Abstract

Drawing on institutional theory, we position CSR reports as a crucial communication practice that provides evidence of shared norms, values, and relationships among organizations operating within the institutionalized environment. Through Fortune Global 500 companies’ CSR reports published in 2018 and using named entity recognition, we analyzed interorganizational networks to understand the driving forces behind CSR institutionalization. After fitting exponential random graph models (ERGMs) to the network, we found that standards-setting organizations played the most prominent role. In addition, we identified distinct sectoral preferences in companies’ interorganizational positioning in relation to legitimacy-granting organizations such as (inter)governmental agencies and financial organizations. We discuss the implications of the emphasis on standardization, sectoral differences, and network dynamics among various legitimacy-granting organizations on CSR institutionalization and CSR reporting as communicative constitution of institutional legitimacy.

Introduction

Contemporary corporations are increasingly expected not only to integrate societal and environmental concerns into business decisions (i.e., do corporate social responsibility or CSR) but also to engage with a wide array of stakeholders and communicate about their ongoing CSR efforts (i.e., talk about or communicatively signal CSR) (Bator & Stohl, 2011). Accordingly, CSR reporting practices have garnered growing attention as organizational tools to communicate attention to issues beyond the economic, technical, and legal requirements. Research findings in recent years have indicated that CSR reports positively influence stakeholders’ perceptions of the organizations (Michelon et al., 2015) and that CSR reporting itself has become an institutionalized practice (Shabana et al., 2017).

Institutionalization is defined as “the processes by which societal expectations of appropriate organizational action influence the structuring and behavior of organizations in given ways” (Dacin, 1997, p. 48), and occurs as social actualities gradually take on a rule-like status in a given environment (Meyer & Rowan, 1977). When a practice is institutionalized, it connotes that the practice has become part of a generally accepted norm and culture in social systems. With CSR, organizations can utilize formal CSR reporting as a normative behavior to construct the meanings of their CSR activities and gain institutional legitimacy. To do so, they often look to various stakeholders operating within the same environment, including collaborative partners (Scalet & Kelly, 2010) and standards-setting organizations (e.g., The Global Reporting Initiative) for guidance on acceptable and desirable practices. Organizations may also explicitly refer to those external actors and their relationships within CSR reports to communicate the relevance and significance of their CSR activities (Shumate & O’Connor, 2010a).

Drawing on institutional theory (DiMaggio & Powell, 1983), we position CSR reporting as an institutionalized practice and argue that content in CSR reports provides evidence of shared norms, values, and relationships among organizations. Even though the reports are produced by individual organizations, an analysis of CSR reports across companies can reveal organizations that are pivotal to the implementation and communication of companies’ CSR. Thus, we used a sample of Fortune Global 500 companies’ CSR reports in 2018 (n = 113) and the named entity recognition method for extracting mentioned organizations (Finkel et al., 2005) in order to examine (a) interorganizational networks constructed via CSR reports of multinational corporations (MNCs); (b) which of the organizations in the networks may be prioritized over others and how they shape the institutionalization of CSR reporting practice; and (c) whether particular sectoral differences exist in constructing the networks through CSR reporting.

Exploring these issues will enhance our current understanding of CSR and CSR reporting practices in three main ways. First, this exploration will reveal the landscape of institutionalized CSR practices and reporting (i.e., the major organizations instrumental to CSR implementation and communication). As most existing studies have focused on specific types of organizations and their relationships (e.g., NGOs, Shumate & O’Connor, 2010a; financial ratings, Flammer, 2013; standards-setting organizations, Scalet & Kelly, 2010; regulatory entities, Arya & Zhang, 2009), taking a comprehensive look at the complicated interorganizational networks constructed in MNCs’ CSR reports will reveal valuable insights into the key actors of all types and their relative importance. Second, exploring sectoral preferences will help to contextualize strategic CSR reporting patterns by acknowledging the unique concerns of industry sectors. Finally, we theorize that companies’ CSR practices and meanings are constructed through their interorganizational positioning via CSR reports, which will enhance our understanding of CSR as a communicatively institutionalized practice.

Literature Review

Institutionalization of CSR and CSR Reporting

Institutional theory helps to explain how certain patterns of organizational behaviors emerge and become “authoritative guidelines” (Scott, 2004, p. 408). Scholars adopting this theory view CSR as an emerging field and examine how the relationships between companies and their external environment shape activities through legal, moral, and/or cultural mechanisms (Avetisyan & Ferrary, 2013). Much of CSR research applying institutional theory has concluded that CSR practices are bounded by expectations of various stakeholders as well as the pressure to become similar to other companies operating in the same environment (i.e., isomorphic pressure; DiMaggio & Powell, 1983; Martínez-Ferrero & García-Sánchez, 2017).

Scholars have also suggested that it is not only CSR practices that have become institutionalized, but also how organizations communicate about their CSR to stakeholders (Campbell, 2007; Shabana et al., 2017). Although there is no unified regulatory mechanism, public CSR reporting has become a norm across contexts (Tschopp & Huefner, 2015) due in large part to isomorphic pressure (Shabana et al., 2017). Communication scholars have advanced our understanding of how institutionalized CSR is reinforced and transformed through the constitutive role of communication; that is, CSR reports are “a significant communicative platform for the institutionalization of CSR” that allows for stakeholders’ expressions, exchanges, and co-constructions of meanings of CSR (Lee, 2020, p. 293). In line with this notion, O’Connor and colleagues (O’Connor & Gronewold, 2012; O’Connor et al., 2017; O’Connor & Shumate, 2010) have utilized companies’ CSR reports to examine CSR institutionalization as both “a process and an outcome, representing the manner of attaining a social order that reproduces itself, as well as a state of having realized this order” ((Colyvas & Jonsson, 2011, p. 38); as cited in O’Connor et al., 2017). Considering that institutionalization takes time to materialize and is thus difficult to identify while it is happening (O’Connor et al., 2017), analyzing CSR reports offers a feasible way to not only understand institutionalized CSR (i.e., an outcome) but also generate insights into the institutionalization of CSR (i.e., a process) indirectly by showing the patterns of reproduction of CSR communication.

By publishing CSR reports, organizations can communicatively signal that their actions are desirable and consistent with the socially constructed norms, thereby gaining legitimacy (Dowling & Pfeffer, 1975; Shabana et al., 2017). In doing so, they can position themselves strategically in their external environment by signaling their relationships with other actors to gain institutional capital (O’Connor & Gronewold, 2012). Especially when existing norms or standards are unclear, organizations tend to imitate other actors to reduce uncertainty about acceptable practices (Shumate & O’Connor, 2010b). In this way, isomorphism manifests at the interorganizational level and contributes to defining what is normal (DiMaggio & Powell, 1983; Shumate & O'Connor, 2010a; Sommerfeldt & Xu, 2017). Though it is not feasible to directly test isomorphic pressure through CSR reporting, examining which actors companies rely on when articulating their CSR effort will reveal the invisible interorganizational infrastructure and influential actors within the institutionalized environment.

In sum, if we view CSR reports as a platform in which organizations communicate the intentional framing of their actions and position, actors mentioned within CSR reports should carry communicative significance. Specifically, entities frequently mentioned across established companies’ CSR reports are likely to be major actors who are believed to have power to grant legitimacy and institutional capital. In turn, we can interpret those major actors as playing instrumental roles in the institutionalization of CSR and CSR reporting. To identify major actors that serve as institutional forces, we ask the following research question (RQ):

Who are the major actors in Fortune Global 500 CSR reports?

Interorganizational Positioning in CSR Reports

To examine MNCs’ interorganizational positioning—i.e., companies’ intentional macro communication practice to position themselves within a network of organizations as relevant and legitimate partners (adapted from institutional positioning; see McPhee & Zaug, 2008)—we consider four main types of stakeholders that influence companies’ institutional legitimacy: regulatory agencies, standards-setting organizations, financial organizations, and nongovernmental organizations (NGOs). In institutionalized environments, these organizations hold the power to establish, regulate, and monitor industrial standards or serve as strategic partners. Due to their ability to set the parameters for what is (or is not) desirable and motivate companies’ CSR activities, they can be considered legitimacy-granting organizations. Companies’ efforts to construct themselves in relation to such legitimacy-granting organizations are key to unpack both what they do with and how they communicate about their CSR practices (Yang & Saffer, 2019).

Regulatory agencies

Regulations are put forward by groups given authority to limit or facilitate the behaviors of particular sectors or organizations. At the nation-state level, governments can use their position to enforce regulations upon private companies within the national boundary (e.g., Environmental Protection Agency in the United States). At the global level, interorganizational agencies such as the Word Trade Organization (WTO) and the United Nations (UN) can also put forward guidelines and international laws for multinational corporations to abide by (Scherer & Palazzo, 2011). These regulatory agencies are key stakeholders of MNCs because of their ability to grant institutional legitimacy when companies engage in CSR practices within the existing regulations.

However, regulatory agencies’ role in CSR institutionalization may be diminishing for a few reasons. National governments are not able to sufficiently regulate activities related to transnational causes and effects, such as global warming and deforestation (Scherer & Palazzo, 2011). In addition, government regulations often fail to adapt quickly to changes in economic, social, and environmental needs (Polishchuk, 2009). Intergovernmental agencies also face limitations due to their non-intervention principles in nation-states and the influence of national egoisms (i.e., weak enforcement mechanisms; Scherer & Smid, 2000). Most important, the contemporary notion of CSR emphasizes collaborative and dialogic approaches by which MNCs develop their responsibilities and impacts with a larger set of stakeholders (Stohl et al., 2017), instead of merely relying on laws and regulations. Thus, an empirical investigation is warranted to examine the extent to which MNCs draw on regulatory agencies in their CSR reports, compared to other types of stakeholders we discuss below.

Standards-setting organizations

We define standards-setting organizations as those operating independently from regulatory agencies to provide guidelines and standards for CSR (either issue-oriented or comprehensive), which are to be adopted by companies voluntarily. A prime example is the International Organization for Standardization (ISO), which is “the world’s largest developer of voluntary International Standards” based on a consensus among global experts and national delegations (ISO, n.d.). Although the extent to which companies accommodate different stakeholders’ expectations may vary across market conditions (Avetisyan & Ferrary, 2013), scholars have begun to recognize organizations’ growing attention to broader international standards concerning CSR (Moratis & Widjaja, 2014).

We may expect MNCs to draw on standards-setting organizations, possibly more than regulatory agencies, for several reasons. Research suggests that regulative forces play an important role in the early phase of institutionalization, but normative forces operate more strongly in later phases (Delmas & Montes-Sancho, 2011). Considering how CSR has grown significantly as a field and become an expected practice, companies in the contemporary global context likely engage in voluntary initiatives to draw on norms and standardization than merely respond to regulative forces. The normative forces created by standards-setting organizations can also help to fill governance gaps and fine-tune existing expectations (Utting & Marques, 2010). Given the constant scrutiny MNCs face, following international standards can allow them to reconcile different expectations across market economies and gain positive evaluations from a wide range of stakeholders (Kang & Moon, 2012). Due to the limited insights available about the role of standards-setting organizations in the extant literature (Moratis & Widjaja, 2014), we pose the following RQ to explore their relative importance in institutionalized CSR reporting:

To what extent do MNCs draw on standards-setting organizations, compared to regulatory agencies, in their CSR reporting?

NGOs

NGOs can serve as MNCs’ strategic partners and help to contextualize and demonstrate companies’ commitment to CSR (Shumate & O’Connor, 2010a). NGO alliances enhance MNCs’ social capital because the public tends to trust NGOs more on issues related to the public good (Wootliff & Deri, 2001), and functional differences between MNCs and NGOs can be leveraged to construct social, political, and economic values (Liu & Shin, 2019; Shumate & O’Connor, 2010b). Overall, past studies have shown that corporations try to communicatively constitute their legitimacy through disclosing their alliances with NGOs in public reports. However, limited empirical evidence is available about the role of NGOs in institutionalized CSR reporting in comparison to other types of legitimacy-granting organizations.

A key limitation of NGO alliance network found in public reports is related to the fact that companies selectively report their relationships with NGOs. As Shumate and O’Connor (2010b) suggest, companies may highlight some alliances in their CSR reports but not others if they perceive risks associated with communicating about certain affiliations (e.g., when their NGO partners also share relationships with competitors). Compared to such uncertainties and risks associated with reporting NGO alliances, regulatory agencies and standards-setting organizations provide companies with rules and norms that are clearly spelled out, reducing uncertainty about how to respond to various demands and expectations in the institutionalized environment. Hence, we expect regulatory agencies and standards-setting organizations to play a more prominent role in MNCs’ CSR reports than NGOs.

Standards-setting organizations (H1a) and regulatory agencies (H1b) are more popular compared to NGOs in MNCs’ CSR reports.

Financial organizations

MNCs today separate financial reporting and CSR reporting because, from the view of financial stakeholders or investors, CSR reports can lack comparability and decision-useful information (Tschopp & Huefner, 2015). Nevertheless, with the growing emphasis on a multistakeholder approach to CSR, MNCs pay increasing attention to socially responsible investors as they seek to achieve financial gains through their CSR reporting (Renneboog et al., 2008). Research suggests that the demand is high for MNCs to have their CSR reports independently assured by accounting and financial auditing firms so as to reduce errors and possible cost of capital (Ballou et al., 2018). Such CSR assurance gives investors more confidence in the credibility, benefits, and outcomes of MNCs’ CSR practices (Chen et al., 2016). Given this trend, we can expect financial organizations to be highly visible in large global companies’ CSR reports as compared to other types of for-profit stakeholders.

However, the presence of financial organizations may be less strong compared to standards-setting organizations and NGOs. When MNCs communicate about their CSR activities, shareholders are important, but only a subset of the global audience. Companies’ annual financial reports are more specifically targeted at financial stakeholders (Roychowdhury et al., 2019), and their CSR reports need to be inclusive of various stakeholders to engage with a wider audience. Further, MNCs are likely to be motivated to accumulate institutional legitimacy beyond capital gains by communicating about their CSR (Chen et al., 2016). To do so, they may exercise caution in their CSR communication so as not to appear accommodating financial organizations’ expectations, and instead, draw on global norms, standards, and strategic partnerships that will provide them with normative and regulative capital. Hence, we hypothesize:

Financial organizations are more popular in MNCs’ CSR reports than other types of for-profit stakeholder organizations (H2a), but less popular when compared to standards-setting organizations (H2b) and NGOs (H2c).

Contextual Factors Influencing Interorganizational Positioning in CSR Reports

Corporations’ interorganizational positioning in CSR reports may be influenced by various contextual factors, such as sociocultural expectations and economic conditions (e.g., Avetisyan & Ferrary, 2013; Kang & Moon, 2012). To gain a comprehensive understanding of MNCs’ institutionalized CSR reporting in the global environment, we focus on two specific factors that transcend national boundaries: global issues and sectoral characteristics.

Global issues

In MNCs’ communicative effort to gain legitimacy through CSR reporting, they likely make decisions about which global issues to highlight in reports. Stakeholders, especially activist organizations, often select a particular issue domain before targeting companies to situate themselves as relevant and powerful actors (Hendry, 2006; Yang, 2020); thus, which issue(s) to focus on in CSR reports can be a consequential decision. Past research has examined global corporations’ CSR initiatives and practices focusing on issues ranging from worker safety and rights (O’Connor & Shumate, 2010; Stohl et al., 2017) to labor abuses (Yu, 2009) to the environment (Flammer, 2013) to anti-corruption (Joseph et al., 2016)—all of which are specified in the UN Global Compact’s Ten Principles (United Nations, 2021) as the minimum responsibilities of corporations. Global movements against business practices negatively affecting such public issues have increasingly necessitated CSR to involve strategic justification of companies’ goals and priorities in terms of specific issue domains (Heath, 2002).

Although comparative studies on which issues matter more to contemporary MNCs’ CSR are unavailable, business experts and scholars alike suggest that addressing environmental issues has become essential in companies’ ability to gain institutional legitimacy. For example, Epstein (2018) identify environmental protection as one of the central issues to cover in best practices of CSR regardless of industries; and Allen and Craig (2016) note climate change as the most challenging global problem that can redefine what CSR means for today’s organizations. Research also suggests that investors hold favorable views of companies with higher ratings on environmental performances, enhancing possibilities of their share price increasing (Flammer, 2013). In addition, due to mimetic isomorphism, companies’ environment-friendly practices have converged (González-Benito & González-Benito, 2010; Martínez-Ferrero & García-Sánchez, 2017). These findings indicate that MNCs’ attention to environmental issues has become no longer an option but a necessity for their survival and growth. Accordingly, we may expect MNCs’ interorganizational positioning in CSR reporting to highlight their alliances with NGOs focusing on environmental protection in order to create discursive values (Shumate & O’Connor, 2010b). Hence, we hypothesize that MNCs’ CSR reporting will communicate about their relationships with environmental NGOs more frequently than other types of NGOs. H3: Environment NGOs are more popular in MNCs’ CSR reports, compared to NGOs in other global issue domains.

Sectoral characteristics

Business industry sectors vary in their characteristics that can influence the institutionalization of CSR in different ways, such as how close they are to consumers in the value-chain and types of product (Rowley & Berman, 2000). In this study, we focus on the extent to which the business poses direct risks to health, safety, and environment (i.e., high- versus low-risk sectors; see Young & Marais, 2012). For example, industry sectors that exploit natural resources in their manufacturing processes and/or can cause hazardous effects on human conditions (e.g., mining, petroleum, and pharmaceutical) are considered high-risk; comparatively, industries focusing on consumer services and information technology (e.g., finance, entertainment, telecommunication, and software) are considered low-risk.

Research has shown that high-risk sectors are highly institutionalized due to regulatory requirements related to safety and stakeholder activism that works as coercive isomorphic pressure (see O’Connor et al., 2017; Young & Marais, 2012). In contrast, low-risk sectors may leverage flexibility in how they frame their CSR by focusing on philanthropy and diverse social issues (Tagesson et al., 2009). While such sectoral patterns have been identified and provide valuable insights about CSR communication (see O’Connor & Shumate, 2010), how companies in high- and low-risk sectors engage in interorganizational positioning in CSR reports remains unclear. On the one hand, due to the high level of institutionalism and expectations for normative practices, high-risk sectors likely draw heavily on and emphasize their relationships to regulatory agencies so as to minimize potential risks and enhance institutional legitimacy. On the other hand, they may try to differentiate themselves from other companies within the same sector to gain social capital by intentionally signaling their relationships with diverse stakeholders. For instance, O’Connor and Gronewold (2012) revealed that CSR disclosure documents of companies in the petroleum industry used both institutional language (i.e., accommodating regulations and laws) and competitive language (i.e., strategically describing themselves and their CSR as superior to companies in the same sector). Based on this finding, we may expect that companies in high-risk sectors will not only position themselves in relation to regulatory agencies but also establish themselves as competitive partners by indicating their affiliations with other stakeholder organizations. Even though companies often utilize ambiguous language to present abstract values in their CSR communication (O’Connor & Shumate, 2010), they likely mention specific organizations in constructing interorganizational networks within their CSR reports. Examining such explicit indications of various legitimacy-granting organizations will help us understand the varying roles played by those stakeholders in institutionalized CSR reports in high- versus low-risk sectors. To that end, we ask the following RQ: RQ3: How does popularity of regulatory agencies, standards-setting organizations, financial organizations, and environmental NGOs differ between high- and low-risk industry sectors?

Method

Data Collection

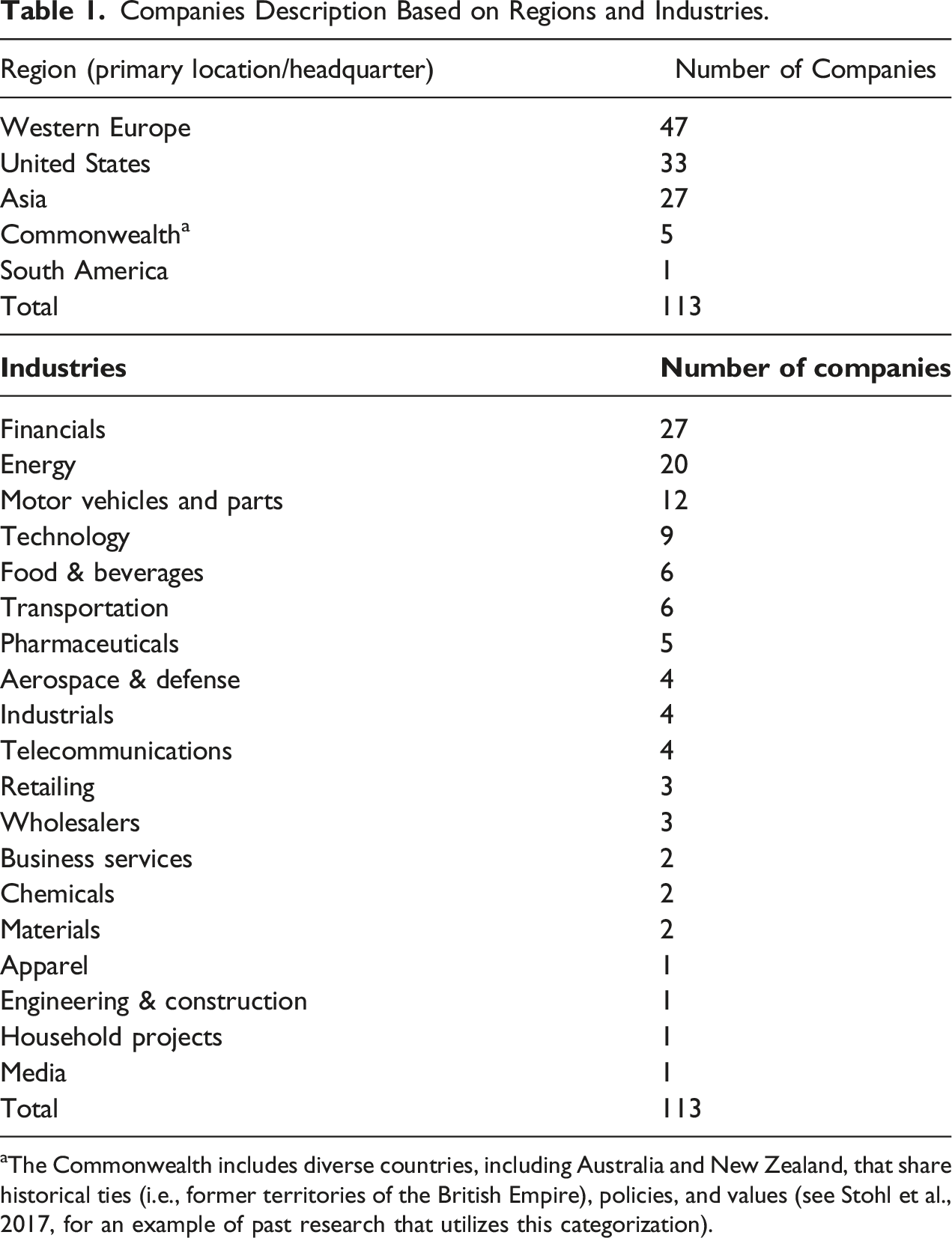

We engaged in a multi-step process to collect MNCs’ CSR reports for this study. First, because we aimed to identify companies with steady global presence and influence to understand institutionalized CSR reporting practices, we considered the Fortune Global 500 lists not only from the year we collected the data (2018) but also five and 10 years earlier (2013 and 2008). By comparing the three lists, we found 297 companies that were consistently listed over the decade. Second, two trained research assistants (RAs) used the list of the 297 companies and searched for their CSR reports published in 2018 (the year in which our data collection occurred) from their official websites. When multiple reports were published in the same year, RAs were instructed to save the most recent report. During this research process, the RAs noted companies that did not make their full CSR reports accessible or had their CSR reports written in languages other than English. After discussions between the authors and the RAs, we decided to eliminate those companies from our data set, resulting in a reduced list of 113 companies.

Companies Description Based on Regions and Industries.

aThe Commonwealth includes diverse countries, including Australia and New Zealand, that share historical ties (i.e., former territories of the British Empire), policies, and values (see Stohl et al., 2017, for an example of past research that utilizes this categorization).

Data Processing and Analysis

To extract the network of organizations from collected CSR reports, we first processed all the texts in the pdf documents into data frames in R. Then, we relied on Stanford’s natural language processing backend (Finkel et al., 2005) for named entity recognition (NER). After extracting mentioned organizations in each CSR report, we first retained organizations that were mentioned at least twice in each report to ensure these organizations were not merely fleeting mentions, and then proceeded with manual data cleaning. The NER algorithm over-identified organizations. For example, any phrases with initial letters capitalized (e.g., the Labor Committee or a section title Compliance Report) were recognized as organizations. Over-identifying was good news because it meant that the organization list was comprehensive. As a result, we manually cleaned the dataset by eliminating these errors. The final network ties emerged from these CSR reports based on Fortune 500 companies’ mentions of all organizations and companies in their CSR reports. For example, if company A mentioned Organization B, then a directed tie from A to B was established in the network.

After data cleaning, the network contained 3042 edges (i.e., ties) among 652 unique organizations, including the 113 Fortune Global 500 companies. By reading each organization’s “about us” page or Wikipedia entry, the first author first coded 100 randomly selected organizations from the entire dataset into seven mutually exclusive categories: (1) standards-setting organizations that provide standards on good practices, services, products, and/or CSR measurement; (2) governmental or intergovernmental agencies; (3) financial organizations that provide financial advice, consulting, and loans for other companies; (4) environmental NGOs; (5) other non-environmental NGOs; (6) academic institutions; and (7) for-profit companies that were not related to finances. It should be noted that assigning organizations to a single category required careful decision-making, particularly when determining between standards-setting organizations and intergovernmental agencies. We followed the aforementioned definition of standards-setting organizations (i.e., entities operating independently from regulatory agencies and providing CSR guidelines for companies’ voluntary adoption) when an organization had overlapping characteristics of standards-setting organizations and intergovernmental agencies. For example, the UN Global Compact (UNGC) sets up the framework to encourage businesses to adopt sustainable business models, resembling what a standards-setting organization does. In this case, we gave more weight to the fact that UNGC was initiated by the UN, which is an intergovernmental agency designed to facilitate and coordinate intergovernmental collaborations with regulatory influences, and categorized UNGC as an intergovernmental agency. This allowed us to capture UNGC’s regulatory or semi-regulatory role in CSR reporting.

Given that the categories were mutually exclusive, the coding process involved assigning each organization into one category from the list. To train a graduate RA as a coder, the first author and the RA had a training session where each category was explained. Following the training session, the RA coded the same set of organizations (n = 100) coded by the first author earlier and it resulted in 100% agreement. The graduate RA then coded the rest of the organizations in the network, which resulted in identifying: 56 standards-setting organizations (e.g., GRI and ISO); 145 governmental or intergovernmental agencies; 80 financial organizations (e.g., KPMG); 31 environmental NGOs; 81 other NGOs; 40 academic institutions; and 219 various for-profit companies (including the original 113 Fortune Global 500 companies). These categories, along with the industry sector categories of the Fortune Global 500 companies in our data set, were passed on to define nodal attributes in the network object.

We conducted network analysis to test hypotheses. From a network approach, indegrees (i.e., times a node receives ties) represent popularity (Wasserman & Faust, 1994). If one type of organizations has more indegrees compared to others, it means that they carry more weight and significance in companies’ communicative externalization of their CSR activities. Particularly, exponential random graph models (ERGMs, Robins et al., 2007; Snijders et al., 2006) were fitted. In ERGMs, the probability of observing a graph depends on various configurations expressed by the model, including network statistics such as reciprocity and nodal attributes (Robins et al., 2007). With suitable constraints on certain parameters, a significant coefficient in an ERGM model can be interpreted as that particular configuration having a significant effect on the probability of a tie between nodes being higher/lower than expected by chance. ERGMs are particularly useful for the current investigation given that the probability of a mention of certain organizations should be influenced by isomorphism. Namely, the mention of an organization in one specific company’s CSR reporting is not independent from another company’s mention of the same organization. This dependent nature fits the very purpose of using ERGMs to model tie probabilities. Furthermore, though organizations’ mentioning networks through CSR differ from interpersonal networks, common tendencies such as reciprocity (e.g., two companies emphasizing mutual partnership) and triangles (two similar companies gravitating towards a similar set of companies and organizations) should exist. ERGMs can incorporate these structural features into analysis, making it more advantageous compared to other types of analysis. We constructed the network object using the R package statnet and passed along the categories as a nodal attribute. We then used the package ergm to fit ERGMs. Best models were chosen based on model interpretability, model convergence, and goodness of fit information.

Results

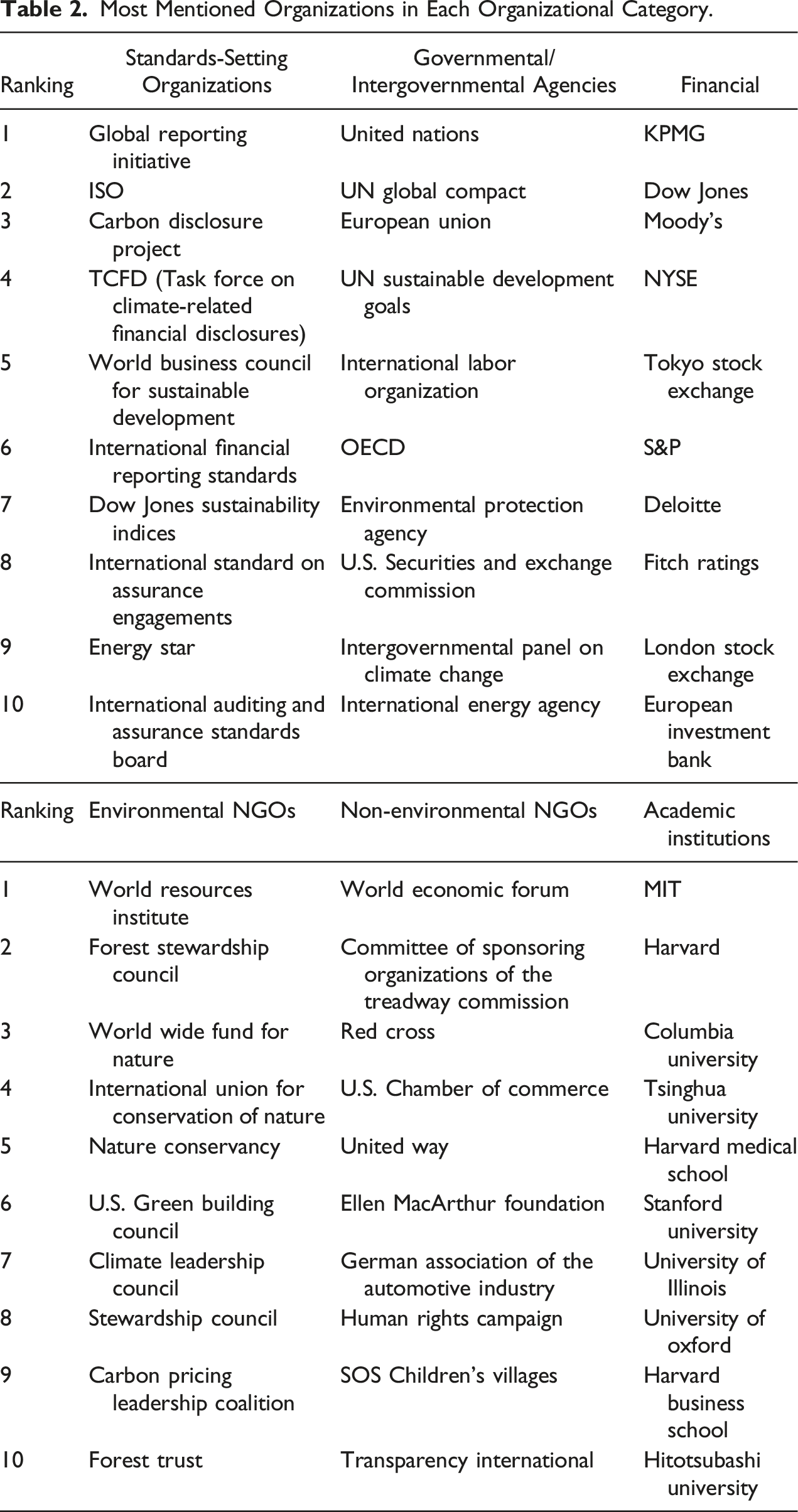

Most Mentioned Organizations in Each Organizational Category.

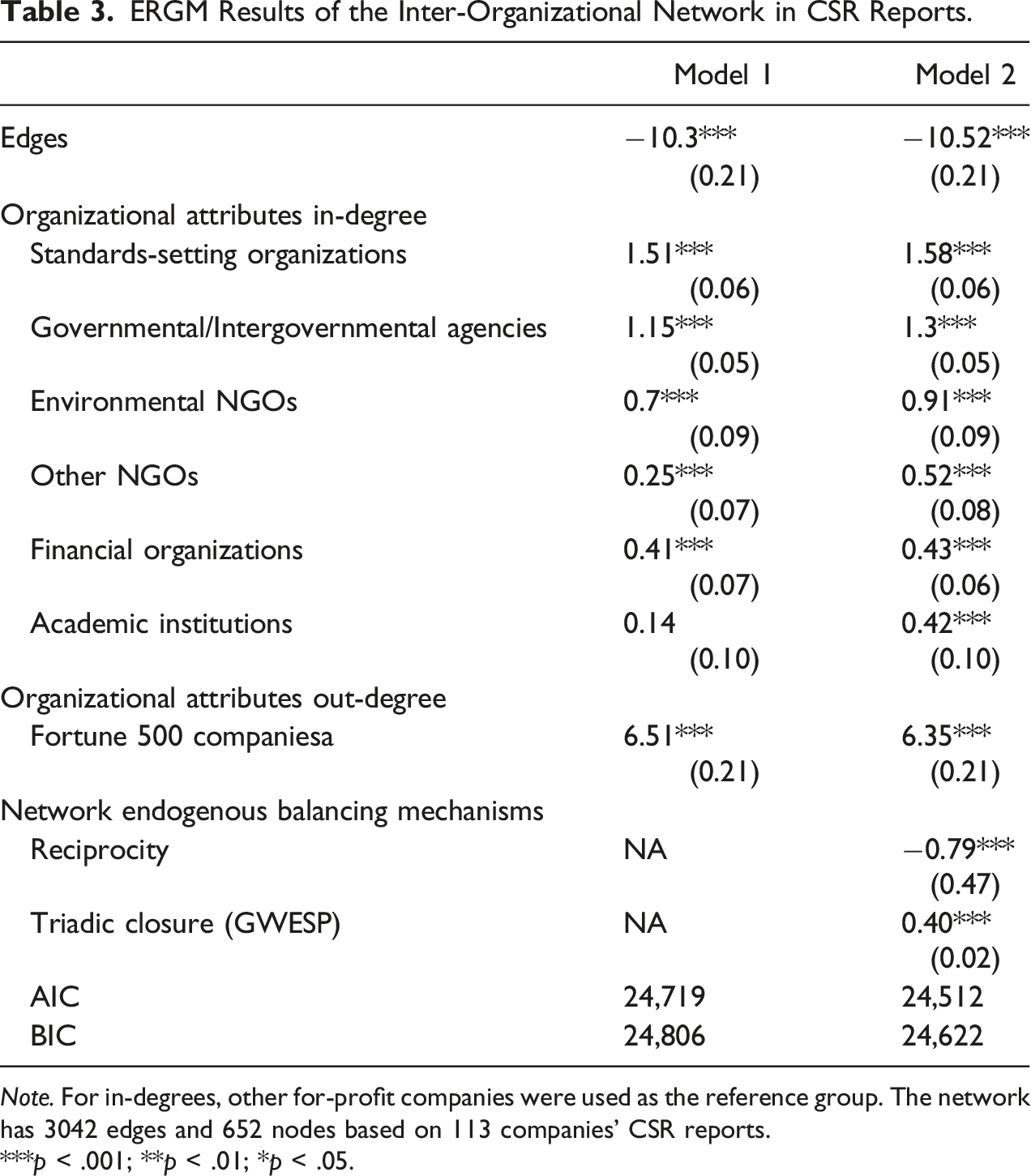

To answer RQ2 and test H1-H3, ERGM models with nodal attributes of the organizational types were fitted. The first model only included nodal attributes, and the second model controlled for reciprocity (mutual) and transitivity (GWESP). After controlling these network mechanisms, the coefficients mostly remained the same. In other words, after controlling the mechanisms of mutuality and transitivity, two prominent dyadic dependence measures, the probability of ties between two organizations due to the specified nodal attributes was still valid. We proceeded with interpreting the coefficients.

ERGM Results of the Inter-Organizational Network in CSR Reports.

Note. For in-degrees, other for-profit companies were used as the reference group. The network has 3042 edges and 652 nodes based on 113 companies’ CSR reports.

***p < .001; **p < .01; *p < .05.

H1 predicts that standards-setting organizations and regulatory organizations have more indegrees compared to NGOs. This hypothesis was supported, given that standards-setting organizations were the most likely to receive ties, followed by (inter)governmental agencies. In addition, financial organizations were more likely to receive ties compared to other for-profit companies. This result supported H2a and H2b. However, the comparison between financial organizations and NGOs depends on NGOs’ issue domains. Environmental NGOs were more likely to receive ties compared to financial organizations, but not NGOs in other issue domains. This result partially supported H2c. Finally, environmental NGOs were indeed more popular and common in CSR reports compared to other NGOs, supporting H3.

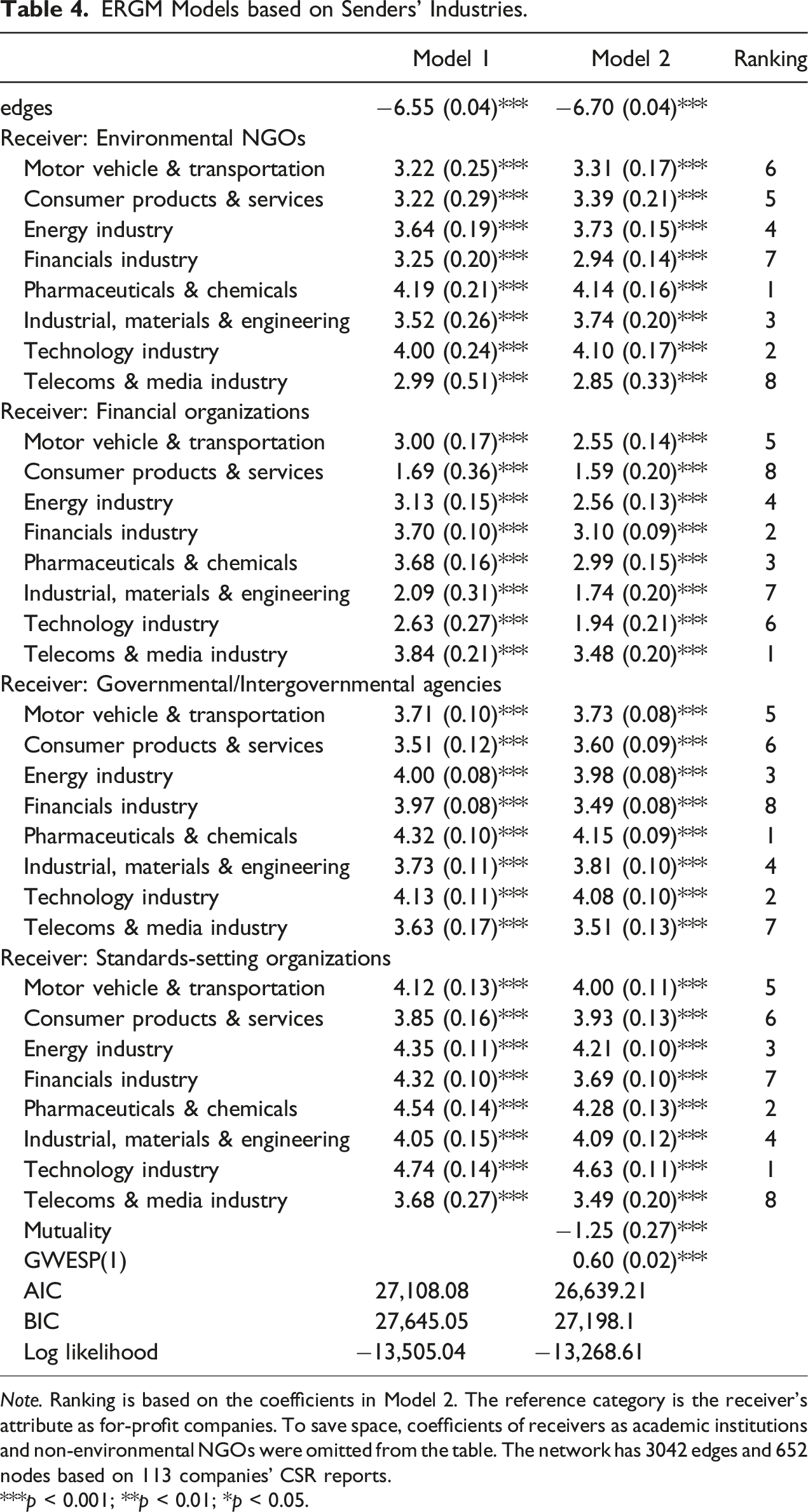

Regarding RQ3, we specified ERGM models with mixing matrix cells and margins. In other words, given the nature of the network, we used sectors as nodal attributes of senders and organizational types such as standards-setting organizations, (inter)governmental agencies, environmental NGOs, and financial organizations as receivers’ attributes to calculate the marginal log odds of the ties. Receivers as for-profit companies were used as the reference group. Overall Wald tests showed that coefficients were different in each group based on receivers’ attributes: χ2(7) = 68.99, p < .001 in the environmental NGOs group, χ2(7) = 130.56, p < .001 in the financial organizations group, χ2(7) = 86.18, p < .001 in the (inter)governmental agencies group, and χ2(7) = 75.41, p < .001 in the standards-setting organization group. Wald tests essentially constrain the parameters in the model to be equal and compare the more constrained model with the unconstrained one. The significant test results above indicate that companies in different sectors differed in terms of their probabilities of sending ties to different types of organizations.

ERGM Models based on Senders’ Industries.

Note. Ranking is based on the coefficients in Model 2. The reference category is the receiver’s attribute as for-profit companies. To save space, coefficients of receivers as academic institutions and non-environmental NGOs were omitted from the table. The network has 3042 edges and 652 nodes based on 113 companies’ CSR reports.

***p < 0.001; **p < 0.01; *p < 0.05.

When focusing on the likelihood of ties to receivers as standards-setting organizations and (inter)governmental agencies, the results were consistent. In both groups, companies in low-risk sectors (e.g., consumer services and products) were generally less likely to mention standards-setting organizations or (inter)governmental agencies in their CSR report compared to those in high-risk sectors (e.g., energy, healthcare, drug, and chemicals industries). This finding suggests that the role standards-setting organizations and (inter)governmental agencies has become more convergent. In other words, companies reporting heavily on their relationships with standards-setting organizations also tended to lean heavily on (inter)governmental agencies that usually provide regulatory mandates and guidelines.

There were, however, some unexpected findings. While companies in high-risk sectors were more likely to send ties to environmental NGOs, companies in the technology sector were also most likely to mention environmental NGOs in their CSR reports. In fact, the Wald test showed that the two coefficients (b = 4.10 for the technology industry and b = 4.14 for the HDC sector, difference χ2(1) = 0.019, p = .89) were not significantly different. Also, technology companies, though in a relatively low-risk sector, were also very high up on their likelihoods to mention standards-setting organizations and (inter)governmental agencies. We discuss possible reasons for these findings in the following section.

Discussion

By theorizing MNCs’ interorganizational positioning as a key organizational communication practice aimed at constituting themselves as relevant and legitimate partners, we posit that the interorganizational networks embedded in CSR reports contribute to understanding key actors and their relative importance in the institutionalization of CSR. In that sense, CSR reports may be seen as more than just communicative “platforms” for companies’ externalization of their CSR activities for stakeholders, but also as a discursive mechanism utilized to position themselves strategically within the institutionalized environment. By uncovering Fortune Global 500 companies’ interorganizational networks constructed via CSR reports, we were able to understand (a) how isomorphism shaped those networks by finding common trends and the sources of network pressure; and decipher (b) how they prioritized certain stakeholder organizations in seeking legitimacy of their CSR. Below, we discuss interpretations and significance of our study findings, implications for future directions, and limitations.

First, Fortune Global 500 companies rely on a variety of organizations that can potentially grant institutional legitimacy to frame and communicate their CSR activities. These organizations span from intergovernmental agencies to nonprofit organizations and to standards-setting organizations. Whereas past empirical investigations of CSR have focused on a particular type of organizational relationship in the constellation of companies’ interorganizational networks (e.g., Arya & Zhang, 2009; Flammer, 2013; Scalet & Kelly, 2010; Shumate & O'Connor, 2010a), the current study highlights and supports the importance of focusing on how organizations position themselves in the constellation of legitimacy-granting organizations to understand the relative roles of the various types of stakeholder organizations and how particular companies gain legitimacy through their CSR reporting. More specifically, the interorganizational positioning revealed in companies’ CSR reports show how a company leverages its relations with different organizations to communicatively construct the meanings of their CSR practices and construct legitimacy (O’Connor & Gronewold, 2012; O’Connor et al., 2017; Yang & Saffer, 2019).

Second, the finding that standards-setting organizations were the most popular mentioned organizations and are pivotal to companies’ interorganizational positioning in CSR reports attests to the isomorphic pressure companies face in the current CSR landscape. Isomorphism is a process and a consequence of institutionalization simultaneously, whereby companies seek legitimacy through conforming to the norms, rules, and regulations (Fortanier et al., 2011; Shabana et al., 2017). As our study results indicated, the most prominent force behind institutionalization of CSR reporting is standards-setting organizations, exceeding traditional regulatory forces assumed by governmental or intergovernmental agencies. The findings are consistent with past research that has shown that standards-setting organizations are playing an increasingly important role in setting up the guidelines and frameworks for CSR reporting and CSR activities (Avetisyan & Ferrary, 2013; Scalet & Kelly, 2010; Waddock, 2008).

The implications of the rise of standards-setting organizations over traditional regulatory organizations are important to discuss. Though intergovernmental organizations (e.g., the UN) and government agencies (e.g., the Environmental Protection Agency) still play a nontrivial role as regulatory forces behind companies’ CSR reports, standards-setting organizations typically recommend frameworks or provide guidance on companies’ CSR activities that lack measures of enforcement. On one hand, this confirms the largely voluntary nature of companies’ CSR activities. On the other hand, the rise of these unenforceable frameworks of recommendations may be problematic and troublesome, particularly because some standards-setting organizations are established by corporate leaders and companies themselves (e.g., the Responsible Business Alliance that was funded by electronics companies themselves).

Companies have great incentives to reduce business risks (Jo & Na, 2012; Young & Marais, 2012), including uncertainty regarding how to disclose and report their CSR activities. This uncertainty is exacerbated by isomorphic pressure (Li & Ding, 2013; Shabana et al., 2017). Reliance on standards-setting organizations can provide guidance for companies to reduce uncertainty and avoid running into problems of straying away from norms. In the meantime, the standards-setting organizations can play a crucial role in reproducing the institutionalization of CSR practices and reporting, while unintentionally promoting self-regulation particularly when the reliance on standards-setting organizations is self-serving.

The popularity of environmental NGOs over other NGOs also supports that companies prioritize certain issues to maximize legitimacy gains (Yang, 2020). However, Fortune Global 500 companies’ CSR practices and reporting are still heavily compliance-based. Namely, CSR is practiced and communicated in a way to showcase that the company is meeting the standards and regulations. This poses an important question about the real impacts of CSR. Critiques have already been raised on environmental CSR efforts and their real outcomes on the environment and ecology (Milne & Gray, 2013) as well as the suitability of the guidelines established by standards-setting organizations to enforce positive changes from companies (Garcia-Torea et al., 2020; Scalet & Kelly, 2010). Our study results imply that the institutionalized CSR practices that heavily rely on standards-setting organizations and (inter)governmental agencies may not be suitable to create real, meaningful changes.

Finally, by investigating how MNCs in different industry sectors construct interorganizational networks differently in CSR reports, our study results provide implications related to sectoral influences, particularly in terms of industry risks. Institutional theory posits that institutionalized norms and behaviors offer consistency among those operating within a certain field or environment (Shabana et al., 2017), which makes institutionalization more likely in industries that have high regulatory pressures (O’Connor & Gronewold, 2012; Tagesson et al., 2009). Our finding of technology companies’ consistent mentions of environmental NGOs, standards-setting organizations, and (inter)governmental agencies is noteworthy because the technology sector is generally considered to have lower regulatory pressures (Young & Marais, 2012). Two main reasons may be behind such results. First, the motives of companies in the technology sector may differ from those in the high-risk sectors. Companies in traditional high-risk sectors usually engage CSR, particularly environmental CSR, as a proactive buffer because their operations and production place a burden on the environment. Companies in the technology sector, given their relatively new status, may take CSR as a core organizational mission and treat CSR activities as integral to companies’ operations. Second, the technology sector has become increasingly scrutinized by the general public and governments, due to recent high-profile cases of unethical practices and growing concerns of data-related privacy issues. The growing pressure may contribute to companies in the technology sector being more eager to seek legitimacy from these organizations.

It is possible to consider the technology companies’ communicative signaling of various interorganizational relationships as reflective of the industry’s cultural norms of openness and prosocial ideals, which may contribute to the ongoing process of institutionalization. With the shift from coercive isomorphism toward mimetic isomorphism (Shabana et al., 2017), we may expect cultural norms to shape institutionalization processes more than regulatory or legal norms in emerging industries. Nonetheless, the study results support past research that interorganizational positioning of companies in different sectors differ because of unique sectoral characteristics and priorities (O’Connor et al., 2017; O’Connor & Shumate, 2010; Yang, 2020).

Limitations and Future Directions

A key limitation of the current network approach to understanding organizations’ communicative constitution of institutional legitimacy is its inadequacy to articulate companies’ motives or processes of reshaping the meaning of their CSR practices (i.e. how and why companies reshape the meanings of CSR in the model). For example, the current research cannot provide adequate answers to how CSR report writers or companies internalize standards-setting organizations’ recommendations, the incentives of depending on these recommended frameworks beyond potential rewards of compliance, and how the reshaping of CSR meaning takes place within an organization. This set of questions is better addressed through surveys or qualitative methods, and future research can center around the reshaping of CSR meanings in our conceptual model to provide more understandings of the conscious and unconscious choices that companies, and specifically CSR reports writers, need to make. Such insights can unpack how legitimacy is constructed or reconstructed and how the meanings of CSR are shaped or reshaped through multiple levels and types of communication, both from within and outside a company.

In addition, given our key finding about the critical role of standards-setting organizations, a more in-depth examination of the current landscape of standards-setting organizations warrants further attention. With the rising popularity of such organizations in setting up frameworks for CSR reporting and CSR practices, an examination of the nature of these organizations’ influence on CSR disclosure can greatly contribute to more nuanced understandings of the role of standards-setting organizations in CSR institutionalization.

Finally, our study results can be only interpreted in the context of the Global Fortune 500 Companies. We acknowledge that this is a very small group of companies and most of them are in Western and more developed countries and in certain sectors such as finance and energy. More research needs to be done to test our findings in other types of companies and/or contexts.

Conclusion

Going beyond focusing on companies’ strategic partnerships with one type of organizations (e.g., NGOs), the current study offers a bird’s eye view of how institutionalized CSR reporting is implicated by various types of stakeholder organizations and their relative roles, and provides a more comprehensive view of various kinds of legitimacy-granting organizations and how MNCs leverage their relations with these organizations to determine priorities in their CSR practices and construct CSR legitimacy. More specifically, the current study reveals that companies increasingly rely on standards-setting organizations in their CSR reporting, and that these organizations exert more influence than traditional corporate watchdogs such as (inter)governmental regulatory agencies. The prominent influence of standards-setting organizations in companies’ CSR reports indicates that standards-setting organizations play a crucial role in reproducing and perpetuating the institutionalization of CSR practices and reporting. Overall, our study results suggest that institutionalization needs to be understood through consideration of the various forces and interests assumed by all types of legitimacy-granting organizations and each company’s overall interorganizational positioning in the constellation of organizational relationships and partnerships. Furthermore, companies in different sectors showcase distinct sectoral preferences in their CSR reporting. In general, high-risk industries tend to compensate for their high (negative) impact on the environment and society by having stronger ties with standards-setting organizations and regulatory forces, indicating a more compliance-based approach. Sectoral constraints and homogenization are also important pieces in CSR institutionalization.

Footnotes

Acknowledgements

We want to thank Macee Tinker and Shelby Luttman for their help with the coding of organizations in this study. We also want to thank the editor and the anonymous reviewers for their valuable suggestions and feedback.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.