Abstract

The aim of this research is to study the moderating role of family management in the relationships between the intensity of research and development and the occurrence of continuous technological innovation and between the existence of technological innovation outcomes and long-term firm performance. The results show that family management reduces efficiency in the conversion of research and development expenses into technological innovation outcomes over time. Our findings also suggest that the influence of family management significantly contributes to improving the effect of the achievement of technological innovation on long-term performance.

Introduction

Technological innovation is essential for economic growth, and family firms are ubiquitous and significant organizational forms of economies worldwide (La Porta, Lopez-de-Silanes, & Shleifer, 1999), substantially contributing to job creation and to boosting the gross domestic product on a global scale (Family Firm Institute, 2015). Therefore, an advanced understanding of family firms’ innovation behavior is urgent (Duran, Kammerlander, van Essen, & Zellweger, 2015).

Technological innovation is often defined as the set of activities through which a firm conceives, designs, manufactures, and introduces a new product, service, or technique. Technological innovation is influenced by research and development (R&D) expenditures (David, Hitt, & Gimeno, 2001), normally years after consumption, generating a continuous sequence of technological innovation (Ireland, Hitt, Camp, & Sexton, 2001) for a given period of time (continuous technological innovation [CTI]). The previous literature also shows that the achievement of technological innovation is an important determinant of superior long-term performance (Blundell, Griffith, & van Reenen, 1999) and leads to performing better than competitors do (De Massis, Frattini, Pizzurno, & Cassia, 2013).

To date, the existing research on the effects of family involvement on innovation has basically focused on the effect of family involvement on innovation inputs, activities, and outputs (De Massis, Frattini, & Lichtenthaler, 2013; Padilla-Meléndez, Diéguez-Soto, & Garrido-Moreno, 2015). Studies are largely consistent in noting a negative relationship between family involvement and technological innovation inputs (e.g., Block, 2012; Kotlar, De Massis, Frattini, Bianchi, & Fang, 2013) and obtaining mixed empirical evidence with regard to the effect of family involvement on technological innovation outputs (e.g., Classen, Carree, Van Gils, & Peters, 2014; Matzler, Veider, Hautz, & Stadler, 2015). There have been some attempts to illuminate these puzzling results. Thus, Matzler et al. (2015) have recently focused on large public companies, confirming that family management has a negative impact on innovation input and a positive influence on innovation output. Similarly, Duran et al. (2015) maintain that family firms with a family chief executive officer invest less in innovation but have an increased conversion rate of innovation input into output and, ultimately, a higher innovation output than do other firms.

However, although CTI requires a specific and efficient combination of technical, financial, and human resources (Claver, Llopis, Garcia, & Molina, 1998), and family involvement—considered in terms of management and control (Liang, Li, Yang, Lin, & Zheng, 2013)—is very likely to affect technological innovation (De Massis, Frattini, Pizzurno, et al., 2013), there has not been research on whether family-managed firms are more efficient than nonfamily firms in the conversion of innovation input into CTI. Furthermore, although the real importance of innovation outcomes is materialized through their direct and indirect effects on economic growth and firm performance (Schumpeter, 1942), we have very limited insight into whether family-managed firms more efficiently generate economic consequences from technological innovation than do non–family-managed firms. Recently, Block, Miller, Jaskiewicz, and Spiegel (2013) have confirmed that family-managed firms produce innovations of low economic and technological importance in terms of patent citations, even when controlling for R&D spending. However, although technological innovation has important implications for the survival of the family firm (Llach & Nordqvist, 2010), there have been no studies that analyze whether the technological innovation effects on the firm’s long-term performance in family-managed firms are different from what they are in their nonfamily counterparts.

Simultaneously, the previous literature has recognized family management as a proxy for the importance of socioemotional wealth (Berrone, Cruz, & Gomez-Mejia, 2012), and a growing body of research based on the socioemotional wealth perspective (Berrone et al., 2012; Martínez-Romero & Rojo-Ramírez, in press) is providing evidence regarding the paradox of family firm innovation. Studies in this domain argue that family firms have a superior ability (discretion to act) to innovate but lower willingness (disposition to act) to do so (Chrisman, Chua, De Massis, Frattini, & Wright, 2015). We assume that, from the perspective of socioemotional wealth, family management can act as a driver of the willingness and ability to influence technological innovation efficiency, defined as the relative ability of R&D expenses and technological innovation, successfully generating CTI and long-term performance, respectively. Thus, family management can have a bearing on technological innovation efficiency with regard to making the best of R&D investment, producing CTIs (efficiency in terms of CTI), and optimizing the act of obtaining technological innovation–yielding long-term performance (efficiency in terms of long-term performance).

Bearing in mind the previous considerations, our research addresses the following research questions. Does family management moderate the positive expected influence of R&D intensity on the existence of CTI? Does family management moderate the positive expected influence of the existence of technological innovation on long-term performance? To that end, we developed an empirical study with different econometric models that cover the hypotheses, using a panel data sample of 551 Spanish manufacturing small and medium-sized enterprises (SMEs) in the period from 2000 to 2012. The data were obtained from the Survey on Business Strategies.

This study contributes in a twofold manner. First, it distinguishes between efficiency in terms of optimizing the action of investing in R&D that yields CTI and efficiency in terms of generating long-term performance from the act of obtaining technological innovation. In this manner, it illuminates the conflicting views regarding family firm innovation.

Second, building on the role of family management and the socioemotional wealth agenda (Gomez-Mejia, Cruz, Berrone, & De Castro, 2011), this study shows that family management has a negative moderating effect on the relationship between R&D intensity and CTI and a positive moderating effect on the relationship between the occurrence of technological innovation and long-term performance. Thus, it contributes to an enhanced understanding of the moderating role of family management (Zahra, 2007) in technological innovation efficiency in SMEs, providing a more comprehensive and nuanced picture of family firm innovation.

In addition, the study develops a more fine-grained understanding of family firm innovation by relating innovation inputs, technological output, and economic outcomes, in addition to applying a continuous measurement to some of these dimensions. Hence, instead of assuming a priori that the act of spending on R&D and the achievement of technological innovation have an immediate impact on the occurrence of technological innovation outputs and firm performance in a single year, respectively, we introduce a continuous measurement of these dimensions (CTI and long-term performance) into our discussion of the contribution of innovation to the firm’s future, highlighting the long-term instead of the short-term view and results.

In the next section, we present our framework and hypotheses. In the remainder of the article, we present the data and method, results, discussion, and conclusions.

Theory Development and Hypotheses

R&D Intensity, Continuous Technological Innovation, and Family Management

R&D investments are essential for firms because they bestow on businesses the experience that is necessary to turn research projects into successes (Hambrick & Macmillan, 1985), they build long-term benefits for the firm, and they are a prerequisite for creating new or improved products and/or technologies (e.g., Schmid, Achleitner, Ampenberger & Kaserer, 2014). The R&D effort is one of the determinants of technological innovation (Souitaris, 1999; Porter, 1980). Nevertheless, the R&D intensity’s influence on technological innovation is not immediately effective; there is some delay between R&D spending and research outcomes (e.g., patentable products, product innovation, process innovation; Chin, Chen, Kleinman, & Lee, 2009). In other words, R&D intensity is especially prone to providing mid- and long-term benefits (Eberhart, Maxwell, & Siddique, 2004; Hall & Oriani, 2006).

Furthermore, the previous literature has maintained that innovation is “path dependent” (e.g., David, 1975, 1988). That is, the traditional model of technological development plays an essential function in shaping the pace of future technological change (Redding, 2002). Prior technological innovation is expected to make a positive contribution to the firm’s current technological innovation by accelerating innovation or providing the basis for increased novelty and customer satisfaction (Kyriakopoulos & De Ruyter, 2004). Hence, past technological innovation contributes to generating CTI, a process by which enterprises continuously implement new methods and ideas in upgrading products, internal processes, technologies, systems, and operations to create strategic flexibility in satisfying customers (Boer & Gertsen, 2003; Soosay, 2005). Thus, the concept of continuous innovation implies a continuous wave of innovations (Ireland et al., 2001) and stresses the significance of a continuous sequence of generating and applying innovative ideas throughout the life of the firm (Shang, Wu, & Yao, 2010).

On the other hand, the preservation of socioemotional wealth in family firms may affect the relationship between R&D intensity and the existence of CTI; having a family manager running the firm is “a common source of socioemotional wealth for a family” because he or she has a more immediate and direct influence on strategy (Block et al., 2013, pp. 182). Because family firms are motivated not only by financial objectives but also by nonfinancial objectives, such as emotional and social objectives, and attempt to preserve their socioemotional wealth, that is, the “affective endowment” (Gomez-Mejia, Haynes, Núñez-Nickel, Jacobson, & Moyano-Fuentes, 2007), family-managed firms tend to be more risk averse in their business decisions than non–family-managed firms. Family managers are not willing to cede control—for example, to nonfamily investors—because doing so would restrict their shareholder voting power (as family owners) and also limit the influence of their managerial actions and decisions (as managers). Hence, family managers refuse to make substantial investments in innovation because financing innovation input frequently cannot be performed internally, thus requiring external capital and, in ceding control of the firm, risking their socioemotional wealth (Duran et al., 2015). Among innovating firms, family-managed firms tend to invest less intensively than non–family-managed firms (Classen et al., 2014), most likely because the strength of the family in management teams increases the focus on family goals and values and, striving to protect socioemotional wealth (Gomez-Mejia et al., 2007), a dominant family objective, the family is unwilling to jeopardize its discretion (Classen, Van Gils, Bammens, & Carree, 2012) and its wealth by taking excessive risks (Zahra, 2005). Consequently, a lower intensity of R&D should cause a lower likelihood of obtaining CTI in relative terms over time based on reasons of synergy.

Furthermore, family-managed firms are subject to a lack of executive talent (ability) and a conservatism (willingness) that limit the conversion of R&D expenses into technological innovation. Nepotism, the entrenchment of untalented family managers, and altruism (Bertrand & Schoar, 2006), which benefits undeserving family members, lead to inadequate expertise. Family management reduces nonfamily managers’ discretion and freedom to act (Zahra, 2005); it also limits human capital (Sraer & Thesmar, 2007) and escalates emotional family issues and conflict (Kellermanns & Eddleston, 2004), restricting the accomplishment of technological innovation.

If family-managed firms are likely to invest less intensively in R&D because of an unwillingness to endanger their affective endowment and have a lower probability of achieving technological innovation because of a lack of executive talent, then they will not be especially prone to frequently accomplishing technological innovation and regularly achieving acts of technological innovation, that is, attaining CTI. Moreover, because the involvement in a continuous sequence of technological innovations, with mid- and long-term consequences, increases the difficulty of predicting their results (Sorescu, Chandy, & Prabhu, 2003), family management may avoid risk-taking decisions, hindering the ability to convert R&D investments and past technological innovation into CTI.

Thus, we assume that family management negatively influences efficiency in terms of CTI. Thus, we propose the following hypothesis:

Technological Innovation Outcomes, Long-Term Performance, and Family Management

The previous literature supports the notion that technological innovation has a major influence on industrial competitiveness and national development (Tidd, Pavitt, & Bessant, 2001) because technological innovation creates value and economic growth (Amit & Zott, 2001; He & Wang, 2009) and is an important determinant of superior long-term performance (Blundell et al., 1999; Lee, Bennett, & Oakes, 2000; Strecker, 2009). Nevertheless, firms that introduce more technological innovation are not necessarily those that perform better, and because innovation behavior is important for family-managed firms, there is a need to further understand the dimensions of innovation and determine their effects on firm performance (Llach & Nordqvist, 2010).

With regard to strategic choices, family-managed firms are able to be simultaneously risk taking and risk averse (Gomez-Mejia et al., 2011). As claimed above, family managers express their risk aversion by declining to invest considerably in R&D because, in ceding control of the business, they are endangering their socioemotional wealth. However, we argue that they also prove to be risk taking once the technological innovation outcomes are obtained, giving them their complete support to achieve higher technological innovation efficiency, defined as the ability to successfully translate technological innovation outcomes into long-term performance.

Considering that technological innovation efficiency relates to how much long-term performance can be obtained from a given occurrence of technological innovation, family managers may view inefficient technological innovation not only as a threat to the firm’s ability to produce economic returns but also primarily as a threat to their socioemotional endowment (Gomez-Mejia et al., 2011). Thus, we argue, from the perspective of family managers, technological innovation outcomes may be particularly risky because they possibly involve potential losses in terms of economic and noneconomic family-centered goals. Consequently, family managers may become extraordinarily competent and sensitive in reacting very strongly and changing course completely, if necessary, when the long-term consequences of technological innovation outcomes for firm performance are not appropriate. Although the uncertain results of technological innovation can place noneconomic utilities at risk, reducing family managers’ control over the manner in which business activities are managed and organized (De Massis, Di Minin, & Frattini, 2015), once the firm has opted to implement a certain technological innovation, the high ability—as discretion—of the managers and the alignment of interests between owners and managers in family-managed firms decrease the barriers to integration into the firm’s existing operations, increasing the likelihood of accomplishing the appropriate long-term performance.

Indeed, family-managed firms are typically characterized as firms that give up on unprofitable innovation projects as soon as they are revealed to be so and that do not insist on continuing with them. Family managers may also be aware that if the family firm does not take risks, betting decidedly on its technological innovation outcomes to obtain a proper performance in the current changing environment, then they may actually be more risk taking and may be endangering the preservation of their socioemotional endowment (Zellweger & Dehlen, 2011).

Furthermore, family managers are endowed with superior tacit knowledge (Von Krogh, Ichijo, & Nonaka, 2000) of their firm’s members, routines, and stakeholders; thus, their management is beneficial for harvesting such advantageous human capital and will allow a more effective leveraging of the firm’s unique resources and thus a more efficient conversion of technological innovation into performance. Another core element is social capital. The social capital of family firms is characterized by the protection of the family name and reputation in relation to interested external parties (Dunn, 1996) and by the cultivation, nurturing, and development of long-term relationships with the firms’ stakeholders (Miller & Le-Breton Miller, 2005). Social capital may be a factor that contributes to higher firm performance because the greater-quality relationships with stakeholders in family-managed firms enhance innovation strategies (Carney, 2005). Greater connections with external stakeholders should expose family members to new knowledge, decreasing the rigidity of the mental models of family decision makers, thereby increasing performance (Chrisman, Fang, Kotlar, & De Massis, 2015). Moreover, the social capital owned by family firms and by insiders involved in the management also positively contributes both to cost efficiency strategies and to strategies of incremental innovation and the adaptation of new technologies to the needs of specific clients (Uhlaner, Stel, Duplat, & Zhou, 2013), which may provide better long-term firm performance. Thus, we theorize that under the influence of the family management, family firms create a distinctive social resource and support base (Habbershon & Williams, 1999) from the family, the business, and the individuals outside the firm that contribute to generating higher efficiency in terms of long-term performance. Based on the foregoing arguments, we propose the following hypothesis:

Data and Method

Sample and Data Sources

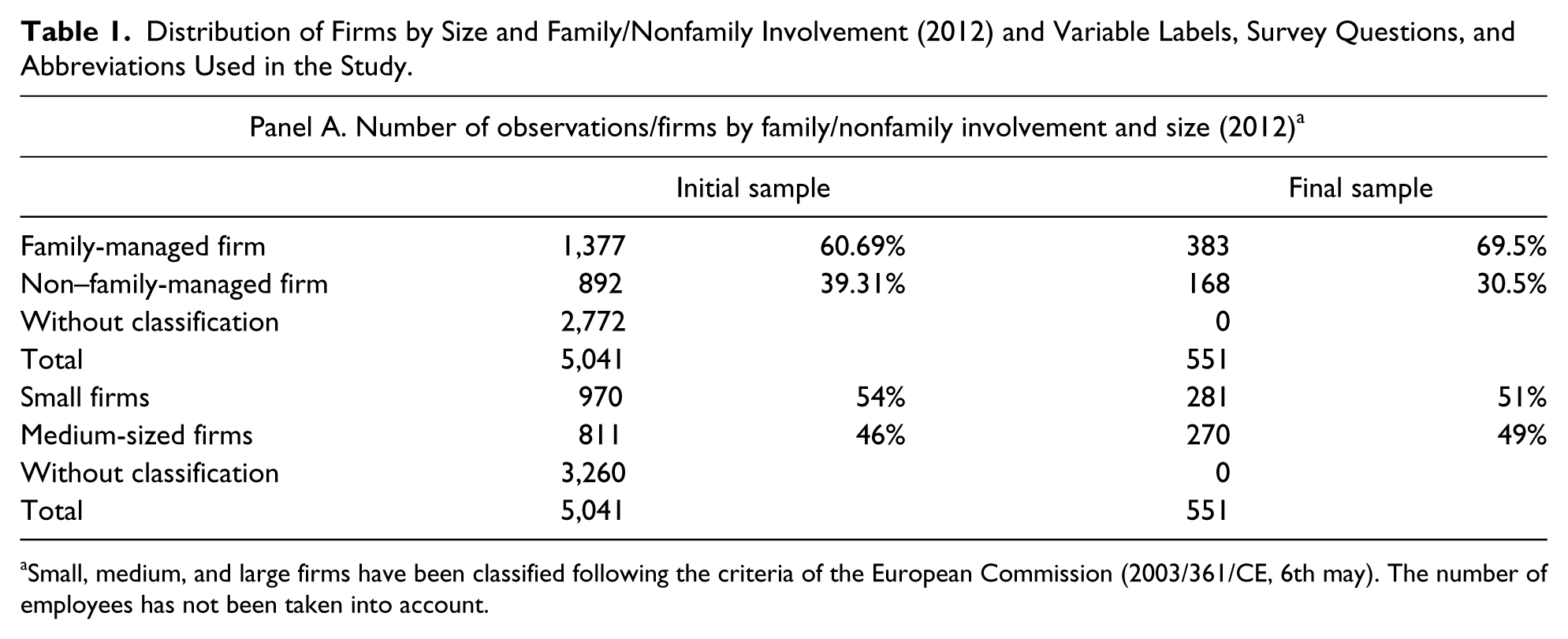

The data used to contrast the hypotheses came from the Survey on Business Strategies, which is administered by the State Partnership of Manufacturing Equity foundation on behalf of the Spanish Ministry of Industry. This survey is built on information from Spanish manufacturing firms. According to the State Partnership of Manufacturing Equity, the Survey on Business Strategies includes unbalanced data covering 1,800 firms on average per year. The sampling procedure ensures the representativeness of the manufacturing sector, following both exhaustive and random sampling criteria. The reliance on multiple respondents, the survey’s validation process, and the objective nature of the information collected through the survey should reduce common method bias (Kotlar, Fang, De Massis, & Frattini, 2014). The survey counts on a sample of 5,304 firms in the 2012 panel. For these firms, accounting and innovation data were collected for the years 2000 to 2012. After removing firms with missing data and outliers for the analyzed variables, the final sample was composed of 551 SMEs, resulting in a balanced panel of 7,163 observations. To test the potential bias and representativeness of the final sample, we compared the final estimation sample of 551 firms with the initial sample of family-managed firms and non–family-managed firms for the year 2012 (see Table 1, Panel A). Similarly, the representation of the size and sector of the firm has been tested. Considering the results of the two distributions, we conclude that there is no bias between the initial and final samples. In addition, the maximum for a finite population has been calculated. The maximum error is small (e = 3.95%, α = .95), leading to the consideration that the final sample is representative of the initial sample. Additionally, the fact that the data came from a public agency guarantees the quality of the information according to the arguments of Dorling and Simpson (1999), that is, a high level of participation, a high response rate, and the representativeness of the population.

Distribution of Firms by Size and Family/Nonfamily Involvement (2012) and Variable Labels, Survey Questions, and Abbreviations Used in the Study.

Small, medium, and large firms have been classified following the criteria of the European Commission (2003/361/CE, 6th may). The number of employees has not been taken into account.

Manufacturing firms are particularly affected by innovation practices because their products suffer from a high degree of obsolescence (Kotlar et al., 2014). This fact makes the study of technological innovation in this industry particularly important. Most important for the purposes of this study, family firms seem to be common among private and manufacturing firms (Astrachan & Shanker, 2003), which justifies our focus on the comparison between family-managed firms and non–family-managed firms. Indeed, this database has been frequently used in empirical analyses (e.g., López, 2008), particularly for innovation and family business studies (e.g., Kotlar et al., 2014).

Variables

Independent Variables

Technological innovation

Based on the previous literature (Utterback & Abernathy, 1975) and according to the process-based conceptualization of technological innovation (Freeman, 1976), two types of innovation were distinguished: product innovation and process innovation. To define this variable, we take as a reference the firms’ answers to the questions included in the Survey on Business Strategies. We created one dummy variable that takes the value of 1 when there is any type or both types of technological innovation (product innovation and/or process innovation) and 0 otherwise.

In the field of innovation, there exists a large body of research on the use of this concept of technological innovation. In particular, another concept based on the number of patents or patent citations can underestimate the innovation activity of SMEs because such firms are generally unwilling to file patents because of the fear that their new ideas will be appropriated (Deng, Hofman, & Newman, 2013) or because they cannot afford the exposure and time involved in the patenting process (Kalantaridis & Pheby, 1999). To address this limitation, the previous research has utilized both types of innovation—product innovation and process innovation—as technological innovation outcomes in the context of SMEs (Uhlaner et al., 2013).

R&D intensity

This variable is measured as the ratio of R&D expenditure to total sales income. Following previous studies, we use a lagged expression of the variable (R&Dt−1; e.g., Liang et al., 2013).

Family-managed firm

We consider a family firm to be an enterprise with a particularistic vision of business and goals resulting from the active involvement of a controlling family (Chua, Chrisman, & Sharma, 1999). Indeed, the family vision and goals are found to be highly correlated to the extent of family involvement in the firm (Chrisman, Chua, Pearson, & Barnett, 2012). We opted for an objective measure of family influence on decision making because a direct measure of family vision and goals was not available (Diéguez-Soto, López-Delgado, & Rojo-Ramírez, 2015). Particularly, we followed the definition of Kotlar et al. (2014), who considered both family ownership and family involvement in top management to build a binary measurement of family-managed firms. Previous studies in this field have used similar measurements to capture the perspective of family-managed firms (see, e.g., Sirmon, Arregle, Hitt, & Webb, 2008).

Dependent Variables

Continuous technological innovation

As a measure of innovation, the literature has also considered whether the firm introduced innovation during a determined number of years (Clausen, Pohjola, Sapprasert, & Verspagen, 2012). Following this perspective and to take the dynamism of technological innovation into account, we created a proxy of CTI. Specifically, we defined a categorical variable from 0 to 3 by the accumulation of technological innovation for the years t, t + 1, and t + 2. Thus, the variable of CTI takes the following values: CTI = 0 when there is no type of technological innovation; CTI = 1 when there is product innovation, process innovation, or both in 1 year in a 3-year period; CTI = 2 when there is product innovation, process innovation, or both in 2 years in a 3-year period; and CTI = 3 when there is product innovation, process innovation, or both in 3 years in a 3-year period. The consideration of a 3-year period is in line with the previous literature (Laursen, Masciarelli, & Prencipe, 2012; Salavou, Baltas, & Lioukas, 2004), overcoming certain limitations related to temporal measures of innovation.

Long-term firm performance

In this study, performance is measured by the return on assets, which is widely supported in the literature on family firms (Rutherford, Kuratko, & Holt, 2008) and innovation in family firms (e.g., Schepers, Voordeckers, Steijvers, & Laveren, 2014). Long- term performance is the mean return on assets in a 3-year period (t, t + 1 and t + 2).

Control Variables

The literature has emphasized the role of the firm’s size in innovation. Thus, Cohen and Klepper (1996) argue that large firms’ advantages in terms of internal knowledge, financial resources, sales base, and market power contribute to increasing the level of innovation. However, there are also arguments regarding the advantages of small firms. Thus, previous studies refer to a better ability to exploit the external economies likened to the innovative environment (Audretsch & Vivarelli, 1996) or to capture the networking innovation (Rogers, 2004). Regarding the firm’s age, the previous literature shows consistent findings that indicate that innovation performance depends on the life stages of firms (Craig & Moores, 2006) and that advance the understanding of the firm’s age as an important predictor of entrepreneurial behavior (De Massis, Chirico, Kotlar, & Naldi, 2014). Additionally, the higher potential for the innovation orientation of younger firms has been highlighted by some studies (e.g., Kraiczy, Hack, & Kellermanns, 2014). Furthermore, we controlled for potential industry-level influences on innovation strategies and performance. Because business sectors can have different degrees of innovation propensity and profitability, we included 20 subindustry dummy variables as a further control in our analysis. The first dummy (the food industry) was used as the reference group and was thus omitted in regression to avoid overdetermination problems in the model. Finally, given that organizations with greater financial resources have higher levels of financial slack to invest in new projects, we controlled for firm leverage (Kotlar et al., 2013) and the subsidies for innovation received by firms (Raymond, Mohnen, Palm, & van der Loeff, 2010).

Method

Two econometric models were developed to test the hypotheses previously proposed above. In all cases, a panel data structure has been followed (551 firms × 13 years). All variables were indexed by i for the firms (i = 1, . . . , N) and t for the time period (t = 1, . . . , T).

Model 1: Moderating effect of family management involvement on the relationship between R&D intensity and CTI (Hypothesis 1)

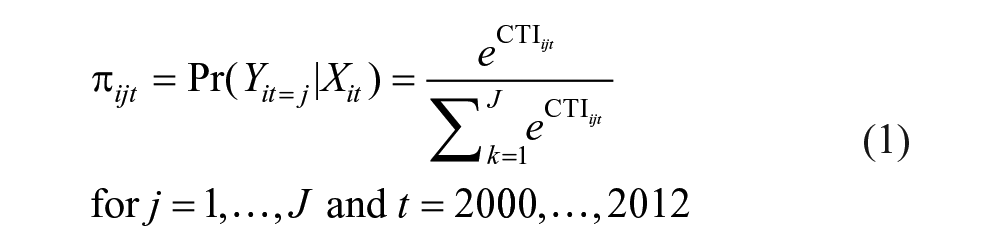

To estimate the probabilities of developing CTI, we used a panel multinomial logit model with a longitudinal data structure and random effects (Chen & Kuo, 2001) to control for unobserved heterogeneity or spurious dependence between individuals. The hypothesis is that the achievement of previous innovation outputs is a compulsory step in the creation of CTI. As discussed above, the process by which firms continuously implement new products or processes implies a continuous wave of technological innovation outcomes, that is, for at least 2 years. According to this line of reasoning, the dependent variable takes four different response categories. The lack of technological innovation is taken as the reference category (j = 1, β1 = 0). The other categories represent any type of technological innovation in 1 year of a 3-year period (j = 2), 2 years of a 3-year period (j =3), and all 3 years of a 3-year period (j = 4). Thus, CTI occurs when the variable takes the values of 2 and 3 (j = 3, j = 4).

The relative probabilities of choosing the alternative j are expressed as follows:

where

Model 2: Moderating effect of family management involvement on the relationship between technological innovation outcomes and long-term firm performance (Hypothesis 2)

A panel data methodology was used to examine the moderating effect of family management involvement on the relationship between technological innovation outcomes and long-term firm performance. Fixed effects and random effects were selected as the techniques to estimate the models. To test which model best fits the data, the Hausman (1978) test was used to decide between random effects and fixed effects. This test checks the absence of correlation between the individual effects and the independent variables; thus, when the null hypothesis is not rejected, a higher degree of efficiency in the estimation is indicated, which leads to the use of the random effects model (Croissant & Millo, 2008). To evaluate the importance of endogeneity or unobserved heterogeneity problems (dynamic endogeneity, simultaneity, and unobserved heterogeneity), different tests have been used.

Results

Summary Statistics

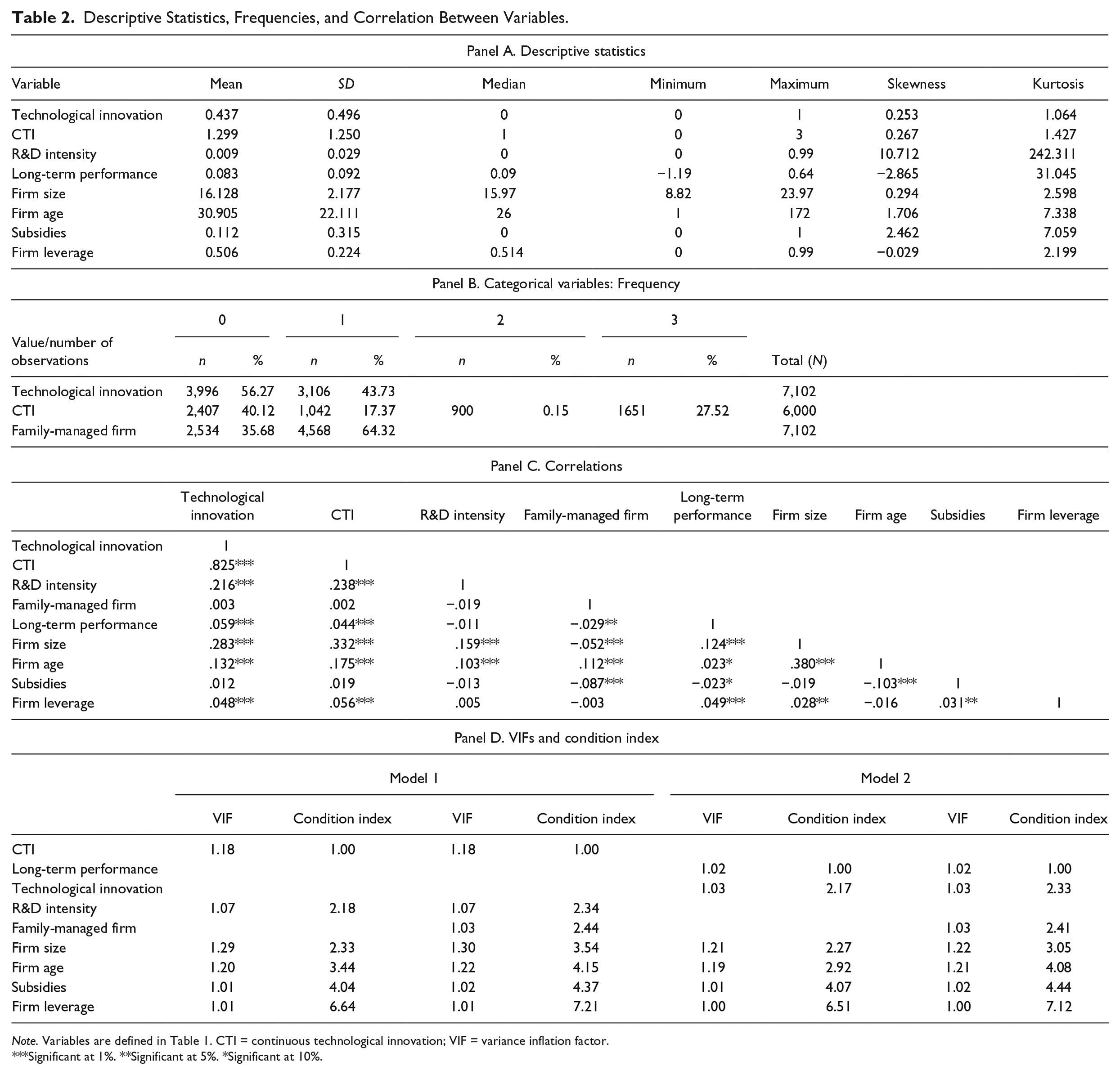

The descriptive statistics, frequencies for categorical variables, and correlations for the complete panel are summarized in Table 2. Table 2, Panel B, reflects that the occurrence of technological innovation is reached in close to 44% of the cases under analysis (there are 3,106 cases with product and/or process innovation; CTI = 1). Additionally, 27.52% obtain technological innovation (product and/or process innovation) over three consecutive years (CTI = 3), and only 40.12% of the sample do not have any type of innovation throughout the same period (CTI = 0). A total of 64.32% of the sample are considered family-managed firms, against the 35.68% of non–family-managed firms in the year 2012 (see Table 1, Panel A).

Descriptive Statistics, Frequencies, and Correlation Between Variables.

Note. Variables are defined in Table 1. CTI = continuous technological innovation; VIF = variance inflation factor.

Significant at 1%. **Significant at 5%. *Significant at 10%.

Table 2, Panel C, provides the bivariate correlations between the variables, and Panel D shows the results of the variance inflation factors and the condition index. Although there are significant correlations, all are below .4 (Tabachnick & Fidell, 1996), and both tests in Panel D show values below the warning levels of less than 10 (all <1.30) and 20 (all <7.21) (Johnston, 1984), as suggested by previous studies. These results allow us to assert that multicollinearity is not a significant concern. Additionally, the size of the sample is large, which contributes to the reduction in the standard errors.

Regression Results

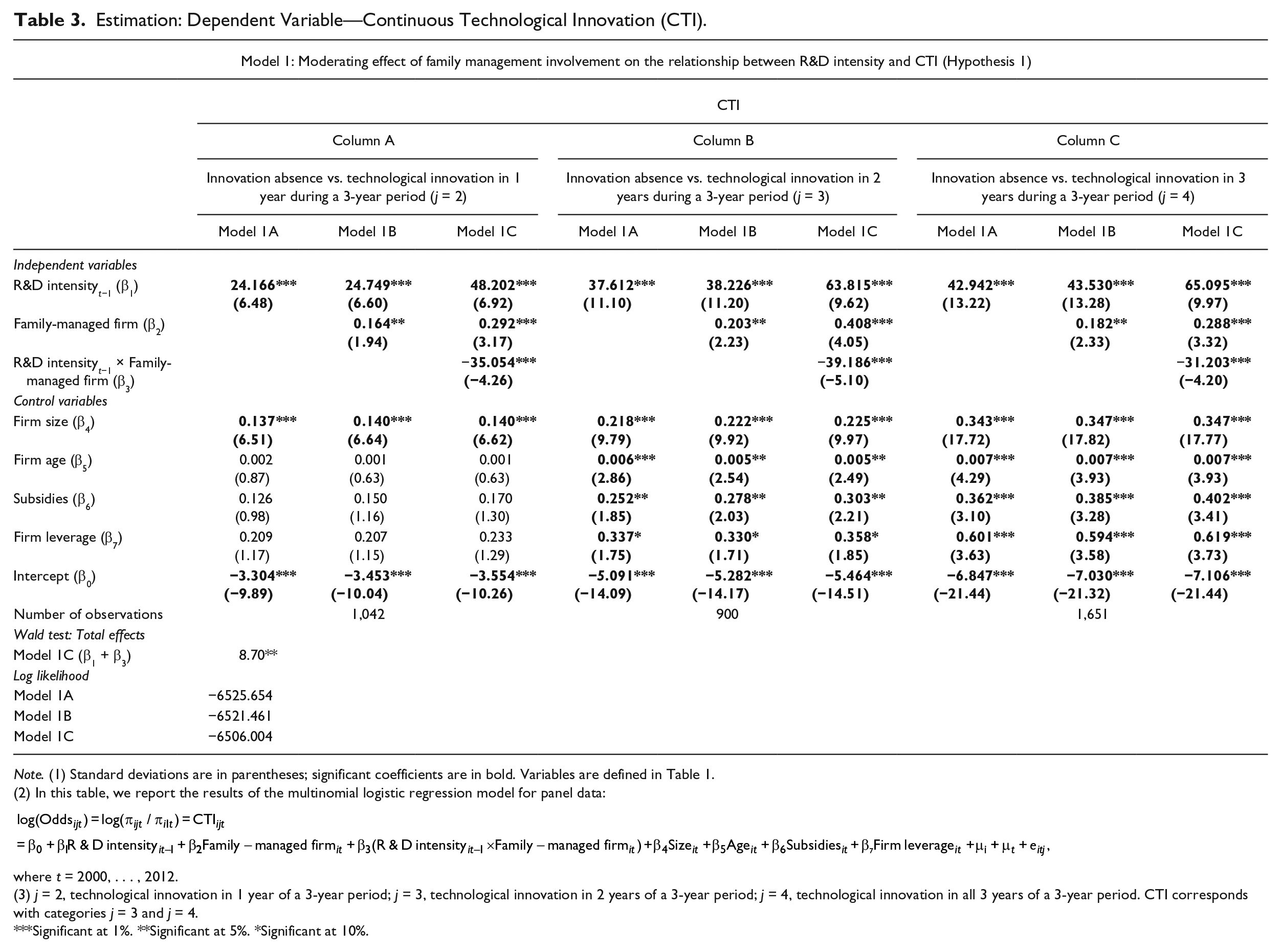

Table 3 reports the results of the panel multinomial logit regressions used to test Hypothesis 1, which predicts a negative moderating effect of family management on the relationship between R&D intensity and CTI. The Stata command of GLLAMM (Rabe-Hesketh, Skrondal, & Pickles, 2004) is used to calibrate the panel multinomial logit model. Both the spatial and the temporal heterogeneities of the data are considered. The standardized values of the multiplicative terms have been used to mitigate multicollinearity concerns (Cohen, Cohen, West, & Aiken, 2003).

Estimation: Dependent Variable—Continuous Technological Innovation (CTI).

Note. (1) Standard deviations are in parentheses; significant coefficients are in bold. Variables are defined in Table 1.

(2) In this table, we report the results of the multinomial logistic regression model for panel data:

where t = 2000, . . . , 2012.

(3) j = 2, technological innovation in 1 year of a 3-year period; j = 3, technological innovation in 2 years of a 3-year period; j = 4, technological innovation in all 3 years of a 3-year period. CTI corresponds with categories j = 3 and j = 4.

Significant at 1%. **Significant at 5%. *Significant at 10%.

The results of Model 1A (Columns B and C) suggest that the probability of developing CTI increases with additional investment in the previous year. This finding is confirmed for 2 (β = 37.61, p < .001) and 3 (β = 42.94, p < .001) years of technological innovation achievement. The moderating effect of family management involvement appears to be significant, and as a result, the positive effect of R&D investment on the likelihood of achieving CTI declines when there is family management involvement (j = 3, β = −39.186, p < .001; j = 4, β = −31.203, p < .001). The total effect of family management on CTI is tested through the Wald test. The sum of the effect of the individual variables and their interaction terms, in Model 1C (β1 + β3), is significant and confirms a negative and significant influence of family management on the likelihood of developing CTI (p < .001). This result provides support for Hypothesis 1.

In terms of the control variables, SMEs with a greater size are more likely to develop CTI, which is consistent with previous research (Cohen & Klepper, 1996). Additionally, given the experience of the firms over the years, older firms are more likely to develop technological innovation repeatedly in 2 or 3 years (Craig & Moores, 2006). Regarding financial support resources, the subsidies received by firms seem to be particularly important in differentiating between companies that achieve innovations in 2 or 3 years and those that do not innovate. Taking into consideration the financial support of creditors, debt has a strongly positive impact on the probability of achieving innovation over three consecutive years.

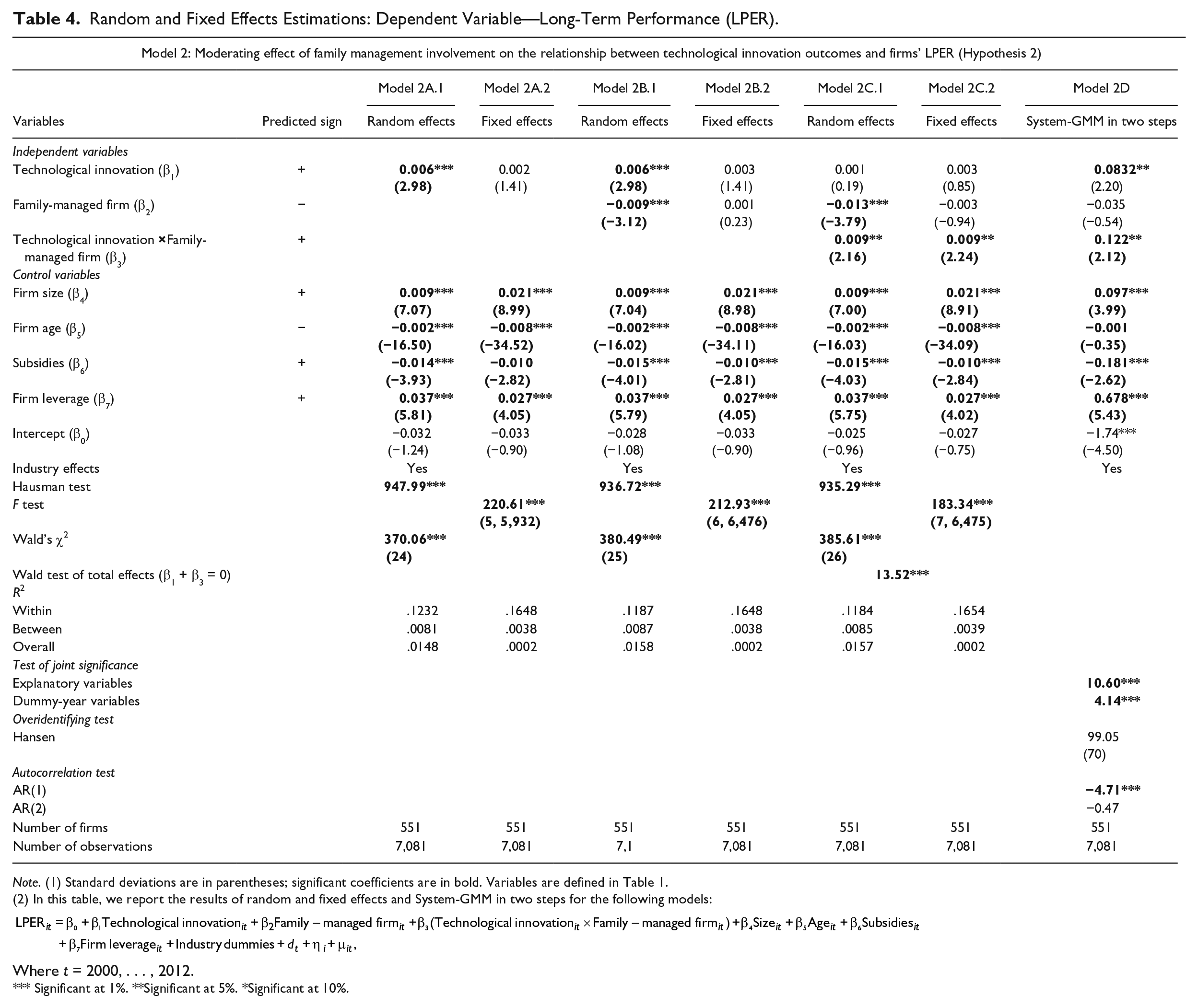

Finally, another set of four models (2A, 2B, 2C, and 2D) were developed to verify the relationship between the presence of technological innovation outcomes and long-term performance and the moderating effect of family management on this relationship. These results are listed in Table 4.

Random and Fixed Effects Estimations: Dependent Variable—Long-Term Performance (LPER).

Note. (1) Standard deviations are in parentheses; significant coefficients are in bold. Variables are defined in Table 1.

(2) In this table, we report the results of random and fixed effects and System-GMM in two steps for the following models:

Where t = 2000, . . . , 2012.

Significant at 1%. **Significant at 5%. *Significant at 10%.

In the first three cases, the Hausman test points to the fixed effect model as being the most suitable for our data set. For this reason, we chose these models to develop the following analyses (Models 2A.2, 2B.2, and 2C.2). The results show (Model 2A.2) that obtaining technological innovation outcomes has a positive but insignificant impact on long-term performance (β = .002, p > .1). The moderating effect of family management, which is included in Model 2C.2, is significant and positive, showing that family management has a positive influence on the relationship between technological innovation outcomes and long-term performance (β = .009, p < .05).

Moreover, the corrections over the panel data proposed by Arellano and Bond (1991) and Blundell and Bond (1998) have been estimated to overcome the problems of heterogeneity and endogeneity in the model. Therefore, the generalized method of moments system was applied, using a two-step estimator, so that the estimators of these models are efficient and asymptotically robust in the presence of heteroscedasticity. The results of this model support Hypothesis 2 (Model 2D). According to these results, the moderating effect of family management appears to be significant, and as a result, the positive effects of technological innovation on long-term performance are greater when the family is involved in management.

All of these relationships are explained in detail in the following section.

Finally, we conducted two additional analyses to test the robustness of the results. First, according to Chen, Tsao, and Chen (2013), innovation depends on the level of technology required to compete in a particular industry; therefore, the industry’s technology can affect the moderating role of family management in the relationship between R&D investment and CTI. Thus, we reestimated the models, distinguishing between high-tech and non–high-tech firms. As a second robustness test, we controlled for endogeneity problems. Our major concern was whether firms with a greater probability of developing CTI may also consider investing more in innovation projects. Following the recommendations of the previous literature (Czarnitzki & Kraft, 2009), all exogenous variables were lagged once and the models reestimated. The results of both tests provide robustness to those shown in Table 3. Not all of the robustness test results are reported here in full, but they are available from the authors on request.

Discussion and Conclusion

As an essential catalyst of sustained competitive advantage in firms, technological innovation has direct and indirect effects on economic growth and firm performance (Schumpeter, 1942). Unfortunately, research on innovation has ignored the effects of family management on technological innovation efficiency, that is, on the relative ability to successfully transform R&D expenses and technological innovation into CTI and long-term performance, respectively. In particular, whether family management influences technological innovation efficiency has not been addressed, despite the call by Duran et al. (2015) for additional research on the “conversion rate” of innovation input into output. This research contributes to filling this gap.

Although socioemotional wealth, which is anchored at a deep psychological level among family owners, whose identity is inextricably tied to the organization (Berrone, Cruz, Gomez-Mejia, & Larraza Kintana, 2010), is typical in family-managed firms (Martínez-Romero & Rojo-Ramírez, 2015), it can vary considerably from one family firm to another (Berrone et al., 2012). In particular, not all types of executives have the same motivations and goals, and hence they may tackle technological innovation efficiency in a distinctive manner. Thus, we draw on socioemotional wealth to determine whether family management may either improve or worsen technological innovation efficiency. The preservation of socioemotional wealth seems to be particularly high among family firms that are family managed (Block et al., 2013), and it can be used to explain the paradoxical effects in family firm innovation. This issue is particularly important because there is a need to further research the paradoxes engendered by the interactions between the ability and the willingness to engage in innovation (Chrisman, Chua, et al., 2015).

It seems that family management decreases the willingness and the ability to accomplish CTI based on R&D intensity. In particular, the orientation of family-managed firms to preserve the affective endowment, their opposition to constraining family managers’ ability to exercise their discretion to act through their ceding of control to external capital, and their lack of executive talent seem to hamper the obtaining of regular acts of technological innovation, that is, the attainment of CTI.

With respect to the effects of technological innovation, family management increases the willingness and the ability to achieve long-term performance from the occurrence of technological innovation. Family-managed firms, which are more orientated toward the pursuit of family-oriented goals, may be aware that not wagering decidedly based on the results of technological innovation to efficiently obtain long-term performance may endanger their socioemotional wealth (Gomez-Mejia et al., 2007). They become riskier than they otherwise would have been and put all their resources to work on making a minimum return from the investment and to protect the family over the long run. Once the firm has decided to adopt a technological innovation, it strategically decides to proceed and behave more riskily than in other circumstances, and its high discretion decreases the obstacles to the integration of technological innovation into its current operations in the long term. Furthermore, the firm’s great discretion to direct, allocate, add to, and dispose of its resources to decrease the barriers to the integration of technological innovation into its existing operations increases the likelihood of accomplishing appropriate long-term performance based on the achievement of technological innovation, thus better protecting its socioemotional wealth (Gomez-Mejia et al., 2011).

Therefore, our findings agree with those of studies that state that family management teams restrain the positive relationship between R&D investment and innovation performance (Liang et al., 2013) and that family managers are more efficient in exploiting their given technological innovation outputs, which in turn increases firm performance (Rosenbusch, Brinckmann, & Bausch, 2011).

In short, this study suggests making an important distinction regarding the role played by family management in both components that affect technological innovation efficiency (the impact of R&D on CTI and the influence of technological innovation on long-term performance): Family-managed firms are less likely to produce CTI based on R&D expenses, whereas for obtaining long-term performance from the occurrence of technological innovation, the opposite seems to be true.

Theoretical Implications

Our findings have several implications for the previous literature. First, our study has implications for the ongoing discussion regarding the antecedents of the conversion rate of innovation input into CTI and the conversion rate of technological innovation into long-term performance, answering the call for a shift in scholarly attention (Duran et al., 2015). We thereby extended and challenged the current literature by studying a unique element that affects the conversion rates in opposite ways, namely, family management. To the best of our knowledge, this research is the first to analyze the impact of such a factor on the antecedents and on the effects of technological innovation—even though they are different between family and nonfamily firms (De Massis, Frattini, & Lichtenthaler, 2013)—and to provide a consistent theoretical explanation for these findings. It is particularly interesting because previous research with regard to the indirect/moderating effects of family involvement on the relationship between technological innovation inputs and technological innovation outputs is practically nonexistent (De Massis, Frattini, & Lichtenthaler, 2013).

Second, this research offers an enhanced understanding of the existing models of the antecedents and long-term effects of technological innovation, particularly in SMEs. Studies that research these topics have mainly used data collected from public firms, and we do not know much about the specific context of private SMEs (Verhees & Meulenberg, 2004). Furthermore, this article introduces a more fine-grained understanding of whether the acts of investing in R&D and obtaining technological innovation contribute to creating long-term effects. This issue is notably important because it helps in having a wider understanding of firms’ risk-taking behavior related to innovation management and in identifying the reasons why some firms are able to maximize performance through technological innovation, as demanded by the previous literature (Keupp, Palmié, & Gassmann, 2012). In doing so, this study contributes to ongoing discussions on innovation and performance differences between family and nonfamily firms (e.g., Rauch, Wiklund, Lumpkin, & Frese, 2009) and helps explain why the results regarding the influence of family involvement on performance are still mixed (Stewart & Hitt, 2011).

Our findings also have certain implications for research on socioemotional wealth (Berrone et al., 2012; Gomez-Mejia et al., 2007, 2011). Prior studies have confirmed that family firms are very heterogeneous in the emphasis that they place on socioemotional wealth (Chrisman & Patel, 2012), distinguishing the motivational differences between family and founder managers (Block et al., 2013), making a distinction between family ownership and family management (Block, 2010), or analyzing how socioemotional wealth evolves over generations (Berrone et al., 2012). Our findings suggest that the socioemotional wealth influence of family management can be different depending on whether decision making is focused on efficiency in terms of CTI or long-term performance.

Practical Implications

Our results also have important practical implications for family firms. The pernicious effects of a family’s socioemotional wealth agenda on the conversion rate of R&D expenses into CTI may be combated by retaining highly skilled employees, especially in research-intensive industries, in which the job requirements are particularly demanding, and by a higher outsider influence (e.g., on the board) that is able to effectively monitor family managerial conduct in the protection of socioemotional wealth and take measures to control losses. In this sense and given that it has been proven that R&D intensity is an important source of competitive advantage for most innovative firms, it may be a good idea to appoint industry or academic experts from outside the family to identify the specific obstacles that family-managed firms are facing in efficiently achieving CTI. Government agencies and institutions can provide policies that cover the gap between family-managed firms and non–family-managed firms regarding this issue (e.g., the latest pronouncement of the European Parliament, 2015). Practitioners and advisors must adapt their best practices to meet the idiosyncratic characteristics of their firms. It must be taken into account that both socioemotional protection and measures to control losses may hinder the possibility of the employment of resources for higher-risk innovation, reducing the efficiency of the innovation process. Furthermore, families should be actively engaged to seize their unique process of human and social capital building, among others, and to foster bridges between the family and the business to create singular resources that make the exploitation of innovation output more efficient.

Limitations and Implications for Future Research

Despite the interesting results that can be derived from our analyses, we nevertheless must note a few shortcomings of this study and the implications for future research. Although this study considers family-managed firms as a particular group, we have not considered that there is heterogeneity among them. Recent research has highlighted this fact (e.g., Chrisman, Fang, et al., 2015; Kraiczy et al., 2014). In this sense, further research should be conducted to evaluate the differences among family-managed firms with regard to long-term innovation strategies. Further research also may investigate whether our conclusions change when generations evolve or when a firm changes status from founder to family. Given that socioemotional wealth appears to increase over generations, the analysis of its consequences for technological innovation efficiency seems to be a good opportunity for future research discussion. Although this study has important theoretical and practical implications, family management should be considered from a more global perspective, considering whether it implies the implementation of more formal structures, training, and/or meritocratic values, among other factors. Future research can also address how different styles of family management can affect the efficient use of R&D resources and the performance yielded from the technological innovation outcomes. Although our measures for innovation input and output have been used frequently in the literature, as cited above, it would be advisable for future articles to offer some insights into the quality of technological innovation. Finally, we are aware that the relationships explored may change across countries based on cultural contingencies (Hayton, George, & Zahra, 2002). Thus, the validity of our findings may be limited by our use of a specific sample of Spanish manufacturing SMEs.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.