Abstract

The concept of corporate social responsibility (CSR) has a long tradition in business, but it is relatively new in public administration. Recently, there has been general consensus that there is a need to promote CSR in public administrations so as to improve transparency, governance, and the efficient allocation of public resources. We develop a new scale for measuring local public corporate responsibility (LPCR) based on CSR international standards and inputs from experts and academics, who evaluate whether the selected indicators are relevant, useful, adequate and practical for measuring LPCR. We test the tool empirically by analysing the CSR practices of 24 municipal councils in a Spanish territory. The result is a scale that allows us to determine the extent to which the municipal councils are socially responsible. This tool gives citizens access to information about CSR in their municipal councils and enables the identification of areas where municipal councils face challenges and require improvement.

Keywords

Introduction

The concept of corporate social responsibility (CSR) has a long tradition in the business world (Moura-Leite and Padget, 2011; Rodríguez-Fernández, 2007). Interest in CSR has grown since the early 21st century, as seen in the special attention paid to CSR by the European Union, which has developed a European Strategy for it (European Commission, 2011). In this strategy, CSR is defined as ‘the responsibility of enterprises for their impacts on society’. The strategic approach adopted by the European Union remarks the benefits of CSR, which encompasses cost savings, access to capital, customer relationships, human resource management, and innovation capacity (Aguinis and Glavas, 2012).

CSR has served as a seed for many other closely related notions, such as university social responsibility, educational social responsibility, and environmental responsibility (Ahmad and Crowther, 2013; Fenwick, 2009; Garde-Sánchez et al., 2013; Uecker-Mercado and Walker, 2012). One of them is CSR in the public sector. As companies, governments are facing growing demands to make commitments to sustainable development, good governance practices, and information transparency (Bingham et al., 2005; Steurer, 2010). An example of these demands is the Sustainable Development Goals, a multilateral initiative promoted by the UN for companies, governments and civil society that aims to achieve sustainable development in its three dimensions – economic, social and environmental (United Nations, 2015).

These demands are especially relevant in the local arena, given the ability of municipal councils to ascertain and address the needs of the people they govern and the economic, social, and environmental impacts of the exercise of governance (Marcuccio and Steccolini, 2009; Piotrowski and Van Ryzin, 2007).

In this context, the concept of local public corporate responsibility (LPCR) emerges LPCR, which is being adopted by increasing numbers of municipal councils, is useful for legitimising the actions local corporations take on behalf of citizens. Numerous studies have sought to measure CSR and transparency at the national (Chapple and Moon, 2005; Gjølberg, 2009; Greiling et al., 2015), regional (Alcaraz-Quiles et al., 2014; Lodhia et al., 2012), and local levels (Navarro-Galera et al., 2018; Niemann and Hoppe, 2018; Tejedo-Romero and Esteves Araujo, 2018a). Nevertheless, a homogeneous standard for measuring LPCR has yet to be developed. Such a standard is essential for comparing responsibility performance between administrations or tracking the evolution of social responsibility over time.

This study develops a scale for measuring LPCR in order to determine its status on municipal councils. This scale is constructed using a methodology based on studies on CSR measurement (O’Connor and Spangenberg, 2007; Ruf et al., 1998). The scale is empirically tested on 24 municipal councils in a Spanish territory, the region of Murcia.

The study creates the scale by first identifying the initiatives for measuring and standardising CSR activities most significant at the international level and then selecting the indicators closely linked to LPCR from among them.

The result is a scale of 132 indicators grouped into four dimensions that address the following arenas of LPCR: ethics and CSR, economic/financial information, social and contracting issues, and the environment and sustainability. This scale brings together in one tool the virtues of each of the individual initiatives from which it draws. Going forward, it will be possible to measure CSR in local administrations, which will contribute to the ranking of LPCR and the subsequent implementation of measures to improve CSR management in public administrations.

The next section analyses the responsibility of public administration and LPCR, highlighting the importance of the latter for accountability to citizens. Section Proposal for measuring LPCR describes how the LPCR measurement scale is developed and explains its application in Spanish municipal councils. The paper closes by outlining the study’s theoretical and practical conclusions and pointing to avenues for future research.

Social responsibility and public administration

Public management and CSR

Public management evolves over time (Bryson et al., 2014; Iacovino et al., 2017). The traditional public administration approach of public management, which was consolidated by the mid-twentieth century, was based on political theory and a pragmatic foundation, and focused on efficiency. By the end of that century, changes in the global context, such as globalisation and technology development, had provided the foundation for a new approach: new public management. This approach had an economic basis and a positivist foundation, and prioritised both efficiency and effectiveness. New public management set the foundations for the popular assertion that “government should run like a business”; however, this assertion has been strongly criticised, since public administration has its own specificities (Lindberg et al., 2015; Beckett, 2000). Likewise, the global economic crisis evidenced the weaknesses of this approach (Levy, 2010). In this context, the new public governance approach emerged (Morgan and Cook, 2014; Osborne, 2009). Public governance attempts to overcome the politician–manager dichotomy by reconciling interests at the administrative level and fostering values such as equity, transparency, ethics, quality, sustainability, and accountability in public management (Iacovino et al., 2017).

In particular, CSR encompasses these values (Ghobadian et al. 2015; Kolk, 2016; Lee, 2008) and grants a special role to stakeholders. Indeed, CSR is a stakeholder-centred management model (Freeman et al., 2010; O'Riordan and Fairbrass, 2014). From a stakeholder management theory perspective, we distinguish between instrumental, normative, and descriptive CSR (Donaldson and Preston, 1995): the first is value oriented, the second focuses on norms, and the third is a contingent approach. From a descriptive perspective, stakeholders should be considered in public management with respect to legal requirements, either participating in different kind or processes or being their object. Additionally, stakeholders play both normative and instrumental roles in public administration. Descriptive and normative motivations are connected, since laws have a normative basis (Olson, 2003). From an instrumental perspective, public administrations, and municipalities in particular, could see stakeholders as a source of strategic importance, since administrations need stakeholders to achieve their goals (Schafer and Zhang, 2018, 2016).

CSR is an organisational concept that has the same tenets in both public and private organisations – that is, better governance, the integration of social demands in management, and closer links with stakeholders. However, while in the private sector these methods pursue instrumental, normative, or descriptive goals, in the public sector they strengthen the link between citizenship and institutions, making the latter accountable for the resources spent. Thus, from the new public governance approach to CSR management, CSR fosters the normative management of public administration bodies.

However, public and private organisations differ in terms of their goals, ownership, and authority limits (Nutt, 2006). Concerning these factors, CSR in the public sector has singularities in at least three areas: Goals: The goals of public administration have a service- and community-oriented nature (Wright and Pandey, 2011), while private companies aim to create value for stakeholders, particularly shareholders. Owners: Shareholders own private companies, while citizens own public administration bodies. The CSR approach is instrumental in the former case, and normative in the latter. Authority limits: The public sector has greater implications for stakeholders, since it entails more stakeholders who believe they have a right to participate in the decision making (Nutt, 2006).

The perspectives and approach of CSR and stakeholders differ significantly in the case of companies versus public administrations. Stakeholder management was first examined by Freeman (1984), and relies on a conceptual foundation of value creation through the cultivation of a network of relationships between the organisation, decision makers, and customers within the internal and external environments. Clarkson (1995) identified stakeholders in the particular case of public administration as “the government that provide infrastructure, and to whom obligations may be due; and the communities who are beneficiaries of the infrastructure, and liable to meet those obligations”. In public administrations the primary stakeholder comprises citizens, since they play several roles as those who receive the services of public administrations, vote, and press for improvement. Other stakeholders can include employees, enterprises and companies, users, unions, academia, civil society, transportation planners, suppliers, or political groups. In general, the stakeholder management framework thus implies a strategic approach to managing the expectations and participation of those that affect and are affected by project planning and implementation phases. This interest among international organisations in government environmental and social sustainability is accompanied by increasing demands from stakeholders for public bodies to be aware of their social responsibility and to recognise the growing need for information about governmental sustainability (Coglianese, 2009). Transparency in policy development is increasingly expected by stakeholders and is being increasingly emphasised by governments (Field, 2019; Riege and Lindsay, 2006).

The public sector can foster sustainable development through CSR via four key roles: mandator, facilitator, collaborator, and promoter (Fox et al., 2002). These roles deploy the special capabilities of the government to ease the adoption of CSR practices by companies. In the present research we focus on why public administrations should apply CSR in their own management, and how CSR can be measured. One of the four roles proposed, the promoter, is related to this aim, since, by example, governments can adopt CSR practices (Albareda et al., 2007). Public administrations could use this role to foster the other three and, in fact, create a CSR framework for other public administrations to follow.

Demand for CSR in the public sector

Public administrations should aim to protect basic rights and administer the general interest at the economic, social, and environmental levels (European Commission, 2011; Hawrysz and Foltys, 2015; Petkoski and Twose, 2003; United Nations, 2010). This constitutes a commitment, not required of other social agents, to guarantee citizens’ expectations concerning the above. Meanwhile, public administrations, like all organisations, generate social, labour, environmental, and economic impacts through their actions, as they provide employment, consumer goods and services, and promote public policies. Therefore, the criteria that underlie the concept of social responsibility should be applied to them, and they should be exemplary in promoting behaviours that go beyond legal compliance.

The recent economic crisis has demonstrated that, among other failures, public administration in general has faced a constant loss of confidence among citizens because they feel that it acts slowly and cannot adapt or respond to new challenges, and also perceive a lack of transparency in its actions and, though isolated, instances of public corruption (Canyelles, 2011). These factors have created citizen expectations that have led to a need to improve efficiency and transparency among public entities (Piotrowski and Van Ryzin, 2007), leading to demands for social responsibility by various stakeholders, as in the private sector (Crane et al., 2008).

Similarly, demands for the public sector to adopt CSR criteria in its management have been driven by the public sector’s prominence in the economy and the provision of goods and services in European Union nations. Crane et al. (2008) have asserted that governments provide a large quantity of goods and services in most industrialised countries, estimated at 40% to 50% of GDP. In some ways, demands for CSR implementation in the public sector could be considered even more important than those in the private sector, given that public entities such as schools, hospitals, and universities have, by definition, social objectives and their management is not motivated by profit (Seitanidi, 2004).

As Cueto-Cedillo and De la Cuesta (2016) and Melle (2014) suggest from a theoretical perspective, CSR management offers various utilities and focuses that provide the basis for and explain demands for CSR implementation in the public sector. From an instrumental perspective, CSR can be exploited as a differential factor or competitive advantage. In political terms, CSR implementation can legitimate institutional power through proof of its responsible exercise. In ethical terms, CSR implementation entails the promotion of socially ethical behaviour among organisations. Finally, adopting a multifaceted approach entails strengthening reputation, legitimacy, and trust across a society through holistic responsible management via policies of transparency and good governance, employability, procurement and contracting, investment, and public financing.

Social responsibility in local administration

Municipalities are immediate channels for citizen participation in public affairs that institutionalise and autonomously manage the interests of the corresponding groups (Nevado-Gil and Gallardo-Vázquez, 2016). Local autonomy is understood as the right and capacity of local entities to structure and manage public affairs within the framework of the law under their own responsibility and for the benefit of their inhabitants; this implies territorial protection, the principle of self-organisation, and control under the law. Local governments and administrators play an essential role in the functioning of the democratic system due to their proximity to citizens and their centrality in managing the resources in their area of jurisdiction, as they have direct and indirect impacts on global sustainability at the economic, social, and environmental levels (Alpenberg et al., 2018; Dankova et al., 2015; Cueto-Cedillo, 2014; Albareda et al., 2007; Moon, 2004). These levels are also at the core of CSR, but this concept focuses in private sector rather than in public one. CSR is based in international and national political initiatives promoted by institutions such as United Nations, The Organisation for Economic Co-operation and Development, and Global Reporting Initative (Dankova et al., 2015).

Municipal councils have their own competence or obligations, which are different from those of other administrations, such as national or regional competences. Additionally, concerning national and regional competences, municipal councils help carry out them. It should not be taken for granted that public administrations behave responsible. Indeed, public administration bears a negative image (Waeraas and Byrkjeflot, 2012). This is especially true in developing countries, but also in developed one. The corruption perception index published by transparency international evidences this fact (Transparency International, 2018). CSR in public administration stress this need and provides the tools necessary to monitor public administrations governance. LPCR brings these needs and tools to municipal councils.

This measurement of CSR is expected to contribute to improving the CSR of public administrations in general. Following such improvement, the RSC of the different public administrations can be compared. This will undoubtedly contribute to improving CSR management in order to provide better indicators in the final measurement. Citizens can be expected to demand more rigor and action from their administrations if the score obtained for CSR is low, and call for improved corporate governance, ethics, sustainable tourism, or responsible public contracting according to the results obtained via the measurement. In this sense, CSR is a signal of distinction between municipal councils, and can be seen as a reputation driver (Waeraas and Byrkjeflot, 2012). CSR in public administrations brings to public management international and national political initiatives, whose end goal is to boost public administrations’ reputation and good governance.”

A CSR focus in local public entities should go beyond mere legal compliance and control and strict economic rationality, to show a commitment to sustainability that is explicit in local government and public administration (Weyzing, 2009). Therefore, LPCR could be defined as ‘a voluntary commitment that goes beyond compliance with legislation regarding competence at the local level’ (Cueto-Cedillo and De la Cuesta, 2014).

The concept of LPCR is not settled in the literature. Research about sustainability and CSR in municipal councils is abundant (Alpenberg et al., 2018; Giacomi et al., 2018; Navarro-Galera et al., 2018; Niemann and Hoppe, 2018; Ortiz-Rodríguez et al., 2018; Tejedo-Romero and Esteves Araujo, 2018a; Tejedo-Romero and Esteves Araujo, 2018 b; Navarro-Galera et al., 2017; Nevado-Gil and Gallardo-Vázquez, 2016; Tirado-Valencia et al., 2016; Navarro-Galera et al., 2014; Bonsón et al., 2012; ), but lacks of a common denominator, a shared concept across the literature. Through this research, we propose how to measure a concept for the practice of CSR by municipal councils.

Each country legally defines the policies of public administrations. The local public administrations’ competences usually (depending on the country) include local security, spatial planning, tourism, promotion of health and sports, housing, or the provision of basic services such as water. It will be CSR, first, to efficiently provide those services (according to Carroll (1979), this would correspond to the economic dimension). In addition, all policies for the promotion of education, culture, health, transparency, ethics, local suppliers, etc. (competences not limited to local administration), among other things, can be considered CSR, since they are not mandatory but are implemented on a voluntary basis

Local public administrations are called upon to demonstrate the integration of CSR into their own management systems and relationships with their interlocutors; this involves external and internal dimensions. References to good corporate governance and its application to the public arena affect both the decision-making process and the formulation and implementation of policies; this entails a form of public management that is transparent, participatory, and egalitarian, considering in all cases the principle of accountability (Nelson, 2008). For this reason, information about sustainability in the public sphere requires the evaluation of transparent and responsible management (Navarro-Galera et al., 2014).

This study aims to quantify the extent to which local administrations are socially responsible by designing and proposing an LPCR scale. This exercise goes beyond mere proposition because it is applied to a concrete practical case: an analysis of LPCR in municipal councils in Murcia.

Proposal for measuring LPCR

Design of LPCR scale

Many research about sustainability and CSR in municipal councils draw on the indicator framework proposed by Navarro-Galera et al. (2014) (Navarro-Galera et al., 2018; Ortiz-Rodríguez et al., 2018; Navarro-Galera et al., 2017; Nevado-Gil and Gallardo-Vázquez, 2016; Tirado-Valencia et al., 2016 ). This framework contains GRI indicators and includes recommendations by bodies such as the Audit Commission (2007), the Chartered Institute of Public Finance and Accountancy (CIPFA, 2007), the OECD (2006), and the Spanish Association of Accounting and Business Administration (AECA, 2004).

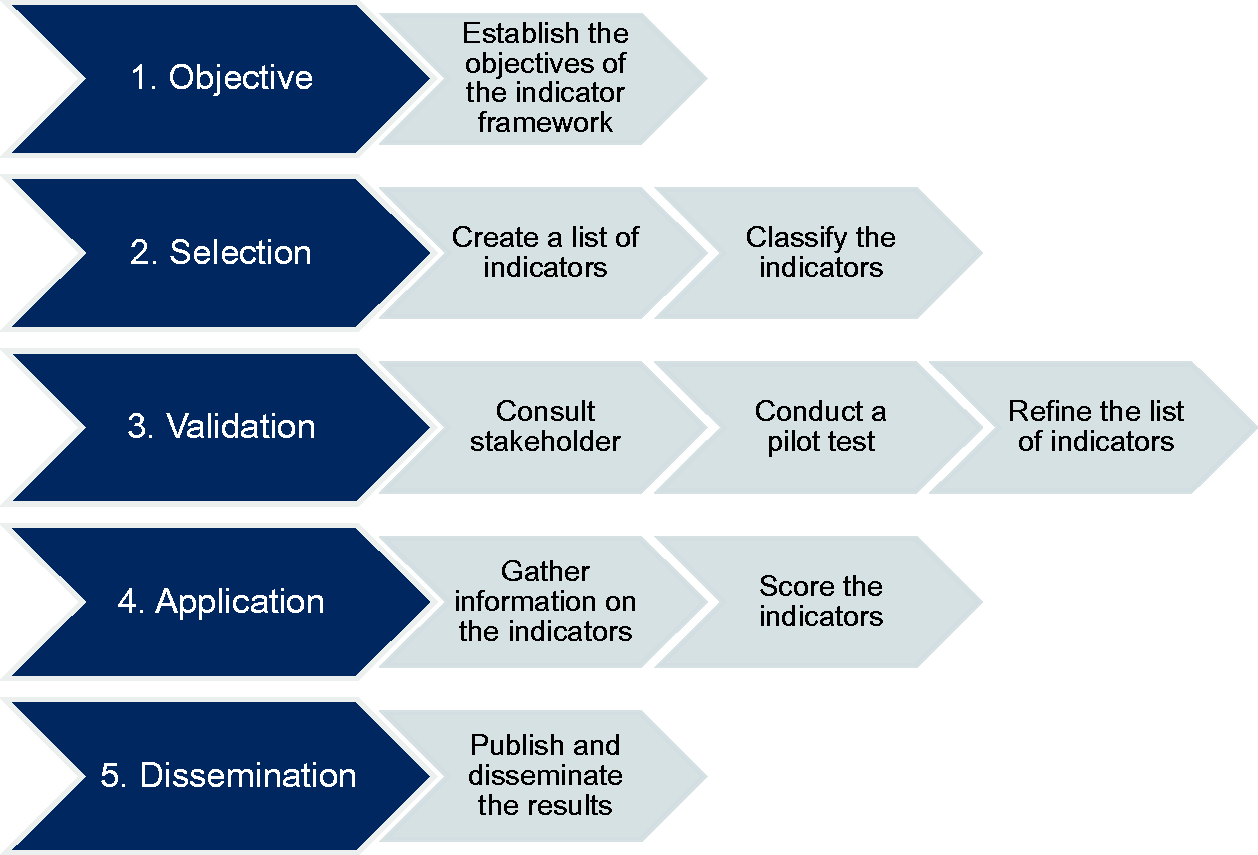

There is no universally accepted standard procedure for creating indicator frameworks; each author uses the process that best suits their needs (Lin et al., 2017; Rahdari and Rostamy, 2015; Perevochtchikova, 2013; Zhao et al., 2012; O’Connor and Spangenberg, 2007; Ruf et al., 1998 ). As illustrated in Figure 1, however, scales are often created in the following stages: The study establishes an objective, identifies the material indicators, contrasts the indicators with stakeholders, applies the scale in practice, and finally, disseminates the results.

Process of development of the framework.

This subsection describes the first three phases in the process (as illustrated in Figure 1), while the fourth phase is addressed in the following subsection. This division seems advisable because, in the fourth phase, the scale is put into practice through a concrete case: an analysis of LPCR among municipal councils in Spain (the region of Murcia). Thus, the design of the scale is separate from the way it is put into practice.

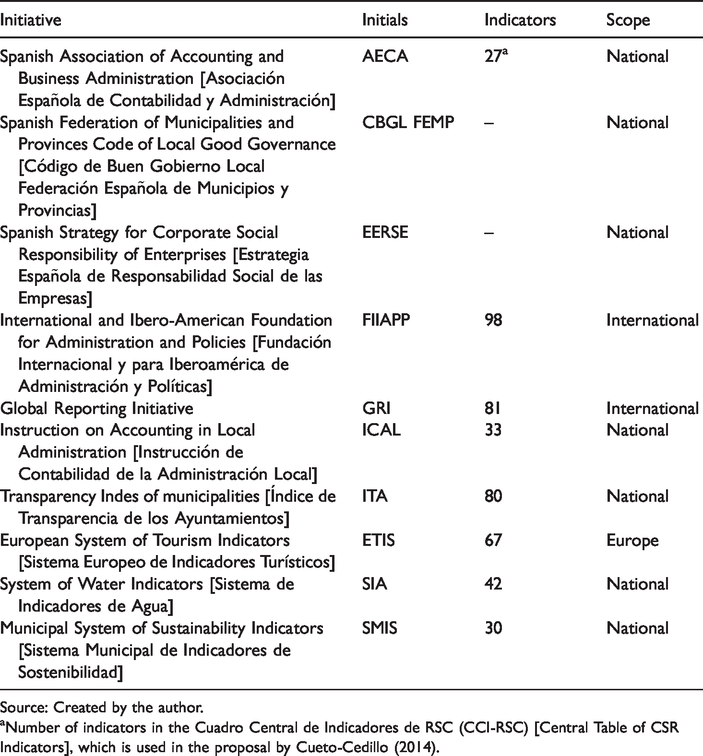

The objective of the scale is to be an operative measure of LPCR. The relevant scale indicators and items were identified by reviewing national and international initiatives related either directly or indirectly to CSR or LPCR. Table 1 lists the initiatives consulted. While we acknowledge that other initiatives exist, we have included just those we used as a source of indicators.

Sources for indicators.

Source: Created by the author.

aNumber of indicators in the Cuadro Central de Indicadores de RSC (CCI-RSC) [Central Table of CSR Indicators], which is used in the proposal by Cueto-Cedillo (2014).

Ten initiatives containing 458 indicators were reviewed. Some initiatives did not contain indicators but provided recommendations or basic guidelines based on the LPCR perspective. In such cases, the indicator was designed based on the recommendations.

Following a review of the indicators identified, the seven-member research team held a discussion that had two purposes: to identify priority indicators and to define blocks and groups of indicators.

To identify the priority indicators, three criteria were adapted from Accountability (2018): relevance, possibility, and content. Relevance refers to the usefulness of the indicator for citizens and public administration. Possibility indicates whether it is feasible to obtain the information required to publish the indicator. Finally, content indicates whether the indicator’s information has a significant impact on stakeholders and should thus be available to them. The relevance and possibility criteria were evaluated using a dichotomous scale; each indicator was assigned a score of 0 if it was not relevant or possible and 1 if it was relevant or possible. This procedure is similar that used by Transparency International (2017) in the ranking of indicators. The content criteria were analysed qualitatively through a debate between the research team members.

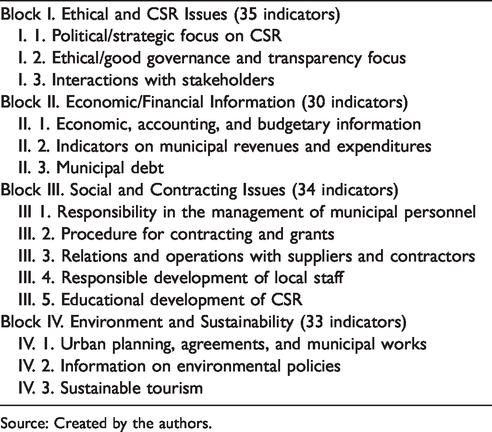

Previous literature about CSR in municipalities (Navarro et al., 2008, 2010; Cueto-Cedillo, 2014) have used a framework of indicators divided into four blocks. We have followed this approach, which in turn is based on GRI (2006). The indicators were divided into these blocks: Block I. Ethics and CSR Block II. Economic/Financial Information Block III. Social and Contracting Issues. Block IV. Environment and Sustainability

Emphasis was placed on indicators relating to activities of great importance in Murcia: sustainable tourism, water resources, and agriculture (Ibarra-Marinas, 2017). It is necessary to clarify that the third block refers to public expense. Sometimes the public service is offered by the public administration and other times it is offered through a hired third party. Thus, the block mixed both social and contracting.

The research team had an initial meeting with six academic experts from three research centres of the University of Murcia. A quantitative survey identified the relevant items for these experts. Ultimately, 143 indicators were selected as candidates for inclusion in the scale. The first version of the scale was obtained after the indicator identification, discussion, selection, and classification processes were completed.

In a second phase, professional experts participated in the local administration. We met with everyone to explain what we wanted from them. We visited each of them to explain what they saw in the questionnaire. The objective was the conceptual delimitation: a) that the scale includes everything that CSR can mean in a local administration and b) that the scale does not include anything that does not make sense. A quantitative questionnaire for item cleaning and dimensions was also made.

In the validation phase, various professional experts interested in LPCR checked the indicators included in the first version of the LPCR indicator framework. This process was intended to refine the initial indicator framework as well as to validate it at a micro or indicator-to-indicator level. In this step, the list of indicators was sent to several municipal councils in Murcia so that experts on politics, the economy, the environment, and civil society could provide an external perspective on the indicators. We visited each of them to explain know their opinion about the questionnaire. The objective of the meeting was a conceptual delimitation. Concretely, the scale should include everything that CSR can mean for local administrations, and it has to exclude items that does not make sense. A quantitative questionnaire for item cleaning and dimensions was also made.

Among the positions of the technicians consulted for discussion of indicators are: A Council Local Development Agent and President of the association of Agents of Local Development of the Region of Murcia. A secretary of City Councils. An auditor of two municipalities included in the study.

As per the method followed by the research team, each of the experts checked the indicators using the criteria of relevance, possibility, and content. Researchers gave to the technicians a list of items, and they were asked to rate the relevance of each item, as well as the validity of content, indicating to what extent the item fits a CSR practices.

The first version of the scale was refined by taking into account the opinions of both the research team and the municipal council experts. The result was a final set of 138 indicators divided into four blocks, each with a different number of groups. The scale was also tested in practice. The LPCR performance was analysed in the four most populous municipalities in the region of Murcia: Murcia, Cartagena, Lorca, and Molina de Segura.

The pilot test was carried out in the following way. First, the scale was presented to the municipal councils and its objectives explained to them. Subsequently, the researchers used the information available on the municipalities’ websites to complete the table of indicators and sent this information to the municipal councils. Indeed, disclosing information through the websites of public entities is an exercise of political accountability (Lourenço, 2015), a mechanism for achieving administrative transparency that has gained importance in recent years due to the use of new information and communication technologies (Navarro-Galera et al., 2018). Thus, websites are considered a suitable means of studying public information regarding sustainability, given the increased opportunities the internet provides to strengthen communication with and commitment to stakeholders (Frost, 2007; Navarro-Galera et al., 2014). However, websites analysis has also its limitations, since these webs have the risk to be simple “data repositories” (Lourenço, 2015).

This procedure assumes that everything the city council does is posted on its website. Until a few years ago this was not the case, but today the activity of city councils is typically comprehensively detailed online. In fact, the Internet is considered the main communication channel used by public administrations (Pernagallo and Torrisi, 2020). This fact has been reinforced by the current COVID-19 pandemic and by regulations on transparency that have mandated that extensive information published online (Gesuele et al., 2018).

Each of the four municipal councils analysed was considered a case study. The procedure used to score LPCR is based on the Transparency Index of Municipalities (Transparency International, 2017), and it has been used in other empirical studies (Tejedo-Romero and Esteves Araujo, 2018). The system included three options: ‘YES’, to which we assigned a value of 1 for cases in which the entity had disseminated the information to which each item referred. ‘NO’, to which we assigned a value of 0 when the entity had not disseminated the information reflected in each question. ‘PARTIAL’, to which we assigned 0.5 points if the information had been partially published on the web.

We reduced researcher bias in the information gathering and analysis processes by making a record of each website of reference, so that this information could be consulted by third parties interested in the study.

After each item was scored, we obtained a summary score for both the blocks of indicators and the municipal councils. The maximum summary rating was 10, and the minimum was 0. For the final rating, the statistical weight in the sum was 1 for the percentage of YES, 0.5 for PARTIAL, and 0 for NO, as indicated in the following equation:

The municipal councils reviewed the table, expressing agreement or disagreement with the scores assigned by the research team. Finally, a classification of municipal councils was formulated in which their ranking depended on the number of indicators about which they had published information on the web; the more indicators they had published, the better their ranking. Transparency is closely related to CSR (Ghobadian et al. 2015; Mazutis and Slawinski, 2015). These two terms are different, but transparency is needed in order to assess CSR. At a first glance, the scale provides insights about transparency. However, it also allows to evaluate public management, since it reveals whether the information needed for that is available. The scale consists in a first quantitative approach to CSR in public administration, which allows to perform a qualitative analysis of information provided by municipal councils. Transparency enables stakeholders to have information available so that they can evaluate municipalities’ management. Additionally, this information disclosed on their websites, which is used to complete the table of indicators, has been previously checked by the municipal councils. Consequently, municipalities had the opportunity to increase the information about their management, and therefore to get a higher score.

In the pilot test, the scale yielded satisfactory results. The municipal councils demonstrated a positive attitude towards the initiative. The results of the test made it possible to continue refining the indicators. The scale was revised and adapted based on the comments offered by the municipal councils, reducing their number and length. In this way, the second or final version of the scale was obtained, which had 132 indicators. The breakdown of indicators by blocks and groups can be seen in Table 2. The complete list of indicators is available to download through this link.

Structure of table of indicators for analysis of LPCR on municipal websites.

Source: Created by the authors.

Practical application: Case of municipal councils in Spain (region of Murcia)

Once the final version of the scale was obtained, it was empirically applied to Spain. Spain is a decentralized state in which the political is distributed between national (central government), regional (autonomies) and local (municipal councils) institutions (Aja and Colino, 2014). The 7/1985 Regulatory Law of the Bases of the Local Regime sets the powers of the municipal councils. We analyse the case of 24 municipal councils in Murcia. The available sample is representative of LPCR in the region, as the 24 municipal councils analysed comprise 88% of the region’s population. Each municipal council was analysed separately (thus each constitutes one case study), and the municipal councils were subsequently classified based on their score in the scale.

The selection of the 24 case studies was carried out through theoretical sampling, rather than statistical sampling, and an attempt was made to choose municipalities that offered greater opportunity for learning through the data published on their websites. We also followed the recommendation that the number of cases should not exceed 10 (Eisenhardt, 1989). Additionally, population criteria were taken into account. Most studies by the Spanish Statistical Office (Instituto Nacional de Estadística [INE]) use the 15,000/inhabitant threshold because municipalities with a population of this size or more represents approximately two thirds of the population in Spain. Population living in large cities can determine the number and diversity of stakeholders, as well as the resources available for disseminating information. Population criteria have also been used in earlier empirical studies (Bastida and Benito, 2007; Navarro-Galera et al., 2014; Pina et al., 2009, García Sánchez et al., 2013).

Thus, this mode of analysis facilitates the study of both the content and context of the data gathered through the identification of blocks or thematic areas selected based on the analysis of several sources of reference and research articles and the development of a database of the information gathered (Bonache, 1999).

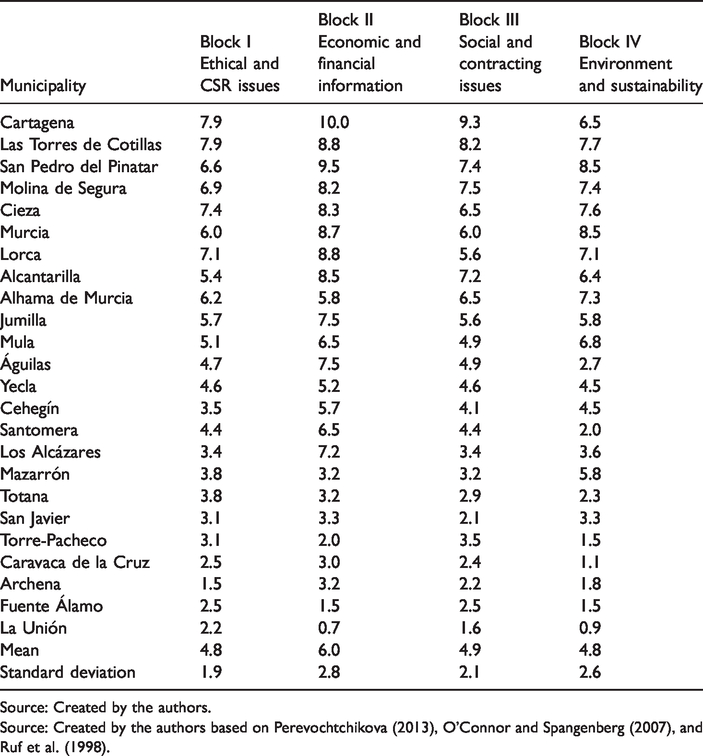

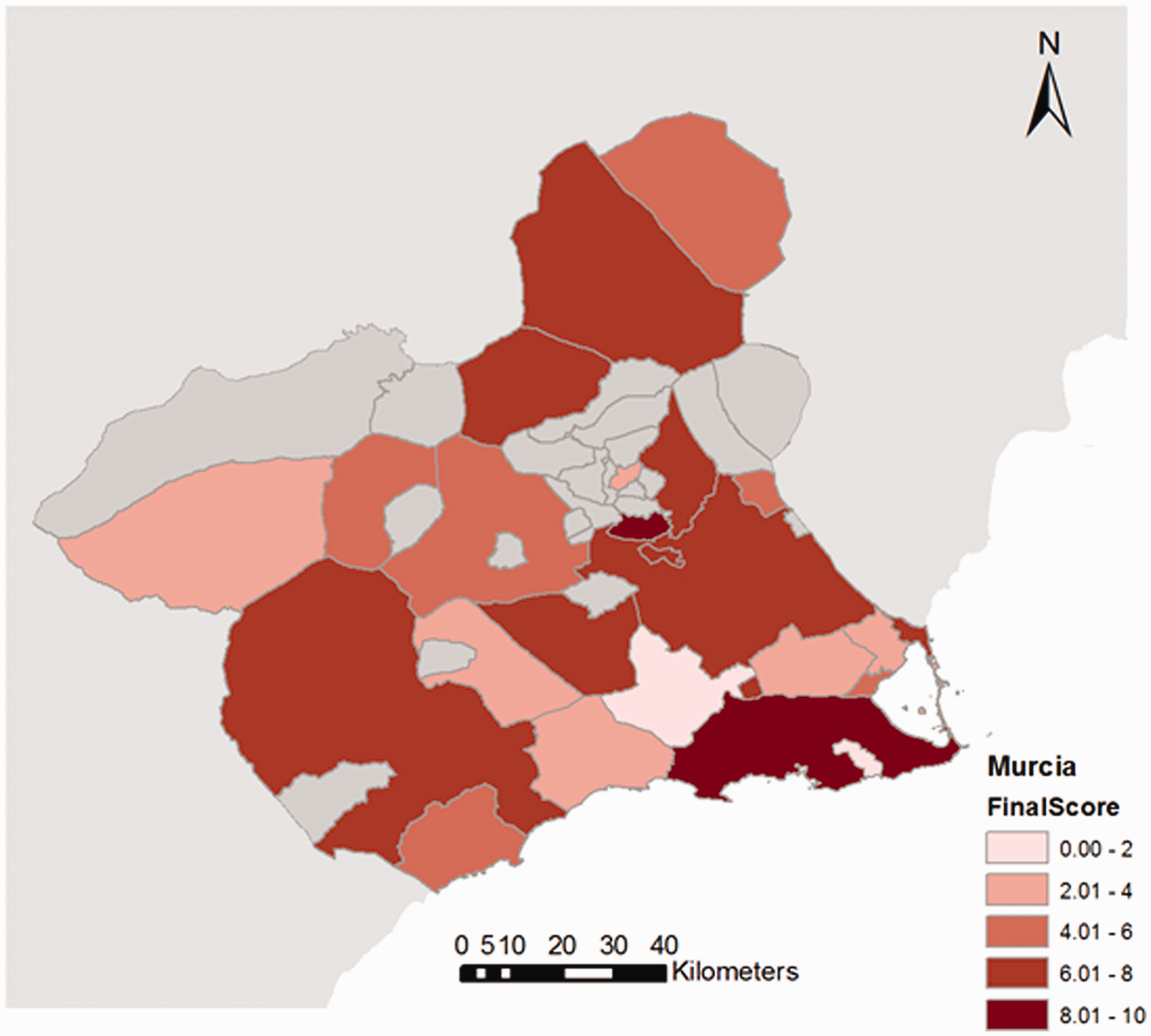

The procedure used to obtain indicator scores for the 24 municipal councils was the same as that followed in the pilot test. Table 3 shows the results at the general level, while Figure 2 provides a map displaying the geographical distribution of the results. The results demonstrate that half of the analysed municipal councils have achieved an acceptable level of commitment to CSR. The remaining municipal councils were divided between those that needed to make greater efforts to carry out management in line with CSR principles and those with a low level of commitment to CSR, with results that could clearly be improved.

Results of municipal councils within scale (by blocks).

Source: Created by the authors.

Source: Created by the authors based on Perevochtchikova (2013), O’Connor and Spangenberg (2007), and Ruf et al. (1998).

LPCR overall score by municipal council.

Comparing the results for the municipal councils across the blocks (see Table 3) shows that the majority have very satisfactory results in the block related to economic and financial aspects (Block II). At the other extreme, the municipal councils show the poorest results in the block regarding environmental and sustainability issues (Block IV). Similarly, the scores of most of the municipal councils evidence the need for improvement on ethical issues as well as social and contracting issues.

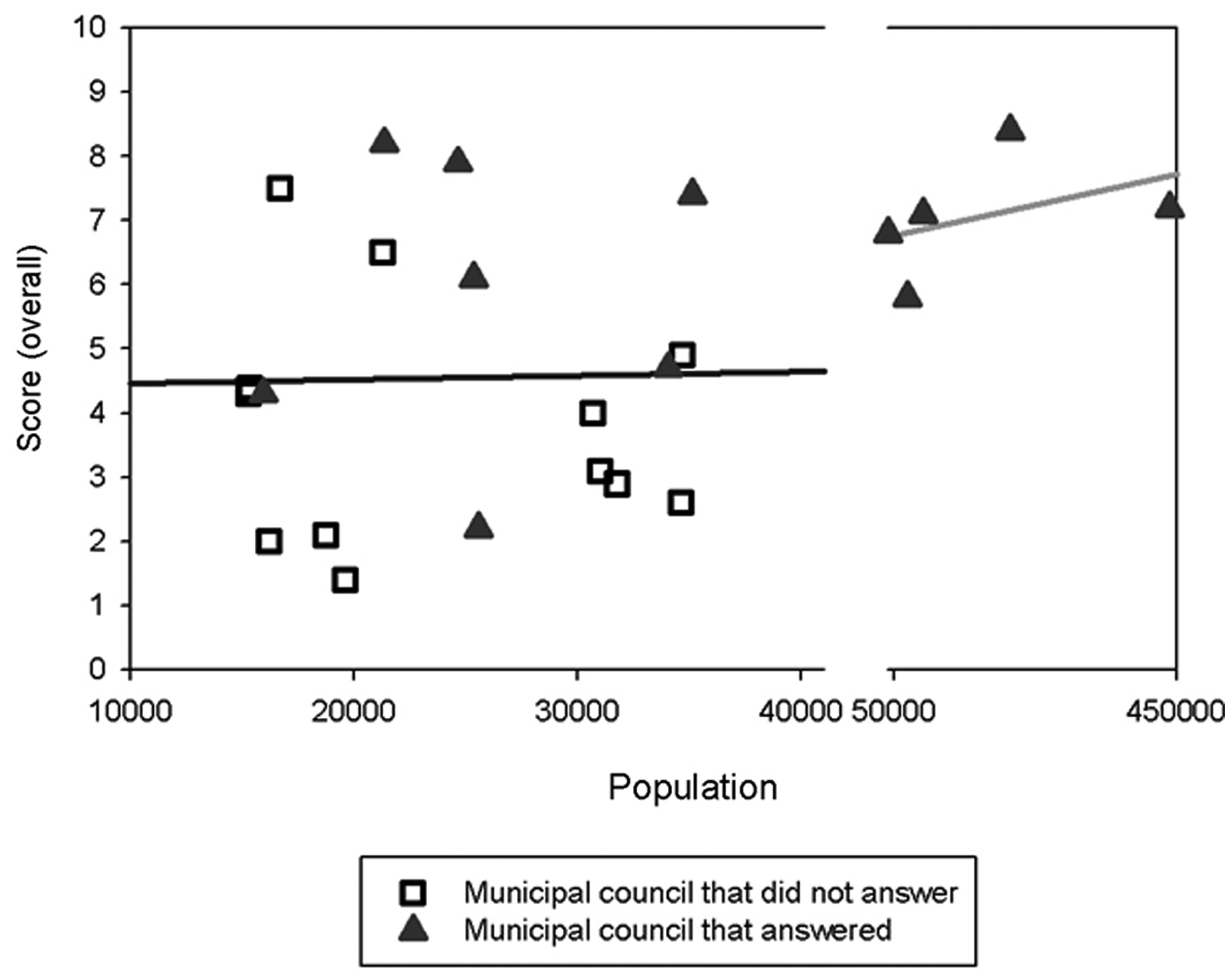

Figure 3 depicts the relationship between the size of the municipal council and LPCR overall score. The results evidence that, for municipalities of fewer than 40,000 inhabitants, the relationship is non-existent. In municipalities with more than 40,000 inhabitants, however, LPCR information is commonly disclosed. This finding demonstrates that, for the sample selected, municipalities with larger populations show a greater level of commitment to LPCR. This might be because they have more economic resources, but also because small municipal councils are physically closer to their stakeholders and thus they can be accountable in a direct way.

LPCR overall score by municipality size.

Conclusions

This study developed a measurement scale for LPCR in municipal councils based on previous studies conducted at the national and international levels. For this purpose, up to 10 CSR and sustainability indicators were used as sources. The scale was then improved with the participation of professionals with significant experience in local administration. The measurement scale comprises 132 indicators grouped into four blocks: Ethical and CSR Issues, Economic/Financial Information, Social and Contracting Issues, and Environment and Sustainability.

A scale of measurement for CSR in local administration enables us to analyse how public administrations generate positive impacts for society in economic, social, and environmental terms. This study contributes to the literature by quantifying LPCR. No measure of LPCR exists, and our scale makes it possible to determine the LPCR levels of municipal councils based on a set of LPCR indicators included in national and international CSR and LPCR initiatives. LPCR is a broad concept that can be divided into several blocks. The scale makes it possible to obtain an overall measure of LPCR as well as a partial measure for each of the blocks or groups of scale indicators.

This study has both theoretical and practical contributions. From a theoretical perspective, it links CSR with new public governance, setting the basis for further research. The study also study identifies the links between CSR and public administration at the local level and provides a tool for measuring LPCR. Additionally, it clearly delimits the different aspects or blocks comprising LPCR.

However, the paper’s main contribution is practical. The research develops a scale that goes beyond the sustainability of public administration and serves to measure LPCR. The scale contributes to the scientific literature by improving the measurement of CSR in public administration in five ways. First, it combines aspects of both sustainability and responsibility. Second, it draws from up to 10 national and international LPCR initiatives. Third, it is refined via the participation of experts through interviews and communication with municipal councils. Fourth, the measure provided by the scale serves to establish comparisons between the LPCR of different municipal councils. This comparison can be made not only at the level of overall LPCR but also at the level of its individual blocks. Using this scale, municipal councils can establish concrete objectives for LPCR issues and evaluate their achievement thereof. Finally, this study’s scale facilitates communication by making it possible to bring LPCR to citizens and promote governance transparency.

To achieve greater levels of CSR commitment, municipal councils must balance development levels among all CSR aspects, paying attention not only to responsible management and reporting to citizens regarding economic and financial issues but also to the adoption of an ethical focus and planning CSR deliberately. Similarly, social and contracting issues deserve to be given priority on the agendas of municipal councils, as does searching for information about actions carried out in this regard. Finally, municipal councils must not overlook their responsibility to the environment and sustainability, the issues generally attended to the least by the municipal councils evaluated.

This scale has two advantages over the scales used in previous studies: First, it incorporates indicators from up to 10 different LPCR initiatives, and second, it was refined through the participation of experts via interviews and communication with municipal councils. The scale is not only indicative of transparency in quantitative performance indicators but also goes a step further by reporting on the existence of public policies linked to LPCR regarding ethical, environmental, social, economic, and financial issues.

Regarding practical implications, the scale makes it possible to quantify LPCR in municipal councils. This will allow managers to compare their councils to others and to identify the LPCR issues at which they excel and those that require improvement. Regarding the latter, it is easier to specify objectives and monitor improvement measures once a measurement indicator is available. This will also give managers a tool for communicating their management of LPCR issues to citizens.

While this study reports important findings, it is not without limitations. The scale does not indicate whether the LPCR measures included in some of the indicators are effective in practice. Moreover, LPCR performance was not reported for all municipalities in Murcia; only the largest municipalities were included. This scale can be considered an important contribution, however, given that, at this level, no tool is available that provides an overall summary of the LPCR information published by municipal councils.

Finally, the avenues for further study are varied and interesting. The theoretical underpinning of CSR in public administration should be further developed. We suggest the term of Public Administrations Social Responsibility to study this link. LPCR would be just one part of Public Administrations Social Responsibility focusing on municipal councils, since national and regional administrations bear different duties. From a local government perspective, the scale should be tested across different types of local governments, or event across different countries, through comparative studies. It would also be useful to adapt the measurement scale to the particularities of small municipalities and extend the analysis to those cases. Such studies would enable the scale to be improved and made more robust. The analysis of the relationship between the political persuasions of municipal council governments and their LPCR performance levels is another interesting line of research. Finally, institutional agenda is paying growing attention to SDGs, which could be measured totally or partially with the scale proposed. In any case, it is apparent that LPCR is here to stay regardless of how research evolves.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.