Abstract

This study addresses an under-explored nexus in environmental economics by offering the region's specific evidence on how financial-technology diffusion influences carbon dioxide emissions within South Asia, where rapid output growth remains coupled with dominant fossil-fuel use. Existing studies either omit the subcontinent from cross-country panels, apply first-generation estimators that neglect cross-sectional dependence and slope heterogeneity, or assume FINTECH to be unconditionally benign. This study uses panel dataset of five South Asian countries from 1995 to 2022, we deploy the Augmented Mean Group (AMG) and Common Correlated Effects Mean Group (CCEMG) estimators that jointly accommodate country-specific coefficients, unobserved common factors, and dynamic feedbacks. The long-run estimates reveal that a one-percentage-point increase in green innovation, natural-resource rents, and renewable-energy penetration reduces CO₂ emissions by 0.048%, 0.383%, and 0.286%, respectively, whereas equivalent expansions in FINTECH adoption and urbanization augment emissions by 0.038% and 0.543%. These findings imply that regulators should embed verifiable environmental screens within FINTECH sandboxes, earmark resource-rent windfalls for scalable renewable-energy infrastructure, and enforce compact-city zoning integrated with low-carbon public transit. Collectively, these targeted interventions provide South Asian policymakers with a coherent strategy to advance SDG 13 without compromising the growth imperatives articulated in SDG 8.

Introduction

Expanding economic activities proved helpful in reducing unemployment and poverty in the world. These economic growth activities increase the energy demand. The core portion of energy demand is fulfilled by using fossil fuels for energy due to their lower cost. 1 Using fossil fuels for the growing energy demand increases greenhouse gas emissions. The release of these greenhouse gases becomes a basic reason for climate change and the upsurge in global temperature. 2 The increasing worldwide temperature and climate change trend have become a major concern for the world's leaders. 3 To address these severe concerns, the United Nations (UN) proposed different sustainable development goals (SDGs) as basic guidelines for the patrons. 4 After the development of these goals, many conferences took place in different countries of the world in which the world's leaders sat together and discussed the ways in which they could contribute to achieving these goals. A noteworthy objective was achieved in the Paris Agreement 2015, 5 in which it was decided collectively that all the leaders would try to bring down the increase in global temperature to under 2°C. After setting the targets, a lot of debate was made by scholars on accomplishing these sustainable goals. 6 This study supports the South Asian nations in attaining numerous United Nations Sustainable Development Goals (UN SDGs).

The goal of innovation and sustainable industrialization set by the UN cannot be achieved without the positive contribution of financial institutions. One possible way to combat the problem of climate change is to introduce innovation and technology in the economic system.7,8 Regarding this matter, financial technology (FINTECH) is a valued addition to the financial system. It's about using the internet, blockchain, data clouding, and artificial intelligence in financial systems. In the existing literature, there are mixed findings about FINTECH and its effect on the environment. Some scholars advocated that the use of FINTECH can improve environmental quality by providing an alternative source of energy, energy efficiency, and loans for sustainable actions.9,10 Nonetheless, certain scholars’ contention that the practice of FINTECH, which encompasses digital banking, blockchain, and AI-driven financial tools, has been widely seen as a facilitator of economic efficiency and innovation, and also increases the electricity demand at the same time. The electricity used to validate the blockchain, mine cryptocurrency, and run FINTECH data centers is significant, especially in areas where electricity is generated with fossil fuels. 11 And without corresponding transitions to renewable energy (RE), these energy-intensive processes can certainly increase CO₂ emissions. Therefore, for developing economies such as South Asia, where RE adoption is in its infancy stage, the proliferation of FINTECH may lead to environmental pollution more than restoration. 12 Further, the affiliation between FINTECH and CO2 emissions, especially in the context of developing countries, is overlooked by the researchers. Hence, there is a need for an extensive study to address the deficiency in the literature.

Green innovation (GI) is the resolution to attain the dual objective of development with sustainability.13,14 GI improves the performance of the business and reduces the detrimental effects on the environment. This can lead the world to attain the objective of carbon neutrality by solving climate change and environmental issues. To attain the complete benefit from GI, there is a need to make policies and execute the proper plan by the organizations and legislators of the nations. 15 Proper formulation of implementing GI policies by the governments of different nations can reduce carbon emissions by about 60%. 16

The use of natural resource rents (NRR) plays an imperative role in economic development. It creates employment and helps in poverty reduction. However, when these resources are extensively used or poorly managed become the cause of environmental damage like the destruction of forests, water pollution, soil erosion, and harm to biodiversity. 17 The aforementioned factors become the reason for climate change, lower productivity, and harsh weather conditions, and create hurdles to achieving the goal of sustainability. On the other hand, studies also suggest that effective use of NRR can improve the economic conditions along with the environment. 18

Energy consumption and economic progression directly relate to each other, but with negative effects on the environment. 1 RE is a substitute source that can be used to achieve the purpose of economic growth without environmental damage. The primary challenge for energy transformation is the substantial installation cost of RE. 19 This problem can also be solved by the improvement of financial institutions and their support for the conversion of non-RE to RE cradles. This type of energy conversion is the best substitute for fossil fuel energy. 20

Subsequently, this study's overarching goal is to probe how FINTECH, green innovation, NRR, RE, and urbanization affect CO2 emissions in South Asian economies. There are multiple reasons for accounting for South Asian economies. First, the worst-case scenarios related to climate change are already bearing down on this region, which can be addressed through the implementation of green growth in economic activities. The region will be threatened by a rise in temperature from 2°C to 6°C. 21 Second, this region has prompt economic growth, which increases the energy demand in the region. The excessive reliance on fossil fuels for energy generation increases CO2 emissions and causes global warming. As per the World Bank report, 9 out of 10 countries with the worst air quality are located in the South Asian region. 22 As per the WHO, over 2 million people lose their lives every year due to this contamination. Thirdly, it is a well-known reality that the majority of nations in this area experience poverty, and economic growth can easily increase their income. But this growth cannot be achieved at the cost of environmental degradation. Hence, it is essential to keep stability between economic progress and sustainability in the designated region. 23 By considering this, the goal of decent work and economic growth can be achieved in the region. Fourth, owing to a lack of capital, South Asian economies are lagging in terms of innovative technologies. 24 It is essential to examine the influence of these technical indicators on the environment in the five selected countries of South Asia over the period from 1995 to 2022. Pakistan, Bangladesh, India, Nepal, and Sri Lanka are chosen for this study. In addition to data availability constraints, the excluded South Asian economies were omitted due to limited FINTECH market maturity, structural instability during the study period, and their relatively small economic scale, which could introduce volatility and comparability issues in panel estimation. The selected five countries represent the dominant share of regional GDP, emissions, and FINTECH activity, ensuring both representativeness and econometric robustness.

Novelty and contribution of the study

This study examines the influence of FINTECH on CO2 emissions in the South Asian region, and provides the significant insights into potential impact of FINTECH on the environment in a region characterized by distinct constraints, such as restricted RE infrastructure. This analysis on FINTECH-environment dynamics in South Asia addresses a notable gap in the study in the research, which has predominantly focused on developed regions.

Second, unlike conventional methods, which often assume cross-sectional independence and homogeneous slope coefficients, we utilize the Augmented Mean Group (AMG) and Common Correlated Effects Mean Group (CCEMG) estimators, which are specifically designed to handle cross-sectional dependence and heterogeneity in panel data. These methods are particularly important for South Asian economies, where the effects of FINTECH and environmental indicators are likely to differ among countries due to variation in green innovation, RE adoption, use of NRR, and urbanization.

Third, this study significantly contributes to the achievement of several UNSDGs, particularly SDG 7 (Affordable & Clean Energy), SDG 8 (Decent Work & Economic Growth), SDG 9 (Industry, Innovation, and Infrastructure), and SDG 13 (Climate Action). This study provides policymakers with actionable insights to navigate the complex challenge of reconciling economic growth with environmental sustainability.

The next sections present the literature survey, theoretical framework, results and discussions, conclusion, policy recommendations, limitations, and opportunities for future research.

Literature review

The link between digital transformation and environmental sustainability is now getting attention from scholars of environmental economics. They are trying to check the influence of FINTECH, green innovation, RE, NRR, and urbanization on CO2 emissions. However, the findings are contradictory and fragmented, especially in the context of South Asia. The following section integrates the literature on significant theoretical and empirical debates and identifies the gaps that need to be addressed in the context of South Asia.

FINTECH and CO2 emissions linkage

The impact of FINTECH on the environment is theoretically ambiguous and empirically doubtful. According to the ecological modernization theory, financial and technological innovation assists individuals and business owners by improving the living standard of the people by providing low-cost and time-efficient services in financial markets.25,26 From this prospective FINTECH provides a proliferation of digital banking platforms; blockchain-based financial applications; mobile payment platforms; and AI-enabled financial services, which include automated lending and credit scoring. It also aligned the sustainable lending towards RE and promoted green investment. Through this, it not only reduces the cost but also improves the global environment by reducing CO2 emissions. 27

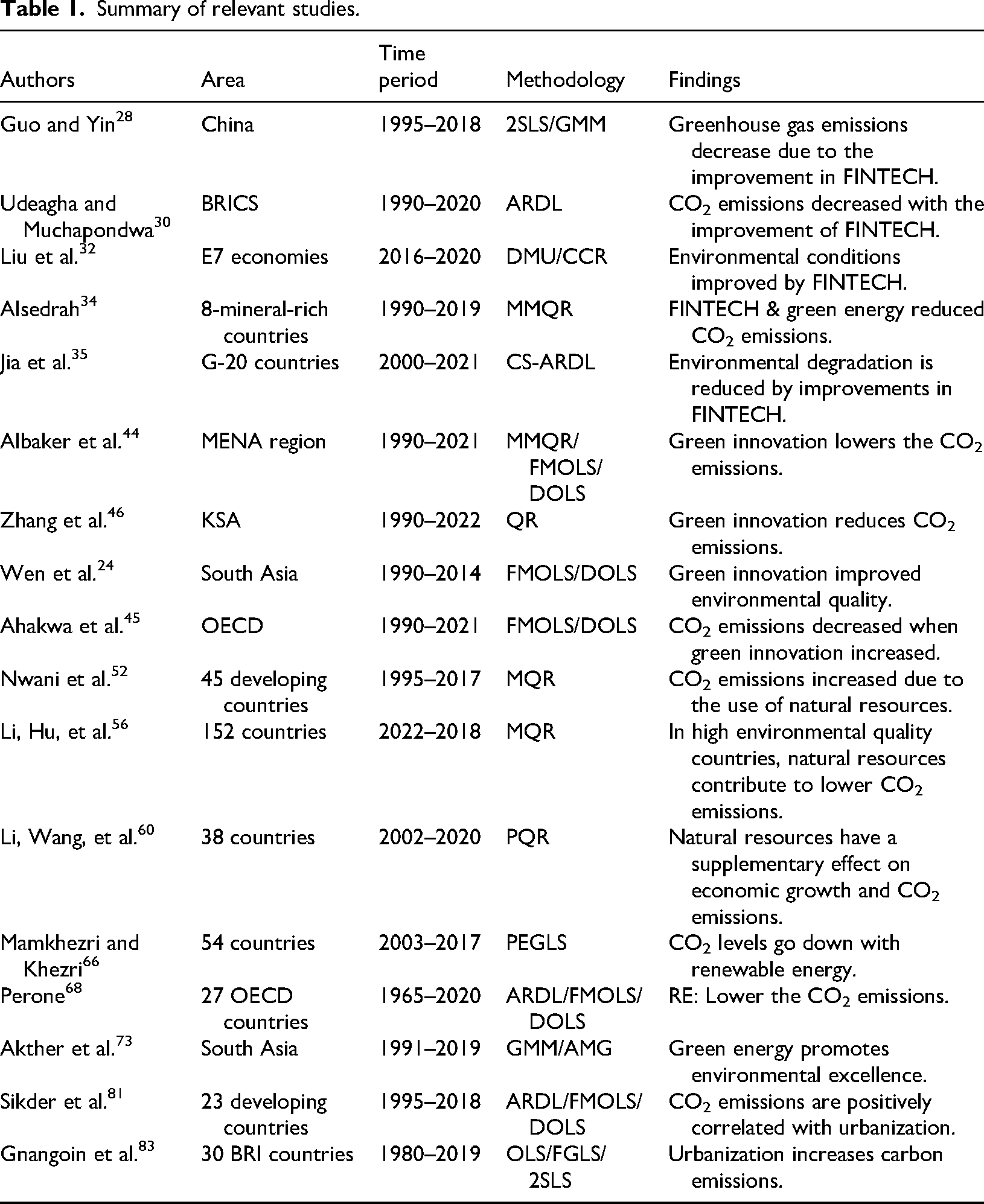

Empirically, the studies relevant to China, BRICS, and G-20 countries often support the above argument, that development in FINTECH reduces carbon emissions by enhancing energy efficiency and promoting RE. For instance, Guo and Yin 28 and Tao et al. 29 discussed in their studies that improvement in FINTECH reduced the greenhouse gases and CO2 emissions in China. Udeagha and Muchapondwa, 30 using the data from 1990 to 2020, suggested in their study that development in FINTECH is very helpful in achieving the goal of carbon neutrality in the BRICS region. Udeagha and Ngepah 31 applied the CS-ARDL approach to the data taken from 2000 to 2018, supporting the argument that FINTECH condensed the carbon emission in the BRICS countries. In E7 economies, Liu et al. 32 used the data from 2016 to 2020, and they used the CCR approach to estimate the result. They concluded that FINTECH and CO2 emissions are negatively correlated with each other. Lu et al. 33 also witnessed that FINTECH improved the environmental quality in BRICS economies.

In the case of 8 mineral-rich countries, Alsedrah 34 piloted a study by using the data from 1990–2019 and employed the MMQR technique. They suggested that FINTECH, along with green energy, reduced the carbon emissions in the specified eight mineral-rich countries. Jia et al. 35 also led a study on G-20 countries and believe that environmental damage can be prevented by upgrading FINTECH in G-20 economies.

On the contrary, FINTECH also requires high computational power, as in the case of blockchain verification and data storage, which becomes a reason to increase CO2 emissions in the economies of the South Asian region, where energy grids are still dominated by fossil fuels. 36 There are several studies that designate that FINTECH leads to high energy consumption and leads to high carbon emissions.12,37

Further, digital monetary development in informal economies can lead to increased e-waste and urban energy use. 38 Thus, FINTECH in South Asia should be considered a Janus-faced trend regarding sustainability, as it can both facilitate and hinder it depending on the way it is designed, governed, and supported in its energy sources. Given this contrasting evidence and limited country-specific findings for South Asia, this paper seeks to explore the FINTECH CO2 nexus by employing the superior second-generation model.

Green innovation and CO2 emissions linkage

Green innovation (GI) is considered an important mechanism for decarbonization and achieving sustainable development. 39 GI facilitates the structural transformation towards low carbon emissions. 40 Many of the empirical studies from high- and middle-income economies support this theoretical concept. Scholars consider green innovation as the finest elucidation of environmental degradation. 41

For instance, Li et al. 42 and Ali et al. 43 discussed in their studies that green innovation, along with energy efficiency, reduced carbon emissions in China and in BRICS countries, respectively. In the case of the MENA region, Albaker et al. 44 acquired the data from 1990 to 2021 to investigate how GI affects CO2 emissions. The results showed that CO2 emissions can be lowered through the improvement of GI.

In certain developing contexts, some studies advocate that complete benefits of GI can be obtained through financial development, expansion in RE, and policy consistency. Ahakwa et al. 45 conducted a study on Ghana from 1980 to 2018 and used a quantile-on-quantile regression approach, suggesting that ecological deterioration can be mitigated by improving green innovation and expansion in RE. Zhang et al. 46 checked the impact of GI on CO2 emissions in the Kingdom of Saudi Arabia from 1990 to 2022. They analyzed the relation with and without income level. They concluded that GI provides the solution to environmental degradation in both models. Ahakwa et al. 45 revealed in their work on OECD countries that CO2 emissions decreased as GI increased. Wen et al. 24 also proved that GI functions in a monumental manner in making a better South Asian environmental quality.

Although there is overwhelming evidence for a negative relationship between green innovation and emissions, most research is concentrated on developed countries. These countries have relatively advanced infrastructure, strict regulatory systems, and supportive financing systems. Consequently, the validity of these findings is still uncertain for structurally different regions. Our study considers the South Asian region to account for the analysis of structural constraints and clarify whether limited innovation contributes meaningfully to emissions reduction.

NRR and CO2 emissions linkage

It is quite evident in the research that NRR have a satisfactory result on the growth of economies.47,48 Nevertheless, the results are at odds with one another regarding the environmental influence of natural resources. Some studies linked NRR directly with CO2 emissions,49,50 but other shows an inverse correlation between carbon dioxide emissions and rents from natural resources. 51 For evolving economies, Nwani et al. 52 discussed that carbon emissions increased due to the use of natural resources. Cai et al. 53 carried out research on BRICS nations from 1990 to 2020 and employed a panel quantile regression methodology to suggest that resource rents and CO2 emissions have a positive relationship with each other. Fan et al. 54 used data from China from 1988 to 2018 and used the GMM model to conclude that excessive use of resource rents degrades the environment.

Chen et al. 55 analyzed 38 industrialized and developing economies. Li, Hu, et al. 56 analyzed a big data set of 152 countries from 2002 to 2018. Shang et al. 57 took the case of the top 10 emitting economies. Chen and Chen 58 also discuss the connection between resource rents and carbon emissions in China. They all concluded that carbon emissions increased due to the increasing trend of resource rents in different countries.

In contrast to the above debate, NRR is a useful tool to decrease carbon emissions by investing these rents in RE and sustainable development projects. 59 There are several studies which proved this stance that effective management of resource rents can reduce carbon emissions in different regions and countries. For example, the study of Nwani et al. 52 revealed that rents from natural resources can be negatively associated with carbon emissions of territorial activities in three different countries. Li, Wang, et al. 60 proved the mitigating effect of NRR on carbon emissions. Li, Hu, et al. 56 suggested that carbon emissions can be reduced by investing these rents in green and sustainable development. Zheng et al. 61 and Adanu and Adams 62 concluded the same results that investing these rents in technological development can lead to lower carbon emissions. Voumik, Mimi, et al. 63 conducted a study on selected South Asian countries from 1972 to 2021 and employed the CS-ARDL approach for the analysis, proving that CO2 emission was reduced in the region due to NRR.

Despite having a sufficient degree of resource dependence across the region, there is limited research on the South Asian region. Few studies are available in the literature that assessed whether rents from resources are channeled towards sustainable development or used in the expansion of carbon emissions in the region. Moreover, existing studies in the literature often failed to integrate natural resource to broader digital structure that includes FINTECH and innovation in the context of South Asia.

RE and CO2 emissions linkage

Theoretically, RE is considered one of the cornerstone strategies for the global goal of decarbonization. 64 Scholars have considered the impact of RE on the environment. You et al.. 65 Take the example of 64 BRI countries and discuss how RE lessens carbon emissions in selected BRI countries. Assessing the data of 54 countries from 2003 to 2017, Mamkhezri and Khezri 66 suggest in their study that the usage of RE aids in decreasing carbon emissions. Kwilinski et al. 67 performed a study on the transport sector of EU countries from 2007 to 2020. They used the PEGLS method and concluded that the replacement from traditional to RE in the transportation industry can help reduce CO2 emissions in EU countries.

Further, there is evidence in the studies of Perone, 68 Adebayo and Ullah, 69 Bergougui 70 that RE and carbon emissions are negatively associated in Sweden, Algeria, and the OECD region. These studies revealed that green energy reduces dependence on fossil fuels and improves environmental quality. reduce the dependence on fossil fuels, which lowers the carbon emissions, especially in the OECD region,

The studies also revealed that the countries where RE adoption strategies gained institutional support provided more robust results. Yadav et al. 71 include supporting data in their study that green energy significantly contributes to the BRICS nations’ environmental sustainability. Alam and Hossain 72 demonstrated in their study that green energy provided support to minimize the environmental degradation in China from 1990 to 2019. The pieces of evidence are also available in the studies that RE promotes environmental superiority in the South Asian region.73,74 However, the effect of RE on the environment depends on the institutional support, structural context, policy preferences towards green energy adoption, and technological efficiency.75,76 Otherwise, the results will not be more reliable.

The regional energy demand continuously rises due to economic growth and rapid urbanization. 77 Although the portion of green energy increases, it is still lower than the total increase in energy demand. Additionally, the contribution of this article is to fill in the gap by making an attempt to calculate the long-run effects of RE on CO₂ emissions along with digitalization, innovation, and structural drivers within a unified framework in the context of South Asian countries.

Urbanization and CO2 emissions linkage

The early and middle stage of urbanization (URB) increases the industrial activity, transportation demand, and energy consumption, which elevate carbon emissions. 78 Although proper planning, use of artificial intelligence, technological advancement, and high-quality infrastructural helps to reduce carbon emissions, usually in the advanced stage of urbanization.79,80

Many researchers conducted studies to check the results of URB on CO2 emissions. Sikder et al. 81 executed a study on 23 developing nations from 1995 to 2018 by utilizing the ARDL technique. The findings exposed the substantial positive stimulus of urbanization on CO2 emissions. In contrast to this, URB in many Chinese cities has reached a level where it reduces carbon emissions. Grodzicki and Jankiewicz 82 took the five high carbon emissions in European countries and analyzed the data from 1985 to 2018 by using the spatiotemporal approach. The study results display that the increasing trend of urbanization damages the environment in the nominated countries. Gnangoin et al. 83 discussed the 30 BRI countries, and the results exposed that urbanization has a positive impact on CO2 emissions. Liu et al., 84 Addai et al., 85 and Nguea 86 concluded the same result in their studies that carbon emissions increased due to urbanization in China, black sea region, and 44 selected African countries.

However, there are some studies that support the second argument that carbon emissions decreased due to the expansion of urbanization.87,88 URB with human capital can provide aid to decrease the region's CO2 emissions. Via a panel quantile regression approach on the data of 77 countries from 2004 to 2019, Purwono et al. 89 also suggested that environmental quality can be improved by controlling urbanization. Ma and Shi 90 also revealed that growth in urbanization with the adoption of green transformation can efficiently reduce carbon emissions.

By focusing on South Asian countries. Ridwan et al. 91 revealed that URB increases carbon emissions in South Asia. The regional structural features of the region suggest that the urbanization effect on the environment in South Asia may be different from that of most studies’ advanced urban systems. Furthermore, the integration of digital, innovative, and RE adoption indicators helps to understand whether urbanization independently increases carbon emissions or interacts with other variables to help environmental development in the region. Table 1 presents the summary of relevant studies in the present literature.

Summary of relevant studies.

Gaps in prior research

Despite the significant contributions of these studies to our understanding about the relationships between FINTECH, green innovation, and environmental performance, important limitations persist which can fill with current study. First, the majority of empirical research is highly focused on China, BRICS, the EU, and OECD countries, leading to a regional bias with implications for generalization to other contexts. Although it is known for having fast-growing FINTECH ecosystems and deteriorating environmental conditions, little research on FINTECH and the environment has been done in the region. Second, the majority of studies adopt single-country time-series models or first-generation panel methodology, which fail to capture cross-sectional dependence and heterogeneity across countries. Such methodological limitations reduce the strength of the chain of long-run inferences, especially in such a globally connected area. Lastly, few studies investigate the dual nature of FINTECH as both a sustainability facilitator and a possible emissions inducer, in the nuanced energy and financial architecture of developing countries such as those in South Asia. We intend to address the above limitations of the literature in our study by using advanced econometric techniques and by considering five South Asian countries.

Theoretical framework

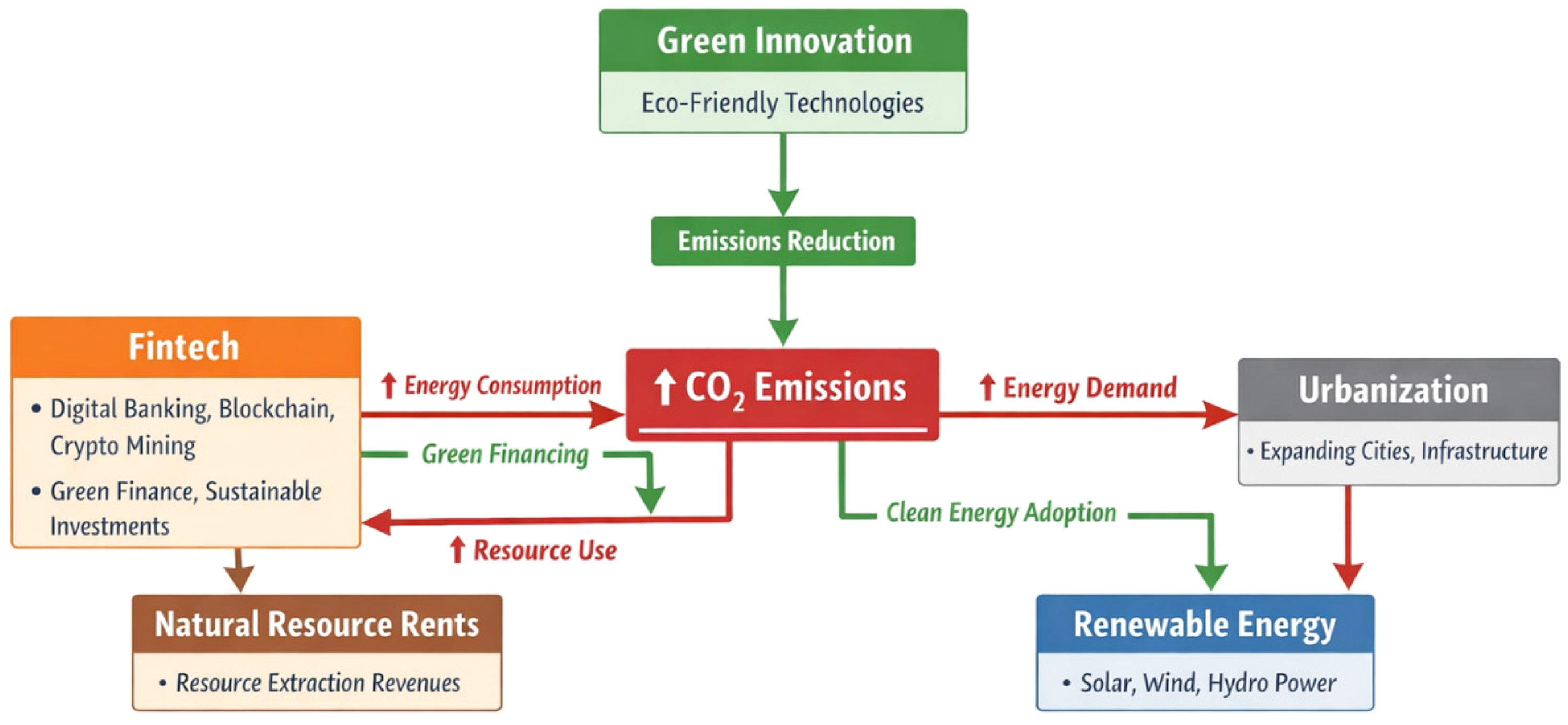

This paper integrates several theories to explain the influence of FINTECH, green innovation, NRR, RE utilization, economic development, and urbanization on CO2 emissions in South Asia. This framework considers structural interactions within regionally interconnected economies, rather than treating these variables independently.

There is ambiguity in the environmental implications of FINTECH. As per ecological modernization theory, advancement in technology and modernization in institutions can reduce environmental degradation by improving efficiency and enhancing cleaner production. From this point, FINTECH enhances digital payments, green lending via ESG-matching finance, and energy access platforms. 92

However, the energy-intensive mechanism argues that the expansion in FINTECH, like cryptocurrency mining, blockchain validation, data centers, and cloud computing, can increase the energy demand.

93

The easy access to credit due to FINTECH also leads to industrial expansion, which increases energy consumption and becomes the reason for higher emissions. Empirically, the studies proved that FINTECH reduces emissions through financial inclusion, green capital allocation, and efficiency gains in developed economies.29,94 On the other hand, it increases carbon emissions in developing economies. The South Asian region has a distinguishing structural context, where rapid expansion in FINTECH is combined with fossil-dominated energy and limited assimilation of RE. In such a scenario, the energy intensity channel may overshadow the efficiency gains.

95

Hence, in connection to FINTECH and carbon emissions we can formulate the following hypothesis.

Endogenous growth theory emphasizes the role of technological innovation in enhancing production and environmental performance. Green innovation (GI) introduces new processes and develops new technologies that lessen the adverse impact of production on the environment by reducing carbon emissions.

96

It has been evident in the studies that GI can meaningfully lessen CO2 emissions in upper and middle-income economies. However, the effect of GI is linked with institutional capacity, research and development intensity, and dissemination mechanism.

97

In resource-constrained countries, the effect of innovation may be limited by financial and technological barriers. Countries like South Asia are categorized by emerging and uneven innovation systems. Irrespective of structural constraints, increasing environmental patent activity and international knowledge spillovers may enhance emissions reduction capacity.

98

Hence, the following hypothesis can be formulated in the context of South Asian countries.

As per the effects of NRR on the environment, they can be discussed within the resource curse hypothesis versus the resource blessing framework. The resource curse hypothesis proposes that countries with heavy use of natural resources lead to intensive carbon growth and also compromise environmental-related regulations. On the other side, the resource blessing hypothesis proposes that the undesirable impact of NRR can be managed by the effective use of these resources.

99

The rents of these resources can provide the funding for sustainable infrastructure, RE, and improve the environment. Through this, the resource curse can be changed with resource blessings.

100

Empirically, there are mixed findings across developing regions. In some scenarios, resource dependence increases emissions

101

; while in others, the environmental impacts can be moderate through institutional quality.

102

In the case of South Asian economies, if these resources are directed toward productive and sustainable investment rather than carbon expansion, they may help to reduce the carbon emissions.

Energy transition theory postulates green energy as a substitute for fossil fuels.

103

Green energy consumption refers to the practice of RE sources that provide a better option for energy sources with low carbon emissions. Most of the empirical results of the researches supports that RE helps the process of decarbonization. However, the magnitude of decarbonization depends on the expansion of RE usage.104,105 The energy demand in the South Asian region is increasing day by day. It is also noticed that the capacity of RE has expanded in recent years. But the percentage of fossil fuels is still dominant in the energy mix of the region. Therefore, the role of RE in reducing carbon emissions depends on its amount in the total energy mix.

106

The given policy commitments in the region towards the expansions in RE are expected to lead to lower emissions. Hence, we proposed the following hypothesis in relation to RE and CO2 emissions.

Urban environmental transition theory discusses the beneficial and damaging effects of urbanization on the environment. Normally, urbanization (URB) increases the production level, and societies shift from agrarian to industrial, which elevates the energy demand and significantly increases carbon emissions, which badly pollute the environment.

107

The other argument suggests that the availability of resources is higher in urban regions than in rural areas. Spending these resources to combat the negative consequences of CO2 on the environment and also introducing innovative technologies to enhance energy efficiency can mitigate the antagonistic effect of urban progress on the ecosystem.

108

Empirically, it is evident that CO2 emissions increased due to unplanned expansion in urbanization. The South Asia region experienced urban growth with deficient infrastructure and fossil-based energy, which leads the region to higher emissions.

109

The consolidative framework of this paper connects these theories to deliver an in-depth analysis of the elements distressing CO2 emissions in the economies of South Asia. The interactions of FINTECH, green innovation, RE consumption, NRR, and urbanization are multifaceted. This paper seeks to offer a nuanced analysis of the roots of CO2 emissions and offer operative policy actions for lowering carbon footprints in the region. Figure 1 illustrates the conceptual framework of the study.

Conceptual framework of the study.

Methodology

Model construction

Our study guides the association between carbon emissions and FINTECH, green innovation, NRR, RE, and urbanization. To get more reliable and comprehensive results, we incorporate additional explanatory variables into our study, such as urbanization. Based on the variables of FINTECH, green innovation, NRR, RE, and urbanization, we developed the CO2 function in the following equation (1).

Where FINTECH stands for FINTECH, NRR stands for NRR, GI stands for green innovation, RE stands for RE, CO2 represents carbon dioxide emissions, and URB stands for urbanization. The transformation of all metrics to natural logarithms lessens the issue of heteroscedasticity, skewness in panel data, and standardizes the measurement scale across all countries. The enhanced multivariate analysis of the transformed log-linear model in a panel framework is as follows in equation (2):

Where β1,…., β5 signify the grade of adaptability of CO2 emissions about FINTECH, green innovation, RE, NRR, and urbanization. Here, individual cross-sections are represented by i, and time (1995‒2022) is represented by t.

Econometric approach

While employing panel data, Heterogeneity and cross-sectional dependence are imperative issues. Obobisa et al.. 110 Disregarding these problems could lead to uneven outcomes. Consequently, we employed the cross-sectional dependence test established by Pesaran 111 and Pesaran and Yamagata, 112 early econometric analysis homogeneity tests to search for heterogeneity and cross-sectional dependence. In the second phase of the investigation, the CIPS unit root test suggested by Pesaran 113 was employed to scrutinize the amalgamation features, considering the prospect of enduring cross-sectional dependency and inconsistency within the panel data framework. Third, to settle cointegration among the heterogeneous variables, we used panel co-integration utilizing Pedroni 114 and Westerlund. 115 Finally, to estimate the long-run relationship between the variables, use the augmented mean group (AMG) estimator by Bond and Eberhardt 116 and the common correlated effects mean group (CCEMG) estimator by Pesaran. 117 These long-run assessment techniques are for both country-level heterogeneity and cross-sectional dependence. GMM or SEM might be able to deal with such dynamics, but were not used here for many reasons. First, we have a panel with five countries and a long period of observation (1995–2022), which generates an unbalanced panel with few cross-sectional units and thus may make the use of System GMM problematic due to instrument proliferation and weak identification. 118

Second, SEM relies on strong theoretical causal assumptions, whereas our interest lies in long-run macro-panel dynamics. Classical estimators [e.g., the fully modified ordinary least squares (FMOLS)] predict cross-sectional independence and homogeneous slope coefficients across panel entities. But for regional panels such as South Asia, countries are closely linked to each other in both economic and environmental aspects, and cross-sectional dependence could distort or even undermine the FMOLS/DOLS results. These methods assume that data is independent across the countries, which is not accurate for South Asian region. Further, no consideration is given to unobserved common shocks or individual-specific heterogeneity in the long-run coefficients. While AMG and CCEMG estimators correct for these shortcomings by assuming common factors are explicitly modeled, and thus they account for heterogeneous dynamics, and deliver more stable and consistent long-run estimates.117,119 Due to these merits, AMG and CCEMG appears to be more appropriate for examining the long-run environmental impact of digital and economic variables across diverse regions such as South Asia. We also employ the Dumitrescu-Hurlin panel causality test to investigate the lead-lag relationship, and emphasize that it does not imply structural causality. The AMG long-run estimating technique is consistent in two steps. The panel regression model designated below is used to estimate the proposed model, as shown in equation (3).

The “first difference order” with (T-1) time dummies is represented by the acronym.

Where

The connection may be used to approximate parameters concerning the subsequent explanatory variables:

In this equation,

Dumitrescu-Hurlin causality (DH) test

Recognizing potential endogeneity is crucial given the potential for reverse causality; for example, increased CO2 emissions could stimulate green innovation, the adoption of RE sources, or regulatory FINTECH, or each. Although the AMG and CCEMG estimators employed in this study remove well the CS and SH biases, they fail to purge the endogeneity bias from the contemporaneous relationships. To investigate the possible reverse causality, the Dumitrescu-Hurlin (D-H) panel causality test, which can detect both unidirectional and bidirectional causality between variables, was applied.

The concluding stage in the observed inquest is to do a causality test to determine which way the variables are causally related. A causal relationship that may be one-way, two-way, or non-existent was subjugated by the causality test of Dumitrescu and Hurlin,

120

which emphasizes the main aspects of heterogeneity. The heterogeneity of the causal link and the heterogeneity of the regression model are therefore superior to the traditional Granger Granger

121

causation test for directional causation, as presented in equation (8).

The cross-section observables

The Wald statistic is

Data and variables

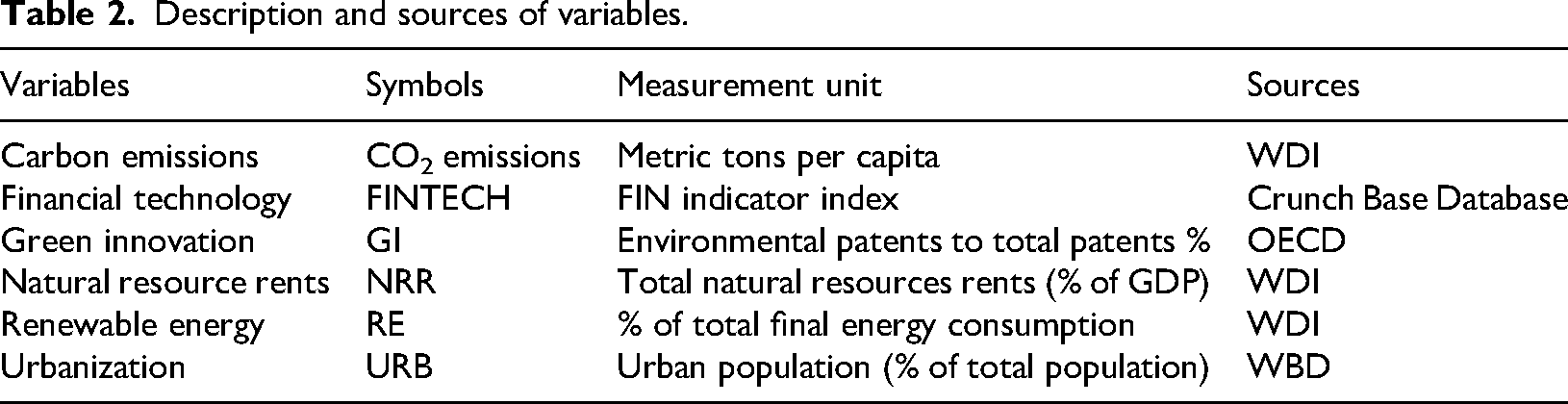

The study utilized the yearly panel data encompassing five nations of South Asia from 1995 to 2022 to assess the effects of FINTECH, green innovation, NRR, RE sources, economic development, and urbanization. The five selected South Asian nations included Bangladesh, Nepal, India, Pakistan, and Sri Lanka. Table 2 includes a comprehensive list of every study component.

Description and sources of variables.

The complete description of each variable is given below:

Results and discussions

Descriptive statistics

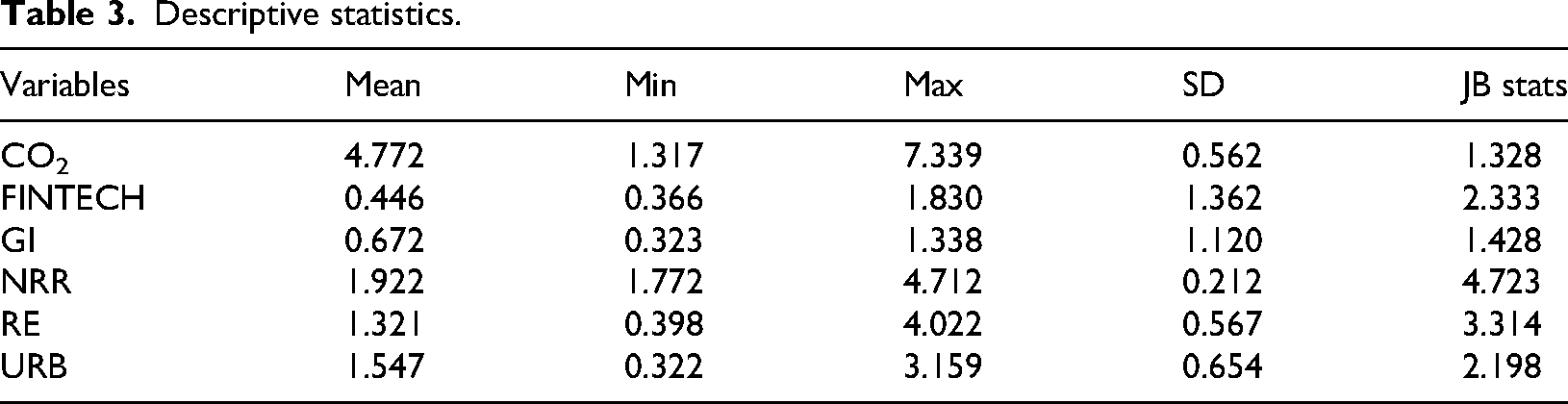

In Table 3, the descriptive analysis shows a standard deviation of CO2 at 0.562, with the mean calculated to be 4.772. The range of CO2 emissions was observed between 1.317 (minimum) and 7.339 (maximum). Additionally, our foremost independent variables, FINTECH, green innovation, NRR, and RE, have mean values of 0.446, 0.672, 1.922, and 1.321, respectively. The mean values discuss the average observation of the variables that are part of the data set. The lowest and highest values inform about the range of each indicator from lowest to highest. FINTECH spans from 0.366 to 1.830, and the value of green innovation exists between 0.323 and 1.338. The standard deviation shows the variability of each indicator. In the results, NRR show the lowest variability (SD = 0.212), and FINTECH has the highest variation (SD = 1.362).

Descriptive statistics.

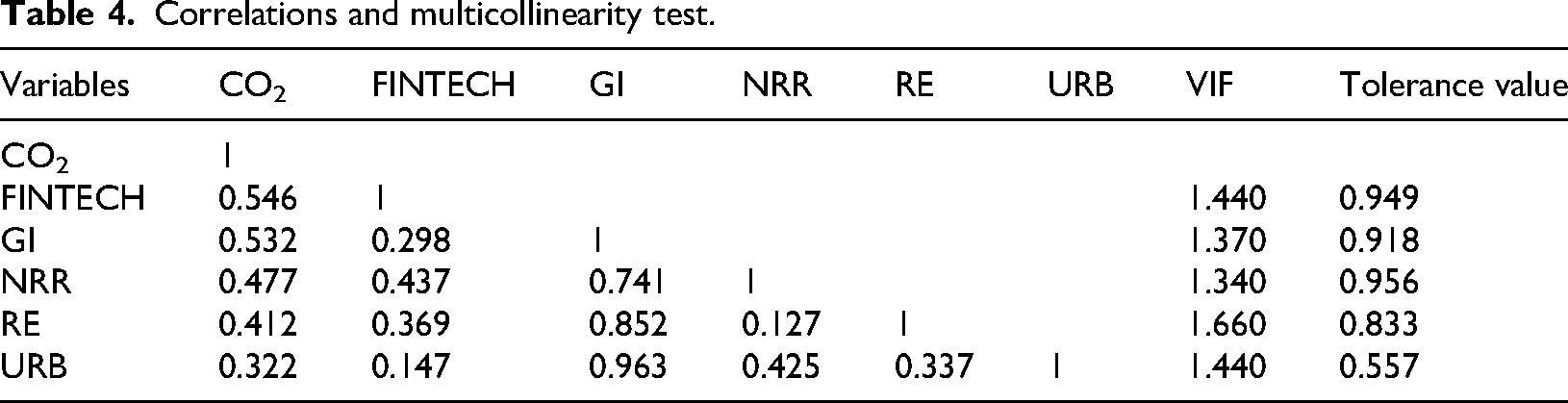

Correlations and multicollinearity test

The study is notable for its extensive utilization of explanatory variables in a multivariate context, which may result in strong interdependence concerns (multicollinearity). To tackle this issue, tolerance tests, the VIF, and a correlation matrix are used to scrutinize multicollinearity matters amongst the regressors. Table 4 shows the fallouts of the multicollinearity and correlation tests. The correlation matrix, in which correlation assessments are substantially below 5, shows a poor link between all of the explanatory variable pairings. We can say that problems with multicollinearity are not unlikely to be a matter that warrants worry in the analysis. The correlation matrix among the repressors is validated by tolerance checks and the Variance Inflation Factor (VIF), where each independent variable exhibits values below 5 and above 0.2, respectively.

Correlations and multicollinearity test.

Cross-sectional dependency and homogeneity test

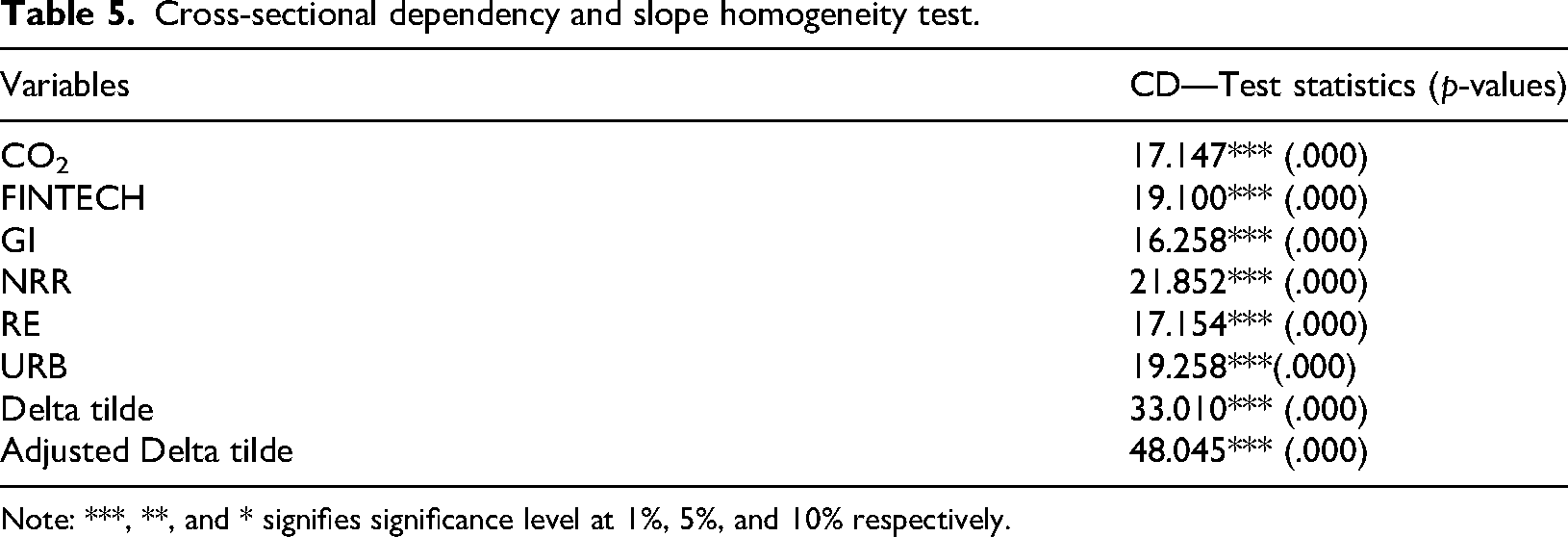

The prospects and correlations identified through tests for CSD and homogeneity are presented in Table 5. The evidence fails to substantiate the hypothesis of cross-sectional independence; therefore, we reject it. The findings indicate potential issues with cross-sectional connectivity in the utilized panel data. The economic stability of one South Asian country can considerably influence the economies of its neighboring member nations, as indicated by the cross-sectional dependence observed in the panel data. Further details of the homogeneity test are provided in Table 5. The tilde-delta (Δ ̅) test and adjusted delta (adj Δ ̅) test led to the denunciation of the null hypothesis, which posited that all variables have similar slope coefficients. The findings demonstrate the stationarity of all model concerns attributable to utilizing panel data, necessitating a second-generation unit root test to verify the stationarity of the variables.

Cross-sectional dependency and slope homogeneity test.

Note: ***, **, and * signifies significance level at 1%, 5%, and 10% respectively.

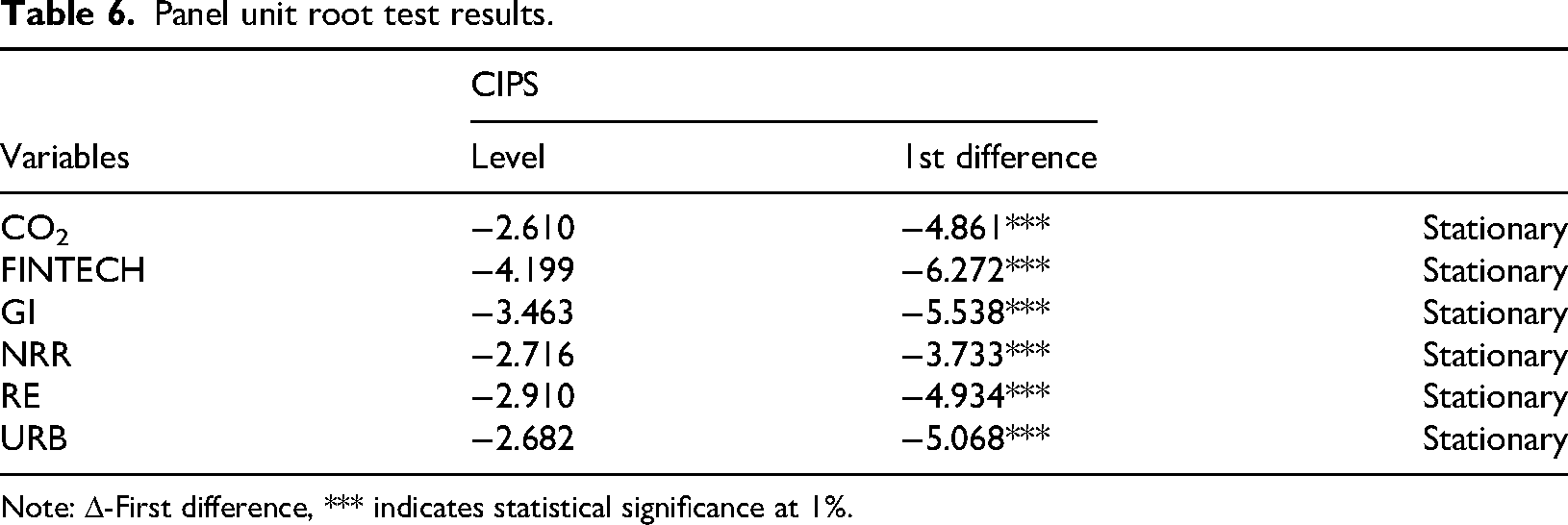

Panel unit root test results

The cross-sectional Im, Pesaran, and Shin (CIPS) panel unit root test evaluates the stationarity of the data 113 (Table 6). Signposts the CIPS unit root test that demonstrates that variables are non-stationary at levels but attain stationarity upon first difference (I(1)). This proposes that all pragmatic variables consist of a similar order.

Panel unit root test results.

Note: Δ-First difference, *** indicates statistical significance at 1%.

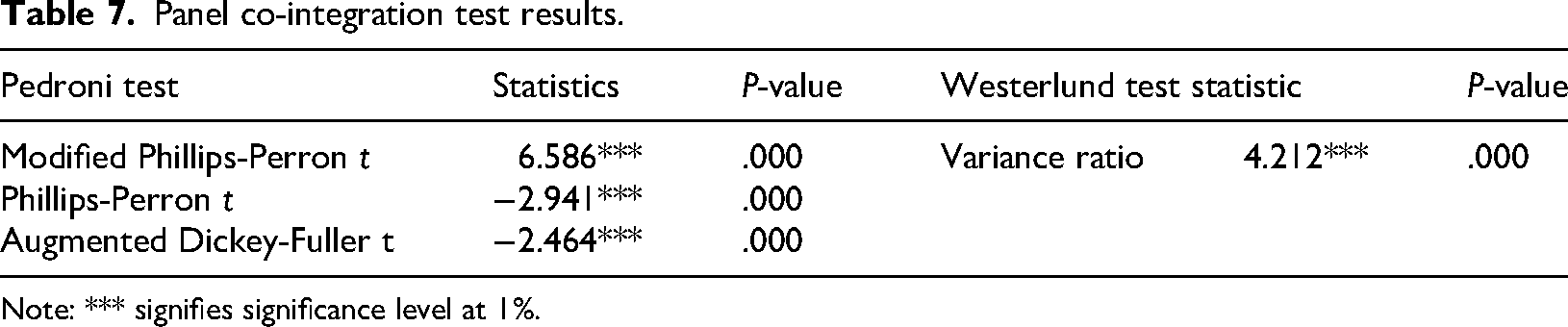

Panel co-integration test results

The Pedroni and Westerlund cointegration tests are displayed in Table 7. Convincing evidence suggests that at a 1% significance level, neither test can reject the null hypothesis of non-cointegration. These data further corroborate the persistent mutable connotation between CO2 emissions and FINTECH, RE use, green innovation, NRR, and urbanization in South Asian economies.

Panel co-integration test results.

Note: *** signifies significance level at 1%.

Long-run estimation test results

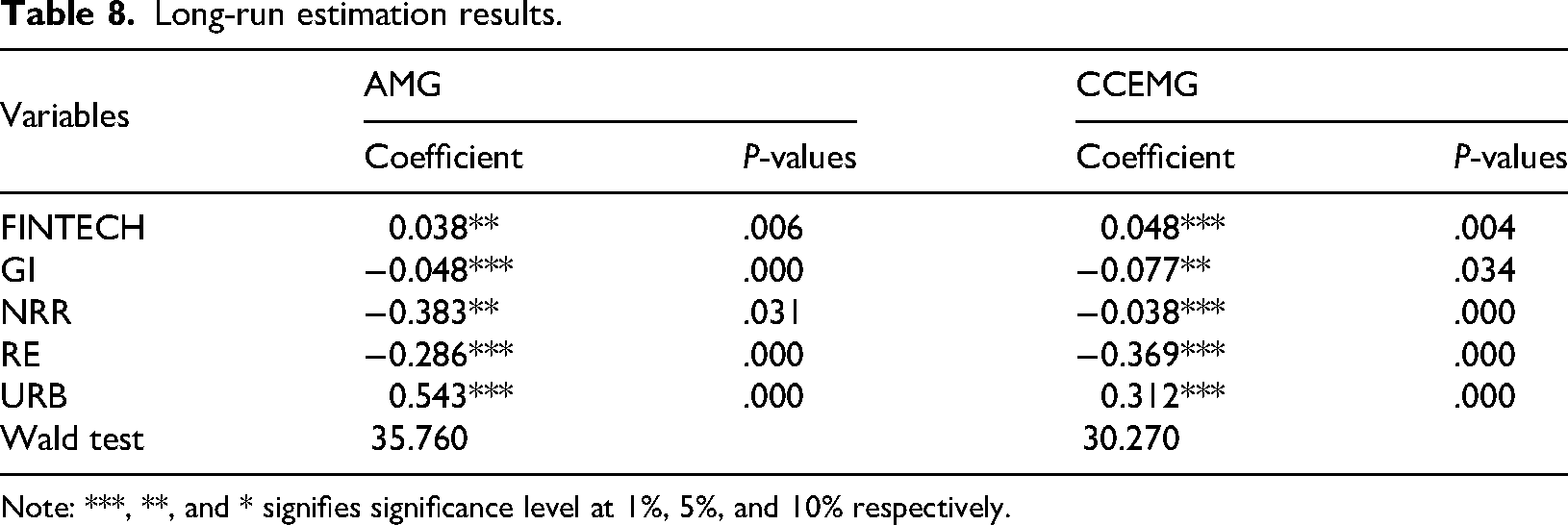

We engaged AMG and CCEMG to estimate approaches to inspect the long-term ramifications of some variables on CO2 emissions: FINTECH, green innovation, rents from natural resources, use of RE, and urbanization. In Table 8, the results illuminate the subtleties of CO2 emissions in South Asia and indicate how each component contributes to regional emissions patterns in its distinct way.

Long-run estimation results.

Note: ***, **, and * signifies significance level at 1%, 5%, and 10% respectively.

The increase in FINTECH activities adds to environmental degradation, as indicated by the statistically positively associated coefficient for FINTECH with CO2 emissions. In particular, the AMG model predicts a 0.038% rise in CO₂ emissions for every 1% rise in FINTECH, whereas the CCEMG model predicts a 0.048% increase. Although the estimated coefficient seems small in magnitude, it bears economic significance and policy implications. With the rapid expansion of FINTECH in South Asia, digital financial transactions and startups are increasing at rates of 20–30% a year in some countries, even small marginal effects can have a big impact over time. 123 Second, these minor increases of 0.038% are scalable by millions of transactions, with combinations of FINTECH applications increasing CO₂ inevitably at the national level. In addition, the finding is relevant in policy settings that require gradual management of sectoral emissions, such as national carbon budget setting or digital infrastructure planning.

However, this study's results are in line with the broader hypothetical view that FINTECH, especially the energy-intensive technologies used in cryptocurrency mining and blockchain operations, can have negative impacts on the environment. Bitcoin mining uses a lot of energy, mostly coal; therefore, there have been empirical studies that have found comparable patterns, such as Dilek and Furuncu 124 and Hileman and Rauchs. 125 Further, using non RE for digital transactions raises emissions levels, which in turn contribute to rising global temperatures and potential health hazards. 126 These findings highlight the region's need for better policy frameworks that combine digitalization with environmental goals. This integration could lead to a low-carbon digital economy in South Asia.

Regarding CO2 emissions, green innovation exhibits a negative elasticity, suggesting a positive environmental impact. According to the AMG and CCEMG models, a 1% increase in green innovation lowers CO2 emissions by 0.048% and 0.077%, respectively, indicating that improvements in green technologies greatly enhance the environmental quality of South Asian economies. This result is consistent with theoretical frameworks on environmental sustainability and technological innovation, which hold that green innovations facilitate switching from conventional energy sources to sustainable alternatives, therefore lowering emissions. These findings are supported by empirical data from Long et al. 127 and Shao et al., 128 which show that technological improvements are linked to less environmental deterioration because they enable better resource management and energy efficiency. Furthermore, R&D and clean technology advancements boost industrial performance, enabling economies to transition from traditional fuels to RE sources, thus promoting green economic transitions.

NRR have a large negative coefficient, indicating that rising resource rents help lower CO2 emissions. In the AMG model, emissions decrease by 0.383%, and in the CCEMG model, by 0.038%, for every 1% increase in the availability of natural resources. These findings are contrary to the resource curse hypothesis, which suggests that carbon emissions increased with dependency on rents of natural resources in South Asia.129,130 These findings can be attributed to the region's recent development towards the use of resource rents to finance sustainable development initiatives, such as RE and green innovations. In South Asia, countries such as India and Pakistan have begun to utilize these rents to resolve the environmental challenges by adopting green energy and developing sustainable infrastructure.131,132 Further, India's bio-energy Projects and Pakistan's green initiative are predicated on public sector investment generated through extractive revenue. This may indicate that, rather than rent-cursed zones, South Asian countries are increasingly rerouting rents towards sustainable initiatives that will help mitigate CO2. 99

These findings challenge the prevailing assumption in the literature and underscore the significance of efficient governance and policy initiatives that prioritize sustainable resource management. 60 It shows that developing countries like South Asia, which have a lot of resources, are capable of breaking the resource curse by connecting resource rents with green growth and sustainable projects. 133

The AMG and CCEMG models show a negative and statistically substantial linkage between RE usage and CO₂ emissions; a 1% increase in RE usage reduces emissions by 0.286% and 0.369%, respectively. This supports the notion of transitioning credence to the idea that switching to RE sources is indispensable for attaining low-carbon growth, since it lessens dependency on fossil fuels, which is the core source of CO₂ emissions. Numerous studies have validated that RE sources (such as solar, wind, and hydropower) meaningfully reduce emissions in different economies. These include the works of Namahoro et al. 134 and. 135 Solar and wind power can help South Asia satisfy its energy demands sustainably because of the region's wealth of renewable resources. Governments in South Asia have pledged to grow RE infrastructure in response to mounting environmental challenges. They have also instituted policies to inspire the espousal of RE sources, which should lead to better environmental performance overall.136,137

Larger urbanization is allied to higher CO2 emissions, as shown by the positive and statistically significant measurement for urbanization. Emissions grow 0.543% under the AMG model and 0.312% under the CCEMG model for every 1% increase in urbanization. This finding lends credence to the idea that urbanization, especially when left unchecked, can put pressure on natural resources and raise emissions due to increased energy use in cities. This conclusion is backed by data; research in Pakistan and China, where unchecked urbanization is causing environmental degradation, has shown similar outcomes.138,139 As more people and money move to cities, industrial activity ramps up, using energy-dense resources and adding to pollution levels. Greater CO2 emissions, increased resource demand, and worsened pollution might result from urbanization that lacks strong urban planning and eco-friendly legislation.

Overall, the findings show that South Asian emissions of CO2 are mitigated through green innovation, rents from natural resources, and consumption of RE, even though growth in FINTECH and urbanization are linked to higher emissions. The results highlight the importance of well-rounded policy strategies that mitigate the destructive effects of urbanization and the growth of FINTECH on the environment while simultaneously encouraging green innovation and RE. These findings align with theoretical prophecies and concrete evidence, highlighting the significance of sustainable development strategies for attaining environmental quality in the long run.

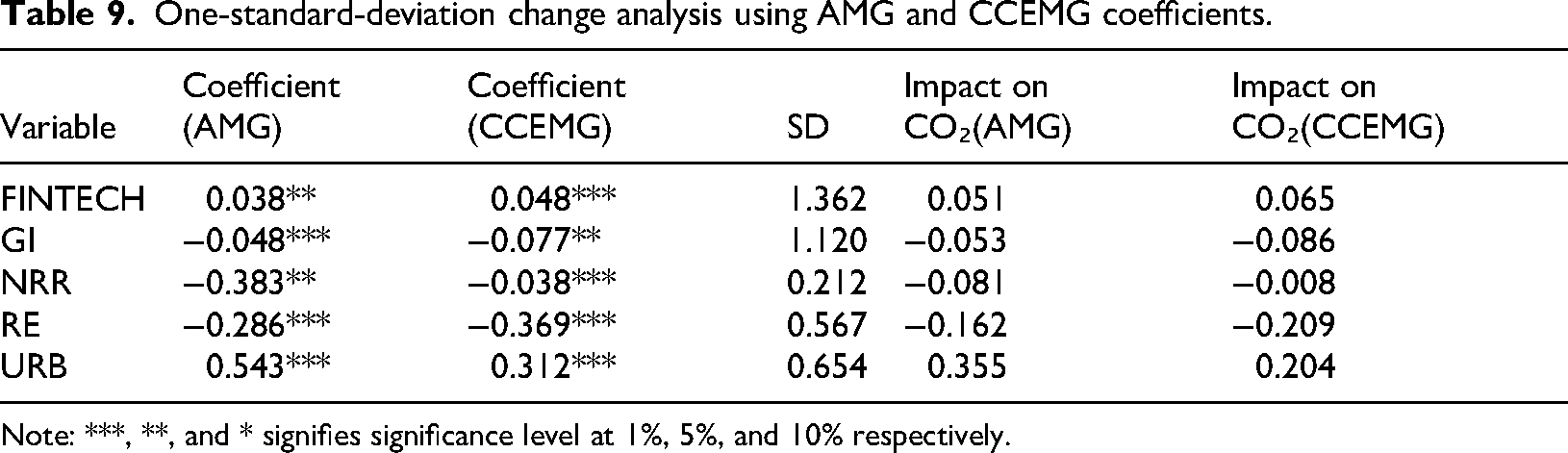

One-standard-deviation change analysis using AMG and CCEMG coefficients

Table 9 shows one unit change in standard deviation in each variable of the study and its impact on CO2 emissions, using AMG and CCEMG coefficients. As per the results of the table, RE has the strongest impact on lowering CO2 emissions (0.162 and 0.209 units) with a one-unit increase in standard deviation. A one-unit increase in GI standard deviation also reduces the CO2 emissions by 0.053 (AMG) and 0.086 (CCEMG). While a one-unit increase in Urbanization standard deviation increases the carbon emissions by 0.355 (AMG) and 0.204 units (CCEMG), this indicates the high energy demand for the expansion of urbanization activities. NRRR has a moderate reduction effect on carbon emissions as it reduced emissions 0.081 units (AMG) and 0.008 units (CCEMG) with a one-unit increase in the standard deviation of the respective variable. This reduction effect shows effective use of resource rents for green and sustainable projects.

One-standard-deviation change analysis using AMG and CCEMG coefficients.

Note: ***, **, and * signifies significance level at 1%, 5%, and 10% respectively.

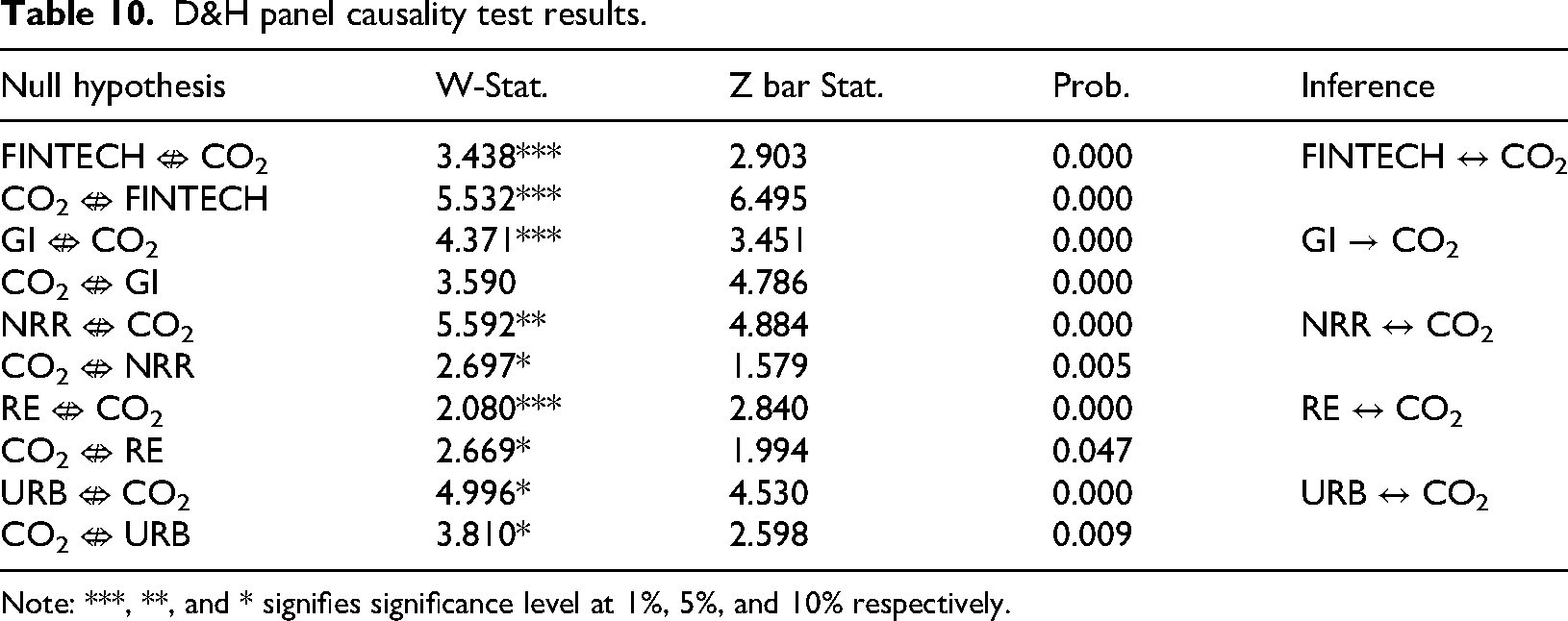

Dumitrescu Hurlin panel causality

Several important variables in South Asia, including green innovation, FINTECH, rents from natural resources, consumption of RE, and urbanization, are shown to have a directional causative relationship with CO2 emissions according to the Dumitrescu and Hurlin (D&H) panel causality test (Table 10). An interactive relationship between increasing FINTECH activity, which frequently entails high energy consumption and rising CO2 emissions, is suggested by the bidirectional causality between the two.

D&H panel causality test results.

Note: ***, **, and * signifies significance level at 1%, 5%, and 10% respectively.

This shows that changes in environmental outcomes may relate to FINTECH, and conversely, the state could affect the dynamics of FINTECH. On the one hand, FINTECH could increase emissions if the rise in energy use for data centers, the digital economy, and blockchain applications is significant in energy grids that are largely powered by fossil fuels. But alternatively, it can also encourage green financial activity (i.e., for investments that align with ESG, paperless banking, low-carbon transactions, etc.), leading to potential emissions reductions under some policy regimes. This ambivalent role is ascribed to the theoretical lens of ecological modernization, which argues that the environmental implications of technology are contingent upon regulatory and institutional context. Conversely, increased CO2 emissions, which can be associated with urbanization and climate stress, or environmental degradation, are also likely to increase demand for sustainable finance, impact investing, or FINTECH for energy access. In India and Bangladesh, higher pollution is associated with increased policy commitments to fostering green FINTECH ecosystems. Thus, our results are in line with that.124,125

The reciprocal influence between CO2 emissions and NRR suggests that resource extraction and use, when not sustainably managed, contribute to higher emissions. Conversely, increasing emissions may drive resource management policies that prioritize sustainable practices, thereby influencing the rents derived from natural resources. This bidirectional relationship lines up with the judgments of Bekun et al. 140 and Khaddage-Soboh et al., 141 showing that resource abstraction and CO2 emissions mutually reinforce one another, especially when environmental management practices are insufficient.

Empirical evidence suggests that RE reduces emissions, which in turn reinforces renewable adoption to meet environmental standards. This suggests that higher CO2 levels may encourage greater reliance on renewable sources and that greater adoption of RE can directly reduce emissions.134,142

Given the two-way causation between urbanization and CO2 emissions, it stands to reason that industrialization and increased energy demand cause emissions to rise as cities expand, and higher emissions can prompt urban planning reforms to improve environmental quality. This result is coherent with what Ali et al. 138 and Liu et al. 139 found that, in the absence of sustainable urban policies, urbanization tends to increase emissions. Carbon dioxide (CO2) emissions and socio-economic variables like urbanization, resource management, RE usage, and FINTECH are constantly influencing one another, as shown by these D&H panel causality results. To promote sustainable development in a balanced manner, South Asian policymakers could use these insights to build integrated strategies that deal with the direct and feedback impacts of these variables on emissions.

Conclusion and policy suggestion

Conclusion

The existing research focused on checking the imprint of FINTECH, green innovation, RE, NRR, and urbanization on CO2 emissions in the South Asian region from 1995 to 2022. This study analyzes how these factors facilitate attaining sustainable development goals (SDGs) and help resolve the world's environmental problems, especially in South Asia. To strengthen the consistency and validity of the study, several statistical tests, such as slope homogeneity (SH) and cross-sectional dependencies (CSD), panel unit root, and panel co-integration, were performed. AMG and CCEMG tests are employed to assess the association between variables. This panel causality test was also used in this study to examine the causal relationship between FINTECH, green innovation, NRR, RE, urbanization, and CO2 emissions.

The results show FINTECH is positively associated with carbon emissions. Although FINTECH promotes economic activities, increases financial inclusion, and makes easy access to green financing, on the energy-intensive side, like blockchain, crypto mining, leads to more emissions. This highlights the need to link FINTECH with the goals of sustainability in South Asia. The findings of the study also challenge the resource curse hypothesis by supporting the arguments that South Asian resource rents can be used for sustainable development. This proved that the proper management of NRR leads to a low-carbon economy in the region.

Further, the study's results suggest that the use of green innovation and RE will help to combat the problem of environmental degradation in the South Asian region. The study provides a pathway to the leaders on how they can alter their current strategies to environmentally friendly strategies by considering the current study to accomplish the goal of sustainable development. These insights of the study are aligned with the World's SDGs, especially SDG7 (Affordable & Clean Energy), SDG8 (Decent Work & Economic Growth), SDG9 (Industry Innovation & Infrastructure), and SDG13 (Climate Action). This study emphasized green innovation, NRR, and RE to improve environmental conditions in the region.

Policy suggestions

This study highlights the multifaceted interplay of FINTECH, green innovation, NRR, RE, and urbanization in shaping CO2 emissions and achieving SDGs in South Asian economies. Based on the unique circumstances of the region, we suggest some empirical insight-based policies for the legislators. The policymakers can get the dual advantage of economic progress and environmental improvements by converting these policies into actions. These policies support SDGs, which were suggested by the World leaders to combat the problem of environmental degradation and develop a sustainable, inclusive, and more prosperous future for the next generations.

There is a need that policy makers should develop region-specific rules to integrate FINTECH with green finance. For instance, India and Bangladesh could establish a green FINTECH system that can support investment in low-carbon and RE technologies. Pakistan has an opportunity to promote microfinancing for RE source (solar energy) initiatives, and by providing access to banking services in rural areas. Further, tax incentives and subsidies for green bonds can accelerate the financing for sustainable infrastructure.

The use of renewable energy sources has the potential to reduce CO2 emissions. Further, FINTECH has the potential to accelerate this process by providing financing for RE development through a public‒private partnership. Countries like Nepal can engage in microgrid technology backed by digital financial services, while Sri Lanka has the potential to expand its solar financing through the development of mobile payment systems. This initiative directly aligns with SDG7 (Affordable & Clean Energy). Further, South Asian countries should take serious steps for digital literacy, especially in remote areas of Pakistan, Bangladesh, and India. Governments of these countries can provide the solution to clean energy by integrating mobile banking with green energy access.

The countries in South Asia can make better use of resource rents by investing in green technologies and renewable infrastructure. For example, Pakistan's green energy initiative and India's Bio-energy project can be expanded by the revenues of the countries’ rents received from the resources. In Addition to this, effective resource management policies should be implemented for environment friendly resource extraction process in these countries. These policies will also lead nations to accomplish the SDG8 (Decent Work & Economic Growth).

Policymakers should invest more in R&D so that the share of green technologies and green energy consumption is enhanced in these economies. Governments in South Asia should organize R&D grants targeted at clean-tech startups, co-locate technology incubators that specialize in green hardware and software, and extend tax credits to private-sector R&D related to climate-resilient agriculture and smart grid systems. Tax incentives from the government are needed to promote green innovation in production processes. These recommendations are aligned with SDG9 (Industry Innovation & Infrastructure).

The negative effects of urbanization can be reduced by the application of active policies. The nations of the South Asian region should introduce proper plans for recycling, waste management, and transportation. The hybrid transport system should be introduced in countries to lessen the dangers of traditional fossil fuels. Energy-efficient and clear sources of energy should be introduced in production and service processes. There is a need in this region to introduce sustainable tourism policies, such as the use of efficient and clean energy transport and ecological facilitation for accommodations.

Although this analysis provides regional-wide policy suggestions for South Asia as a whole, we recognize that there is large heterogeneity across South Asian countries in FINTECH development, level of urbanization, energy infrastructure, and innovative capabilities. For instance, India has the opportunity to regulate the environmental impact of hyperscale data centers, taking into account mandatory energy disclosure and blockchain carbon accounting. India's advanced infrastructure allows it to have a head start in green digital finance, including in ESG-friendly lending apps and in green bonds platforms. FINTECH-enabled investment platforms could support financing for clean energy. On the other side, Pakistan's power and digital infrastructure offer different challenges and opportunities. There is a need for Pakistan to focus on digital financial inclusion in its energy-poor regions, connecting mobile banking solutions to solar microfinancing schemes.

The countries like Nepal and Bangladesh with much less comprehensive digital infrastructure and lower energy diversification may focus more on integrating basic mobile banking with clean energy access programs. While Sri Lanka can improve finance for climate-resilient infrastructure with the use of FINTECH-supported insurance and catastrophe bonds. As a middle-income nation with rising urbanization, the incorporation of green transport payment systems and EV-linked FINTECH platforms into policy frameworks can also support a reduction in urban emissions.

Now, there is a need to strike a balance between the economy and the ecology for sustainable development in South Asia. Digitalization, urbanization, and resource use are crucial to speed up economic growth and reduce poverty, but these efforts should be supported by policies for reducing damage to the ecosystem. This could be done through the use of green growth narratives that link investment in clean technologies and circular economy models with productivity and emissions extraction. Governments must encourage coordination between finance, energy, and environment ministries to integrate national development plans with climate objectives. There can also be financial integration of environmental protections into the heart of economic planning. South Asian countries can make certain that the growth of today will not undermine environmental sustainability for the generations to come.

To sum up, there is a need for regional cooperation for promoting sustainable development. Green energy projects, environmental regulations, and FINTECH development should all be coordinated with all countries of the region. The regions can strengthen their ability to combat environmental problems and promote sustainable growth by sharing information, best practices, and collaborative actions.

Limitations and future direction

This Study has its limitations, which can become the prospective research direction for the researchers. First, our FINTECH index is based upon FINTECH adoption obtained from Crunchbase databases. It may therefore not fully account for unregistered digital finance, such as the use of mobile money in rural areas, locally owned e-wallets, or peer-to-peer lending networks in some parts of the region. Future research can explore alternative data sources, such as mobile money services networks. Further, using annual data in this study may also hide the short-term changes and seasonal effects. Future research can use the high-frequency data to analyze the CO2 emissions and innovation cycles.

Secondly, we used AMG and CCEMG estimators to correct for heterogeneity and cross-sectional dependence, and endogeneity issues, and forward-looking feedback effects cannot be entirely precluded, as previously noted. Future studies can also use the alternative models seeking to model feedback loops and mediating variables. Finally, this study relied solely on CO₂ emissions as an indicator of environmental degradation. Its popularity, policy implications, and the data sets available. However, this focus is a limitation, considering that methane (CH₄), nitrous oxide (N₂O), and particulate matter (PM2.5) are also important components of the environmental quality, especially in the rapidly urbanizing areas. In subsequent research, a wider range of environmental indicators should be used to determine the complete ecological consequences of FINTECH, urbanization, and other digital transitions.

Footnotes

Ethics approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Availability of data and materials

The data can be obtained from the corresponding author upon reasonable request.