Abstract

The question of whether Chief Executive Officers (CEOs) should receive financial incentives to act ethically sits at the intersection of corporate governance, behavioral theory, and normative ethics. Existing debates reflect polarized views on the efficacy and morality of paying leaders to uphold ethical standards. The aim of this paper is to offer a balanced perspective on the competing arguments surrounding ethical compensation for CEOs, evaluating the strengths and limitations of key theoretical approaches while proposing an integrated framework for future practice. This perspective synthesizes existing literature and theoretical contributions, including agency theory, behavioral economics, normative ethics, and feminist organizational theory to highlight tensions and overlapping principles in the discourse. In addition, the paper draws on five short case analyses of high-profile corporations. The paper highlights that incentive-based ethics programs may align executive behavior with stakeholder expectations under certain conditions, but also risk commodifying morality and encouraging symbolic rather than substantive ethical compliance. Measurement challenges and contextual ambiguity further complicate such an implementation. Ethical leadership cannot be reduced to monetary rewards alone. A hybrid model combining intrinsic development, transparent performance metrics, and stakeholder engagement may offer a more sustainable path toward ethical accountability. This nuanced approach invites continued interdisciplinary dialogue across business, ethics, and policy domains.

Keywords

Introduction

In an era marked by growing scrutiny of corporate behavior and rising expectations for ethical leadership, the question of whether Chief Executive Officers (CEOs) should be financially incentivized to act ethically sits at the crossroads of philosophy, economics, and governance (Brennan et al., 2021; Fabrizi et al., 2014; Velte, 2020). As high-profile scandals, from environmental negligence to financial fraud, continue to punctuate the corporate landscape, the call for accountability has intensified (Kumar & Verma, 2024; Lopes et al., 2025). Ethics is no longer considered a soft ideal but a strategic imperative tied closely to brand equity, investor trust, and stakeholder engagement (Khanna, 2025; Singer, 2010). However, despite the increasing demand for moral integrity in the executive suite, the mechanisms for cultivating ethical behavior among CEOs remain contested and complex (Roy et al., 2024).

Within traditional contexts, the prevailing assumption in both society and boardrooms is that ethical conduct constitutes an inherent aspect of leadership (Brown & Treviño, 2006; Naeem & Syed, 2024). Executives, especially those at the leading positions, are expected to demonstrate moral courage without needing financial reinforcement (Provitera et al., 2023; Sekerka et al., 2009; Tracy, 2025). The ethical leader archetype is a figure guided by values, social responsibility, and personal integrity and is held up as the highest standard (Brown et al., 2005; De Hoogh & Den Hartog, 2008; Rothausen, 2023). However, modern corporate structures often prioritize profit maximization, short-term returns, and competitive positioning, inadvertently creating misaligned incentives that test even the most principled leaders (Yeh, 2022). This tension raises a provocative question: “If the system itself rewards risk and results, might aligning ethical behavior with compensation improve outcomes?” Or “Does paying someone to do what is ‘right’ reduce ethics to a transactional exercise?”

Supporters of incentive-based ethics draw from agency theory and behavioral economics, arguing that executives, like other agents, respond predictably to performance-linked rewards (Jensen & Meckling, 1976; Martin et al., 2020; Pepper, 2021). If unethical behavior stems partly from misaligned motivations such as bonuses tied to quarterly profits, then restructuring compensation to include ethical benchmarks could realign CEO actions with societal and stakeholder interests (Perel, 2003). By integrating metrics related to environmental stewardship, diversity efforts, transparent governance, and responsible risk-taking, corporations might not only reduce misconduct but also promote a culture of ethical excellence (Jámbor & Zanócz, 2023). Case studies from ESG (environmental, social, and governance)-driven companies and investor coalitions offer promising signs that performance on ethical dimensions can be tracked and rewarded meaningfully (Marzuki et al., 2023).

However, this pragmatic approach invites sharp criticism, particularly from scholars of normative ethics, feminist organizational theory, and organizational psychology (Fotaki & Pullen, 2024; Perel, 2003; Rutherford et al., 2015). Critics emphasize that monetizing morality undermines the foundational principle that ethics should stem from personal conviction, not extrinsic gain (Novak & Skitka, 2025). By turning ethical leadership into a game of metrics and bonuses, organizations might run into the risk of hollowing out genuine responsibility and fostering performative compliance (Ellertson et al., 2016). Moreover, measuring ethics, which is often qualitative, contextual, and culturally nuanced, presents its own challenges (Scheytt & Pflüger, 2024; Taquette & Souza, 2022), asking the questions such as “What constitutes ethical success?” “Can it be quantified and audited with the same precision as financial performance?” The danger lies in incentivizing the appearance of integrity rather than the practice of it, leading to ethics checklists rather than principled behavioral outcomes (Ellertson et al., 2016).

This tension reflects broader philosophical debates about the nature of morality, motivation, and leadership. “Should ethics be treated like any other key performance indicator (KPI), integrated into bonus structures and contracts?” Or “Is there something fundamentally different about moral responsibility that resists commodification?” In many respects, the conversation mirrors public debates about performance-linked pay in sectors such as education, policing, and politics. The stakes are especially high in corporate leadership, where decisions affect not just shareholders but communities, ecosystems, and global economic stability (Maak et al., 2016).

Rather than reducing this issue to a binary— to pay or not to pay, this perspective argues for a hybrid approach. Ethical behavior should begin with intrinsic values, but institutions can amplify and reinforce these values through transparent, thoughtful reward systems (Manzoor et al., 2021). Ethical training, stakeholder engagement, and long-term incentive alignment might offer a middle ground between morality-as-duty and morality-as-performance (Kujala et al., 2022; Mitchell et al., 2020). Ultimately, the question is not just whether CEOs should be paid to be ethical, but how organizations can embed ethics into leadership structures without compromising authenticity.

While ethical incentives are often narrowly interpreted as mechanisms that promote moral reasoning or integrity, this paper adopts a broader lens including prosocial value alignment, ESG-linked performance metrics, and deterrents for unethical behavior. Recent scholarship demonstrates that executive compensation increasingly incorporates ESG criteria, thereby embedding ethical orientation into pay structures (Agarwal et al., 2025; Chaigneau & Sahuguet, 2025). Prosocial values, such as those exemplified by Patagonia’s commitment to sustainability and stakeholder well-being, illustrate how ethical incentives can be operationalized through corporate culture and compensation. Similarly, firms like Unilever and Danone have tied CEO rewards to ESG outcomes, reinforcing ethical orientation through measurable performance targets (Chaigneau & Sahuguet, 2025). Conversely, cases such as Wells Fargo highlight the punitive dimension of ethical incentives, where misconduct leads to reputational damage and financial penalties, underscoring the deterrent side of ethical compensation. Accordingly, the case studies selected for this paper illustrate the multifaceted nature of ethical incentives in practice, encompassing positive reinforcement of prosocial and ESG values as well as sanctions against unethical behavior.

Therefore, the core focus of the paper includes aligning pay with purpose; incentivizing ESG, prosocial values, and ethical leadership; rewarding purpose-driven performance; linking compensation to ethics and prosocial values; and using compensation as a lever for ethical and prosocial corporate behavior. This paper contributes to the existing literature by advancing a multidimensional perspective on ethical compensation for CEOs. Rather than treating ethics as an abstract or immeasurable construct, the paper conceptualizes ethical incentives through three interrelated dimensions: prosocial value alignment, ESG-based performance metrics, and deterrence of misconduct. This framing extends prior research by linking philosophical foundations of integrity with measurable organizational practices and outcomes. The case-based analysis further illustrates how these dimensions are operationalized in diverse corporate contexts, thereby offering both theoretical innovation and practical guidance for governance in high-stakes environments.

To sum up, this paper explores the nuanced arguments on both sides of the debate, drawing from theory, case examples, and emerging practices in ethical compensation design. It seeks to advance a balanced view that respects philosophical foundations while acknowledging the realities of corporate governance in environments characterized by intense competition, significant financial rewards, and heightened public scrutiny. By integrating ethical reasoning with practical considerations, the paper highlights how compensation structures can serve not only as mechanisms for motivating performance but also as instruments for reinforcing integrity, prosocial values, and accountability. In doing so, the paper contributes to a deeper understanding of how organizations can align executive incentives with broader societal expectations, thereby promoting sustainable leadership and long-term trust in corporate governance.

Literature Review

The debate surrounding ethical incentives for CEOs has captured the interest of scholars across disciplines, including economics, moral philosophy, business ethics, and organizational behavior (Brennan et al., 2021; Park, Park, & Barry, 2022). As corporations grapple with reputational risks and increasing calls for social responsibility, the existing literature reveals a rich tapestry of theories and critiques about whether and how ethics can be woven into executive pay structures (Edmans et al., 2017; Ferrarini & Ungureanu, 2025).

One of the earliest and most cited frameworks in compensation studies is agency theory, introduced by Jensen and Meckling (1976). It conceptualizes executives as agents acting on behalf of principals (i.e., shareholders), suggesting that compensation must align CEO interests with shareholder goals. So far, these goals have focused almost exclusively on financial outcomes, inadvertently encouraging CEOs’ behaviors that prioritize short-term gains at the expense of long-term ethical concerns (Edmans et al., 2017; Ferrarini & Ungureanu, 2025; Sandberg, 2019). Scholars such as Bebchuk and Fried (2010) criticize the over-reliance on stock options and performance bonuses, arguing that such incentives can promote excessive risk-taking, manipulation of financial statements, and neglect of social responsibilities. This line of critique paves the way for discussions on expanding the scope of performance metrics to include ethical dimensions, such as sustainability, employee well-being, and regulatory compliance (Alhazemi, 2025; Qamar et al., 2023).

In contrast, stakeholder theory, introduced by Freeman (1984), broadens the scope of accountability to include employees, customers, suppliers, communities, and the environment. This approach asserts that ethical leadership must recognize and address the needs of diverse stakeholders, not just shareholders (DesJardine et al., 2023). Compensation structures aligned with stakeholder theory often incorporate ESG metrics, which serve as proxies for ethical performance (Chaigneau & Sahuguet, 2025; Cohen et al., 2023). Eccles et al. (2014), for example, emphasize how ESG-linked pay can incentivize sustainability and responsible governance. A growing body of research (such as Cheema-Fox et al., 2020; Clément et al., 2023; Friede et al., 2015) indicates that companies with robust ESG frameworks outperform peers over the long term, suggesting that ethical incentives may not merely be a moral imperative but also a strategic advantage.

However, even ESG-based ethical compensation is not without its criticism. Measuring ethics remains a complex, multifaceted endeavor. Ethical conduct often depends on context, culture, and subjective interpretation. Some scholars (such as Espeland & Sauder, 2007; Shore & Wright, 2000) argue that over-reliance on measurable indicators reduces ethics to a checklist rewarding form over substance. On the other hand, some very recent studies (Ben Mahjoub, 2025; Poiriazi et al., 2025; Ruggeri et al., 2025) on the Global Reporting Initiative (GRI) note inconsistencies in ESG reporting standards, raising concerns about “greenwashing” or “ethics-washing,” where companies appear ethically sound but fail to engage in substantive moral practices.

Adding another layer, behavioral ethics delves into the psychological dynamics behind ethical decision-making (Chugh et al., 2016; Tenbrunsel & Smith-Crowe, 2008). According to Bazerman and Tenbrunsel (2011), individuals often perceive themselves as more ethical than they actually are, due to cognitive blind spots and social biases. They suggest that ethical lapses frequently stem from ambiguous norms and pressure to conform, rather than overt malice. In this context, ethical incentives can help CEOs become more aware of their decision-making processes and hold themselves accountable. However, behavioral scholars warn that incentives alone cannot substitute for deep cultural transformation (Coate & Hoffmann, 2022). Ethics training, mentorship, and corporate culture all play vital roles in shaping ethical behavior.

From a philosophical standpoint, the literature offers divergent views. Deontological ethics, rooted in Kantian moral philosophy, sees morality as duty-based (Allison, 2011). According to Kant, ethical behavior should be driven by rational principles and respect for human dignity, not by reward. This perspective criticizes incentive-based ethics as reducing virtue to self-interest. A Kantian view would argue that if a CEO needs to be paid to act morally, then the action lacks moral worth (Wood, 2007).

On the other end of the spectrum, utilitarianism, pioneered by Jeremy Bentham and John Stuart Mill, judges actions based on outcomes (Lu, 2020). A utilitarian might argue that if incentivizing ethical conduct results in greater overall well-being such as fewer scandals, better stakeholder trust, and more sustainable practices, then it is not only permissible but also desirable (Bentham, 1996; Mulgan, 2020). This consequentialist lens so far has influenced many corporate governance frameworks, which increasingly weigh social impact alongside financial returns (Shmelev & Gilardi, 2025).

Feminist organizational theory offers a compelling alternative, emphasizing relationships, care, and interconnectedness (Calhoun, 2004; Gilligan, 1982; Held, 2006; Lindemann, 2019). Carol Gilligan, whose work challenges traditional moral development theories, highlights how ethical behavior is often rooted in empathy and relational responsibility (Held, 2006; Li, 2025; Lindemann, 2019). Feminist theorists argue that compensation schemes miss the relational subtleties of ethical leadership such as listening, emotional intelligence, and conflict resolution (Ndlovu et al., 2016; Pullen & Vachhani, 2023). Rather than metrics, they advocate for inclusive decision-making processes and ethical cultures that support collaborative and community-driven values.

Empirical studies provide valuable insights but still remain inconclusive (Moriarty, 2009; Perel, 2003). According to a 2021 analysis in “Harvard Business Review,” companies linking CEO pay to ESG metrics have reported marginal improvements in ethical outcomes and stakeholder engagement (Gosling et al., 2021). However, it has also noted risks of compliance theater where leaders meet benchmarks without enacting real change. Meanwhile, a 2022 “World Economic Forum” report has recommended a multi-pronged approach, combining transparent ethical metrics, leadership training, and long-term incentive structures to foster moral integrity across organizations (World Economic Forum. September 6, 2023).

Recent examples from the corporate world illustrate these tensions (Ethisphere, 2024). Patagonia, for instance, is widely praised for embedding ethics into its leadership DNA, not through pay incentives alone, but through purpose-driven practices and stakeholder-centric governance (Atkinson, 2022). In contrast, the fall of companies like Theranos and Wirecard underscores how charismatic leadership devoid of accountability can lead to catastrophic ethical failures (Stone Prime Consultancy, 2023). These cases suggest that ethics must be embedded holistically through culture, structure, and yes, perhaps compensation.

Ethics as a concept is difficult to quantify, since it does not lend itself to measurement along a continuum such as moderately ethical or highly ethical. What can be observed more reliably are unethical behaviors, which organizations often penalize, and prosocial or ESG-oriented practices, which can be rewarded. For this reason, this paper frames ethical incentives as a broader category that includes measurable proxies such as prosocial value alignment and ESG-linked performance metrics, alongside deterrents for misconduct. This approach allows to connect the theoretical emphasis on ethics with practical mechanisms that organizations can implement in executive compensation design.

Recent scholarship emphasizes the role of prosocial ethical incentives in shaping executive behavior. Park, Eaglesham, et al. (2022) argue that compensation systems can be designed to promote socially beneficial outcomes by rewarding behaviors that align with stakeholder interests and long-term societal goals. This perspective complements our broader framing of ethical incentives, which includes prosocial value alignment, ESG-linked metrics, and deterrents for misconduct. By incorporating prosocial incentives into executive compensation, organizations can reinforce ethical orientation in a way that is both measurable and impactful.

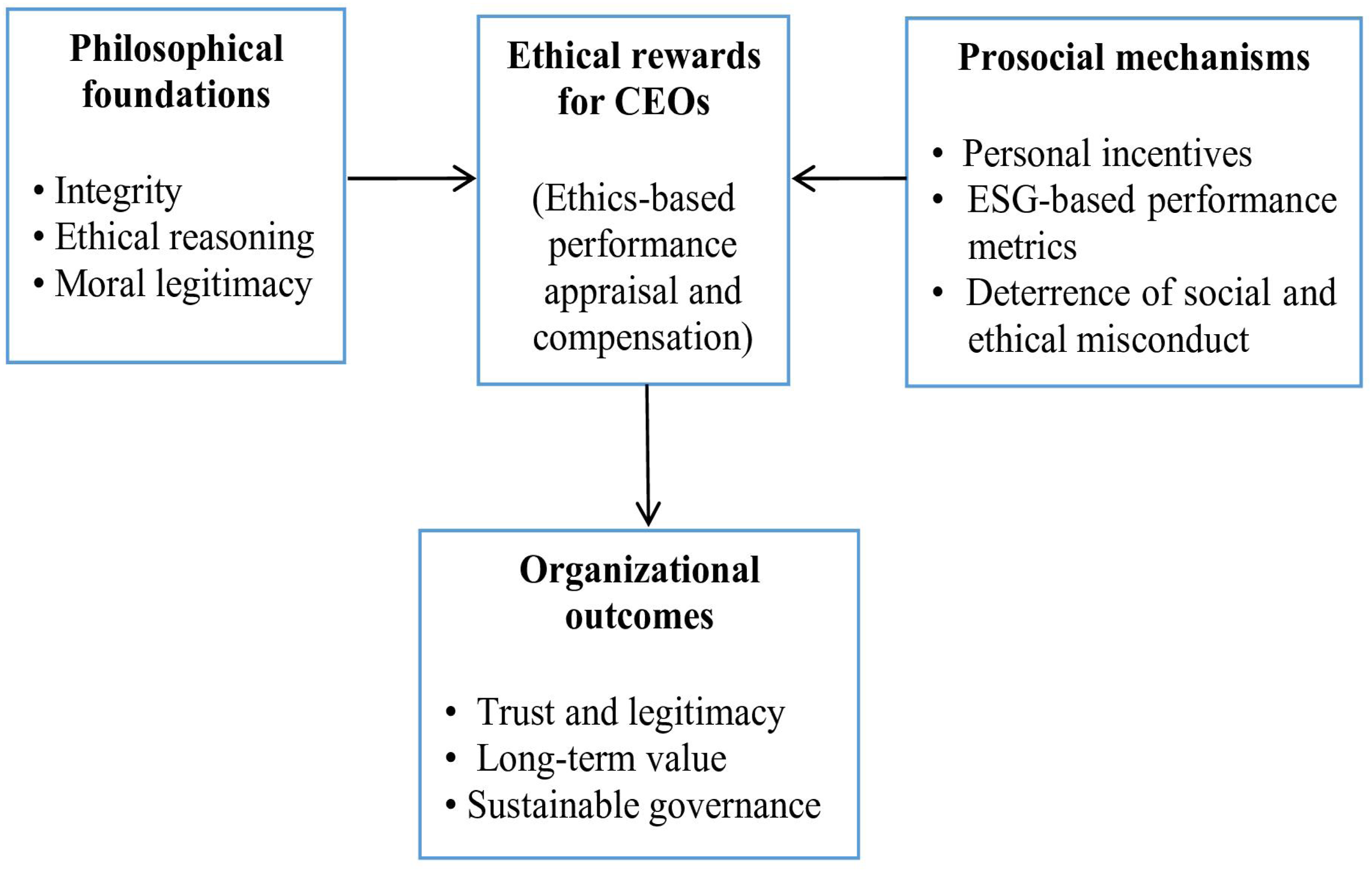

Although ethical behavior, corporate social responsibility (CSR), and ESG-based practices are sometimes discussed together, they are distinct constructs. Ethical behavior refers to individual or organizational adherence to moral principles. CSR emphasizes the broader responsibility of firms to society, while ESG focuses on measurable criteria used by investors and stakeholders to evaluate corporate performance. As Fischer (2004) notes, clarifying these concepts is essential for analytical rigor, and in this paper they are treated as related but not interchangeable. Figure 1 illustrates the conceptual framework developed by the author. Conceptual framework (source: the author).

In conclusion, the literature presents a complex picture of ethical incentivization. While theoretical and empirical evidence supports the idea that aligning pay with moral performance can curb misconduct and elevate corporate responsibility, scholars remain cautious about over-simplifying ethics through metrics. A growing consensus points toward a balanced approach, one that respects intrinsic motivation, cultivates ethical cultures, and strategically integrates ethical incentives to reinforce good behavior without commodifying virtue.

Research Methodology

Research Design

This paper is based on a qualitative case study approach to examine how ethical considerations can be integrated into CEO compensation systems. Case studies are particularly suited to exploring complex organizational phenomena where context, leadership characteristics, and structural incentives interact (Park, Park, & Barry, 2022). By analyzing multiple firms across industries, the paper highlights both successes and failures in aligning compensation with integrity.

Case Selection

Cases were chosen to represent a spectrum of approaches to ethical CEO compensation: - Firms emphasizing cultural reinforcement without financial incentives (Patagonia). - Firms linking compensation directly to ESG metrics (Danone). - Firms where misaligned incentives have produced negative outcomes (Wells Fargo). - Firms adopting hybrid approaches that integrate ethical culture with incentive alignment (Unilever and Salesforce).

This case-based analytical approach is expected to ensure diversity of practices and outcomes, allowing the conceptual model to be tested against contrasting real-world examples.

Data Sources

The analysis drew upon publicly available materials, such as annual reports, sustainability disclosures, press releases, interviews, and secondary literature. These sources were used to provide insights into both compensation structures and leadership orientations.

CEO Selection and Ethical Traits

In addition to compensation structures, CEO selection processes and ethical traits were examined. Recognizing that incentives alone are insufficient to guarantee integrity, attention was directed to how boards identified and appointed leaders (of that five companies) predisposed to act responsibly. Key dimensions included the following.

Track Record of Integrity

Evidence from prior roles, controversies, and stakeholder relationships.

Values Orientation

Statements, interviews, and leadership behaviors revealing intrinsic motivation toward social responsibility.

Stakeholder Reputation

External perceptions of trustworthiness and fairness.

Succession Planning Criteria

Whether ethical leadership was explicitly embedded in board-level selection processes.

By integrating these dimensions, the methodology acknowledges that ethical compensation systems are most effective when paired with leaders who possess intrinsic ethical orientation.

Analytical Strategy

Each case was analyzed in relation to the theoretical framework of balanced ethical compensation. The role of CEO traits and selection processes was examined alongside structural incentives to assess how integrity is incentivized in practice. Cross-case comparison highlighted patterns and divergences, enabling refinement of the conceptual model.

Case Analysis: Ethics and Executive Compensation

The debate over paying CEOs to be ethical is not theoretical alone, it plays out in boardrooms and business cultures worldwide. The following cases examine contrasting approaches to ethical incentives, highlighting lessons from success, failure, and controversy.

Patagonia: Embedding Ethics into Leadership Culture

Patagonia Inc. is frequently cited as a gold standard in socially responsible leadership. Founded by Yvon Chouinard, the outdoor apparel company built its business model around environmental sustainability, fair labor practices, and corporate transparency. From its inception, Patagonia has rejected conventional growth-at-all-costs strategies, instead prioritizing long-term ecological and social impact. While the CEO’s compensation has never explicitly included ethics-based bonuses, the entire governance structure has been designed to promote ethical stewardship through embedded values, stakeholder engagement, and mission alignment.

In 2022, Chouinard made global headlines by transferring ownership of Patagonia to the Patagonia Purpose Trust and the Holdfast Collective, a nonprofit dedicated to combating climate change and protecting undeveloped land. This unprecedented move ensured that all profits not reinvested in the business would be used to preserve the planet, effectively institutionalizing Patagonia’s ethical mission beyond any single leader’s tenure. Chouinard’s modest salary and absence of equity windfalls stand in stark contrast to the excesses often seen in executive compensation, challenging industry norms and reinforcing the company’s commitment to integrity.

Rather than relying on extrinsic incentives, Patagonia fosters a values-driven culture that aligns purpose with leadership behavior. Ethical conduct is not a performance metric, it is a foundational expectation. Employees are encouraged to engage in activism, participate in environmental initiatives, and make decisions that reflect the company’s core values. This holistic approach to governance demonstrates that ethical leadership can be sustained through culture, structure, and purpose, not just compensation.

Lesson Learnt

Ethics can be incentivized structurally and culturally, even without financial rewards when leadership is mission-driven and stakeholder-centered.

Danone: ESG-Linked CEO Pay and Strategic Shifts

French multinational Danone took a more formal and metrics-driven approach to ethical leadership. Under former CEO Emmanuel Faber, the company became a prominent advocate for integrating ESG principles into core business strategy. Faber championed the concept of “responsible capitalism,” aiming to redefine corporate success beyond shareholder value. Under his leadership, Danone pursued B Corp certification, a rigorous designation that evaluates companies on social and environmental performance and set ambitious sustainability targets across its global operations.

A hallmark of Faber’s tenure was the incorporation of ESG metrics directly into executive compensation. The company’s 2019 remuneration report revealed that a substantial portion of CEO bonuses was tied to non-financial performance indicators, including carbon footprint reduction, employee engagement, and supply chain transparency. This move signaled a shift from traditional profit-centric incentives to a more holistic view of leadership accountability. Faber’s approach positioned Danone as a pioneer in aligning corporate governance with societal impact.

However, in 2021, Faber was abruptly ousted following mounting pressure from activist investors and shareholders concerned about lagging financial returns. The decision sparked a broader debate about the viability of ethical leadership within publicly traded companies. Critics argued that Danone’s ESG focus diluted short-term profitability and distracted from core business performance. Supporters, on the other hand, contended that Faber’s vision was forward-thinking and necessary in a world increasingly shaped by climate risk, social inequality, and stakeholder activism.

The episode highlights a fundamental tension in modern corporate governance: “Can ethical leadership truly coexist with shareholder primacy?” Danone’s experience suggests that while ESG integration can elevate a company’s reputation and long-term resilience, it may also expose leaders to backlash if financial metrics falter. Faber’s legacy continues to influence conversations around sustainable capitalism, even as companies grapple with balancing purpose and profit.

Lesson Learnt

Ethics-linked pay structures can promote long-term stakeholder value, but they must be carefully balanced with financial imperatives and backed by board support.

Wells Fargo: Ethics Incentives without Cultural Reform

Wells Fargo presents a cautionary tale in the realm of corporate ethics and leadership accountability. The bank’s 2016 fake accounts scandal where employees created millions of unauthorized accounts to meet aggressive sales targets exposed a toxic culture driven by unrealistic quotas and relentless internal pressure. The fallout was severe: regulatory fines, reputational damage, executive resignations, and widespread public scrutiny. In response, Wells Fargo’s leadership pledged to overhaul its incentive systems and embed ethics into its performance framework.

Post-scandal, the bank introduced a series of reforms aimed at restoring trust and preventing future misconduct. These included the implementation of “risk metrics” and “culture audits” in executive evaluations, as well as adjustments to bonus eligibility based on ethical conduct and compliance. The goal was to shift the focus from pure sales performance to a more balanced assessment of behavior and risk awareness. Ethics training was expanded, whistle-blower protections were reinforced, and governance structures were revised to improve oversight.

However, critics argued that these reforms were largely superficial, more cosmetic than transformative. Ethics appeared bolted on rather than built into the organizational DNA. While the language of integrity became more prominent in corporate communications, many employees and executives reportedly continued to feel intense performance pressure. The underlying incentive structures and cultural norms that had fueled unethical behavior remained largely intact. Regulatory investigations persisted for years, suggesting that the root causes of misconduct were not fully addressed.

Wells Fargo’s experience underscores a critical lesson: ethical leadership cannot be retrofitted. It must be cultivated through systemic change, not just policy tweaks. True reform requires a re-imagining of corporate values, leadership behavior, and incentive design. Without a genuine cultural shift, ethics initiatives risk becoming performative, serving as window dressing rather than meaningful safeguards. The case remains a stark reminder of how deeply embedded cultural flaws can undermine even the most well-intentioned reforms.

Lesson Learnt

Incentivizing ethics cannot succeed in isolation, it must be supported by cultural overhaul, clear accountability, and systemic transparency.

Unilever: Purpose-Driven Metrics and CEO Pay Alignment

Unilever, a global consumer goods powerhouse, offers a nuanced and influential model for ethical incentivization in corporate leadership. Under the stewardship of former CEO Paul Polman, the company launched its ambitious “Sustainable Living Plan,” a strategic framework that embedded environmental stewardship, social responsibility, and ethical governance into the heart of its business operations. Polman’s leadership marked a departure from traditional quarterly earnings pressures, advocating instead for long-term value creation that benefited both shareholders and society.

A key feature of Polman’s tenure was the integration of sustainability metrics into executive compensation. His pay package included performance targets related to sustainable sourcing, reductions in environmental impact, improvements in public health outcomes, and fairness across the supply chain. These metrics were not peripheral, they were central to how leadership success was measured. By tying financial rewards to ethical outcomes, Unilever signaled a commitment to aligning corporate incentives with global challenges such as climate change, poverty, and inequality.

This ethics-first strategy earned Unilever widespread acclaim. The company was frequently cited as a leader in corporate responsibility, and its brands such as Dove, Ben & Jerry’s, and Seventh Generation benefited from strong consumer loyalty rooted in shared values. Polman himself became a prominent voice in global sustainability circles, advocating for responsible capitalism and urging other CEOs to adopt similar models.

However, the approach was not without controversy. Some financial analysts expressed concern that Unilever’s intense focus on social and environmental goals came at the expense of short-term profitability. Certain product lines experienced margin pressures, and critics questioned whether ethical performance should be weighted so heavily in executive pay. The tension between purpose and profit sparked broader debates in the business community: “Can companies truly balance stakeholder interests with shareholder expectations?” and “Does linking compensation to ethics risk diluting financial discipline in market-driven industries?”

Unilever’s experience under Polman illustrates both the promise and complexity of ethical incentivization. It shows that value-driven leadership can elevate brand equity and global reputation— but also that embedding ethics into pay structures requires careful calibration to avoid unintended consequences. As ESG metrics become more mainstream in executive compensation, Unilever remains a case study in how far companies can and should go in aligning leadership rewards with moral responsibility.

Lesson Learnt

Ethics-based incentives can enhance brand reputation and stakeholder loyalty when integrated into broader strategy but must adapt to market realities to remain sustainable.

Salesforce: Leading with Values and Executive Accountability

Salesforce CEO Marc Benioff has emerged as one of the most prominent champions of ethical capitalism in the tech industry. Known for his outspoken advocacy on issues ranging from social justice and climate change to workplace equality and mental health, Benioff has consistently positioned Salesforce as a company where business success is inseparable from social impact. His leadership reflects a belief that corporations have a moral obligation to serve not just shareholders but all stakeholders, including employees, communities, and the planet.

This philosophy is not just rhetorical; it is embedded in Salesforce’s governance and executive compensation structures. The company’s performance evaluations for senior leaders include measurable ESG goals such as workforce diversity targets, pay equity progress, and reductions in environmental footprint. These metrics influence not only annual bonuses but also long-term incentive plans, signaling that ethical performance is a core dimension of leadership accountability. Salesforce also integrates ESG outcomes into its corporate reporting and investor communications, reinforcing transparency and aligning financial strategy with social responsibility.

Benioff’s approach blends intrinsic values with structured accountability. He argues that capitalism must evolve to address systemic challenges and that companies should be judged not only by their profits but also by their contributions to society. Under his leadership, Salesforce has taken bold stances on political and social issues, including opposing discriminatory legislation, supporting climate action, and promoting inclusive hiring practices. These efforts have helped build a corporate culture rooted in purpose, attracting top talents who seek mission-driven work and investors who prioritize sustainability and governance.

The result is a company widely recognized for values-driven leadership. Salesforce consistently ranks high in ESG ratings and has earned accolades for its workplace culture, environmental initiatives, and social impact programs. Benioff’s model demonstrates that ethical capitalism is not only viable, but it can also be a competitive advantage. By aligning executive incentives with broader societal goals, Salesforce offers a blueprint for how modern corporations can lead with conscience while still delivering strong financial performance.

Lesson Learnt

Combining strong ethical rhetoric with measurable incentives enhances credibility and aligns leadership with broader societal trends.

These case studies reveal that incentivizing ethics is not one-size-fits-all. While some companies embed morality through mission and culture (Patagonia), others formalize it through ESG-linked pay (Danone and Unilever). Yet, without cultural buy-in and genuine accountability (Wells Fargo), ethical compensation can become symbolic rather than substantive.

The emerging consensus points toward hybrid models, where ethical leadership is nurtured through a blend of personal conviction, cultural reinforcement, and incentive alignment. As corporations navigate reputational risks and stakeholder demands, these models may become central to leadership design in the years ahead.

Balancing ESG Incentives with Ethics and Financial Performance

Concerns often arise that linking CEO compensation to ESG outcomes signals reduced attention to financial performance. Equally important is the perception that ethical leadership may be undervalued if incentives focus narrowly on measurable ESG metrics. To address these concerns, firms can adopt strategies that integrate ethical principles with both sustainability and financial priorities.

Integrated Ethical and ESG Metrics

Compensation systems can combine ESG indicators with measures of ethical conduct such as compliance with governance standards, fair treatment of stakeholders, and transparent decision-making. This ensures that ethical behavior is rewarded alongside sustainability and financial outcomes.

Balanced Scorecards with Ethical Dimensions

Boards can design scorecards that assign weight not only to ESG and financial metrics but also to ethical leadership indicators. Examples include fostering a culture of integrity, maintaining stakeholder trust, and avoiding reputational risks.

Long-Term Ethical and Financial Orientation

Ethical leadership contributes to long-term financial health by reducing risks of misconduct and enhancing stakeholder confidence. Linking incentives to both ESG outcomes and ethical behaviors reframes integrity as a driver of profitability and resilience.

Transparent Ethical Communication

Boards should disclose how ethical considerations are embedded in compensation systems. Clear communication demonstrates that ethical leadership is inseparable from ESG performance and financial accountability.

Governance Oversight of Ethics and ESG

Strong governance mechanisms can monitor ethical conduct alongside ESG and financial outcomes. This oversight reinforces the message that integrity is not optional but a core expectation of CEO performance.

By embedding ethics into ESG-linked incentives, firms can design compensation systems that balance integrity, sustainability, and profitability. This approach strengthens stakeholder trust while ensuring that ethical leadership remains central to corporate success.

Discussion and Analysis

The cases examined suggest several viable options for embedding ethical considerations into pay-for-performance systems. One approach is to link a portion of stock options or restricted stock units to ESG-based performance metrics, ensuring that long-term value creation incorporates environmental and social outcomes. Another option is to adopt merit pay systems to reward prosocial behaviors such as mentoring, stakeholder engagement, or community initiatives, thereby signaling that ethical conduct is valued alongside financial results. Profit sharing and gain sharing can also be structured to include ethical performance thresholds, ensuring that collective rewards are contingent on responsible practices. Finally, clawback provisions tied to ethical breaches provide a deterrent mechanism that reinforces accountability. Together, these examples illustrate how ethical incentives can be operationalized within familiar compensation structures, offering organizations practical pathways to balance integrity with performance.

The cases presented reveal a wide spectrum of approaches to incentivizing ethical behavior among CEOs, from Patagonia’s values-based culture to Danone’s formal ESG-linked pay and Wells Fargo’s failed reform attempt. This diversity reinforces a core insight: ethical leadership cannot be engineered through compensation alone; it requires a confluence of individual morality, institutional design, and stakeholder alignment. The challenge lies not simply in paying CEOs to be ethical but in designing a system that supports authenticity, accountability, and long-term integrity (Harward, 2022).

Drawing from agency theory, we see that pay structures significantly influence behavior. When ethical metrics are woven into compensation packages, as in Danone and Unilever, CEOs are more likely to make decisions that balance financial outcomes with social good. These arrangements shift the incentive landscape, nudging executives toward considering broader stakeholder interests. However, as observed in Danone’s leadership upheaval, tensions emerge when ethical priorities appear to undermine financial performance or conflict with shareholder expectations. This underscores a recurring critique: ethics-linked pay must be supported by governance structures that accommodate longer-term value creation rather than short-term gains.

While ethical incentives may face criticism for potentially undermining financial performance, it is important to distinguish between actual negative effects and perceived negative effects. The Danone case illustrates how perceptions of risk can generate strong stakeholder resistance, even when the long-term financial impact remains uncertain. Addressing these critiques requires both practical and theoretical strategies. Practically, organizations can design reward systems that balance ethical and financial metrics, thereby demonstrating that integrity and performance are not mutually exclusive. Theoretically, reframing ethical incentives as investments in trust, legitimacy, and sustainable value creation helps counter the narrative that they are purely costs. By making this distinction between perception and reality, firms can better manage stakeholder concerns and strengthen the legitimacy of responsible reward systems.

The behavioral ethics lens further explains why incentive design must go beyond numbers. Ethical blind spots, cognitive biases, and situational pressures often distort CEO judgment (Fasolo et al., 2024; Mandel et al., 2022). Wells Fargo’s post-scandal reforms attempted to install ethics-based performance criteria, but without cultural change, these efforts remained superficial. Employees continued to feel incentivized by performance metrics misaligned with ethical conduct, highlighting that compensation reforms alone cannot substitute for ethical leadership development, clear messaging, and psychological safety.

Theoretical tensions also arise when contrasting deontological ethics with utilitarianism (Chukwuneke & Ezenwugo, 2021). “Should morality be principled and self-directed, as Kantian ethics advocates, or can it be externally nudged toward desirable outcomes?” The case of Patagonia leans toward the former, where ethical behavior is embedded in purpose and values. In contrast, Salesforce and Unilever reflect a utilitarian outlook, leveraging incentives to produce ethically desirable outcomes across environmental, social, and governance dimensions. This juxtaposition prompts a reconsideration of whether ethical incentives are best viewed as reinforcements or replacements for moral conviction.

Moreover, feminist organizational theory adds critical nuance by emphasizing the relational and emotional dimensions of ethical leadership. Compensation metrics, while rational and quantifiable, often fail to capture qualities like empathy, inclusivity, and interpersonal accountability (Muss et al., 2025; Urbanska et al., 2019). This points to the need for human-centered metrics, perhaps 360-degree feedback mechanisms or stakeholder engagement indicators that reflect not just outcomes but processes and relationships. Without such measures, ethical incentives risk becoming performative or reductive.

An important takeaway across case studies is the effectiveness of hybrid models. Patagonia’s culture-driven ethics and Unilever’s formal ESG metrics are not mutually exclusive; in fact, when combined, they may produce more resilient and authentic leadership. Ethical compensation should not stand alone but be integrated with leadership training, board oversight, and transparent stakeholder dialogue (Perel, 2003). CEOs must operate within environments that encourage ethical reflection, invite dissent, and support values-aligned decision-making (Osei Bonsu et al., 2023; Pless et al., 2022).

Furthermore, companies must distinguish between ethics as compliance and ethics as culture. Financial incentives can drive surface-level behaviors such as checking boxes and submitting reports, but authentic ethics requires cultural transformation (Tenbrunsel & Messick, 2004). Boards and HR leaders should prioritize mechanisms that promote ethical learning and dialogue, such as mentorship programs, ethical dilemma workshops, or narrative-based evaluations. Ethics must be an ongoing conversation, not a quarterly metric.

Ultimately, the decision to pay CEOs to be ethical is not a simple yes or no proposition. It is about designing leadership systems that promote moral behavior intrinsically while reinforcing it extrinsically (Alhaidan, 2024; Ayoko, 2022; Brown & Treviño, 2006; Kaptein, 2008; Treviño et al., 2000). Compensation can play a vital role, especially when ethics are hard to measure or easy to sideline but it must be part of a constellation of tools (Brown & Treviño, 2006; Kaptein, 2008). Just as financial performance does not exist in isolation, neither does ethical integrity.

As business environments grow more complex and socially intertwined, the expectation for ethical leadership will only intensify. Organizations that treat ethics as a strategic asset, grounded in values, supported by incentives, and lived through culture, are more likely to weather reputational storms and deliver sustainable value (Alemu, 2025; Florea et al., 2013; Kaptein, 2008; Roy et al., 2024). Whether through pay, practice, or principle, the real question is not if CEOs should be ethical, but how ethics becomes inseparable from executive leadership itself.

Suggestions for Ethics-Based CEO Compensation Design

Ethics-based CEO compensation is increasingly recognized not as a trend but as a necessary evolution in leadership accountability (Al-Shaer & Zaman, 2019). As companies navigate global scrutiny and shifting stakeholder values, the way they reward top executives can either reinforce meaningful progress or undermine it. One effective approach is to develop a multi-dimensional ethics framework that goes beyond financial performance. Ethical leadership should encompass governance transparency, social responsibility, and environmental impact (AlHares, 2025; Parra da Silva & Saraiva, 2025). For example, Unilever under Paul Polman integrated sustainability goals into CEO evaluations, demonstrating how long-term purpose can be embedded into executive compensation. Research also shows that companies with sustainability committees and external assurance mechanisms are more likely to include ESG metrics in pay contracts (Al-Shaer & Zaman, 2019; Tumewang et al., 2025).

Blending intrinsic and extrinsic motivation is another key strategy. Ethical behavior is more sustainable when leaders are internally driven by purpose rather than solely by financial incentives (Boatright, 2010; Perel, 2003). A study by Deci and Ryan (1985) suggests that intrinsic motivation fosters long-term ethical behavior, while excessive reliance on extrinsic rewards can diminish it. Executive coaching and purpose-led mentoring, as explored by Athanasopoulou and Dopson (2015), have proven effective in cultivating ethical decision-making and leadership resilience. These programs might help CEOs align personal values with organizational goals, creating a culture where ethics are lived, not just rewarded.

Transparent and accountable metrics are essential to avoid vague benchmarks and build trust (Argyrous, 2012). Companies can use independently verifiable KPIs, external audits, and open disclosures to assess ethical performance. The Institute of Business Ethics recommends ethics oversight committees and benchmarking to monitor leadership behavior. Transparency not only improves internal confidence but also enhances public trust, especially when ethical goals are clearly communicated and externally validated (O’Neill, 2006).

Aligning incentives with stakeholder theory ensures that CEO compensation reflects broader societal impact (Nasta et al., 2024; Shabbir et al., 2024). This means integrating community engagement, employee well-being, and environmental outcomes into performance reviews. Firms like New Belgium Brewery, a certified B Corporation, tie executive rewards to social and environmental performance, demonstrating how stakeholder-oriented CSR can enhance both internal commitment and external reputation. Winkler et al. (2018) and O’Riordan (2021) support this approach, showing that stakeholder-focused strategies improve employee engagement and long-term value creation.

A long-term orientation in compensation structures helps prevent superficial compliance (Flammer & Bansal, 2017). Deferred equity and bonuses linked to sustained ethical achievements encourage deeper commitment to responsible leadership. A study conducted by Flammer and Bansal (2017) indicates that long-term incentives correlate with improved firm value and stakeholder trust. Companies adopting deferred share plans have reported stronger alignment with ethical goals and reduced risk of ESG greenwashing, reinforcing the importance of patience and persistence in ethical leadership (Chaigneau & Sahuguet, 2025; Winschel & Stawinoga, 2019).

Customization by industry is also crucial. Ethical benchmarks should reflect sector-specific challenges such as privacy in tech, labor rights in manufacturing, and diversity in service industries (Business for Social Responsibility, 2023; Dhirani et al., 2023; The Manufacturing Institute, 2023; UNEP Finance Initiative, 2023). IBM, for instance, integrates fairness and transparency into its AI governance, holding executives accountable for ethical innovation. Apple’s privacy-first approach similarly reflects tech-sector priorities, showing how tailored incentives can drive sector-relevant ethical outcomes.

Embedding ethics into governance structures institutionalizes accountability (Khamzina et al., 2025). Ethics committees or panels can regularly assess leadership behavior, ensuring that ethical goals remain central to executive decision-making. Johnson & Johnson’s crisis response and Puma’s transformation under Jochen Zeitz illustrate how governance-led ethical leadership can restore trust and drive cultural change. Research from Association of Certified Anti-Money Laundering Specialists (ACAMLS) and International Compliance Training Network (ICTN) supports the role of governance in fostering ethical integrity across organizations (ACAMS & ICTN, 2023).

Finally, fostering stakeholder dialogue and feedback transforms ethical measurement into a shared conversation (Cashore et al., 2019). Surveys, town halls, and community forums allow stakeholders to voice concerns and influence leadership evaluations. Tools like CommunityClick enable real-time feedback, enhancing transparency and inclusivity. Studies by the Urban Institute show that community-engaged surveys improve trust and legitimacy in leadership decisions, making ethics a participatory process rather than a top-down declaration (Urban Institute, 2021).

Together, these strategies shift CEO compensation from a reward for performance to a recognition of responsible power. Ethical incentives can motivate leaders to act with courage, transparency, and care— qualities that define not just effective executives but transformative ones (Caldwell et al., 2012).

Managerial and Policy Implications

As corporations grapple with evolving expectations around leadership accountability and ethical governance, the topic of this paper— “incentivizing CEOs to act ethically,” carries significant implications for both management practices and public policy.

Managerially, firms must adopt a proactive stance in embedding ethics into executive evaluation systems. This involves developing robust, multidimensional performance indicators that go beyond traditional financial metrics. Managers and boards should integrate ethical KPIs, such as stakeholder engagement quality, ESG compliance, diversity and inclusion efforts, and community impact into compensation structures. These metrics need to be transparent, independently verifiable, and context-sensitive. Moreover, leadership development programs must emphasize moral reasoning, relational accountability, and ethical decision-making. Ethics should not be treated as a reactive mechanism post-crisis, but as a strategic pillar guiding everyday choices. Executive dashboards and regular ethics reviews can promote a culture of reflection, reinforcement, and improvement.

Companies also need to balance short-term results with long-term ethical objectives. This requires rethinking pay models to include deferred incentives, long-term impact assessments, and dynamic feedback loops. Managers must be wary of tokenistic reforms that may breed skepticism or box-ticking behaviors. Ethical compensation is most effective when embedded within a broader ethical culture, one supported by governance, employee voice, and clear consequence management (McCabe, 2019; Xia et al., 2023).

From a policy perspective, governments and regulatory bodies can play a vital role in standardizing ethical compensation frameworks. Mandating disclosure of ethics-linked pay components in executive remuneration reports would promote transparency and comparative accountability across industries (Siwendu & Ambe, 2024). Regulators may also define minimum ethical criteria, for example, anti-corruption measures, supply chain fairness, and environmental stewardship that must be included in CEO performance evaluations. Such standards help level the playing field and signal seriousness about corporate responsibility.

Furthermore, policy initiatives could incentivize ethical compensation through tax breaks, ESG certifications, or public procurement advantages for companies with verified ethical pay practices. Cross-border collaboration and shared ethical governance principles (such as via the UN Global Compact or OECD guidelines) can prevent regulatory arbitrage and harmonize expectations in global firms (Rasche, 2021).

Together, these managerial and policy shifts might encourage a new paradigm where ethical behavior is not merely expected but systematically supported. By designing compensation systems that reward principled leadership, organizations and governments can co-create a more accountable, resilient, and values-driven business ecosystem (Groysberg et al., 2021).

Conclusion

Linking CEO compensation to ethical behavior is more than a corporate trend, it is a transformative shift in how leadership is understood, measured, and rewarded. By aligning financial incentives with moral accountability, companies signal a commitment to long-term sustainability, stakeholder well-being, and responsible governance. Such compensation models not only promote ethical conduct at the executive level but also set a powerful tone across the organization, reinforcing a culture where values matter as much as results. The managerial implications of this shift are profound. It requires boards and senior leaders to redesign performance metrics, prioritize transparency, and build mechanisms that recognize ethical excellence alongside financial success. Ethical KPIs, long-term incentives, and internal feedback loops all serve to institutionalize integrity within corporate strategy.

On the policy front, governments and regulators have an essential role in guiding and supporting this evolution. By establishing disclosure requirements, defining ethical standards, and offering incentives for compliance, public institutions can foster a more consistent and equitable framework for ethical pay across industries. International collaboration may further enhance impact, ensuring that global firms uphold these principles regardless of where they operate.

Ultimately, tying CEO pay to ethical outcomes is not a complete remedy, but it is a powerful lever. It can reshape the narrative of executive leadership from one of individual gain to one of collective stewardship. When done thoughtfully, it can build trust, drive authentic engagement, and help businesses navigate complex societal expectations. In a time when integrity is increasingly linked to corporate success, this approach offers a compelling blueprint for purpose-driven leadership.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.