Abstract

This article examines the impact of the 2008–2009 economic crisis on the automotive industry. The uneven nature of the crisis contributed to the gradual shift in production from traditional core areas of the global automobile industry to selected less developed economies. In this context, the paper analyses the firm-level effects of the economic crisis in the Czech and Slovak automotive industries as two examples of automotive industry peripheries that were integrated in the European automobile production system and experienced rapid production increases after 1990. The analysis draws on unique data collected during a survey of 274 Czech-based and 133 Slovak-based automotive firms conducted in autumn 2009 and spring 2010, 98 company interviews conducted with automotive firms in Czechia in 2010 and 2011, and 30 interviews conducted in Slovakia in 2011. Changes in revenues, production and employment during the economic crisis are compared between Czechia and Slovakia, and are analysed according to ownership, the involvement of firms in the automotive value chain and firm size. The article also investigates plant closures and relocations in the Czech and Slovak automotive industries during the economic crisis.

Introduction

The 2008–2009 economic crisis has been considered to be one of the most severe in modern history (Cattaneo et al., 2010). Various explanations, ranging from institutional and cultural to neoclassical and Marxist, have been presented, and geographers have emphasized the importance of spatial perspectives in a full understanding of the crisis (e.g. Gowan, 2009; Harvey, 2011; Martin, 2011; Smith and Swain, 2010). In the automotive industry, the impact of the crisis was more severe than in other economic sectors with the exception of housing and finance, and only the banking sector saw larger government intervention (Van Biesebroeck and Sturgeon, 2010). Global vehicle production declined 3.7% in 2008 and 15.8% in 2009 (OICA, 2012). Albeit unevenly, all segments of global vehicle production were affected by the crisis. This decline is hardly surprising given the automotive industry’s sensitivity to business cycles. However, differences existed in the automotive output of different world regions. Since saturated vehicle markets of developed economies are typified by replacement demand, consumers tend to postpone purchases of new vehicles during periods of economic uncertainty (Dicken, 2011). During the 2008–2009 crisis, the situation was exacerbated by worsening access to consumer credit, which has traditionally financed a high share of new vehicle purchases, especially in the United States. Consequently, saturated markets, including those in North America and Western Europe, have been hit the hardest by the crisis, despite government efforts to encourage consumer demand for new vehicles (Klier and Rubenstein, 2010; Stanford, 2010). The situation has been different in rapidly growing developing economies because of their steadily expanding new demand for vehicles. Although large developing countries, including China, India and Brazil, saw lower demand for new cars in 2008 and 2009 than 2007, their new vehicle sales continued to grow during the crisis (Van Biesebroeck and Sturgeon, 2010; Cruz and Rolim, 2010; OICA, 2012).

Van Biesebroeck and Sturgeon (2010) argued that the crisis led to further consolidation of the supplier base as surviving smaller, local suppliers were more vulnerable to closure and bankruptcy than large ‘global’ suppliers. So far, however, studies concerning the impact of the crisis in the supplier sector have been rare because reliable data about numerous automotive suppliers are difficult to collect. Therefore, the goal of this paper is to analyse the crisis in the supplier sector at firm level and to evaluate to what extent the consolidation of the automotive supplier sector took place during the economic crisis. The case study focuses on Czechia and Slovakia, which together produced more than 1.8 million vehicles in 2011. In Europe, only Germany, France, Spain and Russia assembled more vehicles in that year. The case study draws on unique data collected by the author in a survey of 274 Czech-based and 133 Slovak-based automotive firms in autumn 2009 and spring 2010, and on 98 company interviews conducted with automotive firms in Czechia in 2010 and 2011 and 30 interviews conducted in Slovakia in 2011. 1 The data suggest that the effects of the economic crisis in the Czech and Slovak supplier sectors were significant, although not as dramatic as originally thought. The economic crisis resulted in relatively few bankruptcies, plant closures and relocations among automotive suppliers in both Czechia and Slovakia. The firm-level analysis did not uncover any substantial differences between the effects of the economic crisis in the Czech and Slovak automotive industries.

This article begins with a brief discussion of the role of global production networks (GPNs) during the economic crisis. The second section reviews the 2008 and 2009 crisis in the global automotive industry, stressing its uneven geographic nature. The third section introduces the Czech and Slovak automotive industries as being part of a relatively new and rapidly growing periphery that was integrated into the European automotive production system in the 1990s and 2000s. The fourth section discusses production and employment trends in the Czech and Slovak automotive industries during the economic crisis. The fifth section analyses firm-level data concerning revenues, production and employment change in the Czech and Slovak automotive industries during the 2008–2009 economic crisis. The sixth section investigates bankruptcies and relocations in the automotive industries of Czechia and Slovakia during the crisis. The main findings of the analysis are summarized in the conclusion.

Global production networks and the economic crisis

Geographers, amongst others, have applied their spatial perspective to better understand the uneven nature of the 2008–2009 economic crisis at various geographic scales (e.g. Martin, 2011; Smith and Swain, 2010). The ‘varieties of capitalism’ literature has also emphasized the variegated impacts of the economic crisis across east-central Europe (ECE), which was influenced by different modes of growth and economic integration in the 1990s and 2000s (e.g. Bohle, 2009; Drahokoupil and Myant, 2010). 2 However, this literature largely limits its interest to national scale differences in various factors underlying the geographically uneven national economic performance during the different stages of the economic crisis. Myant and Drahokoupil (2012) present a more sophisticated approach to explain the vulnerability of individual countries to the economic crisis in ECE by considering different modes of integration of ECE countries into the global economy, and by emphasizing international integration through financial inflows and exports as the two most important channels transmitting the crisis into ECE. This approach still suffers from a national-scale bias typical of the ‘varieties of capitalism’ literature (e.g. Bohle and Greskovits, 2007; Farkas, 2011), which limits our understanding of processes that are primarily organized at different geographic scales (e.g. Dicken, 2011). However, it suggests that GPNs organized from outside the region constituted one of the principal transmission channels through which the crisis was transmitted into ECE economies. In other words, the incorporation of ECE producers in the externally organized GPNs increased the vulnerability of ECE to the economic crisis. This argument echoes the work of GPN and global value chain (GVC) scholars who have maintained that transnationally organized GPNs and GVCs were the principal mechanisms through which the economic crisis was transmitted around the world economy (Cattaneo et al., 2010; Smith and Swain, 2010). One of the advantages of the GPN and GVC approaches is their focus on internationally organized production networks and value chains instead of national economies, which makes it possible to analyse the economic crisis at the industry and firm levels (e.g. Cattaneo et al., 2010). This, in turn, allows for a more nuanced analysis of the uneven impacts of the economic crisis within particular industrial sectors, which might take into consideration differences between groups of firms within the same sector, depending, for example, on their position within the production network or value chain, their different ownership or their different size (e.g. Pavlínek and Ženka, 2010). Such an analysis then allows for a better understanding of the resilience of particular types of firms to economic crises and their abilities to upgrade their position within GPNs and GVCs. At the same time, it also allows for the identification of the types of firms that are particularly vulnerable to systemic crises because of their limited opportunities to upgrade within the existing GPNs. Consequently, such firms might be more susceptible to downgrading, relocation or closure.

Since there are important differences in the way GPNs are organized in different industries (Gereffi et al., 2005), there are important differences also in the resilience and vulnerability of different industrial sectors to economic crises and in the ways in which the economic crisis has been transmitted through GPNs in these sectors (Cattaneo et al., 2010). We also need to consider national differences in institutional environment, which influence how a particular industrial sector is integrated into the global economy through GPNs.

The uneven nature of the 2008–2009 economic crisis as a symptom of the broader geographic shift in global automotive production

The global automotive industry is geographically organized in regional clusters of production networks nested in macro-regions (e.g. North America, South America and the European Union) or individual countries with large domestic markets (e.g. China, India) (Sturgeon et al., 2008, 2009). These regional clusters of production reflect the need for geographical proximity of the most important suppliers to assembly operations and the need of automotive lead firms to design and produce vehicles customized to consumer preferences in particular markets. They also reflect political pressures for local production and the need for automotive lead firms to meet various regulatory requirements that differ in contrasting parts of the world (Sturgeon et al., 2008). This strongly regional geographic structure of the global automotive industry (Carrillo et al., 2004; Humphrey et al., 2000) contributed to large differences in regional performance during the crisis as its effects have mostly been contained within the most important production regions and their respective countries (Van Biesebroeck and Sturgeon, 2010).

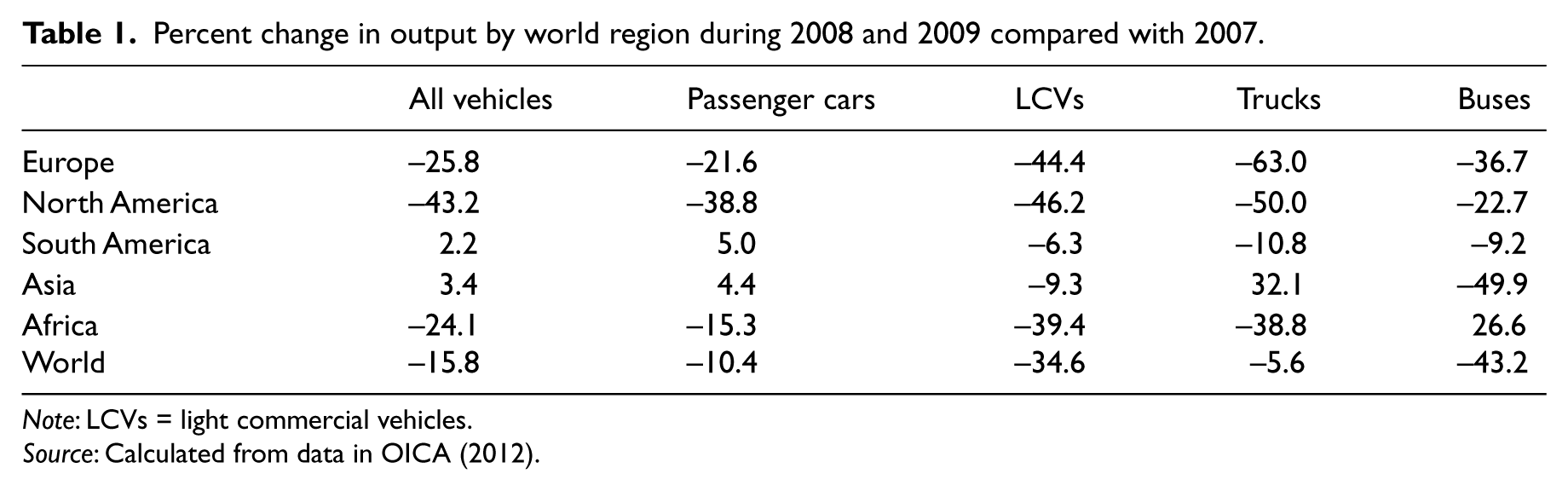

At one extreme, North America, 3 which already experienced a decline in total vehicle production in 2006 and 2007, suffered a 16% drop in 2008 followed by an additional 32% decrease in 2009, representing the steepest production decline since the Great Depression and the deepest production decline of all world regions. Conversely, in 2010, North America experienced the strongest recovery, with a 38.7% increase in vehicle production from 2009. At another extreme, Asia’s vehicle production kept growing by 1.9% and 1.5% during 2008 and 2009. Sustained production in Asia during the economic crisis was mainly due to China, whose vehicle production increased by 7% in 2008 and by 45% in 2009 (OICA, 2012). North America experienced 4 years of negative annual growth and Europe experienced 3 between 2005 and 2010, compared with only 1 in South America and zero in Asia during the same period. 4 Production trends were also regionally uneven according to the individual segments of the automotive industry. During 2008–2009, global production declined across all vehicle segments (Table 1; OICA, 2012). European and North American automotive production declined across the board. In South America, only passenger car production did not decline, but the decline in the rest of automotive assembly was much smaller than in Europe and North America. In Asia, the decline was limited to light commercial vehicles (LCVs) and buses. A 50% decline in the assembly of buses in Asia was the largest of all world regions. At the same time, Asia’s truck production increased by one-third. The extent of production decline in the individual segments of the automotive industry was strongly affected by the nature and extent of government intervention during the economic crisis (Stanford, 2010; Van Biesebroeck and Sturgeon, 2010).

Percent change in output by world region during 2008 and 2009 compared with 2007.

Note: LCVs = light commercial vehicles.

Source: Calculated from data in OICA (2012).

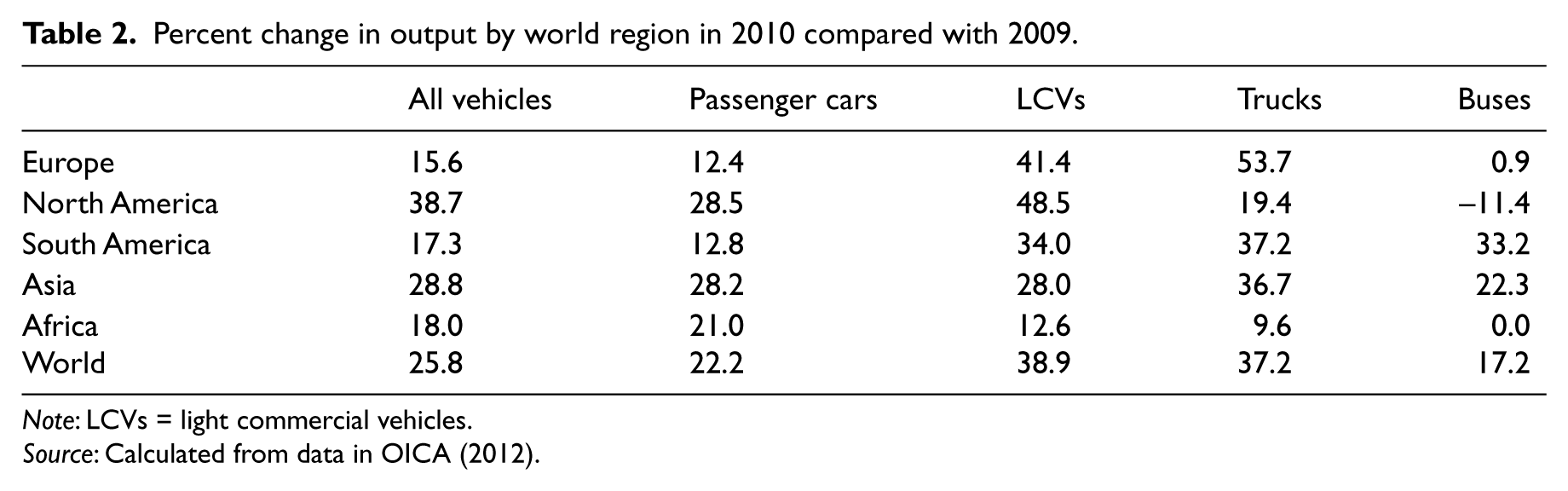

The 2010 recovery was surprisingly strong, considering the lingering effects of the economic crisis especially in Europe and North America, although there were significant sectoral differences in the strength of output recovery (Table 2). Global vehicle production exceeded the 2007 pre-crisis level by 5.9% in 2010. The output of passenger cars and heavy trucks was higher in 2010 than in 2007, while the output of LCVs and buses was lower (OICA, 2012). The growth in output continued in 2011. 5

Percent change in output by world region in 2010 compared with 2009.

Note: LCVs = light commercial vehicles.

Source: Calculated from data in OICA (2012).

The diverging production trends between more developed and less developed countries have been symptomatic of a general shift in output in favour of non-core areas of global automotive production caused by rapid production increases in less developed countries since the 1990s. The share of global vehicle production decreased in traditional automotive core countries from 66% to 36% between 1997 and 2010, while it increased outside the core from 34% in 1997 to 64% in 2010 (OICA, 2012). 6 Two types of less developed economies have particularly benefited from this shift. First are rapidly growing less developed countries that have (potentially) large domestic markets and might further benefit from regional economic integration. Examples of such ‘protected autonomous markets’ include China, India and Brazil (Cruz and Rolim, 2010; Humphrey and Oeter, 2000; Lung, 2000; Van Biesebroeck and Sturgeon, 2010). Second are peripheral areas located close to large markets of developed regions that were integrated into production networks of traditional core areas of the automotive industry. Examples of such ‘integrated peripheral markets’ include Mexico, Spain and ECE (Humphrey and Oeter, 2000; Layan, 2000; Pavlínek, 2002a; Pavlínek et al., 2009; Sturgeon et al., 2010).

ECE’s position in the European automotive production system

Since the early 1990s, the European automotive industry has been increasingly organized in trans-European rather than national production networks (Hudson and Schamp, 1995). ECE represents an example of a peripheral region of the automotive industry that has been integrated into the European and global automotive GPNs through large inflows of foreign direct investment (FDI) in the 1990s and 2000s (Pavlínek, 2002a, 2002b; Pavlínek et al., 2009). This peripheral integration has been organized and financed by foreign automotive lead firms through their profit-seeking strategies to enhance their overall competitiveness by exploiting the spatial division of labour in the European automotive industry. As a result, the ECE automotive industry is now owned and controlled by core-based transnational corporations (TNCs). In order to maximize the advantage of ECE’s cheaper and less organized labour, the role of the ECE automotive industry in the European production system has been three-fold: mass production of small passenger cars, labour-intensive low-volume production of luxury cars, and experimentation with new production methods and flexible labour practices (Havas, 2000; Pavlínek, 2002a). The post-1990 development of the automotive industry in ECE has been strongly supported by favourable government policies based upon generous investment incentives to attract foreign assembly plants and foreign component suppliers. Central European countries have engaged in competitive bidding for automotive assembly plants and investments by large foreign suppliers (Pavlínek, 2008).

Following the large investment by foreign assemblers and component suppliers, ECE’s passenger car output increased by five times between 1991 and 2011, from 608,000 to 3.3 million units (3.4 million units of all vehicles). In 2011, ECE accounted for 19% of the total EU vehicle production and 21% of the EU passenger car output (OICA, 2012). At the same time, however, the development of more value-added and higher-order functions, such as research and development competencies, has been limited in the ECE automotive industry. The opportunities for industrial upgrading have been mainly confined to process and, to a lesser degree, product upgrading, while functional upgrading has been much more limited (Pavlínek, 2012; Pavlínek and Ženka, 2011). This situation is not surprising given the captive (or quasi-hierarchical) nature of automotive value chains, in which power is concentrated in powerful lead firms. Lead firms use their power, among other things, to organize and govern hierarchical networks of component suppliers, and to control their chances of functional upgrading (Gerefi et al., 2005; Humphrey and Schmitz, 2002, 2004). This transnational organization of automotive production networks has, at least theoretically, made ECE automotive operations, and regional and local economies specialized in the automotive industry, more vulnerable to economic crises, as simpler and lower value-added production tends to be more susceptible to closure and/or relocation during economic downturns. The externally organized GPNs constituted the main transmission channels through which the crisis was transmitted into the ECE automotive industry. In the rest of this article, the analysis of the 2008–2009 crisis in the Czech and Slovak automotive industries will be presented.

The Czech and Slovak automotive industries

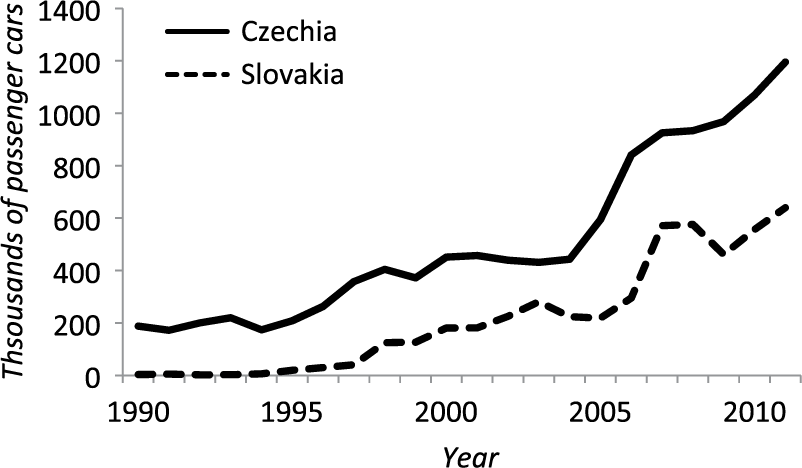

In Czechia and Slovakia, the 2008–2009 economic crisis interrupted 15 years of rapid FDI-driven development of the automotive industry, which followed the trade and FDI liberalization of the early 1990s. The prospects of low-cost production, based upon the combination of low wages, geographic proximity to the west European market and strong governmental investment incentives, attracted large inflows of automotive FDI (e.g. Jakubiak et al., 2008; Pavlínek 2002a, 2008; Pavlínek et al., 2009). Czechia and Slovakia now rank among the most important automobile producers within ECE and the entire EU, and their combined production of 1.8 million passenger cars in 2011 represented 56% of the ECE total and 12% of the EU total (OICA, 2012). Czech passenger car production increased more than six times from 188,000 cars in 1990 to more than 1.2 million in 2011, and Slovak output increased from 3,453 units in 1990 to 640,000 in 2011 (Figure 1). The production of automotive components increased even more rapidly than the assembly of cars as many foreign TNCs set up their export-oriented operations in Czechia and Slovakia to supply both locally based assembly plants and assembly plants located in western and central Europe (e.g. Pavlínek and Janák, 2007; Pavlínek and Ženka, 2011).

Passenger car production in Czechia and Slovakia, 1990–2011.

Different starting positions of the Czech and Slovak automotive industries in the early 1990s reflected differences in their previous development (e.g. Pavlínek, 2008; Pavlínek and Smith, 1998; Vagac, 2000). In the 1990s, Volkswagen (VW) played the decisive role in the automotive industries of both countries through the acquisition and restructuring of the Czech assembler Škoda and the launch of new production in the former BAZ factory (the Bratislava automobile works) in Slovakia. VW also pressured existing suppliers to substantially improve the quality and timing of supplied components and encouraged ‘follow sourcing’ by its Western European, mostly German, suppliers. These corporate strategies led to the restructuring and further development of the Czech and Slovak supplier industries (e.g. Pavlínek, 2003, 2008). In the 2000s, Czechia and Slovakia attracted four additional greenfield passenger car assembly plants: the joint venture of Toyota, Peugeot and Citroën (TPCA) at Kolín (Czechia); Hyundai at Nošovice (Czechia); Kia at Žilina (Slovakia); and Peugeot at Trnava (Slovakia). In all four cases, the investments in assembly were followed by investments by foreign suppliers. As a result of this development, the automotive industry now represents the most important branch of industry in both Czechia and Slovakia, and its share of total manufacturing employment and output has been steadily increasing. In Czechia, the automotive industry had the highest share of revenues (19.4%) and exports of all manufacturing industry in 2009. The narrowly defined employment in the automotive industry increased from 58,000 in 1994 (NACE 34) to 146,000 in 2011 (NACE 29), accounting for 11.4% of total industrial employment in 2011 (CSO, 2011). 7 In Slovakia, employment increased from 6000 in 1993 (NACE 34) to 51,000 in 2010 (NACE 29) (SME, 2011). The automotive industry accounted for 27.5% of total industrial revenues (74% of total manufacturing revenues) and 15.9% of industrial employment (46% of total manufacturing employment) in Slovakia in 2010. Its share of total industrial production is projected to reach 40% by 2013 (SME, 2011). The more broadly defined automotive industry (NACE 29+30) employed 165,000 workers in Czechia and 60,000 workers in Slovakia in the middle of 2011 (CSO, 2011; SSO, 2011).

Although this rapid development of the automotive industry has been viewed as a success by both the Czech and Slovak governments and by industry analysts, it has significantly increased the dependence of the Czech and Slovak economies on the export-oriented automotive industry. In 2007, following Germany (11.7%) and Sweden (10.6%), Czechia had the third (8.8%) and Slovakia the fourth (8.0%) highest share of automotive employment (NACE 34) among total manufacturing employment in the European Union (Eurostat, 2011). The Czech share increased to 12.0% by 2011 (CSO, 2011) and the Slovak share increased to 15.9% by 2010 (SME, 2011). Of total manufacturing employment, both countries also had high shares of employment in automotive components manufacturing (NACE 29.3), with Czechia at 8.6% in 2009 (MIT, 2011) and Slovakia at 11.6% in 2010 (SME, 2011). It has been argued that a high degree of regional specialization increases regional economic instability (Baldwin and Brown, 2004; Ezcurra, 2011; Trendle, 2006). This is also the case with externally controlled economies, which are more vulnerable to disinvestment during economic crises (Dicken, 1976). Therefore, the dependence on externally controlled export-oriented automotive manufacturing tends to make the Czech and Slovak economies vulnerable to plant closures and large-scale layoffs in times of economic crises during which consumer demand for passenger cars may dramatically decrease. The rest of this article investigates to what extent these arguments are empirically supported by the firm-level effects of the 2008–2009 economic crisis in the Czech and Slovak automotive industries.

General effects of the economic crisis on the Czech and Slovak automotive industries

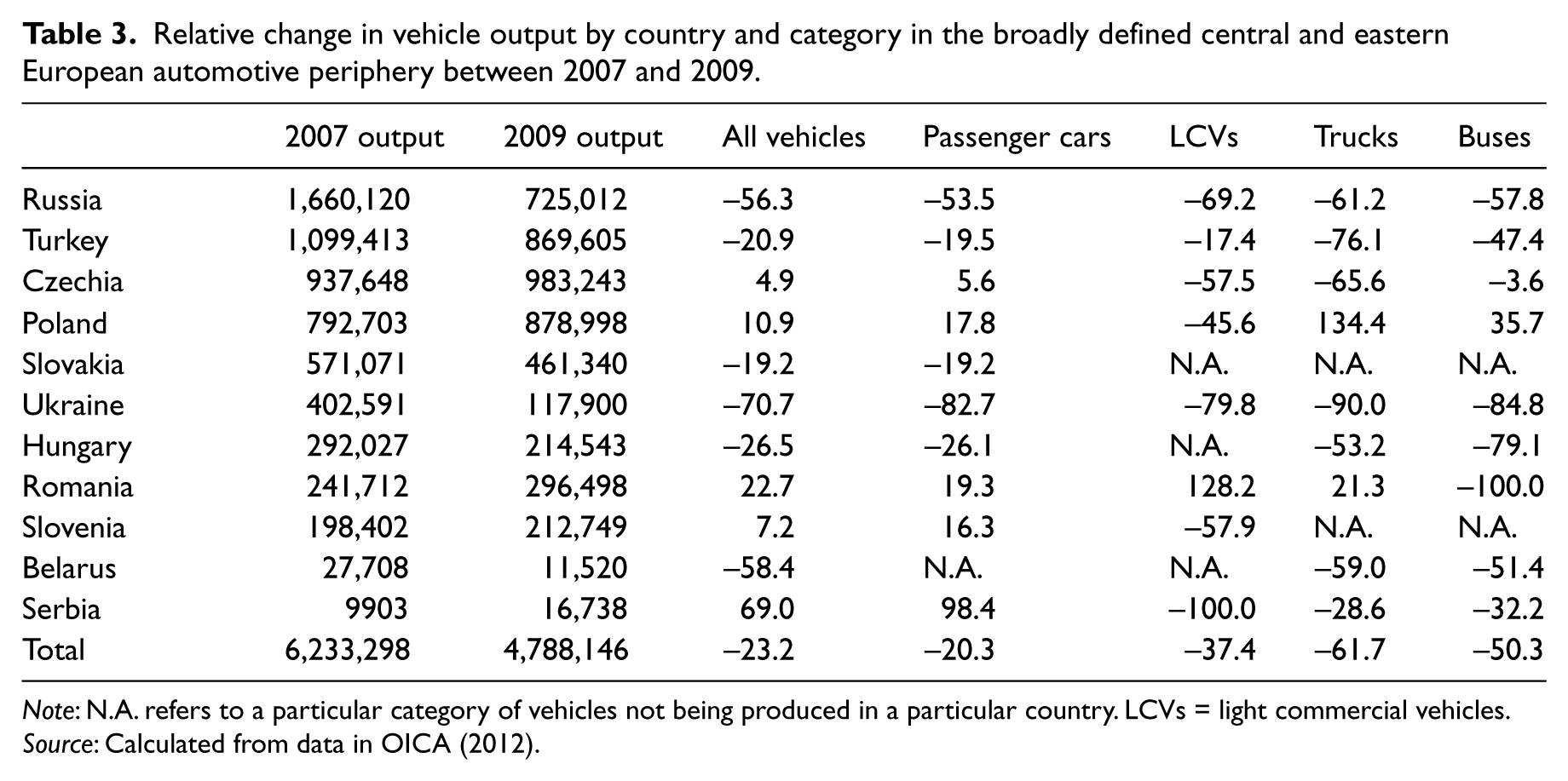

The effects of economic crises in peripheral regions of the automotive industry, such as ECE, depend on several factors. First is the degree of their dependence on exports to saturated markets, since these markets are most likely to be affected by significantly lower sales because they are dominated by replacement demand for vehicles. Integrated export-oriented peripheral markets, including Mexico and ECE, would thus tend to be more affected than more isolated ‘protected autonomous markets’ (e.g. China and India) (Humphrey and Oeter, 2000) serving domestic markets which are driven by new demand for vehicles. Second, product portfolio plays a role since different classes of vehicles are likely to experience different changes in consumer demand during economic crises. Third, the effects of economic crisis in peripheral locations also depend on the corporate policies of core-based lead firms. On the one hand, they might be more likely to downsize production in foreign locations rather than their home countries because of domestic political pressures. On the other hand, they might be compelled to shift more production to foreign peripheral locations in order to reduce production costs and thus increase their competitiveness. Fourth, the extent of government intervention, if any, in the automotive industry might influence the severity of the crisis. All of these factors affected the development of the automotive industry crisis in ECE. At the national level, different combinations of these factors and particular national circumstances resulted in a highly uneven automotive industry crisis across the broader East European automotive periphery, composed of ECE, the non-EU European countries of the former Soviet Union (Belarus, Moldova, Russia and Ukraine) and Turkey (Table 3).

Relative change in vehicle output by country and category in the broadly defined central and eastern European automotive periphery between 2007 and 2009.

Note: N.A. refers to a particular category of vehicles not being produced in a particular country. LCVs = light commercial vehicles.

Source: Calculated from data in OICA (2012).

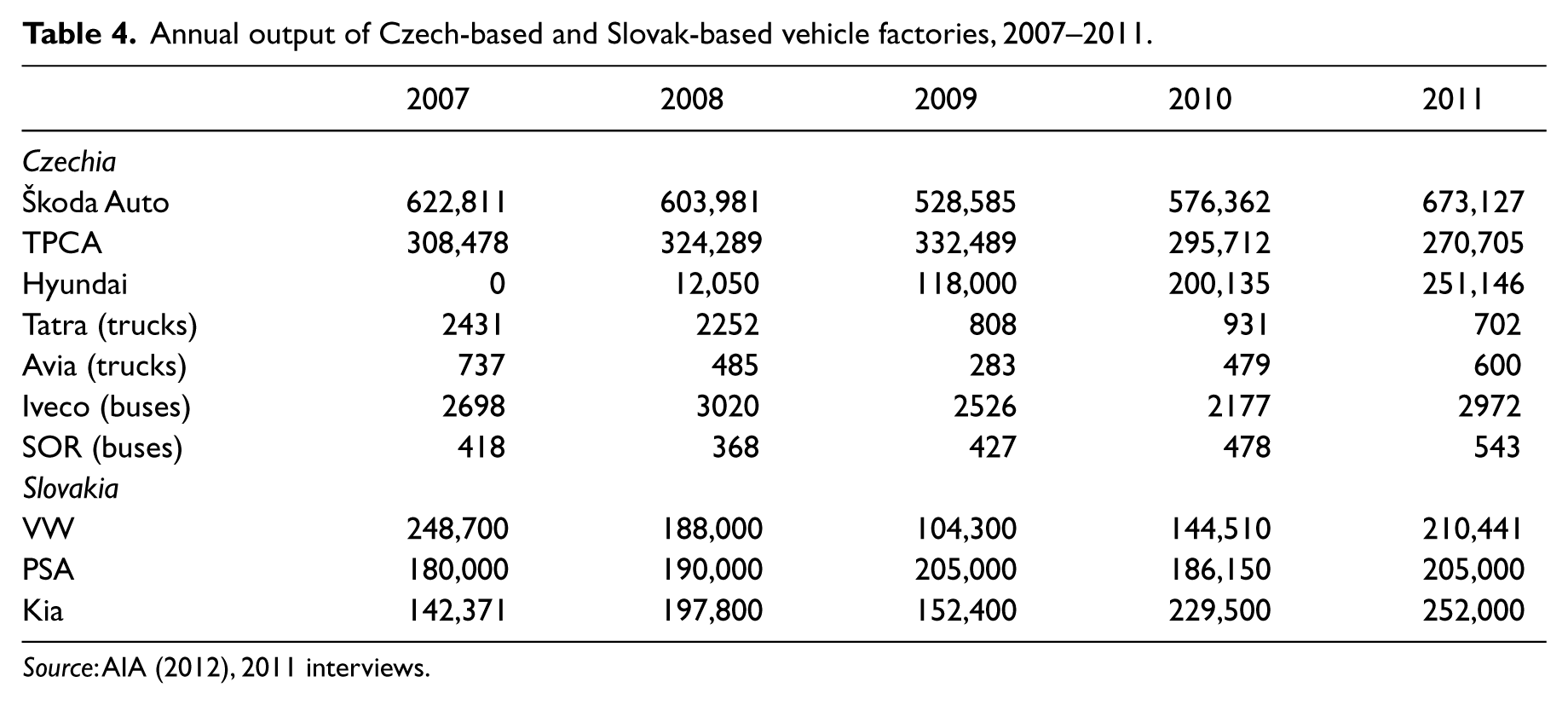

At first glance, data for passenger car production do not reveal any economic crisis in the Czech automotive industry in 2008 and 2009 because Czech vehicle output increased by 0.9% in 2008 and by 4.0% in 2009. The growth in output further accelerated in 2010 and 2011 with increases of 9.5% and 11.5%, respectively (AIA, 2012; OICA, 2012). Together with Romania, Poland, Slovenia and Serbia, Czechia was one of only five European countries that recorded production increase in the output of passenger cars during the 2008–2009 crisis. Its 2010 production was 15% higher than its 2007 output (Figure 1). However, this national-level measure of the impact of the economic crisis in the automotive industry is misleading for several reasons: it considers only passenger car assembly, ignoring the rest of the automotive industry, although passenger cars accounted for 99.4% of assembled vehicles in 2010; it reflects only domestic assembly, ignoring the changes in exports of components; and it is strongly affected by the fact that a newly opened Hyundai assembly plant in November 2008 was gradually increasing its output throughout 2009 and 2010. Firm-level data thus reveal a more complex picture, as there were important differences among the individual assemblers (Table 4). Another indicator of the extent of the automotive industry crisis in Czechia is the fact that during 2009 the three Czech-based passenger car producers assembled 383,000 fewer passenger cars than they had originally planned because production targets were not met by Škoda Auto and Hyundai (HN, 2008). These pre-crisis plans were still not realized in 2011. Table 4 also suggests much more serious effects of the crisis in the truck industry than in the passenger car industry. Tatra, the largest surviving Czech-based producer of heavy trucks, suffered a revenue decline of 45% and its production dropped by 64% in 2009. The company laid off half of its workers during the economic crisis, and its employment dropped from 4,400 in June 2008 to 2,280 at the end of 2009. Avia, the second (barely) surviving producer of medium-sized trucks stopped its assembly line for 7 weeks between December 2008 and January 2009, and it operated only for 3 or 4 days per week in the first half of 2009. The company also dismissed almost half of its workforce during the economic crisis. The trends in the production of buses differed from both passenger cars and trucks (Table 4).

Annual output of Czech-based and Slovak-based vehicle factories, 2007–2011.

Source: AIA (2012), 2011 interviews.

Based upon annual vehicle output, the Slovak automotive industry was hit harder by the crisis, especially in 2009, when total vehicle production decreased by 19.9%. Despite the 20.7% increase in 2010, the 2010 output was still 2.5% lower than in 2007. As in Czechia, different assemblers were affected differently by the crisis (Table 4). Slovakia does not produce any trucks and buses.

Job losses were significant. In Czechia, 28,000 jobs, representing 17.2% of the automotive industry (NACE 29) total, were lost between the first quarter of 2008 and the third quarter of 2009. In the second quarter of 2011, there were still 17,000 fewer jobs than before the crisis despite the 15% increase in the passenger car output (CSO, 2011). This suggests that the automotive firms rationalized production and became more efficient during the crisis. In Slovakia, employment in the broadly defined automobile industry (NACE 29 + 30) peaked in September 2008 at 61,078, and it reached the lowest point in June 2009 at 51,177, suggesting the loss of 9,901 jobs or 16.2% of the pre-crisis employment. 8 After June 2009, employment began to recover, but, with 59,768 workers as of July 2011, it still failed to reach pre-crisis levels (SSO, 2011).

The firm-level effects of the crisis in the Czech and Slovak automotive industries were affected by institutional factors and government policies. Many European governments introduced various programmes and incentives to support the automotive industry during the economic crisis in order to prevent plant closures and large-scale layoffs. These programs ranged from favourable loans, loan guarantees, wage subsidies and direct subsidies to various cash scrappage incentives (see, for example, Stanford, 2010). The Czech government, however, did not implement any such programme, and it only launched several active labour policy programmes, which supported job training and worker education (see Pavlínek and Ženka, 2010). Slovakia followed a different strategy by introducing the scrappage scheme for passenger cars. Consumers could receive up to a €1500 subsidy for the purchase of a new passenger car priced at less than €25,000. Some 44,200 old cars were scrapped, but, beyond environmental and safety improvements, the effect of this policy on the Slovak-based assemblers was negligible since the vast majority of new passenger cars replacing the old ones were not assembled in Slovakia. More importantly, both Slovak and Czech-based assemblers and component suppliers benefited from scrappage schemes introduced in their large markets, such as Germany, the United Kingdom, France and Italy, in 2009.

Firm-level effects of the 2008–2009 economic crisis in the Czech and Slovak automotive industries

In order to evaluate the effects of the 2008–2009 crisis in the Czech and Slovak automotive industries, a survey was administered in Czechia at the end of 2009 and in Slovakia at the beginning of 2010 to collect firm-level data about changes in revenues, production, employment and investment plans in 2009 (during the past 12 months). The survey targeted firms with 20 or more employees and involved 800 firms in Czechia and 299 in Slovakia. It yielded a response rate of 35% (274 firms) in Czechia and 44% (133 firms) in Slovakia. The survey results show significant firm-level effects of the 2008–2009 economic crisis in both countries. Especially in Czechia, the survey results generally do not correspond with the overall growing assembly of automobiles in 2008 and 2009.

Declines in revenues and production

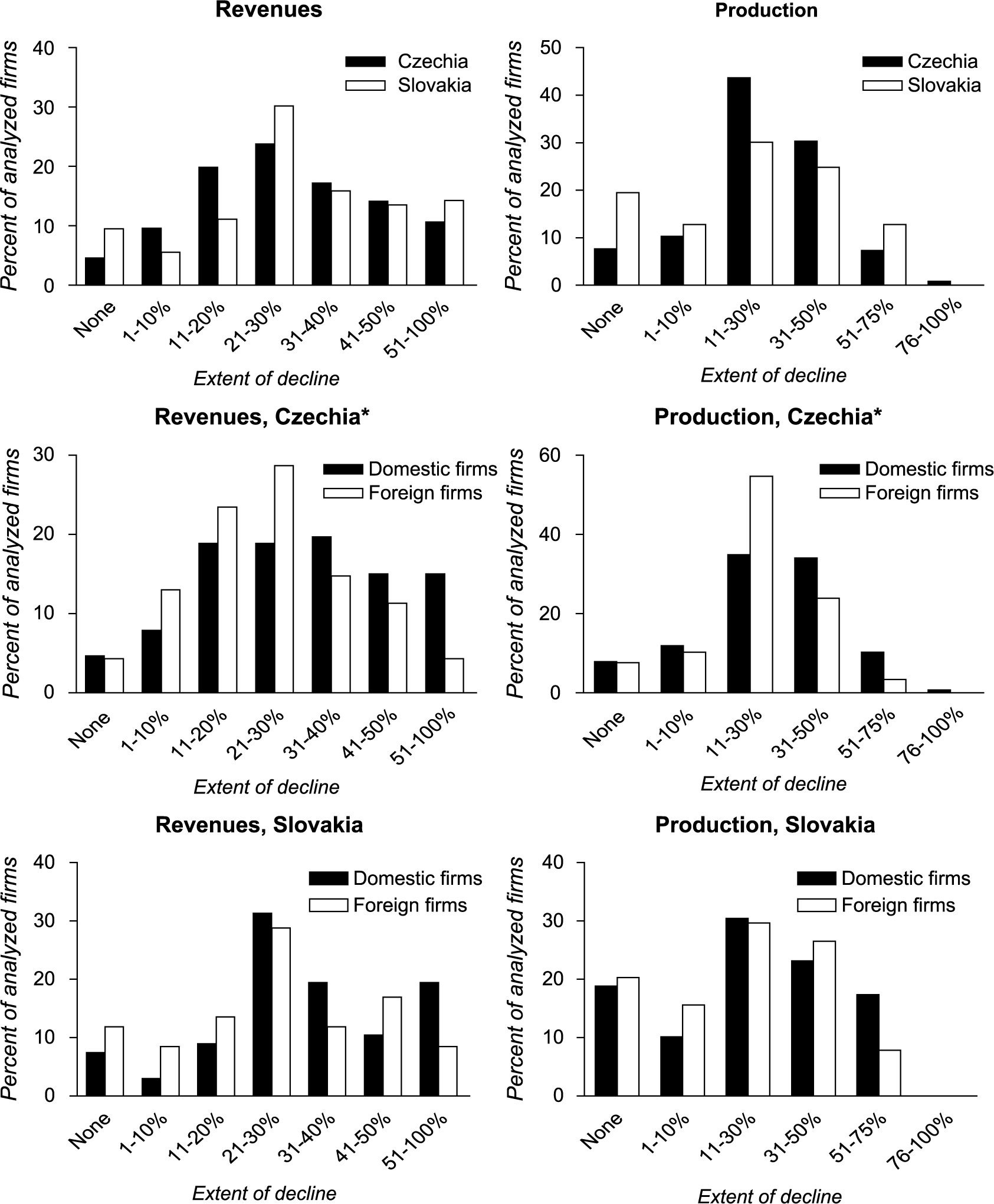

Overall, 95% of the surveyed firms reported a decline in revenues in Czechia and 91% in Slovakia. Production decline affected 92% of the surveyed firms in Czechia and 80% in Slovakia. However, overall differences in declines in revenues and production between Czech and Slovak firms as a whole are not statistically significant and suggest that the firm-level effects of economic crisis were similar in the Czech and Slovak automotive industries, despite slightly greater declines in Czechia (Figure 2). 9

Decline in revenues and production in Czech and Slovak automotive firms in the past 12 months during 2008 and 2009.

Differences in economic performance between foreign-owned and domestic-owned firms (henceforth foreign firms and domestic firms) during the economic crisis were statistically significant. 10 In Czechia, domestic firms experienced a statistically significant greater decline in revenues (t-test, p=0.005) and production (t-test, p=0.043) than foreign firms. In Slovakia, however, there were no statistically significant differences between foreign and domestic firms in declines in revenues and production during the economic crisis (Figure 2). I was also interested to see whether the extent of involvement of firms in the automotive industry affected the degree of decline during the economic crisis. Firms were compared according to the share of automotive production among their total revenues. All firms were grouped into five classes: 100%, 75–99%, 50–74%, 25–49% and 1–24% of automotive production. In Czechia, these groups of firms did not statistically differ in the extent of revenue and production decline. These results suggest that the automotive industry was not affected harder by the economic crisis than the rest of the manufacturing industry and that the effects of the crisis were universal across the Czech manufacturing industry. In Slovakia, the results differed from those in Czechia. The five groups of firms according to the extent of their involvement in the automotive industry statistically differed in the extent of decline in revenues and in production (one-way ANOVA nonparametric test, p=0.005 and p=0.003). Further analysis of the t-test revealed that firms with 75–99% of the automotive production suffered a greater production and revenue decline than firms fully dedicated to automotive production (p=0.001 and p=0.004) and firms with 1–24% of automotive production (p=0.001 and p=0.001). There was also a statistically significant greater decline in revenues in firms with 25–49% than in the firms with 1–24% of automotive production (p=0.019).

Finally, the extent of decline in small and medium-sized enterprises (SMEs) and large firms was analysed. In Czechia, 171 SMEs (250 employees and fewer) in the database were compared with 101 large automotive firms (more than 250 employees). The statistical difference in revenue decline between these two groups of firms was highly significant (t-test, p=0.0004). On average, SMEs experienced a greater decline in revenues than large enterprises. The statistical difference in production decline was not significant. However, 45% of SMEs suffered a greater than 30% decline in production compared with only 26% of large companies. In Slovakia, there were 31 large firms and 102 SMEs in the database. The differences in declines in revenues and production between large firms and SMEs were not statistically significant. However, 18% of SMEs suffered revenue declines of more than 50% compared with zero among larger firms, and declines of more than 30% were experienced by 50% of SMEs compared with only 22% of large firms. In terms of production, 41% of SMEs reported declines exceeding 30% compared with only 26% of large firms. This suggests a greater decline in revenues and production among SMEs than large firms in Slovakia. SME automotive suppliers are generally found in the lower tiers of the supplier hierarchy. Company interviews revealed that these suppliers were particularly squeezed during the economic crisis. For example, a director of a Czech-owned automotive supplier argued that: We were forced to lower our prices by 10–20% after the crisis. Our prices always keep on going down. What cost €10 ten years ago costs €4 now. However, the greatest decrease was in the past three years during the economic crisis when we got really squeezed by assemblers. More or less, we were included in global sourcing together with the Chinese and Indians and assemblers squeezed everything out of us that was left.

Employment effects

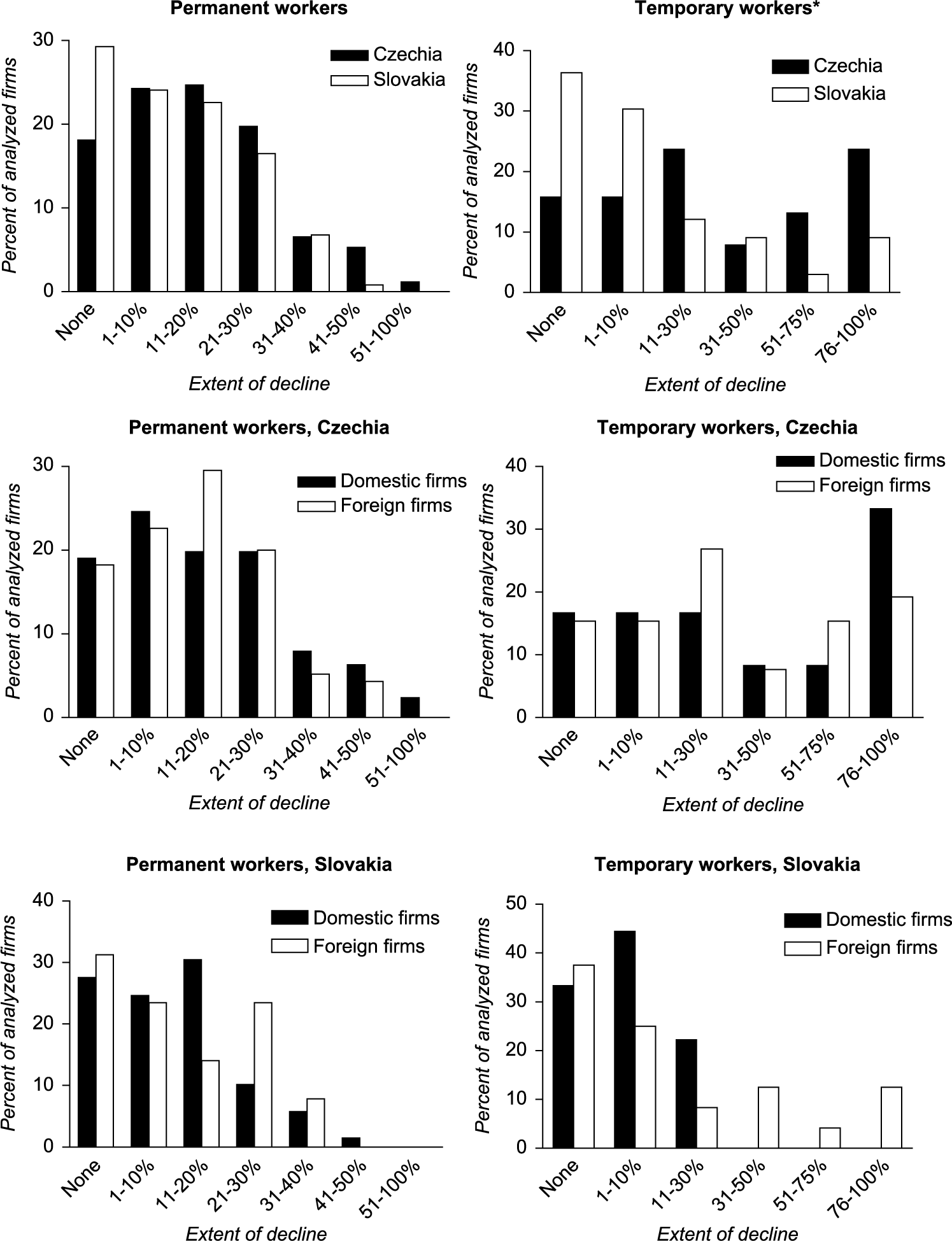

The employment effects of the economic crisis in the form of job losses were significant because 82% of the surveyed firms laid off permanent workers in Czechia compared with 71% in Slovakia. Before the economic crisis, both the Czech-based and Slovak-based automotive firms had increasing difficulties in recruiting workers because of strong demand for automotive workers. This was due to the rapidly growing employment in the automotive industry following large inflows of FDI. At the same time, however, the traditional high-quality vocational training system disintegrated in both countries in the early 1990s. As a result, the supply of young skilled workers greatly diminished, and shortages became acute in the 2000s. In order to cope with surges in demand and with local labor shortages, firms increasingly relied on temporary workers. One-third of all surveyed firms in Czechia (33.6%) and one-fourth (27.7%) in Slovakia employed temporary workers between 2004 and 2009. In Czechia, many of these workers were recruited by work agencies from neighbouring countries, including Poland, Slovakia and Ukraine. In some cases, Czech automotive companies began to recruit temporary low-skilled workers from more distant countries, such as Vietnam and Mongolia. Generally, however, the quality of this temporary labour force was poor, and temporary workers were the first to lose their jobs during the economic crisis (2010 interviews). The difference between Czech and Slovak firms in the extent of the layoff of temporary workers was statistically significant (t-test, p=0.005), and Czech firms on average laid off a higher share of temporary workers than Slovak firms. Foreign and domestic firms did not significantly statistically differ in the extent of layoffs of temporary workers in both Czechia and Slovakia.

A different situation developed with respect to permanent workers. The dismissal of permanent workers is considered by firms to be a last-resort strategy. As a result, the companies first typically reduced the working hours or working days of permanent employees to prevent their layoffs. As the result of these strategies, only 13% of the Czech-based surveyed firms laid off more than 30% of their permanent workers compared with 23% in Slovakia. However, the difference between Czech and Slovak firms in the extent of layoffs of permanent workers was not statistically significant, suggesting a similar extent of layoffs of permanent workers in both countries. In Slovakia, in order to prevent layoffs, VW Slovakia introduced flexible working time (the so-called flexi account) in January 2009. In this system, workers are paid for work days during which they do not work because there is no work for them, but when demand recovers they are required to work those hours as overtime for which they have already been paid. The maximum deficit can reach 300 hours per worker over 4 years. The flexi account was introduced by 60 additional firms in Slovakia because it allows them to keep workers at times of low demand (interview at VW Slovakia, 14 June 2011).

One of the interviewed managers described how his Czech-based company, which employs about 300 temporary workers, dealt with employment issues during the economic crisis: In 2008, we had to react to the crisis. We lost about 30% of our turnover. We did everything that was possible, first of all not using temporary workers supplied by external companies. Then we stopped using people with limited temporary contracts. We did not extend these contracts. The last possibility was to lay off some permanent workers, and we had to do it, too. But we resorted to that only at the beginning of 2009. Already in autumn 2009, the situation started to get better, so we started to take on people again. First, people from external companies, in order to be flexible, then slowly also permanent workers.

11

Although in Czechia domestic firms experienced a statistically significant greater decline in revenues and production than foreign firms, there was not a statistically significant difference between domestic and foreign firms in terms of layoffs of permanent and temporary workers (Figure 3). This suggests that domestic firms have been more reluctant to lay off workers than foreign firms during the economic crisis given their greater drop in revenues and production. It also suggests that foreign firms tend to be more flexible in using their labour force and react more quickly to changing market conditions. Thus, the situation in the Czech automotive industry would support the argument that foreign or domestic ownership may influence the propensity of firms to lay off workers during economic crises. In particular, foreign firms are generally quicker to lay off redundant workers when demand for their products declines (e.g. Pennings and Sleuwaegen 2000), because they tend to protect employment in their home country and attempt first to reduce labor costs in their foreign subsidiaries during an economic recession. In Slovakia, however, there was no statistically significant difference between foreign and domestic firms in the extent of layoffs of permanent workers and temporary workers during the economic crisis (Figure 3).

Decline in permanent workers and temporary workers in Czech and Slovak automotive firms in the past 12 months during 2008 and 2009.

In Czechia, the extent of involvement of firms in the automotive industry affected the extent of layoffs of permanent workers (one-way ANOVA nonparametric test, p=0.005). 12 Given the fact that these groups of firms did not statistically differ in the extent of decline in revenues and production, it suggests that the automotive industry was not more greatly affected by the economic crisis than the rest of manufacturing industry and that the effects of the crisis were universal across the Czech manufacturing industry. However, the automotive industry and manufacturing industry as a whole were more seriously affected by job losses than the Czech economy as a whole during the economic crisis. Further analysis showed greater decline in permanent workers in firms involved 75–99% in automotive production than firms completely involved in automotive production (p=0.043) and firms with the smallest share of the automotive production (1–24%) (p=0.010). Firms with a 50–74% share of automotive production suffered a greater decline in permanent workers than firms with a 1–24% share of automotive production (p=0.043). In Slovakia, the five groups of firms according to the extent of their involvement in the automotive industry statistically did not differ in the extent of layoffs of permanent workers.

Similarly, the statistical difference between SMEs and large firms in the decline in the number of permanent workers was insignificant. However, more SMEs were reluctant to dismiss their permanent workers than large companies. Compared with 26% of large firms, 45% of SMEs laid off fewer than 10% of their permanent employees. At the same time, 17% of SMEs dismissed more than 30% of their permanent workers compared with 7% of large firms.

As in Czechia, Slovak SMEs were more reluctant to shed permanent workers than large firms; 33% of SMEs did not dismiss any permanent workers compared with 19% of large firms. However, two-thirds of large firms (68%) shed fewer than 10% of their permanent workers compared with only half (50%) of SMEs. As in the case of Czechia, Slovak automotive SMEs were affected more seriously by the economic crisis because of their more vulnerable position in the automotive value chain and their greater dependence on lower value-added activities. A high percentage of these firms in both countries are third-tier and second-tier automotive suppliers. The differences in decline in permanent workers were not statistically significant between SMEs and large firms in Slovakia.

Bankruptcies and relocations during the economic crisis

Another way to evaluate the effects of the economic crisis in the Czech and Slovak automotive industries is to analyse plant closures and relocations during the crisis period. It has been argued elsewhere that foreign companies are more likely to engage in disinvestment than domestic companies (Dicken, 1976; Henderson et al. 2002) and, therefore, especially foreign subsidiaries, at the lowest levels of the value chain, are most susceptible to the risk of closure during economic crises. Small countries with open economies, such as Czechia and Slovakia, are especially vulnerable to relocation (Pennings and Sleuwaegen 2000). A high level of plant relocations and plant closures would also suggest a low degree of embeddedness, especially of foreign automotive suppliers, in Czechia and Slovakia. Generally, the most labour-intensive low-skilled activities and the products with the lowest transportation costs and limited significance in relation to just-in-time delivery, such as standardized cable harnesses, are most at risk of relocation. Pavlínek et al. (2009) argued before the crisis that the danger of large-scale relocations of automotive suppliers from central Europe to lower-cost locations elsewhere was relatively low because of the increasing embeddedness of these firms in the region. Did their argument hold during the 2008–2009 economic crisis?

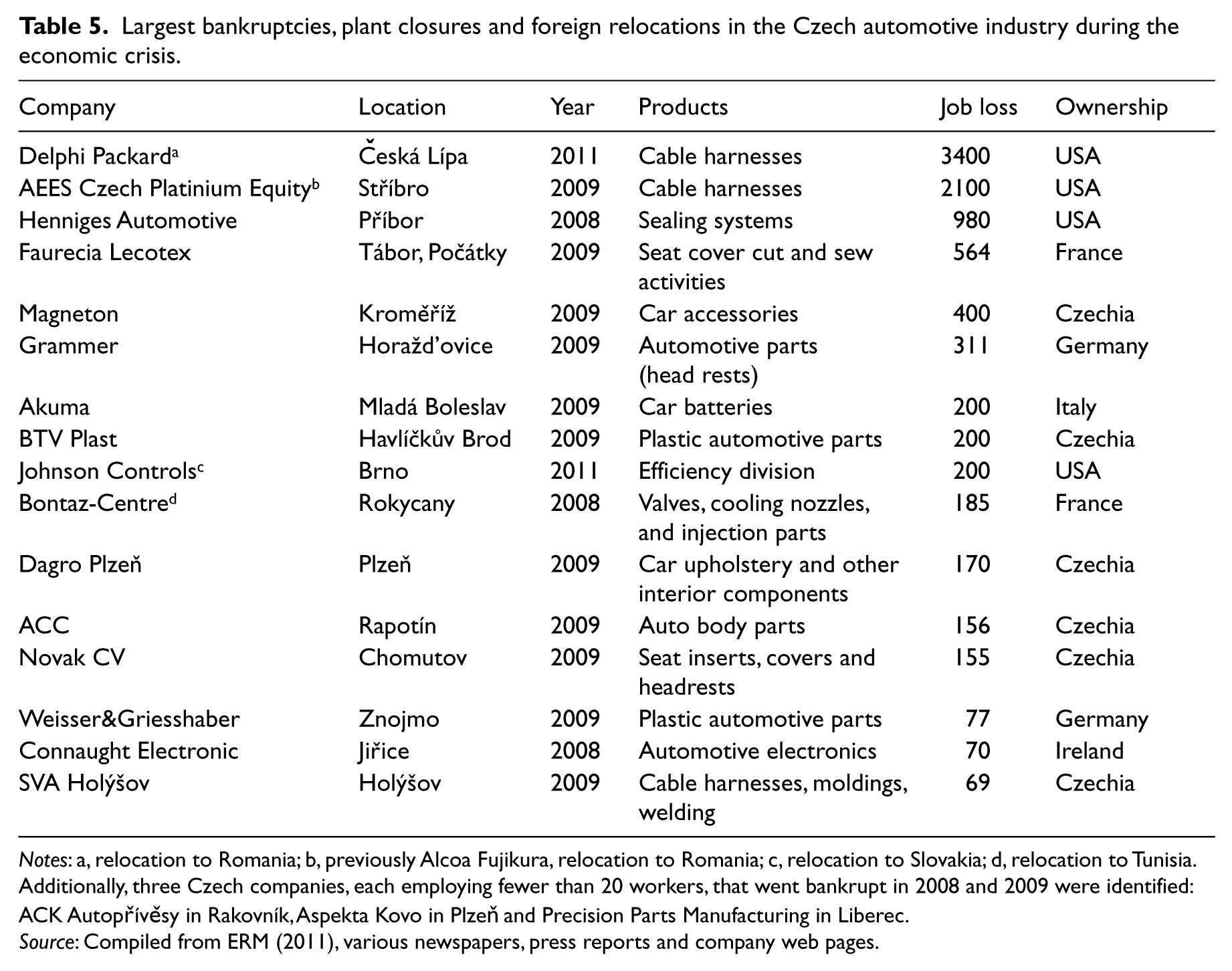

Overall, there were 15 bankruptcies and/or plant closures and four relocations abroad in the Czech automotive industry during and immediately after the economic crisis, which resulted in 9200 job losses (Table 5). In 13 cases these plant closures led to job losses of at least 100 workers each. Overall, however, the number of relocations was low during the economic crisis given the overall size of the Czech automotive industry, and it suggests a relatively high degree of embeddedness of automotive companies in Czechia. This is hardly surprising if one considers the importance of sunk costs, transportation costs, supplier links and the proximity of suppliers to assemblers in the contemporary automotive industry (see also Domański and Gwosdz 2009; Jürgens and Krzywdzinski, 2009; Pavlínek et al., 2009). The data presented in Table 5 also suggest that both foreign and domestic firms were similarly affected by bankruptcies and plant closures in Czechia.

Largest bankruptcies, plant closures and foreign relocations in the Czech automotive industry during the economic crisis.

Notes: a, relocation to Romania; b, previously Alcoa Fujikura, relocation to Romania; c, relocation to Slovakia; d, relocation to Tunisia. Additionally, three Czech companies, each employing fewer than 20 workers, that went bankrupt in 2008 and 2009 were identified: ACK Autoprˇíveˇsy in Rakovník, Aspekta Kovo in Plzenˇ and Precision Parts Manufacturing in Liberec.

Source: Compiled from ERM (2011), various newspapers, press reports and company web pages.

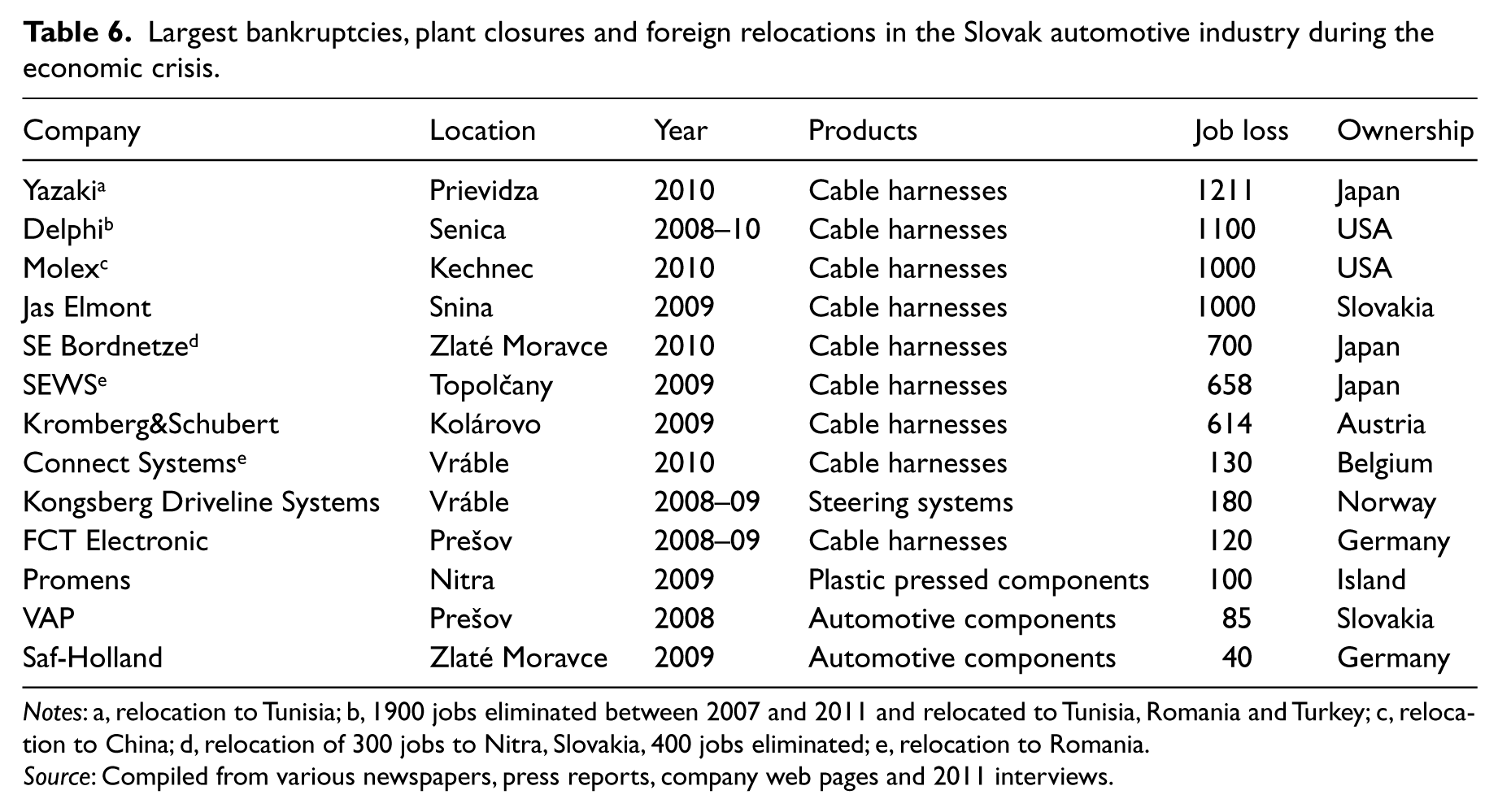

In Slovakia, at least 6928 jobs were lost because of plant closures and relocations in the automotive industry during the economic crisis (Table 6). The majority of jobs were lost in the labour-intensive assembly of simple cable harnesses. As of 2011, these activities were surviving in Slovakia in two settings. First were peripheral low-wage locations, such as eastern Slovakia. In 2011, the average monthly wage in the assembly of cable harnesses was €360 in eastern Slovakia compared with €550 in western Slovakia (2011 interviews). Second was the production of complex high value-added cable harnesses at Delphi Senica (main cockpit harnesses and main body harnesses) for luxury vehicles delivered in a just-in-time regime to VW Slovakia. Each of these cable harnesses is distinct, and they have to be delivered in 14 hours after the order has been placed by VW Slovakia, which requires spatial proximity. 13 Still, Delphi Senica had to resort to large-scale layoffs during the economic crisis, and its number of workers was reduced from 2800 in 2006 to 900 by 2010. Only production for luxury sport utility vehicles (SUVs) survived at Senica, and even its future is uncertain. The assembly of more simple cable harnesses for PSA was relocated to Tunisia and for Mercedes to Romania and Turkey (interview on 13 June 2011).

Largest bankruptcies, plant closures and foreign relocations in the Slovak automotive industry during the economic crisis.

Notes: a, relocation to Tunisia; b, 1900 jobs eliminated between 2007 and 2011 and relocated to Tunisia, Romania and Turkey; c, relocation to China; d, relocation of 300 jobs to Nitra, Slovakia, 400 jobs eliminated; e, relocation to Romania.

Source: Compiled from various newspapers, press reports, company web pages and 2011 interviews.

Overall, the largest bankruptcies and relocations in both Czechia and Slovakia affected labour-intensive, low-wage and low-skilled assembly of cable harnesses. Although job losses were considerable, they were largely confined to a particular low-end segment of the automotive value chain. The 2008–2009 crisis did not lead to widespread relocations that would affect the automotive industry across the board. Thus, it did not support the arguments about the ‘footlooseness’ of the central European automotive industry (Rugraff, 2010).

Conclusion

The goal of this article has been to evaluate the effects of the 2008–2009 global economic crisis in the automotive industry in the context of the peripheral automotive production region. The analysis concentrated on a case study of the Czech and Slovak automotive industries as examples of ‘integrated peripheral markets’. Both the Czech and Slovak automotive industries were negatively affected by the economic crisis. The vast majority of companies experienced significant declines in production, revenues and workers. However, with the exception of the labour-intensive assembly of simple cable harnesses, the economic crisis did not lead to waves of bankruptcies or large-scale relocations of automotive suppliers from Czechia and Slovakia to cheaper production locations in foreign countries as some have feared. The low number of closures and relocations suggests the relatively strong embeddedness of the automotive firms in the Czech and Slovak economies. A high share of bankruptcies and relocations in the assembly of cable harnesses underscores the fact that central European countries are no longer competitive in the export-oriented low-cost and labour-intensive simple assembly of standardized components. Thus, the partial consolidation of the supplier base envisioned by Van Biesebroeck and Sturgeon (2010) did take place, although it was not limited to small domestic suppliers as they have argued. Instead, the consolidation also affected large foreign subsidiaries, especially in the assembly of cable harnesses. Suppliers were strongly squeezed by lead assembly firms during the crisis, which might further endanger future prospects of especially small domestic suppliers at the bottom of the supplier hierarchy.

This article has demonstrated the advantages of the firm-level analysis of the effects of economic crises, especially when compared with national-level approaches that would be limited to measuring changes in national levels of production and employment. The firm-level analysis revealed that the effects of the economic crisis were similar in the Czech and Slovak automotive industries despite very different national production trends during the crisis. This can be explained by the similar nature of the passenger car industries in these countries. Both the Czech and Slovak passenger car industries are predominantly specialized in the export-oriented assembly of small passenger cars and the production of automotive components. Insignificant differences between Czechia and Slovakia also suggest that the presence (in the case of Slovakia) or absence (in the case of Czechia) of active government policies to support the export-oriented passenger industry during the economic crisis had no significant effect on the extent of declines in revenues and production.

The employment effects of the economic crisis were extremely important because more than four-fifths of the surveyed Czech-based firms and more than two-thirds of the Slovak-based firms shed permanent workers, despite various efforts to maintain them. Among the surveyed Czech-based firms, domestic firms were more badly affected by the economic crisis than foreign firms. This finding reflects the generally weaker and more vulnerable position of domestic firms in the automotive value chain because of their significantly smaller average size, their greater concentration among the third-tier and second-tier suppliers than foreign firms, and thus their greater reliance on the production of simpler and lower value-added components (see Pavlínek and Janák, 2007). SMEs were more negatively affected by the economic crisis than large companies because of their less diversified production and their weaker and more vulnerable position in the automotivevalue chain.

The 2008–2009 crisis in the automotive industry exposed the dependence of the Czech and Slovak automotive industries on the west European automotive industry. The FDI-driven integration of Czech- and Slovak-based automotive firms into GPNs organized from abroad puts small domestic and foreign firms at the bottom of the supplier hierarchy in an especially weak, dependent and vulnerable position, with only limited chances for a successful upgrading. Because of the predominant truncation effects of FDI in the ECE automotive industry (Britton, 1980; Hayter, 1982; Pavlínek, 2012), the positive long-term regional development consequences of this type of captive value chain and the related industrial development are likely to be limited mostly to jobs in low value-added assembly operations in the supplier sector. The overwhelming foreign ownership and control contribute to the transfer of profits abroad and low value capture in ECE. Given this situation, it is clear that the future success of automotive industries in Czechia and Slovakia, as well as in ECE as a whole, will be closely tied with the continuing competitive success of the West European automotive industry.

Footnotes

Acknowledgements

The author wishes to thank the two anonymous reviewers and the editor for helpful comments on an earlier version of this article. He also wishes to thank Pavla Žížalová and Jan Ženka for their help with the administration of the company survey in 2009 and with company interviews in 2010 and 2011.The research and article preparation were supported by the European Commission (Grant Agreement No. PIRG03-GA-2008–230886), by the Czech Science Foundation (Grant Agreement No. 205/09/0908), and by the Czech Ministry of Education, Youth and Sport (Research Program No. MSM 0021620831).