Abstract

This study examines the implications of excess cash in nonprofit hospitals. Using a nationally representative sample of hospitals, I benchmark nonprofit cash holdings against for-profit cash holdings, and find that nonprofit hospitals hold significantly more cash. I consider three potential uses of excess cash in nonprofit hospitals: (a) investment in fixed assets, (b) increased charity care provision, and (c) higher executive compensation. I find that excess cash is associated with investments in fixed assets but not with increased charity care provision. Moreover, I find a positive relationship between excess cash and growth in CEO compensation. The results suggest that while nonprofit hospitals may accumulate cash to finance fixed assets, some of the accumulated cash may be diverted toward executive compensation. Overall, concerns regarding agency problems in nonprofit organizations may not be unfounded.

Introduction

The nonprofit sector in the United States represents a sizable share of the economy, contributing 5.6% to GDP in 2016 (Urban Institute, 2020). The nonprofits tax-exempt under Section 501(c)(3) of the Internal Revenue Code (commonly referred to as “public charities”) hold more than three trillion dollars in assets and earn more than a trillion dollars in revenue each year. A large portion of these funds are deployed in the hospital industry where the nonprofit organizational form is more common than the for-profit form (American Hospital Association, 2023). In recent years, as nonprofit hospitals have accumulated vast resources, the U.S. Congress has increasingly questioned the justification for their tax-exempt status. The Senate Finance Committee has repeatedly asked the IRS to ensure that nonprofit hospitals justify their tax-exempt status by providing sufficient charity care (Kane, 2007). The hospital industry has long maintained that the community benefits it provides far outstrip the total value of tax exemption it receives; however, some studies suggest otherwise (American Hospital Association, 2019; Herring et al., 2018; Rosenbaum et al., 2015; Zare et al., 2022). Furthermore, there are concerns about the high levels of profits and executive compensation in nonprofit hospitals that could otherwise be used for charitable purposes (Andrzejewski, 2019; Doroghazi, 2016; Ofri, 2020).

The resources controlled by nonprofit hospitals, particularly cash, have grown significantly in recent decades (Jenkins & Ho, 2023; McCue, 2001). Studies have consistently documented that nonprofit hospitals hold considerably more cash and other liquid assets than their for-profit counterparts (Rivenson et al., 2000; Song & Reiter, 2010). The primary objective of this study is to examine how nonprofit hospitals use their surplus cash resources. A nonprofit hospital may optimally need to hold high levels of cash to guard against short-term volatility, fund maintenance and improvement of equipment, and obtain high bond ratings. However, high levels of cash may be suboptimal if insufficient safeguards and oversight allow managers to use the cash for private benefits (Fisman & Hubbard, 2003; Jensen, 1986). Despite its significance, cash has received inadequate attention in the nonprofit management literature (Pizzini & Sterin, 2023). This gap is especially noteworthy because a vast literature exists on the implications of cash holdings in for-profit organizations. A body of work examines the role of cash in the nonprofit sector as a whole (Core et al., 2006; Ramirez, 2011), and several studies use broader measures of liquidity like operating reserves (Bowman et al., 2007; Calabrese, 2013), but few studies focus on the implications of cash holdings in nonprofit hospitals. Several distinct features of nonprofit hospitals, such as relatively smaller share of donations in total revenue, operating in a highly regulated industry, and large investments in fixed assets, justify examining nonprofit hospitals separately from the rest of the nonprofit sector. The present study aims to fill this gap by shedding light on the size and consequences of excess cash in nonprofit hospitals.

I benchmark the cash levels, defined as cash on hand and in bank, of nonprofit hospitals against those of for-profit hospitals. The observed differences in cash levels between nonprofit and for-profit hospitals may be explained by a variety of institutional factors such as ownership form and governance structure. Nonprofit hospitals may optimally hold more cash than for-profit hospitals, on average, because the former lack access to equity financing to acquire long-term assets. Likewise, nonprofit hospitals may need a stronger cash buffer than their for-profit counterparts because the former provide more uncompensated care (Song, Lee, et al., 2013). Importantly, excess cash in and of itself may not be suboptimal as it simply represents a deviation from the benchmark.

Well-governed for-profit organizations often return excess cash to shareholders to minimize value-destroying acquisitions and managerial self-dealing (Dittmar & Mahrt-Smith, 2007; Harford, 1999). Core et al. (2006) argue that in the absence of shareholders and other market disciplinary devices (such as hostile takeovers), managers in nonprofit organizations may hold suboptimally high levels of cash. This issue is further exacerbated by the fact that nonprofits lack a mechanism like dividends to return surplus funds to donors. Hansmann (1990) suggests that nonprofit managers can have incentives to hold excess cash to increase private benefits. Therefore, I consider three potential implications of excess cash holdings: (a) excess cash may be accumulated for investments in fixed assets; (b) excess cash may lead to increased spending on charity care; or (c) excess cash may be used by CEOs to increase their own compensation.

The analysis shows that nonprofit hospitals hold significantly more cash than for-profit hospitals. Consistent with previous studies, I find evidence that nonprofit hospitals accumulate excess cash for future investments in fixed assets. However, the results suggest that excess cash is not associated with increased charity care but positively associated with the change in CEO compensation. Additional tests suggest that excess cash is also positively associated with the change in CEO bonuses. Thus, although there are legitimate reasons for nonprofit hospitals to accumulate excess cash, concerns about its potential misappropriation cannot be ruled out.

This study makes an important contribution to the nonprofit management literature by examining the implications of excess cash in nonprofit hospitals using a rich nationally representative dataset derived from the Centers for Medicare and Medicaid Services (CMS) and the American Hospital Association (AHA). Furthermore, this paper makes two methodological contributions. First, I benchmark nonprofit hospitals’ cash holdings against those of for-profit hospitals. This approach is novel and based on prior research that suggests that corporate governance and oversight may be stronger in the for-profit sector (Vermeer et al., 2014). Second, I use a newly available compensation dataset that includes employee titles to accurately identify CEOs. Prior research, in the absence of identifying information, relied on the unsubstantiated assumption that the highest-compensated employee is the CEO.

The paper proceeds as follows. The next section discusses the literature related to cash holdings in nonprofit organizations. Section “Hypothesis development” develops three key hypotheses. Section “Research design” describes the models. Section “Data and sample selection” summarizes the data sources and the sample. Section “Descriptive statistics” presents the results of the analyses, and sections “Discussion” and “Conclusion” conclude the paper.

Background and Literature Review

Theory suggests that organizations (for-profit, nonprofit, or public) hold cash and other liquid assets for various reasons. The transaction motive suggests that organizations prefer to hold cash to avoid the transaction costs involved in converting illiquid assets to cash, and vice versa (Baumol, 1952). Organizations also hold cash to guard against future adverse economic conditions, called the precautionary motive (Almeida et al., 2004; Keynes, 1936). Jensen (1986) introduced the idea that an organization’s excess cash holdings can be explained using agency theory as large free cash flows often lead managers to make acquisition decisions that destroy shareholder value. However, empirical research on the relationship between cash and agency problems in for-profit firms shows mixed results (Bates et al., 2009; Graham & Leary, 2018; Harford et al., 2008; Opler et al., 1999).

The extant nonprofit management literature considers multiple measures of liquidity. A body of work examines the role of operating reserves (operationalized as liquid unrestricted net assets [LUNA 1 ]) in improving outcomes such as stability and sustainability (Bowman, 2011). These reserves are closely related to cash but can also include other less liquid assets such as receivables and investments. Academic work suggests that to qualify as reserves, funds should be: (a) liquid; (b) free from donor-imposed restrictions; and (c) designated by the board (Grizzle et al., 2015). However, nonprofit practitioners also include a wide range of other resources in their definition of reserves (Sloan et al., 2015, 2016). Research shows that nonprofits hold reserves to maintain services and overall stability under adverse economic conditions, consistent with the precautionary motive (Calabrese, 2012, 2018; Hansmann, 1990; M. Kim & Mason, 2020; Mitchell, 2017; Tevel et al., 2015). Reserves are particularly important for small nonprofits which often have limited access to borrowing (Bowman, 2002). Yet, a significant number of nonprofit organizations report small or no reserves (Blackwood & Pollak, 2009; Grizzle et al., 2015). Reserves can also signal good financial health and future viability, which donors favor, but excess reserves can negatively affect future donations (Calabrese, 2011a; Marudas, 2004). There is no evidence that operating reserves are associated with agency problems, nor that liquidity (measured as the ratio of working capital to total assets) is associated with organizational mortality (Calabrese, 2018; Park et al., 2022). Research on Australian nonprofits suggests that younger, larger, and government funded organizations tend to hold smaller reserves which is associated with financial vulnerability and high levels of debt (Booth et al., 2017; Cortis & Lee, 2019). Irvin and Furneaux (2022) argue that the optimal size of reserves should be determined in the context of organizational size and operational volatility.

Fisman and Hubbard (2003) develop a model of optimal “endowments” (measured as total net assets) for nonprofits which considers the tradeoff between benefits in the form of smooth operations and the potential costs of agency problems. In this framework, principals (donors) want to maximize the charitable output and therefore create financial “endowments” to minimize disruption caused by operational volatility. However, self-interested agents (managers) may, in the absence of adequate monitoring and oversight by the principals (donors), divert such “endowments” for private benefits. This framework provides several testable hypotheses to understand why nonprofit organizations accumulate resources. Fisman and Hubbard (2005) predict and find that contributions to “endowments” (measured as total net assets) are higher in nonprofits with stronger government oversight. Core et al. (2006) build upon this framework and suggest that another reason for holding excess “endowments” (measured as the sum of cash, savings, and investments) is to fund future growth opportunities (called the speculative motive). However, they find that nonprofits with excess “endowments” do not exhibit higher growth or higher program spending compared with other nonprofits. Instead, excess “endowments” are positively associated with executive compensation, which indicates agency problems. Core et al.’s (2006) measure of “endowments” is different from Fisman and Hubbard (2005) but similar to what is used in the for-profit literature (Opler et al., 1999). Frumkin and Keating (2010) show that executive compensation is positively associated with “endowments” (measured as the ratio of total investments to total assets). Ramirez (2011) finds that excess cash reserves (measured as cash on hand and in bank) held by nonprofits can be explained by the precautionary and speculative motives rather than agency problems. Using the same measure of cash, Rivenson et al. (2011) focus on nonprofit hospitals and find the cash is positively associated with profitability and total asset growth, negatively associated with debt, and not associated with volatility. Pizzini and Sterin (2023) find that better governance is associated with higher levels of cash reserves (measured as the sum of cash, savings, and investments).

Hospitals require a considerable amount of capital for investment in equipment and information systems. A for-profit hospital could finance such investments through some combination of equity, retained earnings, and debt, whereas a nonprofit hospital is constrained to rely on retained earnings and debt. According to the pecking order theory, managers prefer to use retained earnings (internal liquidity) rather than external financing due to information asymmetry (Myers & Majluf, 1984). Obtaining debt can be costly or impossible for nonprofit organizations, as lenders may perceive a higher risk compared with similar for-profit entities that have access to equity financing in the event of a potential default. Indeed, evidence suggests that nonprofit hospitals lean toward using internal cash rather than debt to finance capital investments (Adelino et al., 2015; Huang et al., 2018; Smith et al., 2000; Turner et al., 2015). In this context, both speculative motive and the pecking order theory find support in the empirical relationship between accumulated cash and capital investment.

Overall, empirical evidence suggests that operating reserves help organizations maintain operations during economic volatility and signal good financial health. Operating reserves may not be associated with agency problems potentially because they are board-designated funds, which may attract greater oversight, and often include less liquid assets such as receivables. Cash, which is the most liquid asset and often not board-designated for a specific purpose, may be more likely than operating reserves to be misappropriated. In the next section, I develop testable hypotheses.

Hypothesis Development

One reason nonprofit hospitals prefer to hold more cash than their for-profit counterparts is that raising external capital is often more challenging for nonprofits. Turner et al. (2015) suggest that debt is more accessible to for-profit hospitals than to nonprofit hospitals, and among nonprofit hospitals, it is more readily available to larger entities compared with smaller ones. Evidence suggests that liquidity constraints in nonprofit hospitals negatively impact capital investments critical for providing health care (Adelino et al., 2015; Choi, 2017; T. H. Kim & McCue, 2008; Reiter et al., 2008), and this effect is more pronounced in nonprofit hospitals than for-profit hospitals (J. Kim et al., 2022). Even when nonprofit hospitals seek debt financing for capital investments, their cash holdings influence bond ratings which determine borrowing costs (Moody’s Investor Service, 2018; Rivenson et al., 2011). Therefore, regardless of the source of financing, nonprofit hospitals must maintain significant cash holdings to fund capital investments (Smith et al., 2000). Furthermore, the IRS requires nonprofit hospitals to direct surplus funds toward maintaining and improving equipment and facilities to obtain and maintain their tax-exempt status (Government Accountability Office [GAO], 2023). Prior work suggests that cash holdings of nonprofit hospitals are positively associated with asset growth (Ramirez, 2011; Rivenson et al., 2011). The distinction between cash and operating reserves is important here because the latter are primarily accumulated to stabilize operations during economically challenging times and, therefore, neither intended nor used to grow the size of assets, as suggested by the extant literature. I state my first hypothesis as follows:

If a nonprofit hospital has exhausted all avenues for program spending and capital investment, it may consider using surplus resources for community benefits (Kauer & Silvers, 1991). Potential sources of surplus could be accumulated excess cash and operating reserves, but the latter is usually board-designated for fiscal stabilization and thus unlikely to be available for other purposes such as expanding charity care provision. Excess cash may be a better proxy for highly liquid and readily available resources that can be deployed for community benefits.

The IRS requires nonprofit hospitals to provide charity care to maintain their tax-exempt status (GAO, 2023). Although no formal threshold exists for the level of charity care, the IRS previously used 5% of the total revenue rule (House Ways and Means Committee, 2005). Bakken and Kindig (2015) report that in most states, the average community benefit expense of nonprofit hospitals exceeds 5% of the total expenses. Attempts to legislate minimum requirements by states have had little effect on charity care provision, which suggests that most nonprofits already exceed the minimum threshold (Kennedy et al., 2010; Rothbart & Yoon, 2022). Research suggests that nonprofit hospitals are more likely than for-profit hospitals to provide uncompensated and unprofitable medical services (Bruch & Bellamy, 2021; Garthwaite et al., 2018; Horwitz, 2005). Surplus cash may give a nonprofit hospital the financial strength to pursue its charitable mission more intensely. Chen et al. (2009) show that financially strong nonprofit hospitals provide more charity care than financially weak nonprofit hospitals. Dranove et al. (2017) show that nonprofit hospitals were more likely to eliminate unprofitable services after the 2008 recession due to financial weakness. However, some studies suggest that increase in margins and non-operating income is not associated with increased charity care provision (S. M. Desai & McWilliams, 2018, 2021; Song, McCullough, & Reiter, 2013). I state my second hypothesis:

A potential risk of holding too much cash is that it can be used by executives for private benefits (Fama & Jensen, 1983). Research on the relationship between excess liquidity (using various measures) and executive compensation in nonprofits shows mixed results. Some studies suggest that excess cash is positively associated with CEO compensation (Balsam et al., 2020; Core et al., 2006; Feng et al., 2022; Frumkin & Keating, 2010; Yonce, 2023), while others find no relationship (Calabrese, 2018; Ramirez, 2011). Among nonprofit subsectors, hospitals pay the highest executive salaries on average (Gaver & Im, 2014; Ramirez, 2011). Nonprofit hospitals are also more likely than other nonprofits to pay bonuses to executives (Balsam & Harris, 2018). Naturally, executive compensation in nonprofit hospitals attracts significant attention from scholars (Ackerman et al., 2005; Akingbola & van den Berg, 2015; Brickley et al., 2010; Cardinaels, 2009; T. Carroll et al., 2005; Mulligan et al., 2022).

Research shows that while CEO base salaries are higher in nonprofit hospitals compared with for-profit hospitals, for-profits pay significantly larger bonuses than nonprofits (Ballou & Weisbrod, 2003; Mulligan et al., 2020; Preyra & Pink, 2001). Furthermore, there is evidence to suggest that excess executive compensation may be associated with weak monitoring by fund providers (Fisman & Hubbard, 2003; Gaver & Im, 2014). Notably, Balsam et al. (2020) show that monitoring by donors is associated with lower perquisites. While major donors often play a role in monitoring executives within donation-driven nonprofits, the reliance of nonprofit hospitals on patient revenue limits the effectiveness of donor oversight (Aggarwal et al., 2012). I propose my third and final hypothesis:

Research Design

I estimate a benchmark model for nonprofit cash holdings using a pooled sample of nonprofit and for-profit hospitals. I create my sample by merging data from the Centers for Medicare and Medicaid Services (CMS) cost reports, American Hospital Association (AHA), and Statistics of Income (SOI) data files. I measure cash holdings as cash on hand and in banks (CMS Worksheet G, Line 1). Following Bates et al. (2009), the dependent variable in the benchmark model is cash as a percentage of total assets or simply Cash Ratio (CASH_R). 2 I include a dummy variable that takes the value “1” for all nonprofit observations and “0” otherwise (NFP). The nonprofit dummy variable measures the average difference in the cash ratios of for-profits and nonprofits, after controlling for other factors.

Organizational liquidity is influenced by the riskiness of cash flows and revenue (Irvin & Furneaux, 2022). Following Core et al. (2006), I proxy for revenue uncertainty using Revenue Volatility (CVREV), which is calculated by dividing the standard deviation of total revenue by the mean of total revenue, both measured over the 3 years from year t − 2 to year t. Total revenue is the sum of net patient revenue (Worksheet G-3, Line 3) and total other income (Worksheet G-3, Line 25). At least 3 years of data on total revenue is required to calculate Revenue Volatility; otherwise, the observation is dropped.

The transaction motive for holding cash suggests that larger organizations hold less cash. To control for organizational size, I include the natural logarithm of total assets (Worksheet G, Line 36). Organizations with access to debt may hold less cash because capital investment needs can be satisfied through borrowing. For-profit organizations tend to have easier access to debt because they can borrow against future profits by offering shares as collateral, an option unavailable to nonprofits. Following Core et al. (2006), I include a dummy variable to control for access-to-debt heterogeneity (ACCESS_TO_DEBT). The variable is coded “1” if the organization has obtained long-term debt in any of the three preceding years (year t − 2 to year t) and “0” otherwise. If an organization reports an increase in total long-term liabilities (Worksheet G, Line 50) in year t from year t − 1, the organization is considered to have obtained debt.

Research suggests that there may be systematic differences between for-profit and nonprofit hospitals in the speed of collection from debtors and payments to creditors, which could influence the need for working capital (Plante, 2009). I control for working capital heterogeneity between nonprofits and for-profits using Cash Conversion Cycle (CCC), defined as the sum of the days of inventory outstanding, the average collection period, and the negative of the average payment period. Days of inventory outstanding is defined as 365 divided by the inventory turnover ratio, calculated as total revenue divided by inventory (Worksheet G, Line 7). The average collection period is measured as net accounts receivable (Worksheet G, Line 4 minus Line 6) divided by net patient revenue and multiplied by 365. The average payment period is measured as current liabilities (Worksheet G, Line 45) divided by total expenses (Worksheet G-3, Line 4 and Line 27) less depreciation (Worksheet G-2, Part II), multiplied by 365. Cash Conversion Cycle measures the average number of days an organization takes to convert its cash into inventory, inventory into sales, and sales into cash.

Teaching hospitals often have higher profit margins and liquidity than non-teaching hospitals (McCue & Thompson, 2011). To control for this potential confounder, I include a dummy variable (TEACH) that is coded “1” if the hospital reports the Council of Teaching Hospitals (COTH) designation in the annual AHA survey and “0” otherwise. Being a member of a multi-hospital system can increase access to capital and reduce the need for cash (N. Carroll, 2016). I include a dummy variable (SYSTEM) that is coded “1” if the hospital is part of a health care system (as indicated in AHA survey) and “0” otherwise. I include year, state, and service specialty (e.g., general medicine, psychiatric, acute long-term care) fixed effects to control for any confounding effects of these variables. The benchmark cash model I estimate is as follows:

After estimating the benchmark model, I generate the predicted values for all nonprofit hospitals in the sample. I subtract the coefficient on NFP from the predicted values to obtain what would be the predicted values of the cash ratio if the organizations were for-profit hospitals. Then, I subtract the values thus obtained from the observed values of cash ratio to obtain Excess Cash Ratio (EXCESS). To be precise, excess cash equals observed cash ratio minus predicted cash ratio. The predicted cash ratios from the benchmark model represent average cash ratios of comparable for-profit hospitals. So, a positive (negative) value of excess cash indicates higher (lower) cash holdings than those of a similar for-profit hospital. The assumption here is that after adjusting for a range of differences (revenue volatility, access to debt financing, working capital requirement, teaching designation, system membership, etc.), nonprofit and for-profit hospitals would hold similar levels of cash. Systematically higher cash holdings by nonprofit hospitals are deemed “excess” and examined in subsequent analyses.

At this stage, I drop all for-profit firm observations and focus the subsequent analyses only on nonprofit hospitals. To test H1, I examine the relationship between excess cash holdings, represented by the three explanatory variables, and the change in fixed assets. I use a continuous variable Excess Cash Ratio, a dummy variable TOP_HALF (takes the value “1” for observations with above median values of Excess Cash Ratio and “0” otherwise), and a dummy variable Q4 (“1” for observations in top quartile of Excess Cash Ratio and “0” otherwise). I estimate the following regression equation:

where D_FIX represents the percentage change in the value of total fixed assets (Worksheet G, Line 30) from year t to year t + 1. This operationalization is consistent with Core et al. (2006) and Calabrese and Gupta (2018). The percentage change from 1 year to the next is influenced by the size of existing fixed assets. A large fixed asset base tends to grow at a slower rate compared with a smaller fixed asset base. Therefore, I control for the size of fixed assets using the natural log of total fixed assets (LOG_FIX). Exclusion of the size of fixed assets may cause omitted variable bias if Excess Cash Ratio is correlated with the size of fixed assets within an organization. For example, if high growth in fixed assets is primarily due to the small size of existing fixed assets which in turn is positively correlated with excess cash, then the results may falsely attribute the growth in fixed assets to excess cash.

Research shows that nonprofit hospitals use profits to fund organizational growth (Lu & Park, 2024). Therefore, I control for profitability using Profit Margin (PROFIT), measured as the difference between total revenue (Form 990 Part VIII, Line 12(A)) and total expenses (Part IX, Line 25(A)) divided by total revenue and multiplied by 100. Explanatory Var is replaced by Excess Cash Ratio, Top Half Indicator, and Top Quartile Indicator in the different estimations of equation 2. I also include year and organization fixed effects to control for year- and organization-specific confounders.

To test H2, I estimate the following regression equation:

where D_CHARITY represents the percentage change in “financial assistance at cost” (Schedule H Part I, Line 7a(e)) from year t to year t + 1. I control for the level (size) of current charity care expenses using the natural logarithm of “financial assistance at cost” (LOG_CHARITY) because a higher (lower) current level might change at a slower (faster) rate. A highly profitable organization may be inclined to provide more charity care to avoid regulatory scrutiny (Leone & Van Horn, 2005). I include Profit Margin to control for the effect of profitability on charity care expenses. Organizations that receive significant private contributions may feel obligated to provide community benefits (Park & Peng, 2020). I include PRIV_CONT, measured as nongovernment contributions (Part VIII, Line 1h minus 1e) as a percentage of total revenue, to account for heterogeneity in private contributions.

The test for H3 examines the relationship between CEO compensation and excess cash. I use the following regression to test my third hypothesis:

where D_CEO represents the percentage change in the CEO’s total compensation (Part VII, sum of columns D to F) from year t to year t + 1. Highly paid CEOs may experience slower compensation growth rates. I include the natural logarithm of CEO compensation (LOG_CEO) to control for the current compensation level. Following Balsam and Harris (2018), who find a positive relationship between profitability and executive incentive pay, I include Profit Margin to control for the effect of profitability on CEO compensation. Finally, I include the natural logarithm of total revenue (LOG_REV) to account for any changes in executive compensation driven by growth in total revenue.

I trim all continuous variables at the 1st and 99th percentiles separately for nonprofits and for-profits to reduce the influence of extreme values. I inflation-adjust all monetary values based on the Consumer Price Index (CPI), using 2010 as the base year. I log-transform several variables to reduce the degree of skewness. Because log is undefined for 0, I add a positive constant to the raw value before taking the natural logarithm. The next section discusses the data sources and sample selection process.

Data and Sample Selection

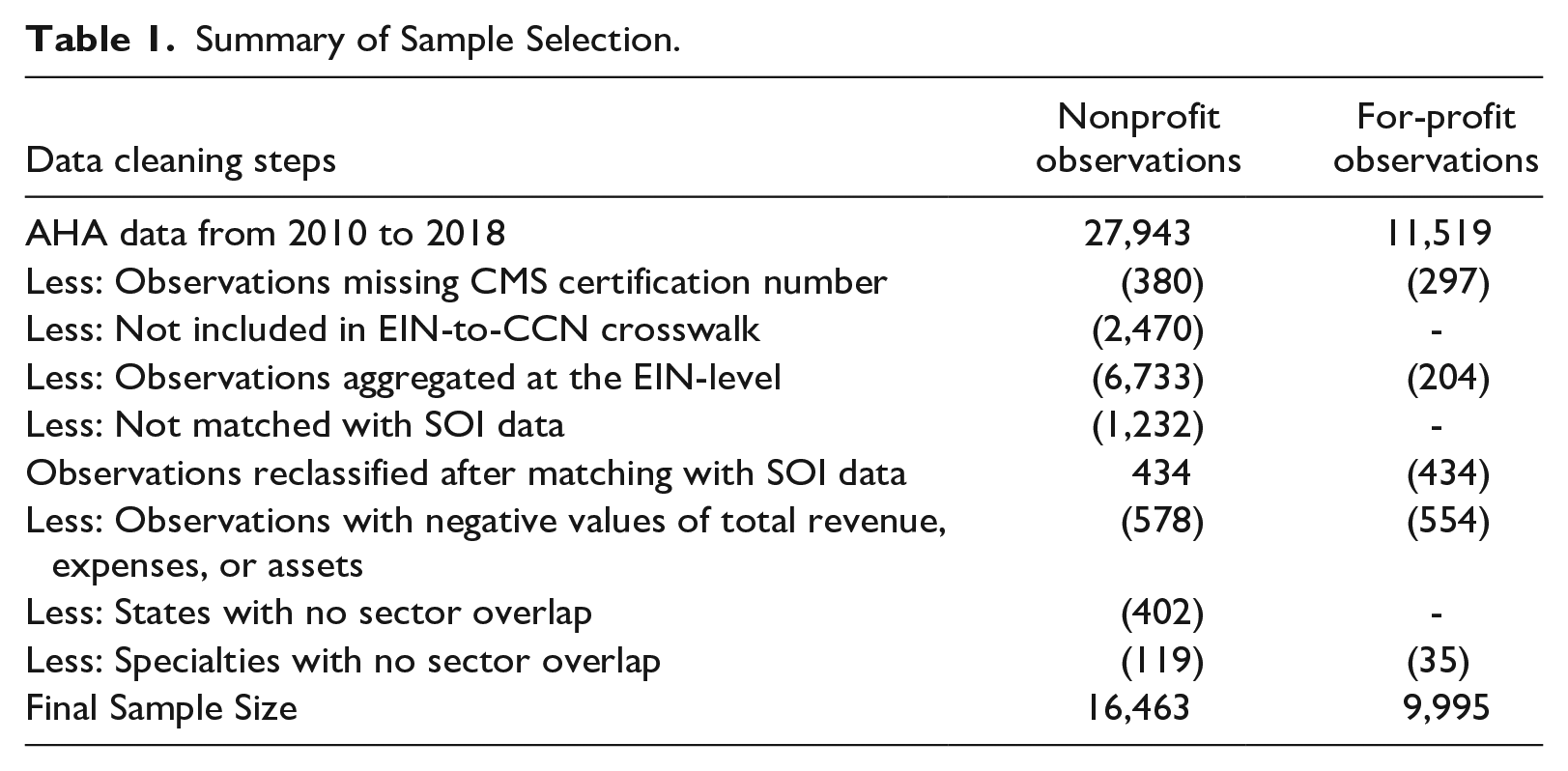

The data for this study comes from three sources: CMS cost reports, the AHA, and the National Center for Charitable Statistics (NCCS). I purchased data on for-profit and nonprofit hospitals from the AHA, which contains proprietary data from the AHA Annual Survey and publicly available data from CMS cost reports. Each hospital in the dataset is uniquely identified by its CMS certification number (CCN). To merge the AHA data with the SOI dataset published by the NCCS, I use the publicly available Community Benefit Insight (CBI) Hospital Data API 3 which provides a CCN to Employer Identification Number (EIN) crosswalk.

I start with the AHA data, which contains annual observations from 2010 to 2018 on 6,479 unique hospitals of various ownership types: government, nonprofit, and for-profit. I merge this data with the CBI crosswalk and exclude all unmatched nonprofit observations. Many health care groups operate multiple hospitals but file a single Form 990 return because of which many EINs in the sample are linked to multiple CCNs. To keep the analysis at the EIN level, I aggregate all hospital-level continuous variables to the EIN level through summation. Subsequently, each observation is uniquely identified using EIN and year. For binary variables, which cannot be aggregated by summing, I compute averages weighted by total assets and recode as “1” if the aggregated value crosses the 0.5 threshold and “0” otherwise. For categorical variables, I use the modal value for aggregation. I then merge the remaining AHA data with the IRS SOI dataset, which contains information on charity care, contributions, and executive compensation. I reclassify an observation as a nonprofit if it is matched with SOI data, even if the AHA data coded it as a for-profit hospital. All observations that report negative values for total assets, total revenue, and total expenses are excluded. To keep the sample comparable across the for-profit and nonprofit sectors, I exclude all observations belonging to states and service specialties in which there is no cross-sector competition. 4

Although nonprofits are required to report employee job titles in Part VII of Form 990, the SOI files do not contain that information, without which CEOs cannot be identified. To overcome this challenge, I extracted Part VII data from the Form 990 e-filings available on Amazon Web Services (AWS). For nonprofits that do not e-file, I purchased hand-collected Part VII data from Candid (formerly GuideStar). My Part VII dataset covers nonprofits with assets greater than US$50 million from 2012 to 2018. Prior studies that use the SOI data rely on the assumption that the highest paid officer is the CEO of the organization (Balsam & Harris, 2018; Core et al., 2006; Ramirez, 2011). While this assumption is reasonable in the absence of identifying information, it may introduce bias if the CEO is not the highest compensated employee. My dataset allows me to empirically test this assumption. 5

The final sample contains 2,130 nonprofit hospitals with 16,463 observations and 1,528 for-profit hospitals with 9,995 observations. Table 1 summarizes the sample-selection process.

Summary of Sample Selection.

Descriptive Statistics

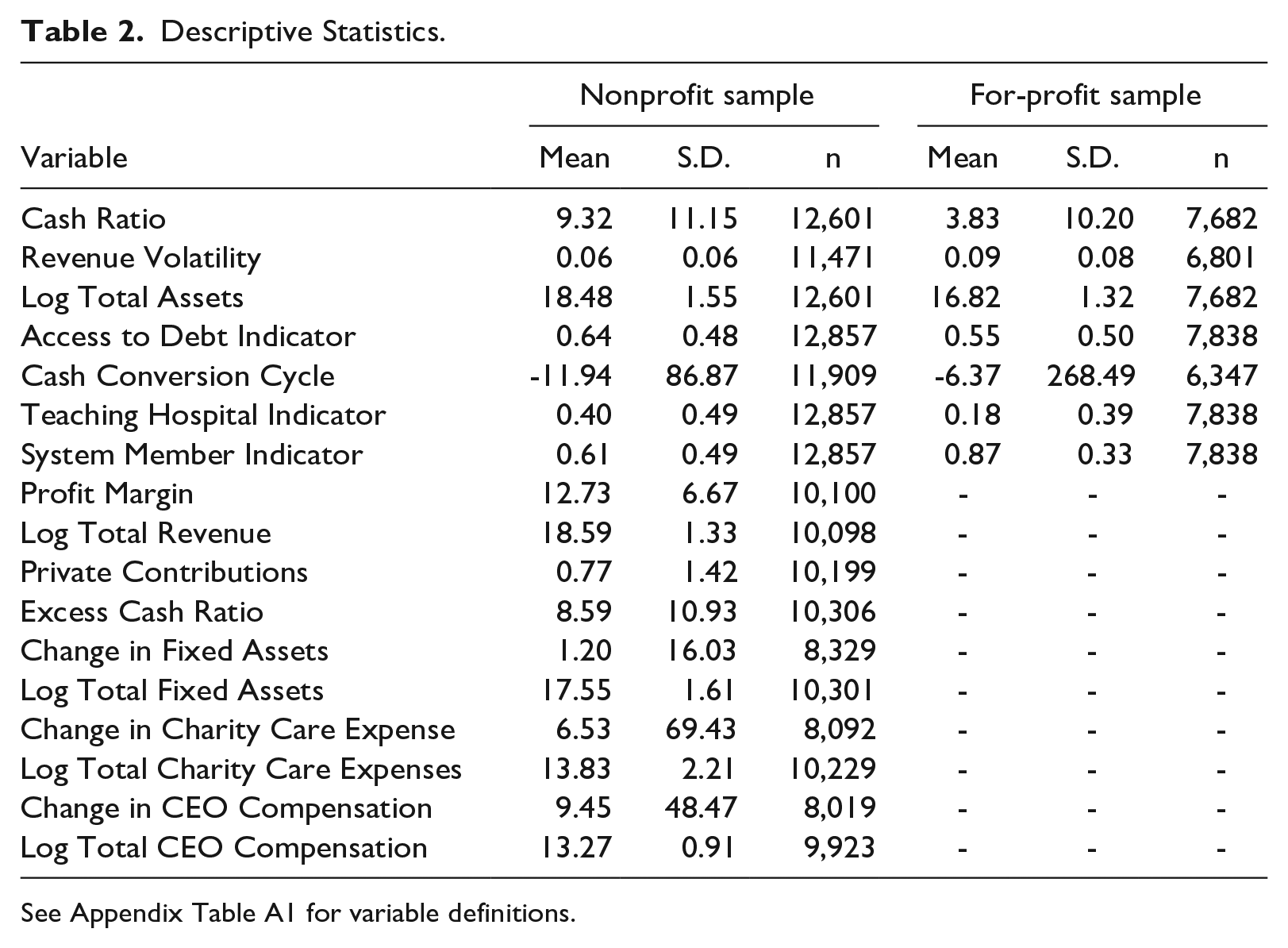

Table 2 presents the descriptive statistics for the nonprofit and for-profit samples. The mean values of cash ratio show that nonprofit hospitals, on average, hold more assets in the form of cash than for-profits. Table 2 shows that for-profit hospitals face higher revenue volatility, on average, than nonprofit hospitals. The average organizational size is larger for the nonprofit sample than for the for-profit sample. On average, 64% of the nonprofit sample has access to debt financing, compared with only 55% of the for-profit sample. This difference suggests that for-profit hospitals may not borrow as much as nonprofit hospitals because they can obtain equity financing which is not available to nonprofits. The mean values of cash conversion cycle are negative for both nonprofit and for-profit hospitals which suggests that average payments periods are longer than average collection periods. A negative cash conversion cycle indicates that the organization is paid by its customers before it pays its suppliers.

Descriptive Statistics.

Table 2 shows that teaching hospitals are significantly more common in the nonprofit sector (40%) than for-profit sector (18%). Health care system membership is more common in the for-profit sample (87%) than nonprofit sample (61%). The descriptive statistics for Profit Margin, Private Contributions, Change in and Log Fixed Assets, Change in and Log Charity Care Expense, and Change in and Log CEO Compensation are reported only for the nonprofit sample because these variables are used in models that apply only to nonprofits. The table shows that CEO compensation increased by 9.4% each year, on average, and charity care spending increased by 6.5% each year.

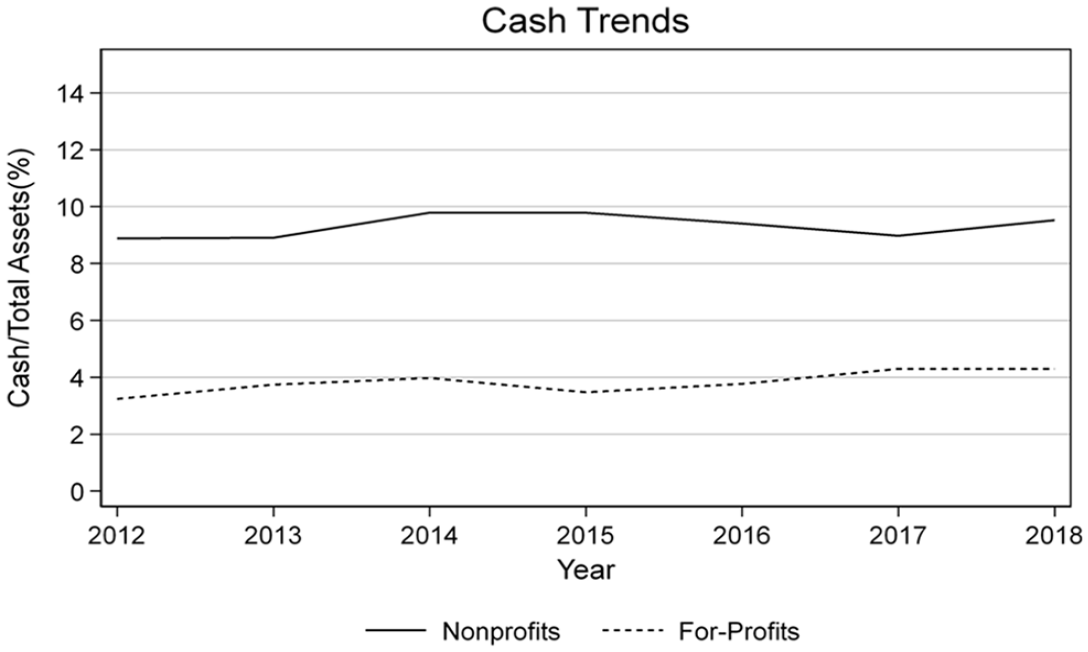

Figure 1 visually presents mean cash ratios by sector and year, showing that nonprofit hospitals consistently hold more cash than for-profit hospitals. Throughout the study period, a significant gap is evident between the cash ratios of for-profit and nonprofit hospitals. In 2012, the average nonprofit hospital held 8.88% of total assets in cash, while the average for-profit hospital held only 3.24%. By 2016, the average cash ratio for for-profit hospitals had increased to 3.77%, whereas that of nonprofit hospitals had risen to 9.41%. Notably, each year, nonprofit hospitals held at least twice as much cash on average as their for-profit counterparts, as a proportion of total assets.

Mean Cash Ratios by Sector.

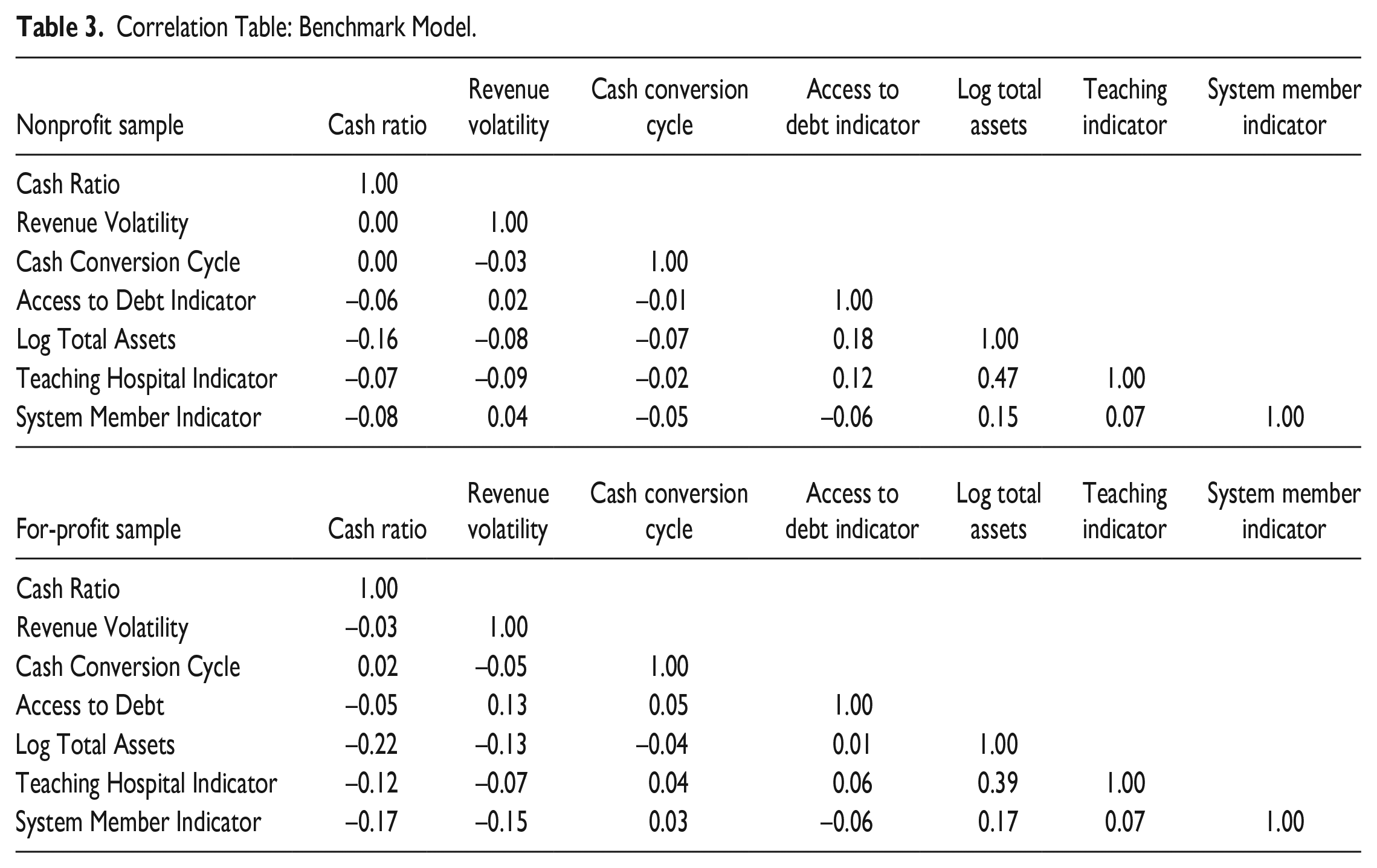

Table 3 presents the pairwise correlation matrix for both the nonprofit and for-profit samples. In both samples, the cash ratio is negatively correlated with organizational size (Log Total Assets) and system affiliation, which is consistent with the transaction motive of holding cash. The nonprofit sample shows a positive correlation between access to debt financing and organizational size, whereas the for-profit sample does not. This suggests that debt financing may be out of reach for small nonprofit hospitals though not for small for-profit hospitals. Both samples show a strong positive correlation between organizational size and teaching status. The next section summarizes the results of the regression analysis.

Correlation Table: Benchmark Model.

Results

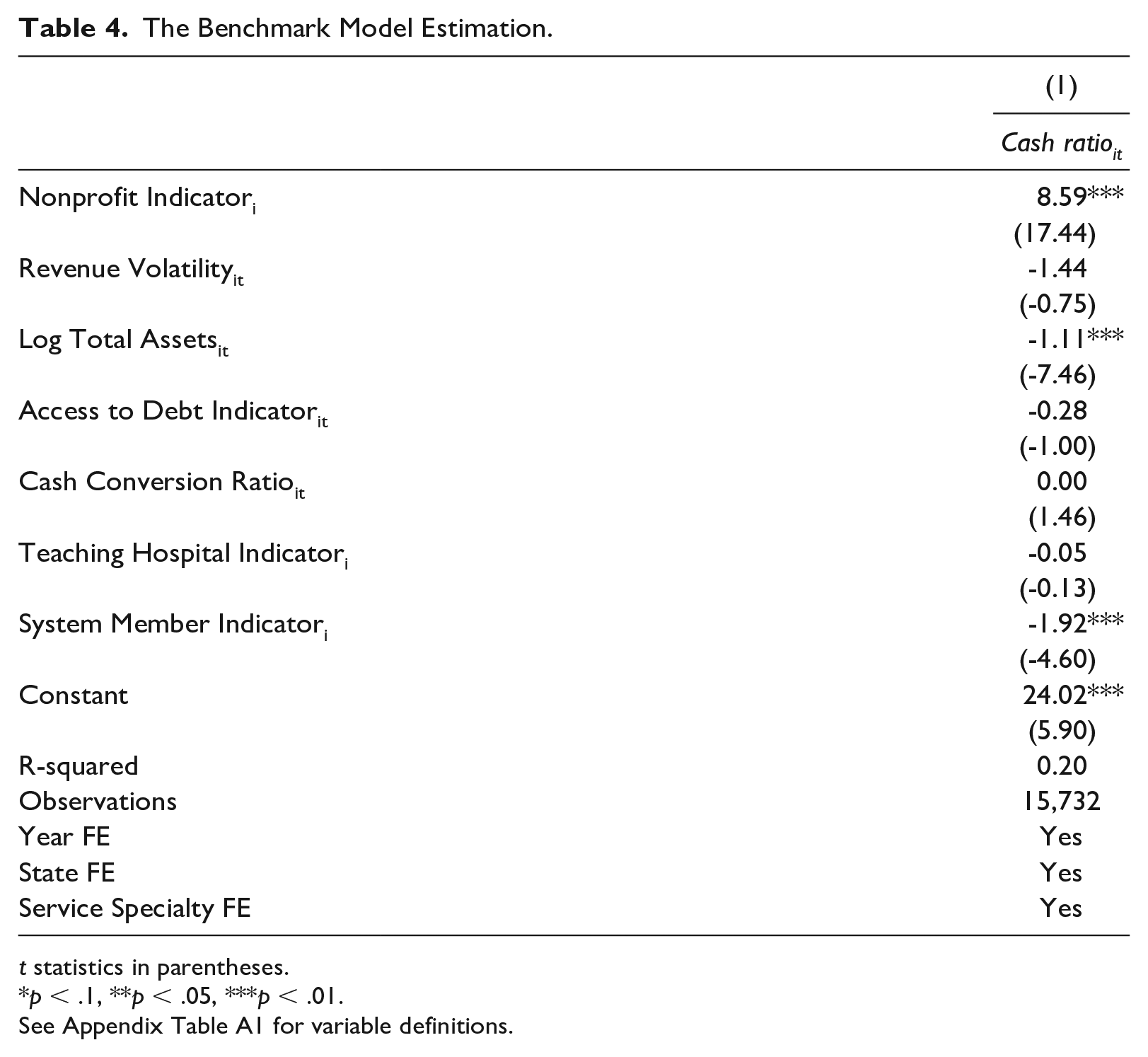

Table 4 presents the benchmark cash model estimation results (Equation 1). The coefficient on the nonprofit binary variable suggests that the nonprofits’ cash ratio is 8.59 percentage points higher than the for-profits’ cash ratio, on average. The coefficient on Revenue Volatility suggests that organizations facing greater revenue uncertainty tend to hold less cash; however, consistent with Rivenson et al. (2011), this estimate is not statistically significant. The negative and statistically significant coefficient on Log Total Assets, consistent with the transaction motive of cash holdings, suggests that larger organizations tend to hold less cash than smaller ones. The coefficient on Access to Debt Indicator suggests that organizations that can obtain debt financing require smaller cash buffers, but it is not statistically significant. The coefficient on Cash Conversion Cycle is positive but statistically and economically insignificant. The coefficient on System Member Indicator is negative and statistically significant, suggesting that hospitals that are part of a health care system require smaller cash holdings.

The Benchmark Model Estimation.

t statistics in parentheses.

p < .1, **p < .05, ***p < .01.

I use the estimates from the benchmark model to calculate excess cash, which is used in the subsequent models as the main independent variable. The mean and median values of Excess Cash Ratio are 8.59 and 5.31, respectively. About 15% of the nonprofit sample reports negative excess cash and 85% reports positive excess cash. The subsequent analyses focus on the effect of Excess Cash Ratio on Change in Fixed Assets, Charity Care Expense, and CEO Compensation in nonprofit hospitals. A correlation table for the variables used in the analyses is presented in Appendix Table A2.

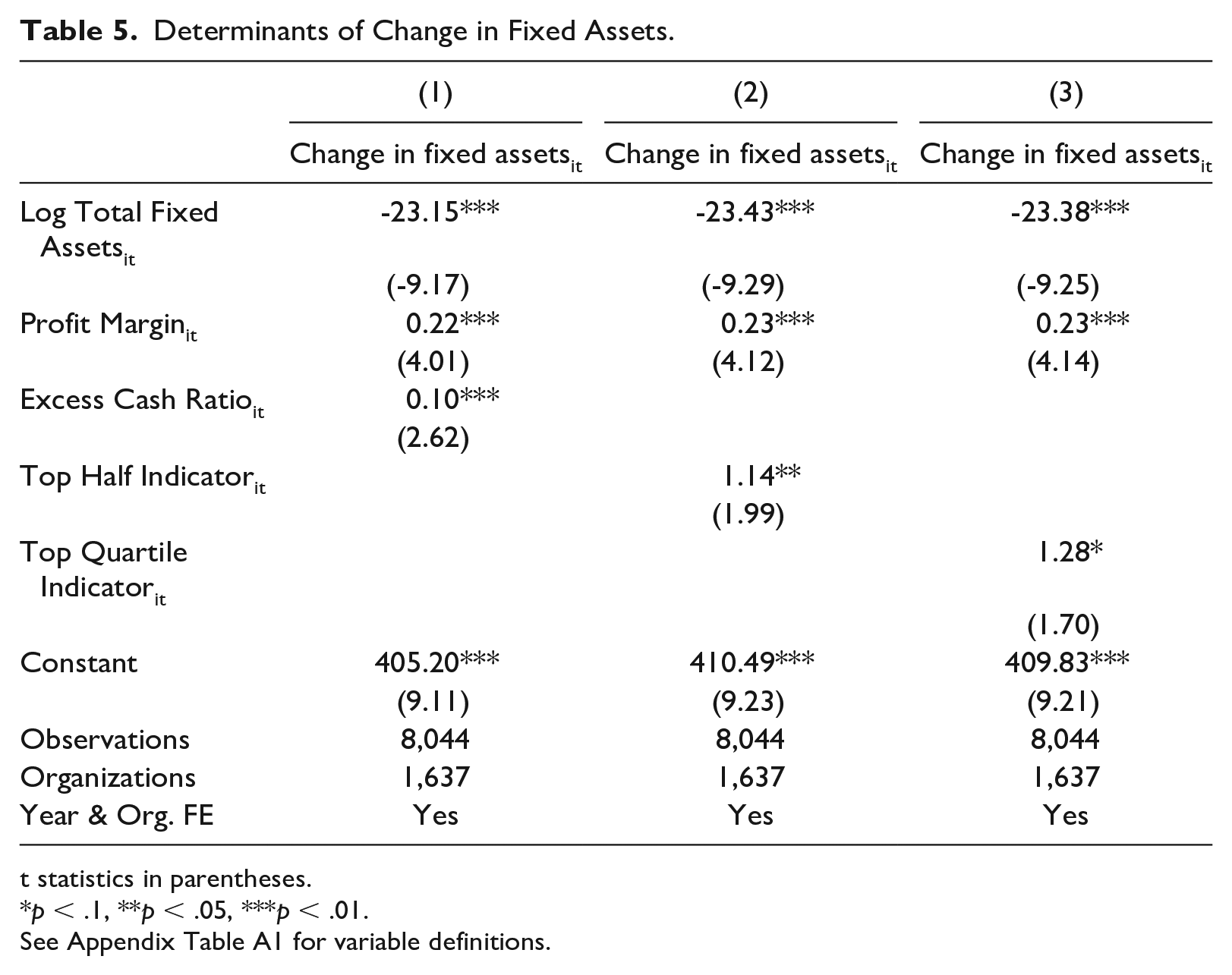

Table 5 presents the results of estimating Equation (2). The dependent variable in all three columns is the percentage change in fixed assets from year t to t + 1. The first column reports a positive and statistically significant coefficient on Excess Cash Ratio, which suggests that a one percentage point increase in excess cash is associated with a 10 basis point higher growth in fixed assets. This effect size may not seem large at first; however, because fixed assets are typically high-value assets, even a 0.1 percentage point increase can be economically meaningful. The coefficient on Top Half Indicator is positive and statistically significant in the second column, which suggests that nonprofits in the top two quartiles of excess cash show a 1.14 percentage point higher growth in fixed assets than nonprofits in the bottom two quartiles. The third column shows that nonprofits in the top quartile of excess cash report a 1.28 percentage points higher growth in fixed assets than nonprofits in the other three quartiles. However, this relationship is statistically significant only at the 10% level. The coefficients on Log Total Fixed Assets are negative and statistically significant in all three columns, suggesting that fixed asset growth is inversely related to the size of existing fixed assets. Overall, the results in Table 5 suggest that nonprofits with excess cash tend to invest more in fixed assets.

Determinants of Change in Fixed Assets.

t statistics in parentheses.

p < .1, **p < .05, ***p < .01.

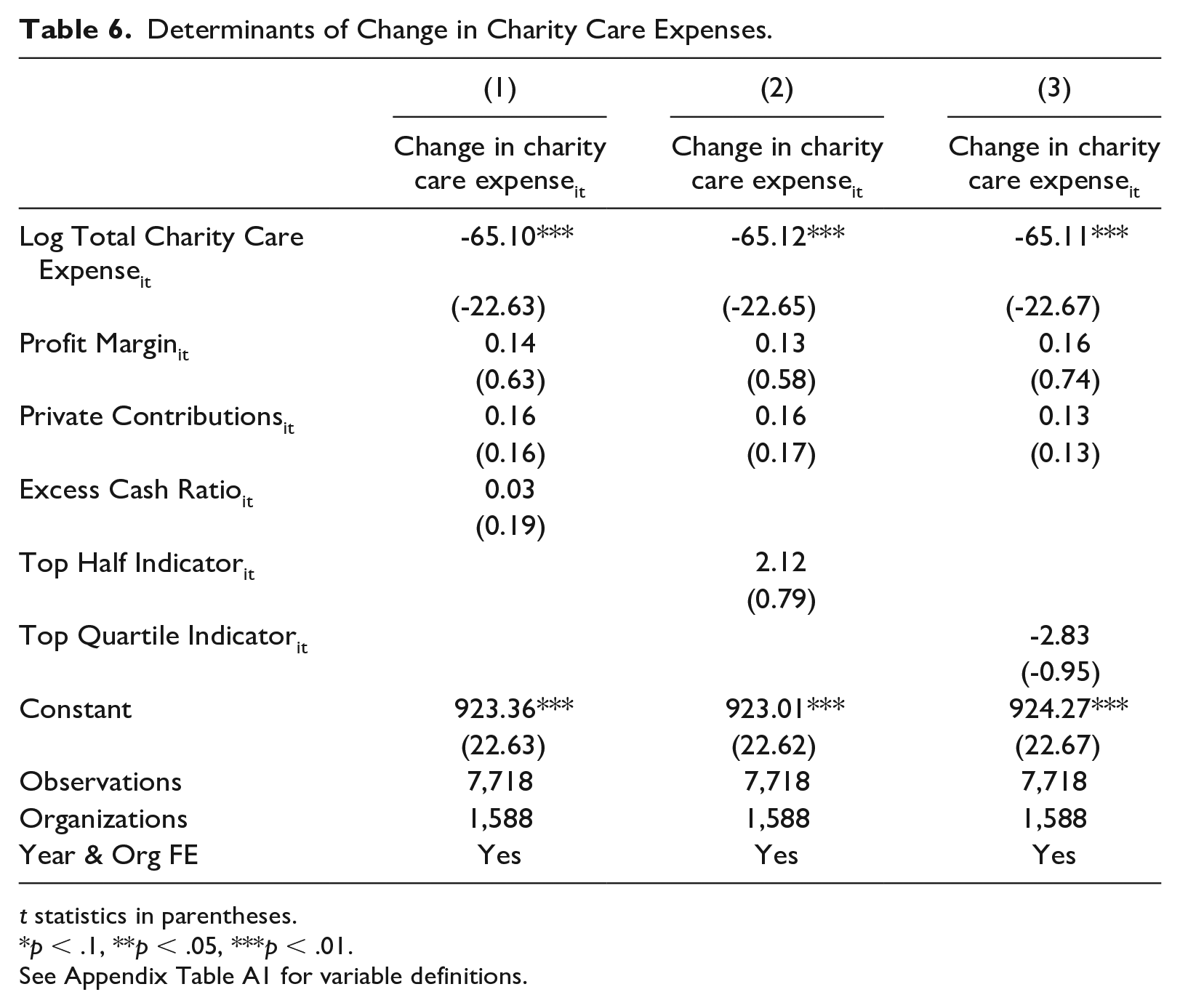

Table 6 presents the results of estimating Equation (3). The dependent variable in all three columns is the percentage change in charity care expenses from year t to t + 1. 6 The first column reports a positive but statistically and practically insignificant coefficient on excess cash. The second column reports an economically significant but statistically insignificant coefficient on Top Half Indicator. The third column reports a negative and statistically insignificant coefficient on Top Quartile Indicator, suggesting that organizations in the top quartile of excess cash report a lower percentage change in charity care than organizations in the bottom three quartiles. The negative and statistically significant coefficients on Log Total Charity Care Expense suggest that organizations that provide less charity care tend to increase charity care at a higher rate than those that provide more. Overall, Table 6 shows no evidence to support H2 that excess cash is related to charity care expenses. As a robustness check, I examine the relationship between excess cash and two other measures of charity care expense—“financial assistance and means-tested government programs” (Schedule H Part I, Line 7d(e)) and “financial assistance and other community benefits” (Schedule H Part I, Line 7k(e)). I find no relationship between excess cash and alternative measures of charity care.

Determinants of Change in Charity Care Expenses.

t statistics in parentheses.

p < .1, **p < .05, ***p < .01.

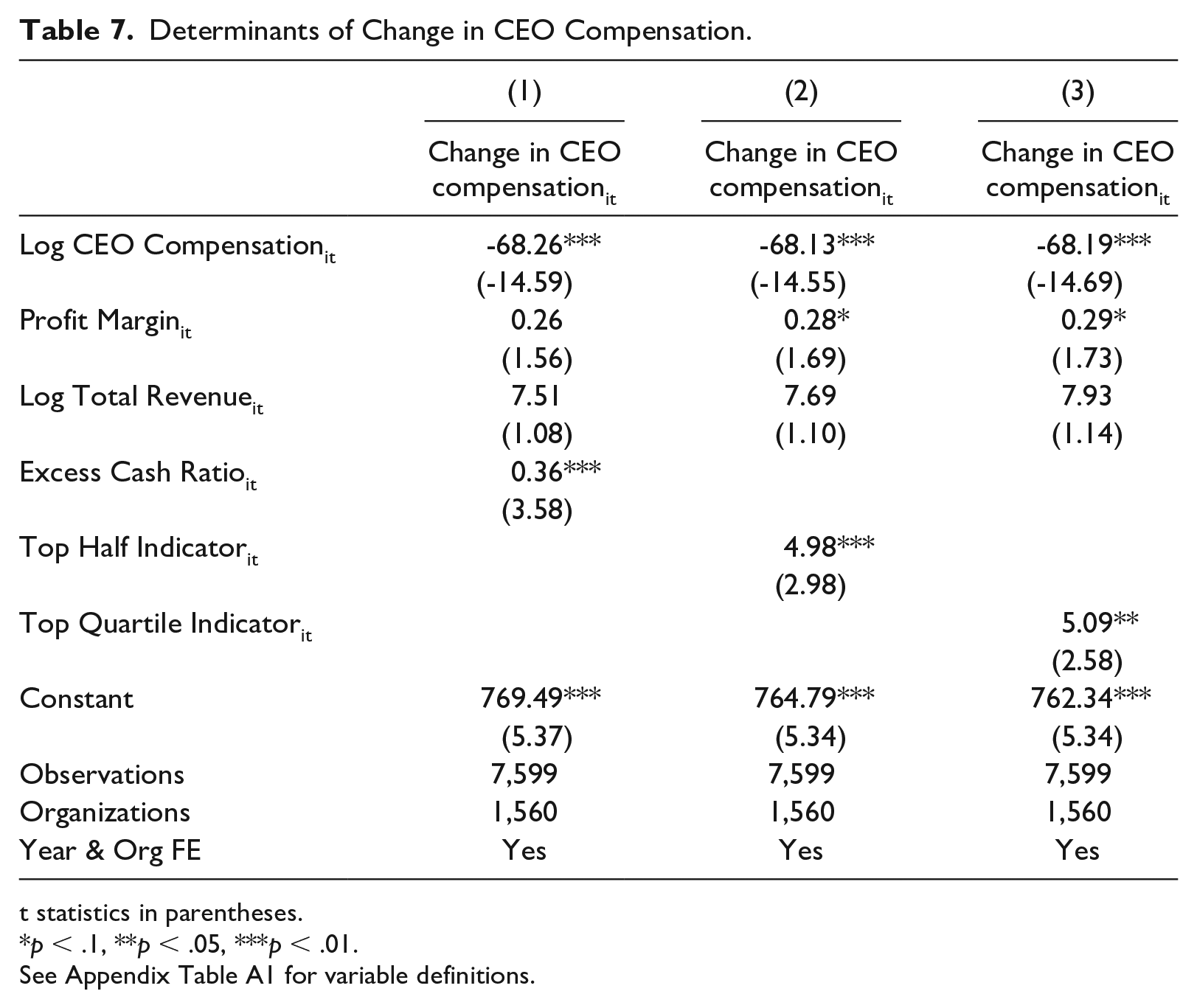

Table 7 reports the results of estimating Equation (4). The dependent variable in these regressions is the percentage change in total CEO compensation from year t to t + 1. 7 The coefficients on Log CEO Compensation are negative and statistically significant which suggests that highly paid CEOs tend to experience slower growth in compensation than modestly paid CEOs. The coefficients on Profit Margin are positive and statistically significant at the 10% level in Columns (2) and (3), suggesting that CEO compensation is partly influenced by organizational profitability. All three explanatory variables report positive and statistically significant coefficients. Specifically, the coefficient on excess cash in the first column suggests that a one percentage point increase in excess cash is associated with a 36 basis point higher growth in CEO compensation. 8 The coefficient on Top Half Indicator in Column (2) suggests that organizations in the top two quartiles of excess cash report a 4.98 percentage point higher growth in CEO compensation than those in the bottom two quartiles. Overall, the findings suggest that excess cash is positively associated with growth in CEO compensation.

Determinants of Change in CEO Compensation.

t statistics in parentheses.

p < .1, **p < .05, ***p < .01.

To assess the benefit of identifying information, I examine the relationship between excess cash and the compensation of the highest-paid employee rather than that of the CEO. I repeat the analysis in Table 7 after replacing Change in CEO Compensation with Change in Highest Compensation, which represents the change in the compensation of the highest-paid employee, and replacing Log CEO Compensation with Log Highest Compensation, which represents the level of the highest compensation. Appendix Table A3 presents the estimation results, which show that the magnitudes and statistical significance of the coefficients on the main explanatory variables differ from those in Table 7. The results suggest that proper identification of CEOs can influence the relationship between excess cash and executive compensation. Future research should test whether identifying information is influential in other contexts.

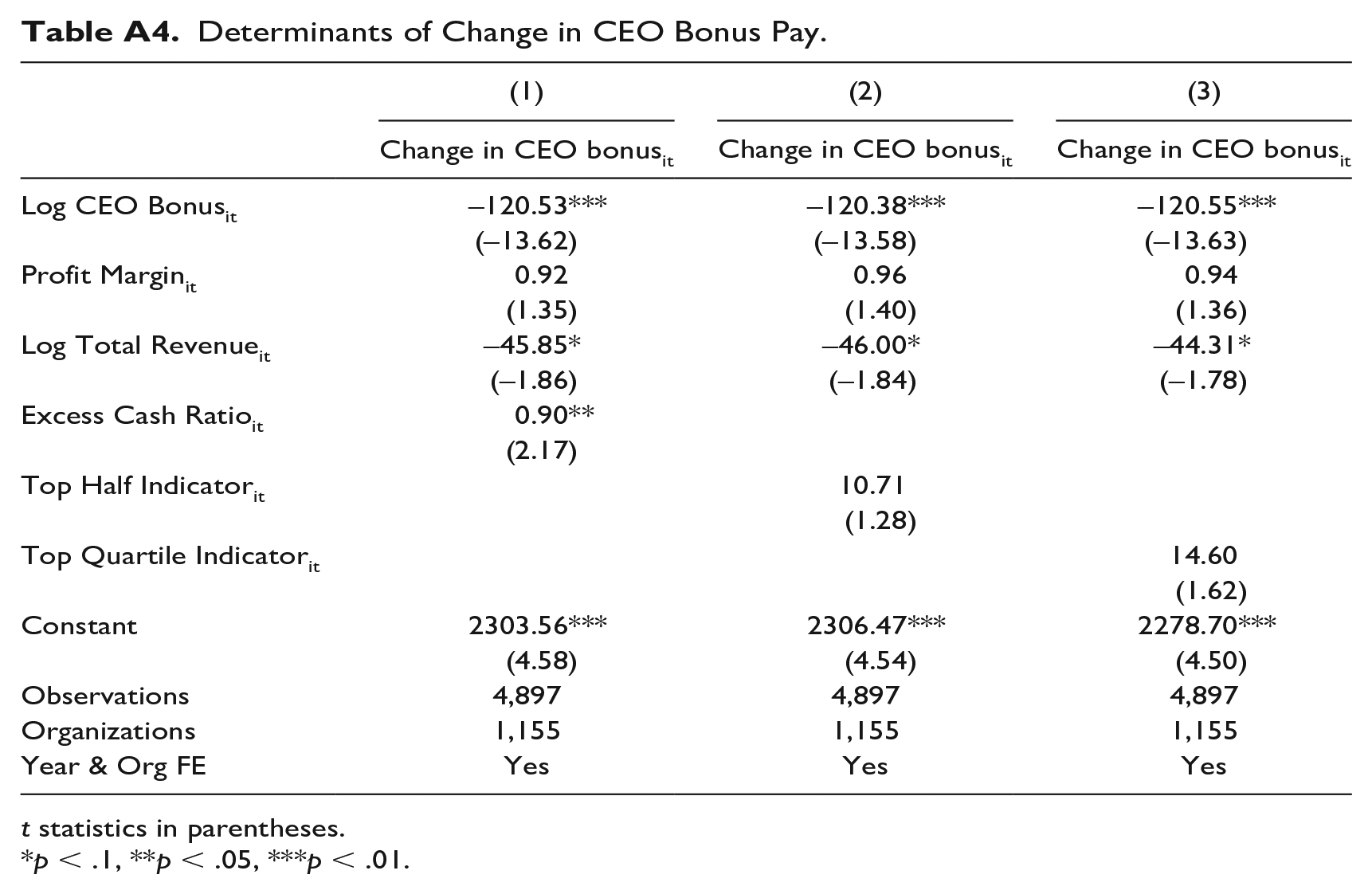

Although excessive executive compensation is generally controversial, donors have a particular aversion to high bonuses (Balsam & Harris, 2018; Galle & Walker, 2016). As an additional test, I examine whether excess cash is associated with growth in CEO bonus pay. I replace Change in CEO Compensation and Log CEO Compensation in Equation (4) with Change in CEO Bonus and Log CEO Bonus, respectively. Change in CEO Bonus represents the change in bonus pay (Schedule J Part II, Column B(ii)) and Log CEO Bonus represents the natural logarithm of bonus pay. Appendix Table A4 presents the results of this analysis, showing a positive and statistically significant relationship between excess cash and changes in CEO bonus pay. However, excess cash is estimated to have a positive but statistically insignificant relationship with Top Half Indicator and Top Quartile Indicator.

Discussion

Liquidity is vital for smooth functioning of nonprofit organizations, but excessive liquidity can lead to suboptimal results. This study advances our understanding of excess cash in nonprofit hospitals. The findings of this study suggest that excess cash is positively associated with growth in fixed assets, which is consistent with a harmless view of excess cash. This is also consistent with prior research that shows that nonprofit hospitals with significant capital requirements generally prefer internal cash to external borrowing (Calabrese, 2011b). The findings also suggest that there is no relationship between excess cash and growth in charity care expenses. If cash is accumulated specifically for investments in fixed assets, it may not be desirable to use that cash for increasing charity care provision. This finding is consistent with prior research that shows that nonprofit hospitals do not increase uncompensated care in response to higher profits (S. M. Desai & McWilliams, 2018, 2021; Lu & Park, 2024).

The finding that excess cash is positively associated with growth in CEO compensation and bonus is noteworthy, but it should be interpreted with caution. There are several explanations for this relationship, some more anodyne than others. First, the board of directors may reward the CEO of a growing organization when the organization is not cash constrained. However, this is somewhat implausible because the regression models in this study control for organizational size (using total revenue as a proxy). Second, the board may increase the compensation of a CEO who is underpaid relative to his or her for-profit peers when the organization is not cash constrained. Prior research suggests that the base salaries of CEOs are higher in nonprofit hospitals, but for-profit hospital CEOs earn more overall because of large performance bonuses (Ballou & Weisbrod, 2003; Mulligan et al., 2020). Given the lack of executive compensation data for for-profit hospitals, I cannot empirically examine this possibility. Third, consistent with the agency perspective, CEOs may use their authority to undeservedly increase their own compensation when surplus cash is available. This view is also consistent with Galle and Walker (2014), who show that executive compensation is higher in organizations with weak donor oversight.

The findings of this study underscore the importance of good governance in nonprofit organizations, particularly in nonprofit hospitals. These organizations often manage significant financial assets akin to publicly traded corporations but lack oversight from shareholders and investors. Robust governance practices are necessary to ensure that their resources are used appropriately. Boards of directors play a crucial role in promoting good governance in nonprofits which is associated with favorable outcomes such as lower executive bonus (Balsam et al., 2020) and better program service ratios (M. A. Desai & Yetman, 2015). A nonprofit may need to accumulate large sums of cash for future capacity expansion, but this should be balanced against the risk of potential misappropriation. Regardless, boards should implement measures to prevent idle cash from being used for executive pay raises. Future research should examine if governance quality moderates the relationship between excess cash and executive compensation and bonuses.

Conclusion

I examine whether nonprofit hospitals hold more cash than for-profit hospitals and how the former use their cash. Using a pooled sample of for-profit and nonprofit hospitals, I benchmark the cash holdings of nonprofit hospitals against those of for-profit hospitals. The benchmark model results show that nonprofit hospitals hold significantly more cash than similar for-profit hospitals. I test the relationship between excess cash and several potential uses of cash.

Excess cash may be optimal if it is accumulated and used in building organizational capacity, such as investments in fixed assets, or furthering the organization’s mission, such as charity care provision. However, excess cash can lead to agency problems if executives use it for private benefits. The results suggest that excess cash is associated with higher growth in fixed assets. Furthermore, I find no relationship between excess cash and charity care provision, suggesting that nonprofit hospitals may not provide more charity care when surplus cash resources are available. Finally, I find a positive relationship between excess cash and growth in CEO compensation, which may indicate agency problems. The results suggest that organizations in the top quartile of excess cash report a 5.1% higher growth in CEO compensation than those in the bottom three quartiles, which is a sizable difference.

This study contributes to the literature on liquidity in nonprofit organizations. While prior research reports no association between operating reserves and agency problems, this study finds excess cash may be associated with agency problems. A potential explanation for this divergence may lie in the differences in the nature of operating reserves and cash. Operating reserves are board-designated for a specific purpose and less liquid while cash is often undesignated and highly liquid. This study also contributes to the relatively small literature on excess cash in nonprofit organizations. Unlike prior research, it focuses on nonprofit hospitals and shows that excess cash may be explained by both the speculative motive and agency problems. Several unique aspects of nonprofit hospitals vis-à-vis other nonprofits, such as their limited dependence on donations, competition with for-profit hospitals, and operating in a highly regulated industry, may explain why the findings of this study are distinct. Furthermore, this study utilizes employee title information to more accurately identify the CEO which may partially explain the differences in findings. Future research should examine whether accurately identifying the CEO using Form 990 data matters for other research questions as well.

Finally, researchers would benefit from increased disclosures about compensation setting practices of nonprofit organizations in general. The current version of Form 990 does not clearly identify the CEO and offers limited information regarding how their compensation is determined. The IRS should consider expanding disclosures related to executive compensation after careful consideration of relevant costs and benefits.

Footnotes

Appendix

Determinants of Change in CEO Bonus Pay.

| (1) | (2) | (3) | |

|---|---|---|---|

| Change in CEO bonusit | Change in CEO bonusit | Change in CEO bonusit | |

| Log CEO Bonusit | –120.53*** | –120.38*** | –120.55*** |

| (–13.62) | (–13.58) | (–13.63) | |

| Profit Marginit | 0.92 | 0.96 | 0.94 |

| (1.35) | (1.40) | (1.36) | |

| Log Total Revenueit | –45.85* | –46.00* | –44.31* |

| (–1.86) | (–1.84) | (–1.78) | |

| Excess Cash Ratioit | 0.90** | ||

| (2.17) | |||

| Top Half Indicatorit | 10.71 | ||

| (1.28) | |||

| Top Quartile Indicatorit | 14.60 | ||

| (1.62) | |||

| Constant | 2303.56*** | 2306.47*** | 2278.70*** |

| (4.58) | (4.54) | (4.50) | |

| Observations | 4,897 | 4,897 | 4,897 |

| Organizations | 1,155 | 1,155 | 1,155 |

| Year & Org FE | Yes | Yes | Yes |

t statistics in parentheses.

p < .1, **p < .05, ***p < .01.

Data Availability Statement

The data are not publicly available due to ethical, legal, or other concerns.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.