Abstract

Neuroeconomics is an interdisciplinary approach that combines cognitive psychology, economics, and neurobiology in studying how people make decisions. A peculiar feature of this approach is the use of neuroscientific methods for individuating the neural correlates of the cognitive processes involved in decision-making. The rationale motivating this use is that neurobiology can provide physical evidence for theoretical and abstract constructs that define the cognitive processes responsible for the human deliberative capacity. In this contribution, I’ll provide a critical account of the above assumption. I’ll argue that, in order to consider neurobiological data as reliable empirical evidence for decision-making theories, neuroeconomists need to adopt a very strong assumption about the relation of brain activity to mental states: mind–body identity theory. Without such an assumption, we should consider these data only in terms of correlation and thus too loose to be truly informative.

Keywords

In the beginning of their classic 1984 paper, the psychologists Kahnemann and Tversky pointed out that many different disciplines (such as mathematics, statistics, psychology, sociology, economics, philosophy, etc.) share the topic of decision-making (p. 341). They attribute the great interest in this topic to the fact that it addresses both normative and descriptive questions. The former kind of questions deal with the nature of rationality and the logic of decision-making. By contrast, the latter regard people’s beliefs and preferences as they are, not as they should be.

It is commonly argued that economics aims to respond to normative questions (Simon, 1959, pp. 253–254), whereas psychology aims to respond to descriptive ones. This can be true for psychology, but not necessarily for economics. In fact, in the last two decades, some economists have begun to pay attention to the methods and results of psychological research, and create the base for a new descriptive discipline known as “behavioural economics” (Camerer, 2003, p. 1673; Camerer, Loewenstein, & Prelec, 2005, p. 9). Very briefly, behavioural economists use the findings and methods of cognitive psychology to understand how people take their decisions (Zak, 2004, p. 1737).

It is worth noting that, more or less in the same period, some cognitive psychologists have started to look at the neurobiological data and tools and have created a new interdisciplinary field known as “cognitive neuroscience.” Cognitive neuroscience aims at providing a means to test the accuracy of cognitive psychology’s constructs by assessing how the nervous system performs the cognitive processes described by these constructs (Ward, 2006, p. 6). In doing this task, cognitive neuroscientists explore and define the relationships between specific neuroanatomical structures of the nervous system and specific cognitive operations considered to be responsible for behaviour (Reber & Reber, 2001, p. 464; Tranel & Damasio, 2000, p. 119).

Now, if we assume that behavioural economics is strictly connected to cognitive psychology and, in turn, cognitive psychology to cognitive neuroscience, it is easy to understand why some experimental economists and cognitive psychologists have focused their attention on the neural underpinnings of the mental processes involved in decision-making. In such a view, neuroeconomics is a sub-field of cognitive neuroscience that attempts to combine not only neurobiology and cognitive psychology, but also economics (or, at least, behavioural economics).

It is interesting to note that, in neuroeconomic literature, the role attributed to cognitive psychology and behavioural economics is different from that assigned to neurobiology. In fact, whilst the former’s role is to provide conceptual tools for describing and modelling decision-making capacity, the latter’s role is to offer methods for quantitatively analysing the mechanisms responsible for this kind of capacity (Glimcher & Rustichini, 2004, p. 447; Kenning, Plassmann, Deppe, Kugel, & Schwindt, 2005, p. 341). In such a view, neurobiological data appear to be invested with a crucial evidentiary function (Antonietti, 2010, p. 208), equal to (or more important than) that attributed to observable behaviour.

However, this methodological division of labour (along with various other topics regarding the relationships among these three disciplines) is a matter of heated debate. Quite recently, I witnessed a clear example of such a debate at a one-day meeting about the connections among the methodologies of psychology, economics, and neurobiology in an Italian university. On this occasion, a neuroscientist presented a few slides showing the results of a series of recently published neuroeconomic studies. During the debate after the talk, an economist said that she found the results very interesting but that, unfortunately, she didn’t really understand their relevance to economics. The neuroscientist was not sure how to reply, and said that the data she expounded weren’t intended to challenge economic and psychological theories, but that to know how the brain works is always something scientifically interesting.

This example of incommunicability is not of course representative of the debate between economists and cognitive neuroscientists. In fact, if we take a look at the neuroeconomic literature, we can find many examples of economists with a good knowledge of cognitive neuroscience’s methodology and, vice versa, cognitive neuroscientists with a solid expertise in economic methods. Probably, the reason why most neuroeconomic papers deal with methodological issues is that neuroeconomics is still a young interdisciplinary field. In this article, I’ll focus upon a crucial methodological and conceptual issue, that of the definition of psychological and economic constructs by neuroeconomists.

Neurobiological constructs versus psychological and economic constructs

The neuroeconomic approach puts emphasis upon the methods and techniques of neurobiology in searching for the neural mechanisms underlying the cognitive processes involved in decision-making. In fact, many neuroeconomists assume that neurobiology can suggest specific functional forms to replace “as if assumptions” that have never been empirically well supported (Camerer et al., 2005, p. 11). These “as if assumptions” are the theoretical constructs of economics and psychology (Kenning & Plassmann, 2005, p. 343).

In all scientific disciplines, theoretical constructs are considered part of the theoretical vocabulary, and are distinguished from those pertaining to the observational vocabulary because they cannot be either observed or directly measured, but only postulated through theorizing. More precisely, theoretical constructs are assumed to be autonomous from those referring to observable entities, and thus cannot be eliminated in their favour in any way, although they must always have empirical content and explicit connections with the observational vocabulary (Hempel, 1952, p. 31, 1958, pp. 41–71; see also Fetzer, 2010). There are many examples of these constructs in every branch of science, in physics as well as in cognitive psychology and in behavioural economics. In defining their meaning, the physicist, the cognitive psychologist, and the economist work in the same way: that is, through theorizing.

However, at the moment, the physicists’ appeal to theorization shows an important difference from that of cognitive psychologists and economists. In fact, most of the theoretical constructs of cognitive psychology and economics are abstract, which means that they do not yet have a material and concrete reference (on this point see Fodor, 1968, p. 84; Neisser, 1967, pp. 6–7). In other words, the theoretical vocabulary of physics appears to have quite strong connections to the observational vocabulary, contrary to that of psychology and that of economics. In this sense, most of the theoretical constructs of psychology and economics appear to be mainly abstract and lacking in empirical content.

Thus, the abstract character of psychological and economic constructs seems to be the main target of the neuroeconomists’ arguments. For example, let us consider the conclusion made by the neuroscientist Glimcher and the economist Rustichini in the summary of their important 2004 review article: “The recent research we have been surveying describes how desirability [emphasis added] is realized as a concrete object [emphasis added], a neural signal in the human and animal brain, rather than a purely theoretical construction [emphasis added]” (p. 452). In my opinion, the previous quotation shows the ambitious research programme of neuroeconomics: to lose the abstract character of psychological and economic terms by finding the “material proof” of their existence.

According to neuroeconomists, such a material proof can be found in the brain (or, by a further extension, in the nervous system). In this sense, they a priori postulate that a specific psychological or economic construct must refer to a specific function performed by the brain. In neuroeconomic literature, this position can be found explicitly formulated in the following three points (see, e.g., Camerer et al., 2005, pp. 9–10; Kenning & Plassmann, 2005, pp. 343–344):

Theoretical constructs cannot provide a solid ground either for economics or for psychology. This is because, by virtue of their abstractness, these constructs are neither observable nor measurable in principle.

Neurobiological constructs, by virtue of their concreteness and physicality, can give “flesh and blood” to abstract economic and psychological constructs. In other words, neurobiological constructs can provide objective (or intersubjective) evidence that serves as “anchor points” for the abstract constructs of psychology and economics.

The object of study of cognitive psychology and behavioural economics must be the same as that of cognitive neuroscience: the brain and its functions. Only in this way behavioural economics, cognitive psychology, and neurobiology can be unified in a single discipline aimed at developing a single unified theory of deci- sion-making behaviour (Glimcher & Rustichini, 2004, p. 447).

As we can see, these three points are strictly intertwined. In fact, the first point aims at defining what are for neuroeconomists the problematic features of cognitive psychology and behavioural economics, whereas the second and the third aim at proposing a possible solution to them.

“Naturalizing” economics and psychology

In the previous section I pointed out that neuroeconomists’ aim is to provide physical “anchor points” for the constructs of the economic and psychological theoretical vocabulary by appealing to the neurobiological observational vocabulary. Following this line of reasoning, neuroeconomists assume that the focus upon the nervous system and its functioning allows us to dispose of more objective data and quantitative methods for studying decision-making behaviour than those offered by cognitive psychology and behavioural economics (Glimcher, Dorris, & Bayer, 2005, p. 215; Sanfey, Loewenstein, McClure, & Cohen, 2006, p. 111). In this view, decision-making can be studied through the experimental methods typical of natural sciences (Glimcher et al., 2005, p. 254), and this should guarantee to make reliable predictions of the phenomena of interest (McCabe, 2008, p. 345). In other words, neuroeconomists argue that, through the methods of cognitive neuroscience, they can study decision-making behaviour in a highly controlled setting like a laboratory.

But what exactly does a cognitive neuroscience (and thus neuroeconomics) experiment consist of? Very briefly, it consists of a comparison between the nervous system’s activities (measured through neuroimaging techniques and physiological indexes) of two groups of participants (or, in some cases, of two single participants) performing two different tasks. If there is a difference in these activities, it is possible to infer that different areas of the nervous system underlie different cognitive processes (Camerer et al., 2005, p. 12; Craver & Alexandrova, 2008, pp. 382–383, 396).

An example of this procedure can be the following: A researcher aims to assess whether the brain areas devoted to speech are distinguished from those devoted to syntax. To perform this assessment, she tests one group with a speech task and the other with a syntax task. The participants of both groups have to perform these tasks and, during such a performance, their brains are scanned with the fMRI, a type of magnetic resonance imaging that permits one to observe brain activity whilst it is taking place (Reber & Reber, 2001, p. 289). Thus, the result of these scans is a certain number of images representing which areas of the brain were activated during the task. The images of the two groups are then compared through a series of complex statistical analyses, and, if they produce different results, the researcher will infer that the cognitive processes devoted to speech are “dissociated” from those devoted to syntax.

This experimental procedure is called “the dissociation method” and is based upon an empirical assumption known as “localization.” According to this claim, specific cognitive operations have relatively defined and relatively circumscribed cortical locations (Reber & Reber, 2001, p. 401). For neuroeconomists, by localizing nervous system activations during a specific decision and relating them neuroanatomically, brain imaging methods allow visualization of various dissociated areas responsible for decision-making (Kenning & Plassmann, 2005, p. 352). In other words, these methods allow us to find a physical proof of the existence of the cognitive processes that determine our choice behaviour.

An example from neuroeconomic research: The case for expected utility

In this section, I want to show an example of how neuroeconomists deal with a central notion of economics and psychology concerning decision-making, that of expected utility, by using the dissociation method, and thus by applying the principle of localization described above.

In 1738, the Swiss mathematician Daniel Bernoulli tried to give an account of why people tend to be averse to risk and why this risk aversion decreases with increased wealth. He pointed out that the traditional account of this question did not take into consideration a very simple fact: that is, that not every person follows the same rules for evaluating a certain gamble (Bernoulli, 1738/1954). Thus, he argued that the value of an item must not be based on its price, but rather on the utility it yields. The price of the item is dependent only on the thing itself and is equal for everyone; the utility, however, is dependent on the particular circumstances of the person making the estimate. (p. 23)

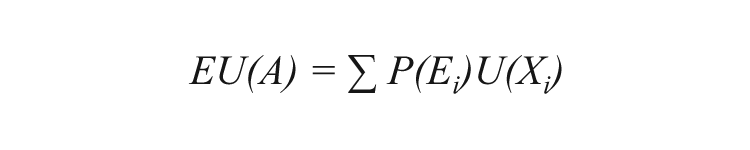

Following this line of reasoning, we can say that, for example, the expectation of gaining €1,000 in a lottery is differently (subjectively) valued by a poor and a rich person, although the amount of money to be won is (objectively) the same. In this sense, people seem to assess prospects not on the basis of the expectation of their monetary outcomes of a gamble (the prize of €1,000 in the previous example), but rather on the basis of the expectation of the subjective value (or expected utility) of these outcomes. In other words, for Bernoulli, the traditional maxim according to which the most advantageous gamble to choose is the one with the expectation to win the highest amount of goods or money seems to work at best as a rule of thumb and thus should be substituted by the notion of expected utility as a more reliable principle. Bernoulli’s expected utility can be formulated in the following way (Slovic, 1995, pp. 91–92):

where: (a) EU(A) represents the expected utility of a course of action A having a certain number of consequences X1, X2,… Xn, depending upon a series of events E1, E2,… En; (b) P(Ei) represents the probability of the ith outcome of the action A; and (c)U(Xi) represents the utility of that outcome.

As I said above, the appeal to expected utility allowed Bernoulli to explain why people are generally averse to risk. For a better understanding of this point, let’s consider the following example: A player has to choose between two prospects, A and B. A is a gamble that offers an 80% chance to win €1,200 (with a 20% chance to win nothing) and B is a sure gain that offers a 100% chance to win €900. As most of us would probably do, people generally tend to choose B because they consider the expected utility of its outcome, even though A has a higher expectation [in fact, (0.80 × 1,200) + (0.20 × 0) = €960 is higher than (1.0 × 900) = €900]. In other words, people tend to give a higher (subjective) value to the certainty of winning €900 (by choosing gamble B) than to the huge probability of winning €960 (by choosing gamble A).

It is important to stress that Bernoulli wanted not only to explain and describe risk aversion in general terms, but also to account for the different risk attitudes of rich and poor people (Kahneman, 2002, p. 460). For this reason, he conceived utility to be strictly related to the person’s states of wealth (or, to use his words, to the “quantity of goods possessed” by a person; Bernoulli, 1738/1954, p. 25). More precisely, “[I]n the absence of the unusual, the utility resulting from any small increase in wealth will be inversely proportionate to the quantity of goods previously possessed” (p. 25). In this view, the little money that may be significant to a poor person would be considered almost irrelevant by a rich one. This is the reason why a poor merchant would be more inclined to buy insurance for protecting his goods than a rich one. In other words, by considering the previous example, the rich should be more disposed to choose gamble A than the poor.

As I pointed out above, Bernoulli’s analysis of utility is a central and very debated issue in economics and I do not intend here to discuss its validity and the debate around it (see Savage, 1954, pp. 91–104 for an interesting historical account and Schoemaker, 1982, for an exhaustive review). What I want to do is simply to make an example of how neuroeconomists deal with this and similar constructs. Thus, I consider a 2005 article by the neuroscientists Knutson and Peterson where they reported to have found a neural mechanism responsible for the computation of Bernoulli’s expected utility (p. 305).

The empirical evidence Knutson and Peterson reported is all based upon the results from a series of fMRI studies with the Monetary Incentive Delay task. This task is a computer game designed to elicit neural responses to monetary incentive anticipation and outcomes. It is composed of a certain number of trials, each one having the following format: First, a shape cue indicating whether participants can respond to gain money, to avoid losing money, or to not respond for no monetary outcome is presented. Second, participants wait for a delay period during which they have to fix a crosshair in the centre of the screen. Third, participants see a rapid target to which they must respond by pressing a button: if they respond while the target is on the screen, the trial is coded as a “hit”; otherwise, the trial is coded as a “miss.” Fourth, depending upon which shape cue was presented, and whether the trial was coded as a “hit” or a “miss,” participants receive feedback indicating how much they won or lost on that trial and their cumulative total up to that point (Knutson & Pearson, 2005, p. 308). To reduce possible learning effects, participants receive previous training on the task and take a test indicating that they are explicitly aware of the incentive contingencies prior to entering the fMRI scanner. In the end, the experimenter also shows participants the cash they can win and informs them that they will leave the experiment with the amount they accumulate during the experiment.

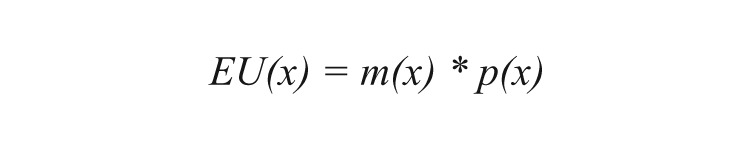

The experimental data showed an increasing activation of the nucleus accumbens (a cerebral region in the ventral striatum) for increasing anticipated gains, but not for losses (Knutson & Pearson, 2005, p. 310). Knutson and Peterson argued that these results permitted to infer which are the neural areas implementing the first term of Bernoulli’s formula for expected utility (as they formulate it). In other words, they argued that Bernoullian utility could be expressed in this way:

where m(x) indicated the scaled magnitude (the amount of money that can be gained or lost at Monetary Incentive Delay task) and p(x) represented the probability of the rewarding outcomes (x).

Thus, because the nucleus accumbens activated in proportion to the magnitude of anticipated monetary gains, Knutson and Peterson (2005) concluded to have identified a neurophysiological mechanism (that means, to have found the “physical evidence”) for the computation of the first term m(x) (p. 312). For this reason, according to Knutson and Peterson, their “findings represent a step towards a neural reconstruction of expected utility” (p. 313).

The relevance of mind–brain identity theory

As I pointed out above, for neuroeconomists, neurobiology can provide physical “anchor points” for psychological and economic constructs. By assuming a physical reference, these constructs can be open to some form of observation or, at least, of detection. It is important to note that, in general, neuroeconomists do not appear to support an elimination of the theoretical vocabulary of cognitive psychology and behavioural economics in favour of an observational neurobiological one. Rather, when they argue about the replacement of the “as if assumptions” that have never been empirically well supported, they actually deal with the definition of the nature of the entities to which the constructs of cognitive psychology and behavioural economics refer.

In other words, according to this view, the psychological and economic entities are conceived as physical entities, more precisely as neurobiological entities observable or detectable through neurophysiological or neuroimaging techniques. It is important to note that this is not an empirical assumption that can be demonstrated a posteriori, but rather a philosophical claim assumed a priori known as “mind–brain identity theory.” Such a claim holds that mental states and processes must be conceived as identical with cerebral (or physiological) states and processes (Kim, 1998, pp. 53–54; Smart, 2000).

But, in this case, what does “identical” mean? Let us consider a simple example proposed by the philosopher Kim (1998): Why does lightning occur only when there is an electrical discharge among the clouds or between clouds and the ground? Because lightning is nothing more than the electrical discharge involving the clouds and the earth. Thus, because lightning and electrical discharge are not two distinct phenomena but only one, this means that they are identical (p. 50). In the same way, there are no mental states over and above the neural or physiological processes: Mind and brain refer to the same phenomenon (p. 52). According to identity theory, as in the past the empirical and theoretical research in meteorology has shown us the identity relation between lightning and electrical discharge, so in the future the empirical and theoretical research in cognitive neuroscience will show us that specific mental states are identical to specific neural or physiological states.

It is important to note two important features of identity theory: First, it does not assume that every mental state is caused by some physical state (specifically, by some cerebral or physiological state), but that the mental is only a physical state (cerebral or physiological; Guttenplan, 1994, pp. 91–92); second, it does not say that non-physical (in this case, non-cerebral and non-physiological and thus mental) states are really physical (cerebral or physiological), because this view does not conceive any sort of non-physical (cerebral or physiological) state (Crane, 2001, pp. 51–52). In my opinion, neuroeconomists propose to redefine the abstract constructs of cognitive psychology and behavioural economics used for explaining behaviour in physical terms by appealing to these two features. In this sense, although I have never found a declared appeal to any version of identity theory in neuroeconomic literature, I can maintain with a certain degree of certainty that many neuroeconomists support a version of it.

In philosophical literature, identity theory is generally found formulated in two versions: that is, in terms of “tokens” or of “types.” The distinction between tokens and types is a distinction between instances and sorts of things (Guttenplan, 1994, p. 597). A token is a single individual thing whereas a type is a class of tokens showing a similarity in some respect (Rey, 1997, p. 548). For example, we have only one type of Bukowski’s masterpiece Factotum (because every copy of this book consists of the same words in the same order), but many tokens of it (because there are different copies of it in various formats). Applied to the mind–brain relation, we have a type identity if we assume that an instance of a certain mental state must always be considered as an instance of a specific cerebral or physiological state. By contrast, we have a token identity if we assume that a single instance of a particular mental state occurring in a certain subject at a certain time is identical only with a particular cerebral or physiological state in that subject at that time.

I think that neuroeconomists (and cognitive neuroscientists in general) tend to support a type identity rather than a token identity claim. This is mainly for two reasons: First, token identity theory is much weaker than the type one, and there are some doubts about its reliability in providing a real account of the relation between mind and body. In fact, by adapting an example from the philosopher Crane (1994, p. 483), it is as if we would explain why all Italian Prime Ministers have been white males by simply asserting that each particular Italian Prime Minister is identical to some particular white male. Second, at the core of the cognitive neuroscientific (and thus neuroeconomic) practice, there is the attempt to identify specific neurobiological or neurophysiological types with specific psychological types (Bechtel & McCauley, 1999, pp. 68–69; Bechtel & Mundale, 1999, pp. 202–203). This is because the localizationist assumption at the basis of the dissociation method discussed above is strictly connected to type identity theory. In fact, every attempt to localize a specific cognitive process in a specific nervous system activity or area implies that there exists a type identity relation between a particular mental operation and a particular neural mechanism (Bechtel, 2008, p. 69).

In neuroeconomic literature, we can find many examples that appear to refer to type identity theory (or, at least, that appear to indicate an adherence to it by neuroeconomists). For example, let us consider the so-called “syllogism of neuroeconomics” proposed by the neuroscientist Padoa-Schioppa (2008, p. 451):

If neurobiological data will lead to better psychological theories.

If psychological theories will lead to better economic theories of decision-making.

Then, neurobiology will lead to better economic theories of decision-making.

It is important to stress that Padoa-Schioppa justified (1) through the following identitistic claim: [T]he distinction of neuroscience and psychology is arguably fictitious. Although the levels of description are certainly different, cognitive processes and brain activity are ultimately one and the same. The problem is not reducing the mind to brain activity – the mind is brain activity. The problem is to understand the mind/brain. (p. 454)

Thus, following the previous syllogism, “economic theories of decision-making” can also be identified with neurobiological ones. Another example of the appeal to identity theory in neuroeconomics can be found in Glimcher et al. (2005) in reference to the notion of expected utility: Neoclassical theory has always made the famous as if argument: it is as if expected utility was computed by the brain. Modern neuroscience suggests an alternative, and more literal, interpretation. The available data suggest that the neural architecture actually does compute a desirability for each available course of action. This is a real physical computation, accomplished by neurons, that derives and encodes a real variable. (p. 220)

As clearly pointed out by the economist Zak (2004, p. 1741), in this statement Glimcher and co-workers infer from their studies that the expected utility function is nothing but a physiological or neural property (other similar considerations can be found in Camerer, 2008, p. 370 and Sanfey et al., 2006, p. 113).

Although Padoa-Schioppa (2008, pp. 450–451) declares himself unsympathetic with reductionism, if we accept that a mental property is (identical with) a neural one (and that the distinction of neuroscience and psychology is arguably fictitious), we must also accept that the mental is in principle reducible to the neural (and that cognitive psychology’s theories can be reduced to neuroscience’s theories) at the ontological and/or at the explanatory level. In other words, the acceptance of identity theory means acceptance of a form of reductionism (Crane, 2001, pp. 51–55; see also Ross, 2008, pp. 479–482). I think that, if neuroeconomists are truly convinced that neurobiological data can permit the making of better predictions than behavioural data (Rustichini, 2005, pp. 201–202), they should endorse the type identity claim and its strong reductionistic implications.

Matters of correlation

Type identity theory is a highly demanding assumption, since it postulates that mental states or operations are only cerebral processes, not merely correlated with cerebral processes (Smart, 2000). For understanding this point, it is necessary to clarify what correlation actually means. Basically, the term “correlation” refers to a statistical notion that, in its simplest form, describes the relationship between two (or more) variables usually expressed as the dispersion of data points about a graphed line relating the two (or more) variables (Uttal, 2003, p. 124). Thus, by taking two variables, A and B, we can calculate a number (called “correlation coefficient”) indicating the degree and direction of the relationship between them. This coefficient can take any value from −1.00 (as one variable changes, the other changes in the opposite direction by the same amount), from 0.00 (as one variable changes, the other does not change at all), to +1.00 (as one variable changes, the other changes in the same direction by the same amount; Field, 2005, p. 741; Reber & Reber, 2001, p. 159).

The issue of correlation deals with that of causation and its interpretation is a matter of controversy among statisticians (for an interesting article on this point, see Aldrich, 1995). For our aims, it is sufficient to say that highly significant values of the correlation coefficient for two variables do not necessarily indicate that a direct correlation among them actually exists (Aldrich, 1995, p. 364). This is because other “third factors” could jointly determine the high correlation value between the two variables, A and B, and it seems to be practically impossible to eliminate them even from the best-designed experiment (Uttal, 2003, pp. 125–126). Furthermore, in cases of high correlation values in which we can exclude the intervention of other third factors, it appears to be very difficult to infer the existence of a direct causal relationship. In other words, in such cases, it is very easy to commit the fallacy of interpreting a certain correlation as indicating a direct causal relationship where none actually exists (Aldrich, 1995, p. 370, 374).

This point appears to be clear in the following example (Schield, 1995, pp. 4–5): suppose that, in every election for the US President, the taller of the two candidates has won the election. Thus, we have a perfect positive correlation (+1.00) between the two variables considered: that is, height and the number of elections previously occurred. Now, it is clear that, although in this case we have at disposal such a perfect correlation, without some good reasons to envision this relationship as persisting, we are not allowed to conclude that height is so strongly associated with any of the qualifications of being elected President. In this sense, we can say that the strength of the correlation coefficient considered per se is never sufficient for inferring causality (at best, it may be an important sign of it; Schield, 1995, p. 1). Even if +1.00 or −1.00 correlation between two phenomena that are reliably strictly linked (such as cigarette smoking and lung cancer) were found, we should not be allowed to talk of the existence of a causal relationship (Uttal, 1998, p. 126).

Of course, this does not mean that a correlation index is a useless or inefficacious statistical tool. In fact, although a high correlation coefficient between two (or more) variables is not sufficient by itself for inferring a causal relationship also in presence of strong theoretical reasons, a zero or near-to-zero correlation coefficient between two (or more) variables is sufficient by itself for inferring the absence of a causal relationship also in presence of strong theoretical reasons. Let’s reconsider the previous example and suppose that there are solid motives for thinking that height has something to do with the US President’s electability, but no correlation between the two variables is found. We can conclude that our solid motives for believing in the existence of such a relationship are wrong and thus our theory can be rejected only on the basis of a simple correlation index.

Analogous considerations can also be made about the link between correlation and mind–brain identity. In this sense, even if we found a perfect correlation between a specific neural activation and a specific mental operation (which can be inferred only from the behavioural performance at a certain cognitive task), we should not take it by itself as an argument for the reduction of the latter to the former (or, vice versa, of the former to the latter). The reason for this was clearly explained by one of the pioneers of identity theory, the psychologist and philosopher Place in his classic 1956 paper. In this paper Place argued that, if we appealed to a mere (although systematic) correlation to establish an identity relation, we should be allowed to say that there exists an identity also in those cases “where we have no temptation to say that the two sets of observations are observations of the same event” (p. 49).

For example, the systematic observed correlation between the movements of the tides and the stages of the moon may not be interpreted as a good reason that the former phenomenon is the same as the latter. Rather, it may be interpreted as a good reason for speaking of a causal relationship of the latter phenomenon over the former. As we can see from this example, for speaking of correlation or of identity/reduction, we need to appeal to something more than a mere correlation. More precisely, we need to dispose of a certain number of logical criteria and a coherent body of empirical evidences of various sorts.

At the moment, such logical and empirical requirements do not appear to be well defined and established in cognitive neuroscience. For this reason, such a puzzling but crucial issue does not seem to be systematically discussed in the neuroeconomic literature, in spite of the many (pseudo)identitistic assumptions made by neuroeconomists. If we consider my references, we can find only a few mentions in Zak (2004, pp. 1740 and 1745) and a more articulated formulation in Kenning and Plassman (2005). In this latter article, Kenning and Plassmann pointed out that there are still many unanswered questions about the neurobiological measures used in neuroeconomics and that “in a strict sense most experiments are only able to give evidence for a correlation between fulfilling a specific task and brain activity of specific areas. This must not be misunderstood as a proof for an actual causal relation” (p. 352). The previous quotation seems to indicate that identity theory (upon which the methods of neuroeconomics and cognitive neuroscience are based) is not coherently followed in neuroeconomic practice. In fact, what neuroeconomists seem to do in their laboratories is to record two types of measure (the behavioural performance at a decision-making task and the neural or physiological activations occurring during it) and to try to correlate them. A clear example of the application of this correlative practice can be found in the Knutson and Peterson (2005) paper discussed above, but also in various others such as Montague and Berns (2002), Platt and Glimcher (1999), and Sanfey, Rilling, Aronson, Nystrom, and Cohen (2003)—only to quote the most influential and debated ones.

Personally, I agree with Kenning and Plassman’s cautions about neurobiological methods, but I am quite surprised that they expressed them in their article. In fact, in the introduction to their article (Kenning & Plassman, 2005, pp. 343–344), they enthusiastically pointed out that one of the main problems of psychology and economics is that their constructs are abstract and theoretical, and thus impossible to observe and objectively measure, and that the appeal to neurobiology and its methods can be the solution to this problem. However, on the basis of my previous discussion, this position would be plausible only if mind–body type identity theory were adopted and coherently applied. The fact that most of neuroeconomics’ findings and data are correlational appears to indicate that neuroeconomists are quite far from a full application of the highly demanding assumptions of type identity theory, and thus from a reduction of the mental to the neurobiological.

Concluding remarks

In this contribution I argued that, in order to unify neurobiology, cognitive psychology, and behavioural economics in a single discipline, most neuroeconomists tend to endorse a reductionistic outlook. This outlook amounts to the acceptance of any version of a demanding philosophical claim known as type identity theory. According to my analysis, it appears that, at present, there are not strong empirical and conceptual reasons for accepting such a claim, and thus to assume that neurobiological constructs can provide solid “anchor points” for psychological and economic constructs. In this sense, neurobiological data cannot provide, at present, better insights on psychological and economic issues than other data (like introspective reports or behavioural data).

The main reason for these conclusions concerns the correlational nature of neuroeconomics studies. In fact, the detection of a correlation between a certain activation in the nervous system and a behavioural performance at a decision-making task does not allow per se the inference that the former is both necessary and sufficient for (and so reducible to) the latter. Certainly, it is true that neuroeconomics is still a young field which needs time and work to develop its potential. However, I fear that the reductionist outlook embraced by many supporters of neuroeconomics could represent a serious obstacle to its development.

Footnotes

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

Author biography

![]() ) and a psychotherapist at the University of Milan. His published and presented papers include discussions of the concept of mind in the various psychological approaches, the relevance of Jerry Fodor’s modularity thesis for neuropsychology, the examination of Benjamin Libet’s experiments, and the assessment of the epistemological status of the psychoanalytic theory. Address: Giuseppe Lo Dico, via Castelvetro, 7, 20154 Milan, Italy. Email:

) and a psychotherapist at the University of Milan. His published and presented papers include discussions of the concept of mind in the various psychological approaches, the relevance of Jerry Fodor’s modularity thesis for neuropsychology, the examination of Benjamin Libet’s experiments, and the assessment of the epistemological status of the psychoanalytic theory. Address: Giuseppe Lo Dico, via Castelvetro, 7, 20154 Milan, Italy. Email: