Abstract

Even as economic incentives are increasingly used by policy makers to spur state and local economic development, their use is controversial among the public and academics. The authors examine whether state and local incentives lead to higher rates of business start-ups in metropolitan counties. Existing research indicates that start-ups are important for supporting (net) job creation, long-term growth, innovation, and development. The authors find that incentives have a statistically significant, negative relationship with start-up rates in total and for some industries including export-based and others that often receive incentives. The findings support critics who contend that incentives crowd out other economic activity, potentially reducing long-term growth. The authors also find that greater intersectoral job flows are positively linked to total start-ups, consistent with claims of those who advocate for policies that enhance labor market flexibility through reducing barriers to job mobility.

This is the Eighth Wonder of the World. . . . one of the great deals ever . . .

The value of economic incentives has long been debated by academics and the public, even as policy makers increase their use. The beginning of the modern U.S. tax incentive and subsidy era is typically attributed to Mississippi’s Balance Agriculture with Industry (BAWI) initiative enacted during the Great Depression. 1 BAWI worked very much like modern incentive schemes, using bonds, free land, tax abatements, and other subsidies to attract business. Yet BAWI was disbanded in 1940 in response to the same concerns that linger in today’s debate. Specifically, are such subsidy and incentive schemes worthwhile, or do they crowd out existing business expansions and potential business start-ups that would have otherwise occurred? Are they fiscally responsible and generate new revenues to offset their costs, or do they lead to other tax increases and service cutbacks? In sum, do incentive packages provide a good example of the “winner’s curse” with winning communities overpaying? We examine this issue by appraising whether incentives affect overall firm start-up rates, which play a key role in long-term growth.

Economists have mixed findings regarding the effectiveness of business incentive and subsidy packages because they appear to be “picking winners” and distort markets. For example, Goetz et al. (2011), Patrick (2014), and Calcagno and Thompson (2004) found that incentives are generally ineffective and may harm employment growth. More recently, Neumark and Grijalva (2017) examined state job tax credits and report that some types of credits are effective at boosting job growth; however, their results also implied that credits are more effective at increasing hiring than at generating net job growth. On the other hand, Chirinko and Wilson (2008, 2016) studied job tax credits and investment tax credits and provided evidence that incentives can be effective, albeit with modest effects. The estimates from Greenstone et al. (2010) suggested substantial benefits associated with highly incentivized plants.

Two recent examples of business incentive competitions provide good examples for why the debate is so contentious. First is the 2017 $4.5 billion Wisconsin package—the largest in the United States to be given to a foreign company (Witte, 2019)—to lure a Foxconn factory to assemble televisions (Carr, 2019). Foxconn promised the factory would employ 13,000 at an average $23 hourly wage. Foxconn’s plans were highly touted by many and they were central in then Wisconsin Governor Scott Walker’s economic development plans. However, in early 2019, Foxconn announced it would not build its factory, stating that assembling TVs in the United States is unprofitable. Indeed, U.S. TV production had ceased decades ago. However, Foxconn quickly reversed course after White House pressure, though its exact plans are unclear. Yet what does seem clear is that Foxconn’s initial promises will be unfulfilled (Witte, 2019).

The second example comes from Amazon’s plans for a second headquarters (HQ2; Bhattarai, 2017). The company promised the new headquarters would employ 50,000 with $5 billion in capital expenditures. Amazon stated that low business taxes and generous incentives would be key deciding factors in its location decision. 2 With over 200 cities submitting bids, Amazon announced in late 2018 that Northern Virginia and New York City were the winners, receiving about 25,000 jobs apiece. While Northern Virginia mainly celebrated, New York’s “victory” generated significant local controversy due to nearly $3 billion dollars in subsidies, as well as other costs, including more congestion and greater housing prices that could deter other businesses from locating there (Goodman & Weise, 2019). New York’s internal debate was so fierce that Amazon decided not to locate there. Indeed, this case shows how incentives can generate such widely diverging views.

Incentive proponents typically point to many potential benefits: new economic activity reinforced by a new supply chain created to serve the incentivized firm(s); enhanced local spending from newly hired employees; new state and local tax revenues; and agglomeration effects in which the new business activity pushes a region above critical thresholds, leading to a developmental takeoff. Central to these positive effects to arise is that new business start-ups and local entrepreneurship intensify to satisfy many of these new demands.

As noted above, incentives may also have adverse effects on the local economy. Indeed, key deciding factors listed in Amazon’s HQ2 RFP was a desire for low taxes but also for a range of public services, illustrating a desire for both low taxes and quality public services. 3 Incentive proponents often argue that new business activity helps “bankroll” good public services from the new revenues (e.g., former Virginia Governor Terry McAuliffe is an outspoken advocate of this view; Vozzella, 2019). Yet, if such projects generate insufficient revenue, then who pays for public services and at what level? What happens to the region’s overall competitiveness if other businesses are crowded out as other input costs bid up?

Our primary question is whether new business start-ups are crowded out by incentives. Small businesses and new businesses are especially vulnerable because tax incentives and subsidies are typically aimed at larger firms (and existing firms). As the Amazon case suggests, after attracting a large company, local policy makers will be expected to cater to its wishes, which may diverge from the needs of new and small firms in the region. Thus, while incentive proponents argue that new firms and existing small and medium-sized enterprises benefit from the new economic activity, it very well could be that they are the biggest (net) losers if the incentives crowd out enough small firms, offsetting benefits from the incentivized firm’s input purchases from small firms as well as any other local purchases from the incentivized firm’s owners and workers. 4

The net effect of incentives on local business start-ups is then critical to the current and future health of local economies. Specifically at the national level, Neumark et al. (2011) found that small firms experience disproportionately faster net job creation compared with large firms—illustrating the possibility that by incentivizing large firms, a local region would be shifting to a composition of firm sizes that typically have slower long-term job growth. Haltiwanger et al. (2013) showed that new firms, which often start small, disproportionately create more net jobs, illustrating how start-ups are a key feature of future job growth. To be sure, these studies were conducted at the national level and did not consider any “local spillovers” that affect local growth.

Higher initial shares of small firms and self-employment are also associated with subsequently faster local economic growth rates, illustrating a positive spillover (Bunten et al., 2015; Goetz et al., 2012; Komarek & Loveridge, 2014, 2015; Rupasingha & Goetz, 2013). Tsvetkova et al. (2019) found that (net) creation of self-employment is linked to both considerably higher local employment and income multipliers than for existing firms—including large firms. Hence, reducing start-ups and small business activity can have adverse consequences on short- and long-term growth. Given the recent interest in lagging regions (i.e., “left behind regions”), it is also noteworthy that small business/self-employment activity has been found to promote economic growth in lagging regions (Stephens et al., 2013; Stephens & Partridge, 2011).

Given the central place of business incentives in modern U.S. economic development policy and the importance of small businesses and new start-ups for long-term economic growth and resilience, we examine how incentives affect business start-ups. We do this by studying start-up behavior in a subset of metropolitan counties using a new tax incentive data set available from the W.E. Upjohn Institute for Employment Research (Bartik, 2017) combined with the data on business start-ups from the U.S. Census Bureau. We use several estimation techniques including an instrumental variable (IV) approach, ordinary least squares (OLS), and negative binomial (NB) analysis. The findings consistently suggest that incentives are negatively related to firm formation both in the industry groupings that received the incentives and in total. The findings suggest that tax incentives and subsidies crowd out start-ups despite their positive effects of directly supporting economic activity. Thus, incentives appear to reduce long-run job and income growth, at least when focusing on the start-up “channel,” forming a clear opportunity cost to incentive schemes.

The next section reviews relevant literature and is followed by an overview of the incentives and taxes data from the W.E. Upjohn Institute. The data and empirical methodology are then described, followed by a presentation of the estimation results and an assessment of their robustness. The final section summarizes our findings and makes recommendations for policy and future research.

Literature Review

The existing literature shows that start-ups are important for regional economic well-being. They disproportionately contribute to job creation directly and indirectly while promoting technological innovation and productivity (Fritsch, 2013; Fritsch & Mueller, 2004; Haltiwanger et al., 2013; Tsvetkova et al., 2019). Start-up rates vary widely across regions (Bosma et al., 2008; Reynolds et al., 2007), which highlights the importance of regional factors in their ability to succeed. Economic development policies often seek to stimulate business entry, particularly in some industries or places (Harger & Ross, 2016).

In general terms, state and local policy makers can promote economic development and business entry through tax policies and specific economic development incentive programs. There is a larger literature on the economic development effects of taxes because tax data are more readily available and comparable across locations. The results of tax studies, however, may be difficult to interpret because taxes also pay for public goods and services that benefit firms. Although less voluminous than the tax literature, there is also a long tradition of economic development incentives research, but there are very few studies on how standard business incentives affect start-ups (by contrast, see Hanson & Rohlin, 2011a, for how a place-based policy affects start-up rates).

Despite the increase in state and local incentives and their growing associated costs (Bartik, 2017), there is still no consensus on whether economic development incentives work, how they work, and in what types of regions, industries, and types of firms they work (Neumark & Simpson, 2015). In part, the mixed results may be attributed to difficulties in obtaining meaningful and comparable data on incentives across locations—a challenge the current paper overcomes by using a new incentive data set discussed in the next section. Another challenge is the endogeneity of incentives to local economic conditions. Bartik’s (2018) recent review concludes that most existing studies use methodological approaches likely to produce biased estimates and reports a smaller range of estimated effects when focusing on the unbiased studies only. More recent literature also indicates that mixed results may be due to heterogeneous effects across business types, locations, and industries (Patrick et al., 2017).

For example, there is a growing body of evidence suggesting that targeted economic development incentives may help some industries at the expense of others. Harger and Ross (2016) found both positive and negative effects of the New Markets Tax Credit program on employment growth, depending on the industry. Heterogeneous effects across industries are likely influenced by the fact that many incentive programs are designed so that capital incentives dominate labor incentives (Peters & Fisher, 2002). As a result, these programs should have more of an effect on the behavior of firms in capital-intensive industries and less so on those in labor-intensive industries. Patrick (2016) found that increasing capital subsidies results in decreased employment density, changes in local industry mix, and facilitates capital-labor substitution within establishments. Likewise, Hanson and Rohlin (2011b) found that labor-targeted subsidies lead to greater concentration of labor-intensive industries at the expense of capital-intensive industries.

All in all, it is plausible that economic incentives would have different effects on the behavior of start-ups compared with other types of economic activity. Given the prominent role of start-ups in growth, there is surprisingly little evidence on how economic development incentives affect them. Bruce and Deskins (2012) used counts of tax and nontax incentives in a panel framework and found a small positive relationship between tax incentives and their measures of entrepreneurial activity and a small, negative relationship between nontax incentives and sole proprietorships. Using a state-level version of the data used in this article, Tuszynski and Stansel (2018) found that incentives are negatively related to patents and small business establishments, are positively related to large business establishments, and have no significant relationship with new business formation or sole proprietorships. These two studies represent the most recent and comprehensive evidence regarding start-ups and economic development incentives. However, they both rely on the panel fixed-effects methods to address endogeneity of incentives and much more aggregate data than the present study. We use county-level data, first-differencing, IV, and other approaches to carry out a comprehensive and robust examination of the relationship between business incentives and business entry.

Overview of Incentives and Taxes

The Panel Database on Business Incentives for Economic Development, or Panel Database of Incentives and Taxes (PDIT) for short (Bartik, 2017), offers state-level information on a range of incentives and taxes that are a part of the “standard deal” offered to new medium-sized facilities that state and city officials wish to attract. It is probably the most comprehensive data source for tax incentives. 5 Although the publicly available database is reported by state, it is based on annual data for one or more cities in the state, generally the largest principle city of the state’s largest metropolitan statistical area (MSA) and other economically important MSAs. We use the unpublished city-level PDIT data for our analysis.

The measures reported by the data capture common incentives offered to what reflects a representative, incentivized firm in each industry, in contrast to occasional incentives aimed at only a few firms. The following taxes are included in the tax burden calculations: (a) business property taxes, (b) state and local sales taxes on business inputs, (c) state taxes on corporate income and state gross receipts taxes. Certain tax types such as local corporate income taxes, taxes on business income through the individual income tax system, public utility taxes, and insurance premium taxes are not included in the tax burden calculations. The incentive calculations include (a) property tax abatements, (b) customized job training subsidies, (c) investment tax credits, (d) job creation tax credits, and (e) research and development R&D tax credits.

The “deal-closing” programs are only included if program data provide useful statistics. General sales tax exemptions are included for general categories of inputs if such exemptions are not discretionary. The database also does not include tax incentive data on geographically targeted programs (e.g., enterprise zones and brownfield programs), tax-increment financing, discretionary incentives that provide sales tax relief on input purchases, and incentives with a minimum investment requirement of greater than $100 million. For each city over a 20-year period, the Upjohn model generates annual values of gross taxes before incentives, the values of incentives, and net taxes after incentives. The present value of taxes and incentives is divided by the present value of value added to generate the tax and incentive rates.

In contrast to widely used databases such as the Council for Community and Economic Research (C2ER) State Economic Development Spending Database and the Good Jobs First Subsidy Tracker database, the PDIT provides data on the present value of a comprehensive and standardized set of taxes and incentives that are applicable to any eligible business in the state and city. The C2ER spending database only details state budgetary spending on economic development, including marketing and administrative activities. It does not include incentives that are tax expenditures rather than budgetary allocations, nor does it include detail on local taxes and incentives. The Good Jobs First Subsidy Tracker database provides recipient-level detail for programs in states for which the nonprofit is able to collect data; however, the database does not include comprehensive data for all programs within a state or all states. In fact, there is considerable variation in which programs are reported within a state over time, as well as between states over time. Additionally, the Subsidy Tracker reports the undiscounted value of multiyear awards in the first year. In some cases, this is the combined value of state and local incentives and in others, it is the multiyear value of a single program award. Compared with these other sources for incentives data, the PDIT is preferable for our analysis because it provides standardized data over time for a comprehensive set of state and local taxes and incentives—avoiding artificial variation induced by state differences in reporting over time and incentives allocated through budgetary spending versus tax expenditures. Furthermore, the standardized value in the PDIT avoids the endogenous relationship between awarded incentives and economic outcomes, whereby places with better (or worse) economic outlooks award either more or less incentives.

As noted above, we use the unpublished city-level tax and incentives data to study start-ups in the cities’ MSA counties. Most of the incentive programs in the PDIT are provided through the state and are uniformly available to eligible businesses in any county in the state. Thus, some of the variation in the city-level measure is the same variation for all locations in the state. The remaining variation comes through local tax incentives, such as property tax abatements. Our use of the city-level PDIT for cities’ MSA counties assumes that the tax incentive policies of the principal city in the MSA represent the tax incentive policies of local governments in the MSA. This is a reasonable assumption given that the existing research on tax and incentives competition indicates that competitive pressures erode tax and incentive differentials between nearby locations (Agrawal, 2015). In addition, given that our empirical modelling uses first differences, we need a weaker assumption than the assumption that the principle city and its nearby suburban and exurban metropolitan counterparts have the same level of incentives. Instead, our models assume only that they raise and lower incentive packages in tandem, which is most consistent with the tax competition literature.

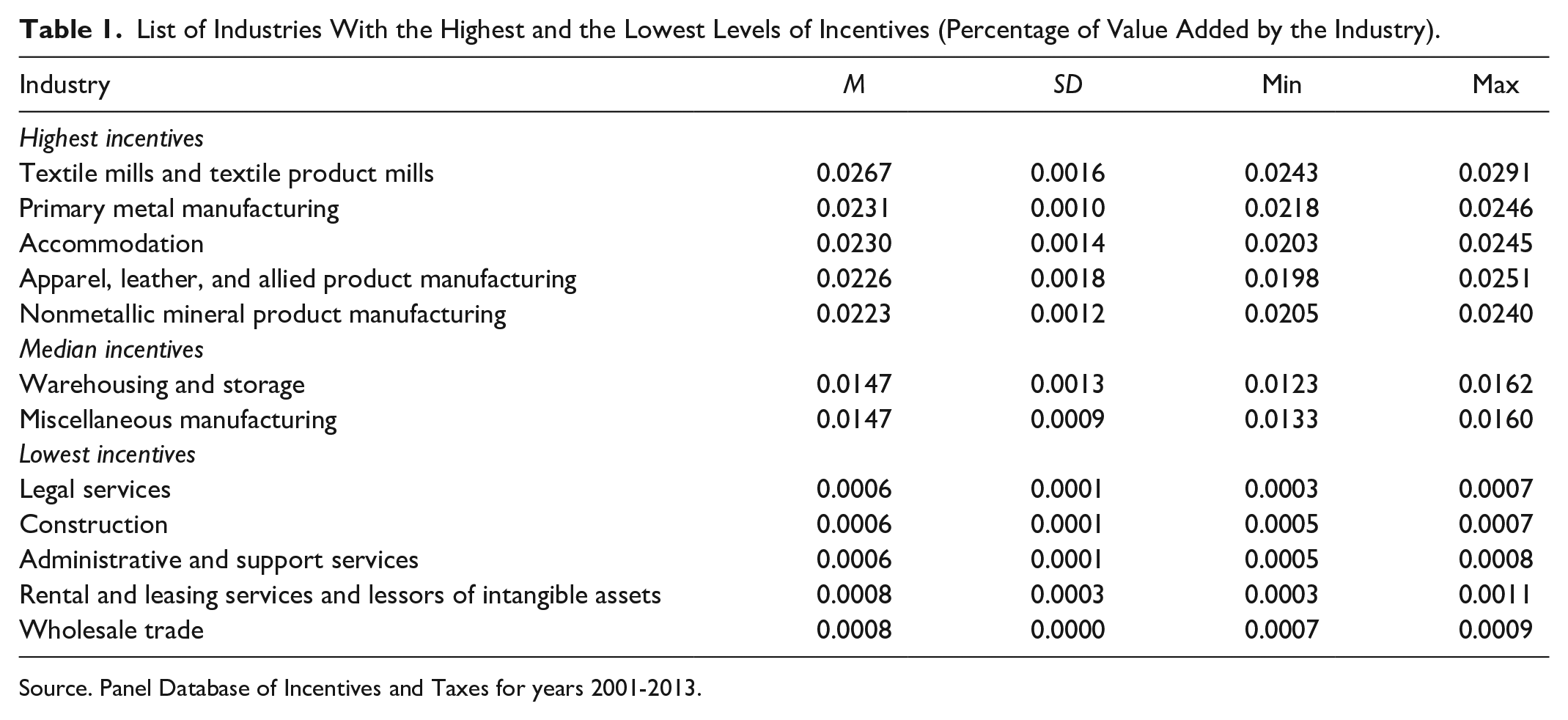

Table 1 reports the average incentives as a share of value added for the five industries that receive the highest shares, the five that receive the lowest shares, and the median tax-incentive industries during our study period. Not surprisingly, four of the five top recipients are in manufacturing, as well as hotels/accommodations, which are often subsidized in medium and large urban downtowns near convention centers and arenas. The least incentivized industries are typically in services, although construction is on the list, whereas miscellaneous manufacturing and warehousing and storage are among the median industries for incentives. 6

List of Industries With the Highest and the Lowest Levels of Incentives (Percentage of Value Added by the Industry).

Source. Panel Database of Incentives and Taxes for years 2001-2013.

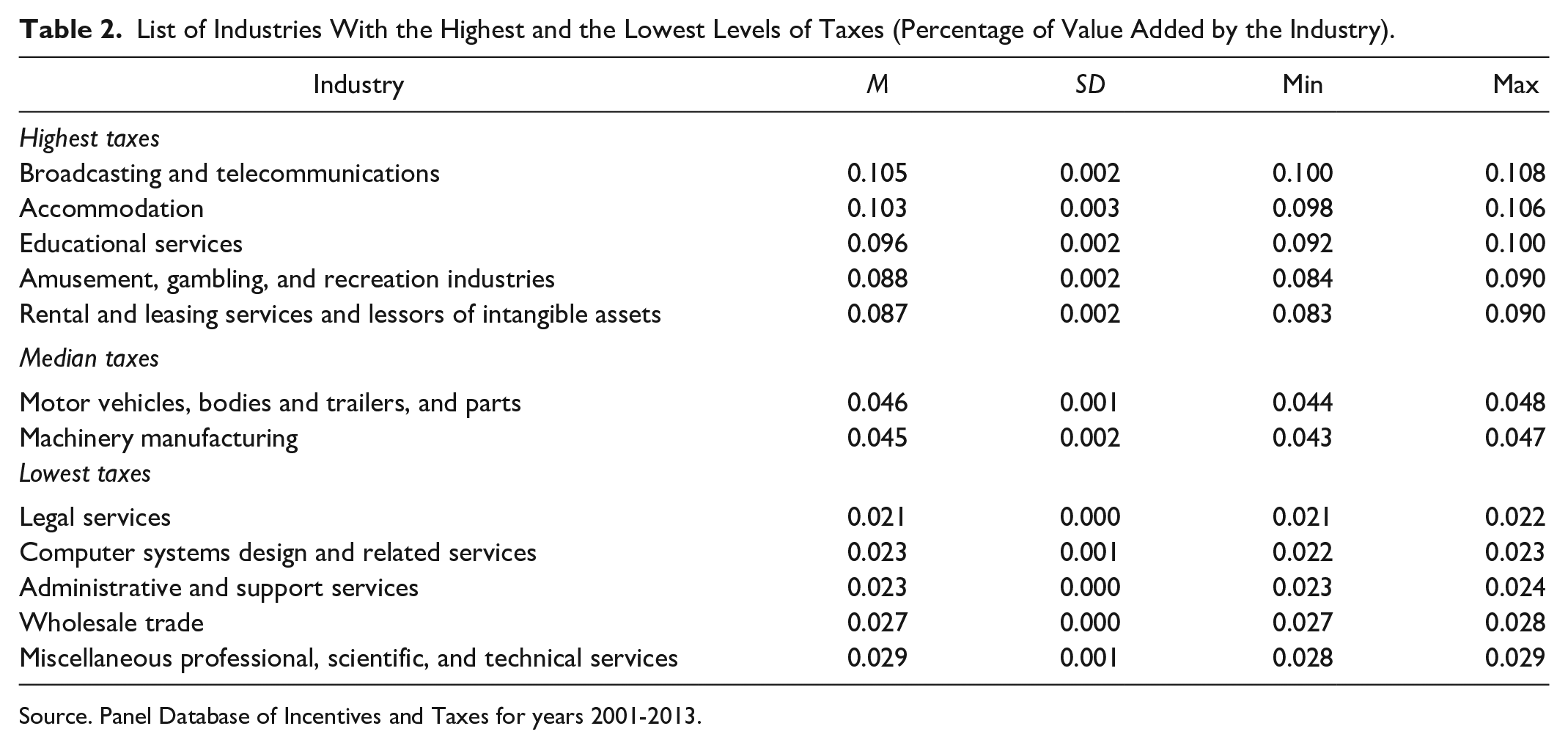

Table 2 shows the average of state and local taxes as a share of industry value added for the five industries that face the highest tax shares, the five that have the lowest tax shares, and those industries in the median. Accommodation is one of the highest taxed industries, which may be a reason why it receives higher incentives. Following the same logic, many of the lowest taxed industries are also the lowest incentive recipients. The overall correlation between total taxes and total incentives in our data set is 0.509. Yet it is noteworthy that no manufacturing industries are among the highest taxed firms, even as they are often among the highest incentive recipients.

List of Industries With the Highest and the Lowest Levels of Taxes (Percentage of Value Added by the Industry).

Source. Panel Database of Incentives and Taxes for years 2001-2013.

To estimate the effects of business incentives on U.S. county establishment births, our econometric analysis starts with the first-difference OLS along with the IV approach to further drill down into the effects of incentives. We focus on the 2001 to 2013 period due to the data availability for the dependent variable. Later we utilize count-data approaches.

Our sample is defined by the PDIT’s geographical and industry coverage. The PDIT provides incentive and tax values for 47 cities in 33 states 7 across 45 industries. As explained by Bartik (2017), city-level data are the basis for PDIT state-level aggregations reported in the data set. If two or more cities for a given state are included in the data set, the PDIT reports their average value. 8 In our analysis, we use county-level data within MSAs that correspond to the cities and states reported by the PDIT in unpublished data. 9 One advantage of this approach is that we rely on more observations in the empirical estimation. Our sample contains 261 metro counties in 40 distinct U.S. BEA economic areas (used for clustering the residuals). Because we use MSA county-level observations that proxy their incentive and tax rates from the MSA’s largest principle city, this measurement error generally biases the incentive variable’s coefficient toward zero.

We first analyze the effects of incentives on the total business start-up activity and then separately focus on export-intensive industries and manufacturing, as well as three subgroups of manufacturing industries defined by their R&D intensity. We use the PDIT-provided export and manufacturing indicators to identify export-based and manufacturing industries, respectively, and classify the latter into low, medium, and high R&D groups following Conroy et al. (2016). 10 To perform the analysis at the various levels of industrial aggregation, we calculate the magnitude of incentives by taking the total dollar value of incentives and dividing by the respective total value added in dollars.

First-Difference/Instrumental Variable Approach (Lewbel)

The first-difference Lewbel approach is our base specification. The dependent variable is the annual logged number of establishment start-ups per capita for each MSA county in the data set. The data are from the U.S. Census Bureau (the Business Information Tracking System [BITS] for business entry and annual population estimates for population). 11 To account for the county-level fixed effects, we difference the dependent variable (logged number of per-capita start-ups) over 3-year periods, and we use as the incentive explanatory variable a 3-year differences in actual incentives measured as percentage of value added. Thus, county fixed effects are removed, which, by definition, means that we also remove the MSA fixed effect for all of the MSA’s counties (along with the idiosyncratic county portion of the fixed effect). We difference over 3 years instead of 1 year because that helps alleviate measurement issues in annual data and allows for a longer period for adjustments in start-up behavior. For example, Tsvetkova and Partridge (2016) found that using 1-year first differences rather than 3-year differences yield similar findings and have greater efficiency. Additionally, the instruments perform better with 3-year differences. We cluster standard errors in all specifications at the 2004 BEA economic area level to account for spatial autocorrelation. 12

Equation 1 shows the estimated model.

where ΔY cit is a 3-year difference in log number of start-ups per capita in county c, sector i (own sector) or j (other sector), in which i stands for all industries (total); export; manufacturing; high R&D manufacturing; medium R&D manufacturing; low R&D manufacturing in year t between 2001 and 2013. 13 Incentives and Taxes refer to the total incentive measure (measured continuously as percentage of value added) and total tax measure, respectively, as reported by the PDIT (aggregated to the sector/subsector under consideration). The JobsFlow variable, described further below, is measured in year t - 3, the initial year of each 3-year differencing period. The model also includes year fixed effects (μ t ) to factor out common national (annual) patterns such as the Great Recession or the economic expansion. Appendix Table A1 (Supplementary Materials available online) provides a summary of the variable descriptions and data sources, and Appendix Table A2 (Supplementary Materials available online) presents descriptive statistics for all the continuous dependent and independent variables used in the main models.

All variables in Equation 1 (except the binary ones) are standardized by subtracting the mean and dividing by the standard deviation to obtain beta coefficients for comparability. Thus, each regression coefficient reflects the expected standard deviation change in the dependent variable in response to a 1 standard deviation change in the explanatory variable. The control variables are described in the next subsection.

The most likely specification concern is that common unobservable factor(s) such as government quality that affects both incentives and the number of start-ups introduce endogeneity. Another possibility is the direct reverse causation through the potential for start-ups to directly affect economic conditions (i.e., changes in local start-up rates may induce states and localities to alter their incentive packages). Furthermore, strong economies may give localities greater resources to offer more incentives or weak economies may prompt governments to offer more incentives to stimulate growth. Similarly, it is possible that correlation between the incentive variable and the residual could be caused by measurement error. To address any endogeneity caused by possible reverse causation and time-varying omitted variables, we use an IV approach to estimate Equation (1).

Within this approach, the potentially endogenous variable Incentives is instrumented using the 2000 value of the Incentives Environment Index (IEI) developed by Patrick (2014). The IEI measures the degree that each state’s constitution limits the ability of state and local governmental entities to use public money, credit, property, or financial relationships to aid private businesses. The IEI is based on three state constitutional provisions that arose in response to government participation in risky and failed economic development projects during the mid to late 19th century. Patrick (2014, 2015, 2016) demonstrated that the availability and financing of economic development programs within a state are directly governed by state constitutional provisions reflected in the IEI. Variation across states in events that instigated state constitutional policy responses yields remarkable heterogeneity in the provisions, and, therefore, the IEI across states.

As indicated in Patrick (2014, 2015, 2016) and in our empirical results, the IEI is a strong predictor of combined state and local economic development incentives in a location. These state constitutional provisions predate our analysis by over 100 years. This fact coupled with the arduous process of amending a state constitution and the limited likelihood that one county’s economic outcomes leads to state constitutional change yields variation that is plausibly exogenous to the changes in county start-up activity that we study. To create time variation in the instruments, we interact the 2000 IEI value with time-period dummies. The time-period interactions help identify temporal variation in the IEI value’s effect because incentives vary over time due to changes in the business cycle or changes in the intensity of their use over time.

To further improve identification over the standard IV analysis, our base analysis relies on the Lewbel (2012) procedure, which in addition to the IEI instrument, uses heteroscedasticity in the error terms to form an additional instrument (e.g., created by an omitted variable). The Lewbel instrument equals

Control Variables

In addition to the incentive measure, all models include control variables to account for the influence of other factors that the literature shows to be related to business entry. First, we include measures of regional economic activity and economic structure. The most important of these are Taxes, IndMix, and JobsFlow. The variable Taxes approximates the business tax burden in a given sector/subsector and county. It is derived from the PDIT in a way that is consistent with derivation of the incentives measure.

The IndMix variable approximates local demand shocks (also known as the Bartik instrument); higher values indicate favorable economic conditions for starting a business. It is calculated as the expected employment growth rate in a county over the 3-year period if all local industries grow at their respective national growth rates. 14 The employment data are from County Business Patterns (CBP) from the U.S. Census Bureau. Because CBP county/industry data are often suppressed for confidentiality reasons, we use data from the W.E. Upjohn Institute for Employment Research that estimates the suppressed values in the original CBP data (Bartik et al., 2018) using an algorithm from Isserman and Westervelt (2006).

The JobsFlow variable measures the approximate ease of finding a job in a different sector if an employee changes jobs or is displaced from work. After accounting for the industry structure’s direct effects on labor demand shocks (through IndMix), JobsFlow measures whether the county’s industrial structure facilitates worker movements across sectors. Thus, because it is easier for workers to move from (relatively) slow-growing sectors to (relatively) fast-growing sectors, a greater JobsFlow value should support faster job growth in response to positive or negative shocks. It also indicates greater job availability and an industrial structure that facilitates movements to new start-ups and expanding firms. Much like the industry-mix (Bartik) variable, the JobsFlow variable uses job-to-job flow information at the two-digit North American Industry Classification System (NAICS) national level from the U.S. Census Bureau Longitudinal Employer-Household Dynamics program and the county’s initial industry composition from the CBP (meaning it should be exogenous). 15

A set of socioeconomic controls is included in all models. They include employment shares in manufacturing (total); labor-intensive manufacturing; 16 agriculture and mining; 17 shares of the adult population with only a high school diploma, with some college; and with at least a bachelor’s degree (not completing high school is the omitted group). These additional control variables are measured in 1990 to minimize endogeneity concerns. Finally, all models include 3-year time fixed effects to account for common national cyclical and trend effects.

Estimation Results and Discussion

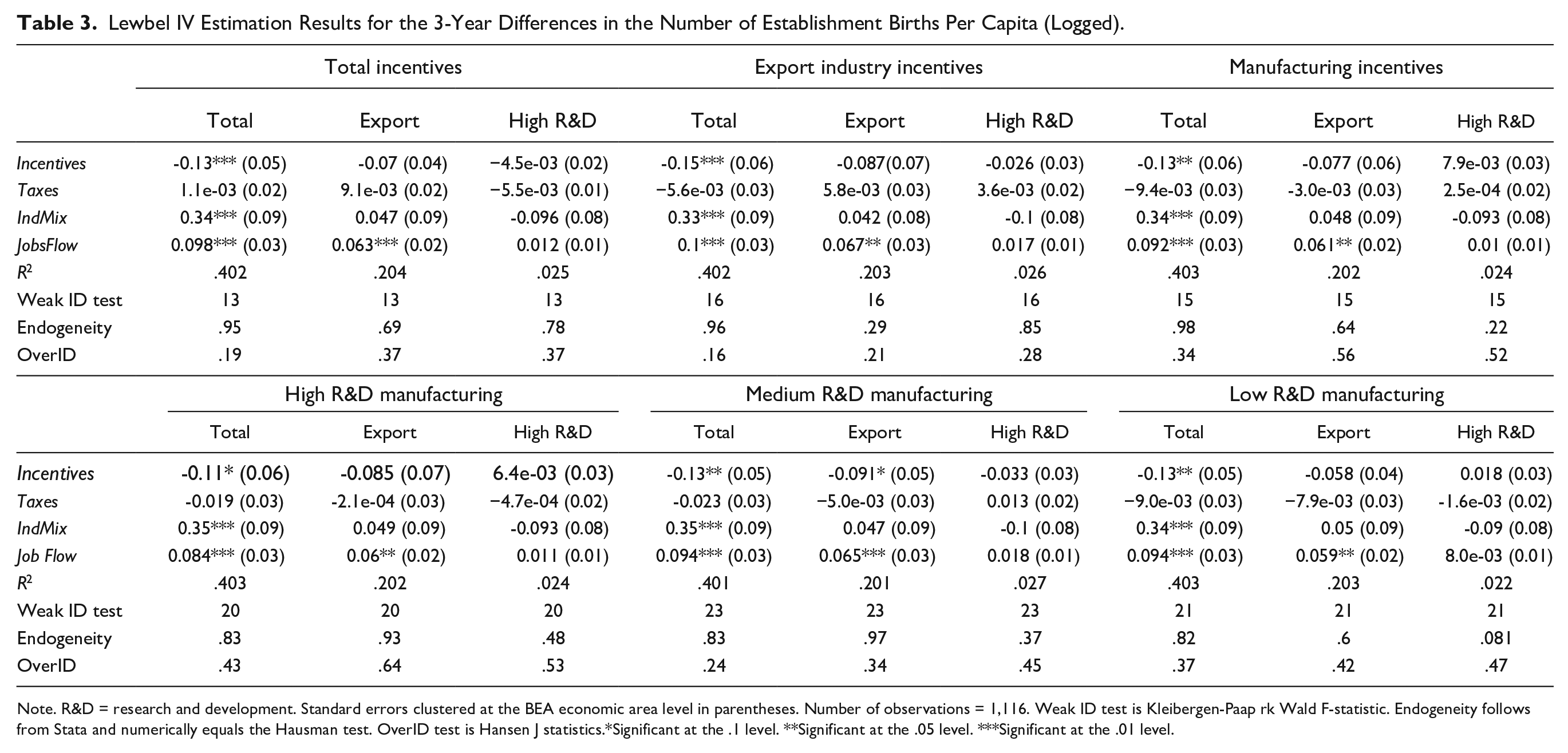

Lewbel IV Results. The Lewbel IV results are our base results, leaving discussion of the standard IV results in the next section. Table 3 reports the 3-year first-difference Lewbel IV results, in which the estimated coefficients reflect the expected effect of a 1 standard deviation change in a given variable on start-ups (measured in standard deviations). Table 3 is organized as follows: In the three columns within the “Total incentives” panel, the coefficients on Incentives, respectively, reflect the effect of a 1 standard deviation change in total incentives on (a) total start-ups, (b) export industry start-ups, and (c) high R&D manufacturing start-ups. Similarly, the three corresponding columns in the “Export industry incentives” panel, respectively, show the expected influence of export incentives on (a) total start-ups, (b) export industry start-ups, and (c) high R&D manufacturing start-ups. The other columns are organized in an analogous manner.

Lewbel IV Estimation Results for the 3-Year Differences in the Number of Establishment Births Per Capita (Logged).

Note. R&D = research and development. Standard errors clustered at the BEA economic area level in parentheses. Number of observations = 1,116. Weak ID test is Kleibergen-Paap rk Wald F-statistic. Endogeneity follows from Stata and numerically equals the Hausman test. OverID test is Hansen J statistics.*Significant at the .1 level. **Significant at the .05 level. ***Significant at the .01 level.

Before discussing the results, we note that the first-stage F-statistics (at the bottom of the table) for the strength of the instruments range from 13 to 23 (well above the rule-of-thumb value of 10), which suggests that the instruments are sufficiently strong. Furthermore, in no case do the overidentification tests reject the null hypothesis that the instruments are uncorrelated with the residuals, implying that the models are well identified. A test for endogeneity performed by STATA points that the OLS models do not suffer from endogeneity bias. However, given that endogeneity tests are often skeptically viewed, and that economic theory suggests that endogeneity bias is likely to exist, we use the Lewbel IV models as our base case. Nonetheless, we discuss the OLS results as a robustness check in the next section. 18

Turning to the specific results, a 1 standard deviation change in total incentives is associated with a -0.13 standard deviation change in total start-ups, consistent with overall crowding-out effects.19,20 For export and high R&D start-ups, total incentives also have a negative coefficient, but they are statistically insignificant. 21 For total incentives, the overall crowding out of start-ups is inconsistent with stories of positive economic multiplier effects for new business creation or related “cluster” stories being a dominant feature. 22 Similarly, incentives for export industries and manufacturing are also associated with fewer total start-ups (i.e., crowding out), while those that are statistically insignificant effect elsewhere. Turning to the subsector results, regardless of the case, total start-ups are negatively associated with incentives given to the specific subsector. Although not shown for brevity, we find that medium R&D manufacturing incentives are also inversely associated with fewer export-industry start-ups, which further supports this point.

In sum, these results suggest that incentives generally crowd out total start-ups and start-ups in other industry categories as well, which is inconsistent with the arguments of incentive proponents. For example, if a local government incentivizes a Thai restaurant in a retail district, our findings suggest that other possible Thai restaurant start-ups and other restaurant start-ups in general may be crowded out because of the new subsidized competition. In addition, because large firms are more likely to receive incentives than start-ups, start-ups may face further cost disadvantages as labor and land prices are bid up.

Regarding the interpretation of the overall tax coefficient, one needs to keep in mind the government budget constraint (Dalenberg & Partridge, 1995; Helms, 1985). The government budget constraint implies that if the government receives one more dollar of revenue, then by identity, expenditures must rise by $1 (treating the net budget balance as an expenditure category). Since both the expenditure and revenue effects simultaneously occur, one must weigh the net effects of the (likely) negative effect from higher average taxes plus the effects of an equal-sized increase in average government expenditures. One can imagine that the (probable) positive effects of government spending on factors such as education, public safety, and infrastructure could overwhelm the adverse effects of higher taxes. The point is that the tax coefficient does not only reflect the effect of taxes but also the effects of the expenditures that are funded by the new taxes.

The results suggest that state and local overall tax burdens have a statistically insignificant influence on start-ups across all cases, in which the magnitude of the tax coefficients is very small, suggesting that higher taxes themselves do not deter start-ups. These insignificant tax results also do not support arguments that start-ups are stimulated when the incentives successfully produce higher government tax revenue and expenditures.

Turning to the industry-mix demand-shock variable (i.e., Bartik instrument), the results suggest that a 1 standard deviation-sized exogenous demand shock is associated with about a 0.35 of a standard deviation increase in total start-ups, which goes in line with previous findings of the defining role of local economic conditions in economic performance (e.g., Tsvetkova et al. [2019] reported this to be the case for employment growth). What is interesting is that the negative effect of incentives is over one third of the positive size of the effect of local demand shocks (measured in beta coefficients). Together, this suggests that incentives have relatively large adverse effects on overall start-ups when considering their relative impact compared with economic shocks. By contrast, industry demand shocks are statistically unrelated to start-ups in export industries and high R&D manufacturing. This finding is also expected given that local county conditions are unlikely to define demand in these industries.

Increased labor market flexibility as indicated by an industry composition that facilitates intersector job mobility (JobsFlow) is positively associated with greater total and export industry start-ups but not high R&D manufacturing. Indeed, for total start-ups, the size of the jobs flow coefficient is nearly one third the size of the industry mix demand shock coefficient, indicating its relative importance. While not exactly the same, this finding indirectly supports those who argue that job mobility should be increased through policy changes such as limiting the enforceability of noncompete clauses or limiting state occupational licensing. 23

Robustness Tests

We further test the robustness of our results in this subsection by exploring whether the results are affected by using (a) Lewbel IV that assesses temporal heterogeneity of the results, (b) standard IV, in which the model does not utilize the additional Lewbel instrument, (c) OLS, (d) NB estimation using the number of start-ups as the dependent variable, and (e) examining several narrowly defined key industries.

The period we examine contains the Great Recession, which may produce differing results, pre, post, and during the recession. Thus, we interact a Great Recession 2007 to 2010 period dummy with our incentive variable and reestimate the Lewbel IV model (see Appendix Table A3, Supplementary Materials available online). Yet the interaction variable was economically small and statistically insignificant at the 10% level in all cases, indicating little temporal effect.

Next, we reestimated the Lewbel IV model using 1-year first differences to appraise how the estimates change (see Appendix Table A4, Supplementary Materials available online). Regarding the incentives, these results are very similar to the base results in terms of pattern and statistical significance. The main difference is that the magnitude of the results is about one third the size in the 1-year first-difference models, which is unsurprising. In sum, these results suggest that the crowding-out effects of the incentives are immediate. It would be nice to assess if the crowding-out effects persist for a decade or more in the long run. However, given the short span of our data, we are unable to explore this issue in a first-difference or panel setting to account for fixed effects. Furthermore, in long time spans, the incentive packages of localities can also significantly change, making it difficult to measure their importance. Thus, we leave it to future research to further appraise this question.

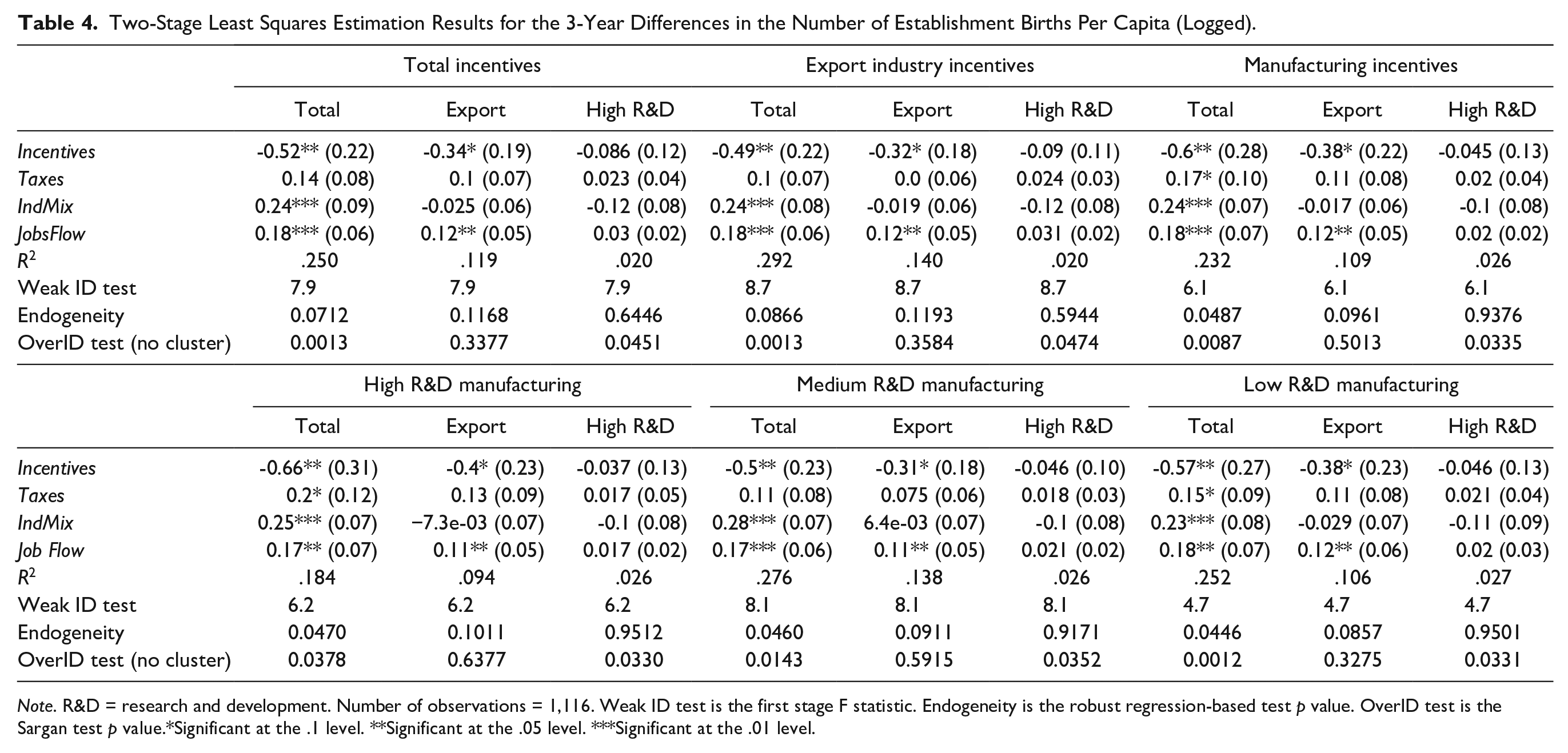

The standard IV first-difference results that only use the IEI value (and its time-period interactions as instruments) for the incentive variables are reported in Table 4. These results are qualitatively like the reported Lewbel results in Table 3. Specifically, greater total and export incentives, respectively, are associated with fewer total and export industry start-ups, whereas incentives in total manufacturing and high R&D manufacturing are associated with fewer export industry start-ups. Likewise, when we consider the effects of total incentives on start-ups, the pattern of incentive results is virtually the same as in the Lewbel IV estimation. Another interesting result is that the negative effect of total incentives on total start-ups is larger than the corresponding Lewbel result—that is, a 1 standard deviation change in total incentives is now associated with a 0.52 standard deviation decrease in total start-ups, or about double the effect of industry mix demand shocks in the standard IV estimation and about four times greater than the response of total start-ups to total incentives in the Lewbel model.

Two-Stage Least Squares Estimation Results for the 3-Year Differences in the Number of Establishment Births Per Capita (Logged).

Note. R&D = research and development. Number of observations = 1,116. Weak ID test is the first stage F statistic. Endogeneity is the robust regression-based test p value. OverID test is the Sargan test p value.*Significant at the .1 level. **Significant at the .05 level. ***Significant at the .01 level.

Although the standard IV results suggest a much larger negative response for start-ups, the key reason we prefer the Lewbel model over the standard IV is that the multivariate F-statistics for the strength of instruments in the standard IV model range from four to nine—or below the rule-of-thumb threshold of 10 for strong instruments. Conversely, the corresponding Lewbel model first-stage F-statistics are always over 13 and the specification testing suggests that the Lewbel models are well identified. Finally, as for the Lewbel models, the endogeneity test does not reject the null hypothesis of no endogeneity in the standard IV estimation.

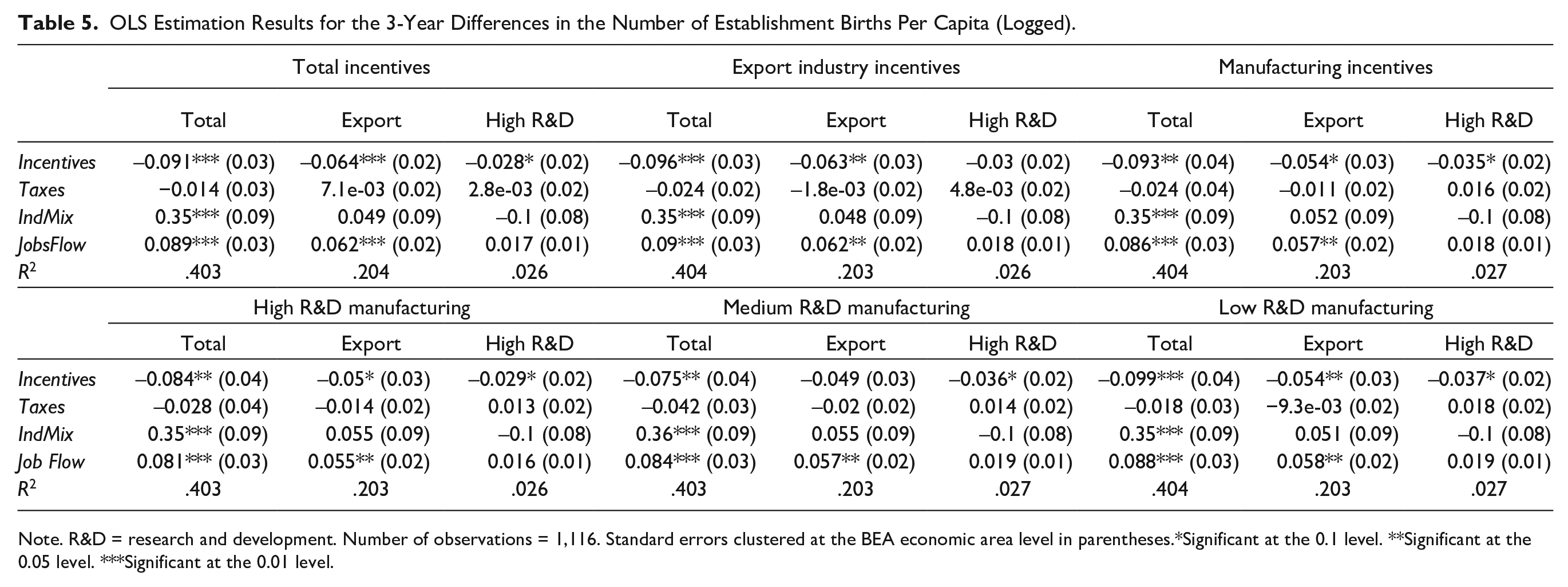

Given that both the Lewbel and the standard IV models suggest that endogeneity may not be a concern, we also estimate first-difference OLS models that are reported in Table 5. These results are also quite consistent with the Lewbel estimates. A couple of noteworthy differences are that now total, manufacturing, and high R&D incentives are statistically significant and negatively related to high R&D manufacturing start-ups (and the same applies to low R&D and medium R&D manufacturing incentives). Similarly, incentives in manufacturing and high R&D manufacturing have a statistically significant negative relationship with export start-ups. There is no OLS case in which incentives have a statistically significant positive coefficient and we continue to find little evidence that the overall tax burden deters start-ups. In sum, the OLS results make an even stronger case that incentives crowd out start-ups.

OLS Estimation Results for the 3-Year Differences in the Number of Establishment Births Per Capita (Logged).

Note. R&D = research and development. Number of observations = 1,116. Standard errors clustered at the BEA economic area level in parentheses.*Significant at the 0.1 level. **Significant at the 0.05 level. ***Significant at the 0.01 level.

We model start-ups in a log change form (approximately percentage change) because that is economically more meaningful in assessing their growth rates. However, given that start-ups originate as count data, a Poisson or a NB estimation is an alternative modelling procedure. Thus, as another robustness test, we estimate count models, in which we choose the NB approach because the start-up dependent-variable counts are overdispersed, given the large differences in the size of county population. However, we do not use the zero-inflated NB version because MSA counties tend to have at least one start-up in each of our categories.

In the NB models, we follow a two-stage procedure; wherein the first step, we regress incentives from the PDIT on IEI, its time interactions, and all controls and use the predicted value as an explanatory variable in the second step. Our NB models include all controls as well as year and state fixed effects. Because we do not correct the standard errors for using a predicted incentive value in the model (errors are not bootstrapped), the standard errors are not exactly accurate, although we cluster them at the BEA economic area. Clustering should account for correlations within economically linked regions; nevertheless, the statistical significance of the NB models should be interpreted with some caution.

The NB results reported in Appendix Table A5 (Supplementary Materials available online) continue to suggest a story consistent with the previously reported tax and incentive results. 24 All types of incentives appear to crowd out total start-ups. Another general result is that average state and local tax burdens play no statistical role in affecting start-up counts, which is in line with the previously reported results.

Finally, using the Lewbel IV models as before, we examine some more disaggregated results for seven key industries (not shown for brevity): food, beverage, and tobacco manufacturing; computer and electronic product manufacturing; electrical equipment, appliance, and component manufacturing; motor vehicles, bodies and trailers, and parts manufacturing; other transportation equipment manufacturing (mainly aircraft); computer systems design and related services; and accommodations (hotels are highly incentivized in downtowns and near stadiums and convention centers). We examine the effects of incentives in these industries on start-ups: in total, in their own industry, export industries, manufacturing, and high R&D manufacturing. Yet there is no case where the incentive effect is positive and statistically significant at the 10% level, while estimation coefficients are almost all negative. Regarding total start-ups, incentive coefficients are negative and statistically significant in five of the seven cases and are statistically insignificant in six cases for start-ups in their own industry. The only significant coefficient in own industry is in the motor vehicles, bodies and trailers, and parts manufacturing where incentives in this industry decrease own start-up rates. Finally, incentives in accommodation reduce export-industry start-ups. Furthermore, the findings remain the same for overall taxes with statistically insignificant coefficients except for a negative and significant coefficient for food processing start-ups.

Conclusion

Using data from the Panel Database on Business Incentives for Economic Development (Bartik, 2017) and the U.S. Census Bureau’s BITS, we estimate the effects of business incentives on establishment births in U.S. counties. According to our preferred empirical approach, which addresses the endogeneity of incentives by differencing out county fixed effects and by using the Lewbel (2012) IV procedure, a 1 standard deviation change in total incentives is associated with a -0.13 standard deviation change in total start-ups. Incentives for export industries and for manufacturing, in particular, are negatively associated with the change in total start-ups. These findings suggest that, in contrast to their intended purpose, incentives crowd out new firms, and the crowding out effect is so large that it offsets any effect incentives might have in attracting new firms to U.S. counties. We further find that the state and local tax burden has no statistical effect, but local demand shocks and intersector job mobility are both positively associated with higher total start-up rates.

We conducted multiple robustness checks because all our individual approaches may have limitations. Yet these findings consistently point to the base pattern described above. Taken together, these findings suggest that, while the overall tax burden does not deter new firm formation, incentives may crowd out new firms that would have formed in the absence of the incentives themselves, and this negative effect is only partially offset by favorable shocks to local labor demand shocks or an industrial composition that facilitates high intersector job mobility. Indeed, policy makers need to better account for such adverse spillover effects from incentives in their decision making rather than using (often overhyped) direct effects. An important caveat of the reported findings is that we treat all new businesses as homogenous and are unable to account for the “quality” of the start-ups that are crowded out. If incentives improve performance of firms that benefit from them (in terms of increased employment, higher productivity, and/or other important metrics) and this improved performance outweighs the loss of economic activity resulting from crowding out as a result of incentives, the reported results are less discouraging. Economic theory, however, and the existing evidence seem to suggest that this case is unlikely.

Future research should investigate heterogeneous effects of incentives and the overall tax climate across industries and should focus more broadly on identifying what local policy makers can do to effectively incentivize new business formation with its strong long-term economic growth effects, rather than incentivizing large firms that dominate the incentive arena. Our research findings of a positive relationship between enhanced intersectoral labor mobility and business start-ups invite more research on the effects of promoting labor market flexibility through, for example, policies that limit noncompete contracts or state-level occupational recertification.

Supplemental Material

EDQ916249_APPENDIX – Supplemental material for The Effects of State and Local Economic Incentives on Business Start-Ups in the United States: County-Level Evidence

Supplemental material, EDQ916249_APPENDIX for The Effects of State and Local Economic Incentives on Business Start-Ups in the United States: County-Level Evidence by Mark Partridge, Sydney Schreiner, Alexandra Tsvetkova and Carlianne Elizabeth Patrick in Economic Development Quarterly

Footnotes

Acknowledgements

Mark Partridge appreciates the partial support of the Agriculture and Food Research Initiative Grant #11400612 “Maximizing the Gains of Old and New Energy Development for America’s Rural Communities.” The views expressed are solely of the authors and can in no way be taken to reflect the official opinion of the OECD or its member countries.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.