Abstract

Researchers search for factors explaining the disruptive impact of labour platforms on work, yet very few studies explore how platforms approach product markets and the resultant effects on platform workers’ working conditions. Looking at this question, this paper studies distinct but similar international and regional food delivery platforms in Poland and Italy, exploring which factors explain differences in their working conditions. Two findings emerge. Firstly, international and regional platforms differ substantially in terms of how they approach product markets. Secondly, these differences account for the variety within (and across) platforms’ employment outcomes.

Keywords

Introduction

Labour platforms, usually understood as digital intermediaries between users and workers (Woodcock and Graham, 2020), are gaining in significance, attracting growing numbers of workers and clients (Graham et al., 2017). Operating in a ‘legal void’ (Bothello et al., 2019) outside institutional and legal frameworks (Prassl, 2018), platforms challenge the traditional means for reducing asymmetry in employment relationships.

Labour platforms affect employment in a variety of ways, bringing down wages and jeopardising minimum standards (Dunn, 2016), creating boundaries to social security (Behrendt et al., 2019) and hindering unionisation (Graham et al., 2017). Yet, the way and the extent to which platforms disrupt employment by violating institutional regulatory settings can differ. Thelen (2018) study on Uber questions the assumption that labour platforms impact institutional regulatory settings in a similar manner, considering the variation to be contingent upon the socio-political constellations between consumers and local governments created in a particular institutional setting (see also Kenney and Zysman, 2020). Similarly, Oppegaard et al. (2021) report on the ‘political will’ underpinning Uber’s ‘fastest and most radical deregulation’ when entering the Nordic economies (Oppegaard et al., 2021: 30), whilst Adler (2021) investigates the role of socio-cultural frames in the deregulation of ride-hailing in Boston.

We use qualitative data from a study on international and regional food delivery platforms in Poland and Italy conducted between June 2020 and May 2021 to suggest factors explaining how and to what extent platforms engage with regulation. Developing an approach premised on the ‘differential embeddedness’ of labour platforms, we attempt to explain differences in employment conditions and outcomes resulting from the heterogeneous operating modes used by international and regional platforms within (and across) different regulatory settings, taking account of the influence of product markets.

In our view, arguments highlighting the importance of product markets for employment (Brown, 2008) similarly apply to the platform economy, though not uniformly. Building on studies stating that regional platforms’ practices may differ from those of international ones (Steinberg and Li, 2017), we ask whether platforms approach product markets differently and how this accounts for differences in working conditions between platforms within and across countries. Looking at our two case study countries, Italy and Poland, our finding is that regional platforms construct market niches in an attempt to avoid price competition from international platforms. We contend that the strategies adopted by regional platforms influence their employment models, subsequently determining working conditions. Mechanisms can differ depending on the national institutional setting. In Poland with its relatively stronger health and hygiene standards in food delivery markets, regional platforms leverage product market regulation to construct a quality-oriented niche. Due to stronger union pressure in Italy regarding the misclassification of couriers as self-employed independent contractors, regional platforms engage with workers as a means of constructing product- and quality-differentiated niches.

The paper is organised as follows. We start by framing our argument within relevant theory and debates. After discussing our research design and methodology, we go on to present our findings, analytical comparisons and conclusion.

Product markets, working conditions and platform work

Operating in competitive product markets, companies not maximising production efficiency or developing new products can be outcompeted and eventually crowded out of the market. Much of market-making consists of stabilising and routinising competition by pursuing different market segments (high- or low-road quality) and by diversifying products (Fligstein, 2018).

Competition can be limited by product market regulation setting market entry rules (such as licences or permits) and consumer protection rules (such as health and safety and other standards products and services should meet) (Nicoletti et al., 1999). Such regulation affects working conditions (Gall et al., 2011). Firstly, it can limit competition based on wages and working standards (Brown et al., 2009) by forcing employers to accommodate arm’s length relationships through concessions on pay and working conditions (Walton et al., 2000). Where companies face less competition, unions can bargain for wage increases and better working conditions (Metcalf, 2002), because ‘what [workers] and employers have to fight over is decided by the employers’ profits’ (Brown, 2008: 114). Secondly, product market regulation can set a framework for workforce management by establishing minimum standards for producing goods and services (Turnbull, 1986).

Going back in time, Commons (1909: 50) offered a remarkable account of how price competition between wholesale and retail sellers undermined the common interest of masters and journeymen and ‘split their community of interest into the modern alignment of employers’ associations and trade unions’ by incentivising employers to search for cheap labour, thereby dragging down labour costs and working conditions. Interplaying and positioning within product markets can be a source of competitive advantage for firms as it can help circumvent labour market institutions (Pulignano et al., 2016; Pulignano and Keune, 2015; Schwellnus et al., 2019), (e.g. labour law and collective bargaining arrangements) regulating wages and working conditions (Holmlund, 2014). For example Harvey and Turnbull (2020) show how Ryanair’s use of equal access to a Single European Aviation Market allowed it to avoid trade union strongholds.

Studies on the platform economy illustrate how platforms might refuse to recognise legally mandated social rights of workers by engaging in regulatory arbitrage, that is ‘structuring activity to take advantage of gaps or differences in regulations’ (Pollman, 2019: 567) through, for instance claiming to be just technological intermediaries (Rosenblat, 2018). Operating as ‘marketplaces’, platforms can in principle evade national regulations by not providing rights or transferring obligations to comply with regulations on workers, thereby assuming no responsibility for injuries or damage to tools and avoiding the necessity to pay for idle time, that is shifting costs and risks directly to workers (Ravenelle, 2019). This in turn leads to lower incomes (Berger et al., 2018), irregular working time (De Stefano, 2015) and a lack of control over work (Franke and Pulignano, 2020). Platforms are ‘institutional chameleons’ (Vallas and Schor, 2020) whose effects on employment depend on the environment (Daugareilh, 2020; Drahokoupil and Vandaele, 2021), and are impacted by different forms of worker representation (Heiland, 2020), union traditions (Englert et al., 2020; Marrone and Finotto, 2019), reactions from local governments (Spicer et al., 2019), situation on the local labour market (Altenried et al., 2021), as well as by trajectories of regional business evolution (Alvarez-Palau et al., 2021). Thelen (2018) comparative study on Uber found that worker misclassification is prevalent in the United States, where social insurance is directly tied to employment status. Elsewhere, Uber poses a threat not to employment status but to urban transportation systems (Germany) or to tax revenues needed to support the welfare state (Sweden) (Alsos and Dølvik, 2021). Apart from evading employment regulations, platforms increase price competition, lowering the ‘margin’ left for workers as customers and providers engage in multi-homing, that is using multiple platforms to seek similar products/services and choosing on price (Rochet and Tirole, 2003). Multi-homing makes product differentiation – a standard way of lowering competitive pressures – more difficult (Kim et al., 2017). At the same time, network effects related to multi-homing ‘leads to platforms having a natural tendency towards monopolisation’ (Srnicek, 2016: 45). This might incentivise them to foster even more aggressive market strategies aiming at lowering costs and crowding out competitors (Vallas and Schor, 2020).

Building on these arguments, we contend that understanding platforms’ practices from a market embeddedness perspective is important for assessing the employment outcomes they generate. We also claim that whether and how platforms undercut working standards are dependent on this level of embeddedness.

Research design and methodology

We use a multi-case comparative design of two international and two regional food delivery platforms in Poland and Italy. The country selection is motivated by the differences in product and labour market regulation, allowing us to understand differences in how regional and international platforms operate within and across different national settings. Poland and Italy vary in their food safety procedures, whilst both lack statutory regulations on platform employment, opening up possibilities to utilise non-standard contracts within food delivery. However, they differ with respect to collective labour regulation, with Italian platforms facing higher union pressure. This combination of contextual similarities and differences offers a unique comparative research design allowing us to assess whether and how platform workforces affect – and are affected by – different product and labour market structures. To assess the impact on working conditions, we refer to selected job quality dimensions defined by Eurofound (2021), that is contractual status, earnings, working time, work intensity and safety.

Product market regulation

In both countries, regulation of food delivery is based on food safety standards grounded in European law, that is Regulation 178/2002, laying down the general principles and requirements of food law, and Regulation 852/2004 on the hygiene of foodstuffs. Both regulations mandate the use of the Hazard Analysis and Critical Control Points System (‘HACCP’), a preventive approach aiming to reduce and avoid hazards in the production process rather than inspecting the final product, as well as laying down general principles on food production and services, including delivery, such as the necessity to use easily cleanable spaces and temperature controls.

Polish regulations extend European standards, with all food service infrastructures, including delivery, subject to HACCP approval by public health inspectorates. This also covers food delivery vehicles, with inspectorates only approving cars and scooters adapted in some way for food delivery. Bikes are accepted exceptionally and only when they are specifically designed for catering services (e.g. coffee bikes). Secondly, all persons involved in food services need to undergo medical checks for infectious diseases, normally organised by the employer. There are however many possibilities of circumventing both requirements due to low fines and control (in)frequency (Malinowska, 2017).

By contrast, in Italy the food delivery regulations simply transpose the general obligations set forth in the EU regulations (Parisio, 2015). Food service companies are obliged to maintain HACCP documentation for employees and those working for them and to provide training. There is no vehicle approval system as in Poland, and audits, if at all, only analyse compliance with general public health provisions and applicable documentation.

Labour market regulation

In Poland there is no specific statutory labour regulation or collective agreements concluded for either food delivery or platform work. Platforms should adhere to the binding statutory regulation which allows the use of civil law contracts and self-employment – instead of regular employment contracts – commonly found on platforms (Polkowska, 2021). Civil law contracts and self-employment have been largely regularised in recent years and are now subject to health and social security contributions and the statutory minimum wage. However, in contrast to regular employees, workers on civil law contracts and the self-employed are not subject to obligatory sickness insurance, have no right to paid leave, and are outside working time regulations. Civil law contractors and self-employed are covered by health and safety rules and can unionise, but trade unions are very weak in the service sector – including horeca – in Poland, in line with the generally weak collective organisation of labour (Czarzasty and Mrozowicki, 2018).

In Italy, food delivery platform workers can work in four different employment schemes. Firstly, workers on occasional employment, with a yearly earnings threshold of 5.000 EUR, are exempt from charging VAT but are not covered by social security except for accident insurance introduced as of February 2020 (Rota, 2020). Secondly, workers exceeding the threshold must register as self-employed (Partita IVA). Such workers are included in the social security system (excluding unemployment benefit) and have healthcare insurance but are subject to higher taxation (are required to charge VAT). Thirdly, workers can have a ‘parasubordinate’ status, meaning they are partially covered by social security and healthcare insurance. Occasional employment, self-employment, and parasubordinate work are not subject to any minimum wages, regulation of working time and have no holiday rights. Finally, couriers on certain platforms (including Takeaway and Mymenu) are covered by logistics sector collective agreements covering hourly wages, working time, paid leave and additional allowances (Eurofound, 2018). Irrespective of their type of employment, workers can join trade unions, which are present in the sector and bargain with employers’ organisations. In recent years, the food delivery platform sector has experienced growth in formal and informal unionism and subsequent struggles leading to the introduction of collective labour regulation on some platforms, manifesting unions’ ability to use their still relatively significant power to gain concessions (Marrone, 2021; Marrone and Finotto, 2019).

Selected platforms

We selected two international and two regional food delivery platforms – Glovo and Just Eat Takeaway (international); Stava (regional in Poland) and Mymenu (regional in Italy) for our fieldwork (June 2020–May 2021) in Poland and Italy.

The selection of Glovo and Just Eat Takeaway was motivated by that both belong to the largest food delivery platforms on the market.

Glovo entered Poland in late 2019 and rapidly gained a foothold on the market, expanding to over 30 cities by 2021. In Italy, Glovo started in 2016 and progressively expanded to 40 cities. Glovo is a ‘universal’ delivery platform offering fast delivery services, including from grocery stores. Takeaway entered Poland in 2014 by purchasing food ordering service pyszne.pl (a brand under which the platform still operates in Poland) (hereinafter: ‘Takeaway PL’). In 2017, the platform began to hire couriers and offer deliveries. As of 2021, the platform operates in 22 cities. In Italy, the platform is known as Just Eat, even though the Takeaway visual branding replaced the Just Eat logo in 2020, following Takeaway’s takeover of Just Eat. In Italy since 2011, Just Eat Takeaway (hereinafter: ‘Takeaway IT’) operates in 30 cities in 2021.

Stava in Poland and Mymenu in Italy were selected as regional platforms, as both are established food delivery platforms operating in the respective regions. Founded in Opole in 2014, Stava provides food delivery services for restaurants, without its own client-app. In 2017, Stava evolved into a franchising model, signing strategic partnerships with several large international fast-food chains. The company now has over 40 branches in all Poland. Founded in Padua (Italy) in 2013, Mymenu has gained a strong position in the Veneto region. In 2018, the platform merged with Bologna’s Sgnam and Milan’s BachetteForchette whilst retaining Mymenu as its brand name. Today, the platform is active in six cities in northern Italy, targeting upper-middle class consumers and businesses (B2B).

Methods

Overview of interview.

Source: own elaboration.

The interview design consisted of three parts: workers were asked to recount their working lives and work experiences; in the second part we asked follow-up questions regarding the narrative; the third part contained additional semi-structured questions primarily related to platform work. In line with Schütze’s approach, the interviews were focused on recollections of personal experiences rather than interviewees’ current interpretations of events (argumentations). In addition, we conducted 11 semi-structured interviews with experts (4 in Italy, 7 in Poland) – platform managers, policymakers, academics and trade unionists – on regulatory changes, the role of stakeholders, and the challenges associated with platform work. We recruited respondents via social media and snowballing and used our contacts to approach experts. Each interview took 1.5–3 h and was conducted remotely via Zoom/Skype due to COVID-19. All interviews were fully transcribed and coded in NVivo.

Product markets and international and regional platforms in Poland and Italy

Focusing on price competition within the general food delivery market, international platforms in Poland are primarily interested in expanding their customer bases and lowering operating costs. To do this, Glovo PL and Takeaway PL do not provide workers with vehicles approved by health inspectorates and do not require workers to have medical check-ups. Their ability to circumvent product market regulations is rooted in their intermediary structure, with Glovo PL using ‘fleet partners’ whose ‘role is purely formal, […] they are formally employers but in fact they only facilitate financial flow’ (Interview with a Polish expert), settling payments in the platform’s name. Neither Glovo PL nor its intermediaries check whether the vehicles used are approved by health inspectorates, or whether workers are tested. Workers are assured that ‘everything is done legally’ (Interview with a Polish expert). Takeaway PL couriers deliver the food either on their own non-approved e-bikes or scooters, or on those supplied by the platform where approval is uncertain. The circumvention of product market regulations is evidenced by one courier who ‘rides his own [uncertified] bike’ and who ‘applied to Takeaway because [he] needed a job that doesn’t require medical testing’ (#18). Operating this way, international platforms can lower their costs and thus compete on price more effectively.

Promising a high-quality and efficient delivery service, regional platform Stava is focused on developing B2B relations with restaurants. In contrast to international platforms, it does not run its own client-app, merely handling orders placed either on a restaurant’s own app or on food ordering apps (including those operated by international platforms), that is Stava handles international platforms not as competitors but rather as a source of orders (Stava, 2021). Although the platform could avoid product market regulations because of its intermediary structure similar to international platforms, Stava supplies workers with ‘well-equipped and comfortable’ cars approved by health inspectorates and ‘organizes medical testing for workers’ (#31). Stava leverages product market regulation to create its niche market, thereby sidestepping competition from international platforms. By using certified cars and handling deliveries with tested workers, the platform claims to offer transportation ‘under very safe conditions’ (#33), creating ‘chains’ of deliveries with a view to reducing empty runs. Nevertheless, the platform remains subject to competitive pressure from international platforms as it has not diversified (e.g. it only services a few exclusive restaurants). This is reflected by Stava workers ‘making fun that UberEats and Glovo are their enemies’ (#36) and manifested by the platform’s business situation: the branch of one of our interviewees (#31) lost multiple contracts when restaurants turned to deliveries by international platforms due to Stava being more expensive.

The situation is similar in Italy. International platforms compete on price within the general food delivery market. All platforms, including Mymenu, comply with product market regulations, which are however less expensive to follow than in Poland, as they only require the employing organisation to provide simple training, described as a ‘20–30 min video showing how to do things, get given a bag, a powerbank, a phone holder, and activate account’ (#3).

To keep up with ‘ongoing competition from Takeaway, Deliveroo and other platforms’ (#24) and in the context of a lack of product market regulations able to firmly anchor the niche (as present in Poland), Mymenu is engaged in product diversification based on quality, maintaining an image of being a more ethical company engaging with workers: ‘Mymenu made a market choice to aim for a niche sector, with more expensive restaurants, rather than take a slice of the market from the international platforms [which focus on more affordable restaurants – authors]’ (#27). In 2019, its co-founder claimed that, whereas average orders on international platforms amounted to 20 EUR, they averaged 38 EUR on Mymenu, and even 51 EUR in Milan (NewsFromThePlatform, 2019). One courier stated that ‘it’s not impossible for a person with a butler to order on Takeaway, but when [he] order[s] with friends, they all open Takeaway, Deliveroo, and no one has Mymenu’ (#27). The image is heightened by the platform’s more socially responsible approach to workers, since ‘Mymenu respects the Charter [providing workers with rights - authors] to present itself as an exception compared to other food delivery platforms, maintaining an image of being ethical platform from a worker point of view, in contrast to Takeaway, Glovo or Deliveroo’ (#22). This contributes to the image of a company upholding ‘Italianness’ (italianità) at the service of the region and its citizens (MyMenu, 2020). Operating in such a market niche allows Mymenu to work with higher margins than international platforms, with a ‘minimum delivery cost of 3.90 euro, whereas at Deliveroo it’s sometimes free, Takeaway is free, and Glovo almost pays the customer to order’ (#27). Product and quality diversification based upon exclusive restaurants and engaging with workers better shelters Mymenu’s market niche from competition than Stava’s in Poland.

International and regional platforms and working conditions

In both countries, platforms’ approaches to product markets impact working conditions, with employment models constructed to compete within markets. Whilst international platforms aim to construct uniform models across countries and avoid engaging with existing regulation if it would make them incur additional costs, regional platforms engage with regulation as a way of competing within product markets, meaning that regulatory structures and constraints impact their employment models and working conditions.

In Poland, the differences in terms of how a product market influences working conditions on international and regional platforms result from Stava’s decision to provide certified vehicles and medical testing for workers, thereby anchoring its quality-oriented market niche whilst at the same time complying with product market rules. Because Stava manages both its workers (for whom it provides medical testing which entails costs) and cars (organising which is expensive), it does not benefit from labour oversupply and operates with a regular workforce. The use of cars also lowers work intensity and improves workers’ safety, but in order to raise its competitiveness in the face of higher costs, Stava engages in regulatory arbitrage. Conversely, because international platforms circumvent the standardisation of vehicles imposed by product market regulations, workers are also exposed to higher work intensity and lower work safety.

In Italy, the differences in terms of how a product market influences working conditions result primarily from Mymenu’s decision to construct a product- and quality-differentiated market niche built on worker engagement. Investing in a sustainable reputation, the company adopts an employment model based on a socially responsible approach towards its workers, enabled by its higher margins. By contrast, international platforms compete on prices, cutting costs associated with employment or putting pressure on productivity. In contrast to Poland, Mymenu is more sheltered from competition from international platforms, with the price competition fuelled by international platforms not undercutting working conditions. Earnings differ between regional and international platforms, with the former offering higher wages due to their higher margins. International platforms also have less stable working time arrangements. Moreover, and in contrast to Poland, platforms in Italy have been on the radar of formal and independent trade union initiatives able to put pressure on platform operations in the food delivery sector (see Marrone, 2021), as we will explain in greater detail below.

Poland

Glovo PL uses a highly algorithmised employment model based on cost minimisation to increase its competitiveness. Able to maintain labour oversupply, the company benefits from greater flexibility in terms of wages, working time and work intensity. Couriers ‘have two civil law contracts with the intermediary: the first on driving for Glovo, and the other a contract leasing your car to Glovo, which is strangely structured so workers can basically make more money, as if they lend their cars to Glovo’ (#11). Constituting regulatory arbitrage, this tax-engineered set-up blurs workers’ contractual status, as well as cuts the company’s social security contributions and circumvents the requirement to operate approved vehicles.

Glovo PL pays a piece-rate combining both a fixed fee per delivery (3.5–5 PLN, i.e. 0.8–1.2 EUR) and per kilometre (1–1.5 PLN, i.e. 0.25–0.4 EUR). Thanks to the piece-rate, Glovo PL can operate with labour oversupply, as it ‘accepts everyone without any screening’ (#11) and because it ‘has no costs: 10 couriers can be logged in, be available, and Glovo pays exactly nothing’ (#10). Occasionally, to attract or retain couriers, the platform uses guaranteed rates (top-ups). Otherwise, earnings vary, being sometimes much higher than the hourly minimum rate, but usually lower. Overall, frequent changes in payment structures allow the platform to exert selective pressure on competitors in specific locations, resulting in workers being subject to fluctuations in earnings, as described by one courier who had ‘a guaranteed minimum rate of 20 PLN [ca. 4.5 EUR - authors] […]; a few weeks later, it went down to 19 PLN, and now […] they’ve given up this rate and introduced a kind of multiplier; the effect was that at the end it came out to be the same, but this multiplier is now 1.1 [lower – authors]’ (#8).

Glovo PL makes extensive use of algorithmic performance measurements where workers’ delivery times and service quality are assessed by clients and restaurants. This is possible because the platform does not supply workers with vehicles and – as a result – workers use their own vehicles. Workers’ ratings determine their access to shifts, forcing workers to be continuously available and limiting the possibility of rejecting even unprofitable tasks, as ‘below a score of 80 out of 100 you can only select the worst and most random slots’ (#9). This allows Glovo to lower costs and foster competitiveness whilst exerting pressure on workers’ performance at the expense of working time stability.

To lower their costs, most workers use their bikes for deliveries. This is possible due to the lack of vehicle standardisation resulting from the platform’s circumvention of product market regulations. Algorithmic performance measurement incentivises workers to deliver as fast as possible, negatively impacting their safety, as stated by one courier: ‘this is a dangerous work […] not really recommended unless you have good physical strength […] to earn decent money, you need to do 100 km per day on a bike’ (#8).

Takeaway PL uses a more traditional employment model with pressure on workers to increase their productivity, thereby boosting competitiveness. Workers are hired on regular civil law contracts without extra non-standard components and are paid between 18.50 and 20 PLN [4 – 4.5 EUR] an hour with a bonus for each delivery above a monthly threshold, meaning that they earn equal to or more than the minimum wage: ‘compared to platforms like Glovo, Wolt or UberEats, Takeaway is the only one that doesn’t have a piece-rate, and there are no nonstandard components in pay like calculation for kilometres or number of orders’ (#17).

Takeaway PL has a more standard system of assigning shifts: workers report their availability each week and dispatchers distribute working hours, albeit with some cuts. The platform ‘requires workers to be available at least 40 h per month’ (#20) to ensure a stable workforce. To increase flexibility, the platform often changes shifts without consulting workers: ‘when demand is low then […] they often shorten the shift by 10 min, half an hour, an hour, without paying for it’ (#18). This counterbalances the cost of maintaining a more regularised workforce.

Workers deliver on bikes and scooters (some supplied by the platform), in line with the platform’s decision not to engage with product market regulations. Algorithms are used to assess couriers’ work, but without dictating greater work intensity. However, the platform uses more direct performance management with ‘dispatchers calling all the time and asking whether workers do not want to shorten the break or prolong the shift […] or telling them to deliver faster: when workers decline, dispatchers become passive-aggressive’ (#16). Workers can be ‘fired for not improving delivery times’ (#17). This reveals an employment model focused on improving productivity to increase competitiveness, translating into high work intensity.

Since the platform circumvents product market regulations and couriers deliver on bikes and scooters, whilst at the same time being pressured to improve delivery times, there are ‘many safety issues; […] couriers complain all the time about having “duels” with trams, buses, and cars’ (#16).

Stava adopts a more traditional employment model intertwined with pressure on productivity. Working conditions have improved due to the platform’s engagement with product market regulations. However, to reduce employment-associated costs and boost its competitiveness, the platform engages in regulatory arbitrage in terms of working conditions. Workers are hired on civil law contracts without non-standard components such as couriers leasing their vehicles to the company (as practiced by Glovo). The platform is unable to make use them as – due to its engagement with product market regulations – it supplies workers with cars. ‘All Stava couriers are students aged 20-25’ (#34), as the platform wants to lower social security costs and student contributions are paid by universities. The platform thus counters its higher costs associated with engaging with product market regulations by hiring workers whose employment is cheaper.

Stava pays an hourly rate 12–17 PLN (2.7–3.8 EUR), plus 1.5–two PLN (0.4–0.5 EUR) per delivery, with bonuses for economic driving and fast delivery times. Due to the decision to engage with product market regulation and work with certified cars, workers are required to be available in specific timeframes to optimise car use. Workers effectively earn around or slightly more than the statutory minimum wage, as highlighted by one courier who had ‘worked in food delivery for many companies and platforms and thinks Stava provides really good conditions in terms of rates and equipment’ (#33). However, we detected two situations where the minimum wage was circumvented by not paying for all working time. Branch management cited financial difficulties in competing against international platforms, with ‘restaurants threatening they will go away if Stava does not lower its fees’ (#30). Since engaging with product market regulation (providing workers with cars) costs Stava more compared to international platforms, it engages in another form of regulatory arbitrage (minimum wage violations) to remain competitive.

Stava workers report high working time stability. Shifts are assigned by dispatchers after workers report their availability, without an algorithm being used. As the size of the platform workforce is dictated by the size of its car fleet, there is little or no labour oversupply, meaning that ‘shifts always corresponded with availability; sometimes the boss would call asking if [he] could stay an hour longer because it’s busy, but the boss doesn’t mind if [he] refused because [he] has other plans’ (#33).

Unlike international platforms, Stava does not use algorithmic performance measurement. ‘There’s a rumour that restaurants rate couriers but there have never been any consequences for couriers’ (#31). This results from Stava’s market positioning, with it being more oriented towards restaurant satisfaction and direct quality management rather than relying on customer reviews. Whilst an algorithm calculates delivery times, workers are not punished for not meeting them and are not forced to work faster. Couriers praised the quality of the cars used, as this improved work comfort and lowered fatigue in comparison to scooter and bike deliveries, whilst also increasing safety: ‘the cars are new, so it’s also automatically safer […] and more comfortable’ (#33).

Italy

As with Glovo PL, Glovo IT uses an employment model greatly reliant on algorithmic management to optimise employment-related costs. It hires on an occasional employment or self-employment basis and uses piece-rates calculated per delivery and distance, in line with its concept of providing a low-cost delivery service for affordable restaurants. This results in highly volatile earnings: ‘rates vary by distance, so there are times when you earn 3 euros per delivery, and others when you earn 8 – 9’ (#4). However, because Glovo is cheaper than other services it ‘has more demand, more visibility’ (#4). Therefore, ‘although Glovo pays little, there’s a constant flow of orders’ (#13). Workers can earn around average hourly wages, though this requires substantial effort.

Glovo IT uses a rating system to manage access to work and increase work intensity, with an algorithm forcing workers to accept unprofitable deliveries and incentivising overworking to retain profitable time slots. Thus, ‘it’s not true that couriers can decide when to work, because there’s rating according to which they access certain slots’ (#7). This results in uneven access to working time, with workers ‘sometimes unable to find any slot’ (#3). Glovo couriers also report safety issues due to the hectic pace of work and being incentivised to work as fast as possible: ‘When you get an order, Glovo calls and asks “have you already picked up the order?“. How can I be at the pick-up place the minute after I get a new delivery? Then they call again but I don’t answer. The police caught me once whilst I was on the phone and they told me to pay more attention because you risk having an accident or going through a red light’ (#6). To preserve its competitiveness, Glovo joined Assodelivery, an organisation of international platforms aiming to prevent further regulation. As a result of trade union pressure, the Italian government passed a law in November 2019 forcing employers to negotiate a collective agreement in the food delivery subsector, with automatic inclusion in the logistics collective agreement if no agreement was reached. In late October 2020, Assodelivery signed a collective agreement with the ‘yellow’ trade union UGL to prevent the inclusion, thereby allowing Glovo to maintain its employment model and avoid regulation (Marrone, 2021).

Takeaway IT offered similar working conditions to Glovo IT before the merger. After ‘Takeaway took over JustEat, it imposed a format entailing the regularisation of employment relations’ (#15) yet putting pressure on workers to increase their productivity. Due to an employment model focused on improving productivity and less on algorithmic management, the platform – after withdrawing from Assodelivery – signed a collective agreement with trade unions in early 2021. This regularised workers’ contractual status, provided for the hourly rates used in the logistics sector (with derogations), and overtime premiums, whilst at the same time allowing the platform to increase working time flexibility in order to stay competitive. The agreement was signed under pressure from the government and unions, but Takeaway IT used it to implement a more regularised, productivity-focused model consistent with the mode of operation adopted in other countries (including Poland). Takeaway IT now hires 70% of workforce on open-ended contracts regulated by the collective agreement (with some derogations) and 30% within more flexible contractual forms. Workers are paid on an hourly basis with overtime premiums. Rates are lower than those stipulated in the logistics collective agreement due to the derogation clause but are overall higher than on other international platforms: ‘Takeaway pays 8 EUR for the same amount of work for which you get 3.50–4 EUR at Glovo’ (#14).

Similar to its Polish counterpart, Takeaway IT assigns shifts ‘manually’. Shifts are flexibly adapted by dispatchers before and during the workday and ‘are problematic’ (#13), resulting in volatile working hours. The platform requires availability and punishes absence: ‘if you don’t cancel your shift, you incur a penalty’ (#14). Because workers are no longer self-employed but hourly-paid workers covered by a collective agreement, the platform can ‘force shifts on workers and change schedules before a shift begins’ (#15) – a drawback of regularised employment. The intention to bind workers closer to the company is manifested in the creation of the mid-management positions of ‘fleet captains who refer back to the company and quell possible conflicts [including union activity – authors]’ (Interview with union expert in Italy).

Workers are pressured to improve delivery times and work intensity is increased by dispatchers and fleet captains ‘dictating the timing’ (Interview with union expert in Italy). This again causes safety problems, as illustrated by a courier who ‘used to ride against the flow under the colonnade and always risked being insulted by pedestrians’ (#22).

Mymenu uses a more traditional and standard employment model to maintain its image as a sustainable company, putting it in a less competitive niche. It signed the ‘Charter of fundamental rights of digital labour in the urban context’ in 2018, together with major trade unions (CGIL, CISL, UIL), informal trade union Riders Union Bologna, and Municipality of Bologna as representative of the local government, which is a local agreement regulating both labour standards and product services. Charter provides for negotiated minimum wages, seniority increments, 13th and 14th salaries, paid holidays, sick leave, full social security contributions, and working time regulation. The platform holds ‘regular meetings with workers’ (#23) where ongoing problems are discussed. It has relatively good relations with unions, in line with its image of an ‘ethical company’ (#22) and ‘platform best for workers’ (#27). In contrast to international platforms, it engaged in collective bargaining long before being pressured by unions and the government, thereby standing out from international platforms and using Charter as a hallmark. It is thus carving out its niche by opportunistically accommodating collective pressure from workers as a means of positioning itself within product markets.

Mymenu allows workers ‘to choose between different contractual statuses’ (#26): occasional employment, parasubordinate work and employment contracts regulated by collective agreement negotiated in the logistics sector. It pays workers 7–8.50 EUR an hour, plus 0.50 EUR for each delivery. Rates are reportedly higher than on international platforms due to Mymenu operating in a less competitive niche: ‘maybe 20 out of 300 Deliveroo couriers earn 2000-2200 EUR, but the others earn a lot a lot less […] Mymenu pays well’ (#27).

Workers enjoy a high level of control over their working hours due to Mymenu’s socially responsible approach and a collective agreement guaranteeing a minimum number of working hours. As a result, ‘unlike other apps where you struggle to book hours on a calendar with slots, at Mymenu you fill out the Excel sheet with your availability […] and a dispatcher assigns shifts’ (#23). Workers report their satisfaction with this system, reflecting the platform’s image-boosting intention to offer better working conditions.

Rating systems and algorithmic performance measurement are banned by the collective agreement. Workers are not punished for not meeting delivery times calculated by app and are not forced to boost work intensity. Indeed, work intensity is lowered by a ‘more prevalent human factor compared to Glovo and Takeaway’ (#22), smaller delivery zones and less pressure to improve delivery times. As a result, workers feel safer, with one courier reporting that ‘when working for Takeaway and Glovo [he] used to ride against the flow under the colonnade and always risked being insulted by pedestrians […] But with Mymenu [he] can fortunately avoid doing that’ (#22).

Comparing international and regional platforms across countries

The central question was whether international and regional platforms approach product markets differently and to what extent this shapes working conditions.

We found that international platforms engage in price competition in both countries, avoiding the relatively more stringent product market rules in Poland and not being affected by the less stringent ones in Italy. This corroborates previous research showing that platforms avoid engaging with country-based market regulation (Seidl, 2020; Thelen, 2018), also by creatively reacting to changes in product market rules specifically designed to target them (Allegretti and Rodrigues, 2021). Platforms thereby ‘set the rules for market participants and enforce these self-made rules [...] in a largely unregulated setting’ (Hassel and Sieker, 2021: 29). Our research adds elements on how platforms set these ‘self-made rules’ by adapting sectors they enter either through circumventing market regulation (Poland) or benefiting from less stringent market regulation (Italy), and thereby creating their own differentiated embeddedness. We shed light on the knock-on effects the operations of international platform have on regional platforms and their working conditions, explaining how international and regional platforms engage in adapting sectoral market rules by creating their own differentiated embeddedness within the institutional market context they contribute to shape.

In both Poland and Italy, international platforms engage in price competition within product markets to build a dominant market position, with employment outcomes differing between platforms but similar across the two countries, regardless of the institutional framework. Glovo uses an algorithmized employment model aimed at improving performance and optimising costs, resulting in the platform using non-standard forms of employment and piece-rate payment, which in turn lead to volatile working hours, high work intensity and low safety levels. Takeaway adopts a standard employment model which enhances productivity through work intensity (dispatchers, target-setting, etc.), whilst offering more standard contracts and hourly pay, resulting in more regularised working time (albeit flexibly adjustable by dispatchers), high work intensity and low safety levels. This intersects with collective labour regulation. In Italy, regulation enforced by trade unions within the sector has induced international platforms to experiment. Glovo IT, for example is engaging in bargaining with a ‘yellow’ union to avoid regulation, whilst Takeaway IT is using bargaining to implement a regularised model and align its local operations with their global competitive strategy. It shows how distinctive elements of labour market settings can be creatively used by platforms to continue their operations in product markets in an undistorted manner (compare: Drahokoupil and Piasna, 2019; Ilsøe, 2020; Jesnes et al., 2019).

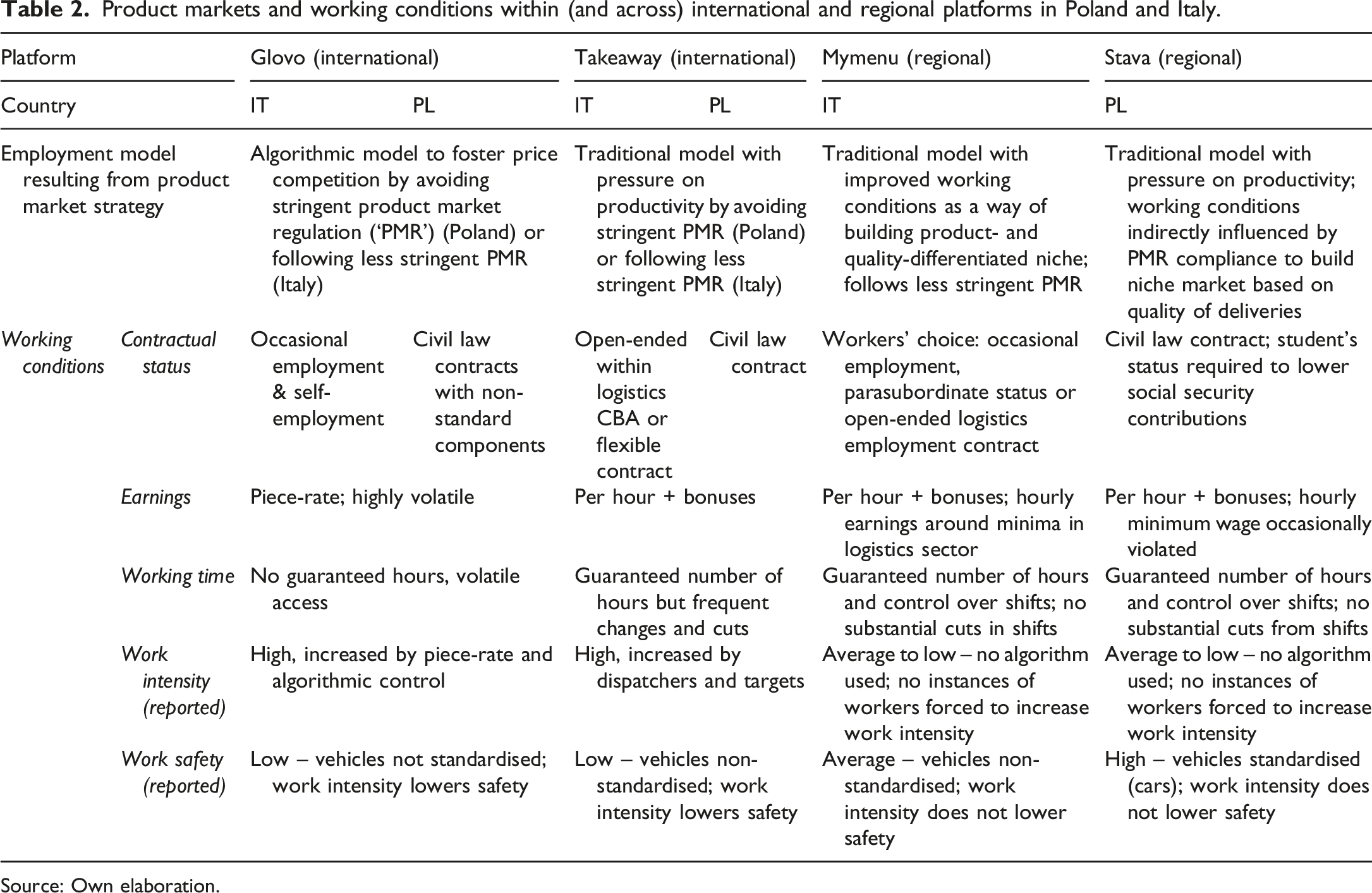

Product markets and working conditions within (and across) international and regional platforms in Poland and Italy.

Source: Own elaboration.

The distinctive way in which regional platforms are embedded in product markets explains how they engage with existing market regulation, shaping employment models which deliver working conditions different to those of international platforms. Especially, we posit that working conditions differ between international and regional platforms, with the former constructing their employment models in an institutional void, whilst the latter engage with regulation as a means of competing against their international counterparts. Working under the dictates of regulatory frameworks, regional platforms adopt different employment models and generate different working conditions, generally offering greater working time stability, lower work intensity (with no algorithmic performance measurement) and higher safety levels. At the same time, because regional platforms are impacted by country-specific regulations, we observe cross-national differences, with Polish regional platforms impacted more by statutory regulation (health and safety standards mandating the use of cars), and Italian ones impacted more by pressure from organised labour (with platforms opportunistically accommodating this pressure as a means of positioning themselves within product markets).

Conclusion

Our study suggests that international and regional platforms adapt to market rules, thereby constructing their embeddedness differently. International platforms foster price competition within product markets to build dominant market position by circumventing market rules, thereby impacting working conditions. Conversely, regional platforms uphold the rules as a means of circumventing competition from international platforms and carving out market niches.

Our study also suggests that country-specific contexts matter. In the Polish context, where product market regulation exists, the regional platform engages with it, with consequences for its employment model and working conditions. In the Italian context, the regional platform has built a coalition with customers, local government and workers to shape a market niche, forcing and allowing it to provide better working conditions. When ground for differential embeddedness is limited to engaging with product market regulation, as in Poland, working conditions are only indirectly affected by management having to integrate rules protecting customers in the employment model. However, platforms might have to position themselves within product markets by engaging with labour markets as well – as evidenced by the Italian case. Overall, in the Italian case labour market influences how platforms interface with product markets, with platforms having to accommodate stronger pressure from workers, local governments and customers in how they position themselves within product markets and subsequently how they shape their employment model. It shows that the mode of approaching product markets may be impacted by this variegated set of influences.

Our findings point to the necessity to jointly analyse labour and product markets when attempting to explain how platforms shape working conditions. Firstly, platforms can contribute to deteriorating working conditions – but this premise is rooted not only in the way they tackle labour market regulation, but also product market regulation. Regulation protecting customers (e.g. standards of service provision, permits and licences) may set the framework for managing workers, whilst not engaging or circumventing such regulation can indirectly impact working conditions. Secondly, product markets are also affected by labour markets – the demand from customers for a more sustainable service fuelled by collective action has the potential to improve working conditions on platforms.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: The research on which this paper is based received funding from the European Research Council (ERC Advanced Grant) under the European Union’s Horizon 2020 research and innovation programme (grant agreement n° 833577 – Project ResPecTMe – ‘Resolving Precariousness: Advancing the Theory and Measurement of Precariousness across the paid/unpaid work continuum’).

Ethical approval

The research project ResPecTMe has been reviewed and given a favourable opinion from the Social and Societal Ethics Committee, dossier G-2019 07 1689. The research project ResPecTMe has been reviewed by the European Research Council Executive Agency, with ethics approval granted on 10 July 2019, Ref. Ares(2019)4404751, and reviewed in the framework of the ERC ethics monitoring process with ethics periodic monitoring approved on 21 August 2020, Ref. Ares(2020)4364550. It has been further reviewed by external ethics advisor on 22 February 2021.