Abstract

We explore how publicly listed family and nonfamily firms engage in self-serving attributions in their annual financial reports. We empirically examine how both types of firms emphasize internal attributions for good firm performance (internal-positive attributions) and external attributions for poor firm performance (external-negative attributions). We find that family firms make more external-negative attributions and that the stock market reacts more negatively to external-negative attributions made by family firms. This suggests important theoretical and practical implications for attribution theory and impression management in family firm research.

Introduction

Corporate communication is an important means of influencing a firm’s stakeholders (Zerfass, 2008). In particular, corporate financial reports, such as annual reports, are often used as a tool for conveying corporate information. For instance, the Securities Exchange Commission defines one of the main objectives of Management Discussion and Analysis (MD&A) sections of the financial reporting as “to provide a narrative explanation of a company’s financial statements that enables investors to see the company through the eyes of management” (https://www.sec.gov/rules/interp/33-8350.htm). Clatworthy and Jones (2003) note that accounting narratives are considered important and are widely used by private and institutional investors in their investment decisions. However, MD&As are also used for engaging in impression management, such as through the use of self-serving attributions where favorable outcomes are attributed to internal factors and unfavorable outcomes are attributed to external factors, beyond the firm’s control. This impression management might affect shareholder expectations, among other outcomes (W. Li, 2010).

In this article, we investigate differences between publicly traded family and nonfamily firms in their financial reporting, by focusing on the nature of the attributions that they make in these reports. Specifically, we are concerned with impression management via self-serving attributions that come in the form of either internal-positive or external-negative attributions. When self-serving attribution patterns take the form of managers making more internal attributions for good outcomes, they are called enhancing attributions because these attributions put the managers in a favorable light. When managers make more external attributions for bad outcomes they are called defensive attributions because they are shielding themselves from bad outcomes. Our focus is on these enhancing and shielding attributions in the context of company annual reports’ MD&A sections. We argue that there are attribution differences between family and nonfamily firms based on two different arguments in line with socioemotional wealth (SEW) theory. On one hand, family firms could be less interested in self-serving attributions motivated by impression management than nonfamily firms due to concerns for maintaining reputation and SEW over the long term. For example, family ownership and control have been argued to be indicative of superior corporate governance as evidenced by better firm value and performance. In this regard, Anderson and Reeb (2003) show that to an extent, higher family ownership increases firm performance. Similarly, Villalonga and Amit (2006) show that family ownership, especially in the presence of family control in the form of founder-CEO/chair, mitigates owner-manager conflict and leads to greater firm value. Family firms may also want to present the company in a light that will best reflect the values of the family based on long-standing trust (Miller & Le Breton-Miller, 2005) and on concerns for long-term orientation (LTO), longer CEO tenure, and intentions for transgenerational control (Chrisman, Chua, & Litz, 2003; Gomez-Mejía, Cruz, & Imperatore, 2014; Gomez-Mejía, Haynes, Núñez-Nickel, Jacobson, & Moyano-Fuentes, 2007; Lumpkin & Brigham, 2011; Tsai, Hung, Kuo, & Kuo, 2006; Ward, 1997). Thus, family firms are less compelled to deliberately manage the impression of the firms. This reduced self-threat decreases the likelihood of providing self-serving attributions (Campbell & Sedikides, 1999).

On the other hand, it has been suggested that the value placed on ownership is exaggerated over time due to extended self-attribution (Zellweger, Kellermanns, Chrisman, & Chua, 2012). For example, it has been noted that CEO perceptions in family firms are skewed compared to those of nonfamily members in the business. For instance, Poza, Alfred, and Maheshwari (1997) find that nonfamily managers are much less optimistic than family members in the business with respect to growth prospects and managerial capabilities, potentially due to differences based on a lack of awareness of perceptions held by nonfamily members of the family member CEO. This may also be due to family members shying away from placing blame for poor performance on other family members to avoid conflict, to avoid placing blame for failures on family business leaders (File & Prince, 1996), or due to nepotism-based biases in the allocation of credit and blame (Stewart, 2003). Hienerth and Kessler’s (2006) study of small family businesses reveals a strong tendency to exaggerate internal strengths as opposed to external aspects as reasons for business success.

We provide two novel contributions in this article. First, while the literature suggests that self-serving attributions exist in family firms (e.g., Hienerth & Kessler, 2006), these differences as compared to nonfamily firms have not been thoroughly explored. To that end, we extend the literature to provide theoretical reasoning, based on Gomez-Mejía et al.’s (2014) treatment of entrenchment and alignment incentives driven by SEW considerations, and empirically test competing arguments concerning self-serving attributions (internal-positive and external-negative attributions) in MD&A sections of annual reports to stockholders. This is important inasmuch as it helps address emerging issues in language framing and attribution research (Fiss & Zajac, 2006; Gomez-Mejía et al., 2014). By analyzing the distinct pattern of self-serving attribution in family firms, we are able to gain novel insight into attribution differences and understand the reasons why this may occur. Second, we explore how these differences might be important through the impact of the attributions on stock market reaction. Specifically, we examine the extent to which family versus nonfamily status alters the relationship between self-serving attributions and stock market valuation. While prior research has examined market responses to firm attributions (Baginski, Hassell, & Hillison, 2000; Kim, 2010; Libby & Rennekamp 2012), studies have been limited to whether markets react favorably or unfavorably to the type and extent of performance attribution in general. As such, our article makes a novel contribution to this area of research by examining how the stock market differentially reacts to family and nonfamily attributions (Anderson & Reeb, 2003) based on perceived alignment or entrenchment effects. This is important as external reactions to attributions may provide insights into how family firms are perceived by the market, including their trustworthiness.

Theory and Hypotheses Development

Attribution

Attribution theory is concerned with how an individual or entity explains the causes of an outcome. In the context of the firm and firm strategy, attributions are usually examined with respect to the top management team (TMT; Baginski, Hassell, & Kimbrough, 2004; Bettman & Weitz, 1983; Lee, Peterson, & Tiedens, 2004; W. Li, 2016; Staw, McKechnie, & Puffer, 1983). This is because, at the firm level, decision-making power is dispersed across the TMT and attributions are made and presented collectively. Furthermore, when attributions are studied in relation to stakeholder response, such as stock market reaction, the importance of focusing on individual or top management attributions is less relevant since attributions made by any constituent of a firm is just additional information regarding the firm (Baginski, Hassell, & Wieland, 2011; Conlon & Murray, 1996; Elliott, Hodge, & Sedor, 2011).

The need for attribution can come out of a variety of reasons: It can be driven by the need to understand the cause of an outcome in its own right and as a source of self-improvement, it can be used to convey competence to outside observers or as protection against their criticism, or it can be used to maintain one’s own self-esteem (Heider, 1958; Weiner, 2000). Studies on attribution at the organization level take two views. The first view is that attributions by a dominant coalition allows the organization to develop firm-wide learning heuristics and make sense of the problems faced by the firm (Ford, 1985; Nottenburg & Fedor, 1983). The second view is that attributions are an attempt at impression management (Aerts, 2005; Bettman & Weitz, 1983; Ingram & Frazier, 1983), which may be a conscious choice or subconsciously motivated. This logic is also supported by the broader literature on impression management at the organizational level (Bolino, Kacmar, Turnley, & Gilstrap, 2008; Highhouse, Brooks, & Gregarus, 2009; Osma & Guillamón-Saorín, 2011).

In management research, TMT’s attributions concerning firm performance have been of particular interest (Barker & Barr, 2002; Hayward, Rindova, & Pollock, 2004). Specifically, the attributional dimension of locus of causality has come into focus in understanding the use of impression management through self-serving attributions (Clapham & Schwenk, 1991; Keusch, Bollen, & Hassink, 2012; Merkl-Davies & Brennan, 2007). The locus attribution elicits strong responses in terms of both rewards and punishments from others (Harvey, Madison, Martinko, Crook, & Crook, 2014). Locus of causality refers to whether the cause of an outcome is identified as being internal to the actor or as something external, which is beyond the actor’s control (Weiner, 1985). Examples of internal attribution could be company initiatives, organizational strategy, or operational capabilities, whereas external attribution could be macroeconomic conditions or customer demands (Baginski et al., 2000; Baginski et al., 2004). Furthermore, the attribution may be positive or negative in nature, meaning that the event attached to the attribution had a positive, helpful effect or a negative, harmful effect. Combing the locus of causality with the positive or negative valence of the attribution leads to four different attribution types: internal-positive, internal-negative, external-positive, and external-negative (Gooding & Kinicki, 1995).

While attributions may be made to internal or external causes, the motivations, beliefs, and information underlying it may lead to lack of objectivity. In particular, when management feels the need to self-enhance, self-protect, or have effective control over future events, they would make attributions that are self-serving (Kelley & Michela, 1980). Often it takes the form of impression management in firms, wherein the top management tries to create specific impressions on the stakeholders by manipulating the type of attributions they make (Gardner & Martinko, 1988; Staw et al., 1983; Zott & Huy, 2007). Impression management is defined as conscious or unconscious attempts to “control images that are projected in real or imagined social interactions” (Schlenker, 1980, p. 6). It is frequently used at the organization level to influence outsiders’ and insiders’ perceptions of an organization (Brown, 1997; Elsbach, 1994). Notably, when the motives of self-enhancement and self-protection are involved, managers tend to make internal attributions for positive outcomes and external attributions for negative outcomes (Zuckerman, 1979). Instances of self-serving attributions are pervasively present across letters to shareholders, annual reports, and CEO interviews (Aerts, 1994; Clapham & Schwenk, 1991; F. Li, 2010b; Kim, 2010).

On the other hand, it has also been argued that the presence of such a pattern of attribution is not necessarily intended to be misleading (Merkl-Davies & Brennan, 2007; Miller & Ross, 1975). The main argument in this regard is that individuals do not purposefully pursue activities that result in failure and that it is quite possible that when failure does arise, they believe it is in spite of the positive internal factors. Thus, the preponderance of internal (external) attributions for positive (negative) outcomes may be not because they are a form of impression management but because that is what the firm’s management actually believes. As skewed as these beliefs may be, the attributions are only intended to provide incremental information (Baginski et al., 2000; Libby & Rennekamp, 2012).

Attribution in Family Firms

Studies addressing attribution and, in particular, attribution differences in family versus nonfamily firms are relatively scant. For instance, while Hienerth and Kessler (2006) find that small family businesses mostly attribute internal factors positively and external factors negatively, their study is not concerned with whether such self-serving patterns are distinct to family firms. However, several studies have conceptually examined the possibility of such differences. For instance, Zellweger, Nason, Nordqvist, and Brush (2013) suggest that the overlap between family and firm identity and family’s need for transgenerational continuity means that family firms are more concerned with the maintenance of corporate reputation and SEW in a way that does not compromise the firm in the long run. Reputation and SEW can discourage family firms from engaging in impression management, whereby they use internal-positive and external-negative attributions that are self-serving, because their reputation—a nonfinancial aspect of their firm—is wrapped up in their identity and is necessary to meet their affective needs. At the same time, they suggest that the family’s desire to preserve a positive self-image, their visibility in the public eye, and consequent institutional pressures to meet expected firm performance can incentivize impression management (de Vries, 1994; Zellweger et al., 2013).

Others have suggested that familial altruism can affect the way in which the causes of performance are evaluated in family firms. Eddleston and Kidwell (2012) suggest that altruism in parent-CEOs cause them to regard the actions of their children more generously and be more forgiving of their workplace deviance. Furthermore, altruism leads to bias in how family firms’ CEOs perceive their children as employees (Schulze, Lubatkin, Dino, & Buchholtz, 2001). Gomez-Mejía, Nunez-Nickel, and Gutierrez (2001) suggest that “assessment of agent performance under family contracting may shift negative performance attributions from the agent to exogenous forces” (p. 84). Similarly, Stewart (2003) posits that nepotism, the offshoot of altruism in family firms, makes it difficult to recognize mistakes and give credit where it is due. In short, research on altruism in family firms may affect impression management by shifting negative attributions from internal to external causes, in the name of protecting the good names of family members.

Family Firms: Agency Effects and Self-Serving Attributions

While prior literature has alluded to the possibility of differences in family and nonfamily attributions, we do not have a comprehensive understanding of how family firm characteristics affect their performance attributions via impression management. The existence of such differences can have important consequences because the information content in financial reports plays a key role in the decision-making process of investors (Clatworthy & Jones, 2003; W. Li, 2010). To examine differences in family firm impression management, we apply the lens of agency theory and draw on Gomez-Mejía et al.’s (2007) conceptualization of SEW wealth in family firms. In particular, we look at family firms’ distinct set of pecuniary and nonpecuniary incentives, how they lead to entrenchment and alignment motives, and consequently how they lead to greater or lesser self-serving attributions.

Entrenchment effect

Family members who are deeply involved in the business are privy to more inside information and possess more knowledge about the internal functioning of the firm due to their long-standing association with it, over and above others in firm leadership who are not family members. Such inside knowledge can give them an advantage over other less informed stakeholders and give them ample opportunity to manipulate firm affairs and expropriate funds for private benefit. Furthermore, a potential downside of beneficial ownership in family firms is that it gives family owners the power to use the firm to maximize their personal benefits as opposed to those of its shareholders. When this is coupled with the objective of generating SEW, family firms engage in activities that go beyond the immediate expropriation of funds. For instance, the need to retain family control can make family firms more sensitive to the cost of capital, and incentivize them to withhold inside information that can increase the cost of capital (Prencipe, Markarian, & Pozza, 2008; Zellweger, 2007). The importance of transgenerational control can also put more pressure on family firms to meet analyst expectations and prevent any vulnerability in the market for corporate control (Gomez-Mejía et al., 2014). Issues of succession and futurity also heighten the levels of dependence between family members within the firm (File & Prince, 1996), making them more willing to collude. Given this, family employees could be more willing to conceal damaging information and collude in the creation of a common front to reduce the risk of displeasing its stakeholders. This in turn can lead to family firms managing impressions through making more self-serving attributions (internal-positive and external-negative) in their financial reports, particularly because it is only a cosmetic form of manipulating stakeholder impressions as opposed to riskier forms such as earnings management (Gomez-Mejía et al., 2014).

Beyond family control, the SEW in family firms also hinges on their ability to maintain family harmony and identity. Family firms may have a stronger motive to assert their identity (Zellweger, Eddleston, & Kellermanns, 2010). Prior literature suggests that family firms believe they have greater influence over firm activities and tend to have a more optimistic self-view than other nonfamily employees (Hienerth & Kessler, 2006; Poza et al., 1997). They also engage in more self-enhancement and attempts to create a positive self-image (Berrone, Cruz, & Gomez-Mejía, 2012). Thus family firms may have a more flattering self-view than nonfamily firms. Finally, the well-being of the family members, both within and outside of their family firm, depends on their ability to preserve harmonious relationships. This can cause them to shy away from placing blame or punishing other family members, even when they are responsible for the worsening of firm performance. Furthermore, the greater cohesiveness between family members also makes the firm more vulnerable to group-serving attributions (Ensley & Pearson, 2005). Thus, if the entrenchment effect dominates in family firms, we expect them to make more self-serving performance attributions than nonfamily firms, that is, family firms manage impressions through making more internal-positive and external-negative performance attributions in their MD&As.

Alignment effect

The flip side of the entrenchment effect is the alignment effect, whereby beneficial owners can use their controlling ownership and superior firm knowledge to better monitor the activities of the firm and ensure that managements’ actions are aligned with shareholder interests. Some argue that this alignment effect is accentuated in family firms due to LTO (Wang, 2006). The desire to retain transgenerational control creates greater incentive to forego actions that provide family firms with only short-term benefits. Instead, it creates stronger incentive for family firms to engage in activities that help build their reputations and sustain them in the long run, such as better monitoring (Anderson & Reeb, 2003). We extend their line of reasoning to assert that family firms are not as concerned about how the stock market reacts to them in the short run, or the temporary changes in debt costs, as they are with the long-term outlook these stakeholders have of their firms. Thus, family firms’ impression management efforts would be directed toward preserving their good name and image through quality reporting with less self-serving attributions (internal-positive and external-negative). Better alignment between management and stakeholders may also allow family firms to develop a stronger identification with close stakeholders. This identification may be manifest by long-term employee loyalty (Anderson & Reeb, 2003) and lower cost of debt with creditors (Anderson, Mansi, & Reeb, 2003), reducing the need for self-serving attributions. Both family and nonfamily firms may reap the benefits from this alignment—a strong identification with stakeholders—yet we expect stronger alignment effects among family firms, as suggested by the literature (Wang, 2006). Overall, if the alignment effect dominates in family firms, we expect them to make fewer self-serving performance attributions than nonfamily firms, that is, family firms would make fewer internal-positive and external-negative performance attributions in their MD&As.

Given that prior literature on agency effects provide opposing predictions regarding the dominant agency effect in family firms, we make the following competing hypotheses, regarding attributions in family firms:

Family Firm Attributions and Stock Market Response

The extant literature suggests that investors take into account the type of performance attributions that are made by an organization’s management (e.g., Brennan & Merkl-Davies, 2013; Salancik & Meindl, 1984). It should not be surprising that investors are well aware of impression management through self-serving attributions by managers, especially voluntarily released information. Specifically, Kimbrough and Wang (2014) find that “investors neither ignore seemingly self-serving attributions nor accept them at face value, but rely on industry- and firm-specific information to assess their plausibility” (p. 635). Along these lines, Barton and Mercer (2005) show that external attribution for poor performance improves stock valuation when the attribution seems plausible but worsens the valuation when the attribution seems implausible.

While self-serving attributions have been shown to exist in firms generally, and family firms in particular (Hienerth & Kessler, 2006; Staw et al., 1983), there is a paucity of research examining the extent to which any differences in self-serving attributions across family and nonfamily firms might influence the market in their response to firms’ disclosures. Of importance in exploring this issue is to highlight that while earnings announcements give the market concrete data about a firm’s performance, it is in the annual report of a firm that upper management explains why the firm performed as it did. In other words, exploring the impact of management attributions, and importantly the potential self-serving attributions about performance that are manifest in firm annual reports, provides the market an opportunity to respond to those attributions shortly following the report’s release. Naturally, there are a large number of other factors that may affect changes in share price, but our focus is in line with scholarly research that suggests that MD&As report on incremental—but still potentially impactful—information relevant to analysts’ and the stock market’s decision making and forecasting (Barron, Kile, & O’Keefe, 1999; Clarkson, Kao, & Richardson, 1999; Cole & Jones, 2004; Davis & Tama-Sweet, 2012; Lang & Lundholm, 1996; F. Li, 2010a; Zhang & Wiersema, 2009).

It is also important to note that our arguments with regard to stock market price are not on the basis that family firms have direct motivations or intentions to engage in impression management via self-serving attributions in order to influence the stock market. In other words, any differences in impression management patterns may not be due to deliberate deception, and impression management may not always be purposeful. Nevertheless, the market may react to the perceived intentions behind any self-serving attributions in their financial reporting and thereby affect how it “rewards” or “punishes” firms for any impression management. In other words, the messaging of the attributions contained in the MD&As offers signals from firms to the market, and it is the stock market’s perception regarding the attributions that ultimately affect stock value. We propose that the perceived intentions—as viewed by the stock market—underlying self-serving attributions made by family firms connect SEW theory to market response. For example, Baginski et al. (2000) show that the level of credibility of performance attributions can vary, and this variability can affect the stock price. As a consequence, the market will react more negatively to family firms’ perceived self-serving attributions if they are viewed as “lower quality” or inaccurate. Conversely, the market will react more positively to family firms’ perceived self-serving attributions if they are viewed as “higher quality.” The distinct perception regarding the quality or plausibility of family firm attributions is a result of the notion that family firms focus on SEW in addition to monetary wealth maximization.

The entrenchment and alignment effects of SEW theory provide competing views on how the stock market may react to self-serving attributions. From an entrenchment effect perspective, the stock market may view any perceived self-serving attribution with skepticism, and therefore consider it less plausible. If the market reckons that family firms are engaging in deliberate impression management, it is likely to “punish” family firms in the short term (as compared to nonfamily firms). This would be due to the view that the market may interpret self-serving attributions as based on placing SEW preservation above the pursuit of financial wealth for the firm (Gomez-Mejía et al. 2007; Martin, Campbell, & Gomez-Mejia, 2016). There are a number of potential reasons why a family firm may be viewed as engaging in impression management. For instance, the firm may be viewed by the stock market as trying to maintain family control; possessing a more positive self-view of their own skills (Zellweger et al., 2013); being biased in favor of family members in a leadership position (Schulze et al., 2001); prioritizing the family’s interests, such as job security, avoidance of conflict, and access to business resources, above those of nonfamily stakeholders (Le Breton-Miller & Miller, 2013); or even having altruistic tendencies toward other family members in the firm (Eddleston & Kidwell, 2012). If this is the case, then the performance attributions are going to be viewed as having lower plausibility. Consequently, the market should react more negatively to perceived self-serving attributions in family firms.

From an alignment perspective, the stock market may view the incentives of family firms as better aligned with those of its stakeholders (Wang, 2006). For instance, the stock market may believe that family firms have greater LTO and hence are more focused on building and maintaining their reputations. The care for the long-term SEW of the family firm may create incentives to build and sustain long-term relationships with all stakeholders by increasing trust and establishing greater monitoring (Anderson & Reeb, 2003). Additionally, long-term SEW creates incentives to maintain firm well-being for later generations and is manifest by competent, motivated family members who invest generously in the business and in its continual renewal (Le Breton-Miller & Miller, 2013). Therefore, the alignment effect would also assume that the stock market believes that the family firm has an incentive to be ethical in their attributions and reporting, rather than engage in any behavior that might put at risk their SEW (Martin et al., 2016). In other words, perceptions of an alignment effect would increase the perceived plausibility, as family firms with strong SEW alignment would avoid any behavior that puts at risk the firm’s reputation (Berrone et al., 2012), such as inaccurate or self-serving attributions. In this case, family firm performance attributions would be viewed more credibly than those made by nonfamily firms, making the market react less negatively to self-serving attributions of family firms. For these reasons, we make the following competing hypothesis, to represent perceptions of entrenchment and alignment effects:

Method

Sample

Qualitative disclosures are a source of incremental information and a means for reducing information asymmetry. For instance, Merkley (2014) show that qualitative R&D disclosures increase the information content and reduce the information asymmetry in firm performance. Research in finance has likewise shown that factors such as tone, negativity, and other communicative aspects present in narrative disclosures such as annual reports are important to stock performance (Loughran & McDonald, 2011; Loughran & McDonald, 2014). Davis and Tama-Sweet (2012) find that negative disclosures by a firm are related to its stock performance. The usefulness of qualitative disclosures as a source of information would be greatest when there is perceived performance uncertainty. The need to reduce information asymmetry will be particularly strong in the pharmaceutical industry where given the vicissitudes of the external environment, the uncertainty of drug development and the unpredictable actions of competitors, weaving an array of scientific, clinical, regulatory and commercial data into a numerical representation of value for a drug is a substantial challenge. (Cha, Rifai, & Sarraf, 2013, p. 737)

Hence we believe that our data set, which consists of the population of publicly traded firms in the pharmaceuticals (SIC 2384) industry, is appropriate in the context of the study.

There are several other reasons why the pharmaceutical industry is an appropriate context for our study. First, it has a relevant mix of family and nonfamily firms. Although other industries share this attribute with pharmaceuticals, it is a necessary condition that eliminates many other industries, especially those where the majority of firms are privately (as opposed to publicly) held. Having a notable amount of publicly held firms is a necessarily precondition for our study as, at least in the United States, only these publicly held firms provide available financial reporting and MD&As (the source of our attribution data). The proportion of family firms in the pharmaceutical industry is also representative of the proportion of family firms among publicly listed firms (approximately 35%), as compared to the S&P 500 data of Anderson and Reeb (2003). Relatedly, we also needed an industry that was large enough to provide adequate statistical power while also maintaining the benefits of a single-industry study such as controlling for unexplained variance.

Second, it was important to have a relatively homogenous set of industry conditions and similarity among success factors. Relative to other industries that have many subindustries, the pharmaceutical industry is comparatively homogeneous. This is useful to the extent that this allows us to eliminate alternate macro or subindustry explanations for our findings. Indeed, while Cool and Schendel (1987) found differences in market share between pharmaceutical firms in their 20-year study of the industry, there was no difference in terms of profitability, risk, and risk-adjusted performance.

Third, it was important that the industry be important to market analysts, since a condition of the effects that we propose to see will hold true only if individuals read and attempt to scrutinize the attributions that are made in the MD&As. The pharmaceutical industry has consistently been one of the most profitable industries, with margins topping 20% in 2015 (Chen, 2015), while stock market returns beat the S&P 500 by more than 27% over the past 10 years (89.51% vs. 70.40 %; Fidelity, n.d.). These results suggest that this industry should be important to analysts and worthy of their attention, hence the importance of attributions in management communications to this stakeholder group.

Fourth, the pharmaceutical industry is marked by low munificence, 0.44 standard deviations below the median of the 50 largest industries in Compustat (Moss, Payne, & Moore, 2014). In other words, this industry is marked by higher levels of competition, fewer opportunities for growth, and fewer available resources compared to other industries we could have chosen (Dess & Beard, 1984). And since higher stock prices lead to greater resource availability due to market desirability, it is reasonable to expect that management communications with analysts would be more important to industries marked by lower munificence in order to increase the stock price.

Fifth and finally, the literature on LTO has consistently shown that family businesses have a greater LTO than nonfamily businesses (Brigham, Lumpkin, Payne, & Zachary, 2014). This finding aligns well with our industry choice because pharmaceuticals, being an R&D-intensive industry, has a greater long-term perspective than other types of industries due to the uncertainties of drug development, making this industry an appropriate choice for a family business study than other industries with a shorter time horizon. Teasing out the influence of family businesses in an industry already marked by a high LTO provides an even more challenging context for our study.

We took the entire population of publicly listed U.S. firms that have 10-K/KSB filings in the Securities Exchange Commission Edgar database for the fiscal years 2005 and 2006. Thus we had 219 firms and 427 firm-year observations in our initial sample, as not all firms have filings for both years. We eliminated firms that had fewer than two attributions in the entire MD&A statement, since we are interested in the share of different types of attribution made in the MD&A. This reduced our sample to 365 firm-year observations. After eliminating firms with missing data for performance growth (a control variable) for Hypotheses 1 and 2, we have 113 family firm-year observations and 206 nonfamily firm-year observations. For Hypotheses 3 and 4, we include a control for unexpected earnings (UE), which is typically used as a predictor when cumulative abnormal returns (CAR) is the outcome variable. This led to a sample of 87 family firm-year observations and 184 nonfamily firm-year observations. On average, the firms included in our study on average 24 years old (with a maximal age of 157 years) and quite large (mean total assets of $2.72 billion and standard deviation of $11.95 billion). These size numbers are slightly skewed by the eight largest firms (e.g., Pfizer, Johnson, & Johnson, Merck, Wyeth, Abbott, Bristol-Myers-Squibb, and Lilly [Eli]). The average age of the firms is also slightly skewed by the 10 firms that are over 100 years old and the 52 firms that are fewer than 10 years old.

Variables and Measures

Attribution

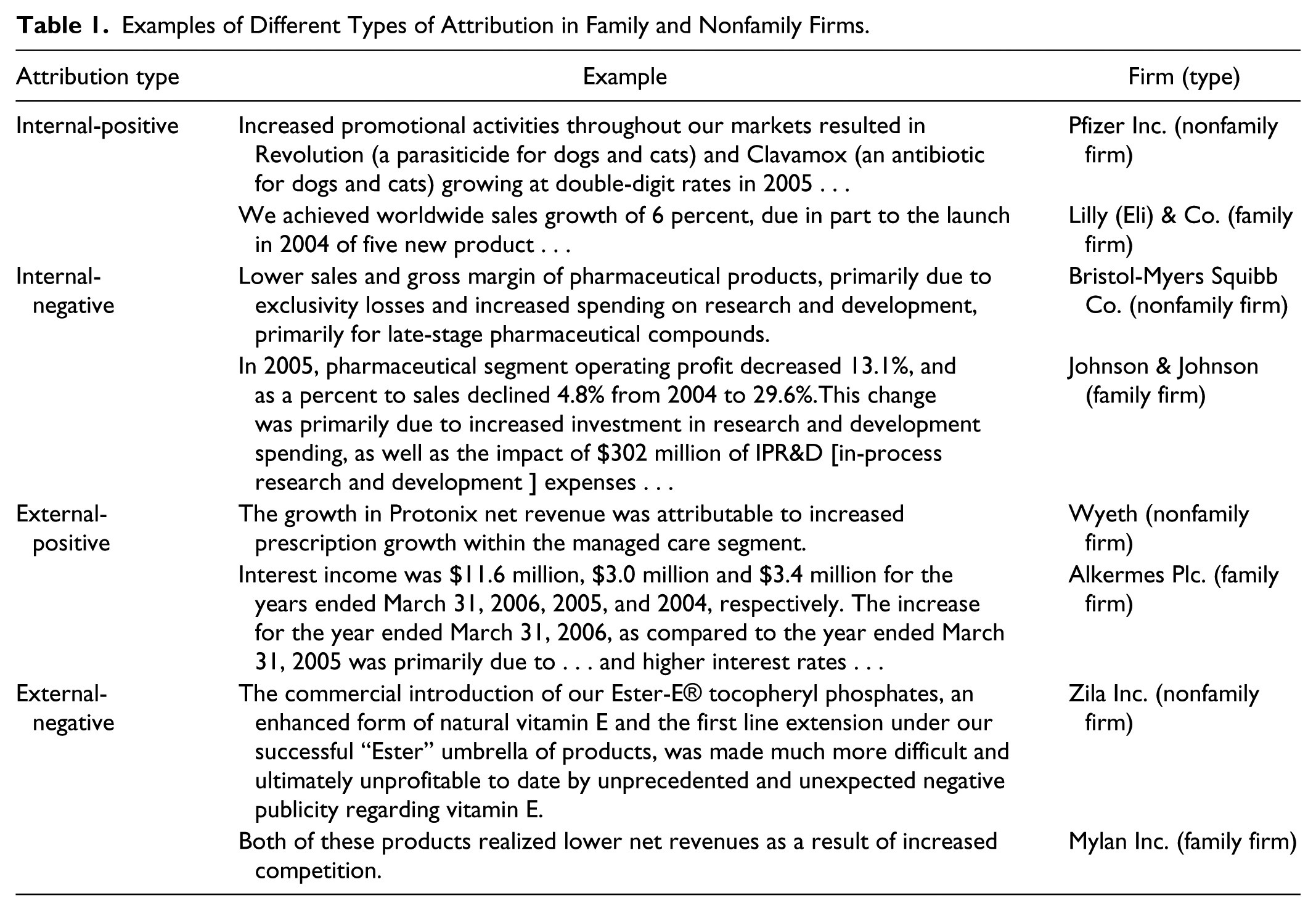

We use attribution as the dependent variable for Hypotheses 1 and 2 and the independent variable in Hypotheses 3 and 4. We use content analysis to develop our measures for attribution. Specifically, we draw on the MD&As of the company 10-Ks to code top management’s view of the internal and external causes of firm performance. As we describe in greater depth below as to our specific coding, we view internal causes as including items such as strategic decisions made by the firm, product launches, operational costs, and efficiencies. In contrast, external causes include new legislation, lawsuits, 1 customers, macroeconomic factors, and unforeseen circumstances among others. This classification of firm performance attribution is in line with the literature, where internal causes pertain to the skills, organization, and strategy of the firm and external causes pertain to things that happen outside the firm such as economic, environmental, governmental, and third-party issues (Baginski et al., 2000; Baginski et al., 2004). If an internal cause relates to positive change in performance, it is coded as an internal-positive attribution, while if it relates to a negative change, it is an internal-negative attribution. Similarly, if an external cause leads to better performance, it is coded as external-positive, or an external-negative for worse performance. Table 1 illustrates these with excerpts from firm MD&As. As our focus is on the potential of self-serving attributions, we focus our tests on internal-positive and external-negative attributions only. We capture these as ratios (i.e., the number [count] of internal-positive attributions divided by the sum total count of all attributions in the MD&A section) to control for the salience of these types of attributions.

Examples of Different Types of Attribution in Family and Nonfamily Firms.

In terms of the coding process, the first step involved reading through sample MD&As to see what kind of performance measures firms were making attributions for. To identify an attribution as codeble we use Bettman and Weitz’s (1983) notion of causal reasoning, wherein they define it as “a phrase or sentence in which some performance outcome, such as profits, sales, or return on investment, was linked with a reason for that outcome” (pp. 172-173). If causal attribution was made for an improvement in performance, it was classified as a positive attribution. Conversely, if causal attribution was made for a worsening in performance measure, it was classified as a negative attribution. This part of coding an attributional instance was relatively straightforward, since the direction of performance change that is being discussed is obvious. Next, we identified the causal factor associated with the performance outcome as either internal or external. We define causal attribution as the indication of an internal or external cause for performance change in the MD&A. In addition to using the classification logic applied in the literature (Baginski et al., 2000; Bettman & Weitz, 1983), we tried to see what impressions the attributions gave in terms of the cause being internal or external, that is, we allowed the various categories within external and internal attributions to emerge from the data. This led to a two-by-two attribution classification: internal-positive attributions, internal-negative attributions, external-positive attributions, external-negative attributions.

After coding sample MD&As in this fashion, further subcategories were created to understand some of the underlying themes within these external and internal attributions. Following this, we created an attribution identification and classification scheme. This allowed us to more readily discuss the logic behind internal and external attributions with the second trainee coder. A summary of our attribution coding schema is provided in the appendix.

The primary coder proceeded to code the MD&As in our study using the Nvivo software. With this software, each instance of an attributional coding of a firm’s MD&A was filed and linked to the relevant text in the actual MD&A. The software allowed us to give each firm-year four separate folders, one for each type of attribution categories. Within these folders, each instance of a specific type of attribution was marked along with the appropriate text from the MD&A. Clicking on any of the text segments within a specific attribution folder brought us to the firm’s MD&A and the segment of the MD&A from which the text was abstracted. This allowed the primary coder to revisit all the codings later, to ensure that the attribution classification scheme still held both before and after the second coder’s attribution ratings. If it did not, the coder simply moved the specific text to the appropriate attribution folder. Doing this also simultaneously corrected the attribution count indicated by the attribution folders.

To ensure the validity of the attribution codings, we trained a second coder to cross-check the original coder’s ratings. In cases where there were initial disagreements between the coders, the two coders discussed and attempted to reach an agreement in line with the coding scheme. In the few cases where an agreement could not be reached, a third reviewer versed on the coding provided an independent view. This third reviewer cast the decisive coding. We examined the reliability of attribution codings by looking at the average Pearson correlation between coders’ tally for each of the attributions (internal-positive (.86), internal-negative (.61), external-positive (.75), and external-negative (.73)). Thus we have an interrater reliability of .73 on average. We also looked at the intraclass correlation (ICC) between coders for each of type of attribution. Since each firm’s attributions were coded by the same two coders, we specified a two-way ICC model. Additionally, we specified a single-measures ICC, since we did not use an average of the attribution codings of the two coders. As per cutoffs and nomenclature provided in the literature for qualitative coding, the absolute agreement in these ratings was excellent for internal-positive attributions (.86), good for external-negative and external-positive attributions (.67 and .69), and fair for internalnegative attributions (.59; Cicchetti 1994; Hallgren, 2012).

Stock Market Response

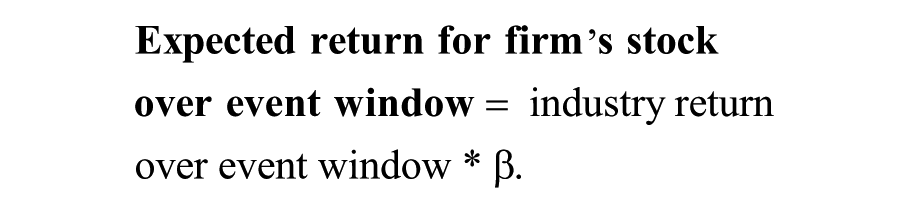

We use stock market response as the dependent variable for Hypotheses 3 and 4. We use Wharton Research Data Services Center for Research in Security Prices data to capture stock price response of the market to firms’ performance attribution. We use CAR around the release of the 10-K (from which we extract the MD&A for coding attribution) to capture market response. CAR is the difference between the return on the stock in question and its expected return averaged over a window of 2 days on and after the release of the firm’s 10-K. Following Baginski et al. (2000), we estimate the stock’s expected return based on the performance of the stock relative to the performance of the market over a period of 200 to 31 days prior to the release of 10-K. Mathematically, the formula for CAR for firm i can be expressed as follows:

where

β is firms’ stock return volatility compared to industry return volatility. It is calculated by regressing firms’ stock return on industry return, over a period of 200 to 31 trading days before the event.

Family Firm

Following other research in the family business literature for publicly traded firms, our main definition of a “family firm” is a firm where the firm founder, his or her family members, or both were either on the board of directors or in a senior management position and the founding-family has at least 5% percent ownership in the firm (Anderson & Reeb, 2003; Chrisman & Patel, 2012; Villalonga & Amit, 2006). We chose this definition because accounting for both family ownership and control allows us to ensure that the family has influence over the construction of the MD&A. This definition also accommodates the continuing theme of family firm heterogeneity (cf., Jaskiewicz & Dyer, 2017), also present in the pharmaceutical industry. For example, family firms in this industry are both large (e.g., King Pharmaceuticals, >3000 employees) and small (e.g., Depomed, <50 employees). We also expect family pharmaceutical firms—which should have a relatively long time horizon—to differ from family firms in other industries with a shorter time horizon, despite age differences (Le Breton-Miller & Miller, 2013). To determine a firm as family or nonfamily we went through the firms’ annual reports, DEF (definitive) 14A, and other online sources such as Bloomberg and BusinessWeek. We code family firms as a binary variable, with a coding of 1 for family firms and 0 for nonfamily firms.

Control Variables

We include controls for change in performance, measured as the growth in sales, that is, change in sales in the current year compared to sales in the previous period, (sales t − salest − 1)/sales t − 1, in order to control for any year-to-year changes that might affect the tone of the MD&A discussions. We log-transformed this measure in order to make it normally distributed, circumventing the concern that firms with smaller sales bases can grow exponentially. We also control for year (fiscal year) to capture potential differences in our results between our 2 years of data collection, firm size and firm age. We operationalize firm size using total assets and firm age with the number of years since founding. We collected founding year data primarily from firm websites, Bloomberg, and company annual reports. Since firms are often founded prior to their IPOs, we relied on IPO data (from Compustat) only if founding year data were not available from other sources. Nonetheless, we also noted that sometimes company annual reports also present their IPO date as their year of inception. This may account for the large number of young firms. Since firm size and firm age are highly correlated and not normally distributed, we log-transformed the two measures.

In Hypotheses 3 and 4, where CAR is the dependent variable, we include an additional control for UE. A firm is said to have UE when its reported earnings are different from its expected earnings. When reported earnings are higher than expected, the stock market response tends to be positive and vice versa. Thus, it is typical to control for UE in a test of CAR calculated around the release of annual earnings announcements. However, the MD&A is released after there has already been an earnings press release and so the market is informed of any earnings “surprise.” Thus the market has had the opportunity to factor in earnings information and need not respond to the unexpected earnings, when the MD&A comes out. Nonetheless, as a precaution, we control for UE.

UE is calculated as the difference between the firm’s actual earnings per share (EPS) and the analyst forecast of EPS scaled by stock price in the previous month. We collected the analyst forecasts closest to the date of a firm’s earnings announcement date. We use analyst data provided by the Institutional Brokers’ Estimate System (IBES). IBES defines analyst as follows: “Person at the sell-side institution or contributing analyst making the forecast” (I/B/E/S Detailed History User Guide, a Guide to the Analyst-by-Analyst Historical Earnings Estimate Database, March 2013, Partners’ Edition). Analyst forecasts were available in IBES for 259 firm-year observations. For the remaining firms we used the random walk model (Baginski et al., 2000; Foster, 1977). We calculate UE for firm i at time t using the following formula:

Analysts typically follow more substantial firms. In the case where firms did not have an analyst forecast, we follow Foster (1977) and measure expected earnings as the product of EPS in the previous period (EPS i,t − 1 ) and the 5-year average annual change in sales (∆sales average i ).

Results

Main Results

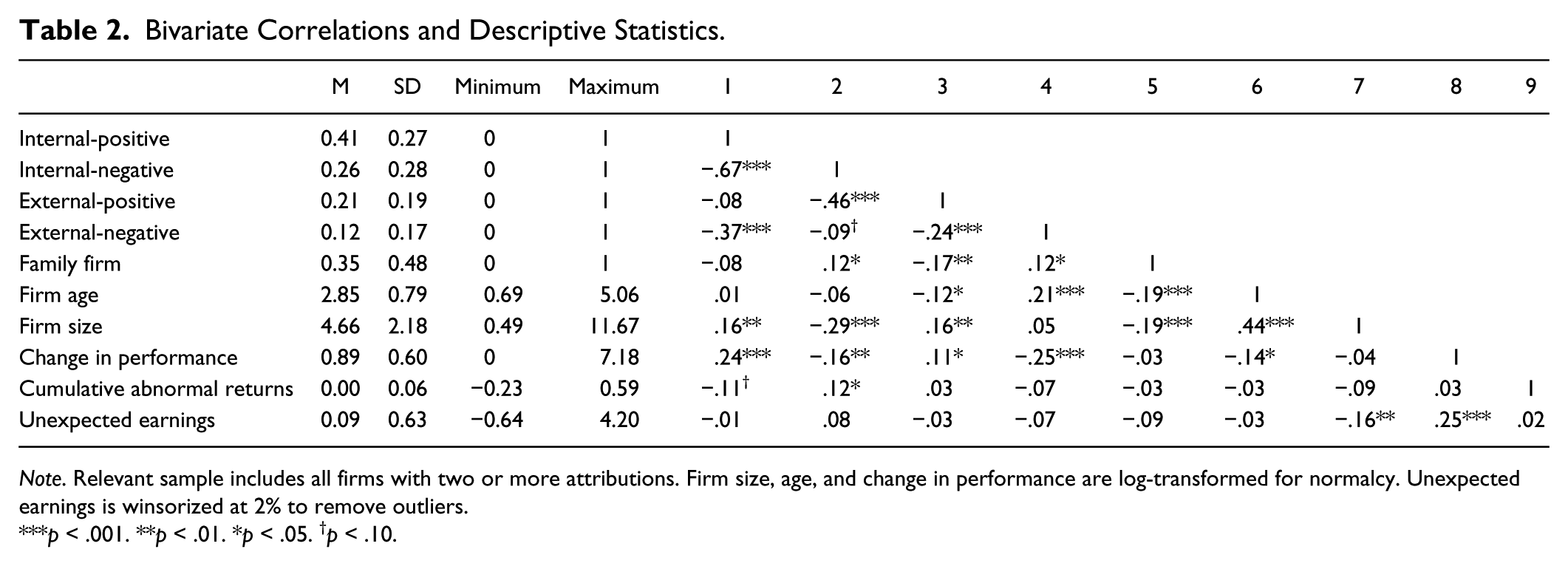

The bivariate correlations and descriptive statistics are available in Table 2. We note that internal-positive attribution is not statistically significantly correlated with family firms, whereas external-negative attribution is positively correlated with family firms (p < .10). While the former does not support our hypothesis, the latter does provide some initial insights. To test our hypotheses, we use a model that is appropriate for panel data. We cannot use a fixed effects model because the family/nonfamily status is a time-invariant characteristic. Consequently, it would be absorbed by the intercept. We therefore use a random effects model clustered by firm. Random effects models have been applied in other studies examining the determinants of abnormal returns (Beckman & Haunschild, 2002; Madsen & Rodgers, 2015; Malmendier & Tate; 2008; Park & Mezias, 2005).

Bivariate Correlations and Descriptive Statistics.

Note. Relevant sample includes all firms with two or more attributions. Firm size, age, and change in performance are log-transformed for normalcy. Unexpected earnings is winsorized at 2% to remove outliers.

p < .001. **p < .01. *p < .05. †p < .10.

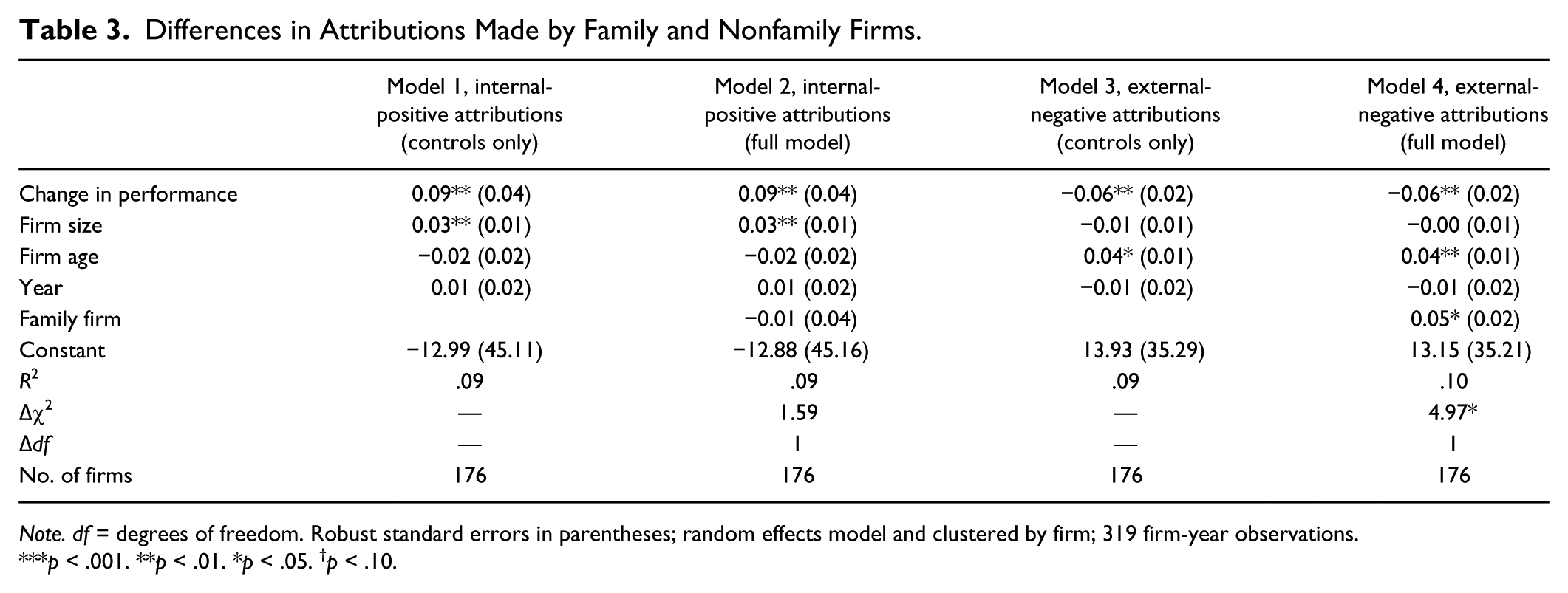

To test Hypotheses 1 and 2, we run separate regressions with our variables of interest: internal-positive and external-negative attributions (Table 3), since these two would be most illustrative of self-serving attribution. Models 1 and 3 contain the control variables, while in Model 2 we regress internal-positive attributions (the independent variable in Hypotheses 1 and 2) on all the controls and family status. The findings in the models suggest that firm size is the only variable that is positively and significantly related to the use of internal-positive attributions. This does not provide support for Hypotheses 1a and 2a. In Model 4 we regress external-negative attribution on all the controls and family firm status. We find that being a family firm is positively and significantly related to the use of external-negative attributions (β = 0.05, p < .05). The change in χ2 is also statistically significant (p < .05), with the inclusion of external-negative attributions. Thus, we find support that family firms use more external-negative attributions (Hypothesis 1b). Given the competing nature of the hypothesis, this finding eliminates support for Hypothesis 2b.

Differences in Attributions Made by Family and Nonfamily Firms.

Note. df = degrees of freedom. Robust standard errors in parentheses; random effects model and clustered by firm; 319 firm-year observations.

p < .001. **p < .01. *p < .05. †p < .10.

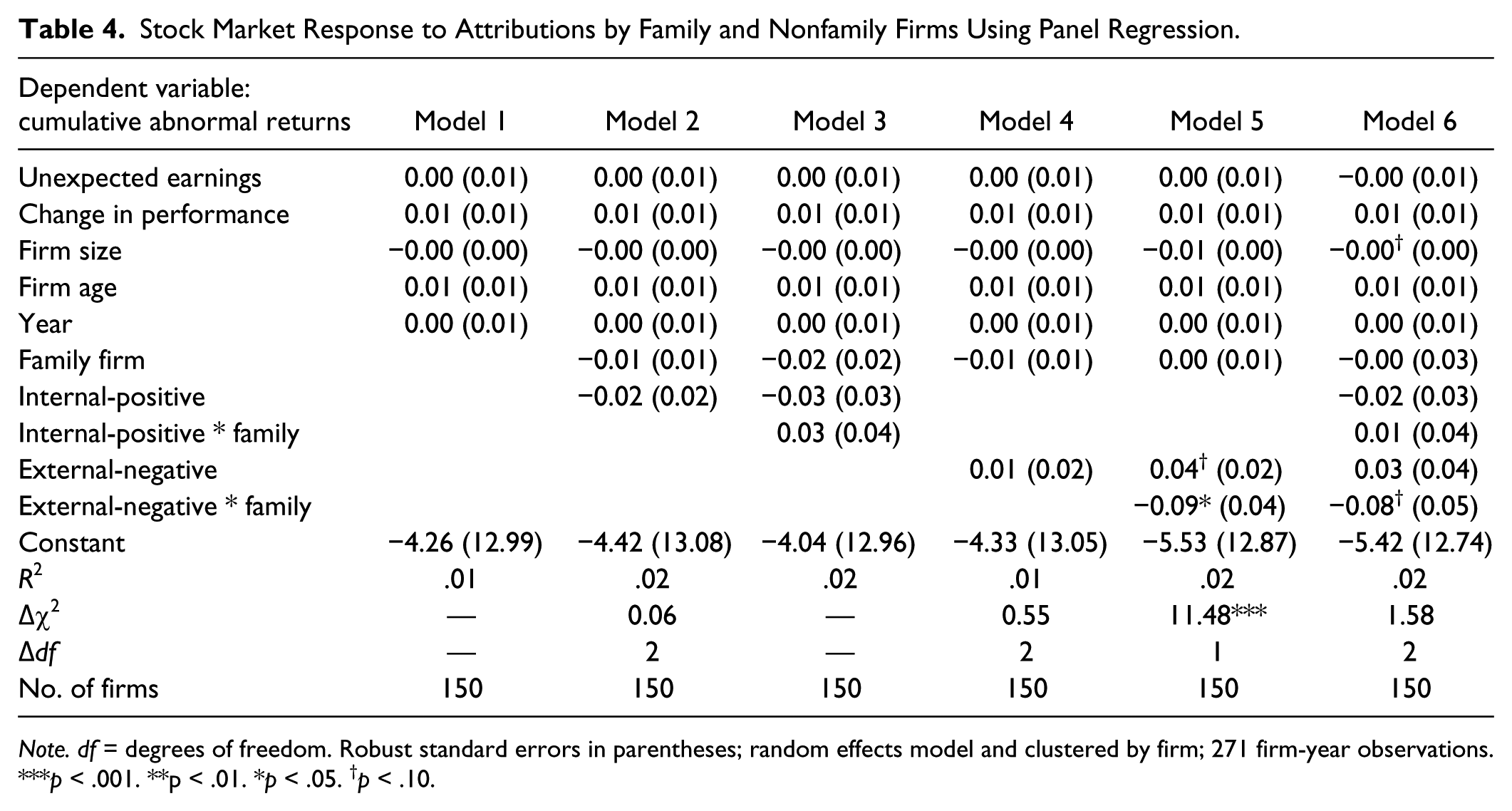

To examine Hypotheses 3 and 4, we look at whether performance attributions involving a self-serving bias have a significantly different effect on the CAR of family firms versus nonfamily firms. For this, we first run a random effects model clustered by firm (Table 4). We use hierarchical regression, similar to what we did for Hypotheses 1 and 2, whereby we first enter the group of control variables (Model 1). We then include the focal attribution variable(s) and family firm variable (Models 2 and 4). Next we include the interaction of each attribution variable with family firm variable (Models 3 and 5). Finally, in the full model (Model 6), we include all the controls, family firm variable, and both attribution variables and their interactions with the family firm status. If the market believes that family firms display a self-serving bias, we expect the interaction term between family firm status and relevant attribution variables to be negative.

Stock Market Response to Attributions by Family and Nonfamily Firms Using Panel Regression.

Note. df = degrees of freedom. Robust standard errors in parentheses; random effects model and clustered by firm; 271 firm-year observations.

p < .001. **p < .01. *p < .05. †p < .10.

In the regressions (Table 4, Model 3), we see that the coefficient of the interaction term involving internal-positive attribution is not statistically significant. This does not support our expectation that the stock market would respond negatively or positively to internal-positive attributions by family firms (i.e., Hypotheses 3a and 4a). Next, we compare the coefficients of the interaction term involving external-negative attribution and family dummy (Table 4, Model 5). The coefficient is negative and statistically significant (β = −0.09, p < .05). The change in χ2 is also statistically highly significant (p < .001), with the inclusion of external-negative attributions (Model 5). Thus external-negative attributions seem to have a stronger negative impact on stock market response for family firms, providing support for Hypothesis 3b and the entrenchment effect. This thereby implies that we do not find support for Hypothesis 4b.

Robustness Checks

We conduct a number of robustness tests to further validate our findings. With regard to Hypotheses 1 and 2, we examine if family firms make more internal-positive than internal-negative attributions in their total attributions and, similarly, if they make more external-negative than external-positive attributions in their total attributions. We find statistically significant (p < .000) support for the notion that family firms use external-negative attributions to a much greater extent but not for internal-positive attributions (p > .10). This offers further evidence of attribution differences among family and nonfamily firms with respect to external-negative attributions. We also perform a robustness check with the alternate specification of external-negative over all negative attributions and internal-positive over all positive attributions. There are no statistically significant differences for family and nonfamily firms. Combining the results of our initial results and the robustness tests, our findings suggest that it is not that family firms are using external attributions solely for negative performance. However, they do seem to have a tendency to take on a defensive tone, and shield themselves by invoking external causes more often when performance is poor than when it is good.

For Hypotheses 3 and 4, we examine the impact of including the other attributions (i.e., internal-negative and external-positive) as control variables in our regressions. Due to perfect multicollinearity involved when including all four types of attributions, given the common denominator involved in our ratio calculations, only three attributions are included at the same time. Our results hold fully with the addition of the controls.

Overall, we find partial support for the notion that the stock market responds more negatively to attributions that may be potentially self-serving when they are made by family firms, and full support for negative stock market response to potentially self-serving external (i.e., external-negative) attributions by family firms. Thus, when family firms make external-negative attributions, the stock market may be viewing these attributions as a way of “deflecting blame” to external factors for performance and therefore lowering stock prices. Combined, our robustness tests provide support for our main results.

Post Hoc Analyses

The family business literature suggests that there is substantial heterogeneity among family firms (Chua, Chrisman, Steier, & Rau, 2012; Jaskiewicz & Dyer, 2017). Given the nature of our results, we wanted to more deeply examine any potential differences across firms that might constitute potential boundary conditions of our theorizing and results. We do this as the notions of entrenchment and alignment that we build on provide some general guidance as to direct effects, yet do not give detailed insight into the effect of moderators on these direct relationships.

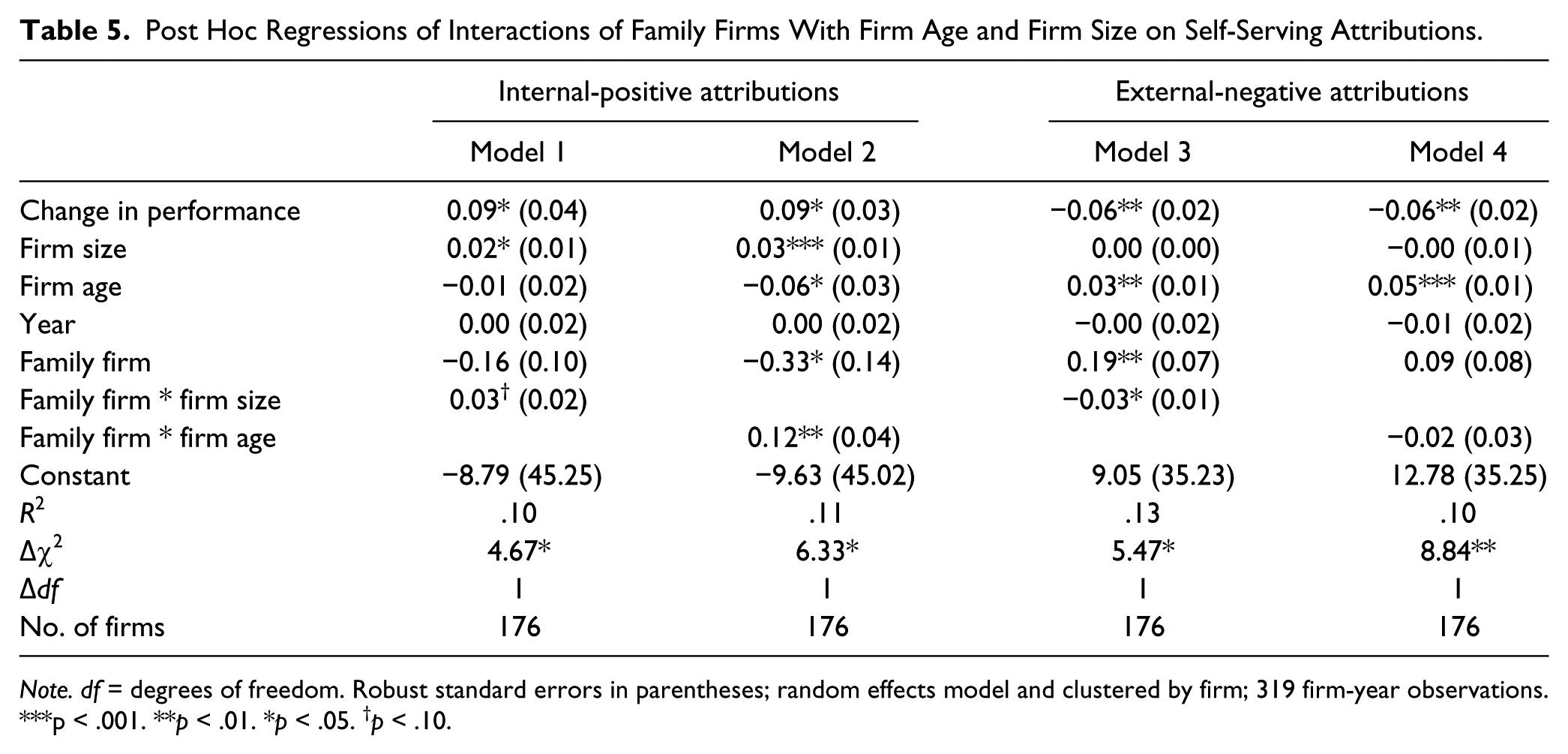

We thus conducted a series of post hoc analyses building on our hypotheses. First, we more fully examine the impact of firm age and firm size as potential moderators in the relationship between family firms and self-serving attributions. Factors such as experience, credibility, reputation, and firm visibility are linked to firm age and size, and can in turn affect the way firms make attributions. We find that firm age positively moderates the relationship between family firms and internal-positive attributions, that is, we find that older family firms (as compared to younger family firms and older nonfamily firms) make more internal-positive attributions. With regard to size, we find that size negatively moderates the relationship between family firms and external-negative attributions (Table 5). Specifically, we find that while larger family firms make fewer external-negative attributions than smaller family firms, large and small nonfamily firms are similar in their use of external-negative attributions. We will return to the implications of these post hoc findings in the discussion.

Post Hoc Regressions of Interactions of Family Firms With Firm Age and Firm Size on Self-Serving Attributions.

Note. df = degrees of freedom. Robust standard errors in parentheses; random effects model and clustered by firm; 319 firm-year observations.

p < .001. **p < .01. *p < .05. †p < .10.

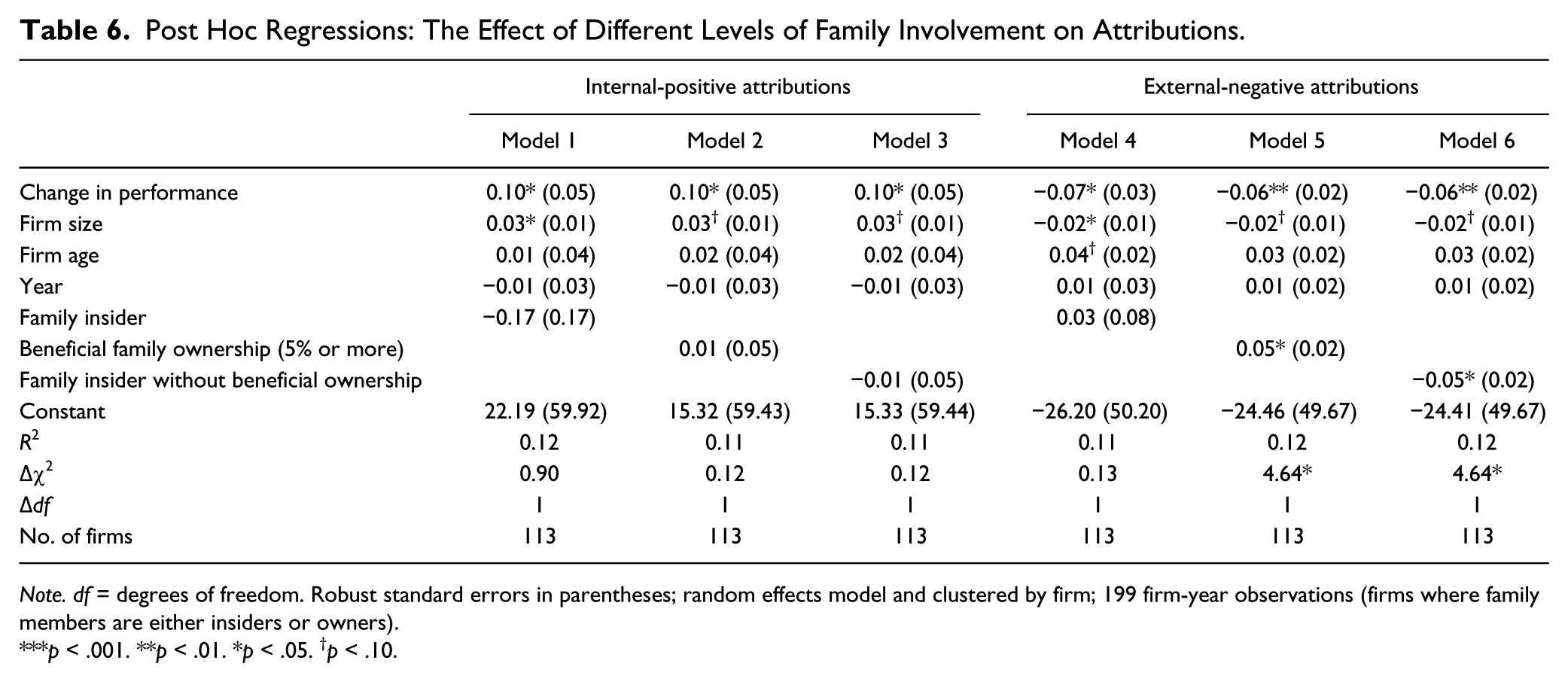

Second, we examine the impact of different types of family involvement in the relationship between family firms and self-serving attributions (Table 6). Specifically, we examine the subset of firms with direct family influence on the firm, such as having a family insider (i.e., a family member in the TMT or board of directors) or as a beneficial family owner (i.e., owning 5% of more of the firm). We also categorize these firms along the lines of (1) whether it has a family member “at the top” (i.e., whether the family member is a CEO or chairperson of the firm) and (2) whether it is a lone-founder firm (i.e., whether the founder and only the founder is present as a beneficial owner or insider or both). To explore this, we run separate regressions to isolate the effect of these differing methods of family influence. We did not find any statistically significant differences in the number of self-serving attributions based on “insider” presence alone. In contrast, we find that having family owners significantly increases external-negative attributions. Additionally, we look at the effect of having insiders who are not owners. We find that family presence without family ownership in fact reduces external-negative attributions (even when we include nonfamily firms). Thus, our findings suggest that it is family ownership, rather than family management presence, that drives self-serving attributions. These findings are presented in Table 6. We then delve further into the family leadership role, such as having a family member as CEO or Chair of the board. 2 We find partial support (p < .10) for the presence of family member at the top (as either CEO/chair) leading to greater numbers of self-serving attributions. Specifically, we find that having a family member at the top leads to greater use of external-negative attributions relative to external-positive attributions. Overall, these post hoc findings suggest that self-serving attribution is in line with entrenchment incentives only when family insiders are “at the top” or when possessing ownership greater than 5%. Viewed in other terms, the entrenchment effect seems to be in place when the family bears the risks associated with ownership or final management authority, rather than simply being present within the firm.

Post Hoc Regressions: The Effect of Different Levels of Family Involvement on Attributions.

Note. df = degrees of freedom. Robust standard errors in parentheses; random effects model and clustered by firm; 199 firm-year observations (firms where family members are either insiders or owners).

p < .001. **p < .01. *p < .05. †p < .10.

We now turn our attention to how being a lone-founder firm (founder and no other family member is present as owner or as a TMT/board member) rather than having another family member present as owner or as a TMT/board member affects self-serving attribution 1 . We find that lone-founder firms use fewer external-negative attributions relative to external-positive attributions. Thus lone-founder presence seems to reduce self-serving attributions.

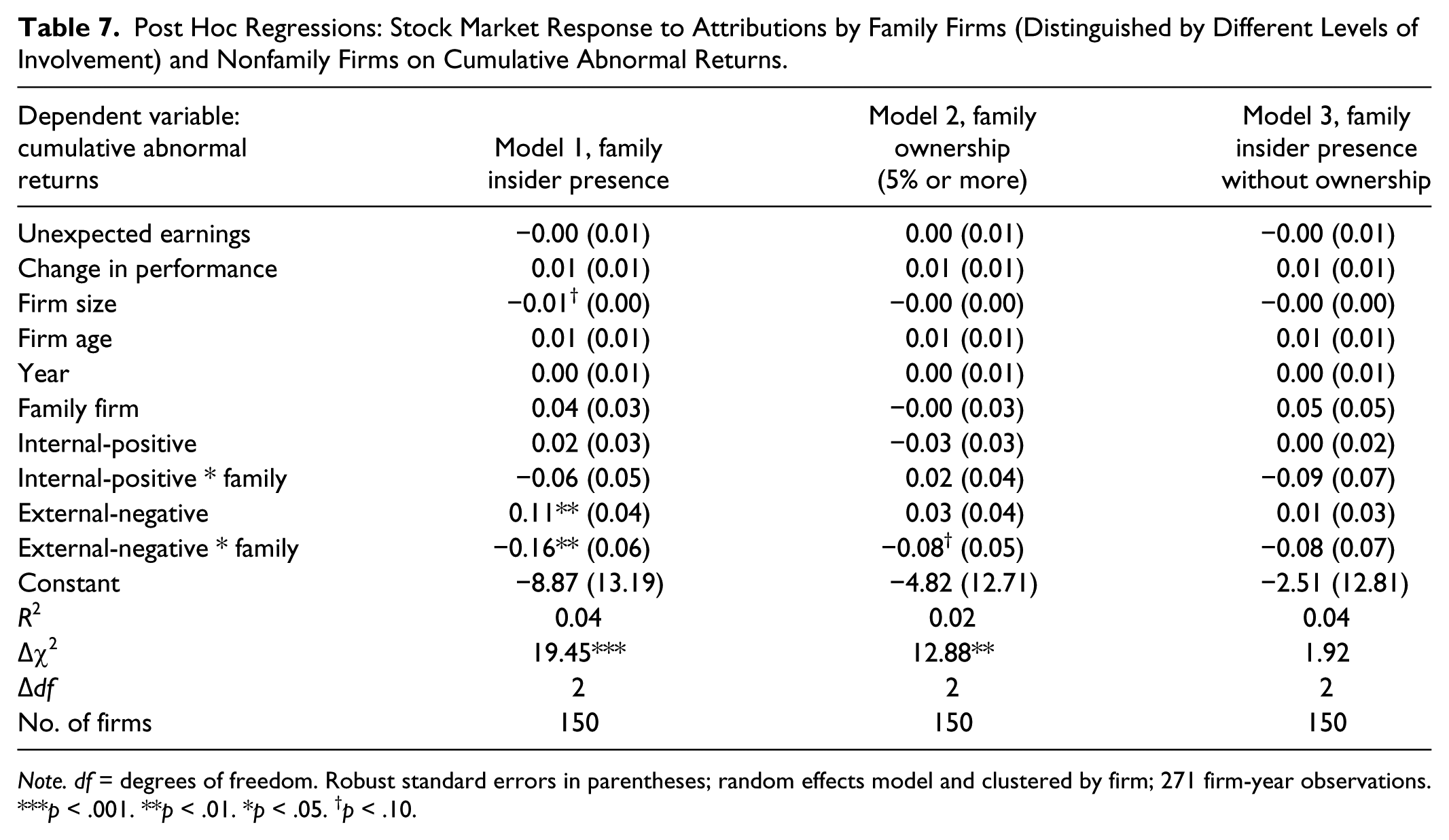

We also conducted a post hoc test examining the stock market impact on self-serving attributions (Table 7). We start with examining the effects of family ownership and family insider presence as potential moderators in the relationship between attributions and stock market response. We find that a family insider presence combined with beneficial ownership leads to a more negative stock market reaction (p < .01) when there are external-negative attributions. This may be interpreted as the stock market perceiving an entrenchment effect. These findings are substantially weaker for beneficial family ownership alone (p < .10) and for the possession of insiders without ownership (n.s.). We find a similar pattern when examining the presence of a family member at the top (i.e., as CEO or chair; p < .001) and for the lone founder (p < .001) for the effects of the usage of external-negative attributions on stock market price. 3 In other words, there appears to be a stronger perceived entrenchment effect for self-serving attributions when there is a family member in a top leadership position. We provide the post hoc table related to family ownership and family insider presence. We discuss the implications of these post hoc findings in the section that follows.

Post Hoc Regressions: Stock Market Response to Attributions by Family Firms (Distinguished by Different Levels of Involvement) and Nonfamily Firms on Cumulative Abnormal Returns.

Note. df = degrees of freedom. Robust standard errors in parentheses; random effects model and clustered by firm; 271 firm-year observations.

p < .001. **p < .01. *p < .05. †p < .10.

Discussion

Our results make several contributions and have implications for future research in family business. First, we find that family and nonfamily firms differ in the way they attribute performance. We find that family firms have higher self-serving attribution with respect to the extent to which they place “blame” on external factors for performance. This seems to fall in line with the predictions from the entrenchment line of reasoning, rather than the alignment view. Although there are many potential reasons that could lead to an entrenchment effect, it appears as though family firms are more interested in impression management through their use of external-negative attributions. While impression management might conceivably lead to higher focus on internal-positive attributions of firm performance, we find that only one part of self-serving attributions seems to hold—that of external-negative attributions. This does not necessarily mean that family firms avoid using internal-positive attributions for impression management. Rather, it shows they do not use it in a significantly different way compared to nonfamily firms.

As such, it seems that there is a more tempered approach to entrenchment, whereby family firms engage in additional self-serving attribution that is less obvious than attributing performance only to internal factors. With this moderate self-serving behavior, family firms likely seek to maintain their long-term reputation, protect the management team, and appear less involved in impression management (Zellweger et al., 2010). As a consequence, the greater focus on external factors would likely lead to greater cohesion between family members and the reciprocal and stable relationships that family firms have with stakeholders. This reduces self-threat and the need for subsequent self-enhancement.

Relatedly, the findings also extend our understanding of multidimensional manifestations of entrenchment effects in language made available for public use or dissemination. Previous work stresses an internal view of entrenchment, whereby family members’ economic wealth and SEW are promoted through withholding information, family member interdependence and collusion, and the assertion of greater control over firm activities (e.g., File & Prince, 1996; Poza et al., 1997; Zellweger, 2007), which would logically be manifest as internal-positive attributions. Yet our finding that family firms have higher external-negative attributions provides evidence that external-facing views are also germane to entrenchment explanations for self-serving attributions in family firms. Our findings thus serve as a starting point for further entrenchment studies exploring just why family firms, more than nonfamily firms, feel the need to stress outside influences as attributions of poor performance.

Our post hoc findings have a number of implications for theory building in attributions, and the nature of family firm heterogeneity (Chua et al., 2012; Jaskiewicz & Dyer, 2017). We found that firm age and firm size have varying effects on the type of attributions manifest in annual reports for family and nonfamily businesses (Table 5). This suggests that present perceptions of entrenchment versus alignment effects are complex, and it reveals insights into the boundary conditions of attribution theory. This is perhaps most notable given our relatively narrow focus on publicly traded firms in the U.S. pharmaceutical industry. Firm age has a stronger positive effect on internal-positive attributions by family firms than by nonfamily firms, refining theoretical boundaries regarding entrenchment. Entrenchment is strengthened as family firms are older: They have a more flattering self-view and seek to preserve harmonious family relationships, resulting in increasing internal-positive attributions. Additionally, firm size has a stronger negative effect on external-negative attributions by family firms than by nonfamily firms, showing how our knowledge of theoretical boundaries regarding alignment effects are improved when we account for firm size: alignment is improved as family firms become larger, resulting in decreasing external-negative attributions. Larger firms are likely also more well-known than smaller firms, and thus larger family firms would have increased reputational pressure to be less self-serving through higher quality reporting. And while there was a moderate correlation between size and age in our sample (r = .44, p < .001), there is enough difference to suggest that there is value in examining these factors separately—as the post hoc results in Table 5 suggest.

Our post hoc results with respect to the different aspects of family presence in family firms suggest a number of discrepancies based on the level of family involvement in the family firm. First, we find that there are stronger ownership—rather than management—effects for the engagement in impression management. In fact, our findings show that family involvement via leadership (but without beneficial ownership) engages in less impression management. Thus, any potential alignment benefits of being a family firm only seem to appear without the presence of beneficial ownership. Second, there is some evidence to suggest that having a family member at the top (as either CEO/chair) leads to greater impression management. This could be because a family member who is at the helm of the firm feels far more pressure to put up a front of efficacy and retain control of the firm. However, for lone-founder firms, impression management is actually lower. This could be due to the founder treating the firm as his or her “own” creation and therefore putting more stress on the long-term reputation of the firm than managing stakeholder expectations. It could also be because founder motivations are uncorrupted by the presence of other family members.

Our results show that the stock market more heavily “punishes” family firms for their self-serving attributions, which we view as being based on perceived entrenchment effects. This would suggest that the stock market does not view self-serving attributions as plausible and would be wary of family firms’ perceived attempts to deflect blame by attributing performance to external factors. Indeed, prior studies point to the stronger influence of external attributions on market expectations (Baginski et al., 2004; Baginski et al., 2011; Barton & Mercer, 2005). Our post hoc results strengthen those findings by highlighting that the “punishing” effects come primarily when there is a family member acting as an “insider” or “at the top,” rather than family ownership or insider status without beneficial ownership alone. Family firms should be aware that external perceptions of (rather than purposeful action on the part of the firm) preserving the firm’s SEW have strong market response implications. In the case of our sample, the market was notably punitive in the short term.

Our finding is relatively surprising given that previous work in related areas has often suggested that family firms perform better in the long run (Miller & Le Breton-Miller, 2005) and have more favorable impressions by outsiders (Martin et al., 2016; Zellweger et al., 2013). Therefore, the punishment that family firms face due to external-negative attributions may simply be a reaction to the way that family firms explain bad news in the short term. If the market is expecting higher performance from family firms, then external attributions for poor performance may be more harshly penalized than if the attributions occurred in nonfamily firms where the performance is expected to be lower. Our results also point to another potential explanation—that the market may be skeptical of information relayed from managers in family firms. This may be due to a general market perception of entrenchment motives in family firms or to the stock market’s awareness of the tendency of family firms to have more external-negative attributions. In either case, our findings are in line with an entrenchment effect and are worthy of future investigation.

Our findings contribute to the agency debate on whether family involvement is an effective substitute for external monitoring and enforcement. For instance, Ali, Chen, and Radhakrishnan (2007) find that family firms have better quality earnings reports and suggest that this is because family firms face less severe hidden-action and hidden-information agency problems. Similarly, Jiraporn and DaDalt (2009) suggest that family ownership reduces managerial myopia and the threat that managers face from the stock market for corporate control. Consequently, they argue managers in family firms are less inclined to manipulate earnings for the sake of pleasing the stock market. They support this with their finding of lower earnings management in family firms. However, a second camp of researchers argues that family firms have lower earnings quality. Jaggi, Leung, and Gul (2009) find that family control compromises board independence leading to greater earnings management in family firms. Yang (2010) suggests that insider ownership in family firms leads to greater entrenchment and, therefore, greater earnings management. Our finding regarding the presence of self-serving external-negative attributions in the MD&As of family firms are consistent with these latter findings of greater managerial manipulation of information related to firm performance. While the publicly traded family firms in our sample were not overly positive about their own business activities, as would be expected in impression management, they were generally negative about the business environment in which they operated. One possibility is that family firms are more comfortable engaging in cosmetic manipulations (Gomez-Mejía et al., 2014), such as the manipulation of language in their annual reports, but only to the extent that it does not unreasonably raise stakeholder expectations. This would explain why family firms overemphasize external factors for poor performance without a parallel emphasis on internal factors for good performance. However, the negative stock market response to family firms’ external-negative attributions in Hypothesis 3 suggests the market does not buy into the attribution to external causes for poor performance, and treats family firms as having less than plausible attributions.

Furthermore, our study contributes to attribution theory (Harvey et al., 2014) as it identifies a previously unexamined organization-level characteristic as an explanatory factor for attribution differences in firms. As such, it extends attribution research into the domain of family business. Our findings support the notion of transgenerational control and concern for corporate reputation increases impression management through self-serving attributions (Zellweger et al., 2013). While we are not able to identify which specific mechanisms lead to the attribution differences, our preliminary results suggest that there are some inherent factors germane to family firms that may affect attribution.

Overall, our study offers a novel approach at the intersection of attribution and family firms, and where there is potential for further theoretical pollination. To our knowledge, we are the first to empirically examine the notion of attribution in family firms and specifically examine differences compared to nonfamily firms as well as the potential impact of these differences on stock market valuation. In doing so, we begin to raise ideas of how attribution may be linked to issues such as succession, governance and maintenance of managerial and familial relationships within the family firm. This is admittedly a first step in a potentially long journey to truly understanding attribution in family firms. There are a number of unanswered questions related to attribution that can be related to important family firm topics. For instance, how does attribution relate to issues of succession? Are there likely to be more internal attributions irrespective of the outcome so that the family firm can convey a willingness to take on personal responsibility? Or does a need to defend their worth lead to bias? Is the type of attribution affected by having multiple successors in the running? Is it affected by the quality of relationship between the successor and the predecessor? Do the training and tenure in the business affect the attributions of the successor?

Furthermore, issues related to governance and attribution remain unexamined. How is self-serving attribution in family firms affected by higher concentrations of family ownership or the presence of multiple family members in governance? For instance, does the existence of multiple family members in the TMT lead to greater planned and impression management? Or are family firms even cognizant of their own attributions? Do CEOs and other leaders use the MD&As to deliberately defend themselves or are there pressures from others in ownership to provide those defenses? Finally, unlike in nonfamily firms, attributions in family firms have the potential to affect both professional and familial relationships. For that very reason, attributions are also likely to be influenced by the nature of the family relationship outside the firm. If family relationships are already strained, then additional negative attributions for firm performance directed at, say, a son or a wife could be taken as a personal attack. These very negative attributions could be viewed as fair and appropriate if the family relationships are healthy.

Additionally, scholars could conduct research to better explain the antecedents of the attributions made by family and nonfamily businesses. What is the causal mechanism between altruism and attributions? Or family closeness/group cohesiveness and attributions? And what causes these to differ between family and nonfamily firms? For example, it is well-known that firms use corporate philanthropy as a form of risk management against negative performance (Godfrey, 2005). How does this type of altruism affect the types of attributions made by firms, and are there differences between family and nonfamily firms in this regard? It stands to reason that family businesses could be more altruistic toward causes that are near and dear to the family, while nonfamily firms may support altruism that has a more direct connection to the operation of the business, as a form of strategic advantage (Porter & Kramer, 2006).

Finally, attribution could also be examined in light of other types of performance measures. While our study focused on CAR as a measure of performance, other measures can gauge the impact over longer periods, such as quarterly or annually. Our focus in this study was on the annual reports, where many of the earlier performance may already have been known to shareholders via quarterly reports. CAR is a useful measure of short-term performance, as the MD&A section could be in the forefront of investor consciousness shortly after it is issued. On the other hand, MD&A sections also lay out management’s strategic direction over the coming year, and investors expect positive performance in one year to hopefully continue in the following year. Future studies that examine performance over multiple time horizons for a more holistic measure would we a welcome addition to our study.

Managers may want to consider the fact that while self-serving attributions may be relatively commonplace for corporations, the stock market is aware of incentives within a firm that can accentuate such self-serving tendencies. As such, whether deliberate or incidental, the choice of attributions has an impact whereby the market feels that its impressions are being deliberately managed. Family firm leaders may want to therefore continue to act in the spirit of transparency and plausibility and seek to provide a balanced set of attributions by more readily acknowledging both the positive effects of external factors and negative effects of internal factors on firm performance. This would be especially true when there is a family member in a leadership position who may be viewed as “needing defense.” Regardless of intent, family firms may benefit from being cognizant of their self-serving tendencies, particularly when it comes to making negative rather than positive performance attributions to external factors.

Limitations