), but in the absence of organization-provided information they are more likely to turn to coworkers (communication pay information) or external sources (archival pay information). Our findings imply that organizations may be best served by focusing primarily on process pay transparency information so that employees will be less likely to turn to other sources of pay information. Moreover, as Montag-Smit et al. (2023) suggest, process pay transparency may even reduce potential negative impacts of outcome pay transparency. Finally, our findings indicate that organizations choosing to provide outcome pay transparency information will benefit from providing this information in the aggregate rather than providing actual pay amounts.

Limitations and Future Research

Despite these valuable implications, our research is subject to certain limitations that offer opportunities for future research in the pay transparency realm. First, our study participants were recruited via a network sampling technique tapping into the networks (e.g., professional, friends, family, and social media) of the study authors and undergraduate students who were offered course credit in exchange for their recruitment efforts. This approach increases the possibility of a non-representative sample that mirrors the recruiters’ demographics (e.g., upper-middle class individuals). However, as Scott and Jordan (2018, p. 35) have noted, “research on pay transparency often is limited to experimental studies with student subjects, samples of employees from single organizations or surveys of compensation professionals.” In contrast, our sampling approach yielded a diverse sample representing a variety of different industries and professions. In addition, we see no reasons to suggest that employee perceptions of pay awareness would vary based on socio-economic status and meta-analytic findings suggests that student-recruited samples are equivalent to samples collected using other approaches (Wheeler et al., 2014). Still, future research should probe the generalizability of our scale in other samples of interest.

Second, recommendations for scale development suggest that the generalizability of findings should be further validated with additional independent samples (Hinkin, 1998). Given the advice of Williams and Hanna (2023) regarding using both EFA and CFA in a confirmatory manner as two differing analytical lenses in the scale development process, we used a single large sample to confirm the a priori five-factor structure of the PIAQ in our EFA, CFA, and validity analyses. Nevertheless, Krzystofiak et al. (1998) argue that factor analytic techniques used in scale development can yield sample specific results and therefore future research should aim to replicate the factor structure of the PIAQ in other samples and contexts of interest.

Third, we chose to develop a comprehensive multi-dimensional pay transparency scale that operationalizes pay transparency based on employee awareness of each type of pay information. This measurement perspective seems especially appropriate for exploring pay transparency relative to employee attitudinal and behavioral outcomes because attitudes and behaviors stem from perceptions of reality rather than from an objective reality (Lewin et al., 1936). However, for some research purposes a more objective assessment of company pay transparency policies and practices may be preferred. For example, future researchers interested in why companies implement various transparency approaches may wish to choose a different measurement tool.

In closing, our research makes an exciting contribution by integrating the various dimensions of pay transparency within a comprehensive and consistent framework for assessment founded on employee awareness perceptions. This framework and the associated measurement scale, the PIAQ, developed and validated in this study provides future researchers and organizational practitioners with a critical tool for exploring the impacts of pay transparency policies and practices on employee attitudes and behaviors. A richer understanding of employee perceptual reactions to pay information from various sources should help organizational decision-makers to choose the best approaches to pay transparency to enhance employee satisfaction and engagement.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.