Abstract

Nowadays, more fashion companies have started to adopt various sustainability practices and communicate these practices through their annual public CSR reports. In this study, we aim to provide a holistic perspective of fashion companies’ sustainable development and investigate the sustainability practices of global fashion companies. A total of 181 CSR reports from 29 fashion companies were collected. A Dictionary approach text classification method, combined with Latent Dirichlet Allocation (LDA), a computer-assisted topic modeling algorithm, was implemented to detect and summarize the themes and keywords of detailed practices disclosed in CSR reports. The findings identified 12 main sustainability practices themes based on the triple bottom line theory and the moral responsibility of corporate sustainability theory. In general, waste management and human rights are the most frequently mentioned themes. The findings also suggest that global fashion companies adopted different sustainability strategies based on their product categories and competitive advantages.

Keywords

As a huge, multi-trillion-dollar global industry, fashion has the potential to make an enormous positive impact on the world (Fung et al., 2020). However, it is also one of the most polluting industries in the world, contributing to a variety of environmental and ethical issues. From raw material production and processing to the manufacture and supply of goods, sustainability issues are prevalent throughout the entire fashion supply chain. Intensive use of chemicals, water, energy, and undegradable fabrics leads to problems such as the rapid increase in damaging plastic microfibers, hazardous ingredients pollution, and large amounts of waste. Violation of wage laws, child labor, labor abuse, forced overtime, harassment, hostile working environments, and unguaranteed safety and health directly affect the people involved in this industry (Rudell, 2006). Increasingly, fashion customers are prioritizing ethics when it comes to their shopping choices. Stakeholders are also demanding greater transparency from fashion companies about their operations, particularly their supply chains. The fashion industry must wake up and recognize that business-as-usual cannot go on much longer (Fung et al., 2020).

As a result of new demands by customers, many fashion companies have started to adopt various sustainability practices and communicate their efforts and improvements to the public through different communication platforms such as social media, newspapers, and public service advertisements (Reilly & Larya, 2018). Many fashion companies have begun to oversee their suppliers more closely, set codes of conduct, audit and measure the suppliers’ sustainability performance (Jia et al., 2015), and publish corporate social responsibility (CSR) reports to convey their sustainability practices in detail (Kozlowski et al., 2015; Reilly & Larya, 2018). This effort helps stakeholders make informed decisions about the companies they buy from, work for, engage with, and invest in through more systematic, transparent, official, and publicly available information with accurate and insightful data. CSR reports have become an important information resource for the public and stakeholders, including consumers, media, nonprofit organizations, workers, and investors, to watch and monitor the sustainability practices of fashion companies (Kozlowski et al., 2015; Reilly & Larya, 2018).

Even though CSR reports provide rich and valuable insights to the public, it is hard to discover hidden patterns and specific key information across various companies and multi-year reports. Previous studies have used content analysis to explore sustainability indicators disclosed in CSR reports from different industry sectors (Kozlowski et al., 2015; Roca & Searcy, 2012). In the fashion field, researchers also utilized CSR reports as an important data source to investigate sustainability practices. For example, Yang and Ha-Brookshire (2019) analyzed 86 sustainability reports from top performing textile and apparel companies in China to explore their sustainability performance. Jestratijevic et al. (2020) analyzed the transparency levels of 100 fashion brands by exploring the Fashion Transparency Index (FTI) 2017 scores, which is a comprehensive index that includes the transparency levels of both corporations and supply chains. However, to our knowledge, no systematic approach has been established to extract and classify information regarding the detailed sustainability practices of fashion companies. In addition, it is challenging to compare the specific efforts toward sustainability across different fashion companies due to the difficulties in identifying target information from multi-year CSR reports.

Grounded in the triple bottom line (TBL) theory (Elkington, 1998) and moral responsibility of corporate sustainability (MRCS) theory (Ha-Brookshire, 2017), we employed a text mining approach to extract text data from CSR reports and identify latent themes related to sustainability in fashion. With the advent of modern cognitive computing technologies, we aimed to (1) provide a holistic perspective of fashion companies’ sustainable development, (2) build a sustainability dictionary that can be used in the fashion industry, (3) detect and summarize the major sustainability practices of global fashion companies, and (4) compare different emphases and paths of fashion companies to achieve sustainability goals. To the best of our knowledge, we are among the firsts to establish such a dictionary, which covers the most prevalently used sustainability practice themes and keywords in the fashion field, and which could be further developed by feeding new data sets.

Literature Review

Sustainability and CSR Communication in the Fashion Industry

The use of reporting as a means of communicating a corporation’s sustainability actions and initiatives has been growing. Despite the difficulties and inconsistencies surrounding CSR reporting, it has been found to improve the competitive advantage of an organization, as it contributes to building and maintaining a strong reputation (Reilly & Larya, 2018). CSR communication by top corporate leadership reinforces a company’s strategic commitment to sustainability actions. It provides a window to stakeholders and the public through which to understand the culture of an organization and to make sense of that organization’s way of managing its communication processes and information outcomes (Reilly & Larya, 2018). In the fashion field, Hazel and Kang (2018) demonstrated the importance of perceived CSR information to build brand trustworthiness and brand likability.

CSR communication may vary across companies in terms of communication channels, formats, content, and frequency. Most large global companies have recognized the importance of formal CSR communication and regularly provide some form of sustainability data to their stakeholders. Many firms publish separate CSR documents; others provide this information as part of their annual 10-K submissions (Center for Sustainability and Excellence, 2018). In addition, a variety of names have been adopted in reference to this type of reporting: “sustainability,” “accountability,” “sustainable development,” “corporate social responsibility,” “corporate responsibility,” and “triple bottom line” reports (Roca & Searcy, 2012). In this study, we use “CSR report” to cover all of these terms. In the United States, the Securities and Exchange Commission (SEC) requires Publicly Listed Companies (PLC) to submit their CSR reports on a “comply or explain” basis for the first three years. Based on the reporting guideline from SEC, PLCs need to disclose their non-financial performance across economic, environmental, and social aspects (SEC, 2019). Corporate participation in the Global Reporting Initiative (GRI), the most widely accepted third party assessment, is voluntary (CSE, 2018; Reilly & Larya, 2018). In general, CSR reports have been considered an incredibly effective and insightful information source for stakeholders. However, CSR reports often contain a huge amount of complex information with terminology that is difficult for stakeholders to quickly search in an effort to identify key information.

In the fashion industry, companies publish CSR reports with different foci depending on the main product category, stages of growth, market segments, etc. For example, luxury companies (e.g., Kering and LVMH) and fast-fashion companies (e.g., H&M and Inditex) may initiate and execute various strategies to approach sustainability based on their diverse experiences, the company’s past and present efforts, their business strategies, and their commitments (Amed et al., 2018). Jestratijevic et al. (2020) pointed out that the transparency of supply chain disclosure among mass-market brands is higher than luxury brands. Thus, companies communicate with stakeholders using an assortment of information in their CSR reports (Goswami & Ha-Brookshire, 2015). Meanwhile, diverse groups of stakeholders, such as customers, clients, employees, and those with environmental concerns, may demand specific information or communication approaches from CSR reports. Investors may link CSR reports to financial performance, while customers may care more about product safety measures, marketing policies, and data privacy issues. Employees utilize CSR reports to understand their company’s culture and values and to feed their pride and motivation to work for a “good” company. With this being said, it is not always easy for diverse groups of stakeholders to distinguish and extract their target information from the massive documents, which may decrease communication efficiency.

Most research has focused on the CSR reports’ quality assessment (Wolniak & Hąbek, 2016), credibility, and trustworthiness (Lock & Seele, 2016). In the fashion field, for example, Yang and Ha-Brookshire (2019) analyzed CSR reports among top textile and apparel companies in China and explored whether companies perceived sustainability as a perfect duty or not based on their disclosed CSR information. Some researchers have begun to analyze CSR reports using quantitative analysis. Jestratijevic et al. (2020) explored the transparency status of fashion brands by quantifying the transparency scores of the sustainability disclosures. Although previous studies (Jestratijevic et al., 2020; Yang & Ha-Brookshire, 2019) have evaluated and ranked individual companies’ CSR efforts, there is still a gap in the literature to find an approach to identify the detailed CSR actions adopted by fashion companies and quantify CSR data for in-depth analysis from CSR reports.

Theoretical Framework

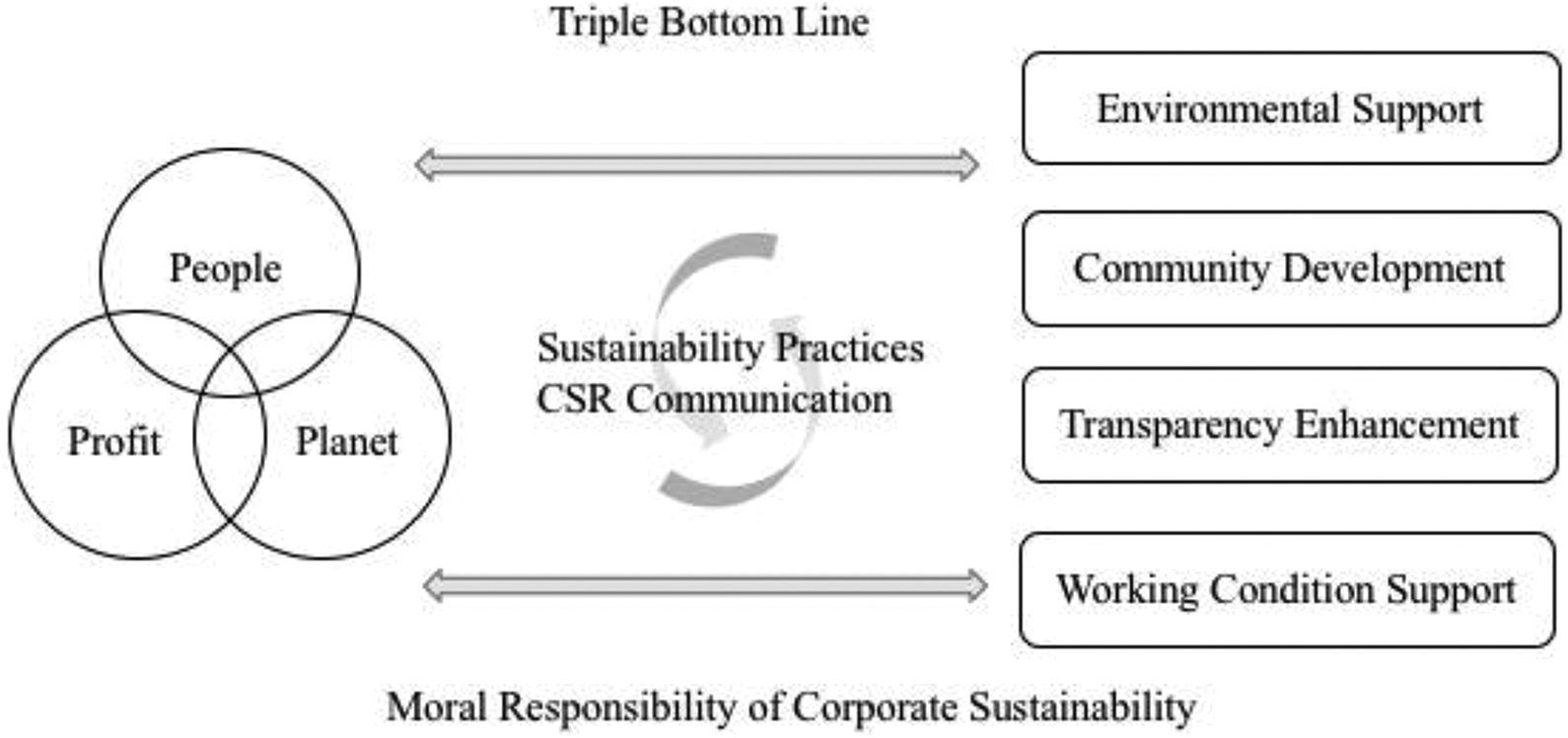

To better extract valuable information from CSR reports in an effort to understand the sustainability practices and motivations adopted by fashion companies, this research combines the triple bottom line theory and moral responsibility theory to guide the data analysis. Triple bottom line (TBL), first proposed by Elkington (1998), shifts the focus of a business so that it is not just centered on profits but on generating profits in a way that is better for both people and the planet. This triple bottom line of people, planet, and profit considers the social and environmental impacts of a business in its pursuit of profits. An increasing number of researchers have studied the sustainability assessment model and performance indicators to evaluate sustainability levels in various fields by adopting TBL (Hadjikakou et al., 2019; Lim & Biswas, 2018). For example, TBL provides sustainability criteria for water supply options to meet environmental, social, and economic requirements (Hadjikakou et al., 2019). Lim and Biswas (2018) developed the Key Performance Indicator to implement a sustainability assessment framework in the palm oil industry. In the fashion field, researchers adopted TBL theory to analyze the key factors in achieving sustainable fashion in product development (Fung et al., 2020). Jia et al. (2015) investigated the optimal supplier selection problem for sustainable materials supply in fashion clothing production and framed criteria to evaluate suppliers based on TBL dimensions. Through examining the correlation between performance indicators and TBL dimensions, Govindan et al. (2016) highlighted the importance of balance between financial, environmental, and social dimensions.

In addition, TBL theory has been widely utilized in investigating sustainability activities through annual CSR reports. Raar (2002) investigated environmental disclosures and explored environmental initiatives and practices from annual reports of firms. The result showed a trend of triple-bottom reporting with an increasing tendency of quantity and quality of environmental information in reports. Ho and Taylor (2007) investigated public disclosures and developed 20 disclosure criteria for each of the TBL dimensions. These criteria include: a companies’ use of waterless dyeing, efforts to increase the use of renewable energy sources, improving employees’ health and safety, reducing child labor, eliminating discrimination, etc. Almost all specific practices included in CSR reports could be classified through TBL dimensions and demonstrate fashion companies’ efforts to achieve sustainability. Therefore, TBL theory can be effectively used to extract the themes of companies’ detailed sustainability practices from CSR reports.

It is clear from both the UN’s and Elkington’s concept that the growth of financial stability is not sustainable unless it attends to social responsibility and environmental protection. However, due to today’s highly fragmented and intertwined global business economy, corporations and their suppliers may attach different levels of importance to sustainability performance, and it is difficult for corporations to oversee all the suppliers’ activities and ensure the whole supply chain is truly sustainable.

According to the moral responsibility of corporate sustainability theory, corporate sustainability performance can be determined by three factors: (1) whether the corporate members see sustainability as a perfect or an imperfect duty, (2) whether they have clear goals for sustainability, and (3) whether well-defined corporate structures are in place to achieve the goals (Ha-Brookshire, 2017). Corporations that perceive sustainability as a perfect duty will perform sustainability in all situations, while corporations that perceive sustainability as an imperfect duty will decide how to fulfill it in only certain circumstances, leading to arbitrary sustainability-related behaviors. Furthermore, clear goals and well-defined corporate structures help to keep employees and their corporations consistent in their understanding and actions toward sustainability. Depending on performance in the three factors, the spectrum of corporate sustainability behaviors ranges from truly sustainable, to occasionally unsustainable, and to occasionally sustainable in all or selected circumstances. The fundamental idea of MRCS posits that depending on the levels of moral responsibility, companies may attach different levels of importance to corporate sustainability, have varied performances in the three factors, and pursue different phases of corporate sustainability goals (Ha-Brookshire, 2017).

According to the MRCS theory, the four duties of corporate moral responsibility are categorized as environmental support, community development, working condition support, and transparency enhancement (Jung & Ha-Brookshire, 2017). Environmental support consists of preserving nature, making active efforts to improve the environment and designing eco-friendly products. Community development includes educational and medical support for the community, such as helping to improve the lives of the socially disadvantaged through partnerships with other supporting organizations who help people in need. Working condition support addresses caring for the working environment and workers’ fair treatment. Transparency enhancement is associated with disclosing information publicly and having certifications through regular audits by third-party organizations that multiple stakeholders are able to monitor. Jung and Ha-Brookshire (2017) analyzed the importance of these four duties from consumers’ perspectives. The results showed that consumers perceived environmental support and working condition support as perfect duties, while they perceived community development and transparency enhancement as imperfect duties. This morality spectrum helps companies to have a clear understanding of consumers’ expectations with regard to the duties of corporate moral responsibility. Companies need to place more weight on the perfect duties rather than imperfect duties and thus need to convey more information related to environmental support and working condition support in an effort to meet the expectations of consumers.

MRCS theory is brought into this research to help interpret the sustainability communication of fashion companies, as well as their practices and development with regard to the four duties of corporate moral responsibility. Analyzing CSR reports can be very challenging and time-consuming due to the large amount of unstructured documentation. A new computer-assisted text analysis method is needed, which is discussed in the following section. Overall, to achieve the goals of this research, we use a theoretical framework as shown in Figure 1.

Theoretical framework.

CSR Reports and Text Mining

Research has been done to investigate CSR reports in various ways. Content analysis based on both human and computer-assisted techniques has been widely used to code and analyze qualitative data (Campopiano & De Massis, 2015; Lock & Seele, 2016). Recently, text mining has been recognized as a novel approach to quickly analyze trends and patterns in sustainability reporting and identify which aspects are the most disclosed in reports (Liew et al., 2014; Liu et al., 2017). Text mining is “the discovery by computer of new, previously unknown information, by automatically extracting information from different written resources” (Hearst, 2003). This can also be in alignment with exploratory data analysis. Unlike content analysis, which is used to (re-)construct a “reality” based on the interpretations of a text made by researchers, text mining is rooted in the positivist research philosophy of “hard science” and seeks universal generalizations using quantified measures (Rynes & Gephart, 2004). In addition, text mining uses natural language processing (NLP) to uncover patterns and provide predictive information based on a more sophisticated understanding of language. As a subfield of artificial intelligence and computational linguistics, NLP focuses on the automatic analysis of human language with use of algorithms that can handle complex structures (Nadkarni et al., 2011). Text mining employs NLP to analyze the data as though a human coder reads the text. Text mining could help improve not only the ability to analyze large-scale, complex data sets but could also improve the reliability, reproducibility, and flexibility of analysis (Lang et al., 2020). It ensures a baseline of consistency across results and offers an objective measure of accuracy. It also has the potential to be optimized by feeding in more data. Considering this, our study introduces text mining to accurately and efficiently retrieve, manage, and interpret CSR reports.

A few studies have explored the application of text-mining in interpreting CSR reports. For example, Liu et al. (2017) conducted text mining to determine the benchmark of the environmental performance indicators by extracting distinctive terms from CSR reports. However, their study focused on the petrochemical industry and only showed distinctive terms such as “dyeing,” “energy,” and “impact” instead of more detailed practices such as “waterless dyeing,” or “efficient energy.” Liew et al. (2014) analyzed and compared the CSR reports of the chemical process industry to identify major issues as well as the companies’ priorities regarding sustainability. However, these studies all focus on counting term frequencies but do not perform detailed conceptual-level analysis. In addition, most researchers who have applied a text mining approach to analyze CSR reports have done so from a computer science perspective. There is a lack of research focusing on CSR practices in the fashion industry by simultaneously adopting a text mining approach and bringing in a theoretical understanding. With the given theoretical framework, the desired text mining method could be applied to identify and classify CSR topics in fashion on a detailed, conceptual level, and, in turn, help researchers and stakeholders understand the document intuitively.

In natural language processing, Latent Dirichlet Allocation (LDA) is one of the most widely used topic modeling algorithms and has been frequently used to extract and identify topics from documents (Blei et al., 2003). LDA is a powerful tool to discover and exploit the hidden thematic structure in large archives of texts and works well on various types of documents (Blei et al., 2003). Researchers have used LDA for various purposes from summarizing and clustering legal judgements through semi-structured legal documents (Kumar & Raghuveer, 2012) to measuring similarities between diseases through free text descriptions (Frick et al., 2015). It has also been utilized in CSR reports studies. Benites-Lazaro et al. (2018) identified 36 main themes that demonstrate the rule-setting power of the ethanol industry by using LDA algorithms to analyze a large volume of CSR reports.

A dictionary-based approach is a straightforward approach to classifying themes. Researchers develop a dictionary, which is a list of keywords that correspond to topics or themes that they wish to identify in the text. The computer then scans the documents for the presence of these keywords. If a word from the dictionary is present, the computer annotates the document as containing the topic or theme (Cho et al., 2014). A dictionary-based approach, also known as a lexicon-based approach, is used prevalently in sentiment analysis. For example, sentiment analysis of product reviews is used (Cho et al., 2014) to identify the positive/negative attitudes of consumers toward the products. In biomedical fields, researchers built a professional biomedical concept dictionary and then used a dictionary-based approach to identify the related concepts from a large amount of literature to save searching time and increase text classification efficiency (Gong et al., 2017). However, to the best of our knowledge, there are no dictionaries developed focusing on sustainability keywords and themes in fashion. In this study, an initial dictionary was built to fill this gap and increase future research efficiency in the fashion sustainability field. This dictionary could be further developed by feeding in more raw text data with the new occurrences of concepts and themes in fashion sustainability, thus always adequately reflecting the entire large data set.

Research Methods

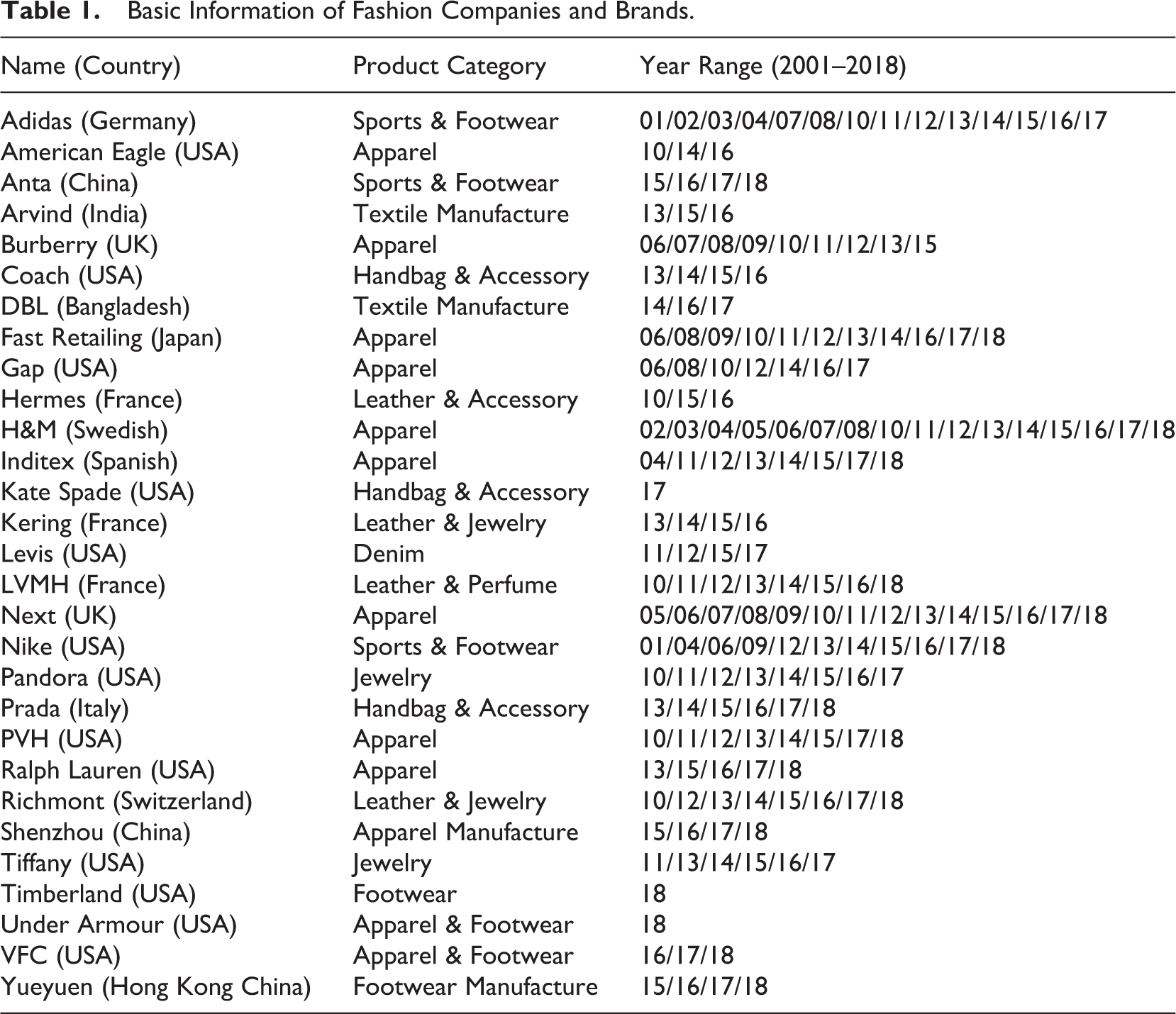

To achieve our research goal, we first chose 24 fashion companies that have the largest market capitalization and have published their CSR reports (Fashion United, 2018). Since all these companies are headquartered in developed countries, we then chose five fashion companies from three developing countries that also have high market capitalization in an effort to diversify our data set. We collected all of the published CSR reports from 2001 to 2018 from these companies. The specific years of reports from each company are listed in Table 1. Finally, we collected 163 CSR reports from 24 top fashion companies in developed countries and 18 CSR reports from five fashion companies in developing countries. The total data set consisted of 6,725 pages. All the names and types of fashion companies are also listed in Table 1. Most companies in developing countries focus on manufacturing, while fashion companies from developed countries emphasize retailing or wholesaling. Product categories range from textile and apparel to accessories, from luxury brands to mass market brands.

Basic Information of Fashion Companies and Brands.

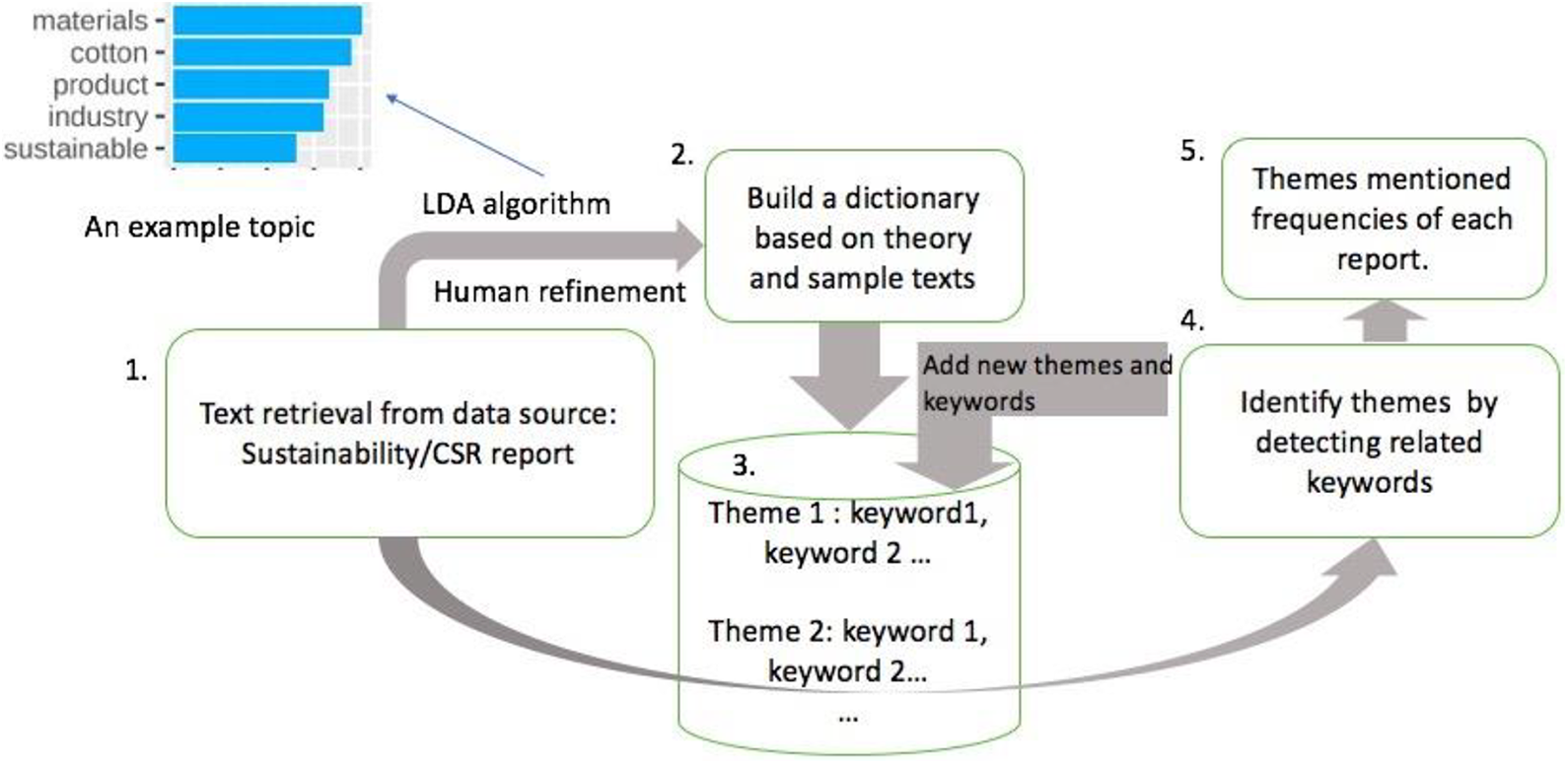

To improve the accuracy and efficiency of text analysis, we selected a small sample of data to establish the initial themes and associated keywords to be used for analysis of the whole data set. LDA was used first to extract the topics from a small initial data sample. After human refinements, the fashion sustainability dictionary was established. Then, the dictionary-approach classification was brought in to classify themes and keywords from a large data set. The whole method flow is shown in Figure 2. Following is the detailed text mining process and human refinements steps.

Research method flowchart.

The first step involves both machine-based pattern recognition and adjustments/refinement from human coders. To make it clearer, we use “topic” to refer to the results of machine identification, and we use “theme” to refer to the refinement result of human coders. After data collection, 200 pages of CSR reports were randomly selected from the 6,725 pages and used for the first round of theme-generating in R programming with the LDA algorithm implemented. These 200 pages of reports were gathered from a mix of companies and a mix of sections in an effort to cover the themes as thoroughly as possible. LDA algorithms consider each document being represented as a random mixture of latent topics, whereas each topic is characterized by a probability distribution of words over a vocabulary (Blei et al., 2003). Based on LDA, the computer can generate topics automatically by displaying the most important words in these topics. In this research, the computer was set to show the five most important words for each topic. An example topic that the computer generated is shown in Figure 2, which is comprised of five words: “materials,” “cotton,” “product,” “industry,” and “sustainable.”

Next, after extracting the topics from a sample data set by LDA, three human coders—either Ph.D. students or faculty members majoring in fashion—were chosen to assist with this study. All of them have had experiences conducting fashion sustainability-related research. They all read sample reports and learned the basic concept of text mining. Human coders reviewed and refined key topics to improve the accuracy and reliability, guided by TBL and MRCS. For example, the theme “sustainable material” emerged from the example topic in Figure 2, and since the words “product” and “industry” were too broad and not necessarily related to sustainable material, researchers selected “sustainable cotton” and “sustainable materials” as the associated keywords. Researchers then combined similar themes and their keywords and deleted some themes that were too broad, such as “sustainability approach” and “management issue.” In the second and third rounds of auto theme-generating, more pages were randomly selected and analyzed by computer and human coders until there were no new themes or keywords emerging. In total, 300 pages of data were analyzed in the theme-generating process. The themes and keywords extracted from theme generating made up a dictionary. As mentioned previously, this dictionary can be kept updated by feeding it more themes and keywords to make sure it always adequately reflects the entire data set.

Then, using Python, all the collected historical text data of each company was detected sentence by sentence based on the dictionary developed in previous steps. Each time a keyword was detected, the related theme was considered mentioned in that sentence. The proportions of themes of each company that were mentioned in their reports were calculated and compared to investigate the sustainability practices performed by each fashion company.

Results and Discussions

Fashion Sustainability Dictionary

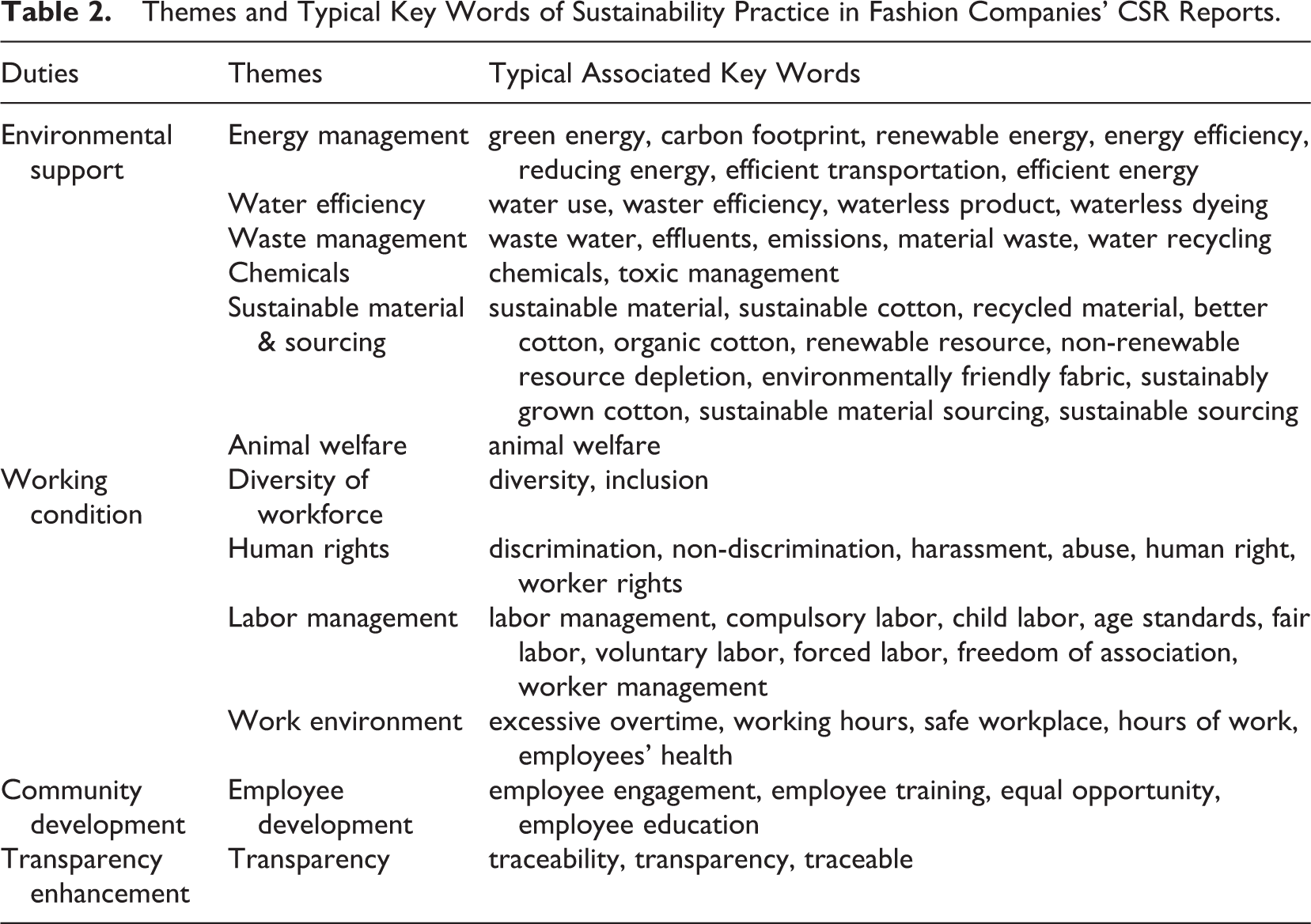

In total, 12 sustainability practice themes and 59 associated keywords are identified in Table 2. This result covers the most important and frequently mentioned sustainability practice themes and keywords. These themes and keywords revealed that fashion companies tend to emphasize two major aspects when communicating with their stakeholders: an environmental aspect and a social aspect, which are two important dimensions in TBL theory. Since companies address financial issues in their financial reports, there are few finance-related keywords appearing in LDA results, thus no major themes regarding financial performance emerged.

Themes and Typical Key Words of Sustainability Practice in Fashion Companies’ CSR Reports.

Sustainability Practices and Development

From an environmental perspective, sustainability practices adopted by top fashion companies mainly focus on optimizing energy management, increasing water efficiency, improving waste treatment and management, choosing sustainable sourcing, and ensuring the welfare of animals. Detailed practices related to major topics were revealed by associated words. CSR reports mentioned that top fashion companies not only urge manufacturing factories to adopt renewable energy, but also search for efficient transportation to reduce energy consumption. Since fashion production processes utilize enormous quantities of water, some fashion companies also pay attention to raising water efficiency by employing practices like waterless dyeing. Waste management is also an important part of sustainability for fashion companies. Fashion brands adopt practices such as reducing emissions and effluents, improving waste treatments, and recycling. In addition, eco-friendly material and sustainable sourcing is a fundamental part of the sustainable fashion industry (De Brito et al., 2008). Organic fabrics are produced using less water and fewer harmful chemicals, and innovative fabrics make it possible to use digital printing and non-toxic dyeing and to reduce environmental impacts in the subsequent processes (Kozlowski et al., 2012).

From a social perspective, the keywords of “human rights” show that fashion companies adopt practices to prevent the occurrences of harassment, abuse, and discrimination. More than half of the fashion companies also mentioned that it was important to keep their teams diverse and inclusive to develop thoughtful and original ideas. The sustainability practices adopted in labor management include reducing the incidents of child labor, forced labor, and compulsory labor. To maintain a positive workplace, fashion companies take care to keep employees safe and healthy, adjusting working hours to help employees achieve a better work-life balance. To address community development, some companies provide various training programs and guarantee equal opportunities for employees’ development. Fashion companies also pay attention to transparency in an effort to improve the traceability of their supply chain.

All the themes in Table 2 were categorized into the four important duties from MRCS theory: environmental support, working condition, community development, and transparency enhancement. Environmental sustainability practices are reflected by six themes and social practices are reflected by another six themes (one theme for community development, one theme for transparency, and four themes for working conditions). From the research of Jung and Ha-Brookshire (2017), consumers perceived working conditions and environmental support activities to be the most important corporate duties, followed by community development and transparency enhancement activities. In this research, most themes mentioned heavily in CSR reports fall under the categories of environmental support and working conditions. Practices regarding community development and transparency were also mentioned, but the themes that emerged in these two categories are fewer than the former two. The frequency of themes reveals the importance spectrum in corporations’ CSR reports, which is consistent with the importance spectrum from consumers’ views (Jung & Ha-Brookshire, 2017).

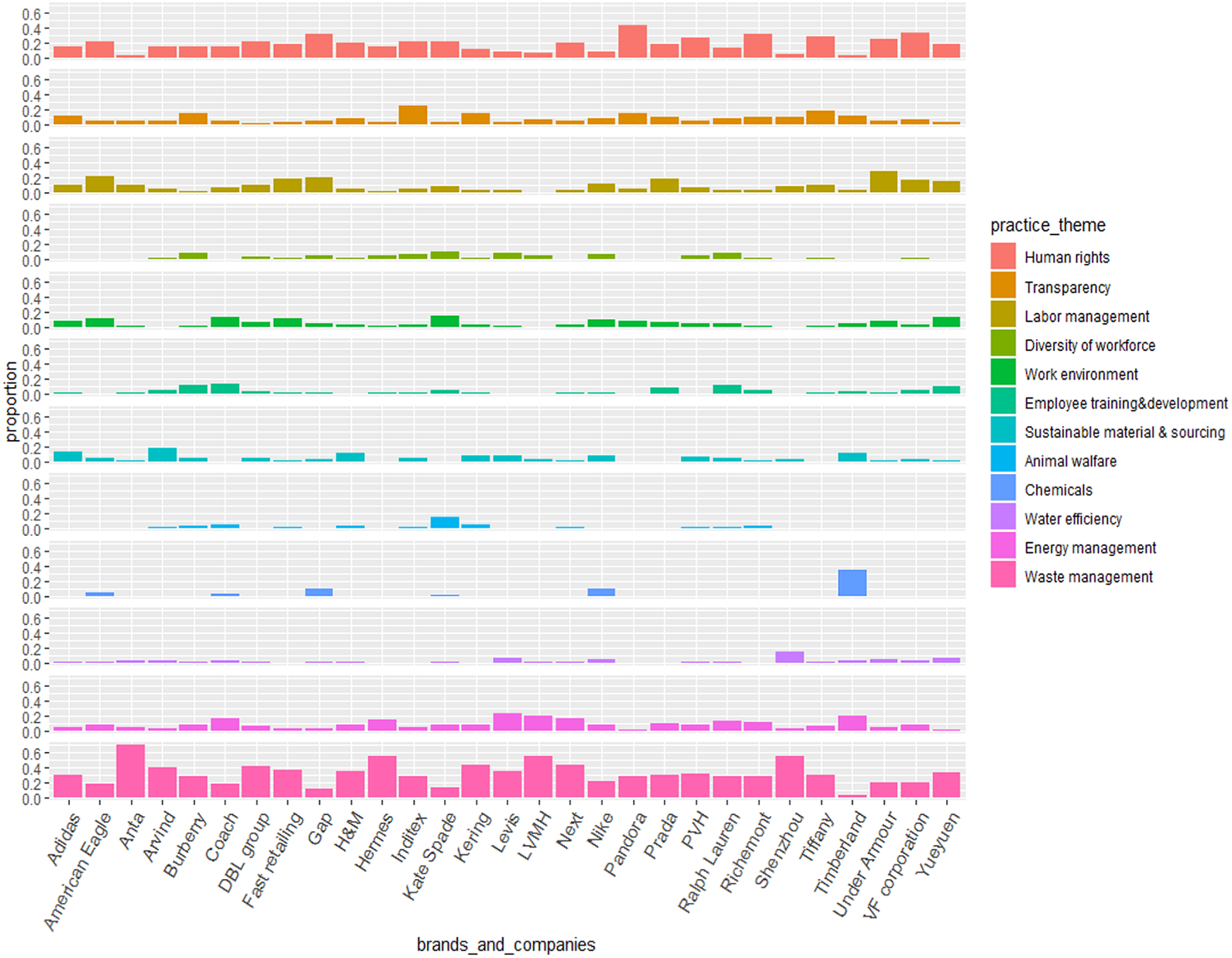

Figure 3 shows the sustainability practice proportions among these fashion companies. Overall, waste management and human rights are the top two most heavily mentioned themes in fashion companies’ CSR reports. The results demonstrate that companies have varying priorities regarding CSR practices. The practices related to corporate transparency, such as waste management, energy management, and diversity were prioritized over issues related to supply chain transparency, such as child/forced labor and working hours (Jestratijevic et al., 2020). Meanwhile, information on governing bodies and policies were more visible than supply chain information. Since waste management is one of the most touted policies in the headquarter-located countries, fashion companies have put much effort into reducing wastewater and waste material (Jestratijevic et al., 2020) and communicating waste management procedures. In regard to the social aspects, the fashion industry, which predominantly employs women as workers, witnesses a range of labor abuses, from discrimination to sexual harassment. Therefore, global fashion companies all have a responsibility to ensure human rights through their supply chain and tend to convey the messages by their reports, such as the prohibition of harassment, elimination of abuse, and improvement of non-discrimination.

Sustainability practice proportions of fashion companies and brands.

Comparison of Fashion Companies’ Sustainability Emphases

Figure 3 indicates that fashion companies within the same product categories, such as footwear companies and apparel companies, tend to adopt similar sustainability practices. The common visions of most footwear companies include improving creativity and innovation. Since it takes 30–40 years for a pair of sneakers to fully decompose in landfills, Adidas, Nike, and Timberland all address sustainable materials by adopting advanced technologies to develop novel materials and use recycled materials. Most apparel companies commit themselves to building a healthier community. To benefit more people and build brand image, American Eagle, Gap, and Fast retailing pay attention to labor management. Kate Spade and Coach address animal welfare since they are known as handbag brands that claim to be fur-free.

Figure 3 also reveals the least mentioned themes of each fashion company. For example, it is a surprise to see that Hermes, famous for their leather products, does not disclose any information regarding animal welfare and sustainable material sourcing, while other leather companies demonstrate their kindness to animals. Shenzhou and LVMH miss the information on work environment and employee development, which indicates that these two companies ignore sustainability in the social realm. It is noted that 11 of 29 fashion companies do not mention diversity of the workforce. Yueyuen, Anta, and Shenzhou are headquartered in a mono-ethnic state, China; Adidas and Next are headquartered in nation-states, Germany and England, respectively. These companies may adopt less practices to increase racial diversity and religious diversity than the companies headquartered in multi-ethnic countries.

Even though some fashion companies adopt the same sustainability practices, the mentioned proportions are different, meaning they emphasize detailed sustainability practices differently and have different priorities in terms of achieving sustainability. For example, Levi’s emphasizes water efficiency and waste management because of the large amount of wastewater involved in the dyeing process in the denim jeans industry compared with other companies. Instead of using innovative materials and recycled materials like Nike and Adidas, Anta places the most importance on waste management and energy efficiency to show their effort at environmental protection. Anta is listed on the Hong Kong Stock Exchange, which published the “Environmental, Social and Governance Reporting Guide.” This guide encourages companies to disclose their policies regarding air and greenhouse gas emissions and management of hazardous and non-hazardous wastes. Under Amour also values improving human rights and labor management. They make efforts to protect our planet by showing respect to the people who make their products.

Conclusions

While many researchers have explored and assessed the credibility and quality of CSR reports from different sectors (Lock & Seele, 2016; Wolniak & Hąbek, 2016), this is the first time a computer-assisted text analysis approach has been applied to establish a sustainability dictionary in fashion and explore the detailed sustainability practices adopted by global fashion companies through their public CSR disclosures. The findings identify 12 main sustainability practice themes based on the TBL theory and MRCS theory that global fashion companies communicated most in their reports and suggested that global fashion companies implement different sustainability strategies based on their product categories and competitive advantages.

In general, waste management and human right were the most heavily mentioned themes in fashion CSR reports. Companies from developing countries, such as Anta and Shenzhou from China, place more weight on waste management than those from developed countries. In terms of priorities, footwear companies focus more on environmentally friendly strategies. Nike disclosed little about ethical sustainability and were more concerned about waste management and sustainable sourcing, and Timberland revealed many practices regarding chemicals and energy management, while apparel companies report more about the progress of their social and ethical efforts. American Eagle, Gap, and Under Amour all communicated their accomplishments in improving human rights and labor management. Denim companies, such as Levi’s, invest in the well-being of employees and reduce wastewater in their finishing processes. Although some companies failed to mention certain themes, these themes may be important aspects of sustainability development and thus need to be adopted as needed.

Implications

This study has made significant theoretical contributions. First, through a novel dictionary-based approach, this study explored corporations’ sustainability practices and identified environmental support, working conditions support, transparency enhancement, and community support—currently the four major categories mentioned in fashion CSR reports—providing empirical support to TBL and MRCS theory. Second, this study demonstrates global fashion companies’ emphases on and implementation of sustainability practices. Interestingly, the findings remain consistent with customers’ perceptions toward the four duties of MRCS in previous studies (Jung & Ha-Brookshire, 2017). Third, this study compares companies’ practices to achieve sustainability, differentiating them by their product category and goal.

These findings provide valuable information for consumers as they will be able to get a holistic idea of the sustainable practices performed by various fashion companies while choosing products and causes they care for. Using this dictionary and detection schema, consumers and other stakeholders can quickly monitor and investigate sustainability themes, as well as find and compare the sustainability efforts that different fashion companies have implemented. These findings will also be beneficial for fashion companies that want direction on what to emphasize to achieve a particular sustainability goal. For example, fashion manufacturing companies may begin their sustainability paths through environmental efforts, such as using green energy and recycling waste.

The new research scheme developed from our research has proven to be an innovative and efficient way to discover knowledge from textual data sources. In this research, the first fashion sustainability dictionary for text mining was built based on TBL and MRCS theory and could be expanded when more themes and keywords emerge from public disclosures. Using this tool, researchers could classify, investigate, compare, and analyze the sustainability practices adopted by fashion companies efficiently and accurately. For example, if researchers wanted to investigate the historical sustainability practices adopted by Nike from their CSR reports, they could scan all textual information based on this dictionary and get the frequency of mentioning each theme in one report, thus gaining a better understanding of Nike’s sustainability practices. What is more, if researchers are only interested in one theme, for example, “waste management,” they could use this tool to examine Nike’s waste management practices in detail. Researchers are also encouraged to develop dictionaries in other areas of interest using this research schema and glean knowledge from large amounts of textual data related to CSR and sustainability.

Limitations and Future Studies

There are several limitations in this research that could lead to future research opportunities. First, this research only compared the total practice themes of fashion companies, ignoring temporal analysis of sustainability development. The historical sustainability practices of fashion companies could also be tracked to investigate trends over time. Second, this study only analyzed the textual data from CSR reports of global fashion companies. In future research, data from other sources regarding sustainability, such as social media and website content, could be fed into the system to continue refining and improving associated themes. Third, this study only collected data from public and large-scale fashion companies. To diversify the company type, more data can be collected based on firm size or geographic location to better understand sustainability practices. Fourth, since text-mining is a novel approach in the fashion field, other text-mining techniques such as text clustering, text summarization, and network analysis could be integrated to improve the validity.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.