Abstract

Developing carbon finance is significant to a green-oriented transition of energy but suffering risks in China. This article aims to construct a framework for the risk identification, analysis, and solution of carbon finance development. It could help trading parties, third-party intermediaries, and government to understand the main obstacles to carbon finance and then take effective control measures. Firstly, 12 risk factors in policy, economy, environment, technology, and society five aspects are identified. Secondly, the risk analysis data is obtained through a comparison of the mutual influence degree of factors, where hesitant fuzzy linguistic term set is used to collect the initial information and triangular intuitionistic fuzzy number is employed to quantify the qualitative linguistics. Expanding the analysis into fuzzy environment can avoid the loss of decision information caused by traditional single real number evaluation. Thirdly, the improved decision-making trial and evaluation laboratory (DEMATEL) and interpretative structural modeling methods are combined to gain the risk analysis results. K-means is used to refine the influence relationship between factors in traditional DEMATEL to three categories: high effect, low effect, and no effect, which enhances applicability of the model in reality. Finally, corresponding improvement schemes and policy suggestions are proposed for each risk factor. The findings of research show that among the risks hindering carbon finance development: low carbon price, immature carbon abatement technology, lack of carbon financial products, and operational risk are the direct factors; adjustments in international climate policy is the fundamental factor.

Introduction

The deterioration of climate environment has badly affected human survival and occupies an influential position in the international political game. Promoting the green transformation of energy 1 and developing the low-carbon economy 2 become important solutions to alleviate the current climate tensions. As the largest energy consumer and carbon emitter around the world, China has proposed a strategic goal of “carbon peak and carbon neutrality.” 3 This strategy would change the style of energy mix and production, requiring significant financial support to achieve the transformation goal. 4 Fortunately, carbon finance is an important economic tool to promote greenhouse gas emission reduction, which can benefit the transformation of low-carbon and provided new ideas to guide the innovation of traditional financial fields. 5 Therefore, it is necessary to develop carbon finance. Generally speaking, carbon finance refers to carbon emissions trading, further, it can be referred to the investment and financing behaviors related to low-carbon projects or resulting activities. 6 In this paper, carbon finance is deemed as all financial activities and matched financial regulations to limit carbon emissions, 7 including carbon markets and related financial intermediary activities. Besides the circulating funds, carbon finance can increase the effectiveness of reducing carbon emissions, 8 and alleviate the pressure to reduce carbon emissions. 9 It can be concluded that a complete and full-functional carbon finance system can benefit both the financial industry and ecological environment. On the one hand, carbon finance provides financial institutions with a way to transfer environmental risks. 10 On the other hand, carbon finance has the potential to increase the effectiveness of solving environmental problems, 11 which supports ecological environment development.

Carbon finance in China is at the embryonic and explorative stage, the government announced several policies to promote its development, such as Overall Plan for Reforming the System for Promoting Ecological Progress, Guidelines for Establishing the Green Financial System, Work Plan for Climate Investment and Financing Pilot, Overall Plan for the Pilot Reform of Comprehensive Market-based Allocation of Factors of production. However, there is still a significant gap between Chinese and international carbon finance, 12 and its development in China has always been accompanied by risks, such as policy factors, 13 talent factors, 14 and social factors. 15 Guo et al. 16 pointed out that the policy of carbon market would affect carbon finance development. Zhou and Li 7 emphasized that the key barriers to carbon finance are the absence of information systems and professionals, shortage of policies and regulations, and lack of product innovation. Li et al. 17 proposed that carbon emissions allowance (CEA) price directly affects the efficiency of carbon finance. Liu 18 believed that the environmental consciousness of people has the biggest impact on carbon finance development. Zhang 19 discussed the obstacles to carbon finance developing from the view of institution building. He found that inefficient markets, insufficient market dynamics, lack of national hierarchy, and lack of legal regulation were important barriers to carbon finance development. Chai and Zhou 20 measured the integration risk of carbon finance, pointing out the multiplicity and nonlinearity of its risk factors.

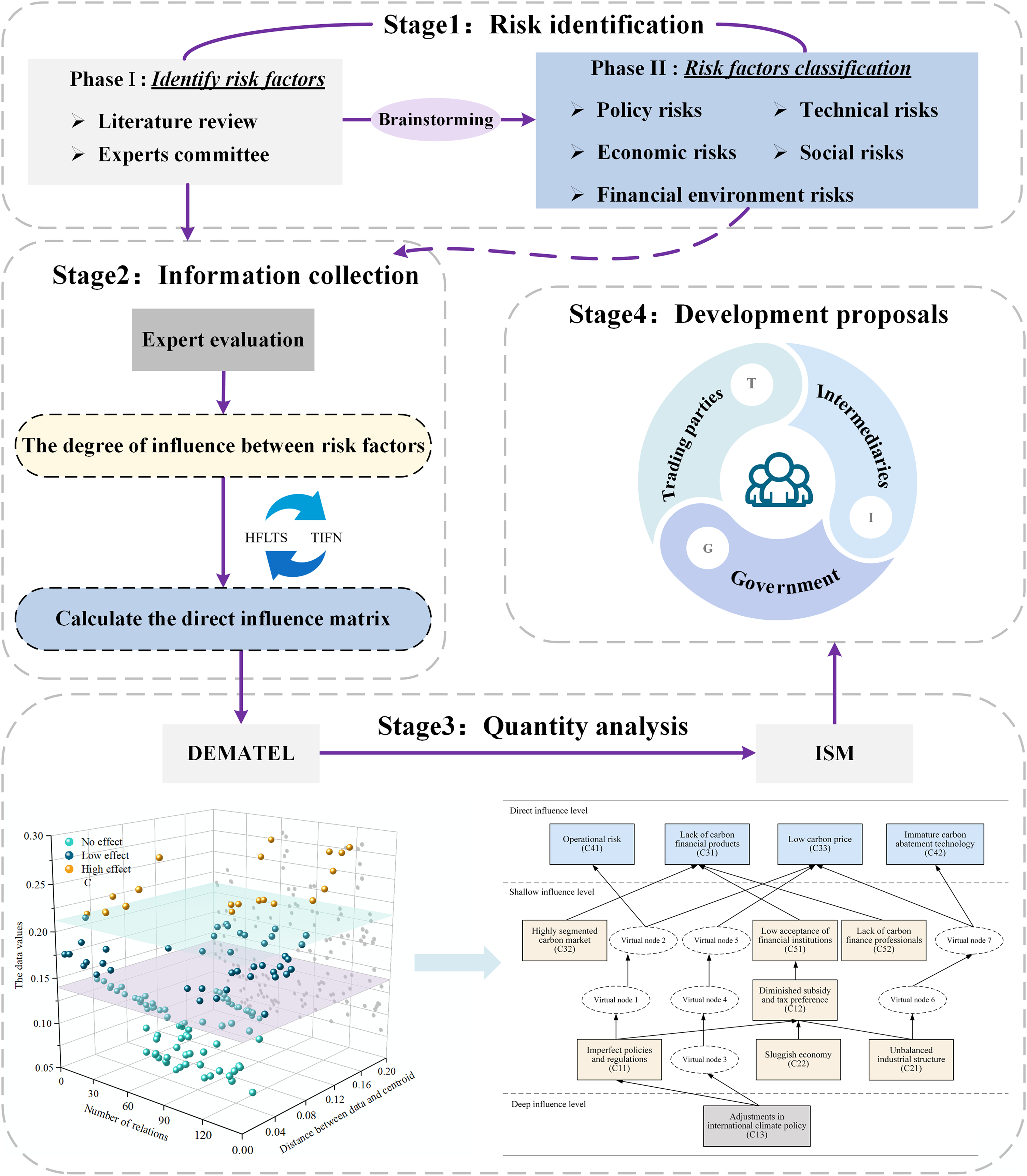

The above analysis shows that carbon finance would be affected by various risk factors, which are interrelated to form a complicated system. It is important to identify and analyze the risks of carbon finance development comprehensively and accurately, so as to put forward the proper solution. But the most current research on carbon finance risks focuses on qualitative exploration, lacking quantitative research to make risk analysis results more objective and persuasive. At present, three problems can be summarized in studying the risks of carbon finance development in China: (1) Developing carbon finance involves many risk factors, but there is no formed index system; (2) The relationship between risk factors is complex and mutual influence is difficult to be quantified; (3) Lack of quantitative and qualitative research methods to obtain analytical models and conclusions. Governments and policymakers would better cope with the development of carbon finance if they could focus more on the most critical risk factors. For the first issue, the article utilizes literature analysis and Delphi method to identify key risk factors from five aspects in policy, economy, financial environment, technology, and society. For the second issue, decision-making trial and evaluation laboratory–interpretative structural modeling (DEMATEL-ISM) provides a clear description of the causal relationship among complex factors and their hierarchy in the whole system, and has good applicability in complex systems analysis such as carbon finance development. Therefore, the DEMATEL-ISM method is introduced for quantitative analysis of the influence relationship between risk factors. For the third issue, this paper extends the model to a fuzzy environment, which can effectively solve the information loss of expert decision-making in the quantification process of the traditional DEMATEL method, and the risk factors are divided into three levels: direct influencing, shallow influencing, and deep influencing.

In summary, this paper aims to carry out comprehensive research on carbon finance development risk. The main content can be summarized as identification of risk factors, risk quantitative analysis based on DEMATEL-ISM, and suggestions for risk control. The contribution of the study could be refined as three aspects. (1) Constructing a risk index system for carbon finance development, including 12 factors from policy, economic, financial environment, technology, and social five aspects. The content of each risk factor is explained in detail, which can provide a reference for relevant researchers in carbon finance. (2) Proposing a quantitative analysis framework of risk factors, which realizes the analysis of importance, correlation and hierarchy of risk factors, providing methods and model support for risk managers. (3) Giving detailed suggestions and measures for risk factors control, which provides strategic support for the trading parties, third-party intermediaries, and government to accelerate carbon finance system building in China. The innovations of the study could be summarized in the dimensions of theoretical approach and practical application. From the perspective of theory and method: (1) Improving the determination of threshold in traditional DEMATEL based on K-means. Compared with other clustering algorithms, K-means algorithm has advantages in operation and calculation. The employment of K-means can expand the mutual relationship between risk factors in DEMATEL from “no effect” and “effect” into “no effect,” “low effect,” and “high effect,” which refined the influence degree and increased the compatibility with the actual demand. (2) Expanding the decision-making process to the fuzzy environment, hesitant fuzzy linguistic term set (HFLTS) and TFN are used to collect and process information for risk analysis decision-making. The former can effectively describe the hesitancy of decision-makers, and the latter can reduce the information loss of qualitative language quantification. Compared with the presentation of information by single real number, the combination of HFLTS and TFN can improve the utility of decision information and the accuracy of decision results. From the perspective of practice and application: (1) Sorting out the risk factors of carbon finance development in China, and constructing a new risk analysis index system through five aspects: policy, economy, financial environment, technology, and society. (2) The DEMATEL-ISM method is applied to risk analysis of carbon finance to clarify the mutual relationship and assess the influence of various risk factors.

Literature review

Development of carbon finance

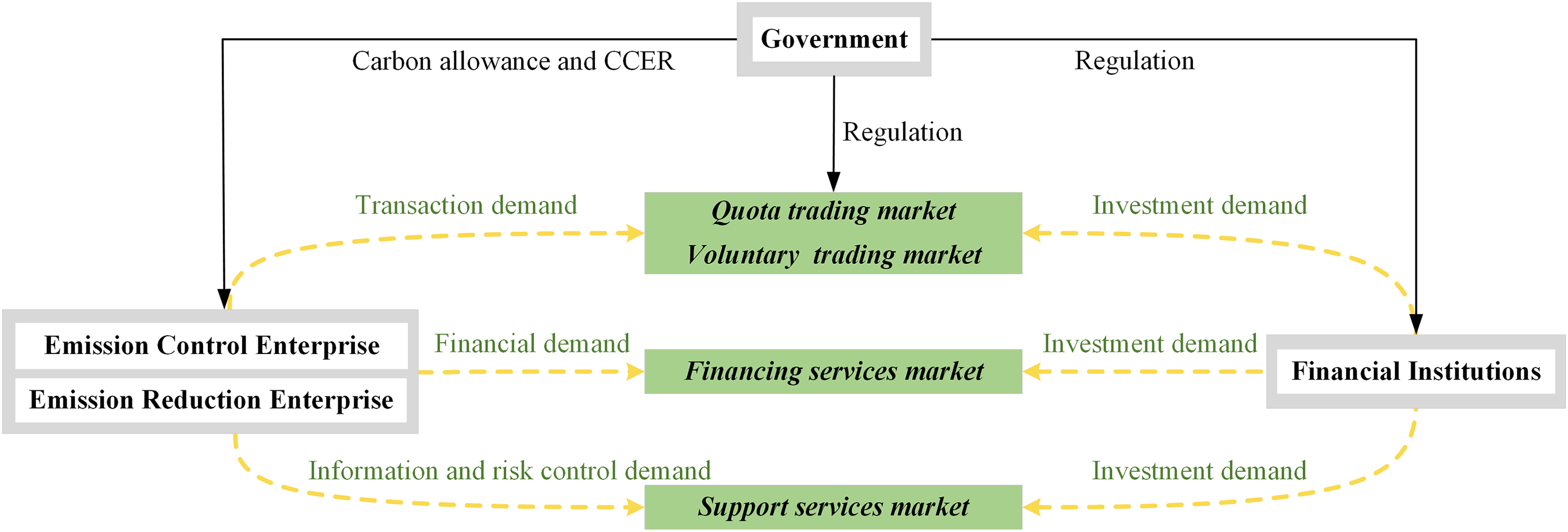

Carbon finance is a market-based approach to mitigating climate change, which was first defined by the World Bank in the 2006 annual report as financial resources used to purchase greenhouse gas emission reductions. 21 Labatt and White 22 argued that carbon finance was a branch of environmental finance. Some scholars believed that carbon finance primarily refers to all financial system arrangements and financial transactions aiming at carbon emission reduction, including trade and investment of CEA, development and financing of emissions-reducing projects, and other intermediation activities.23–25 This paper summarizes the main views of carbon finance mentioned above, as shown in Figure 1.

Main participants and participation methods of carbon finance.

As a financial innovation under climate change, 22 carbon finance is established on legal foundations, highly relying on the design of institutional structures. The policy related to the global response to climate change has a direct impact on carbon finance development.26–30 Xu et al. 31 believed that active environmental policy formulation can promote green finance development, and carbon finance is included in the concept of green finance. Wang et al. 32 analyzed the causes and impacts of carbon market risks based on international cases. He believed that relevant authorities should speed up legislation in the early stage of carbon finance development to effectively prevent and control risks. Zhu et al. 33 evaluated the risks of Chinese pilot carbon markets and discovered that a lack of regulations is a main barrier to carbon market development.

A series of empirical studies have enriched the literature on macroeconomic factors affecting carbon market trading activities. Wu et al. 34 analyzed the impact factors of carbon finance by the logarithmic mean index method, and found that economic growth affected carbon finance. Tan and Wang 35 used the quantile regression method to analyze the influence path and dependence of macroeconomic risk factors on CEA in the European carbon market. He found that macroeconomic risk factors had an effect on CEA, and the attitudes of the public or financial institutions are also major obstacles to carbon finance development. Liu 18 argued that the environmental awareness of the population has an influence on carbon finance development.

In addition, the rapid growth of carbon finance is inseparable from a stable financial environment. Firstly, the construction of a carbon financial market requires financial institutions to continuously improve their innovation capabilities in carbon financial products.36,37 Zhang 38 pointed out some shortcomings of carbon finance in China, such as imperfect development of the intermediary market and lack of pricing advantages in carbon trading. Secondly, the carbon price is often used to represent the growth of the external financial environment of the carbon market. Zhang et al. 39 measured the comprehensive risk of carbon finance in China, and pointed out that there are carbon price risks in its development at present. Fang and Cao 40 considered that extreme changes in carbon price will affect the stakeholders, which seriously hinders the development of carbon market. 41

Moreover, the other study found that technological advances could affect the stable operation of carbon finance, 42 and the system loopholes caused by the imperfect technology of the control system could cause operational risks. 33 Pan 43 researched a risk evaluation system of commercial banks’ carbon finance from the aspect of operation. Yan and He 44 believed that carbon finance has risks in both insufficient information disclosure and operation, which is caused by a lack of business professionalism. On this basis, this study will promote a systematic discussion of the risks of carbon finance development in China.

Method in risk analysis

The risk analysis of carbon finance development depends on the scientific methodology. Traditional risk analysis can be carried out based on two approaches, the one is to assess the risk of a business or project, and the other is to analyze the influence degree and mutual relationship of risk factors. The representative methods of the former are TOPSIS, VIKOR, Choquet integral, TODIM, and other MADM methods with integrated functions. These methods are suitable for obtaining the final risk level through integration under the condition, where the decision attributes of risk factors had been obtained. The representative methods of the latter mainly include AHP, ANP, DEMATEL, and ISM. These methods are applied to the mutual comparison between multiple risk factors, which can obtain the importance of each risk factor and the mutual relationship between factors. For example, Liu and Wei 45 calculated the risk levels of electric vehicle charging infrastructure projects based on Fuzzy TOPSIS. Yu et al. 46 conducted risk assessments of submarine pipelines based on the extended VIKOR method. Ruan 47 utilized Choquet integral to assess the risk of software development. Yin and Liu 48 used the improved TODIM in the risk assessment of Chinese photovoltaic-energy storage utilization projects. It is obvious that the methods adopted in these studies are focused on the specific micro project, which are not suitable to the demand of risk analysis of carbon finance development from a macro-perspective. Furthermore, scholars have proposed the utilization of AHP, ANP, and other methods for risk analysis from macro-perspective. Unver and Ergenc 49 used AHP to identify and prioritize safety risks in forest logging activities, and Wu et al. 50 used ANP to analyze risk importance in renewable energy investment. However, the AHP method does not consider the influence relationship between indicators in risk analysis, and the ANP method is relatively complex in calculation and cannot draw the influence relationship between indicators. To address these limitations, scholars proposed DEMATEL, which can identify important factors and analyze influence relationship between indicators. Feng and Ma 51 used the fuzzy DEMATEL to identify key factors affecting service innovation in manufacturing firms, and analyzed the influence relationship between them. Zhou et al. 52 quantified risk factors of applying blockchain to power trading using the improved DEMATEL.

At present, there are more researches that focus on hybrid approach of DEMATEL and other methods, particularly DEMATEL-ISM, which can reduce the complexity of matrix calculation. DEMATEL can reveal the relationship between indexes in research system, and identify the correlation of indicators by drawing the cause-and-effect diagram. ISM can analyze the correlation order of system indexes, and transform complex relationships in the system into an intuitive hierarchical structure model. Therefore, DEMATEL-ISM can clearly describe the mutual relationship between various factors and structure the complex factors in corresponding levels in system. It is worth mentioning that many literatures are using DEMATEL-ISM. Thakur and Wilson 53 applied DEMATEL-ISM to analyze barriers that affect consumer adoption of community solar. Yong et al. 54 identified the main factors affecting the development of energy storage sharing by using DEMATEL-ISM. The above analysis showed that DEMATEL-ISM is suitable for identification and analysis of risk relationships.

However, the traditional input of DEMATEL relies on qualitative evaluation from experts and is usually quantified into 1–9, which is difficult to reflect the subjectivity of expert decision-making and easy to cause information loss. Fuzzy theory performs well in solving these problems and makes results more accurate. 55 Rodriguez et al. 56 proposed HFLTS, which could obtain subjective information of experts flexibly. 57 And so, HFLTS is introduced into the DEMATEL method in this study. Meanwhile, the clustering algorithm is introduced in threshold determination, avoiding the arbitrariness of the traditional DEMATEL in determining interrelationships between comprehensive factors. K-means uses Euclidean distance for similarity assessment and has the advantages of excellent clustering effect than other algorithms,58,59 so that it can be regarded as a pre-optimization method for various models. Wu et al. 60 improved DEMATEL with K-means for further obstacle analysis of dispersed wind power development in China, and Xu et al. 61 also used K-means in threshold determination of DEMATEL. Therefore, it is feasible to apply DEMATEL-ISM for risk analysis, and the method can be further optimized to enhance the objectivity and comprehensiveness of analysis results.

The findings of literature review

According to the above work, carbon finance is an effective way to deal with climate change. However, the carbon finance development in China started late and faced many risks. Current research focuses more on the Chinese carbon market and lacks quantitative studies on the risk of carbon finance development. This paper tries to study the risk factors affecting the development of Chinese carbon finance to fill in the blanks. For the risk analysis of carbon financial development, it is necessary to clarify the importance and mutual influence of different factors, and DEMATEL-ISM can well meet this demand. But there are still the improvements on this method, such as improving the utility of decision information and reducing the subjectivity in expert decisions. Therefore, the research questions of the paper can be presented as follows:

This paper hopes to meet the shortcomings of the previous study. (1) There is insufficient systematic research on the risks of carbon finance development and the unquantified risks. This paper aims to systematically explore all the possible risks of Chinese carbon finance development, analyze the influence mechanism between risk factors in detail, and determine the crucial factors. (2) The current application of the DEMATEL-ISM method can be improved further, reflecting in evaluation information-gathering and threshold determination. In this research, HFLTS and triangular intuitionistic fuzzy number (TIFN) are employed to collect and quantify the decision information, K-means is used to determine the threshold. Based on literature research, the study pinpointed that the risk factor of carbon finance development is complex. To promote this research related to risk identification, analysis and solution to carbon finance, the research hypotheses are given as follows:

Risk factors identification and system construction

The risk identification of carbon finance development process is determined through a two-step approach. First, investigators search a large number of literature and industry reports on carbon finance for risk index selection. Second, professionals in carbon finance domains are invited to form an expert committee, and use the Delphi method for screening factors. According to the progress in carbon finance, the paper replaces and supplements factors to improve the list of risks, which provides ideas and suggestions for research design.

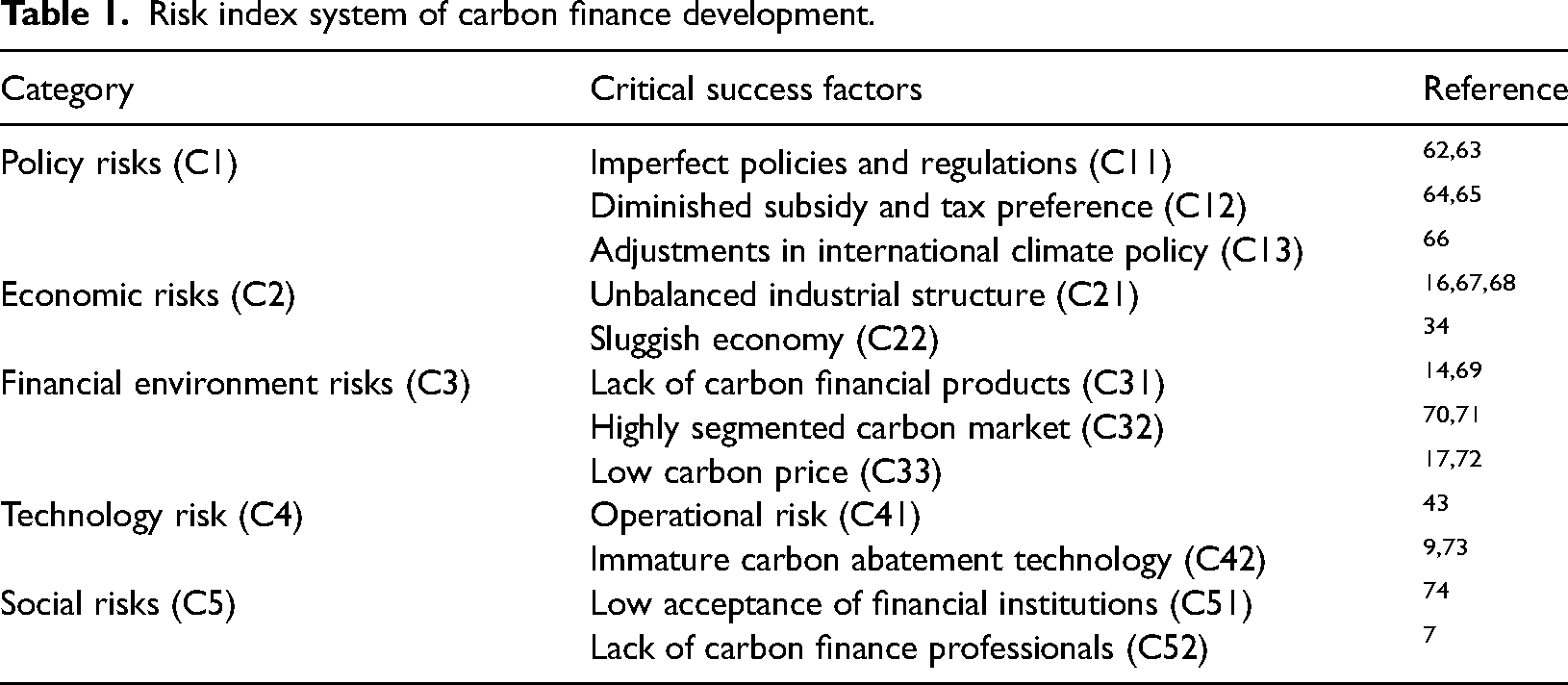

After analyzing the risk factors, this paper constructs a new index system that includes adjustments in international climate policy and highly segmented carbon market. In addition, 12 risks affecting the carbon finance development are identified and divided into five categories: policy, economic, financial environment, technology, and social (as described in Table 1).

Risk index system of carbon finance development.

Risks at the policy level

Imperfect policies and regulations (C11): Imperfect policies and regulations mainly refer to the lack of legal constraints and policy guarantees for carbon finance. For example, the government lacks punishment mechanisms for high-pollution enterprises. Inadequate environmental regulations will increase the levels of pollution. 75 Unclear attribution of responsibility will also hurt the quantity, price and structure of carbon finance. In addition, the lagging of relevant institutions and standards will reduce the activity of carbon finance. 7 Improving the top-level design is the premise of promoting the healthy development of carbon finance. 76

Diminished subsidy and tax preference (C12): On the one hand, due to the lack of effective risk compensation, tax reduction and other comprehensive supporting policies, financial institutions cannot avoid risks. Some financial institutions will be cautious about carbon finance and have to raise the threshold to cover business risks. On the other hand, enterprises are not willing to promote transition of low-carbon production without tax preference. 65 At the same time, the development of carbon market will be hampered because enterprises, financial institutions, and other participants lack incentives to meet consumer needs.

Adjustments in international climate policy (C13): Carbon finance markets are particularly susceptible to policy changes because they are policy-based and rely heavily on policy and regulatory constraints. Furthermore, the laws and regulations of different countries have a great effect on supply-demand in carbon market. 77 Many countries may change their policies at any time to maximize their interests, which expands the uncertainty of carbon finance development. In this case, financial institutions are required to be aware of any potential risks to international policy when engaging in carbon financial trading. As a result, they are hesitant to invest in carbon finance projects.

Risks at the economic level

Unbalanced industrial structure (C21): Industrial structure determines the carbon emissions. According to the three main industries, the higher proportion of the secondary industry, the more carbon emissions will be generated. This situation will aggravate pollution, which lead to a continuous reduction of social demand for CEA. In contrast, the expanding tertiary industry will increase the need for certification emission reduction, which contributes to carbon finance development. 16 Therefore, the higher proportion of the secondary industry will result in an unbalanced industrial structure that prevents the development of carbon finance.

Sluggish economy (C22): Investor expectations and confidence are affected when the real economy's growth slows, which leads to a decrease in investment. 78 Such bad signals could also reduce investor demand for CEA. The risk of economic slowdown will cause a long bear market, which have an impact on regular operation of carbon finance market.

Risks at the financial environment level

Lack of carbon financial products (C31): Carbon financial products can be divided into trading instruments, financing instruments, and support instruments. Intermediate services are also included, such as account management for customers and credit enhancement services. The abundant products will expand the scope of financial services, 14 which provide a guarantee for the increasingly active carbon finance.

Highly segmented carbon market (C32): International carbon finance markets are governed by different governments, so there are great differences in policy standards and price levels. Both parties in the market need to pay huge transaction costs, 71 which increases their risk. The rising efficiency of the whole carbon finance market requires the establishment of effective linkages between different markets. 70

Low carbon price (C33): Carbon market is regarded as a good policy instrument for promoting carbon finance development. 16 A fair price of CEA can mirror the marginal abatement cost and provide accurate price signals for low carbon enterprises. It can also motivate enterprises and residents to improve the development and application of carbon abatement technology. If carbon price keeps going down, the enterprises are reluctant to reduce emissions, 17 which is bad for the long-term stability of the carbon market.

Risks at the technology level

Operational risk (C41): Carbon finance business is more complex and difficult to operate than other businesses. As the basic assets of carbon financial trading, CEA is a kind of virtual electronic certificate and only exists in the registration system. Operational risks in carbon finance markets can lead to quota theft and reuse, such as human errors, system loopholes, and faults in the registration system. This risk will spread rapidly in a short time, resulting in significant economic losses. 79

Immature carbon abatement technology (C42): Carbon finance must depend on carbon abatement technology. 73 Numerous energy-saving and emission-reduction technologies are still in the pilot phase. It is more difficult to accurately assess the prospect of a commercial application under uncertain prospects of technical advancement. The risk of loans for low-carbon technological enterprises and the profit of associated technological projects are both indirectly influenced by the uncertainty of technology. These factors will have an impact on how carbon finance develops.

Risks at the social level

Low acceptance of financial institutions (C51): At present, only a few large banks have focused on carbon finance, while some small financial institutions pay less attention to it. A lack of financial institution participation will raise transaction costs for enterprises and discourage additional businesses from participating, 74 which makes it harder for them to form a trading relationship.

Lack of carbon finance professionals (C52): Carbon finance is a new emerging field. Governments, intermediaries, financial institutions, and other subjects participating in carbon financial market still lack sufficient response ability in risk identification and management. 80 The lack of a significant number of professionals will lead to operational risks caused by improper operation, which is irreparably damaged.

Methodology

Description of improved DEMATEL

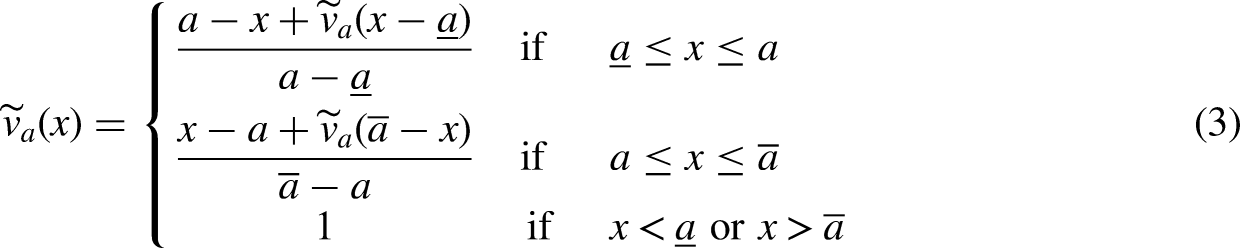

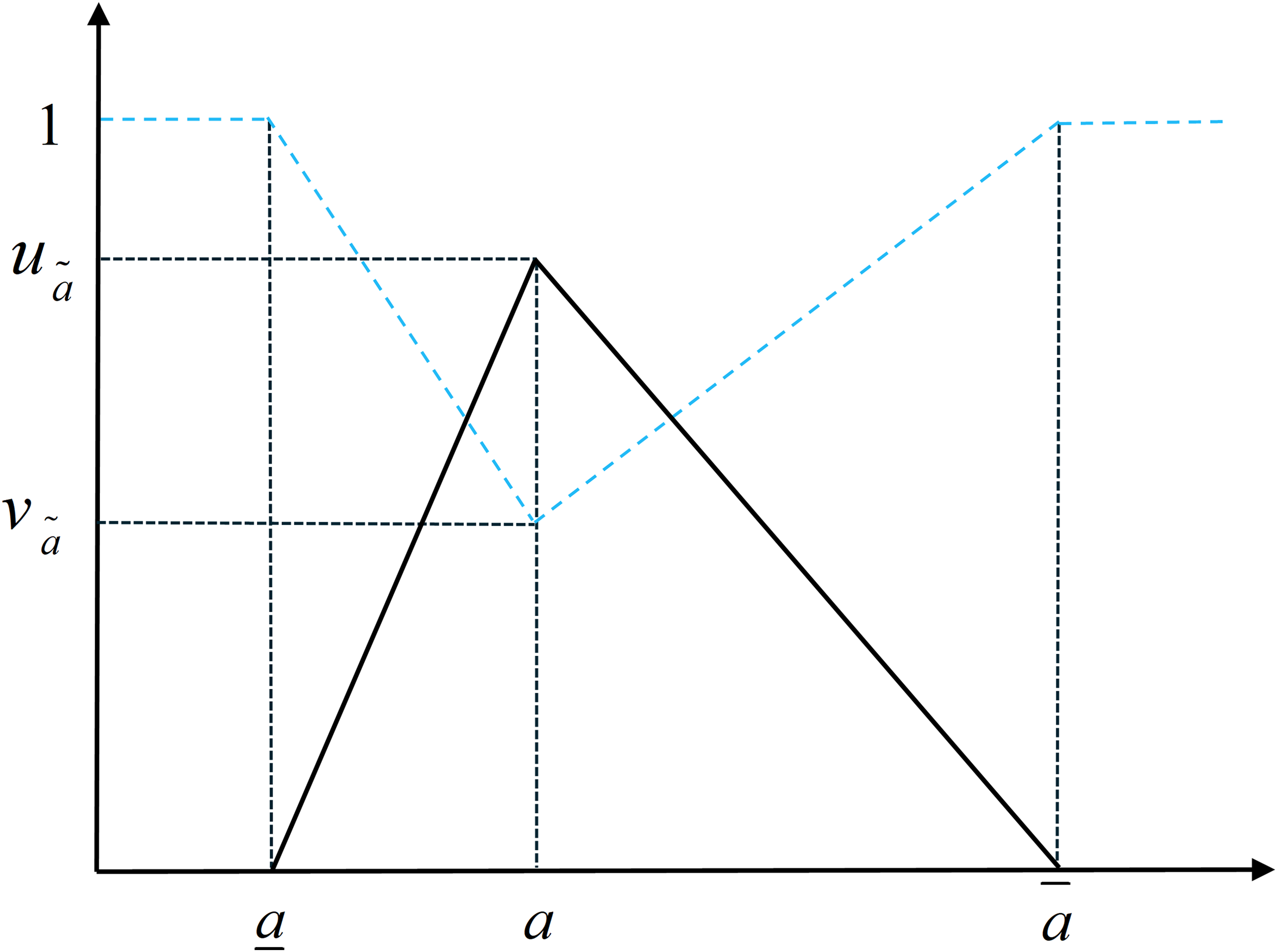

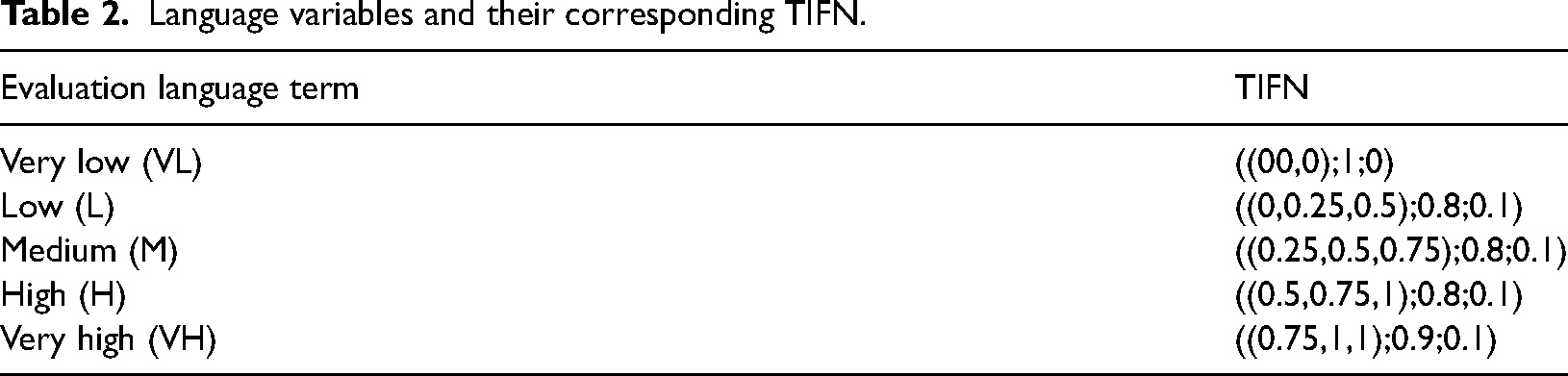

The first step of DEMATEL is to assess the mutual influence between the risks. For the input data of the analysis, the influence extent between different risks is assessed by expert evaluation. The traditional DEMATEL uses scores 1 to 9 to obtain the calculable value for evaluation, where the higher scores indicate the higher influence extent. Considering the inherent ambiguity of human thinking while making subjective evaluations, it is hard for experts to choose an exact numerical value to describe research object. Therefore, this paper collects expert evaluation information based on HFLTS, and quantifies the qualitative evaluation into calculable values by TIFN. HFLTS allows experts to use multiple evaluation languages to express their opinions, which is close to human decision-making custom. TIFN contains more decision information than a single real number, which can reduce the information loss of qualitative information during quantization. This can effectively address the uncertainty and ambiguity of objects caused by subjective decisions of experts and increase reliability of evaluation results. Furthermore, K-means is employed to overcome arbitrariness when defining the interrelationships between comprehensive factors in traditional DEMATEL. In summary, the study presents the improved DEMATEL method, which is carried out as below.

An expert committee is formed and each expert is invited to evaluate influence extent between risk factors. Experts can use multiple evaluation languages to express their views, where VL, L, M, H, and VH indicate five classes of the degree of influence between risk indicators. To further demonstrate the level of confidence in the mind of the expert when giving different evaluation languages, this paper improves the reliability of individual language words by adding a probability measure to each unit of the HFLTS. The probability of HFLTS is shown in equation (1).

Triangular intuitionistic fuzzy number.

Language variables and their corresponding TIFN.

According to the quantitative rules, HFLTS could be aggregated and transformed as TIFNs, shown as equation (8). And then, TIFN could be defuzzified through equation (9).

Determining risk factors

Then the cluster is developed on the elements in

Description of ISM method

ISM is a method for system analysis with a complex hierarchy and influencing factors. Based on the analysis result from DEMATEL method, ISM method is chosen to divide the risk into corresponding hierarchies, which benefits the deeper analysis of risk factors affecting the development of Chinese carbon finance. The analysis steps based on ISM can be shown as follows:

Research framework

The risk factors affecting carbon finance development in China form a complex system. The research framework of the paper consists of four parts, as shown in Figure 3. (1) Risk identification. Through literature collection and expert consultation, 12 risk factors are determined from policy, economy, financial environment, technology, and society five aspects. (2) Information collection. Considering the hesitation of expert decision-making and avoiding information loss in the process of qualitative transformation, the improved HFLTS is used to collect expert evaluation information and TIFN is used to quantify the expert evaluation linguistics. (3) Quantification of the relationship between risk factors. DEMATEL is utilized to calculate the comprehensive influence between risk factors and K-means is utilized to deal with the subjectivity of determination in traditional thresholds. After calculating the reachability matrix, ISM is used to visualize the risk levels. (4) Development suggestions. Based on the analysis results from above steps, the paper put forward corresponding risk management and control recommendations to the government, financial institutions, and enterprises.

Risk analysis framework of developing carbon finance.

Application of the proposed framework

Case study

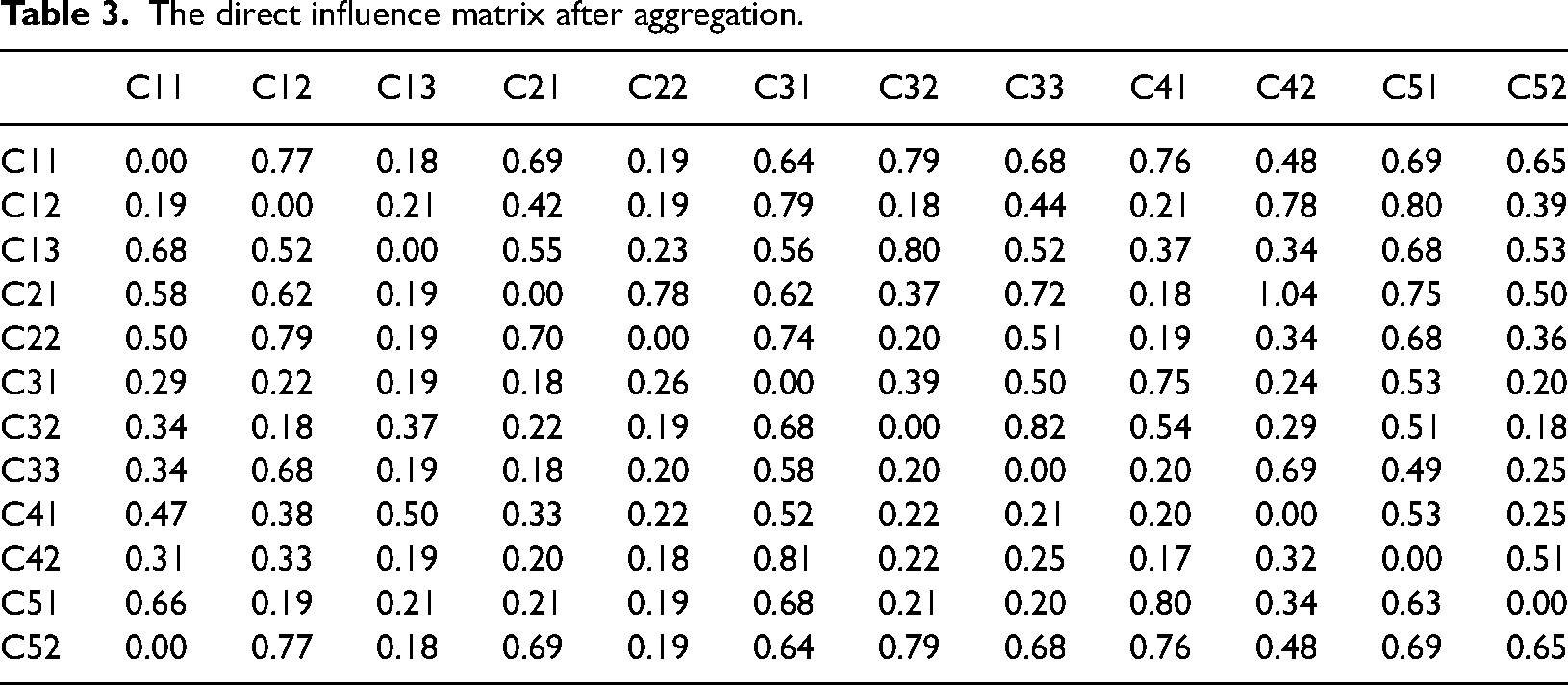

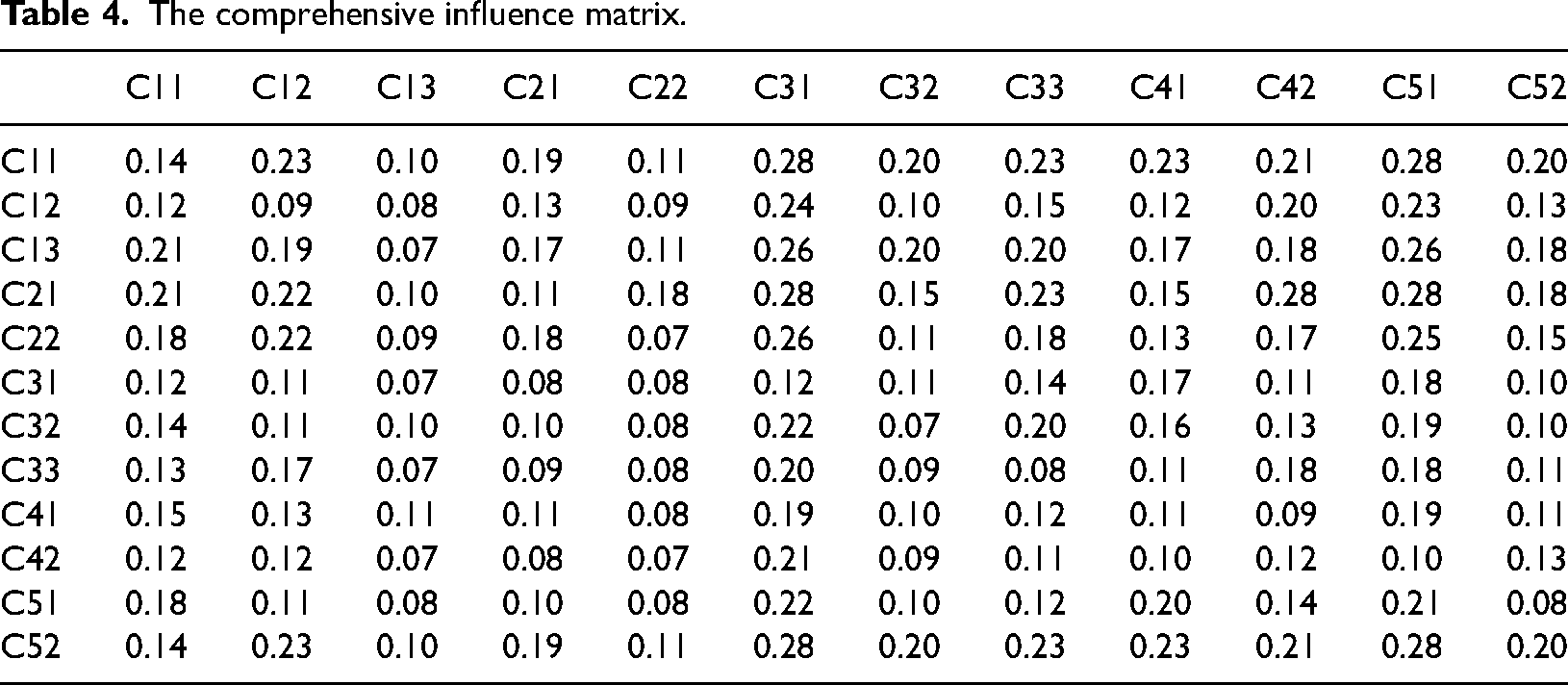

This chapter will analyze the risks of carbon finance development in China through the research framework mentioned above. Firstly, collecting and processing the basic information for risk analysis of carbon finance development, which is obtained by setting up an expert committee and inviting experts to make subjective judgments on the influence relationship of risk factors. The expert committee is composed of five experts from universities, enterprises, financial institutions, carbon emission trading centers, and financial regulatory departments. Specific composition and division of labor can be seen in Appendix A (Table A.1). Then, a questionnaire is designed and distributed to experts, who are invited to answer the questions in the questionnaire to obtain the basic information of risk analysis for carbon finance development, as shown in Appendix A (Figure A.1). In the process of measuring the influence degree among risk factors, improved HFLTS is applied to collect information, which avoids the negative influence from expert's hesitation on reliability of evaluation results. Due to the limitation of space, the expert decision can be shown in Appendix A (Table A.2). Considering the qualitative information cannot be calculated directly, the linguistic evaluations given by experts are quantified through TIFN. Then, they are aggregated and defuzzified through corresponding rules, and all experts are given equal weight. The aggregated direct influence matrix and the calculated comprehensive influence matrix are shown in Tables 3 and 4, respectively.

The direct influence matrix after aggregation.

The comprehensive influence matrix.

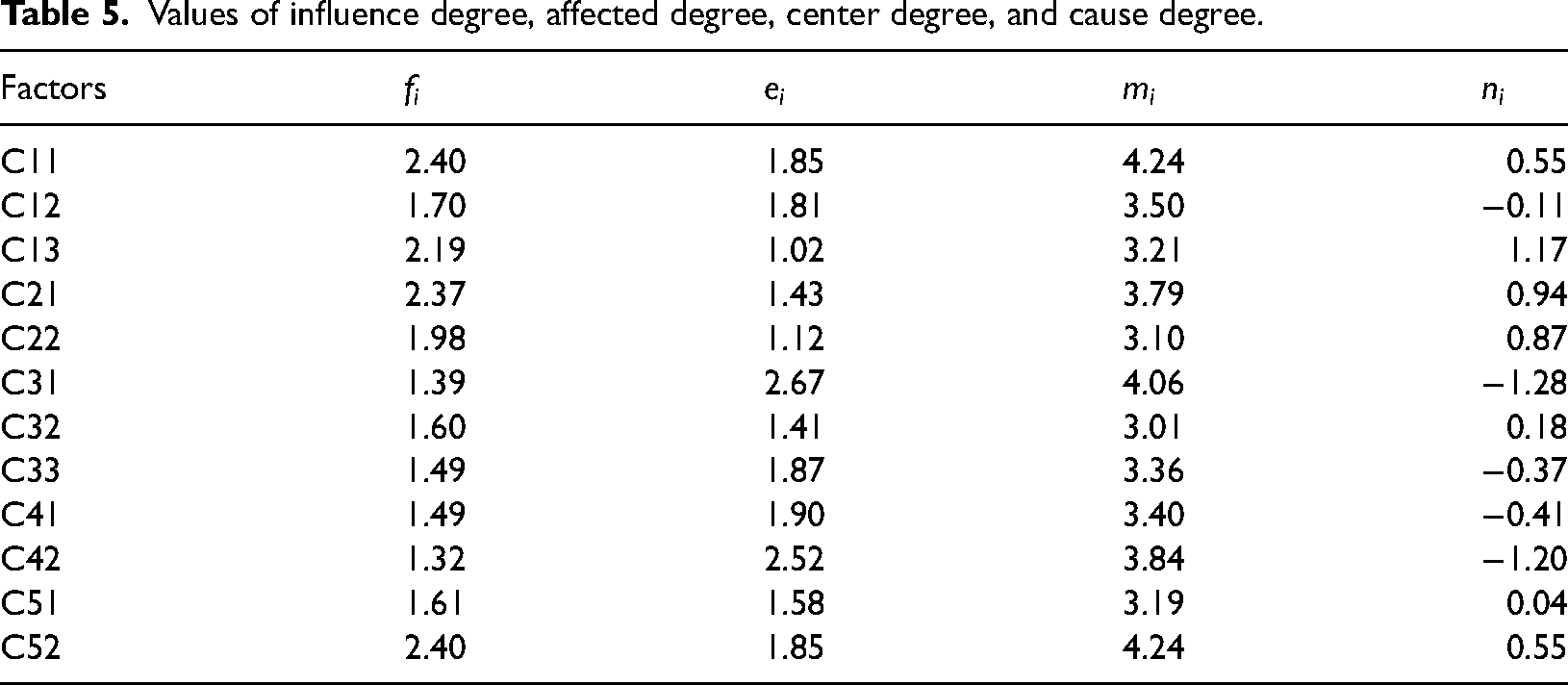

Following the steps of DEMATEL, the influence degree, affected degree, center degree, and cause degree of each factor in the risk index system of carbon finance development can be calculated through equation (21) to equation (24), as shown in Table 5.

Values of influence degree, affected degree, center degree, and cause degree.

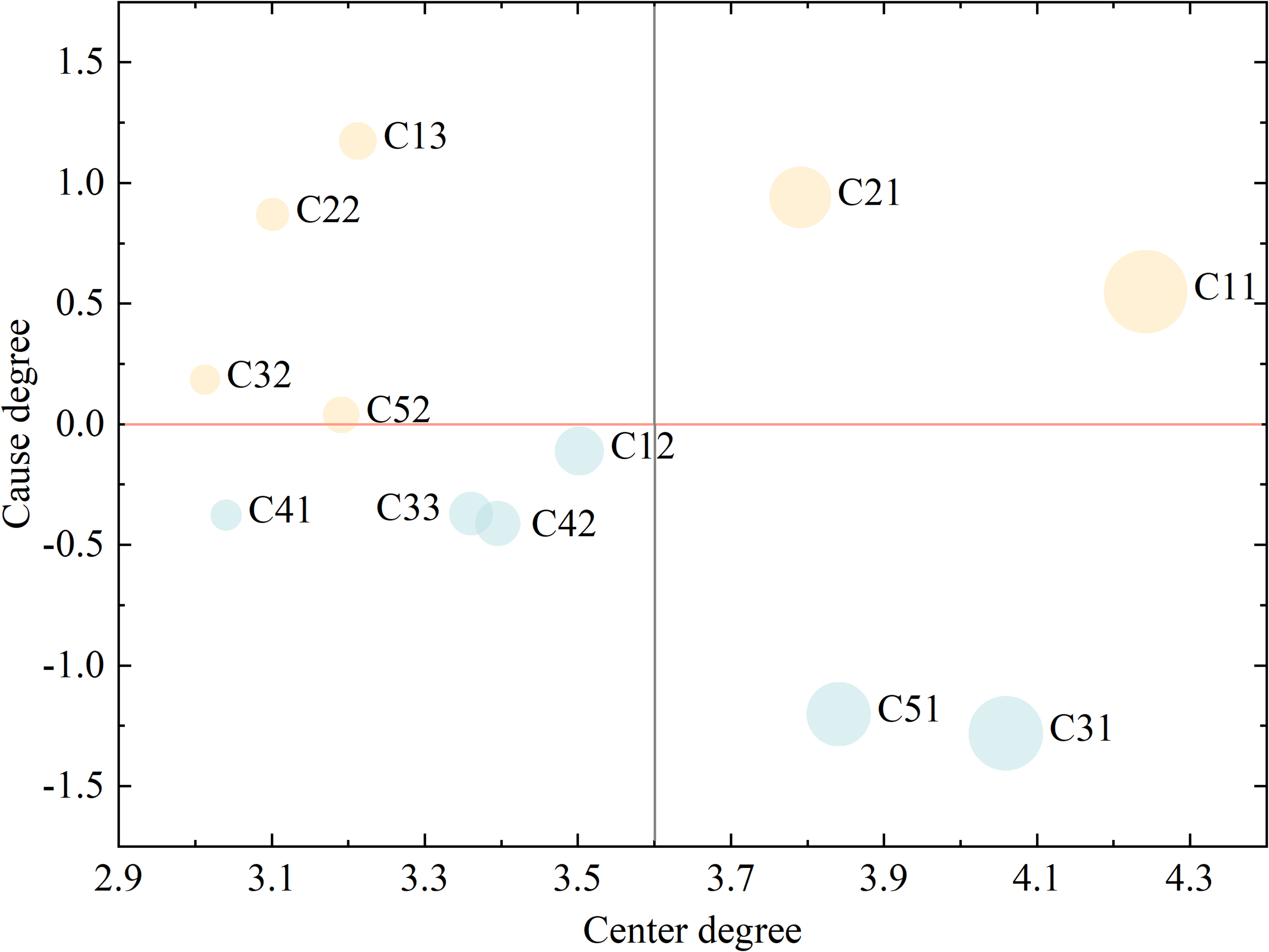

Then, the cause-and-effect diagram of risk factors of carbon finance development is drawn as seen in Figure 4. The bubble size and color indicate the centrality and positive/negative degree of the factor respectively. The positive one belongs to the cause factor and is colored in orange. The negative ones are the outcome factors, shown in blue. Imperfect policies and regulations (C11), unbalanced industrial structure (C21), lack of carbon financial products (C31) and low acceptance of financial institutions (C51) are the important factors affecting carbon finance development. Adjustments in international climate policy (C13), imperfect policies and regulations (C11), unbalanced industrial structure (C21), sluggish economy (C22), highly segmented carbon market (C32), and lack of carbon finance professionals (C52) are cause factors, which means these factors affect both carbon finance development and other factors. It is worth noting that C11 is both important and influential. Perfect policies and regulations can help the carbon finance market perform the important function of price discovery and risk management. Therefore, the combination of government-led with financial institutions and enterprises cooperating would promote carbon finance development and activate financial qualities of carbon market.

The center–cause degree for risk factors.

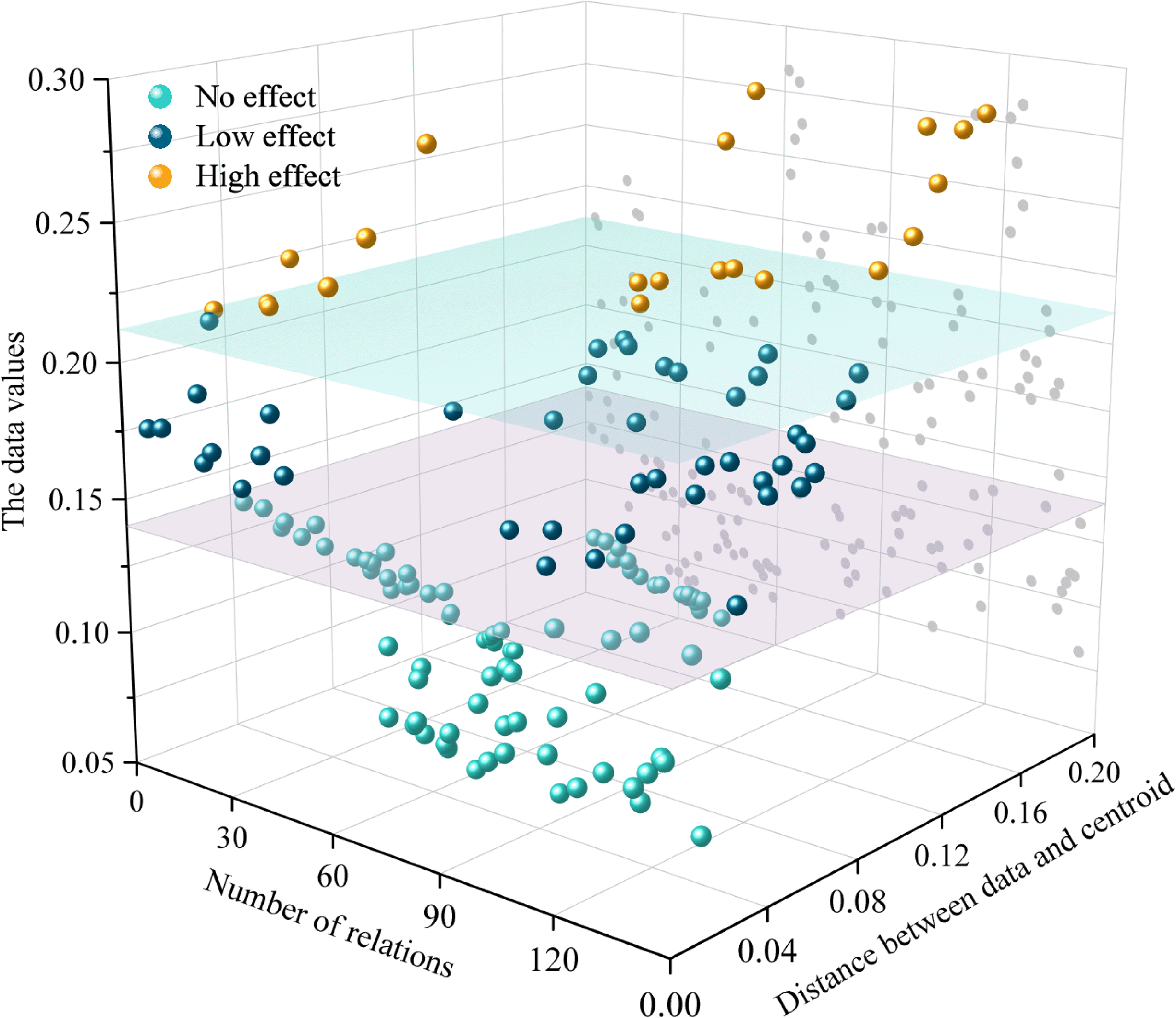

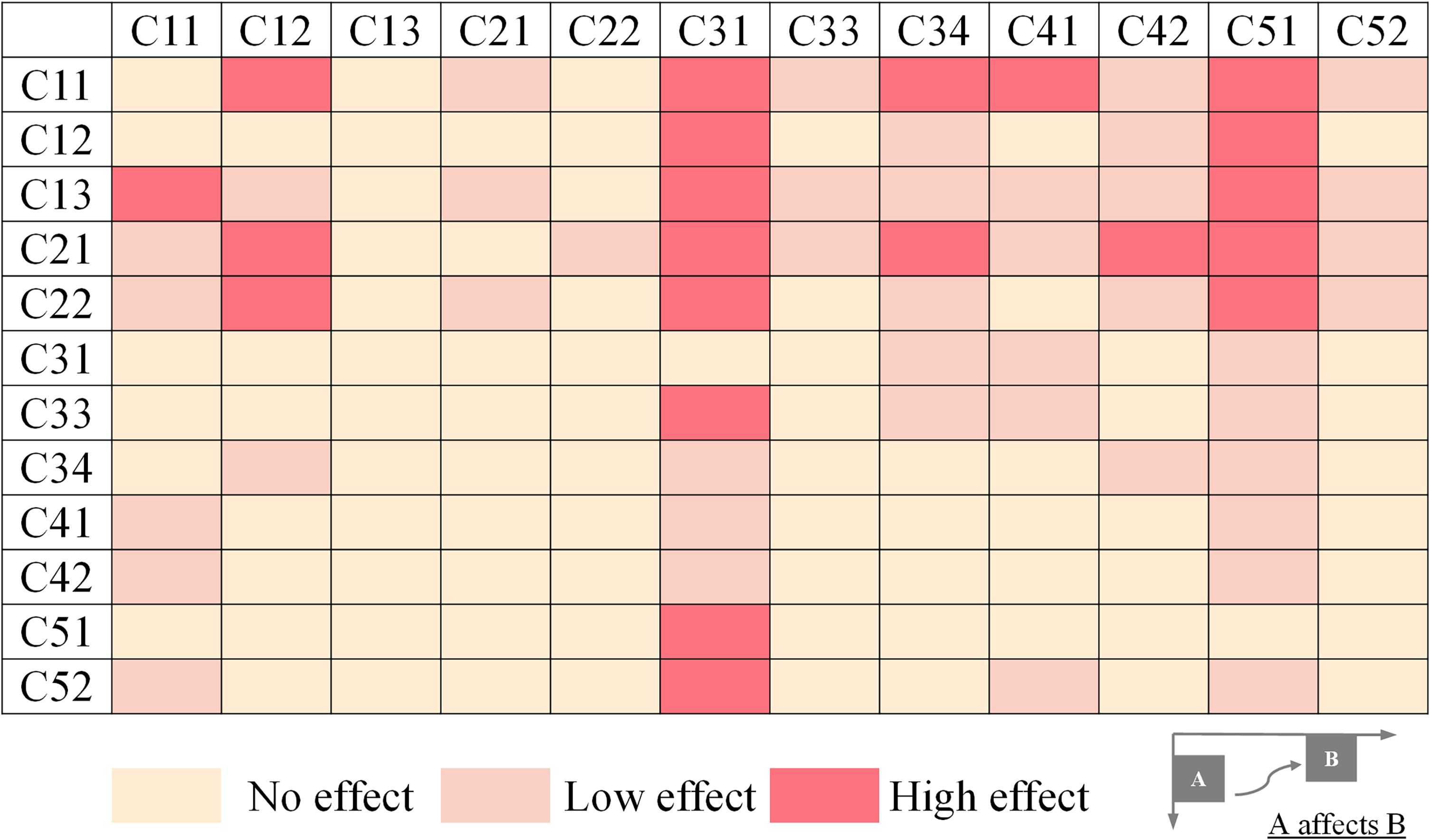

The traditional DEMATEL analyzes the mutual relationship between risk factors through threshold setting, which is based on subjective judgment. K-means is more objective and reliable, and the influence between factors can be extended to high effect, low effect and no effect, which provides more scenarios and inspirations for decision-makers to formulate strategies. Figure 5 shows the clustering results of influence relationship between various risk factors. In particular, the threshold value between “no effect” and “low effect” is 0.14, and between “low effect” and “high effect” is 0.212. Figure 6 shows the detailed influence relationship of 12 risk factors based on the classification threshold (vertical axis factors affecting the horizontal axis factors). Rosy red represents a high effect, light pink represents a low effect, and light orange represents no effect. It is observed that the three risks of C31, C34, C41, and C42 do not affect other risk factors. C31 is sensitive and affected by many risks.

Determining the threshold by the K-means.

The mutual relationship between risk factors.

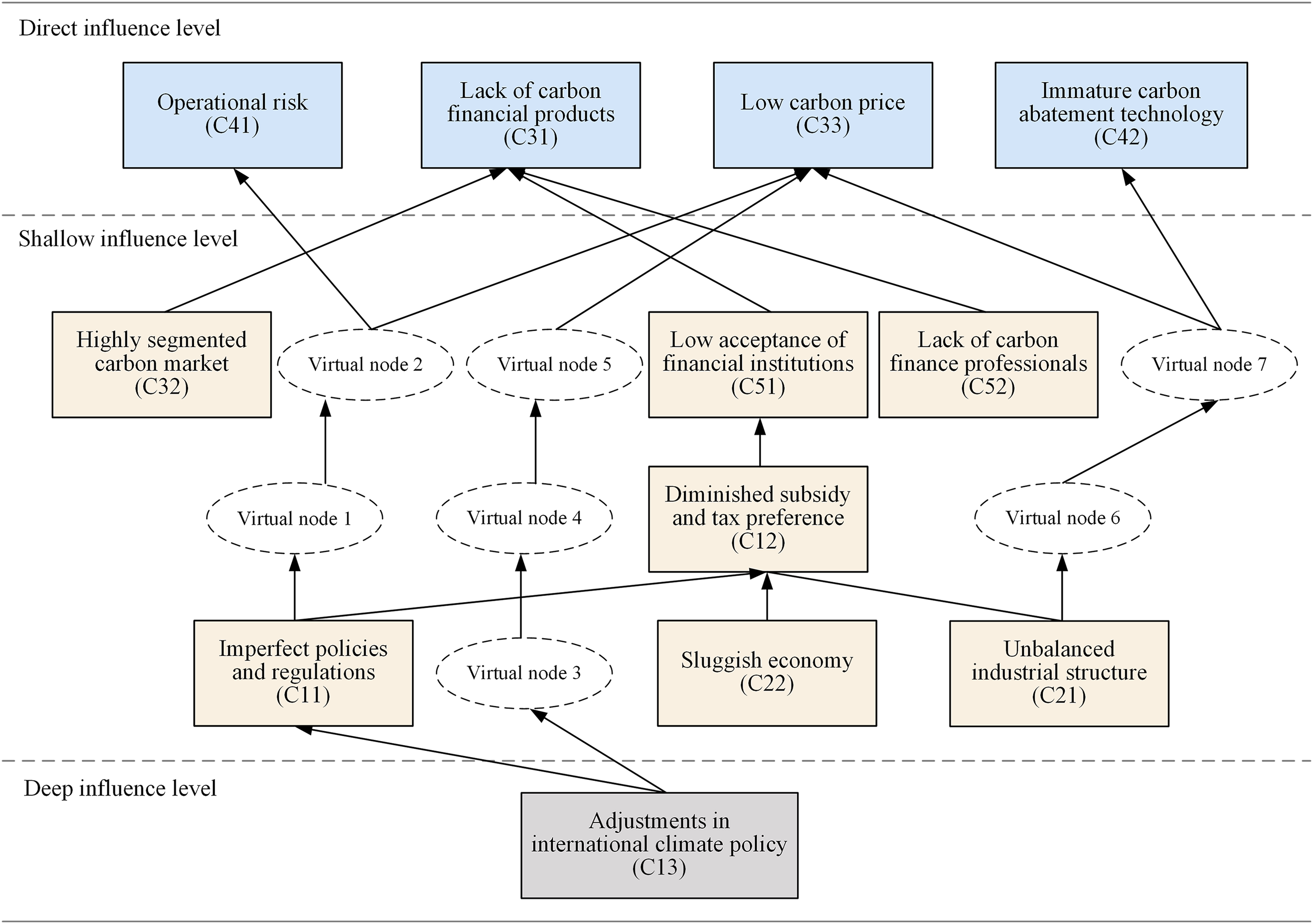

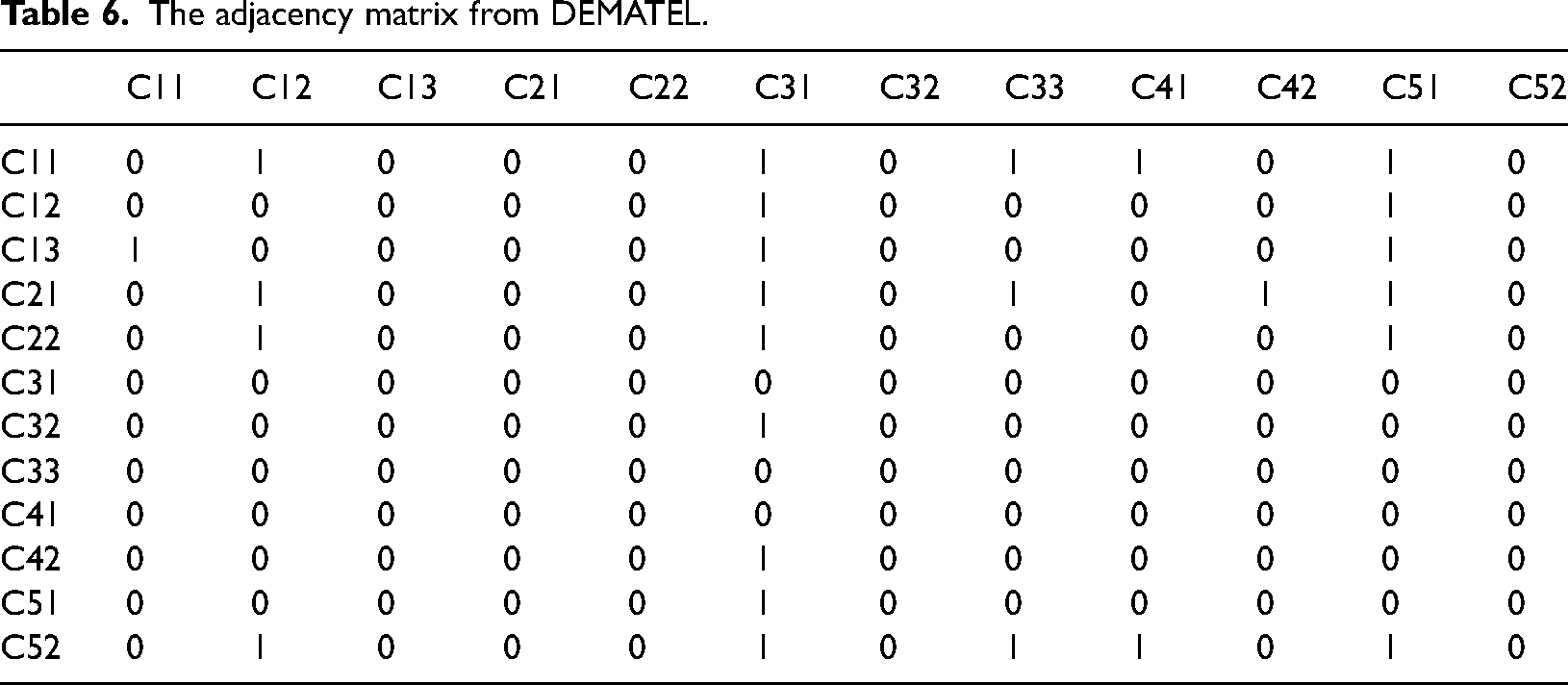

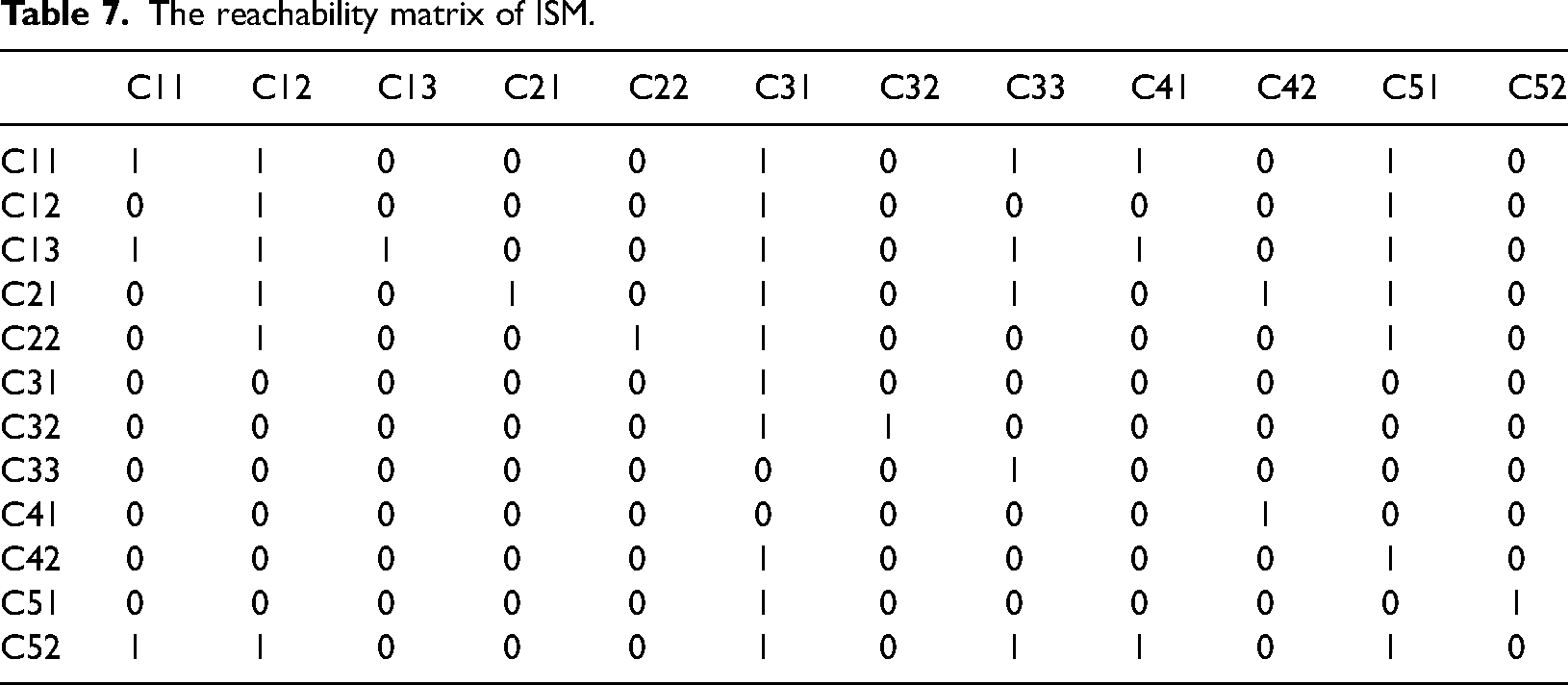

The calculated adjacency matrix and reachability matrix are shown in Tables 6 and 7. Then, risk factors are finally divided into five levels by equations (27–29). The detailed hierarchical division results are

Hierarchical diagram of risks to carbon finance development in China.

The adjacency matrix from DEMATEL.

The reachability matrix of ISM.

The ISM model can reflect the hierarchical structure and mutual influence relationship of risk factors, and the structure is improved by adding virtual nodes in order to obtain a more ideal hierarchy. Virtual nodes mean that there is no such factor in the system and can be regarded as the image of related nodes. In Figure 7, virtual nodes 1 and virtual nodes 2 (the image of C11) are added to adjust the cross-layer influence relationship of C11, C31, C33, and C41; virtual nodes 3, 4, and 5 (the image of C13) are added to adjust the cross-layer influence relationship of C13, C33, and C41; virtual nodes 6 and 7 (the image of C21) are added to adjust the cross-layer influence relationship of C21, C33, and C42. The arrow line connecting the two factors indicates that there is a relationship between them. Therefore, the following findings can be obtained.

The factors of direct influence include risk of low carbon price, immature carbon abatement technology, lack of carbon financial products, and operational risk. They are the direct risk factors affecting carbon finance development, where the previous two are indicators of benefits and costs. The cost of carbon abatement technology will decrease as it becomes more advanced, which will motivate more social funds to invest in its widespread application. At the same time, investors might see enormous profit margins as CEA price rises, which attracts many people to participate and makes greater carbon finance market liquidity. Furthermore, the progress of carbon financial products will affect feasibility of financial institutions providing carbon financial services. More products will help them better assist enterprises in revitalizing carbon assets, expand financing channels for green projects, and reduce financing costs for enterprises. Compared with other transactions, the trading of carbon financial products is more complex, human error or other operational risks in the trading system will cause carbon financial system breakdown. The factors of shallow influence include imperfect policies and regulations, diminished subsidy and tax preference, highly segmented carbon market, low acceptance of financial institutions, lack of carbon finance professionals, unbalanced industrial structure, and sluggish economy, all of which act on the direct influence factors. The creation of carbon financial products is closely related to a link among carbon markets, finance professionals, and the acceptance of financial institutions. The subsidy and tax preference encourage green projects to be financed, which will increase the confidence of institutions to start carbon financial services. Strengthening supervision and management of financial institutions through the formulation of regulations is important in preventing operational risks. The policies and regulations include not only the regulatory systems for carbon finance, but also the institutional systems related to carbon market. If there is no design mechanism, the carbon price will lack a foundation logic to sustain the relationship with the carbon market, making it challenging for carbon price to accurately feedback on the real situation of the market. The unbalanced industrial structure will inhibit the demonstration effect of low-carbon policies. Investors and enterprises are unable to realize the importance of green transformation, which will reduce their investment in low-carbon programs and affect carbon prices. Accelerating industrial restructuring will drive carbon abatement technology advances. Moreover, the factors like unbalanced industrial structure, sluggish economy, imperfect policies, and regulation will also reduce subsidy and tax preference. The deep influence factor is adjustments in international climate policy. Carbon finance is the financial activity resulting from the change in international climate policy. Adjustments in international climate policy will lead to unclear trading prospects of carbon market, which would affect the overall trend of CEA prices. In addition, international regulations will affect the interactive communication between the state and the international system. The sense of constraint and urgency caused by the gap between domestic reality and future trends will affect the formulation of domestic policies and regulations.

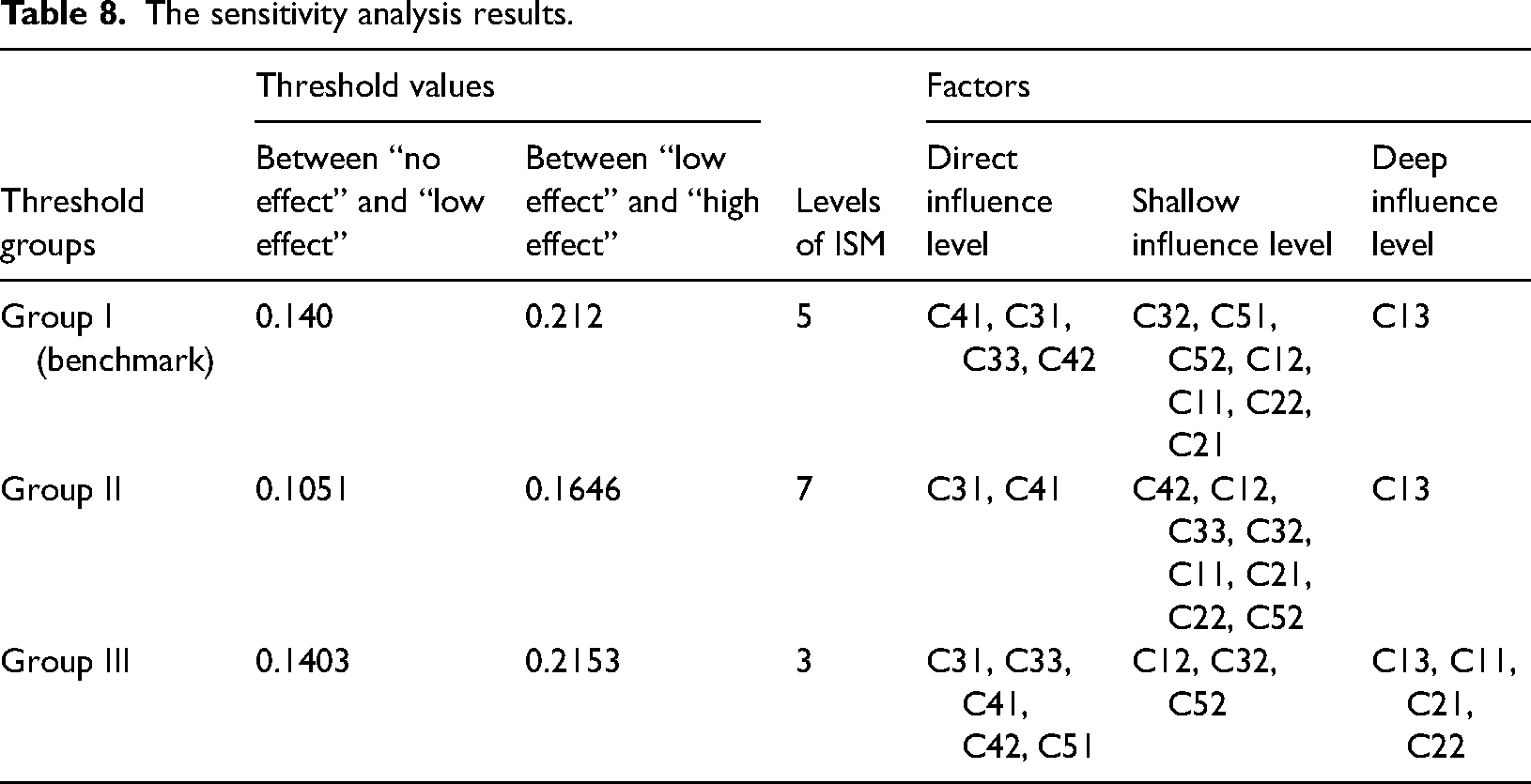

In order to verify the stability of analysis result, a sensitivity analysis is carried out. The sensitivity analysis is developed by changing the thresholds classification in K-means in DEMATEL method, where the K-means cluster algorithm is carried out 30 times, and the three stable groups of thresholds are obtained for classifying the influence factors into three layers. Table 8 presents the result for sensitive analyses, where group I is the threshold used for this paper.

The sensitivity analysis results.

According to Table 8, the hierarchical classification of risk factors of carbon finance development is not consistent under different thresholds. But it does not affect the direct, shallow, and deep influence factors, which are obtained based on the ISM method. In addition, Table 8 also shows that C13 is always the deep influence factor, and the direct influence factors are also mainly composed of C31, C33, C41, and so on. The identification results of the risk factors obtained with different thresholds are consistent with the results of this paper, which indicates the result has good stability. Although the influence factors of each level are not completely consistent under different thresholds, the overall changes are not significant, which validates that the model constructed in this paper has robustness.

Solutions and management implications

In order to realize the closed-loop management of risk factors in carbon finance development, there is a need to seek solutions after completing risk identification and analysis. Therefore, combining identified risk factors and survey results, this paper provides the following recommendations for carbon finance development. It will be beneficial for carbon finance participants to carry out corresponding risk control measures on time. In general, carbon finance participants include trading parties, third-party intermediaries, and government. Trading parties refer to emission reduction project owners, emission control enterprises, financial institution investors, and individual investors. Third-party intermediaries refer to carbon emission verification agencies and other institutions providing related consulting services.

For imperfect policies and regulations: On a legal level, the legislative process of carbon market construction should be completed as quickly as possible. For instance, clarification of the nature and legal obligations of carbon emission rights is required. At a regulation level, it is necessary to unify carbon financial market regulation, trading system, impelling-binding mechanism, accounting, and tax treatment.

For diminished subsidy and tax preference: By implementing a special support plan of discount interest and guarantee, the government can evoke the enthusiasm of financial institutions to participate in carbon finance market. Additionally, emission reduction project owners, emission control enterprises, and financial institutions can integrate their carbon finance initiatives with rural revitalization strategies to receive individual support.

For adjustments in international climate policy: The government ought to actively align with international rules, including improving measures to address climate change following international policies. Financial institution investors and emission control enterprises should establish basic management guidelines based on a set of international norms. In addition, third-party intermediaries must design targeted industrial policies for environmentally sensitive enterprises, and fulfill their social obligations in carbon finance development.

For unbalanced industrial structure: First of all, it is important to adjust environmental regulation policy. For example, the government should eliminate some high-carbon enterprises and strictly control their loans from financial institutions. Secondly, the government should promote growth of the tertiary industry to realize its full functions in energy conservation and carbon abatement. Finally, the government has to support new low-carbon enterprises, such as new energy, energy conservation, and environmental protection enterprises. The increasing proportion of low-carbon industries in the secondary industry can form a circular and green industrial ecosystem.

For sluggish economy: Enhance economic endogenous power. The financial sector should actively provide loans to enterprise owners to assist them in restarting operations. The government should advance the reform of income distribution system and rural revitalization to raise incomes of low-income groups, which will increase effective consumption.

For lack of carbon financial products: Financial institution investors and third-party intermediaries should broaden the scope of traditional carbon financial products. Financial products created by financial institutions should complement each other and form their characteristics to achieve the serialization of carbon financial products. Then, provide more basic support for the product. On the one hand, financial institutions should gather data continually and improve fundamental conditions to develop new carbon financial products. On the other hand, the government can enact incentives and ease market access to stimulate vitality of carbon market. Cooperation between the government, trading parties and third-party intermediaries also needs to be strengthened to match the products with its market basis.

For highly segmented carbon market: The critical condition of forming carbon market links is their development relatively mature. Therefore, the government should improve relevant supporting measures to accelerate the carbon market development. In addition, concerning the successful experience of links between international carbon markets, the government can make a trial in some pilot markets. In the future, different “Belt and Road” carbon market links and cooperation strategies should be gradually explored.

For low carbon price: In order to control market expectations and reduce the imbalance of carbon prices, it is suggested that the government improve quota allocation and introduce offset mechanisms. For example, by creating a carbon quota reserve pool, an open market operation mechanism can be established to form a reasonable carbon price. The price limit mechanism can also be set to limit the percentage of the maximum daily decline and enhance carbon price regulation.

For operational risk: It can be considered to carry out the supervision during the whole process of carbon financial trading. By strengthening the registration requirements and audit of market participants, the possibility of non-compliance operations from the source would be lessened. Meanwhile, the functions of the registration and trading system can be strengthened to guarantee stability and security. Enterprises could implement digital transformation strategies to impelled deep convergence of digital technology and carbon finance. 81 Using fintech to replace relevant operators can partly reduce problems such as trading errors.

For immature carbon abatement technology: On the one hand, the government could improve the preferential taxes on industries that develop carbon abatement technology, and stipulate that commercial banks grant preferential credit to related projects. On the other hand, a platform for promoting and applying achievements could be established to accelerate the spread and use of technology. On this basis, encouraging domestic enterprises to collaborate and participate in international exchanges and promoting knowledge sharing and cooperation in solving problems of carbon abatement technology.

For low acceptance for financial institutions: To encourage financial institutions to invest in carbon finance, the government should actively develop support tools for carbon emission reduction. For example, financial institutions can be provided with targeted preferential financing interest rates and special re-loans. Meanwhile, the preferential policies in terms of capital adequacy ratio and required deposit reserve can be considered. In addition, the government could improve the definition and supporting measures of information standards, such as emission reduction verification. Financial institution investors and individual investors can timely and accurately obtain effective information about carbon assets.

For lack of carbon finance professionals: The participant should increase training input and cooperate with authoritative institutions. It can enhance the supervision, service, and verification capabilities of carbon finance market practitioners. Meanwhile, the government also needs to improve the treatment and formulate a set of systematic professional regulations for carbon emission managers, which can construct a strong talent base to boost carbon finance.

Conclusion

Leveraging carbon finance for carbon peaking and carbon neutrality is one of the important ways, but its development in China is in the initial stage now. Therefore, it is crucial to determine the risk factors in carbon finance development. In order to support high-quality development of carbon finance, the study establishes a comprehensive research framework. Firstly, 12 risk factors affecting carbon finance development are identified from five aspects of policy, economy, environment, technology, and society. Secondly, the improved DEMATEL-ISM is used in risk analysis under fuzzy environment. Then, significant risks are identified according to mutual relationship and hierarchical diagram from the analysis. Lastly, the suggestions are put forward from three perspectives of trading parties, third-party intermediaries, and government, which inspire to help the stakeholders control the risks and promote carbon finance.

To sum up, the findings of research are shown as: (1) Factors as low carbon price, immature carbon abatement technology, lack of carbon financial products, and operational risk have a direct influence on carbon finance development; (2) Factors as imperfect policies and regulations, diminished subsidy and tax preference, highly segmented carbon market, low acceptance of financial institutions, lack of carbon finance professionals, unbalanced industrial structure and sluggish economy are important risks for carbon finance developing; (3) Factor as adjustments in international climate policy is the most fundamental risk influencing the development of carbon finance. The study has presented a complete framework including identification, analysis, and solution for risk factors of carbon finance development in China. The contribution of the article can be summarized as (1) The proposed risk index system of carbon finance development can be used as a reference for researchers of carbon finance; (2) The proposed methods and framework of risk analysis can provide methodological and modeling support for risk management; (3) The proposed suggestions on risk control of carbon finance development can provide reference for the trading parties, third-party intermediaries, and government.

However, there are still some limitations in the paper because of the authors’ practical experience. On the one hand, the risk identification in the study of carbon finance development is not absolutely comprehensive, which could be adjusted appropriately according to actual demand. On the other hand, the collection and processing of decision information under fuzzy environment can increase data utilization and integrity, but it is still unable to guarantee that there is a non-loss of information. In the future, we will consider introducing big data technology or higher-order fuzzy numbers to enhance the objectiveness and comprehensiveness of risk analysis. Moreover, risk analysis of carbon finance could be extended to other world economies for a deeper understanding of the issue.

Footnotes

Abbreviations

Author contributions

Yuanxin Liu: conceptualization, methodology, writing-original draft. Xu Luo: data processing, writing-review. Shuo He: grammar revision. Jiahai Yuan: resources, supervision. Yao Tao: software, data processing.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.