Abstract

Single-family offices are increasingly important actors in impact investing, yet little is known about how they translate impact intentions into desired outcomes after investing. Drawing on the socioemotional wealth perspective, we conduct an abductive qualitative study based on a dual perspective of nine single-family offices and eight portfolio companies. We identify four impact intention translation strategies, three barriers, and two enabling mechanisms. Building on these findings, we develop a typology of four impact translation logics—hands-on controllers, embedded stewards, relational investors, and formalized partners—that explains heterogeneity in how family-based priorities and intentions shape impact translation.

Keywords

Introduction

How do single-family offices (henceforth SFOs) with a focus on impact investments translate their non-financial impact intentions into desired outcomes within their portfolio companies? What are the barriers and enablers encountered in pursuing this translation? Answering these questions matters since translating impact intentions into outcomes when investing in ventures with purposes extending beyond financial value creation is particularly challenging in the SFO context. This is because impact investing often involves long-term horizons, uncertain measurement, and tensions between financial discipline and social ambition. For SFOs, these challenges intersect with family-specific priorities such as preserving control, protecting legacy, maintaining trusted relationships, and avoiding reputational loss. As a result, the pursuit of impact is rarely a purely technical investment decision. Yet existing research offers limited insight into how family-based considerations shape what SFOs do once they invest and how they translate their impact investment strategies into desired outcomes (Hayoz et al., 2025; Rivo-López et al., 2017, 2021; Schickinger et al., 2023). This is a problem because family business research has repeatedly documented that business families seek to support ventures with purposes that extend beyond financial profits, including sustainable financing, social entrepreneurship and impact investing (e.g., Ferreira et al., 2021; Häußler & Ulrich, 2024; Randolph et al., 2022), while research on impact investing still predominantly focuses on financial performance, trade-offs, or investor motivations (e.g., Agrawal & Hockerts, 2021; Barber et al., 2021; Markman et al., 2019).

Indeed, the lack of attention to how impact investing intentions are translated into outcomes in portfolio companies leaves an important gap, particularly given that impact investing aims to actively deploy capital to solve societal and environmental problems, sometimes at the expense of short-term financial returns (Brest & Born, 2013). This gap is especially salient in the private capital market, where SFOs are rapidly becoming central actors (Block et al., 2024; Schickinger et al., 2022; Zellweger & Kammerlander, 2015). Unlike public capital markets, private investors are better positioned to tolerate market imperfections and longer time horizons, making SFOs important providers of patient capital for impact ventures (Bierl & Kammerlander, 2019; Brest & Born, 2013; Kenyon-Rouvinez & Park, 2020). As a unique form of family enterprise, many SFOs serve a business family and emphasize long-term orientation, leading to goal setting that can align well with actions for social and sustainable development in addition to financial wealth creation (De Massis et al., 2021; Needham & Harvey, 2020; Sun et al., 2023). Often driven by next-generation members and by an increase in public awareness of the issue, SFOs’ intention to impact society has increasingly been directed toward impact investing specifically (“Family Offices: Global Landscape and Key Trends,” 2020; PwC, 2025; Samuelson et al., 2021). But even if there is some research on the general financial outcomes of impact investing to determine whether it provides competitive financial performance (Barber et al., 2021; Berk & Van Binsbergen, 2025; Bugg-Levine & Emerson, 2011), we know little about how SFOs move from articulated impact investing intentions to the realization of impact within portfolio companies.

The purpose of this article is to address this gap and to extend our understanding of how SFOs translate their impact investing intentions into desired outcomes in the companies in which they invest. In doing so, we embrace the perspectives of both the SFOs and the impact portfolio companies. Such a dual perspective is important because translating the impact intention of the SFO into the desired outcomes produced by the venture involves not only the intentions and strategies of the SFO, but also the perceived ability of the impact venture entrepreneurs to deliver the outcome. The dual perspective also enables us to explore potential tensions in the expectation-realization relationship between the SFO and the portfolio company that may play a role in the translation of impact intention at the SFO into desired outcomes by the venture.

Conceptually, we draw on the socioemotional wealth (SEW) perspective as our theoretical lens (Gómez-Mejía et al., 2007) and the FIBER framework and its five dimensions (Berrone et al., 2010) as a sensitizing framework through which we study it empirically. SEW provides a well-established framework for understanding how family enterprises balance financial and non-financial goals over time (Berrone et al., 2012; Calabrò et al., 2026; Murphy et al., 2019; Naldi et al., 2024). However, while SEW has been widely applied to family firms, we are yet to explore how SFOs mobilize SEW dimensions as they pursue strategies such as impact investing (Hayoz et al., 2025; Schickinger et al., 2023). What tends to make SFOs different compared to other types of family enterprises is the focus on investing in diversified asset classes and on providing support services to a specific business family rather than managing an operative business (Zellweger & Kammerlander, 2015). Given that most SFOs have a close relationship with an owner-family and are set up with the often-sole purpose of serving this specific family, SEW is a particularly relevant perspective to understand their strategic behaviors. SEW offers a sharp focus on the family-based non-financial goals that SFOs are set up to protect, such as family identity, legacy, privacy, and cohesion, in addition to financial investments (Bettinelli, Lissana, et al., 2022; Bettinelli, Mismetti, et al., 2022; Krüger et al., 2025). In comparison, for instance, stewardship theory emphasizes pro-organizational behavior and alignments between, for example, principals and agents or investors and ventures, while institutional logics foreground norms at the field level, such as a market or an industry and hybrid organization theory is relevant to study the potential internal hybrid nature of SFO as organizations, while our focus is at the level of the SFO and the relation with the portfolio company in which it invests.

Empirically, we rely on an abductive qualitative study drawing on the dual perspective of nine SFOs and eight portfolio companies in Northern and Western Europe. We define SFOs formally as a private family enterprise that invests in multiple businesses (Zellweger & Kammerlander, 2015), thereby including private family-owned investment firms, instead of limiting SFOs to organizational setups for family wealth management and preservation (Rosplock & Welsh, 2012).

Our study makes two main theoretical contributions. First, we contribute to research on SFOs and impact investing by developing a typology of SFO impact translation logics that takes into account heterogeneity in how SFOs translate impact intentions into outcomes in portfolio companies. Building on our identification of four impact translation strategies, three barriers, and two enabling mechanisms, the SFO typology illustrates how different combinations of ownership/control and formality shape the translation process. In doing so, we move beyond whether SFOs pursue impact or not to further our understanding of how they seek to realize impact through value alignment, governance structures, relational operations, and active ownership involvement.

Second, we contribute to the SEW literature by extending our knowledge on how family-based non-financial priorities matter at the SFO–portfolio company interface before and after an investment. More specifically, using FIBER as a sensitizing framework, we illustrate how SEW dimensions play out in multi-firm investment structures such as SFOs. This extends the SEW literature beyond traditional operating family firms and offers new insights regarding the way family control, identification, binding social ties, emotional attachment, and renewal can both enable and constrain the translation of impact intentions into desired outcomes.

Taken together, these theoretical contributions are important because they enhance our understanding of how the values and impact ambitions of the owner families behind the SFOs are turned into actual investment decisions, governance practices, and intended societal impact. They also address the current lack of explanations in the literature regarding why SFOs with similar intentions might differ in their realized outcomes. The typology extends the limited knowledge on SFOs by offering a conceptual categorization of approaches an SFO takes when seeking to translate non-financial impact intentions into desired outcomes. In terms of practice, this contribution implies that owners and executives in SFOs can use the typology as a tool to assess whether their current impact approach fits their ambitions based on the values and intentions of the owner family.

Prior Research and Guiding Theory

SFOs and Impact Investing

Within family business research, SFOs remain an under-researched area and there is no universally accepted definition of SFOs (Rivo-López et al., 2021; Rosplock & Welsh, 2012), even if a SFO is often seen as “a corporate structure owned by a single family and primarily dedicated to the management of family assets and the fulfillment of individual and tailored needs of family members” (Schickinger et al., 2023:1). In addition to the management of assets, investing strategies and family services, research highlights the strategic importance of SFOs for long-term succession planning, and preservation of family identity distinguishing them from other investment entities (Block et al., 2019; Krüger et al., 2025; Rosplock & Welsh, 2012). While the population of SFOs is diverse, ranging from highly institutionalized structures with varying degrees of owner-family involvement to more informal organizational setups (Block et al., 2024), we focus on SFOs with high to relatively high owner-family involvement and that serve to balance and consolidate the financial and non-financial goals of a single family (Schickinger et al., 2023; Welsh et al., 2013; Zellweger & Kammerlander, 2015). Given our research questions, a focus on SFOs with a high level of family involvement is particularly relevant because these SFOs most clearly reflect the intentions, values, and strategic priorities of the owning family. In contrast to SFOs with less family involvement and that might be primarily managed by non-family executives and managers, SFOs with high family involvement allow us to better observe how the family-specific motives in focus in the SEW perspective influence impact investing intentions and decision-making.

Recent studies suggest that SFOs can be seen as a type of family enterprise and that concepts and theories applicable to the broader family business field are relevant in understanding the behavior and strategies of SFOs (Cruz et al., 2021; Welsh et al., 2013; Wetter & Nordqvist, 2024). In this vein, Hayoz et al. (2025) provide the most comprehensive review of the SFO literature to date and explicitly call for more research into how SFOs organize and pursue impact investing. We suggest that impact investing is relevant in the SFO setting since, like other types of family enterprises, SFOs are guided by business goals—financially oriented—as well as family goals—which are often non-financial and relate to maintaining family control, family harmony, reputation and emotional capital (Kotlar & De Massis, 2013; Schickinger et al., 2022). These non-financial goals typically aim to secure a long-term orientation, concern for employees and the local community, as well as engagement in the broader society (Dyer, 2003; Zellweger et al., 2013). For instance, research indicates that the more a family identifies with their firm, the more likely they are to adopt non-financial goals in addition to financial goals (Cabrera-Suárez et al., 2014; Schulze et al., 2001). Family business research has shown that these affective and social goals can promote engagement in business activities and efforts that support social and sustainable development, such as impact investing (Clauß et al., 2022; Ferreira et al., 2021; Mariani et al., 2023; Mismetti et al., 2025).

As an investment strategy in new ventures that have a purpose to achieve social, civic or sustainable development and betterment while delivering financial returns (ter Braak-Forstinger & Selian, 2020), impact investing gained prominence after the 2007 to 2008 financial crisis as companies began directing capital toward sustainability and socially relevant projects (Agrawal & Hockerts, 2021). Quinn and Munir (2017: 117) encapsulate these developments in their definition, which we adopt in this study: “Impact investing refers to the use of investment capital to help solve social- or environmental problems around the world with the expectation of financial returns.” Recently, impact investing has received more attention among investment companies, such as SFOs, active in the private markets compared to the public markets, where competitive financial returns are typically expected (Brest & Born, 2013). Existing literature observes that while there is significant interest in impact investing within SFOs (Hayoz et al., 2025; Schickinger et al., 2023; Wessel et al., 2014), there is a dearth of research into how SFOs invest in impact ventures and act to achieve their desired outcomes (e.g., Hayoz et al., 2025; ter Braak-Forstinger & Selian, 2020). In this article, we set out to investigate this with a focus on the strategies that SFOs pursue to translate their non-financial impact into desired outcomes within their portfolio companies, as well as the barriers and enablers in this process. To examine this, we are conceptually guided by the SEW perspective and its influential operationalization through the FIBER framework (Berrone et al., 2012).

Socioemotional Wealth and FIBER

Rooted in behavioral theory, the SEW perspective posits that many family-owned businesses are prepared to sacrifice financial performance to preserve their family’s non-financial, affect-related value from owning and controlling the firm (Gómez-Mejía et al., 2007). SEW encompasses family-centered goals such as maintaining control and influence, preserving family identity and legacy, sustaining trusted social relationships, and ensuring continuity across generations (Calabrò et al., 2026; Murphy et al., 2019). Scholars have used the SEW perspective to understand what drives business families’ engagement in society and sustainability (Berrone et al., 2010), offering insights into their varying motivations for seeking impact beyond financial value creation and through sustainable actions (Åberg et al., 2025; Herrero et al., 2024; Kammerlander, 2022). Since we focus on SFOs with high to relatively high involvement of the owner-family that are set up to serve a specific family and its long-term goals and vision, SEW is a particularly relevant theoretical framework. For instance, De Massis et al. (2021) suggest that this type of SFO tends to be set up to respond to family needs and to maintain transgenerational control over the financial, human, and SEW of the family.

In this study, we use SEW as the theoretical perspective and FIBER as the sensitizing framework through which we examine and operationalize which family-based non-financial priorities become salient in SFO impact translation. We rely on Hayoz et al. (2025, p. 8), who suggest that scholars should draw on the SEW perspective and the dimensions offered by the FIBER to identify “emerging patterns” that can provide “valuable insights to guide the SFOs in meeting the family’s expectations.” With the intention to provide what could become an operationalization of SEW, Berrone et al. (2012) developed the FIBER framework. In comparison with the original definition of SEW (Gómez-Mejía et al., 2007), this framework allows for a more granular and direct investigation of different SEW subdimensions, consisting of five distinct components: (F) Family Control & Influence, emphasizing the family’s effort to retain control and influence over the business, either through direct roles such as CEO or chairman or by influencing these appointments; (I) Identification with the Firm, focusing on how family members align their identity with that of the firm, which is often manifested when the business bears the family name; (B) Binding Social Ties, highlighting the significant social networks and bonds that family businesses cultivate, extending beyond mere economic interactions to foster deep social bonds and trust with various stakeholders; (E) Emotional Attachment, exploring the range of emotions family members experience through their involvement in the business, deeply influencing strategic decisions; (R) Renewal of Family Bonds through Dynastic Succession, reflecting the family’s desire to perpetuate its legacy by transitioning the firm to future generations.

Research drawing on the FIBER framework to study SEW has highlighted that not all components carry equal weight in all family enterprises (e.g., Gerken et al., 2022; Hauck et al., 2016; Naldi et al., 2024). For instance, often control and renewal (F & R) are considered necessary conditions for fostering non-financial goals, but they alone do not guarantee such outcomes. For these conditions to foster non-financial goals related to impact and sustainability, elements of identification (I), social ties (B), or emotional attachment (E), in particular, need to be actively engaged (Swab et al., 2020).

Given the purpose and characteristics of SFOs with high to relatively high family involvement, we treat the FIBER dimensions as a sensitizing framework that guides our empirical analysis. This helps us identify which aspects of SEW become salient, how they are enacted, and how they may function as enablers or barriers in the translation of impact intentions into outcomes. Thus, building on recent calls to examine how SEW travels beyond traditional operating firms and into new organizational settings, such as SFOs (Hayoz et al., 2025; Kammerlander, 2022), our study draws on the SEW perspective and we use the FIBER framework to explore more in detail how specific SEW dimensions are mobilized to shape the strategies, governance mechanisms, and relational practices through which SFOs seek to influence their impact-oriented portfolio companies.

Methodology

Research Design Choices and Process

Study Context

We situate our study in Northern and Western Europe, with a focus on SFOs operating in Sweden, Norway, the Netherlands, and Germany. This geographical context is particularly relevant for examining the translation of impact intentions into outcomes for several reasons. First, these countries are characterized by a strong tradition of family ownership and intergenerational business continuity (e.g., De Massis et al., 2018; Haag et al., 2023), where families often play an enduring role in both economic and societal development (Zellweger, 2017). In this cultural and institutional environment, SFOs are primary actors for both wealth preservation and long-term societal impact. Second, the European policy and regulatory environment places increasing emphasis on sustainability and impact. The European Union has placed increased commitment through initiatives such as the EU Sustainable Finance Disclosure Regulation. This creates both opportunities and pressures for European SFOs to incorporate impact considerations into their investment strategies (Busch, 2023). Third, the social contract between business and society is particularly pronounced in the selected countries. Nordic countries, such as Sweden and Norway, are known for their emphasis on equality, social welfare, and stakeholder responsibility, which influences families’ expectations for their offices to contribute to societal well-being (Midttun et al., 2015). Similarly, the Netherlands and Germany have traditions of stakeholder-oriented corporate governance and institutionalized mechanisms for balancing shareholder and societal interests (e.g., Bottenberg et al., 2017). These cultural and institutional characteristics make the translation of impact intentions a strategic choice for SFOs as well as a response to broader societal expectations. Finally, the increase in SFOs in Europe provides a timely opportunity to study this phenomenon.

Research Design

To address our two research questions, we employed a qualitative, abductive design (De Massis & Kotlar, 2014; Edmondson & McManus, 2007). Given the lack of prior research explicitly linking SFOs’ impact investing intentions to outcomes, an abductive approach enabled us to iteratively move between empirical material and theoretical frameworks, refining our understanding as insights emerged (Alvesson & Kärreman, 2007; Timmermans & Tavory, 2012). The abductive process shaped both data collection and analysis. In line with this approach, the interview guide and the coding scheme evolved over the course of data collection and analysis, allowing us to explore both anticipated and unanticipated themes in a systematic way. In practice, our initial interview guides began with broad, open-ended questions about impact priorities and investment practices. As patterns began to emerge, we refined subsequent interview guides to explore these themes more in-depth. For instance, early interviews highlighted identity alignment and measurement challenges. Likewise, our coding process moved back and forth between open coding (to capture new insights in respondents’ words) and theory-driven coding (to explore themes related to SEW/FIBER). This back-and-forth process allowed us to build an empirically grounded yet theoretically informed understanding of how SFOs enact their impact orientation.

The SEW perspective and FIBER framework (Berrone et al., 2012) provided our initial theoretical point of departure, sensitizing us to family-specific, non-financial priorities. At the same time, we remained open to novel insights that extended or challenged these categories. For example, early interviews highlighted themes around measurement and additionality, yet the link to FIBER was implicitly evident, prompting us to investigate these issues in later interviews. Similarly, while dimensions such as Family Control and Influence and Identification with the Firm were immediately salient in the data, others such as Renewal and Emotional Attachment appeared less directly, often requiring interpretive iteration between theory and data. Likewise, not all the FIBER dimensions were equally salient across cases. For instance, Renewal of family bonds appeared consistently, but Emotional attachment surfaced less explicitly, with some themes challenging the framework—particularly inertia and path dependency, which complicate the idea that SEW preservation always facilitates continuity. These tensions illustrate the value of an abductive approach, allowing us to extend SEW to account for both enabling and constraining dynamics of SFOs’ impact investing.

Finally, we also chose to focus data collection on respondents with close involvement in the overall phenomenon of interest, hoping that their insights and expertise would provide the most thorough descriptions and interpretations of the topic. In relation to our research questions, the structuring of the interviews aimed to uncover recurring themes and explore connections between them, while FIBER guided the analysis of the empirical material that we gathered. By doing so, the study aims to elaborate on existing, rather than build new, theory (Timmermans & Tavory, 2012).

We focused exclusively on the non-financial priorities of SFOs with an emphasis on impact investing. Our analysis is centered on the investment strategies of the studied SFOs (Bell et al., 2022). This method specifically facilitated exploration of how family-specific factors influenced the strategies of the SFOs and their involvement in the portfolio companies as they pursued the translation of their impact investing intentions to desired outcomes in the ventures. We rely on a dual perspective of nine family offices and eight portfolio companies.

Sample

Our sample was selected purposively based on the research questions. We focused on SFOs engaged in impact investing and on the portfolio companies in which they had invested. Because our theoretical focus concerns the role of SEW in settings where family involvement is high, we deliberately restricted the sample to SFOs with high or relatively high owner-family involvement and a strong connection to a specific family. To identify cases, we first used desktop research to map SFOs active in impact investing in the relevant countries and then approached potential participants through direct contact and introductions from our professional networks. After securing an interview with an SFO, we asked for introductions to associated portfolio companies, which enabled a snowball sampling process (Bell et al., 2022).

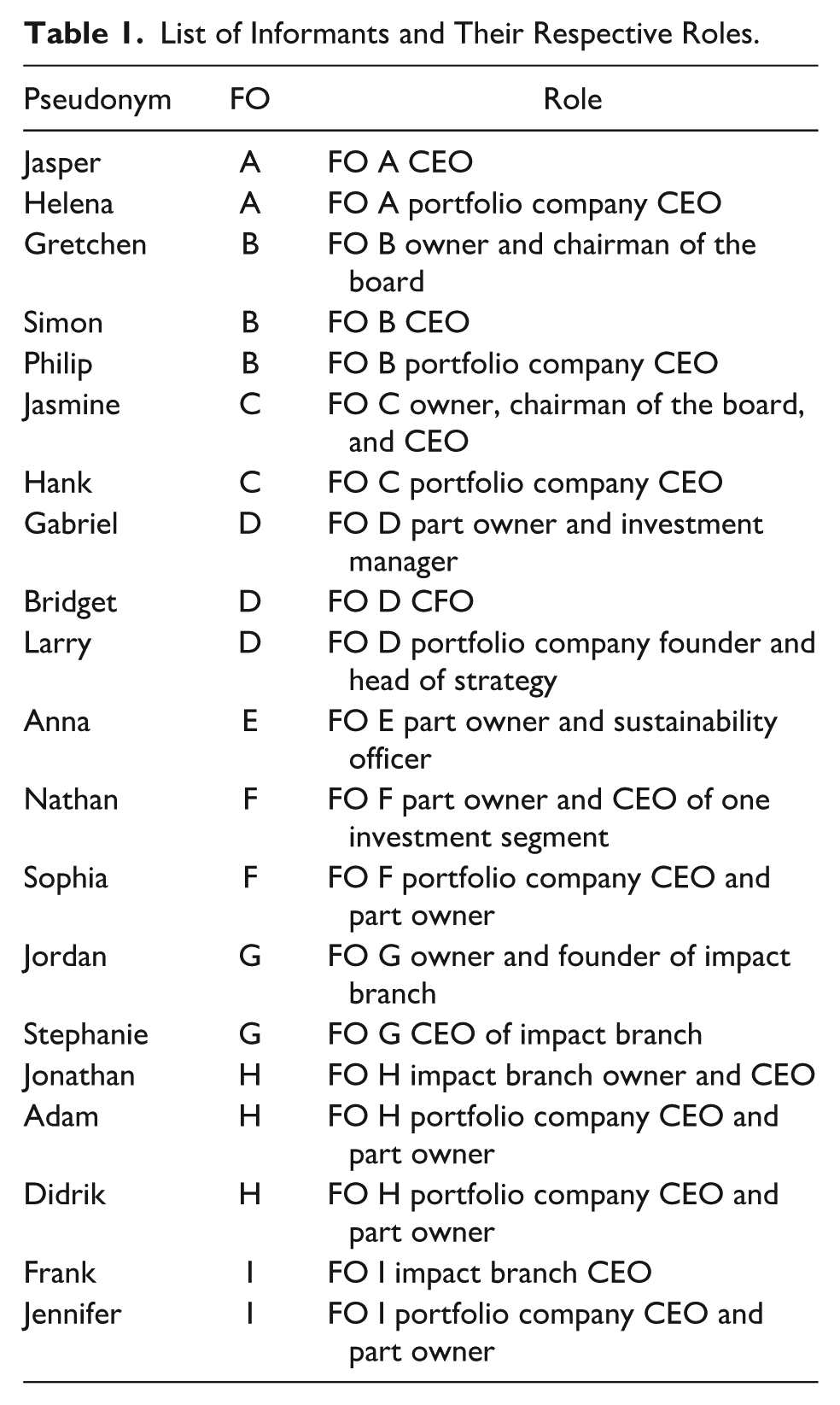

Given our sample choice, we encountered some challenges in gathering insights from founders and CEOs of SFOs and their portfolio companies, who are very busy professionals and difficult to access. Securing their participation required extensive desktop research and several months of engaging in networking events and leveraging our networks for introductions. In addition, the focused nature of the sample group meant that fewer interviews were necessary to reach theoretical saturation (Aguinis & Solarino, 2019), confirmed by the generation of minimal new codes after the 15th interview (Corbin & Strauss, 2014). These factors confirmed that the sample selection was appropriate for the research project’s scope and goals (Treviño et al., 2014). In sum, building on a dual perspective, our sample consists of 21 informants representing 9 different SFOs operating in Sweden, Norway, the Netherlands, and Germany. At the FOs, we interviewed seven active family members and six non-family member managers. In addition, the sample included eight portfolio companies, where we consistently interviewed one founder and/or executive. Table 1 provides details on the informants and their respective roles.

List of Informants and Their Respective Roles.

Data Collection: Interviews, Secondary Data and Informal Conversations

The guiding semi-structured interview protocol was constructed on a common foundation, with slight variations in questions tailored to the roles of the interviewees. The interview guide evolved through data collection (Pratt et al., 2020), where initial rounds focused on broad experiences with impact investing, while later iterations incorporated more targeted questions, for instance, on measurement challenges, SEW-related dimensions, and intergenerational dynamics, reflecting emergent themes from earlier analysis. This iterative refinement of the guide was part of the abductive process and helped us explore themes that emerged during the study rather than restricting inquiry to pre-defined categories. Before each interview, we reviewed available secondary information, including company websites, LinkedIn profiles, and prior email communications, to tailor the discussion to the specific context of the respondent and firm.

We simultaneously collected an array of informal conversations with family owners, CEOs and active members of SFOs and portfolio companies. These conversations served two purposes. First, they helped us sharpen the interview protocol and understand the contextual background of each case. Second, they contributed to triangulation by deepening our interpretation of the formal interview material. We treat the recorded and transcribed interviews as the primary empirical data, while the informal conversations informed interpretation and contextual understanding rather than constituting a separate coded data corpus. In addition, informing the interviewees about the interview process, including General Data Protection Regulation (GDPR) guidelines and the anonymization of their responses, helped establish trust and a safe environment, fostering more open information sharing (Bell et al., 2022). Interviews were recorded and transcribed verbatim within 48 hours. Interview lengths ranged from 33 to 66 minutes, with an average duration of 51 minutes.

Data Analysis

To organize, manage, and code the material, we utilized NVivo 14 software. This tool was instrumental in storing, organizing, and coding the rich data, which facilitated the identification of trends, themes, and relationships, thus supporting a rigorous and in-depth analysis. Following Timmermans and Tavory’s (2012) logic of abductive analysis, we moved back and forth between the empirical material and our theoretical framework, using SEW and FIBER as sensitizing concepts (Atkinson et al., 2003) to refine our understanding of how SFOs translate impact investing into portfolio-company outcomes.

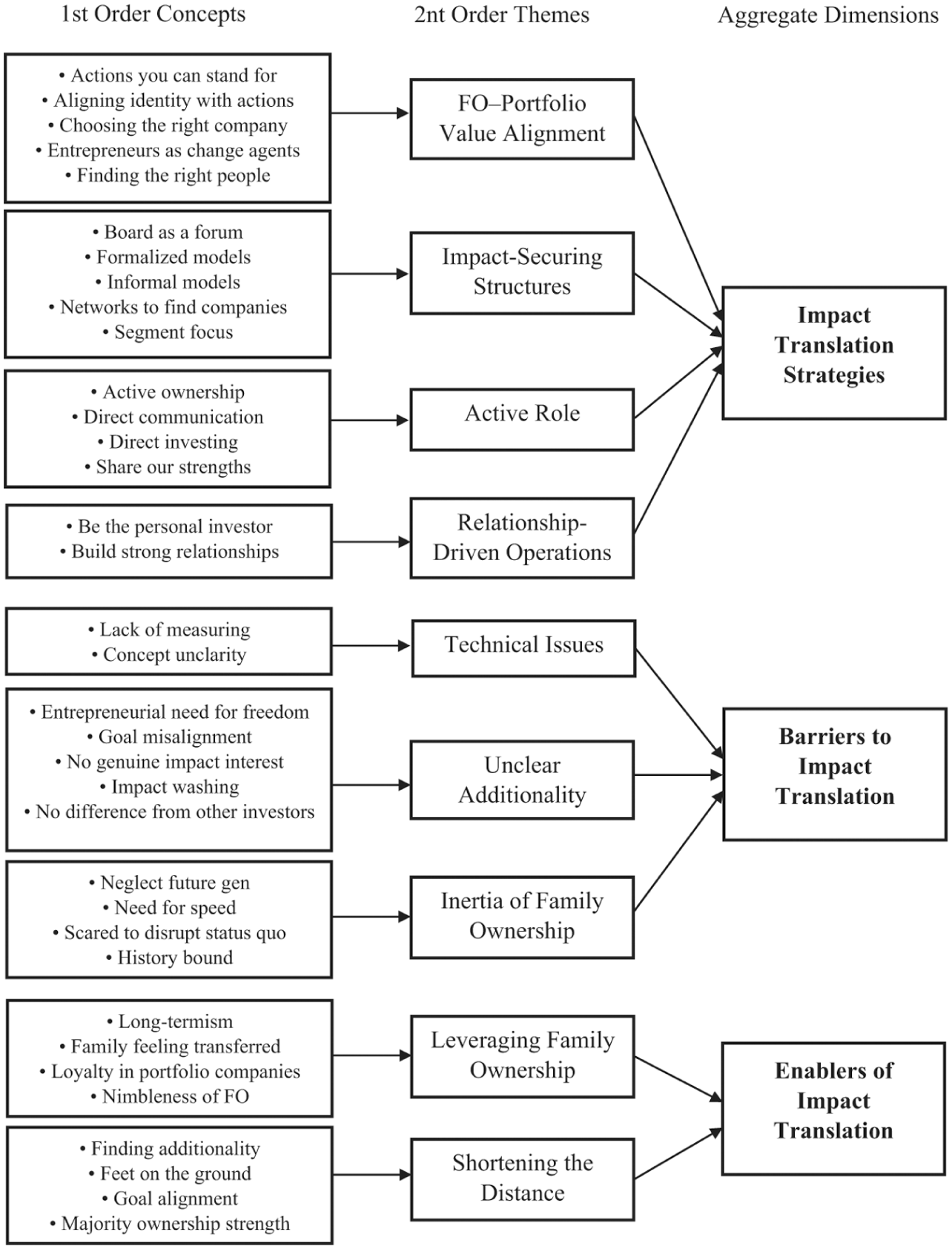

The analysis unfolded in several steps. First, we conducted open coding of the interview transcripts. This phase aimed to stay close to the informants’ language and capture recurring words, phrases, and ideas in their own terms. These first-order codes reflected concrete practices (e.g., “board as a forum,” “finding the right people,” “lack of measuring”) and subjective perceptions (e.g., “actions you can stand for,” “scared to disrupt status quo”). Second, we compared these first-order codes across interviews and grouped them into second-order themes that captured broader patterns in the data, such as value alignment, active role of ownership, or technical issues. During this phase, SEW and FIBER guided our interpretation, helping us assess which family-based non-financial priorities were most visible in the data and how they shaped the translation of impact intentions. For instance, codes related to “active ownership” resonated strongly with the Family Control and Influence dimension, while others such as “entrepreneurs as change agents” and “aligning identity with actions” reflected the Identification with the Firm dimension. Importantly, not all five FIBER dimensions were equally salient in the data. Family Control and Influence, Identification with the Firm, and Binding Social Ties appeared frequently and directly in the interviews, while Emotional Attachment and Renewal through Dynastic Succession were less directly expressed and tended to surface implicitly. For example, legacy-related inertia and risk aversion were coded as part of “history bound” or “need for speed,” which we later connected to Renewal. The abductive process also meant that theory and data informed each other dynamically and allowed us to see not only which SEW dimensions mattered, but also how they could function as both enabling and constraining forces in impact translation.

Third, we examined how the second-order themes clustered into three aggregate dimensions: Impact Translation Strategies, Barriers to Impact Translation, and Enablers of Translation. This aggregation helped us identify the main mechanisms through which SFOs seek to translate impact intentions and the conditions under which these mechanisms become more or less effective. For instance, early codes around “impact washing” and “goal misalignment” prompted us to revisit the impact investing literature and sharpen our understanding of additionality and legitimacy concerns.

We assessed theoretical saturation by examining whether new interviews generated fundamentally new second-order themes (Corbin & Strauss, 2014). After the 15th interview, additional data produced limited new conceptual insight, suggesting saturation had been reached. Several steps were taken to enhance the credibility and transparency of the study. First, the dual-perspective design allowed us to compare how SFOs and portfolio companies described the same relationship from different vantage points. Second, the use of secondary data and informal conversations supported triangulation and contextualization. Third, the abductive approach ensured that the interview guide and coding scheme evolved as the study progressed, while remaining anchored in the research questions and theoretical framing. Finally, we documented the analysis process carefully in NVivo and checked emerging interpretations against the data throughout the study, which helped us remain close to the empirical material while developing theoretically informed insights. To enhance transparency and visually illustrate how the data moved from first orders to second orders to aggregate dimensions, we present our data structure in Figure 1 (Gioia et al., 2013).

Data structure.

Findings

The empirical findings are structured according to the aggregate dimensions related to how SFOs translate their intentions in impact investment to desired outcomes in the companies in which they invest: Impact Translation Strategies, Barriers to Impact Translation, and Enablers of Impact Translation.

Impact Translation Strategies

Impact-focused SFOs employ several strategies to ensure that non-financial priorities are emphasized in portfolio firms. These strategies unfold both before and after investment, relying on a combination of value alignment, governance impact-securing structures, active involvement, and relational operations.

Pre-Investment: Establishing SFO and Portfolio Company Value Alignment

A key factor for SFOs is to secure value alignment with entrepreneurs. Families emphasized “finding the right people” rather than simply the right ventures. Entrepreneurs were described as “change agents of society” who could carry forward the family’s legacy and identity. Inherent in many SFOs is also a strong awareness of the entrepreneurs’ situation, translating into a clear idea of how the SFO can effectively support the portfolio companies. This support includes patience and giving the entrepreneur the time necessary to develop. Some SFOs make it explicitly clear that they do not want to be identified as asset managers who just want to manage wealth, but that they act as entrepreneurs themselves:

The entrepreneurs are the change makers of society. So, we should support the entrepreneurs, the early stage because that’s where the capital is needed. We can provide patient capital; we can be on the entrepreneurs’ side of the table. So, let’s invest in entrepreneurs. (Gabriel, SFO D part owner and investment manager) We are entrepreneurs ourselves and involve ourselves in business, so we look for investments where the founders are fine with our support. (Nathan, SFO F part owner and CEO of one investment segment)

Choosing the right venture with the right people to invest in is also seen as vital for value alignment. This often meant investing in individuals and teams whose values matched the SFO’s ethos, even creating ventures around trusted entrepreneurs rather than entering existing firms. To illustrate, one SFO in our sample made attempts to instead invest in a company profile they appreciated but quickly realized that the people were insufficient to secure the value alignment needed to set the company on a desired path. In the CEO’s own words:

When we invested in some early-stage companies, we found that the cultures were not completely value aligned. And so, then instead of investing in companies, we started investing in people and suggested that they could start a company and then we could do something together. And that means that we have an influence on the choices being made there. (Stephanie, SFO G CEO of impact branch)

Pre- and Post-Investment: Impact-Securing Structures

SFOs deployed impact-securing structures, both pre- and post-investment. Majority owners often relied on networks to identify opportunities and positioned themselves in key operative roles (e.g., CFO) to steer portfolio firms directly. SFO F, for instance, takes leading roles in portfolio firms, such as the CFO role in the interviewed portfolio company. This enables them to ensure control of what occurs in the portfolio firms. Particularly within this cluster, the identification of interesting firms to invest in is done through the extensive network of the owners. Jamine, an SFO owner, chairman and CEO, explains,

Other impact investors usually only have a few percentages of portfolio companies. We will in many of the cases have a majority, which is between 50 and 80%, so we are defining the work. Advantages and disadvantages, but one advantage is to have more freedom to operate and short decision ways and including local people in making the decisions. (Jasmine, SFO C owner, chairman of the board, and CEO [Majority owner])

Minority owners, in contrast, leaned on formalized models and due diligence to ensure alignment prior to investment. Several developed proprietary Environmental, Social, and Governance (ESG) or impact management models, embedding family identity in codified processes. These models seem to aid the rationalization of what the SFOs are trying to achieve, and one of the SFOs named the model after the family. To illustrate,

We have something called the “Family name” ESG management maturity model. So, there’s basically a set of questions or things we kind of want the company to develop or have in place already, which basically puts them on this kind of ladder, that we then see, OK, you know this we want you to develop [in terms of proactive sustainable practices]. (Anna, SFO E part owner and sustainability officer) We are giving them [portfolio companies] some issues to work with and if they fulfill the social goals, then we will switch the money into equity, right? So, it goes from a kind of loan into equity–if they succeed in the social mission. What we try to do now is being that really social investor, so we need to link the social effects in the companies with the money. (Frank, SFO I CEO of impact branch)

Another way to translate the impact intent of SFOs is clear market segmentation. Apart from one SFO, all sampled SFOs choose investment areas similarly. They choose to invest in markets that largely align with the interests and/or expertise of the family members and top management, in combination with a clear opportunity for impact. The remaining SFO’s segmentation, SFO C, is purely driven by where the impact is the largest. This SFO also has an identity that is closest to philanthropy. The segment choice also often connects back to the legacy of the original family firm that generated the initial wealth, which creates logical progression toward certain areas, even when extending the business toward impact. In the words of two SFO CEOs,

I started to analyze what areas are the most important for the earth to stay inhabitable. I think that were the reasons why we ended up with these [investment areas] and of course that we understand a little bit of these systems. So, Jordan [SFO G owner] is very good when it comes to science and I’m very good when it comes to food & agriculture and communication. So, therefore, we decided to land on these four big areas. (Stephanie, SFO G CEO of impact branch) The companies that we invest in are within mental health education and integration. [. . .] The upside of also sort of having the original success firm legacy is obviously that we are a subsidiarity to a bigger investment company. [. . .] So basically, you know [we] continue building on the network and the knowledge and the experience from the original success firm. (Jasper, SFO A CEO)

Post-Investment: Exercising Active Ownership and Relational Operations

After the investment, SFOs enacted two distinct modes of involvement. First, active ownership which involved formal roles such as board seats, frequent meetings, and direct investments. Majority investors in particular emphasized their ability to “shorten decision paths” and actively steer portfolio firms. They engaged in tasks revolving around non-financial issues, where they often ask themselves how they can support the portfolio companies in a way that pushes them into thinking about a future aligned with the SFO vision, as Frank exemplifies:

We are very often active owners. So, my people will meet with their entrepreneur once a week or every second week. They are working really closely on building the company and what to do. So, if we start noticing that we have different interests, then we have to stop being an owner. We need to have a common vision with the entrepreneur on where to go, if we are to be an investor. (Frank, SFO I CEO of impact branch)

Communication is important. Contacts are made between the SFOs and their portfolio firms weekly among most of the SFOs, and in some instances, multiple times per week. These conversations are both short-term decisions and are used to continuously identify where the SFO can support in both non-financial and financial issues. The type of support that is given is often connected to the personal expertise and strength of the SFO team, also here in the early stages of a portfolio company. For instance, Nathan reports:

Founders who only need money have a problem. It’s never just the money, it’s also a lack of experience or a particular issue [. . .] And when we believe we can solve the problem, then we are the right partner. (Nathan, SFO F part owner and CEO of one investment segment)

Second, I almost already had decided that whatever he [Jordan, SFO G owner] wants me to do, if I could be part of his journey, I would say yes. Even if he says maybe, you can clean the office every day [laugh]. No, but in some way, I had a great trust in Jordan and his belief and his values. (Stephanie, SFO G CEO of impact branch) I think I put more demands on myself because of loyalty to the owner. But I also know if something happens, they will be there for me, my family, and the company. (Philip, FO B CEO of portfolio company)

Many of the owners see the trust generated in relationships with the portfolio firms as a guarantee for impact to be emphasized, as it would otherwise be a breach of trust. This belief often dates back long in family history, and SFO D, for example, follows a principle stating that business partners are always treated with the highest level of fairness, which they then believe will be reciprocated.

Another way of expressing the relationship mindset is for SFO owners to treat their investments as a personal extension of their family values. It is personally important for the SFOs that the impact intentions progress, especially when they are named after the family. In addition, the fact that the SFOs see it as “their money” makes them more personally involved, as stated by Nathan:

It’s all our own money and of course, you have a different perspective if you invest your own money, then when you invest other people’s money. So, we have worked for the money, and we have paid taxes for the money and therefore we might be more personally involved and more dedicated. Also more careful doing the right things by using our own money rather than just managing other people’s money. (Nathan, SFO F part owner and CEO of one investment segment)

The responses in some portfolio companies support this view, where portfolio executives emphasized the authenticity and loyalty of SFOs as investors, contrasting them with venture capital investors:

First of all, Jasmine [SFO C owner] is real. Second, it’s Jasmine’s money, so she does what she wants with it. Then Jasmine’s decision-making time becomes like super short, she moves very fast. (Hank, SFO C portfolio company CEO) SFO D always supports and it’s because they are the money, right? The issue is that when you are dealing with the VC, you have a VC team. So, you have an investment manager that is your contact person, and that person has different interests than the money. (Larry, SFO D portfolio company co-founder and head of strategy)

Barriers in Impact Translation

Despite these strategies, SFOs encountered three main challenges. The first is technical issues, mainly revolving around how to define the guiding concept of impact and practical impact measurement. The second is unclear additionality, which concerns mostly how SFOs struggle to stand out compared to other investors. Third, the family ownership inertia arises where some common characteristics of SFOs provide obstacles for impact translation.

Technical Issues

A persistent barrier was the difficulty of measuring and defining impact. This also relates to ambiguity with regard to how to define the impact concept itself. Indeed, our empirical data describe that SFOs acknowledged the challenge of selecting reliable key performance indicators (KPIs) and attributing impact. This problem occurs both before the investment decision and continues to run through the ownership. Bridget provides an example:

The whole team is struggling with how to measure this ex-ante and ex-post. How do we know how much impact this will have, and this is the biggest problem of all I would say because we are not even close to measuring it the whole way and it’s very cumbersome and it’s very difficult to do it. (Bridget, SFO D CFO)

While all SFOs struggle with measuring the impact, the approach to solving the issue differs. Some SFOs rely on being patient and that an effective measuring process will be created bottom-up over time, meaning that the portfolio companies are expected to drive the process. In some cases, it is considered sufficient, with the belief that the invested-in company will create impact, even though it cannot yet be confirmed through measurements. Another more structured approach used by around half of SFOs is to actively get involved in the measurement process and utilize active ownership as a way of defining and measuring impact.

The implications of technical issues with defining and measuring impact are significant for the translation process. This uncertainty complicated both internal decision-making and external communication, leading some portfolio firms to doubt the credibility of SFO impact claims. This is, for instance, the case with the ones working far away from the owning company:

I don’t want family offices that want to support impact to leave a big mess behind. I think we could solve that by educating them, making them more aware, including some KPIs about ownership or decision-making, representation, etc. (Hank, SFO C portfolio company CEO)

Adding to the measurement issue, there is the lack of clarity around the definition of impact. Some of the SFOs themselves question this point, as in the case of Anna:

I think when you bring in the word impact . . . What is impact? You know, I think that is also something that is so easy to throw out there. But it’s really up to every family business to define “what is impact for us?” (Anna, SFO E part owner and sustainability officer)

Unclear Additionality From SFOs

Linked to the measurement issue was the challenge of demonstrating additionality. This relates to the difficulty of attributing the achieved impact to specific SFO investors, especially from portfolio companies. Often, the impact is taken for granted, whereas portfolio companies see investors, including SFOs, not considering impact in their day-to-day business:

I don’t really see anyone caring too much about impact, right, and maybe that’s sort of a little bit unfair because it’s sort of . . . it’s something that comes very naturally. If we are successful, we’re going to have a positive impact. (Helena, SFO A portfolio company CEO and part owner)

This highlights that, in some instances, SFOs do not pressure portfolio companies to prioritize impact by using formal governance structures, are actively involved as owners, and fostering close relationships. Indeed, it is rather the portfolio companies own interpretation of the impact intentions that drives the direction of the venture priorities:

[on whether Jonathan in SFO H put strict demands on impact] No, definitely not. We haven’t really given much reason for him to complain so far. For example, if we were to start pulverizing slaughterhouse waste, I believe Jonathan would intervene, but that’s something we simply won’t do. (Adam, SFO H portfolio company CEO and co-founder) At the end of the day, a family office is just an investment company. And if you are lucky, they are a bit nicer than the rest. (Sophia, SFO F portfolio company CEO and part owner)

Alongside this, a problem with investing heavily in entrepreneurs appears, mainly based on their need for freedom. This need seems to be strong among many of the entrepreneurs behind the portfolio firms and it creates a distance between the SFOs and the portfolio companies. On the one hand, this distance seems to be a precondition for an effective working family office investor-portfolio company entrepreneur relationship. On the other hand, this provides a greater challenge for translating the attempted active ownership to impact outcomes in the portfolio firms. Therefore, a tension between being a good owner in the eyes of the portfolio company and simultaneously driving the impact agenda is created, where the entrepreneurs state to experience full freedom if they act responsibly:

A good owner is an owner that really doesn’t interfere with the company. Everything just runs and the owners are happy, and they make sure the company has the resources it needs. (Gabriel, SFO D part owner and investment manager) The daily business it’s run by . . . I feel like this is my company, but it’s owned by SFO B. I can do whatever I want. But I need to take responsibility. They trust me 100%. Loyalty is very important. They have never told me what to do. (Philip, SFO B portfolio company CEO)

Inertia in Family Ownership

The final barrier is a built-in inertia that family ownership can bring. Important to many of the SFOs, especially the ones with a long history, is to honor and thus not deviate extensively from the principles of the original family business that generated financial wealth and success. This is mostly prevalent in the older generations, while the younger generations are more open to change. However, in most studied SFOs the next generation were not yet in a position of control, meaning that the possibility of making a real change from the younger generation is seen as difficult. The implication of this is a less authentic and disruptive impact effort:

I was trying to change his [father of SFO H] company [towards impact] which is very difficult when I mean . . . If you go to your parents and tell them, well, nicely done so far, but just for your information, you’re missing the whole point, we are doing it differently now. [. . .] In the end, people in the company listen to me and they make the appointment because I’m the son of the boss. But in the end, nothing is happening afterward. (Jonathan, SFO H Impact branch owner and CEO [youngest gen]) I’m not saying that the different things we do have to be only impact first, but it’s missing a little bit of it. So yeah, that’s something at least the next gens are starting to talk about and look into. [. . .] If I may be very honest, sometimes it feels that the older generation is still holding on to you know, certain things. And they still want to prove themselves and leave their footprint here which means that, yeah, I’m not sure you know how much they actually listen to the next generation. I mean, if the mission is to create a better world for future generations, you need to listen to the future generations. It’s a very common problem in family businesses. (Anna, SFO E part owner and sustainability officer [7th gen, 6th gen currently in control])

The family ownership inertia can also be interpreted as a fear of leaving the path that has laid the foundation for the family’s business success and wealth, leading to a lack of clear intention from current generations to create significant change. Thus, the strong fear of change seems to be emotionally attached to the history of the family. Findings from some portfolio firms and SFOs themselves indicate that families tend to be afraid to lose both the financial and SEW that has been created by previous generations. Hank explains his view:

Some people [in SFOs] are super afraid of failing because they’ve inherited this so what you must do, is to make sure that the money you got will be well-managed and brought to the next generation. The life mission is holding them back on what they feel they can do because. . . say that you’re investing in an impact company and that’s failing. Then you’ll be criticized immediately. It’s easy to criticize things that are out of the mainstream. (Hank, FO C portfolio company CEO)

Families feared reputational loss if impact investments failed, leading to a preference for safe bets over transformative ventures. Younger generations often expressed frustration at this conservatism, highlighting intergenerational tensions over how boldly to pursue impact. Several SFOs are seen by the portfolio companies as afraid, and even to express hatred, toward losing money. The fear of significant change is also reflected in the closeness of the relationship with portfolio firms and external parties. As mentioned, the relationship is a strategy for translating impact intentions to outcomes, but caring too much for the relationships potentially mitigates actions that could provide real change:

It’s too important for them [SFOs] to have a reputation of being founder friendly or founder fair than it is to really push the management team or push the CEO to, you know do better or change or whatever it is that they need to do right. (Helena, SFO A portfolio company CEO and part owner)

Enablers of Impact Translation

Alongside barriers, our analysis revealed mechanisms that supported the translation of impact intentions. The themes are seen as mitigating the barriers faced and potentially contributing to the extent to which the intended impact is translated to the desired outcomes. In short, they can be described as leveraging family ownership with long-term orientation for enabling impact and shortening the “distance” between the portfolio companies and the SFOs.

Leveraging Family Ownership

Common for most SFOs, irrespective of the stake, is the flip side of the inertia challenge, namely family-ownership-specific factors that, in contrast, align with the impact concept and make them a suitable partner. Here, family ownership can serve as leverage for pursuing impact. The foundation for this leverage is the long-term orientation that we found in all the SFOs in the sample. This is characterized by thinking in generations rather than quarters, with the intention to maintain ownership through generations.

Interviewees explain impact itself as characterized by the need for patience and long-term orientation and this is offered by SFOs that have the intention and ability to ride out short-term “storms” and also focus on non-financial priorities. Thus, SFOs can instead lead the way in terms of making riskier investments, as they lack urgency for quick financial return, enabling explorative freedom for portfolio firms to take the time and do things differently. To exemplify,

They [SFO I] knew us and I knew them, so for me, it was important to know that these are people and a family office you want to have with you during a long winter night when it gets cold and the wind blows, which it always does in companies that want to change things. It is an important thing for me that they are someone we could trust [about SFO I going in as equity owner]. (Jennifer, SFO I portfolio company CEO and part owner)

Consequently, even though SFOs experience barriers making larger shifts in their organization, the long-term orientation can enable more significant thinking of change in the portfolio firms. This is described as a clear difference from more conventional venture capital structures focused on impact, which aims for competitive and timely financial returns. As such, SFO impact venture funding is nimbler and more adaptable, and thus attractive for entrepreneurs who want to pursue impact:

There is a huge need and a huge gap in financing and that’s why so many organizations [impact-oriented] aim for this so-called patient capital and they’re all going for the next gens and for all those families who have the money and where in the end, if they get 2 or 10% return doesn’t really matter for them because they have the money and there’s a huge financing gap. (Jonathan, SFO H impact branch owner and CEO) If you can go to the family offices, you should always do that because you have better valuations, much less strict monitoring, and you cannot have direct relationships with the people with money like Gabriel [SFO D co-founder], anywhere else. They are much more long-term and much more supportive. So, if you can go for them, it’s always better. (Larry, SFO D portfolio company co-founder and head of strategy)

Shortening the Distance Between Portfolio Companies and SFOs

SFOs also reduced the “distance” to portfolio companies through close involvement, especially for those that adopt the strategy of majority ownership and directly appointing themselves in leading positions (e.g., board roles) in the portfolio firms. In this way, it becomes more natural to become an involved and active owner, control can be exercised more clearly, and the SFO influence becomes significant even in day-to-day business. Even though the entrepreneurs who started the portfolio companies still perceive a high sense of freedom, the portfolio companies are more dependent on the SFOs which makes their voice more potent. This also creates a situation where the goal alignment between the SFO and the portfolio firm becomes stronger and several cases more personal. Hank illustrates the relationship between his SFO and portfolio company:

Me and Jasmine [SFO C owner and CEO] like each other a lot and we work very well together. We share the same values. So, me and Jasmine have been creating different businesses together. [. . .] We speak like every day. So, we’re very much aligned and trust each other. (Hank, SFO C Portfolio company CEO [FO C is majority owner])

Thus, shortening distance facilitated knowledge sharing and goal alignment, while trust, both affective (in terms of emotional bonds) and cognitive (in terms of confidence in competence), served as linking mechanisms. Shortened distance also facilitates overcoming the barrier of additionality and for the SFOs to be different compared to other owners. The proximity of the SFO to the portfolio firms helps the identification of how and where the SFO can support the portfolio company to progress in the goal-aligned direction, as illustrated in SFO H:

They really came in with know-how in this energy transition [impact] part for sure. So, they provided companies, network partners, money, and cooperation possibilities. (Adam, SFO H Portfolio company CEO and part owner [SFO H is majority owner])

Discussion

In this article, we set out to address two questions that pertain to a pressing challenge for many SFOs investing in ventures with purposes that extend beyond traditional financial value creation: (a) how do SFOs with a focus on impact investments translate their non-financial impact intentions into desired outcomes within their portfolio companies? and (b) what are the barriers and enablers encountered in pursuing this translation? We adopted a dual perspective, recognizing that translating the SFO’s impact intention into outcomes necessarily involves both the intentions and strategies of the SFO and the ability of portfolio companies to deliver those outcomes. This allowed us to consider tensions in the expectation-realization relationship between SFOs and portfolio companies and to view the SFO and portfolio company connection, in line with SEW, as more relational than transactional.

Translating Impact Intentions: Strategies, Barriers, and Enablers

In relation to the first research question, we find that impact-oriented SFOs pursue four strategies to translate their impact intention into desired outcomes: seeking value alignment between the SFO and the portfolio company, building impact-securing structures, taking on an active role in the venture, and facilitating relationship-driven operations. Crucially, these strategies span both pre-investment and post-investment phases. This builds on and advances prior research on SFOs and impact investing, which has established that SFOs are increasingly important actors in sustainable and impact-oriented private markets, but has offered less insight into what they actually do once they invest to influence portfolio-company outcomes (Hayoz et al., 2025; Listl & Mueller, 2026; Schickinger et al., 2023).

Regarding the second question, we identify three main barriers in this translation. First, technical issues in relation to the appropriate measurement of impact complicate both internal decision-making and external communication. Second, unclear additionality can make it difficult to specify what the SFO contributes to the portfolio company beyond financial means. Third, family ownership inertia emerges especially when older generations prioritize preservation and fear reputational loss, making it difficult to pursue impact ventures. While prior impact investing research tends to focus on the financial outcomes of impact investing to determine whether it provides competitive financial performance (Barber et al., 2021; Berk & Van Binsbergen, 2025; Bugg-Levine & Emerson, 2011), we take a different perspective, which reveals that the challenge is not only whether impact can be measured or financially rewarded, but also whether investor influence can be attributed, accepted, and enacted in the relationship with the portfolio company. At the same time, we identify two enabling mechanisms, where the first pertains to the fact that family ownership also can act as a leverage. If there is a close alignment between the SFOs intentions and the focus of the impact venture, family ownership allows portfolio firms to experiment and pursue impact strategies that do not fit a short‑term return view. Second, shortening the distance between SFOs and portfolio companies through more active involvement strengthens goal alignment and makes it easier to translate intentions into desired outcomes. In this way, our findings extend research on SFO behavior by illustrating that patient capital and family involvement are not only general characteristics of SFOs (Hayoz et al., 2025; Listl & Mueller, 2026) but also become concrete mechanisms through which impact intentions are translated into portfolio-company practices.

The mechanisms we found that serve as enablers or barriers also reveal crucial boundary conditions in the SFO impact translation. While proximity and closeness between SFO and impact ventures can enhance alignment, excessive SFO involvement risks being perceived as overreach by the impact ventures. Similarly, long-term orientation and patient capital generally enable impact, but in some cases, they delay necessary strategic exits or foster complacency. Recognizing this boundary condition helps to understand the SFO uniqueness and highlights that the same enablers can, under certain circumstances, become barriers.

A SEW Perspective on Impact Translation in SFOs

Given that most SFOs are set up with the often-sole purpose of serving a specific family, we relied on Hayoz et al. (2025) and drew on SEW to further interpret these findings. Prior SEW research has suggested that family firms often pursue non-financial goals related to control, identity, social ties, emotional attachment, and renewal. Our findings advance this literature by illustrating how these SEW dimensions, combined in the FIBER framework in the SEW literature (Berrone et al., 2012; Swab et al., 2020), are not only relevant in operating family firms but are also projected outward through the SFO’s investment relationships with portfolio companies.

Accordingly, our findings suggest that both SFO and portfolio companies tend to prioritize value alignment, which is achieved primarily through the SFO supporting identity-aligned impact ventures. This reflects a concern for identification with the firm (I), which is a central dimension of SEW (Berrone et al., 2012; Murphy et al., 2019). Rather than evaluating ventures solely on financial or market-based criteria, the SFOs emphasize relational and personal connections, which underscores the importance of binding social ties (B). For instance, SFOs actively engage in trust-building relationships and knowledge sharing with their portfolio firms, sustaining trust in the broader entrepreneurial family context (Sundaramurthy, 2008). Again, this relational rather than transactional focus highlights that SEW is not only preserved internally within the family, but through its impact investing translating strategies, the SFO seeks to extend this focus through fostering a close relationship with the portfolio company. The binding ties SEW dimension is also important from two other perspectives. First, the SFOs can offer the portfolio company access to business opportunities through their external network. Second, the binding ties serve as a way to address the concern about lack of additionality; if the SFO struggles in finding ways to add value in the relationship beyond financial investments, our findings suggest that its access to other ties through networks can be sources of added value. This extends prior SEW literature (e.g., Calabrò et al., 2026) by illustrating that binding social ties may operate not only as intra-family or stakeholder relationships around a focal family firm but also as resources mobilized across an investment portfolio.

Our findings also suggest that family control and influence (F) play an ambivalent role. On the one hand, majority stakes, board seats, and occasional operative roles in portfolio firms enable SFOs to embed impact priorities in governance structures, shorten decision paths, and actively support impact ventures. On the other hand, control can foster inertia when it is used primarily to protect the status quo and to avoid reputationally risky impact ventures. Compared to prior family business research, which often treats family control as a source of long-term orientation and stewardship (Le Breton–Miller & Miller, 2006; Lumpkin & Brigham, 2011), we theorize that control can both support and constrain impact translation depending on how it is combined with generational priorities, governance structures, and relational engagement. Despite these variations, all SFOs emphasize the importance of active ownership, which aligns with a long-term orientation to their investments in the impact ventures. Typically, family ownership seems to become a barrier in translating impact intentions into outcomes when the older generation controls the SFO as well as the engagement in the portfolio company. This relates to protecting family control as a key SEW dimension but can be an expression of the SEW dimensions emotional attachment (E) and Renewal through dynastic succession (R), although less explicit in our sample (Berrone et al., 2010; Naldi et al., 2024).

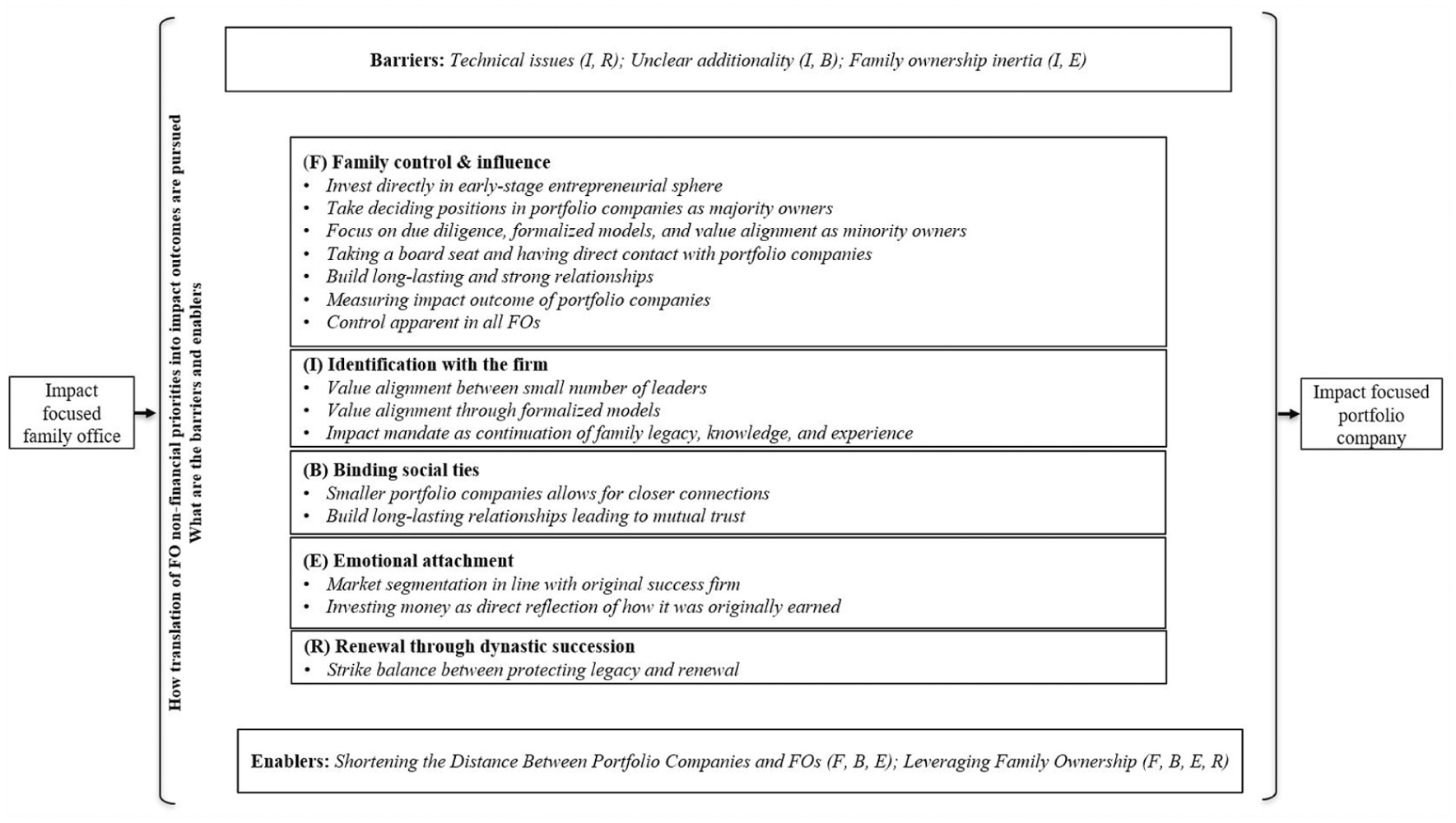

Our findings indicate that when family ownership is seen as a leverage, the younger generation is typically in charge and driven by a stronger commitment to the SFO’s role as a driver of impact outcomes. Thus, we suggest that the SFOs’ desire to maintain control and to preserve the family’s legacy and reputation can conflict with the flexibility required to pursue growth in impact ventures, while it can also promote growth depending on the generation in charge. In either case, the SFO’s considerations of SEW and the perspective from the portfolio companies mean an increased likelihood of playing a role in the alignment of each SFO’s control, identification, social ties and emotional and generational priorities with the strategic objectives of portfolio firms, ultimately either facilitating or constraining the translation of impact intentions into desired outcomes. Figure 2 provides a summary and visualization of the findings in relation to the SEW and five FIBER dimensions.

Summary of findings in relation to the five SEW FIBER dimensions.

Building on this SEW interpretation, we next elaborate on the observed heterogeneity in SFO impact translation through a typology of four impact translation logics.

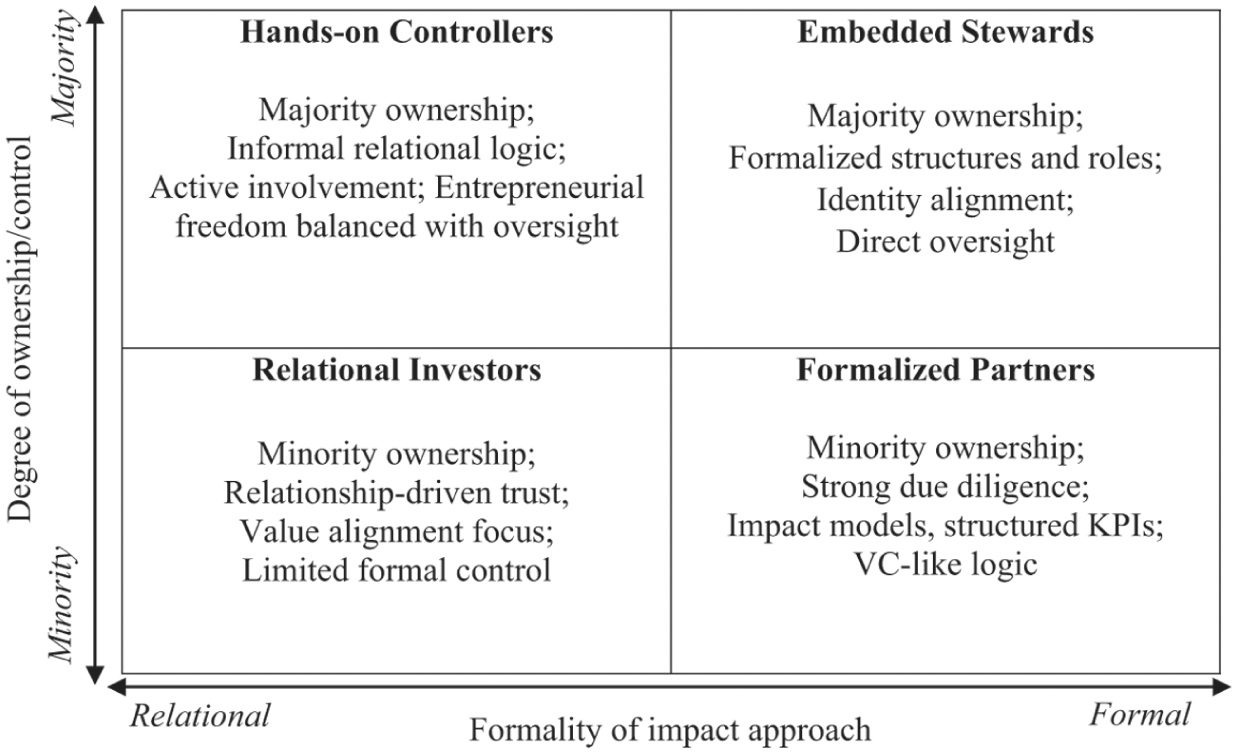

A Typology of SFO Impact Translation Logics

While all SFOs in our sample combine the four strategies and encounter similar types of barriers and enablers, our analysis also revealed notable differences in how they configure their practices. Building on the general findings discussed above, we identified two key dimensions shaping their practices: the degree of ownership/control (majority vs. minority) and the formality of impact approach (relational vs. formal). Together, these two dimensions yield four types of impact translation logics, which are illustrated in Figure 3. We propose these four logics as ideal types rather than fixed empirical categories. They represent conceptual configurations that help to understand recurring patterns in how SFOs combine ownership/control and formality when translating impact intentions into outcomes in their portfolio companies. Individual SFOs may combine elements of more than one logic or move between impact translation logic over time and across investments. The typology therefore helps to clarify boundary conditions for impact translation as it is grounded in the strategies, barriers, and enablers identified in the findings. This means that each logic reflects a different configuration of value alignment, impact-securing structures, active ownership, relational operations, measurement challenges, additionality concerns, family ownership inertia, and the enabling mechanisms of patient capital and shortened distance. Overall, the typology is a conceptual way to highlight the potential heterogeneity of SFO impact translation and describes how combinations of SEW considerations through governance structures and ownership positions shape the translation of intentions into outcomes.

Typology of single-family office impact intention translation logics

The top left quadrant in Figure 3, Hands-on Controllers (Majority ownership, Relational approach), showcases controlling investors emphasizing trust and loyalty, aligning portfolio firms through stewardship and personal engagement. They tend to rely on direct communication and trust to steer firms, but face tensions when founders’ autonomy collides with owners’ active presence. Here, decision-making processes are typically shorter, ensuring that the SFO’s control is more pronounced. In addition, financial capital can have substantial impact (Chrisman et al., 2012), so can also the SFOs' ability to promote value alignment be via a strong degree of identification and emotional attachment. The closeness between the SFO and the portfolio company, based on trust and loyalty, also means that social ties are stronger and provide an added layer of internal support, and not only access to new business opportunities.

The top right quadrant, Embedded Stewards (Majority ownership, Formal approach), emphasizes SFOs with high ownership stakes and structured impact models exercised through strong control. These SFOs design impact models, link financing to performance on social goals, and occupy operative roles in portfolio companies. However, this comes at the cost of reduced flexibility. In this type, family control and identification are expressed through formal mechanisms, such as impact metrics, contracts, and board processes that institutionalize the family’s impact intentions. Binding social ties remain important but are complemented by codified expectations. This logic increases the clarity and measurability of impact but can reduce flexibility and may come across as more “managerial” or transactional than relational to portfolio companies.

The bottom left quadrant, Relational Investors (Minority ownership, Relational approach), focuses on partners emphasizing long-term, trust-based collaboration, and value alignment with entrepreneurs. Yet their ability to push for measurable outcomes is limited due to weaker control, leading to challenges around additionality. However, leveraging the network connected to the SFO is one way to support the additionality by shortening the distance to the portfolio companies and establishing SFOs as unique, impact-oriented owners (Lester & Cannella, 2006). Further, engaging closely with the impact ventures is a way for these SFOs to strengthen their identification with them through the social and sustainability causes they are founded to address, even if they do not have strong actual influence in the venture because they have deliberately kept formal control low.

The bottom right quadrant, Formalized Partners (Minority ownership, Formalized approach), includes SFOs with limited ownership that adopt a structured approach by using impact models, due diligence, and KPIs. However, relational depth with impact ventures is often thinner than in relational logics. In this SFO type, SEW considerations are generally weaker in comparison with the other three SFO types. Minority ownership puts limits to the extent to which family control can be exercised in the portfolio company, and the formalized approach to seeking to translate impact intention means less emotional attachment and less identification with the venture. The binding social ties are primarily external and focus on channeling new business opportunities via the SFO to the portfolio company. This impact intention logic establishes a foundation for formal SFO influence and enhances impact generation by positioning SFOs where they can effectively contribute and provide additional value to the portfolio companies (Zellweger & Kammerlander, 2015).

By articulating these four types of impact translation logics, our typology offers three main insights. First, from the dual perspective of both SFOs and portfolio companies, it demonstrates that SFO-driven impact investing is heterogeneous and can be translated into different combinations of control and formality, leading to different strengths and vulnerabilities in translation. Second, it shows how an SFO’s configurations of SEW dimensions according to the FIBER framework (Berrone et al., 2012) are linked to distinct impact translation logics. For example, Hands‑on Controllers and Relational Investors both leverage binding ties and identification, but only the former can systematically use family control to reinforce impact priorities. Embedded Stewards and Formalized Partners both use structured tools, yet the former can embed these tools deeply in governance because of majority stakes, while the latter must rely on persuasion and contract design. Third, the typology clarifies that the boundary conditions for family ownership of SFOs are likely to function as an enabler or barrier. Family control and emotional attachment are more likely to foster enabling impact intention translation in a portfolio company when coupled with either strong relational engagement (Hands‑on Controllers) or robust impact structures (Embedded Stewards). Conversely, these same FIBER dimensions may become barriers for impact intention translation when they are not combined with mechanisms that confront risk aversion.

Theoretical Contributions

Our study makes two main theoretical contributions. First, we contribute to research on SFOs and impact investing by developing a typology of SFO impact translation logics. Prior research has emphasized that SFOs are important, yet under‑studied, actors in sustainable and impact‑oriented investing (e.g., Bierl & Kammerlander, 2019; Block et al., 2019; Hayoz et al. 2025; Schickinger et al., 2023). We extend this work by illustrating that SFOs with similar impact intentions may differ in how these intentions are translated into outcomes in portfolio companies. Building on our identification of four impact translation strategies, three barriers, and two enabling mechanisms, the SFO typology explains how different combinations of ownership/control and formality shape the translation process. In doing so, we move beyond whether SFOs pursue impact to explain how they seek to realize impact through value alignment, governance structures, relational operations, and active ownership involvement.

Second, we contribute to the SEW literature (Calabrò et al., 2026; Gómez-Mejía et al., 2007) by extending our understanding of how family-based non-financial priorities play a role at the SFO–portfolio company interface before and after investment. Drawing on the SEW perspective and using FIBER as a sensitizing framework (Berrone et al., 2012), we reveal how SEW dimensions play out in multi-firm investment structures such as SFOs. This extends the SEW literature beyond traditional operating family firms and clarifies how the FIBER dimensions family control, identification, binding social ties, emotional attachment, and renewal can both enable and constrain the translation of impact intentions into desired outcomes (e.g., Kammerlander, 2022). In so doing, we respond to recent calls to better understand SEW considerations in SFOs’ organizational arrangements, risk behaviors, and investment strategies (e.g., De Massis et al., 2021; Hayoz et al., 2025; Mismetti et al., 2024). Further, we consider the views of both the SFO and the portfolio company, thereby offering a dual-perspective approach that emphasizes the relational, rather than the transactional, nature that has dominated previous impact investing research (Barber et al., 2021; Berk & Van Binsbergen, 2025; Bugg-Levine & Emerson, 2011).