Abstract

In recent years, the European Union has supported the development of a new civil security market, capable of providing security technology for new and global security challenges. This article analyses the emerging growth market for civil security in relation to contemporary notions of potential crisis and emergency. Building on ongoing academic analysis of what Melinda Cooper has termed ‘economies of emergence’, the article points out how the figure of emergence generates investment in more flexible, adaptive and, so it is argued, potentially lucrative markets for civil security. Drawing on observations at a number of security trade shows and stakeholder workshops, the analysis demonstrates that ‘civil’ aspirations, concepts and technologies build on earlier formulations of military strategic discourse in the so-called Revolution in Military Affairs – though in complex and sometimes contradictory ways. More generally, the motivation behind the analysis is to investigate civil security and civil markets as performative enactments, and so to critically engage with the emergence of the civil security market as a priority in EU policymaking.

Introduction

On 26 July 2012, the European Commission published a communication on a ‘Security Industrial Policy’ in which it called for the development of a better functioning internal market for security technology. In the staff working document that accompanied the communication, the Commission explains that ‘the threats to which our society is confronted are permanently evolving’, and that ‘terrorists and criminals will always look for loopholes in our technologies and try to bypass our security systems’ (Commission of the European Communities, 2012a: 4). In such a context, ‘no security concept is thinkable without adequate technologies’, making the European Union (EU) security industry ‘the conditio sine qua non of any viable European security policy’.

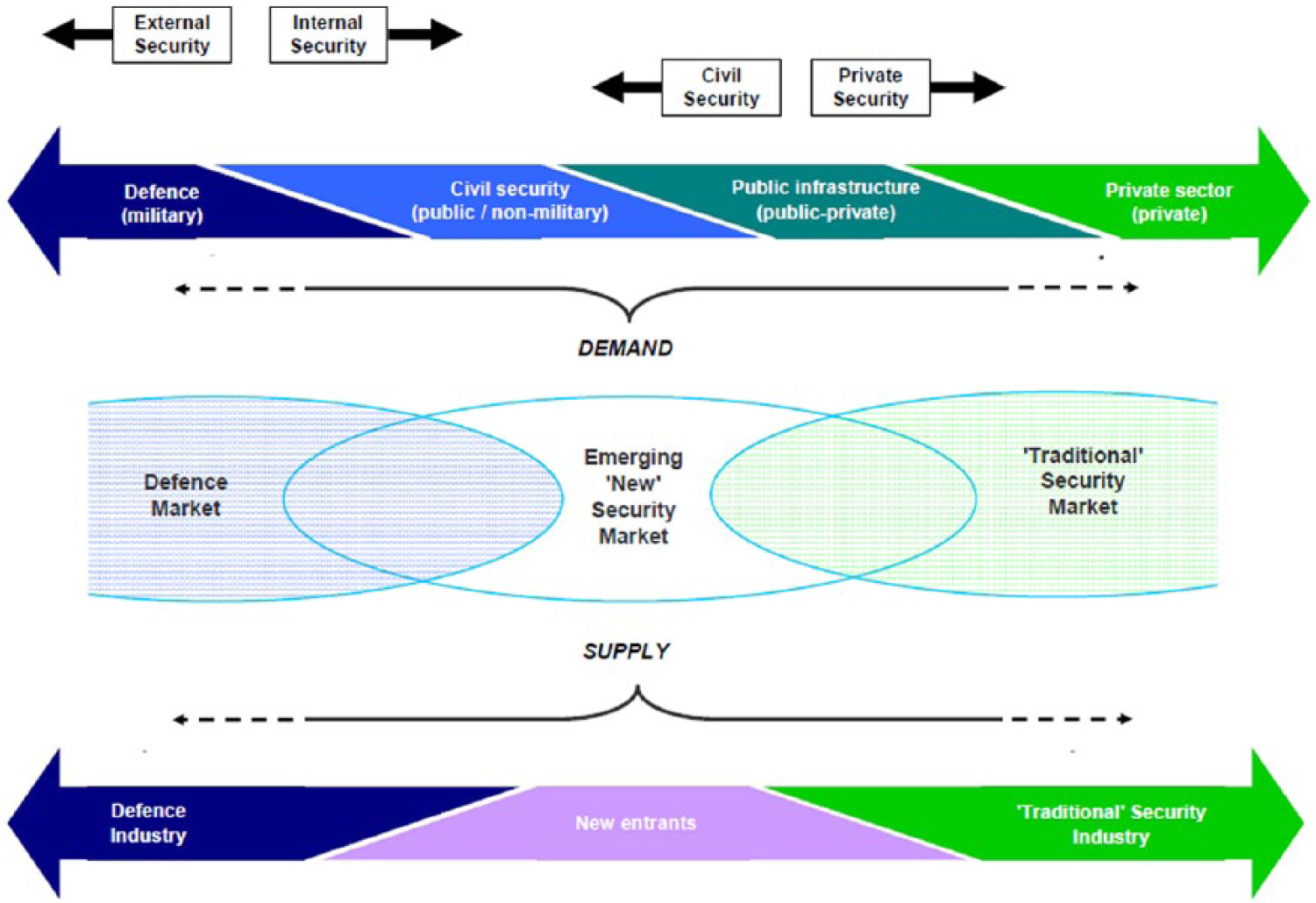

These and related claims about the unpredictability of new and global security challenges have been rehearsed in many EU policy papers, public statements and research documents published over recent years. Together, these statements underpin the call for the development of a new civil security market, capable of providing technology for what is considered a more asymmetric and fluid threat environment. Examples of such technologies include tracking and tracing systems for the security of maritime and land borders; explosives detection and identification capabilities for the protection of critical infrastructure and urban transport networks; and vaporizers, vaccines and sensors for disaster management (Commission of the European Communities, 2004: 18–19). Figure 1, which featured in a study on the competitiveness of the EU security industry conducted by the Dutch consulting company Ecorys and commissioned by the European Commission, visualizes how the purportedly changing threat environment functions as an important impetus for market development. The figure consists of three ovals representing three security submarkets, with the middle, overlapping oval representing the ‘emerging “new” security market’ for civil equipment. The image further depicts the characteristics of the demand and supply side for different security markets. In terms of a categorization of the demand-side security responsibilities, two final distinctions are made between external and internal security, and between civil and private security.

Overview of the security market: Supply and demand characterization.

Underlying the image, a distinction is made between two security threat categories: traditional and new threats. Corresponding to ‘endogenous threats’ posed by ‘ordinary’ criminal activity, the private security sector supplies equipment for protecting against the traditional security challenges, including physical access control, intrusion detection, and CCTV and video surveillance. The new security threats, by contrast, concern ‘exogenous threats’, most notably terrorism and organized (cyber) crime, but also other major non-man-made catastrophes (Ecorys Research and Consulting, 2009: i). As the figure displays, these threats are considered best targeted by an emerging new market that cuts through the traditional public–private distinction and bridges the defence market and the private security market. In so doing, it is suggested that this market will provide equipment for a more diffuse range of customers, including public but non-military authorities (law enforcement, civil order and emergency response entities) and public–private partnerships, for instance in the area of critical infrastructure protection, counter-terror intelligence and aviation security.

Looking at the supply side, the figure also points to the business and trade opportunities related to the emerging new market. Although not (yet) fully mature or realized (the market is left blank in the image), the new market enables traditional defence and private-sector companies to amplify and diversify their production of equipment, and new companies to enter the market space. The European Commission echoes the potential of the market in the communication cited above, pointing out that the global security market has grown nearly tenfold from €10bn to a market size of €100bn in 2011, and that the global demand for security equipment is projected to grow by 5% annually in the coming years, primarily benefitting civil security providers (Commission of the European Communities, 2012b). In this context, a key priority for the Commission has become the development of policy initiatives that exploit potential market growth. The most fundamental of these initiatives has been the establishment of a large-scale security research programme under the Seventh Framework Programme (FP7), through which the EU has invested €1.4bn for research and development of civil applications of security technology between 2007 and 2013. 1

This article analyses the emerging growth market for civil security in relation to contemporary notions of potential crisis and emergency. Adopting the Commission’s notion that this is an ‘emerging “new” security market’, the article examines how the market is embedded in a longer history of thinking about processes of emergence as sources of both threat and opportunity. Accordingly, the article’s analysis has a dual focus. First, and in line with the theme of this special issue, it investigates how the growing interest in civil security arises from the notion that the occurrence, origins and unfoldings of contemporary threats have become uncertain and inherently speculative. In Europe, these framings underpin investment in more ‘flexible’, ‘adaptive’ and, so it is argued, potentially lucrative markets that cut through traditional public–private and civil–military distinctions (Commission of the European Communities, 2006: 68). Second, this article examines how these civil markets have their roots in earlier formulations of military strategic discourse in the ‘Revolution in Military Affairs’ (RMA) in the late 1990s. Building on the work of Manuel de Landa (1991) and Michael Dillon and Julian Reid (2009), among others, the article draws out how the aspirations, concepts and technologies that appear as distinctively ‘civil’ are embedded in military discourse. Situating civil security in ongoing academic analysis of what Melinda Cooper has termed ‘economies of emergence’, this article contributes to these discussions by inquiring how military logics and concepts – notions of interoperability and situational awareness, in particular – are now also participating in constituting civil markets (Cooper, 2008: 96–98, following Marazzi, 2008).

In this manner, the article relates to conversations about the growing importance of private actors in security governance and the relation between commerce and security more broadly. To date, research has primarily addressed the deployment of private military companies in war situations (Avant, 2006; Leander, 2005), or has focused on the everyday work of private security contractors in weak states where the public sector is underdeveloped (Abrahamsen and Williams, 2009, 2011; Leander and Van Munster, 2007). Taking seriously Rita Abrahamsen and Michael Williams’ (2009: 13) claim that the coming into existence of security practices that are simultaneously public and private is ‘neither rare, nor limited to weak Third World governments’, this study presents an enquiry into private-sector involvement in Europe. In so doing, the article is concerned less with the day-to-day involvement of security service providers, and more with an analysis of the constitution of security markets.

Thus, an important motivation behind this research is to examine the ways in which civil security has been articulated as a security problem and a site for intervention. In fact, ‘civil’ is not a stable concept that preceded security practices developing in its name (Bialasiewicz et al., 2007); rather, it has required considerable discursive work across expert and policy documents and specific locations such as security exhibitions and stakeholder workshops (Huysmans, 2006; Walters, 2008). Similarly, as work on the performativity of markets reminds us, markets themselves are effects of performed operations of what Michel Callon calls ‘framing’ and ‘disentangling’ (Callon, 1998: 16–17; see also De Goede, 2006). That is, markets do not pre-exist these performances, but they are made possible only by a wide variety of procedures, calculating tools and devices, including the figure presented earlier (Best, 2012). Understood in these terms, it is, in fact, impossible to speak of ‘the market’ for civil security. 2 What we have to analyse instead are the multiple ‘workings’ or effects of civil security, and the ways in which civil markets are always in formation as new alignments, arrangements and exclusions are produced (Mitchell, 2007). As the introduction to this special issue indicates, examining civil markets as performative also means drawing attention to the ways in which market effects may be contradictory, or to how contestation and dissent give active shape to market development and security practice. In the following text, the analysis thus specifies how market development is rooted in ambivalence over the boundaries of civil security and its relations with the military domain.

The analysis is based on observations at a number of industry-oriented events, as well as 24 interviews conducted with Commission officials, industry representatives and journalists between June 2012 and November 2013. Furthermore, I draw on a close reading of key reports and policy documents in the field, with special attention paid to the competitiveness study published by Ecorys and the Research for a Secure Europe report by the Group of Personalities in the Field of Security Research (Commission of the European Communities, 2004). The argument proceeds in four steps. I begin by tracing notions of emergence and analysing how processes of emergence have been incorporated in security strategy and practices. Building on this framework, the next section traces in detail the co-emergence of civil security and security markets in European policy discourse. The article will then explore the themes, aspirations and technologies that emerge as distinctively ‘civil’ in discursive documents and security trade shows. Finally, I will consider some of the political concerns surrounding the emergence of a market for civil security.

Emergence and profit

A rich body of literature points out that security governance today is characterized by its orientation toward preemption, particularly in the context of the so-called war on terror (Amoore and De Goede, 2008a, 2008b; Anderson, 2010; Aradau and Van Munster, 2008; Massumi, 2007; Simon, 2012). A preemptive security mode, according to these contributions, addresses itself to threats that are irregular, incalculable and in important ways unpredictable. In her analysis of US neoliberalism and the emergent possibilities of the life sciences and biotechnology, Melinda Cooper (2008: 89) considers preemption to act against a threat that is ‘emergent’ – that is, ‘a threat whose actual occurrence remains irreducibly speculative, impossible to locate or predict’. Cooper traces the notion of emergence in the work of microbiologist René Dubos, who, she argues, was the first to coin the term as a way of defining the temporality of biological evolution. According to Cooper, Dubos, writing in the 1950s, dismissed the then dominant belief that the evolution of life developed in linear ways and hence could be predicted and controlled. Dubos claimed instead that microbial life evolved continuously, unexpectedly and in complex alignment with human cells and all other forms of life on earth. Decades later, Dubos’ writings are central to a new public health discourse that, as Cooper puts it, ‘defines infectious disease as emerging and emergent – not incidentally, but in essence’ (Cooper, 2008: 80, emphasis in original). ‘What public health policy needs to mobilize against’, she writes, ‘is no longer the singular disease with its specific aetiology, but emergence itself, whatever form it takes, whenever and wherever it happens to actualize’ (Cooper, 2008: 80, emphasis in original; see also Elbe et al., this issue).

For the purpose of this article, what is key is Cooper’s argument that the new discourse on emerging infectious disease has resonated with more recent post-Cold War reformulations of US defence strategy. Not only has the US military become concerned with emerging infectious disease as a security threat, and begun to integrate biological weapons into its defence arsenal, it has also come to define the global threat environment as emergent more generally. This applies to the new global terrorism in particular, which, it is argued, is no longer confined to state boundaries, but uncertain, emergent and potentially catastrophic by nature. Similarly, others have analysed the close relation between ‘life-as-emergence’ and transformations in thinking about security and war (Anderson, 2011: 395; De Landa, 1991; Dillon, 2007; Dillon and Reid, 2009; Martin, 2007; Massumi, 2009). Michael Dillon and Julian Reid, in their analysis of the ways in which the ‘liberal way of rule and war’ has come to evolve around life itself, observe how in the wake of the confluence of the molecular and digital ‘revolutions’, life has become framed as information and as a process that is emergent, complex and contingent. These understandings have changed threat perception in fundamental ways. Across multiple domains of life, Dillon and Reid write, ‘molecular processes of emergence … become prime sites of insecurity’. Once their life-like qualities are foregrounded, ‘so is also their potential for becoming-dangerous’ (Dillon and Reid, 2009: 108, emphasis added).

As life has been defined by emergence, the force of becoming has also become incorporated in security strategies and practices. Dillon and Reid situate the origins of contemporary military strategic discourse in the growing importance of information-based technologies and the development of cybernetics and new command-and-control systems during and after World War II. In particular, they show how the wartime work of Norbert Wiener, whose design of the anti-aircraft predictor laid the foundations for the science of cybernetics, was further developed in dialogue with bio-evolutionary theorists working on processes of complex emergence (see also De Landa, 1991: 43). What Dillon and Reid consider the ‘biologization’ and ‘informationalization’ of warfare has found its expression most prominently in the Revolution in Military Affairs (RMA) of the late 1990s. The RMA’s significance does not simply lie in the purchase of intelligent weapons systems. Rather, it entails ‘a whole scale re-engineering of military strategic discourse that in turn embraced all the key concepts, while also adopting much of the same biologized vocabulary, as that of the complexity as well as the information and communication sciences’ (Dillon and Reid, 2009: 114). In this sense, the life sciences have come to function as a focal point to which reference is made when military forces recognize military bodies as adaptive, mutable bodies – or ‘swarms’ – or when they reorganize military command structures according to decentralized ‘networks’ (Dillon, 2007: 13; see also De Landa, 1991).

Several commentators have interrogated how the figure of emergence has given rise not only to new sources of danger, but also to new enterprises (Anderson, 2011; Braun, 2011). In particular, theorists working at the intersection of insurance and global security have begun to draw out the close relation between emergence and profit (Ericson and Doyle, 2004; Martin, 2007; O’Malley, 2004). They point out that insurers have come to recognize and insist on the commercial value of indeterminable and uncontrollable risks. What is common to the insurance industry and other industries profiting from ambiguity is their reliance on what Linsey McGoey calls a ‘politics of conditionality’ – that is, the notion that economic authorities thrive on their inability to predict or verify future threats (McGoey, 2012: 8, following Massumi, 2007). In this context, McGoey writes, one can never really be wrong: if a predicted threat materializes, authorities are credited for their foresight; if an unpredicted threat materializes, authorities can call upon the inability to prevent low-probability risk. More so, if a predicted threat fails to manifest itself, this only nurtures the idea that the next crisis is near and that we need to become prepared. Similarly, when the expectations surrounding new technologies or markets prove uncertain, this only generates further investment, ‘for more hope and hype are needed to remedy thwarted expectations’ (McGoey 2012: 8; see also Sunder Rajan, 2006).

Melinda Cooper analyses these developments in terms of the rise of an ‘economy of emergence’ that relies on the deployment of speculation and affective perceptions of contingency and unpredictability. Drawing on Christian Marazzi, who discusses the venture-capital model of accumulation as an economy in which ‘everyday productivity is increasingly determined by the capacity to respond in unforeseen and unforeseeable situations, emergent situations’, (Marazzi, 2008: 51, emphasis in original), Cooper argues that this is a model of economic growth in which production comes to be contingent on the inconsistencies of stock market investment (2008: 96). She discusses in detail how, in the USA during the 1990s, investment in the life sciences and biotech industries was generated on the prospect of economic growth following the emergence of new information and communication technologies. But, when the economy slowed in the early 2000s, the pursuit of economic development became, according to Cooper, tied to a new strategic vision under President George W. Bush. Regarding the life sciences, there was again investment, ‘but this time on the pretext of permanent war rather than permanent growth’ (Cooper, 2008: 97; see also Marazzi, 2008: 151). Both neoliberalism under President Bill Clinton and neoconservatism under Bush, then, mobilized speculation, but there is a key difference in the two subtexts of profitable emergence. Whereas during the 1990s emergence spurred further investment based on the widely held belief in the opportunities associated with new information and communication technologies, under Bush investment became linked to preempting radical unknowns in the context of the global war on terror. What changed, then, ‘is the affective valence of “our” relation to the future – from euphoria, to panic to fear, or rather alertness’ (Cooper, 2008: 97).

Cooper’s conceptualizations are not just applicable to the US context. They offer a fruitful way to explore the emergence of a new civil security market in Europe. First, contemporary threat imaginaries that support market development formulate that Europe has become exposed to ‘global’ security challenges that are indeterminate and incalculable (Commission of the European Communities, 2003, 2004; Council of the European Union, 2003). According to these narratives, the end of the bipolar order has given way to a more ‘fluid’ threat environment with new types of threats (including bio-threats) that ignore traditional state borders and target European interests both inside and outside EU territory (Commission of the European Communities, 2004: 6). In a world marked by potential disasters and crisis, security is supposed to remain open to new and unknown connections and to become emergent itself. Concerning civil markets, as we will see, this is translated into the aspiration to bring together expertise from telecommunications, biotechnology, electronics, and defence and aerospace, and to cut through traditional civil–military distinctions.

Second, the notion that threats could emerge from anywhere at any time has been joined with the desire to integrate security and economic profit in a seamless manner. What we see in Europe – and what is being visualized in Figure 1 – is a strongly held belief in the opportunities associated with civil security, even though it is recognized that, as of yet, market structures are immature and fragmented, and market development overall is insecure. More so, the uncertainties surrounding market development and the proclaimed specificities of the civil market – the problem that the market is event-driven and largely dependent on public demand – have only contributed to further investment in civil security. This is, then, a market that relies on a double speculative move, speculating on future threat scenarios and on future production and profit.

Third, analysing the civil market as an economy of emergence renders visible how what is constituted as civil security draws on military strategies, rationalities and technologies of emergence. As discussed by Dillon and Reid, Manuel de Landa and others, contemporary military strategy is closely connected to notions of life as emergence. Military literature in the RMA has expressed this most clearly, applying ‘a blend of [information and communication technology] thinking with complexity sciences to the problematic … of war’ and promoting the exploitation of new information and communication technologies (Dillon and Reid, 2009: 114). The last section of this article explores how civil concepts, aspirations and technologies draw on military responses to the emergence of new information-based technologies. Before turning to these developments, though, I first discuss the co-emergence of civil security and the market in EU policy discourse in recent years.

Fluid security/flexible markets

EU efforts to establish a common market for civil security have their origins in concerns about the development of the defence sector. In 1996 and 1997, the Commission published two communications on the ‘defence-related industry’, emphasizing that despite developments toward a common foreign and security policy (formally introduced as the European Security and Defence Policy with the Treaty of Amsterdam in 1997), ‘there can be no European defence policy or identity without a healthy and competitive European technological and industrial base’ (Commission of the European Communities, 1997: 4). These attempts to frame armaments trade and production as economically vital and belonging to internal market considerations encountered significant opposition from the member-states. But, where EU involvement in the field of defence failed to materialize, the Commission has been much more successful in raising activities for what could become a lucrative market for civil security.

The objective of strengthening an internal market for civil security has become closely linked to an understanding of threats as more dynamic and non-linear. As part of this narrative, it is argued that traditionally separate notions of internal and external security have merged after the end of the Cold War and that in an environment that is increasingly characterized by open borders, ‘global’ security challenges may compromise Europe’s security also on a more local level (Council of the European Union, 2003; for a critique of how ‘new’ these developments are, see Campbell, 1992; Weldes et al., 1999). The 2003 Commission communication on ‘European Defence – Industrial and Market Issues’ for the first time connects a need to anticipate emerging threat scenarios to security technology and the objective of looking at ‘the functioning of the single market and the economic interests of a variety of civil [security] industrial sectors’ (Commission of the European Communities, 2003: 16). Concretely, the communication proposes the launch of the ‘Preparatory Action on Security Research’ (PASR) programme, a funding scheme for pilot projects in the areas of explosives detection, aviation and maritime security, and emergency response, and the precursor of the Seventh Framework Programme (FP7) for security research. Between 2004 and 2006, the PASR programme funded 39 research projects for a modest total contribution of €44.5m and without clear research results (Bigo and Jeandesboz, 2009). The introduction of the program has been crucial, however, as a way of convincing the European Parliament to allow investment in civil security, and as an important first instrument for the Commission to foster market-making in this field. Security research has been, and will remain, one of the key practices pushing along the civil security market.

In order to establish guidelines and priorities for security research, the Commission constituted the so-called Group of Personalities in the Field of Security Research (2003–2004), a high-level advisory group co-chaired by the Commissioner for Enterprise and Information Society and the Commissioner for Research, and comprised of eight security-industry chairmen and chief executives (representing defence-oriented companies such as Thales, EADS, Finmeccanica and BAE Systems), four serving members of the European Parliament, four heads of research institutes, two European defence-ministry officials and two high-level European politicians (former President of Finland Martti Ahtisaari and former Prime Minister of Sweden Carl Bildt). The Group’s final report, Research for a Secure Europe (Commission of the European Communities, 2004), sets out the structure and scope of a common research program and provides the rationale for the constitution of the civil domain. In particular, the report subscribes to the viewpoint that there is a need for further investment in security research and technology, both as a response to the rise of new security challenges and as a way of contributing to EU competition and growth policies. The Group’s report reflects and reinforces the notion that contemporary threats are no longer confined to state boundaries, but uncertain, emergent and potentially catastrophic. According to the Group of Personalities, ‘political, social and technological developments have created a fluid security environment where risks and vulnerabilities are more diverse, less visible . . . and less predictable than those Europe faced during the Cold War’. As part of this context, threats ‘can evolve rapidly … are often asymmetric and can threaten the security of member states both from outside and inside EU territory’ (Commission of the European Communities, 2004: 10, emphasis added). Further, in a world that is marked by increasing interdependence and circulation, threats are increasingly ‘interrelated’ and ‘multifaceted’, often combining different security challenges – such as bad governance, human trafficking, organized crime and terrorism (Commission of the European Communities, 2004: 10).

The previous section has suggested a new comprehension of the economic value associated with emergence. For the Group of Personalities, the prospect of growth hinges on the ability to foster cross-sector transformation and integration between civil and defence applications of security technology. The Group writes: Civil and defence applications increasingly draw from the same technological base and there is a growing cross-fertilization between the two areas. Technologies initiated for defence purposes have already led to important commercial applications. The Internet and the Global Positioning System (GPS) are the most prominent examples of such dual-use technologies. However, ‘spill-over’ effects increasingly work both ways: the so-called ‘Revolution in Military Affairs’, in particular, is based on a combination of electronics, information technology and telecommunications…. In the key area of ‘network-enabled capability’, there is a distinct technology flow from the civil to the defence sector. (Commission of the European Communities, 2004: 12)

The appropriation of the information revolution opens up new enterprises for the military as it did for business. This notion of spill-over thinking was central to the military literature in the RMA: just as business was dealing with the challenges of an enlarging market by exploiting information technology, so too US forces were grappling with a presumably more global threat environment after the Cold War, capitalizing on similar types of technology (Lawson, 2011). The RMA entailed a rearticulation of military doctrine according to the insights offered by the information sciences – that is, military formations were to organize themselves in networks that would generate power through the distribution of information. In this sense, pioneers of the RMA sought to revise traditional distinctions between the civil and the military domains, viewing military force instead as deeply embedded in a broader network of informationally constituted relations (Dillon and Reid, 2009: 117).

Economic growth in civil security relies on the capacity to tune security applications of information technology – most of them first produced for military purposes – to the civil domain. The Group of Personalities writes in this respect that ‘the technology base for defence, security and civil applications increasingly forms a continuum’ (Commission of the European Communities, 2004: 12). While civil markets build on the spill-over thinking that has marked the RMA, they also entail a reversal of that thinking. This time, civil security needs to parallel transformations that have taken place in the ways in which military force has been organized. For instance, in Europe, we hear that civil markets need to embrace a common culture of planning, programming and foresight that is similar to that of the military (Security and Defence Agenda (SDA)/European Organization for Security (EOS), 2011). Looking jealously at the work of the Defense Advanced Research Projects Agency (DARPA) in the USA, various commentators in Brussels point out that Europe requires a more ‘flexible’ approach to research and innovation that has the potential to bridge the gap between civil and traditional defence research (see e.g. Commission of the European Communities, 2004). ‘In the US’, one Commission official told me, ‘they just decide that they need a soldier that can heal himself when he gets shot and then DARPA invests in this self-healing soldier for the next twenty years.’ What we need in Europe, he claimed, ‘is somewhat of a similar dynamic’. 3

To a large extent, the notion that traditional civil–military distinctions need to be cut through has been promoted by the larger European defence companies. As Guittet and Jeandesboz (2010: 237) write, the growing importance of civil technology has been one of the most fundamental changes to the defence sector, particularly in Europe. In fact, as becomes apparent from the composition of the Group of Personalities, those representing the ‘industry’ in Europe, especially in the early years of security research, were the larger-scale companies with ties to the defence equipment and armaments domain (Jeandesboz et al., 2012: 199). It is companies like Thales, BAE Systems and Finmeccanica that have supported a civil market that combines new electronics and information and telecommunications technology with (traditional) defence technology and expertise. Pointing to the successful collaboration of the European aerospace industry that led to the Airbus venture in the late 1990s, these companies have called for channelling research funds to the emerging domain of civil security as well. They have also benefitted from the lobbying work of organizations such as the Aerospace and Defence Industries Association of Europe (ASD) and the European Organization for Security (EOS). The latter, in particular, has emerged as an influential and active player in European security matters since its establishment in 2007.

The role of the European Commission has been equally important in raising the issue of civil security. For the Commission, putting forward the notion of global or civil security reflects an attempt to bypass member-states’ apprehension towards EU involvement in the defence sector during the late 1990s. That is, placing emphasis on the development of a less sensitive market for civil security has enabled European intervention in the security domain without alarming the member-states. We thus find that EU efforts to establish a common market for civil security have their origins in the failed attempt to integrate European defence markets. Above all, the Commission’s attempt to frame civil security as an issue subject to internal market considerations means that it has been able to claim competence and expertise in this domain and to cast (civil) security as a profitable and politically neutral product (Abrahamsen and Williams, 2009, 2011). In their analysis of the private security industry in South Africa, Abrahamsen and Williams observe how private logics of business and trade function as an important impetus for intervention and investment in security matters. In what they call global security assemblages, ‘the private logics of global business circulate through public institutional domains’. Operating with private security actors, these public domains, in turn, become ‘powerful agents for globalization’ (Abrahamsen and Williams 2011: 100–101).

In Europe, it is not without significance that civil security has been assigned to the Directorate-General for Enterprise and Industry, and not, as was expected, to the Directorate-General for Research and Innovation (RTD) or the (former) Directorate-General for Information Society and Media (INFSO). Under the Directorate-General for Enterprise and Industry, the empowerment of the security industry has taken place with the active endorsement of European authorities. For the Directorate-General for Enterprise and Industry, more than enhancing security, the emphasis has come to lie on establishing a profitable and more coherent functioning internal market for civil technology through security research. Put differently, as one Commission official complained: ‘DG Enterprise and Industry is not interested in policymaking; they don’t issue policy’. 4

Criminologists have analysed the growing importance of private security as closely connected to the commodification of security and the spread of consumer culture more broadly. They have pointed out that security has become a service or product that can be bought and sold in the marketplace and traded globally (see also Garland, 2002; Loader, 1999; Zedner, 2006). This article underwrites the notion that, under the Directorate-General for Enterprise and Industry, civil security has emerged as a politically neutral service or product – that is, a commodity. At the same time, market development in this context is not seamless and cannot be understood as driven by the free and constant circulation of products across borders in a liberal world economy. In particular, this is not a market that relies on responsible individuals and organizations consuming security; on the contrary, many envisioned customers – airports, urban transport operators – resist responsibility for security work and often refuse to invest in civil security technology (Wesseling, 2013). Similarly, these civil operators have questioned the Commission’s focus on technology and market development, emphasizing that security challenges in the civil domain require a more varied approach. They have been supported by the sector-specific Directorates-General in the Commission, such as the Directorate-General for Transport, who have claimed that what they consider are very diverse and complex security matters in the civil domain cannot be dealt with by market development only.

The objective of this section was to trace the co-emergence of civil security and the market and to problematize both as stable categories. To a large extent, the Commission and the industry are themselves uncertain about the qualities and boundaries of the market. For them, an emerging strategy has been to frame the new market as ‘fragmented’ and ‘immature’, yet potentially lucrative (see e.g. Commission of the European Communities, 2012b). Further, they have argued that this is a market that is largely dependent on the manifestation of events that have not yet emerged, or have not yet even been identified – a market that depends on what may happen. What has been suggested, however, is that it is precisely these twin potentialities that support further investment in civil security research and innovation.

Correspondingly, the European Commission and the industry alike have been ambivalent about what constitutes civil security. While those participating in the Group of Personalities have argued that the technology base for defence and civil security applications increasingly forms a continuum, this is increasingly contested by sector-specific Directorates-General and civil operators who claim that civil security is a specific and more complex domain that is defined in opposition to the defence sector. These discussions raise the question of how civil markets are performed in different discursive practices, including expert documents, competitiveness studies and security exhibitions.

Interoperability and visuality

Cooper (2008: 98) writes that, in the wake of 9/11, ‘permanent warfare has become the new driving force behind US economic growth, feeding off its own ineptitude as it generates a seemingly inexhaustible demand for security services of all kinds’. Rather than a demand for security services ‘of all kinds’, field research suggests the rise of a particular type of civil security equipment in Europe that is nevertheless embedded in longer histories of security and emergence. Drawing on observations at security trade shows and stakeholder workshops, the objective of this section is to explore the conceptual exchanges that have taken place between the military domain and civil security. I suggest that dominant civil aspirations of distributing threat information, fusing data and visualizing incidents have their roots in military logics and concepts earlier formulated in the context of the RMA in the USA.

The growing number of security trade fairs and exhibitions that are organized in and outside Europe are interesting sites for studying the trends and themes in civil security. More conceptually, these are also locations where we can analyse the co-constitutions and enactments of civil security and the market. The organization of security trade events is not a new phenomenon (Guittet and Jeandesboz, 2010), but today’s exhibitions indicate that a shift has taken place from a focus on traditional private security equipment (e.g. access protection, CCTV applications, etc.) to civil security technology. For instance, the organizers of the German Security Essen exhibition claim that it is the international meeting place ‘for solutions relating to everything to do with civil security’, focusing on technology for the civil domain, including the security of public spaces, transport security and ‘systems solutions’. 5 The Counter Terrorism Expo in London, in turn, writes on its website that this is the world’s largest event concentrating on ‘current modern day risks’ in new fields of concern such as international terrorism and intelligence, but also cyber-security, critical national infrastructure protection, and maritime security and anti-piracy. 6 At the same time, the trade fairs that I have visited continue to cater to the average police officer, fireman or security guard, exhibiting locks, protective clothing, bollards, fences, nets, guns and video cameras – whether presented in more ‘digitized’ or sophisticated forms or not. In other words, we find that there are no complete rewritings of the ‘old’ with the ‘new’ technology (see also De Goede et al., this issue). Rather, they converge and coevolve, indicating that the civil market indeed emerges in multiple and sometimes contradictory ways.

Still, observations at these security trade shows pinpoint a number of civil themes and technologies. In particular, these concern equipment at the intersection of the civil and defence domains that have their origins in defence but correspond to what are claimed to be new and ‘high-level’ vulnerabilities in civil security (Ecorys Research and Consulting, 2009: 18). Many of these, in addition, relate to a growing concern for bioterrorist attacks (see Cooper, 2008; Elbe et al., this issue). CBRNE (chemical, biological, radiological, nuclear and explosives) detection equipment developed for civil targets such as airports and harbours, mail distribution centres and mass (sports) events provides one example of dual-use technologies often shown at security exhibitions. Other technologies that emerge as civil applications of defence technology are different kinds of sensors and scanners used for crisis management (e.g. ‘microfluidic’ scanners and ‘smart dust’ scanners) and border and infrastructure protection (e.g. acoustic and thermal sensors and lasers) (Commission of the European Communities, 2004: 18–19).

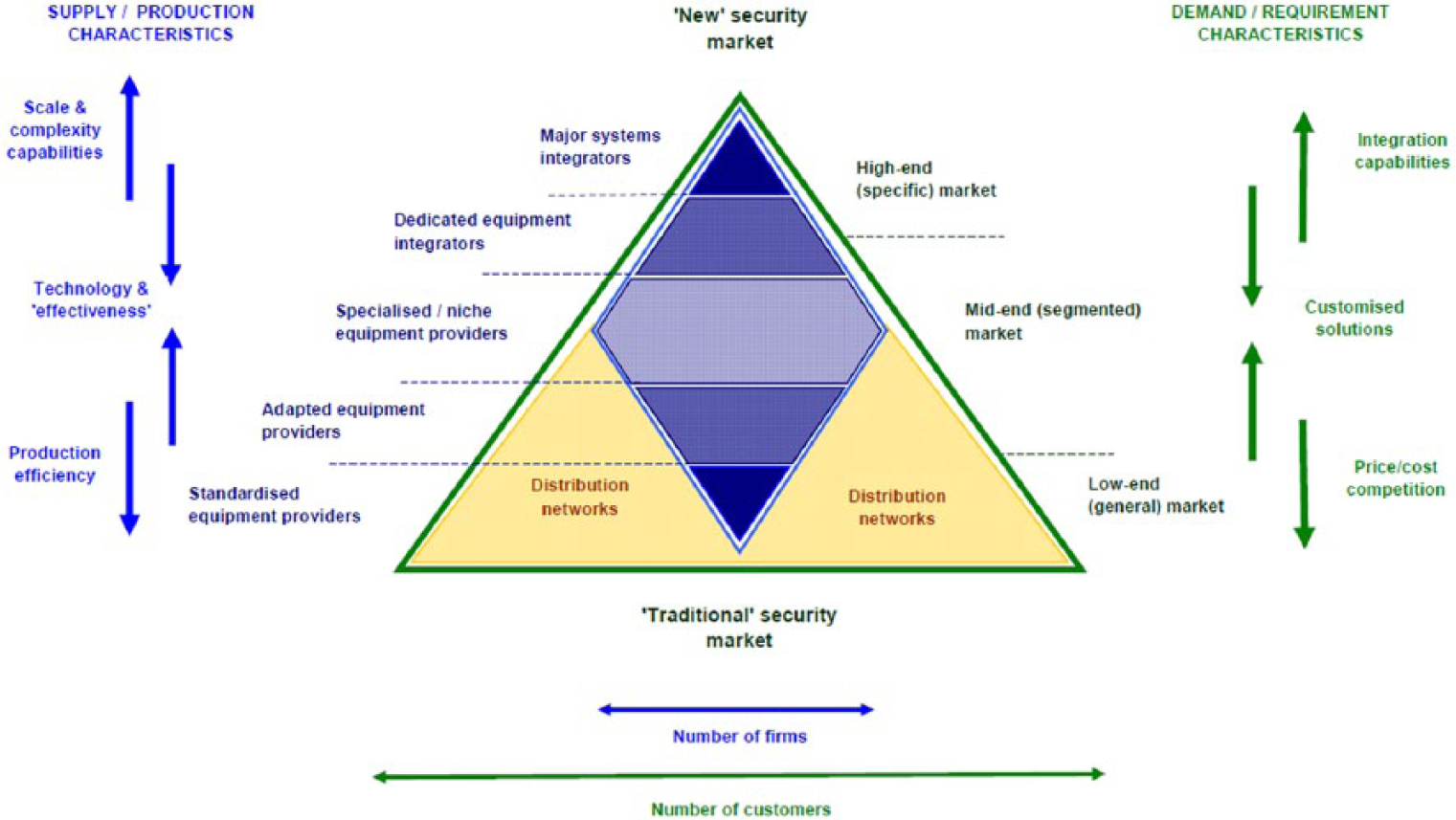

More specifically, what is emerging as a key feature of the civil security market is the integration or interoperability of dual-use technologies and sensors. 7 Examples of such ‘integrated systems solutions’ shown at security exhibitions involve software tools for the integration of data from physical security devices (access control, video, sensors, etc.), enabling the ‘tracking of suspects as they move on live and recorded video’, 8 or security management systems for asset, critical infrastructure and perimeter protection (involving video surveillance, fence protection and different forms of (leak) detection systems). 9 The focus on integrated security systems in civil security markets is echoed in Figure 2, which featured in the Ecorys study on the EU security market. The image provides an overview of the type of equipment produced by the European security market, depicting the market as a pyramid, with the ‘traditional’ private security market at the base providing primarily ‘low-end’ standardized equipment. Higher up, we find the more specialized suppliers – first, at the ‘mid-end market’, the niche equipment providers, typically comprising the small and medium enterprises (SMEs). At the top of the pyramid, we see the emerging new security market, characterized by a smaller number of companies, the ‘major systems integrators’, and a much smaller number of potential customers. Drawing on a certain economy of scale, these companies at the ‘high-end market’ respond to a demand for ‘integration capabilities’ and the customization of security systems.

Characterization of security equipment supply and demand.

The focus on systems integration and the notion of interoperability resonates with what appears as a key theme in EU documents and policy and research initiatives in this field. The Group of Personalities writes that policy and research efforts in the security domain should embrace interoperability and connectivity ‘as key functions for security management in a distributed environment’, and that common standards and protocols for ‘systems-of-systems’ should be defined at an early stage in order to ‘enhance IT security and interoperability between systems and users communities’ (Commission of the European Communities, 2004: 21). More concretely, two large-scale security research projects (SECUR-ED and PERSEUS) that the European Commission funds as part of the Seventh Framework Programme have as their primary objective the development of hardware and software tools that can be ‘packaged with interoperable interfaces’ and integrated in, respectively, the mass transport sector and border control (Eurotransport, 2012). In a similar manner, the EUROSUR border surveillance system that the European border agency Frontex has established puts forward a systems-of-systems approach, envisioning shared ‘situational pictures’ for all member-states, consisting of information collected from local information systems. 10

So, how can we explain the prevalence of interoperability in civil security? First, interoperability and related notions of shared awareness and systems integration have their roots in military responses to the emergence of new command-and-control systems and the growing role of information in the conduct of war more generally. They can be traced back to the military strategic doctrine of network-centric warfare presented by Arthur Cebrowski and John Garstka (1998) in a pioneering article published in the Proceedings of the U.S. Naval Institute in 1998, and further elaborated in three other semi-official publications between 1999 and 2003 (Alberts and Hayes, 2003; Alberts et al., 1999, 2001). The literature on network-centric warfare suggested that the compression of time and space caused by the shift to networked business could also affect the conduct of warfare. These changes were considered necessary in the light of what was claimed to have become an increasingly complex and obscure battlefield after the Cold War. Cebrowski and Garstka pointed out that, to reduce the emerging fog of war, military formations had to operate in networks, sharing information and battlefield awareness with all network participants. Interoperability, in this context, emerged as a key concept in order to ensure ‘information superiority’, and to allow military commanders to make decisions faster, more efficiently and more accurately (Mitchell, 2009: 34). It was presented as both a technological and an organizational imperative. In relation to the latter, interoperability entailed distributing information and making sure that the right content of information was shared with the responsible network actor. In terms of technology, it referred to the capacity to make disparate systems work together and have them exchange capabilities, or to notions of ‘joining up’ data and data systems (Amoore, 2011; Ruppert, 2012).

Similarly to how network-centric warfare would enable military commanders to more efficiently organize military force on an increasingly complex battlefield, the same network-enabled capabilities are now said to contribute to a better understanding of the purportedly non-linear threat environment that operators across civil domains deal with. Interoperability, so the argument goes, offers civil operators the capacity of accessing, revealing and intervening in information patterns that were previously unidentified. At security trade shows, interoperability refers to the physical integration of technological capabilities, such as when X-ray scanning and biometrics are combined to provide ‘identification solutions’, or to integrated management systems that exchange data and facilitate ‘real-time’ decisionmaking. The latter ambition, in particular, has given rise to a great number of new products in civil security that draw on military aspirations of distributing threat information, fusing data and sharing awareness. In fact, many of these technologies are about qualifying or visualizing incidents and potential threats. For instance, Thales’ award-winning integration system called the Hypervisor promises operators the capacity to visualize and manage real-time events and incidents. Shown at the 2013 Millipol exhibition in Paris, the Hypervisor claims to offer a broad comprehensive picture of the environment, combined with an easy-to-use but advanced ‘decision support tool’ that enhances efficient event management. 11 According to Thales, the Hypervisor is designed for complex environments and particularly appropriate for managing critical infrastructure (airports, energy and utilities, defence sites), transportation systems and cities.

Second, the prevalence of interoperability and integration capabilities in civil security is driven by emerging interests and the prospect of economic growth. Whereas the expectation of revenue generates investment in the civil security market as a whole, there is a strongly held belief in the opportunities associated with the development of integration capabilities in particular. These are said to depend on a growing demand for integrated solutions combined with a trend toward larger-size contracts, and on the position of the European security industry as one of the global experts at the ‘high end’ of this market. In particular, the importance of interoperability has been articulated by the ‘major systems integrators’ that are shown at the top of the pyramid of Figure 2. These are, in fact, the same companies that have close ties to the traditional defence industry and that have earlier participated in many of the EU’s research and policy initiatives. What an analysis of brochures demonstrates is that companies such as Thales or the Spanish Indra Sistemas are no longer focused on the development of the perfect single technology; rather, their work is based on connecting separate technologies to an overarching system. These companies are not so much concerned with the provision of security equipment per se, but with the integration of security technology into a ‘complete toolkit’ (Ecorys Research and Consulting, 2009: 18). 12 They have become interested in placing interoperability on the agenda because they are, as they themselves claim, in the best position to do large-scale integration work. On the one hand, these companies draw on their experience developing large-scale systems for military environments and on their self-proclaimed capability to integrate these systems across the civil domain. On the other hand, they assert that only they have the right size or economies of scale required by this type of integration work.

The emergence of interoperability as a key concept in civil security indicates that further analysis of the effects of and the logics underlying the call for the ‘seamless’ integration of technological and information systems is needed. Accordingly, this involves taking seriously the political dimension of technology and distancing ourselves from an understanding of technology as ‘a fix and a solution’ (Guittet and Jeandesboz, 2010: 235; see also De Hert and Gutwirth, 2006). It means that we should be attentive to how the idealized renderings of technology, such as the notion that interoperable technologies can distribute and join information while conforming with data-protection standards, fail to perform. Even more so, there is a need to highlight the ways in which new and older forms of technology may be contested, overruled, reworked or simply not bought. Throughout this article, I have pinpointed these and other moments of dissent – including how civil operators and sector-specific Directorates-General have challenged efforts to cast civil security as a politically neutral product by focusing on market development, or how civil actors have claimed that civil security is a specific and complex domain that is defined in opposition to the defence market. In so doing, I have put forward an analysis of security markets as situated in between an understanding of markets as uncontrollable, on the one hand, and seamless and interest-driven, on the other.

Conclusions

This article has analysed the rationalities underlying the emergence of civil security as a growth market in Europe. Situating civil security in ongoing academic analysis of economies of emergence, the article has contributed to these discussions in two ways. First, it has shown how notions of emergence offer a fruitful way to explore security-market growth beyond the context that Cooper and Marazzi describe. That is, the analytical lens of the economy of emergence is not limited to the US bioterrorist agenda and military strategic discourse under Bush, but can be expanded to Europe and to the civil domain. Second, the article has explained recent empirical developments in the European security field in close relation to notions of potential emergencies and broader discussions about threat preemption and anticipation. In so doing, it has pointed out that what emerges as civil security and technology draws on military discourses, strategies and technologies that can themselves be traced back to the emergence of new information-based technologies in the second half of the 20th century.

The notion that civil security is emerging as a priority in EU policymaking raises a number of important political questions. Under the headings of civil security research, close relationships between the Commission and industry representatives are being forged, rendering lobby organizations such as the European Organization for Security (EOS) increasingly influential players in the field of European security. Together, these actors have come to invest large amounts of resources in civil security, but without broader questions about the purpose and desirability of the civil market being asked. As Lucia Zedner (2006: 282) has put it, instead of evaluating ‘what security is for, for whom it must be secured and by what means, the emphasis is upon ensuring the health and profitability of the industry’. As the Commission is in the preparatory phase of the Horizon 2020 research programme, which, it is expected, will intensify investment in civil security, further critical analysis is needed to examine the precise scope and effects of the innovations and commercializations that are set in motion by the emergence of civil security markets.

Footnotes

Acknowledgements

The author would like to thank Louise Amoore, Otto Holman, Julien Jeandesboz, Gavin Sullivan, Rens van Munster, and three anonymous reviewers for very helpful comments on previous versions of this article. Special thanks to Marieke de Goede and Stephanie Simon for their support and guidance.

Funding

This work was supported by the Dutch Council for Scientific Research (NWO), through the VIDI-grant European Security Culture (grant number 452-09-016).