Abstract

From a mixed gamble perspective, we contend that family firms (FFs) with different family shareholder structures are confronted with different trade-offs among current and prospective financial and socioemotional wealth (SEW), leading to differences in their international acquisition choices. We also explore the moderating role of family leadership and performance aspirations. Our findings show that FFs with a dominant family owner are more likely to pursue international acquisitions, especially when FFs are led by a family CEO or when they experience below-target performance, as in such cases, they prioritize prospective financial and SEW gains, thereby sacrificing current SEW and financial wealth.

Introduction

Acquisitions represent a unique form of strategic venture through which one firm acquires another firm (target firm) with the aim of enhancing its long-term value (e.g., Capron, 1999; Haleblian et al., 2009; McNamara et al., 2008; Miozzo et al., 2016), mitigating risks through diversification (Hitt et al., 2006), or fostering external growth (Achtenhagen et al., 2017; Lockett et al., 2011; McNamara et al., 2008; K. E. Meyer & Tran, 2006). However, acquisitions can also threaten acquirers’ wealth due to their high risk of failure (Bauer & Matzler, 2014). Such a threat is even stronger in the case of international acquisitions due to cultural and other institutional differences between countries (Seth et al., 2002).

Given the effectiveness of acquisitions in generating rapid growth, scholars have dedicated increasing attention to investigating how they unfold in different types of contexts, such as family firms (FFs; e.g., Defrancq et al., 2016; Gómez-Mejía et al., 2018; Miller et al., 2010). In fact, in times of ever-increasing globalization and a persistently growing number of cross-border acquisition targets (Lewis & McKone, 2016), FFs must often take certain risks to avoid falling behind in their markets (Geppert et al., 2013). For these firms, international acquisition decisions are based on both economic and non-economic factors. Non-economic factors are related to the preservation of socioemotional wealth (SEW)—that is, the stock of affect-related value that the family derives from its controlling position (Gómez-Mejía et al., 2007, 2011). The literature examining acquisitions through the lens of SEW has produced contrasting findings. The majority of these works suggest that FFs are reluctant to undertake international acquisitions to preserve their SEW (e.g., Caprio et al., 2011; Miller et al., 2010). However, according to some studies, international experience and slack resources, as well as the intention to transfer the firm to the next generation (Strike et al., 2015) or performance below aspirations (Gómez-Mejía et al., 2018), may have a positive influence on international mergers and acquisitions (M&As). This influence can potentially mitigate acquisition consequences (Iyer & Miller, 2008) and assist FFs in increasing their SEW stock (Boellis et al., 2016; Debellis et al., 2021; Hussinger & Issah, 2019).

We argue that these conflicting findings can be attributed to previous applications of SEW in studying FFs’ acquisitions, which overlook the unequal distribution of SEW among family members (Miller & Le Breton-Miller, 2014; Souder et al., 2017). It is crucial to differentiate SEW among family principals to capture the inherent heterogeneity that characterizes the realm of FFs (Chua et al., 2012; Marques et al., 2014; Nordqvist et al., 2014). To address this gap, and in line with previous studies (Miller & Le Breton-Miller, 2014) that differentiated, for example, between restricted SEW (narrow and short-term benefits to the family) and extended SEW (more enduring benefits to a broader range of stakeholders), we consider FFs’ international acquisitions as mixed gambles. In many cases, family owners are confronted with trade-offs between financial and SEW gains and losses, leading to differences in their choices. Moreover, within a group of family owners, there might be different needs for SEW preservation (Souder et al., 2017). Accordingly, we distinguish between current and prospective SEW and argue that different types of family owners—dominant versus (vs.) minority (Li et al., 2017; Purkayastha et al., 2019; Sutton et al., 2018; Young et al., 2008)—might prioritize these forms of SEW in different ways and thus reach different international acquisition decisions.

By integrating arguments from both the SEW perspective and the principal–principal (PP) conflict literature (Young et al., 2008), the aim of this study was to investigate FFs’ international acquisition choices as mixed gambles (Kotlar et al., 2018) between contrasting SEW preservation tendencies (i.e., current vs. prospective SEW) derived from differences in the family shareholder structure (i.e., dominant family owner vs. minority family ownership). Furthermore, to provide a more granular picture of FFs’ international acquisition choices, we define the boundary conditions of SEW (Souder et al., 2017) by considering what happens when FFs are led by a family CEO (Strike et al., 2015) or experience performance below aspiration levels (Calabrò et al., 2018). We test our main predictions on a database consisting of the entire population of Italian FFs with revenues higher than 50 million euros, covering the years 2000–2014, with 137 international acquisitions. Our main findings show that FFs with dominant family owners are more likely to engage in international acquisitions, as they tend to prioritize prospective SEW and financial gains by sacrificing current SEW and financial wealth. Moreover, the propensity to acquire international targets for FFs with dominant family owners is enhanced when there is a family CEO or when the firm is experiencing below-target performance. This study makes several contributions. First, by theorizing the differentiation of SEW (current and prospective) in the context of FFs’ international acquisitions, we contribute to the debate on FF heterogeneity by showing the importance of distinguishing SEW among family owners and argue that it is unlikely for SEW to be equally vested in all family members and that it may vary based on different circumstances (Miller & Le Breton-Miller, 2014; Strike et al., 2015; Vandekerkhof et al., 2018). There is, in fact, a different trade-off between the financial and SEW motives (Chrisman & Patel, 2012; Gómez-Mejía et al., 2018) of minority versus majority family owners that leads to nuances in SEW theorization and, consequently, different preferences in terms of international acquisition choices. Moreover, our findings advance the debate on the importance of identifying boundary conditions to highlight the impact of financial and SEW priorities on FFs’ strategic choices (Souder et al., 2017). Specifically, this is achieved by adding evidence of the contingency-dependent nature of SEW (Schulze & Kellermanns, 2015). In addition, we add to the debate on family PP conflicts regarding the difference between dominant and minority family owners in predicting strategic choices and outcomes (Connelly et al., 2010; Li et al., 2017; Purkayastha et al., 2019; Thomsen & Pedersen, 2000). Finally, our findings add evidence to studies on FFs’ internationalization (Pukall & Calabrò, 2014) and growth. Specifically, we offer evidence that under specific ownership, leadership, or firm conditions, some FFs might be more willing than others to implement the riskiest strategic choices and thus make an international acquisition.

Theoretical Framework and Hypotheses Development

Socioemotional Wealth in the Context of International Acquisitions

International acquisitions represent a specific type of venture because the acquirer has to place large initial investments abroad and is therefore exposed to risk and other uncertainties (Seth et al., 2002). These acquisitions expose firms to additional risk given their internationalization (Lu & Beamish, 2004; Matta & Beamish, 2008; C. B. Meyer, 2008), higher market uncertainty, and the more substantial information asymmetry between the acquiring firm and the foreign target (Woodcock et al., 1994). It is commonly accepted in the literature that while shareholders have interests across different businesses and are thus almost exclusively concerned with returns on their investments, family owners are mainly tied to their firm (Minichilli et al., 2016) and would prefer not to put their investment at risk, as their private and emotional wealth is also often invested in that firm. Applying predications based on the behavioral agency model (BAM; Lim et al., 2010; Wiseman & Gómez-Mejía, 1998) to SEW, the dominant view suggests that FFs are willing to sacrifice economic gains to minimize threats or losses to SEW (Leitterstorf & Rau, 2014). Thus, when deciding upon international acquisitions, FFs will also consider the consequences that a particular choice has on their desire to preserve the accumulated SEW endowment (Berrone et al., 2012), thus dividing outcomes into potential gains and losses to their SEW (Gómez-Mejía et al., 2007; Wiseman & Gómez-Mejía, 1998). FFs would thus avoid international acquisitions that could threaten their SEW, even if that meant sustaining some costs. To put it differently, family decision makers would likely accept a higher performance hazard risk due to their ultimate goal of protecting their accumulated SEW (Cennamo et al., 2012). Following this logic, FFs generally avoid acquisitions or favor national ones (Gómez-Mejía et al., 2010) with lower volume and value (Miller et al., 2010), as international acquisitions are more complex in terms of cultural and institutional differences and pose major threats to their SEW. Only a few studies have focused on FFs’ international acquisitions, with diverging findings. Some studies show that FFs prefer national targets due to their risk aversion (Gómez-Mejía et al., 2010) or related interests in diversification (Miller et al., 2010). Others highlight a higher propensity for international acquisitions when the family CEO intends to transfer the firm to the next generation (Strike et al., 2015), when performance is below aspirations (Gómez-Mejía et al., 2018), or in the case of a more protective and shareholder-oriented legal system (Menendez-Requejo et al., 2018). In the same vein, Gómez-Mejía et al. (2018) theorized that FFs are more likely to engage in international acquisitions if they have abundant slack resources that can mitigate potential SEW losses.

While the underlying assumption behind the evidence produced so far is that family principals address SEW in a homogeneous way, on the contrary, we contend that SEW might not be equally vested in all family owners. Indeed, they might have different SEW preservation needs (Souder et al., 2017) and consequently might be willing to implement different strategic choices (Strike et al., 2015). There have been few attempts to differentiate SEW, with earlier categorizations being made in terms of short-term versus long-term SEW (Leitterstorf & Rau, 2014), focused versus broad SEW (Gu et al., 2019), external versus internal SEW (Vardaman & Gondo, 2014), restricted versus extended SEW (Miller & Le Breton-Miller, 2014), and wise versus blind SEW (Calabrò et al., 2018). Directly or indirectly, these distinctions are based on the concept of a mixed gamble (Kotlar et al., 2018), which is derived from prospect theory (an important theoretical root of the SEW paradigm). We broaden this perspective by incorporating recent advancements in prospect theory (Kahneman & Tversky, 1979) and propose the existence of mixed gambles, wherein decision makers can consider their current and prospective wealth as alternative reference points (Bromiley, 2010). These advancements are based on the premise that the reference point is not solely linked to immediate outcomes but can also encompass future scenarios (Levy, 1992). This notion finds support in studies on executive stock options, where a focus on future wealth orientation leads to greater risk taking in the present (Martin et al., 2013). More specifically, within FFs that are mostly fully family-owned and with a majority family owner and minority family owners, we distinguish between current versus prospective financial wealth and current versus prospective SEW, which may differently influence FFs’ international acquisition propensities. Indeed, by prioritizing current SEW, family control and influence take precedence, and consequently, the future financial and SEW gains deriving from an international acquisition take the back seat. On the contrary, striving for prospective SEW means focusing on preserving and expanding the family’s dynasty and creating opportunities for future generations through the prospective financial gains derived from international acquisition (Martin & Gómez-Mejía, 2016).

Family Principal–Principal Conflicts and International Acquisition Propensity

Differences in family ownership determine different risk-taking behaviors (Villalonga & Amit, 2006), which have various effects on FFs’ international acquisition propensities. Here, we focus on one characteristic of the firm ownership structure: the presence of a dominant family owner with the concentration of shares (and thus decision-making power) in his or her hands, and few or several minority family members on the other side. This type of ownership structure brings forth family PP conflicts, which consist of goal incongruences and alternative reference points between controlling and minority family shareholders (Li et al., 2017). Due to familiar relations, conflicts escalate easily and can quickly reach a personal level (Frank et al., 2011; Kidwell et al., 2012). Conflicts normally occur when decisions, especially riskier ones, need to be made. Because of its position, a dominant family owner often decides autonomously to exploit minority family members (Purkayastha et al., 2019) and thus benefits the most from the financial success of the firm. This fosters riskier behavior and more financially oriented strategies, which preserve competitiveness and family control alike (Miller et al., 2010; Zellweger & Astrachan, 2008), even if this means that value must be appropriated from minority family members. In fact, dominant family owners have a strong interest in safeguarding the long-term economic success and competitiveness of the firm as well as their dominant position within it. International acquisitions would indeed provide long-term value, as they reduce volatility in earnings, give access to qualified staff and a wider customer base, and, in general, increase a firm’s financial security (Haleblian et al., 2009). Hence, the financial benefits that might derive from international acquisitions are important in ensuring the preservation of the dominant position and the continuance of the family dynasty (which are surely ways to ensure the preservation of SEW in the future; Souder et al., 2017). More specifically, international acquisitions provide an opportunity to fulfill certain family obligations, such as the preservation and expansion of the family’s dynasty, which secures the business for future generations and provides them with increased opportunities (Fernández & Nieto, 2005).

On the contrary, for minority family members, the financial rewards linked to their ownership position are low, and the pressure for financial success and ultimate control is limited and, even if present, difficult to enforce. This fosters their risk-averse behavior in making strategic decisions, with a stronger focus on preserving their current control and the related short-term financial utilities (e.g., dividends) deriving from it. Therefore, the current SEW has become more important for minority family members. Accordingly, when faced with the prospect of an international acquisition, family decision makers are confronted with the fact that financial outcomes may generate trade-offs (mixed gambles) between preserving current SEW or aiming for prospective SEW gains. When these positions of power are linked to the preservation of a family’s personal control, internal conflicts between the two different categories of principals (i.e., dominant family owners and minority family owners) prevail. In these situations, dominant family owners may advance their own personal interests without regard to minority owners (Cheung et al., 2015; Li et al., 2017; Young et al., 2008; Zardkoohi et al., 2017), thereby making decisions that can lead to the misappropriation of minority owners’ SEW. Dominant owners have an idiosyncratic long-term reference point that clashes with the short- to medium-term focus of minority members. Hence, if the choice involves a riskier strategy, such as acquiring a firm from a foreign market (Lu & Beamish, 2004; Matta & Beamish, 2008), the dominant family owner will be more willing to sacrifice current SEW and focus instead on financial benefits and prospective SEW gains.

Therefore, in FFs characterized by concentrated ownership, the likelihood of encountering conflicts among family PPs may be more pronounced than in FFs with dispersed ownership structures. In FFs with lower family ownership concentrations, with family owners each controlling a small percentage of the firm, family PP conflicts are less frequent, as “one principal cannot unilaterally force its particularistic agenda on the rest” (Gómez-Mejía et al., 2011, p. 688). This might lead to inertia in making strategic decisions, as each individual family owner has the same reference point and self-interest. These family owners might indeed prefer to maximize the financial gains (dividends) deriving from their family owner status instead of pursuing an international acquisition, which might jeopardize the future economic returns of the FF (Gómez-Mejía et al., 2010; Miller et al., 2010). Thus, they may feel that this strategic choice is a real threat to their current SEW. In addition, no one member has enough decision power to expropriate others. Hence, this inclines family owners to be more oriented toward preserving their current SEW (Souder et al., 2017).

In sum, while FFs with dominant family owners (i.e., a high family ownership concentration) value the financial benefits and prospective SEW gains associated with international acquisitions more, FFs with dispersed family owners (i.e., a low family ownership concentration) are less prone to embrace the risks associated with international acquisitions, as they prefer to maintain their current SEW and the financial benefits (dividends) linked to their owner status. Thus, we formulated the following hypothesis:

The Moderating Role of Family Leadership

As differences in leadership determine different risk-taking behaviors (Villalonga & Amit, 2006), and CEOs’ preferences are drivers for investments in foreign markets (Lin, 2014), to understand FFs’ international acquisitions, we must account for what happens when the CEO is a family member. In this case, we focus on family leadership as an additional contextual aspect given that international acquisitions are risky strategic investments (Matta & Beamish, 2008), high cost, provide more uncertainty on the short-term return, and, if unsuccessful, negatively impact the assessment of the CEO’s performance (Matta & Beamish, 2008). Furthermore, shareholders’ wealth destruction, especially in international acquisitions, is often linked to the opportunistic motives of CEOs in acquiring firms (Seth et al., 2002). Finally, the role of the CEO is widely recognized as a crucial avenue for gaining deeper insights into acquisitions (Hoskisson et al., 2017; Iyer & Miller, 2008), and further exploration is warranted to understand the unique behavior exhibited by family CEOs (Miller et al., 2014). With only a few exceptions (Chen, 2008; Martin et al., 2013), CEOs have been described as solely applying their own compensation as a reference point (Wiseman & Gómez-Mejía, 1998). While this holds true for most non-family CEOs, family CEOs possess an additional emotional attachment to the firm, which introduces an extra reference point. Consequently, when family CEOs are faced with decisions regarding international acquisitions, they employ a distinct logic and may frame their strategic choices differently.

In fact, the leadership of a family CEO (Cannella et al., 2015; Van Doorn et al., 2020) can have a divergent impact on a family firm characterized by concentrated family ownership. Specifically, in FFs with a dominant family owner, the presence of a family CEO would make the focus on prospective SEW even stronger, as in this type of situation, firm ownership and management preferences are more aligned. Indeed, in such cases, there is an alignment of interests and less asymmetric information between dominant family owners and family CEOs that can make international acquisition deals much more efficient and effective. This lies in the fact that strategic decisions and the execution of the acquisition strategy can be faster and more synchronized given that FFs have more breath in the competitive market. If a family is more involved in the firm’s operations through the presence of a family CEO (dual family involvement), this gives rise to a flow of information on the acquisition deal that will likely mitigate the overall risk perception associated with this strategic choice. Moreover, the family CEO may validate the correctness of focusing on future prospects (e.g., financial gains) derived from the acquisition and prospective SEW gains by sacrificing current ones (e.g., current SEW). This is also in line with recent studies showing that family CEOs make more international acquisitions when prospective SEW considerations, such as transgenerational preservation, are in focus (Strike et al., 2015). Based on the above arguments, we formulated the following:

The Moderating Role of Below-Target Performance

To fully apply the SEW approach, define its boundary conditions (Calabrò et al., 2018; Souder et al., 2017), and provide a more granular picture of FFs’ international acquisition choices, we also consider what happens to the relationship between family ownership concentration and international acquisition propensity when an FF’s performance is below aspiration levels (Gómez-Mejía et al., 2018).

Based on the behavioral theory of the firm (Cyert & March, 1963), when family decision makers experience performance below aspiration levels, they may initiate a problemist search, and an organizational change may be developed to restore satisfactory performance (Greve, 1998; Iyer & Miller, 2008). Such a situation indicates that the current strategy is not in line with the demands of the market due to a multiplicity of reasons (i.e., difficulty in gaining access to skills or local stakeholders, customer-related issues, or insufficient planning or lack of knowledge). Performance shortfalls drive exploration and make risk-seeking strategies more likely to be accepted (Rajagopalan & Spreitzer, 1997), such as making an acquisition in a foreign country (Geppert et al., 2013; Kim et al., 2015).

As “success narrows down search to the neighborhood of the status quo, whereas failure promotes gradually more exploratory search” (Billinger et al., 2014, p. 93), we argue that when performance does not reach aspirational levels, the dominant family owner in an FF with concentrated ownership might perceive this situation as a failure and see his or her SEW (both current and prospective) at stake and being more prone to international acquisitions. Following this logic, experiencing performance below aspirations may push the dominant family owner to search for a riskier solution to preserve the FF’s continuity and legacy (Calabrò et al., 2018; Gómez-Mejía et al., 2018). Moreover, being the dominant family owner allows for undisputed decision-making power to make an international acquisition, which may have significant consequences for the firm and the family.

In contrast, in FFs with a low family ownership concentration, when performance does not reach the desired levels, family owners are likely to struggle with the decision to make international acquisitions, as they might have different opinions on the right way to address the negative performance feedback that has increased internal family PP conflicts. Furthermore, they could be overruled by conflicting SEW concerns (Berrone et al., 2012), as some family owners might prefer to preserve their current SEW, while others might opt in favor of prospective SEW. This SEW conflict (Vardaman & Gondo, 2014) among equally influential principals in cases of dispersed and below-target performance FFs hinders decision-making. Consequently, such FFs may be stuck in the middle, as no dominant family coalition has the say, and international acquisition will be avoided.

In sum, in FFs with a high family ownership concentration, the dominant family owner is in a different framework than that in a dispersed family ownership setting. Below-target performance, as a hazard for financial performance and a source of potential SEW losses (including prospective SEW), immediately jeopardizes specific SEW dimensions, such as the need to preserve transgenerational control (Zellweger et al., 2012). Consequently, such a situation may push the dominant owner to take on more risk-seeking behaviors in terms of acquisitions. Thus, we formulated the following hypothesis:

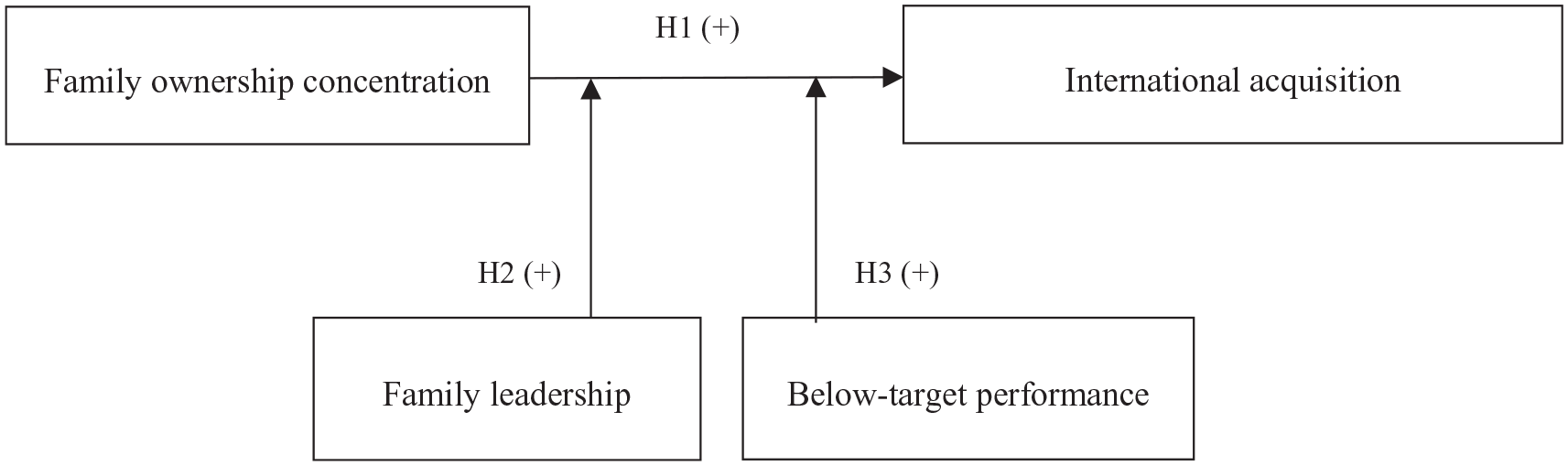

The research model and the main hypotheses are shown in Figure 1.

Research Model.

Method

Sample and Data Collection

In this study, we analyzed a sample of Italian FFs. The Italian setting was perfectly suitable for our study, as FFs represent the strongest component of the Italian economy. Among these FFs, we selected firms whose annual sales exceeded the threshold of 50 million euros in fiscal year 2013 as the initial criterion. This number is typical for medium- and large-sized firms in the Italian context and is considered an appropriate setting in which to investigate external growth choices, whereas smaller firms are often characterized by their focus on internal growth (Naldi & Davidsson, 2014). We had to exclude FFs operating in the financial services industry due to legal regulations in this business domain, which also affect potential firm M&As. We also eliminated firms with missing data on key control variables and predictors. We defined “FF” as a family firm in which at least two members with the same surname owned at least 50% of equity shares. In addition, we verified whether at least two members of the same controlling family had a position on the board of directors (De Massis et al., 2014; Miller et al., 2007). The reason for selecting this threshold was because privately held firms in Italy are characterized by concentrated ownership structures (Amore et al., 2011; Singal & Singal, 2011), and thus a 50% share is often needed to exert ultimate control. Consistent with other studies, the threshold was reduced to 30% for listed firms (Salvato et al., 2012). The family ownership structure was inspected each year, making our definition of an FF time variant. Thus, an FF may have been included or excluded from the sample according to a possible change in its status during the period.

Annual information on company shareholders was taken from official public filings at the Italian Chamber of Commerce. The identity of family members was established by looking at the surname affinity with that of the family owner and augmented by a cohabitation criterion to discover spousal family leaders (Miller et al., 2018). The database contained detailed information on the financial performance and acquisitions of Italian FFs. For each firm, we gathered the financial data from Analisi Informatizzata delle Aziende Italiane (AIDA), and the relevant acquisition information from Zephyr, the most reliable source for global M&A deals. Both types of data are provided by the Bureau van Dijk and contain information on more than 160 million firms worldwide. We collected data on acquisitions that were carried out in the period 2005–2014 with a stake in the target firm of more than 50% (if not listed) and 30% (if listed), which we labeled as majority deals. Information on firm ownership and corporate governance was collected and cross-validated through the Bureau van Dijk’s AIDA database. Subsequently, we merged our sources and dropped observations with missing values in the key explanatory variables or a negative or zero book value of assets. The result was a panel data set that allowed us to monitor the behavior of each entity over the complete period of 2005–2014. In summary, we started from the entire population of Italian FFs with revenues higher than 50 million euros, which included 2,122 firms. Of those, 94 FFs performed at least one acquisition in a 10-year period, for a total of 137 international acquisitions.

Variables

As a dependent variable, we created a dummy variable labeled international acquisition, which was coded as 1 in each year during which the firm had performed at least one international acquisition (i.e., when the firm obtained the majority of a target outside Italy), and 0 if otherwise (without any acquisition in the period under investigation; Collins et al., 2009). Therefore, we removed companies that underwent domestic acquisitions during the period under investigation. The firm received a value of 1 on the acquisition propensity variable only for the year in which the acquisition was carried out. Firms with more than one acquisition abroad in a year were also coded as 1 given that the underlying rationale for the acquisition activity was the same (Gómez-Mejía et al., 2018). In our sample, we had limited cases of firms with more than one acquisition.

Our data allowed for a continuous measure of family ownership concentration to be computed, which helped account for differentiation in terms of SEW (Gu et al., 2019; Minichilli et al., 2016). For each year of the period investigated in our analyses (from 2005 to 2014), we measured the family ownership concentration through the Herfindahl index (Demsetz & Lehn, 1985), calculated by summing up the squared percentages of shares controlled by the top seven family shareholders, which results in a value between 0 and 1 (Miller et al., 2013). The Herfindahl index is a very suitable measure for detecting the power distribution of the FF, meaning that if the value is close to 1, the main family shareholder has exclusive autonomy to make decisions. Furthermore, the higher this number, the less the risk was shared among family owners, resulting in a higher financial risk concentration (Gómez-Mejía & Wiseman, 2016; Hoskisson et al., 2017). On the contrary, a number close to 0 reveals that ownership and financial risk were equally distributed among family owners. For our study, ownership concentration was computed for the majority family shareholders group, and, in turn, the degrees of dominant control and risk-bearing were likely to have an impact on their acquisition behavior. It is thus a good proxy for SEW (in comparison to dummy variables) and allows for a more granular assessment of family concerns (Villalonga & Amit, 2006).

To investigate the effect of family management, we used a moderator to measure family involvement in leadership positions, labeled as family leadership, which was equal to 1 when the CEO was a family member (or more than one CEO, but all being family members) and 0 otherwise (Miller et al., 2014; Strike et al., 2015). To test Hypothesis 2, we focused on the interaction between the Herfindahl index and family leadership to estimate the degree of influence and control exercised by the family on acquisition strategies (Caprio et al., 2011).

To measure the moderating effect of performance below aspirations, we used below-target performance. Following Gómez-Mejía et al. (2018), we considered the return on sales (ROS) and compared the average of the FF’s financial performance in the 5 years before the acquisition (starting in 2005, with a maximum of two missing values) with the performance of its competitors. For the performance of competitors, we measured the median performance (commonly referred to as social aspirations; Cyert & March, 1963), which is a well-accepted measure in acquisition studies (Gómez-Mejía et al., 2018; Iyer & Miller, 2008; Kim et al., 2015; Malhotra et al., 2018). This number includes all firms (family and non-family ones) with sales exceeding the threshold of 50 million euros in the respective two-digit NACE category to control for industry differences (Basuil & Datta, 2015; Vaara et al., 2012). While the existing literature largely views social and historical aspirations as similar, Kim et al. (2015) stress that both measures matter significantly in the strategic context of acquisitions. We opted against the alternative, widely used measure of own historical aspirations (Levinthal & March, 1981) as FFs were found to be less sensitive to their own performance (Gómez-Mejía et al., 2007), although they do fear threats from competition. To measure the discrepancy in performance relative to competitors, we took the absolute value of the difference if negative; otherwise, the variable was set to 0.

Based on a comprehensive review of prior studies, we included control variables for the characteristics of the acquirer to rule out potential confounding factors that could affect our dependent variables. Related acquisitions were measured as a dummy variable equal to 1 if the first two-digit NACE code of the acquiring and target firms was the same, and 0 otherwise (Hussinger & Issah, 2019). Acquirer age was computed as the logarithmic transformation of the number of years since the firm’s foundation; older FFs are widely regarded as becoming increasingly diversified and professionalized (Anderson & Reeb, 2003; Miller et al., 2007), which should result in a higher propensity to make international acquisitions. Acquirer size was measured as a logarithmic transformation of total sales, as larger firms usually have more resources and are therefore less reluctant to undertake acquisitions and more confident about their success (Kim et al., 2011). Acquirer leverage represents the ratio between the book value of the total assets and the equity book value of the firm. We expected that financial numbers would influence how solvent a firm would need to be to follow international acquisition strategies (Haleblian et al., 2009). The acquirer liquidity ratio was calculated as the ratio of current assets to current liabilities. 1 With a dummy variable (listed), we checked whether the family firm was listed (3.2% of the firms were listed in our sample). On the leadership side, given the importance of career horizon in the field of international acquisitions, we also included CEO career horizon, measured by deducting the CEO’s current age from 70. Following Strike et al. (2015), we based this on the assumption that while the retirement age is 65 years, CEOs generally remain with the firm for another 5 years as board members before ending their careers. Finally, we included a variable that considered the leadership model, which was measured by the number of people who held the CEO position (No. of CEOs), as about one-third of FFs included in the sample had a collegial leadership model (e.g., having more than one CEO). We also included controls for corporate governance structures. Furthermore, we distinguished among the family generation involved in the firm, as this may have influenced board decision-making processes (Gómez-Mejía et al., 2010; Stockmans et al., 2010). We also dichotomized between FFs run by the first generation, second generation, and those controlled by a later generation (used as a baseline). The presence of relevant non-family minority shareholders was a possible missing but important control variable, as a venture capitalist/investor national/international as a minority owner can significantly influence international acquisition propensity. Thus, we controlled for non-family minority shareholders, which was measured by the percentage of the firm’s shares not held by members of the owning family. As all of our firms were family-controlled, the maximum value was 49.9% for not-listed firms (Arregle et al., 2012; Calabrò et al., 2013).

To complement the firm-level controls, we also included several country-level control variables. First, we accounted for the GDP growth rate to control for the overall host country’s market potential, measuring the GDP growth rate of the country (Collins et al., 2009). Second, we controlled for institutional differences (Xu & Shenkar, 2002) using Kogut and Singh’s (1988) measure of cultural distance, as prior research suggests that cultural differences between the home country of the acquiring firm and the host country affect acquisition activity in new markets (Barkema & Vermeulen, 1998).

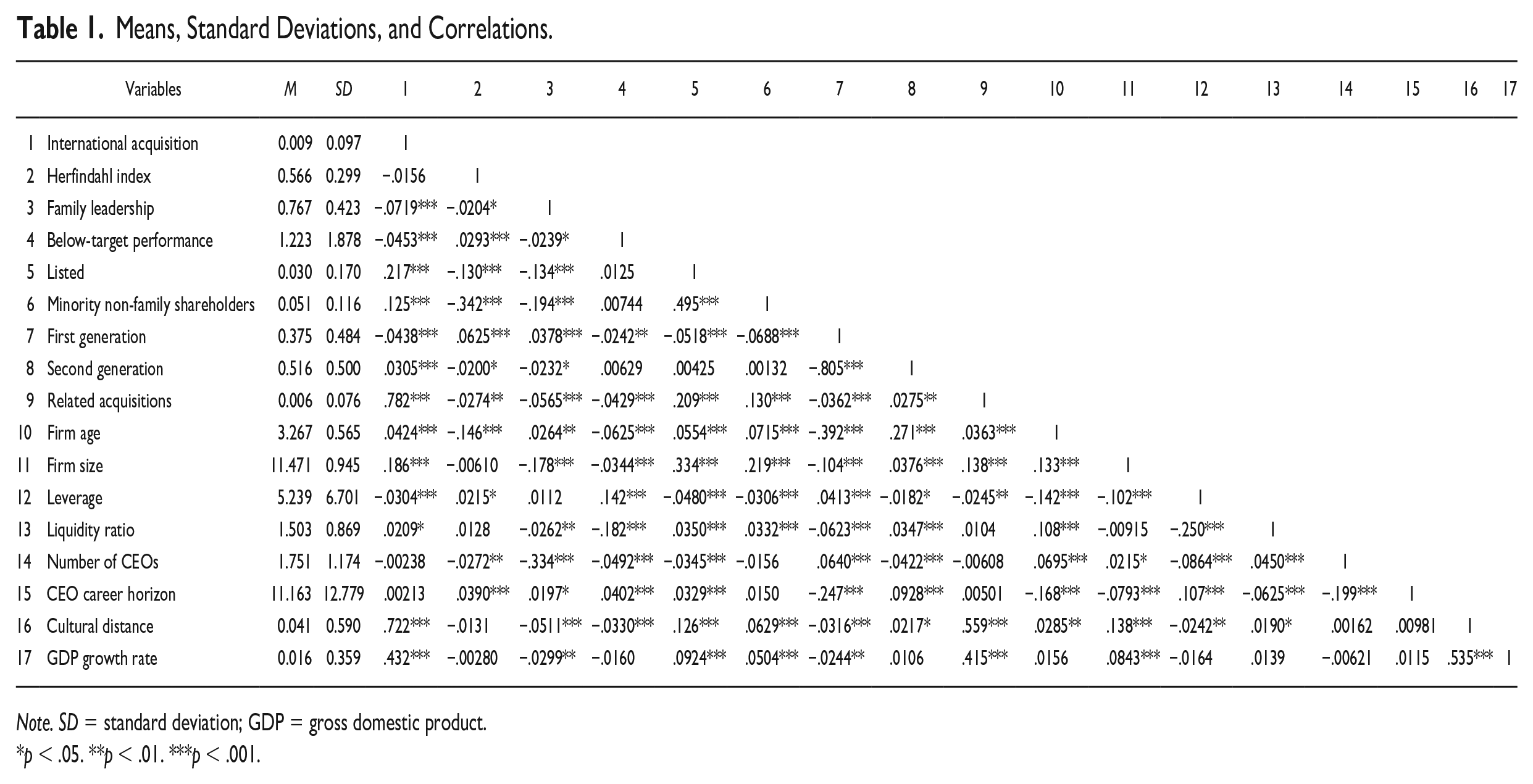

Table 1 shows the means, standard deviations, and Pearson correlation matrix among all variables, excluding the interactions because of their high correlation with the respective originating variables. The table does not show unusual levels of correlation between any of the variables. We assessed multi-collinearity problems by the variance inflation factor (VIF) using the common threshold of 10, which was never exceeded across our models (Hair et al., 2006). We standardized both the main variables and the moderators before the interactions. Thus, multi-collinearity did not bias our analysis.

Means, Standard Deviations, and Correlations.

Note. SD = standard deviation; GDP = gross domestic product.

p < .05. **p < .01. ***p < .001.

Analysis and Robustness

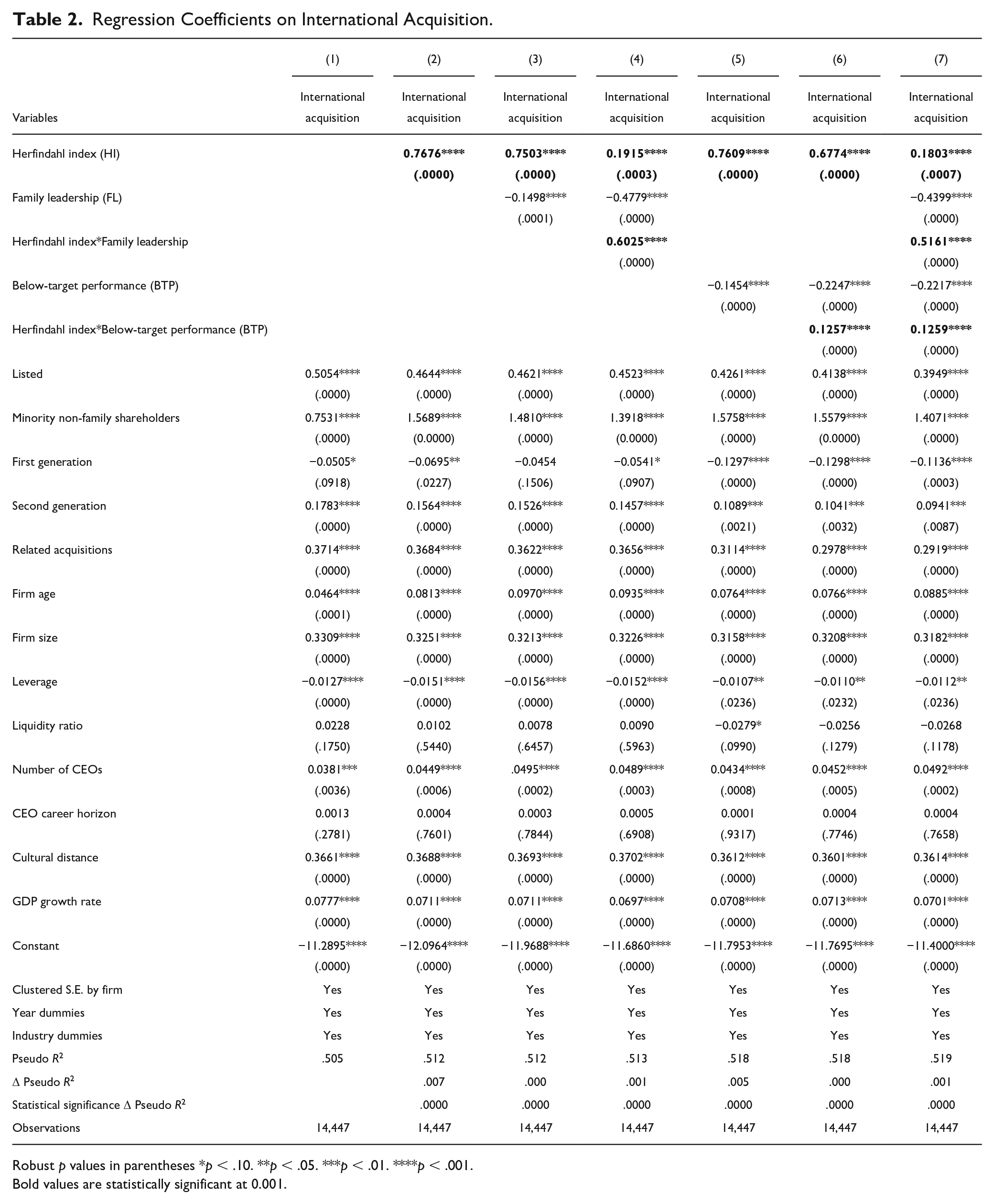

Table 2 presents the results of the econometric estimates, where international acquisition served as a dependent variable, while family ownership concentration (Herfindahl index), below-target performance (ROS), and family leadership and their interactions were the explanatory variables. Given the dichotomous nature of the dependent variable (i.e., whether a firm did or did not undertake an international acquisition), we employed a probit model to study the effect of the regressors on the propensity to choose an international target (Gómez-Mejía et al., 2018). The models were controlled for the previous factors and included both the industry and year fixed effects, as our data constituted a time series panel where not all observations were independent (i.e., even in a few cases, we had firms that undertook more than one acquisition over the considered time frame). Therefore, standard errors were clustered by firm to account for heteroskedasticity and serial correlation at the firm level. Finally, all independent and control variables were lagged by one year from the dependent variable.

Regression Coefficients on International Acquisition.

Robust p values in parentheses *p < .10. **p < .05. ***p < .01. ****p < .001.

Bold values are statistically significant at 0.001.

The seven models in Table 2 tested the three hypotheses. Hypothesis 1 posited that family ownership concentration positively relates to international acquisition propensity over the years 2005–2014 and is presented in Model 2. Hypothesis 2 assumes that the relationship between family ownership concentration and international acquisition propensity is positively moderated by the presence of a family CEO (Model 4), while Model 6 investigates whether international acquisition propensity is moderated by below-target performance (Hypothesis 3). Model 7 shows both moderating variables simultaneously in the same econometric regression.

The first model displays the link between the control variables and international acquisition propensity. The second model revealed a positive relationship between family ownership concentration and the likelihood of acquiring an international target. As shown in Table 2, Model 2, the coefficient of family ownership concentration was positive and statistically significant (+0.7676; p < .001). This result supported Hypothesis 1. In the third model, we introduced the impact of family leadership on the propensity to acquire an international target, suggesting that FFs managed by family members exhibit a lower likelihood of making international acquisitions. The first two-way interaction between the Herfindahl index and the presence of a family CEO (Model 4) revealed that the propensity to acquire international targets for FFs with a high ownership concentration was enhanced when there was a family CEO. The coefficient was positive and statistically significant (+0.6025; p < .001), thus providing support for Hypothesis 2. In the fifth model, we introduced the impact of below-target performance on the propensity to acquire an international target, suggesting that FFs with below-target performance exhibit a lower likelihood of making international acquisitions. The sixth model added the interaction term between family ownership concentration and below-target performance. The results suggest that FFs with high family ownership concentration and with below-target performance show a significant increase in their international acquisition propensity (+0.1257; p < .001). In other words, FFs characterized by a high family ownership concentration and what experience below-target performance prioritize financial success by sacrificing current SEW and are more likely to engage in an international acquisition for prospective SEW gains. Hence, Hypothesis 3 was supported. Finally, in Model 7, we ran the full model, including both two-way interactions with the Herfindahl index (i.e., below-target performance and family leadership). Thus, Hypotheses 2 and 3 were fully supported. Moreover, the difference in the pseudo R2 between the seven models was always significant.

We performed different robustness tests to strengthen and better contextualize our findings. As a first robustness check, we tested our hypotheses through different performance measures (ROA and ROI) for below-target performance. The results remained significant at the same level, thus supporting our set of hypotheses. Second, above-target performance might imply that FFs have slack resources, which should affect their willingness to conduct risky investments, such as acquisitions; we thus performed a robustness test by restricting the sample only to FFs that had below-target performance. The results showed that Hypothesis 2 was supported, as in the main model (and the same results held if we used ROA or ROI as the base to calculate below-target performance). Third, we performed the analyses by splitting our sample into two subsamples for unrelated and related acquisitions, and our results revealed that Hypotheses 2 and 3 were supported only in the subsample of unrelated acquisitions. This result is very interesting, as it gives special support to our theoretical contention that FFs with high family ownership concentration make unrelated international acquisitions (which are supposed to be riskier than related acquisitions), especially when the firm experiences below-target performance and is led by a family CEO. The results of this test will be further commented on in the discussion and findings section, as they add more nuance to our understanding of FFs’ international acquisition choices.

Furthermore, we used an alternative method to calculate the Herfindahl index and establish the robustness of our findings. Specifically, we calculated the same type of Herfindahl index across all large shareholders (family and non-family; Miller et al., 2013). In this way, we moved to the firm level to measure ownership concentration (instead of only the family level), and the results were basically unchanged. We then used an alternative measure to assess the dominance of major shareholders. Specifically, we considered the percentage of shares held by the first family shareholder, and the model had the same levels of significance as the main model. Finally, we examined the effect of acquisition experience (Bauer & Matzler, 2014). In fact, as FFs face less executive turnover, they might remember and benefit more from what they have learned from previous acquisitions. We measured acquisition experience by considering the number of acquisitions in the previous 5 years. The variable was positive and statistically significant, suggesting that previous acquisition experience affects international acquisition propensity. Tables and further details related to the tests described above are available upon request from the authors.

Discussion and Conclusion

By considering FFs’ international acquisition choices as a mixed gamble, the aim of this article has been to theorize and test the theoretical contention that family decision makers face a trade-off in prioritizing between current and prospective financial and SEW gains, which could lead to different international acquisition choices. Moreover, we have also explored the outcome of the mixed gamble when the FF has a family CEO or experiences below-target performance. Our main finding largely supports our theoretical contention, suggesting that FFs with a dominant family owner have a higher likelihood of engaging in international acquisitions when they are led by a family CEO or experience below-target performance, as they then prioritize prospective financial gains and prospective SEW gains, thereby sacrificing current SEW and financial wealth.

In taking a more systematic look at our findings, as shown in the results section, Hypothesis 1 was supported, suggesting that in FFs characterized by the presence of multiple family shareholders (that together have many company shares), SEW preservation logics in relation to international acquisition choices operate differently among majority versus minority family owners. These findings shed light on the overall belief that having concentrated family ownership in a firm would automatically lead to more conservative strategies and less risky choices as long as they would be a threat to the degree of accumulated SEW. Distinguishing SEW preferences between majority and minority family owners and considering that reference points to SEW may help differentiate how different family principals prioritize current versus prospective SEW (and current vs. prospective financial wealth) in relation to international acquisition choices. Our findings show that in international acquisitions, dominant family owners see the opportunity to renew the family’s dynastic succession for the next generations and thus give priority to the prospective SEW and financial wealth resulting from a successful operation.

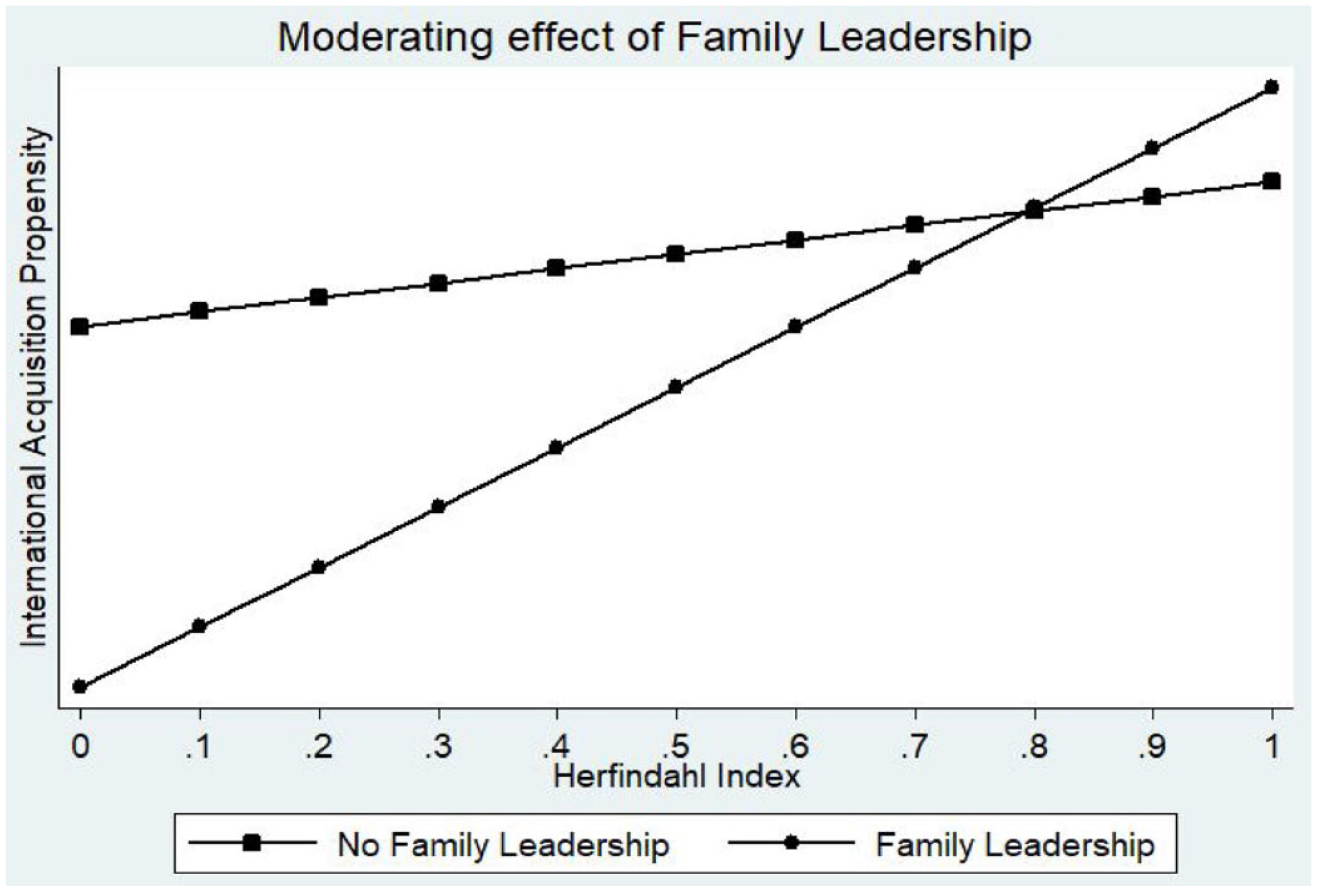

To define the boundary conditions under which the mixed gamble between current and prospective financial wealth and current and prospective SEW works, our findings further suggest (i.e., Hypothesis 2) that FFs with a high family ownership concentration have a higher likelihood of engaging in an international acquisition, especially if led by a family CEO (see Figure 2).

Interaction Between Family Ownership Concentration and Family Leadership.

This finding is in line with the work of Hoskisson et al. (2017), who stressed the urgency to better differentiate between decision makers, as some executives have the “discretion to force his or her will” (p. 156). In fact, FFs with a dominant family owner are not only more risk seeking but also have the means of taking risks (Cruz et al., 2010), as a family CEO can enforce the decision of an international acquisition with the aim of maintaining the long-term continuity of the firm (Carr & Bateman, 2009) and that of the family (Gómez-Mejía et al., 2011). In other words, the family CEO has the obligation to prevent the FF from defaulting and has virtually no choice other than to take alternative measures, as prospective SEW in the form of family control and influence and dynastic succession is otherwise at stake (Berrone et al., 2012). As a consequence, care for prospective SEW looms higher for family CEOs than for non-family ones (Strike et al., 2015). A possible alternative explanation is that FFs with a dominant owner and a family CEO could leverage large amounts of survival capital more easily, such as extra voluntary work or interest-free loans from other family members, which can be utilized as the firm needs (Arregle et al., 2007; Sirmon & Hitt, 2003). On the contrary, FFs with concentrated family ownership and a non-family CEO may face a “paralysis” of decision-making, as the conflict between SEW and economic success, as well as family versus non-family decision makers, is likely to erupt (Souder et al., 2017).

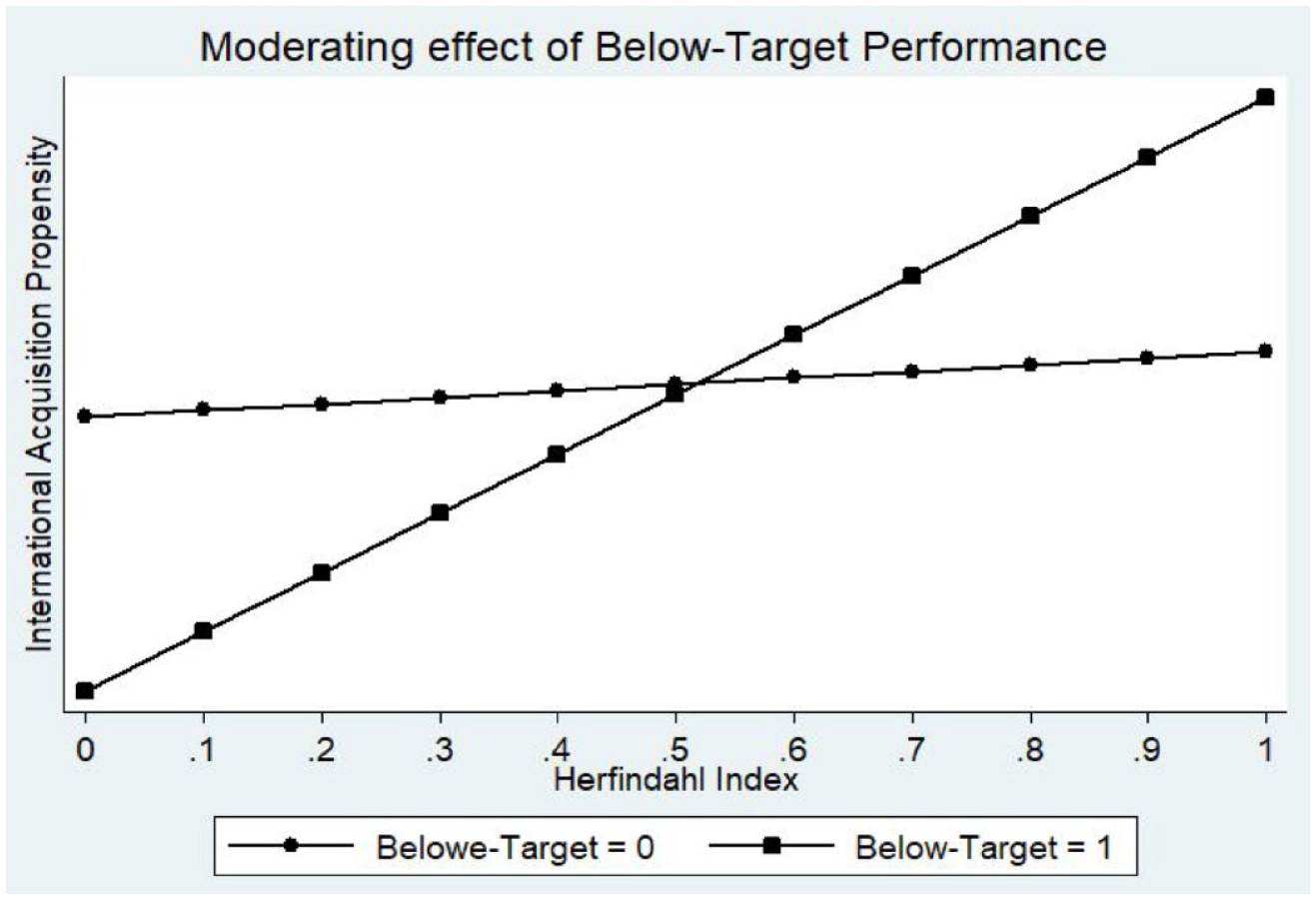

Integrating a recent extension of SEW through the mixed gamble approach (Gómez-Mejía et al., 2014; Kotlar et al., 2018) and additional research on the importance of defining boundary conditions for SEW (Calabrò et al., 2018; Chrisman & Patel, 2012; Gómez-Mejía et al., 2018), our confirmation of Hypothesis 3 further supports the view that FFs with a dominant owner who are also experiencing below-target performance have a higher likelihood of engaging in international acquisitions (see Figure 3).

Interaction Between Family Ownership Concentration and Below-Target Performance.a

This is happening as the dominant family owners prioritize prospective financial benefits and prospective SEW gains, which place concerns regarding current SEW on the part of minority family owners in the back seat. This logic is in line with the recent findings of Gómez-Mejía et al. (2018), suggesting that performance below aspirations results in riskier strategies as a last resort to protect FF continuity and legacy. On the contrary, in FFs with a low family ownership concentration, when performance does not reach the desired levels, family owners may be overruled by conflicting SEW concerns (Berrone et al., 2012; Vardaman & Gondo, 2014), which can slow down the making of decisions and create organizational inertia, as no dominant family owner has a final say on the international acquisition strategy. Therefore, in this type of FF, the already low individual influence of family owners is expected to become even more diluted in the aftermath of an international acquisition, as external funds and additional stakeholders interfere with family discretion (Gómez-Mejía et al., 2010). Consequently, they might be more focused on prioritizing their current SEW to preserve their family control and influence (Berrone et al., 2012).

Contributions to Theory

Our study contributes to family business research by consolidating the use of SEW as the main theoretical paradigm. We achieved this by explaining FFs’ strategic choices through the mixed gamble approach (Gómez-Mejía et al., 2014; Kotlar et al., 2018) and by differentiating SEW (Miller, & Le Breton-Miller, 2014; Strike et al., 2015; Vandekerkhof et al., 2018). Specifically, we consider international acquisition choices to be mixed gambles, thereby adding to the trade-off between financial and SEW motives (Chrisman & Patel, 2012; Gómez-Mejía et al., 2018), which can be understood in terms of the differentiation between the current and prospective financial wealth and the current and prospective SEW associated with different levels of family ownership concentration. We thus contribute to the debate by showing that reference points can also lie in the future (Bromiley, 2010; Levy, 1992) and that this future wealth orientation (i.e., orientation toward prospective SEW) increases the current level of risk-taking (Martin et al., 2013) on the part of dominant family owners toward international acquisitions. Our findings also contribute to the recent debate on the importance of identifying boundary conditions to understand the impact of financial wealth and SEW priorities on FFs’ strategic choices (Souder et al., 2017) by adding evidence of the contingency-dependent nature of SEW (Schulze & Kellermanns, 2015). In fact, FFs do engage in international acquisitions when they have a dominant family owner and the CEO is a family member or if the firm is experiencing negative performance feedback. We thus offer a more granular picture of family owners’ risk-taking behavior, suggesting that the most conservative players in terms of preservation of current SEW and prioritization of current financial wealth are the minority family owners who will deny acquiring internationally (thus being more risk adverse) to preserve their current family control and influence. In line with Minichilli et al. (2016), our findings also suggest that family CEOs take significantly more risks than their non-family counterparts. These findings further support and complement those reported by Gu et al. (2019), who suggest that FFs appreciate different SEW dimensions, whereby some owners focus on safeguarding the family dynasty and long-term economic success and competitiveness, which drives risky strategies, while others try to preserve their current family influence and, as such, reject any potential drawbacks to current SEW endowment.

We also contribute to the acquisition literature, especially the debate about PP conflicts between the dominant family owner and minority family members, in predicting strategic choices and outcomes (Connelly et al., 2010; Li et al., 2017; Purkayastha et al., 2019; Thomsen & Pedersen, 2000). In particular, we show how dominant family owners play a key role in taking on risky strategies, such as international acquisitions. If only one family member dominates, decision-making is facilitated (Feltham et al., 2005) and potential PP conflicts are silenced by his or her dominant position, whereas FFs with less discretion of single owners are prone to more conflicts (Martin et al., 2017). Thus, family ownership concentration may not only cause differences in the importance assigned to SEW dimensions but also influence the ability of family owners to enforce their managerial decisions and personal risk preferences on the other shareholders and thus solve potential PP conflicts. In addition, we highlight the role of family owners by using a measure of family ownership concentration, which provides additional finer-grained evidence than previous findings on the relationship between family ownership and acquisition choices (Gómez-Mejía et al., 2018; Miller et al., 2010). We further underline the importance of accounting for heterogeneity in the risk preferences of FFs (Hoskisson et al., 2017) by focusing on a measure of ownership that helps catch the actual power of family shareholders; furthermore, by conditioning the analyses to the group of FFs, we offer a more nuanced version of ownership dynamics in FFs. Our findings also add to the literature on managerial motivation for acquisitions (Gamache et al., 2015) by highlighting the importance of considering the motivation of owners as well as those of CEOs, as differences in leadership determine different risk-taking behaviors (Villalonga & Amit, 2006). In particular, we complement existing findings on differences between family and non-family CEOs (Miller et al., 2014; Minichilli et al., 2014; Strike et al., 2015; Zahra, 2005) by revealing that family CEOs are not less risk-seeking per se than their non-family peers, but that their function as safeguards of family wealth and legacy sometimes requires risky actions.

In addition, our findings add evidence to the debate on FF internationalization (Pukall & Calabrò, 2014), particularly on entry mode choices. In fact, we provide evidence that FFs do not exclude international acquisitions per se because this equity entry mode requires more commitment of resources but that under specific ownership, leadership, or firm conditions, some FFs might be more willing than others to execute the riskiest strategic choice (i.e., making an international acquisition).

Finally, we add to the literature on FF growth by recognizing the importance of FFs embarking on international acquisitions to foster firm growth. Indeed, in an aggressive global market rife with competition, international strategy is a way to grow beyond national borders and nurture FFs’ competitive advantages and thus overcome eventual economic downturns (De Massis et al., 2018).

Implications for Managerial Practice

This study has practical implications, especially for family decision makers facing international acquisition decisions. When the family is confronted with an international acquisition decision, minority family owners may feel less secure and might be afraid of losing control over the firm. Thus, to make them more comfortable in embarking on an international acquisition, it is important to recognize the challenges and find potential solutions to ensure the well-being of both the family and the business. In this way, minority family owners could become more prone to engage in international acquisitions. In addition, as family ownership concentration appears to be the means to solve PP conflicts, sharing ownership among different family members does not appear to be a successful choice, especially when the firm is confronted with risky decisions, such as embarking on an international acquisition. Indeed, having ownership rest in the hands of one dominant family shareholder would facilitate the decision-making process and help avoid conflict, which would likely have a positive effect on the international acquisition strategy.

Limitations and Future Research

Our work is not exempt from limitations that may pave the way for avenues for future research. First, we do not measure SEW explicitly; rather, we use the Herfindahl index as a proxy for it. In comparison with the use of a dummy variable, we were able to obtain a more granular assessment of family concerns. However, as we do not consider SEW as a multidimensional measure, future studies could measure SEW using established scales (Berrone et al., 2012), as an increasing amount of research is calling for multidimensional measures of SEW (e.g., Berrone et al., 2012; Debicki et al., 2016; Hauck et al., 2016; Swab et al., 2020).

Although the Italian country setting can be considered representative of the Western world, we encourage scholars to apply the model presented here to other countries and to develop studies contrasting cultural, legal, and economic differences between the acquiring and the target countries. In this regard, it might be interesting to investigate how cultural differences between countries, as well as families, shape the drivers and consequences of this strategic choice. In this study, we do not consider some variables that could be especially relevant to understanding international acquisitions in the context of FFs. Specifically, by following prior studies (e.g., Bettinazzi et al., 2020), future studies could control for similarity in ownership concentration. Indeed, looking at the difference in ownership between the acquiring and the target companies would provide a better understanding of the decision-making process. In addition, international acquisitions are risky strategies, and the level of risk also depends on the size of the deal. Generally, the bigger the deal, the riskier the international acquisition, and the greater the effect on the FF’s decisions. Therefore, future studies could take this dimension into account.

Given previous success with an activity, a firm is more likely to repeat similar activities. This is because it has learned certain skills and capabilities and may find such persistence less risky compared with firms having limited experience, for example, by having access to professional managers (Basuil & Datta, 2015; Boellis et al., 2016). Therefore, although we operationalized acquisition as an outcome variable, it might also function as an antecedent or moderator for risk-taking. As experience with a given activity makes a firm more confident and decreases perceived uncertainty, the field would benefit from further elaboration on the force of acquisition experience in FFs. Prior experience has been positively associated with acquisition propensity, whereas knowledge-based resources foster a preference for greenfield investments (Klier et al., 2017). Accordingly, it is worth exploring how experience and knowledge may drive FF acquisitions.

Although the literature assesses different motives for international acquisitions, future studies could consider additional motives, such as growth (e.g., when the home market is saturated), synergies, or new business models, which would all add more nuances to our findings.

Another important dimension to investigate is whether FFs pay a high acquisition premium because they may believe that they can repeat prior successes and extract greater value from the current acquisition than the premium paid (Kim et al., 2011; Krishnan et al., 2007). Furthermore, as shown by Leitterstorf and Wachter (2016), investigating acquisition premiums from an SEW perspective and combining them with different ownership and leadership characteristics could shed more light on acquisition motives, as premiums are a very suitable proxy for how family decision makers perceive the risks of an acquisition (Geppert et al., 2013). Moreover, and along a similar line of investigation, even though we consider the CEO’s career horizon (Strike et al., 2015) to be a control variable, our model does not capture how different family CEOs’ retirement prospects might affect international acquisition choices. Future research could better incorporate the CEO’s career horizon into the analysis by exploring how nearing retirement might influence international acquisition decisions and the prioritization of SEW dimensions within FFs.

Risk-taking by dominant family owners can also lead to principal–principal conflicts when the dominant family coalition uses its voting power to hurt minority shareholders (Jiang & Peng, 2011; Young et al., 2008). Recently, the dilemma has shifted to the SEW paradigm, potentially influencing internationalization decisions and procedures (Martin et al., 2017). Thus, scholars may examine how majority vs. minority family owners influence internationalization decisions and procedures. In addition, psychological ownership (Lee et al., 2019) may affect strategic decisions and explain why some FFs are more prone to engage in international acquisitions.

Finally, the research assumes a dominant family CEO, but non-dominant family members may influence decision-making differently. Non-dominant CEOs may have different SEW priorities, viewpoints, and decision-making methods, complicating family ownership and international acquisitions. Future research could therefore examine how non-dominant family CEOs affect family ownership and international acquisitions. Such studies would further illuminate the complex relationship between family ownership, CEO traits, and international acquisition choices.

Concluding Remarks

As international acquisitions offer promising financial benefits but equally bear uncertainty, they are an ideal context in which to analyze risk preferences in FFs. Our study shows that FFs with different family shareholder structures (dominant vs. minority family owners) are confronted with different trade-offs among current and prospective financial wealth and SEW, leading to differences in their international acquisition choices. Generally, we found that FFs with a dominant family owner have a higher likelihood of engaging in international acquisitions when they are led by a family CEO or experience below-target performance, as they come to prioritize prospective financial gains and prospective SEW gains, thereby sacrificing current SEW and financial wealth.

Supplemental Material

sj-docx-1-fbr-10.1177_08944865231205847 – Supplemental material for Family Firms’ Shareholder Structure and International Acquisitions: A Differentiated Socioemotional Wealth Approach

Supplemental material, sj-docx-1-fbr-10.1177_08944865231205847 for Family Firms’ Shareholder Structure and International Acquisitions: A Differentiated Socioemotional Wealth Approach by Andrea Calabrò, Mariateresa Torchia, Fabio Quarato, Alfredo Valentino, Domenico Rocco Cambrea and Fynn-Willem Lohe in Family Business Review

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.