Abstract

In this article, we investigate the diversity of healthcare delivery organizations by comparing the market determinants of hospitals entry rates with those of ambulatory surgery centers (ASCs). Unlike hospitals, ASCs is one of the growing populations of specialized healthcare delivery organizations. There are reasons to believe that firm entry patterns differ within growing organizational populations since these markets are characterized by different levels of organizational legitimacy, technological uncertainty, and information asymmetry. We compare the entry patterns of firms in a mature population of hospitals to those of firms within a growing population of ASCs. By using patient-level datasets from the state of Florida, we break down our explanatory variables by facility type (ASC vs. hospital) and utilize negative binomial regression models to evaluate the impact of niche density on ASC and hospital entry. Our results indicate that ASCs entry rates is higher in markets with overlapping ASCs while hospitals entry rates are less in markets with overlapping hospitals and ASCs. These results are consistent with the notion that firms in growing populations tend to seek out crowded markets as they compete to occupy the most desirable market segments while firms in mature populations such as general hospitals avoid direct competition.

Introduction

Countries in Europe and other parts of the world have to a various extent shifted towards a regulated competition model in both the healthcare providers and health insurance markets. 1 While internationally this move towards competition and contestability is a relatively recent trend, the United States has the longest and broadest experience in competitive markets. As a byproduct of its relatively competitive markets, starting from the early 1990s, the United States has witnessed the market entry and proliferation of new organizational forms such as urgent care centers, ambulatory surgery centers (ASCs), and specialty hospitals. This increasing diversity in healthcare delivery organizations in the United States can be best described as the growth of specialized facilities and the contraction of the traditional “do-it all” general hospitals.2–5 This trend is not restricted to the United States, other countries has also witnessed an increase in the number of specialized healthcare delivery organizations. In the United Kingdom, specialty hospitals have been encouraged by the National Health Service (NHS) for the potential gains they offer in terms of efficiency and quality. 6

In the United States, in addition to the proliferation of specialty hospitals, 3 ASCs’ growth might be the fastest among new specialized healthcare delivery organizations. In 2005, there were 4445 ASCs in the United States, 7 while there were only 400 in 1983 and 3300 in 2001. 8 ASCs capitalized on the shift away from inpatient towards outpatient procedures. They perform surgical procedures for which an overnight hospital stay is not required and could be multi-specialty centers or single specialty, with ophthalmologic, gastroenterologic, and orthopedic centers being the most dominant types. 9

Competition and market entry of healthcare delivery organizations are important for policymakers as well as managers worldwide. As governments continuously seek to shape their healthcare markets in ways that encourage efficiency and improve quality, it is imminent to understand the driving forces that impact market entry rates of new organizational forms, specifically specialized healthcare delivery organizations or “focused factories.” Research from other industries indicates that mature organizational populations such as general hospitals behave differently from growing organizational populations such as specialty hospital and ASCs. Moreover, theory from other sectors suggests that entry decisions of growing populations are influenced by different if not opposing forces from market entry decisions of mature populations such as hospitals. 10 One of these key forces that are worth studying given its policy implications is competition. The majority of research in healthcare treats competition as attribute of a defined market. However, organizations within the same market are faced by different levels of competition based on the level of overlap in the services they provide. 11 In this paper, we rely on the niche overlap theory perspective to investigate the impact of relational competition on the market entry of hospitals and ASCs. We also provide a framework to differentiate between market entry into growing or emerging organizational populations and mature populations in healthcare delivery markets. Specifically, we rely on r- and K-selection processes to investigate the market entry into the growing population of ASCs and the mature population of hospitals. We use patient-level datasets from the state of Florida to evaluate the impact of niche density on ASCs and hospital entry rates.

Theoretical framework

Research on the determinants of market entry of healthcare organizations is not abundant. In general theories explaining market entry rates in healthcare can be grouped under two general categories: (1) health economics and (2) organizational ecology. 12 The health economics perspective focuses on forces of supply and demand and market competition. 13 However, the organization ecology perspective focuses on populations of organizations that occupy different niches and the factors that influence the market entry and exit of different organizational populations. 12 In this paper, we incorporate both the health economics perspective by controlling for forces of supply and demand and the organizational ecology by examining two organizational populations: ASCs and general hospitals. Our theoretical framework relies on niche overlap theory and extends the literature on market entry by incorporating the r- and K-selection processes. The main contribution of our model is that it provides a framework to study market entry by integrating competition between organizations with the same form and competition between organizations with different forms, i.e., generalist and specialists. Moreover, our model provides a theoretical framework that distinguishes between entry into mature markets such as hospitals versus entry into emerging markets such ASCs. Our model provides a comprehensive framework for studying the emergence and rise of new organizational forms and the interaction between emerging organizational forms and incumbent ones. Finally, we do not limit our model to competition but we also incorporate other dynamics such as mutualism.

Niche overlap theory

Traditionally, competition in healthcare markets is treated as an attribute of a defined market whereby all hospitals in the market face the same level of competition. 11 Niche overlap theory, however, provides a relational view of competition where competition is measured by the level of overlap in the resource niches between two hospitals which allows for a more fine-grained conceptualization of competition faced by hospitals. 11 According to the niche overlap theory, every organization in a population occupies an organizational niche characterized by a location in resource space.14,15 Depending on the organizational niches they target, organizations face different competitive landscapes. Organizations that operate in the same organizational niche experience competitive effects since they compete directly for scarce resources. Organizations that occupy non-overlapping organizational niches experience mutualistic effects by, for example, cooperating directly or providing services that create complementary demand. Therefore, the level of competition between two ASCs or two hospitals is proportional to the overlap in the required resources rather than a concentration measure that characterizes all hospitals in their market. 16

Baum and Singh

15

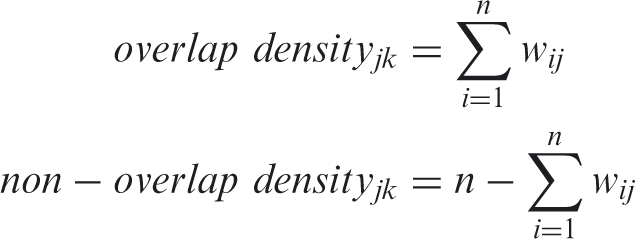

argued that the degree of organizational niche overlap and non-overlap also influences the organizational niches in which entrepreneurs choose to create organizations. They define overlap density as the total number of firms with overlapping niches, i.e., providing the same services or products. Higher overlap density signals to entrepreneurs high level of competition. Organizations targeting niches that are more crowded have a much lower likelihood of being founded than organizations targeting less densely niches. More precisely, the higher the overlap density, the greater is the intensity of competition, and the lower the entry rate. Therefore, consistent with classical economic theory, niche overlap theory suggests that hospitals are less likely to enter into markets where there is a high level of overlap in the services already provided. Hypothesis 1: Overlap density is negatively related to the entry rate of hospitals.

Likewise, they defined niche non-overlap density to be the total number of firms with non-overlapping niches. 15 Non-overlap density captures the number of organizations in the population that do not offer the same services or have the same resource requirement as the focal organization. Baum and Singh argued that non-overlap density has the opposite effect on market entry. Non-overlap density captures information about differentiation of organizational niches. This differentiation leads to complementarities between organizations that occupy different niches and thus create mutualistic interdependencies among them. For example, organizations benefit from the broader social acceptance and greater institutional support posed by non-overlapping firms with the same organizational population. Likewise, there exist opportunities for demand enhancement and other cooperative endeavors among non-overlapping organizations. The confluence of these factors suggests that non-overlap density will have a positive effect on the firm entry rate.

By examining both mutualistic effects and relational competition, niche overlap theory provides a different perspective in treating competition and market entry in the healthcare delivery markets. The niche overlap theory has found support regarding the impact of niche overlap and non-overlap on firm entry and exit rates within a variety of settings including daycare centers and the automobile industry.15,17–19 Yet, while niche overlap found support in the literature, the theory remains limited in its scope since it emphasize micro-niches and had not yet explored the effect of niche overlap and non-overlap between organizational populations occupying different macro-niches—specifically, specialist and generalist organizational forms. Therefore, we draw from existing theory to pose some hypotheses regarding the effects of competition between these two organizational forms at different stages of industry evolution. Specifically, we rely on the r- and K-selection processes and density dependence theories.

R and K-selection and entry strategies

Previous research on market entry of healthcare organizations has ignored differences between more established forms such as hospitals and new organizational forms such as ASCs. Brittain and Freeman

10

point out that organizations frequently pursue different entry strategies, depending on the stage of industry evolution. In order to justify their theory, they draw from models used by biologists to model the growth of populations in finite environments:

Pure r-strategists are organizations that move quickly to exploit resources as they first become available. 10 Their structure makes them relatively inexpensive to set up since they concentrate on activities that require low levels of capital investment and simple structures. Their success depends heavily on first-mover advantages, which makes them high-risk and high payoff organizations that gain maximally from temporarily rich environments. K-strategists, on the other hand, are organizations that are structured to compete successfully in densely settled environments. 10 K-strategist organizations generally expand more slowly into new resource spaces than r-strategists because the structures generating competitive efficiency frequently preclude the rapid adjustments necessary to capture first-mover advantages. Competition on the basis of efficiency generally involves higher levels of investment in plant and equipment and more elaborate organizational structures.

In industries with changing products, developing technologies, or rapidly increasing market munificence, competition is dominated by r-selection which favors emerging organizations capable of moving quickly to exploit new resource opportunities in the resource rich but uncertain environments that characterize low-density conditions. As the emerging population continues to grow, its markets become connected and environmental uncertainty is reduced as demand becomes more predictable. As an industry stabilizes and the organizational population reaches its carrying capacity, the resources available to its members are exploited fully and competitive pressures shift to K-selection, which favors organizations competing on the basis of efficiency.

Therefore, the r- and K-selection processes may produce different patterns of firm entry into organizational niches. In the case of mature populations, such as general hospitals, characterized by K-selection processes, organizations compete on the basis of efficiency

10

and these competitive pressures increase within markets that are more crowded. Thus, general hospital should avoid direct competition with other firms and favor uncrowded niches. Yet this differs within a growing population of a new organizational form such as ASCs. The theory suggests that r-selectionists like ASCs will compete on the basis of market positioning and will seek out the most profitable markets regardless of whether they are relatively crowded or not. Thus, surgery centers will enter markets in which there is high niche overlap density. Surgery centers represent an excellent example of a growing organizational population since the rapid increase in the number of facilities indicates that it is characterized by r-selection processes. Meanwhile, the hospital sector has existed for centuries and the fact that the number of U.S. hospitals is declining would suggest that the organizational population is relatively mature and characterized by K-selection processes. Hypothesis 2: Overlap density is positively related to the entry rate of ASCs.

Methods

We chose the state of Florida as our study site for several reasons. First, it is the state with the second highest number of ASCs in the United States. In fact, the number of surgery centers in Florida grew from just 110 in 1993 to 379 in 2006, so it closely mirrors the trends in ASC growth being observed throughout the country. More importantly, the state of Florida requires that healthcare facilities report data on all inpatient and outpatient surgical procedures that they perform. Patient data reported by Florida healthcare facilities is compiled by the Agency for healthcare administration (AHCA) and represents a complete census of all inpatient and outpatient surgeries that have occurred within the state from 1997 to 2006. For the inpatient data, surgical procedures are represented by ICD-9-CM/ICD-10-CM procedure codes. Within the outpatient data, surgical procedures are represented by CPT/HCPCS procedure codes. In order to transform these patient datasets into quarterly procedure counts, we coded these procedures and categorized them within surgical specialties. Clinical classification software (CCS) from the Healthcare utilization project (HCUP) allowed us to classify both ICD-9-CM/ICD-10-CM and CPT/HCPCS codes among 244 different procedure types. Cross-tabulating these procedures types with facility IDs and patient county codes produced two panel datasets in which the unit of observation is the facility-quarter and county-quarter while each column represents that facility and county’s procedure count within each of the 15 surgical specialties, respectively. We modeled facility entry as a function of each specialty’s characteristics within each county. We subsequently converted these datasets from wide to long datasets so that the each unit of observation was the facility-specialty-quarter and county-specialty-quarter. Our dependent and independent variables were calculated from these two datasets.

Conveniently, the state of Florida maintains data on the location of all surgery centers and general hospitals, which allows us to assign them to their county of residence. Each of these 67 counties was subsequently assigned to one of 17 health service areas (HSAs) based upon the market boundaries established by the National Center for Health Statistics. 21 We defined these HSAs to be their own markets for the purposes of this study, and all explanatory variables were initially measured at the HSA level. Although HSAs provide a convenient starting point from which to define markets, they span very large geographic areas. Therefore, we elaborated upon them in order to distinguish between local and diffuse market conditions since travel distances clearly play a role in the market for outpatient services.21,22 We calculated our local measures from the county within which each surgery center resides and our diffuse measures from all other counties within that surgery center’s HSA. Our explanatory variables were also divided and calculated separately in the same manner.

Dependent variables

We began our analysis with the dataset of quarterly procedure counts that we had tabulated by facility ID codes in which the unit of observation is the facility-quarter. Facilities enter this panel dataset as they enter the market for outpatient services and so this panel provided us a starting point from which to observe facility entry. The state of Florida also maintains information on all licensed and accredited outpatient facilities in the state. This dataset extends back to the early-1990s and provides the date(s) of opening for all such entities. This licensure dataset was merged with our outpatient procedure dataset through AHCA ID numbers in order to validate the patterns of activity produced by our panel dataset with the state’s official entry. From these datasets, we identified a total of 193 entries among 406 ASCs and 10 entries among 222 hospitals from 1997 to 2006, which represent fairly reasonable sample sizes when multiplied by the number of specialties that each of these facilities enter over 40 quarters.

We assessed the causes of facility entry not simply into counties but rather into each specialty within those counties as a function of those county-specialty characteristics. The county-specialty is the unit of observation for the dependent variable in our empirical models while our independent variables were initially measured at the HSA level and were subsequently broken down by facility type (ASC vs. hospital) and geographic location (local vs. diffuse). In order to assess whether dependent and independent variables should be calculated from the same geographic area, we ran separate analyses with all variables measured at the county and HSA level to check the robustness of our results.

Independent variables

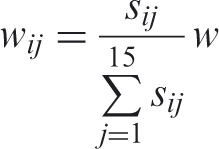

In order to calculate competition at the county-specialty level, we divided each facility up by the proportion of its total procedure volume that it devoted to each surgical specialty. Following the example of Baum and Singh,

15

we constructed niche overlap weights from the proportion of each facility’s procedure volume that was devoted to specialty j:

We also included a variety of control variables at the county and county-specialty level. For county-specialty controls, we included payer mix participation in order to account for the possibility that certain specialties are reimbursed more generously and therefore are more appealing. Although the Florida outpatient dataset utilizes 16 different payer codes, we collapsed these codes into three categories: public, private, and other. We included variables representing the proportion of a facility’s business that is reimbursed by public and private payers while omitting the variable representing other payers as a comparison group. We broke these variables down in order to observe whether they were dependent upon geographic location (local vs. diffuse).

Summary statistics.

Empirical model

Our empirical models estimate the probability of facility entry as a function of market characteristics which include overlap density, non-overlap density, demand size, and market control variables. We modeled our dependent variable, the quarterly number of entries within a county-specialty in quarter t, as a function of our independent variables in quarter t–1.

We utilized negative binomial regression to estimate our model but we also validated the robustness of our results by running a Poisson regression model as well. One of the assumptions of the negative binomial model is that all the observations be independent. However, we know that facility entries within a county-specialty may not be independent since multi-specialty facilities enter more than one specialty at a given point in time. So we clustered our standard errors by county in order to allow for intragroup correlation, which relaxed the requirement that the observations be independent. We also included year and quarter dummy variables in order to control for any time trends present in the data.

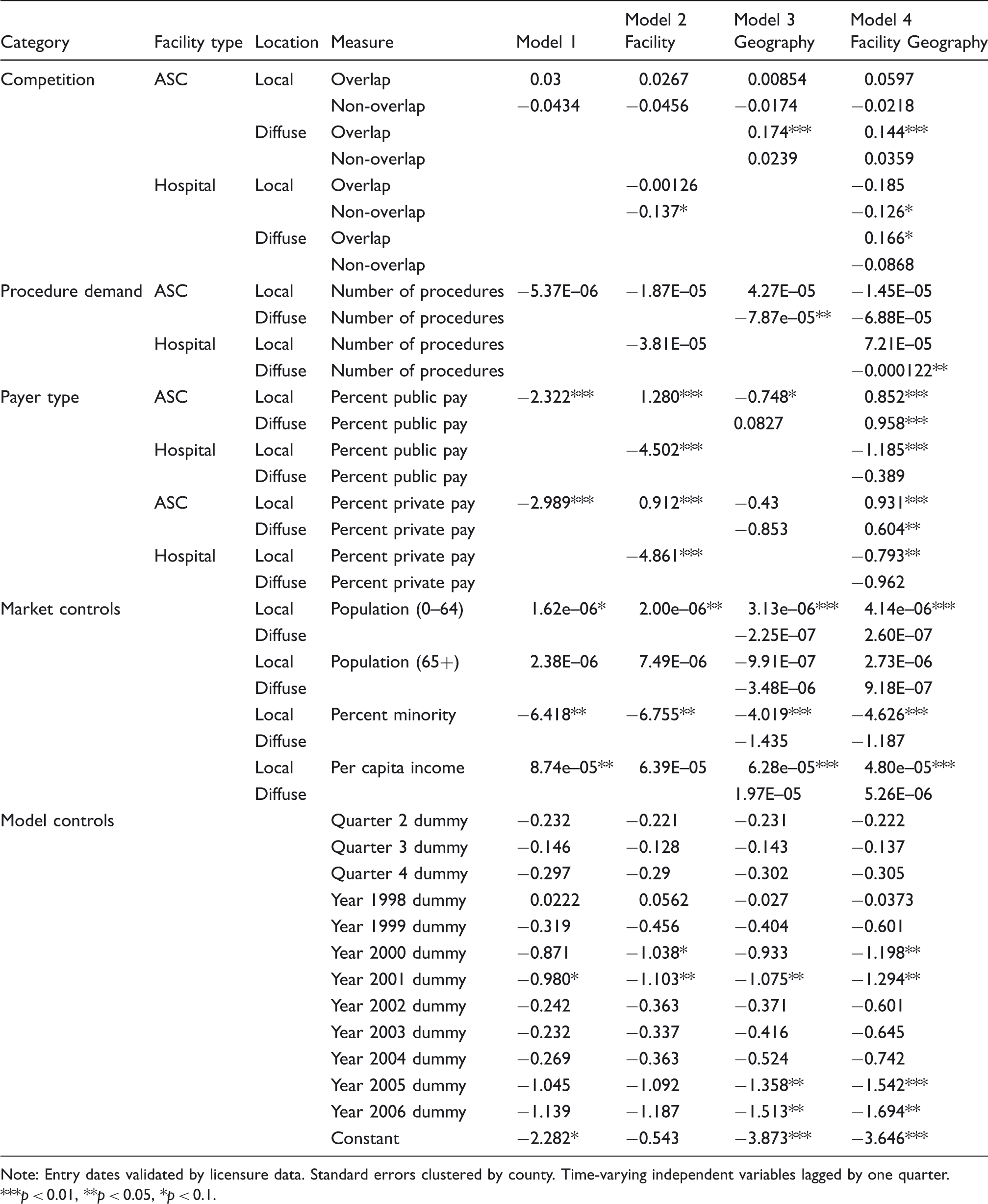

Surgery center entry—negative binomial model.

Note: Entry dates validated by licensure data. Standard errors clustered by county. Time-varying independent variables lagged by one quarter.

p < 0.01, **p < 0.05, *p < 0.1.

Hospital entry—negative binomial model.

Note: Entry dates validated by licensure data. Standard errors clustered by county. Model excludes observations from 1997. Time-varying independent variables lagged by one quarter.

p < 0.01, **p < 0.05, *p < 0.1.

Results

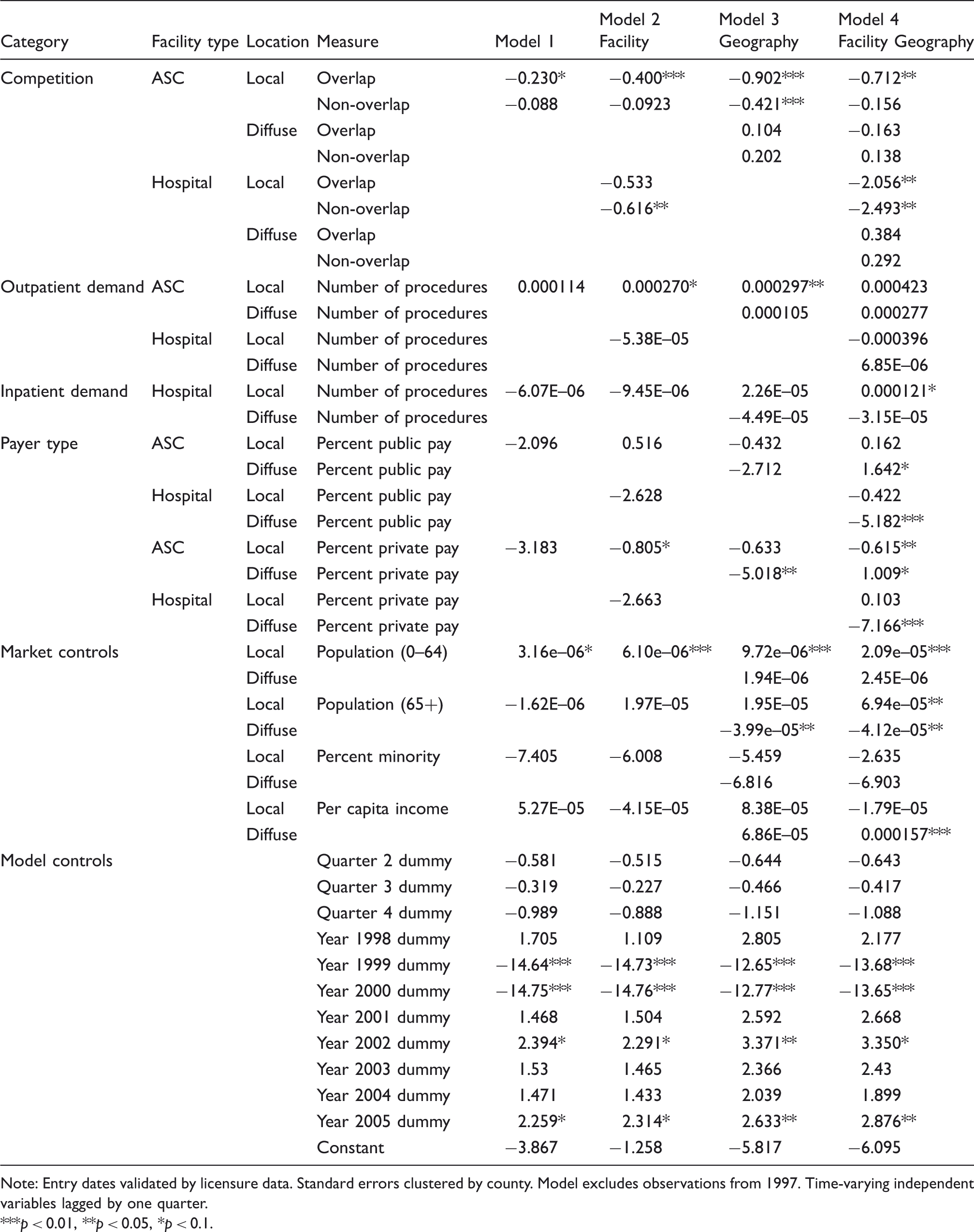

Our negative binomial models yielded log likelihood statistics that were highly significant (p < 0.0001). Our models generally produced coefficients with the expected signs, but we ran Poisson models to check the robustness of our results and found that none were substantively different. Higher levels of market demand for outpatient procedures are associated with a higher probability of ASC entry (Models 1 to 4, p < 0.05), while hospital entry is only positively associated with outpatient demand from ASCs (Model 4, p < 0.05) and inpatient demand (Model 2, p < 0.05).

In terms of market control variables, ASC entry rates were significantly higher when ASCs are reimbursed predominantly by public and private payers (Models 2 and 4, p < 0.05) and when hospitals are reimbursed predominantly by other payers (Models 2 and 4, p < 0.05). Hospital entry rates were significantly higher when diffuse facilities and diffuse hospitals receive a low proportion of reimbursements from private payers (Models 3 and 4, p < 0.01). As expected, both ASC and hospital entry rates had a positive relationship with the size of the population age 0–64 (Models 2 to 4, p < 0.05), but hospital entry rates had a negative relationship with the diffuse size of the population age 65+ (Model 3, p < 0.05). Across the board, ASCs tended to enter markets in which there were a relatively low proportion of minority residents (Models 1 to 4, p < 0.05). Per capita income also had the expected positive relationship with facility entry rates, although ASC entries were affected more strongly by local per capita income (Models 3 and 4, p < 0.01) while hospital entries were affected more strongly by diffuse income levels (Models 3 and 4, p < 0.05).

Regarding our hypotheses, we find strong support for hypothesis 1, which suggests that hospitals entry rates are negatively related to niche overlap density among outpatient facilities (Model 3, p < 0.01), which includes ASCs and hospitals (Model 4, p < 0.05). Our finding on the effect of overlap density on entry patterns within a mature organizational population of hospitals was as predicted.

We also find support for hypothesis 2 as our results indicate that surgery center entry rates are highest in markets with high niche overlap density among local and diffuse outpatient facilities (Models 1 and 3, p < 0.05) and particularly among surgery centers (Model 4, p < 0.05). However, surgery center entry rates do not appear to be influenced by hospitals overlap density. Taken together, these results provide support for the idea that firms within a growing organizational population tend to seek out crowded niches. This is the exact opposite phenomenon of what we observed from hospitals.

Discussion

The confluence of results from our models suggest that entry patterns do differ significantly within the mature population of hospitals and the growing population of ASCs. Hospitals tend to avoid direct competition with surgery centers and other hospitals by not entering markets with higher number of ASCs and hospitals with overlapping niches. Meanwhile, surgery centers appear to seek out markets in which there are surgery centers with overlapping niches. In simple words, at this stage of their evolution, ASCs are not hindered by the level of competition in the markets they plan to enter. While in the hospital population, competitive pressures discourages hospitals from entering markets with higher level of competition. Our findings also indicate that ASCs have higher entry rates in markets with higher demand, per capita income, and publicly and privately insured individuals, and lower proportion of minority groups. This is not surprising since the majority of ASCs are for-profits and entrepreneurs might view these markets as highly favorable.

Hospitals play a critical role in any healthcare system both in terms of the services they provide and also in terms of the workforce they employ. Previous research indicates that hospital exit rates are higher in markets characterized by competition from ambulatory surgery centers. 2 Our findings indicate that entry rate of hospitals into such markets is lower. Therefore, based on our findings on exit and entry rates, healthcare systems worldwide that are considering or already encouraged a more competitive healthcare delivery landscape should consider the impact market entry of specialized healthcare delivery organizations have on the existing hospital population. Moreover, these specialized healthcare organizations are targeting traditionally profitable service lines such as surgery and orthopedics. 23 For instance, previous research indicates that there is a relationship between the market entry of specialty hospitals and the operating margins of the procedures they specialize in. 24 Therefore, there are concerns that as these population grow, general hospitals’ ability to cross-subsidize less profitable service lines such as psychiatric services might diminish. Finally hospitals since their emergence have played a key role in their local communities. Their closure and redistribution would pose concerns in terms of patient access and continuity of care.

It is valuable to note that ASCs, and even specialty hospitals, represent just the tip of the iceberg as there has been similar growth among other specialized providers dedicated to gastrointestinal endoscopy, diagnostic imaging, sleep disorders, peripheral vascular disease, cosmetic surgery, radiation therapy, lithotripsy, cardiac catheterization, and cancer chemotherapy. 25 These facilities may have a competitive advantage when competing with general hospitals as a result of their leaner organizational form. While the changing landscape of healthcare delivery organizations might have substantial impact on general hospitals, many on the other hand argue that specialization leads to performance improvement and better patient outcomes. Christensen et al. 26 argue that focused healthcare organizations such specialty hospitals, ASCs, eye centers, and other specialized organizations are value adding process businesses that are capable of delivering comparable level of quality, if not better, at lower prices. This is supported by empirical research which found an association between better outcomes and specialization in healthcare delivery organizations.27,28 Moreover, in a comparative study in the United Kingdom, specialized treatment centers were found to be more efficient as evident in their shorter length of stay. 29

Our findings have implications from a strategy perspective. Given that these specialty organizations compete with hospitals directly on their most profitable service lines, 30 hospitals should be aware that the market entry of specialized healthcare organizations will encourage more focused organizations to enter their market, even as the market gets crowded. Hospitals in more profitable markets with lower proportion of minority residents, higher size of age 0–64 population, and higher per capita income, need to especially be aware of this phenomenon. While this seems to indicate potential undesired competition for hospitals from specialized organizations, incumbent hospitals that are already in crowded markets need not fear the entry of other general hospitals since that event is unlikely. Thus, hospitals can focus their efforts on strengthening their position and competitiveness in the market against current competitors by improving their efficiency and quality.

In conclusion, in this paper, we provide a conceptual framework that can be applied to study the market entry in health services research that extends beyond surgery centers into other specialized providers that have caused a variety of services to migrate away from the general hospitals. It is important to note though that eventually the rapid growth exhibited by surgery centers should slow as the industry experiences a shakeout and ultimately reaches maturity. During this time, the r-selection processes we have examined will give way to K-selection processes. Given 10 more years of data and further industry evolution, it would be fascinating to study firm entry and exit patterns during this transitional period since we only examine them at opposite ends of the spectrum.