Abstract

This article investigates the development over time of the automotive and textile industries post-1989 in four Central European countries in order to identify the key reasons behind sectoral growth or decline. The analysis demonstrates a divergent pattern of sectoral development, one that is in contrast to the perceived initial endowments of the countries and the structural positions of the sectors at the outset of the transition. Comparing the two sectors and individual success stories within them against a broader background of sectoral success and failure allows us to understand and isolate factors that lie behind the high status of the automotive sector by not only regional but also international standards. The article identifies three crucial factors that can be attributed to these outcomes: presence of foreign capital in the sector, active government support, and cooperative strategies among the firms in the sector and among the firms and other institutions in the countries.

Introduction

Most observers analyzing the political economy of Central and Eastern Europe (CEE) in the early 1990s would have been surprised to find that already a decade later sophisticated engineering goods were produced in some of the transition economies. By mid-2000s, four CEE economies were successful in adapting their production profiles, and a vibrant automotive cluster emerged in the Czech Republic, north-western Hungary, western Slovakia, and south-western Poland, that is, the Visegrad Four (V4) countries. 1 Moreover, among the CEE economies, specialization in the complex sectors is typical for Visegrad (and Slovenia) while a very different pattern of less sophisticated industrial structure has been formed in the other parts of CEE, that is, the Baltic countries or South-East Europe. The latter countries’ economic structure has been composed mainly of light and labour-intensive industries, such as wood processing or textile and clothing production. 2

The V4 region’s rapid and successful integration into the European and global car production networks has been a subject of intensive scholarly debates and because of the obvious implications on the development of these countries, gained a fair share of policy attention as well. 3 The most recent research has identified a series of questions and controversies related to the rise of the automotive sector and the evaluation of the position of V4 car plants within the production networks as well as the role of the state in the processes. 4 Nevertheless, the automotive industry in the V4 is comparable to the quality and sophistication of the car industry on the Iberian peninsula and, moreover, it achieved its status in terms of product profile and value added in half the time that it took Spain. 5 Contrary to the automotive sector, the textile and clothing industries in the region have experienced a secular decline over time. Studies have identified clear subordinate relationships between the production sites in the Visegrad countries (but also the CEE region more widely) and the Western European competitors on the European periphery that have used the cheap labour in the East for the low-end part of the production cycle of the textile or clothing industry. 6

This article compares these two sectors and their very different trajectories over time in order to isolate factors that can be attributed to the industrial rise and decline. The automotive and textile industries are defined broadly and in the context of value chains, that is, including production of car parts and industrial vehicles, engines, buses, machines, etc. within the automotive industry and apparel, leather, accessories, footwear, and retail within the textile industry. 7 Both were important sectors in the pre-1989 economies and had very similar starting points in the late 1980s, but evolved differently thereafter. The comparison between the two is particularly enlightening since on the basis of initial factor endowments of the region—abundant and cheap labour, technological obsolescence, and lack of capital—the textile sector was in a better condition to succeed. Contrary to that, the automotive industry, which requires higher capital and skill intensity, fared well both relative to other sectors in the region and in respect to the sectoral developments in the rest of Europe. However, there have also been individual failures in the automotive sector (e.g., the Ford closure in Plonsk, Poland) 8 and successes of individual companies within the textile sector. The latter will be looked at as well in order to enrich the analytical framework.

By a sectoral comparison over time, the article aims to isolate and generalize factors that can be attributed to these strikingly different outcomes. The work identifies three crucial factors that underpin the successful sectoral (and company-level) outcomes: the entry of foreign capital, active government support, and cooperative strategies among the firms in the sector. These factors are evaluated against the broader literature on economic development that has studied determinants of economic growth and sectoral success elsewhere in the world. The findings for Central Europe generally confirm expectations stemming from the literature on sources of success of the automotive and textile industries in Latin America or East Asia. However, the Visegrad region is unique in the degree of penetration of foreign capital and concurrent ability to embed complex industrial production into economies in a very short period. Cooperative strategies that this work identified are both an evidence of such embedding and also represent an important tool of strategic coordination in the era of increased competition and market vulnerability. The most “provocative” finding in the context of neo-liberal Central European economies, which are typically perceived as having withdrawn the state from economic governance, is the crucial role of governments in both attracting and spurring development of the automotive sector.

The article starts by setting up the framework for the comparison in providing a general empirical overview of the performance of the two sectors in the decades following the fall of the Berlin wall. Background to the logic of the functioning of the two sectors identifies key factors necessary for development of each sector and briefly discusses their historical origins. The sectors are then discussed separately by providing empirical evidence about the key elements underlying sectoral (or individual company) success or failure: foreign presence, the role of government policies in enhancing it, and the cooperative strategies. The concluding part combines the empirical evidence in a more general argument on the determinants of sectoral advancement in the economic development of CEE and draws wider implications from the findings.

From Level Playing Field to Uneven Outcomes

The macro-level empirical evidence about the development over time of the sectors demonstrates a marked divergence in the importance of each sector in the economy, its added value, and contribution to employment creation. The importance of the car industry and the textile industry in the export and production structures was comparable in the late 1980s. Global competition after 1989 has been handled very differently by both sectors, although export volumes rose markedly in both industries and integration with the Western and other markets took place very fast. 9 While the rise in export volumes has been documented in most single-sector studies about the textile industry and interpreted as a measure of growth and successful integration into world markets, such an approach is misleading because many studies overlooked the relative decline of the industry. It is also important to keep in mind that special EU-CEE outward processing arrangements were in place in the 1990s that fostered export of finished products until 1998 under a protective regime, that is, without fully liberalized trade between the accession countries and Western Europe. In spite of that, the sector faced a secular decline, as figures below document.

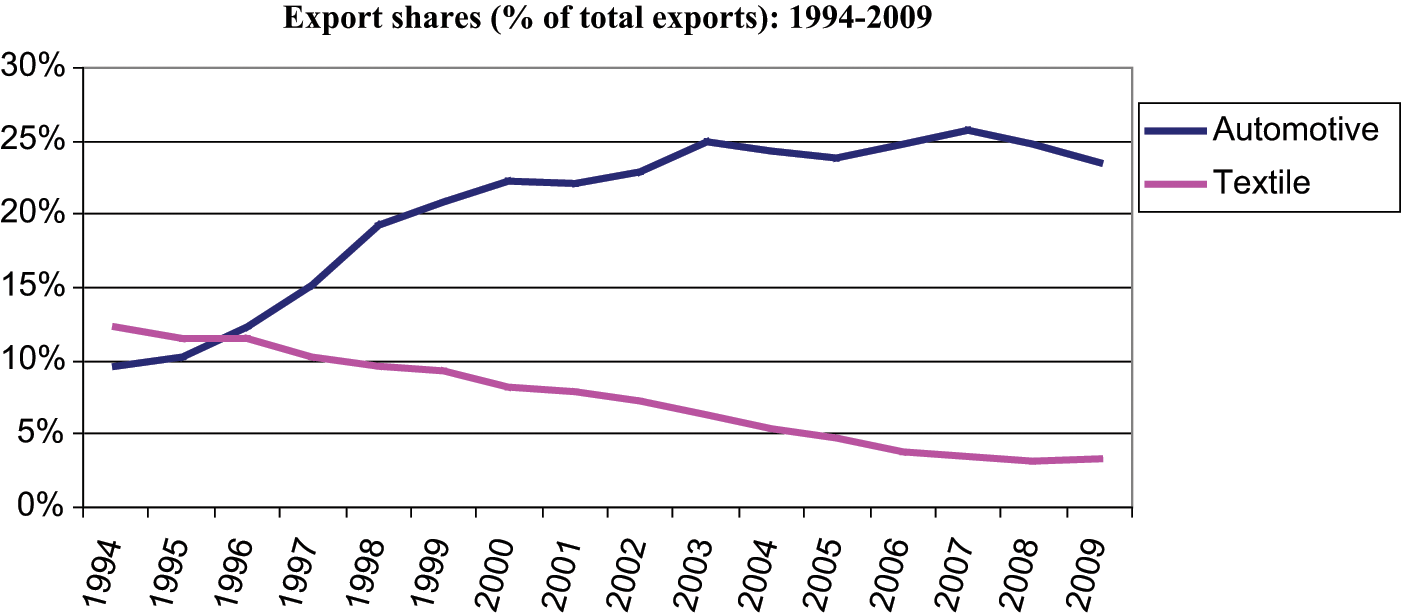

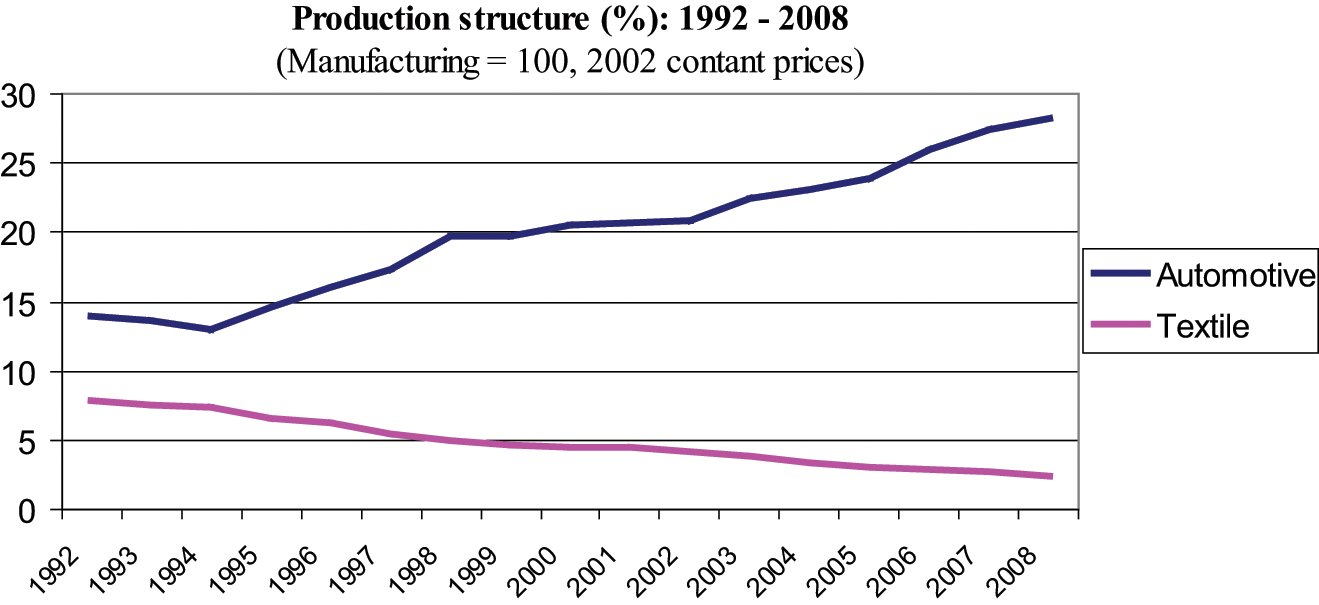

After starting from relatively similar positions in terms of export shares and shares of manufacturing output in the early period of the transition, the textile sector has gone through a protracted process of decline while the automotive industry has grown rapidly (Figures 1 and 2). On average, automotive sector exports and the share of manufacturing output rose from about 10 per cent in 1994 to 25 per cent in 2008 for exports and from nearly 15 per cent to more than 28 per cent for output between 1992 and 2008. The trend has been the opposite for the textile sector: a decline of more than 8 per cent (from 12.5 per cent to less than 4 per cent) in export share and of 5 per cent (from 8 per cent to 3 per cent) in output share took place between 1994 and 2008.

Export shares: Visegrad average: 1994-2009

Production structure: Visegrad average: 1992-2008

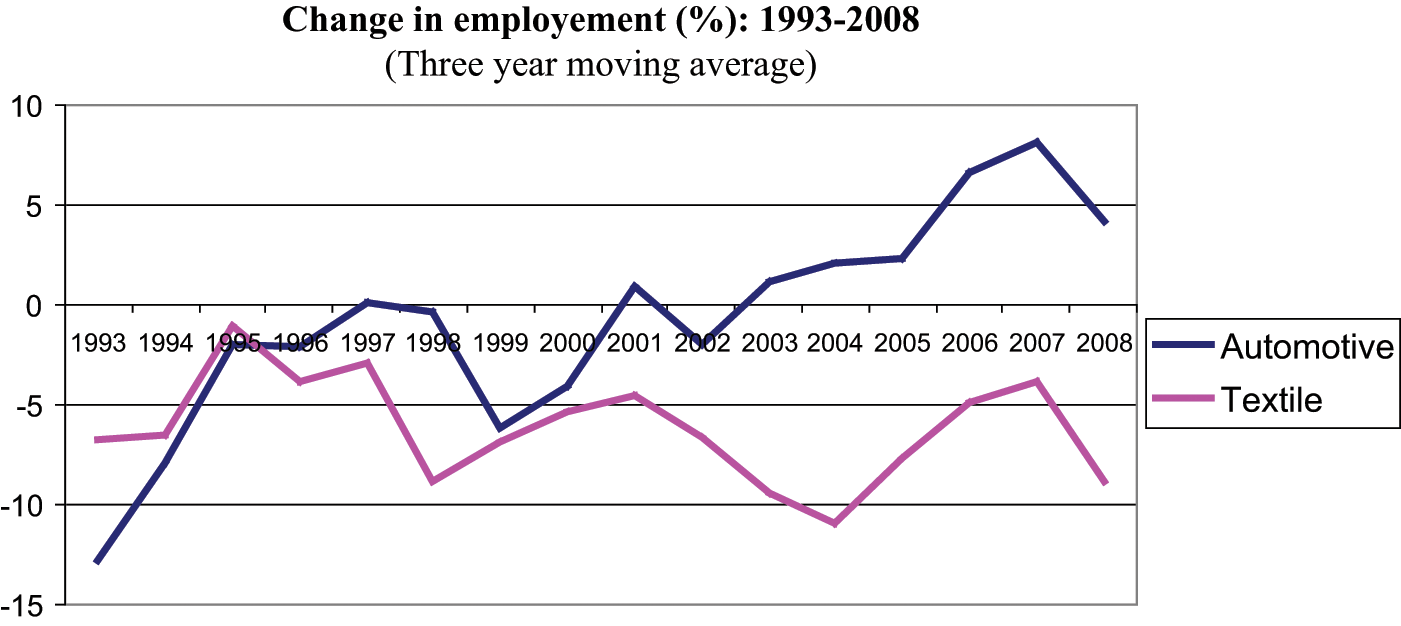

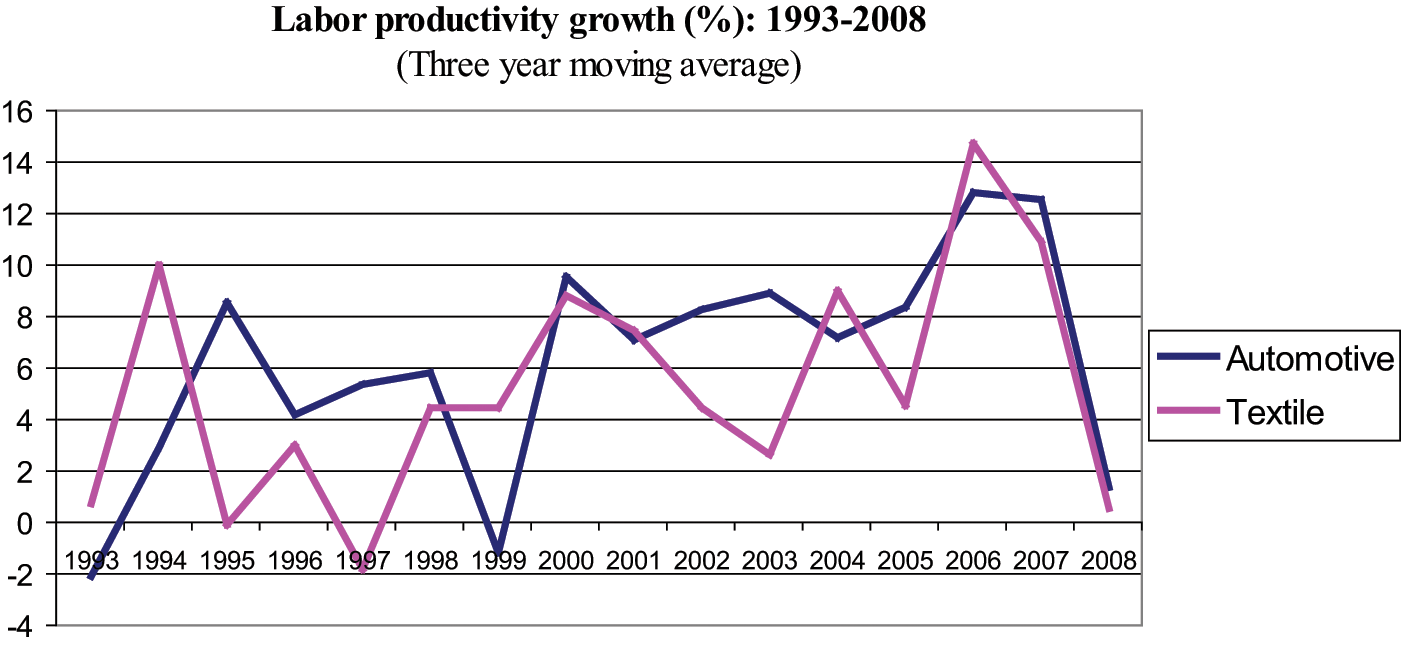

Further, at the turn of the century, the sectors started to diverge significantly in the ability to create jobs and attract labour. The textile industry was losing its share in employment throughout, the automotive sector began to contribute significantly to the job creation from early 2000s (Figure 3). Combining these evolutions with figures on labour productivity, which has risen in both industries, suggests that labour productivity in textiles has increased at the expense of employment while the opposite is true for the automotive industry (Figure 4). On the basis of these indicators and further evidence presented next, it is justified to treat the automotive sector as a success and the textile sector as a failure.

Change in employment: Visegrad average: 1993-2008

Labour productivity growth: Visegrad average: 1993-2008

Production Chains and Factors Underlying Sectoral Success

Both the automotive and the textile industries are highly competitive, internationalized and global industries which function in the integrated production systems consisting of highly specialized, segment-specific, horizontally and/or vertically organized transnational firms coined as commodity chains or value chains. 11 However, the two industries are structurally very different and represent prototypes of producer-driven (automotive) versus buyer-driven (textile) commodity chains. Both of these two sectors have been important vehicles in the industrialization and economic development in different parts of the world, ranging from Latin America to South-East Asia. Differences in the organization of the industry imply different factor intensities necessary for their development and growth.

The automobile industry is a classic example of a producer-driven commodity chain. The automotive sector is among the largest and most internationalized industries. The industry has a high intensity in capital, technology, and skills, and exhibits high barriers to entry. The high barriers to entry, in turn, imply that the sector tends to have an oligopolistic structure, with only a few companies playing a major role in one country and in world competition.

A change in the organization of the industry from Fordism to the Japanese model of lean manufacturing and the system of just-in-time parts delivery has transformed the organization of the supply industry. Logistics and material movement have become skills in themselves and have forced firms to specialize in this area, imposing high demands on the quality of a host country’s infrastructure. Further, the industry is undergoing another structural evolution, with its shift toward collaborative engineering and production, resulting in even greater outsourcing. 12 Consequently, lower-income countries with large labour supplies only lack a comparative advantage in the automotive industry. 13 To summarize, the automotive industry necessitates well-developed physical infrastructure, skilled labour, and because of its capital intensity, sufficient source of capital. Studies discussing the factors contributing to the development of automotive industry in less developed parts of the world jointly highlight the crucial role of government policies in attracting investment and/or protection of the industry. 14

The textile industry, in contrast, is a prototype of a buyer-driven commodity chain based on decentralization and a decoupling of design and retail from the actual production of goods. Production is generally carried out by tiered networks of third world contractors that make finished goods for foreign buyers. The specifications are supplied by large retailers who order the goods. Skill intensity thus varies greatly along the different segments of the chain, with the production part requiring low-skilled labour and relatively little capital or knowledge. 15 The production segment is characterized by a myriad of small firms, which employ disproportionate numbers of women and handicapped and older people. Unlike the automotive industry, it can therefore be set up in regions with a weak infrastructure and low-skilled workforce, and it also requires less financial capital.

While the textile and clothing industry is typically much less concentrated in the hands of foreign capital, foreign direct investment spurred by the processes of growing liberalization and generous government incentives was a key factor, in addition to low labour costs, behind the successful overtake of the U.S. and Western European textile and clothing production by the East-Asian countries in the 1980s and 1990s. 16 Foreign investment in Central Europe was arguably crucial as a source of capital and technological progress necessary to upgrade quality and to face labour-cost-based competitive pressures later on.

Theoretical works about the dynamics of commodity chains increasingly highlight the importance of strategic alliances in industries with short product cycles (e.g., textile and clothing) and high R&D costs (e.g., automotive). The ability to create networks and to cooperate has become a vital asset because of the rising competition in both sectors and in recent years also because of the volatility stemming from the world economic crisis. 17

Historical Origins of the Sectors in the CEE

Among the factors contributing to sectoral success, tradition and local knowledge are considered key because they typify human and physical capacity to produce certain goods. While these attributes are absent in the developing countries characterized by backwardness, the situation in Central Europe at the break of the regime was different. 18 The industrial tradition in these areas almost invariably dates back to before the Cold War era and both sectors played an important role in the pre-1989 Central European economies. While the Czechoslovak automotive tradition goes back to the 1920s, when the Škoda factory was set up, the history and experience of the textile industry in the region dates all the way to the fifteenth century for some of the Czech guilds, and to the late nineteenth and early twentieth century for several other firms in the region that have survived the whole century. 19

Under socialism, the more western parts of the eastern bloc, today’s new EU member-states, served as industrial bases for processing primary commodities coming from the Soviet Union, a decision that was built on the existence of comparative advantage and experience from the pre–Cold War era. 20 Therefore, in relative terms, the factories based (especially) in today’s new EU member countries were typically advanced, and moreover, original branding and R&D accompanied the leading producers in the individual sectors.

The textile and clothing industry was particularly developed. Czechoslovakia had its own R&D capacity connected partly to the existence of other industries in the region (i.e., chemical industry) and/or brand manufacturing (e.g., Makyta Púchov and Ozeta Trenčín in Slovakia). 21 Because of the fact that Poland and Hungary began to liberalize their economic and political systems already under the Soviet regime, textile and clothing products were exported to the European Community in the 1980s, providing an important cushion in the early years of transition. 22 In the Slovak case, the lack of direct links with the West was supplemented by the structure of the sector typified by large formerly state-owned firms with long-standing tradition that were able to manage the beginnings of transition partly by organizing the networks of small firms within the country. 23 Contrarily, in the automotive sector, Škoda was the only original brand manufacturer while the remaining car production facilities were typically developed based on licences from the West (e.g., “Polsky” licence from Fiat). 24

This discussion highlights that the initial position of the two sectors was comparable. With the exception of Czech Škoda, the automotive sector lacked domestic-based production and was dependent on foreign (i.e., Western) licenses. 25 The textile industry was embedded in the economies, well developed, and even integrated into Western markets already in the late 1980s. At the outset of the transition, the textile industry had greater chances for success and this, indeed, originally was the case in Hungary and also in the Baltic countries. Considering these factors, the rise of the automotive sector in the Visegrad countries that happened in spite of the competition coming mainly from the developed economies (and a rising automotive sector east of CEE) while a decline of textile industry that had to compete on the grounds of low labour costs urges us to consider the factors that contributed to the success of the car industry in the Visegrad region “against all odds.”

From “Favorit” to Successful Regional Automotive Agglomeration

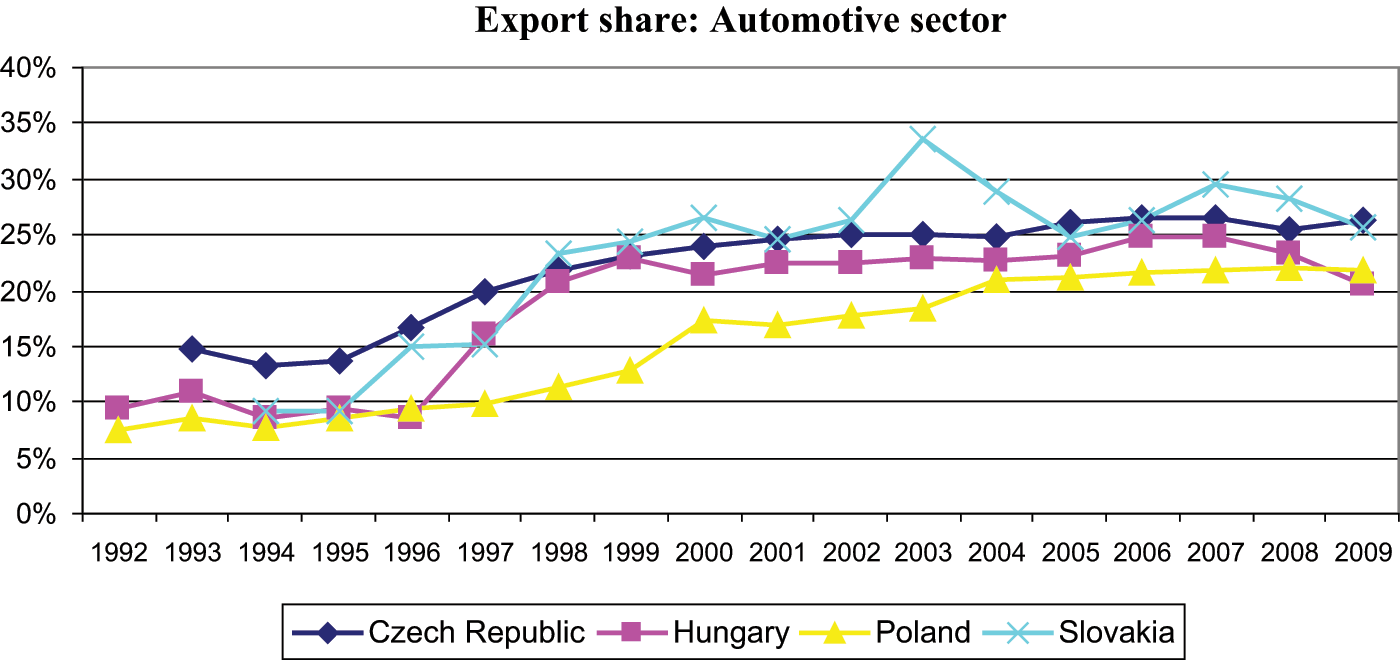

The automotive industry has been the single most important sector in the high-growth V4 geographical region. By the mid-2000s, this industry and its offshoots alone comprised a significant part of the GDP in all of the countries. In 2005, the share of manufacturing on the GDP gross value added represented 18 per cent in Poland, 23 per cent in Hungary, 24 per cent in Slovakia, and 28 percent in the Czech Republic. 26 The sector accounted for the bulk of exports, peaking to between 22 per cent and 30 per cent in 2007 and declining in the crisis peak in 2009 (Figure 5).

Automotive sector exports per total exports

The automotive industry in the CEE is characterized by massive involvement of foreign automotive multinational companies that were motivated to invest in the CEE states by a mix of different factors. 27 Initially, the CEE served mainly as the target market for multinational corporations (MNCs) that followed a build-where-you-sell strategy, motivated by cheap, productive, and skilled labour and the expectations of the market growth. A follow-the-leader pattern of investment became evident when after the initial Volskwagen (VW) investment in former Czechoslovakia, many other brands soon followed. However, the small size of the Central European market and the slowly growing disposable household income in the region has led firms to use Central Europe as a production base to serve the EU markets. 28 The prospects of EU accession significantly encouraged car manufacturing MNCs to enter the market or expand their activities, and instigated a second wave of automotive investment that took place from the late 1990s. Today the region produces more cars per head than any other region in the world, and the growth in volume has been extremely fast since the start of stable production in the late 1990s. By 2007, the yearly passenger car production in Visegrad rose from about two million to four and a half million. At the same time, the share of Visegrad production on the European production doubled from about 12 per cent to (striking) 24 per cent. 29

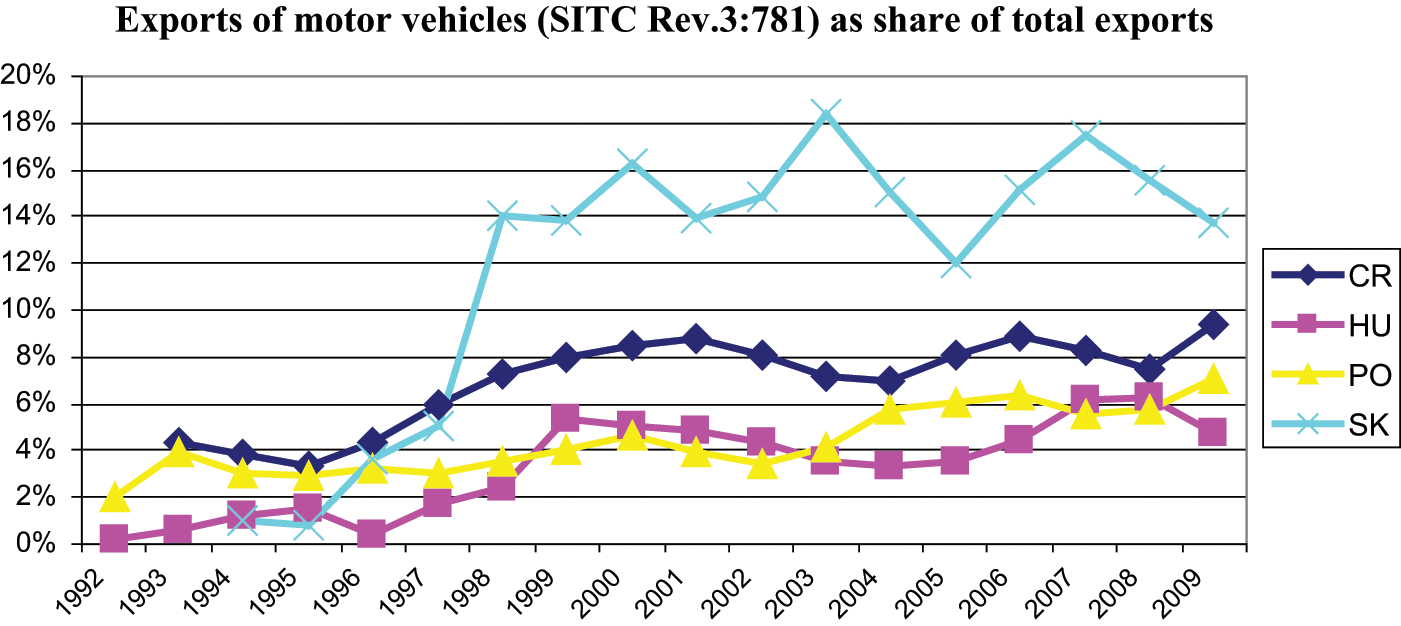

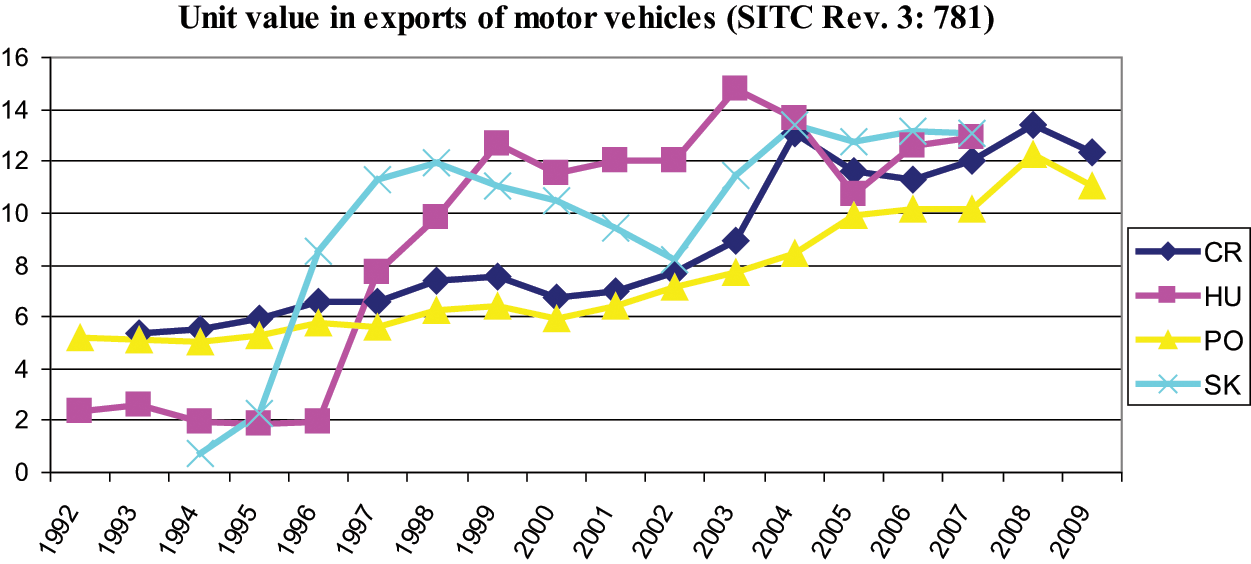

Two additional processes seem to have characterized the evolution of the sector. First, the product market strategies have shifted from manufacturing of long combination vehicles (LCVs), trucks, agricultural tractors, and motorcycles to passenger cars (and partly to buses). Secondly, there has been a clear upward shift in terms of product and production profile. Car producing operations in Central Europe also tend to use the most modern equipment and are typically among the most advanced within their companies. 30 The plants have marked a sharp upward shift in the product range from relatively small, simple cars to high-end ones, such as from VW Polo or Opel Corsa to the large, high value-added off-roader Audi Q7 or the Opel Zafira. The upward shift in product and skill sophistication is also visible in Figures 6 and 7, which present export shares and unit values (the average monetary value of a single car produced, a good proxy indicator for quality and skill) for motor vehicles only (rather than the broadly defined automotive sector in Figure 5). Between 1994 and 2009, the unit value has risen on average about three and a half times, gradually in Poland and the Czech Republic while increasing more sharply since the late 1990s in Slovakia and Hungary. These processes can be directly connected to the changes in the product profiles described above. To conclude, in about fifteen years after the transition, car plants in the V4 region have transformed with great speed from low-wage extended workbenches of western operations to flexible high-end producers, able to combine the advantages of large volume with a focus on product range variability and high quality and value addition.

Motor vehicles: export share

Motor vehicles: unit value

What seems to have emerged in the automotive industry in the V4 region is an industrial structure that can no longer be characterized simply as a low-cost competitor in low-value-added market segments but a full-fledged robust industrial system that has managed to capture higher-end product market segments. 31 From being highly dependent initially on strategic decisions made in headquarters in the centre, car producers in the region have increased their operational autonomy and have been renegotiating strategic and R&D capacities with the centre. Importantly, the pessimistic assessments presented a decade ago about a lack of the use and development of domestic engineering and design skills and a suggested reduction of local R&D facilities have changed. 32 Pavlínek, Domański, and Guzik identified forty engineering and technical centres in 2006, although distributed very unevenly across the countries and among the MNCs as well. 33 As elsewhere in the world where domestically based production or domestically generated capital was missing, foreign investors played a key role in the development of the sector by bringing capital and knowledge.

This particular development in the car industry, however, cannot be separated from industrial policy that fostered the development of the sector since the very beginning of the transition. These interventions initially represented forms of market protection with the aim to support the development of the sector, mixed with particular privatization strategies and policies to attract the FDI. While the countries initially varied in the type of policies towards FDI generally and the automotive sector in particular, they gradually converged.

In the 1990s, Hungary was the most forthcoming towards foreign capital. Already in 1993 the country adopted a policy of industrial export processing zones (EPZs) that offered simplified customs regulations, duty-free treatment for imports into EPZs, investment incentives and government support in terms of infrastructural development, training schemes, and tax holidays. 34 Partly as an outcome of these efforts, four motor manufacturers were active in the country already by the mid-1990s, all in anew plants. The Czech government was the first one to negotiate access of foreign capital into the automotive sector and offered four-year protection from imported cars to Volkswagen as part of the Škoda agreement negotiated in 1990. Restrictive trade policies of the Polish government in the 1990s and high import duties on EU-produced cars in effect until 2002 were the main reasons for establishing assemblies in Poland. 35 Both Hungary and Poland introduced a system of import licenses targeting second-hand cars from the EU until the early 2000s. 36 Slovakia was initially the most hesitant to support the sector and increased its efforts to support the industry further only in late 1990s via a governmental decree in 1998 that approved tax incentives to VW. 37 Although some of the more general policies implemented in the Visegrad, such as EPZs, industrial parks or incentive schemes, were not targeted at the automotive industry explicitly, automotive companies and, even more importantly, their supplier networks were in fact great beneficiaries of these policies. 38

As the EU accession approached, the government support shifted from state protection to direct help in the form of investment incentives that included tax holidays and financial contribution for employment creation and skill development. The size of investment packages was driven up by fierce competition among the countries in the region because of the perceived structural and institutional similarity on the side of the investors. 39 The amounts offered by government incentives were exuberant and the types of benefits wide-ranging. All Visegrad countries participated in the bidding war, but Poland was the least successful at attracting automotive FDI in mid-2000s (or the least willing to pay such large incentives). Because the industry became such an important player, it received unique attention and support also during the world economic downturn in 2008-2009. The introduced measures differed in type and scale, reflecting ideological position of the governments and budgetary constraints. The Czech and Slovak governments introduced targeted support to the sector aimed at stimulating domestic demand, 40 such as car-scrappage schemes. 41 Flexibilization of working time through the amendment of labor codes in Slovakia was passed in response to the specific needs and calls of the automotive sector; a similar arrangement was vocally debated in Hungary. 42 Additionally, the Czech government shortened the depreciation period for all vehicles purchased after January 2009 and amended the system of VAT deductions to include personal cars (not only LCVs) and passenger public transport vehicles. Poland was the only country in the region that did not offer targeted support to its automotive sector.

The third element contributing to the success of the automotive sector has been the ability of producers and suppliers to form strategic networks among each other and with other institutions in the countries, such as schools. Before the economic crisis, such cooperation was particularly apparent in the area of the provision of skills. Soon after the second wave of automotive investment settled in the individual countries, the firms and their supplier networks began to face problems with labour recruitment and labour turnover. Given their longer-term strategic goals, this had led nearly all companies, some earlier than others, to engage in the investment in training and education, setting up various forms of cooperation with local secondary schools, universities, and among themselves. 43 For example, Audi Hungaria in Győr began in 2001 a long-standing cooperation with a local technical high school by establishing a training program for the skilled labour segment of the industry that ran parallel to an educational centre in the factory. In 2008, such activities were extended to the level of tertiary education and own department of internal combustion engines on the Széchenyi István University was established. In Slovakia, more bodies have been involved in a similar educational initiative. The “Campus of Occupations” (Kampus povolaní) project worth a €2.3 million was set-up by PSA Peugeot Citroën Slovakia in cooperation with the Slovak and French Ministries of Education and regional-level administration. Over three years, PSA trained for its own needs nearly 2,200 engineers (5,500 employees in total) and thirty Slovak teachers in different training centres. The training centres in Slovakia were later transferred to the competence of vocational high schools under whose supervision they have been run, in effect making the established capacities available not exclusively to the PSA but also to other companies. 44 Further, Hancké discusses the case of the emergence of strategic coordination in skill formation among the automotive companies in Slovakia that was mediated or facilitated by the Chambers of Commerce in the country. 45 These organizations played a crucial role representing their member companies also in the negotiations with the government in respect to the changes in major legislation, such as the labour code or vocational education act. 46 Thus, the spatial clustering of automotive companies and their supplier networks in the Visegrad region also grew into a novel form of interfirm cooperation in strategic matters. The automotive industry continued to phrase vocally and in a relatively uniform fashion its requests even during the downturn; as the earlier discussion showed, it was quite successful. This pattern of development and embedding that has characterized the automotive sector and that includes upgrading in product market strategies, cooperation, strategic engagement of local resources, and a set of governmental policies protective of the sector or conducive to such development, is very different from what we find in the textile sector. As we will see, nearly all the elements that have made the automotive industry in Central Europe a success story are absent in the case of the textile industry.

Decline of the Textile Industry

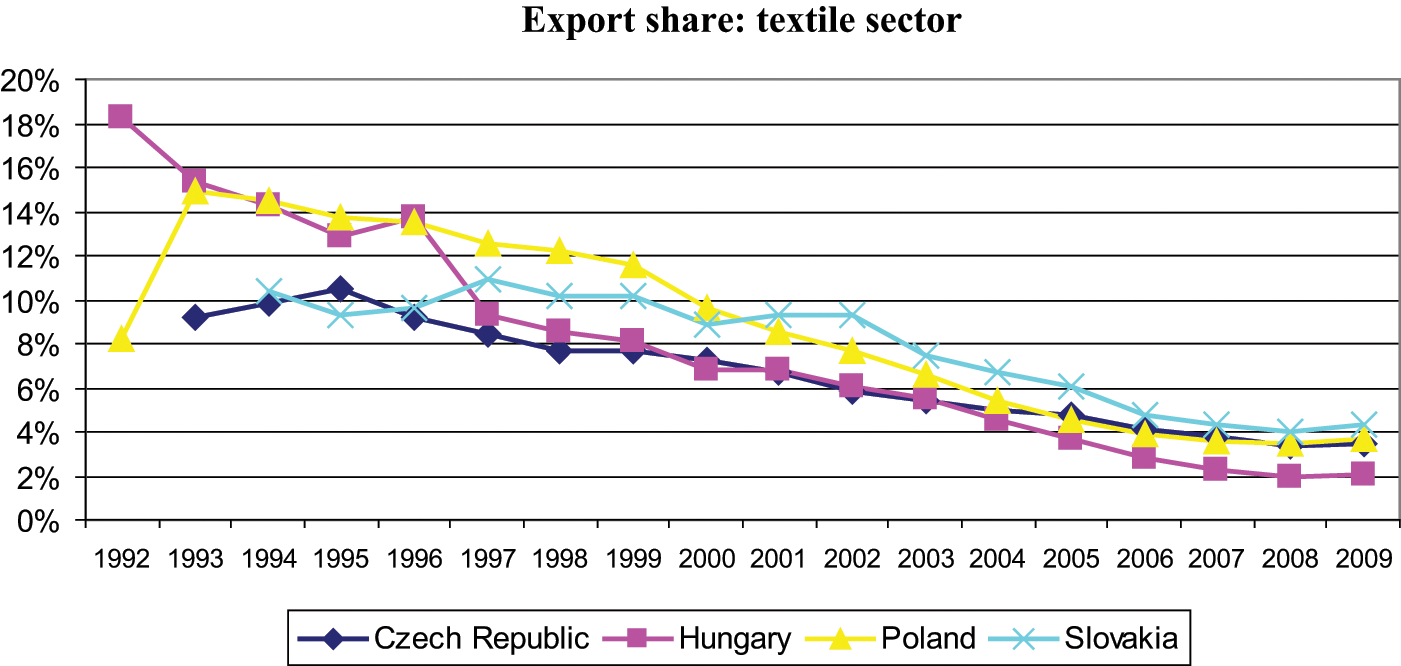

The textile industry in Central Europe is a sector with a long and successful tradition dating back several centuries. Before the late 1980s, more than half of the production in the region was directed to the Soviet Union as part of the exchange for raw materials and other economic arrangements. Because of secure demand, no sophisticated development or modernization was necessary. In the initial stages of the transition, the industry fared reasonably well but the peak of the mid-1990s was followed by a general decline of the sector in terms of employment levels and export shares (Figure 8). The initial relatively good position of the industry was due to favourable trade regulations between the EU and the accession countries, in effect until 1997, that supported the outward processing (OP) trade by exempting the OP components from import duties when they returned to the original country in a further processed form. 47 Facing the competition from Asia and unfavourable textile trade treaties with China on the EU level, the decline in the textile industry has hit Europe generally, not only the Visegrad countries. 48

Export shares in textile industry in Visegrad

Unlike the automotive industry, the textile industry has generally seen limited amount of foreign direct investment (FDI). This is partly due to the OTP arrangements in the 1990s that while guaranteeing better marked access, also put into relative disadvantage foreign direct investment in the industry. 49 Further, unlike investments into complex sectors, foreign investment in the textile industry received little government support, with the exception of tax breaks during the 1990s that perversely resulted in the closure of these companies after the ten-year tax holidays expired, partly because of the lack of embedding of these firms into the local economies. The industry in Hungary in particular further suffered from the minimum-wage legislation introduced in the early 2000s (50 per cent increase in 2001 and another 25 per cent rise in 2002) which had a negative effect on low-skilled industries, such as textiles, in particular, 50 but facilitated the transition from low-wage manufacturing to production in complex and skill and capital demanding sectors very successfully. 51

The lack of greater involvement of firms with local economies is also reflected in the peculiar development in the area of R&D. While the industry used to have research centres running parallel to production centres in the past, these have in fact ceased to exist or became dysfunctional in, at least, Slovakia and Hungary. The cooperation between the two existing research centres in Slovakia and firms was in mid-2000s very weak. This is partly a function of the fact that most firms that still functioned at that time were fully or partly foreign owned (meaning that the R&D or design development functions were typically kept in the foreign firm headquarters), but it also reflected the inability of the remaining R&D centres to cooperate closely with those firms that would be interested in moving some R&D functions to Central Europe. Still, in the Czech Republic, R&D in textile and clothing was preserved and further developed, partly a result of a greater share of textiles in the industry mix in the early 1990s, characterized by a higher technological intensity than clothing, but even more importantly because of the clustering of firms in the Liberecko area north of Prague, which made it possible to combine existing resources and to share knowledge more than elsewhere in V4.

Against this broad background of general decline and a limited ability to move to more sophisticated and research-informed production in Central Europe, however, several success stories of individual firms exist within the sector. Analyzing these in the framework introduced for the overview of the automotive industry helps us to validate and generalize the factors identified as crucial for the sectoral outcomes.

A crucial element that exists in all the successful companies, that is, those that manage to hold on to a stable share of the regional market and/or produce products with higher value added, is the presence or full ownership of foreign capital or cooperative strategy with other firms. A few examples illustrate this point. Backed up by a Swiss investor, Rekos in Revúca, in Slovakia, has been able to produce carpets with sophisticated technology. With Danish capital and know-how, Titex in Humené, in Slovakia, produces sanitary and health textile for a large part of Europe. 52 Another example is the Czech PLEAS, which was sold directly to a strong Swiss foreign investor as early as 1994. The DM10 million investment into renewing and developing the equipment and production sites in 1995 proved a good choice and the company managed to keep its trademark as well as a stable share in several stages of clothing production, including preparation and development of knitwear/fabric (knitting, colouring, and design), cutting, and sewing of the clothing. 53 Pickles et al. (2006, 2320-21) highlight the example of crucial relationship between one of the most successful new private firms in the Prešov region in Eastern Slovakia and one of the leading UK investors in the Slovak apparel industry. 54 The relationship started on a subcontracting basis a decade ago but gradually developed into one where the Slovak manager seeks advice on pricing or buyers’ expectations from his UK colleague, and in exchange provides him with crucial contacts with reliable production partners in Bulgaria and Ukraine, where both of the firms by now developed their operations. Indeed, the success of many Visegrad firms has stemmed from their ability to move up the value chain through outsourcing of the simplest and most labour-intensive parts of the production processes further East, from Ukraine to China. 55 The ability to become “network organizers of cross-border production systems” is what has given them competitive advantage within the value chains with respect to foreign buyers or owners. 56 On the whole, though, the clustering and in some cases tight networking that has characterized the automotive industry has not taken place in the textile and clothing sector. With the exception of the Czech textile sector clustering and some of the examples discussed above, firms tend to act in isolation rather than cooperate, even in situations where they are unable to meet their orders.

Conclusion

This article investigates the development over time of the automotive and textile industries post-1989 in four Central European countries in order to identify the key reasons behind sectoral growth or decline. The analysis measured the performance of the sectors along different indicators and over time and demonstrated a divergent pattern of sectoral development. The automotive sector saw increases in exports and manufacturing share, rise in labour productivity together with rise in employment, upgrading in product and skill profiles, and emergence of R&D facilities in the region. The textile sector experienced falling shares in exports and production structure and an increase in labour productivity only with falling employment in the sector. Upgrading was limited to few successful firms but the sector overall lacked product or skill profile upgrading, while the originally existent R&D capacity dilapidated. Such sectoral outcomes stand in contrast to the perceived initial endowments of the countries based on cheap labour. In addition, historical legacies and performance of the sectors at the beginning of the transition gave the industries a similar starting position. Overall, while the textile industry has mainly faced competition from developing countries in Asia, the successful automotive sector in V4 has (so far) been able to stand its ground against competition from across the world.

Discussing a broader background of sectoral success and failure has allowed us to understand and isolate factors that can explain sectoral rise (and decline) in the context of fast integration into world markets. The article has identified three crucial factors that can be attributed to these outcomes: presence of foreign capital, active government support, and cooperative strategies among the firms in the sector and among the firms and other institutions in the country aimed at resolving collective problems and so better face the external competitive pressures.

First, the automotive sector is characterized by a strong presence of foreign capital that entered the sector at a very early point in the transition and, because of a combination of various factors, gradually changed its strategic orientation to export and production of high-end products. The foreign presence secured sufficient capital for plant modernization and transfer of technological, managerial, logistical, and other know-how essential for car production in the twenty-first century. Contribution of foreign capital was especially essential also in the context of the lack of capital and technological obsolescence with which the region entered the transition from socialist economy. The textile industry, on the other hand, attracted considerably less foreign investment. However, those firms in the textile sector that managed to secure foreign capital and know-how have performed well, often reaching regional leadership positions.

Second, the degree and form of government intervention across these two sectors varied greatly. The textile industry did not receive the extensive support that car manufacturing collected through protective trade policies and especially more directly in the form of investment or training subsidies to the green-field investment. The extent to which the favouring of the automotive sector as the ‘leading sector’ has been a deliberate and thought through strategy is unclear, but it is a matter of the fact that policy decisions that were taken on the part of the governments facilitated the success and embedding of the automotive car plants in the region. For any industrial upgrading, foreign direct investment has been essential. The fact that it entered the region, however, is not independent from concrete governmental policies, including sectoral industrial policy and support given to the leading and other companies. 57 This sectoral comparison therefore leads us to attribute a great weight to the leverage of state policies in the success of the automotive industry in the Visegrad countries. 58 While this is in line with what literature on sectoral and economic development has argued, it stands in contradiction to the perception of the CEE region as governed by neoliberal policy and characterized by a withdrawal of the state from the economy. While lower penetration of textile industry by foreign capital is partly a function of the organization of the sector, research elsewhere has shown that investors can be incentivized to enter this sector and their presence ensures inputs such as technological and organization innovation, leading to higher productivity and sectoral expansion. 59

Third, sectoral as well as firm-level success has depended on the development of cooperative networks that allowed the companies to resolve collective problems, be successful in lobbying for their needs in respect to crucial legislation, or share technological knowledge. Such strategic behaviour enabled automotive firms and their suppliers to organize their voice and their action in areas where governments were unable to fully secure their needs, such as education and training, because with the growth of the sector and opening of the labor markets in the West after the EU accession, specialized human capital became a scarce good. Serving as the network organizers of cross-border production systems with firms further East gave the successful companies in the textile industry crucial competitive advantage that helped them stand against the pricing-related competitive pressures. This part of the argument has been in line with other works that have concluded that regional economic growth can be achieved in less favoured regions by building “cooperative advantage.” 60

The sectoral developments discussed and empirically evidenced largely for the period from the beginning of the transition to the beginning of the crisis hold also in the time of the world economic crisis. While heavy reliance of the V4 economies on the automotive industry and its off-shoots led to marked declines in exports and loss of employment, in relative terms the Visegrad countries (with the exception of Hungary) have fared much better than, for example, the Baltic countries, which have pursued a different path of economic development during the transition. 61 The effect of the crisis has been less severe and the economic recovery swifter not least because the governments—East and West—hurried to support the automotive sector. And, as in the time of the boom so in the times of the bust, instances of inter-firm cooperation existed, this time even across borders when VW Bratislava lent skilled labour to Škoda, which needed to meet the demand stimulated by the government packages. 62

In general, the findings of this article can be of relevance to the debate on the role of the state in industrialization and steering of sectoral development. It also sheds light on the trajectories of structural change in Central Europe and the degree to which the government policies contributed to particular sectoral developments in these countries.

Footnotes

Author’s Note:

This paper was written with the financial support provided through the STACEE FP6 project (Project CIT1-CT-2004-506392). The author would like to thank Bob Hancké, Vera Scepanovic, and an anonymous reviewer for helpful comments. All errors remain my own.