Abstract

Given the tourism sector's considerable environmental impact and economic relevance, assessing environmental sustainability is important. This is particularly relevant given the commitments established in the UN 2030 Agenda for Sustainable Development. A sample of 147 firms from 39 countries and Refinitiv data accessed via LSEG Workspace were used to construct an index of material environmental disclosure based on Sustainability Accounting Standards Board standards. Using a Generalized Method of Moments approach, we find that environmental disclosure is positively associated with market capitalization, with a stronger relationship observed in common law jurisdictions. These findings underscore the value of managerial proactivity in adopting materiality-based sustainability disclosures and highlight the role of regulatory initiatives in fostering such practices, which may strengthen investor confidence and enhance firm value.

Introduction

Sustainability has become a major corporate concern. Companies face growing pressure to adopt and report sustainable practices. 1 Sustainable development is now central to business and society following the adoption of the United Nations 2030 Agenda and its 17 Sustainable Development Goals (SDGs). 2

Sustainable development encompasses environmental, social, and governance (ESG) dimensions across sectors. 3 However, sustainability is particularly relevant to the tourism sector due to its economic importance, environmental impact, and connection to the 2030 Agenda, as explicitly mentioned in several SDGs (e.g. SDG 8, 12, and 14). 4 According to the World Travel and Tourism Council, 5 despite the difficulties resulting from the COVID-19 pandemic, the tourism sector is expected to contribute a record 11.7 trillion USD to the global GDP in 2025, representing 10.3% of the global GDP. However, this economic contribution has significant environmental impacts. For instance, global tourism's carbon footprint reached approximately 5.2 gigatons of CO2-equivalent in a year, accounting for approximately 8.8% of global greenhouse gas emissions if direct and indirect impacts are considered. 6

Businesses are increasingly accounting for their social and environmental impacts. Consequently, they must publish sustainability reports detailing environmental and social actions and policies. 7 Sustainability reports enable investors to make more objective and informed investment decisions by identifying companies with a positive impact aligned with social and environmental values.8–10

The Sustainability Accounting Standards Board (SASB) metrics provide a standardized framework for voluntary disclosure of material sustainability risks and opportunities with potential financial impact. Consolidations in the standard-setting landscape strengthened SASB's role as a reference framework through its integration into the Value Reporting Foundation and subsequent consolidation under the IFRS Foundation's sustainability initiatives, reflecting investor demand for consistent, financially material disclosure frameworks. 11 Material information increases the price informativeness of ratings, whereas immaterial information has no financial impact. 12 These standards align corporate reporting with shareholder expectations, regarding long-term financial performance and sustainability-related risks and opportunities. 12 SASB standards provide a transparency tool for tourism companies to signal sustainability commitments, attract responsible investors, 13 and support informed shareholder decision-making. 14

The regulatory landscape for environmental sustainability reporting is shifting rapidly from voluntary to mandatory disclosure. This shift is evident in major markets such as the United States and the European Union, where initiatives such as the Securities and Exchange Commission's (SEC) climate-related disclosure rules and the EU's Corporate Sustainability Reporting Directive (CSRD) aim to harmonize reporting standards. 15 The recent adoption of the European Sustainability Reporting Standards (ESRS) presents both challenges and opportunities. According to De Villiers et al., 16 integrating standardized reporting frameworks, particularly SASB standards, reflects a broader policy-driven push toward harmonized environmental disclosure. Recent empirical studies on renewable energy, green technology, and carbon-neutral pathways emphasize that credible environmental disclosure and technological innovation are essential mechanisms for advancing the SDGs and achieving long-term climate targets.17,18 While the SASB has long been recognized for its investor-focused approach to material sustainability disclosures, its incorporation into the International Sustainability Standards Board (ISSB) framework underscores the regulatory push for globally consistent and comparable sustainability reporting. These public policies reinforce the importance of material environmental disclosures as a key factor influencing market valuation and investor decision-making. 19 They also allow tourism companies to demonstrate sustainability leadership and enhance competitiveness among environmentally conscious consumers. 20

Empirical evidence21–23 suggests that corporate financial performance and firm value may be positively influenced by a company's environmental performance, particularly when the environmental issues are material. The relationship between financial performance and environmental reporting has also been observed in the tourism sector24–27; however, the role of materiality in this context has received limited attention, with existing research focusing only on investment decisions and specific subsectors.28, 29

A country's institutional context may significantly affect the impact of environmental disclosures on firm performance. The legal origin of a firm's headquarters country can lead to significant organizational differences, as laws and external pressures shape corporate decision-making processes. 30 Some studies highlight that firms in common law jurisdictions tend to exhibit higher performance and market valuation than those in civil law countries because of enhanced investor protection and corporate governance structures.31–33

First, this study focuses on the tourism sector as an environmentally intensive industry, characterized by substantial natural resource use, high levels of energy and water consumption, and contribution to environmental externalities (e.g. water and energy use, waste generation, and ecological footprint).34–36 Recent bibliometric research further highlights the prominence of environmental concerns in tourism ESG literature, given the sector's intensive natural resource use and stakeholder pressure for environmental transparency.37,38 By focusing on a single environmentally intensive industry and a cross-country firm-level sample, we provide evidence of how capital markets process material environmental information, thereby enhancing the interpretability and practical relevance of sustainability disclosures for investors, managers, and policymakers.

Second, we examine the relationship between material environmental issues and firms’ market capitalization in the tourism sector, where the role of materiality has been largely overlooked. Although the SASB materiality map was designed to help investors identify financial material sustainability issues, 39 its effectiveness in guiding market valuation in the tourism sector remains insufficiently tested. Most of the literature concentrates on the theoretical development of materiality,40,41 with limited empirical evidence on whether these guidelines improve investors’ evaluation of company's environmental and market value. By constructing an SASB-aligned measure that captures the environmental issues most financially relevant for tourism firms, our study advances both the measurement and empirical understanding of material environmental disclosures. Our analysis also contributes to the emerging strand of sustainability accounting research that emphasizes the importance of sector-specific materiality assessments over generic ESG disclosures.42,43 Consistent with recent findings highlighting the need for firms to adopt structured processes and frameworks, such as SASB, to enhance ESG transparency, 44 our study provides empirical evidence that sector-specific approaches can improve the materiality and clarity of sustainability disclosures, thereby reinforcing the call for additional research on SASB implementation. Third, we offer novel evidence of the institutional conditions that shape the value relevance of material environmental information by examining the moderating effect of a country's legal origin (common law vs. civil law). To the best of our knowledge, this moderating effect has not been explored in tourism or in other sectors.

To achieve these objectives, we analyze an unbalanced panel of 147 publicly listed tourism firms from 39 countries over 2012–2023 (1340 firm-year observations). The empirical analysis uses dynamic panel data models estimated via two-step difference GMM. The results yield implications for academia, managers, and policymakers.

Literature review and hypotheses development

Prioritizing shareholders aligns with shareholder primacy theory, which holds that a firm's primary responsibility is to maximize shareholder value. 45 However, this view has been subject to criticism in recent years, because an exclusive focus on shareholders may neglect other interests and overlook environmental and social externalities.46,47 In this context, adopting standards, such as SASB metrics helps balance shareholder value maximization and corporate ESG responsibility. 48

Signaling theory 49 suggests that companies use public disclosures to signal quality and strategy to investors. Voluntary disclosures can signal firms' quality and attract investment; firms with strong ESG performance are more inclined to disclose trustworthy information to investors.50,51 Thus, the information asymmetry between a company and its investors is reduced. 52 This underscores the importance of accurate and transparent communication to reduce misinterpretation, strengthen investor confidence, and ultimately enhance market capitalization. 53

Recent empirical advances employing Fourier-based, asymmetric, and AI-augmented methods indicate that environmental outcomes respond nonlinearly to financial and low-carbon energy investments and that positive and negative shocks to low-carbon technology and energy investment can have asymmetric effects on sustainability metrics.18,54,55 These findings support the view that disaggregated material sustainability disclosures, such as SASB metrics, provide higher-quality signals of future environmental risks and transition opportunities, thereby affecting market valuation.

According to institutional theory,56,57 companies adopt practices and structures considered legitimate within their social and regulatory environments. Organizations adapt to laws and norms and seek legitimacy through the institutional environment. In particular, being located in a common law or civil law country may influence the expectations placed on businesses and, consequently, their ability to earn legitimacy within their institutional environment. 58

SASB standards disclosure and firms’ market capitalization

Growing interest in sustainability and the integration of ESG factors into corporate reporting are widely recognized as drivers of financial performance and market valuation. Key challenges in the tourism sector, such as elevated energy and water consumption, and habitat destruction, require strategies to achieve sustainable tourism. 59 Thus, this sector, characterized by its significantly negative environmental impact,34,35,60 is increasingly being scrutinized by investors, policymakers, and the general public.

It is imperative for companies to disclose information about environmental issues to ensure transparency and accountability. 61 This may result in higher sustainability rankings and positive responses from capital markets. 62 Eccles et al. 63 suggest that strong sustainability reporting helps firms manage long-term risks valued by investors. García et al. 64 find that environmental performance influences the financial risk of tourism firms, showing that adopting sustainable environmental practices is crucial for financial stability. By providing relevant and transparent sustainability information, companies can increase investors’ trust and improve market valuation and reputation.65,66 Clear and consistent reporting of material ESG factors mitigates information asymmetry between firms and investors, as well as among investors. 67 In the tourism sector, Ionescu et al. 68 find a positive correlation between ESG performance and the company's market value, affirming the importance of the environmental sustainability score. Prior studies also support the positive impact of environmental reporting on tourism firm performance.24–2769

Recent empirical studies show that low-carbon energy consumption, energy R&D, and related investments influence environmental quality in complex and often non-linear ways.70,71 These results suggest that market responses to environmental disclosure depend not only on disclosure quality but also on the underlying dynamic and asymmetric relationships between energy investments, technology diffusion, and environmental outcomes. Therefore, material SASB disclosures that reveal these exposures and strategies can enhance investors’ assessments of long-term value.

As investors demand reliable and comparable sustainability information with clear links to financial performance, SASB identifies a subset of sustainability issues likely to be material to investors. Growth in financial accounting standards is an important element of capital market development and the efficient allocation of capital in an economy. 72 Materiality maps can help companies identify key sustainability-related business issues they should consider. 39 By voluntarily disclosing relevant information on material sustainability-related risks and opportunities, companies can reduce information asymmetries commonly found in financial markets. 12 This increased transparency facilitates consistent and objective decision-making by investors, contributing to more accurate valuation and higher market capitalization.73,74 Recent studies further show that disclosure of financially material environmental information is positively reflected in firms’ market valuation, whereas non-material ESG disclosures have limited impact.40,75

Thus, adopting these standards reflects alignment with social and environmental expectations and serves as a strategic tool to enhance competitiveness and attract long-term investments. According to Eng et al.,

22

reporting material issues under SASB standards enables companies to demonstrate sustainability commitments clearly, enhancing reputation and investor confidence. Carvajal and Nadeem

21

also find a positive relationship between sustainability reporting and firm performance; this association is stronger when sustainability disclosures are financially material, as defined by the SASB. Shen et al.

23

find that firms adopting and transparently reporting environmentally sustainable practices, particularly under SASB metrics, experience superior financial outcomes. These companies benefit from enhanced reputational capital, improved risk management, and increased investor confidence, contributing to higher market value. In this context, we hypothesize the following:

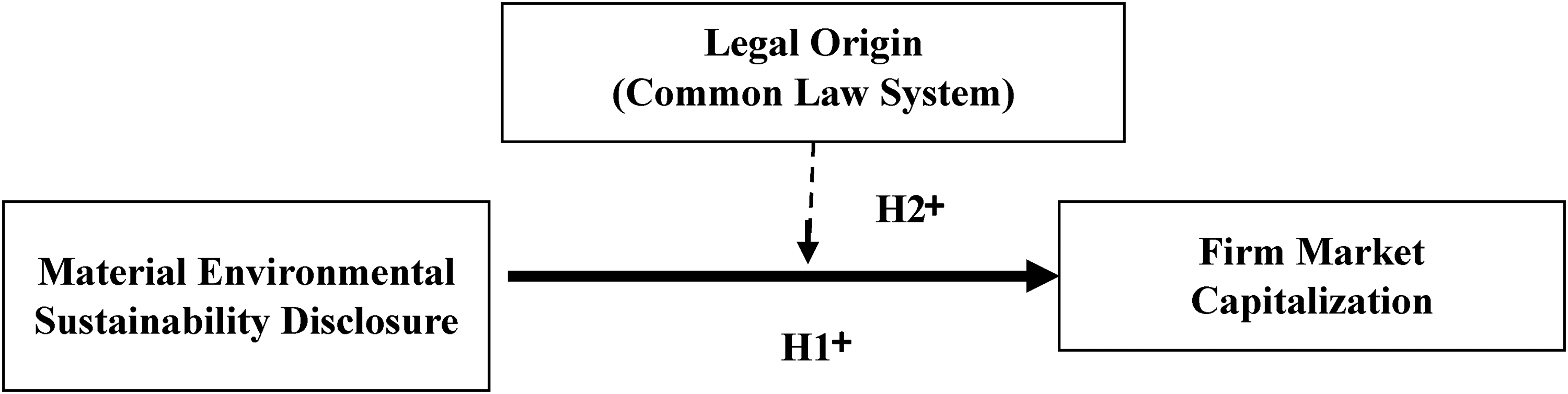

Hypothesis 1: The disclosure of material environmental issues by companies in the tourism sector positively impacts their market capitalization.

The moderating role of the common law legal system

The legal origin of a company's headquarters country can lead to significant organizational differences, as laws and external pressures shape corporate decision-making processes. 30 Political and legal systems play a critical role in shaping organizational strategies and activities, affecting sustainability goals and performance. 76 The effectiveness of sustainability disclosures varies across jurisdictions, due to differences in legal and institutional contexts. Previous studies have demonstrated that external contextual factors can moderate the relationship between corporate social responsibility and financial outcomes. 77 Specifically, countries with common law systems tend to exert less political influence on economic activities, allowing organizations to prioritize shareholders’ needs over the interests of other groups. 78 Recent evidence also shows that legal origin continues to shape firms’ disclosure environments, with institutional differences affecting transparency and investor information asymmetry. 79 Furthermore, common law systems feature more flexible, market-based governance mechanisms that facilitate stronger shareholder engagement. 33 In common law countries, where regulations and expectations concerning corporate transparency and sustainability are stricter and more oriented toward investors,58,80,81 companies may experience greater benefits in terms of market capitalization by disclosing material sustainability information following these standards.

Moreover, macro-level evidence on national pathways to net zero and the role of low-carbon technology and R&D suggests that institutional contexts that promote and finance low-carbon innovation amplify the economic relevance of environmental disclosures.54,71 Accordingly, the moderating effect of legal origin on the disclosure–valuation link may operate, in part, through cross-country differences in support for low-carbon technology and energy R&D, which affect how future environmental performance is priced by investors.

The mission of material sustainability disclosures, and particularly, SASB standards, is to help companies identify, manage, and disclose sustainability issues most relevant to investors, thereby facilitating informed decision-making aligned with investors’ interests. These standards are designed to provide greater transparency in key sustainability areas that directly impact firm value, making them appropriate in common law environments, where shareholder orientation and corporate transparency prevail.

Thus, institutional research suggests that common law legal origin is associated with higher disclosure levels because these jurisdictions often feature stronger investor protection and market-oriented governance. 82 Özcan 83 shows that companies in common law countries disclose more substantial sustainability information, reflecting stronger investor pressure and disclosure expectations.

Given the link between sustainability disclosures and financial performance, institutional context can strengthen these effects. Frías-Aceituno et al. 84 highlight that a country's legal system shapes corporate disclosure practices. Their findings indicate that stronger investor protection and market-driven governance in common law countries enhance disclosure relevance and impact. Recent cross-country evidence further shows that the performance implications of ESG-related corporate practices vary across legal and institutional environments. Huang et al. 85 document significant heterogeneity in these effects, suggesting that the legal context (civil law vs. common law) influences how sustainability-related information is reflected in firm performance and value. Moreover, firms with high-quality ESG reporting tend to experience more favorable market reactions, indicating that robust ESG disclosures can enhance firm valuation. 12 Khlif et al. 86 find that the relationship between environmental disclosure and corporate performance varies depending on the legal system. Their cross-country analysis shows that voluntary environmental disclosure has a significant positive effect on corporate performance only in common law countries. This suggests that firms in common law countries derive greater benefits from sustainability disclosures, possibly because of stronger institutional frameworks and higher investor expectations of transparency. This aligns with the broader argument that stronger investor protection and market-driven governance in common law countries enhance the credibility and financial relevance of voluntary disclosure.

Therefore, in common-law countries, the alignment between shareholder orientation and SASB standards leads to higher market valuations, as investors value disclosures that meet their transparency expectations. Hence, the following hypothesis is proposed:

Hypothesis 2: The positive impact of material environmental sustainability disclosures on firms’ market capitalization is stronger in countries with common law legal systems than in those with civil law legal systems.

The proposed model is shown in Figure 1.

Research model.

Methods

Sample, variables, and methodology

To test the proposed hypotheses, we analyzed listed companies in the tourism sector worldwide over the period 2012–2023. Refinitiv data accessed through LSEG Workspace were used to identify the sample and collect most of the information required to construct the variables. This database is frequently used in empirical studies on sustainability and firm performance due to its global coverage and accuracy.24,87–89 Tourism firms were also classified into three subsectors: hotels, restaurants, and leisure activities, aligned with prior literature.42,89

The sample includes companies listed in the tourism sector during the study period with available data on the dependent and independent variables. Because some companies entered and others exited the stock market during the study period, the sample comprised an unbalanced panel of 147 companies and 1,340 firm-year observations. Using an unbalanced panel avoids survivorship bias and ensures that the analysis captures both surviving and non-surviving firms, thereby increasing the representativeness of the results.90,91 The research period began in 2012, aligned with the development of the SASB standards. This coincides with SASB's first public launch of standard-setting activities, which provided a structured framework for assessing and reporting sustainability performance. The sample comprised firms from 39 countries worldwide, and firm observations were distributed throughout the study period.

Information on firm market capitalization and most control variables was obtained from the Refinitiv data accessed through LSEG Workspace. Data on tourist arrivals by country and year were obtained from The World Tourism Organization, and country populations were obtained from the World Bank. Firms were classified according to the legal system of the country in which they are headquartered, distinguishing between common law and civil law systems, as commonly used in the literature.58,92

Measures

Dependent variable

The dependent variable is firms’ market capitalization (MARKET_CAPITALIZATION), expressed in euros and measured as the natural logarithm of the market value of equity. This represents the sum of the market values across all relevant issue-level share types. The issue-level market value is calculated by multiplying the requested share types by the latest closing price. This approach aligns with prior studies that explore how firms’ sustainability reporting activities impact their market capitalization.93,94

Independent variable

The independent variable is the disclosure of information on material environmental matters (MAT_ENV_DISCLOSURE). We conducted a mapping exercise between the environmental standards outlined by the SASB and the ESG environmental indicators provided by the Refinitiv data accessed through LSEG Workspace. This mapping was guided by the principle of materiality, ensuring that only the most relevant environmental factors were considered for each subsector, namely hotels, restaurants, and leisure activities. These indicators are designed to provide material and decision-useful information to investors while remaining cost-effective for reporting companies. They are different for each subsector. Thus, there were 8, 11, and 3 environmental materiality indicators according to SASB for hotels, restaurants, and leisure activities, respectively. From those indicators, we manually identified 5, 6, and 2, respectively, available in Refinitiv. Companies were scored based on the proportion of indicators relevant to the respective subsectors on which they provided information. Focusing on material sustainability aspects improves alignment between SASB standards and available ESG data, enhancing evaluation precision for each tourism subsector. Therefore, for each firm-year, we scored whether the matched indicators were disclosed or not. The final variable is the proportion of material SASB indicators disclosed by each firm, yielding a subsector-specific materiality-based disclosure measure. Compared to existing approaches in the literature, which typically use broad ESG environmental scores, simple disclosure counts, or PCA-based indices, our SASB-aligned measure explicitly focuses on material environmental topics for each tourism subsector. This approach aligns with prior studies that have also employed mapping between the SASB standards and different sustainability indicators to enhance corporate environmental performance assessment.95,96

Moderating variable

The legal origin of the country (LEGAL_ORIGIN) was defined as a dummy, taking the value of 1 if the company's headquarters was located in a country with a common law legal system and 0 if the headquarters was in a country with a civil law system.97,98

Control variables

Six control variables were considered. The firm's age (AGE) is measured as the number of years between firm foundation and the reference year (2012–2023). Firm's size (SIZE) is measured by total consolidated revenue expressed in Euros. The AGE and SIZE variables were log-transformed for the analyses. Firm leverage (LEVERAGE) is measured as total borrowings reported by the company, including short- and long-term debt. Studies have highlighted the relevance of firm age, size, and leverage in sustainability, firm performance, and value-related research.99–101 Most studies report a significant and positive relationship between firm age, size and performance, probably because older and larger firms benefit from an established market presence and experience.102,103 Several studies find a negative relationship between firm leverage and performance, as higher debt levels can increase financial risk and constrain operational flexibility.104,105 However, some studies show a significant and positive relationship106–108 because debt can play a positive role in mitigating managerial-stockholder conflicts through bankruptcy supervision and bondholder monitoring. 109 The fourth control variable, INTERNATIONALIZATION, is defined as the percentage of total revenue generated from foreign sales. This variable captures the extent of a firm's international market presence and is commonly used to assess globalization and internationalization strategies. While some studies show that internationalization positively impacts firms’ market capitalization,110,111 others, such as Jung et al., 112 affirm that internationalization has a negative impact on restaurant firms’ market value.

A country-level control variable capturing tourism intensity (ARRIVALS) is included. It is measured as the number of international tourist arrivals per year divided by the country's total population. Previous studies have used this variable in the context of tourism. 113 The final control variable is an institutional variable (RULE_LAW), defined as an indicator capturing the quality of legal durable system of laws, institutions, norms, and community commitment that delivers four universal principles: accountability, just law, open government, and accessible and impartial justice. We include it to account for cross-country variations in institutional quality that may affect firms’ disclosure incentives, the enforcement of environmental regulations, and investors’ pricing of sustainability information. Prior studies show that national-level institutions shape corporate social and environmental behavior and materially influence firm valuation and financing outcomes.114,115

Finally, dummy variables are added to control for annual and subsector (hotels, restaurants, and leisure activities) effects.

Methodology

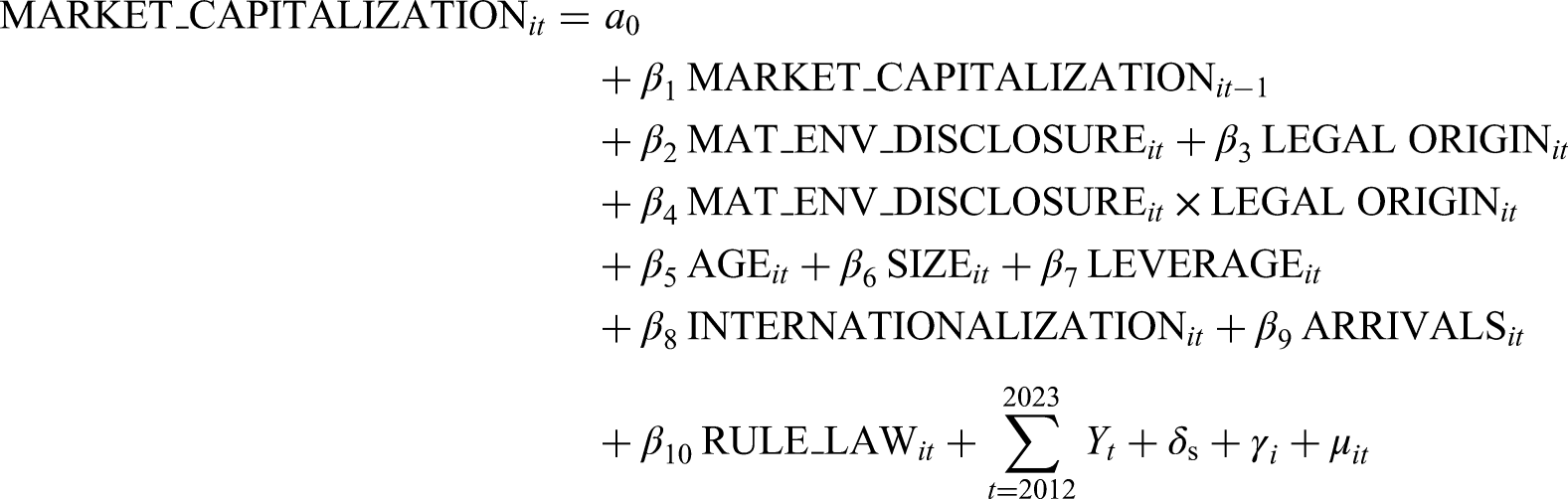

To test our hypotheses, we employ the two-step difference GMM estimator for dynamic panel data models developed by Arellano and Bond. 116 Dynamic panel data analysis is a more robust methodology that allows us to control for individual heterogeneity and unobservable individual effects by using first differences and addressing potential endogeneity. The GMM estimator uses internal instruments based on lagged values of explanatory variables to mitigate endogeneity concerns. (Our analysis reveals the presence of simultaneity or bidirectional causality between firms’ market capitalization and several control variables that capture their firm characteristics. One possible way to address this issue is to use instrumental variables (IV). However, identifying valid instruments is inherently challenging. As highlighted by Pindado and Requejo, 117 the main difficulty lies in selecting external instruments that are uncorrelated with the error term while still providing sufficient explanatory power for the endogenous regressors. Moreover, as Baum et al. 118 point out, although conventional IV estimators are consistent, they can become inefficient when heteroscedasticity is present.) All endogenous right-hand-side variables of the model were lagged from t − 1 to t − 3 for the equations in differences. An excessive number of lags may generate more instruments than firms or groups, potentially weakening the result reliability. However, we re-estimate the models using alternative lag structures, and the results do not vary significantly. We also consider the dependent variable lagged by one year as an explanatory variable in our model.

Therefore, the general dynamic panel data regression model used is as follows:

To test our hypotheses, we follow a hierarchical regression approach for moderation analysis. First, we include the control variables in Model 1. In Model 2, we consider the main explanatory variable along with the control variables. In Model 3, we add the moderating variable, and in Model 4, we include the interaction term between the main explanatory variable and the moderating variable.

Results

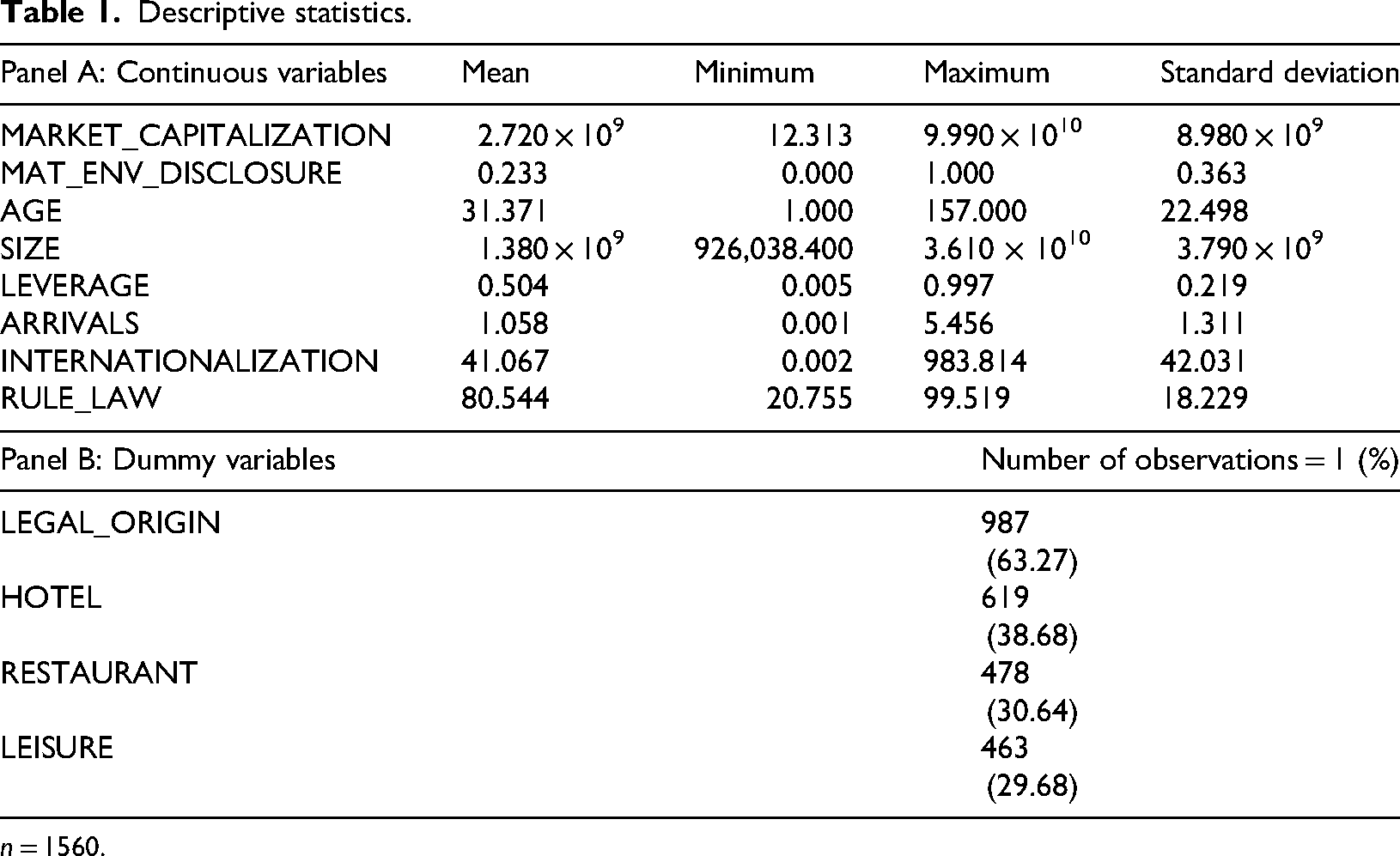

Table 1 reports descriptive statistics of the variables included in the analysis, offering insights into the distribution and scale of the data. The mean value of market capitalization is 2.72 × 109, with a minimum of 12.313 and a maximum of 9.99 × 1010. Similarly, MAT_ENV_DISCLOSURE, the proxy for material environmental sustainability disclosure, has a mean of 0.233 with a relatively large standard deviation of 0.363, indicating substantial heterogeneity in disclosure practices across the firms. The sample is dominated by firms in the hotel subsector, accounting for 38.68% of the observations, followed by restaurants (30.64%) and leisure activities (29.68%). The legal system variable indicates that 63.27% of the observations correspond to the civil law legal system and 36.73% to the common law legal system.

Descriptive statistics.

n = 1560.

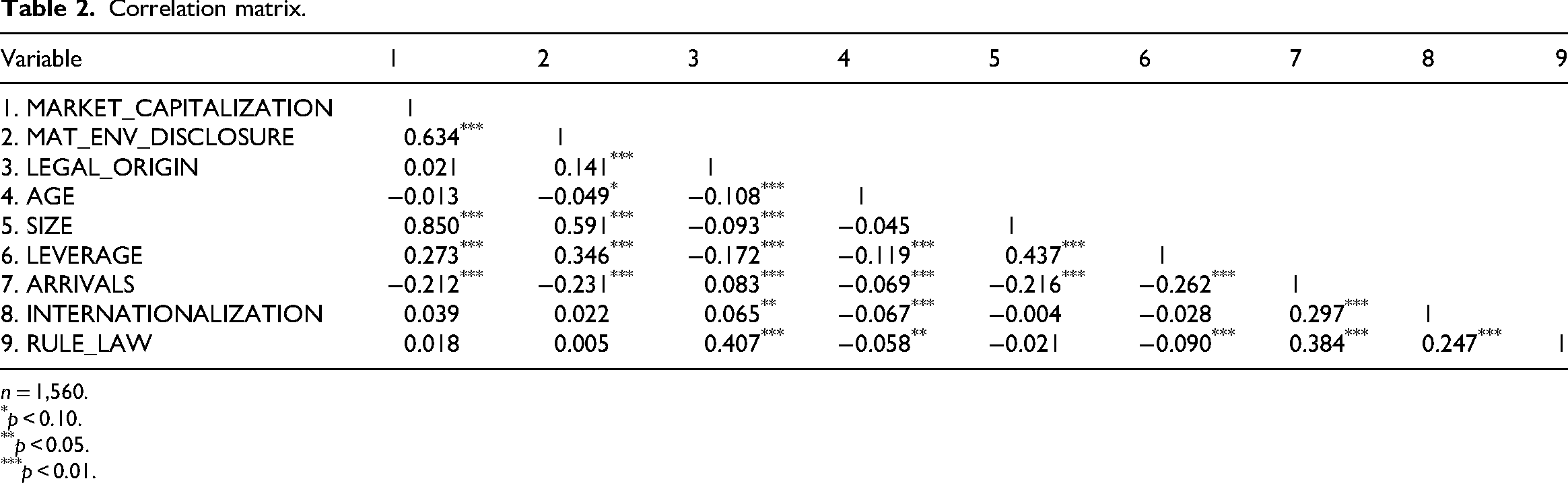

Table 2 presents the correlation matrix among the variables, providing preliminary evidence on variable relationships and potential multicollinearity. We used Spearman's correlations because Pearson correlations perform poorly with discrete or non-normal continuous variables,119,120 which was the case for some variables in this study. Nevertheless, variance inflation factors (VIF) did not show evidence of multicollinearity, as they were all below 10. 121 Notably, firms’ market capitalization exhibits a strong positive correlation with the main independent variable (0.634, p < 0.01).

Correlation matrix.

n = 1,560.

p < 0.10.

p < 0.05.

p < 0.01.

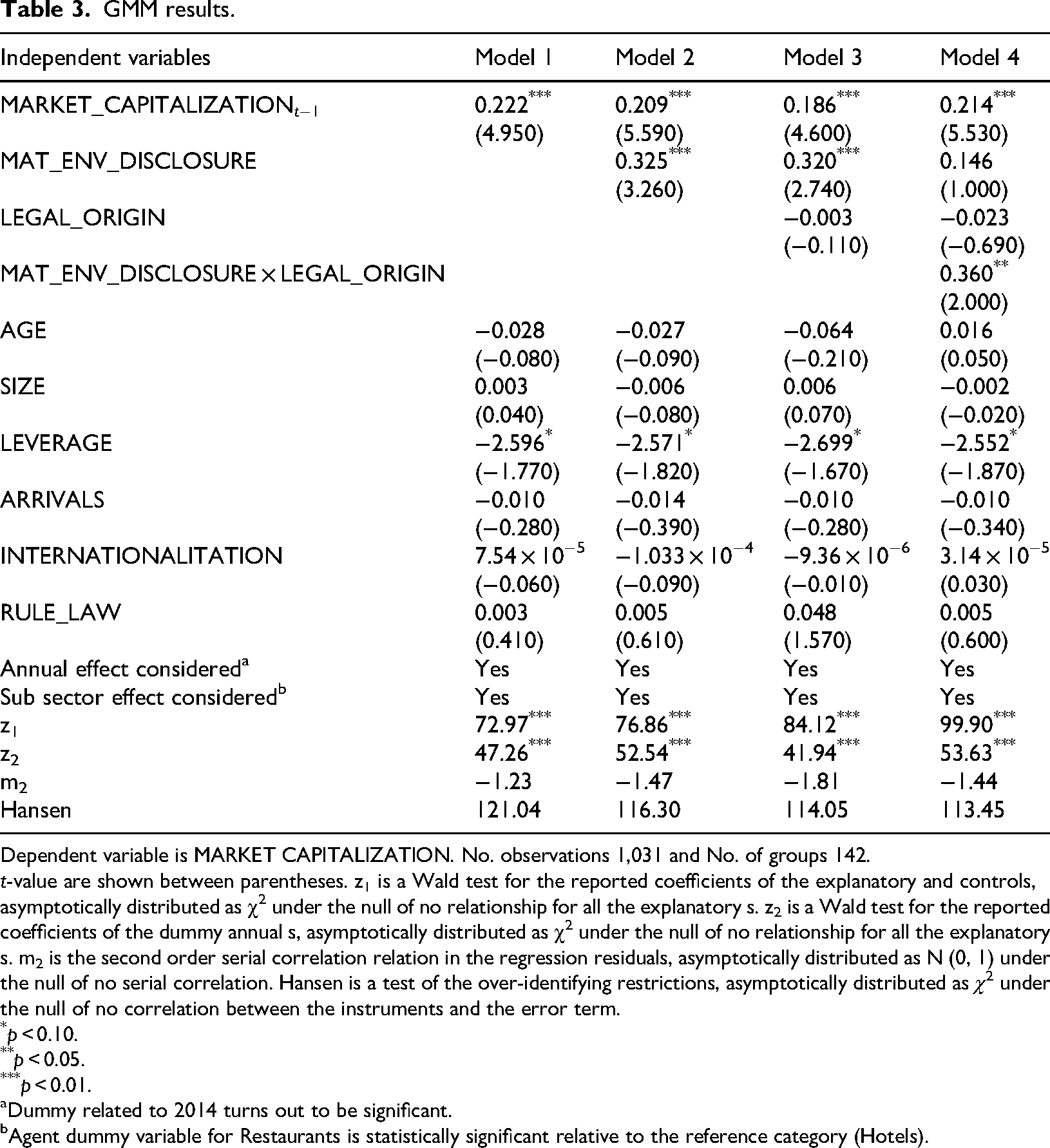

Table 3 reports the GMM estimation results. As the GMM requires four consecutive years without missing values to compute the m2 statistics, the final estimations are based on a sample of 1,031 observations.

GMM results.

Dependent variable is MARKET CAPITALIZATION. No. observations 1,031 and No. of groups 142.

t-value are shown between parentheses. z1 is a Wald test for the reported coefficients of the explanatory and controls, asymptotically distributed as χ2 under the null of no relationship for all the explanatory s. z2 is a Wald test for the reported coefficients of the dummy annual s, asymptotically distributed as χ2 under the null of no relationship for all the explanatory s. m2 is the second order serial correlation relation in the regression residuals, asymptotically distributed as N (0, 1) under the null of no serial correlation. Hansen is a test of the over-identifying restrictions, asymptotically distributed as χ2 under the null of no correlation between the instruments and the error term.

p < 0.10.

p < 0.05.

p < 0.01.

Dummy related to 2014 turns out to be significant.

Agent dummy variable for Restaurants is statistically significant relative to the reference category (Hotels).

Model 1 presents the effects of the control variables on the firms’ market capitalization. Model 2 includes the main explanatory and control variables. The independent variable exhibits a positive and statistically significant effect on firm value (at the 1% level), indicating a positive association between the disclosure of material sustainability information and firms’ market value, consistent with Hypothesis 1. Gerged et al. 122 and Al-Shaer and Zaman 123 highlight that capital markets generally respond favorably to sustainability reporting. In particular, Shen et al. 23 highlight the importance of environmental materiality in sustainability reporting for enhancing market value. The results are also consistent with evidence from other sectors showing a positive performance effect of reporting on material sustainability issues.21,29,124

In Model 3, the moderating variable capturing the legal system of the company's headquarters was added. The coefficient on the legal system is not statistically significant. In Model 4, the interaction term between the main explanatory and moderating variable was included and was positive and significant (β = 0.360, p-value = 0.046), supporting Hypothesis 2. This indicates a positive moderating effect on the relationship between material environmental sustainability disclosures and companies’ market capitalization. Firm leverage is negatively related to market capitalization, consistent with conventional financial theory, which suggests that debt-related costs may outweigh potential benefits.100,105

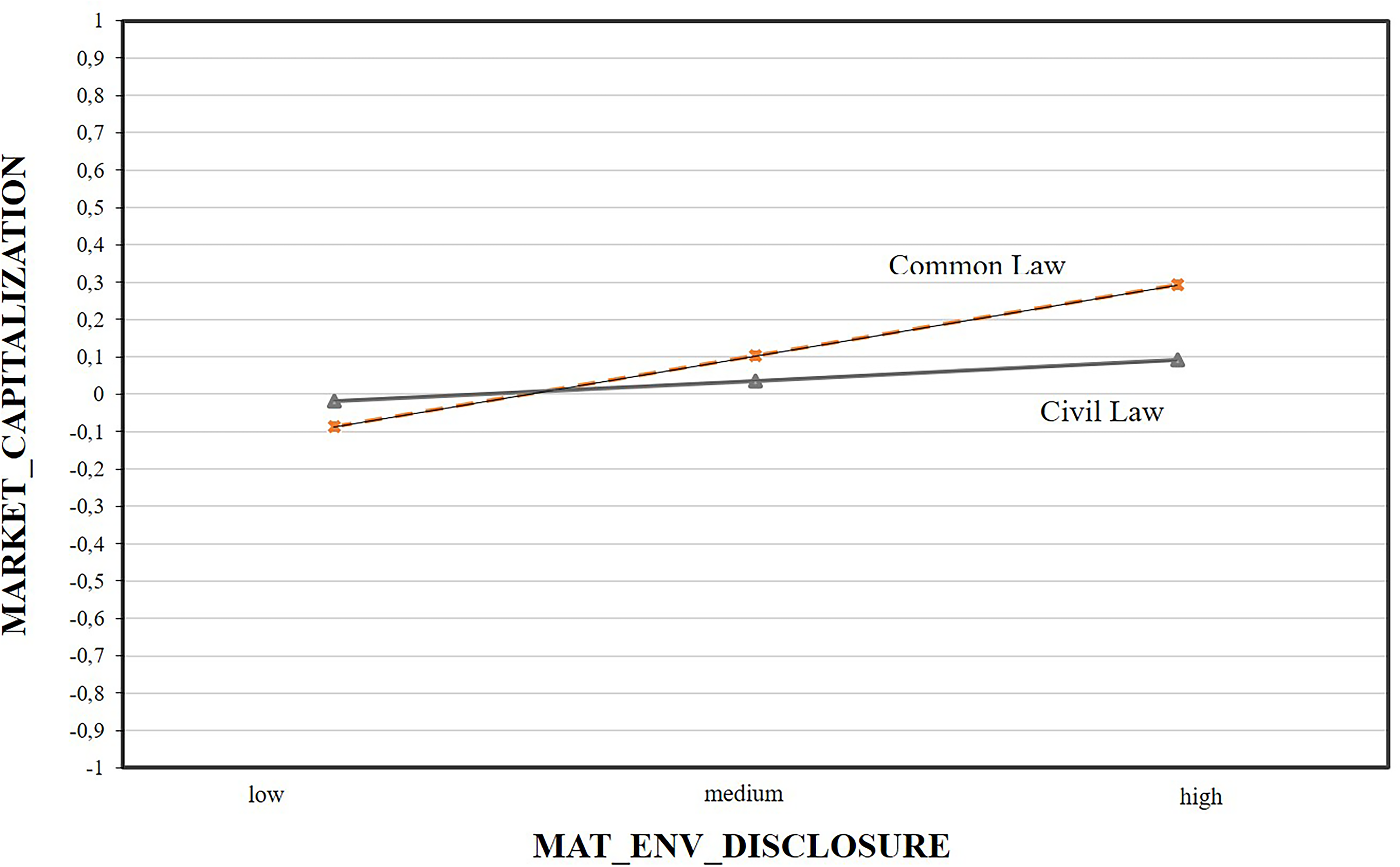

Given the significant moderating effect of legal origin, we further examine this interaction. Graph construction was one of the main techniques used in this analysis. 125 Accordingly, we plot the interaction using a line graph (Figure 2) with the Modgraph program. 126 This graph shows two regression lines for firm market capitalization as a function of material environmental disclosure (MAT_ENV_DISCLOSURE), corresponding to the two values determined for the moderating variable (one if the variable takes a value of 1 and the other if the value is 0). As shown in Figure 2, the positive association between material environmental disclosure and company's market value is stronger for firms headquartered in common law countries.

Moderation analysis.

Robustness tests

In order to establish the robustness of our results, our estimations are repeated using additional measures, and additional estimations. Additionally, to test the sensitivity of the results to the measurement of firm size, total assets was used as an alternative proxy instead of sales. The results remained the same. We performed PSM as a robustness test to address potential concerns regarding endogeneity and selection bias. Following best practices in the literature, this approach enables us to compare treated and untreated firms with similar observable characteristics, thereby reducing bias due to non-random treatment assignments.127–129 PSM was estimated using a logit model, with the treatment group defined as MAT_ENV_DISCLOSURE > 0.

We then estimated both the average treatment effect (ATE) and the average treatment effect on the treated (ATET) using nearest-neighbor matching (1 and 2 matches), caliper (0.05), and kernel matching. Across all specifications, ATE and ATET remain positive and highly significant, showing that treated firms have significantly higher market capitalization than the matched controls. The stability of the estimates across matching methods suggests robustness to model specification and sample composition, and aligns with prior PSM-based research in management, strategy, and sustainability.130–133

As a complementary robustness test to the moderated hierarchical regression analysis, we performed a subgroup analysis. 134 This procedure compares regression coefficients across subsamples defined by different states of the moderator variable. The sample was divided into two subgroups based on the legal origin of the country in which the firms’ headquarters are located. The Chow test 135 was used to assess model equivalence, with a significant statistic supporting the moderation hypothesis. When comparing the “Common Law” and “Civil Law” subsamples, the coefficient of Legal Origin is only significant in the first case (at a 1% level), and the Chow test is significant [F (15, 1285) = 5.810, p = 0.000]. This indicates that legal origin acts as a moderating variable, corroborating the main findings.

Conclusions, implications, and future research

Conclusions

This study builds on prior empirical evidence showing that companies disclosing material environmental issues experience positive effects on market value and firm performance.21–2374 We extend this literature by presenting novel sector-specific evidence for the tourism sector (147 listed tourism companies from 39 countries, 2012–2023), showing that firms that report material environmental issues aligned with SASB standards exhibit higher market capitalization. This positive relationship is robust to dynamic panel estimation and robustness checks and is stronger in countries with common law legal origins, indicating that legal origin moderates the disclosure–valuation relationship.

Implications

For the academic community, this study addresses a notable gap in the literature by focusing specifically on the tourism sector, an industry characterized by unique environmental dependencies, combining sector-specific materiality measures with cross-country empirical analysis. We provide empirical evidence on the importance of sector-specific material environmental disclosure in shaping firm valuation and investor perceptions, also, support the call for additional research on SASB disclosure. 44 Furthermore, this study provides new empirical evidence, regarding how disclosing material environmental issues can influence tourism firms’ financial performance, which has been underexplored in previous studies.

For tourism companies, our findings underscore the importance of adhering to recognized sustainability reporting standards such as those set by the SASB. Companies should prioritize the identification and disclosure of material environmental issues to communicate sustainability commitments and respond to stakeholder expectations, thereby enhancing market capitalization. Transparent communication on material sustainability issues could also provide a competitive advantage and attract responsible investors. For investors, this study highlights the importance of considering material environmental disclosures as a key factor in investment decision-making. Such disclosures provide clearer insights into company's long-term sustainability and financial prospects, supporting more informed investment decisions. Moreover, policymakers and regulators should prioritize mandating or incentivizing standardized sustainability reporting, such as SASB standards, to enhance transparency and market confidence. Our evidence supports policies that promote materiality-based disclosure to improve market efficiency and investor protection. In civil law jurisdictions, where the impact is weaker, reforms of governance and disclosure frameworks may be needed to align incentives and reduce information asymmetry. Aligning corporate interests with sustainability goals through tax incentives or subsidies can encourage transparency. Cross-jurisdictional learning should be promoted to adapt best practices from common law systems, and investor education on sustainability reporting should be enhanced to support informed decision-making and market efficiency.

Limitations and future research

SASB indicators are increasingly used as a global reference for financially material sustainability information, and their structure closely aligns with prevailing reporting practices in many jurisdictions. For example, the KPMG Survey of Sustainability Reporting 136 shows that 41% of the largest 100 companies in each of 58 countries apply SASB standards. However, adoption remains heterogeneous across regions and firm sizes. Despite the relevance of SASB standards, a key limitation arises from the lack of SASB-compliant data for a sufficiently large international sample of tourism firms. Consequently, we relied on information available in the Refinitiv data accessed via LSEG Workspace, widely used in previous research, which required manually matching available indicators to SASB metrics rather than extracting disclosures directly from SASB-aligned reports. To minimize subjectivity, we carefully screened more than 300 environmental variables in the LSEG Workspace and selected only those that matched the SASB accounting metrics exactly in both wording and definition. This conservative approach reduces the likelihood of false matches but may result in some loss of information in the materiality analysis. Future research could also extend our analysis by incorporating other firm- or country-specific characteristics (such as ownership structure, corporate governance practices, and ESG reputation). These variables may act as alternative moderating or mediating mechanisms through which environmental disclosures influence a firm's market valuation. It could also complement large-sample quantitative analyses by using qualitative approaches, such as case studies or stakeholder interviews, to explore additional mechanisms (such as reputation, operational improvements or investor recognition) through which environmental disclosure influences market value.

Footnotes

Ethical approval and informed consent

This study did not involve human participants or animals requiring ethical approval.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Project PID2022-137379NB-I00, funded by MCIN/AEI/10.13039/501100011033/ and ERDF A Way of Making Europe (grant number PID2022-137379NB-I00).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.