Abstract

Nearly all modern public pension programs involve a substantial transfer of wealth from workers to retirees. If parents love their children, why are these intergenerational transfers politically sustainable? This paper develops a cross-national overlapping generations model to explore the impact of income mobility on the way workers and retirees calculate the long-term value of these programs to their children. Mobility affects their evaluations because these programs also redistribute intragenerationally. The analysis shows why a majority of rational voters who care about their descendants can insist on the preservation of current public pension benefits for themselves but accept a future reduction. Implications of this explanation are tested using comparative intergenerational mobility data and a 2001 Eurobarometer survey on pensions.

1. Introduction

Public pension programs in modern democratic societies redistribute income in two ways. One, they redistribute from higher wage to lower wage workers. This intragenerational redistribution is not surprising since in all these societies a majority of voters have below-average incomes. Two, public pension programs redistribute from workers to the elderly. This intergenerational redistribution is more surprising since in these societies the median voter is below the normal retirement age. There is a huge literature examining how a generic majority interest in redistribution is affected by labor unions, global competition, electoral institutions, social values, and cross-cutting cleavages. But the distortion of the majority’s will is not the issue here. Public pension programs remain both politically strong and popular.

An obvious explanation for the political sustainability of intergenerational transfers is that workers anticipate benefitting from the same lopsided arrangement when they retire. Yet given the typical program’s benefit structure, pay-as-you-go (PAYG) financing, and the demographic trends found in all advanced democracies, this intergenerational redistribution is for all practical purposes irrevocable (Gokhale, 2007; Mulligan and Sala-i-Martin, 1999a). The life-cycle will not redeem the workers’ sacrifice.

To many observers, therefore, the best explanation for this transfer lies with the disproportionate political capacity of the elderly to raid the coffers of their descendants (e.g. Grossman and Helpman, 1998; Mulligan and Sala-i-Martin, 2004; Pampel and Williamson, 1989; Thomson, 1993; Wilensky, 1975). Since conflict is endemic to politics, this explanation has a natural appeal.

If parents are generally altruistic toward their children, however, the puzzle of intergenerational transfers cannot be dispatched so easily. Indeed if parents are altruistic, the very fact that the basic financial structure of public pension programs is consistent with a model of intergenerational political conflict is puzzling. In essence, the pattern of apparently selfish behavior exhibited by ostensibly altruistic parents constitutes the central puzzle addressed in this paper.

I will assume that parents are altruistic toward their children. Yet their willingness to support current programs and thereby accept irrevocable transfers from their progeny is rooted in rational expectations about what their children’s economic situation will be when expected financial challenges to these programs materialize and when the debt associated with the current financial structure comes due. With no lack of moral consistency, one generation may politically support a program for itself that must be scaled back for its children.

Specifically, I develop an overlapping generations model involving three generations: children, their working parents, and retirees. The latter two vote on a uniform income tax determining the next period’s level of spending on a public pension program, which is funded on a PAYG basis. In this model, anchored in work by Tabellini (2000) and Bénabou and Ok (2001), parental altruism rules out pure exploitation. What confounds the ordinary impact of altruism, however, is not only naked self-interest but parents’ expectations about the future value of the income-producing endowments their children inherit. Given empirically reasonable parameter estimates about income distributions and the evolution of these endowments, the model implies that a majority of voters can rationally expect their children and grandchildren to have above-average incomes. These parent-voters will then provide less support for the long-term intragenerational redistribution characterizing, to varying degrees, all the public pension programs the paper will examine.

In short, those voters currently benefitting from a public pension program’s progressivity may accept its future retrenchment precisely because they believe their descendants are more likely to be hurt by the program’s redistributive character. By the same logic, redistributive public pension programs maintain support from altruistic poorer voters whose children will pay relatively less for the benefits their retired parents will enjoy (see Fuster, 1999). 1

The model identifies specific forces affecting the time-varying support for public pension programs. These forces are embodied in two empirical hypotheses. One, the higher individuals’ incomes are, the less likely they are to support intragenerational redistribution through public pension programs. Yet, two, the greater the degree of income mobility in a country, the less likely are its citizens with below-mean income to support such redistribution. Public pensions programs are governed by a political version of the Lake Wobegon effect: a majority of voters rationally expect that their children will be above average.

Although the income and mobility hypotheses are relatively straightforward, complications emerge when they are tested in a cross-country setting. Despite the structural parallels already noted, public pension programs vary in many respects, and the institutional contexts in which democratic voters make choices about welfare spending vary enormously as well. The need for comparable data on intergenerational mobility suggests looking to Europe to examine the political basis of the typical public pension program. I test the preceding hypotheses using a 2001 Eurobarometer survey on pensions (Christensen, 2006). Consistent with the model, the subsample is limited to democratic countries for which comparable income mobility data are available, although with suitable modification the model applies to any regime sensitive to popular opinion.

Political scientists have shown little inclination to examine the assumption that narrow self-interest determines individual political support for public pension programs (Lynch and Myrskylä, 2009). Instead they often rely on potentially misleading inferences drawn from generational accounting exercises. But in light of the major budget and welfare implications of public pensions and other social insurance programs targeted at the elderly, a simple appeal to cui bono arguments should not be allowed to substitute for an explicit consideration of the politics sustaining these programs. The comparative analysis undertaken here not only documents the empirical role of mobility in sustaining the PAYG approach to financing public pensions. It also provides support for the underlying model of parental altruism rationalizing this role.

2. The politics of intergenerational transfers

Why do politically popular public pension programs typically entail net permanent losses for younger relative to older generations? This section inventories leading explanations in the literature.

One explanation appeals to the bounded rationality of older voters. According to this view, their contradictory and uninformed beliefs, often dependent on elites, compartmentalize their concern for their children and their concern for their own pocketbooks (e.g. Kotlikoff and Burns, 2004; Lynch, 2006; Retirement Confidence Survey, 2006).

While this kind of open-ended explanation is difficult to refute—contradictory beliefs can explain anything—the size of the current tax burden for most workers should make it hard for the public to ignore the economic ramifications of these programs (Tabellini, 2000). Evidence from the US suggests that the public, and the elderly in particular, are relatively well informed about Social Security (e.g. Campbell, 2003; Jacobs and Shapiro, 1998). A large majority of German and Italian respondents are aware that their generous PAYG systems are unsustainable, although a majority do not fully understand the mechanics (Boeri et al., 2002). In any case, we will see that individuals behave as if they were rationally influenced by the relation of their personal income to the mean and by differences in income mobility.

It has been argued that financial rebalancing has been blocked by policy and institutional path dependence (Campbell, 2003; Lynch, 2006; Pierson, 1993). But in this context, the appeal to path dependence seems to have limited explanatory bite. For one thing, in each of the countries studied here, the initial programs were explicitly designed, so we have to explain the original financial inequity. Moreover, these programs have been redesigned multiple times over the years, in each case reproducing and typically increasing the intergenerational transfer and muddying the contrast between different welfare regimes (e.g. Arza, 2008; Arza and Kohli, 2008; Galasso, 2006; McHale, 2001).

Institutional context and previous welfare policy choices affect the feasible alternatives and electoral incentives of politicians, but the voters ultimately decided to maintain these institutionalized transfers and respond to the financial bait offered by politicians. As Andreß and Heien (2001) argue, furthermore, self-interest plays an important role in determining attitudes within different institutional contexts.

Path dependence, in short, is another way to describe the political puzzle: why retirees are seemingly complicit in the use of elections and political pressure against the interests of their own descendants. More than the relative generosity of these programs, the crucial question is why those programs are structured as intergenerational transfers, often in the form of unfunded liabilities that do not appear in official expenditure statistics.

As noted in the introduction, another popular approach dissolves this puzzle by denying the assumption of parental altruism. True, widespread and manifest examples of parental altruism suggest that parents would take into consideration the interests of their children when voting on pension programs. On the other hand, to proponents of the political conflict model, the actual structure of these programs says otherwise. Conventional wisdom about altruism notwithstanding, the size and persistence of the intergenerational transfer indicate that, in practice, the elderly have triumphed in distributional conflicts between the generations. According to Mulligan and Sala-i-Martin’s (1999b) ‘gerontocracy’ model, for example, the elderly have succeeded because their lower productivity translates into lower opportunity costs of leisure activity, which can be directed toward lobbying and voting. As a result, organizations of the elderly enjoy a competitive advantage when promoting public pension programs. This advantage is reinforced by retirement incentives built into those very same programs.

Nevertheless, despite their many strengths, the gerontocracy model and related political conflict models are incomplete. There is little evidence of systematic age differences in attitudes toward public pensions, and what differences exist often do not fit the selfish elderly hypothesis (e.g. Boeri et al., 2002; Furati and O’Donoghue, 2009; Goerres, 2009; Van Groezen et al., 2009; Hamil-Luker, 2001; Kohli, 2008; Lynch and Myrskylä, 2009; Wilensky, 1990; see also Busemeyer et al., 2009; Cattaneo and Wolter, 2009; Gallup Organisation, 2009). Nor is there strong evidence for disproportionate influence of elderly citizens on the generosity of public pensions (e.g. Tepe and Vanhuysse, 2009).

Of course talk is cheap and empirical evaluations of parents’ actual financial altruism toward their children are mixed (Laferrère and Wolff, 2006). However, some of the leading negative findings regarding so-called pure altruism by parents (e.g. Altonji et al., 1997) are invalid when the child’s future income is uncertain (McGarry, 2000), as it is assumed to be here. Villanueva (2002) similarly finds empirical support for the altruism assumption when there is parental uncertainty about children’s wage opportunities and effort.

The breadth of political support for public pension programs challenges the intergenerational conflict model, not necessarily the self-interest assumption itself. In an attempt to show the compatibility of this assumption with majority support for these programs, Bohn (2005) develops a noncooperative game theoretic model in which voters of median age or higher will support the tax increases needed to sustain their PAYG financial structure (see also Cooley and Soares, 1999; Galasso, 2006). To reach this formal result, Bohn assumes that voters treat their previous contributions as sunk costs when calculating the program’s future net benefits. Even though the median voter is below retirement age, her support for the current program is motivated each period by ‘trigger strategies’ entailing the program’s destruction if any cohort of retirees fails to receive the appropriate benefit.

Bohn’s analysis is designed to demonstrate how an implicit intergenerational compact can be sustained in the absence of altruism. ‘Altruism is almost too powerful to be interesting: social security is obviously viable if the young are eager to make transfers to the old’ (Bohn, 2005: 49). The key problem with his preferred explanation is that the old may be altruistic as well. 2 Voters rationally ignore their own sunk costs at each decision point, but the empirical puzzle is why voters also ignore the new ‘sunk costs’ they impose on their descendants. The imposition of these costs seems to contradict the sacrifices that otherwise distinguish typical parental behavior: ‘Parents spend money, time, and effort on children through child care, expenditures on education and health, gifts, and bequests’ (Becker and Murphy, 1988: 3).

Becker and Murphy attempt to resolve this contradiction by arguing that pension benefits and similar transfers reflect a different kind of implicit political contract: negative bequests by parents help offset their earlier sacrifices, principally productivity-enhancing investments in public education that redound to their children’s benefit (see also Boldrin and Montes, 2005). One problem with this explanation is that, according to the scholarly consensus, the elderly have received excessive returns from their investment (e.g. Mulligan and Sala-i-Martin, 1999c). Further, even if Becker and Murphy’s money’s worth calculations were correct at one time along with their assumption of a net reproduction rate of unity for the population (1988), decreasing mortality rates among those 65 and older have changed the age-composition of the population (see, e.g., Preston et al., 2001) and progressively increased the financial burden on workers.

Kohli (1999) extends the notion of an implicit contract by noting that within the extended family, labor taxes that support public pensions can be exchanged for child care and similar services provided by grandparents (see also Williamson and Watts-Roy, 1999). But why is the implicit contract only partially internalized? After all, in the absence of public pensions, workers could redirect their generally considerable tax contributions to their own parents in exchange for nonmonetary services. The answer seems obvious: complete internalization precludes the redistribution produced by the public scheme of risk pooling.

In sum, the scale of the intergenerational redistribution projected for most public pension programs outstrips any plausible effect of either grandparents’ nonmonetary services or long-term economic growth on children’s well-being. Insofar as this redistribution seems to challenge a simplistic vision of parental altruism (see Becker and Murphy, 1988), conflict models are not entirely without merit. By the same token, for the reasons Becker and Murphy list, models recognizing altruism cannot be replaced tout court by models based on intergenerational conflict. We are back to the original question: why have altruistic parents not intervened in the face of massive transfers? Their failure to do so presents a political puzzle.

Of course, none of this is meant to suggest that only relative income, the insurance motive, and mobility determine support for redistributive public pension programs. Iversen and Soskice (2006), for example, argue that electoral systems also affect the amount of redistribution. But since their analysis, like many others, assumes fixed income class assignments, it may miss trends in mobility that influence the lower class’s redistributive preferences.

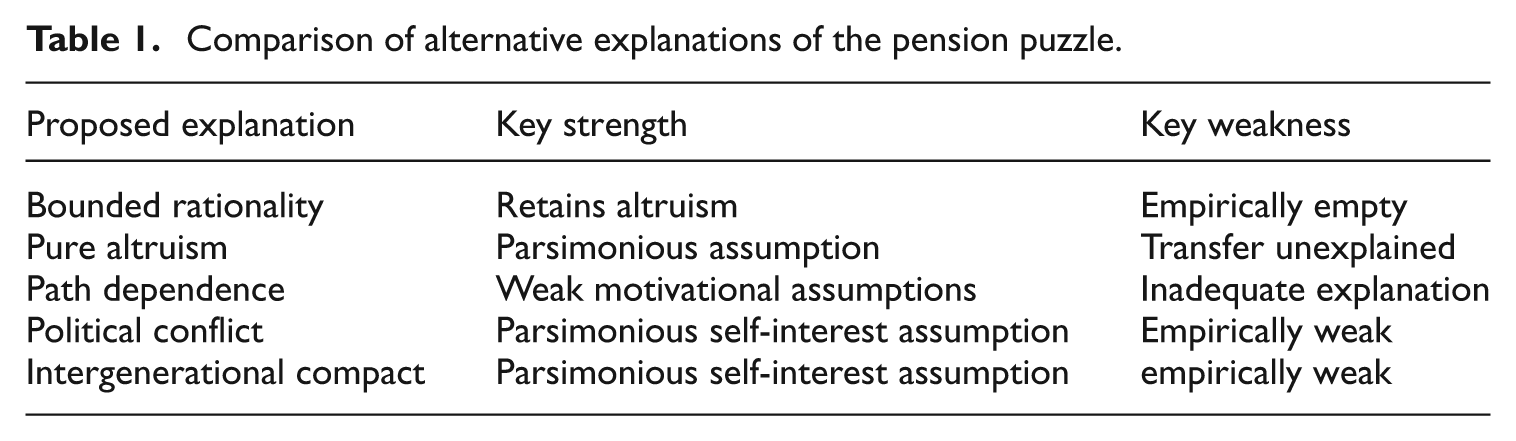

Table 1 summarizes, without nuance, the preceding discussion of current approaches to the pension puzzle:

Comparison of alternative explanations of the pension puzzle.

The next section develops an explanation for the coexistence of intergenerational transfers and parental altruism.

3. Income mobility and redistribution

In country after country, public pension programs are characterized by substantial intergenerational transfers. Due to demographic trends and the limits of economic growth, these transfers cannot be duplicated for subsequent beneficiaries. Compounding this problem, PAYG financing also makes each subsequent generation pay for the windfall experienced by the first generation of retirees. All of this demands an explanation. Of course, the existence of public pension programs per se is not particularly puzzling. Risk-averse individuals planning ahead to retirement will want to insure themselves against bad wage histories and uncertainty about individual longevity. But these concerns lead to intracohort redistribution. The puzzle is the degree of redistribution across generations.

An important building block of my explanation for the political dynamics of public pension programs is a modified version of Bénabou and Ok’s (2001) Prospect of Upward Mobility (POUM) model of voting on redistribution. Bénabou and Ok posit a fairly standard income mobility process in which expected future income is a positive function of current income but increases at a decreasing rate, a process akin to regression to the mean. Given this and a few more technical assumptions, they show, somewhat paradoxically, that a majority of voters may oppose future redistribution because they rationally expect to have above-average incomes. Their result can be extended to the case of intergenerational social insurance: voters who currently benefit from the progressivity of a public pension program may be willing to accept its subsequent restriction because they expect their descendants to be hurt by the program’s redistributive character.

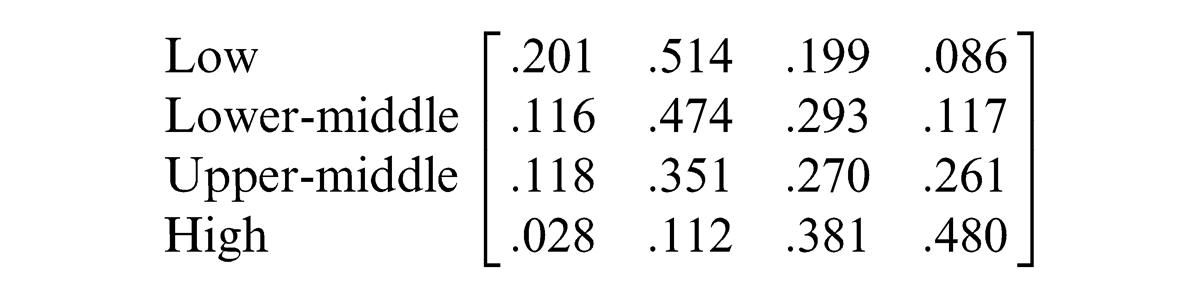

A simple application to Italian income data and the associated income mobility process will help illustrate how the voters’ calculations might work in practice. Based on 1977–2002 data, Piraino (2006) summarizes Italian income mobility using a four-class income transition matrix:

where, reading from the top down, the first column of the matrix defines the respective probabilities that sons of low, lower-middle, upper-middle, and high income fathers will enter the lowest class next period, the second column defines the transition probabilities to the lower-middle class, the third column defines the transition probabilities to the upper-middle class, and the fourth column defines the transition probabilities to the high income class. 3 Notice that the sons of fathers in the lowest class have only a small chance of entering the next generation’s upper class directly, while the sons of fathers in the highest class face a negligible risk of entering the lowest class directly.

In 2002, mean Italian income was €14,631, and the first three income classes were capped respectively at €8477, €12,810 (i.e. median income), and €19,215; the maximum income in the sample was €245,388 (income data are from Clementi et al., 2010). Clearly a majority of the population had below-average incomes and would have rationally supported contemporaneous redistribution.

Since some fraction of the upper-middle class had above-average income, the crucial swing group for the POUM effect is the lower-middle class. Let us make it difficult for them to expect an above-mean income for their children by setting their initial income equal to that of the lowest class’s cap (i.e. the lower-middle floor) and the income of the high class to its floor, the income cap of the upper-middle class. With these restrictions, the expected income for the sons of lower-middle fathers was €18,749. 4 In other words, in 2002 a majority of the Italian population would have rationally expected their children to have above-average incomes. If their calculations were risk neutral, they would have rejected a future policy of redistributive taxation, say to finance a public pension program.

Of course, the typical voter is risk averse and a public pension program represents an important form of insurance. Consider, then, the situation of a voter who is considering laissez-faire versus complete redistribution, which insures her descendants against any idiosyncratic income risk. Assume she has the standard utility function

where y t is her income at time t and γ measures her degree of relative risk aversion or, more intuitively, the concavity of the function. 5 This utility function has several attractive properties. One, it increases with income. Two, since it describes someone who prefers to insure against risk, by construction it works against a POUM explanation of why parents reduce their children’s social insurance. Three, the attitude toward risk implied by this utility function scales in the sense that risk-related behavior is the same over different levels of income (see Raskin and Cochran, 1986).

For the Italian data, after assigning just €20,000 to the high income class the maximum risk aversion parameter consistent with majority opposition to redistribution is 1.7, which is within standard estimates. More realistic estimates for the high income class increase this parameter ceiling.

4. Intergenerational altruism and support for public pension programs

The preceding section illustrated the hypothetical impact of the POUM process for the Italian case. This section develops a more general political–economic model of a public pension program consistent with two stylized facts: (a) the program is supported by a majority of voters in the short run, yet (b) the benefits it provides may be reduced or eliminated by voters who nonetheless are altruistic toward their children. The model is based on Tabellini (2000), but modified to introduce POUM calculations, including an expansion from two to three overlapping generations (Bengston (2001) and Arrondel and Masson (2006) document the empirical significance of this expansion).

Before diving into the details of the model, it may be worthwhile to outline its basic structure. Parents understand that their children face an uncertain financial future. This future is dictated by a stochastic ‘social mobility’ function mapping the financial situation each child inherits to a wage the child receives as a worker. The child’s time spent as a worker coincides with her parent’s time spent as a retiree. To prepare for retirement, parents can save from their own wage but also can vote to support a public pension for themselves funded contemporaneously by taxes paid by workers, including their own children.

If parents were entirely self-interested, they would not be ambivalent about taxing the succeeding generation of workers. By assumption, however, they are altruistic toward their own children. This element of realism introduces two complications. One, the parent must trade off her children’s well-being, which is diminished by paying taxes, against her own well-being, which is enhanced by receiving tax revenues. Two, since the pension program is redistributive, altruistic parents who expect their children to have above-average wages will be less inclined to support a robust program than those parents who expect their children to have below-average wages. In light of these considerations, the model determines the conditions under which a majority of voters consisting of workers and retirees will support a public pension program imposing intergenerational transfers.

Turning to the model details, in each country j three generations coexist: dependent children, working parents, and retired parents, that is, grandparents. Parents and grandparents vote. Each child has one parent and lives for three periods. 6 The country’s net rate of population growth is nj , so for each parent there are 1+nj children (for the sake of notational simplicity, from here on the country subscript is suppressed unless needed). There is one consumption good jointly consumed by each working parent and her dependent children.

With i indexing these single-parent families, children from generation t inherit productive endowments

The utility of the t − 1 generation working parent in the i th family is described by

where

I only consider this direction of altruism since in industrialized nations there is a strong ‘downward’ asymmetry in transfers, particularly financial transfers (Arrondel and Masson, 2006; Bengston, 2001). The altruism of working parents toward their own retired parents, on the other hand, is irrelevant to the political issue we are considering. As noted below, voters are determining the tax rate imposed on the income of the next generation of workers when current retirees have left the model.

At first sight 0 < α < 1 is a more natural restriction to impose on the typical working parent’s altruism measure. However, the worker’s direct expectation about her children’s future is not the only channel for her altruism. As a retiree she will also have altruistic concerns for the working children supporting her. Specifically, at time t the utility of each t − 2 generation retiree in the i th family is described by

where

The worker’s budget constraint is

where for simplicity the ‘base’ market wage w is assumed to be constant; τt

, 0 ≤ τt

≤ 1, is a proportional income tax dedicated to funding time t public pension benefits; and

The retiree’s budget constraint is

where pt is a lump-sum pension from the government. Because productive endowments are unequally distributed and there is a uniform retirement benefit, the program is redistributive. The government budget is balanced each period, so, with mean endowment 0, pt = τt (1+n)w.

The impact of children’s endowments on their individual earning capacity as workers cannot be fully predicted a period earlier, an assumption reflecting the financial uncertainties voters typically confront (cf. Ichino et al., 2011). In particular, childhood endowments are governed by a concave stochastic transition function f:

where

To keep the model tractable, I follow standard practice by assuming that workers and retirees vote directly on the tax. Since the annual pension budget is in balance, a vote on taxes is indirectly a vote on the size of the pension benefit itself. In particular, votes in period t determine the period t+1 tax burden of workers’ children and the benefits these workers receive when they retire. The delay in implementation reflects the common understanding that significant changes in public pension programs are phased in to allow sufficient time for workers to adjust their retirement plans (Natali and Rhodes, 2008), which Galasso (2006) interprets as a divide-and-conquer strategy across age groups. 10

The delay built into the model, however, need not be interpreted literally. Even if promised benefits are held constant, the typical changes in public pension programs that have been proposed or have already taken effect increase current public pension taxes and the eligibility age (for Europe, see http://ssa.gov/policy/docs/progdesc/ssptw/2010-2011/europe/ssptw10europe.pdf). These changes are not primarily directed at current beneficiaries but constitute reductions in the net lifetime value of the public pension for current tax payers. Therefore these program reductions are only fully realized over their lifetime (the behavioral implications of a decision on current taxes are discussed in Appendix A).

By focusing on taxation, the choice faced by voters reduces to one policy dimension, the selection of the tax level, instead of the timing of the tax or the retirement age. Since benefits are equal lump-sum distributions, this vote is, in effect, a vote on the size of the benefits and on the amount of redistribution: the higher the tax, the greater the degree of redistribution. 11

For the analysis of simple two-party majority-rule representative democracies, it is common to treat the position of the median voter as decisive in determining the tax level because the Median Voter Theorem instructs parties to converge to her position. Translating different electoral rules such as proportional representation (PR) into a model of direct democracy may seem more complicated. However, Boix (2003) and Kang and Powell (2010) argue that the median voter prevails in both plurality and PR systems. This may also hold true for programs engineered through social compacts between business and labor, as in Sweden and Germany, since ultimately each compact must be implicitly sanctioned within the electoral framework.

The key issue, then, is how the median voters’ utility functions respond to future tax increases. From Appendix A, the response of the worker and the retiree’s utility to a tax increase is respectively

The utility of retirees is affected by the projected impact of policy changes on their children. Moreover, substituting for

Unpacking equation (5a) (see Appendix A) yields

This reformulation implies that increasing risk aversion among model workers and retirees moderates their preferences over public pensions. Risk aversion (γ) tempers opposition to public pensions rooted in high-endowment expectations since endowment realizations can fall short; it also tempers support rooted in low-endowment expectations since they can turn out to be overly pessimistic.

Given w > γ, equation (A4) also implies that each voter’s expected utility from the tax decreases monotonically as her (grand)children’s expected endowment increases. There is less perceived need for redistribution when expected income is higher. When that expected endowment is sufficiently large, in other words, she will vote for less spending. But if her (grand)children’s expected endowment is below average (

There is also a unique equilibrium workers’ consumption

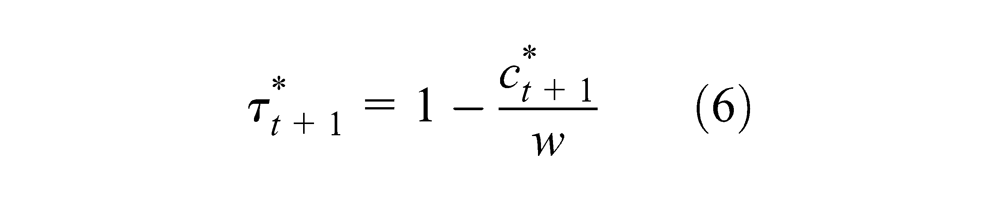

Thus the public pension program survives when the optimal tax creates a wedge between the base wage and equilibrium consumption, that is, when

Appendix B shows that whether

As for the rate of decline, because of differences in their underlying economies and intragenerational redistribution policies, some countries, independent of public pension policy, have more concave income transition functions than others. 12 This greater income mobility strengthens the POUM effect. Conversely, to the extent parents fear for the financial future of their children, support for public pension programs should increase.

When taxes decline, the new generation of retirees has paid a higher tax in support of their parent’s generation than the tax now supporting them. Strictly speaking, within the model these declining public pension taxes do not imply that the new retirees experience a negative net lifetime return on public pension taxes paid. Theoretically, population growth could offset the impact of declining tax rates. But empirically this is not a serious qualification. Even for the countries studied here that have positive population and productivity growth, economic growth has been trumped by the increasing longevity of retirees. 13

Given sufficient income mobility and increasing longevity, then, democratic politics imposes intergenerational transfers by allocating lower net benefits to later cohorts. At first sight, it is true, the median voter should support a redistributive payroll tax sufficient to maintain the existing benefit level since median income is consistently below mean income. Yet, as illustrated by the Italian data, the median endowment can remain perpetually below the mean, while, due to income dynamics, the median and expected mean reverse their customary positions. In that case, altruistic median voters will support public pension reductions for their descendants. Moreover, the distribution of endowments implies that what is true of median voters will apply to voters whose endowments lie within some finite interval below the median endowment.

Finally, note the crucial role played by altruism in generating these results. For the limiting case of no altruism—when α = 0 —equation (5a) says that workers’ utility increases with increases in taxes on their children, while equation (5b) says that retirees are indifferent to taxes that will not change their own benefits.

5. Empirical analysis

The POUM-based model explains why the financial structure associated with so many public pension programs has been politically acceptable even though their future retrenchment is a foregone conclusion. Beyond this aggregate-level result, it is important to determine whether, on the margin, actual individuals take into account the kinds of forces identified by the POUM-based model: relative income and mobility. Unfortunately, although the model embeds individuals in a closed political economy yielding equilibrium outcomes, available data are insufficient to estimate the key parameters of such a model. Even calibration of the model’s parameters is insufficiently constraining to render a clear empirical judgment (see note 5). This means it is not possible to explain fully the level of support for redistributive public pension programs and thereby predict their political future.

Fortunately, available individual-level data allow us to confirm whether POUM-based forces affect individual support as hypothesized. Of course, while the distribution of endowments is a key driver in the model, they are unobservable. Endowments, however, are positively associated with income and income is observable (see, for example, Cigno et al., 2003).

Intergenerational income mobility, then, can be used to measure the intergenerational link between current and future endowments. The expected income distribution associated with this income mobility, in turn, has implications for political behavior since public pensions in the model, as in practice, are redistributive: the tax burden is a positive function of income but, in the model, benefits are distributed in equal lump-sum amounts. The fact that the model program is redistributive is key to understanding how income mobility affects parents’ willingness to retrench the program. Accordingly, from the implication that utility from the tax is declining in endowments (Section 4) we have:

Hypothesis 1: The higher an individual’s income, the less likely she is to support public pension redistribution.

Income mobility, however, can change this calculation. For voters with above-mean incomes, mobility increases the likelihood that future redistribution will help their (grand)children. Similarly, for voters with below-mean incomes, mobility increases the likelihood that future redistribution will hurt their (grand)children. Specifically, from (A4) and Section 4 we have:

Hypothesis 2: The greater the degree of income mobility the less likely is an individual with below-mean income to support redistribution through public pensions.

This hypothesis, juxtaposed with the first, constitutes the signature implication of the model.

One question in the 2001 Eurobarometer survey on pensions addresses the fundamental redistributive dimension of public pensions:

Q. 62.7 (V389): ‘A good pension system should contribute to greater equality in income and living conditions among the elderly.’ The coding is: Strongly disagree, 1; Slightly Disagree, 2; Slightly Agree, 3; Strongly Agree, 4.

14

This question allows us to determine whether the key factors identified by the model—relative economic position and mobility—affect views on distributive principles in the appropriate way. Intuition suggests that surveyed support for a particular way of organizing a current public pension program should be associated with support for the same organization in the future. What makes this inference tricky is the model’s demonstration that support for current benefits does not imply support for the same level of future benefits. This is the altruism puzzle. In principle, then, elicited support for one kind of pension plan could disguise support for a very different plan for the future.

But this survey question is posed normatively, which generally suggests (anticipated) stability in responses over time. Moreover, normative responses are not detached from material interests, an assumption the first hypothesis tests empirically. If indeed normative responses are linked to material interests, we can treat the second hypothesis as reflecting the model’s implication that lower income respondents experiencing higher intergenerational mobility will tend to respond at the margin less favorably toward redistributive principles than lower income individuals with worse prospects.

This pension question has one other advantage. When studying public opinion concerning the welfare state it is important to disaggregate the general category of welfare spending into the appropriate policy area (Busemeyer et al., 2009). Note, in this respect, that unlike a welfare policy such as public education, pensions do not directly affect mobility rates. This means our test of the mobility hypothesis is much cleaner than it would be for some other policy areas.

I test the two hypotheses using a two-level hierarchical ordered logit model. The level-one variable measuring support for redistributive public pensions (PubPen) is regressed on the set of variables listed below. 15

The level one exogenous variables are: Income (D.29), after-tax household income in quartiles coded 1–4 and centered around its mean; BelowMean, coded 1 if income is below the national mean income, 0 if not; 16 Age (D.11); Age 2; Male (D.10), to control for a public pension program’s negative actuarial impact on men relative to women, coded 1 if male, 0 if female; and Ideology (D.1.1), to control for independent regard for redistributive programs, coded 1–10 Left–Right and centered around its mean. 17 Education is a natural variable to include, but the data indicate only the year education ended, which is quite different. Also, the effects of education could well confound the effects of income as a measure of endowment (see Fong, 2006).

The level-two variable is Immobility, a measure reflecting each country’s pre-tax income mobility based on parent–child income elasticities. 18 This hierarchical organization helps control, however crudely, for cross-country differences, including differing levels of redistribution built into the national programs. The countries are Belgium, France, Germany, Ireland, Italy, Portugal, and Spain.

Fortunately, while the selection of countries is dictated by mobility data, their political commitment to the elderly, measured by public spending as a percent of per capita GDP, varies considerably (Lynch, 2006) as does the degree of redistribution built into their programs (Conde-Ruiz and Profeta, 2007; Disney, 2007). 19 Nevertheless, countries with ‘Bismarckian’ low-redistribution systems also tend to have lower income inequality (Conde-Ruiz and Profeta, 2007), so the broader financial context facing respondents is not as dissimilar as it might first appear. Finally, this set of countries also spans Lynch’s (2006) classification of national social welfare programs as predominantly citizenship-based, occupational, or mixed, and her classification of political competition as particularistic or programmatic.

The associated mixed model produces ImmobilBlw, which is formed by the interaction of Immobility with BelowMean. The model assumes that the coefficients βij on the level-one intercept and variable BelowMean ij are given by βij = γ 0j +γ 1j Immobilityj , where i and j designate individuals and countries respectively. The cut points are designated by ck , k = 1, 2, 3, with c 1 = 0.

The resulting model is:

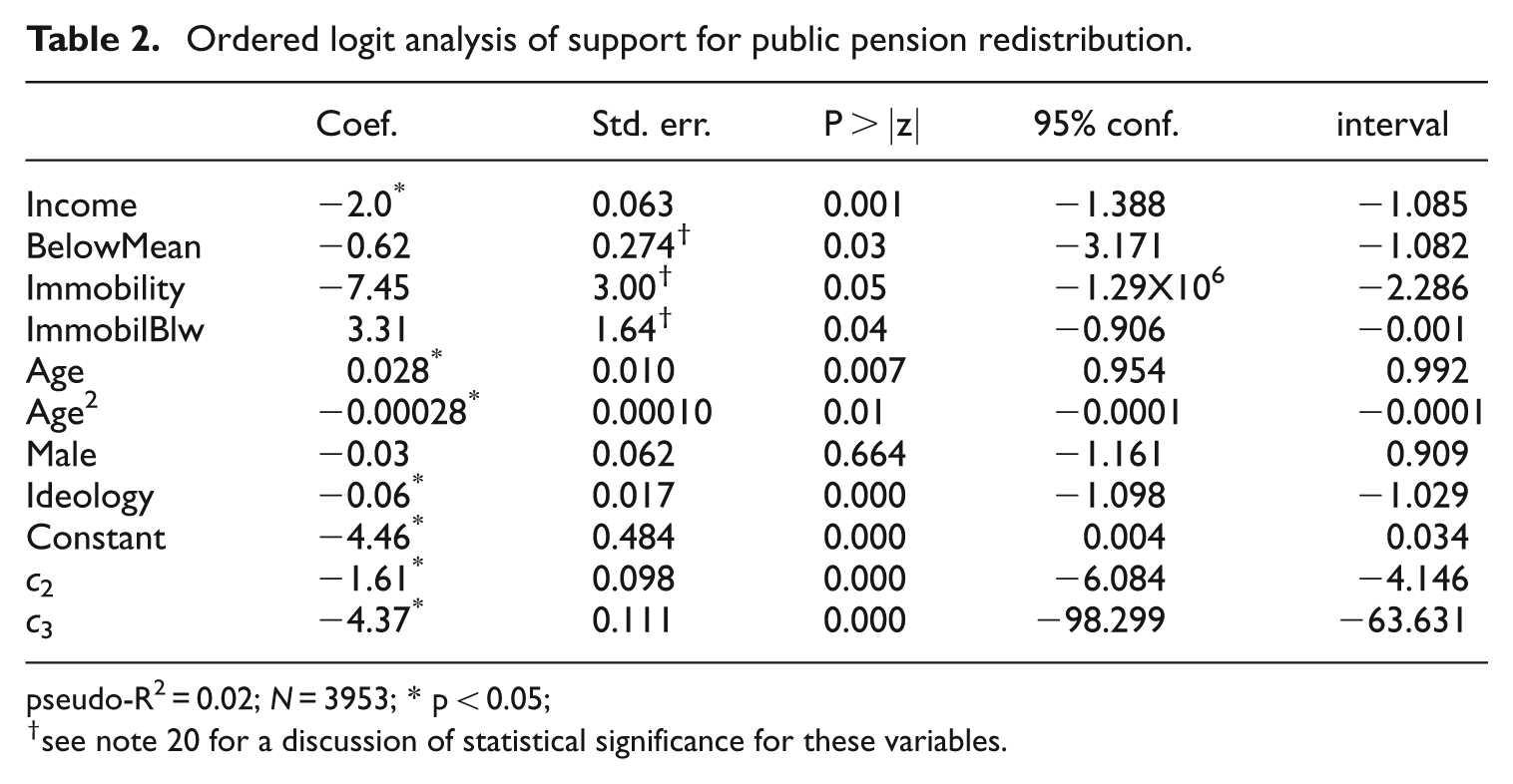

Regression results for the model are presented in Table 2.

Ordered logit analysis of support for public pension redistribution.

pseudo-R2 = 0.02; N = 3953; * p < 0.05;

see note 20 for a discussion of statistical significance for these variables.

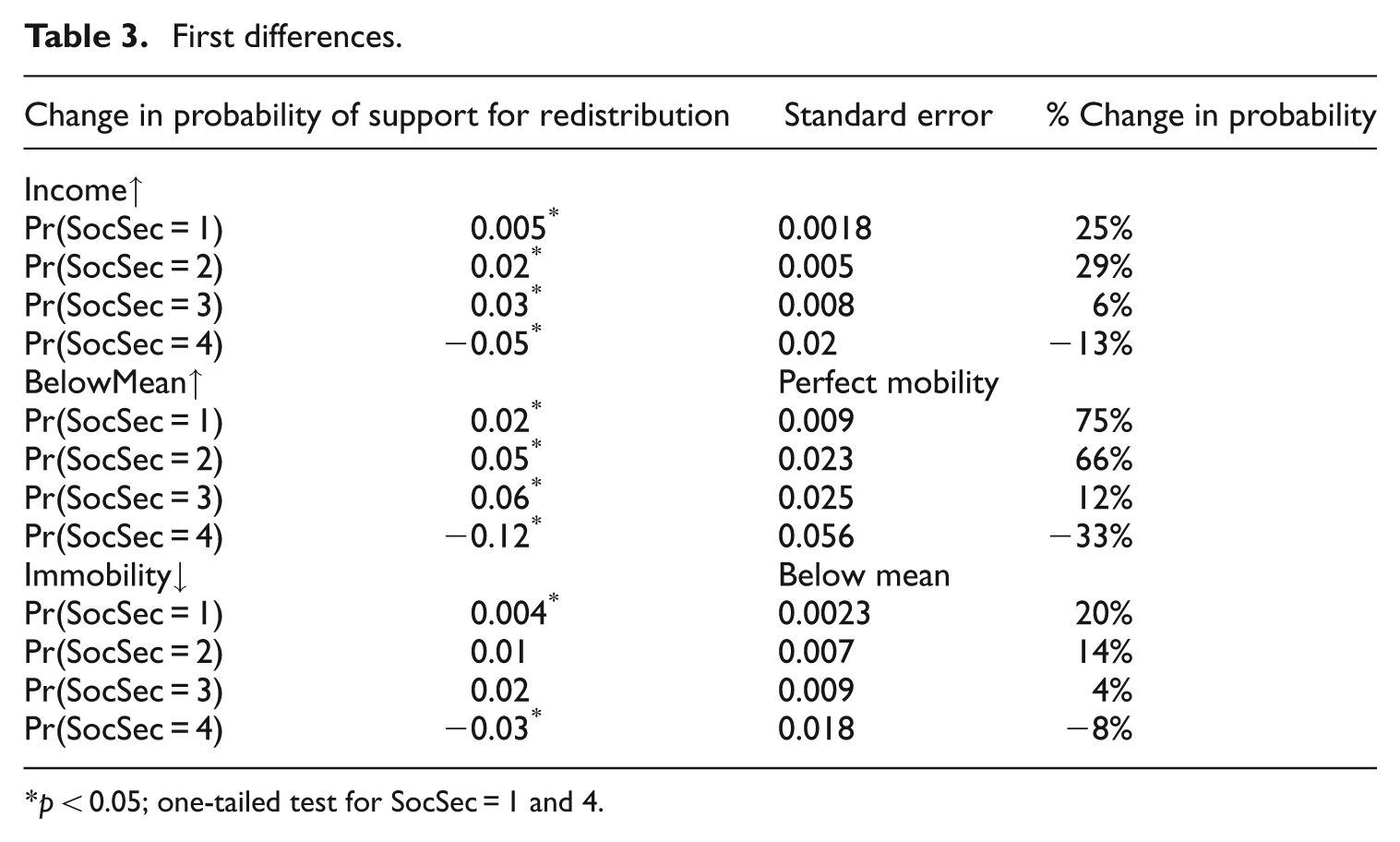

Before unpacking the full quantitative implications of Table 2, it is worth noting that the qualitative results are consistent with Hypothesis 1: income is negatively associated with support for redistribution. This suggests that answers to the normative question about public pensions are consistent with self interest. Unfortunately, the implications for Hypothesis 2 cannot be read directly off the table (Ai and Norton, 2003). 20 I simulate first differences to estimate the quantitative implications of the model’s two hypotheses. Table 3 reports the percent change in Pr(PubPen ij ) from the base probability with all variables set to their means except for the variable in question.

First differences.

p < 0.05; one-tailed test for SocSec = 1 and 4.

Income↑, a one standard deviation increase in Income from its mean, strongly shifts preferences against redistribution. Although the shift is not perfectly monotonic, the probability of strongly opposing redistribution increases by 25% and in the next strongest category by 29%. The probability of offering the strongest support for redistribution declines by 13%. It is worth bearing in mind that only probabilities for the extreme categories of the public pension response are unambiguously affected by a change in the relevant variable, while probabilities for the middle categories are sensitive to specific densities of the public pension variable. In any case, the results regarding income are not as obvious as they might first appear (see, e.g., Fong, 2001; Moene and Wallerstein, 2001).

BelowMean↑ shifts an above-mean income individual (BelowMean = 0) in a perfectly mobile society (Immobility = 0) to below mean (Income is shifted from the third quartile for the country to its first quartile). As predicted this simulated change pushes respondents strongly toward opposition to redistribution: those at the bottom half of the income ladder are now more likely to see redistribution as a brake on expected success. For those in the upper half, by contrast, mobility is less likely to work in their favor.

Immobility↓ shifts a below-mean individual from a society with mean mobility to a society whose mobility is one standard deviation above the mean. 21 This interaction variable is statistically significant with a one-tailed test (with the caveats about interactions already noted) and the substantive results are consistent with theoretical predictions. Indeed the percentage changes are fairly large, particularly for those categories reflecting explicit opposition to redistribution.

In sum, the data provide consistent support for the two hypotheses, which are designed to capture the kinds of POUM forces affecting the intergenerational politics of public pensions. Although income drives respondent preferences in a rationally self-interested fashion, we see that mobility considerations temper their calculations.

6 Conclusion

Western industrial nations initiated major social insurance programs in the late nineteenth century and brought them to maturity in the twentieth. These programs were designed to pool risk and thereby attenuate the impact of individual misfortune. Yet in one important respect they concentrated risk by imposing a disproportionate financial burden on later generations. The resulting retrenchment, which entails a major shift in financial exposure, has been politically reaffirmed for many decades. How is this possible if parents genuinely care for their children?

The period in which social insurance programs developed also witnessed an extraordinary increase in public spending on education and public health, as well as a general decline in the impact of social caste. While broadly part of the same political movement, the resulting increase in economic mobility may have had an unintended impact on social insurance. For rising mobility increases the likelihood that key insurance programs of the welfare state will impose net losses on a majority of the next generation. However strong the public’s political support for current programs, the rational expectation of an above-average financial outcome may in fact have motivated an implicit acceptance of their future restructuring.

In light of this possibility, this paper has explored an overlapping generations model of public pension programs whose existence and size are determined by altruistic parent-voters. Rather than using a static voting model with voters distributed by age or income, this approach recognizes the particular dynamics that arise when voting has implications for multiple generations of electorates. Two testable hypotheses emerge from the model. One, those with higher incomes will be less inclined to support redistribution through public pensions. Two, the greater the degree of income mobility, the more likely are those with below-average incomes to reduce their support.

An analysis of data from a 2001 survey of European attitudes toward pension programs provides consistent support for these hypotheses. The prospect of upward mobility induces a voting majority to protect their progeny against too much social insurance. This result also suggests, conversely, that support should increase when upward mobility falters, for example, when parents become less optimistic that their children will have better lives than they have.

Footnotes

Appendix A

Using equations (1)–(4), the equilibrium conditions for the model are:

where

From condition (A1a), then, the marginal utility of consumption equals the discounted marginal utility of savings. Because U(·) is identical across individuals, all workers must have the same consumption for these conditions to hold. 22 This means that loans from workers with above-average endowments (who receive the market interest rate It ) increase the consumption of workers with below-average endowments (who pay the market rate of interest).

Substituting these equilibrium conditions into the utility functions of workers and retirees yields respectively:

The first term on the right-hand side of (A2a) represents the worker’s utility from consumption; the second term represents the after-tax impact of savings or loans; and the last term sums her expected retirement benefits and her concern for the utility of her children when they are workers. Equation (A2b) has a parallel interpretation.

Finally, differentiating

Using the equilibrium conditions (A1), the law of iterated expectations to substitute for

This can be simplified using the formula for the coefficient of relative risk aversion γ (see note 5):

Contrast this with the results obtained from a model in which voters choose the current tax rate. The equilibrium conditions described by (A1) are unchanged but after substitution (A3) becomes

Since

In short, a setup with voting on contemporaneous taxes without upward intergenerational altruism and a median voter who is still working yields an optimal tax

Appendix B

To analyze the politics of taxation, designate the expected endowment of the children and grandchildren of the median voters by

where f −1(·), the inverse of the transition function, produces the endowment of the worker who is a median voter and a second application of f −1(·) produces the endowment of a retiree who is a median voter. 23

By setting equation (A4) to 0 and using the economic equilibrium condition

From equation (B2) and the assumption that γ < w, U″(·) < 0, and

By definition Gj

(·) is strictly increasing, so

Since the equilibrium conditions require

equilibrium consumption is associated with a unique equilibrium tax rate

To determine whether this condition is in fact satisfied, define

Whether a public pension program is politically sustainable, in short, depends on the expected distribution of endowments. Also, since

Acknowledgements

I thank Markus Crepaz, Keith Dougherty, Asha Gupta, Sharda Jain, Manuel Sánchez de Dios, Michael Tolley, and attendees at the States and Markets Speaker Series at SUNY at Buffalo for helpful comments on earlier versions of this paper. They are not responsible for any of its errors.

Funding

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.