Abstract

Encouraging organizations to be more open has been a key issue in contemporary debates over nonprofit accountability. However, our understanding of what motivates organizations to the disclosure decision is weak. We aim to enhance our understanding of this critical issue by developing and testing a model of the determinants of voluntary disclosure decision making, using data gathered on the population of not-for-profit medical institutions in Taiwan during a period where the government encouraged—but did not require—disclosure on a centralized website. As a result, we are able to conduct a “natural experiment” of the voluntary disclosure behavior of an important population of non-donor-dependent organizations. We find voluntary disclosure is more likely in organizations that are smaller, have lower debt/asset ratios, and are run by larger boards with more inside members. Our data suggest that, from a policy perspective, voluntary disclosure regimes are not an especially effective means of promoting public accountability.

Keywords

Nonprofit organizations are responsible for two key domains of accountability: performance and finances (Behn, 2001; Brinkerhoff, 2001). By disclosing details of financial standing and social performance, nonprofit organizations can build community trust, provide relevant information to donors, demonstrate their responsive to stakeholders, and generally help fulfill their “societal quid pro quo” (tax-exempt status) by providing evidence they are responsibly targeting their social mission (Gandía, 2011; Saxton & Guo, 2011). The issue of disclosure, especially concerning finances and performance, is thus at the heart of contemporary debates over creating a more open and accountable nonprofit sector. However, our understanding of what motivates organizations to be more open with the information they share with the public is only now beginning to be addressed by nonprofit scholars (Behn, DeVries, & Lin, 2010; Saxton & Guo, 2011). Accordingly, in this article we aim to help enhance our understanding by developing and testing a model of the determinants of voluntary nonprofit financial disclosure.

The explanatory model we use builds on the literatures on nonprofit disclosure, nonprofit accountability, and information disclosure in the government and for-profit sectors, and incorporates four factors—strategy, capacity, governance, and environment. To test our model, we use a probit analysis on the population of not-for-profit medical institutions in Taiwan (N = 40) during a key period (2003) when the government first implemented a centralized voluntary financial disclosure regime. Before this time, there were no laws either requesting or requiring that Taiwan’s not-for-profit hospitals make their financial statements publicly available. This enables us to conduct a “natural experiment” of the disclosure decision under a new, fully voluntary disclosure regime.

The design chosen for this study yields several other benefits. To start, this study differs from much of the past voluntary disclosure literature which has focused mainly on cases involving the level of voluntary disclosure that occurs above and beyond mandated levels. Instead of such “incremental” disclosure, we focus on disclosure in a new, wholly voluntary regime. This allows us to tap the determinants of voluntary disclosure more fully than prior tests. Our outcome variable also involves a standardized set of disclosed documents which facilitates interorganizational comparisons. Finally, the population studied is a set of organizations that is not heavily donor dependent. This allows us to examine the factors that motivate the disclosure decision beyond the simple quest for donations—an issue that has dominated existing studies of the outcomes of nonprofit disclosure (see Parsons, 2003). More generally, through our analysis, we can gain a sense of when voluntary disclosure mandates “work.” The results will also prove useful to those in different settings throughout the world who are interested in fostering greater transparency and disclosure in their own communities.

Our findings suggest that elements of organizational strategy (financial leverage), capacity (size in revenues), and governance (board size and proportion of external board members) are particularly important in affecting the disclosure decision. In the end, nonprofit medical institutions in Taiwan, as do most organizations in the global nonprofit sector, obtain their resources directly or indirectly from the public, and hence, have a responsibility to disclose their financial information to that public to be accountable. Accordingly, our study ends with a series of practical and theoretical recommendations that build on our core findings.

The Disclosure Context of Taiwanese Nonprofit Hospitals

Background on the Taiwanese Hospital Sector

As in the United States, there are three main types of hospitals in Taiwan’s medical sector: “public,” administered by public universities or the government; “nonprofit,” established by private universities or groups of donors for research and/or charitable purposes; and, “for-profit,” owned by private individuals or groups. At the time of our study, Taiwan had 95 public hospitals (with 41,646 total beds), 40 nonprofit hospitals (40,058 beds at 82 branches), and 370 for-profit private hospitals (33,512 beds).

Both the for-profit and nonprofit hospitals provide the same medical services. The key difference between the two is that (as in the United States) nonprofit hospitals do not have private “owners” and are not allowed to distribute retained earnings. 1 In addition, by law, nonprofit hospitals are required to provide a certain amount of community-benefit services for which they do not receive payment from consumers.

Disclosure Requirements

At the time of our study, each hospital in Taiwan was required to submit annually a financial statement to the Taiwanese Department of Health (DOH) and a tax return report to the Taiwanese Internal Revenue Service (IRS). However, there were no laws either requesting or requiring that Taiwan’s not-for-profit hospitals make their financial statements publicly available. This is unlike the environment in, for example, the United States, where federal law requires that most tax-exempt nonprofit organizations allow public inspection of their recent federal annual returns (e.g., IRS Form 990 and Schedule A) and their application for tax-exempt status. In Taiwan, there had been no regulated disclosure until 2003 when faced with the pressure of public opinion, Taiwan’s DOH implemented an e-disclosure system that asked nonprofit medical institutions to voluntarily disclose their financial accounting information on a centralized website. We examine the population of Taiwanese not-for-profit medical institutions at this key historical period—when the government first implemented a centralized voluntary financial disclosure regime.

What Can the Public Learn?

In Taiwan, as in the United States, the disclosure of financial statements (whether audited or unaudited) to the general public is generally voluntary. However, unlike in the United States, by law, the Taiwanese IRS cannot disclose any financial information to the public. The public have neither the recourse to an online resource such as Guidestar nor the ability to request a tax-return form directly from the nonprofit organization. As a result, the voluntary disclosure of financial information is more important in Taiwan than in the United States; that is, if a Taiwanese nonprofit voluntarily makes its financial statements available online, this can have a bigger impact than the similar decision by an organization in the United States.

Without voluntary disclosure of the financial statement, the typical Taiwanese citizen can find only basic financial information about the hospital, such as its size. With financial statement disclosure, the average citizen can readily find much more relevant information about such features as the hospital’s profitability, degree of financial leverage, audit information, and levels of community-benefit service. The financial statement can thus be a decision reference for Taiwanese donors, “watchdogs,” and other stakeholders.

That said, the typical nonprofit hospital in Taiwan (as in the United States) is not reliant on donations which comprise roughly 4% of total revenues (DOH, Taiwan, 2011a). Therefore, the key driving force for disclosure is not to appease current donors; according to the agency-cost perspective, in cases where an organization’s financial resources are not primarily obtained from donations, they are less accountable to donors (Rose-Ackerman, 1987). Instead, organizations will be driven to disclose out of (a) consideration of the public good, (b) a desire to avert potential political costs, and/or (c) a desire to attract new donors. In effect, our analyses are especially relevant to understanding the donor decision made by non-donor-dependent nonprofit organizations. This will help counteract the extant literature’s concentration on the agency-cost perspective and the disclosure–donations link. In exploring alternative disclosure motivations for non-donor-dependent organizations, our results can serve as an especially valuable reference point for regulators overseeing these types of institutions.

Disclosure in the Literature

Our theoretical model of the determinants of voluntary disclosure is informed by three relevant streams of research. First, there are the conceptual and theoretical arguments from the nonprofit literature on the roles and purposes of nonprofit disclosure. In this literature, disclosure is seen as a vital, multifaceted component of nonprofit operations that fills several key roles. To start, a relatively large body of research has focused on disclosure as an important aspect of nonprofit governance and accountability (e.g., Brody, 2002; Lee, 2004; Melendez, 2001; Saxton & Guo, 2011). The core argument is that demonstrating financial responsibility and mission-based performance is a key component of nonprofit organizational accountability (e.g., Brinkerhoff, 2001), and that the voluntary disclosure of performance- and financial-related information is a powerful if not essential vehicle for making such demonstrations (Gandía, 2011; Saxton & Guo, 2011).

Another body of research in both nonprofit studies and accounting concentrates on the outcomes of disclosure; specifically, on how the voluntary disclosure of information provides signals and information that are relevant to current and potential donors (e.g., Gandía, 2011; Greenlee & Brown, 1999; Khumawala, Neely, & Gordon, Knock, & Neely, 2009; Tinkelman, 1999; Trussel & Parsons, 2008). Scholars working in this genre typically assume that financial accounting information can assist donors in monitoring their implicit contracts with the nonprofit organization by providing a means for donors to evaluate whether the organization is using their donations in the most efficient and effective manner and in the way originally intended. With the information received via disclosure, donors can decide whether their donation should go to a specific party or not. Nonprofit managers thus have an incentive to selectively disclose financial information (Gordon, Fischer, Malone, & Tower, 2002; Krishnan, Yetman, & Yetman, 2006).

The above research argues disclosure can be a powerful tool for nonprofit organizations hoping to achieve market differentiation, attract greater donations, and boost accountability and public trust. However, beyond the general assumption that organizations are more likely to disclose when they are concerned with donations and/or accountability, none of the above research posits testable hypotheses regarding specific factors that lead to increased disclosure. We do know, however, that the disclosure decision is not without risk, or else all organizations would implement substantive disclosure policies. In the market for charitable contributions, for instance, the payoffs associated with disclosure ultimately vary with donor preferences: donors react differently to disclosure based on the extent to which they are motivated by altruism, fairness, kindness, social impact, publicity seeking, or the “warm glow” from donating (e.g., Bergstrom, Blume, & Varian, 1986; Zhuang, Saxton, & Wu, in press). Moreover, research has shown that, in making the disclosure decision, managers consider competing organizations’ relative levels of openness as well as the risks from disclosing information (e.g., profitability) that current and/or potential competitors might use to their advantage (Healy & Palepu, 2001).

Another body of research on for-profit firms does provide testable arguments about what motivates organizations to disclose. This literature typically analyzes disclosure incentives using an agency model, in which managers (i.e., agents) are able to reveal their efforts through the disclosure of accounting information (Healy & Palepu, 2001; Watts & Zimmerman, 1986). Although not-for-profit organizations have different objectives and behave differently from for-profit firms, the agency problem does affect not-for-profit organizations, as seen in the above charitable contributions literature. The public demand for nonprofit financial statement data is at least partially driven by the inherent agency conflict within the nonprofit setting; disclosing information can be a means of monitoring not-for-profit firms, and thereby, decreasing agency cost (Krishnan et al., 2006).

Finally, there is a nascent body of research on what motivates nonprofit organizations to be transparent with their financial- and performance-related information. First, Behn et al. (2010) conducted an exploratory study on what leads the 300 largest U.S. nonprofit organizations to respond to mail requests for audited financial statements. Focusing on mail requests to view audited statements, the study is more on “transparency” or the passive sharing of information (when asked) than on active public disclosure. Nevertheless, the findings are instructive: they found that debt, contribution ratios, size, and executive compensation ratios were related to the decision to share audited financial statements.

Saxton and Guo (2011), meanwhile, tested a model of the determinants of U.S. community foundations’ Web disclosure practices. Their model weaves together four generic organizational dimensions—strategy, capacity, governance, and environment—that they argue are critical to understanding levels of disclosure on organizational websites. First, organizations select disclosure practices based on the nature of their socially driven mission and their organizational strategy for achieving that mission. Second, the ability to successfully reach strategically motivated aims is determined by internal capacity and organizational resources. When nonprofit organizations’ preexisting capacities are coupled with the notion of organizational strategy, a set of tools is in place for understanding whether and how nonprofit organizations adopt disclosure practices. However, a third dimension, the organization’s governance structure, is essential for ensuring that organizational resources and capacities are properly used and that strategies are properly implemented. Finally, the environment, in which the organization operates, helps drive both the selection and ultimate success of specific communication and disclosure strategies.

Modeling the Determinants of Voluntary Disclosure

To maximize our theoretical contribution, the explanatory model we use represents an extension of the strongest available model. Of the existing studies, the Saxton and Guo (2011) model is most relevant and, hence, serves as our base. Given its outlining of four broad causal factors, the model is readily applicable to different settings. Accordingly, in this section we discuss our extension of the core Saxton and Guo model. We translate the model to our specific context (Taiwanese medical institutions) and, at the same time, take the opportunity to improve on those facets of the model that were less robust empirically than others. We then use this enhanced model to explain the disclosure decision in the context of a purely voluntary disclosure regime.

In line with Saxton and Guo (2011), we propose that a nonprofit’s electronic disclosure decision derives from four sets of factors familiar to nonprofit organizational scholars: strategy, capacity, governance, and environment. Specifically, we posit that an organization’s electronic disclosure practices are a function of (a) the extent to which the organization’s strategy is focused on broad, community-focused service and accountability; (b) the extent of the institution’s basic organizational capacity, as indicated by its size and profitability; (c) the quality of the organization’s governance mechanisms, as reflected by board size, the prevalence of outsiders on the board, and the quality of its financial statements; and (d) the degree to which the external environment is receptive to or demanding of transparent organizational practices. In our sample here, the “environmental” factor is constant across all organizations—all are nonprofit medical institutions in Taiwan. Consequently, our empirical model concentrates on the three most robust dimensions of the Saxton and Guo (2011) model—strategy, capacity, and governance. We discuss each of these dimensions in turn.

Strategy

The particular strategy that a nonprofit organization develops to accomplish its social mission has important implications for its electronic disclosure decision making. We consider two elements here that tap a broad, community-focused service and accountability strategy, the first of which is an organization’s provision of community-benefit services.

By law, Taiwanese nonprofit hospitals have to provide a certain amount of “community-benefit” services, 2 and charges for such services cannot be levied on consumers. Instead, revenue is collected from patient revenue (provision of medical services) and donations. During the time period of our study, the disclosure of information regarding community-benefit services was wholly voluntary. We argue that, if a not-for-profit medical institution provides substantial community-benefit services, it will have a strong incentive to disclose this information to the public (as noted earlier, this information is available to the public in the disclosed financial statements). Institutions that provide few community-benefit services, in contrast, do not have this incentive and are likely to withhold information to avoid monitoring and censuring. We therefore expect a positive association between the extent of services benefiting the community, measured as the ratio of community-benefit service expenditure to total operating revenue, and the probability of disclosure.

We also expect institutions with greater debt to adopt a less transparent, publicly accountable approach. Generally speaking, the more debt financing an organization has, the greater the monitoring costs it faces (Jensen & Meckling, 1976). A for-profit organization in this situation will disclose more information due to the conflict between creditors and stockholders (Schipper, 1981). However, not-for-profit hospitals in Taiwan can issue neither stocks nor bonds. If approved by the DOH, they can receive bank loans for capital investments (not for operational activities). In the case of a loan, the hospital’s credit will be thoroughly checked if it seeks to obtain financing; in effect, the hospital’s accountability—and driving force for disclosure—shifts away from the public (in the form of voluntary e-disclosure) and closer to the bank (private disclosure of financial documents). We therefore expect that the greater the financial leverage, measured as the ratio of long-term debt to total assets, the lower the motivation to publicly disclose financial information.

Capacity

The capacity the organization has to undertake strategically driven initiatives also has implications for the adoption of voluntary disclosure practices. One of the most consistently important capacity factors cited in the literature is organizational size. Size is a particularly important determinant of nonprofit accountability (Behn et al., 2010; Saxton & Guo, 2011). As an organization grows, it becomes more visible and therefore attracts greater attention and scrutiny by external constituencies such as the state, the media, and the general public (Luoma & Goodstein, 1999). The for-profit literature refers to this notion as “political costs,” which asserts larger entities are more likely to encounter increased scrutiny by government, politicians, or the general public that can ultimately result in greater regulatory intervention (e.g., Watts & Zimmerman, 1986). Commonly, this argument is used to predict a positive relationship between size and disclosure. However, given prior research that the disclosure of financial information—in making specific information widely available—reduces external stakeholders’ monitoring costs (Leftwich, Watts, & Zimmerman, 1981), we expect larger nonprofit hospitals (measured by the natural log of total revenues) to be less motivated to disclose their financial information to reduce their exposure to public scrutiny and potentially higher political costs.

Our second capacity variable is profitability which has been shown to affect contributors’ donations to hospitals (Frank, Salkever, & Mitchell, 1990). Depending on the context, profitability could affect managers’ disclosure-related decisions differently. In Taiwan, hospitals with outsized profits have less incentive to make their financial statements widely available, lest the public react unfavorably. 3 With no shareholders, there is no capital markets-type incentive for profitable firms to disclose; instead, the core stakeholders are the general public and the government and the incentive is to make those disclosures that will help secure future profitability. Accordingly, hospitals with weaker (or negative) profits would be motivated to make this information fully available in the hopes that it will drive public opinion—and in turn the DOH—to favor increasing reimbursement rates. We thus expect that the less profitable the institution, measured via return on total assets (ROA), the greater the probability of disclosure.

Governance

The upper-echelons perspective (Hambrick & Mason, 1984) attributes major influence over strategic and performance outcomes to organizational governance. As in the Saxton and Guo (2011) model, we incorporate variables designed to tap both internal and external governance mechanisms. Saxton and Guo’s empirical test measured internal governance via a survey-based “board performance” variable; here, we proxy for board performance via two variables concerning the size and composition (insider representation) of the organization’s board of trustees.

First, we posit a positive relation between board size and disclosure. The logic comes from several arguments is found in the empirical literature on not-for-profit governance. To start, scholars such as John and Senbet (1998) have found that, with more board members, there will be problems of communication, coordination, and decision making that lead to less efficient and effective managerial monitoring; this in turn gives board members the incentive to disclose greater amounts of information to facilitate monitoring by external stakeholders, thus releasing them of some of their supervisory obligation. Moreover, the health care literature has identified large boards with the “philanthropic model” of hospital governance (see Alexander & Lee, 2006), with larger boards more oriented toward asset preservation and fundraising than the strategic exploitation of market conditions. Larger boards have also been found to have more contact with the public, which further facilitates fundraising (Olson, 2000). In effect, larger boards are more “philanthropic” in nature, and, with evidence that financial disclosure is related to increased donations (see Parsons, 2003, for an overview; see also, inter alia, Buchheit & Parsons, 2006; Greenlee & Brown, 1999; Khumawala et al., 2009; Tinkelman, 1999), we expect board size to be positively associated with the probability of disclosing financial information.

Second, the presence of “insiders” on the board, with specific knowledge regarding the operations of the organization, may be necessary for optimal strategic decision making; however, “outsiders” (those who are not full-time employees) provide a level of independence that is essential for monitoring managerial activities (Fama & Jensen, 1983; John & Senbet, 1998). 4 In line with our arguments above concerning board size, we posit that increased internal monitoring capacity is associated with weaker incentives to increase the monitoring capabilities of external stakeholders. Thus, we propose that a larger presence of outsiders on the board of trustees will be negatively related to voluntary disclosure.

Our final variable taps an external governance mechanism. This was the weakest component in the Saxton and Guo (2011) empirical test; accordingly, we have a good opportunity to improve on the model by including an alternative—and, we argue, more appropriate—external governance mechanism. Specifically, we look at whether the hospital’s financial statements are externally audited by an independent CPA firm. During our study period there were no legal requirements that our institutions’ financial statements be independently audited. Yet research has shown that externally audited financial statements are associated with financial report accuracy, better governance, and overall audit quality (e.g., Fan & Wong, 2005; Francis, Maydew, & Sparks, 1999; Krishnan et al., 2006). We therefore expect institutions to have a higher degree of confidence in disclosing financial statements when they have been submitted to an independent audit.

Sample, Data, and Method

To test our model, we use data on the entire population of Taiwanese not-for-profit medical institutions. Specifically, the sample used in this article consists of the 40 not-for-profit medical institutions in continuous operation in Taiwan since 2001. Four are pathology labs/centers and the other 36 are hospitals.

With a sample size of 40 observations and a maximum likelihood estimation technique, we may not have a sufficient amount of statistically valid data. The primary risk we run is the increased probability of a Type II error (failing to reject the null hypothesis when it is actually false), that is, of concluding that the relationship between two variables is not significant when it actually is (Kish, 1965). As a result, in this study, we can safely say that any significant relationships we do find are valid, but that one or more of the insignificant relationships we see may in fact be significant. In any case, the issue here of statistical significance is less critical, because the sample size is equal to the population, rendering the statistical significance of the regression coefficients less important (Kish, 1965). 5 In addition, the issue of statistical significance is more than offset by the fact that we are able to examine a population at a period where there exists a “natural experiment” in the environment of a new, fully voluntary disclosure regime.

Dependent Variable: Voluntary Disclosure

For those organizations that complied with the voluntary regime, the Taiwanese DOH posted their 2001 condensed financial statements on the Web in January of 2003. We therefore obtain the data for our dependent variable from our examination of the DOH website in 2003. All of the condensed balance sheets and income statements have the same accounting standards as their basis; therefore, we do not develop an index to measure the quality of the financial statements (Gordon et al., 2002; Robbins & Austin, 1986). Instead, we create a dichotomous variable, Disclosure, to measure disclosure behavior; if an institution voluntarily disclosed its financial statements in 2003, Disclosure = 1, otherwise 0.

Independent Variables

As noted above in developing our model, we operationalize seven variables to test our hypotheses. All data for our independent variables are from 2001 and are derived from two official databases. First, from the annual financial statements database (DOH, Taiwan, 2011a) we operationalize the following three variables: Financial Leverage, the ratio of long-term debt to total assets; Size, measured as the natural log of total revenues; and Profitability, the return on total assets. The remainders of the variables are derived from information contained in the Annual Operational Activities Survey (DOH, Taiwan, 2011b). These annual DOH surveys cover board governance issues and medical and community-benefit services; the paper surveys are filled out by the executive director at each hospital and are mandatory, thus the response rate is 100%. From these surveys we operationalize the following four variables: Community-Benefit Service Expenditure, measured as the ratio of community-benefit service expenditure to total operating revenue; Board Size, the total number of members on the board of trustees; Percentage of Outside Board Members, the percentage of nonexecutive board members who are not full-time employees of the hospital; and Independent Auditing, a dummy variable with a value of 1 if the financial statements are independently audited by a CPA firm, and 0 otherwise (i.e., “0” indicates no external audit).

Model Specification and Estimation Technique

With a dichotomous dependent variable such as Disclosure, the use of ordinary least squares (OLS) would result in biased, inefficient, and inconsistent parameter estimates (Long, 1997). As a result, we use instead a maximum likelihood technique for our multivariate analyses; specifically, we use probit analysis to estimate the following empirical model:

Results

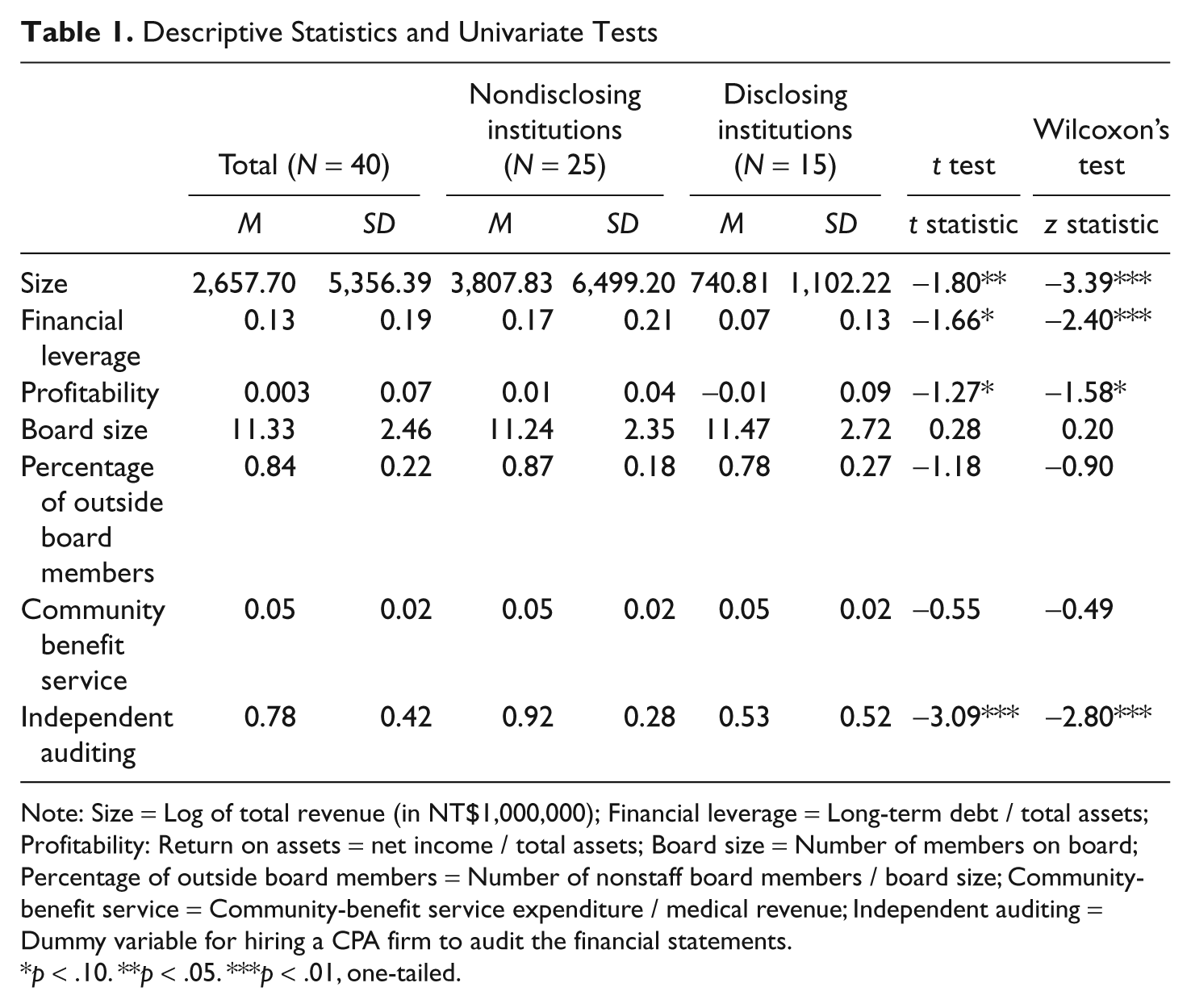

Before turning to our multivariate results, we present relevant univariate analyses. Table 1 contains descriptive statistics (mean and standard deviation) for each of the variables in our analyses. In addition to the population descriptive statistics, Table 1 also shows descriptive statistics for each of the seven independent variables for both disclosing and nondisclosing institutions (which corresponds to the categories of our dependent variable). As seen in the table, we found that 15 of the 40 not-for-profit medical institutions voluntarily published their 2001 condensed balance sheets and income statements on the DOH website in 2003. We can also see that the average disclosing organization has a slightly larger board but is smaller, has lower long-term debt (leverage), is less profitable, has a lower percentage of outside board members, and is more likely to have unaudited financial statements.

Descriptive Statistics and Univariate Tests

Note: Size = Log of total revenue (in NT$1,000,000); Financial leverage = Long-term debt / total assets; Profitability: Return on assets = net income / total assets; Board size = Number of members on board; Percentage of outside board members = Number of nonstaff board members / board size; Community-benefit service = Community-benefit service expenditure / medical revenue; Independent auditing = Dummy variable for hiring a CPA firm to audit the financial statements.

p < .10. **p < .05. ***p < .01, one-tailed.

As shown in Table 1, we also use a series of t tests and Wilcoxon’s signed-rank tests to see whether there are significant differences between firms that voluntarily disclose financial information and those that do not in terms of each of our explanatory variables. What these tests show is that there are significant differences between disclosing and nondisclosing institutions in terms of Size, Financial Leverage, Profitability, and Independent Auditing. All are negatively related to the disclosure decision. In contrast, there is no statistically significant difference between disclosing and nondisclosing institutions in terms of Board Size, Percentage of Outside Board Members, and Community-Benefit Service Expenditures.

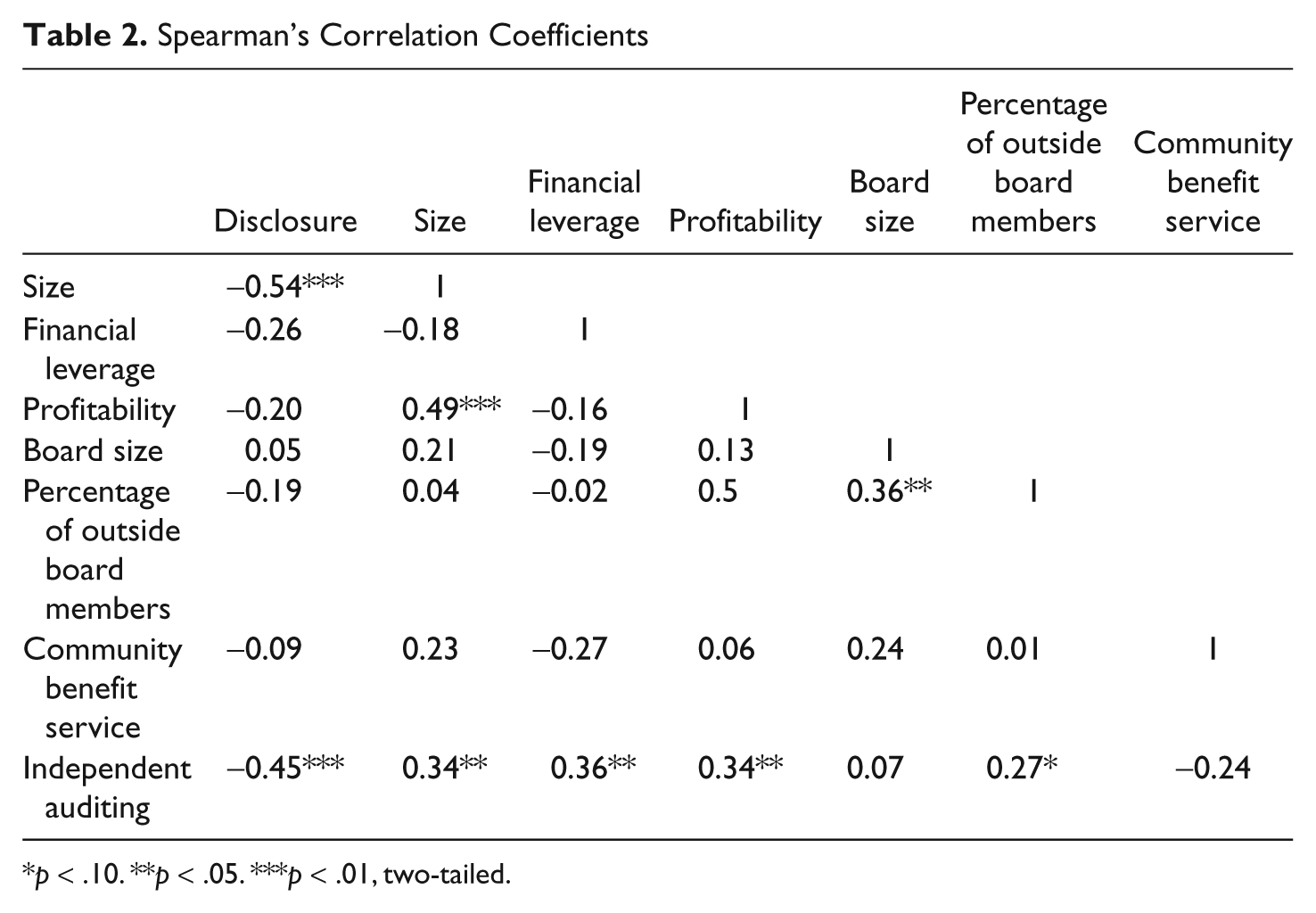

We also examine the zero-order correlations among the model variables, shown in Table 2. We found no evidence of multicollinearity. 6

Spearman’s Correlation Coefficients

p < .10. **p < .05. ***p < .01, two-tailed.

Multivariate Analyses: Probit Model

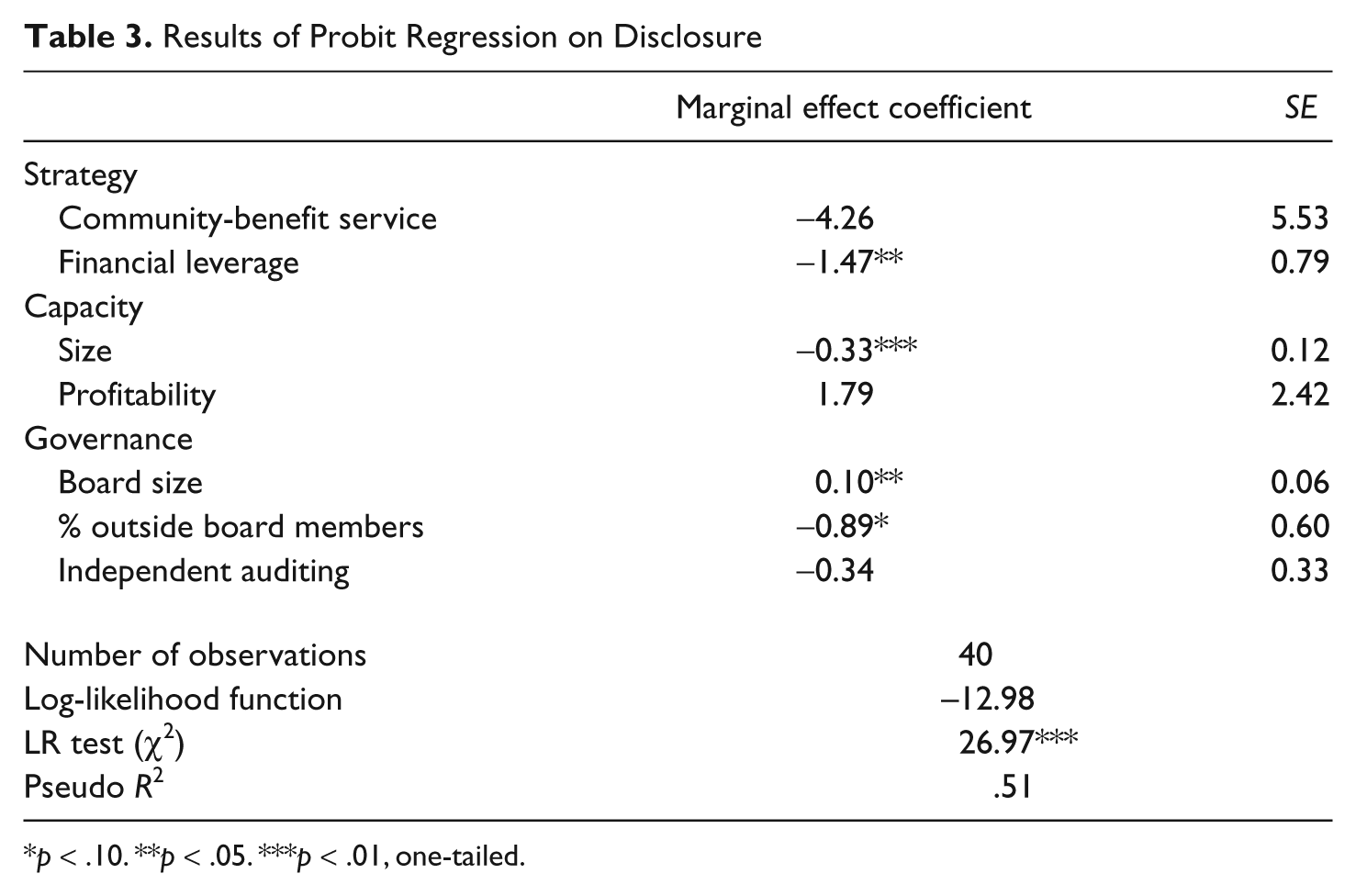

Although the univariate results point to several interesting relationships, to determine the robustness of these relationships we need to examine the findings from our multivariate probit analyses. Our main probit results are presented in Table 3. The probit model has a likelihood-ratio (LR) test statistic of 26.97 and a pseudo R2 of .51, which provides initial evidence of the goodness-of-fit and descriptive validity of our explanatory model.

Results of Probit Regression on Disclosure

p < .10. **p < .05. ***p < .01, one-tailed.

The probit model uses maximum likelihood estimation, which renders the interpretation of coefficients less intuitive. Consequently, we use the standard probit coefficients to calculate the marginal effects of each of the explanatory variables on the probability of disclosure. These marginal effect coefficients are reported in Table 3. For continuous independent variables (all except Independent Auditing), the reader should interpret a variable’s marginal effect coefficient as the change in probability of disclosure for a unit change in that variable—holding all other independent variables constant at their mean values. For the dummy variable Independent Auditing, the interpretation is slightly different: the coefficient reflects the change in the probability of disclosure, holding all other independent variables constant at their mean values, for organizations with independent audit of their financial statements.

Let us first examine the two “strategy” factors, beginning with the institutions’ Community-Benefit Service. The regression coefficient is negative, which suggests that a not-for-profit hospital that spends more on community-benefit services is less likely to publicly disclose its financial statements. This finding goes against our expectations. However, the coefficient is not significant, thus we cannot reject the hypothesis that there is no correlation between community-benefit service expenditure and voluntary disclosure.

Our second strategy variable is Financial Leverage. The coefficient is negative and significant at the .05 level. The marginal effect coefficient (–1.47) can be interpreted as meaning that if the ratio of long-term debt to total assets increases by one unit, the probability of disclosure will decline by 147%. This finding lends credence to our hypothesis that increased dependence on loans shifts accountability from the public to the banks and thus decreases the likelihood of public disclosure. Potentially further strengthening this tendency is that high debt levels may represent “bad news” (e.g., Skinner, 1994) that hospitals would rather not disclose. 7

We next examine the two variables designed to tap organizational capacity. First, the coefficient for Size (measured as log of total revenues) is significantly negative at the .01 level. The coefficient of −0.33 indicates that a one-unit increase in the log of total revenues will result in a decrease of 33% in the likelihood of disclosure, holding all other independent variables constant at their mean values. These results support the view that the larger institutions are more likely to avoid being monitored by the public, potentially because of the higher political costs they might face. Our second capacity variable, Profitability, was not statistically significant, meaning, we cannot reject the null hypothesis.

Our three remaining explanatory variables are designed to measure the quality of the organization’s governance. We start with Board Size. We predicted that larger boards would be positively associated with the disclosure decision. The regression results are consistent with expectations, and indicate that the coefficient is statistically significant and positive at the .05 level. The marginal effect of 0.10 means that a unit increase in board size (i.e., adding another board member) is associated with a 10% increase in the probability of voluntary disclosure.

We also hypothesized the share of outside directors would have a negative effect on the disclosure decision, and the marginal effect coefficient suggests that if the proportion of outside directors increases by one unit, the likelihood of voluntary disclosure declines by 89%. This is in line with our expectation that outside directors are inherently more independent and thus better able to monitor the chief executive internally, which in turn renders the push for disclosure (and external monitoring) less likely. There is, however, evidence that “outsider” status is not necessarily sufficient to achieve independence, and that in some circumstances in the for-profit sector outsider-dominated boards are less effective (Hermalin & Weisbach, 1998). 8 Although we are not able to directly test these competing perspectives here, teasing out the precise nature of this relationship would help advance the nonprofit governance literature.

Finally, we examine Independent Auditing. Contrary to expectations, the results reveal a negative, though not significant, relationship between the use of CPA firms to audit financial statements and the likelihood of voluntary disclosure. One possible explanation is that, with audited financial statements, organizations have less discretion in preparing the statements, which tend to make them less “flattering” for the organization. This decreases the incentive to disclose. 9 Although we do not directly test this idea, there is an opening here for future research.

Sensitivity Analyses

To determine whether our empirical results are robust, we also perform sensitivity analyses in which we use alternate measures of several key variables—Size, Financial Leverage, Community-Benefit Service, Profitability, and Independent Auditing—leaving the remaining model variables unchanged. 10 For all of the above variables, each run on a separate probit regression, the results were similar to those obtained in Table 3, which indicates the overall robustness of our findings.

We also sought to determine whether the disclosure decision was influenced by donations, and thus included the ratio of donation revenue to total revenue and the total amount of donations received as two additional control variables. Both were insignificant when included separately in regressions using our original model, with the sign and significance of the variables in our original model unchanged from what was seen in Table 3. Consequently, we cannot infer that the public disclosure of financial information is affected by donations in our population.

Conclusions

In this study we have investigated nonprofit organizations’ information disclosure behavior. Using data collected from 2001 financial statements from the population of Taiwanese not-for-profit medical institutions, we sought to find the factors that differentiate those institutions that disclose their financial statements on the DOH’s website in 2003 from those that do not. The results show that the larger the institution, the greater the financial leverage, the smaller the size of the board, and the higher the percentage of outside board members, the less likely it is that an institution will voluntarily disclose its financial information.

Our study builds on and extends prior research in several key ways. Most notably, our setting involves the implementation of a new, fully voluntary disclosure regime. We thus have a natural experiment of how the implementation of a voluntary regime affects the disclosure decision. This differs from prior research which, in both the nonprofit and capital-markets settings, has focused almost exclusively on “incremental” voluntary disclosure, or the disclosure of information in addition to what is required by law.

We further add to the nascent literature on nonprofit voluntary disclosure by building on the explanatory model developed by Saxton and Guo (2011). Our multivariate analyses provide additional support for the salience of strategy-, capacity-, and governance-related factors in the disclosure decision. Of our results, perhaps most surprising—and worthy of further empirical examination—are our findings that neither the presence of “outside” board members nor independently auditing of financial statements is associated with an increased probability of voluntary disclosure. If disclosure is not empirically linked to effective governance, then the “disconnect” between organizational efforts and public demands may be bigger than expected.

An interesting extension to our findings would be to explicitly address our belief that boards of directors may in some circumstances have an incentive to advocate disclosure in order to push monitoring outside the organization. The idea is that, if they disclose their financial statements, the public can share in the monitoring and regulating responsibilities. This idea is not farfetched, especially in light of how the Internet has given citizens a far greater role in policing the nonprofit sector—for instance, in how the widespread availability of Form 990 data in the United States has led to the rise of powerful online “watchdog” organizations such as Guidestar and Charity Navigator (see Gordon et al., 2009). This idea of what we might refer to as “decentralized” or “participatory” monitoring would be excellent fodder for in-depth research.

Our findings further suggest that encouraging not-for-profit medical organizations to disclose financial information voluntarily is not an effective means of promoting public accountability. We believe the set of incentives and issues faced by our sample of Taiwanese medical institutions is analogous to that faced by other sectors of the nonprofit economy as well as other countries that are similarly struggling with how to boost the accountability of the nonprofit organizations in their own communities, and that, as a result, our findings are translatable to multiple sectors and settings. To boost accountability and decrease agency costs, it is likely necessary for regulators—elsewhere in the globe as in Taiwan—to enforce the mandatory public disclosure of financial reports, especially in cases where the institutions are not donor dependent, which gives them even less of an incentive to publicly disclose financial information.

There are compelling reasons why a society would want to push for greater levels of disclosure. Overall, not only does disclosure help organizations connect with donors who share their preferences but, in the aggregate, voluntary disclosure, as in the capital markets (e.g., Healy & Palepu, 2001), plays a key role in reducing information asymmetries, maintaining “market” efficiency, and delivering better social outcomes. Moreover, through the voluntary disclosure of pertinent financial and performance-related information, organizations are able to signal their efficiency, effectiveness, credibility, responsiveness, and, most importantly, their accountability, to current and potential stakeholders. Therefore, even if it is not a legal requirement, not-for-profit organizations should disclose their financial information, and accept and invite public supervision of managers’ behavior, to ensure that the organization remains accountable (Lawry, 1995). One could also argue that organizations have a duty to be transparent when, as in our sample here, the revenue of the organizations derives chiefly from National Health Insurance payments and tax exemptions, both of which can be treated as indirect revenue from the public. Full disclosure should thus be seen as a natural extension of the “societal quid-pro-quo.” Above all, accountability and transparency are necessary to maintain public trust and confidence in the not-for-profit sector.

In addition to the public accountability issue, there are strategic reasons for organizations to be more transparent. For Taiwanese not-for-profit medical institutions, the revenue from donations and government subsidies is generally less than the medical revenue. Taiwan’s medical institutions have consequently faced considerable financial pressure following the launching of the government’s National Health Insurance (NHI) program in 1995. Given that insurance payments are insufficient to cover medical costs, many medical institutions have demanded that the NHI increase its payments. Although this may be a compelling reason for the government to increase insurance premiums, it is not enough to convince the general public. This is where disclosure could prove useful; research has shown that, in the face of genuine financial need, disclosure and transparency helps convince otherwise reluctant stakeholders to accept painful policy solutions (Watts & Zimmerman, 1986). As a result, if hospitals wish to persuade the public and policy makers to accept rate increases, they should endeavor to follow the recommendations of the Taiwan Health Reform Foundation (2004) and disclose more information regarding their operations—and specifically, to annually prepare and disclose their financial information such that the public has enough material to meaningfully evaluate their financial condition and overall performance.

In sum, the voluntary disclosure of financial information would tend to both enhance an organization’s public accountability and serve as a means of meeting its strategic goals. Nevertheless, as we have argued above, such arguments do not appear to be sufficiently persuasive to the majority of institutions. Given the shortcomings of the voluntary disclosure regime, the Taiwanese government in fact more actively intervened and began mandating the disclosure of financial statements on the DOH website in 2005. Further research is therefore needed on what motivates the disclosure decision, and on what could in turn boost the effectiveness of voluntary disclosure regimes. Scholars should specifically extend our research and dig deeper into why voluntary disclosure provisions do not seem to work.

Our study points to several additional extensions that could prove fruitful. The goal of this article was to examine the determinants of voluntary financial disclosure. However, future research could focus on the content and the quality of the information provided via voluntary disclosures. Further research could, for example, focus on whether an institution’s financial statements are based on the “Financial Statement Compilation Standard for Not-for-profit Medical Institutions” as advocated by the DOH, as an indicator of disclosure quality. Future research could also look at the outcomes of the disclosure decision—for instance, scholars might investigate whether the content or quality of disclosed documents has an impact on levels of public satisfaction or on subsequent levels of charitable contributions. Although the latter has begun to be addressed (e.g., Gandía, 2011), the former issue remains unexamined empirically. The field would also benefit from comparative research beyond what has been done in the United States and Taiwan. Cross-national investigations of the effects of mandatory versus voluntary disclosure requirements would be especially beneficial.

The nonprofit sector is also in need of practically oriented research that can help inform regulators’ supervision. As the health care market, among others, is characterized by highly asymmetric information and externalities, the disclosure of information on the quantity and quality of medical activities will enhance these institutions’ legitimacy while helping to strengthen overall public accountability. Additional research could help fill in the gaps in regulators’ knowledge concerning what boosts organizations’ willingness and capacity for meaningful transparency.

Footnotes

Acknowledgements

The authors would like to thank Chao Guo and Daniel Neely, along with the editors and the two anonymous reviewers, for their helpful comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The second and third authors gratefully acknowledge financial support from the National Science Council (NSC-96-2416-H-305-006).