Abstract

Despite their role in triggering economic crises, banks remain powerful, influential, and profitable. This study examines how large US banks responded to reputational threats following the 2008 financial crisis. Analyzing shareholder letters from 2000 to 2019, I find that while all banks initially followed traditional impression management tactics, large successful firms like JPMorgan Chase and Wells Fargo shifted strategies during the crisis. They began to use patriotic rhetoric to defend the financial sector as a whole, and they attempted to link patriotism, democracy, and capitalism. The analysis shows how firms use cultural appeals to maintain legitimacy and navigate public backlash during periods of heightened regulatory and societal pressure. More importantly, the findings speak to the current US economic and political environment where we are witnessing tightening linkages between nationalism and capitalism.

Introduction

The 2008 financial crisis arose from a culmination of economic changes: the neoliberal turn, financial market expansion (Krippner, 2005), shadow banking (Thiemann, 2018), new financial instruments (Funk and Hirschman, 2014), and uncertainty of risk and risk scoring (Carruthers, 2013; Langley, 2008). The crisis destabilized the global financial system, and individuals had to manage the impact to their everyday lives. Due to the crisis, the US unemployment rate doubled (Cunningham, 2018) and there were nearly 4 million foreclosures (Dharmasankar and Mazumder, 2016). Despite financial institutions’ role in the crisis, banks remain exceptionally profitable, and if anything, the Great Recession enabled some to become larger and more influential due to acquisitions and market share absorption of their failed peers. How do these organizations maintain their credibility and influence in the face of criticism for their role in crises?

Organizations are adaptive and attempt to both fit within and shape the environment where they operate (King, 2017). The Great Recession prompted regulatory changes and increased scrutiny of financial institutions, threatening their authority and respected position. Reputation is important for most big businesses (Fombrun and Shanley, 1990; Vig et al., 2017), but especially for finance because the nature of the relationship with customers is ongoing (Beckert, 2016). Not only were the financial institutions concerned about rebuilding public trust, but they recognized that if their financial and economic expertise was in question, then their legislative influence would also be diminished. Banks needed to quickly prove that they were trustworthy so that they could influence the direction of new legislation that would be punitive towards them. Essentially, the financial crisis threatened more than their earnings; they now needed to address the public backlash against finance and capitalism.

This paper sheds light on how banks navigated their public image after the financial crisis and provides insight into a broader question about the durability of capitalism. Nearly 20 years post-crisis from the vantage point of the current political and economic climate, this analysis comes at a time when the government is pivoting towards big business interests again. Capitalist motivations fueled both the Great Depression and the more recent Great Recession, yet capitalism endures. Despite the temporary fall from grace, finance is still central to capitalist accumulation and the global economy (Crouch, 2011). Past research in sociology looks at the broader environment of markets and regulations that impact the power of financial institutions (Carruthers, 2015; Davis, 2009; Davis and Kim, 2015; Fink, 2023; Knorr Cetina and Bruegger, 2002; Krippner, 2011). Organizational studies have also investigated the use of cultural and rhetorical arguments used by organizations to build their own image (Sillince, 2006; Suddaby and Greenwood, 2005). These works lay the foundation for the present study, which looks into the explicit efforts of firms to influence the public’s perception.

I analyze shareholder letters from 2000 to 2019 from four small regional banks and four large US banks: JPMorgan Chase, Bank of America, Citibank, and Wells Fargo. I find that the financial crisis pushed them to use their letters in different ways, depending on their relative stability. Prior to 2008, all the letters followed expected impression management tactics, but throughout the crisis and recovery, the more successful firms adopted patriotic rhetoric. Although it is not surprising that they would draw on cultural subjectivities as a defense mechanism, what is surprising is the way they used it. They used American ideals and tropes to moralize their work and the capitalist system.

The following sections describe how businesses often use impression management, and the subsequent sections outline the detailed discourse analysis of bank shareholder letters. I conclude by linking my findings to previous arguments about the ways that firms coopt ideas of “ethics” or “pro-social” claims to bolster their own image, but I expand on those findings by arguing that when the broader system of capitalism is in danger, banks with the most power make patriotic cultural appeals to save it. The discussion section highlights how these findings align with the general trend of increasing intensity of nationalistic rhetoric, as exemplified with the second rise of Trump. Additionally, this study is a reminder that the largest commercial banks rely on free market ideology and decreased oversight, reflecting a familiar pattern that we have seen of the capitalist class resisting punitive legislation (Volscho, 2017).

Impression management and legitimacy

Why does an organization’s image matter? Legitimacy and positive reputations allow firms to access more capital and stability. Organizational legitimacy, as Suchman (1995: 574) defines it, is the “perception or assumption that the actions of an entity are desirable, proper, or appropriate” given the context. Past research has examined how organizations and institutions establish and maintain legitimacy (Doh et al., 2010; Esthappan, 2024; Johnson et al., 2006; Suchman, 1995, p. 199). Legitimacy and trust are especially important for financial firms since they do not necessarily have an “item” to sell; their product is their knowledge, access to markets, and ability to provide the financial services that customers need. Banks rely on investors and consumers to buy into what they do so that they can have a steady inflow of capital to fund their business ventures (Van der Zwan, 2014). Confidence influences how people act (Swedberg, 2010), which makes legitimacy exceptionally vital.

Legitimacy is both contingent on the actions of the firm and on the public that confers it (Deephouse et al., 2017: 201; Schoon, 2022: 2). Thus, powerful private firms use different approaches to actively influence the public’s perception. Legitimacy, status, and reputation are important for organizations because they can strengthen firms and aid them in maintaining stability and profitability in tumultuous environments. Legitimacy is established through conformity to expectations, whereas organizations’ reputations are more specifically tied to their “social identity” (King and Whetten, 2008). And, status goes a step further by accounting for an organization’s position within the industry (Podolny, 2010). By adding reputation (“identity”) and status (“position in the hierarchy”) to legitimacy (conforming to expectations), we get a better understanding of the social environment that organizations operate in.

One strategy for protecting organizational reputations that is examined in business and communications research is impression management (IM), which is based on work by Goffman (1959, 1963). IM was originally used to study individuals within organizations and how people attempt to avoid embarrassment (Goffman, 1959) or avoid stigma and “spoiled identities” (Goffman, 1963). During the 1980s, research began to apply the theories to organizations because they found that firms behave in similar ways (Carter, 2006; Elsbach, 2003; Gardner and Martinko, 1988; Schlenker, 1980). A review of organizational IM shows that firms often use defensive language (such as telling stories, apologizing, making excuses or justifications) when they must explain poor performance (Bolino et al., 2008). The application of IM theories argue that organizations attempt to influence their audiences to view them in favorable ways to further the firms’ own interests.

Firms can use press releases, interviews, annual reports, or their websites to try and build trust and their identity. For instance, websites often use “corporate storytelling” to strengthen their brand and relationship with their audience (Spear and Roper, 2013). Positive reputations are beneficial to firms because they allow them to attract capital and employees, but in times of crisis, good reputations can also protect organizations from negative public perceptions (Coombs and Holladay, 2006; Highhouse et al., 2009; Roberts and Dowling, 2002). Firms with weaker reputations are more susceptible to the negative impact of public scrutiny and more vulnerable to regulation. For instance, firms that use corporate social responsibility rhetoric can better handle negative scrutiny in difficult operating environments (Rim and Ferguson, 2020; Tata and Prasad, 2015).

Furthermore, there is evidence that public press releases can improve the confidence of investors (Henry, 2008), and shareholder letters have a similar function in that they intend to influence the public to trust them in both stable and tumultuous times (Poole, 2016). Graphs in shareholder annual reports are often presented in strategic ways so that they appear more successful to the audience (Beattie and Jones, 2000; Falschlunger et al., 2015). Examining graphs are useful to quantify trends, but an interesting aspect about shareholder letters is the personality that they try to convey. Shareholder letters offer an opportunity to instill confidence in investors and consumers. When experiencing growth, firms highlight their actions that led to successes, but in downturns, they rely on tactics of denial, obfuscation, or offer apologies to rebuild their reputations (Coombs, 2007; Ogden and Clarke, 2005). Others have shown that firms also attempt to increase the sincerity in their tone and show optimism about the future to reassure stakeholders (Patelli and Pedrini, 2014; Poole, 2016). Another study of bank public relations during the crisis shows that firms that were better able to maintain confidence in the public also fared better in the financial downturn (Hearit, 2018). It is unclear if financial performance was a result of more effective communication or if stronger financial performance allowed banks the space to be more assertive publicly.

Impression management theories suggest that firms strategically shape their image to gain influence or increase profits. One common tactic firms use with IM is to compare their performance with others in the industry. Since the economic environment is competitive, they are trying to stand out. Although there are organizations like Business Roundtable and the American Bankers Association that bring these competing firms together, they are still working to advance their own companies. There is some evidence that CEOs will say positive things about other firms in the industry to boost the reputation of others (Westphal et al., 2012), but IM theories do not speak to broader impacts at the industry level or the economic field, which includes regulators. The IM literature shows that organizations attempt to shape perceptions, and some research shows that firms use cultural repertoires to manage their image.

Merging culture and neoliberal ideology

The previous section outlined why firms care about their image: legitimacy equates to more access to capital and stability. Thus, when financial firms were faced with an economic and reputational crisis during the Great Recession, they needed to expand their impression management tactics to protect their broader interests of the system. Deregulation that occurred throughout the prior decades enabled banks to grow larger and profit more, so the prospect of punishing laws threatened their operations. From IM theories, we know that firms try to influence the public’s perception of firm actions and sometimes the actions of others in the industry, but firms exist in a broader complex field. What morals, values, and behaviors must they tap into to garner support? IM research shows that organizations craft narratives that emphasize good work and deflect the bad, so one would hypothesize that these trends would be amplified in times of crisis. However, there are other cultural schemas that corporations could tap into, and in this section, I discuss how neoliberal ideology has become linked to culture in the US, which creates the potential to use neoliberalism as a cultural defense.

In the US, ideas of unfettered free markets and competition are paramount (Block, 2010). There is already an expanse of analyses and explanations about the development of neoliberalism (Campbell, 2010; Centeno and Cohen, 2012; Harvey, 2005; Volscho, 2017), and in this article, I focus on ideas about neoliberal ideology put forth by Mudge (2008), who argues that the term has intellectual, bureaucratic, and political meanings. The first two meanings are associated with the rise of American-based economic expertise (see also Fourcade, 2009) and regulations that support competition (see also Amable, 2011). However, Mudge argues that the political “face” of neoliberalism pushes the state to protect markets in a way that favors business and finance and disregards workers. Mudge’s theoretical framing of neoliberalism is useful because it encompasses some of the ideological work that goes into supporting a neoliberal capitalist system; one of the ways that the state maintains support for it is through perpetuating ideas of freedom and individual responsibility. Others, like Quinn (2019), have shown that financial markets have played an important role in political policy making.

The US state has entrenched a neoliberal capitalist system by making markets appear to be both rational and moral (Fourcade and Healy, 2007). Market logic relies on values of individualism, freedom, and fairness, and the state has contributed to the project of neoliberalism by propagating those values (Amable, 2011), and markets value self-control and self-regulation as much as they value efficiency (Fourcade and Healy, 2007). This change is evident in political speeches; presidential speeches have reflected these morals of responsibility and free markets, even in times of crisis (Coskuner-Balli, 2020). As another example, Powell (1971) was appointed to the Supreme Court in the 1970s, and shortly after appointment, his memorandum was found and shared to the public. That memo explicitly decried the attacks on capitalism and big corporations coming from the media and public, and Powell’s Supreme Court career reflected this positioning.

To make deregulation and neoliberalism more palatable to the public, these ideas had to be tied to cultural values. We see a reinforcing pattern too; the government perpetuates these beliefs, people internalize them, and in turn the public then demands that the government adhere to these tenets. The shifts in the 1980s were coupled with a return to ideas of morality and religion, and the terrorist attacks in the US in 2001 accelerated these changes (Milich, 2006). There are inherent risks associated with capitalism, and culture plays a role in the perception and reaction to them (Beck, 2009; Dake, 1992). Culture is an important aspect that influences behavior and the public’s perception of firm actions (Schurman and Munro, 2009). Thus, in the face of crisis, public figures want to draw on the values of the national milieu.

Large firms have used rhetoric and public campaigns to influence opinions, such as during the rise of unions in the Progressive era (Hulden, 2023) or in response to New Deal legislation (Kruse, 2016; Phillips-Fein, 2009). Even after the crisis in 1929, the New York Stock Exchange still managed to be part of the regulatory decisions in the aftermath (Ott, 2011). Public support is tied to legislative support, meaning firms face less resistance against their regulatory opinions when they have public trust, so these efforts are worthwhile to them. The Great Recession left banks scrambling for legitimation strategies to support them in an extreme downturn in public opinion, and they needed to tap into strategies to moralize themselves. The IM literature shows ways that firms attempt to shape their image and put a human face to business, but we know less about the ways they protect themselves with moral arguments and rhetoric.

Data and methods

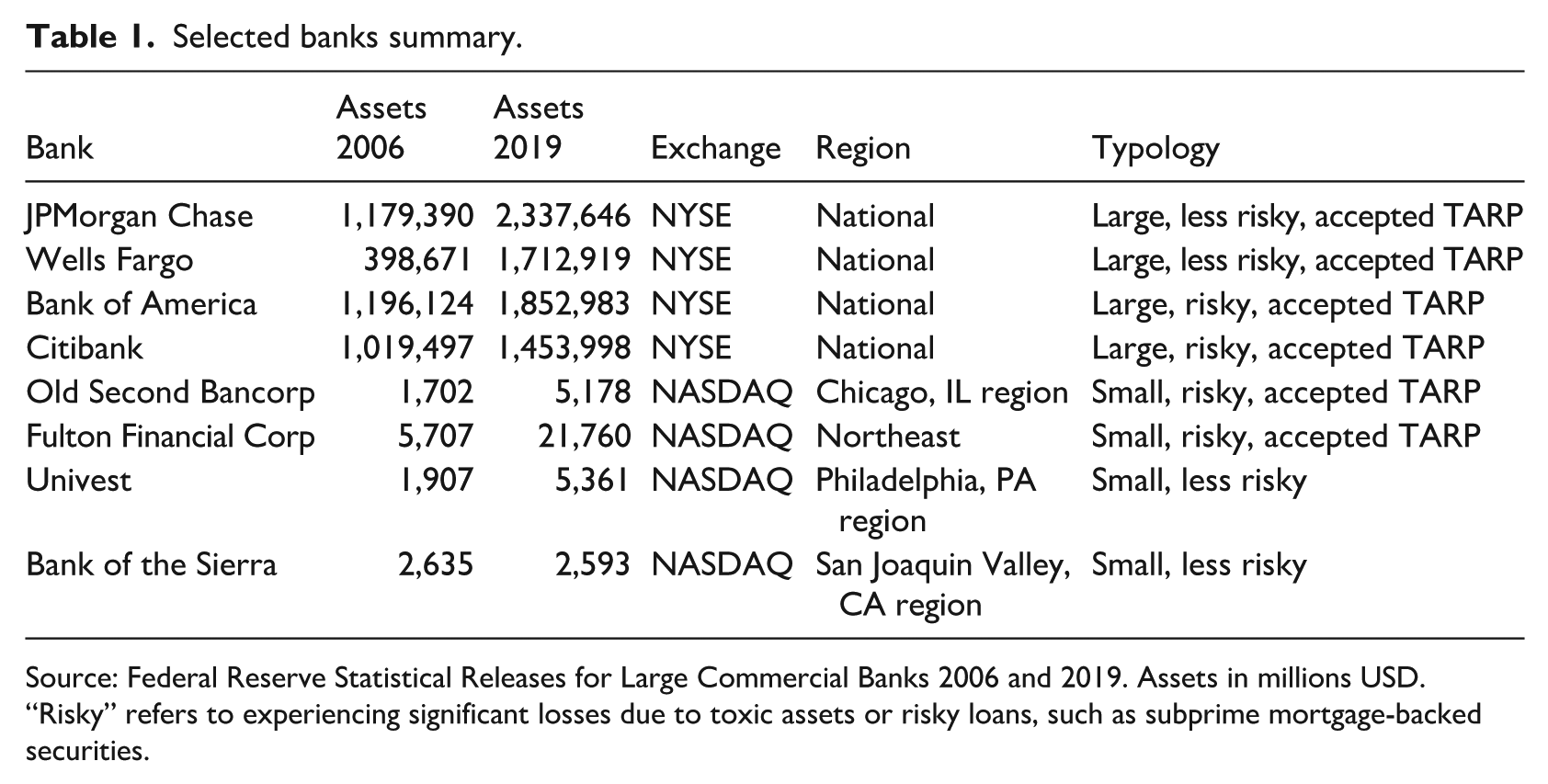

The research question focuses on how banks responded to the financial crisis and the crisis of legitimacy, so I analyzed 122 shareholder letters from eight financial institutions. Case selection proceeded based on insight from Gerring (2017) regarding diverse types and intrinsic importance. Diverse cases capture the variation in relevant criteria, such as the size of bank assets and regional presence. Cases that are “intrinsically important” mean that they are chosen because of their influence on critical events or outcomes, such as the largest banks in the financial crisis. I selected cases based on two main spectrums: riskiness and size. Thus, I selected two banks that are large and risky, large and less risky, small and risky, and small and less risky. By looking at banks that exist in different ends of the two spectrums, I can answer questions about whether trends are based on size, riskiness, or both.

The key analytical cases are JPMorgan Chase (JPMC) and Wells Fargo because both are large financial services firms that emerged from the Great Recession larger and more profitable than before, so large and less risky. Although both firms accepted Troubled Asset Relief Program (TARP) funds, they both repaid them and maintained steady earnings throughout the crisis. Despite this more positive position, they still had to grapple with the negative public sentiments towards their industry. In addition, the cases are comparable to each other since they both benefitted from deregulation and experienced substantial mergers and acquisitions in the decade prior to the crisis, and they both absorbed failing banks during it. The banks are comparable in size and influence; both are one of the “big four” largest banks in the US based on assets.

In contrast, the other two banks of the “big four”—Bank of America (BofA) and Citibank (Citi)—suffered major losses and critical public opinion, so I examine these two banks to compare to the more “successful” ones. These two banks accepted the largest disbursement of TARP funds ($45 billion each), and they required additional government support. These two serve as a direct contrast to JPMC and Wells Fargo since these four banks were similar in size and influence prior to the crisis, but BofA and Citi had taken on more losses as a result of their higher-risk investments, such as subprime mortgage securitization (Citigroup, 2024). Given that the financial crisis created a backlash against very large banks that were “too big to fail,” I also analyzed shareholder letters from smaller regional banks: Bank of the Sierra (2024) (California), Univest Financial Corporation (Pennsylvania), Fulton Financial Corporation, and Old Second Bancorp (2024). These banks are traded on the NASDAQ (publicly traded, so there are shareholder letters) and had less than $10 billion in total assets in 2006. As another dimension of diversity, Sierra and Univest did not accept TARP funds from the federal government, Fulton accepted and repaid the money, and Old Second accepted and repaid only some of the federal funds. You can see this information summarized in Table 1 below.

Selected banks summary.

Source: Federal Reserve Statistical Releases for Large Commercial Banks 2006 and 2019. Assets in millions USD.

“Risky” refers to experiencing significant losses due to toxic assets or risky loans, such as subprime mortgage-backed securities.

These smaller banks are not “too big to fail,” and they also have less capital, which often encourages them to take on less risk (Shen and Hartarska, 2018). Localities with a higher density of community-focused financial institutions were more resilient in the financial crisis (Schneiberg and Parmentier, 2022), which may have protected them from the backlash directed towards large banks. Smaller banks that did not accept Troubled Asset Relief Program (TARP) funds provide an ideal type of comparison to the larger banks more generally because these banks argue that they are more local and can claim that they did not need a taxpayer “bailout.” Their shareholder letters should reflect this more positive position, making the letters a key comparison for the larger banks. I also include TARP-accepting small banks because they were struggling like large banks but faced less public scrutiny. These letters provide a better comparison of shareholder letter usage among small banks.

Literature on impression management emphasizes how firms use shareholder letters as opportunities to instill confidence. They are typically signed by the CEO or management team and released annually, and they are included at the beginning of a company’s annual financial report. The full reports are distributed to shareholders and investors and summarize financial data and follow the Generally Accepted Accounting Principles (GAAP), so many annual reports are structured in similar ways. The reports are vital documents for the company and attaching the letter to the front of them signals their own importance. Although companies are required to share financial reporting, they are not obligated to write a shareholder letter, so the information that they include reflect how they want to shape their “social identity.” These letters are flexible yet consistent, making them informative data to answer questions about changes in tactics and rhetoric over time. Although annual letters are these organizations’ polished public presentations of themselves, they provide valuable insight into the firm. Previous literature shows that firms use public communications to establish and maintain trust and confidence in their organizations. The intended audience is their shareholders and customers, but they are also circulated for the public and reported on by the media.

As noted above, these letters are voluntarily written and circulated by the firm, so formatting differs. Just as the content reflects the individual goals of the firms, the formatting is a stylistic choice that each makes. For example, some years there are more photos of employees and customers interacting and other years, they focus on graphs. The images can often aid in deciphering what character the firms want to publish, making qualitative discourse analysis an ideal method. The length of the letters varies between the firms. Wells Fargo’s are consistently around seven pages, and the smaller banks are only three pages on average. JPMC consistently increased over the period of study to 50 pages.

Although automated textual analyses can provide valuable insight into general patterns, this research focuses on rhetorical changes in structured shareholder letters. Given that much of these letters are dedicated to a summary of the company’s revenue and financial initiatives, some of the rhetorical nuances may be buried within the text, and thus, qualitative close reading is better suited to detect subtle changes. Discourse analysis is fitting for the data since the research question focuses on how these firms dealt with the risks associated with capitalism and then how they attempt to restore trust in the system. As others have noted (Friedline et al., 2024; Lazar, 2007), discourse analysis can be used to uncover power dynamics in the language used.

Discourse analysis is an iterative process, which can involve rounds of coding based on the theoretical and empirical information available. Given the broad interests in the change in rhetoric after the financial crisis and prior knowledge regarding the usage of shareholder letters, I did an initial deep reading of the documents and noted the broader themes, such as the economic environment, company structure, company culture, and risk. I first coded for repeated observations and grouped them within these broader themes. This process aligns with Reyes et al.’s (2021) suggestion to have a “living codebook” where one begins with initial codes, but then identifies patterns and writes memos to focus on codes that answer the theoretical question at hand. In the second stage of coding, I reread the letters and consolidated and refined codes.

Timmermans and Tavory (2012) promote “abductive” analysis, which aims to construct theory from surprising findings in the data. Given the background literature about impression management, much of the information in the letters aligned with previous work. Thus, for this paper I focus on one of the more unexpected emergent codes. Deep reading of the letters revealed a new tactic used by JPMC and Wells Fargo that was unexpected given the previous literature for impression management. These firms incorporated patriotic rhetoric into their letters, which was rare in letters prior to the financial crisis. Once I added a code for patriotism/nationalism, I went back and recoded the letters in relation to this theme. Shareholder letters are intended to highlight a firm’s own accomplishments and deflect negatives; thus, I would hypothesize that the financial crisis would amplify these routine tactics. I find that the firms responded as expected, but I discover that JPMorgan and Wells Fargo also incorporated patriotic and nationalistic rhetoric as a defensive tactic at two levels: the financial industry and capitalism more broadly. The financial crisis threatened the reputation of finance and capitalism, causing JPMC and Wells Fargo to react and defend the broader system. These two large banks were also relatively successful during the crisis, meaning that they may have had the space and authority to defend the industry.

Findings

Prior to the financial crisis, firms used their shareholder letters in line with impression management arguments noted in past literature. Letters typically focused on growth and profit, and in this period, many banks were rapidly expanding via acquisitions in addition to attracting new customers. The earlier shareholder letters attempt to establish trust and credibility in these firms. All banks emphasize growth, acknowledge disappointments, and express optimism. As mentioned above, there is evidence that these reports are designed to cast the firm in a favorable light to gain public confidence, and one effective strategy is showing quantitative data that the firm is making progress. They focus on growth to reassure customers and shareholders that they are a reliable investment, and they use it as a measurement of their success. They also emphasize their commitment to their customers and the communities where they operate, trying to build a favorable public image. These typical impression management aspects are present in subsequent letters as well, but the financial crisis prompted a key change in the large banks that did not suffer as much from problems with mortgage-backed securities.

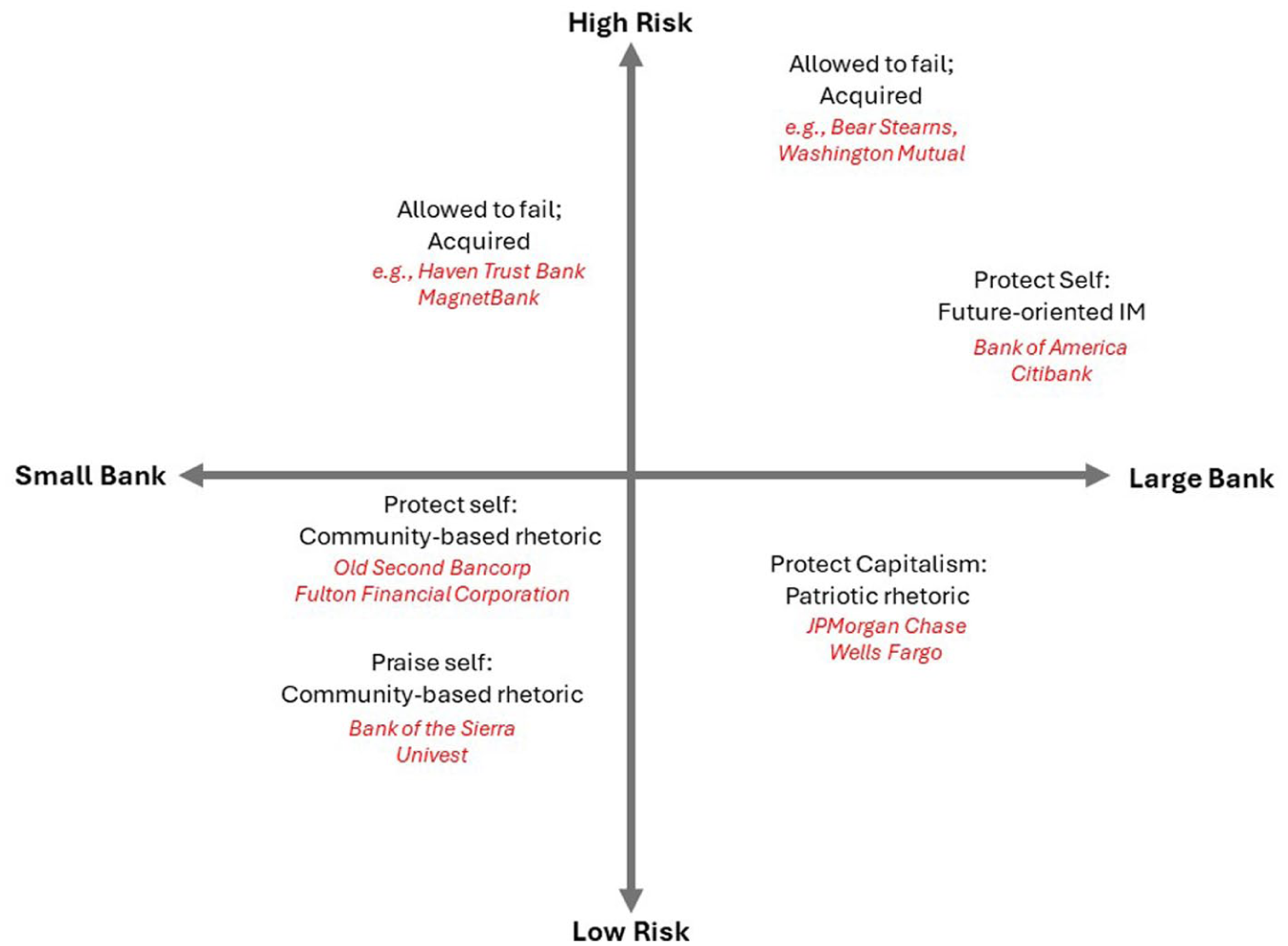

The key findings are summarized in Figure 1 below, which shows how the banks used their shareholder letters in response to the crisis. The analysis reveals a new trend in the use of annual shareholder letters for large firms that performed well during the crisis, whereas the other banks relied on the standard repertoire of impression management tactics.

Analysis summary.

The main argument from the findings is that after the crisis JPMorgan Chase and Wells Fargo introduced more patriotic and nationalistic rhetoric and developed a more general defense of the capitalist system. I argue that these firms expanded the use of their letters to defend not only themselves but to protect the financial industry and capitalism more broadly, in ways unaccounted for in other impression management research or organizational theories. Larger banks that faced severe losses continued to use their letters to protect themselves from criticism by noting how they will perform better in the future, and the smaller, safe banks contrasted their stability to the instability of the broader industry. The respective future-oriented statements and self-praise align with impression management tactics, but the transition to nationalistic rhetoric and concern about the broader system does not. The following subsection briefly describes the tactics used by all banks during and after the crisis, and the next subsections focus on the unique changes in JPMC and Wells Fargo.

Protecting the firm: Impression management

All the banks in the analysis use impression management tactics, as described above. IM focuses on individual strategies, so firms use these narratives to protect their own image in the eyes of their stakeholders and the public. The banks needed to shore up confidence to protect themselves from more losses from investors and shareholders and restore their “spoiled identities” (Goffman, 1963). All banks, whether they were struggling or not, needed to address the magnitude of the financial crisis. The more stable banks (JPMC, Wells Fargo, and the regional non-TARP accepting banks) denied culpability of the crisis, and each noted how they made “smarter” or “safer” investments. They compared their stability to their peers that were floundering or failing and reassured stakeholders and customers that they were managing risk well.

One common tactic of IM is to differentiate an organization from the rest in the industry, and the financial crisis created more cause for banks to distance themselves from their failing peers. For instance, Bank of Sierra emphasizes their “discipline” as the reason for avoiding many of the struggles faced in the banking industry. Similarly, Univest (2009) said that “it wasn’t easy to instill a sense of security during a time of negative economic reports, long-time competitors experienced financial difficulty and record numbers of banks failed – 140 in 2009” (p. 4). And Wells Fargo (2009) said that they are “not a hedge fund disguised as a bank” (p. 7) in a way to distance themselves from failing larger banks and emphasize their difference. Old Second, the smaller bank that did not fully repay TARP funds, noted that they are struggling in 2007 and 2008 letters, but also emphasized that others in the industry are doing worse.

Fulton and Old Second banks struggled more than the other two smaller banks, and because it was more difficult to distance themselves from the industry, they emphasized that they are merely experiencing the same issues that other banks are. Old Second mentions how the entire industry was facing challenges, and Fulton argued that banking is inherently a cyclical business facing a downswing. Interestingly, after 2012 when Old Second did not fully repay the TARP money, the bank stopped having formal shareholder letters, and their annual report is their federal required annual report filing and not a tailored letter. Perhaps given the fact that they are regional and also risky, they had few options to defend themselves and opted to say less, which is an interesting contrast to the large and more successful banks that said more than usual during this time.

BofA and Citi experienced significant losses and backlash for poor risk management, so it was more difficult for them to create space between them and the crisis. They both attempted to highlight their own efforts at stabilization and outlined the actions that they are taking, such as building capital. These two banks relied on a different, but common, IM tactic in which they blame the environment rather than themselves for the economic downturn, which is also present in the struggling regional banks. In 2008, Bank of America said that the “story of how we got here is the story of every great economic bubble in history. Every group of participants in the economy — lenders, borrowers, regulators, policy makers, appraisers, rating agencies, investors, investment bankers — had a motive to push the cycle forward, and most did” (p. 8). This quote first reiterates that this was a typical case of a bubble bursting, and then it casts blame on all group involved to diminish the blame on themselves. Similarly, in 2009, Citi said more succinctly that the “key issues affecting short-term earnings are not internal but environmental” (p. vi).

Another common IM strategy used by all firms in the analysis was to signal commitment to consumers, which is supposed to create an image that cares about society rather than just their bottom-line. This pattern is prevalent in all the shareholder letters, even those prior to the crisis, but banks highlighted their societal benefits post-crisis even more as a way to bolster their public image. Although JPMC and Wells Fargo had more limited losses, the general public was critical of their successes since the country was struggling. Thus, these firms emphasized how they were helping people. In 2009, JPMC noted that they “took a leadership role in helping American homeowners through the most difficult housing market of a generation. . . These efforts have allowed us to begin the mortgage modification process for nearly 600,000 homeowners” (p. 9). Similarly, Wells Fargo (2009) says that they “helped 1.2 million mortgage customers reduce their payments through refinancing and modified mortgage payments for 470,000 customers so they could stay in their homes” (p. 8). They also specify the amount of loans they offered during the crisis and point out how other banks were not offering as much credit. These statements try to prove that they are doing their part to help the people.

The regional banks also noted how they continued to serve local customers and distanced themselves from the larger commercial banks. In 2009, Univest argued that people were switching to them because there was general distrust in larger banks and said “[our] visibility and reputation as a dependable, service-oriented community-oriented bank positioned us well to gain new market share” (p. 5). Fulton Financial Corporation (2009) noted that the press and public opinion around the financial services industry was very negative, and therefore, they reiterated that their “commitment to local community banking is more important than ever” (p. 6). The regional banks that did not need to accept Troubled Asset Relief Program (TARP) funds noted this fact and emphasized that they are well-capitalized and continue to serve their customers. Their response to the crisis was to differentiate and praise themselves for not being embroiled in the bigger problem, which aligns with IM strategies.

For banks that successfully weathered the crisis—especially the larger ones—they used their actions as evidence that they are “good.” They claim that their successful position among their competition proves that they are responsible, reliable, and worthy of being in the business. These tactics align with previous research on impression management and reputation maintenance since they highlight ways that they are novel and important. These firms attribute their success to their customers and devotion to communities, and this strategy is interesting because they are trying to tie themselves to communities to evade some public criticism of their connection to the financial crisis.

Despite their role in the subprime mortgage crisis, BofA and Citi still tried to connect with the communities and customers to bolster their tarnished image. Bank of America (2011) highlights that they “have modified more mortgage loans than any other servicer: More than 1 million homeowners have been helped” (p. 4), and they try to portray this in a way that puts them in a positive light. However, their acquisition of Countrywide Financial included many subprime mortgages, which created the need to modify them. Amid the crisis, Citi and BofA use future-oriented language and discuss how they are taking actions to improve the well-being of their customers. Since they cannot adequately speak to helping people in the present, they reorient themselves to talk about what they will do.

Bank of America and Citi used IM in a way to deflect and protect themselves from criticism of their role in the financial crisis. Although the smaller regional banks performed relatively well, they also used traditional IM to boost their own status and highlight their stability. JPMorgan Chase and Wells Fargo also used IM similarly to the other banks. They wanted to show that they were not at fault and that they were relatively profitable during the peak of the crisis. However, there is a key difference: JPMC and Wells Fargo move beyond impression management to make a broader argument to protect the financial industry and capitalism. The following subsections discuss these findings and focus on these two firms.

Defending the industry: Financing job growth

The analysis shows an increase in patriotic rhetoric that links Americans, finance, and regulations together in JPMorgan Chase and Wells Fargo’s letters. Essentially, their argument is that finance allows for Americans to take risks and achieve their dreams, so regulators should consider laws that can help protect consumers but also allow firms room to maneuver. Both firms began to utilize patriotic rhetoric to bolster public opinion around the financial industry as a whole. They argue that some actors in the financial industry took high risks and made consequential errors, but that overall, finance benefits Americans. The letters advocate support for “good” banks and fair, not vindictive, legislation.

As noted above, all the banks tried to show how they played an important role in supporting communities and customers, such as offering credit or modifying mortgage payments, but JPMC and Wells Fargo go further to defend finance in general. In the aftermath of the crisis when public opinion of banks was low, they describe how big banks are useful for the recovery and individual Americans. They state that they are key to recovery and financial well-being because they offer credit and loans that enable businesses to invest, expand, and hire more Americans. In 2011, JPMC says, The reader should understand that loans, a traditional bank function, are proprietary, illiquid and risky by their nature – but that doesn’t make them bad. And most banks that have gone bankrupt did so by making bad loans – not by trading. Loans and market making both serve a critical function: financing the American business machine. (p. 36)

This quote directly states how the firm sees their role in the economy. In the same year, Wells Fargo states that “no financial product is more important to Americans, more interwoven with their financial security, than their home mortgage” (p. 3). Both firms are signaling that the products and services they offer are essential, and in the US, they are by design.

A few years post crisis these two banks state the economic recovery relies on employment expansion, and that regulations that enable banks to offer more credit will facilitate that growth. In the face of new legislation, both banks use the general argument that credit enables job growth. The two quotes below exemplify how these banks see themselves and credit providers as important pieces of the US economy.

Negative home equity, depressed housing prices, and mortgage foreclosures are not the cause of our sluggish economy. They’re the result of homeowners losing their jobs. . . . Many of our small business and commercial customers have the cash and resources to rehire and expand, but there’s hesitation because of the legislative and regulatory landscape, customer spending habits, and government debt. This can paralyze and confuse business owners, entrepreneurs, investors, and consumers. Government and private enterprise need to stand together to alleviate this uncertainty by promoting fiscal discipline and economic opportunity. (Wells Fargo, 2010: 8) One thing we know for sure is that capital expenditures and R&D spending drive productivity and innovation, which, ultimately, drive job creation across the entire economy. . . . And without the huge capital investments made by big business, job creation would be a lot less. (JPMorgan Chase, 2011: 9)

These banks claim that they want more government collaboration to create regulations that are favorable for themselves and all Americans. Improving employment is a popular proposal for difficult economic times, and they are trying to appeal to this employment rhetoric by emphasizing their role in “innovation” and business development. By framing themselves as part of the solution, they can make the claim that their business should be more involved in policy creation—for the sake of the people.

Protecting the system: Capitalism is Americanism

Moving beyond protecting their industry, I argue that these two banks use rhetoric of American exceptionalism to protect capitalist interests. The 2011 JPMC quote from above comes from a sub-section in the letter that discusses how small business and big business are “symbiotic.” The penultimate sentence of the section says, “like small businesses, big businesses are philanthropic, patriotic and community minded.” In comparison, there is only a small increase in patriotic rhetoric in all banks’ letters after the September 11th terrorist attacks. Even in additional reviews of the 2002 letters, patriotism was mentioned once by each bank, if at all. When there was concern regarding national safety, they mention American “resilience,” but they do not fawn over America as they do during the financial crisis.

The crisis ushered in heightened skepticism around finance, and the annual letters needed to go beyond firm-level damage control. JPMC and Wells Fargo lean into American entrepreneurial arguments. In 2008, Wells Fargo says that they “continue to believe in the spirit, ingenuity, work ethic, creativity and adaptability of American workers. We’re capitalists and proud of it. We believe in free enterprise. We’re Americans first, bankers second” (p. 8). This sentiment continued in the following year where they proclaim, “our capitalist, free enterprise system — the envy of the world — needs breathing room so Americans can be free to do what they do best: Create and innovate and build and rebuild” (Wells Fargo, 2009: 9). In the same year, JPMorgan Chase (2009) introduced similar sentiments of American entrepreneurialism, saying “America was built on the principles of rugged individualism and self-responsibility. We need to continue to foster a sense of responsibility in all participants in the economy” (p. 36). This statement reflects patriotism, but also places subtle blame on individuals for their financial choices. After the financial crisis, some took aim at individuals for taking subprime loans, not on banks for offering predatory terms, and that quote is also trying to deflect blame from the banks.

Both firms continued using this rhetoric for a few years after the crisis. In 2010, Chase ties Americanism to hard work: “The American people have a great work ethic, from farmers and factory workers to engineers and businessmen (even bankers and CEOs). And it still has the most entrepreneurial population on earth. American ingenuity is alive and well” (p. 7). These ideas of “American ingenuity” are linked to their employment arguments above since they claim to be financing people’s endeavors. Similarly, Wells Fargo (2012) notes the advantages of being in the United States: We are blessed in this country with huge advantages: an abundance of natural resources, especially energy; the best rule of law; a culture of innovators and entrepreneurs; the best post-secondary schools in the world; and the world’s best farmers and manufacturers. The world wants what we produce, and our policies should support that. (p. 9)

They reiterate the “hard work” culture of Americans, but they also link it to the importance of policies. They are praising the US and tying individualistic (i.e., capitalistic) cultural arguments to their business to support their policy preferences.

Interestingly, the two firms diverge after 2013, and Wells Fargo stops using patriotic rhetoric and instead, relies on describing their service for customers and the community to support their status and claims, as noted in the previous subsections. Shareholder letters are reactive, which may explain why Wells Fargo stopped using those tactics after 2012; they may have opted to stop the defensive approach with a friendlier customer-focused one after the Occupy Wall Street movement to seem closer to the “99%.” However, JPMC maintains an aggressive commitment to American capitalism in their letters, even after their 2011 scandal, the “London Whale.” Chase has a more extensive international and investment-based business model though, which may explain the desire to focus their efforts on their Americanness. The rest of this section highlights the 2016 JPMC shareholder letter, which exemplifies how they used patriotism in support of capitalism. I focus on one letter to show the extensive use of patriotism throughout one document (JPMorgan Chase, 2016).

A common approach in the JPMC letters is to praise the US then use these praises to justify corporate involvement in bettering America. This pattern is directly seen before the letter introduces a list of regulatory critiques, in which JPMC first notes that “it would be good to count our blessings. Let’s start with a serious assessment of our strengths” (p. 32). Then the letter outlines what it sees as “strengths” such as a culture of “improving things” and increasing productivity (p. 32). The letter normalizes an individualistic ideology that supports capitalism and emphasizes American pride. Immediately afterward, the letter explicates the issues troubling the country. The bank argues that America is falling behind and slowing in growth, and it places some of the blame on the government, citing wars, lack of spending on infrastructure, poor education, and the corporate tax system. But then the letter situates businesses as an important part in solving these issues, trying to justify corporate involvement in policy-making.

The letter argues that the bank is a proponent for government involvement and wants policies to take initiative for solutions, but they also express general concerns about the organization of government. In a subsection titled “How should the U.S. legal and regulatory systems be reformed to incentivize investment and job creation?” the letter poses questions about the US regulatory system, but they still begin with a reminder of their American Pride: “There are many reasons to be proud of our system of government. The U.S. Constitution is the bedrock of the greatest democracy in the world. The checks and balances put in place by the framers are still powerful limits on each branch’s powers” (p. 41). Then they explain how they see the system is in opposition to businesses, and thus, against entrepreneurship and growth. They provide examples of ways that they think that the Administrative Procedures Act and the Fair and Accurate Credit Transactions Act are unfair. They conclude by saying, To be clear, we need regulators focused on the safety and soundness of all institutions. We need enforcement bodies focused on compliance with the law. But we also need to preserve the system of checks and balances – when you cannot get your day in court on some really important issues, we all suffer. We need to improve and reform our legal system because it is having a chilling impact on business formation, risk taking and entrepreneurship. (p. 42, emphasis added by author)

This quote shows that the bank supports regulation if it aligns with their own goals and maintains the tenets of free enterprise.

In response to public backlash against large banks, the letter tries to persuade readers to consider how financial firms are important for the economy, similar to the section above, but the following examples directly link the importance of American success to capitalist support. JPMC tries to dispel arguments that they see as myths or misinformation and say, “When you read that small businesses and big businesses are pitted against each other or are not good for each other, don’t believe it.” (p. 42). A few paragraphs later, they directly defend capitalism: Something has gone awry in the public’s understanding of business and free enterprise. Whether it is the current environment or the deficiency of education in general, the lack of understanding around free enterprise is astounding. . . We need trust and confidence in our institutions – confidence is the “secret sauce” that, without spending any money, helps the economy grow. A strong and vibrant private sector (including big companies) is good for the average American. Entrepreneurship and free enterprise, with strong ethics and high standards, are worth rooting for, not attacking. (p. 45)

Similar to above where this letter maintains the idea that banks are good for Americans; it is trying to strengthen confidence for big companies more broadly, not just themselves. However most interestingly, they are also trying to protect capitalism. They are pleading for confidence in themselves and capitalism. The letters argue that both the public and the government need to support capitalist interests if they want a strong economy. The banks are aware that capitalism requires a strong central government to enable it to work (Deakin et al., 2017; Harvey, 2005; Quintana, 2020).

Analysis

The analysis summary in Figure 1 shows the different responses found in bank shareholder letters after the financial crisis. The riskier large and small banks relied on typical IM tactics in their shareholder letters to protect themselves. Smaller, regional banks that were stable and did not need to use TARP funds also used IM but to praise themselves. One would expect that large banks that were less risky would also praise themselves, but instead, the results show that JPMorgan Chase and Wells Fargo adopted patriotic rhetoric as a means to protect the capitalist system.

These two firms attempted to build confidence not only in themselves, but in the financial industry and capitalist system more broadly by appealing to American values. They needed trust in the industry to improve their operating environment, and they did that by recasting themselves as quintessential American enterprises. The 5-year period after the peak of the crisis encompassed the rise of the Occupy Wall Street movement, which cast light on the stark inequality that finance had a hand in; CEOs getting paid large bonuses, while the rest of the country struggled, enraged an already disgruntled public. Although companies are more willing to make changes in the face of social movements when there are threats to their stock price (Banerjee and Case, 2020), other research shows that firms with CEOs who are more influential and hold more structural power are associated with smaller organizational changes when there is public criticism (Carberry and Zajac, 2021). We have also seen that states that are more market-focused are less likely to support foreclosure prevention policies, exemplifying this link between ideology and outcomes (Eads, 2024).

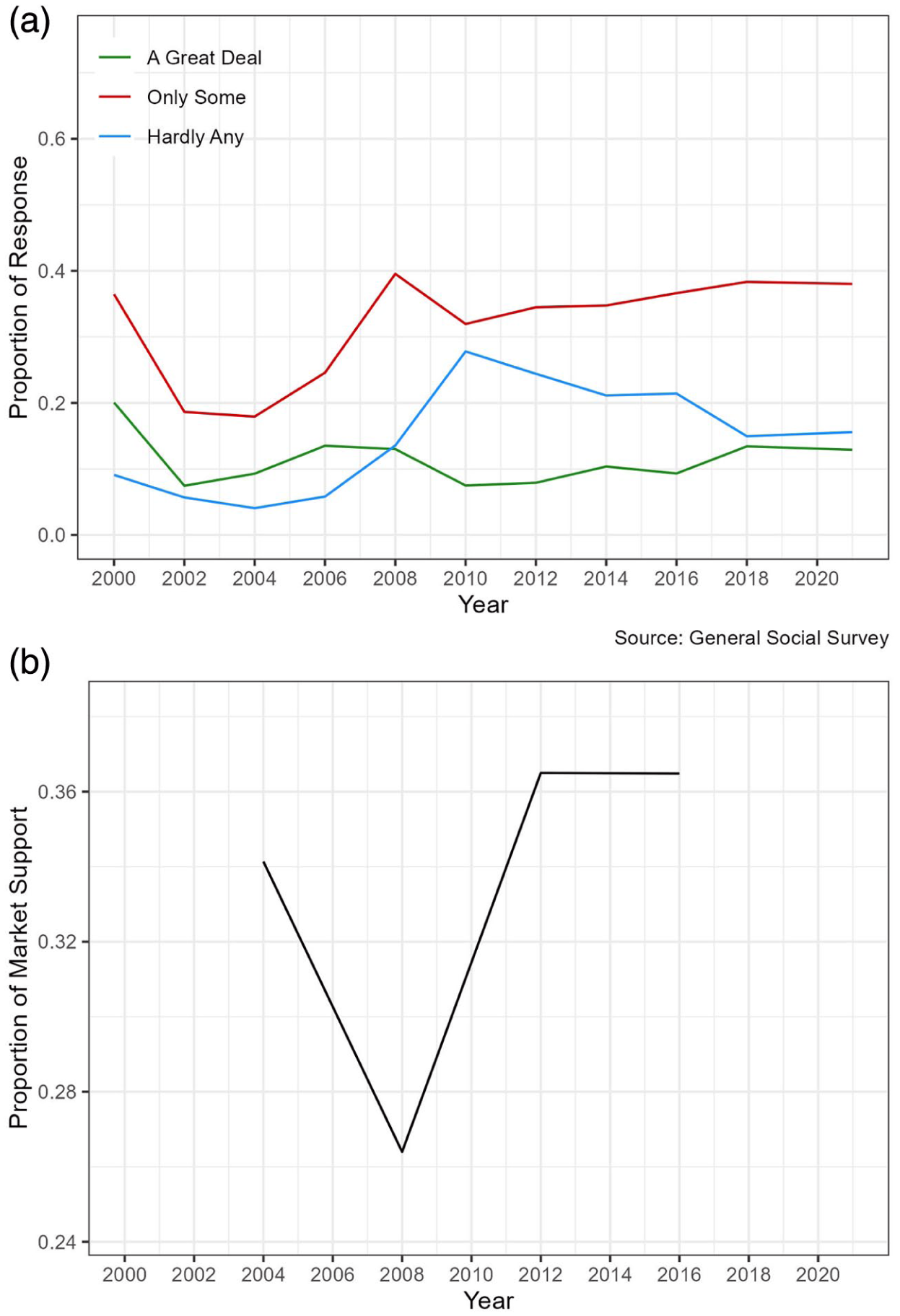

Figures 2(a) and (b) below show the level of confidence respondents had in financial institutions or the market before and after the financial crisis. Figure 2(a) uses data from the General Social Survey from 1990 through 2022 that asks how much confidence people had in banks and financial institutions. As expected, from 2008 to 2010 there is a steep increase in people that said they had “hardly any” confidence in financial institutions (General Social Survey 1972–2022, 2022). Figure 2(b) shows the proportion of respondents who believe that the free market is better at handling complex economic problems compared to a strong government (American National Election Studies, 2022). These data come from the American National Election Studies between 2004 and 2016, and we see a steep drop and then recovery after 2008. Trust in banks and the market is trending upwards again, and it is unclear if the tactics deployed by the banks caused this recovery. However, it is important to note that despite Occupy Wall Street and increased scrutiny, these institutions still managed to rebuild some level of confidence in the public.

(a) Confidence in financial institutions and (b) Confidence in the market compared to the government for managing economic problems.

This study shows how they combatted negative scrutiny by highlighting the role they play in Americans’ lives and well-being. They also framed the problem as one of “bad apples” rather than a problem with capitalism (Hansen and Movahedi, 2010). The shareholder letters are publicly available, and they are also included in media reports that circulate to broad audiences.

The relationship between banks, the economy, and public opinion is complicated, so uncovering a causal link between shareholder letter sentiment and the public is difficult, but we can examine the media discourse surrounding these two cases, similar to Hearit’s study mentioned in the literature review. As the financial sector began to recover, articles began to report on both JPMorgan and Wells Fargo’s thoughts on government involvement in their businesses. One news article title noted that some banks like JPMC and Wells Fargo “want to be left alone” (Bowley and Dash, 2009), and the article reflects the sentiment in JPMC’s 2009 letter that expressed some regret in taking TARP funds when they claimed that they did not necessarily need them.

I know I speak for a number of banks when I say that some of us accepted the Troubled Asset Relief Program (TARP) capital not because we needed it to survive but because we believed we were doing the right thing to help the country and the economy. (p. 26) . . . We did not anticipate the anger or backlash the acceptance of TARP capital would evoke from the public, politicians and the media – but, even with hindsight, I think we would have had to accept TARP capital because doing so was in the best interest of the country (p. 29)

In response to more potential government involvement, these two banks were not going to agree to take any other funds from the government. Another news article discussed how JPMC’s Dimon said that the Durbin Amendment has already hurt JPMorgan (Tse, 2010). These articles show how media reports discussed the banks during and after the crisis, and they show that the thoughts expressed in the letters appear in the media. Past work supports the argument that management actively tries to drive media coverage with their press releases (Tsileponis et al., 2020). As Culpepper and Lee (2022) have shown, media coverage can encourage people to put more pressure on their congressional representatives.

The banks suggest that the reason for economic growth and the US’s global prowess is due to capitalism and argued that proposed regulations were threatening America’s potential. They position themselves as trying to protect American interests and conflate those interests with capitalism. Patriotism is often a tactic used by the right, as evidenced by Trump’s “Make America Great Again” slogan, and Trump’s rhetoric worked at motivating voters (Lamont et al., 2017). Some studies show that individual attachments to the nation can have real impacts on one’s policy opinions and sometimes is tied to more civic engagement (Bonikowski, 2016; Bonikowski and DiMaggio, 2016; Huddy and Khatib, 2007), so the banks’ attempts to strengthen feelings of patriotism could have real impacts on how they are perceived and how the populace feels about new regulations that threaten these capitalist and “patriotic” enterprises. The financial crisis spurred a broader crisis of legitimacy in the capitalist system, so the banks used their resources to maintain the system that benefits them.

Discussion and conclusion

This article investigates the rhetorical tools that the large and less risky financial firms used in the wake of the Great Recession. Large banks rely on the reputation of capitalism more broadly to maintain their power. The firms in this study utilized defensive language (i.e., accounts, apologies, excuses, and justifications) to explain poor performance (Bolino et al., 2008), which are common IM tactics. Yet, impression management does not account for how organizations use their status and reputation to influence the opinions of the broader system. In general, corporate communication strategies remain internally focused on the reputation of a single organization rather than the environment where corporations operate (Cornelissen, 2023). Sociological analyses of organizations offer insight into the structural aspects of organizational behavior by accounting for the networks (Podolny and Page, 1998) and fields (DiMaggio and Powell, 1983; Kluttz and Fligstein, 2016) in which they operate. By combining these two ways of thinking about organizations, we can gain a better understanding of the “strange non-death” of neoliberal capitalism (Crouch, 2011).

The financial crisis coupled with a legitimacy crisis of capitalism prompted banks to explicitly protect the system. According to Volscho (2017), the finance sector orchestrated the neoliberal shift for its own benefit, which eventually led to the financial crisis, and the findings reveal that banks did not want to wait for the recovery to reassert their influence. When banks (and the State) were being held accountable for their role in economic instability, banks like Wells Fargo and JPMorgan Chase attempted to control the narrative in the midst of the crisis to maintain the system that they had worked to create. To shield the legitimacy of capitalism, they linked it to broader American ideological and cultural appeals that were, and continue to be, valued by the general public.

As a system that appears to champion free markets while also creating strong regulations that allow firms to act according to their own interests, neoliberalism requires cooperation between firms and regulators (Centeno and Cohen, 2012; Crouch, 2011). This study moves beyond firms and the government to show that companies control the broader narrative to maintain neoliberal capitalism using strategies that are unaccounted for by IM and other organizational theories. Firms are not just tapping into a cultural repertoire, but rather, they are championing a particular type of culture that ties capitalism to democracy and morality. As Swidler (1986) notes, in “unsettled periods” different cultural meanings are put forth and the “structural and historical opportunities determine which strategies, and thus which cultural systems, succeed” (p. 284). There are cultural schemas that already exist that banks can pull from, and this research shows an interesting pattern where only the large and more successful banks decide to use “patriotic” rhetoric, which is not what they have used in the past. Research on IM and behavioral choices of organizations in the face of backlash show that firms that have previously generated a “prosocial” reputation often do not change their IM tactics because they feel that their past reputation is a bulwark to future criticism (McDonnell and King, 2013). Thus, one would expect that these more successful firms, which had minimal losses and maintain institutional investor confidence would simply rely on the tactics they have always used. Instead, we see that faced with the precarity of their operating environment, they shift their tactics in ways that have been unaccounted for in IM.

Although nationalist appeals are a common tool to influence popular opinion, this study exemplifies the ways that private firms can weaponize it to defend capitalism. Historically, large firms have used cultural ideology to sway the opinions of Americans (Coco, 2014; Kruse, 2016; Phillips-Fein, 2009), and the rise of neoliberalism was paired with perpetuating win-win rhetoric regarding social and economic goals among firms (Brandtner and Bromley, 2022). The writers of the shareholder letters leaned into ideas of “corporate personhood” by making claims that the firms themselves are patriotic and working in the interests of Americans and not only for shareholder value (Collins and Kahn, 2016). In times of crisis, presidential speeches have emphasized values such as individual responsibility and freedom, which support neoliberal policies (Coskuner-Balli, 2020). Firms have a stake in these market policies and seem to use this strategy as well, expanding our understanding of which actors call upon patriotic appeals in this way. There is a link between business, legislation, and American values. The state can perpetuate values such as individual responsibility, freedom, and free markets, and they are building support for neoliberalism by tying it to morals. The firms in this study are coopting that language to build support for themselves; they are trying to signal that they are moral because they are capitalists. Bankers have historically been able to monopolize ideas of “moral authority” (Polillo, 2011), and they can rely on it in times when “technocratic expertise is no longer sufficient to generate legitimacy” (Fourcade and Healy, 2007: 305).

When security and financial crises struck in the 2000s, the project of linking capitalism and democracy was already well-underway (Romano, 2012). The more powerful banks continued this process in their shareholder letters, and then the pattern is mirrored by Congress members. In 2015, a press release titled “Dodd-Frank Act Leaves America Less Stable, Less Prosperous, Less Free” from Republican House Representative French Hill sounds almost indiscernible from the shareholder letters of JPMC or Wells Fargo after the crisis (Hill, 2015). Hill proclaims that the “‘animal spirits’ of free enterprise, entrepreneurial risk-taking and dream-chasing that have identified us as a people are being tamed” by Dodd-Frank, and “[e]conomic freedom fosters these: achievement, productive work, savings, imagination, enterprise.” In Hill’s statements, the sentiments that the regulations put in place after the financial crisis are now causing more issues and do not guarantee financial stability nor prosperity.

In another example, in Trump’s first campaign, he used strong patriotic and nationalistic rhetoric that helped him garner votes. The findings are more important now, in the second era of a Trump presidency, which he won on an “America First” platform. Although the administration is not purely neoliberal due to their views on free trade, they are still encouraging businesses to be free market capitalists. Based on the findings, firms are linking democracy, capitalism, and patriotism, and given the current political environment, we can see a decline in democracy coupled with strengthening capitalism (Thorpe, 2025). The government is attempting to shut the Consumer Financial Protection Bureau down, which was created to protect people from being taken advantage of by large banks, meaning that those financial services companies will be held less accountable to their actions. We have also witnessed business-friendly appointments in governmental departments that will also decrease business oversight.

Firms like JPMorgan or Citi benefit from tax breaks, regulatory leniency, and capitalist market competition. The mirroring of nationalist rhetoric by the administration and these firms shows that the link between American values and capitalism is strong. With a possible recession due to loss of government jobs and increasing prices due to trade wars, these firms will likely continue their campaign using patriotic appeals to get the public on their side. Companies are benefitting from the regulatory environment, but they are still invested in global capitalism and will attempt to influence politicians and the public, perhaps with familiar rhetorical strategies.

Engelen et al. (2012) argue that the financial sector in its current form is not easily regulated and politicians and the public are both subject to its power and whims. The findings in this paper show that financial firms are using cultural and moral rhetoric to persuade the public that the financial industry and capitalism are good for society, but as Engelen and his coauthors argue, the financial system cannot be fixed without bringing the industry under a more democratic system. The financial crisis tightened the market by consolidating some of the largest banks and making them more profitable than ever before in history. If democracy, capitalism, and being American are inherently tied together, it becomes more difficult to extricate one, and as we have witnessed the weakening of federal checks and balances, it has become more important to push for democratic control both of the government and of some of these larger firms, especially as we have seen increased links between firms and conservative groups (Banerjee, 2020).

Despite major crises in the last century, capitalism is still a driving force in the US economy. This research sheds light on how firms used their shareholder letters to propagate the idea that Americanism is one with capitalism. The argument is not a linear one that shows patriotism leading to capitalism, but rather, it is a cyclical feedback loop. The firms are coopting the language of patriotism and entrepreneurial spirit to argue that Americanism is one with capitalism, then they show how their work supports capitalism and thus, supports America. Then they use this argument to push for legislation that supports these values, entrenching the capitalist system further.

Supplemental Material

sj-docx-1-crs-10.1177_08969205261417164 – Supplemental material for Land of the free (markets): US banks’ strategic rhetoric in response to the financial crisis

Supplemental material, sj-docx-1-crs-10.1177_08969205261417164 for Land of the free (markets): US banks’ strategic rhetoric in response to the financial crisis by Katherine Copas in Critical Sociology

Footnotes

Acknowledgements

The author would like to thank Bruce Carruthers, Karin Yndestad, Sino Esthappan, Maura Fennelly, and participants in Brayden King’s Lab Group who offered useful comments on multiple drafts. The author also wants to thank the editor and anonymous reviewers for their engaging and constructive feedback.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.