Abstract

Internationalization, trade union decline, enforcement problems and rising self-employment all strain the effectiveness of collective wage bargaining arrangements in northern European construction. We examine Denmark, Germany, the Netherlands, Norway and the UK, and show that these strains have pushed trade unions to seek assistance from the state to stabilize wage regulation, but with results that vary according to employer strategies and the power balances between the actors. While Denmark and the UK have barely introduced any state support, Norway has followed the Netherlands and Germany in introducing legal mechanisms for extension of collectively agreed minimum wage terms. The country studies suggest that state assistance alleviates some of the strain, but does not reverse the trends, and the comparison indicates that both institutional innovation and reorganization may be required if wage bargaining is not to drift into different functions.

Keywords

Introduction

The distinctive labour and product market conditions of the construction sector affect both the rationale for collective wage regulation and the dynamics of inter-sector and international coordination. While the sector displays high capital and labour mobility, its products are largely immobile, and there is therefore no real scope for export competition. At the same time, it is very sensitive to economic fluctuations. The ‘sheltered’ and volatile nature of the construction sector entails a particular position in the labour market. In periods of economic boom, labour shortages, poaching and wage ‘leap-frogging’ can lead to wage increases in construction that spill over into other parts of the economy, including the export-oriented manufacturing industry. Therefore, wage moderation in construction is typically important for maintaining countries’ international competitiveness. As periods of economic slump and declining employment can place downwards pressure on wages and spur low-wage competition, the fixing of wage floors is important for maintaining labour standards in this volatile, labour-intensive sector. This structural setting results in the enduring importance of collective wage regulations that control competition and stabilize the labour market by covering most actors on both employer and worker sides.

Employers and workers have therefore had a mutual interest in collective wage regulation, with many northern European countries using different forms of cross-sector coordination to set upper norms for wage growth (Hancké, 2013; Sisson and Marginson, 2002) and sector-specific agreements to fix wage floors (Bosch et al., 2013). At the same time, market forces have always influenced wage formation in the sector, and workers in the countries under study have traditionally been paid above the wage floor. However, even this market regulation has typically been mediated by the articulation of bargaining levels (either through differentiation of wage floors between skill groups or through formal demands for local bargaining in two-tier systems). Statutory minimum wages have always played a minor role, but in some countries, statutory regulations in the form of legal extension mechanisms and chain liability have been put into place to support the systems of collective bargaining in mediating the impact of market forces. Together with high organization rates among employers and workers and corresponding bargaining coverage, this institutional setup has ensured a certain stability to employment relations despite construction in northern Europe possessing a somewhat fragmented labour market, with many small firms, relatively high levels of self-employment, long chains of subcontracting, and a labour force that is physically dispatched from work site to work site.

However, institutions are not static entities (Thelen, 2010), and the last decade has seen increasing pressures on industrial relations institutions that have traditionally regulated market forces in construction. We show how the recent eastward enlargement of the EU, the economic crisis and increasing international competition have put pressure on collective wage regulation arrangements in the construction sectors of Norway, Denmark, Netherlands, Germany and the UK. We draw on statistical data, previous literature and interviews with trade union and employer representatives in Denmark, Germany, the Netherlands, Norway and the UK. We identify different kinds of institutional changes and actor responses under these pressures, and argue that, behind a surface of institutional stability in the pre-existing forms of coordination, increasing strains have made actors, including employer organizations, change strategies with regard to collective bargaining solutions and state regulation.

Pressures, changes and actor responses

Our analysis raises three questions. First, what pressures drive changes in wage regulation arrangements? Second, what kinds of changes do we observe? Third, how do the actors respond, especially employers? Three potential drivers of change can be envisioned: increasing competition from southern Europe (‘south-north contagion’), strengthened regime competition among the northern, high-cost countries themselves (‘north-north competition’) and the destabilizing effects of east-north integration driven by the free movement of labour, services and capital (Dølvik et al., 2018). OECD trade statistics suggest that south–north trade in construction has declined over the last decade, making it unlikely that increasing competition from southern Europe is a major driver of change. While these statistics show that northern European countries import most construction services from other northern European countries, the limited scope of export competition makes us expect north-north competition to be less important. By contrast, east-north destabilization seems a plausible thesis. Here, the statistics show a clear upwards trend in the import of construction services from eastern European member states, surpassing southern Europe and coming close to imports from northern Europe. At the same time, the pressures are mirrored in the debate around migrant labour and social dumping in the construction sector.

Regarding the kinds of change (Dølvik et al., 2018) the persistence of collective bargaining in construction – even in the disorganized UK labour market – suggests that rupture or displacement of collective bargaining is unlikely to take place. Moreover, because the construction sector is often a pattern-taker in coordinated economies, significant reconfigurations around pressures unique to construction are unlikely. Instead, we expect change under external pressure primarily to take the form of drift (Streeck and Thelen, 2005), where the effectiveness of institutions diminishes because the reach of the collective regulations shrinks or formal rules are not adapted to changing competitive conditions. As such, formal rule stability may hide changes in everyday employment relations practices. Increasing cost competition may drive wages to the wage floor, the posting of workers may entail circumventions of collective agreement (Berntsen and Lillie, 2015; Wagner, 2015), and the rising numbers of self-employed workers may undermine the effectiveness of collective bargaining as a regulatory tool. Another possibility is layering, where pre-existing institutions are supplemented by new institutions. In our cases, this would often come in the form of state support for collective bargaining, such as legal extension mechanisms, chain liability and social clauses in public procurement tenders that are layered onto collective bargaining institutions to stabilize them and improve their effectiveness, or more direct state regulation through a statutory minimum wage. The stabilizing effects of such initiatives are well-documented (Bosch and Weinkopf, 2017), but new institutions can also gradually undermine old institutions and thus lead to displacement. Nonetheless, the likelihood of new institutions leading to displacement is much less pronounced with state support that layers onto collective bargaining (such as legal extension) than with state regulations that stand on their own (such as statutory minimum wages). Another response to drift may be to opt for stability via adaptation. Due to external pressure, institutional stability will typically not imply total formal continuity, but rather involve minor adaptive change.

This outline of different types of change suggests that while northern European construction sectors may be faced with similar pressures, outcomes in terms of institutional change may vary both because of the severity of the pressure (and thus the problem-load) and because actors can opt for different responses. These may vary across national models, both because such pressures give rise to different problems and because actors have different strategies available depending on the pre-existing institutional setup. As such, we could expect differences in responses between the liberal market economy (LME) of the UK and the coordinated market economies (CME) of the four other countries (Hall and Soskice, 2001). In addition, we could expect differences in responses between the voluntarist Nordic countries, where collective agreements have stood on their own, and the ‘continental’ countries, where collective agreements have been supported by legal extension mechanisms and other statutory regulation. Nonetheless, while such initial classification of cases may be useful for grasping the starting point of institutional change, they should be seen as historical snapshots rather than static equilibria. For instance, the new form of legal extension of collectively agreed minimum wages applying also to posted workers in the German construction sector was established only in the 1990s. More importantly, some of the cases under study show signs of a shift from one model to another.

In the face of such changes in the ‘national’ character, it seems that the strategies of actors (and in particular, employers) are likely to be more important than national models (Lillie and Greer, 2007). In most countries, employers are divided between smaller companies, who want stronger regulation to alleviate competitive pressures from foreign competitors, and larger companies, who want to use cheap subcontractors to stay competitive (Afonso, 2012). Among trade unionists there are, however, differences of opinion between those wanting to close borders and those wanting to organize their new colleagues, as well as differences between those who believe in the importance of trade union self-reliance and those wishing to call on support from the state (Krings, 2009). In addition, there are sometimes cross-sector differences between social partners in construction (more noticeably harmed by low-wage competition) and those in export-oriented sectors (seeing access to cheaper mobile labour as a competitive advantage). In a situation where external pressures may erode the ‘national’ character of the construction sectors, the type of institutional change may be determined by the way the interests of these different groups are balanced and negotiated.

New pressures on a traditional sector

There is a great degree of similarity in the pressures on collective wage regulation in the five countries. Therefore, we make a joint assessment of whether south-north contagion, north-north competition or east-north destabilization is the main driver of change. In our empirical investigation, there are three intervening changes which have been exerting new pressures on the construction sector during the last two decades.

First, following political shifts in the 1980s, financial liberalization in the 1990s and, for some, integration into Economic and Monetary Union since 1999, most European states have become more reluctant to use Keynesian policy tools to stabilize employment in the sector. Instead, investment in construction increasingly follows and amplifies the boom and bust cycles of the overall economy, especially in countries where house-building is generally private and where the financial market is less regulated. This has made employment in the sector even more cyclically volatile, thus increasing the importance of wage regulation to maintain wage moderation during booms and fix wage floors during slumps.

Second, large public and private developers have put pressure on prices in the sector. Export-oriented companies (and their interest organizations) have emphasized that their international competitiveness is affected by the cost of domestic inputs, including the cost of new facilities. In addition, public authorities have systematized practices to obtain more from their procurement budgets, while EU regulation of public procurement has made some public developers more reluctant to emphasize issues other than price in their assessment of tenders (Ahlberg and Bruun, 2014). These developments have increased cost competition in the sector.

Third, internationalization in the form of cross-border mobility of workers and companies has increased markedly after eastward enlargement in 2004. The liberalization of the EU single market for services has made cross-border operations more accessible to smaller and less specialized companies. At the same time, labour cost differences have allowed eastern European subcontractors to deploy more labour-intensive and cost-competitive business strategies than are usual among their specialized and more capital-intensive northern European counterparts (Cremers, 2011).

These three trends are interconnected, but the inflow of foreign labour through regular labour migration and posting (by genuine construction companies or so-called manpower companies) is widely perceived as the most important. It makes a return to Keynesian policy all but impossible (because increasing demand will simply draw in more labour); it makes cross-sector coordination less necessary (because wages can be controlled through increased labour supply during upturns and employees may leave the country during downturns), and it widens the scope for low-cost competition (because of labour cost differences within the EU). As such, east-north destabilization seems to be the most important driver of change, although the two first trends represent an underlying pressure from north-north competition.

Developments in collective wage regulation arrangements in construction

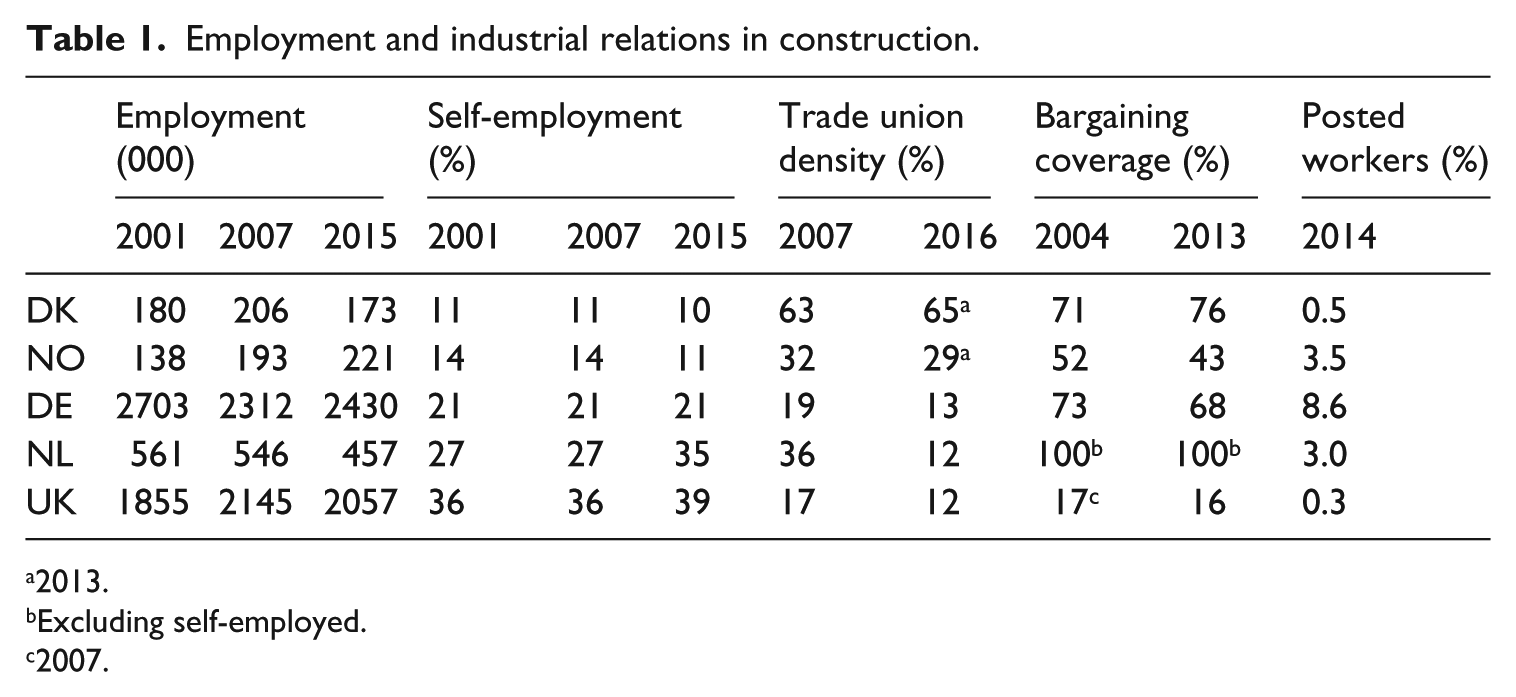

With regard to the kinds of change observed and actor responses, we see a more differentiated picture, affected by different trends in sector employment, union density, collective bargaining and self-employment (see Table 1). This requires a separate account for each country.

Employment and industrial relations in construction.

2013.

Excluding self-employed.

2007.

Denmark: institutional stability through minor adaptation

In Denmark, the main structure of wage regulation has been preserved. An important source of stability is the system of pattern bargaining, where trends in wage movements are set by manufacturing and then followed by construction (Ibsen, 2016; Sisson and Marginson, 2002). Pattern bargaining has deep historic roots and the basic principles of the wage regulation system are not up for negotiation; moreover, it implies that the potential for wage increases is quite clear when negotiations begin in construction. As such, interviewees state that they feel no particular pressure for wage moderation from export-oriented sectors, simply because it is already a self-evident part of the bargaining pattern. At the same time, the inflow of foreign labour has also dampened wage growth in the sector, which means that the strength of pattern bargaining was not tested during the boom in the early part of the 2000s. The economic crisis then caused a pronounced slump, which had significant effects on wages. However, given the flexibility of the two-tier bargaining system, this wage decline occurred within the parameters of the bargaining system and has provided no impetus for reform. The picture of stability is also confirmed by union density, which remains around 65 percent despite absolute membership decline, and bargaining coverage, which still exceeds 70 percent.

The most destabilizing factor in the Danish construction sector has been increasing internationalization. After EU enlargement, there has been a steady increase in labour migration, posting of workers and international subcontracting from CEE. Spurred by the economic boom and labour shortages, companies started recruiting in the CEE countries. At the same time, mobile firms and migrant workers (including self-employed) also entered the Danish market, ready to use their comparatively low wage levels as a competitive factor (Dølvik and Eldring, 2008). Survey data from Copenhagen show that Polish construction workers receive wages substantially below the level of Danish workers (Arnholtz and Andersen, 2016). The lack of a statutory minimum wage or an extension mechanism leaves a wide playing field for companies not covered by a collective agreement. Nonetheless, both the main employer organizations and trade unions have rejected legal extension, arguing that this would undermine the Danish bargaining system. Instead, they have agreed on minor adaptive changes regarding enforcement, with a reverse burden of proof in arbitrations being the most important one.

Trade unions argue that more is needed because they still struggle to maintain bargaining coverage and effective enforcement. They have called for the introduction of chain liability and mandatory coverage of subcontractors in the collective agreements. Employers, however, argue that the problems with factor mobility have been blown out of proportion and maintain that such measures would undermine the traditional bargaining system. They have been under strong pressure from manufacturing employers to maintain this position, while trade unions in construction have gained little support from their strong counterparts in the metal industry. As a result, construction sector bargaining has stalled several times on issues related to these international pressures and there are growing tensions between employers and unions in the sector (Arnholtz and Andersen, 2017). In an attempt to gain new leverage, unions have lobbied public authorities to increase their use of ‘social clauses’ in public procurement tenders, and most state, regional and municipality institutions now demand that contractors and subcontractors be covered by collective agreements. However, many companies working for private clients are not covered, which leaves parts of the sector relatively unregulated and open to drift (Arnholtz and Andersen, 2016). Nonetheless, while several labour court cases document the underpayment of foreign workers, there is no clear sign of a general erosion of labour standards in the sector. One reason may be that it is still relatively well organized in terms of coverage and density. Another reason may be that while foreign workers and companies have been the main topic of concern, the inflow, in comparative perspective, has been relatively modest. A final reason may be that trade unions have made enforcement on foreign companies a top priority.

Norway: layering by state support to achieve stability

As with Denmark, there is a long tradition of pattern bargaining in Norway, and both employers’ associations and trade unions remain firmly committed to it. As in Denmark, the inflow of foreign workers and service providers is the main strain on the system. However, the economic context for this inflow has been very different. In Norway, an economic boom has seen employment in construction grow continuously since the early 2000s, which has had an impact spanning trade union density, bargaining coverage and the inflow of foreign workers and companies. While the absolute number of trade union members has increased slightly, they have far from kept pace with employment growth in the sector, causing declining density. Likewise, more employees are covered by the collective agreement today than 15 years ago, yet the rate has declined by almost 20 percent over the period, from 52 to 43 percent.

One obvious reason is that the continuous expansion in the sector has meant that the inflow of foreign workers and companies has been much more intense than in Denmark. This is especially true in the Oslo area, where around half of construction workers have foreign origins. As with Denmark, surveys among Polish migrant and posted workers in Oslo show that they receive considerably lower wages than Norwegian workers (Friberg and Eldring, 2011; Friberg et al., 2014; Friberg and Tyldum, 2007). In addition, this internationalization trend has been strongly associated with a rise in non-standard employment and changes in product market competition. The posting of workers, self-employment and temporary staffing agencies have been used as ways to gain market share by importing cheap labour into the construction sector. As a result, the system of voluntarist collective regulation has come under increasing strain and trade unions have called for institutional changes that could help stabilize competition and prevent the erosion of wages and labour standards.

Thus, although the debates about international subcontracting and labour mobility causing ‘social dumping’ have been largely similar in Denmark and Norway, the response to such pressures has been much more pronounced in Norway, both because of the greater problem load and because of employers’ willingness to defend their sector. A long-dormant clause on extension of minimum terms in collective agreements has been put gradually into use: first in certain geographical areas and, since 2007, in the whole sector. Legal extension has since been supplemented by chain liability that holds main contractors responsible for subcontractors’ breaches of the legally extended minimum terms. As a result, the share of workers who are legally entitled to collectively agreed minimum wages has risen from approximately half to almost all workers. In addition, the labour inspectorate has gained increased competence and is now involved in the enforcement of the legally extended collective agreement minimum wages (Ødegård and Eldring, 2016). Finally, identity cards have been introduced for all construction workers to improve enforcement, effectively limiting bogus self-employment (Eldring et al., 2011).

The intensification of state involvement in the regulation of wages is a break with the ‘Scandinavian’ voluntarist tradition, but a break that both trade unions and employers in construction deem necessary for preserving the stability of the sector. Nonetheless, this new state support has not gone unchallenged. Employers in manufacturing (especially in shipbuilding) have been very critical of the extension of collective agreement terms, causing tensions within the employers’ confederation NHO (Næringslivets Hovedorganisasjon). At the same time, it is uncertain whether these initiatives can alleviate the pressures. While studies suggest that erosion would have been worse without the statutory interventions (Eldring et al., 2011), wages of eastern workers remain markedly lower than those of Norwegians, and interviewees argue that a significant erosion of wages and labour standards has taken place. The prolonged building boom makes it hard to register this erosion in official wage statistics, although some experts argue that construction workers are lagging behind other sectors. It also remains unknown whether a drop in economic activity will weed out the unorganized parts of the sector and cause an increase in density and coverage (as has been seen in Denmark) or whether this disorganizing trend will continue (as in the Netherlands).

Contained drift in Germany

As with the Nordic counterparts, wage moderation seems an integral part of German wage regulation (even if pattern bargaining is less strictly institutionalized), and all interviewees stated that there has been no particular pressure for wage moderation from manufacturing during the last decade. There is no change in the formal role of the social partners, as they continue to negotiate collective agreements and participate in the bilateral administration of social funds. Survey data suggest that collective bargaining coverage in construction has declined in West Germany (from 79 percent in 2004 to 71 percent in 2013), but increased in East Germany (from 48 percent in 2004 to 57 percent in 2013) (Ellguth and Kohaut, 2005, 2014). For both parts of the country, these figures are high compared to other sectors.

While pressures from international competition are also an issue in German construction, there have been few recent institutional changes to tackle the increasing inflow of labour migrants and companies from the CEE countries (the introduction of a national minimum wage in 2015 is of little relevance in construction). This is because extension of minimum pay clauses in collective agreements and chain liability were already introduced in construction in the late 1990s to tackle challenges posed by the posting of workers. During the massive construction boom that followed German unification, a large number of foreign companies began to operate in the German construction sector. Much of the pressure from internationalization experienced in Norway and Denmark today was seen in Germany back then, and both employers and unions in construction called for adoption of the new extension mechanism and chain liability pertaining also to posted labour, although the German employers’ confederation BDA (Bundesvereinigung der Deutschen Arbeitgeberverbände) was fiercely opposed (Bosch et al., 2013; Eichhorst, 1998).

Nonetheless, when looking beyond the stability of formal institutions, there are signs of drift. The background is, in part, a drop in total construction employment from 3.3 million in 1996 to 2.3 million in 2005, which implies that there is a potential surplus of labour. While local negotiations traditionally implied that wages would be above the minimum rate, the drop in employment has put workers under pressure and caused the collectively agreed minimum rates to become increasingly the going rate, especially in East Germany (Bosch et al., 2013). In response, the extension mechanism has been expanded from covering only minimum pay to include rates for a second skill category. However, this formal reinforcement of wage levels still faces problems of enforcement. Survey data suggest that 17 percent of employees in West Germany and 28 percent in East Germany work in companies that do not observe the collective agreement in their wage-setting (Schulten and Buschoff, 2015). This points to one of the main challenges in the German construction sector: while formal institutions are stable and collective agreement coverage is relatively high, enforcement is poor and agreement violations are thought to occur frequently. Effective enforcement is hampered by the low and falling level of trade union density, and by the low number of workers employed in companies with a works council (around 16 percent) (Schulten and Buschoff, 2015). IG BAU (IG Bauen-Agrar-Umwelt) has lost more than half a million members since 1996, and density dropped from 23 percent in 2006 to 13 percent in 2016. (OECD data aggregate the main construction industry (Bauhauptgewerbe) and the finishing trades (Ausbaugewerbe). Authors such as Bosch et al. (2013) calculate density on the basis of the main construction industry only and estimate it at a higher level, 35 percent, but with the same declining trend.) If one takes into account the self-employed and posted workers, fewer than 10 percent of those working in the German construction sector are members of IG BAU, which therefore lacks the strength to effectively enforce the collective agreements. In other words, there are signs of drift despite the institutional innovations of the 1990s.

Drift beyond the extension mechanism in the Netherlands

In formal terms, the Dutch construction sector is very well regulated and the system is stable. Cross-sectoral coordination stabilizes bargaining as in the other countries, and the legal extension of collective agreements ensures that all regular employees are covered. However, a number of challenges are evident. Most importantly, regular employment is no longer the norm. Both posted and temporary agency workers make up an increasing share of employment in the sector, and they are only covered by parts of the extended agreements. Furthermore, several studies show that temporary agency work, the posting of workers and international subcontracting constitute significant obstacles to the effective enforcement of collective agreements (Berntsen and Lillie, 2015; Wagner and Berntsen, 2016). More salient, however, is the increasing number of self-employed in the sector. While the economic crisis reduced the number of employees in the sector by 25 percent from 2008 to 2016, the number of self-employed has doubled since 2007. They now make up approximately a third of total employment in the sector, but interviewees report that they outnumber regular employees in the parts of the sector covered by the collective agreement. This poses a fundamental threat to the integrity of the wage regulation system, because self-employed are, by definition, not subject to collective agreements or their extension.

There have been several responses to these challenges, but the actors disagree on the appropriate action to take. In 2015, the previous government introduced chain liability, to tackle the problems caused by international subcontracting, as well as a series of soft measures to clarify the legal status of self-employed workers and to penalize abusive contractual arrangements. While the social partners recognize the problems, they disagree on the remedies. The employers’ associations have proposed more working-time flexibility and reduced social contributions in order to make regular employees as cost-competitive as posted workers and the self-employed. The unions have proposed improved enforcement as the best measure to avoid bogus self-employment. Consequently, the last round of bargaining took more than 18 months to conclude, which has challenged the integrity of the cross-sectoral coordination. In the final compromise, unions agreed to heightened working time flexibility in exchange for improved joint enforcement, the introduction of a collectively sanctioned definition of self-employment, and a mandatory contract for self-employed, as well as digital ID passes that should be readily available for inspection (van het Kaar, 2015). However, neither side is truly content. Unions argue that employers have become ‘more self-aware’ and are exploiting the critical situation. One reason for union acceptance of more working-time flexibility was that employers in the painting industry had signed a (cheaper) agreement with a small alternative union when the main union FNV (Federatie Nederlandse Vakbeweging) would not concede during negotiations. Employers highlight the importance of the effective extension of agreements for their participation in collective bargaining and some of the large construction companies threaten to leave the bargaining system if the problems with self-employment are not tackled. Here, however, the social partners have reached the limits of the extension mechanism, because the government has rejected appeals to extend their agreements to self-employed.

Therefore, while the formal structure of the Dutch wage regulation system seems stable and agreements are extended to all employees in the sector, drift is nonetheless occurring. First, increasing internationalization means that unions are struggling to enforce the collective agreement. This is especially true since unions have become weaker as density has fallen by some 20 percentage points over the last 15 years (according to some estimates). Second, the Dutch wage regulation system is threatened by the declining salience of employment relationships and the rise of self-employment. This threat is far more fundamental, insofar as the collective bargaining regime is ill-adapted to (and perhaps incommensurable with) the strong presence of independent contractors. Third, the system rests on institutional guarantors who may withdraw their support. Since the 2017 elections, the PvdA (Labour Party) has been excluded from the coalition government and replaced by right-wing parties which are openly hostile to collective regulation of wages and conditions, enthusiastic about the benefits of self-employment and wish to abolish the extension mechanism. Although a direct assault on the wage regulation system does not appear imminent at present, the system is likely to weaken further in the absence of effective re-regulatory initiatives.

Ongoing drift in the UK

The UK labour market differs from the other north-west European cases with its decentralized collective bargaining structure, low coverage rates and poor employment protection. However, the construction sector is one of the very few parts of the UK private sector which still have multi-employer bargaining. Direct bargaining coverage was only 13.5 percent in 2016, down from 17.4 percent in 2007 (ONS data), but the core provisions of sectoral agreements are more widely applied and therefore the effective coverage can be estimated to be around one third of the workforce. The statutory national minimum wage introduced in 1999 is largely irrelevant in a sector where hourly pay rates are higher. Importantly, collective agreements in the UK are not legally enforceable unless the provisions are transposed into individual employment contracts. With the exception of construction engineering, the employer side is fragmented into a number of organizations, but there are still three main agreements in the construction industry. The CIJC (Construction Industry Joint Council) agrees minimum rates and standards, with an estimated effective coverage of 30 percent. The BATJIC (Building and Allied Trades Joint Industrial Council) covers smaller companies (represented by the Federation of Master Builders). The engineering construction agreement (National Agreement for the Engineering Construction Industry, NAECI) specifies actual rates and standards and has nearly 100 percent coverage in the sub-sector (as adherence is required for tendering, a functional equivalent to legal extension) and includes a strong auditing arrangement. In addition, there are separate agreements for the electrical and plumbing trades. In practice, the CIJC is a flexible agreement allowing decentralized variation of standards. Union density was 12 percent among employees in 2016, down from 17 percent in 2007, and in some parts of the country and segments of the industry anti-union practices such as blacklisting and harassment of activists have widely occurred (Druker, 2016). Tensions over collective bargaining occur more in the North, which tends to be have a higher coverage rate than London, where important collective agreements were struck on major sites such as the Olympic Park and Heathrow Airport, although the small-project residential sector remains very unregulated.

One pressure on the labour market comes from the increasing use of foreign companies and migrant labour, a dominant change since EU enlargement of 2004, although it is rooted in a long-standing national underinvestment in training (Chan et al., 2010). Labour Force Survey data indicate that between 2002 and 2008, the share of foreign-born workers among construction workers increased from 5 to 8 percent, to stabilize after the crisis hit the sector severely, with a loss of 300,000 jobs in 2009 alone. The insecure employment conditions of migrant workers have been linked to worse health and safety conditions (Meardi et al., 2012) and led to cases of open competition with local workers, as in the case of the ‘British jobs for British workers’ strikes in 2009 (Meardi, 2012). Despite these reactions, UK construction unions’ attitude has generally been inclusive, with original efforts at ‘community organizing’ of foreign workers (Fitzgerald and Hardy, 2010). The main union concern has been defending institutionally fragile collective bargaining from disruption by foreign companies, for instance, by demanding wage transparency.

That said, the main problem for unions is the rise of agency work and (bogus) self-employment (Behling and Harvey, 2015), along with the impact of the economic crisis. In addition to falling employment and wages, the crisis caused company closures that have negatively affected employer organizations, as member companies have gone out of business and new ones have not joined their associations. In addition, a shift from larger to smaller projects (involving smaller companies) has been part of the explanation why self-employment has kept increasing, from 35 percent of the workforce in 2008 to 41 percent in 2015 (LFS data). While reported posted worker numbers remain relatively low, temporary work agencies can avoid equal treatment of employees for placements under three months and are also a source of strain in the sector. Therefore, while multi-employer bargaining in construction has long stood in contrast to the generally disorganized UK labour market, pressures from labour migration, the crisis, self-employment and agency work are causing further drift in everyday practices.

Conclusion

Three questions have been addressed in our analysis. First, which pressures (south-north contagion, north-north competition or east-north destabilization) drive changes in collective wage regulation? In the construction sector, our study shows that the most important is the increasing international competition promoted by east-north factor mobility (subcontracting, freedom of establishment, posting of workers and regular labour mobility). In all the countries under study, such cross-border mobility was mentioned by interviewees as one of the main challenges because it either causes or amplifies disorganization and fragmentation. Low wages, lower social costs, atypical employment and unprecedented flexibility seem to surround this factor mobility. At the same time, the pressure from east-north destabilization typically occurs in a context shaped by north-north competition. While wage moderation and the establishment of ceilings for wage increases are often secured by cross-sectoral coordination, the efforts to strengthen cost competition in construction (as illustrated by the opposition of manufacturing employers to the extension of collective agreements in Denmark, Norway and Germany) show that pressure is now put on the articulation between levels of wage determination and the fixing of wage floors. In addition, the pressure from east-north destabilization interacts with economic conditions, the declining organization of workers and employers and the increasing use of atypical employment to produce different outcomes.

Second, we asked what kind of institutional change could be observed. In formal terms, collective bargaining in the countries under study has displayed continuity during the last 10–15 years, so to observe changes and differences in outcomes we had to look beyond the formal institutions. Here, we observe changes as minor adaptions through collective bargaining (Denmark), as new forms of state support layering onto the bargaining system (Germany in the 1990s and Norway after EU enlargement) or as drift in the effectiveness of collective bargaining institutions through on-the-ground erosion (a slow continuous process in Germany, Norway, and the UK, but more rapid in the Netherlands during the crisis). Despite these different processes of change, there seems to be a common trend across countries that minimum wages are increasingly becoming the going rate, albeit primarily for posted, migrant and low-skilled workers (in that order).

Third, we asked how actors have responded to change. Although pressures are similar and trade union demands are broadly the same across countries, institutional responses differ because governments and employers act differently depending on discrepant power relations and perceived problem loads relative to the capacity of institutions to handle competition from foreign operators. In Denmark, the strong cross-sectoral coordination has allowed no room for construction unions to exercise their power to obtain chain liability and mandatory coverage of subcontractors, and the severity of the problems has been insufficient to convince Danish construction employers to break with their employer counterparts in manufacturing. By contrast, higher inflows of labour and subcontractors and a weaker pre-existent collective bargaining system brought Norwegian construction employers to support the unions’ call for state support. In a similar manner, the German government and employers have been convinced of the need to protect the sector’s employment relations, commonly perceived as weakly regulated, leading to innovations from regulation of posting in the 1990s to the recent extension of skill-based pay clauses. This willingness to re-regulate stands in opposition to the Dutch and UK experience, where governments have not in general perceived the need to reinforce institutions, and employers have not felt the need to accommodate trade union demands. Dutch construction employers have used their labour market power to ask for union concessions and have only reluctantly consented to re-regulatory efforts targeted at bogus self-employment.

These strategic choices also imply that models are on the move. The Norwegian wage regulation system is beginning to look increasingly like the German, while increasing use of self-employment and potential withdrawals from multi-employer bargaining may make the Dutch construction sector look more and more like the British. Whether this will be a blessing for employers is questionable. In the UK, employers’ associations are struggling to maintain and promote collective bargaining in an effort to regulate and coordinate the sector. It is, however, an uphill struggle given the fractured nature of the sector, and it is unclear whether construction companies actually benefit from the extent of deregulation. Hence, even strategic choices may have unintended consequences. The same may be said for the responses found elsewhere. In Denmark, the refusal to introduce new measures may leave the sector open to drift. In Norway, new initiatives have primarily concerned the fixing of wage floors, while the articulation between levels has been scarcely discussed, even though construction is a sector where wages are typically raised above the wage floor by local bargaining. In Germany, the lack of union strength on the floor implies that the somewhat elaborate formal system of stabilization is susceptible to circumvention on the ground. As such, the question remains whether institutional solutions exist to resolve the pressures from cross-border factor mobility on both wage bargaining articulation and wage floors.

The overall conclusion is that state support, such as legal extension and chain liability, may alleviate the pressure on wage floors and stabilize collective wage regulation for a while, but no institutional response constitutes a permanent solution because new forms of circumvention are continuously found. Institutions are continuously created, used and remade by actors depending on power relations among them, which means that state support may be most effective when it helps to increase trade union density, labour bargaining power and, more generally, social partners’ capacity to engage more effectively with the pressures of internationalization.

Footnotes

Acknowledgements

We are grateful to Claire Evans, Torsten Müller and Jon Erik Dølvik for their contributions to the data collection. We also thank the other participants in this module of the Euro-strain project, and in particular Jon Erik Dølvik and Paul Marginson, for extensive comments on earlier drafts.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The articles in this special issue form part of a module organized by Fafo within the ‘Euro-strain’-project headed by ESOP, University of Oslo, and have benefitted from funding from the Norges Forskningsråd (Research Council of Norway) ‘Europe in Transition’.