Abstract

This paper examines the influence of family management and firm age on a firm’s decisions on product versus international diversification. Based on socioemotional wealth literature and the temporal dimension of family influence, we hypothesize that family management prefers product diversification and that the positive impact of family management becomes stronger in older firms. Analyzing data from 422 manufacturing firms in the S&P 1,500, we find strong empirical support. Our findings remain robust to endogeneity concerns. This study contributes to the literature by offering new insights into how socioemotional wealth preservation and temporal factors jointly shape diversification strategies in publicly traded firms.

Keywords

Introduction

Corporate diversification is an important strategic decision that influences a firm’s survival and growth (Ahuja & Novelli, 2017; Gómez-Mejía et al., 2010). Product diversification and international diversification represent two modes of corporate diversification. Product diversification involves entering new lines of activity (Palich et al., 2000), whereas international diversification refers to expanding into markets outside a firm’s home country (Hitt et al., 1997). Prior work has offered extensive insights into how family governance influences both modes of diversification (Hafner, 2021; Skorodziyevskiy, Sherlock, et al., 2024). Empirical evidence generally indicates that family firms are associated with lower levels of product diversification (Feldman et al., 2016) as well as international diversification than nonfamily firms (Arregle et al., 2021; Fang et al., 2018). This reluctance to diversify is often attributed to family principals’ emphasis on preserving socioemotional wealth (SEW), in particular, their desire to maintain family control and influence over the firm (Hafner & Pidun, 2022).

Despite these insights, the literature has primarily examined product diversification and international diversification as separate strategic phenomena (Hafner, 2021). While both forms of diversification entail significant challenges (Sambharya, 1995), firms may nonetheless pursue the two strategies simultaneously (Deligianni, 2023; Mayer et al., 2015). Firms may also treat product and international diversification as strategic trade-offs (Kumar, 2009), prioritizing one mode of diversification over the other. Although recent research has increasingly focused on such trade-offs (Deligianni, 2023; Stadler et al., 2018), our understanding of the influence of family governance—and family management in particular—on firms’ strategic preferences between product and international diversification remains limited. This is unfortunate, as top management teams (i.e., TMTs) play a central role in shaping firms’ strategic decisions (Hambrick, 2007; Hambrick & Mason, 1984). Family managers, as a central “faction” within the TMTs, exert a particularly strong influence on strategic decision-making (Gómez-Mejía et al., 2018; Kammerlander et al., 2020).

Drawing on the SEW literature, the present study addresses this research gap and examines the impact of family management on firms’ preferences for product or international diversification over time. Rather than treating product and international diversification as static and isolated strategic outcomes, we adopt a comparative lens to examine the impact of family management on firms’ relative preference for product or international diversification over time. In doing so, we provide a more nuanced understanding of the influence of family management on a firm’s diversification choices and the underlying factors that shape these decisions temporally.

Our investigation extends the family business and diversification literature by examining firms’ relative preference for product or international diversification over time, with a particular focus on the influence of family management. Our focus is motivated by the vital role of the TMT in shaping firm strategy (Carpenter et al., 2004; Hambrick & Mason, 1984; Krause et al., 2022). An emphasis on family management aligns with a growing body of research examining the influence of family management on firms’ strategic decision-making processes (e.g., Minichilli et al., 2010; You et al., 2025). Family managers are not only responsible for operational oversight but also for safeguarding the firm’s economic and noneconomic interests (Ray et al., 2018). Accordingly, family management often signal a strong commitment to family-centered noneconomic (FCNE) goals and to the preservation of SEW (Chrisman et al., 2012; Daspit et al., 2018; Tsao et al., 2021).

Drawing from the SEW literature (Berrone et al., 2012; Gómez-Mejía et al., 2007), we argue that greater family representation in the TMT is positively associated with a stronger emphasis on product diversification relative to international diversification. This preference is rooted in family managers’ desire to safeguard SEW, particularly those aspects that are “restricted” to generating benefits for the family through its influence and control of the firm (Miller et al., 2014). In addition, more recent advances in the SEW literature suggest that SEW reference points are not static but instead evolve over time (Cleary et al., 2019; Nason et al., 2019). As family managers collaborate in strategic decision-making over time, they develop shared structures and experience that reinforce SEW as a salient reference point (Nason et al., 2019). Accordingly, this dynamic suggests that family managers’ preference for product diversification becomes more pronounced in older firms, as the SEW tied to traditional strategies and established lines of business becomes increasingly embedded (Verbeke & Kano, 2012).

This study makes several important contributions to the diversification and family business literature. First, prior literature has typically treated product and international diversification as separate strategic choices. The question related to the effect of family management on a firm’s preference for one diversification mode over the other has received limited attention. By jointly examining product and international diversification and identifying conditions under which family management favors one over the other, this study advances a more comprehensive understanding of the effect of family governance on a firm’s diversification choices.

Second, our finding that family representation in the TMT is positively associated with a preference for product over international diversification shows that family managers engage in selective diversification, making strategic choices that align with the preservation of restricted SEW related to centralized family control rather than risk aversion. In turn, our study moves the conceptualization of family governance from simplistic binary categorizations such as risk-averse and risk-taking to richer depictions of the impact of restricted SEW on a firm’s strategic distinctiveness.

Third, our analyses extend the study of the temporal dimension of family influence (H. E. Lin et al., 2023; Sharma et al., 2014) by demonstrating that firm age strengthens the relationship between family management and diversification preferences. The strengthening effect of firm age suggests that the salience of restricted SEW in strategic decision-making intensifies as family values and traditions become more deeply embedded in the firm over time (Boers et al., 2017; Cleary et al., 2019; Hsueh et al., 2023; Nason et al., 2019).

In the remainder of this paper, we review prior literature on product and international diversification, drawing upon the SEW and restricted SEW literature to develop hypotheses. We then discuss our methods and findings. We conclude the paper by discussing its contributions, limitations, and future research opportunities.

Theory and Hypotheses

Central to corporate strategy (Hitt et al., 1997), product and international diversification represent two critical dimensions of a firm’s diversification strategy (Batsakis & Mohr, 2017; Deligianni, 2023; Kumar, 2009; Mayer et al., 2015). There are different types of risk associated with product diversification and international diversification (Alessandri & Seth, 2014; Gande et al., 2009; Herrero, 2017). Product diversification involves risks and uncertainty associated with the development of new products, technologies, and organizational capabilities. In contrast, international diversification exposes firms to the “liability of foreignness” (Zaheer, 1995), including challenges such as divergent customer preferences, political and regulatory uncertainty, and difficulties in establishing legitimacy (Rugman & Verbeke, 2004). When exporting, firms often face significant uncertainty as they develop marketing channels and acquire information on consumers in different countries (Greenaway et al., 2007). Such firms may depend on intermediaries or other foreign agents to learn about customer preferences and the various rules and etiquette associated with doing business in a different country. Firms may also be exposed to the risk of foreign partners expropriating their technological and marketing know-how (C. W. Hill et al., 1990).

As a result, although both diversification strategies present risk, those associated with international diversification are often more complex due to the heterogeneity of institutional environments, the variability of competitive dynamics across international markets, and the diversity of stakeholder relationships in different countries (Hafner & Pidun, 2022). While product and international diversification are not mutually exclusive, product diversification emphasizes adding new products, whereas international diversification focuses on entering foreign markets (Wan et al., 2011). Since firms often face difficulty managing and funding both types of diversification simultaneously (Deligianni, 2023; Kumar, 2009), they may prioritize one form over the other.

Family involvement constitutes a particularly important governance mechanism that shapes the firm’s diversification decisions. There is an increasing body of research examining how family involvement influences a firm’s diversification choices (Anderson & Reeb, 2003; Gómez-Mejía et al., 2010; Hafner, 2021; Hafner & Pidun, 2022). Empirical findings show that family involvement tends to lead the firm to engage less in product diversification to preserve their SEW (Gómez-Mejía et al., 2010; Muñoz-Bullon et al., 2018). A diversifying firm may need to seek outside financing and recruit external professionals, thus threatening the family principal’s authority and influence (Gómez-Mejía et al., 2010). Research has also shown that family involvement has a negative impact on international diversification (Banalieva & Eddleston, 2011; Fang et al., 2018). International expansion often necessitates greater reliance on external stakeholders (Hitt et al., 1997), which can dilute family control of the firm (Gómez-Mejía et al., 2011).

FCNE goals, which reflect the interests and preferences of the controlling family (Chrisman et al., 2012, 2021; Zellweger & Nason, 2008) and the associated SEW, are often used to explain the reluctance toward diversification. Such goals may include maintaining family control of the firm (Gómez-Mejía et al., 2007), perpetuating the family’s identity (Berrone et al., 2012), maintaining a strong sense of community (Miller & Le Breton-Miller, 2005), and preserving the family business across generations (Zellweger et al., 2012). Among these goals, the goal of maintaining current and future control of the firm is particularly important (Berrone et al., 2012; Gómez-Mejía et al., 2007) and is often viewed as the most fundamental FCNE goal (Dou et al., 2020; Gómez-Mejía et al., 2007). In addition, because of the interconnection between family and business entities, family managers are likely to view their business as an extension of the family (Dyer & Whetten, 2006), and strive to create and maintain a strong family identity, reputation, and brand (Patel & Chrisman, 2014; Spielmann et al., 2022; Zellweger & Nason, 2008).

SEW is defined as the stocks of affective benefits derived from the pursuit of FCNE goals (Berrone et al., 2012; Chua et al., 2015). There are two types of SEW recognized in the literature: “restricted” and “extended” (Miller & Le Breton-Miller, 2014). Restricted SEW encompasses family-centric goals that promote a family-oriented agenda concerning influence and control over the firm, whereas extended SEW involves broader commitments that may also benefit external stakeholders. The prioritization of restricted SEW is often reflected in practices such as nepotism, the appointment of family members in key managerial positions regardless of qualifications, which can entrench less qualified leadership but simultaneously reinforce family influence (Miller & Le Breton-Miller, 2014). The dominance of family members within the management team supports the pursuit of FCNE goals (Daspit et al., 2018) and reinforces the preservation of restricted SEW. This dominance reflects a preference for maintaining family control, preserving family authority over strategic decisions, and protecting the family’s privileged position within the firm (Miller & Le Breton-Miller, 2014; Schierstedt et al., 2020). Accordingly, family management serves as a proxy for restricted SEW because the very act of staffing the TMT with family members symbolizes the priority given to family control and influence—the defining characteristics of restricted SEW. In other words, the extent of family management on the TMT has important implications for understanding family firms’ strategic preferences, particularly their inclination toward product over international diversification.

The Influence of Family Management on a Firm’s Diversification Choice

Recognizing that family management plays an instrumental role in shaping firms’ goals and strategic decisions (Chrisman et al., 2012; Kosmidou & Holt, 2022), we posit that greater family representation in the TMT is positively associated with a stronger tendency toward product rather than international diversification. The composition of the TMT reflects the extent to which family preferences are embedded in strategic decision-making. Family representation in the TMT influences diversification choices because family managers tend to evaluate strategic alternatives not only in terms of expected financial returns but also through the lens of SEW (Gómez-Mejía et al., 2007; You et al., 2025). Consequently, family managers prioritize family-centered goals and exercise substantial decision-making power to pursue these goals (Gómez-Mejía et al., 2010).

In line with this view, the salience of SEW is pronounced in publicly traded family firms, where family identity and reputation are highly visible to external stakeholders (Banalieva & Eddleston, 2011; Block & Wagner, 2014), including investors, analysts, and the media. Given the political and institutional complexity and heightened uncertainty associated with international diversification (Jimenez et al., 2019), family managers may view international diversification as posing elevated reputational risks while also reducing family control. Thus, family managers may be particularly sensitive to the potential downside risks associated with international diversification (Gómez-Mejía et al., 2010; Herrero, 2017).

In addition, international diversification may weaken family managers’ ability to maintain centralized authority and expose the firm to a range of exogenous risks. For instance, in the case of foreign direct investment (FDI), firms must decentralize operational and, in some cases, strategic decision-making by delegating authority to foreign subsidiaries, although ultimate control typically remains at the corporate level (C. W. Hill et al., 1990). Even in the case of direct exporting, the most prevalent form of international expansion (Shaver, 2011), firms generally must cede partial control to foreign partners in marketing, distribution, and selling activities. Overall, international diversification is likely to expose family managers to stronger threats to restricted SEW by decreasing family control of the firm.

By contrast, product diversification is less likely to undermine centralized authority or dilute family control over the firm (De Massis et al., 2016; Kotlar et al., 2014). Although product diversification entails types of risk similar to those associated with international diversification, these risks are generally more controllable and easier to manage. Product diversification involves expansion into new activities or product lines; such strategic changes typically build on existing capabilities and established operational routines that are closely linked to the firm’s identity and brand, which represent important dimensions of SEW that family managers seek to preserve. Accordingly, family managers are likely to perceive the SEW risk associated with product diversification as lower than the SEW risk associated with international diversification. As a result, greater representation of family managers in the TMT amplified the salience of SEW priorities, especially restricted SEW priorities, which in turn shapes managers’ diversification preferences. In contrast, these concerns are generally less salient in firms led by nonfamily managers, for whom strategic decisions are less directly tied to SEW preservation and family control.

Moreover, nonfamily managers, who are often selected for their expertise, may have advantages in monitoring and managing international operations (Banalieva & Eddleston, 2011). While family managers derive influence from their family status, nonfamily managers accumulate authority through their positions, credentials, and professional accomplishments. In global environments characterized by complex competitive dynamics and heterogeneous customer tastes (Batsakis & Mohr, 2017), nonfamily managers may be better positioned to pursue internationalization due to their greater willingness to assume risk (S. H. Lin & Hu, 2007) and stronger commitment to complex internationalization strategies (Claver et al., 2009). As a result, nonfamily managers are more likely to prioritize financial goals and pursue international diversification as a means of introducing new strategic paradigms within the firm (Banalieva & Eddleston, 2011; Gedajlovic et al., 2004).

Taken together, we expect firms with greater family representation in the TMT to have a stronger preference for product diversification relative to international diversification.

The Moderating Role of Firm Age

We further examine the moderating effect of firm age on the relationship between family representation in the TMT and a firm’s diversification preference. This investigation is important because family influence is not static, and family firms’ SEW reference points evolve as firms mature over time (De Massis et al., 2014; Nason et al., 2019).

The duration of a family’s involvement with a business significantly shapes the value and quality of the firm’s brand and identity (Martínez et al., 2019; Spielmann et al., 2022). Older firms tend to have high visibility to external stakeholders and stronger brand identities (Sun & Govind, 2022; Wang et al., 2008), making reputational risk and legacy preservation increasingly salient. The heightened visibility associated with international diversification increases the perceived cost of SEW loss, particularly reputational damage resulting from strategic failure. This risk is amplified by the “liabilities of aging,” which can limit older firms’ ability to adjust to new international environments (Carr et al., 2010). This suggests the reference points of family managers in older firms that are characterized by long-standing family control shift in ways that make them especially sensitive to potential SEW losses (Dou et al., 2014). As a result, family managers in older firms are likely to weigh the downside risk of international diversification more heavily than its potential upside gains. Accordingly, we argue that the positive impact of family representation in the TMT on a firm’s preference for product over international diversification intensifies in older firms.

In addition, older firms may develop organizational inertia and “sclerotic thinking,” leading them to rely more heavily on domestically developed routines (D’Angelo & Buck, 2019). In these firms, family managers can more readily recombine traditional products and prior innovations embedded in existing resource portfolios to pursue product diversification (Verbeke & Kano, 2012). Older firms’ longer histories also imply that values and traditions are more deeply imprinted, and these firms are likely to have a stronger desire to preserve and reinforce those traditions (Deligianni, 2023; Erdogan et al., 2020). Product diversification, especially when it relates to the firm’s existing core business, can more easily strengthen identity, reputation, and brand than international diversification, which typically requires substantial organizational adjustments. In this sense, the rigidity and inertia characteristics of older firms (Li et al., 2020; Thornhill & Amit, 2003) may further weaken family managers’ willingness to pursue international expansion.

Taken together, we argue that family managers in older firms are likely to be more sensitive to the potential loss of restricted SEW associated with international diversification due to organizational inertia and rigidity in thinking of family managers. Therefore, firm age should strengthen the positive relationship between family representation in the TMT and the preference for product over international diversification.

Methods

Sample and Data Collection

We drew our sample and the relevant data from several sources, including Standard and Poor’s (S&P) Compustat, the Center for Research in Security Prices (CRSP), Mergent Online, company proxy statements (DEF 14A), company annual reports (10-K), and company websites. Product and international diversification data were drawn from the Compustat database and CRSP. Firm characteristics data were manually collected from firms’ proxy statements filed with the Securities and Exchange Commission (SEC). 1

The initial data sample consists of 578 manufacturing firms drawn from the S&P 1,500 for the fiscal years 1998 to 2017. We used the sample for fiscal years 1998 to 2017 due to the differences in reporting information about operating segments of a firm pre- and post-1998 (Jiraporn et al., 2008; Kumar, 2009). To keep the industry background consistent, we focused our analysis on manufacturing firms with 4-digit SIC codes ranging from 2000 to 3999. Utility and service firms are subject to specific government regulations compared to other firms (Chrisman & Patel, 2012), and they are also less likely to engage in international actions (Fang et al., 2018). As such, these firms were not included in our analysis. To ensure the direction of causality, one-year lags between the dependent and independent variables are used. The dependent variable is measured from 1999 to 2017, whereas the independent and control variables are measured from 1998 to 2016.

In defining family firms, we used a binary measure to distinguish family firms (=1) from nonfamily firms (=0). We classify firms as family firms when the following two conditions are met: (1) at least 5% of shares are held by the controlling family; (2) at least two family members are or have been employed as significant owners, top managers, or directors in the firm’s history (Fang et al., 2018; Miller et al., 2007). Consistent with prior literature (Miller et al., 2007), lone-founder firms—where only the founder but no relatives of the founder are or have been involved in the firm—are not considered family firms in our study.

From the initial data collection of 578 family and nonfamily firms, representing 11,560 firm-year observations from 1998 to 2017, we dropped observations with missing values associated with sales generated from non-core businesses or sales from foreign markets. We also dropped lone-founder firms from the primary analysis, given their unique features that differ from both family and nonfamily firms (Miller et al., 2007). However, we examined the behavior of lone-founder firms as a robustness test. After dropping missing values in analyses, the final sample for our main analyses yielded an unbalanced panel dataset of 422 firms with 5,136 firm-year observations, including family and nonfamily firms, but no lone founder firms. See Appendix A for the distribution of total observations of family and nonfamily firms by the 2-digit SIC industry without dropping observations with other missing values. See Appendix B for the yearly distribution of firms regarding product and international diversification without dropping observations with other missing values).

Measures

Dependent Variable

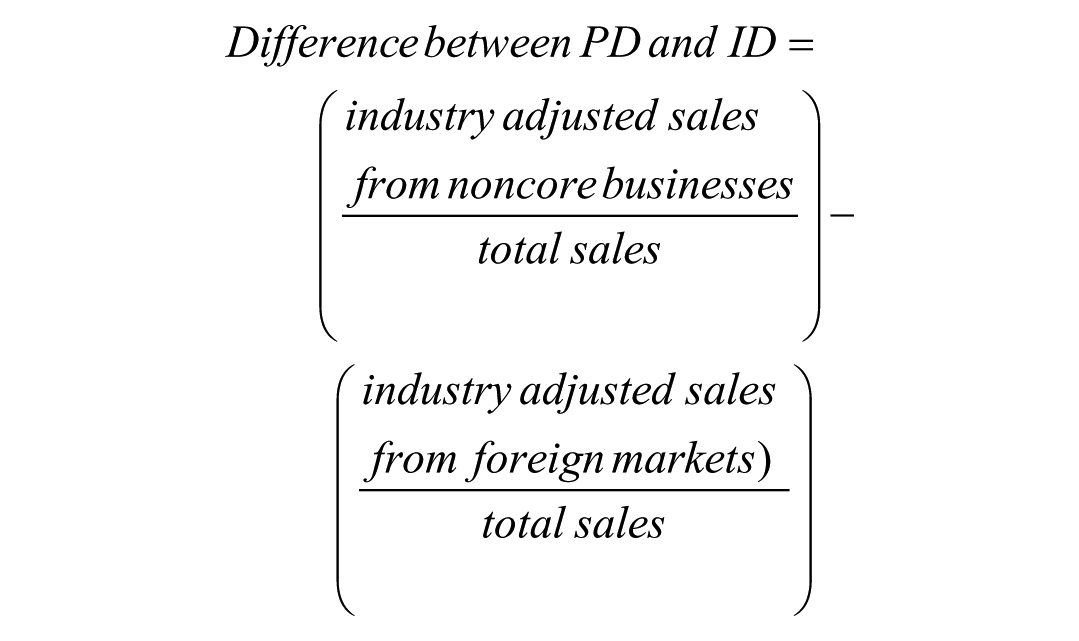

Relative emphasis on product diversification (PD) over international diversification (ID) is measured as follows. For product diversification, following prior literature (Kumar, 2009), we first identified the core business segment of each firm as the segment with the largest sales. Sales in other segments were treated as noncore business sales (Kumar, 2009), which capture the size of new, noncore businesses entered as well as the growth that has occurred in existing noncore businesses. We measured product diversification as the ratio of a firm’s sales generated from noncore businesses to total sales in year t. To measure international diversification, we divide foreign sales by the total sales of the firm in year t (Kang, 2013; Tallman & Li, 1996). We Winsorized both ratios at the 1% and 99% percentile levels in the analyses to mitigate the impact of outliers (Haans et al., 2016) and potential coding errors (Mullins & Schoar, 2016). Also, to exclude industry-specific effects on both types of diversification, we adjusted the two measures by subtracting the industry medians (Berger & Ofek, 1995). Thus, the relative emphasis on product over international diversification is equal to the difference between these two ratios.

Independent Variable

Family representation in the TMT is measured using the number of family managers divided by the total number of managers in the TMT. For nonfamily firms, this variable is coded as 0.

Moderator variable

Firm age is equal to the number of years since the firm was founded.

Control Variables

To account for alternative explanations of the proposed relationships, we control for several variables related to family governance, including family share and family representation on the board, because these variables can affect a firm’s pursuit of strategies that attend to the needs of the controlling family (Duran et al., 2016; Singla et al., 2014). Family share is calculated as the total percentage of ownership held by family members. Family representation on the board is measured as the ratio of family members who serve on the board to the total board size. We control for the impact of generational involvement and influence (Sciascia et al., 2014) by encoding first generation family leaders as a dummy variable which takes the value of 1 when there is at least one first generation family member involved in the ownership, the top management team and/or the board, and 0 otherwise. In addition, we control for firm size (measured as the natural logarithm of the total assets of the firm) and firm financial performance (measured as return on assets [ROA]), as both may affect diversification decisions (Fiegenbaum et al., 1997; Su & Tsang, 2015; Xie & O’Neill, 2014). To control for the international experience of the firm, 2 we define comparative foreign sales advantage as a binary variable that takes the value of 1 if the firm’s international sales are larger than the average of the industry at the 2-digit SIC level, and 0 otherwise. We also control for several important strategic decisions of the firm including debt ratio (debt-to-asset ratio), advertising intensity (natural logarithmic transformation of the ratio of advertising expense divided by total sales of the firm), 3 investment intensity (ratio of capital expenditures divided by plant property and equipment investment), and R&D intensity 4 (ratio of R&D spendings divided by total sales) as these decisions may affect diversification choices (Delios & Beamish, 1999; Russo & Fouts, 1997; Strike et al., 2006). Since diversification is path-dependent (S. J. Chang, 1996) and a firm’s prior diversification experience can affect the firm’s subsequent diversification decisions (Jung et al., 2010; Mayer et al., 2015), we also control for a firm’s prior diversification experience by incorporating the lagged terms of the difference between PD and ID for years t – 1 and t – 2 in our analyses. Finally, we control for the differences in diversification across industries and years by including industry dummies measured at the two-digit SIC level and year dummies, respectively. All control variables discussed above are measured in year t – 1.

Estimation Strategies

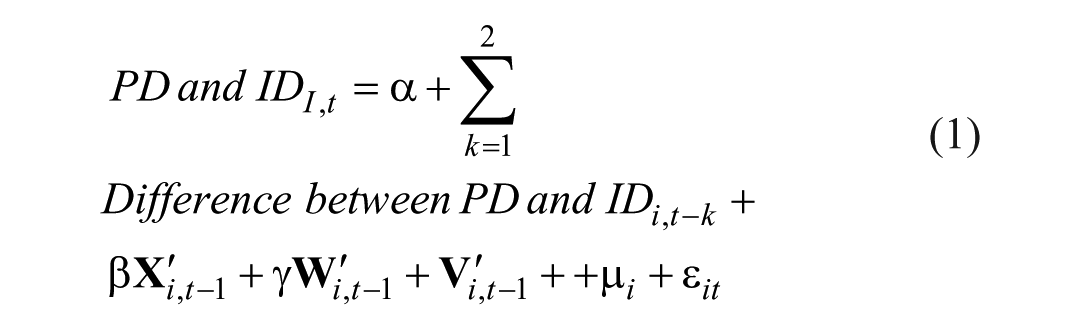

We conduct dynamic panel data analyses using the system generalized method of moments (GMM) procedure, which was developed by Arellano and Bond (1991), Arellano and Bover (1995), and Blundell and Bond (1998), to resolve the potential problems of endogeneity (A. D. Hill et al., 2021), heteroskedasticity, and autocorrelation (Wintoki et al., 2012). Specifically, we employ the xtdpdsys command in STATA (Roodman, 2009; StataCorp, 2023) with the two-step estimation option for the system GMM estimators. In general, we test the hypotheses by estimating the GMM estimators (coefficients of independent variables) in the following functional form of our models:

where difference between PD and ID is the dependent variable, i denotes the firm, and t denotes the year.

The GMM approach supported by the xtdpdsys command allows us to conveniently address the endogeneity concern arising when

Results

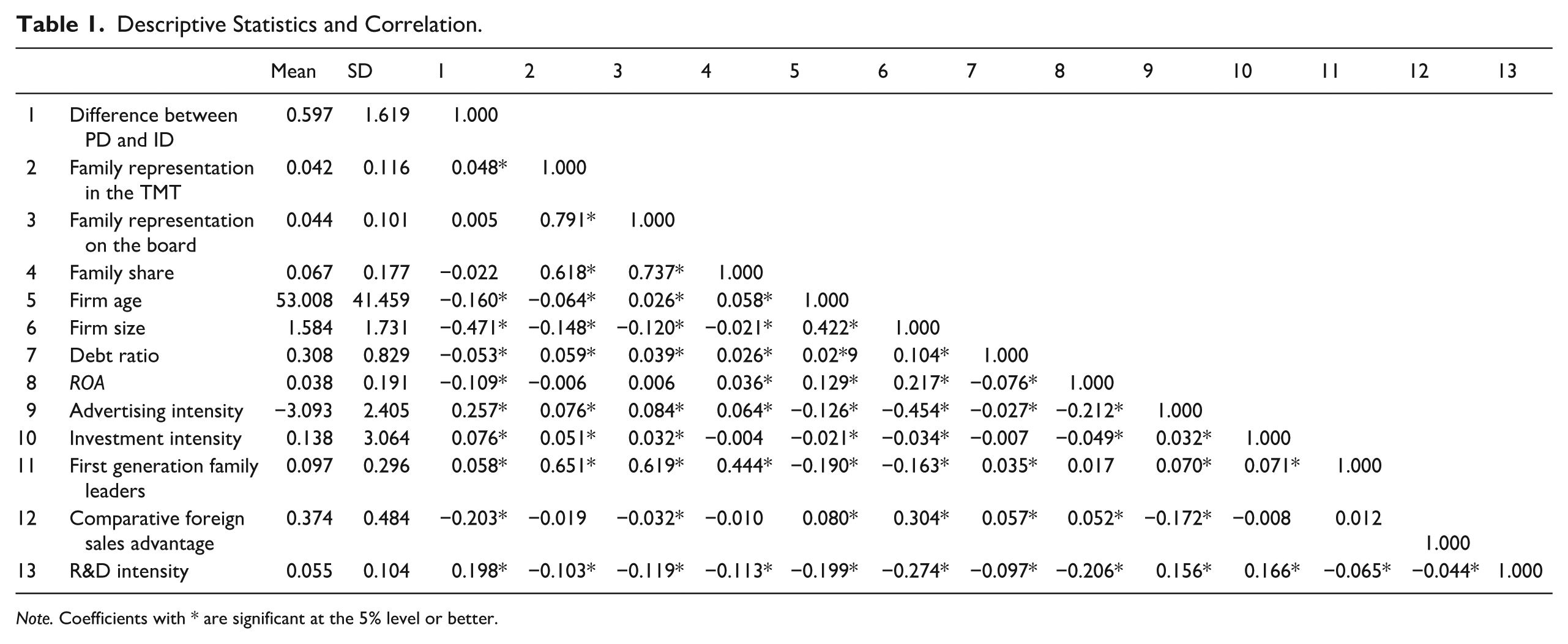

Table 1 presents the means, standard deviations, and pair-wise correlations of the key variables used in our analyses. Consistent with H1, family representation in the TMT is positively and significantly correlated with the difference between PD and ID (r = .048, p = .000). In addition, most control variables exhibit significant correlations with the difference between PD and ID, underscoring the need to include them in our analyses.

Descriptive Statistics and Correlation.

Note. Coefficients with * are significant at the 5% level or better.

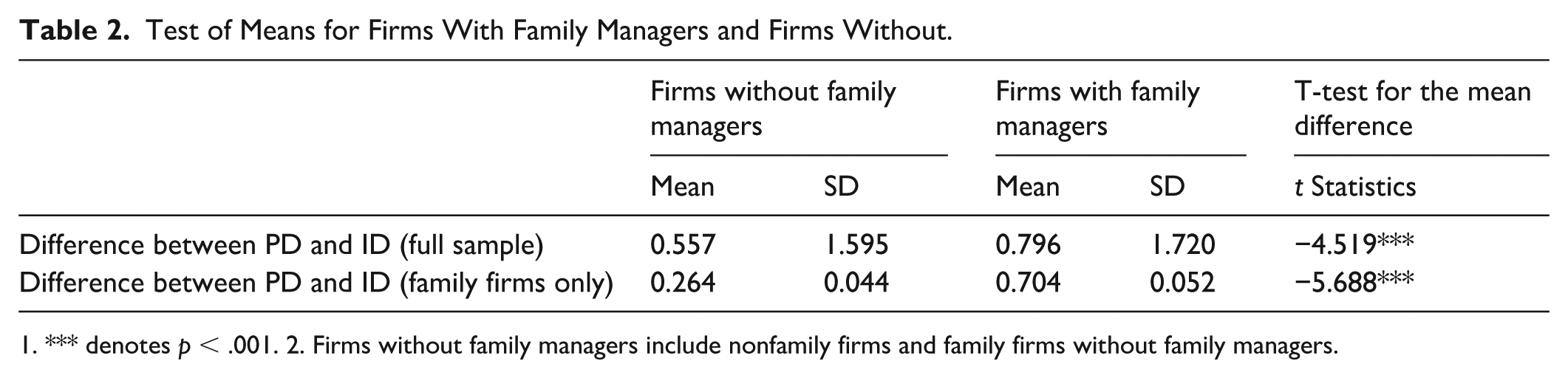

The top row of Table 2 presents the summary statistics of the difference between PD and ID in the full sample, which includes family firms with at least one family manager (excluding lone founder firms) and family and nonfamily firms without any family managers. We compare these two groups of firms with a t-test. The t-statistic of the mean difference of the difference between PD and ID for firms without family managers (i.e., nonfamily firms) and those with family managers (i.e., family firms) is negative and significant (t statistic = −4.519, p = .000). This result is consistent with H1, which predicts that firms with more family managers engage in more product diversification than international diversification compared to firms with fewer family managers. The bottom row of Table 2 shows the summary statistics of the difference between PD and ID in the subsample of family firms with at least one family manager and family firms without any family managers (i.e., only family owners and/or directors). We compare these two groups of family firms with a t-test. The result is consistent with H1 (t statistic = −5.688, p = .000), suggesting that the inclusion of family managers push family firms toward product diversification rather than international diversification. In an unreported analysis, we find insignificant results for the two-sample t-test of the difference between PD and ID between family firms (excluding lone founder firms) and nonfamily firms (t statistic = 0.677, p = .498). The results of these t-tests provide evidence that supports our approach of examining the influence of family managers from that of nonfamily managers in studying firms’ diversification choices.

Test of Means for Firms With Family Managers and Firms Without.

1. *** denotes p < .001. 2. Firms without family managers include nonfamily firms and family firms without family managers.

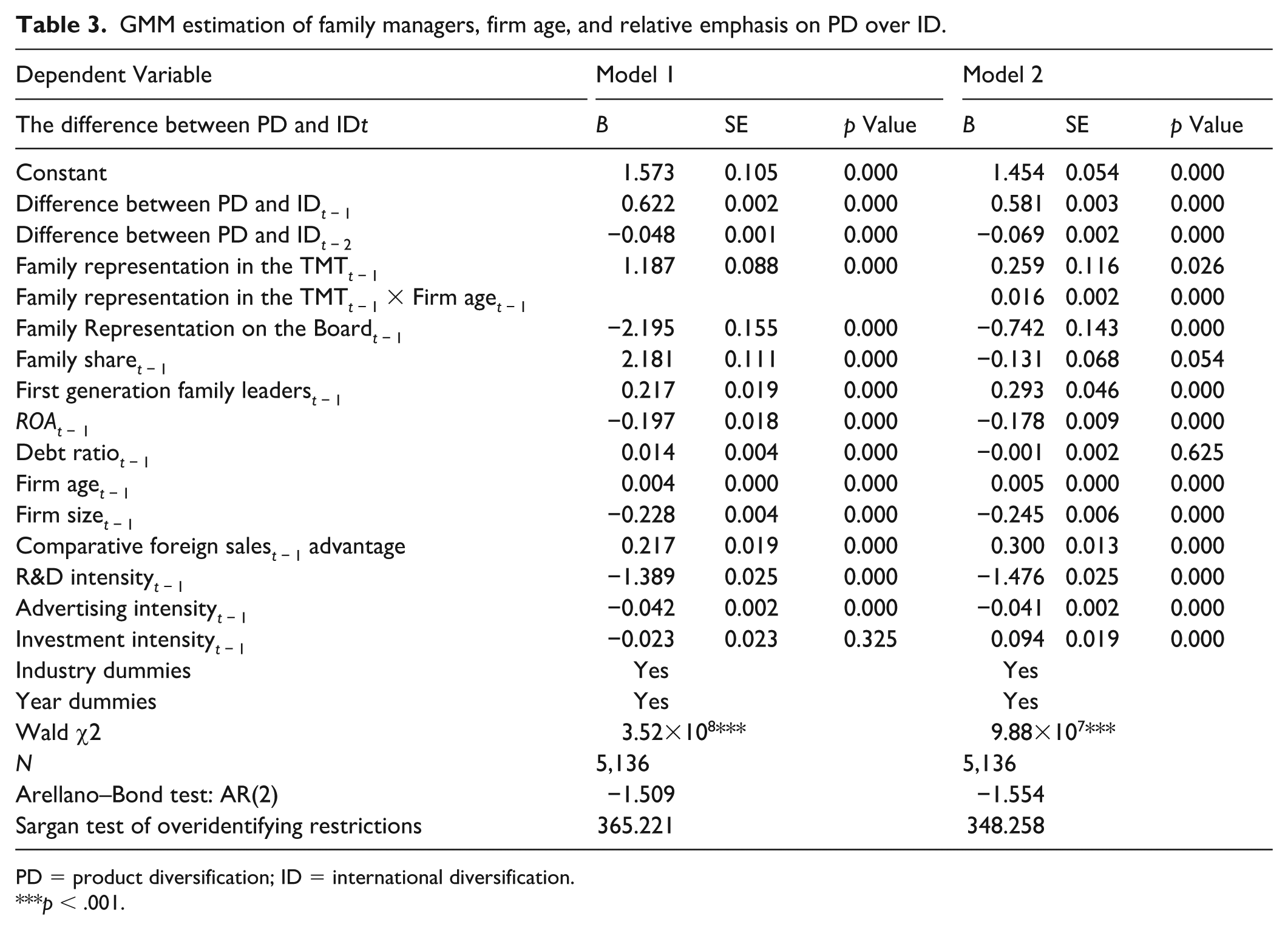

Table 3 documents the results of our dynamic panel data analysis using the GMM procedure. Model 1 offers strong support for H1 as the coefficient of family representation in the TMT is positive and statistically significant (β = 1.187, p = .000). The result shows that the representation of family managers in the TMT has a significantly positive effect on the difference between a firm’s product diversification and international diversification, suggesting that as the representation of family managers increases, the firm is more likely to prefer product over international diversification. Model 2 provides evidence supporting H2, which tests the moderating effect of firm age on the main effect of family representation in the TMT on a firm’s diversification choice. The result shows that this moderating effect is significant (β = 0.016, p = .000), suggesting that the positive effect of family managers on a firm’s tendency to engage in product diversification over international diversification is stronger in older firms.

GMM estimation of family managers, firm age, and relative emphasis on PD over ID.

PD = product diversification; ID = international diversification.

p < .001.

Endogeneity Tests

We conduct several tests to evaluate whether our two-step system GMM approach mitigates the potential problems of endogeneity, heteroskedasticity, and autocorrelation. First, we perform the Arellano-Bond test for autocorrelation (Arellano & Bond, 1991). As shown in Table 3, the AR(2) z scores, which are results of the Arellano-Bond tests for second-order autocorrelation in first differences, are insignificant for Models 1 and 2. The second-order autocorrelation evaluates whether the lags of the dependent variable used as the instruments are endogenous (Roodman, 2009). The tests reveal no such problem in our models. By failing to reject the null hypothesis in this test, we show that our models do not suffer from second-order autocorrelation (Roodman, 2009).

We further conduct the Sargan test of the overidentifying restrictions (Arellano & Bond, 1991). The χ2 reported in Table 3 fails to reject the null hypothesis. This shows that our models do not suffer from the overidentification problem for instrumental variables. In other words, the test results suggest that our models do not include excessive instrumental variables, which may result in biased estimates.

In summary, we do not have autocorrelation in the first-differenced errors, and our instruments satisfy the standard validity criterion. We thus conclude that our model specifications yield valid results by sufficiently addressing the potential problems of sample selection, autocorrelation, heteroskedasticity, and endogeneity.

Robustness Tests

We conduct robust tests to examine whether our main results hold if we adopt alternative empirical approaches, different samples, and revised variable constructs. First, we explore whether our main results are robust to alternative empirical approaches. We rerun tests for H1 and H2 with the same xtdpdsys command in STATA but utilize the one-step estimator instead of the two-step estimator and calculate the robust standard errors to address potential heteroskedasticity. In unreported analyses, family representation in the TMT has a positive and statistically significant relationship with the difference between PD and ID (β = 1.000, p = .049), providing support for H1. In support of H2, the coefficient of family representation in the TMT × firm age is positive and statistically significant (β = 0.040, p = .039).

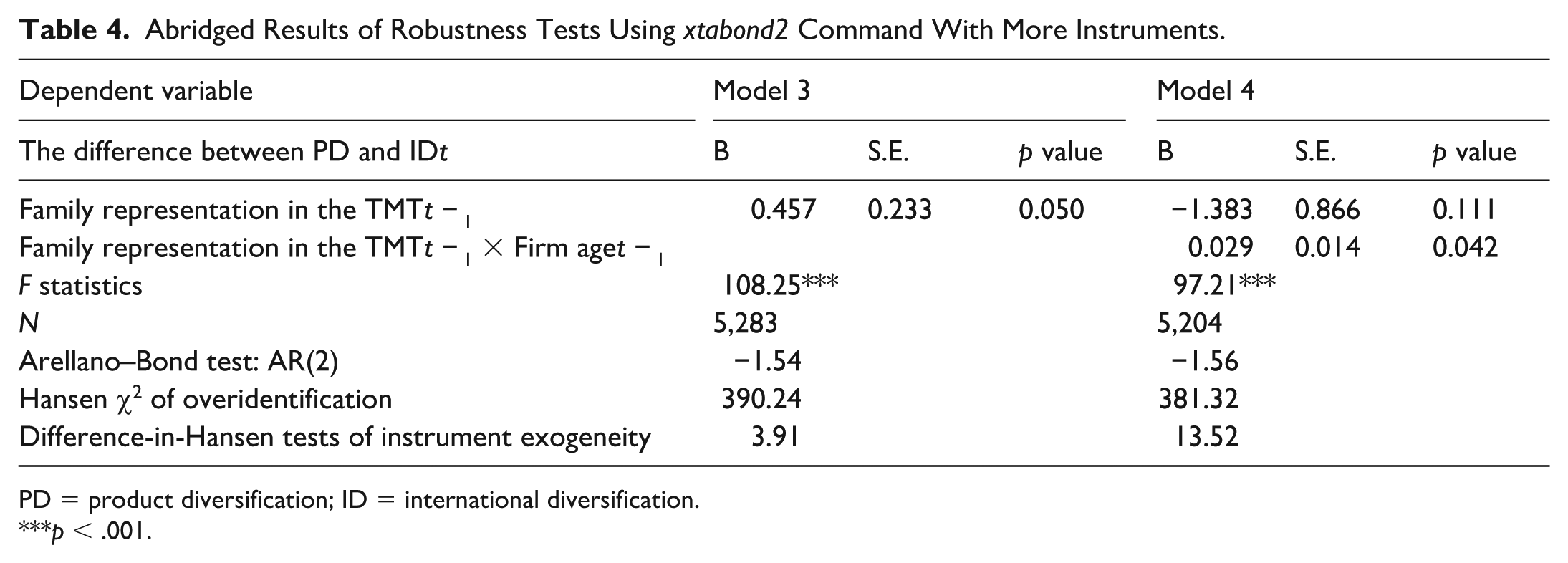

We further employ the xtabond2 command in STATA (Roodman, 2009) with the two-step and the robust standard error options for the system GMM estimators to retest H1 and H2. In addition to the instruments in

Table 4 shows abridged results of the analyses discussed above. Model 3 confirms the positive relationship between family representation in the TMT and the difference between PD and ID (β = 0.457, p = .050). Furthermore, family representation in the TMT × firm age is positively related to the difference between PD and ID (β = 0.029, p = .042) in Model 4. These results offer additional evidence that supports the robustness of our main findings. We also find that the AR(2) z scores are not significant (Roodman, 2009) in our models, which means our models do not suffer from second-order autocorrelation. Likewise, the Hansen χ2 of overidentification that we derive fails to reject the null hypothesis that our models do not suffer from the overidentification problem for instrumental variables. Finally, we cannot reject the null hypothesis that the moment restrictions in our models are valid and that the instruments are exogenous after we perform the difference-in-Hansen tests for the exogeneity of the instruments (Roodman, 2009).

Abridged Results of Robustness Tests Using xtabond2 Command With More Instruments.

PD = product diversification; ID = international diversification.

p < .001.

Next, we examine whether our results are robust to different sample selections in three ways. We start by including lone founder firms in the analysis, which increases our sample size from 5,148 to 5,617. We control for the impact of a lone founder by adopting a dummy variable which is equal to 1 for the lone founder firm, and 0 otherwise. In unreported reruns of Models 3 and 4 discussed above, we find results very consistent with what we reported in Table 4.

We also rerun tests for H1 and H2 with the same xtdpdsys command in STATA but utilize the one-step estimator and calculate the robust standard errors on a subsample of family firms, which reduces the sample size from 5,148 to 944. The unreported results find support for H1 as the coefficient of family representation in the TMTt − 1 is positive and significant (β = 0.817, p = .016); but H2 does not receive support as the coefficient of family representation in the TMTt − 1 × firm aget − 1 is not significant (β = 0.011, p = .552).

To further check the robustness of our findings regarding H1 and H2 in the subsample of family firms, we construct a dummy variable (i.e., family manager dummy), which represents whether a firm has family managers in the TMT or not. Substituting family manager dummyt − 1 for family representation in the TMTt − 1, we employ the same empirical approach discussed above to analyze the subsample of family firms. In unreported analyses, the family manager dummyt − 1 is significantly and positively related with the difference between PD and ID (β = 0.299, p = .009); the interaction between family manager dummyt − 1 and firm aget − 1 is positive and significant too (β = 0.005, p = .050). We find these results consistent with H1 and H2 because family firms conduct more product diversification than international diversification when there is family representation in the TMT and this effect is stronger as firms age.

Finally, we employ a two-pronged approach to verify whether our analyses and results are robust to alternative constructions of the dependent variable which measures the difference between product and international diversification. We first adopt another approach to measure the difference between PD and ID. Specifically, for every year t, we recode difference between PD and ID as 1 if noncore business sales are larger than foreign sales; we assign difference between PD and ID as 0 if noncore business sales are the same as foreign sales; we code the difference between PD and ID as −1 if noncore business sales are less than foreign sales. Using the recoded difference between PD and ID, we again employ the xtabond2 command in STATA (Roodman, 2009) with the two-step and the robust standard error options for the system GMM estimators to retest H1 and H2. In unreported analyses, we confirm H1 but not H2. The coefficient of family representation in the TMT is positive and significant (β = 0.419, p = .042), but the coefficient of family representation in the TMT × firm age is not significant (β = −0.006, p = .287).

We next follow S. C. Chang and Wang (2007) by employing a Herfindahl-index-based approach to reconstruct our dependent variable, relative emphasis on product diversification (PD) over international diversification (ID). 6 For product diversification, we calculate the Herfindahl-index of all 2-digit-SIC-code level sales percentage for every firm and year (i.e., Herfindahl Index product). For international diversification, we group international markets into five regions (i.e., Africa, Asia and Pacific, Europe, Americas, and Other Markets) and then calculate the Herfindahl-index of regional level sales percentage for every firm and year (i.e., Herfindahl Index international). We reverse-code both the Herfindahl Index product (1 − Herfindahl Index product) and Herfindahl Index international (1 − Herfindahl Index product) variables so that higher values of the indices represent greater diversification. We take the difference between the reverse-coded Herfindahl Index product and Herfindahl Index international as the alternative dependent variable, that is, Herfindahl index difference between PD and ID. We substitute Herfindahl index difference between PD and ID for difference between PD and ID and rerun Model 1 and Model 2 with the same xtdpdsys command in STATA. In unreported analyses, family representation in the TMT has a positive and statistically significant relationship with the Herfindahl index difference between PD and ID (β = 0.252, p = .000), providing support for H1. In the test of H2, we find the coefficient of family representation in the TMT × firm age to be positive and statistically significant (β = 0.001, p = .000), providing further support for H2. 7

In sum, the combined results of the main tests and robustness analyses show that our findings are largely robust to alternative empirical approaches, different sample selections, and revised variable definitions. H1 is supported in every test and H2 is supported in over 60% of the robustness tests conducted.

Supplemental Tests

Based on Lee et al. (1980), we adopt Heckman’s (1979) two-stage technique to test our hypotheses after controlling for potential selection bias. We first estimate a probit model in which a variable representing family firms (=1) versus nonfamily firms (=0) was regressed against the two instrumental variables (i.e., family firms’ fraction of sales by industry and family firms’ fraction of capital expenditure by industry) and other controls, including nonfamily block holder ownership, firm age, firm size, debt ratio, firm performance, advertising intensity, investment intensity, family trust holdings, and firm prior diversification experience (Anderson & Reeb, 2003). Based on the first-stage regression, we calculated the inverse Mills ratio and included it in our second-stage models used to test our hypotheses.

In the second stage, we employ a firm fixed effects model to address the potential unobserved heterogeneity issue (Certo & Semadeni, 2006; Hsiao, 1985). We conducted Hausman tests (Hausman & Taylor, 1981) that confirmed the superiority of the fixed effects model over the random effects model (p < .001). Accordingly, all analyses were estimated using the xtreg STATA command with the fixed-effects option (fe). The Wooldridge test (Wooldridge, 2002) and the Breusch-Pagan test (Breusch & Pagan, 1979) provided evidence of serial correlation and heteroskedasticity in our panel dataset. To control for these problems, we estimated robust standard errors using the Huber-White sandwich estimator clustered at the firm level (White, 1980). We examined the correlation matrix of the coefficients for multicollinearity in the xtreg model using the estat vce, corr STATA command. 8 We use the threshold of 0.6 correlation recommended by Allison (1999). The results obtained were well below 0.6, indicating that multicollinearity is not a major concern. In unreported analyses, our post hoc tests find that the results of Heckman’s two-stage analyses are consistent with our main findings. 9

Discussion

Research on corporate diversification spans over five decades and remains one of the most studied topics in the strategy literature (Kang, 2013; Ramanujam & Varadarajan, 1989; Rawley, 2010; Sakhartov, 2024). Product diversification and international diversification represent two dimensions by which firms can expand their scope of operations. There is a growing body of research examining the relationship between family involvement and firms’ diversification decisions, yielding important insights (Hafner, 2021; Hafner & Pidun, 2022). For example, family governance is generally found to have a negative effect on diversification, which has largely been attributed to family principals’ desire to preserve SEW (Gómez-Mejía et al., 2010; Muñoz-Bullon et al., 2018). Despite this important insight, prior research has largely treated product diversification and international diversification as separate phenomena (Hafner, 2021). Given that firms often pursue both forms of diversification simultaneously, yet face challenges in managing them (Mayer et al., 2015), it is important to investigate the influence of family involvement on a firm’s relative emphasis on these two forms of diversification.

To this end, we examine the role of family management in shaping a firm’s relative emphasis between these dimensions of diversification. The vital role of the top management team in shaping firm strategy has been widely underscored in the strategy literature (Carpenter et al., 2004; Krause et al., 2022). In family firms, family managers are the central coalition of the TMT, directing the firm’s attention toward family-centered noneconomic goals and playing a pivotal role in strategic decision-making (Daspit et al., 2018; Duran et al., 2016; Liang et al., 2014; Sharma et al., 2020; Singla et al., 2014). Building on the SEW literature (De Massis et al., 2014; Nason et al., 2019), this study investigates the effect of family management on a firm’s diversification choice. We argue that the representation of family managers in the TMT is positively related to a firm’s emphasis on product diversification which is more conductive to family influence and control than international diversification. We also expect that the positive effect of family managers is stronger in older firms because restricted SEW, which is associated with the direct benefits of strategic initiatives for the family, is expected to be more important as the firm ages. Our hypotheses receive support from an analysis of S&P 1,500 firms between 1998 and 2017.

This study makes several important contributions to the diversification and family business literature. First, while the extant literature generally shows that family governance has a negative effect on diversification (Gómez-Mejía et al., 2010; Hafner, 2021; Hafner & Pidun, 2022; Schierstedt et al., 2020), most prior research has studied product and international diversification separately. The question regarding the effect of family governance in general, and family management in particular, on a firm’s preference for one diversification form over the other remains unanswered. By jointly examining product and international diversification and identifying conditions under which family management favors one over the other, this study deepens our theoretical understanding of the effect of family management on a firm’s diversification choice in alignment with their non-economic priorities.

Second, this study contributes to the SEW literature by highlighting the importance of preserving restricted SEW in explaining the influence of family management on a firm’s preference for product over international diversification. We draw upon the SEW literature to show that family managers’ strategic decision-making is influenced by the preservation of restricted SEW. Our study shows that family managers prefer product diversification because international diversification is likely to impose greater threats to restricted SEW, particularly the preservation of centralized family control. This finding also challenges the prevailing narrative that family involvement leads to a uniformly conservative or risk-averse strategic orientation. Instead, our study illustrates that family managers engage in selective diversification, making strategic decisions that align with SEW preservation that benefits family owners. This behavior reflects calculated prioritization rather than generalized pursuit with respect to SEW preservation. This more nuanced perspective moves the literature beyond binary categorizations of family governance as simply risk-averse or risk-taking, and toward a richer understanding of their influence on a firm’s strategic distinctiveness.

Third, while the temporal dimension of family influence has emerged as an important theme in recent research (Hsueh et al., 2023; Nason et al., 2019; Swab et al., 2020), the way firm age shapes family managers’ strategic decision-making remains underexplored (Boers et al., 2017). Building on this theme, our findings demonstrate that firm age strengthens the relationship between family management and diversification choices. This study therefore extends our knowledge of the temporal dimension of family influence by showing how SEW priorities evolve over time (De Massis et al., 2014; H. E. Lin et al., 2023; Sharma et al., 2014) and highlighting that the salience of restricted SEW in strategic decision-making intensifies as family values and traditions become more deeply embedded in the firm.

This study offers several important practical implications for family businesses. The findings indicate that while both product and international diversification are critical for growth and long-term success, the presence of family members in the TMT is associated with a stronger preference for product diversification over international diversification. This suggests that family management may constrain the extent of international expansion. Family owners and managers should recognize this strategic constraint and proactively approach both product and international diversification. While product diversification may align more closely with the preservation of restricted SEW, an overly conservative stance toward international diversification may hinder global growth opportunities and consequently hinder the opportunities for the development and preservation of extended SEW (Miller & Le Breton-Miller, 2014).

This study also reveals that the positive impact of family management on the preference for product diversification is stronger in older firms. This suggests that over time, deeply rooted family identities and a desire to preserve restricted SEW can reinforce strategic conservatism, further reducing the likelihood of engaging in international diversification. Managers of older family firms should be particularly mindful of this constraint, as it may restrict the firm’s ability to respond to global market pressures. For family firms seeking to expand internationally, these findings underscore the potential constraint posed by family-dominated management, especially in older firms. Such firms may benefit from hiring nonfamily managers who bring greater openness to internationalization and expertise in global markets.

Limitations and Future Research Opportunities

This study has several limitations that represent opportunities for future research. To test our hypotheses, we used a sample of publicly traded manufacturing firms drawn from secondary data on firms in the S&P 1,500 index for fiscal years 1998 to 2017. These firms are quite diverse, particularly in terms of size. Although the restrictions we imposed on our sampling frames render the assessment of the effect of family management on a firm’s diversification choice more reliable, future research using other samples is warranted since our use of secondary data may create measurement problems and our results may not generalize to private firms, smaller firms, or those operating in non-manufacturing industries. Given that family firms are embedded in institutional environments and influenced by legal and political aspects of these environments (Daspit et al., 2024; Skorodziyevskiy, Sherlock et al., 2024), future research is encouraged to examine family firms across different national contexts to gain a better understanding of the impact of family management on a firm’s diversification choices.

We used an involvement rather than an essence approach in defining family firms. This approach limits the possibility of capturing the essence of family influence and measuring goals and SEW directly. In addition, due to the limitations inherent in secondary data, we were unable to directly observe the evolving nature of SEW preservation. Therefore, future research should aim to more effectively capture FCNE goals and SEW through primary data collection. Furthermore, employing more rigorous methods to measure diversification, such as machine learning-based techniques (Choi et al., 2021), could enhance the precision of the analysis.

In addition, while our study examines the moderating role of firm age, we acknowledge that firm age, as a broad construct, may encompass multiple reinforcing processes, including the entrenchment of family identity, heightened stakeholder visibility, and organizational inertia. Future research could decompose the effects associated with firm age by measuring these specific mechanisms directly. Relatedly, data on the tenure of family managers was not systematically available in our dataset. Given that the duration of family managers’ involvement in the TMT may independently shape diversification preferences, future research with access to data on executive tenure could provide a more fine-grained understanding of how the accumulation of influence of family managers over time.

In this study, we examine the impact of family management on a firm’s diversification choices by focusing on restricted SEW, particularly the preservation of family control over firm decision-making. However, SEW as a reference point encompasses multiple goals of the family. Future research could examine the influence of other dimensions of SEW, as well as the dynamic interactions of financial and SEW considerations in shaping a firm’s diversification choices. In addition, a firm’s product diversification consists of related and unrelated diversification and international diversification entails various modes of foreign market entry. Future research can be expanded to investigate the influence of family representation on a firm’s choice between related and unrelated product diversification and different types of foreign entry modes.

Given the significance of the TMT and family management as the central “faction” within the TMT (Gómez-Mejía et al., 2018), this study focuses on examining the impact of family management on a firm’s preference for product versus international diversification. Future research could explore how other aspects of family governance, such as family ownership or family representation on the board, influence diversification decisions. In addition, given the crucial role of the CEO within a TMT and in line with prior literature, which typically includes CEOs as part of the TMT (Krause et al., 2022), we include family CEO as part of the measure for family management. While there is ongoing debate about whether the CEO should be considered part of the TMT (Krause et al., 2022), future research should explore the potentially distinct impacts of a family CEO versus a nonfamily CEO on a firm’s diversification choices. The willingness and ability of a family CEO have important implications for the strategies to achieve FCNE goals and preserve SEW (Skorodziyevskiy, Chandler, et al., 2024).

Finally, the financial impact of firm diversification is another central area of research in the diversification literature (e.g., Feldman et al., 2016; Hafner, 2021; Zahra et al., 2000). Future work can examine the financial implications of firms’ preferences for product over international diversification. Is the preference for product diversification likely to lead to better financial performance? Do firms survive longer because of the preference for product over international diversification? Does family representation in the TMT influence firms’ choice between related and unrelated product diversification and even different types of foreign sales? Corporate social performance outcomes of family firm diversification represent another promising avenue for future research (Kang, 2013), and one that may affect or be affected by preferences for product over international diversification.

Conclusion

Building on the SEW literature and the research on the impact of family involvement and control over time, this study explores the influence of family management on a firm’s preference for product versus international diversification. We theorize and find that family management has a positive effect on a firm’s preference for product diversification, with this effect becoming more pronounced as firms age. Our research extends our knowledge of the implications of the preservation of restricted SEW for a firm’s diversification choices, as well as the contingent effect of firm age on family managers’ diversification preferences.

Footnotes

Appendix

Yearly Distribution of Firms Regarding Product and International Diversification.

| Product diversification | International diversification | Product and international diversification | |||||

|---|---|---|---|---|---|---|---|

| Year | No | Yes | No | Yes | No | Yes | Total |

| 1998 | 145 | 215 | 82 | 278 | 177 | 183 | 360 |

| 1999 | 122 | 252 | 17 | 357 | 128 | 246 | 374 |

| 2000 | 119 | 270 | 4 | 385 | 121 | 268 | 389 |

| 2001 | 119 | 283 | 10 | 392 | 126 | 276 | 402 |

| 2002 | 124 | 285 | 8 | 401 | 129 | 280 | 409 |

| 2003 | 118 | 300 | 8 | 410 | 124 | 294 | 418 |

| 2004 | 122 | 311 | 6 | 427 | 126 | 307 | 433 |

| 2005 | 116 | 314 | 4 | 426 | 120 | 310 | 430 |

| 2006 | 120 | 314 | 7 | 427 | 127 | 307 | 434 |

| 2007 | 122 | 322 | 7 | 437 | 127 | 317 | 444 |

| 2008 | 121 | 334 | 6 | 449 | 126 | 329 | 455 |

| 2009 | 128 | 334 | 4 | 458 | 132 | 330 | 462 |

| 2010 | 136 | 344 | 3 | 477 | 139 | 341 | 480 |

| 2011 | 133 | 354 | 1 | 486 | 134 | 353 | 487 |

| 2012 | 131 | 367 | 4 | 494 | 135 | 363 | 498 |

| 2013 | 137 | 373 | 4 | 506 | 139 | 371 | 510 |

| 2014 | 148 | 376 | 2 | 522 | 149 | 375 | 524 |

| 2015 | 147 | 388 | 2 | 533 | 148 | 387 | 535 |

| 2016 | 154 | 390 | 2 | 542 | 155 | 389 | 544 |

| 2017 | 142 | 351 | 3 | 490 | 144 | 349 | 493 |

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.